A Framework for Risk Management in Small Medium Enterprises in Developing Countries

{kind=link}

Abstract

1. Introduction

2. Literature Review

3. Problem Statement

4. Methodology

5. Findings

5.1. Common Ground of the Studies on ERM

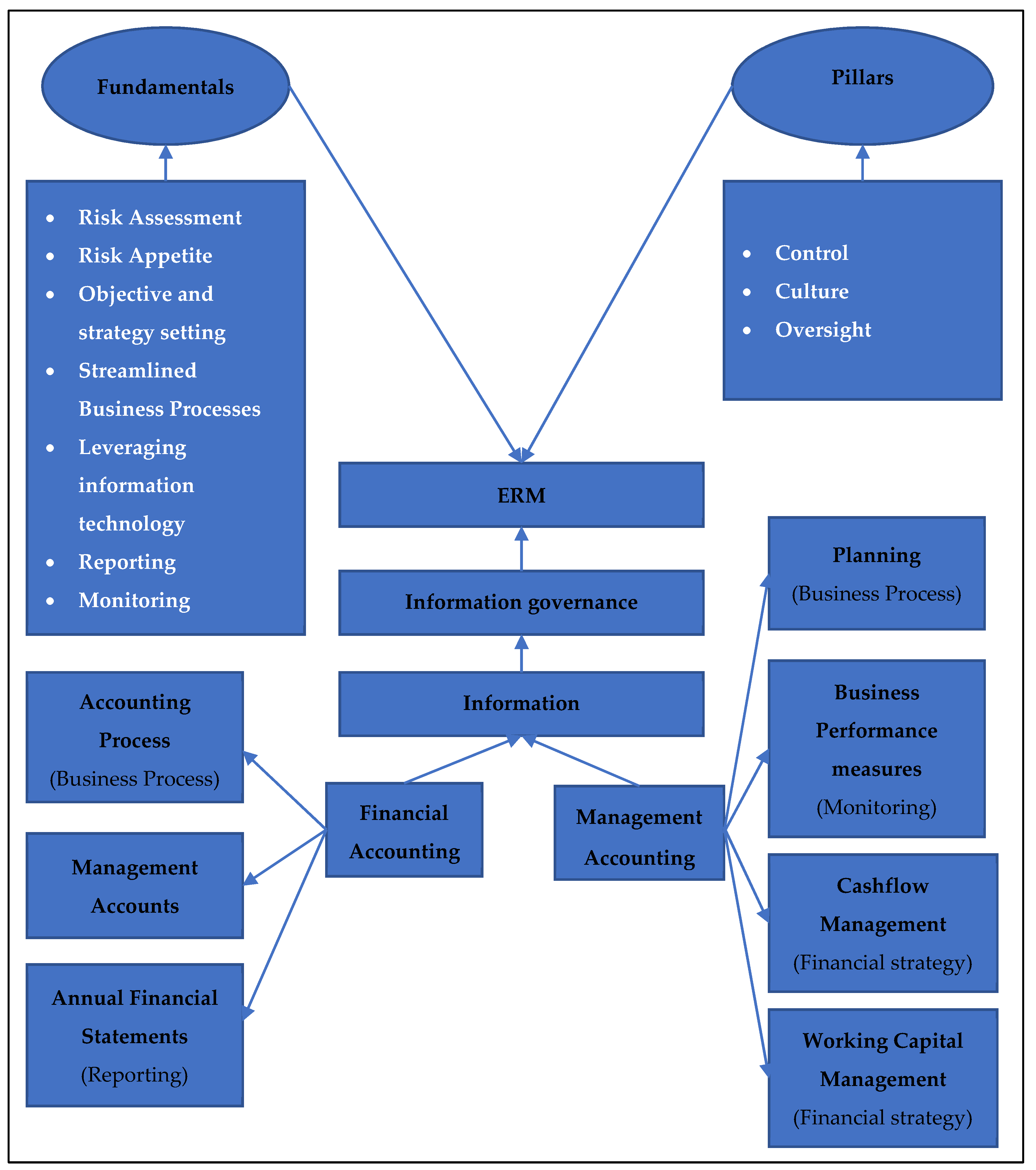

5.2. Components of the Conceptual Framework

- Information Governance

- Information

- Financial Accounting

- The accounting process

- Financial management process

- Management Accounting

- Streamlined Business Processes

- Planning

- Performance measurements

- Culture

- Internal Controls

- Oversight

- Leveraging information technology

- Risk assessment and risk appetite

6. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Conflicts of Interest

References

- Abubakar, Yazid Abdullahi, Chris Hand, David Smallbone, and George Saridakis. 2019. What Specific Modes of Internationalization Influence SME Innovation in Sub-Saharan Least Developed Countries (LDCs)? Technovation 79: 56–70. [Google Scholar] [CrossRef]

- Acar, Emrah, and Yasemin Göç. 2011. Prediction of Risk Perception by Owners’ Psychological Traits in Small Building Contractors. Construction Management and Economics 29: 841–52. [Google Scholar] [CrossRef]

- Afrifa, Godfred Adjapong. 2016. Net Working Capital, Cash Flow and Performance of UK SMEs. Review of Accounting and Finance 15: 21–44. [Google Scholar] [CrossRef]

- Akhtar, Shamim, and Yanping Liu. 2018. SME Managers and Financial Literacy; Does Financial Literacy Really Matter? Journal of Public Administration and Governance 8: 353. [Google Scholar] [CrossRef][Green Version]

- Alade, Muyiwa Ezekiel, and Mercy Oluwatoyin Owabumoye. 2020. Budgetary Control Mechanism and Financial Accountability in Ondo State Public Sector. Accounting & Taxation Review 4: 134–37. [Google Scholar]

- Aldasoro, Iñaki, Leonardo Gambacorta, Paolo Giudici, and Thomas Leach. 2022. The Drivers of Cyber Risk. Journal of Financial Stability 60: 100989. [Google Scholar] [CrossRef]

- Alibhai, Salim, Erwin Bakker, T. V. Balasubramanian, Kunal Bharadva, Asif Chaudhry, Danie Coetsee, James Dougherty, Chris Johnstone, Patrick Kuria, Christopher Naidoo, and et al. 2020. Interpretation and Application of IFRS Standards. Hoboken: John Wiley and Sons, Limited. [Google Scholar]

- Aliona, Birca. 2016. Financial Performance Measurement Tools. Annals-Economy Series 3: 169–73. [Google Scholar]

- Ameen, Ahmed Mohamed, Moataz Fathi Ahmed, and Meral Ahmed Abd Hafez. 2018. The Impact of Management Accounting and How It Can Be Implemented into the Organizational Culture. Dutch Journal of Finance and Management 2: 1–9. [Google Scholar] [CrossRef]

- Azar, Nasrin, Zarina Zakaria, and Noor Adwa Sulaiman. 2019. The Quality of Accounting Information: Relevance or Value-Relevance? Asian Journal of Accounting Perspectives 12: 1–21. [Google Scholar] [CrossRef]

- Bailey, Wendy J., and Janet A Samuels. 2018. Analyzing Two Investments—An Instructional Case to Introduce Basic Financial Accounting Concepts. Issues in Accounting Education 33: 47–56. [Google Scholar] [CrossRef]

- Bauer, Andrew M., Darren Henderson, and Daniel P. Lynch. 2017. Supplier Internal Control Quality and the Duration of Customer-Supplier Relationships. The Accounting Review 93: 59–82. [Google Scholar] [CrossRef]

- Bensaada, Ilies, and Noria Taghezout. 2019. An Enterprise Risk Management System for SMEs: Innovative Design Paradigm and Risk Representation Model. Small Enterprise Research 26: 179–206. [Google Scholar] [CrossRef]

- Berlinger, Edina, and Kata Váradi. 2015. Risk Appetite. Public Finance Quarterly 60: 49–62. [Google Scholar]

- Borocki, Jelena, Mladen Radišić, Włodzimierz Sroka, Jolita Grėblikaitė, and Armenia Androniceanu. 2019. Methodology for Strategic Posture Determination of SMEs. Engineering Economics 30: 265–77. [Google Scholar] [CrossRef]

- Brooks, Chris. 2019. Introductory Econometrics for Finance, 4th ed. Cambridge: Cambridge University Press. [Google Scholar] [CrossRef]

- Bruwer, Juan-Pierré, and André van den Berg. 2017. The Conduciveness of the South African Economic Environment and Small, Medium and Micro Enterprise Sustainability: A Literature Review. Expert Journal of Business and Management 5: 1–12. [Google Scholar]

- Bure, Makomborero, and Robertson Khan Tengeh. 2019. Implementation of Internal Controls and the Sustainability of SMEs in Harare in Zimbabwe. Entrepreneurship and Sustainability Issues 7: 201–18. [Google Scholar] [CrossRef]

- Cheng, Qiang, Beng Wee Goh, and Jae B. Kim. 2018. Internal Control and Operational Efficiency. Contemporary Accounting Research 35: 1102–39. [Google Scholar] [CrossRef]

- Chiwamit, Pimsiri, Sven Modell, and Robert W. Scapens. 2017. Regulation and Adaptation of Management Accounting Innovations: The Case of Economic Value Added in Thai State-Owned Enterprises. Management Accounting Research 37: 30–48. [Google Scholar] [CrossRef]

- Committee of Sponsoring Organizations of the Treadway Commission (COSO). 2017. ERM–Integrating with Strategy and Performance. New York: COSO. [Google Scholar]

- Cooper, David J., Mahmoud Ezzamel, and Sandy Q. Qu. 2017. Popularizing a Management Accounting Idea: The Case of the Balanced Scorecard. Contemporary Accounting Research 34: 991–1025. [Google Scholar] [CrossRef]

- Crovini, Chiara, Gabriele Santoro, and Giovanni Ossola. 2021. Rethinking Risk Management in Entrepreneurial SMEs: Towards the Integration with the Decision-Making Process. Management Decision 59: 1085–13. [Google Scholar] [CrossRef]

- D’Mello, Ranjan, Xinghua Gao, and Yonghong Jia. 2017. Internal Control and Internal Capital Allocation: Evidence from Internal Capital Markets of Multi-Segment Firms. Review of Accounting Studies 22: 251–87. [Google Scholar] [CrossRef]

- Daneshmandnia, Ali. 2019. The Influence of Organizational Culture on Information Governance Effectiveness. Records Management Journal 29: 18–41. [Google Scholar] [CrossRef]

- Darma, Jufri, Azhar Susanto, Sri Mulyani, and Jadi Suprijadi. 2018. The Role of Top Management Support in the Quality of Financial Accounting Information Systems. Journal of Applied Economic Sciences 13: 1009–20. [Google Scholar]

- Davids, Heinrich, and Osden Jokonya. 2019. Investigating Factors Influencing ICT Adoption among SMES in the Hospitality Industry in the Western Cape. In Shifting the Digital Skills Discourse for the 4th Industrial Revolution. Boksburg: National Electronic Media Institute of South Africa (NEMISA), pp. 83–96. [Google Scholar]

- del Carmen Gutiérrez-Diez, María, José Luis Bordas Beltran, and Ana María de Gpe Arras-Vota. 2022. Sustainable Balance Scorecard as a CSR Roadmap for SMEs: Strategies and Architecture Review. In Handbook of Research on Entrepreneurial Leadership and Competitive Strategy in Family Business. Edited by José Manuel Saiz-Álvarez and Jesús Manuel Palma-Ruiz. London: IGI Global, pp. 88–110. [Google Scholar]

- Deng, Ping. 2012. The Internationalization of Chinese Firms: A Critical Review and Future Research*. International Journal of Management Reviews 14: 408–27. [Google Scholar] [CrossRef]

- Deni, Asep, and Ari Riswanto. 2019. Analysis of Factors That Influence The Disclosure Of Enterprise Risk Management in SMEs. Jurnal Konsep Bisnis Dan Manajemen 6: 1. [Google Scholar] [CrossRef]

- Dimitropoulos, Panagiotis E., and Dimitrios Asteriou. 2010. The Effect of Board Composition on the Informativeness and Quality of Annual Earnings: Empirical Evidence from Greece. Research in International Business and Finance 24: 190–205. [Google Scholar] [CrossRef]

- Dimitropoulos, Panagiotis E., Ioannis Kosmas, and Ioannis Douvis. 2017. Implementing the Balanced Scorecard in a Local Government Sport Organization. International Journal of Productivity and Performance Management 66: 362–79. [Google Scholar] [CrossRef]

- Dimitropoulos, Panagiotis E., Konstantinos Koronios, Alkis Thrassou, and Demetris Vrontis. 2020. Cash Holdings, Corporate Performance and Viability of Greek SMEs: Implications for Stakeholder Relationship Management. EuroMed Journal of Business 15: 333–48. [Google Scholar] [CrossRef]

- Division on Investment and Enterprise of UNCTAD. 2016. Investor Nationality: Policy Challenges. In World Investment Report 2016. Geneva: UNCTAD, vol. 23. [Google Scholar] [CrossRef]

- Dong, Linying, and Karim Keshavjee. 2016. Why Is Information Governance Important for Electronic Healthcare Systems? A Canadian Experience. Journal of Advances in Humanities and Social Sciences 2: 250–60. [Google Scholar] [CrossRef]

- Dubihlela, Job, and Lisa Nqala. 2017. Internal Controls Systems and the Risk Performance. International Journal of Business and Management Studies 9: 87–103. [Google Scholar]

- Dudic, Zdenka, Branislav Dudic, Michal Gregus, Daniela Novackova, and Ivana Djakovic. 2020. The Innovativeness and Usage of the Balanced Scorecard Model in SMEs. Sustainability 12: 3221. [Google Scholar] [CrossRef]

- Expósito, Alfonso, and Juan A. Sanchis-Llopis. 2019. The Relationship between Types of Innovation and SMEs’ Performance: A Multi-Dimensional Empirical Assessment. Eurasian Business Review 9: 115–35. [Google Scholar] [CrossRef]

- Falle, Susanna, Romana Rauter, Sabrina Engert, and Rupert J. Baumgartner. 2016. Sustainability Management with the Sustainability Balanced Scorecard in SMEs: Findings from an Austrian Case Study. Sustainability 8: 545. [Google Scholar] [CrossRef]

- Ferreira de Araújo Lima, Priscila, Maria Crema, and Chiara Verbano. 2020. Risk Management in SMEs: A Systematic Literature Review and Future Directions. European Management Journal 38: 78–94. [Google Scholar] [CrossRef]

- Figl, Kathrin. 2017. Comprehension of Procedural Visual Business Process Models: A Literature Review. Business and Information Systems Engineering 59: 41–67. [Google Scholar] [CrossRef]

- Fraser, John R. S., and Betty J. Simkins. 2016. The Challenges of and Solutions for Implementing Enterprise Risk Management. Business Horizons 59: 689–98. [Google Scholar] [CrossRef]

- Gao, Xinghua, and Yonghong Jia. 2016. Internal Control over Financial Reporting and the Safeguarding of Corporate Resources: Evidence from the Value of Cash Holdings. Contemporary Accounting Research 33: 783–814. [Google Scholar] [CrossRef]

- Gatzert, Nadine, and Joan Schmit. 2016. Supporting Strategic Success through Enterprise-Wide Reputation Risk Management. The Journal of Risk Finance 17: 26–45. [Google Scholar] [CrossRef]

- Geer, Dan, Eric Jardine, and Eireann Leverett. 2020. On Market Concentration and Cybersecurity Risk. Journal of Cyber Policy 5: 9–29. [Google Scholar] [CrossRef]

- Gorondutse, Abdullahi Hassan, Rahima Abass Ali, Ahmed Abubakar, and Muhammad Nura Ibrahim Naalah. 2017. The Effect of Working Capital Management on SMEs Profitability in Malaysia. Polish Journal of Management Studies 16: 99–109. [Google Scholar] [CrossRef]

- Gorzeń-Mitka, Iwona. 2019. Interpretive Structural Modeling Approach to Analyze the Interaction Among Key Factors of Risk Management Process in SMEs: Polish Experience. European Journal of Sustainable Development 8: 339–49. [Google Scholar] [CrossRef]

- Greene, Melanie J. 2014. On the Inside Looking In: Methodological Insights and Challenges in Conducting Qualitative Insider Research. The Qualitative Report 19: 1013. [Google Scholar] [CrossRef]

- Haleem, Athambawa, Samsudeen Sabraz Nawaz, and Ahamed Lebbe Mohamed Ayoobkhan. 2020. Determinant of Contingency Factors of AIS in ERP System. Test Engineering and Management 83: 6592–14. [Google Scholar]

- Hanifah, Haniruzila, Hasliza Abdul Halim, Noor Hazlina Ahmad, and Ali Vafaei-Zadeh. 2019. Emanating the Key Factors of Innovation Performance: Leveraging on the Innovation Culture among SMEs in Malaysia. Journal of Asia Business Studies 13: 559–87. [Google Scholar] [CrossRef]

- Hardy, Karen. 2014. Enterprise Risk Management: A Guide for Government Professionals. Hoboken: John Wiley and Sons, Limited. [Google Scholar]

- Harl, Maximilian, Sven Weinzierl, Mathias Stierle, and Martin Matzner. 2020. Explainable Predictive Business Process Monitoring Using Gated Graph Neural Networks. Journal of Decision Systems 29: 312–27. [Google Scholar] [CrossRef]

- Havierniková, Katarína, and Małgorzata Okręglicka. 2019. The Difference in Organization of Risk Management between Slovak and Polish SMEs. Social & Economic Revue 17: 60–69. [Google Scholar]

- He, Chenyang, and Kevin Lu. 2018. Risk Management in Smes with Financial and Nonfinancial Indicators Using Business Intelligence Methods. In Ntegrated Economy and Society: Diversity, Creativity and Technology; Proceedings of the MakeLearn and TIIM International Conference 2018. Naples: ToKnowPress, pp. 405–18. [Google Scholar]

- Hopkin, Paul. 2014. Fundamentals of Risk Management: Understanding, Evaluating and Implementing Effective Risk Management, 3rd ed. London: Kogan Page. [Google Scholar]

- Hudakova, Maria, Matej Masár, and Vladimír Míka. 2019. Assessing the Needs of Risk Management Eduction in the World. Paper presented at 12th Annual International Conference of Education, Research and Innovation, Seville, Spain, November 11–13. [Google Scholar]

- Hutaibat, Khaled, and Zaidoon Alhatabat. 2020. Management Accounting Practices’ Adoption in UK Universities. Journal of Further and Higher Education 44: 1024–38. [Google Scholar] [CrossRef]

- Ibiwoye, Ade, Joseph Mojekwu, and Francis Dansu. 2020. Enterprise Risk Management Practices and Survival of Small and Medium Scale Enterprises in Nigeria. Studies in Business and Economics 15: 68–82. [Google Scholar] [CrossRef]

- Idris, Siti Musliha Mohd, and Azizan Abdullah. 2016. A Conceptual Framework on Determinants of Enterprise Risk Management (ERM) Adoption: A Study in Manufacturing Small and Medium Enterprises (SMEs) BT. In Proceedings of the 1st AAGBS International Conference on Business Management 2014 (AiCoBM 2014). Edited by Jaafar Pyeman, Wan Edura Wan Rashid, Azlina Hanif, Syed Jamal Abdul Nasir Syed Mohamad and Peck Leong Tan. Singapore: Springer, pp. 245–55. [Google Scholar]

- In, Joonhwan, Randy Bradley, Bogdan C. Bichescu, and Chad W. Autry. 2019. Supply Chain Information Governance: Toward a Conceptual Framework. The International Journal of Logistics Management 30: 506–26. [Google Scholar] [CrossRef]

- International financial reporting Standards (IFRS). 2016. A Guide through International Financial Reporting Standards. London: IFRS Foundation Publication Department United Kingdom.

- Isa, Azman Mat, Sabri Mohd Sharif, Rabiah Mohd Ali, and Nordiana Mohd Nordin. 2019. Managing Evidence of Public Accountability: An Information Governance Perspective. International Journal of Innovation, Creativity and Change 10: 142–53. [Google Scholar]

- Islam, Ariful, and Des Tedford. 2012. Risk Determinants of Small and Medium-Sized Manufacturing Enterprises (SMEs)—An Exploratory Study in New Zealand. Journal of Industrial Engineering International 8: 12. [Google Scholar] [CrossRef]

- Kehinde, Adesina, Alabi Opeyemi, A. Benjamin, Ogunjobi Adedayo, and O. A. Abel. 2017. Enterprise Risk Management and the Survival of Small Scale Businesses in Nigeria. International Journal of Accounting Research 5: 1–8. [Google Scholar] [CrossRef]

- Ki-Aries, Duncan, and Shamal Faily. 2017. Persona-Centred Information Security Awareness. Computers and Security 70: 663–74. [Google Scholar] [CrossRef]

- Kim, YoungJun, and Nicholas S. Vonortas. 2014. Managing Risk in the Formative Years: Evidence from Young Enterprises in Europe. Technovation 34: 454–65. [Google Scholar] [CrossRef]

- Kintu, Ismail, Patricia Naluwooza, and Y. Kiwala. 2019. Cash Inflow Conundrum in Ugandan SMEs: A Perspective of ISO Certification and Firm Location. African Journal of Business Management 13: 274–82. [Google Scholar] [CrossRef]

- Kwarteng, Amoako. 2018. The Impact of Budgetary Planning on Resource Allocation: Evidence from a Developing Country. African Journal of Economic and Management Studies 9: 88–100. [Google Scholar] [CrossRef]

- Lai, Fong-Woon, and Muhammad Kashif Shad. 2017. Economic Value Added Analysis for Enterprise Risk Management. Global Business and Management Research: An International Journal 9: 338–47. [Google Scholar]

- Le, Ben. 2019. Working Capital Management and Firm’s Valuation, Profitability and Risk. International Journal of Managerial Finance 15: 191–204. [Google Scholar] [CrossRef]

- Le, Thi Tam. 2020. Performance Measures and Metrics in a Supply Chain Environment. Uncertain Supply Chain Management 8: 93–104. [Google Scholar] [CrossRef]

- Leventis, Stergios, and Panagiotis Dimitropoulos. 2012. The Role of Corporate Governance in Earnings Management: Experience from US Banks. Journal of Applied Accounting Research 13: 161–77. [Google Scholar] [CrossRef]

- Leventis, Stergios, Panagiotis Dimitropoulos, and Stephen Owusu-Ansah. 2013. Corporate Governance and Accounting Conservatism: Evidence from the Banking Industry. Corporate Governance: An International Review 21: 264–86. [Google Scholar] [CrossRef]

- Liem, Christina. 2018. Enterprise Risk Management In Banking Industry. FIRM: Journal of Management Studies 3: 1–13. [Google Scholar] [CrossRef][Green Version]

- Liu, Cong, Hua Duan, Qingtian Zeng, Mengchu Zhou, Faming Lu, and Jiujun Cheng. 2019. Towards Comprehensive Support for Privacy Preservation Cross-Organization Business Process Mining. IEEE Transactions on Services Computing 12: 639–53. [Google Scholar] [CrossRef]

- Llivisaca, Juan Carlos, Diana Jadan, Rodrigo Guamán, Rodrigo Arcentales-Carrion, Mario Pena, and Lorena Siguenza-Guzman. 2020. Key Performance Indicators for the Supply Chain in Small and Medium-Sized Enterprises Based on Balance Score Card. Test Engineering and Management 83: 25933–45. [Google Scholar]

- López-Pintado, Orlenys, Marlon Dumas, Luciano García-Bañuelos, and Ingo Weber. 2019. Interpreted Execution of Business Process Models on Blockchain. Paper presented at 2019 IEEE 23rd International Enterprise Distributed Object Computing Conference (EDOC), Paris, France, October 28–32; pp. 206–15. [Google Scholar]

- Lu, Qinghua, An Binh Tran, Ingo Weber, Hugo O’Connor, Paul Rimba, Xiwei Xu, Mark Staples, Liming Zhu, and Ross Jeffery. 2021. Integrated Model-Driven Engineering of Blockchain Applications for Business Processes and Asset Management. Software: Practice and Experience 51: 1059–79. [Google Scholar] [CrossRef]

- Lyngstadaas, Hakim, and Terje Berg. 2016. Working Capital Management: Evidence from Norway. International Journal of Managerial Finance 12: 295–313. [Google Scholar] [CrossRef]

- Ma’aji, Muhammad M., Nur Adiana Hiau Abdullah, and Karren Lee-Hwei Khaw. 2018. Predicting Financial Distress among SMEs in Malaysia. European Scientific Journal, ESJ 14: 91. [Google Scholar] [CrossRef][Green Version]

- Malagueño, Ricardo, Ernesto Lopez-Valeiras, and Jacobo Gomez-Conde. 2018. Balanced Scorecard in SMEs: Effects on Innovation and Financial Performance. Small Business Economics 51: 221–44. [Google Scholar] [CrossRef]

- Malik, Muhammad Farhan, Mahbub Zaman, and Sherrena Buckby. 2017. Enterprise Risk Management and Firm Performance: Role of the Risk Committee. Journal of Contemporary Accounting and Economics 16: 100178. [Google Scholar] [CrossRef]

- Mamai, Mbiki, and Song Yinghua. 2017. Enterprise Risk Management Best Practices for Improvement Financial Performance in Manufacturing SMEs in Cameroon. International Journal of Management Excellence 8: 1004–12. [Google Scholar] [CrossRef]

- Martinez-Martinez, Aurora, Juan-Gabriel Cegarra-Navarro, Alexeis Garcia-Perez, and Anthony Wensley. 2019. Knowledge Agents as Drivers of Environmental Sustainability and Business Performance in the Hospitality Sector. Tourism Management 70: 381–89. [Google Scholar] [CrossRef]

- Mättö, Markus, and Mervi Niskanen. 2021. Role of the Legal and Financial Environments in Determining the Efficiency of Working Capital Management in European SMEs. International Journal of Finance & Economics 26: 5197–216. [Google Scholar] [CrossRef]

- Mora, Rafael D., and David Cababaro Bueno. 2017. Budgetary Control Processes towards Improved Service Delivery among Catholic Higher Educational Institutions: A Cross-Sectional Analysis. Paper presented at 10th International Conference on Arts, Social Sciences, Humanities and Interdisciplinary Studies (ASSHIS-17), Manila, Philippines, December 17–18. [Google Scholar] [CrossRef]

- Mullon, Paul Anthony, and Mpho Ngoepe. 2019. An Integrated Framework to Elevate Information Governance to a National Level in South Africa. Records Management Journal 29: 103–16. [Google Scholar] [CrossRef]

- Muneer, Saqib, Rao Abrar Ahmad, and Azhar Ali. 2017. Impact of Financial Management Practices on SMEs Profitability with Moderating Role of Agency Cost. Information Management and Business Review 9: 23–30. [Google Scholar] [CrossRef]

- N’Guilla Sow, Abdoulaye, Rohaida Basiruddin, Jihad Mohammad, and Siti Zaleha Abdul Rasid. 2018. Fraud Prevention in Malaysian Small and Medium Enterprises (SMEs). Journal of Financial Crime 25: 499–517. [Google Scholar] [CrossRef]

- Naude, Micheline J., and Nigel Chiweshe. 2017. A Proposed Operational Risk Management Framework for Small and Medium Enterprises. South African Journal of Economic and Management Sciences 20: a1621. [Google Scholar] [CrossRef]

- Ndungo, Jackson Mnago, and Mr. Kingford Rucha. 2017. Factors Affecting the Growth of Smes: A Study of Smes in Kajiado District. International Journal of Finance 2: 58–75. [Google Scholar] [CrossRef]

- Nguyen, H. A. 2015. Small and Medium Enterprises Debt Financing in Vietnam. Kuala Lumpur: Asia Pacific University. [Google Scholar]

- Ogundana, Oyebisi M., Wisdom Okere, Ochuwa Ayomoto, David Adesanmi, Stephen Ibidunni, and Olusogo Ogunleye. 2017. ICT and Accounting System of SMEs in Nigeria. Management Science Letters 7: 1–8. [Google Scholar] [CrossRef]

- Oyebode, Oluwadare Joshua. 2018. Budget and Budgetary Control: A Pragmatic Approach to the Nigerian Infrastructure Dilemma. World Journal of Research and Review 7: 1–8. [Google Scholar]

- Palermo, Tommaso. 2009. Integrating Risk and Performance in Management Reporting. Research Executive Summary Series 7: 12. [Google Scholar]

- Palermo, Tommaso. 2017. Risk and Performance Management: Two Sides of the Same Coin. In The Routledge Companion to Accounting and Risk. Edited by Margaret Woods and Philip Linsley. London: Routledge, p. 13. [Google Scholar] [CrossRef]

- Paletta, Angelo, and Genc Alimehmeti. 2016. SOX Disclosure and the Effect of Internal Controls on Executive Compensation. Journal of Accounting, Auditing & Finance 33: 277–95. [Google Scholar] [CrossRef]

- Pollman, Elizabeth. 2019. Corporate Oversight and Disobedience. Vanderbilt Law Review 72: 2013–46. [Google Scholar] [CrossRef]

- Pugnetti, Carlo, and Carlos Casián. 2021. Cyber Risks and Swiss SMEs: An Investigation of Employee Attitudes and Behavioral Vulnerabilities. Winterthur: ZHAW School of Management and Law, pp. 1–32. [Google Scholar]

- Rasouli, Mohammad Reza, Jos J. M. Trienekens, Rob J. Kusters, and Paul W. P. J. Grefen. 2016. Information Governance Requirements in Dynamic Business Networking. Industrial Management & Data Systems 116: 1356–79. [Google Scholar] [CrossRef]

- Raymond, Louis, François Bergeron, Anne-Marie Croteau, Ana Ortiz de Guinea, and Sylvestre Uwizeyemungu. 2020. Information Technology-Enabled Explorative Learning and Competitive Performance in Industrial Service SMEs: A Configurational Analysis. Journal of Knowledge Management 24: 1625–51. [Google Scholar] [CrossRef]

- Rehman, Amin Ur, and Muhammad Anwar. 2019. Mediating Role of Enterprise Risk Management Practices between Business Strategy and SME Performance. Small Enterprise Research 26: 207–27. [Google Scholar] [CrossRef]

- Reich, Simon, and Richard Ned Lebow. 2017. Influence and Hegemony: Shifting Patterns of Material and Social Power in World Politics. All Azimuth 6: 17–47. [Google Scholar]

- Rekarti, Endi, and Caturida Meiwanto Doktoralina. 2017. Improving Business Performance: A Proposed Model for SMEs. European Research Studies Journal 20: 613–23. [Google Scholar] [CrossRef]

- Rice, John, Nigel Martin, and Bruce Gurd. 2007. Strategic Planning, Budget Monitoring and Growth Optimism: Evidence from Australian SMEs. BPS Competitive 1: 1–17. [Google Scholar]

- Sadgrove, Kit. 2016. The Complete Guide to Business Risk Management, 3rd ed. London: Routledge. [Google Scholar]

- Serag, Asmaa Abdelmonem, Mona Mohamed, and Ali Daoud. 2022. A Proposed Framework for Studying the Impact of Cybersecurity on Accounting Information to Increase Trust in The Financial Reports in the Context of Industry 4.0.: An Event, Impact and Response Approach. In Economic Challenges and Business Opportunities after the Corona Pandemic “A Future Vision” 6th Annual International Conference of Faculty of Commerce. Edited by Khalid Abdul Ghaffar, Zaki Mahmoud and Kamal Okasha. Al Masa: Tanta University, vol. 20, pp. 20–61. [Google Scholar]

- Shabbir, Malik Shahzad, and Okere Wisdom. 2020. The Relationship between Corporate Social Responsibility, Environmental Investments and Financial Performance: Evidence from Manufacturing Companies. Environmental Science and Pollution Research 27: 39946–57. [Google Scholar] [CrossRef]

- Shaikh, Asmat Ara, Anuj Kumar, Asif Ali Syed, and Mohammed Zafar Shaikh. 2021. A Two-Decade Literature Review on Challenges Faced by SMEs in Technology Adoption. Academy of Marketing Studies Journal 25: 1–13. [Google Scholar]

- Sipa, Monika. 2017. Innovation As a Key Factors of Small Business Competition. European Journal of Sustainable Development 6: 344–56. [Google Scholar] [CrossRef]

- Smallwood, Robert F. 2014. Information Governance: Concepts, Strategies and Best Practices. Hoboken: John Wiley & Sons Inc. [Google Scholar]

- Sonia, Lucya Erlinda, and Stefanie Gianto. 2018. The Role of Recording and Reporting Process of Basic Accounting in Small Medium Enterprises of Omah Duren Surabaya. JEMA: Jurnal Ilmiah Bidang Akuntansi Dan Manajemen 15: 35. [Google Scholar] [CrossRef][Green Version]

- Sroka, Włodzimierz, and Richard Szántó. 2018. Corporate Social Responsibility and Business Ethics in Controversial Sectors: Analysis of Research Results. Journal of Entrepreneurship, Management and Innovation 14: 111–26. [Google Scholar] [CrossRef]

- Staszkiewicz, Piotr, and Aleksander Werner. 2021. Reporting and Disclosure of Investments in Sustainable Development. Sustainability 13: 908. [Google Scholar] [CrossRef]

- Too, Eric, Tiendung Le, and Wei Yee Yap. 2017. Front-End Planning—The Role Of Project Governance And Its Impact On Scope Change Management. International Journal of Technology 8: 291–319. [Google Scholar] [CrossRef][Green Version]

- Vanauken, Howard, Semra Ascigil, and Shawn Carraher. 2016. Turkish SMEs’ Use of Financial Statements for Decision Making. The Journal of Entrepreneurial Finance 19: 6. [Google Scholar]

- Vigario, F. 2007. Managerial Accounting, 4th ed. Durban: LexisNexis. [Google Scholar]

- Wang, Liangcheng, Yining Dai, and Yuye Ding. 2019. Internal Control and SMEs’ Sustainable Growth: The Moderating Role of Multiple Large Shareholders. Journal of Risk and Financial Management 12: 182. [Google Scholar] [CrossRef]

- Watson, John, and Rick Newby. 2005. Biological Sex, Stereotypical Sex-roles, and SME Owner Characteristics. International Journal of Entrepreneurial Behavior & Research 11: 129–43. [Google Scholar] [CrossRef]

- Yakob, Sajiah, B. A. M. Hafizuddin-Syah, Rubayah Yakob, and Nur Raziff. 2019. The Effect of Enterprise Risk Management Practice on SME Performance. The South East Asian Journal of Management 13: 151–69. [Google Scholar]

- Yathiraju, Nikhitha. 2022. Investigating the Use of an Artificial Intelligence Model in an ERP Cloud-Based System. International Journal of Electrical, Electronics and Computers 7: 1–26. [Google Scholar] [CrossRef]

- Zaefarian, Reza, Misagh Tasavori, Teck-Yong Eng, and Mehmet Demirbag. 2020. Development of International Market Information in Emerging Economy Family SMEs: The Role of Participative Governance. Journal of Small Business Management, 1–30. [Google Scholar] [CrossRef]

- Zahid, Namig Alizadeh, and Leyla Mammadova Vagif. 2020. Role of Management Accounting in the Organization. Paper presented at 55th International Scientific Conference on Economic and Social Development, Baku, Azerbaijan, June 18–19; pp. 367–72. [Google Scholar]

- Žigienė, Gerda, Egidijus Rybakovas, and Robertas Alzbutas. 2019. Artificial Intelligence Based Commercial Risk Management Framework for SMEs. Sustainability 11: 4501. [Google Scholar] [CrossRef]

- Zimon, Grzegorz. 2020. Working Capital Management Strategies in Polish SMEs. Academy of Accounting and Financial Studies Journal 24: 1–9. [Google Scholar]

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Mthiyane, Z.Z.F.; van der Poll, H.M.; Tshehla, M.F. A Framework for Risk Management in Small Medium Enterprises in Developing Countries. Risks 2022, 10, 173. https://doi.org/10.3390/risks10090173

Mthiyane ZZF, van der Poll HM, Tshehla MF. A Framework for Risk Management in Small Medium Enterprises in Developing Countries. Risks. 2022; 10(9):173. https://doi.org/10.3390/risks10090173

Chicago/Turabian StyleMthiyane, Zodwa Z. F., Huibrecht M. van der Poll, and Makgopa F. Tshehla. 2022. "A Framework for Risk Management in Small Medium Enterprises in Developing Countries" Risks 10, no. 9: 173. https://doi.org/10.3390/risks10090173

APA StyleMthiyane, Z. Z. F., van der Poll, H. M., & Tshehla, M. F. (2022). A Framework for Risk Management in Small Medium Enterprises in Developing Countries. Risks, 10(9), 173. https://doi.org/10.3390/risks10090173