1. Introduction

COVID-19 will most likely accelerate digitalization leading to the absence of medium-term exercises from the division of financial services. Medium-sized banks may be affected the most because procuring fetched efficiencies with huge IT speculations will be difficult. These efficiencies are significant. Thus, managing an account division will favor profound rebuilding, winding up of banks, and solidifying the remaining ones. In the post-COVID-19 world, political deterrence to cross-border mergers will rise as states will become more protective of their national interest, and managing an account champion could be a major arrangement [

1,

2,

3].

Customers have increasingly shifted to online shopping to purchase items they need. Online shoppers have recently increased at present, especially relative to essential supplies and basic family needs. Retailers have recently experienced a surge in online shopping for basic supplies as shoppers stock up on food products and other essentials [

4,

5]. The fast portable payment process has astonished the foremost cutting-edge administration experts [

6,

7].

We are currently living in uncommon times. Amid the COVID-19 emergency, computerized installments have maintained economic health, making a difference by allowing individuals to avoid contact with the infection. Installment suppliers have experienced the greatest impacts of the pandemic, including widespread increment in non-performing advances, a fall in incomes, and noteworthy requests from client benefit groups [

8,

9]. In a brief period, this trend will force installment suppliers to change by prioritizing noteworthy adaptability and modern short-term objectives.

The long-term impacts of the pandemic on worldwide installments are likely to be highly significant [

10,

11]. MFS-related administrations have developed an executioner application that can produce colossal sums of income and thus boost the entire portable trade industry [

12,

13]. Numerous ventures, such as money-related education, MFS administrators, start-ups, and innovation suppliers, have conducted various standardized and commercial endeavors to achieve this opportunity [

1,

14,

15]. Portable exchanges are not restricted by time and effort. High productivity saves exchange time for clients [

12,

13,

16]. The characteristic of a portable terminal is settled, allowing portable e-commerce to supply personalized portable exchange administrations. Versatile e-commerce can provide a wireless interface between clients and businesses [

17,

18]. The objective of this paper is to propose a multi-perspective system to help customers evaluate the MFS frameworks.

The World Health Organization (WHO) has prescribed using contactless installments wherever possible to help control the infection. This approach undermines the utility of cash by forcing numerous retailers to close their entryways and offer products only through online orders. Unused technology assessment and premonition are complex fundamental exercises within the context of complex advancements [

19,

20,

21,

22]. Many parameters must be considered to form a picture of the showcase. By definition, a multi-criterion examination may be a remarkable procedure for managing this complex issue [

23,

24,

25,

26,

27]. The shift from cash to electronic installments will be accelerated by shoppers’ behavior due to the COVID-19 pandemic. This situation considers employing the portable installment industry as a case study.

This study uses the Taiwan mobile financial services (MFS) industry as the case study. The relationship between the different factors used to make a casual map that identifies the casual group and effect group is discussed. MFS industry operators are provided with certain strategic recommendations based on the research results. The remainder of this paper is as follows.

Section 2 reviews prior research on the mobile payment industry.

Section 3 presents the methodology, namely, fuzzy Decision-making Trial and Evaluation Laboratory (DEMATEL), and introduces the research design, research framework, research procedure, sample selection, and empirical results.

Section 4 discusses certain empirical research. Finally,

Section 5, provides the concluding remarks.

2. Mobile Financial Services

COVID-19 gives clients a justified reason to be watchful of open installment terminals. Computerized wallets, such as Apple Pay and Google Pay, allow installments without physically using a card to a terminal. Social distancing and other pandemic mitigation measures are likely to boost the use of advanced management of account administrations. With lockdowns, MFS suppliers have experienced a significant increment in requests for advanced exchanges [

28,

29,

30,

31]. This situation will drive numerous conventional installments suppliers to fast-track their advanced advancement endeavors. In MFS, portable clients use their phones to perform money-related exchanges; thus, MFS may be a promising and energizing space that has developed rapidly [

32,

33,

34]. In contrast, the COVID-19 pandemic may have covered businesses and has proved a boon for most computerized administrations, such as extreme work applications, e-learning apparatuses, and e-commerce arrangements. In any case, one computerized innovation that is not performing as well is portable installments. Portable installments could be a modern installment strategy that employs a versatile gadget through a remote association to conduct an installment [

35,

36,

37,

38,

39].

With the rapid development of artificial intelligence, related technologies have become a solid support for our society, through the performance of information processing algorithms and improvement of technologies and operations. The advances in certain subfields of artificial intelligence have provided additional expertise to intelligent agents through merging knowledge, reasoning, and planning. These combined skills and knowledge enable them to develop action plans and adapt to conditions. Automation is the key process for replicating human actions, which includes automatically improving the MFS and performance of the software functions.

MFS is a software agent that provides financial services and solutions to individuals anywhere and anytime. The derived concept of MFS includes the intelligent agent. Thus, natural language processing and machine learning are applied in artificial intelligence assistants. Customers input contextual information, voices, and images as the specific conditions to raise requests; this process enables the MFS to answer in natural language, providing recommendations and performing actions. Artificial intelligence assistants are designed as personalized applications that gather the preferences and fulfill the responsibilities specified by customers via online resources.

The interaction between humans and MFS commonly takes place through two methods: text and voice. Texting or online chat is a means of communication via the Internet; the text messages are transmitted instantly from the sender (the user) to the receiver (the MFS systems). Alternatively, voice is another direct way to interact with MFS, including speech recognition and voice recognition of human voices. Through speech recognition, MFS can capture spoken words and sentences and convert them into a digital format that can be read by machines. The quality of speech recognition is determined by two factors: accuracy and speed. Accuracy represents the error rate, which is used to identify the inaccuracy of transcription when spoken words are converted into digital data, though the reason for the errors may not be identified. Speed, that is, the dimension of real time, reflects how well MFS can keep up with human speakers. Although speech recognition and voice recognition focus on the human voice, voice recognition works by distinguishing and analyzing the differences between individuals, such as their anatomy, speaking accent, and pitch. The intelligent personal assistant can identify and verify speakers based on their speech patterns.

Expansive shippers and money-related education will have to make noteworthy speculations to control fraud prevention and discovery. MFS is characterized by the employment of a portable gadget [

40,

41]. For instance, a portable phone is used to perform an installment exchange in which cash is exchanged from one party (payer) to another (collector) through a mediator, such as a monetary institution, or directly, without a middle person [

42]. Pousttchi and Zenker [

12] clarified that mobile payment installment is installment exchange preparation in which a payer uses versatile communication procedures along with portable gadgets to start, authorize, and realize the installment [

43,

44,

45]. Ondrus and Pigneur [

14] characterized mobile payments as remote exchanges of money-related esteem from one party to another, employing a portable gadget that can physically shift from a versatile phone to any remote empowered gadgets (e.g., PDA and tablet) that can sagely handle a monetary exchange over a remote arrangement. Versatile payments are commonly anticipated to extend comfort to shoppers by reducing the need for coins and notes in small exchanges and expanding the accessibility of conceivable installment outcomes [

46,

47,

48].

A mobile payment system has three fundamental actors: clients, dealers, and banks [

49]. Clients obtained by administrations are accessible on the web. A vendor gives items or administration to the client on request. The item may be an online object that can be exchanged in the same way received by the client. From the merchants’ point of view, the portable installment framework is expected to decrease moderate exchange costs, increment item or beneficial deals, and increment-obtaining proficiency and buyer fulfillment [

50,

51,

52,

53]. Compared with the telecommunication (telecom) administrator, the bank is, additionally, a central component of the versatile installment industry chain [

54]. Its budgetary capabilities and experience in credit items are basic to the full versatile installment framework [

55,

56]. The major assignment of the telecom administrator is to establish a portable installment stage and provide secure communication channels for portable installment [

57,

58]. They play a crucial role in versatile installment benefit improvement preparation, which serves as bridge-interfacing clients, money-related teaching, and benefit suppliers [

42,

59,

60].

2.1. Assessment Criteria for Mobile Financial Services

Post-COVID-19 MFS suppliers unquestionably play a significant part in improving the endeavors to relieve antagonistic financial effects on struggling families. Moreover, the government must emphasize the appropriation for computerized installment administrations for social security installments and government worker compensation. Clients are key to versatile installment strategies’ acknowledgment [

61,

62]. In this paper, we rely on portable installment studies’ acknowledgment criteria to assess mobile payment methods in Taiwan from the perspective of clients’ prerequisites. Most papers on portable installments cover specialized issues [

14,

63,

64]. These investigation reports focused on installment strategies [

65,

66,

67] and innovation measures [

68,

69,

70,

71].

These reports also explored the components that may impact shoppers in tolerating portable installments [

72,

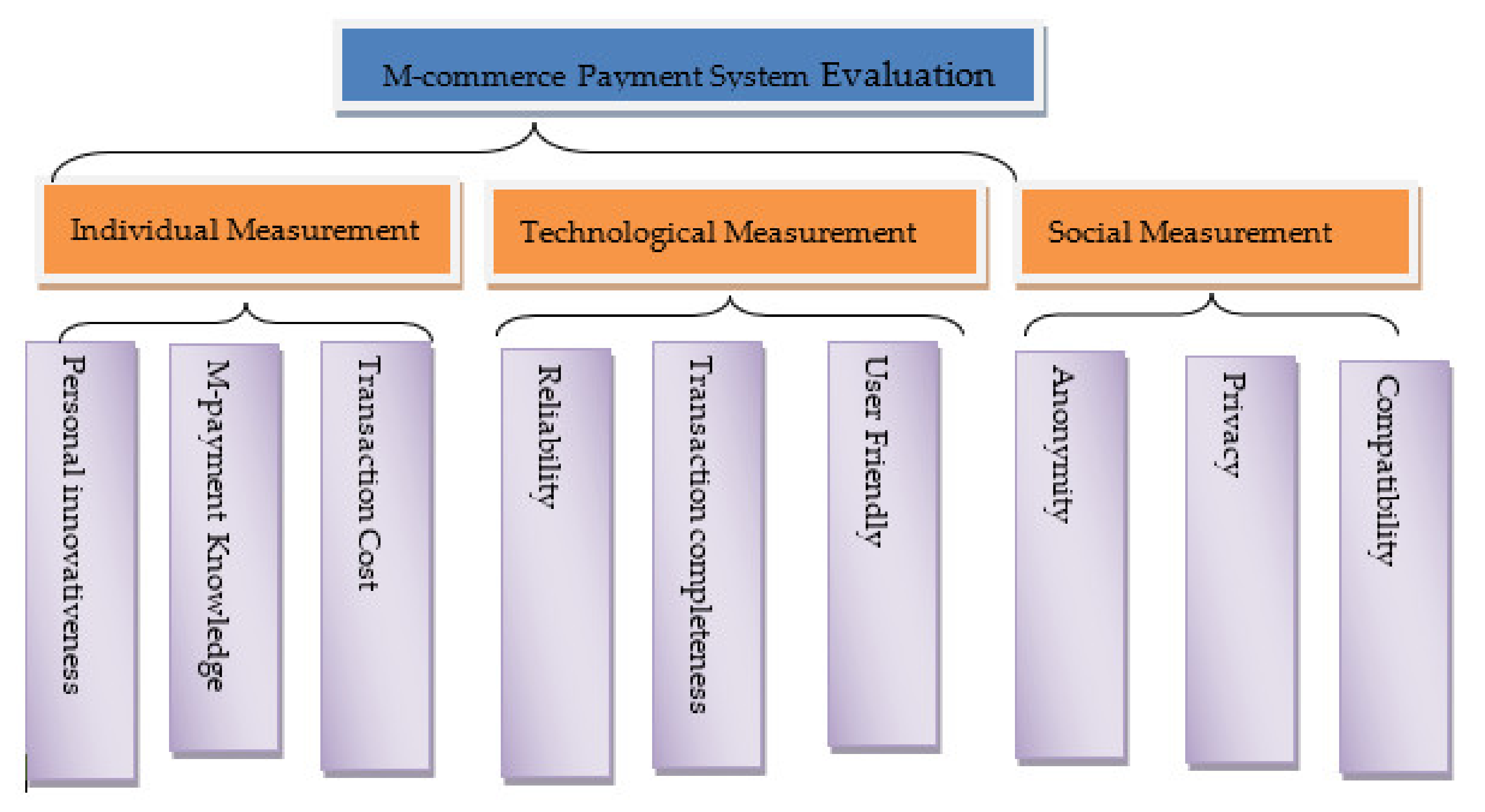

73]. Recently, while performing this investigation, a writing audit was conducted to supply a comprehensive definition of portable installments. We examined the components that seem to impact customers’ tolerance to portable installments. A portable installment framework can be surveyed along with three measurements: individual, innovative, and social measurements.

2.1.1. Individual Measurement

Individuals’ needs are divided into three categories: the personal innovativeness aspect, the degree of m-payment knowledge, and the transaction cost issue [

74,

75].

2.1.2. Personal Innovativeness

Personal innovativeness is characterized by identity development [

76,

77]. This identity development is used to determine shoppers’ imaginative inclinations to embrace broad innovative advancements. Rogers and Shoemaker [

34] characterized innovativeness as a perceptible marvel relative to the time of appropriation. Agarwal and Prasad [

78] delineated personal innovativeness as a characteristic that leads to creative behavior within a micro-computer, that is, “the eagerness of an individual to attempt any unused information technology.” The attempt to use and recognize advanced technology is closely related to the dispersal of advancements [

15]. Thus, individual innovativeness could be a vital calculation in modern innovation selection behavior [

79,

80,

81,

82].

2.1.3. m-Payment Knowledge

The concept of “profession” is related to m-payment. Numerous earlier investigations considered this concept an unequivocal determinant of users’ common competence and cognitive capacity [

65]. Thus, whether any relationship exists between the information and purpose of using m-payment was examined [

83,

84]. We applied “absorptive capacity” to explain this phenomenon. Absorptive capacity alludes to a customer’s capacity to assess and use external information [

54] and measures a customer’s capacity to retain, absorb, and abuse the development [

85,

86,

87,

88].

2.1.4. Transaction Cost

This cost refers to the fetched amount paid by the buyer and included within the exchange [

47,

55]. The viewed costs of creating collaborative connections exceed those related to creating and actualizing legally binding connections. These fetched components influence the accomplice assessment in social trades because they are transient. The fetched concept is derived from the cost–benefit design based on the behavioral choice hypothesis [

84]. The cost–benefit design outlines that individuals’ behavior is impacted by their discernment. The ease of use and convenience are the benefits, whereas the viewed fetched and chances are the costs. In selecting a portable installment framework for small installments, the taken toll incorporates the exchange cost, enlistment charge, or taken toll for an unused gadget when it is required to use the framework and the wellbeing risks.

2.1.5. Technological Measurement

When planning a mobile payment framework, various aspects must be considered: client attraction toward the exchange framework, the degree of unwavering quality compared with other installment frameworks, and the exchange’s completeness of adjustment to the framework.

2.1.6. User-Friendliness

This inquiry about receiving innovation acknowledgments shows that the technology acceptance model (TAM) clarifies clients’ neighborly development. TAM was proposed by Davis in 1989 [

89] and has made a difference in understanding the interceding part of viewed convenience, ease of use, and the connections between framework characteristics and the likelihood of framework use. TAM builds on five concepts: perceived ease of use (PEOU), perceived usefulness (PU), attitude toward use (AT), behavioral intention (BI), and actual use (AU). Davis (1989) proposed that TAM clarifies and anticipates client acknowledgment of data frameworks and innovation. He [

89] defined PU as “the degree to which an individual accepts that employing a specific framework would upgrade his or her work performance” and PEOU as “the degree to which a person accepts that employing a specific framework would be free of effort.” Within TAM, PU could be a major figure, whereas PEOU could be an auxiliary calculation in deciding framework use. Here, Davis [

89] held that PEOU incorporates a positive, circuitous effect on framework use through PU. Other key components inside the illustration consolidate AT, BI, and AU. A user’s AT is determined by PU and PEOU in information innovation use. As TAM is an intention-based view, BI is included in the illustration and theorized as a key calculation between AT and AU. Numerous experiments have extended TAM and may prove crucial to investigate consumers’ deliberate behavior toward innovation or framework use, such as the World Wide Web (WWW) [

46] and Look Motors on the Internet [

46]. Considering the given definition, we can conclude client attraction comprises time and utilities, which are central characteristics of m-payment [

32].

2.1.7. Reliability

Unwavering quality constitutes fitting work that is appropriately planned and soundly used [

47,

72]. Thus, we define unwavering quality as performing appropriate and legitimate installment. To sustain unwavering quality, we use three requested solid capacities: individual recognizable proof-number search, account secret word, and security card.

2.1.8. Transaction Completeness

Payments must be completed to avoid exchange irregularities. A synchronous, moment-clearing, and settlement instrument must be introduced in e-payment frameworks to maintain a strategic distance from exchange inadequacy [

90,

91].

2.1.9. Social Measurement

The mobile installment framework should address the social measurement to fulfill individual desires and specialized measurements of the portable installment framework.

2.1.10. Privacy

Consumers’ concerns about protection and the security of portable installments are commonly related to verification and secrecy issues and auxiliary use and unauthorized access to installments and client information [

92,

93]. The degree of protection and security includes users’ security when storing or withdrawing cash; information, security of application programs, and databases [

94]; security during exchanges and installments; security of the Web and framework; and security upkeep and administration [

92].

2.1.11. Anonymity

Shopper anonymity implies that the vendor and visited location register (VLR) do not require the consumers’ real identity [

95]. In a remote arrangement, a buyer must provide his/her real identity to the benefit arrangement for confirmation. This information must be secured to obstruct extortion [

43].

2.1.12. Compatibility

Compatibility is the degree to which an improvement is seen as consistent with existing values, past experiences, and needs of potential adopters. Compatibility is defined as the degree to which an improvement is seen as unfaltering with the existing values, needs, and past experiences of potential adopters [

34]. Beliefs that contradict the values and standards of a social framework will not be accepted promptly unlike an advancement that conforms to these values and standards. The selection of a non-conforming advancement frequently requires the earlier selection of a new esteem framework, which could be handled moderately [

34,

96].

The research purpose requires that the respondents are either using, have used, or have heard of MFS.

Table 1 below provides the operational definitions of each criterion for effective measurement.

3. Research Method

In real life, humans’ subjective cognition of abstract things is often vague and unquantifiable. It often distorts the valid cognition of respondents through using quantitative scales. Multi-criteria decision-making method (MCDM) includes several techniques that allow rating various criteria and then ranking them based on the opinions of industry experts. The MCDM method can significantly reduce the cost and time to create an appropriate framework for problem-solving. To solve the managerial issue, the study applies the DEMATEL. It is a suitable method that helps in gathering group knowledge to form a structural model and in visualizing the casual relationship between sub-systems through a casual diagram. The judgment of decision-makers is often given as crisp values. However, crisp values cannot adequately reflect vagueness in the real world. Thus, this study combined fuzzy logic and DEMATEL to address this issue.

3.1. Research Objective

The aforementioned theoretical models contributed to our understanding of user acceptance factors. These studies examine a set of potentially relevant factors that drive consumer acceptance of MFS. Moreover, a research gap is evident regarding multi-criteria analysis of mobile payment acceptance and the development of an understanding of the cause–effect relationship of complex social science problems in fuzzy environments. This research proposes a DEMATEL and fuzzy theory as the main analytical tool. Below, we discuss the research method, namely, fuzzy DEMATEL, in detail.

3.2. Expert Interview

Twenty-one experts were invited to evaluate the criteria. We anticipated the interview would last two hours. The first part presented the previous results (i.e., the first MCDM model). The objective was to recall knowledge and open a discussion. This presentation is based on a report distributed to the experts before the interview. We wanted the experts to have a common understanding of the results before evaluating the mobile payment. This analysis was conducted asynchronously with the experts. We collected empirical data from several key experts in different industries. The industry representation was optimal as we covered all relevant industry sectors (financial, telecom, retail, and technology). A great majority of the experts participated in the previous interview campaign. Therefore, they were familiar with our approach.

3.3. Fuzzy Decision-Making Trial and Evaluation Laboratory Method

The contribution of this theory is used as a mathematical structure to express qualitative and quantitative data and provide a realistic judgment [

97,

98,

99,

100]. Let the decision-maker define problems and compare the data [

26,

101]. Fuzzy theory results in things that are not only “yes” and “no” but leads to a concept of degree between “yes” and “no” [

88,

102,

103,

104]. The linguistic variable of fuzzy theory is used as the experts’ scoring scale to solve the inconsistency of subjective cognition and make the question degree closer to reality [

105,

106,

107,

108]. Then, designing fuzzy numbers (FNs) represented by different linguistic variables, let the respondents select the most appropriate meaning [

109,

110]. Next, through the defuzzification process of transforming FNs to a numerical value and decision-making, we combine the traditional MCDM method and fuzzy theory to solve the problem of nurses’ competency appropriately [

111,

112,

113]. We obtained three measurements and nine reasonable criteria to assess the portable installment framework [

97]. The DEMATEL examination steps are based on the inquiry from researchers, including Chou et al. [

97] and Chiang and Birtch [

113]. As a result, the examination preparation is divided into six steps as follows:

- (1)

Defining the characteristics of the quality factor, and establish an evaluation scale.

The assessment scale for causal relations and a pair-wise comparison of the quality variables are built on [

68,

72]. We alluded to the scale planned by Yue et al. [

108] and Büyüközkan and Göçer [

111] and accepted 0, 1, 2, 3, and 4 as five levels of estimation.

- (2)

Obtaining interdependent data for all factors using the expert opinion method.

These pair-wise comparisons between any two components are indicated by a given score of 0–4: “no influence” (0), “low influence” (1), “medium influence” (2), “high influence” (3), and “very high influence” (4) [

109,

110].

- (3)

Calculating the arithmetic mean matrix.

Assume that the number of factors and the value are from professionals who judge the factors based on 0, 1, 2, 3, and 4 five-level evaluation scale:

and

(

i = 1, 2, 3, …,

n;

j = 1, 2, 3, …,

n) represents the degree of influence of factor

to factor

. Then, sum up and average all

from

experts [

107,

111]. The arithmetic mean matrix is calculated using the formula provided below.

- (4)

Calculating the causal matrix.

The casual connection network and total-relation lattice outline the interrelated effect on each calculation as shown in Equation (1) below [

111]. The normalized direct-relation lattice can be obtained as

:

- (5)

Using the causal matrix.

Let

be the quality of the given

y calculation for direct/indirect network

, and

i,

j = 1, 2, …,

n [

98]. Summing up the columns including the direct/indirect matrix (

T), Equation (4) is provided below. It incorporates the coordinate and roundabout effect, which is the degree of the coordinate or the circuitous effect on other variables. When the normalized direct-relation

is obtained, the total-relation matrix

can be calculated. It ought to be guaranteed that the convergence of

. The total-relation lattice appears as Conditions (4) and (5) [

103,

104] as follows:

- (6)

Causal diagram.

The causal graph is delineated in a two-dimensional design, where the full

and contrast

are the level and vertical pivots, respectively. This realistic design can rearrange the complex causal relation into an effectively justifiable visual structure to help us easily understand the issues [

114,

115]. When

is positive and found over the

x hub, the quality calculation

m has a place to the sort of cause. However, if

is negative and found under the

x pivot, then the quality figure has a place to the sort of effect.

4. Results and Discussion

COVID-19 has affected numerous businesses regardless of size. Nevertheless, organizations confront specific challenges as an emergency that is set to be supplanted or expanded by another within the frame of a profound, extended retreat. Although the pandemic has spread globally, the offline-to-online switch has long been developed [

115,

116,

117,

118,

119,

120,

121]. This paper distinguishes and analyzes the basic victory variables of portable installment framework usage. Twenty-one specialists were invited to assess the criteria. This investigation incorporates three measurements and nine assessment criteria.

Figure 1 illustrates the progressive structure of this investigation about choice issues.

Step 1: Generating the arithmetic mean matrix.

This matrix is also called the initial average matrix that utilizes data from the collected questionnaire to calculate the arithmetic mean matrix. We obtained the arithmetic mean matrix by separately adding up all the interrelated factors for every aspect and then averaging their sum. To measure the relationships between the factors demonstrated by

, the experts were asked to make pair-wise comparison sets. Then, the arithmetic mean matrix for the first-tier measurements

can be obtained follows: Arithmetic mean matrix framework can be obtained for the first-level measurement as follows:

Step 2: Normalizing the causal fuzzy matrix.

The linear scale transformation is used to transform the criterion scale into comparable scales. The normalized direct-relation fuzzy matrix can be obtained as

. This research assumes at least one

i such that

. Equations (2) and (3) are used to calculate the average matrix

. We normalized the arithmetic mean matrix as follows:

Step 3: Establishing and analyzing the causal model.

After obtaining the normalized direct-relation

, the total-relation matrix

can be calculated to ensure the convergence of

. The causal matrix

is calculated as follows:

Step 4: Using the causal matrix.

We convey the causal chart by mapping a dataset of .

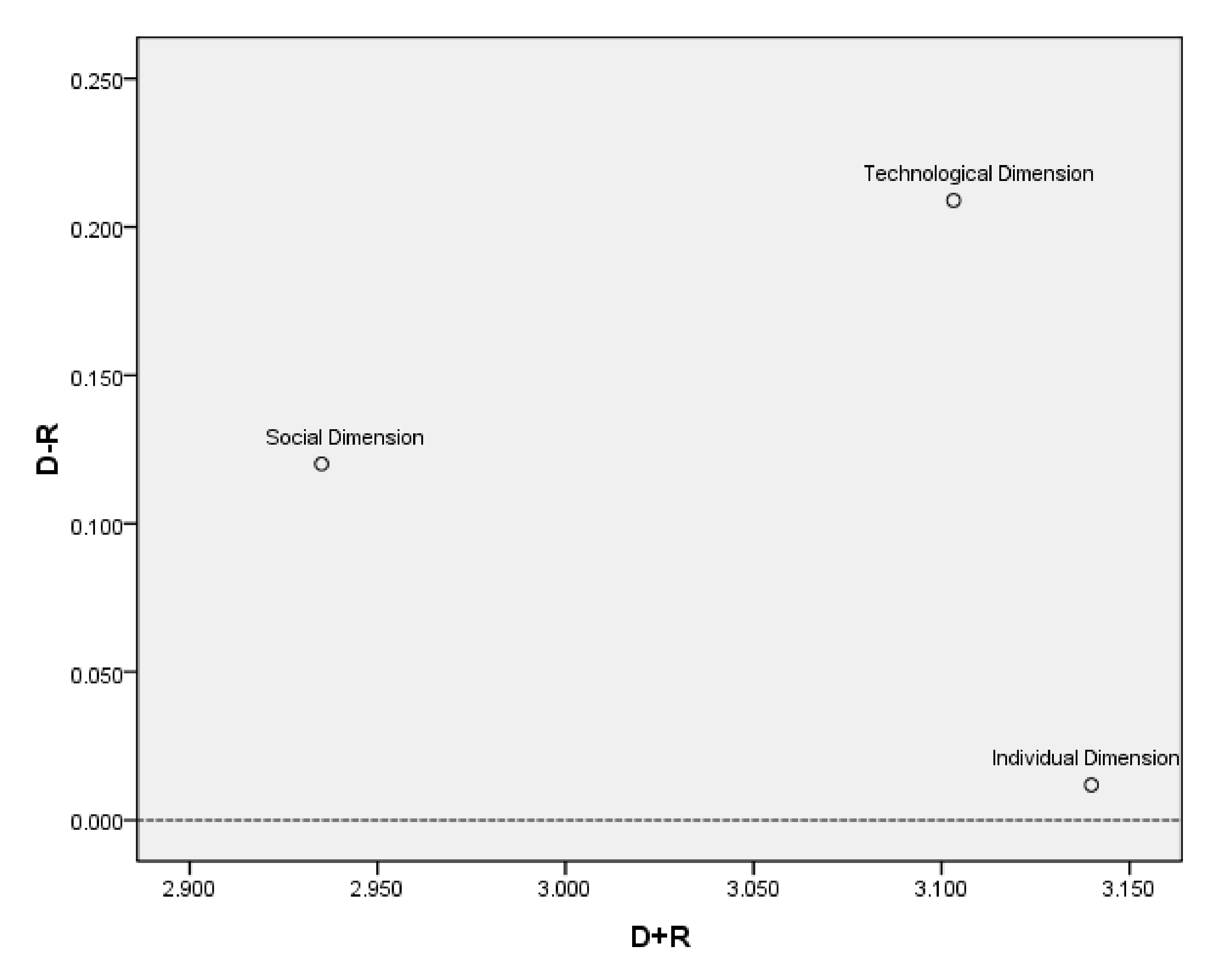

Table 2 above clarifies the coordinate and roundabout impacts of three first-level measurements.

Figure 2 shows the graph of the three first-level measurements.

Table 3 above shows that technological and social measurements are the net causes, whereas the individual measurement is the net collector.

Figure 2 illustrates that technological measurement may be the foremost basic measurement. Social and individual measurements are influenced by each other and the technological measurement. Using the value provided by the direct/indirect matrix main aspect, we performed the interrelation analysis of the main aspects, which was the interrelation impact on every aspect. The coordinate points for the above qualities of each three measurements were input into the graph to complete the DEMATEL causal diagram as shown in

Figure 2.

Figure 2 illustrates the graph of these three measurements. It is clear that technological measurement might be the most critical measurement. To facilitate MFS in the post-COVID-19 world successfully, technological measurement was the key aspect.

Figure 2 shows that the technological measurement may be the foremost basic measurement. The social and individual measurements are influenced by each other and by the technological measurement.

Table 4 and

Table 5 and

Figure 3 depict the cause–effect relationships between the three second-tier criteria of the individual measurement.

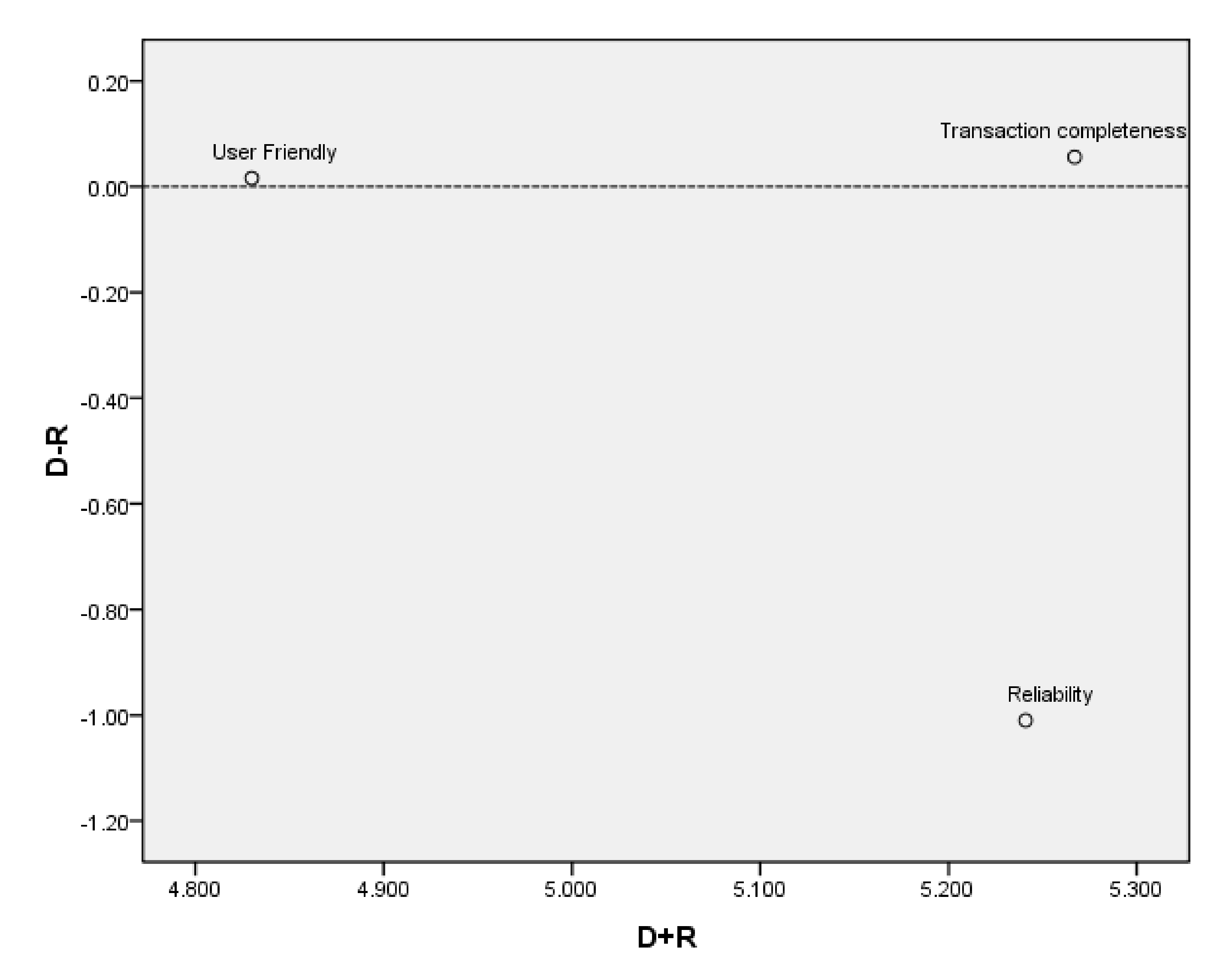

Table 6 and

Table 7 and

Figure 4 depict the cause–effect relationships between the three second-level criteria of technological measurement.

Table 8 and

Table 9 and

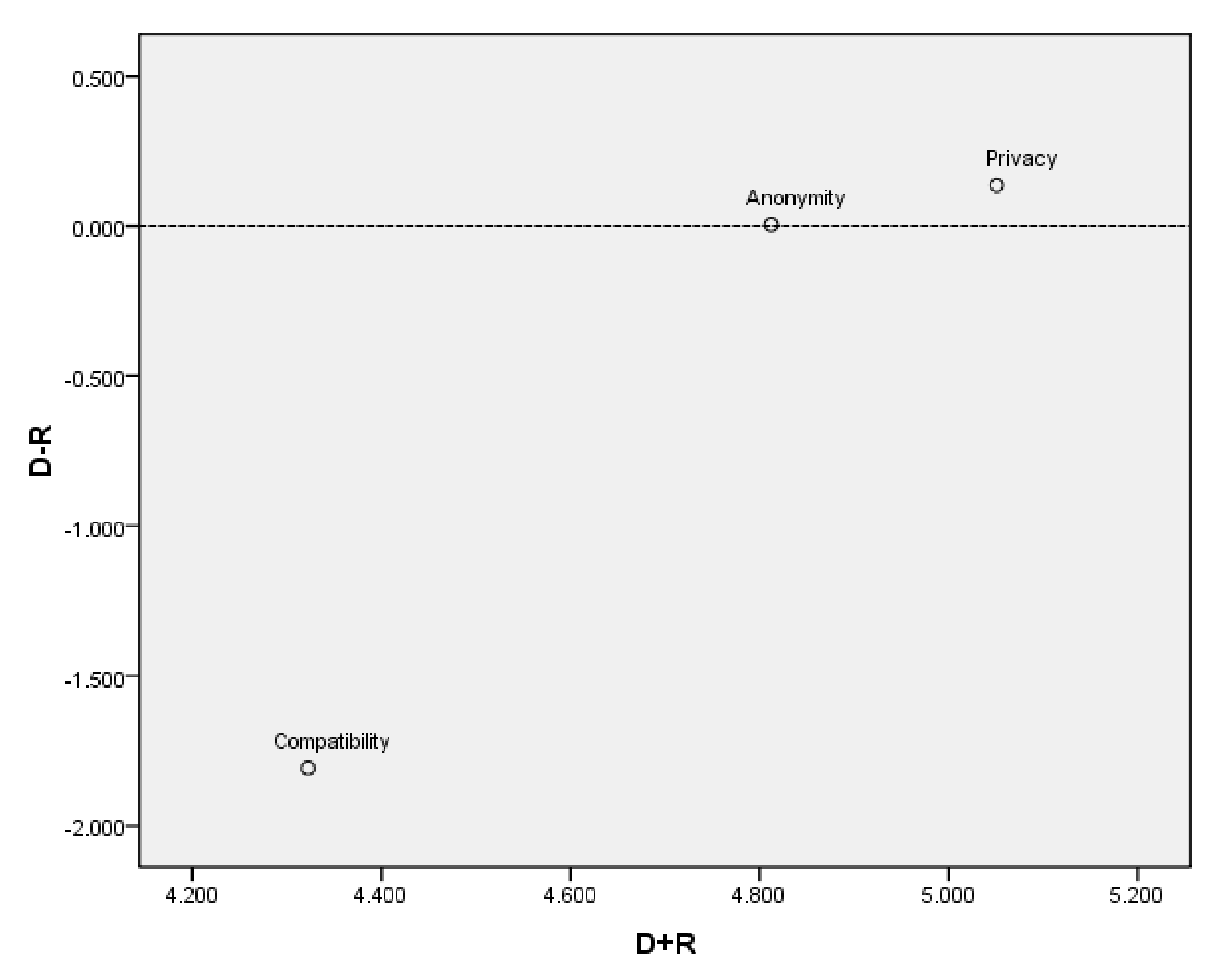

Figure 5 summarize the causal relationships between the three second-tier criteria of the social measurement.

Table 4 and

Table 5 show that individual innovativeness is the net cause, whereas m-payment knowledge and exchange fetched are the net recipients.

Figure 3 illustrates that personal innovativeness may be the foremost basic measurement. M-payment knowledge and transaction cost are influenced by each other and by individual innovativeness. The eagerness to enhance may be a work of identity and environmental perception. Thus, innovativeness is the degree to which a user is intrigued by attempting and tolerating unused things, modern ideas, and an inventive item or benefit.

Table 6 and

Table 7 show that transaction completeness and user-friendliness are the net causes, whereas reliability is the net recipient.

Figure 4 shows that transaction completeness may be the foremost basic measurement. Additionally, reliability is influenced by each other and by transaction completeness and user-friendliness.

Thus, portable installment benefit suppliers must provide legitimate capacities in agreement with consumer needs. As a result, clients can be obtained and time and effort can be saved in addition to increasing installment proficiency in improved client fulfillment and dependability.

Table 8 and

Table 9 show that anonymity and privacy are the net causes, whereas compatibility is the net recipient.

Figure 5 illustrates that privacy may be the foremost basic measurement. Compatibility is influenced by anonymity and privacy. Among these factors, the security of payments is one of the most extreme concerns for customers. Security of exchange is important for payments of a considerable sum. Portable installment makes it accessible to conduct exchange regardless of time and place. This aspect is the greatest advantage of this mode of installment, which is characterized by mobilization and individualization.

5. Conclusions and Remarks

When the WHO released an explanation on 9 March prescribing that individuals turn to computerized installments to fight the spread of COVID-19, the shift toward cashless social orders was expedited. Contactless advanced installments at the point of transaction, such as facial acknowledgment, quick response codes, and near-field communications (NFC), can lessen the spread of infection through cash trades. Advanced installments restrict in-person exchanges and guarantee buyers to purchase essentials from the comfort of their homes. Increased e-commerce activities are significantly making a difference to small businesses to maintain income streams in uncertain times. Versatile installments are making a difference to put jolt stores into consumers’ hands more quickly. A mobile payment framework is composed of numerous connection components.

MFS is composed of many interacting elements. This paper employed the fuzzy DEMATEL method to analyze the model and considered suggestions as to the key influencing factors in MFS evolution. The determinants of MFS were subtracted from the column total to obtain (degree of cause and effect). The higher the positive degree of cause and effect , the easier the item directly influences the other factors. The higher the negative degree of cause and effect, the easier the item is influenced by other factors. From the value, the following showed the important items that influenced other factors: personal innovativeness, transaction completeness, user-friendliness, anonymity, and privacy, whereas m-payment knowledge, transaction cost, reliability, and compatibility were the main items influenced by other factors.

MFS will develop rapidly because of the potential operational efficiencies, comfort, security assurance, and coordination available to the buyer irrespective of location. MFS benefits are discussed approximately as they infer to supplant ordinary cash in the physical world, implying installment within the virtual world. Moreover, electronic installment cannot be distorted, anticipating that the plan is inside and out, because electronic cash may be less difficult and more affordable to use than scheduled cash. The most important part of convenient installment affirmation is in the clients’ hands. In this article it appears that it is vital to plan mobile payments framework that responds to customers effectively. Thus, a profound understanding of customer appropriation inspiration is necessary to create and dispatch portable installment administrations effectively [

54].

The success of MFS can barely be anticipated considering a single measurement. Individual innovativeness is a creative personality of an individual relative to unused technology, characterized as the traveler’s receptivity to online travel shopping. Ching and Hayashi [

51] found that individual innovativeness predicts buyer appropriation of online shopping. Individual innovativeness is an individual characteristic that significantly influences users’ availability to embrace a present-day thing or creative changes and organizations. Therefore, high individual innovativeness positively impacts PEOU and perceived comfort. Client attraction is one of the selected components of the framework victory. The exchange completeness is an imperative versatile installment framework driver. The versatile installment framework must improve the framework and substance quality. System quality includes 24 h availability, online response time, page stacking speed, and visual presence. Substance quality incorporates contemporaneity, understandability, convenience, and exactness [

12,

13]. Shoppers are unpredictable and may not follow completed exchanges. An imaginative interface plan will encourage m-commerce selection. Predominant substance organization, less complex and compelling presentation, and interface arrangement will enable proper selection. A high degree of interface comfort can enable clients to reach their targets better and faster.

Transaction completeness is an important MFS driver. MFS should enhance the system and content quality. System quality includes 24 h availability, online response time, page loading speed, and visual appearance. Content quality includes contemporaneity, understandability, timeliness, and preciseness. Consumers want to be anonymous and prefer not to leave any traces of completed transactions. Innovative interface design will facilitate m-commerce adoption. The better the content organization and the simpler and more effective the presentation and interface design, the more likely the product will be well-received. A high degree of interface usability can be reached, enabling users to reach their goals better and faster.

Clients are concerned with the assurance and security of flexible systems. Their concerns are commonly related to affirmation and mystery issues and assistant utility, unauthorized installments, and client data [

121]. Security is essential for flexible installment and can be challenged amid unstable installment information management or transmission. Portable installment has specific security and security challenges due to their contrasting fundamental advances. The buy preparation should be error-free because it includes a budgetary exchange. Unwavering quality is explicitly necessary for installment innovation.

Similar to any experimental investigation, this study has limitations. First, the observational information was collected from only one country. Various countries have striking contrasts within the utility of versatile installments and administrations. They have significant differences in the use of mobile payments and services. Thus, the findings may vary across countries. Second, the methodology of this study, namely, the fuzzy DEMATEL, also presents limitations in terms of the small sample size. Hence, future research can be conducted to test the adoption factors presented in this study using different methods and larger sample sizes.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}