A Hybrid MCDM Model for Evaluating Open Banking Business Partners

Abstract

1. Introduction

2. Literature Review

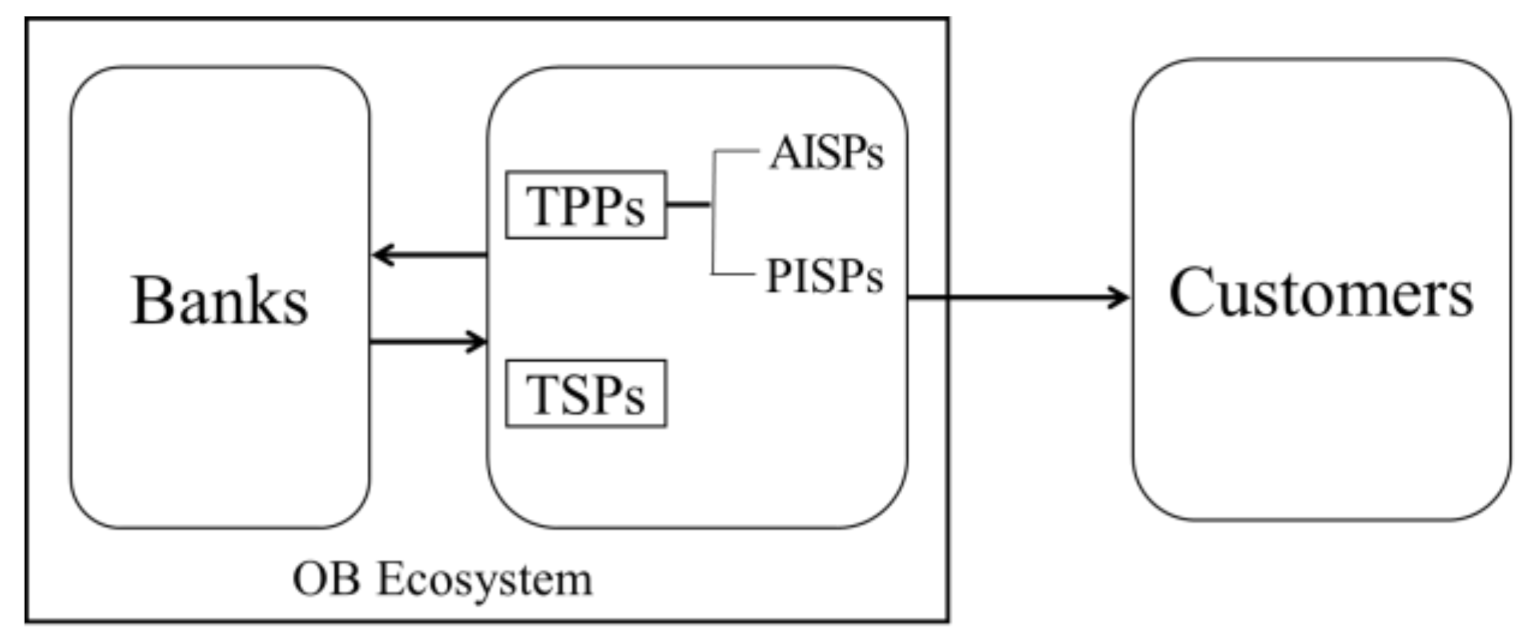

2.1. Introduction to Open Banking

2.1.1. Development of Open Banking

2.1.2. State of Global OB Development

2.1.3. OB-Related Research and Major Discoveries

2.2. Critical Factors of Adopting OB to Strengthen Competitiveness

2.2.1. Superintendency and Regulation

2.2.2. Technology

2.2.3. Environment

2.2.4. Organization

2.3. Applications of MCDM Methods on Selecting TPPs

3. Research Methods

3.1. Best–Worst Method (BWM)

3.2. Modified-VIKOR Aggregator

3.3. Confidence-Weighted Fuzzy Assessment

4. Exemplary Case Study and Discussions

5. Conclusions

- (1)

- The seasoned domain experts helped identify the crucial criteria and their relative importance on evaluating OB partners for the banking sector;

- (2)

- The top three criteria for banks to consider OB are: financial regulations (C1), potential market scale (C7) and rapid services delivery (C9);

- (3)

- The confidence-weighted fuzzy assessment revealed consistent ranking results as the other conventional ones, which may reflect the confidence level of an expert’s judgment on each evaluation. This hybrid approach contains originality and novelty in retrieving experts’ knowledge.

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Glossary of the Acronyms

| Acronyms | Full Names |

| OB | Open Banking |

| PSD2 | Revised Payment Service Directive |

| FinTech | Financial Technology |

| OBIE | Open Banking Implementation Entity |

| TPPs | Third Party Providers |

| AISPs | Account Information Service Providers |

| PISPs | Payment Initiation Service Providers |

| TSPs | Technical Service Providers |

| Open APIs | Open Application Interfaces |

| DMs | Decision-Makers |

| MCDM | Multiple Criteria Decision-Making |

| OBE | Open Banking Europe |

| MAS | Monetary Authority of Singapore |

| TOE | Technology, Organization, and Environment |

| PayTech | Payment Technology |

| AHP | Analytical Hierarchy Process |

| ANP | Analytic Network Process |

| DEMATEL | Decision-Making and Trial Evaluation Laboratory |

| DANP | DEMATEL-Based ANP |

| BWM | Best–Worst Method |

| VIKOR | VlseKriterijuska Optimizacija I Komoromisno Resenje |

| TOPSIS | Technique for Order Performance by Similarity to Ideal Solution |

| MADM | Multiple Attribute Decision-Making |

| SAW | Simple Additive Weighting |

| BO | Best-to-Others |

| OW | Others-to-Worst |

Appendix A. Fuzzy Assessments

{kind=link}

| Expert 1 | Expert 2 | Expert 3 | Expert 4 | Expert 5 | |

|---|---|---|---|---|---|

| High (H) | (0.7, 1.0,1.0) | (0.7, 0.9, 0.9) | (0.7, 1.0,1.0) | (0.7, 1.0,1.0) | (0.8, 1.0,1.0) |

| Moderate (M) | (0.3, 0.6, 0.9) | (0.4, 0.6, 0.8) | (0.2, 0.5, 0.8) | (0.2, 0.5, 0.8) | (0.6, 0.7, 0.8) |

| Low (L) | (0.0, 0.0, 0.5) | (0.0, 0.0, 0.5) | (0.0, 0.0, 0.3) | (0.0, 0.0, 0.3) | (0.0, 0.0, 0.6) |

| C1 | C2 | C3 | C4 | C5 | C6 | C7 | C8 | C9 | C10 | C11 | C12 | C13 | C14 | |

| T | H | M | M | H | H | H | H | H | H | H | H | M | M | H |

| 50% | 70% | 70% | 80% | 80% | 60% | 90% | 80% | 90% | 80% | 80% | 60% | 70% | 70% | |

| M | H | H | H | M | H | H | H | H | H | H | H | M | M | H |

| 50% | 60% | 90% | 80% | 80% | 70% | 90% | 90% | 90% | 90% | 80% | 60% | 70% | 70% | |

| L | M | L | H | H | H | H | H | H | M | H | H | H | M | M |

| 70% | 60% | 90% | 70% | 80% | 80% | 90% | 80% | 90% | 80% | 80% | 60% | 70% | 80% | |

| J | L | M | H | L | M | M | M | M | M | M | M | M | M | M |

| 80% | 70% | 70% | 60% | 70% | 70% | 90% | 80% | 70% | 80% | 80% | 60% | 80% | 80% | |

| (Expert 2) | ||||||||||||||

| C1 | C2 | C3 | C4 | C5 | C6 | C7 | C8 | C9 | C10 | C11 | C12 | C13 | C14 | |

| T | M | H | H | H | H | H | M | H | H | H | H | M | M | L |

| 50% | 70% | 80% | 90% | 80% | 90% | 55% | 80% | 70% | 70% | 80% | 55% | 45% | 40% | |

| M | H | M | H | H | M | M | H | H | H | H | H | H | M | L |

| 70% | 50% | 70% | 70% | 50% | 50% | 80% | 70% | 90% | 90% | 90% | 80% | 60% | 50% | |

| L | H | H | M | M | M | M | H | M | H | H | H | H | M | M |

| 90% | 80% | 50% | 50% | 50% | 50% | 80% | 60% | 70% | 80% | 90% | 80% | 60% | 50% | |

| J | L | L | L | M | M | M | L | M | M | M | L | L | H | H |

| 20% | 20% | 40% | 40% | 50% | 50% | 40% | 40% | 40% | 50% | 30% | 40% | 80% | 70% | |

| (Expert 3) | ||||||||||||||

| C1 | C2 | C3 | C4 | C5 | C6 | C7 | C8 | C9 | C10 | C11 | C12 | C13 | C14 | |

| T | M | M | L | L | M | M | H | M | M | M | L | H | M | M |

| 60% | 60% | 50% | 50% | 70% | 70% | 70% | 70% | 70% | 60% | 50% | 40% | 40% | 40% | |

| M | M | M | L | L | L | L | H | M | M | H | L | M | M | M |

| 60% | 60% | 50% | 50% | 60% | 60% | 65% | 65% | 70% | 60% | 50% | 40% | 40% | 40% | |

| L | M | M | H | H | M | H | H | H | H | H | H | M | H | H |

| 50% | 50% | 80% | 80% | 80% | 80% | 80% | 80% | 70% | 65% | 65% | 40% | 60% | 60% | |

| J | L | L | H | H | H | H | H | H | H | H | H | H | H | H |

| 50% | 50% | 80% | 80% | 80% | 80% | 80% | 80% | 80% | 70% | 65% | 40% | 60% | 60% | |

| (Expert 4) | ||||||||||||||

| C1 | C2 | C3 | C4 | C5 | C6 | C7 | C8 | C9 | C10 | C11 | C12 | C13 | C14 | |

| T | M | M | M | H | H | M | H | M | M | M | H | H | M | M |

| 60% | 80% | 70% | 90% | 80% | 90% | 50% | 60% | 90% | 60% | 50% | 60% | 50% | 30% | |

| M | L | M | M | L | L | L | M | M | M | M | M | H | M | M |

| 60% | 70% | 70% | 50% | 70% | 70% | 50% | 50% | 50% | 60% | 50% | 60% | 50% | 30% | |

| L | H | H | H | M | M | M | H | H | H | H | H | H | M | M |

| 70% | 40% | 80% | 60% | 80% | 80% | 60% | 90% | 80% | 80% | 50% | 80% | 70% | 30% | |

| J | H | L | H | M | M | M | M | H | H | M | H | L | H | H |

| 85% | 20% | 75% | 40% | 60% | 60% | 20% | 80% | 50% | 40% | 30% | 30% | 50% | 20% | |

| (Expert 5) | ||||||||||||||

| C1 | C2 | C3 | C4 | C5 | C6 | C7 | C8 | C9 | C10 | C11 | C12 | C13 | C14 | |

| T | M | M | M | L | M | M | H | L | H | L | L | L | M | M |

| 90% | 70% | 80% | 90% | 80% | 70% | 80% | 80% | 90% | 80% | 80% | 80% | 80% | 80% | |

| M | L | L | L | L | L | L | M | M | M | M | M | M | M | M |

| 90% | 90% | 90% | 80% | 90% | 90% | 90% | 90% | 90% | 90% | 90% | 90% | 80% | 80% | |

| L | H | M | H | H | H | M | H | L | L | L | L | L | M | M |

| 80% | 90% | 90% | 90% | 90% | 90% | 90% | 90% | 80% | 90% | 90% | 90% | 80% | 80% | |

| J | H | H | M | M | M | M | L | M | L | L | L | L | M | M |

| 90% | 90% | 70% | 80% | 70% | 80% | 90% | 80% | 90% | 70% | 70% | 70% | 80% | 80% | |

References

- Aneesh, Z.; Grilo, A. The emergence of digital platforms: A conceptual platform architecture and impact on industrial engineering. Comput. Ind. Eng. 2019, 136, 546–555. [Google Scholar] [CrossRef]

- Payment Services Directive: Frequently Asked Questions. Available online: https://ec.europa.eu/commission/presscorner/detail/en/MEMO_15_5793 (accessed on 23 October 2020).

- Polasik, M.; Huterska, A.; Iftikhar, R.; Mikula, Š. The impact of Payment Services Directive 2 on the PayTech sector development in Europe. J. Econ. Behav. Organ. 2020, 178, 385–401. [Google Scholar] [CrossRef]

- Mansfield-Devine, S. Open banking: Opportunity and danger. Comput. Fraud. Secur. 2016, 10, 8–13. [Google Scholar] [CrossRef]

- Open Banking... So What? Available online: https://www.pwc.com/it/en/industries/banking/future-open-banking.html (accessed on 28 June 2020).

- Get Started. Available online: https://www.openbanking.org.uk/providers/ (accessed on 8 October 2020).

- What is Open Banking? Available online: https://www.openbanking.org.uk/ (accessed on 8 October 2020).

- Premchand, A.; Choudhry, A. Open Banking & APIs for Transformation in Banking. In Proceedings of the 2018 International Conference on Communication (IEEE), Computing and Internet of Things (IC3IoT), Chennai, India, 15–17 February 2018. [Google Scholar] [CrossRef]

- Yip, A.W.H.; Bocken, N.M.P. Sustainable business model archetypes for the banking industry. J. Clean. Prod. 2018, 174, 150–169. [Google Scholar] [CrossRef]

- Bouncken, R.B.; Fredrich, V.; Kraus, S.; Ritala, P. Innovation alliances: Balancing value creation dynamics, competitive intensity and market overlap. J. Bus. Res. 2020, 22, 240–247. [Google Scholar] [CrossRef]

- Huang, J.Y.; Shen, K.Y.; Shieh, J.C.P.; Tzeng, G.H. Strengthen financial holding companies’ business sustainability by using a hybrid corporate governance evaluation model. Sustainability 2019, 11, 582. [Google Scholar] [CrossRef]

- Shen, K.Y.; Zavadskas, E.K.; Tzeng, G.H. Updated discussions on “hybrid multiple criteria decision-making methods: A review of applications for sustainability issues”. Ekon. Istraz. 2018, 31, 1437–1452. [Google Scholar] [CrossRef]

- Our Scope. Available online: https://www.openbanking-europe.eu/who-we-are/ (accessed on 9 October 2020).

- Atzori, M.; Koutrika, G.; Pes, B.; Tanca, L. Special issue on “Data exploration in the web 3.0 age”. Future Gener. Comput. Syst. 2020, 112, 1177–1197. [Google Scholar] [CrossRef]

- The History of Open Banking. Available online: https://knowledge.fintecsystems.com/en/blog/the-history-of-open-banking (accessed on 20 October 2020).

- Background to Open Banking. Available online: https://www.openbanking.org.uk/about-us/ (accessed on 8 October 2020).

- Real Demand for Open Banking as User Numbers Grow to More Than Two Million. Available online: https://www.openbanking.org.uk/about-us/latest-news/real-demand-for-open-banking-as-user-numbers-grow-to-more-than-two-million/ (accessed on 8 October 2020).

- Open Banking Europe: Security & Identification Standards for APIs & Communications. Available online: https://www.openbankingeurope.eu/media/1943/oasis-obe-api-identification-and-security-standards-for-apis-and-communications.pdf (accessed on 20 February 2021).

- Number and Type of TPPs Per Country. Available online: https://www.openbankingeurope.eu/media/1841/tpp-map-september.pdf (accessed on 23 October 2020).

- ABS-MAS Financial World: Finance-as-a-Service API Playbook; Monetary Authority of Singapore: Singapore, 2016; pp. 6–16.

- Open Banking. Available online: https://www.ausbanking.org.au/policy/the-future/open-banking/ (accessed on 2 October 2020).

- The Global Open Banking Report 2020–Beyond Open Banking, Into the Open Finance and Open Data Economy. Available online: https://thepaypers.com/reports/the-global-open-banking-report-2020-beyond-open-banking-into-the-open-finance-and-open-data-economy/r1244913 (accessed on 27 November 2020).

- Hong Kong Monetary Authority. Open API Framework for the Hong Kong Banking Sector; Hong Kong Monetary Authority: Hong Kong, 2018; pp. 3–24. [Google Scholar]

- Open Banking around the World: Towards a Cross-Industry Data Sharing Ecosystem. Available online: https://www2.deloitte.com/tw/en/pages/financial-services/articles/open-banking-around-the-world.html (accessed on 23 October 2020).

- iThome News Report (in Chinese). Available online: https://www.ithome.com.tw/news/137909 (accessed on 12 September 2020).

- Borgogno, O.; Colangelo, G. Data sharing and interoperability: Fostering innovation and competition through APIs. Comput. Law Secur. Rev. 2019, 35. [Google Scholar] [CrossRef]

- Wang, H.; Ma, S.; Dai, H.N.; Imran, M.; Wang, T. Blockchain-based data privacy management with nudge theory in Open Banking. Future Gener. Comput. Syst. 2020, 110, 812–823. [Google Scholar] [CrossRef]

- Wolters, P.T.J.; Jacobs, B.P.F. The security of access to accounts under the PSD2. Comput. Law Secur. Rev. 2019, 35, 29–41. [Google Scholar] [CrossRef]

- Shaikh, A.A.; Alharthi, M.D.; Alamoudi, H.O. Examining key drivers of consumer experience with (non-financial) digital services?—An Exploratory study. J. Retail. Consum. Serv. 2020, 55, 102073. [Google Scholar] [CrossRef]

- Dratva, R. Is open banking driving the financial industry towards a true electronic market? Electron. Mark. 2020, 30, 65–67. [Google Scholar] [CrossRef]

- Nam, D.; Lee, J.; Lee, H. Business analytics adoption process: An innovation diffusion perspective. Int. J. Inf. Manag. 2019, 49, 411–423. [Google Scholar] [CrossRef]

- Zhu, K.; Kraemer, K.L.; Xu, S.; Dedrick, J. Information technology payoff in e-business environments: An international perspective on value creation of e-business in the financial services industry. J. Manag. Inform. Syst. 2004, 21, 17–54. [Google Scholar] [CrossRef]

- Yang, M.; He, Y. How does the stock market react to financial innovation regulations? Financ. Res. Lett. 2019, 30, 259–265. [Google Scholar] [CrossRef]

- Van Loo, R. Making innovation more competitive: The case of FinTech. UCLA Law Rev. 2018, 65, 232–279. [Google Scholar]

- Fratzscher, M.; König, P.J.; Lambert, C. Credit provision and banking stability after the Great Financial Crisis: The role of bank regulation and the quality of governance. J. Int. Money Finan. 2016, 66, 113–135. [Google Scholar] [CrossRef]

- Buffart, M.; Croidieu, G.; Kim, P.H.; Bowman, R. Even winners need to learn: How government entrepreneurship programs can support innovative ventures. Res. Policy 2020, 49, 104052. [Google Scholar] [CrossRef]

- Chik, W.B. ‘Customary Internet-ional Law’: Creating a body of customary law for cyberspace. Part 1: Developing rules for transitioning custom into law. Comput. Law Secur. Rev. 2010, 26, 3–22. [Google Scholar] [CrossRef]

- Shah, M.H.; Siddiqui, F.A. Organisational critical success factors in adoption of e-banking at the Woolwich Bank. Int. J. Inf. Manag. 2006, 26, 442–456. [Google Scholar] [CrossRef]

- Yu, W.; Ding, Z.; Liu, L.; Wang, X.; Crossley, R.D. Petri Net-based Methods for analyzing structural security in e-commerce business processes. Futur. Gener. Comp. Syst. 2020, 109, 611–620. [Google Scholar] [CrossRef]

- Choi, H.; Park, J.; Kim, J.; Jung, Y. Consumer preferences of attributes of mobile payment services in South Korea. Telemat. Inform. 2020, 51, 101397. [Google Scholar] [CrossRef]

- Baker, J. The technology–organization–environment framework. Information Systems Theory: Explaining and Predicting Our Digital Society; Dwivedi, Y.K., Wade, M.R., Schneberger, S.L., Eds.; Springer: New York, NY, USA, 2012; Volume 1, pp. 231–245. [Google Scholar]

- Sengupta, A.; Sena, V. Impact of open innovation on industries and firms—A dynamic complex systems view. Technol. Forecast. Soc. Chang. 2020, 159, 120199. [Google Scholar] [CrossRef]

- Markovic, S.; Jovanovic, M.; Bagherzadeh, M.; Sancha, C.; Sarafinovska, M.; Qiu, Y. Priorities when selecting business partners for service innovation: The contingency role of product innovation. Ind. Mark. Manag. 2020, 88, 378–388. [Google Scholar] [CrossRef]

- Sharma, D.; Pandey, S.K.; Chandwani, R.; Pandey, P.; Joseph, R. Internet channel cannibalization and its influence on salesperson performance outcomes in an emerging economy context. J. Retail. Consum. Serv. 2018, 45, 179–189. [Google Scholar] [CrossRef]

- Piderit, S.K. Rethinking resistance and recognizing ambivalence: A multidimensional view of attitudes toward an organizational change. Acad. Manag. Rev. 2000, 25, 783–794. [Google Scholar] [CrossRef]

- He, D.; Ho, C.Y.; Xu, L. Risk and return of online channel adoption in the banking industry. Pac. Basin Financ. J. 2020, 60, 101268. [Google Scholar] [CrossRef]

- Del Gaudio, B.L.; Porzio, C.; Sampagnaro, G.; Verdoliva, V. How do mobile, internet and ICT diffusion affect the banking industry? An empirical analysis. Eur. Manag. J. 2020. [Google Scholar] [CrossRef]

- Frizzo-Barker, J.; Chow-White, P.A.; Adams, P.R.; Mentanko, J.; Ha, D.; Green, S. Blockchain as a disruptive technology for business: A systematic review. Int. J. Inf. Manag. 2020, 51, 102029. [Google Scholar] [CrossRef]

- Kim, H.W. The effects of switching costs on user resistance to enterprise systems implementation. IEEE Trans. Eng. Manag. 2011, 58, 471–482. [Google Scholar] [CrossRef]

- Stamoulis, D.; Kanellis, P.; Martakos, D. An approach and model for assessing the business value of e-banking distribution channels: Evaluation as communication. Int. J. Inf. Manag. 2002, 22, 247–261. [Google Scholar] [CrossRef]

- Opricovic, S.; Tzeng, G.H. Compromise solution by MCDM methods: A comparative analysis of VIKOR and TOPSIS. Eur. J. Oper. Res. 2004, 156, 445–455. [Google Scholar] [CrossRef]

- Bakioglu, G.; Atahan, A.O. AHP integrated TOPSIS and VIKOR methods with pythagorean fuzzy sets to prioritize risks in self-driving vehicles. Appl. Soft. Comput. 2020, 99, 106948. [Google Scholar] [CrossRef]

- Shen, K.Y.; Tzeng, G.H. A decision rule-based soft computing model for supporting financial performance improvement of the banking industry. Soft Comput. 2015, 19, 859–874. [Google Scholar] [CrossRef]

- Shen, K.Y.; Yan, M.R.; Tzeng, G.H. Combining VIKOR-DANP model for glamor stock selection and stock performance improvement. Knowl. Based Syst. 2014, 58, 86–97. [Google Scholar] [CrossRef]

- Gupta, H.; Barua, M.K. Identifying enablers of technological innovation for Indian MSMEs using best-worst multi criteria decision making method. Technol. Forecast. Soc. Chang. 2016, 107, 69–79. [Google Scholar] [CrossRef]

- Feng, Y.; Hong, Z.; Tian, G.; Li, Z.; Tan, J.; Hu, H. Environmentally friendly MCDM of reliability-based product optimisation combining DEMATEL-based ANP, interval uncertainty and Vlse Kriterijumska Optimizacija Kompromisno Resenje (VIKOR). Inf. Sci. 2018, 442‒443, 128–144. [Google Scholar] [CrossRef]

- Nouri, F.A.; Esbouei, S.K.; Antucheviciene, J. A Hybrid MCDM approach based on fuzzy ANP and fuzzy TOPSIS for technology selection. Informatica 2015, 26, 369–388. [Google Scholar] [CrossRef]

- Joshi, B.P.; Gegov, A. Confidence levels q-rung orthopair fuzzy aggregation operators and its applications to MCDM problems. Int. J. Intell. Syst. 2020, 35, 125–149. [Google Scholar] [CrossRef]

- Kilic, H.S.; Zaim, S.; Delen, D. Development of a hybrid methodology for ERP system selection: The case of Turkish Airlines. Decis. Support. Syst. 2014, 66, 82–92. [Google Scholar] [CrossRef]

- Wang, Y.L.; Shen, K.Y.; Huang, J.Y.; Luarn, P. Use of a refined corporate social responsibility model to mitigate information asymmetry and evaluate performance. Symmetry 2020, 12, 1349. [Google Scholar] [CrossRef]

- Chang, T.W.; Lo, H.W.; Chen, K.Y.; Liou, J.J. A novel FMEA model based on rough BWM and rough TOPSIS-AL for risk assessment. Mathematics 2019, 7, 874. [Google Scholar] [CrossRef]

- Camargo Pérez, J.; Carrillo, M.H.; Montoya-Torres, J.R. Multi-criteria approaches for urban passenger transport systems: A literature review. Ann. Oper. Res. 2015, 226, 69–87. [Google Scholar] [CrossRef]

- Rezaei, J. Best-worst multi-criteria decision-making method. Omega 2015, 53, 49–57. [Google Scholar] [CrossRef]

- Rezaei, J. Best-worst multi-criteria decision-making method: Some properties and a linear model. Omega 2016, 64, 126–130. [Google Scholar] [CrossRef]

- Zavadskas, E.K.; Turskis, Z.; Kildienė, S. State of art surveys of overviews on MCDM/MADM methods. Technol. Econ. Dev. Econ. 2014, 20, 165–179. [Google Scholar] [CrossRef]

- Simon, H.A. Bounded rationality in social science: Today and tomorrow. Mind Soc. 2000, 1, 25–39. [Google Scholar] [CrossRef]

- Fenton, N.; Wang, W. Risk and confidence analysis for fuzzy multicriteria decision making. Knowl. Based Syst. 2006, 19, 430–437. [Google Scholar] [CrossRef]

- Financial Institutes Information. Available online: https://www.banking.gov.tw/ch/home.jsp?id=60&parentpath=0,4&mcustomize=FscSearch_BankType.jsp&type=1 (accessed on 14 February 2021).

- 2020Q3 Mobile Telecommunication Statistics. Available online: https://www.ncc.gov.tw/chinese/gradation.aspx?site_content_sn=4160&is_history=0 (accessed on 1 January 2021).

| Number of Experts | ||||

|---|---|---|---|---|

| Banking or FinTech | Consulting Firm | Academics | Total | |

| Delphi Survey | 5 | 3 | 1 | 9 |

| BWM Weighting Model | 3 | 4 | 1 | 8 |

| Four Alternatives’ Assessments | 1 | 4 | - | 5 |

| Job Titles | Senior Vice President, CEO, IT Department Head, Senior Manager | Vice President, Senior Consultant | Full Professor | |

| Dimensions | Criteria | Description |

|---|---|---|

| Superintendency and Regulation (D1) | Financial Regulations (C1) | Massive government restrictions or supervisions on OB business, or inappropriate regulations on OB innovation services. |

| Conflicts in policies or regulations (C2) | Banks, TPPs, and the government facing conflicts with different laws or regulations, and trying to reconcile among them. | |

| Technology (D2) | API Technology (C3) | Banks being competent for providing mobile API interfaces to serve customers and to experience various OB financial services. |

| Authentication Technology (C4) | Banks capable of providing secure and convenient user authentication technology to facilitate customers to verify account identity and to complete transactions. | |

| OB System Reliability (C5) | OB neo systems operating smoothly and integrating adequately with the banks’ legacy systems to ensure stability and reliability. | |

| Internet Security (C6) | Bank providing strictly protection of customer data and privacy to prevent cybercrimes. | |

| Environment (D3) | Potential Market Scale (C7) | OB service providing a profitable potential market scale for the bank. |

| Response to Competitors’ Action (C8) | Analyzing OB market competition and response to competitors’ action | |

| Rapid Services Delivery (C9) | Enabling OB system to provide rapid and prime quality service. | |

| Organization (D4) | Sales increase in original business (C10) | Original business sales growing due to the increase of market scale of collaborating alliance. |

| New Incomes from OB (C11) | Incomes from newly developed OB service or customers. | |

| Top Management Support (C12) | Authority of controlling and allocating internal and human resources; support to reform the organization, reconcile resistance to change, and resolve organization conflicts | |

| Resistance to Change (C13) | Employees’ resistance or resources dispute due to organization reforming or resource re-allocation. | |

| Organization Conflict (C14) | Conflicts causing by differences in demands, objections, and values among internal organizational departments when OB adoption. |

| Best | Best-to-Others (BO) | Worst | Others-to-Worst (OW) | |||||||

|---|---|---|---|---|---|---|---|---|---|---|

| D1 | D2 | D3 | D4 | D1 | D2 | D3 | D4 | |||

| Expert 1 | D3 | 1 | 5 | 1 | 3 | D2 | 1/9a | 1 | 1/7 | 1/5 |

| Expert 2 | D2 | 5 | 1 | 3 | 3 | D1 | 1 | 1/3 | 1/5 | 1/5 |

| Expert 3 | D3 | 2 | 1 | 1 | 9 | D4 | 1/5 | 1/7 | 1/9 | 1 |

| Expert 4 | D1 | 1 | 3 | 1 | 2 | D2 | 1/4 | 1 | 1/3 | 1/2 |

| Expert 5 | D1 | 1 | 9 | 1 | 2 | D2 | 1/9 | 1 | 1/7 | 1/5 |

| Expert 6 | D3 | 2 | 2 | 1 | 2 | D2 | 1/2 | 1 | 1 | 1 |

| Expert 7 | D3 | 8 | 6 | 1 | 7 | D2 | 1/7 | 1 | 1/9 | 1/8 |

| Expert 8 | D1 | 1 | 2 | 1 | 1 | D2 | 1/2 | 1 | 1 | 1 |

| Best | D1 (BO) | Worst | D1 (OW) | Best | D2 (BO) | Worst | D2 (OW) | |||||||||||||||||||||||||||||||

| C1 | C2 | C1 | C2 | C3 | C4 | C5 | C6 | C3 | C4 | C5 | C6 | |||||||||||||||||||||||||||

| Expert1 | C1 | 1 | 3 | C2 | 1/3 | 1 | C6 | 9 | 7 | 5 | 1 | C3 | 1 | 1/5 | 1/7 | 1/9 | ||||||||||||||||||||||

| Expert2 | C1 | 1 | 5 | C2 | 1/5 | 1 | C6 | 7 | 9 | 3 | 1 | C4 | 1/3 | 1 | 1/5 | 1/7 | ||||||||||||||||||||||

| Expert3 | C1 | 1 | 1 | C2 | 1 | 1 | C6 | 3 | 1 | 2 | 1 | C3 | 1 | 1/2 | 1/2 | 1/3 | ||||||||||||||||||||||

| Expert4 | C1 | 1 | 1 | C2 | 1 | 1 | C5 | 3 | 2 | 1 | 2 | C3 | 1 | 1/2 | 1/4 | 1/3 | ||||||||||||||||||||||

| Expert5 | C1 | 1 | 2 | C2 | 1/2 | 1 | C6 | 9 | 3 | 2 | 1 | C3 | 1 | 1/3 | 1/5 | 1/9 | ||||||||||||||||||||||

| Expert6 | C2 | 1 | 1 | C1 | 1 | 1 | C5 | 2 | 1 | 1 | 1 | C3 | 1 | 1 | 1/2 | 1 | ||||||||||||||||||||||

| Expert7 | C2 | 8 | 1 | C1 | 1 | 1/8 | C6 | 9 | 6 | 6 | 1 | C3 | 1 | 1/7 | 1/6 | 1/8 | ||||||||||||||||||||||

| Expert8 | C1 | 1 | 1 | C2 | 1 | 1 | C4 | 3 | 1 | 2 | 1 | C3 | 1 | 1/3 | 1 | 1/2 | ||||||||||||||||||||||

| Best | D3 (BO) | Worst | D3 (OW) | Best | D4 (BO) | Worst | D4 (OW) | |||||||||||||||||||||||||||||||

| C7 | C8 | C9 | C7 | C8 | C9 | C10 | C11 | C12 | C13 | C14 | C10 | C11 | C12 | C13 | C14 | |||||||||||||||||||||||

| Expert1 | C8 | 3 | 1 | 5 | C9 | 1/3 | 1/7 | 1 | C12 | 9 | 7 | 1 | 3 | 5 | C11 | 1/3 | 1 | 1/7 | 1/5 | 1/5 | ||||||||||||||||||

| Expert2 | C9 | 5 | 3 | 1 | C7 | 1 | 1/3 | 1/5 | C12 | 5 | 3 | 1 | 5 | 7 | C14 | 1/5 | 1/5 | 1/7 | 1/3 | 1 | ||||||||||||||||||

| Expert3 | C7 | 1 | 1 | 3 | C9 | 1/3 | 1/2 | 1 | C10 | 1 | 2 | 1 | 3 | 9 | C14 | 1/9 | 1/5 | 1/7 | 1/3 | 1 | ||||||||||||||||||

| Expert4 | C9 | 2 | 3 | 1 | C8 | 1/3 | 1 | 1/4 | C11 | 3 | 1 | 2 | 4 | 4 | C11 | 1 | 1/4 | 1/3 | 1/2 | 1/2 | ||||||||||||||||||

| Expert5 | C9 | 2 | 1 | 1 | C7 | 1 | 1/2 | 1/3 | C12 | 1 | 2 | 1 | 3 | 8 | C14 | 1/7 | 1/5 | 1/9 | 1/3 | 1 | ||||||||||||||||||

| Expert6 | C7 | 1 | 3 | 2 | C8 | 1/3 | 1 | 1/2 | C12 | 5 | 3 | 1 | 1 | 1 | C10 | 1 | 1 | 1/5 | 1/4 | 1/4 | ||||||||||||||||||

| Expert7 | C7 | 1 | 8 | 6 | C8 | 1/8 | 1 | 1/6 | C12 | 8 | 8 | 1 | 5 | 6 | C13 | 1/7 | 1/7 | 1/9 | 1 | 1/2 | ||||||||||||||||||

| Expert8 | C7 | 1 | 2 | 1 | C8 | 1/2 | 1 | 1 | C12 | 2 | 1 | 1 | 1 | 2 | C14 | 1 | 1 | 1/2 | 1 | 1 | ||||||||||||||||||

| Dimensional Weights | Criteria | Local Weights | Global Weights |

|---|---|---|---|

| D1 (27.14%) | C1 | 64.24% | 17.43% (Top) |

| C2 | 35.76% | 9.71% | |

| D2 (16.37%) | C3 | 9.92% | 1.62% |

| C4 | 22.30% | 3.65% | |

| C5 | 23.74% | 3.89% | |

| C6 | 44.03% | 7.21% | |

| D3 (38.26%) | C7 | 37.73% | 14.44% (Second) |

| C8 | 28.64% | 10.96% | |

| C9 | 33.63% | 12.87% (Third) | |

| D4 (18.23%) | C10 | 16.43% | 3.00% |

| C11 | 17.95% | 3.27% | |

| C12 | 37.77% | 6.89% | |

| C13 | 15.26% | 2.78% | |

| C14 | 12.59% | 2.30% |

| TPPs | Business Category | Registered Capital a (In Million TWD) | No. of Users b (Million) | Official Websites |

|---|---|---|---|---|

| Taiwan Mobile (T) | Telecom. | 35,124 | 7.09 | english.taiwanmobile.com (accessed on 16 February 2021) |

| momo e-Shop (M) | e-Commerce | 1400 | 9.17 | en.fmt.com.tw (accessed on 16 February 2021) |

| Line (L) | Instant Communication | 841 | 21.00 | line.me/zh-hant (accessed on 16 February 2021) |

| JKOPay (J) | Mobile Payment | 612 | 4.00 | www.jkos.com (accessed on 16 February 2021) |

| Criteria | BWM Weights | Crisp Assessment | Confidence-Weighted Fuzzy Assessment | ||||||

|---|---|---|---|---|---|---|---|---|---|

| T | M | L | J | T | M | L | J | ||

| C1 | 17.43% | 5.80 | 5.60 | 7.60 | 5.20 | 3.96 | 3.24 | 5.71 | 3.64 |

| C2 | 9.71% | 6.00 | 5.40 | 6.40 | 4.80 | 4.48 | 3.34 | 4.12 | 2.73 |

| C3 | 1.62% | 5.80 | 5.80 | 7.40 | 6.40 | 4.20 | 4.04 | 6.78 | 5.16 |

| C4 | 3.65% | 7.00 | 4.80 | 6.60 | 5.40 | 5.14 | 2.74 | 5.58 | 3.64 |

| C5 | 3.89% | 7.40 | 5.00 | 6.40 | 5.80 | 6.14 | 2.66 | 5.32 | 4.46 |

| C6 | 7.21% | 6.60 | 5.00 | 6.00 | 6.00 | 5.28 | 2.48 | 5.54 | 4.60 |

| C7 | 14.44% | 7.40 | 6.80 | 8.40 | 5.40 | 5.93 | 5.99 | 7.26 | 2.97 |

| C8 | 10.96% | 5.80 | 6.20 | 6.60 | 6.00 | 4.50 | 5.29 | 5.58 | 5.44 |

| C9 | 12.87% | 6.40 | 6.40 | 6.80 | 5.80 | 6.16 | 5.70 | 5.36 | 3.84 |

| C10 | 3.00% | 5.80 | 7.20 | 7.20 | 6.40 | 4.22 | 6.18 | 5.85 | 3.50 |

| C11 | 3.27% | 6.00 | 6.40 | 7.40 | 5.40 | 4.20 | 4.92 | 5.49 | 3.05 |

| C12 | 6.89% | 5.60 | 7.00 | 6.60 | 5.00 | 3.18 | 4.90 | 5.04 | 1.91 |

| C13 | 2.78% | 5.60 | 5.60 | 6.40 | 6.80 | 3.40 | 3.58 | 4.46 | 5.50 |

| C14 | 2.30% | 5.60 | 5.60 | 6.00 | 6.80 | 3.21 | 3.25 | 4.06 | 4.78 |

| Final Score | 6.27 | 6.00 | 7.03 | 5.57 | 4.79 | 4.37 | 5.58 | 3.74 | |

| (Ranking) | (2) | (3) | (1) | (4) | (2) | (3) | (1) | (4) | |

| Criteria | BWM Weights | Crisp Assessment | Confidence-Weighted Fuzzy Assessment | ||||||

|---|---|---|---|---|---|---|---|---|---|

| T | M | L | J | T | M | L | J | ||

| C1 | 17.43% | 0.42 | 0.44 | 0.24 | 0.48 | 0.60 | 0.68 | 0.43 | 0.64 |

| C2 | 9.71% | 0.40 | 0.46 | 0.36 | 0.52 | 0.55 | 0.67 | 0.59 | 0.73 |

| C3 | 1.62% | 0.42 | 0.42 | 0.26 | 0.36 | 0.58 | 0.60 | 0.32 | 0.48 |

| C4 | 3.65% | 0.30 | 0.52 | 0.34 | 0.46 | 0.49 | 0.73 | 0.44 | 0.64 |

| C5 | 3.89% | 0.26 | 0.50 | 0.36 | 0.42 | 0.39 | 0.73 | 0.47 | 0.55 |

| C6 | 7.21% | 0.34 | 0.50 | 0.40 | 0.40 | 0.47 | 0.75 | 0.45 | 0.54 |

| C7 | 14.44% | 0.26 | 0.32 | 0.16 | 0.46 | 0.41 | 0.40 | 0.27 | 0.70 |

| C8 | 10.96% | 0.42 | 0.38 | 0.34 | 0.40 | 0.55 | 0.47 | 0.44 | 0.46 |

| C9 | 12.87% | 0.36 | 0.36 | 0.32 | 0.42 | 0.38 | 0.43 | 0.46 | 0.62 |

| C10 | 3.00% | 0.42 | 0.28 | 0.28 | 0.36 | 0.58 | 0.38 | 0.42 | 0.65 |

| C11 | 3.27% | 0.40 | 0.36 | 0.26 | 0.46 | 0.58 | 0.51 | 0.45 | 0.70 |

| C12 | 6.89% | 0.44 | 0.30 | 0.34 | 0.50 | 0.68 | 0.51 | 0.50 | 0.81 |

| C13 | 2.78% | 0.44 | 0.44 | 0.36 | 0.32 | 0.66 | 0.64 | 0.55 | 0.45 |

| C14 | 2.30% | 0.44 | 0.44 | 0.40 | 0.32 | 0.68 | 0.68 | 0.59 | 0.52 |

| S | 37.26% | 39.99% | 29.73% | 44.27% | 52.06% | 56.28% | 44.16% | 62.60% | |

| R | 7.32% | 7.67% | 4.18% | 8.37% | 10.53% | 11.79% | 7.47% | 11.08% | |

| Q = 0.95) | 35.76% | 38.38% | 28.45% | 42.48% | 49.99% | 54.05% | 42.32% | 60.02% | |

| Q = 0.90) | 34.27% | 36.76% | 27.17% | 40.68% | 47.91% | 51.83% | 40.49% | 57.45% | |

| Q = 0.85) | 32.77% | 35.15% | 25.90% | 38.89% | 45.83% | 49.60% | 38.65% | 54.87% | |

| (Ranking) | (2) | (3) | (1) | (4) | (2) | (3) | (1) | (4) | |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Daiy, A.K.; Shen, K.-Y.; Huang, J.-Y.; Lin, T.M.-Y. A Hybrid MCDM Model for Evaluating Open Banking Business Partners. Mathematics 2021, 9, 587. https://doi.org/10.3390/math9060587

Daiy AK, Shen K-Y, Huang J-Y, Lin TM-Y. A Hybrid MCDM Model for Evaluating Open Banking Business Partners. Mathematics. 2021; 9(6):587. https://doi.org/10.3390/math9060587

Chicago/Turabian StyleDaiy, Alexander Kuan, Kao-Yi Shen, Jim-Yuh Huang, and Tom Meng-Yen Lin. 2021. "A Hybrid MCDM Model for Evaluating Open Banking Business Partners" Mathematics 9, no. 6: 587. https://doi.org/10.3390/math9060587

APA StyleDaiy, A. K., Shen, K.-Y., Huang, J.-Y., & Lin, T. M.-Y. (2021). A Hybrid MCDM Model for Evaluating Open Banking Business Partners. Mathematics, 9(6), 587. https://doi.org/10.3390/math9060587