1. Introduction

The Sustainable Development Goals (SDGs) are a unique collective agreement of the modern time, which was concluded between government, society, and business at a global scale and which ensures outstanding progress in sustainable development. Society is the direct beneficiary of the SDGs, but bears the lowest expenditures for their implementation and, thus, supports them. The government protects society’s interests, and implementation of the SDGs is among its main responsibilities. Participation of business in the achievement of the SDGs is complex and contradictory, deserving special attention. It is no coincidence that the necessity for the integration of the SDGs into corporate strategies is a part of the agenda in the Decade of Action (

Casias et al. 2022;

Karagiannis et al. 2022;

Trzeciak 2021).

In most cases, support of the SDGs means losses for business (including a shortfall in profits—alternative costs), i.e., contradicts its financial interests. The existing scientific literature distinguishes three approaches to the integration of the SDGs into corporate strategies. The 1st—regulatory—approach is based on companies’ unpreparedness for voluntary losses, so the implementation of the SDGs is a “market gap”. That is the reason why the government does not provide companies with the choice and opportunity to voluntarily support the SDGs (expecting that this will not take place at the required scale). Instead of this, the government adopts and controls the observation of labour and ecological standards, as well as standards of corporate financial reporting (

Batóg and Batóg 2021). On the one hand, this ensures wide support of the SDGs by entrepreneurship, but, on the other hand, government interference with the natural processes distorts the effect of the market mechanism and decreases the effectiveness of entrepreneurship (

Hamed et al. 2022;

Liu 2021).

The other two approaches are based on corporate social responsibility and are widely studied in the existing literature. A lot of scientific publications are devoted to the research of the interconnection between corporate social responsibility and the indicators of a company’s activity (

Fontana 2017;

Jaisinghani and Sekhon 2022;

Kaul and Luo 2018;

Schramm-Klein 2015).

A lot of studies undertook the testing of the interconnection between corporate social responsibility and the indicators of a company’s activity, including profitability, firm risk, stock liquidity, etc. (

Akbar et al. 2021;

Gennaro 2021;

Zhang et al. 2021;

Bednarczyk et al. 2021). Using the existing literature, the following two approaches are differentiated by the criterion of the risks of corporate social responsibility for profit.

The 2nd—non-commercial—approach to corporate social responsibility implies that companies have to voluntarily refuse their financial interests in favour of implementing the SDGs and accept high risks for profit. According to this approach, corporate social responsibility is associated with charity. As a matter of act, charity events, volunteering, and companies’ donations allow accelerating the progress in the achievement of the SDGs.

Many studies (in particular,

Kuzey et al. 2022;

Loor-Zambrano et al. 2022;

Bu et al. 2022) provide arguments in favour of the idea that companies can “do well by doing good”. In other words, a company must experience a loss when it contributes to CSR, especially when stakeholders in the company appreciate the CSR practices.

However, in the background of non-profit activities lie commercial profits, while the widespread deprivation of companies of the principal opportunity to make a profit would lead to their bankruptcy (

Chu and Fang 2021). Only the most successful and stable companies can accept large risks for profit. That is why the non-commercial approach to corporate social responsibility cannot be extended to entrepreneurship, on the whole, i.e., it has limited capabilities for scaling the practices of integrating the SDGs into corporate strategies (

Jackson 2021).

The 3rd—commercial—approach to corporate social responsibility means that, during its implementation, companies are guided by their main goal, which is connected to making a profit, and the achievement of the SDGs is the priority. This ensures low risks of corporate social responsibility for companies’ profit. This approach fits the nature of entrepreneurship in the market economy in the best way and thus has potential for wide practical use since it ensures the largest systemic profit for all interested parties in the long term (

Ang et al. 2022;

Song and Tao 2022;

Xie et al. 2022;

Zhang et al. 2022).

The research question (RQ) of this paper is as follows: do companies implement corporate social responsibility in practice according to the recommendations given in the SDGs (UN standards)? How do they do this in different regions of the world? Which approach do they use? What are the risks for profit? The hypothesis of this research is as follows: companies actively implement corporate social responsibility in practice according to the recommendations given in the SDGs (UN standards) based on the commercial (3rd) approach, but the scale of this practice and its risks for profit are different depending on regions of the world.

The objective of this paper is to study the international experience (in the aspect and taking into account the specifics of regions of the world) of integrating the SDGs into corporate strategies and to identify the following: (1) supported SDGs (UN standards); (2) implemented measures of corporate social responsibility to support the SDGs and (3) the approach from the positions of the risks for profit.

2. Literature Review

This paper uses the theory of integration of the SDGs into corporate strategies, which describes and characterises in detail all three existing approaches to this integration. Their comparative analysis is given in

Table 1.

As shown in

Table 1, the regulatory approach uses the mechanism of state regulation during the integration of the SDGs into corporate strategies. With that, support for the SDGs is forced. Market implications of the integration of the SDGs into corporate strategies are linked to the slowdown of economic growth and development of the shadow economy, and the risks of support of the SDGs for profit are high (

Pizzi et al. 2021;

Rahman 2021;

Raithatha and Shaw 2021).

A serious drawback of the first two (regulatory and non-commercial) approaches is the high risks of support of the SDGs for profit (

Kornieieva 2020;

Lassala et al. 2021;

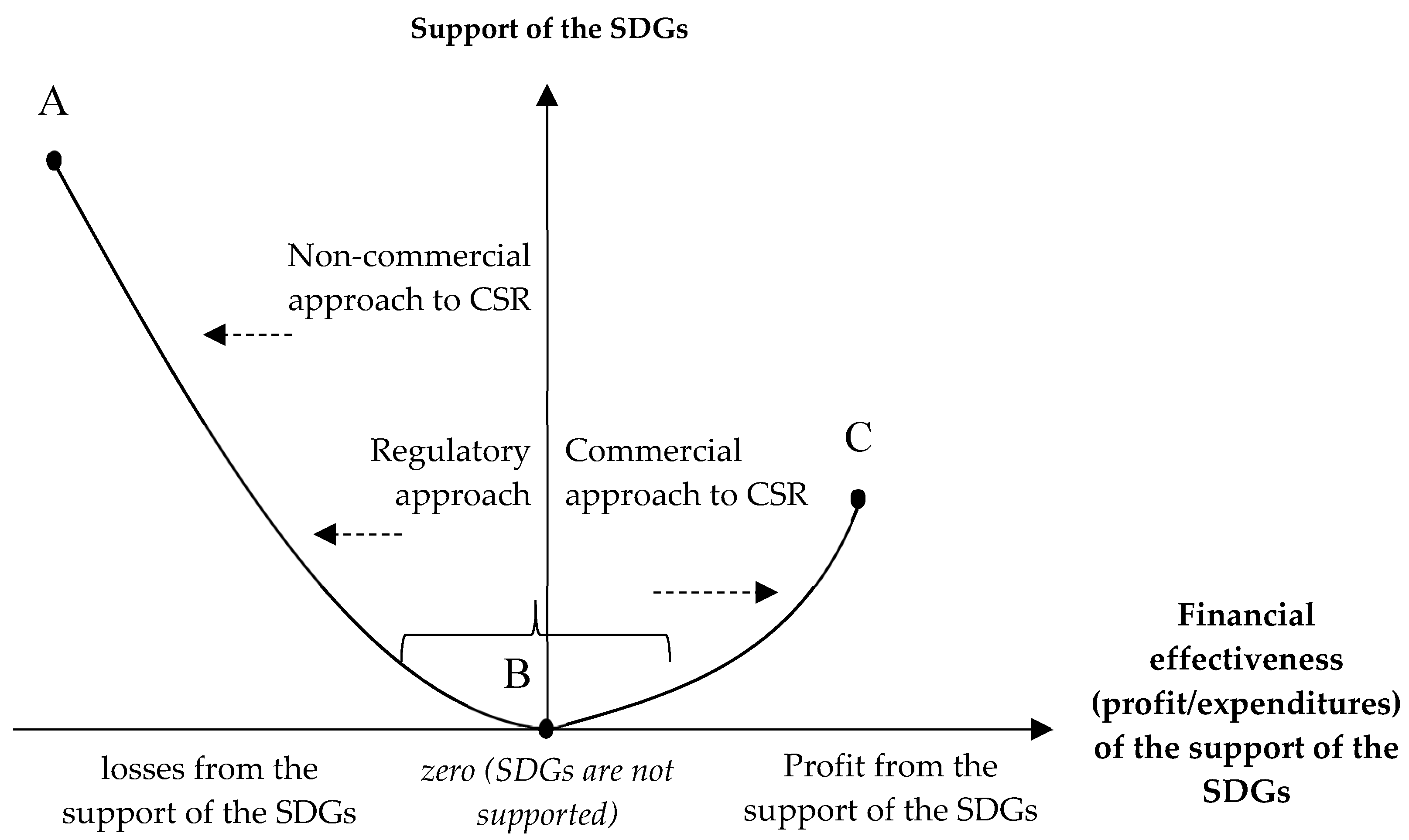

Martí-Ballester 2020). The commercial approach is very different due to the low risks of support of the SDGs for profit. This is illustrated by the bi-directional vector scale of the integration of the SDGs into corporate strategies from the standpoint of financial risks in various distinguished approaches (

Figure 1).

The scale in

Figure 1 shows that the non-commercial approach to CSR and the regulatory approach stimulate the movement from point A to point B. In section BA, business suffers losses from the support of the SDGs, the size of which grows in the course of approach to point A.

The commercial approach to corporate social responsibility opens a perspective for the movement to the right (to point C) along the stretch BC. In the works of

Battisti et al. (

2022),

Kong (

2022),

Quang et al. (

2022),

Wentzel et al. (

2022), it is noted that the risks of integrating the SDGs (UN standards) into corporate strategies are rather high for the risks on the whole.

The detailed characteristics of the integration of the SDGs into corporate strategies in alternative approaches (based on the existing literature) are presented in

Table 2.

As shown in

Table 2, though CSR can support all SDGs at once, it is mostly focused on the following SDGs: SDG 5, SDG 8, SDG 13, and SDG 16. These SDGs have the potential for commercialisation.

Other SDGs belong to the sphere of charity (and the potential contribution of business to their practical implementation is less vivid), so they are not considered in this paper. The performed systematisation allowed distinguishing three key directions of corporate social responsibility to support the SDGs: responsible human resource management (HRM), responsible production (corporate environmental responsibility), and responsible finance.

Let us present specific measures that are implemented in the above directions and provide a more detailed description of the CSR practices and their support for the SDGs. The measures of corporate social responsibility to support the SDGs (UN standards—on the stretch BC in

Figure 1) include the following (from the positions of responsible human resources management (HRM)):

Provision of gender-neutral jobs and fair wages (

He and Kim 2021;

Hirsu et al. 2021). Using this measure, the CSR practices in support of the SDGs imply the creation of equal conditions for the professional activities of all employees, regardless of their gender. Additionally, a transparent and flexible approach to wages, which takes into account the individual results of each employee’s work, is used:

- −

Stability or increase in jobs to support employment (

Zhao et al. 2021). Using this measure, the CSR practices in support of the SDGs imply the refusal of personnel cuts even amid a crisis, the formation of a personnel reserve for continuous filling of jobs, and the creation of additional jobs, apart from the satisfaction of the company’s main needs for personnel in the striving for the growth of the intensity of business processes in the connection to human resources.

- −

Guarantee of labour rights (official employment) (

Chanda and Goyal 2020;

Ramos-González et al. 2021). Using this measure, the CSR practices in support of the SDGs imply providing employees with an expanded spectrum of social labour guarantees, which covers the basic obligations of employers, dictated by the labour law.

- −

Provision of production safety (

Rawshdeh et al. 2019). Using this measure, the CSR practices in support of the SDGs imply accelerated automatisation of the types of labour activities that are potentially dangerous for life and health and employees, with the preservation of jobs (employees perform the function of remote control over automatised business processes).

From the position of responsible production (corporate environmental responsibility):

- −

Improving treatment systems for reducing environmental pollution (

Han and Cao 2021). Using this measure, the CSR practices in support of the SDGs imply a voluntary transition of companies to higher environmental standards of their activities and issued products (for example, automobile manufacturing) and implementation of ecological innovations.

- −

Refusal to include ecological costs in the price (

Setyowati et al. 2021). Using this measure, the CSR practices in support of the SDGs imply a voluntary refusal of companies of a part of the profit in favour of an increase in environmental friendliness of their activities.

From the position of responsible finance:

- −

Business’s fight against corruption (

Dela Cruz et al. 2020). Using this measure, the CSR practices in support of the SDGs imply the companies’ refusal to participate in corruption schemes and disclosure of these schemes.

- −

Full-scale payment of taxes (official business) (

Panos and Wilson 2020). Using this measure, the CSR practices in support of the SDGs imply companies’ refusal to participate in the schemes of tax evasion.

Despite the in-depth elaboration of the issues of the support of the SDGs with the help of corporate social responsibility, the following aspects remain poorly studied and unclear:

- (1)

Which SDGs (UN standards) are supported by companies in different regions of the world (research gap No. 1)?

- (2)

Which (of the list given in

Table 2) measures of corporate social responsibility to support the SDGs are implemented in the practice of companies in different regions of the world (research gap No. 2)?

- (3)

Which approach is used? What are the risks of support of the SDGs (UN standards) with the help of corporate social responsibility for profit (research gap No. 3)?

Based on the above gaps, the research question of this paper is formulated. This paper strives to fill in the research gap (and answer the research question) by studying the international experience of integrating the SDGs (UN standards) into corporate strategies based on corporate social responsibility in isolation in each region of the world and to specify the cause-and-effect links of the support of the SDGs in entrepreneurship for its risks for profit.

3. Materials and Methods

To answer the research question (RQ), the discovered research gaps are consistently filled in and the research is conducted according to the following strategy (

Table 3).

The research objects are 193 countries in 2021, for which the statistics of the achievement of the SDGs are collected and the Sustainable Development Index is calculated; in the multicriterial (given the criteria of geographical location, level of income, and economic integration) classification of the

UN (

2021), they are divided into the following categories:

- −

Africa: 49 countries;

- −

E. Europe and C. Asia: 27 countries;

- −

East and South Asia: 21 countries;

- −

LAC: 30 countries;

- −

MENA: 17 countries;

- −

Oceania: 12 countries;

- −

OECD: 37 countries.

The choice of SDG 5, SDG 8, SDG 13, and SDG 16 is due to the fact that the current statistics on them reflect business’s contribution to the largest extent. Though there are no isolated statistics on how many companies support these SDGs and to what extent, this limitation of the existing statistics could be overcome by the study of the SDGs (the selected SDGs) in which an important (and even main) role belongs to a business. The studied indicators of the UN are obtained not at the level of companies but at the level of the economy on the whole. This allows receiving the unified statistics—compatible data at the level of all regions of the world: universal indicators and their values, without the number of companies and size of countries.

The sample is given in the

Supplementary Materials (Tables S1 and S2). Detailed definitions of the variables are provided in the

Supplementary Materials (Table S11). The advantages of the considered sample are that it is the most detailed study of the experience of the global economic system on the whole and the possibility to specify the features of countries from various categories. The research is performed based on the 2021 data.

According to the research strategy (

Table 3), to achieve the stated goal, this paper solves the following tasks.

The 1st task: determining the level of integrating the SDGs (UN standards) into corporate strategies. The following is done for this:

- −

Determining the activity of the use of CSR measures to support the SDGs (α) with the help of the method of structural analysis by finding the ratio of the number of countries for which the values of the indicators of the support of the SDGs are non-zero (difference between the total number of countries and the number of zeroes for the column) to the total number of countries (in per cent): it must be above 50%.

- −

Evaluating the regularity of the support of the SDGs by companies through CSR measures (β), with the help of the method of analysis of variance (by column, in per cent): it must be below 80%.

- −

Finding the ratio of the use of CSR measures to support the SDGs to the worldwide average value (λ), with the help of the method of comparative analysis (in per cent): it must be above 50%.

The level of integrating the SDGs (UN standards) into corporate strategies for each selected SDG is determined according to the formula: (α+β+λ)/3. As a result, the aggregate integration of the selected SDGs in the corporate strategies is calculated as the arithmetic mean for all selected SDGs.

The 2nd task: determining the specific measures of corporate social responsibility to support the SDGs, which are implemented in the practice of companies in different regions of the world, through the comparison of the selected practices to the measures of corporate social responsibility from

Table 2.

The 3rd task: qualitatively (high/low) evaluating the risks of integrating the SDGs into corporate strategies for companies’ profit. To achieve the stated task, the consequences for various practices of corporate social responsibility for profit are identified with the help of the regression analysis method.

For this, the dependence between the indicator countries of the

UN (

2021) from

Table 2 (let us denote them as CSR

SDG(1)–(9)) and the targeted result—shifted profits of multinationals (let us denote it as SPM, measured in USD billion)—is found (

UN 2021). The economic essence of this econometric procedure consists in identifying the connections between the indicators of implementing the SDGs and companies’ profit (shifted profits of multinationals). The research model of this paper is as follows:

Model (1) is deliberately given in the generalised form (as a function), to allow the inclusion of the different number of factor variables—selected CSR practices (from 1 to all 9)—the connection of which with the resulting variable is reliable (checked with the help of the F test, to ensure the precision of the analysis results). Since the statistics for all variables from model (1) are not available for 2020 (no data for Fundamental labour rights are effectively guaranteed (SRSDG(3)) and Carbon Pricing Score at EUR60/tCO2 (SRSDG(7)), for the full coverage of all selected indicators, model (1) is compiled based on the data for 2021 only—a rather large sample of 193 observations).

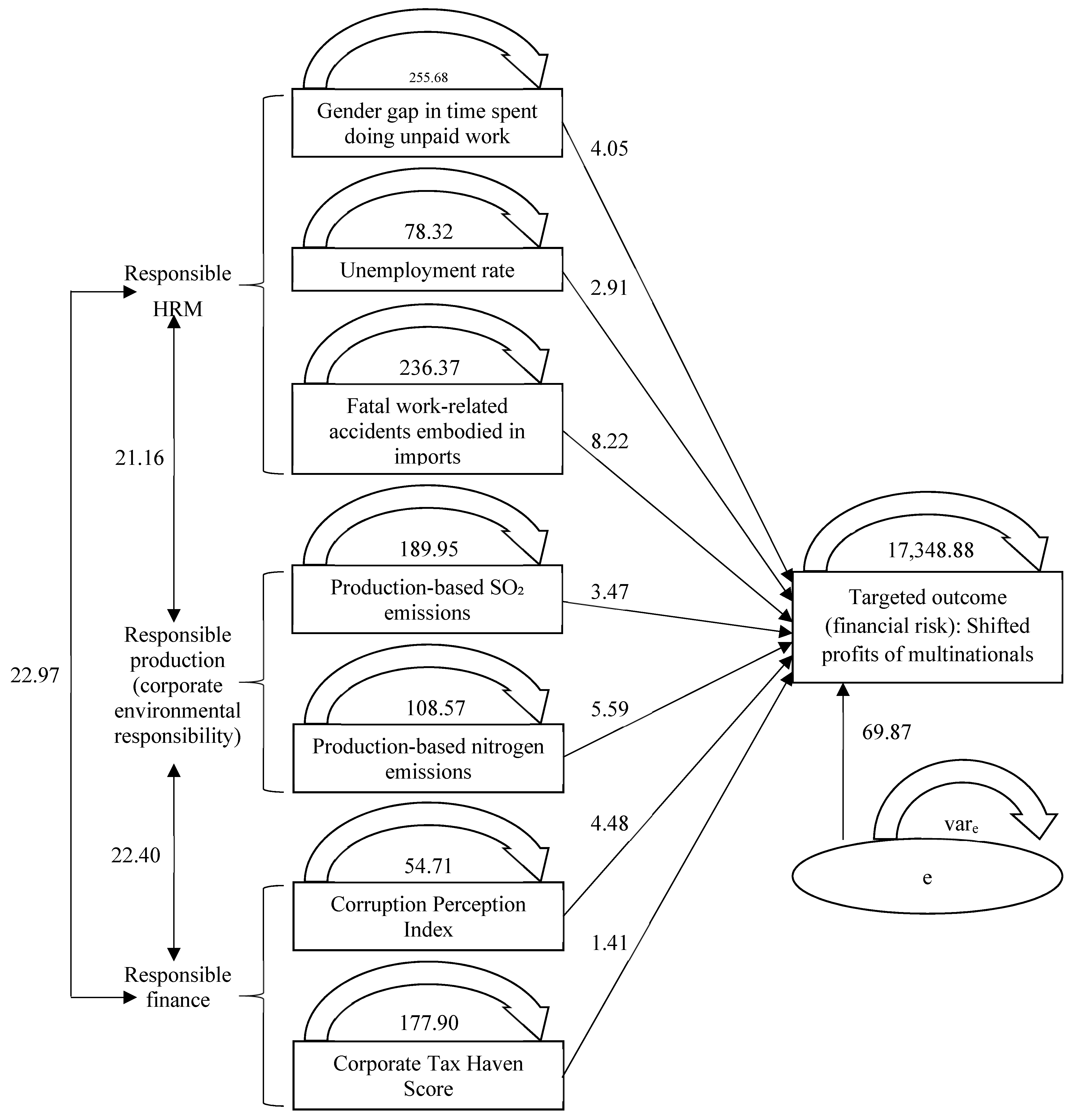

Apart from this, we compiled a structural equation model, which is reflected in the block diagram in

Figure 1.

Figure 2 shows that targeted outcome (financial risk): shifted profits of multinationals depend on the factors of responsible HRM, responsible production (corporate environmental responsibility), and responsible finance, which are interconnected. The targeted outcome (financial risk): shifted profits of multinationals are also influenced by other (residual) factors that are unified into one error of the model (i.e., latent variable). All variables of the structural equation model have their variation (scatter of values: var).

To compile a structural equation model, we form an expanded (unified) sample, which includes the data not only for 2021 but also for 2020, due to which the aggregate array of data contains 386 observations. The sample for SEM is presented in

Table S3. The choice of the method of structural equation modelling (SEM) is explained by it being one of the most precise methods of econometric statistics. It allows the following:

- −

Including in the model any number of factor variables (CSRSDG) and taking into account the systemic and isolated connection between each variable and the targeted outcome. Due to this, model (1) can have several mathematical expressions, which is important for this research, to obtain the most precise results and their correct treatment.

- −

Taking into account and describing in detail the connections between the factor variables and the resulting variable and among each other. To ensure better visualisation of data, the connections between factors, instead of the reflection in the structural equation model, are presented separately in the form of the covariance matrix (which reflects the cross-correlation of factor variables).

- −

Considering covariance of each variable with itself (a measure of its scatter) and the residual components that are not included in the interpretation and are moved beyond the limits of the analysed model (errors of the model). They are important since they ensure the model’s correctness for it is widely known that corporate social responsibility (support for the SDGs) is not the only, and not even the main, factor (set of factors in the context of the SDGs) of companies’ profit and its change (financial risks). Acknowledgement of the imperfection and limitations of the model improves its understanding and raises its practical usefulness.

- −

Determining not only the general connection of indicators but also the regularity of the change in the targeted outcome depending on the change in the factor variables. Due to the determination of this regularity, model (1) will allow not only selecting the CSR practices that are closely connected to profit but also revealing their consequences for profit. This allows differentiating the CSR practices that ensure the contribution to the implementation of the SDGs without financial losses for business (low risk for profit) and the practices that cause losses for the business (high risk for profit). Differentiation between these practices is very important for the answer to the set RQ: explaining the stretch BC in

Figure 1.

Then, based on the results of structural equation modelling (SEM) and using the method of logical analysis, we assess the consequences of the selected practices for profit in regions of the world: positive (low risks for profit) or negative (high risks for profit) consequences.

4. Results

According to

Table 4, the following measures of corporate social responsibility to support the SDGs (UN standards) are implemented in Africa:

Keeping a stable number of jobs or increasing it to support employment.

- −

The activity of the use of CSR measures to support the SDGs (α): 97.96%.

- −

Regularity of support of the SDGs by companies through CSR measures (β): 80.64%.

- −

The ratio of the use of CSR measures to support the SDGs to the worldwide average value (λ): 95.22%.

- −

Level of integrating the SDGs (UN standards) into corporate strategies: (97.96 + 80.64 + 95.22)/3 = 90.94%.

Guarantee of labour rights (official employment).

- −

The activity of the use of CSR measures to support the SDGs (α): 63.27%.

- −

Regularity of support of the SDGs by companies through CSR measures (β): 16.56%.

- −

The ratio of the use of CSR measures to support the SDGs to the worldwide average value (λ): 91.69%.

- −

Level of integrating the SDGs (UN standards) into corporate strategies: (63.27 + 16.56 + 91.69) = 57.17%.

Business’s fight against corruption:

- −

The activity of the use of CSR measures to support the SDGs (α): 100.00%.

- −

Regularity of support of the SDGs by companies through CSR measures (β): 39.23%.

- −

The ratio of the use of CSR measures to support the SDGs to the worldwide average value (λ): 75.01%.

- −

Level of integrating the SDGs (UN standards) into corporate strategies: (100.00 + 39.23 + 75.01)/3 = 71.42%.

The systemic integration of the selected SDGs (UN standards) in the corporate strategies: (90.94 + 51.17 + 71.42)/3 = 73.18% (high).

Table 4.

Representation of the CSR practices to support the SDGs (UN standards) in countries of Africa in 2021.

Table 4.

Representation of the CSR practices to support the SDGs (UN standards) in countries of Africa in 2021.

| | SDG 5, SDG 8 | SDG 8 | SDG 8 | SDG 8 | SDG 13 | SDG 13 | SDG 13 | SDG 16 | SDG 16 |

|---|

| | Gender Gap in Time Spent Doing Unpaid Work (Minutes/Day) | Unemployment Rate (% of the Total Labour Force) | Fundamental Labour Rights Are Effectively Guaranteed (Worst 0–1 Best) | Fatal Work-Related Accidents Embodied in Imports (per 100,000 Population) | Production-Based SO2 Emissions (kg/Capita) | Production-Based Nitrogen Emissions (kg/Capita) | Carbon Pricing Score at EUR60/tCO2 (%, Worst 0–100 Best) | Corruption Perception Index (Worst 0–100 Best) | Corporate Tax Haven Score (Best 0–100 Worst) |

| Number of countries | 49 | 49 | 49 | 49 | 49 | 49 | 49 | 49 | 49 |

| Number of 0 | 49 | 1 | 18 | 3 | 3 | 3 | 49 | 0 | 40 |

| The activity of the use of CSR measures, % | 0.00 | 97.96 | 63.27 | 93.88 | 93.88 | 93.88 | 0.00 | 100.00 | 18.37 |

| Average | 0.00 | 8.41 | 0.54 | 0.23 | 71.62 | 22.87 | 0.00 | 32.31 | 54.85 |

| Standard deviation | 0.00 | 6.78 | 0.09 | 0.55 | 184.71 | 29.80 | 0.00 | 12.67 | 11.53 |

| Variation, % | 0.00 | 80.64 | 16.56 | 243.70 | 257.92 | 130.31 | 0.00 | 39.23 | 21.02 |

| Arithmetic means for the world | 123.33 | 8.01 | 0.59 | 0.71 | 87.74 | 29.49 | 40.86 | 43.07 | 62.19 |

| Average/best value ratio, % | 0 | 95.22 | 91.69 | 314.04 | 122.51 | 128.95 | 0.00 | 75.01 | 113.38 |

According to

Table 5, the following measures of corporate social responsibility to support the SDGs (UN standards) are implemented in E. Europe and C. Asia:

- −

Keeping a stable number of jobs or increasing it to support employment. The level of integrating the SDGs (UN standards) into corporate strategies: 75.43%.

- −

Guarantee of labour rights (official employment). The level of integrating the SDGs (UN standards) into corporate strategies: 57.65%.

- −

Business’s fight against corruption. The level of integrating the SDGs (UN standards) into corporate strategies: 67.25%.

- −

Full-scale payment of taxes (official business). The level of integration of the SDGs (UN standards) into corporate strategies: 47.27%.

The systemic integration of the selected SDGs (UN standards) into corporate strategies: (75.43 + 57.65 + 67.25 + 47.27)/4 = 61.90% (high).

Table 5.

Representation of CSR practices to support the SDGs (UN standards) in countries of E. Europe and C. Asia in 2021.

Table 5.

Representation of CSR practices to support the SDGs (UN standards) in countries of E. Europe and C. Asia in 2021.

| | SDG 5, SDG 8 | SDG 8 | SDG 8 | SDG 8 | SDG 13 | SDG 13 | SDG 13 | SDG 16 | SDG 16 |

|---|

| | Gender Gap in Time Spent Doing Unpaid Work (Minutes/Day) | Unemployment Rate (% of the Total Labour Force) | Fundamental Labour Rights Are Effectively Guaranteed (Worst 0–1 Best) | Fatal Work-Related Accidents Embodied in Imports (per 100,000 Population) | Production-Based SO2 Emissions (kg/Capita) | Production-Based Nitrogen Emissions (kg/Capita) | Carbon Pricing Score at EUR60/tCO2 (%, Worst 0–100 Best) | Corruption Perception Index (Worst 0–100 Best) | Corporate Tax Haven Score (Best 0–100 Worst) |

| Number of countries | 27 | 27 | 27 | 27 | 27 | 27 | 27 | 27 | 27 |

| Number of 0 | 27 | 4 | 11 | 0 | 0 | 0 | 27 | 4 | 18 |

| The activity of the use of CSR measures, % | 0.00 | 85.19 | 59.26 | 100.00 | 100.00 | 100.00 | 0.00 | 85.19 | 33.33 |

| Average | 0.00 | 9.05 | 0.57 | 0.85 | 79.65 | 27.30 | 0.00 | 37.87 | 64.22 |

| Standard deviation | 0.00 | 4.76 | 0.10 | 2.09 | 111.23 | 27.12 | 0.00 | 10.85 | 7.47 |

| Variation, % | 0.00 | 52.60 | 16.84 | 245.95 | 139.66 | 99.33 | 0.00 | 28.64 | 11.64 |

| Arithmetic means for the world | 123.33 | 8.01 | 0.59 | 0.71 | 87.74 | 29.49 | 40.86 | 43.07 | 62.19 |

| Average/best value ratio, % | 0 | 88.49 | 96.86 | 83.62 | 110.16 | 108.01 | 0.00 | 87.93 | 96.84 |

According to

Table 6, the following measures of corporate social responsibility to support the SDGs (UN standards) are implemented in East and South Asia:

- −

Keeping a stable number of jobs or increasing it to support employment. The level of integrating the SDGs (UN standards) into corporate strategies: 115.16%.

- −

Guarantee of labour rights (official employment). The level of integrating the SDGs (UN standards) into corporate strategies: 60.91%.

- −

Business’s fight against corruption. The level of integration of the SDGs (UN standards) into corporate strategies: 49.79%.

The systemic integration of the selected SDGs (UN standards) into corporate strategies: (115.16 + 60.91 + 49.79)/3 = 75.29% (high).

Table 6.

Representation of the CSR practices to support the SDGs (UN standards) in countries of East and South Asia in 2021.

Table 6.

Representation of the CSR practices to support the SDGs (UN standards) in countries of East and South Asia in 2021.

| | SDG 5, SDG 8 | SDG 8 | SDG 8 | SDG 8 | SDG 13 | SDG 13 | SDG 13 | SDG 16 | SDG 16 |

|---|

| | Gender Gap in Time Spent Doing Unpaid Work (Minutes/Day) | Unemployment Rate (% of the Total Labour Force) | Fundamental Labour Rights Are Effectively Guaranteed (Worst 0–1 Best) | Fatal Work-Related Accidents Embodied in Imports (per 100,000 Population) | Production-Based SO2 Emissions (kg/Capita) | Production-Based Nitrogen Emissions (kg/Capita) | Carbon Pricing Score at EUR60/tCO2 (%, Worst 0–100 Best) | Corruption Perception Index (Worst 0–100 Best) | Corporate Tax Haven Score (Best 0–100 Worst) |

| Number of countries | 21 | 21 | 21 | 21 | 21 | 21 | 21 | 21 | 21 |

| Number of 0 | 21 | | 6 | 2 | 1 | 1 | 21 | 0 | 19 |

| The activity of the use of CSR measures, % | 0.00 | 100.00 | 71.43 | 90.48 | 95.24 | 95.24 | 0.00 | 100.00 | 9.52 |

| Average | 0.00 | 4.11 | 0.52 | 0.61 | 59.28 | 20.08 | 0.00 | 39.57 | 69.83 |

| Standard deviation | 0.00 | 2.09 | 0.12 | 1.49 | 90.30 | 20.76 | 0.00 | 15.62 | 16.30 |

| Variation, % | 0.00 | 50.75 | 22.62 | 243.09 | 152.33 | 103.37 | 0.00 | 39.48 | 23.34 |

| Arithmetic means for the world | 123.33 | 8.01 | 0.59 | 0.71 | 87.74 | 29.49 | 40.86 | 43.07 | 62.19 |

| Average/best value ratio, % | 0 | 194.73 | 88.68 | 115.64 | 148.01 | 146.86 | 0.00 | 91.88 | 89.06 |

According to

Table 7, the following CSR measures to support the SDGs (UN standards) are implemented in LAC:

- −

Keeping a stable number of jobs or increasing it to support employment. The level of integrating the SDGs (UN standards) into corporate strategies: 69.86%.

- −

Guarantee of labour rights (official employment). The level of integrating the SDGs (UN standards) into corporate strategies: 69.84%.

- −

Business’s fight against corruption. The level of integration of the SDGs (UN standards) into corporate strategies: 73.82%.

The systemic integration of the selected SDGs (UN standards) into corporate strategies: (69.86 + 69.84 + 73.82)/3 = 71.17 (high).

Table 7.

Representation of the CSR practices to support the SDGs (UN standards) in countries of LAC in 2021.

Table 7.

Representation of the CSR practices to support the SDGs (UN standards) in countries of LAC in 2021.

| | SDG 5, SDG 8 | SDG 8 | SDG 8 | SDG 8 | SDG 13 | SDG 13 | SDG 13 | SDG 16 | SDG 16 |

|---|

| | Gender Gap in Time Spent Doing Unpaid Work (Minutes/Day) | Unemployment Rate (% of the Total Labour Force) | Fundamental Labour Rights Are Effectively Guaranteed (Worst 0–1 Best) | Fatal Work-Related Accidents Embodied in Imports (per 100,000 Population) | Production-Based SO2 Emissions (kg/Capita) | Production-Based Nitrogen Emissions (kg/Capita) | Carbon Pricing Score at EUR60/tCO2 (%, WORST 0–100 best) | Corruption Perception Index (Worst 0–100 Best) | Corporate Tax Haven Score (Best 0–100 Worst) |

| Number of countries | 30 | 30 | 30 | 30 | 30 | 30 | 30 | 30 | 30 |

| Number of 0 | 30 | 4 | 3 | 5 | 5 | 5 | 30 | 3 | 28 |

| The activity of the use of CSR measures, % | 0.00 | 86.67 | 90.00 | 83.33 | 83.33 | 83.33 | 0.00 | 90.00 | 6.67 |

| Average | 0.00 | 10.24 | 0.60 | 0.72 | 150.96 | 37.26 | 0.00 | 41.00 | 85.89 |

| Standard deviation | 0.00 | 4.37 | 0.11 | 2.15 | 259.42 | 45.89 | 0.00 | 14.87 | 19.95 |

| Variation, % | 0.00 | 42.69 | 17.48 | 298.45 | 171.85 | 123.15 | 0.00 | 36.26 | 23.23 |

| Arithmetic means for the world | 123.33 | 8.01 | 0.59 | 0.71 | 87.74 | 29.49 | 40.86 | 43.07 | 62.19 |

| Average/best value ratio, % | 0 | 78.21 | 102.05 | 98.60 | 58.12 | 79.14 | 0.00 | 95.19 | 72.40 |

According to

Table 8, the following CSR measures to support the SDGs (UN standards) are implemented in MENA:

- −

Keeping a stable number of jobs or increasing it to support employment. The level of integrating the SDGs (UN standards) into corporate strategies: 75.49%.

- −

Guarantee of labour rights (official employment). The level of integrating the SDGs (UN standards) into corporate strategies: 50.20%.

- −

Improvement of treatment systems to reduce environmental pollution. The level of integrating the SDGs (UN standards) into corporate strategies: 101.69%.

- −

Business’s fight against corruption. The level of integration of the SDGs (UN standards) into corporate strategies: 77.56%.

- −

Full-scale payment of taxes. The level of integrating the SDGs (UN standards) into corporate strategies: 35.16%.

The systemic integration of the selected SDGs (UN standards) into corporate strategies: (75.49 + 50.20 + 101.69 + 77.56 + 35.16)/5 = 68.02% (high).

According to

Table 9, the following CSR measures to support the SDGs (UN standards) are implemented in Oceania:

- −

Keeping a stable number of jobs or increasing it to support employment. The level of integrating the SDGs (UN standards) into corporate strategies for each of the selected SDGs: 71.65% (high).

Table 8.

Representation of the CSR practices to support the SDGs (UN standards) in countries of MENA in 2021.

Table 8.

Representation of the CSR practices to support the SDGs (UN standards) in countries of MENA in 2021.

| | SDG 5, SDG 8 | SDG 8 | SDG 8 | SDG 8 | SDG 13 | SDG 13 | SDG 13 | SDG 16 | SDG 16 |

|---|

| | Gender Gap in Time Spent Doing Unpaid Work (Minutes/Day) | Unemployment Rate (% of the Total Labour Force) | Fundamental Labour Rights Are Effectively Guaranteed (Worst 0–1 Best) | Fatal Work-Related Accidents Embodied in Imports (per 100,000 Population) | Production-Based SO2 Emissions (kg/Capita) | Production-Based Nitrogen Emissions (kg/Capita) | Carbon Pricing Score at EUR60/tCO2 (%, Worst 0–100 Best) | Corruption Perception Index (Worst 0–100 Best) | Corporate Tax Haven Score (Best 0–100 Worst) |

| Number of countries | 17 | 17 | 17 | 17 | 17 | 17 | 17 | 17 | 17 |

| Number of 0 | 17 | 0 | 9 | 0 | 0 | 0 | 17 | 0 | 15 |

| The activity of the use of CSR measures, % | 0.00 | 100.00 | 47.06 | 100.00 | 100.00 | 100.00 | 0.00 | 100.00 | 11.76 |

| Average | 0.00 | 10.25 | 0.47 | 0.96 | 50.97 | 19.38 | 0.00 | 37.88 | 85.59 |

| Standard deviation | 0.00 | 4.96 | 0.11 | 1.56 | 64.64 | 10.26 | 0.00 | 16.94 | 18.02 |

| Variation, % | 0.00 | 48.34 | 23.24 | 162.22 | 126.81 | 52.92 | 0.00 | 44.71 | 21.06 |

| Arithmetic means for the world | 123.33 | 8.01 | 0.59 | 0.71 | 87.74 | 29.49 | 40.86 | 43.07 | 62.19 |

| Average/best value ratio, % | 0 | 78.13 | 80.30 | 73.64 | 172.13 | 152.15 | 0.00 | 87.96 | 72.66 |

Table 9.

Representation of the CSR practices to support the SDGs (UN standards) in countries of Oceania in 2021.

Table 9.

Representation of the CSR practices to support the SDGs (UN standards) in countries of Oceania in 2021.

| | SDG 5, SDG 8 | SDG 8 | SDG 8 | SDG 8 | SDG 13 | SDG 13 | SDG 13 | SDG 16 | SDG 16 |

|---|

| | Gender Gap in Time Spent Doing Unpaid Work (Minutes/Day) | Unemployment Rate (% of the Total Labour Force) | Fundamental Labour Rights Are Effectively Guaranteed (Worst 0–1 Best) | Fatal Work-Related Accidents Embodied in Imports (per 100,000 Population) | Production-Based SO2 Emissions (kg/Capita) | Production-Based Nitrogen Emissions (kg/Capita) | Carbon Pricing Score at EUR60/tCO2 (%, Worst 0–100 Best) | Corruption Perception Index (Worst 0–100 Best) | Corporate Tax Haven Score (Best 0–100 Worst) |

| Number of countries | 12 | 12 | 12 | 12 | 12 | 12 | 12 | 12 | 12 |

| Number of 0 | 12 | 6 | 12 | 8 | 8 | 8 | 12 | 9 | 12 |

| The activity of the use of CSR measures, % | 0.00 | 50.00 | 0.00 | 33.33 | 33.33 | 33.33 | 0.00 | 25.00 | 0.00 |

| Average | 0.00 | 3.92 | 0.00 | 0.20 | 277.79 | 14.57 | 0.00 | 37.33 | 0.00 |

| Standard deviation | 0.00 | 2.85 | 0.00 | 0.10 | 246.58 | 9.12 | 0.00 | 8.96 | 0.00 |

| Variation, % | 0.00 | 72.66 | 0.00 | 50.88 | 88.76 | 62.61 | 0.00 | 24.01 | 0.00 |

| Arithmetic means for the world | 123.33 | 8.01 | 0.59 | 0.71 | 87.74 | 29.49 | 40.86 | 43.07 | 62.19 |

| Average/best value ratio, % | 0 | 204.42 | 0.00 | 351.49 | 31.58 | 202.38 | 0.00 | 86.68 | 0.00 |

According to

Table 10, the following CSR measures to support the SDGs (UN standards) are implemented in the OECD:

- −

Provision of gender-neutral jobs and fair wages. The level of integrating the SDGs (UN standards) into corporate strategies: 71.65%.

- −

Keeping a stable number of jobs or increasing it to support employment. The level of integrating the SDGs (UN standards) into corporate strategies: 87.46%.

- −

Guarantee of labour rights. The level of integrating the SDGs (UN standards) into corporate strategies: 72.27%.

- −

Provision of occupational safety and health. The level of integrating the SDGs (UN standards) into corporate strategies: 79.59%.

- −

Improvement of treatment systems to reduce environmental pollution. The level of integrating the SDGs (UN standards) into corporate strategies: 69.16%.

- −

Refusal to include environmental costs in the price. The level of integrating the SDGs (UN standards) into corporate strategies: 77.87%.

- −

Business’s fight against corruption. The level of integrating the SDGs (UN standards) into corporate strategies: 92.62%.

- −

Full-scale payment of taxes. The level of integrating the SDGs (UN standards) into corporate strategies: 65.27%.

The systemic integration of the selected SDGs (UN standards) in corporate strategies: (71.65 + 87.46 + 72.27 + 79.59 + 69.16 + 77.86 + 92.62 + 65.27)/8 = 76.99 (very high).

Table 10.

Representation of the CSR practices to support the SDGs (UN standards) in countries of OECD in 2021.

Table 10.

Representation of the CSR practices to support the SDGs (UN standards) in countries of OECD in 2021.

| | SDG 5, SDG 8 | SDG 8 | SDG 8 | SDG 8 | SDG 13 | SDG 13 | SDG 13 | SDG 16 | SDG 16 |

|---|

| | Gender Gap in Time Spent Doing Unpaid Work (Minutes/Day) | Unemployment Rate (% of the Total Labour Force) | Fundamental Labour Rights Are Effectively Guaranteed (Worst 0–1 Best) | Fatal Work-Related Accidents Embodied in Imports (per 100,000 Population) | Production-Based SO2 Emissions (kg/Capita) | Production-Based Nitrogen Emissions (kg/Capita) | Carbon Pricing Score at EUR60/tCO2 (%, Worst 0–100 Best) | Corruption Perception Index (Worst 0–100 Best) | Corporate Tax Haven Score (Best 0–100 Worst) |

| Number of countries | 37 | 37 | 37 | 37 | 37 | 37 | 37 | 37 | 37 |

| Number of 0 | 8 | 0 | 8 | 0 | 0 | 0 | 0 | 0 | 12 |

| The activity of the use of CSR measures, % | 78.38 | 100.00 | 78.38 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 67.57 |

| Average | 123.33 | 7.12 | 0.71 | 1.19 | 82.68 | 45.41 | 40.86 | 66.92 | 59.73 |

| Standard deviation | 45.11 | 3.56 | 0.13 | 0.95 | 64.99 | 19.32 | 13.72 | 15.05 | 14.41 |

| Variation, % | 36.57 | 49.97 | 18.47 | 79.28 | 78.60 | 42.55 | 33.58 | 22.49 | 24.13 |

| Arithmetic means for the world | 123.33 | 8.01 | 0.59 | 0.71 | 87.74 | 29.49 | 40.86 | 43.07 | 62.19 |

| Average/best value ratio, % | 100.00 | 112.42 | 119.95 | 59.48 | 106.11 | 64.94 | 100.01 | 155.37 | 104.12 |

Within the second research task, the specific CSR measures to support the SDGs, which are implemented in the practice of companies in different regions of the world, are identified through a comparison of the selected practices with the CSR measures from

Table 2. The results are shown in

Table 11 and

Table 12.

Table 11.

Specific measures of corporate social responsibility to support the SDGs that are implemented in regions of the world.

Table 11.

Specific measures of corporate social responsibility to support the SDGs that are implemented in regions of the world.

| Direction of CSR | | Indicator of the UN (2021) | Africa | E. Europe and C. Asia | East and South Asia | LAC | MENA | Oceania | OECD |

|---|

| Responsible HRM | SDG 5, SDG 8 | Provision of gender-neutral jobs and fair wages | - | - | - | - | - | - | V |

| SDG 8 | Keeping a stable number of jobs or increasing it to support employment | V | V | V | V | V | V | V |

| SDG 8 | Guarantee of labour rights (official employment) | V | V | V | V | V | - | V |

| SDG 8 | Provision of occupational safety and health | - | - | - | - | - | - | V |

| Responsible production | SDG 13 | Improvement of treatment systems to reduce environmental pollution | - | - | - | | V | - | V |

| SDG 13 | Refusal to include environmental costs in the price | - | - | - | - | - | - | V |

| Responsible finance | SDG 16 | Business’s fight against corruption | V | V | V | V | V | - | V |

| SDG 16 | Full-scale payment of taxes (official business) | - | V | - | - | V | - | V |

According to

Table 11, the universal measures of corporate social responsibility that are implemented to support the SDGs (UN standards) are as follows: keeping a stable number of jobs or increasing it to support employment; guarantee of labour rights (official employment); business’s fight against corruption.

Table 12.

Specific CSR measures to support the SDGs and the scale of their implementation in regions of the world.

Table 12.

Specific CSR measures to support the SDGs and the scale of their implementation in regions of the world.

| Category of Countries | CSR Measures to Support the SDGs | The Activity of the Use of CSR Measures to Support the SDGs, % | Regularity (Variation) of Support of the SDGs by Companies through CSR Measures, % | The Use of CSR Measures to Support the SDGs/the Worldwide Average Value Ratio, % |

|---|

| Africa | Keeping a stable number of jobs or increasing it to support employment | 96.97 | 80.64 | 95.22 |

| Guarantee of labour rights (official employment) | 63.27 | 16.56 | 91.69 |

| Business’s fight against corruption | 100.00 | 39.26 | 75.01 |

| E. Europe and C. Asia | Keeping a stable number of jobs or increasing it to support employment | 85.19 | 52.60 | 88.49 |

| Guarantee of labour rights (official employment) | 59.26 | 16.84 | 96.86 |

| Business’s fight against corruption | 85.19 | 28.64 | 87.93 |

| Full-scale payment of taxes (official business) | 33.33 | 11.64 | 96.84 |

| East and South Asia | Keeping a stable number of jobs or increasing it to support employment | 100.00 | 50.75 | 194.73 |

| Guarantee of labour rights (official employment) | 71.43 | 22.62 | 88.68 |

| Business’s fight against corruption | 100.00 | 39.48 | 9.88 |

| LAC | Keeping a stable number of jobs or increasing it to support employment | 88.67 | 42.69 | 78.21 |

| Guarantee of labour rights (official employment) | 90.00 | 17.48 | 102.05 |

| Business’s fight against corruption | 90.00 | 36.26 | 95.19 |

| MENA | Keeping a stable number of jobs or increasing it to support employment | 100.00 | 48.34 | 78.13 |

| Guarantee of labour rights (official employment) | 47.06 | 23.24 | 80.30 |

| Improvement of treatment systems to reduce environmental pollution | 100.00 | 52.92 | 152.15 |

| Business’s fight against corruption | 100.00 | 44.71 | 87.96 |

| Full-scale payment of taxes (official business) | 11.76 | 21.06 | 72.66 |

| Oceania | Keeping the stable number of jobs or increasing it to support employment | 50.00 | 72.66 | 204.42 |

| OECD | Provision of gender-neutral jobs and fair wages | 78.38 | 36.57 | 100.00 |

| Keeping a stable number of jobs or increasing it to support employment | 100.00 | 49.97 | 112.42 |

| Guarantee of labour rights (official employment) | 78.38 | 18.47 | 119.95 |

| Provision of occupational safety and health | 100.00 | 79.28 | 59.48 |

| Improvement of treatment systems to reduce environmental pollution | 100.00 | 42.55 | 64.94 |

| Refusal to include environmental costs in the price | 100.00 | 33.58 | 100.01 |

| Business’s fight against corruption | 100.00 | 22.49 | 155.37 |

| Full-scale payment of taxes (official business) | 67.57 | 24.13 | 104.12 |

Within the third task of this research, the goal is to determine the CSR practices that have a statistically significant effect on profit. The method of regression analysis is used (according to model (1)) to find the dependencies between all factor variables from

Table 1 and the targeted result (

Table 13).

Table 13.

Regression statistics for all factor variables.

Table 13.

Regression statistics for all factor variables.

| Multiple R | 0.344616 | | | | | |

| R-square | 0.11876 | | | | | |

| Adjusted R-square | 0.07542 | | | | | |

| Standard error | 17.39419 | | | | | |

| Observations | 193 | | | | | |

| Analysis of variance | | | | | |

| | | df | SS | MS | F | Significance F | |

| Regression | 9 | 7461.657 | 829.0731 | 2.740214 | 0.005033 | |

| Residue | 183 | 55,368.07 | 302.5578 | | | |

| Total | 192 | 62,829.73 | | | | |

| | | Coefficients | Standard error | t-Stat | p-Value | Lower 95% | Upper 95% |

| Constant | −2.81524 | 3.249766 | −0.86629 | 0.387466 | −9.22706 | 3.596591 |

| Regression coefficients of factor variables | CSRSDG(1) | 0.114364 | 0.040023 | 2.85747 | 0.004765 | 0.035398 | 0.193329 |

| CSRSDG(2) | 0.043308 | 0.240642 | 0.179968 | 0.857377 | −0.43148 | 0.518098 |

| CSRSDG(3) | 12.53382 | 4.710172 | 2.661012 | 0.008483 | 3.2406 | 21.82705 |

| CSRSDG(4) | −0.17002 | 1.282801 | −0.13254 | 0.894702 | −2.70101 | 2.360959 |

| CSRSDG(5) | 0.00278 | 0.008935 | 0.311144 | 0.756046 | −0.01485 | 0.020409 |

| CSRSDG(6) | −0.01079 | 0.060596 | −0.1781 | 0.858842 | −0.13035 | 0.108764 |

| CSRSDG(7) | −0.37061 | 0.128804 | −2.87731 | 0.004488 | −0.62474 | −0.11648 |

| CSRSDG(8) | −0.00578 | 0.084358 | −0.06853 | 0.945438 | −0.17222 | 0.160658 |

| CSRSDG(9) | −0.06763 | 0.05411 | −1.24994 | 0.212919 | −0.17439 | 0.039125 |

The results of the regression analysis from

Table 11 show three-factor variables that are strongly connected to companies’ profit at the significance level of 0.05:

- −

Gender gap in time spent doing unpaid work (CSRSDG(1)): p-value is 0.004765.

- −

Fundamental labour rights are effectively guaranteed (CSRSDG(3)): p-value is 0.008483.

- −

Carbon Pricing Score at EUR60/tCO2 (CSRSDG(7)): p-value is 0.004488.

This means that all other CSR measures to support the SDGs (UN standards) do not affect companies’ profits.

Specification of this connection allowed obtaining the following equation of multiple linear regression:

According to the equation, the growth of the gender gap in time spent doing unpaid work by 1 minute/day increases companies’ profit by USD 0.11 billion—the effect of CSR on profit, in this case, is negative (the risk of support of the SDGs for profit is high).

The growth of the indicator “fundamental labour rights are effectively guaranteed” by 0.1 leads to an increase in shifted profits of multinationals by USD 11.99 billion—the effect of CSR on profit, in this case, is positive (risk of support of the SDGs for profit is low).

Growth of Carbon Pricing Score at EUR60/tCO

2 by 1% reduces companies’ profit by USD 0.43 billion—the effect of CSR on profit, in this case, is negative (the risk of support of the SDGs for profit is high). Detailed regression statistics for the obtained model are given in

Table 14.

The value of the correlation coefficient (0.3292) that was obtained for this equation in

Table 12 shows that the change of the targeted result by 32.92% is explained by the selected factor variables (the close connection between the variables). R-square and adjusted R-square differ insignificantly (equalling 0.108382 and 0.094229, accordingly), which characterises the considered equation well.

Significance F equals 7.39 × 10−0.5, and the model has successfully passed the F test; therefore, the equation is correct and reliable at the level of significance of 0.01. The confidence interval limits for the regression coefficients are in the range from 0.037795 to 0.19273 (for CSRSDG(1)), from 3.546769 to 20.43144 (for CSRSDG(3)), and from −0.64733 to −0.2216 (for CSRSDG(7)) and are non-contradictory (both limits for each variable have the same sign), which also confirms the reliability of the regression equation. This proves the correctness and reliability of the results obtained and specifies the model (1).

For the systemic reflection of the connections of the studied indicators, we compile a structural equation model (

Figure 2). For this, an expanded (unified) sample is formed, which contains the data for 2021 and 2020, due to which the aggregate data array has 386 observations.

As shown in

Figure 3, the shifted profits of multinationals depend on the factors of responsible HRM, responsible production (corporate environmental responsibility), and responsible finance, which in their totality determine the targeted outcome (financial risk) by 30.13%. Accordingly, the remaining 69.87% are determined by other (residual) factors, which are united in the aggregate error of model (e).

The vivid factor variables are interconnected. The connection between responsible HRM and responsible production (corporate environmental responsibility) equals 21.16%, and with responsible finance—22.40%. The connection between responsible production (corporate environmental responsibility) and responsible finance is 22.97%. All variables of the structural equation model have their variation (scatter of values: var), which is very high in all cases.

For the full consideration and description of the ties between factor variables and the resulting variable and among factor variables, as well as for the better visualisation of data, let us present inter-factor ties—instead of demonstrating them in the structural equation model—separately in the form of the covariance matrix, which reflects the cross-correlation of the factor variables (

Table 15).

The obtained results allowed qualitative (high/low) assessment of the risks of integrating the SDGs into corporate strategies for companies’ profit:

- −

In Africa, E. Europe and C. Asia, East and South Asia, LAC, and MENA, the only practice of corporate social responsibility that influences profit is the guarantee of labour rights (official employment)—since the influence of this practice on profit is positive, the risks of implementing the SDGs for profit are low.

- −

In Oceania, the practice of corporate social responsibility to support the SDGs (UN standards) does not influence companies’ profit (risks for profit are zero, they are absent).

- −

In the OECD, the provision of gender-neutral jobs (fair wages) and refusal to include environmental costs in the price reduce profit to a certain extent, but the guarantee of labour rights (official employment) increases profit significantly. That is why the systemic influence of the CSR practices to support the SDGs (UN standards) on the risks for profit is moderate.

5. Discussion

This paper contributes to the development of the theory of integration of the SDGs into corporate strategies by specifying the features of support of the SDGs with the help of CSR in regions of the world, taking into account the risks for profit (

Table 16).

This paper’s contribution to the literature is as follows:

- −

SDGs (UN standards) are supported by companies in different regions of the world differently. In Oceania, only SDG 8 is supported through the only measure—keeping a stable number of jobs or increasing it to support employment. In Africa, E. Europe and C. Asia, East and South Asia, and LAC, only SDG 8 and SDG 16 are supported. SDG 16 is also supported in MENA. In the OECD, all considered SDGs—5, 8, 13, and 16—are supported. This distinguishes this paper from other works with results on the problems of the SDGs:

Chanda and Goyal (

2020),

He and Kim (

2021),

Hirsu et al. (

2021),

Rawshdeh et al. (

2019),

Ramos-González et al. (

2021), and

Zhao et al. (

2021), in which the measures of integrating the SDGs in corporate strategies are considered in their totality and it is assumed that these measures are widely accessible and used in a complex manner by companies around the world.

- −

CSR measures to support the SDGs are implemented in the practice of companies with different levels of activity in different regions of the world. In Oceania, the result obtained (109.03%) is predetermined by a small number of implemented measures, in combination with which the level of business’s support of the SDGs in Oceania is qualitatively lower than in other regions of the world, but is still high. The highest level of business’s support of the SDGs is observed in the OECD (76.99%). This is the difference between this paper and the existing works on the topic of the integration of the SDGs in corporate strategies:

Dela Cruz et al. (

2020),

Han and Cao (

2021),

Panos and Wilson (

2020), and

Setyowati et al. (

2021), which elaborate on the global support for the SDGs and do not take into account the regional specifics of support for the SDGs in business.

- −

Unlike

Battisti et al. (

2022),

Kong (

2022),

Kornieieva (

2020),

Lassala et al. (

2021),

Martí-Ballester (

2020),

Medentseva (

2017),

Muhmad and Muhamad (

2021),

Petrovskaya et al. (

2022),

Pizzi et al. (

2021),

Roy et al. (

2022),

Rahman (

2021),

Raithatha and Shaw (

2021),

Quang et al. (

2022),

Vagin et al. (

2022), and

Wentzel et al. (

2022), it is proved that the risks of integrating the SDGs (UN standards) into corporate strategies for profit are low (moderate in the OECD). The commercial approach to integrating the SDGs into corporate strategies is implemented in all regions of the world.

6. Conclusions

The following results were obtained in this paper. First, it was discovered that the SDGs (UN standards) are supported by companies in different regions of the world to a different extent, but, on the whole, they are highly integrated into the corporate strategies in each region. The largest support of the SDGs from business is observed in the OECD.

Second, it was proved that the CSR measures to support the SDGs are implemented in the practice of companies with different levels of activity, depending on the region of the world. The universal measures of corporate social responsibility that are implemented to support the SDGs (UN standards) are as follows: keeping a stable number of jobs or increasing it to support employment; guarantee of labour rights (official employment); business’s fight against corruption. Other measures differ among regions of the world.

Third, it was proved that the risks of integrating the SDGs (UN standards) into corporate strategies for profit are low (moderate in the OECD). In all regions of the world, the commercial approach to integrating the SDGs into corporate strategies is implemented.

The theoretical significance of the results obtained consists in the discovered differences showing the necessity for and setting the foundation for the transition from the global to regional management of integrating the SDGs (UN standards) in corporate strategies. This created a wide field for new studies of the experience of different regions of the world. The scientific value of the authors’ conclusions consists in proving the fact that despite the universal (global) formulation of the SDGs, their practical implementation requires the consideration of the specifics of each region of the world. The commercial approach to integrating the SDGs into corporate strategies is the most widespread approach in practice; thus, it deserves to be thoroughly studied.

The practical significance of the authors’ conclusions and developments is due to them allowing increasing the effectiveness of managing the risks of the CSR practices for profit. The dependencies discovered with the help of structural equation modelling (SEM) could be a guide for managing the risks for profit during the integration of the SDGs into corporate strategies for profit. The significance of the developed concept for society is due to the fact that it provided reliable evidence of low risks for profit during the integration of the SDGs into corporate strategies, thus providing companies with a powerful stimulus to expand the CSR measures in business.

It should be acknowledged that the results obtained demonstrated the partial integration of the SDGs into corporate strategies. Therefore, this study made only one of the initial steps on the path to implementing the UN 2030 Agenda for Sustainable Development. The next step should be the development of applied recommendations to fill the gaps in the integration of the SDGs into corporate strategies given the specifics of each region of the world. Future scientific works should be devoted to studying perspectives and developing recommendations for the systemic integration of the SDGs into corporate strategies based on the commercial approach and striving to preserve low risks for profit.

{kind=link}

{kind=link}

{kind=link}