Optimal Structure of Real Estate Portfolio Using EVA: A Stochastic Markowitz Model Using Data from Greek Real Estate Market

Abstract

:1. Introduction

2. Literature Review

- Select the maximum return for a given level of risk;

- The least risk to a given level of return.

- Τhe probability function of the returns can be estimated by investors;

- The basic principle is to maximize the utility function of investor;

- Investors tend to avoid risk in pursuit of profit;

- Financial markets are smooth;

- The existence of transaction cost and taxes is absent.

3. Data

- Residential;

- Office;

- Retail.

- Athens;

- Thessaloniki;

- Rest of Greece.

4. Methodology

The Theoretical Point of View of Our Model

- Apartment;

- Offices;

- Retail.

- Apartment;

- Offices;

- Retail.

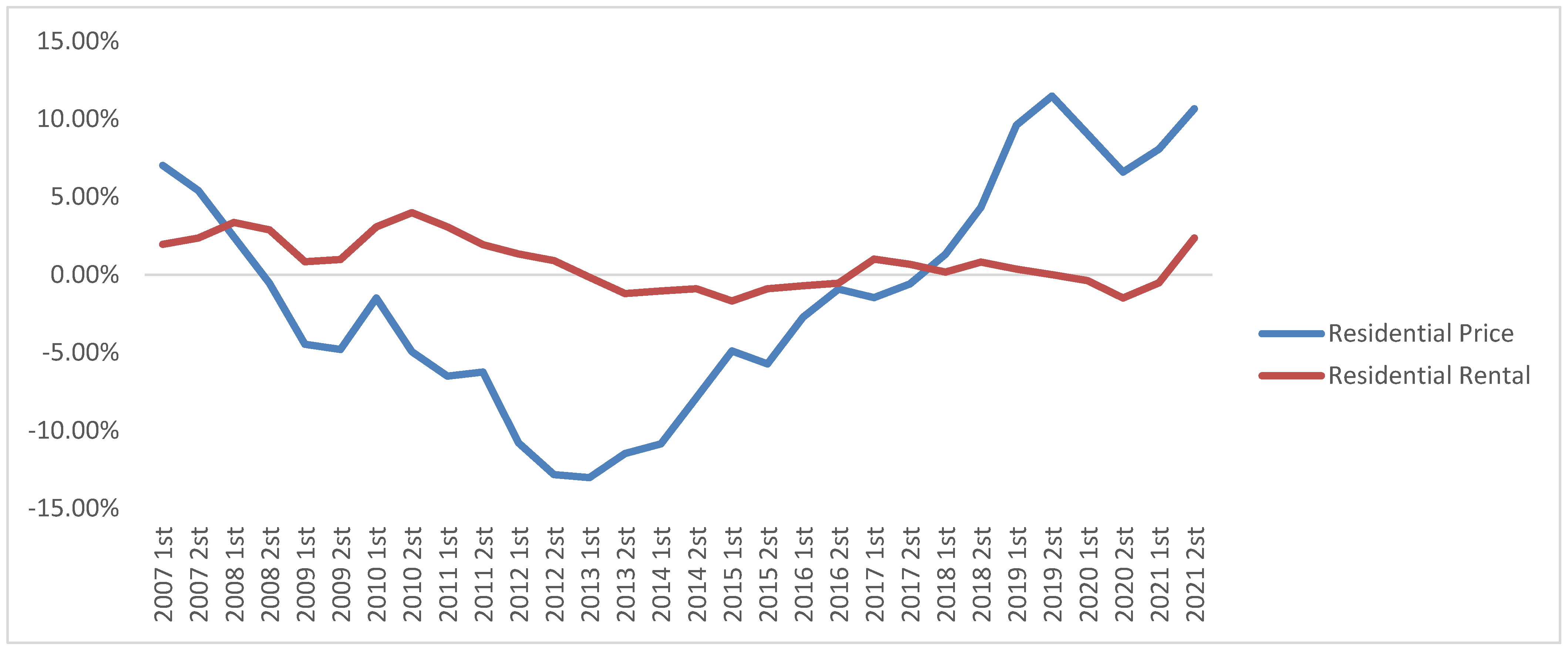

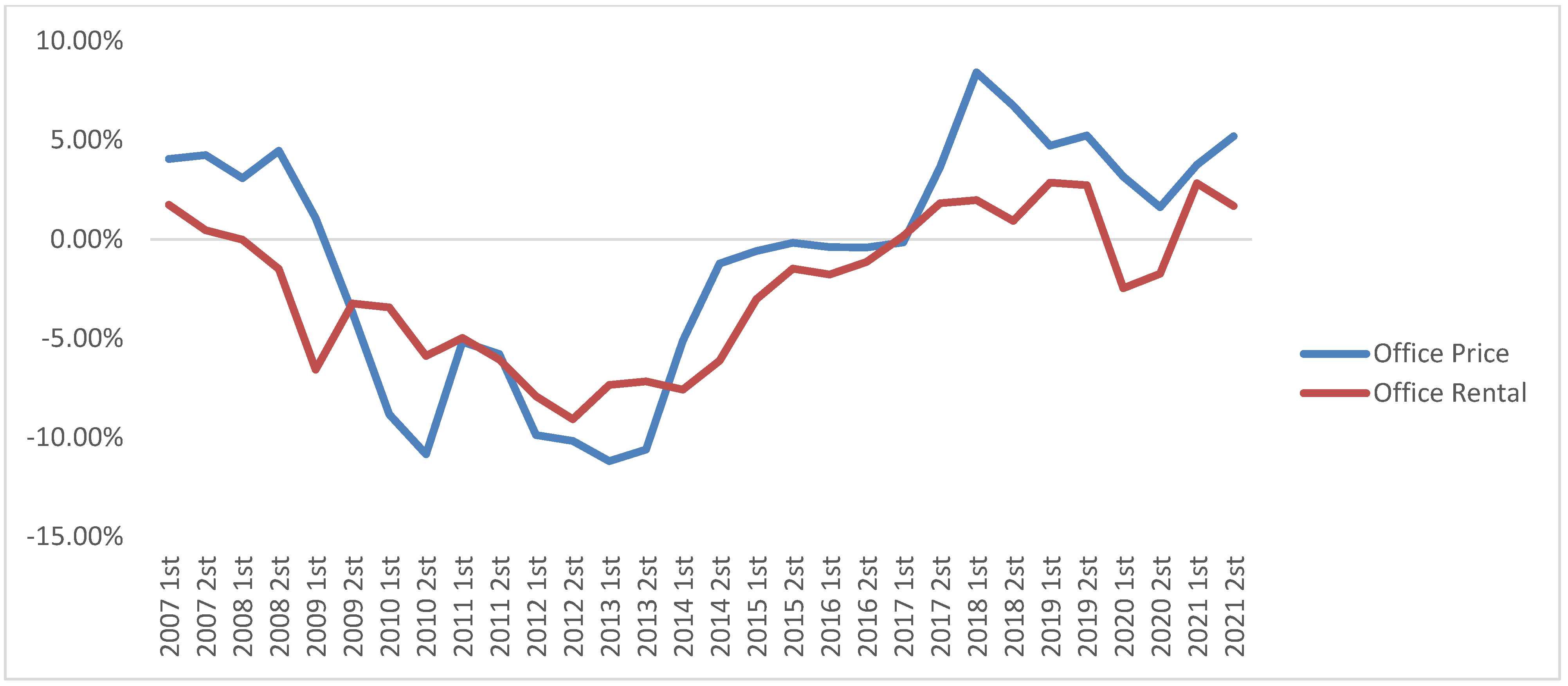

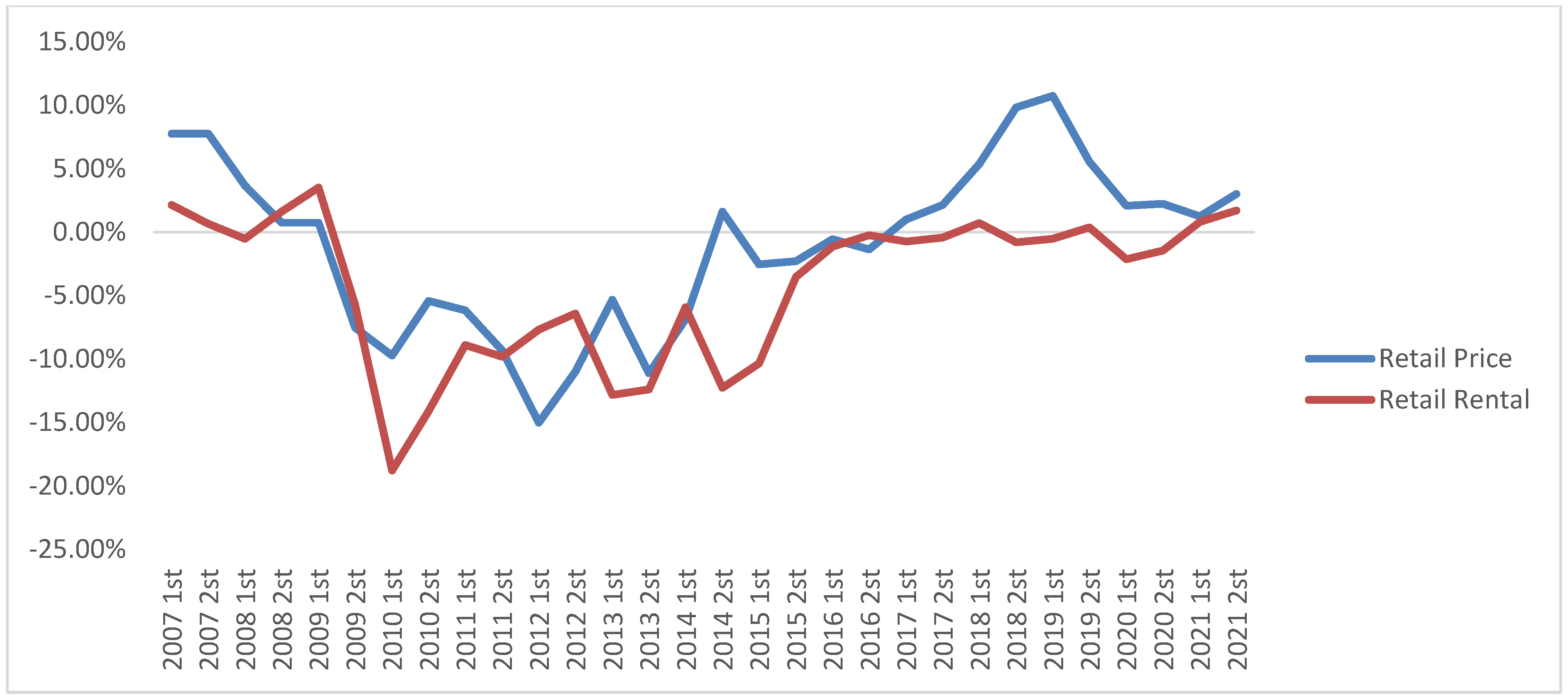

5. Estimations-Empirical Analysis

5.1. Estimations

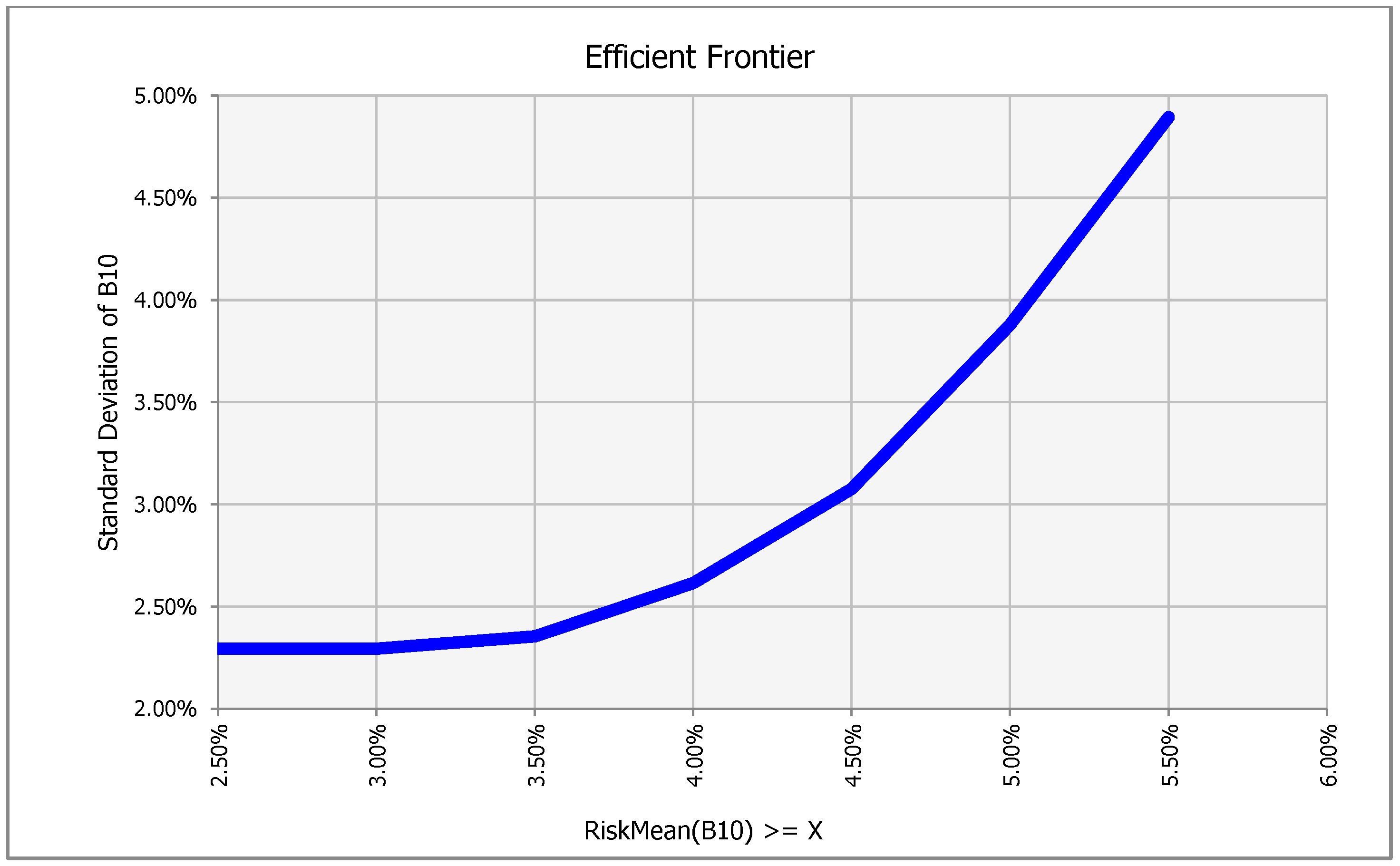

5.2. Portfolio Optimization Results

6. Discussions and Conclusions

6.1. Discussions and Key Findings

6.2. Theoretical Implication-Practical Implication

6.3. Restrictions and Future Work

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

| 1 | We use the median of stock exchange listed companies on Greek Real Estate Market by ICAP database. |

| 2 | Cost of Capital (nyu.edu) accessed on 25 August 2022. |

| 3 | (bankofgreece.gr) accessed on 25 August 2022. |

| 4 | See note 1 above. |

| 5 | The corporate tax rate reduced from 24% to 22% in 2021 year. |

| 6 | RE/MAX 2021 (remax.gr) accessed on 25 August 2022. |

References

- Best, Michael. 2010. Portfolio Optimization. Boca Raton: CRC Press. [Google Scholar]

- Black, Fischer, and Robert Litterman. 1992. Global portfolio optimization. Financial Analysts Journal 48: 28–43. [Google Scholar] [CrossRef]

- Bliss, Barbara A., Yingmei Cheng, and David J. Denis. 2015. Corporate payout, cash retention, and the supply of credit: Evidence from the 2008–2009 credit crisis. Journal of Financial Economics 115: 521–40. [Google Scholar] [CrossRef]

- Bordo, Michael, Barry Eichengreen, Daniela Klingebiel, and Maria Soledad Martinez-Peria. 2001. Is the crisis problem growing more severe? Economic Policy 16: 52–82. [Google Scholar] [CrossRef]

- Byrne, Peter, and Stephen Lee. 1995. Is there a place for property in the multi-asset portfolio? Journal of Property Finance 6: 60–83. [Google Scholar] [CrossRef]

- Chan, Bertram K. C. 2017. Applied Probabilistic Calculus for Financial Engineering: An Introduction Using R. New York: John Wiley & Sons. [Google Scholar]

- Chen, Wei-Peng, Huimin Chung, Keng-Yu Ho, and Tsui-Ling Hsu. 2020. Portfolio optimization models and meanvariance spanning tests. In Handbook of Quantitative Finance and Risk Management. Edited by Cheng-Few Lee, Alice C. Lee and John Lee. Boston: Springer, pp. 165–84. [Google Scholar]

- Chopra, Vijay Kumar, and William T. Ziemba. 1993. The effect of errors in means, variances and covariances on optimal portfolio choice. Journal of Portfolio Management 19: 6–11. [Google Scholar] [CrossRef]

- Cui, Tianxiang, Ruibin Bai, Shusheng Ding, Andrew J. Parkes, Rong Qu, Fang He, and Jingpeng Li. 2020. A hybrid combinatorial approach to a two-stage stochastic portfolio optimization model with uncertain asset prices. Soft Computing 24: 2809–31. [Google Scholar] [CrossRef]

- Dantzig, Tobias. 2007. Number: The Language of Science. The Masterpiece Science ed. New York: Plume Book. ISBN 9780452288119. [Google Scholar]

- Draper, Norman R., and Harry Smith. 1998. Applied Regression Analysis. New York: John Wiley & Sons, vol. 326. [Google Scholar]

- Dutra, Camila Costa, José Luis Duarte Ribeiro, and Marly Monteiro de Carvalho. 2014. An economic–probabilistic model for project selection and prioritization. International Journal of Project Management 32: 1042–55. [Google Scholar] [CrossRef]

- Eichholtz, Piet M. A., Martin Hoesli, Bryan D. MacGregor, and Nanda Nanthakumaran. 1995. Real estate diversification by property-type and region. Journal of Property Finance 6: 39–62. [Google Scholar] [CrossRef]

- Engels, Marnix. 2004. Portfolio Optimization: Beyond Markowitz. Master’s thesis, University of Leiden, Leiden, The Netherlands. [Google Scholar]

- Estrada, Javier. 2008. Mean-semivariance optimization: A heuristic approach. Journal of Applied Finance 18: 57–72. [Google Scholar] [CrossRef]

- Fama, Eugene F. 1965. Portfolio analysis in a stable Paretian market. Management Science 11: 404–19. [Google Scholar] [CrossRef]

- Fulton, Lawrence V., and Nathaniel D. Bastian. 2019. Multiperiod stochastic programming portfolio optimization for diversified funds. International Journal of Finance & Economics 24: 313–27. [Google Scholar]

- Gambrah, Priscilla Serwaa Nkyira, and Traian Adrian Pirvu. 2014. Risk measures and portfolio optimization. Journal of Risk and Financial Management 7: 113–29. [Google Scholar] [CrossRef]

- Glasserman, Paul. 2004. Monte Carlo methods in Financial Engineering. New York: Springer, vol. 53, pp. xiv+–596. [Google Scholar]

- Gottschlich, Jörg, and Oliver Hinz. 2014. A decision support system for stock investment recommendations using collective wisdom. Decision Support Systems 59: 52–62. [Google Scholar] [CrossRef]

- Gruszka, Jarosław, and Janusz Szwabiński. 2020. Best portfolio management strategies for synthetic and real assets. Physica A: Statistical Mechanics and Its Applications 539: 122938. [Google Scholar] [CrossRef]

- Haugen, Robert A., and Nardin L. Baker. 1990. Dedicated stock portfolios. Journal of Portfolio Management 16: 17–22. [Google Scholar] [CrossRef]

- Harding, Don, and Adrian Pagan. 2011. An econometric analysis of some models for constructed binary time series. Journal of Business & Economic Statistics 29: 86–95. [Google Scholar]

- Ivanova, Miroslava, and Lilko Dospatliev. 2017. Application of Markowitz portfolio optimization on Bulgarian stock market from 2013 to 2016. International Journal of Pure and Applied Mathematics 117: 291–307. [Google Scholar] [CrossRef]

- Jorion, Philippe. 1985. International portfolio diversification with estimation risk. Journal of Business 58: 259–78. [Google Scholar] [CrossRef]

- Jung, Jongbin, and Seongmoon Kim. 2015. An adaptively managed dynamic portfolio selection model using a time varying investment target according to the market forecast. Journal of the Operational Research Society 66: 1115–31. [Google Scholar] [CrossRef]

- Kalberg, Jerry, and William Ziemba. 1984. Misspecification in portfolio selection problems. In Risk and Capital. Berlin and Heidelberg: Springer, pp. 74–87. [Google Scholar]

- Kaminsky, Graciela L., and Carmen M. Reinhart. 1999. The twin crises: The causes of banking and balance-of-payments problems. American Economic Review 89: 473–500. [Google Scholar] [CrossRef]

- Konno, Hiroshi, and Hiroaki Yamazaki. 1991. Mean absolute deviation portfolio optimization model and its application to Tokyo stock market. Management Science 37: 519–31. [Google Scholar] [CrossRef]

- Kroencke, Tim-Alexander, and Felix Schindler. 2010. Downside risk optimization in securitized real estate markets. Journal of Property Investment & Finance 28: 434–53. [Google Scholar]

- Kwiatkowski, Denis, Peter C. B. Phillips, Peter Schmidt, and Yongcheol Shin. 1992. Testing the null hypothesis of stationarity against the alternative of a unit root: How sure are we that economic time series have a unit root? Journal of Econometrics 54: 159–78. [Google Scholar] [CrossRef]

- Lee, Chijoo. 2019. Financing method for real estate and infrastructure development using Markowitz’s portfolio selection model and the Monte Carlo simulation. Engineering, Construction and Architectural Management 26: 2008–22. [Google Scholar] [CrossRef]

- Lee, S. L. 1992. Emerging Concepts for the Management of Portfolios and the Role of Research: Property in the Portfolio Context. London: Society of Property Researchers. [Google Scholar]

- Lee, Stephen, and Simon Stevenson. 2005. Real estate portfolio construction and estimation risk. Journal of Property Investment & Finance 23: 234–53. [Google Scholar]

- Liapis, Konstantinos J. 2010. The Residual Value Models: A Framework for Business Administration. European Research Studies 13: 83–102. [Google Scholar]

- Liapis, Konstantinos J., Manolis S. Christofakis, and Harris G. Papacharalampous. 2011. A new evaluation procedure in real estate projects. Journal of Property Investment & Finance 29: 280–96. [Google Scholar]

- Lilliefors, Hubert W. 1967. On the Kolmogorov-Smirnov test for normality with mean and variance unknown. Journal of the American statistical Association 62: 399–402. [Google Scholar] [CrossRef]

- Logue, Dennis E. 1982. An experiment in international diversification. Journal of Portfolio Management 9: 22–27. [Google Scholar] [CrossRef]

- Madura, Jeff, and Gordon Abernathy. 1985. Playing the international stock diversification game with an unmarked deck. Journal of Business Research 13: 465–71. [Google Scholar] [CrossRef]

- Mansini, Renata, and Maria Grazia Speranza. 1999. Heuristic algorithms for the portfolio selection problem with minimum transaction lots. European Journal of Operational Research 114: 219–33. [Google Scholar] [CrossRef]

- Markowitz, Harry M. 1952. Portfolio selection. Journal of Finance 7: 77–91. [Google Scholar]

- Markowitz, Harry. 1959. Portfolio Selection: Efficient Diversification of Investments. New York: Wiley. [Google Scholar]

- Milhomem, Danilo Alcantara, and Maria José Pereira Dantas. 2020. Analysis of new approaches used in portfolio optimization: A systematic literature review. Production 30. [Google Scholar] [CrossRef]

- Mueller, Glenn R., and Steven P. Laposa. 1995. Property-type diversification in real estate portfolios: Size and return perspective. The Journal of Real Estate Portfolio Management 1: 39–50. [Google Scholar] [CrossRef]

- Myer, Neil, and James Webb. 1991. Estimating allocations for mixed-asset portfolios using the bootstrap technique. Paper presented at the American Real Estate Society Meeting, Sarasota, FL, USA. [Google Scholar]

- Pagliari, Joseph L., James R. Webb, and Joseph J. Del Casino. 1995. Applying MPT to institutional real estate portfolios: The good, the bad and the uncertain. The Journal of Real Estate Portfolio Management 1: 67–88. [Google Scholar] [CrossRef]

- Quintana, David, Roman Denysiuk, Sandra Garcia-Rodriguez, and António Gaspar-Cunha. 2017. Portfolio implementation risk management using evolutionary multiobjective optimization. Applied Sciences 7: 1079. [Google Scholar] [CrossRef]

- Rockafellar, R. Tyrrell, and Stanislav Uryasev. 2000. Optimization of conditional value-at-risk. Journal of Risk 2: 21–41. [Google Scholar] [CrossRef]

- Shadab Far, Mahdi, and Yua Wang. 2016. Approximation of the Monte Carlo sampling method for reliability analysis of structures. Mathematical Problems in Engineering 2016: 572656. [Google Scholar] [CrossRef]

- Shadabfar, Mahboubeh, and Longsheng Cheng. 2020. Probabilistic approach for optimal portfolio selection using a hybrid Monte Carlo simulation and Markowitz model. Alexandria Engineering Journal 59: 3381–93. [Google Scholar] [CrossRef]

- Sharpe, William F. 1964. Capital asset prices: A theory of market equilibrium under conditions of risk. Journal of Finance 19: 425–42. [Google Scholar]

- Sharpe, William F. 1966. Mutual fund performance. Journal of Business 39: 119–38. [Google Scholar] [CrossRef]

- Sharpe, William F. 1994. The Sharpe ratio. Journal of Portfolio Management 21: 49–58. [Google Scholar] [CrossRef]

- Stevenson, Simon. 2000. Constraining optimal portfolios and the effect on real estate’s allocation. Journal of Property Investment & Finance 18: 488–506. [Google Scholar]

- Stewart, Bennett. 2009. EVA Momentum: The One Ratio That Tells the Whole Story. Journal of Applied Corporate Finance 21: 74–86. [Google Scholar] [CrossRef]

- Suits, Daniel B. 1957. Use of dummy variables in regression equations. Journal of the American Statistical Association 52: 548–51. [Google Scholar] [CrossRef]

- Thomopoulos, Nick T. 2014. Essentials of Monte Carlo Simulation: Statistical Methods for Building Simulation Models. Berlin and Heidelberg: Springer. [Google Scholar]

- Tobin, James. 1965. The Theory of Portfolio Selection. In The Theory of Interest Rates. Edited by F. H. Hahn and F. P. R. Brechling. London: Macmillan. [Google Scholar]

- Tobin, James. 1967. Life Cycle Saving and Balanced Growth. In Ten Economic Studies in the Tradition of Irving Fisher. New York: Wiley, pp. 231–56. [Google Scholar]

- Zanjirdar, Majid. 2020. Overview of portfolio optimization models. Advances in Mathematical Finance and Applications 5: 419–35. [Google Scholar]

- Zhou, Bei, Li Zongzhi, Harshingar Patel, Arash M. Roshandeh, and Yuanqing Wang. 2014. Risk-based two-step optimization model for highway transportation investment decision-making. Journal of Transportation Engineering 140: 04014007. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

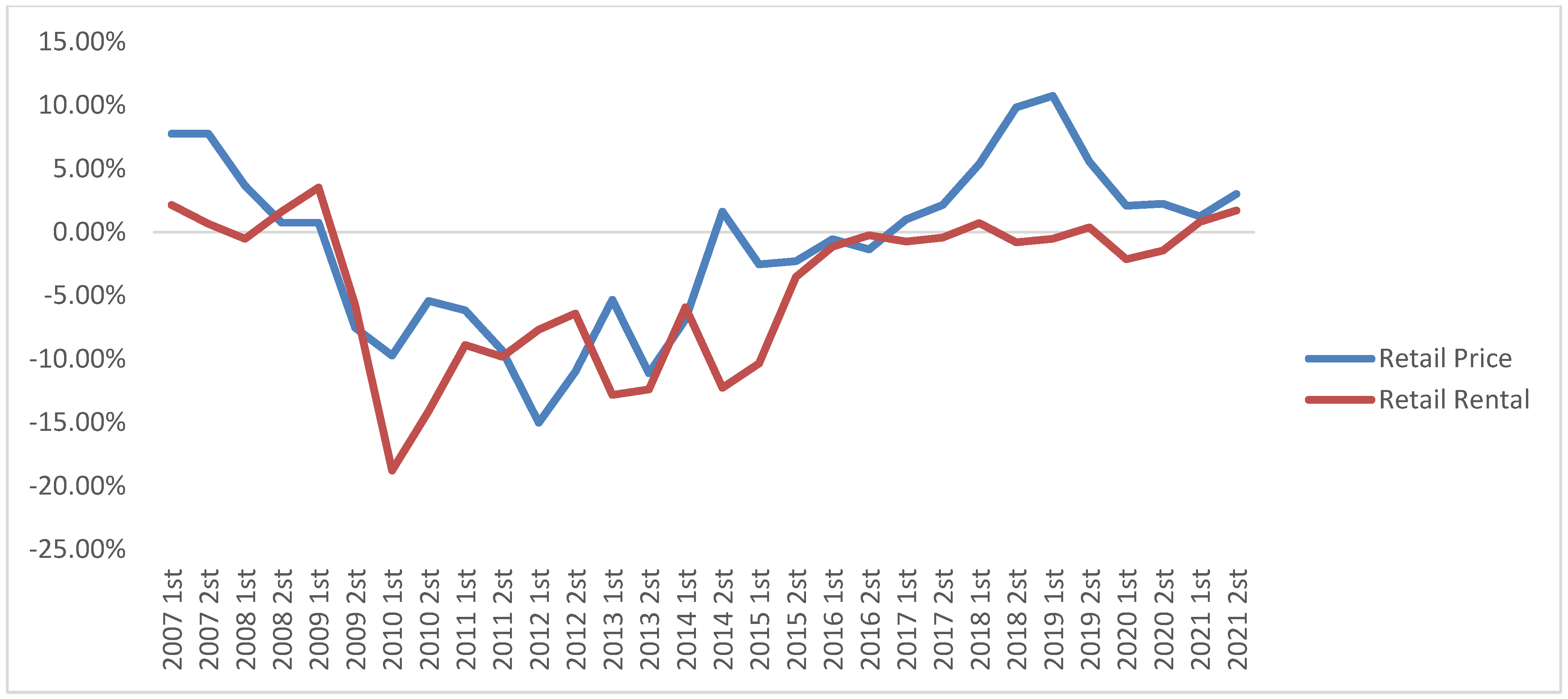

| Trend Calculation | Residential Price | Residential Rental | Office Price | Office Rental | Retail Price | Retail Rental |

|---|---|---|---|---|---|---|

| Constant | 0.084352 ** (0.016981) | 0.024585 ** (0.003304) | 0.099045 ** (0.026144) | 0.056284 ** (0.014164) | 0.137812 ** (0.025751) | 0.074128 ** (0.0293267) |

| Dummy (Crisis) | −0.05005 ** (0.016458) | −0.021662 ** (0.003582) | −0.05338 ** (0.020369) | −0.02444 ** (0.00965) | −0.05128 ** (0.017526) | −0.079506 ** (0.0269355) |

| t | −0.01737 ** (0.003061) | −0.000589 ** (0.000199) | −0.03121 ** (0.009109) | −0.02191 ** (0.004864) | −0.04314 ** (0.008759) | −0.030405 ** (0.0089870) |

| 0.000633 ** (0.000107) | - | 0.002342 ** (0.000594) | 0.00149 ** (0.000353) | 0.003123 ** (0.000601) | 0.002498 ** (0.0005930) | |

| - | - | −4.6 × 10−5 ** (1.12 × 10−5) | −2.7 × 10−5 ** (7.15 × 10−6) | −6.1 × 10−5 ** (1.17 × 10−5) | −5.148 × 10−5 ** (1.22826 × 10−5) | |

| Method | Multiple Regression | Multiple Regression | Multiple Regression | Multiple Regression | Multiple Regression | Multiple Regression |

| Observations | 30 | 30 | 30 | 30 | 30 | 30 |

| R-squared | 0.8682 | 0.7134 | 0.8249 | 0.8223 | 0.8539 | 0.7084 |

| R-squared Adjusted | 0.8530 | 0.6922 | 0.7969 | 0.7938 | 0.8305 | 0.6618 |

| F-Statistic | 57.10521 | 33.60277 | 29.44065 | 28.91856 | 36.5238 | 15.18509411 |

| Real Estate Return | 1 | 2 | 3 |

| Expected Return | 5.46% | 7.72% | 10.19% |

| Standard Deviation | 4.94% | 3.01% | 5.45% |

| V-C | 1 | 2 | 3 |

| 1 | 0.2436% | 0.0965% | 0.2161% |

| 2 | 0.0965% | 0.0905% | 0.1509% |

| 3 | 0.2161% | 0.1509% | 0.2972% |

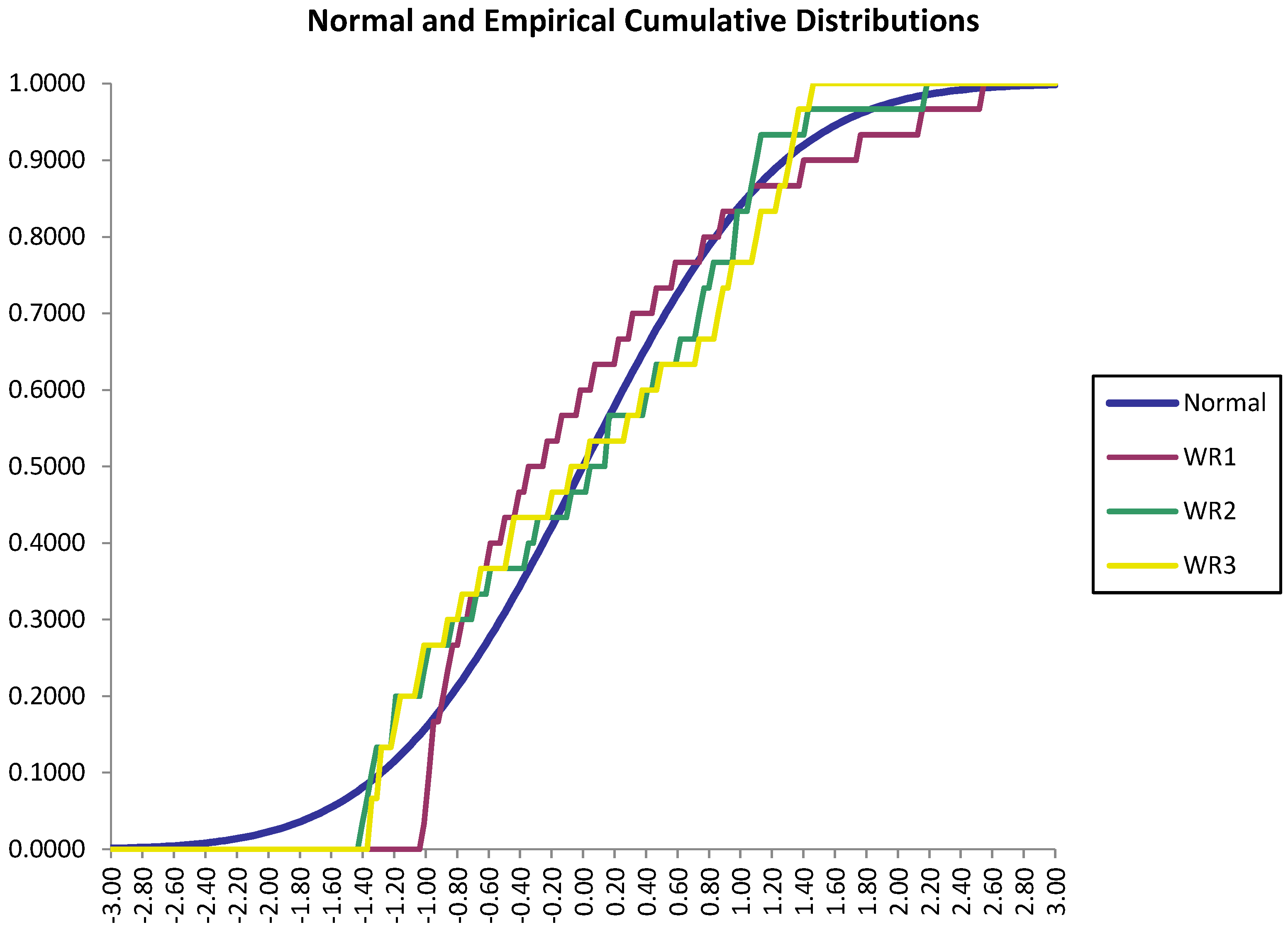

| Lilliefors Test Results | WR1 | WR2 | WR3 |

|---|---|---|---|

| Sample Size | 30 | 30 | 30 |

| Sample Mean | 0.05464 | 0.07720 | 0.10189 |

| Sample Std Dev | 0.04935 | 0.03009 | 0.05451 |

| Test Statistic | 0.1550 | 0.1080 | 0.1364 |

| CVal (15% Sig. Level) | 0.1378 | 0.1378 | 0.1378 |

| CVal (10% Sig. Level) | 0.1457 | 0.1457 | 0.1457 |

| CVal (5% Sig. Level) | 0.1592 | 0.1592 | 0.1592 |

| CVal (2.5% Sig. Level) | 0.1699 | 0.1699 | 0.1699 |

| CVal (1% Sig. Level) | 0.2326 | 0.2326 | 0.2326 |

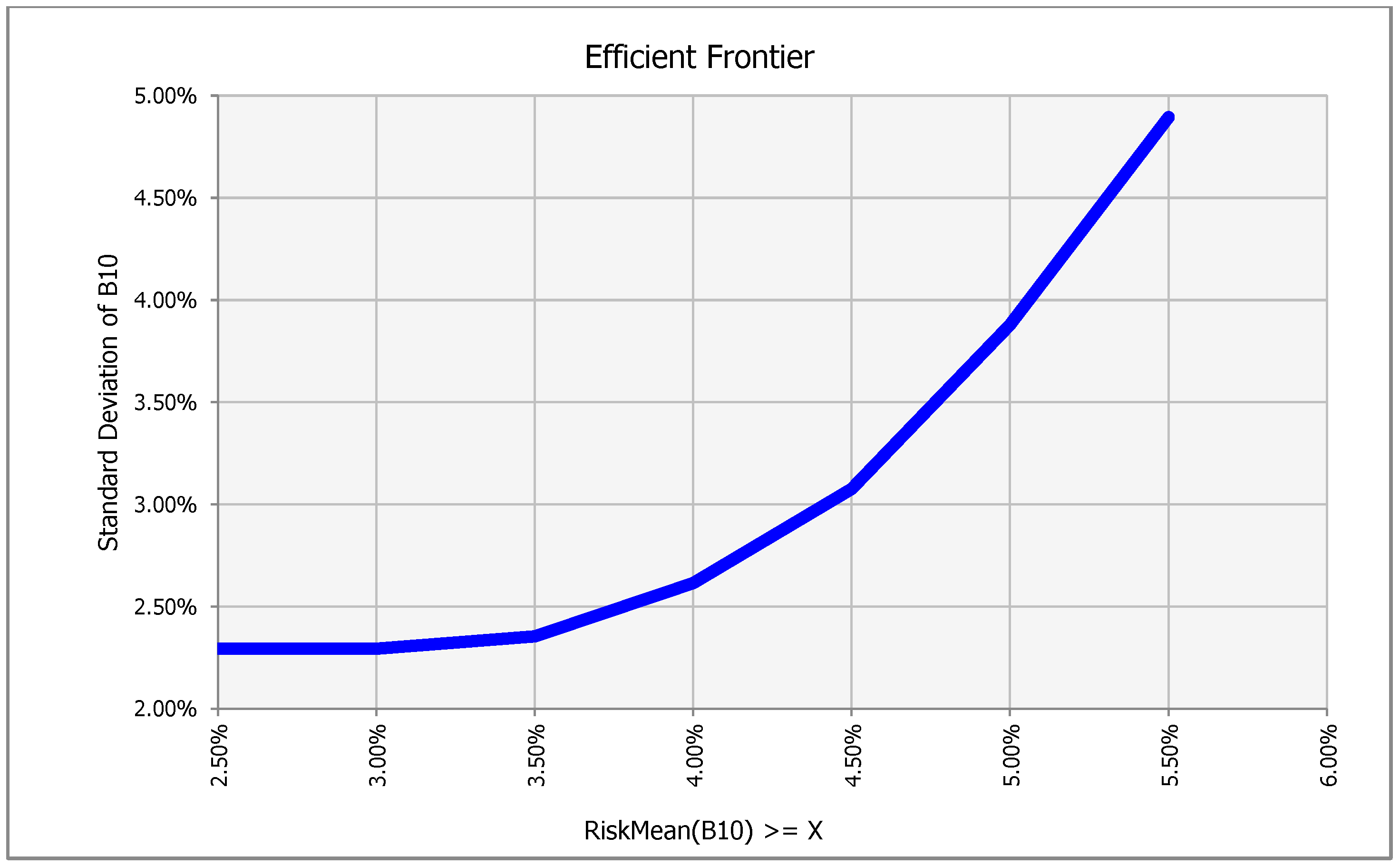

| Constraining Value | Valid Trials | Best Value | Trial | Goal Cell Statistics | Adjustable Cells | Hard Constraints | ||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| (for Constraining Value) | Mean | Std. Dev. | Min. | Max. | B5 | C5 | D5 | RiskMean(B10) | E5 = 1 | |||

| 6.00% | 0 | N/A | N/A | N/A | N/A | N/A | N/A | N/A | N/A | N/A | N/A | N/A |

| 5.50% | 69 | 4.89% | 265 | 5.51% | 4.89% | −9.85% | 23.50% | 0.0% | 10.6% | 89.4% | 5.51% | 1 |

| 5.00% | 182 | 3.88% | 373 | 5.00% | 3.88% | −7.09% | 19.72% | 0.0% | 31.1% | 68.9% | 5.00% | 1 |

| 4.50% | 299 | 3.07% | 760 | 4.50% | 3.07% | −5.51% | 15.98% | 0.0% | 51.4% | 48.6% | 4.50% | 1 |

| 4.00% | 447 | 2.62% | 436 | 4.00% | 2.62% | −5.14% | 12.48% | 3.3% | 65.2% | 31.5% | 4.00% | 1 |

| 3.50% | 595 | 2.35% | 752 | 3.54% | 2.35% | −5.02% | 11.78% | 18.0% | 55.7% | 26.3% | 3.54% | 1 |

| 3.00% | 681 | 2.29% | 800 | 3.25% | 2.29% | −5.50% | 11.14% | 22.7% | 58.7% | 18.7% | 3.25% | 1 |

| 2.50% | 728 | 2.29% | 800 | 3.25% | 2.29% | −5.50% | 11.14% | 22.7% | 58.7% | 18.7% | 3.25% | 1 |

| Constraining Value | Valid Trials | Best Value | Trial | Goal Cell Statistics | Adjustable Cells | Hard Constraints | ||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| (for Constraining Value) | Mean | Std. Dev. | Min. | Max. | B5 | C5 | D5 | RiskStdDev(B10) | E5 =1 | |||

| 2.00% | 0 | N/A | N/A | N/A | N/A | N/A | N/A | N/A | N/A | N/A | N/A | N/A |

| 2.50% | 48 | 3.80% | 471 | 3.80% | 2.48% | −5.94% | 11.20% | 7.7% | 65.1% | 27.2% | 2.48% | 1 |

| 3.00% | 292 | 4.45% | 448 | 4.45% | 3.00% | −6.98% | 13.44% | 0.0% | 53.4% | 46.6% | 3.00% | 1 |

| 3.50% | 400 | 4.79% | 511 | 4.79% | 3.50% | −7.56% | 15.12% | 0.0% | 39.5% | 60.5% | 3.50% | 1 |

| 4.00% | 532 | 5.06% | 766 | 5.06% | 3.98% | −8.55% | 16.90% | 0.0% | 28.6% | 71.4% | 3.98% | 1 |

| 4.50% | 632 | 5.32% | 50 | 5.32% | 4.50% | −9.69% | 19.26% | 0.0% | 18.0% | 82.0% | 4.50% | 1 |

| 5.00% | 788 | 5.56% | 706 | 5.56% | 5.00% | −10.73% | 21.54% | 0.0% | 8.4% | 91.6% | 5.00% | 1 |

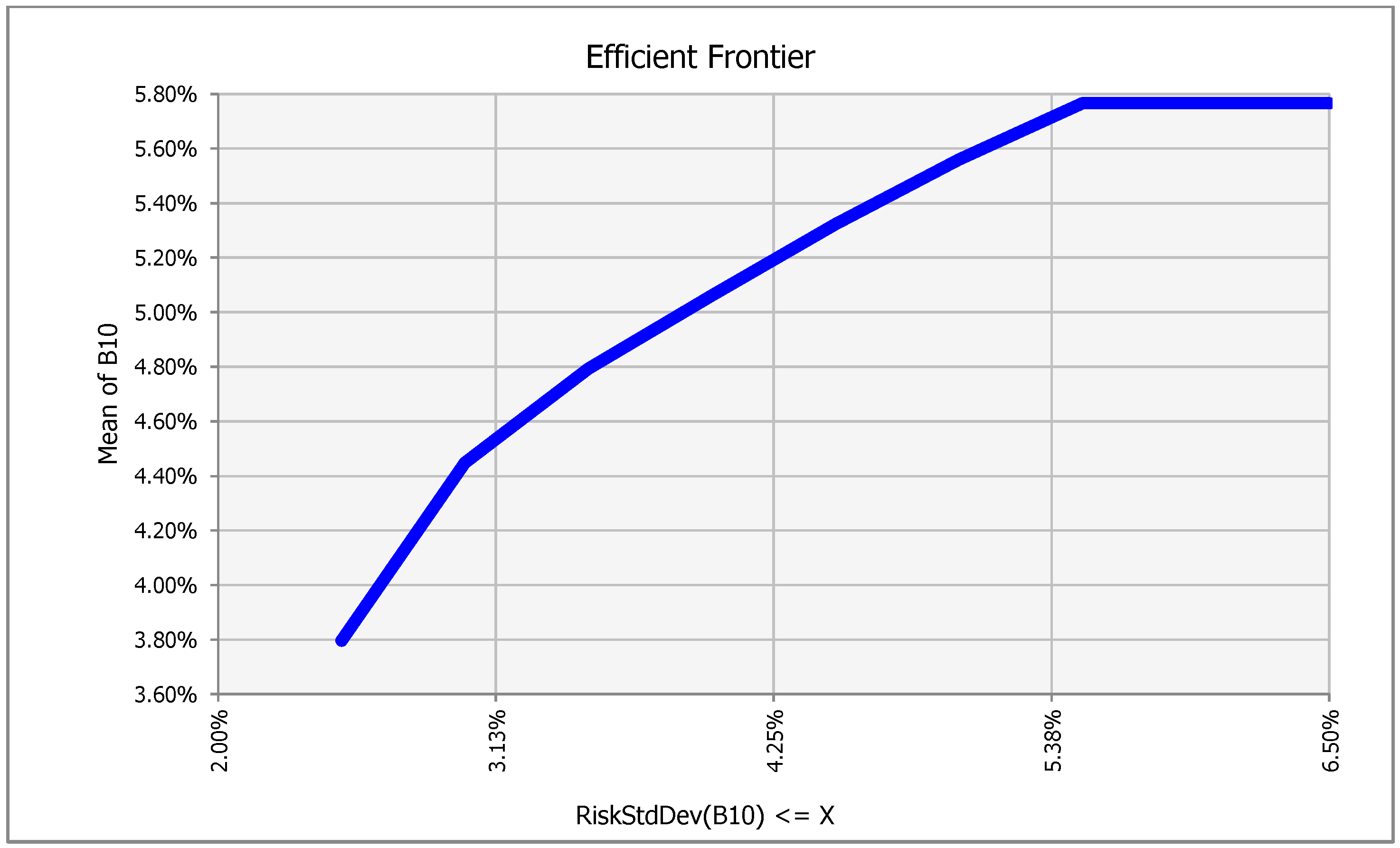

| 5.50% | 1000 | 5.77% | 4 | 5.77% | 5.45% | −11.63% | 23.53% | 0.0% | 0.0% | 100.0% | 5.45% | 1 |

| 6.00% | 1000 | 5.77% | 4 | 5.77% | 5.45% | −11.63% | 23.53% | 0.0% | 0.0% | 100.0% | 5.45% | 1 |

| 6.50% | 1000 | 5.77% | 4 | 5.77% | 5.45% | −11.63% | 23.53% | 0.0% | 0.0% | 100.0% | 5.45% | 1 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Petropoulos, T.; Liapis, K.; Thalassinos, E. Optimal Structure of Real Estate Portfolio Using EVA: A Stochastic Markowitz Model Using Data from Greek Real Estate Market. Risks 2023, 11, 43. https://doi.org/10.3390/risks11020043

Petropoulos T, Liapis K, Thalassinos E. Optimal Structure of Real Estate Portfolio Using EVA: A Stochastic Markowitz Model Using Data from Greek Real Estate Market. Risks. 2023; 11(2):43. https://doi.org/10.3390/risks11020043

Chicago/Turabian StylePetropoulos, Theofanis, Konstantinos Liapis, and Eleftherios Thalassinos. 2023. "Optimal Structure of Real Estate Portfolio Using EVA: A Stochastic Markowitz Model Using Data from Greek Real Estate Market" Risks 11, no. 2: 43. https://doi.org/10.3390/risks11020043

APA StylePetropoulos, T., Liapis, K., & Thalassinos, E. (2023). Optimal Structure of Real Estate Portfolio Using EVA: A Stochastic Markowitz Model Using Data from Greek Real Estate Market. Risks, 11(2), 43. https://doi.org/10.3390/risks11020043