Macroeconomics of Systemic Risk: Transmission Channels and Technical Integration

Abstract

:1. Introduction

2. Literature Review

2.1. Macroeconomics and Financial Crises

2.2. Basel Committee on Banking Supervision Guideline

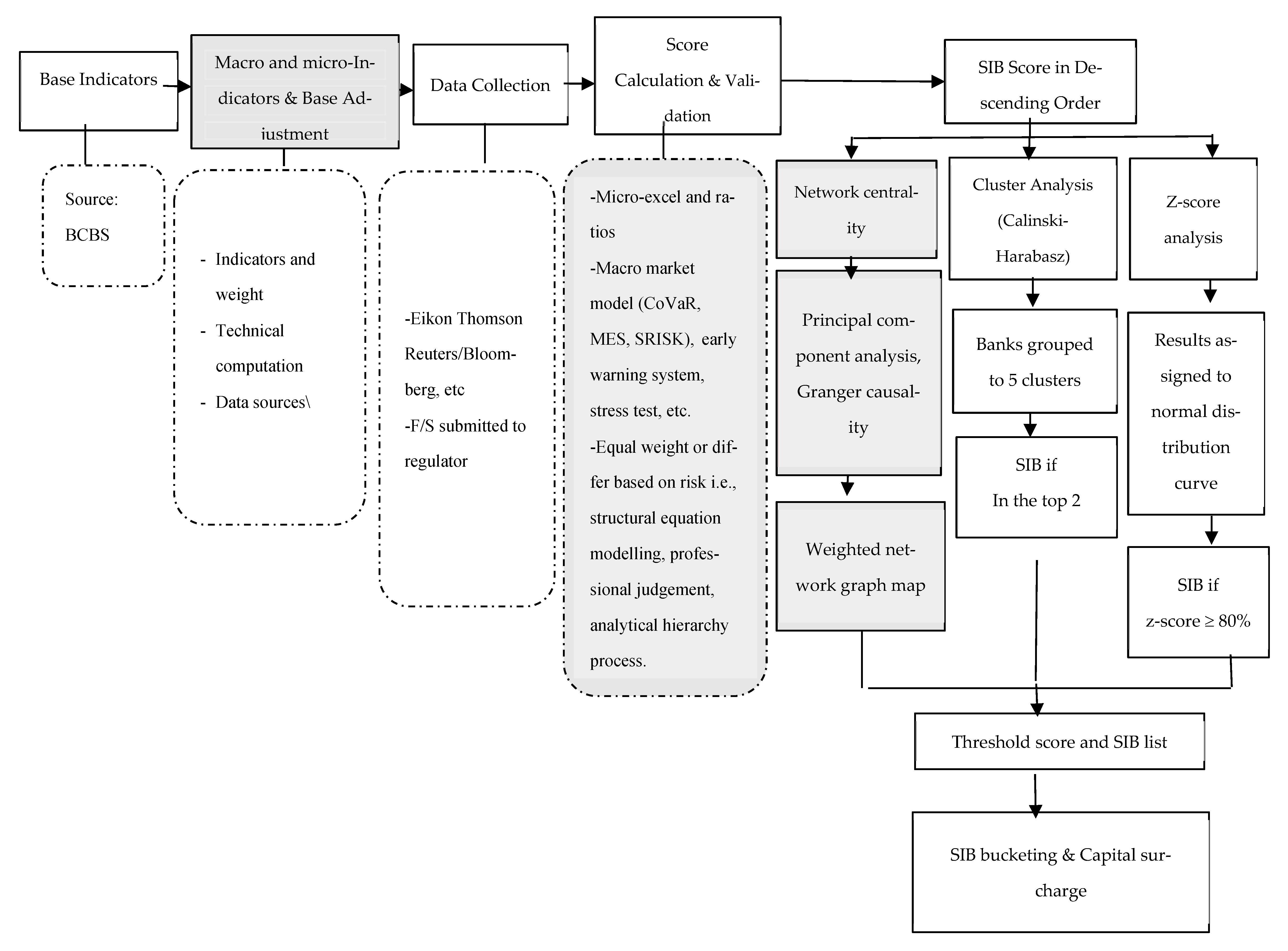

3. Data and Methodology

3.1. Source of Data

3.2. Model Estimation

3.2.1. CoVaR

- = the difference CoVaR of institution j attributed to firm i at time q with its median

- = VaR of institution j attributed to firm i return losses at time q financial distress;

- = VaR of institution j attributed to firm i return losses at time q in normal conditions (when not in crises).

3.2.2. Marginal Expected Shortfall

- = equity returns of institution;

- VaRα = institutions losses at certain confidence level;

- α = significance level.

- = the weight of group i in the total portfolio;

- = firm i’s marginal expected shortfall when the firm doing poorly.

3.2.3. SRISK

CSi,t = k(Di,t + Wi,t) – Wi,t

- CSi,t = capital shortfall of institution i at time t;

- Wi,t = market value of equity;

- Di,t = book value of debt;

- Ai,t = book value of assets;

- k = prudential capital fraction which is set to 8%.

= k Et(Di,t+h|Rm,t+1:t+h < C) − (1 − k)Et(Wi,t+h|Rm,t+1:t+h < C)

- Rm,t+1:t+h = the multiperiod market return of period t + 1 and t + h;

- C = the market decline threshold.

= Wi,t[kLVGi,t + (1 − k) LRMESi,t − 1]

- LVG = leverage ratio (Di,t + Wi,t)/Wi,t.

- LRMES = expectation of firm equity multi period returns conditional on the systemic event. Acharya et al. (2012) approximated it as 1 − exp(−18 × MES).

4. Results

4.1. Statistics Summary

4.2. Systemic Risk Based on Market Model

4.2.1. CoVaR

4.2.2. Marginal Expected Shortfall (MES)

4.2.3. SRISK

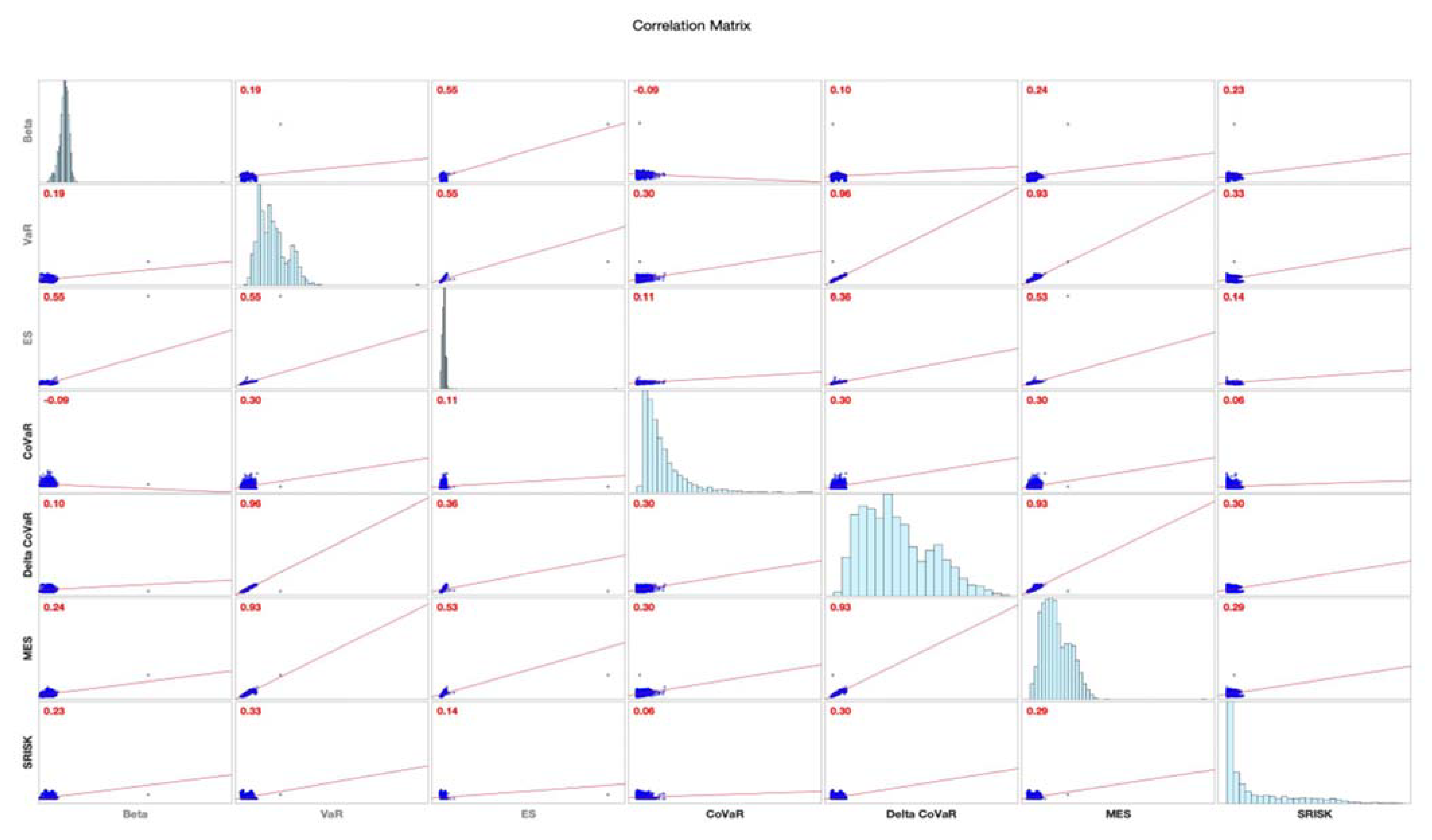

4.3. Regression Results

MES = βMESt−1 + βBETA + βEXC_R + βFFR + βΔTBILL + βJKSEVIX + βLIQSPR + βTEDSPR + ε

SRISK = βSRISKt−1 + βBETA + βEXC_R + βFFR + βΔTBILL + βJKSEVIX + βLIQSPR + βTEDSPR + ε

- Beta and market index volatility: Stock beta have a positive correlation and are statistically significant to the systemic risk in all market model estimations. In this case, the bank systemic risk swings downward or upward in the same direction as the overall market. The results also confirmed that we applied market index volatility. The investigation of using simple beta to sort the systemic bank was also suggested by Benoit et al. (2013).

- Exchange rate: The fluctuation of exchange rate could trigger and amplify the systemic risk in the economy. Its effects statistically significantly validated both the linear and ARCH models. Our findings were similar to Yesin (2013), Mayordomo et al. (2014), and de Mendonça and Silva (2018). However, they were contrary to Tram and Thi Thanh Hoai (2021). The shock of exchange rate volatility influence the banks’ assets and liabilities, especially when there is no hedging or insurance to cover the risk. The Asia Financial Crises in 1997, where Indonesia was one of severely hit economies, is a good example of the catastrophic impact of exchange rate to the banking system.

- Central bank funding and T bill rate: The outcome is statistically significant, while the effect was mixed between estimation models. CoVaR and MES reported the negative effects of FFR on the systemic risk, while SRISK reported the opposite. We suspect that the SRISK methodology, which considered the leverage effect, the outcome where bank assets sensitivity to the monetary policy interest rate changes, which was also studied by Jobst (2014) and Brunnermeier and Pedersen (2009). From another perspective, when we assessed the delta of the 3-month T bill, the implication was the same across all models. The phenomena could indicate that the banks are more sensitive to the FFR than the 3-month T bill rate, as it resembles the overnight money market of short-term liquidity resorts. Ramos-Tallada (2015) also iterated the sensitivity of banks to short-term interest rates and potential losses during the tight monetary policy.

- Liquidity spread: In general, the liquidity spread is not significantly related to the banks’ systemic risk exposure. Because we used the 3-month repo rate, the non-existence could be traced to the very limited repo transactions in the Indonesian banking market. However, the effect could be different for other countries as it very much depends on the banks’ portfolios. On the other hand, TED spread the results are quite mixed among models. CoVaR detected a negative trend for systemic risk and was in line with Ramos-Tallada (2015), while MES and SRISK perceived the change as adding more fuel to the risk (Laséen et al. 2017). Further research should explore the impact of the SRISK model on benchmark rates as it is also arguably in line with the central bank and funding rate.

4.4. Technical Integration

5. Conclusions and Policies Implication

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

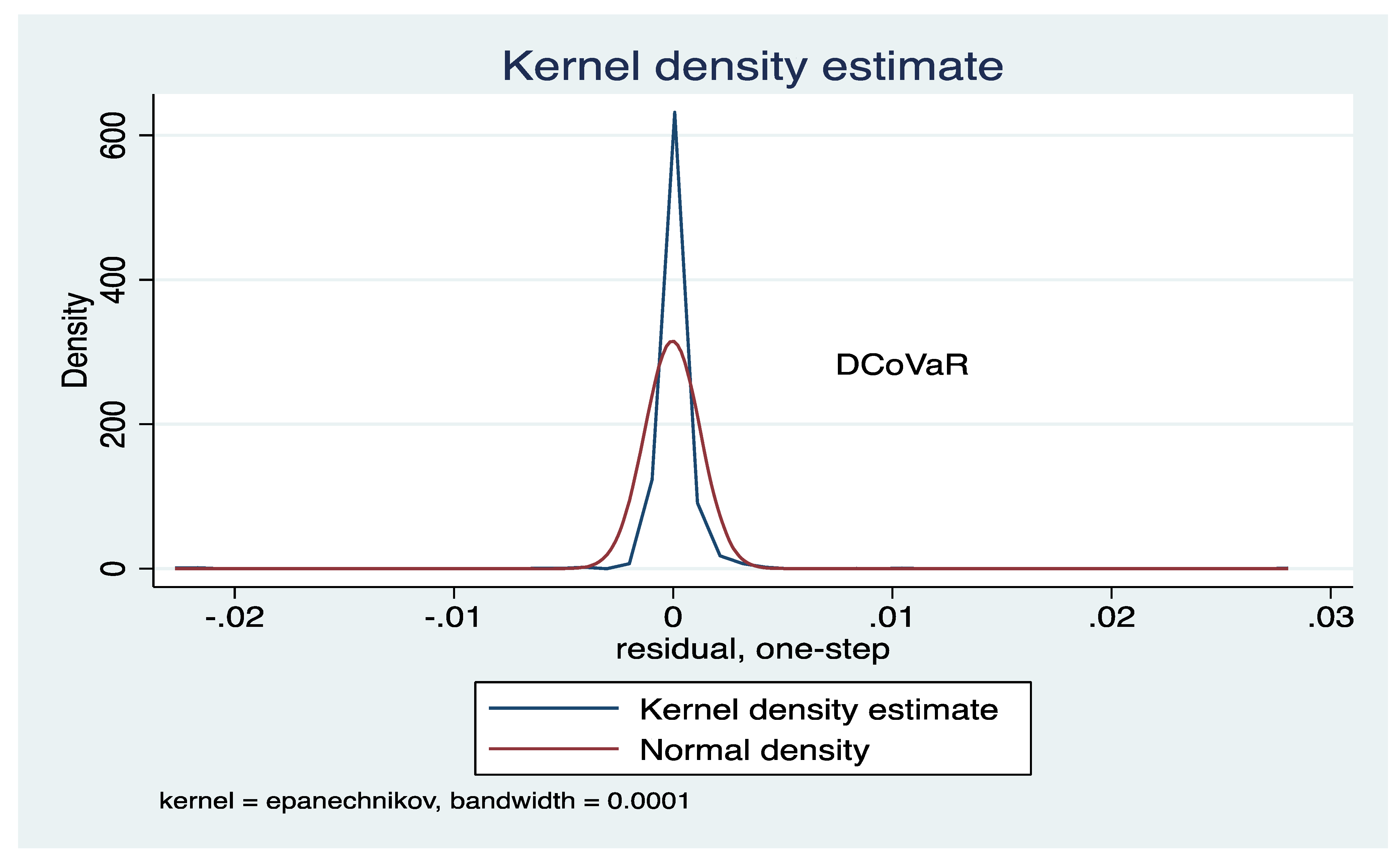

Appendix A. Robustness Test

- Pooled OLS Classical Tests

- To ensure the robustness of results, we run some tests of OLS classic assumptions. First, using Breusch Pagan to detect the heteroscedasticity in the ΔCoVaR series.Breusch–Pagan/Cook–Weisberg test for heteroskedasticityAssumption: Normal error termsVariable: Fitted values of Delta_CoVaRH0: Constant variancechi2(1) = 19.08Prob > chi2 = 0.0000

- Autocorrelation of error terms

| Lags(p) | chi2 | df | Prob > chi2 |

|---|---|---|---|

| 1 | 479.55 | 1 | 0.0000 |

- 2.

- ARIMA (1,0,1) ΔCoVaR

| DCovar_1 | Coef. | St. Err. | t-Value | p-Value | [95% Conf | Interval] | Sig |

|---|---|---|---|---|---|---|---|

| DCovar_1 | |||||||

| _cons | 0.008 | 0.008 | 1.09 | 0.277 | −0.007 | 0.023 | |

| ARMA | |||||||

| ar | |||||||

| L1. | 0.999 | 0.001 | 1773.13 | 0 | 0.998 | 1 | *** |

| ma. | |||||||

| L1. | −0.639 | 0.003 | −223.91 | 0 | −0.644 | −0.633 | *** |

| Constant | |||||||

| /sigma | 0.001 | 0 | 500.40 | 0 | 0.001 | 0.001 | *** |

| LAG | AC | PAC | Q | Prob > Q | −1 | 0 | 1 | −1 | 0 | 1 |

|---|---|---|---|---|---|---|---|---|---|---|

| [Autocor] | [Partial Autocor] | |||||||||

| 1 | −0.0374 | −0.0381 | 0.0417 | |||||||

| 2 | 0.0715 | 0.0802 | 0.0001 | |||||||

| 3 | −0.0416 | −0.0488 | 0.0000 | |||||||

| 4 | −0.0536 | −0.0769 | 0.0000 | |||||||

| 5 | −0.0938 | −0.1109 | 0.0000 | |||||||

| 6 | −0.0315 | −0.0463 | 0.0000 | |||||||

| 7 | −0.0161 | −0.0300 | 0.0000 | |||||||

| 8 | 0.0919 | 0.0907 | 0.0000 | |||||||

| 9 | 0.1099 | 0.1311 | 0.0000 | |||||||

| 10 | −0.0015 | 0.0369 | 0.0000 | |||||||

| 11 | −0.0247 | −0.0091 | 0.0000 | |||||||

| 12 | 0.0302 | 0.0573 | 0.0000 | |||||||

| 13 | −0.0602 | −0.0105 | 0.0000 | |||||||

| 14 | −0.0024 | 0.0197 | 0.0000 | |||||||

| 15 | 0.0122 | 0.0419 | 0.0000 | |||||||

| 16 | −0.0008 | 0.0170 | 0.0000 | |||||||

| 17 | 0.0279 | 0.0332 | 0.0000 | |||||||

| 18 | 0.0188 | 0.0187 | 0.0000 | |||||||

| 19 | −0.0260 | −0.0305 | 0.0000 | |||||||

| 20 | 0.0335 | 0.0405 | 0.0000 | |||||||

| 1 | |

| 2 | Adrian and Brunnermeier (2016) used commonly convention sign q > 50 to represent the median, other like Benoit et al. (2013) write it as median. |

References

- Acharya, Viral, Robert Engle, and Matthew Richardson. 2012. Capital Shortfall: A New Approach to Ranking and Regulating Systemic Risks. American Economic Review 102: 59–64. [Google Scholar] [CrossRef]

- Acharya, Viral, Lasse H. Pedersen, Thomas Philippon, and Matthew Richardson. 2017. Measuring Systemic Risks. Review of Financial Studies 30: 2–47. [Google Scholar] [CrossRef]

- Adrian, Tobias, and Markus K. Brunnermeier. 2016. CoVaR. American Economic Review 106: 1705–41. Available online: https://www.aeaweb.org/articles?id=10.1257/aer.20120555 (accessed on 29 April 2019). [CrossRef]

- Akhter, Selim, and Kevin Daly. 2017. Contagion risk for Australian banks from global systemically important banks: Evidence from extreme events. Economic Modelling 63: 191–205. [Google Scholar] [CrossRef]

- Ali, Ashgar, and Kevin Daly. 2010. Macroeconomic determinants of credit risk: Recent evidence from a cross country study. International Review of Financial Analysis 19: 165–71. [Google Scholar] [CrossRef]

- BCBS. 2011. Global Systemically Important Banks: Assessment Methodology and the Additional Loss Absorbency Requirement. Basel: Bank for International Settlements. [Google Scholar]

- BCBS. 2012. A Framework for Dealing with Domestic Systemically Important Banks. Basel: Bank for International Settlements. [Google Scholar]

- BCBS. 2018. Global Systemically Important Banks: Revised Assessment Methodology and The Higher Loss Absorbency Requirement. Basel: Bank for International Settlements. [Google Scholar]

- Belluzo, Tommaso. 2020. Systemic Risk, 3.0.0 ed. GitHub. Available online: https://github.com/TommasoBelluzzo/SystemicRisk (accessed on 13 June 2019).

- Bengtsson, Elias, Ulf Holmberg, and Kristian Jonsson. 2013. Identifying systemically important banks in Sweden—What do quantitative indicators tell us? Sveriges Riksbank Economic Review 2013: 2. Available online: http://archive.riksbank.se/Documents/Rapporter/POV/2013/2013_2/rap_pov_artikel_3_130918_eng.pdf (accessed on 29 April 2019).

- Benoit, Sylvain, Gilbert Colletaz, Christophe Hurlin, and Christophe Perignon. 2013. A Theoretical and Empirical Comparison of Systemic Risk Measures: MES versus CoVaR. SSRN Electronic Journal. [Google Scholar] [CrossRef]

- Bisias, Dimitrios, Mark Flood, Andrew W. Lo, and Stavros Valavanis. 2012. A Survey of Systemic Risk Analytics. Annual Review of Financial Economics 4: 255–96. Available online: https://www.annualreviews.org/doi/abs/10.1146/annurev-financial-110311-101754 (accessed on 27 October 2018). [CrossRef]

- Brämer, Patrick, and Horst Gischer. 2013. An Assessment Methodology for Domestic Systemically Important Banks in Australia. Australian Economic Review 46: 140–59. [Google Scholar] [CrossRef]

- Brownlees, Christian, and Robert F. Engle. 2017. SRISK: A Conditional Capital Shortfall Measure of Systemic Risk. Review of Financial Studies 30: 48–79. [Google Scholar] [CrossRef]

- Brunnermeier, Markus K., and Lasse Heje Pedersen. 2009. Market Liquidity and Funding Liquidity. Review of Financial Studies 22: 2201–38. [Google Scholar] [CrossRef] [Green Version]

- De Bandt, Olivier, and Philipp Hartmann. 2000. Systemic Risk: A Survey. Working Paper No. 35. Frankfurt: European Central Bank. Available online: https://www.ecb.europa.eu/pub/pdf/scpwps/ecbwp035.pdf (accessed on 8 August 2018).

- de Mendonça, Helder Ferreira, and Rafael Bernardo da Silva. 2018. Effect of banking and macroeconomic variables on systemic risk: An application of ΔCOVAR for an emerging economy. The North American Journal of Economics and Finance 43: 141–57. [Google Scholar] [CrossRef]

- ECB. 2009. Financial Stability Review. Frankfurt: European Central Bank, pp. 134–42. Available online: https://www.ecb.europa.eu/pub/fsr/shared/pdf/ivbfinancialstabilityreview200912en.pdf?a3fef6891f874a3bd40cd00aef38c64f (accessed on 9 December 2018).

- Festić, Mejra, Alenka Kavkler, and Sebastijan Repina. 2011. The macroeconomic sources of systemic risk in the banking sectors of five new EU member states. Journal of Banking & Finance 35: 310–22. [Google Scholar] [CrossRef]

- Glasserman, Paul, and Bert Loudis. 2015. A Comparison of US and International Global Systemically Important Banks; Washington, DC: Office of Financial Research. Available online: https://www.financialresearch.gov/briefs/files/OFRbr-2015-07_A-Comparison-of-US-and-International-Global-Systemically-Important-Banks.pdf (accessed on 24 July 2021).

- Hirtle, Beverly, Anna Kovner, James Vickery, and Meru Bhanot. 2016. Assessing financial stability: The Capital and Loss Assessment under Stress Scenarios (CLASS) model. Journal of Banking & Finance 69: S35–S55. [Google Scholar] [CrossRef]

- Hollo, Dániel, Manfred Kremer, and Duca Lo. 2012. Marco CISS—A Composite Indicator of Systemic Stress in the Financial System. Frankfurt: European Central Bank (ECB). [Google Scholar]

- Illing, Mark, and Ying Liu. 2006. Measuring financial stress in a developed country: An application to Canada. Journal of Financial Stability 2: 243–65. [Google Scholar] [CrossRef]

- Jobst, A. Andreas. 2014. Measuring systemic risk-adjusted liquidity (SRL)—A model approach. Journal of Banking & Finance 45: 270–87. [Google Scholar] [CrossRef]

- Jorion, Philippe. 2007. Value at Risk: The New Benchmark for Managing Financial Risk, 3rd ed. New York: McGraw Hill. [Google Scholar]

- Laséen, Stefan, Andrea Pescatori, and Jarkko Turunen. 2017. Systemic risk: A new trade-off for monetary policy? Journal of Financial Stability 32: 70–85. [Google Scholar] [CrossRef]

- MacDonald, Ronald, Vasilios Sogiakas, and Andreas Tsopanakis. 2018. Volatility co-movements and spillover effects within the Eurozone economies: A multivariate GARCH approach using the financial stress index. Journal of International Financial Markets, Institutions and Money 52: 17–36. [Google Scholar] [CrossRef]

- Mayordomo, Sergio, Maria Rodriguez-Moreno, and Juan Ignacio Peña. 2014. Derivatives holdings and systemic risk in the U.S. banking sector. Journal of Banking & Finance 45: 84–104. [Google Scholar] [CrossRef]

- Oet, Mikhail, John Dooley, and Stephen Ong. 2015. The Financial Stress Index: Identification of Systemic Risk Conditions. Risks 3: 420–44. [Google Scholar] [CrossRef]

- OJK. 2016. Commercial Bank Activities and Business Network based on Core Capital. POJK No. 6/POJK.03/2016. Jakarta Indonesia. Available online: https://www.ojk.go.id/id/regulasi/Pages/Perubahan-POJK-Nomor-6-POJK.03-2016-tentang-Kegiatan-Usaha-dan-Jaringan-Kantor-Berdasarkan-Modal-Inti-Bank.aspx (accessed on 8 November 2019).

- OJK. 2018. Systemically Important Banks and Capital Surcharges. POJK No. 2/POJK.03/2018. Jakarta Indonesia. Available online: https://www.ojk.go.id/id/regulasi/Documents/Pages/Penetapan-Bank-Sistemik-dan-Capital-Surcharge/POJK%202-2018.pdf (accessed on 15 April 2018).

- OJK. 2021. Commercial Banks. POJK No. 12/POJK.03/2021. Jakarta Indonesia. Available online: https://www.ojk.go.id/id/regulasi/Documents/Pages/Bank-Umum/POJK%2012%20-%2003%20-2021.pdf (accessed on 12 December 2021).

- Paltalidis, Nikos, Dimitrios Gounopoulos, Renatas Kizys, and Yiannis Koutelidakis. 2015. Transmission channels of systemic risk and contagion in the European financial network. Journal of Banking & Finance 61: S36–S52. [Google Scholar] [CrossRef] [Green Version]

- Ramos-Tallada, Julio. 2015. Bank risks, monetary shocks and the credit channel in Brazil: Identification and evidence from panel data. Journal of International Money and Finance 55: 135–61. [Google Scholar] [CrossRef]

- Salim, Muhammad Zulkifli, and Kevin Daly. 2021. Modelling Systemically Important Banks vis-à-vis the Basel Prudential Guidelines. Journal of Risk and Financial Management 14: 295. [Google Scholar] [CrossRef]

- Schleer, Frauke, and Willi Semmler. 2015. Financial sector and output dynamics in the euro area: Non-linearities reconsidered. Journal of Macroeconomics 46: 235–63. [Google Scholar] [CrossRef]

- Tram, Thi, Xuan Hong, and Nguyen Thi Thanh Hoai. 2021. Effect of macroeconomic variables on systemic risk: Evidence from Vietnamese economy. Economics and Business Letters 10: 217–28. [Google Scholar] [CrossRef]

- Yesin, Pinar. 2013. Foreign Currency Loan and Systemic Risk in Europe. St. Louis: Federal Reserve Bank of St. Louis., Missouri United States, vol. 95, pp. 219–35. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

| Study | Specific Indicators | Estimation Method | Geographical Areas Covered | Results |

|---|---|---|---|---|

| de Mendonça and Silva (2018) | Bank liquidity, profitability, leverage, total deposit, ROA, policy rate, exchange rate, and GDP | CoVaR regressed using D-GMM and S-GMM | Brazilian bank over 2011–2015. | The leverage increases the systemic risk, higher returns, and rise of monetary policy rate amplify the systemic risk. The bank liquidity lowers the systemic risk. |

| Tram and Thi Thanh Hoai (2021) | Leverage, ROA, monetary policy rate, variation of exchange rate, and GDP growth. | regressed using OLS, REM, FEM and S-GMM | Vietnam financial institutions over 2010–2018 | High exchange rate and low interest rate decrease systemic risk, while economic growth increase the systemic risk. |

| Yesin (2013) | Unhedged foreign currency loan | Foreign currency, CHF mismatch index | 17 countries in Eurozone area over 2007–2011. | Net unhedged foreign currency liabilities contribute to systemic risk |

| Festić et al. (2011) | Non-performing loan, credit growth, GDP growth, foreign debt, inflation, FDI. | Panel regression FE and REM. | 5 EU member countries | Credit growth harm bank performance while credit/asset ratio increases the dynamic of NPL. |

| Akhter and Daly (2017) | The default rates, GDP, 6-mth T-bill, industrial production, debt to GDP ratio | Distance to default using logit regression model | 8 Australian banks from 2006–2014 | Extreme shocks from foreign banks are contagious to Australian banks. Contingency funding and extra liquidity measures are needed to monitor. |

| Illing and Liu (2006) | Banking sector beta, liquidity spread, corporate bond spread, covered interest rate spread, inverted yield curve, weighted dollar crashes, stock market crashes, covered bond T-bill spread | Credit weights, GARCH | Canada form 1980–2004 | Accurate characterization of stress is the prerequisite to forecast financial crises |

| Mayordomo et al. (2014) | Size, Interconnectedness, and substitutability, | ΔCoVaR, ΔCoES, Asymmetric ΔCoVaR, Gross Shapley Value, Net Shapley Value. Analysed using Correlation index and Granger causality. | 95 US banks holding companies from 2002–2011 | Net Shapley Value outperform other models. Derivatives holding is a leading indicator of systemic risk contribution. |

| Ramos-Tallada (2015) | Money market rate, liquidity ratio, capital ratio, long term borrowing, size, and ownership, NPL, volatility, GDP, inflation | VAR, OLS, FEM, GMM | Brazilian bank between 1995–2012. | GDP growth positively correlated credit in demand. Compulsory bank reserve has a negative impact to reduce excess demand. Money market rate affects the lending supply. |

| No. | Ticker | Bank | KBMI |

|---|---|---|---|

| 1 | BBCA | PT. Bank Central Asia Tbk. | 4 |

| 2 | BBRI | PT. Bank Rakyat Indonesia (Persero) Tbk. | 4 |

| 3 | BMRI | PT. Bank Mandiri (Persero) Tbk. | 4 |

| 4 | BBNI | PT. Bank Negara Indonesia (Persero) Tbk. | 4 |

| 5 | MEGA | PT. Bank Mega Tbk. | 3 |

| 6 | MAYA | PT. Bank Mayapada Internasional Tbk. | 3 |

| 7 | BNLI | PT. Bank Permata Tbk. | 3 |

| 8 | BDMN | PT. Bank Danamon Indonesia Tbk. | 3 |

| 9 | PNBN | PT. Bank Pan Indonesia Tbk. | 3 |

| 10 | NISP | PT. Bank OCBC NISP Tbk. | 3 |

| 11 | BNGA | PT. Bank CIMB Niaga Tbk. | 3 |

| 12 | BTPN | PT. Bank BTPN Tbk. | 3 |

| 13 | BNII | PT. Bank Maybank Indonesia Tbk. | 3 |

| 14 | BJBR | PT. Bank Pembangunan Daerah Jawa Barat Tbk. | 2 |

| 15 | BBTN | PT. Bank Tabungan Negara (Persero) Tbk. | 3 |

| 16 | BSIM | PT. Bank Sinarmas Tbk. | 1 |

| 17 | BJTM | PT. Bank Pembangunan Daerah Jawa Timur Tbk. | 2 |

| 18 | SDRA | PT. Bank Woori Saudara Indonesia Tbk. | 2 |

| 19 | BACA | PT. Bank Capital Indonesia Tbk. | 1 |

| 20 | AGRO | PT. BRI Agroniaga Tbk. | 1 |

| 21 | CCBI | PT. Bank China Construction Indonesia Tbk. | 1 |

| 22 | BBKP | PT. Bank Bukopin Tbk. | 2 |

| 23 | BABP | PT. Bank MNC Internasional Tbk. | 1 |

| 24 | BKSW | PT. Bank QNB Indonesia Tbk. | 1 |

| 25 | INPC | PT. Bank Artha Graha Internasional Tbk. | 1 |

| 26 | BNBA | PT. Bank Bumi Arta Tbk. | 1 |

| 27 | BVIC | PT. Bank Victoria Internasional Tbk. | 1 |

| N | Mean | Min | Max | SD | Variance | Kurtosis | |

|---|---|---|---|---|---|---|---|

| Beta | 50,328 | 0.631 | −3.821 | 6.539 | 0.572 | 0.327 | 6.614 |

| DCOVAR | 50,328 | 0 | 0.000 | 0 | 0 | 0 | 5.983 |

| MES | 50,328 | 0.014 | 0.000 | 0.117 | 0.01 | 0 | 5.954 |

| SRISK | 50,328 | 7.32 × 105 | 0.000 | 3.61 × 107 | 2.41 × 106 | 5.82 × 1012 | 47.347 |

| EXC RATE | 50,328 | 1.27 × 104 | 9.45 × 103 | 1.52 × 104 | 1.52 × 103 | 2.33 × 106 | 2.796 |

| FFR | 50,328 | 6.078 | 4.250 | 7.75 | 1.159 | 1.343 | 1.633 |

| TBILL DELTA | 50,328 | −0.004 | −65.220 | 67.33 | 13.029 | 169.746 | 6.188 |

| JKSE VIX | 50,328 | 10.407 | 0.010 | 92.02 | 10.346 | 107.047 | 10.39 |

| LIQ SPR | 50,328 | 1.244 | −0.110 | 3.13 | 0.591 | 0.349 | 2.91 |

| TED SPR | 50,328 | 4.443 | 1.900 | 6.54 | 1.186 | 1.406 | 1.783 |

| Variables | (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | (9) | (10) | (11) | (12) | (13) | (14) |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| (1) Beta | 1.000 | |||||||||||||

| (2) COVAR | −0.045 * | 1.000 | ||||||||||||

| (0.000) | ||||||||||||||

| (3) DCOVAR | 0.678 * | 0.030 * | 1.000 | |||||||||||

| (0.000) | (0.000) | |||||||||||||

| (4) MES | 0.848 * | 0.071 * | 0.644 * | 1.000 | ||||||||||

| (0.000) | (0.000) | (0.000) | ||||||||||||

| (5) SRISK | 0.478 * | −0.012 * | 0.335 * | 0.358 * | 1.000 | |||||||||

| (0.000) | (0.005) | (0.000) | (0.000) | |||||||||||

| (6) DCOVAR_1 | 0.040 * | 0.007 | 0.022 * | 0.076 * | 0.005 | 1.000 | ||||||||

| (0.000) | (0.108) | (0.000) | (0.000) | (0.292) | ||||||||||

| (7) MES_1 | −0.003 | 0.003 | −0.014 * | 0.001 | −0.006 | 0.181 * | 1.000 | |||||||

| (0.559) | (0.465) | (0.001) | (0.811) | (0.160) | (0.000) | |||||||||

| (8) SRISK_1 | 0.005 | −0.004 | 0.000 | 0.004 | 0.003 | 0.008 | 0.002 | 1.000 | ||||||

| (0.295) | (0.343) | (0.967) | (0.406) | (0.537) | (0.057) | (0.696) | ||||||||

| (9) EXC_RATE | 0.050 * | −0.060 * | −0.006 | 0.041 * | 0.146 * | 0.005 | 0.004 | 0.006 | 1.000 | |||||

| (0.000) | (0.000) | (0.149) | (0.000) | (0.000) | (0.262) | (0.361) | (0.181) | |||||||

| (10) FFR | −0.025 * | 0.113 * | 0.017 * | 0.082 * | −0.015 * | −0.004 | −0.001 | −0.007 | −0.205 * | 1.000 | ||||

| (0.000) | (0.000) | (0.000) | (0.000) | (0.001) | (0.375) | (0.844) | (0.123) | (0.000) | ||||||

| (11) TBILL_DELTA | 0.001 | −0.015 * | 0.001 | 0.006 | 0.000 | 0.009 * | 0.002 | 0.004 | 0.000 | −0.002 | 1.000 | |||

| (0.899) | (0.001) | (0.739) | (0.201) | (0.943) | (0.040) | (0.649) | (0.328) | (0.970) | (0.664) | |||||

| (12) JKSE_VIX | −0.058 * | 0.162 * | 0.039 * | 0.100 * | −0.021 * | −0.007 | −0.002 | −0.004 | −0.057 * | 0.119 * | −0.630 * | 1.000 | ||

| (0.000) | (0.000) | (0.000) | (0.000) | (0.000) | (0.127) | (0.632) | (0.320) | (0.000) | (0.000) | (0.000) | ||||

| (13) LIQ_SPR | 0.031 * | −0.005 | 0.009 * | 0.060 * | 0.030 * | −0.002 | 0.000 | 0.000 | 0.249 * | 0.340 * | −0.011 * | 0.014 * | 1.000 | |

| (0.000) | (0.311) | (0.042) | (0.000) | (0.000) | (0.600) | (0.951) | (0.952) | (0.000) | (0.000) | (0.012) | (0.002) | |||

| (14) TED_SPR | −0.013 * | 0.107 * | 0.019 * | 0.094 * | −0.040 * | −0.002 | −0.003 | −0.008 | −0.252 * | 0.818 * | 0.004 | 0.105 * | 0.208 * | 1.000 |

| (0.004) | (0.000) | (0.000) | (0.000) | (0.000) | (0.732) | (0.457) | (0.089) | (0.000) | (0.000) | (0.388) | (0.000) | (0.000) |

| Banks | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | ||||||

| % to Sys | Rank | % to Sys | Rank | % to Sys | Rank | % to Sys | Rank | % to Sys | Rank | % to Sys | Rank | |

| BCA | 30.0% | 2 | 25.4% | 1 | 26.6% | 1 | 21.7% | 2 | 30.9% | 1 | 25.1% | 1 |

| BRI | 15.8% | 3 | 9.0% | 4 | 9.7% | 4 | 10.1% | 5 | 6.4% | 6 | 10.7% | 3 |

| BMRI | 30.9% | 1 | 17.0% | 2 | 19.7% | 2 | 22.4% | 1 | 16.9% | 2 | 22.5% | 2 |

| BNI | 6.1% | 4 | 9.2% | 3 | 8.5% | 5 | 10.2% | 4 | 8.1% | 4 | 8.7% | 4 |

| MEGA | 1.1% | 8.0% | 5 | 1.8% | 2.0% | 2.1% | 1.7% | |||||

| BDMN | 1.5% | 1.6% | 2.0% | 1.7% | 1.4% | 2.1% | ||||||

| PNBN | 0.9% | 1.2% | 1.0% | 1.5% | 1.1% | 1.1% | ||||||

| BJBR | 3.5% | 5.7% | 6 | 10.5% | 3 | 10.3% | 3 | 11.4% | 3 | 7.3% | 5 | |

| BTN | 0.0% | 1.2% | 3.0% | 2.2% | 2.3% | 3.1% | ||||||

| BSIM | 0.4% | 0.6% | 5.0% | 6 | 3.2% | 1.2% | 0.8% | |||||

| BJTM | 0.1% | 0.1% | 0.1% | 0.2% | 7.1% | 5 | 6.2% | 6 | ||||

| SDRA | 1.4% | 2.9% | 2.1% | 2.9% | 2.4% | 2.3% | ||||||

| BACA | 2.1% | 3.6% | 3.5% | 4.1% | 2.6% | 2.5% | ||||||

| AGRO | 0.2% | 1.1% | 0.5% | 0.5% | 0.5% | 0.6% | ||||||

| CCBI | 1.5% | 4.4% | 0.7% | 0.4% | 0.3% | 0.7% | ||||||

| BBKP | 1.7% | 2.2% | 2.1% | 3.2% | 2.0% | 2.2% | ||||||

| MNC | 1.2% | 4.3% | 1.7% | 2.1% | 1.8% | 1.0% | ||||||

| Others—10 banks | 1.5% | 2.5% | 1.3% | 1.3% | 1.3% | 1.5% | ||||||

| Banks | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | ||||||

| % to Sys | Rank | % to Sys | Rank | % to Sys | Rank | % to Sys | Rank | % to Sys | Rank | % to Sys | Rank | |

| BCA | 19.0% | 2 | 24.7% | 1 | 14.9% | 3 | 20.1% | 1 | 20.6% | 1 | 19.7% | 1 |

| BRI | 9.9% | 4 | 11.3% | 3 | 7.0% | 5 | 9.3% | 5 | 7.9% | 5 | 7.5% | 5 |

| BMRI | 19.4% | 1 | 20.9% | 2 | 14.0% | 4 | 16.9% | 2 | 18.9% | 2 | 15.2% | 3 |

| BNI | 11.4% | 3 | 8.6% | 5 | 6.7% | 6 | 10.5% | 3 | 10.2% | 4 | 9.6% | 4 |

| MEGA | 2.2% | 1.6% | 1.3% | 3.2% | 2.4% | 1.9% | ||||||

| BDMN | 2.0% | 1.9% | 1.3% | 3.7% | 1.8% | 1.8% | ||||||

| PNBN | 1.4% | 1.1% | 0.9% | 1.3% | 1.6% | 1.4% | ||||||

| BJBR | 9.7% | 5 | 8.9% | 4 | 23.5% | 1 | 9.4% | 4 | 11.9% | 3 | 16.9% | 2 |

| BTN | 2.9% | 1.4% | 2.6% | 2.2% | 3.2% | 2.5% | ||||||

| BSIM | 1.5% | 1.4% | 0.8% | 5.0% | 2.5% | 2.6% | ||||||

| BJTM | 7.9% | 6 | 6.3% | 6 | 17.2% | 2 | 6.5% | 6 | 7.0% | 6 | 6.0% | 6 |

| SDRA | 2.8% | 2.2% | 1.7% | 2.6% | 3.3% | 5.7% | 7 | |||||

| BACA | 3.4% | 3.2% | 1.9% | 2.8% | 3.4% | 2.5% | ||||||

| BBKP | 2.3% | 1.8% | 2.3% | 2.6% | 2.5% | 2.7% | ||||||

| MNC | 1.3% | 1.2% | 1.1% | 1.0% | 0.8% | 0.8% | ||||||

| Others—12 banks | 2.9% | 3.5% | 2.6% | 2.8% | 2.2% | 3.1% | ||||||

| Banks | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | ||||||

| % to Sys | Rank | % to Sys | Rank | % to Sys | Rank | % to Sys | Rank | % to Sys | Rank | % to Sys | Rank | |

| BCA | 10.77% | 3 | 8.00% | 4 | 7.12% | 5 | 5.29% | 8 | 9.79% | 1 | 6.77% | 6 |

| BRI | 16.51% | 1 | 6.99% | 6 | 8.00% | 2 | 6.52% | 6 | 5.62% | 7 | 8.45% | 2 |

| BMRI | 15.55% | 2 | 7.50% | 5 | 8.33% | 1 | 7.06% | 5 | 7.76% | 3 | 7.75% | 3 |

| BNI | 9.88% | 4 | 13.02% | 1 | 6.89% | 6 | 10.18% | 1 | 1.20% | 10.51% | 1 | |

| BDMN | 6.67% | 6 | 6.77% | 7 | 7.75% | 3 | 4.56% | 6.50% | 5 | 6.93% | 4 | |

| PNBN | 8.37% | 5 | 6.60% | 9 | 6.74% | 7 | 8.01% | 2 | 9.74% | 2 | 6.91% | 5 |

| BTPN | 1.20% | 5.10% | 11 | 3.31% | 5.77% | 7 | 4.05% | 4.23% | ||||

| Maybank | 1.38% | 5.01% | 12 | 3.61% | 4.16% | 3.34% | 2.56% | |||||

| BJBR | 0.64% | 0.95% | 6.42% | 8 | 4.99% | 5.80% | 6 | 3.14% | ||||

| BTN | 0.09% | 2.92% | 7.63% | 4 | 4.65% | 4.28% | 5.77% | 7 | ||||

| BSIM | 0.19% | 0.28% | −0.45% | 7.63% | 3 | 2.57% | 0.71% | |||||

| SDRA | 4.41% | 5.81% | 10 | 4.56% | 5.28% | 9 | 3.80% | 3.89% | ||||

| AGRO | 2.83% | 6.79% | 7 | 3.41% | 2.41% | 3.92% | 2.18% | |||||

| BBKP | 5.66% | 7 | 6.77% | 8 | 5.32% | 9 | 7.17% | 4 | 7.00% | 4 | 5.22% | 8 |

| MNC | 2.44% | 9.24% | 2 | 1.19% | 0.07% | 3.45% | 3.78% | |||||

| BAG | 0.98% | 4.98% | 3.59% | 5.16% | 10 | 1.78% | 2.08% | |||||

| BNBA | 3.94% | 3.47% | 2.11% | 2.27% | 2.25% | 1.65% | ||||||

| BVIC | 3.47% | 8.75% | 3 | 3.38% | 3.88% | 4.45% | 4.00% | |||||

| Others—9 banks | 8.92% | −5.51% | 13.17% | 7.22% | 13.43% | 12.30% | ||||||

| Banks | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | ||||||

| % to Sys | Rank | % to Sys | Rank | % to Sys | Rank | % to Sys | Rank | % to Sys | Rank | % to Sys | Rank | |

| BCA | 5.27% | 7 | 7.49% | 4 | 4.07% | 6.27% | 4 | 4.45% | 5.21% | 9 | ||

| BRI | 7.90% | 2 | 9.89% | 2 | 6.01% | 6 | 8.14% | 3 | 6.36% | 6 | 5.77% | 7 |

| BMRI | 7.02% | 3 | 8.72% | 3 | 5.58% | 8 | 5.83% | 6 | 7.33% | 3 | 5.50% | 8 |

| BNI | 12.10% | 1 | 10.80% | 1 | 8.33% | 1 | 12.23% | 2 | 11.22% | 1 | 10.36% | 2 |

| MEGA | 1.93% | 1.39% | 0.48% | 6.16% | 5 | 3.07% | 2.04% | |||||

| BDMN | 6.75% | 4 | 6.69% | 5 | 6.03% | 5 | 17.08% | 1 | 6.83% | 5 | 6.05% | 5 |

| PNBN | 6.54% | 5 | 5.14% | 8 | 4.94% | 1.81% | 5.99% | 7 | 6.88% | 4 | ||

| BTPN | 3.84% | 2.63% | 1.97% | 3.96% | 3.70% | 3.91% | ||||||

| BJBR | 4.68% | 4.75% | 5.10% | 9 | −0.61% | 2.61% | −0.28% | |||||

| BTN | 6.43% | 6 | 3.10% | 7.27% | 3 | 3.04% | 8.08% | 2 | 5.21% | 10 | ||

| BJTM | 2.57% | 3.19% | 7.01% | 4 | 0.73% | 1.91% | 1.79% | |||||

| SDRA | 4.12% | 2.65% | 2.03% | 2.79% | 1.97% | 3.92% | ||||||

| BACA | 1.62% | 5.18% | 7 | 4.12% | 2.38% | 2.55% | 2.17% | |||||

| BNGA | 2.55% | 1.67% | 3.20% | 2.26% | 3.69% | 3.95% | ||||||

| AGRO | 3.25% | 3.16% | 7.94% | 2 | 3.85% | 3.46% | 8.88% | 3 | ||||

| BBKP | 4.96% | 4.13% | 5.78% | 7 | 5.06% | 7 | 5.95% | 8 | 5.82% | 6 | ||

| MNC | 3.73% | 5.65% | 6 | 4.15% | 2.55% | 1.31% | 1.35% | |||||

| BVIC | 2.10% | 4.04% | 2.92% | 3.89% | 6.96% | 4 | 12.75% | 1 | ||||

| Others—9 banks | 12.64% | 9.71% | 13.06% | 12.60% | 12.56% | 8.70% | ||||||

| Banks | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | ||||||

| % to Sys | Rank | % to Sys | Rank | % to Sys | Rank | % to Sys | Rank | % to Sys | Rank | % to Sys | Rank | |

| BMRI | 31.14% | 1 | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | |||||

| BNI | 29.17% | 2 | 16.13% | 3 | 0.00% | 7.43% | 3 | 0.00% | 39.87% | 1 | ||

| BNLI | 11.30% | 4 | 24.24% | 2 | 31.85% | 2 | 27.93% | 2 | 0.00% | 0.00% | ||

| PNBN | 0.00% | 0.00% | 0.00% | 2.47% | 70.17% | 1 | 22.02% | 3 | ||||

| BNGA | 24.61% | 3 | 44.70% | 1 | 67.64% | 1 | 49.54% | 1 | 0.00% | 0.00% | ||

| BJBR | 0.00% | 13.67% | 4 | 0.00% | 0.00% | 3.83% | 0.00% | |||||

| BTN | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | 26.72% | 2 | |||||

| BJTM | 0.00% | 0.00% | 0.00% | 5.75% | 4 | 0.00% | 0.00% | |||||

| BBKP | 2.81% | 0.00% | 0.00% | 4.04% | 18.48% | 2 | 4.55% | |||||

| BAG | 0.88% | 1.26% | 0.51% | 2.45% | 1.95% | 2.56% | ||||||

| BVIC | 0.00% | 0.00% | 0.00% | 0.39% | 5.57% | 3 | 4.29% | |||||

| OTHERS—16 BANKS | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | ||||||

| Banks | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | ||||||

| % to Sys | Rank | % to Sys | Rank | % to Sys | Rank | % to Sys | Rank | % to Sys | Rank | % to Sys | Rank | |

| BNI | 0.00% | 23.91% | 2 | 26.65% | 2 | 26.11% | 2 | 40.78% | 1 | 49.14% | 1 | |

| BNGA | 19.62% | 2 | 26.94% | 1 | 12.77% | 4 | 0.00% | 11.45% | 4 | 10.52% | 4 | |

| BTPN | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | 1.97% | ||||||

| Maybank | 0.00% | 7.52% | 5 | 0.00% | 0.00% | 0.26% | 1.44% | |||||

| BJBR | 16.16% | 3 | 10.77% | 4 | 0.00% | 0.00% | 0.00% | 0.00% | ||||

| BTN | 43.27% | 1 | 13.48% | 3 | 28.09% | 1 | 0.00% | 28.55% | 2 | 20.15% | 2 | |

| BBKP | 1.84% | 6.62% | 6 | 13.36% | 3 | 52.75% | 1 | 13.36% | 3 | 10.94% | 3 | |

| BAG | 9.18% | 4 | 5.30% | 7 | 3.81% | 14.51% | 3 | 2.38% | 1.79% | |||

| BNBA | 0.93% | 0.32% | 0.46% | 0.00% | 0.00% | 0.00% | ||||||

| BVIC | 8.19% | 5 | 5.13% | 8 | 4.37% | 6.63% | 4 | 3.22% | 3.35% | |||

| BACA | 0.81% | 0.00% | 0.58% | 0.00% | 0.00% | 0.00% | ||||||

| AGRO | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | 0.70% | ||||||

| PNBN | 0.00% | 0.00% | 9.90% | 0.00% | 0.00% | 0.00% | ||||||

| OTHERS—14 BANKS | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | ||||||

| Mean | Max | Min | St.Dev | Kurtosis | Skewness | ||

|---|---|---|---|---|---|---|---|

| 2012 | KBMI 4 | 1.175 | 1.571 | 0.803 | 0.177 | −0.724 | −0.162 |

| KBMI 3 | 0.578 | 0.664 | 0.484 | 0.043 | −0.698 | 0.161 | |

| KBMI 2 | 0.588 | 0.880 | 0.440 | 0.087 | 0.728 | 0.928 | |

| KBMI 1 | 0.325 | 0.617 | 0.202 | 0.063 | 3.372 | 0.945 | |

| 2013 | KBMI 4 | 1.214 | 1.765 | 0.718 | 0.228 | −0.664 | 0.347 |

| KBMI 3 | 0.510 | 0.841 | 0.317 | 0.113 | 0.231 | 0.756 | |

| KBMI 2 | 0.507 | 0.907 | 0.216 | 0.149 | 0.162 | 0.268 | |

| KBMI 1 | 0.248 | 0.456 | 0.145 | 0.060 | 0.861 | 1.101 | |

| 2014 | KBMI 4 | 1.715 | 2.356 | 1.419 | 0.163 | 0.723 | 0.528 |

| KBMI 3 | 0.560 | 0.763 | 0.395 | 0.080 | −0.678 | −0.101 | |

| KBMI 2 | 0.538 | 0.794 | 0.410 | 0.061 | 0.854 | 0.493 | |

| KBMI 1 | 0.332 | 0.584 | 0.181 | 0.064 | 0.477 | 0.323 | |

| 2015 | KBMI 4 | 1.463 | 1.855 | 1.061 | 0.160 | −0.342 | −0.358 |

| KBMI 3 | 0.495 | 0.753 | 0.277 | 0.081 | −0.013 | 0.204 | |

| KBMI 2 | 0.447 | 0.761 | 0.267 | 0.089 | 0.328 | 0.496 | |

| KBMI 1 | 0.343 | 0.629 | 0.173 | 0.086 | 0.214 | 0.628 | |

| 2016 | KBMI 4 | 1.446 | 1.893 | 0.987 | 0.206 | −0.742 | 0.059 |

| KBMI 3 | 0.602 | 1.137 | 0.388 | 0.125 | 1.399 | 0.831 | |

| KBMI 2 | 0.569 | 1.360 | 0.315 | 0.156 | 4.291 | 1.696 | |

| KBMI 1 | 0.452 | 1.248 | 0.200 | 0.165 | 5.292 | 1.917 | |

| 2017 | KBMI 4 | 1.506 | 1.845 | 1.116 | 0.154 | −0.377 | −0.324 |

| KBMI 3 | 0.658 | 1.260 | 0.018 | 0.165 | 3.426 | −0.653 | |

| KBMI 2 | 0.560 | 1.116 | 0.022 | 0.177 | 2.134 | −0.533 | |

| KBMI 1 | 0.550 | 0.994 | 0.240 | 0.139 | 0.604 | 0.766 | |

| 2018 | KBMI 4 | 1.390 | 1.825 | 0.631 | 0.240 | 1.738 | −1.151 |

| KBMI 3 | 0.511 | 0.810 | 0.117 | 0.103 | 3.205 | −1.402 | |

| KBMI 2 | 0.322 | 0.604 | 0.098 | 0.099 | −0.230 | 0.361 | |

| KBMI 1 | 0.363 | 0.509 | 0.200 | 0.065 | −0.674 | −0.210 | |

| 2019 | KBMI 4 | 1.596 | 1.959 | 1.170 | 0.145 | −0.210 | −0.542 |

| KBMI 3 | 0.704 | 1.048 | 0.462 | 0.115 | −0.009 | 0.515 | |

| KBMI 2 | 0.609 | 1.430 | 0.375 | 0.126 | 7.732 | 1.466 | |

| KBMI 1 | 0.418 | 0.637 | 0.300 | 0.071 | −0.217 | 0.651 |

| . | Panel A. DCoVaR | Panel B. MES | Panel C. SRISK | ||||||

|---|---|---|---|---|---|---|---|---|---|

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | (9) | |

| FE FE_DCoVaR | RE GLS RE.GLS_DCoVaR | RE MLS RE.MLS_DCoVaR | FE FE_MES | RE GLS RE.GLS_DCoVaR | RE MLS RE.MLS_DCoVaR | FE FE_MES | RE GLS RE.GLS_DCoVaR | RE MLS RE.MLS_DCoVaR | |

| DCOVAR_1 | 0 *** | 0 *** | 0 | ||||||

| (23.99) | (23.96) | (−0.7) | |||||||

| MES_1 | - | - | - | 0 *** | 0 *** | 0 *** | |||

| (5.56) | (5.56) | (5.56) | |||||||

| SRISK_1 | - | - | - | - | - | - | −0.01 | −0.01 | −0.01 |

| (−0.71) | (−0.71) | (−0.71) | |||||||

| Beta | 0 *** | 0 *** | 0 | 0.02*** | 0.02 *** | 0.02 *** | 20.50 *** | 20.49 *** | 20.49 *** |

| (55.49) | (55.62) | (253.85) | (254.34) | (254.35) | (88.44) | (88.52) | (88.53) | ||

| EXC_RATE | 0 *** | 0 *** | 0 *** | 0 *** | 0 *** | 0 *** | 0 *** | 0 *** | 0 *** |

| (−5.05) | (−5.05) | (−13.46) | (16.74) | (16.74) | (16.74) | (38.97) | (38.97) | (38.98) | |

| FFR | 0 | 0 | 0 *** | 0 *** | 0 *** | 0 *** | 1.91 *** | 1.91 *** | 1.91 *** |

| (0.47) | (0.48) | (8.86) | (9.7) | (9.7) | (9.7) | (16.12) | (16.12) | (16.12) | |

| TBILL_DELTA | 0 *** | 0 *** | 0 *** | 0 *** | 0 *** | 0 *** | 0.02 *** | 0.02 *** | 0.02 *** |

| (30.6) | (30.59) | (33.44) | (63.62) | (63.62) | (63.63) | (3.28) | (3.28) | (3.28) | |

| JKSE_VIX | 0 *** | 0 *** | 0 *** | 0 *** | 0 *** | 0 *** | 0.05 *** | 0.05 *** | 0.05 *** |

| (46.88) | (46.87) | (52.02) | (96.6) | (96.6) | (96.61) | (5.09) | (5.09) | (5.09) | |

| LIQ_SPR | 0 *** | 0 *** | 0 *** | 0 | 0 | 0 | −1.41 *** | −1.41 *** | −1.41 *** |

| (3.05) | (3.04) | (−6.21) | (−0.01) | (−0.01) | (−0.01) | (−9.82) | (−9.82) | (−9.82) | |

| TED_SPR | 0 *** | 0 *** | 0 *** | 0 *** | 0 *** | 0 *** | −0.14 *** | −1.44 *** | −1.43 *** |

| (4.28) | (4.27) | (−4.45) | (18.03) | (18.03) | (18.03) | (−12.94) | (−12.94) | (−12.94) | |

| _cons | 0 *** | 0 *** | 0 | −0.01 *** | −0.01 *** | −0.01 *** | −36.28 *** | −36.28 *** | −36.28 *** |

| (33.58) | (5.35) | (−0.4) | (−23.75) | (−10.48) | (−10.32) | (−41.87) | (−13.5) | (−14.06) | |

| Observations | 50327 | 50327 | 50327 | 50327 | 50327 | 50327 | 50327 | 50327 | 50327 |

| R-squared | 0.1 | 0.1 | 0.59 | 0.59 | 0.17 | 0.17 | |||

| (DCoVaR) | |

| Coef. | |

| Chi-square test value | 24.406 |

| p-value | 0.002 |

| (MES) | |

| Coef. | |

| Chi-square test value | 1.089 |

| p-value | 0.993 |

| (SRISK) | |

| Coef. | |

| Chi-square test value | 0.027 |

| p-value | 1 |

| DCOVAR[ID,t] = Xb + u[ID] + e[ID,t] | ||

|---|---|---|

| Estimated Results: | ||

| Var | SD = sqrt(Var) | |

| DCOVAR | 6.32 × 10−13 | 7.95 × 10−7 |

| E | 4.83 × 10−14 | 2.20 × 10−7 |

| u | 1.34 × 10−13 | 3.66 × 10−7 |

| Test: Var(u) = 0 | ||

| chibar2(01) | =2.1 × 107 | |

| Prob > chibar2 | =0.0000 | |

| Delta_CoVaR | Coef. | Std. Err. | t-Value | p-Value | [95% Conf | Interval] |

|---|---|---|---|---|---|---|

| Delta_CoVaR | ||||||

| DCovar_1 | −15,697.014 | 2877.322 | −5.46 | 0 | −21,336.462 | −10,057.566 |

| Beta | 88.335 | 12.162 | 7.26 | 0 | 64.498 | 112.171 |

| Exch_Rate | 0.069 | 0.002 | 33.07 | 0 | 0.065 | 0.073 |

| FFR | −59.711 | 4.458 | −13.39 | 0 | −68.448 | −50.974 |

| TBILL_DELTA | 0.648 | 0.156 | 4.14 | 0 | 0.341 | 0.954 |

| JKSE_VIX | 1.421 | 0.21 | 6.75 | 0 | 1.009 | 1.834 |

| LIQUIDITY_SPREAD | 19.918 | 6.29 | 3.17 | 0.002 | 7.589 | 32.247 |

| TED_SPREAD | 7.812 | 2.941 | 2.66 | 0.008 | 2.048 | 13.576 |

| Constant | 237.717 | 30.951 | 7.68 | 0 | 177.054 | 298.381 |

| ARCH | ||||||

| arch | ||||||

| L1 | 0.047 | 0.012 | 3.96 | 0 | 0.023 | 0.07 |

| garch | ||||||

| L1 | 0.955 | 0.011 | 85.70 | 0 | 0.933 | 0.976 |

| Constant | 8.457 | 9.509 | 0.89 | 0.374 | −10.18 | 27.095 |

| Coefficient | Std. Err. | t-Value | p-Value | [95% Conf | Interval] | |

|---|---|---|---|---|---|---|

| DCOVAR | 2.82 × 10−7 | 1.83 × 10−9 | 153.92 | 0 | 2.78 × 10−7 | 2.86 × 10−7 |

| DCOVAR | 1.08 × 10−6 | 1.18 × 10−8 | 91.64 | 0 | 1.05 × 10−6 | 1.10 × 10−6 |

| MES | 0.0129582 | 0.0000196 | 662.66 | 0 | 0.0129199 | 0.0129966 |

| MES | 0.0173357 | 0.0000992 | 174.72 | 0 | 0.0171413 | 0.0175302 |

| Category and Weighting | BCBS G-SIBs | Indicator Weighting | Category (Weighting) | Adjusted Indicators D-SIBs | Indicator Weighting |

|---|---|---|---|---|---|

| Size (20%) | Total exposures | 20% | Size (33.3%) | Total exposures | 100% |

| Interconnectedness (20%) | Intra-financial system assets | 6.67% | Interconnectedness (33.3%) | Intra-financial system assets | 33.3% |

| Intra-financial system liabilities | 6.67% | Intra-financial system liabilities | 33.3% | ||

| Securities outstanding | 6.67% | Securities outstanding | 33.3% | ||

| Complexity (20%) | Notional amount of over the counter (OTC) derivatives | 6.67% | Complexity (33.3%) | Notional amount of over the counter (OTC) derivatives | 25% |

| Level 3 assets | 6.67% | Trading and available-for-sale securities | 25% | ||

| Trading and available for sale securities | 6.67% | Domestic indicators | 25% | ||

| Substitutability (payment system & custodian) | 25% | ||||

| Substitutability (20%) | Assets under custody | 6.67% | |||

| Payment activity | 6.67% | ||||

| Underwritten transactions in debt & equity markets | 3.33% | ||||

| Trading volume | 3.33% | ||||

| Cross-jurisdictional activity (20%) | Cross-jurisdictional claims | 10% | |||

| Cross-jurisdictional liabilities | 10% |

| Category and Weighting | BCBS G-SIBs | Indicator Weighting | Category (Weighting) | POJK No. 2/POJK.03/2018 Indicators D-SIBs | Indicator Weighting | Category (Weighting) | Macro-Micro Indicators D-SIBs | Indicator Weighting | |

|---|---|---|---|---|---|---|---|---|---|

| Size (20%) | Total exposures | 20% | Size (33.3%) | Total exposures | 100% | Size (25%) | Total exposures | 100% | |

| Interconnectedness (20%) | Intra-financial system assets | 6.67% | Interconnectedness (33.3%) | Intra-financial system assets | 33.3% | Interconnectedness (25%) | Intra-financial system assets | 33.3% | |

| Intra-financial system liabilities | 6.67% | Intra-financial system liabilities | 33.3% | Intra-financial system liabilities | 33.3% | ||||

| Securities outstanding | 6.67% | Securities outstanding | 33.3% | Securities outstanding | 33.3% | ||||

| Complexity (20%) | Notional amount of over the counter (OTC) derivatives | 6.67% | Complexity (33.3%) | Notional amount of over the counter (OTC) derivatives | 25% | Complexity (25%) | Notional amount of over the counter (OTC) derivatives | 25% | |

| Level 3 assets | 6.67% | Trading and available-for-sale securities | 25% | Trading and available-for-sale securities | 25% | ||||

| Trading and available for sale securities | 6.67% | Domestic indicators | 25% | Domestic indicators | 25% | ||||

| Substitutability (payment system & custodian) | 25% | Substitutability (payment system & custodian) | 25% | ||||||

| Substitutability (20%) | Assets under custody | 6.67% | Macroeconomics shocks (25%) | Currency exposure | 33.3% | ||||

| Payment activity | 6.67% | Market volatility | 33.3% | ||||||

| Underwritten transactions in debt & equity markets | 3.33% | Policies exposure | 33.3% | ||||||

| Trading volume | 3.33% | ||||||||

| Cross-jurisdictional activity (20%) | Cross-jurisdictional claims | 10% | |||||||

| Cross-jurisdictional liabilities | 10% | ||||||||

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Rizan, M.; Salim, M.Z.; Mukhtar, S.; Daly, K. Macroeconomics of Systemic Risk: Transmission Channels and Technical Integration. Risks 2022, 10, 174. https://doi.org/10.3390/risks10090174

Rizan M, Salim MZ, Mukhtar S, Daly K. Macroeconomics of Systemic Risk: Transmission Channels and Technical Integration. Risks. 2022; 10(9):174. https://doi.org/10.3390/risks10090174

Chicago/Turabian StyleRizan, Mohamad, Muhammad Zulkifli Salim, Saparuddin Mukhtar, and Kevin Daly. 2022. "Macroeconomics of Systemic Risk: Transmission Channels and Technical Integration" Risks 10, no. 9: 174. https://doi.org/10.3390/risks10090174

APA StyleRizan, M., Salim, M. Z., Mukhtar, S., & Daly, K. (2022). Macroeconomics of Systemic Risk: Transmission Channels and Technical Integration. Risks, 10(9), 174. https://doi.org/10.3390/risks10090174