Blockchain Technology for Secure Accounting Management: Research Trends Analysis

,

,  ,

,  and

and

Abstract

1. Introduction

2. Literature Review

2.1. Blockchain Technology

2.2. Secure Accounting Management

2.3. Research Questions

- RQ1:

- What has been the evolution of scientific production in this field of knowledge between 2016 and 2020?

- RQ2:

- What were the main lines of research studied in the 2016–2020 period?

- RQ3:

- What are the emerging research directions on this topic?

3. Data and Methods

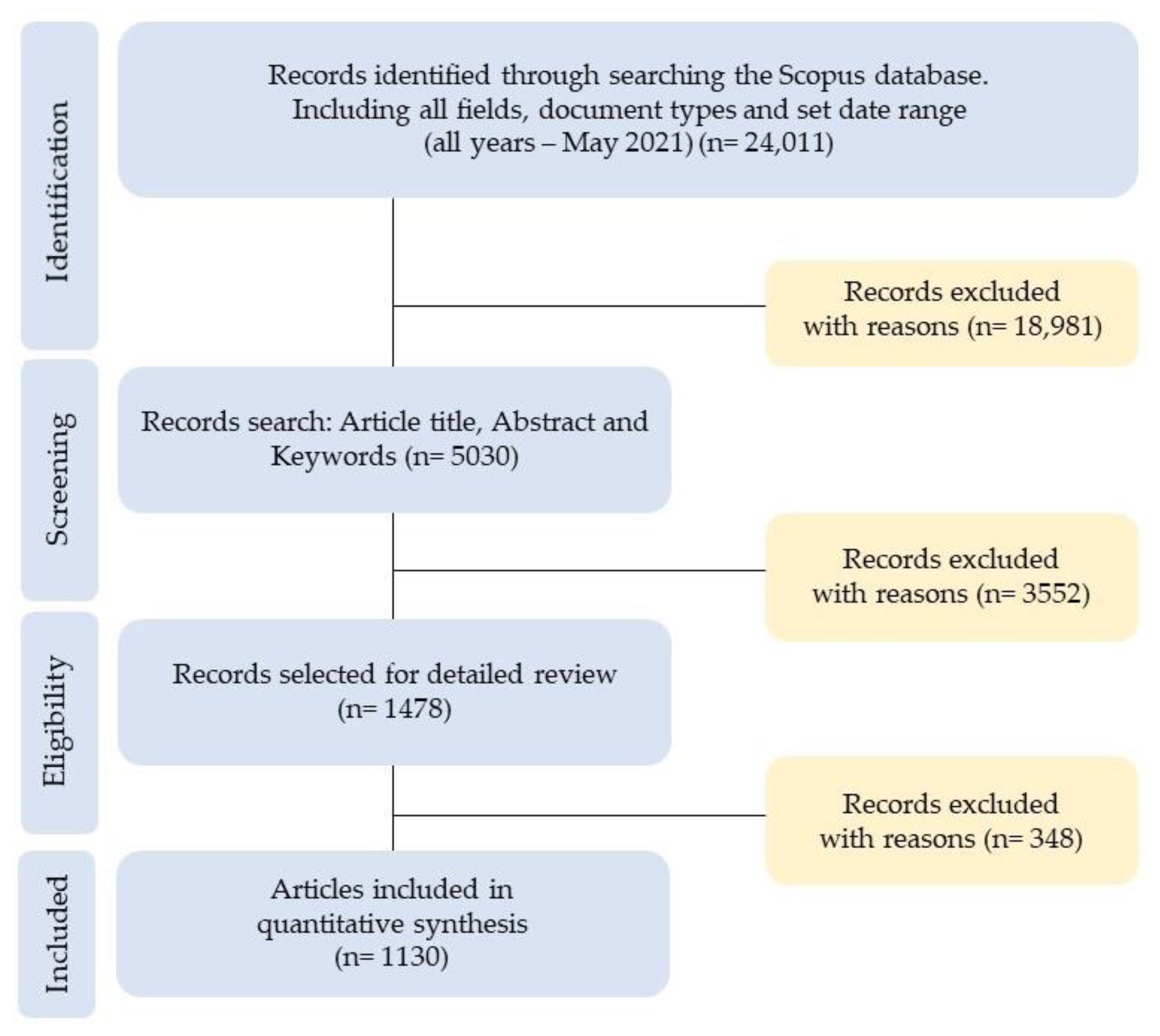

3.1. Data Collection

- Phase 1 (Identification): 24,011 records were detected, considering, for each of the search terms (BC, accounting, and management), obtained from the analysis of the records in Table 1, “all fields”, “all types of documents” and “ all data published in the data range (all years–May 2021)”.

- Phase 2 (Screening): The option “article title, abstract and keywords” was chosen in the field of each search term. In total, 18,981 records were excluded, and 5030 were included.

- Phase 3 (Eligibility): Only “articles” were selected as the type of document, to guarantee the quality of the peer-review process; and, furthermore, in order not to distort the sample, the search was also limited to the subject areas: computer science; business, management and accounting; economics, econometrics and finance; and mathematics. In total, 3552 records were excluded, and 1478 were included.

- Phase 4 (Included): The data referring to the period “every year–2020” were selected, that is, from the first article published on the research topic (2016) to the last full year (2020). In total, 348 records were excluded. Hence, the final sample included 1130 articles (open and non-open access).

3.2. Data Processing

3.3. Key-Terms Co-Occurrence Analysis

- Link: Co-occurrence connection between terms.

- Total link strength: Intensity of each link, denoted by a positive numerical value. For concurrent links, indicate the number of articles in which two terms appear together.

- Occurrence: Attribute that shows the number of articles that contain a keyword.

- Network map: Set of terms and links.

- Cluster: Set of terms included in a network map. Clusters do not need to comprehensively cover all the components of a network map.

- Weight: Attribute used to describe the term, denoted by numerical value.

- Weight of a term: Significance of the term in the field of research analyzed.

- Link weight: Number of links of a term with other terms.

- Link strength weight: Total strength of the links of a term with other terms.

- Score: Attribute that allows classifying by relevance the key terms of the titles and summaries of the analyzed articles.

- nax: Number of elements in the areas a in which the term x occurs.

- nbx: Number of elements in the areas b in which the term x occurs.

- c: This parameter determines the compensation between the following considerations: (i) the frequency of occurrence of term x in area a relative to the frequency of occurrence of term x in area b can be considered as an indication of the relevance of the term x for area a; and (ii) the absolute frequency of occurrence of term x in area a can also be considered as an indication of the relevance of term x.

3.4. Research Limitations

- Characteristics of bibliometric analysis, which is a method mainly focused on quantitative analysis, ignoring certain qualitative aspects.

- The methodology of this research could be extended with other quantitative or qualitative tools, such as Google Scholar, meta-analysis, or data mining (which uses methods of artificial intelligence (AI), machine learning (ML), statistics and data systems). databases), which would provide a different perspective on the results.

- The research sample only contains articles published in scientific journals, due to the reliability of the review system by parts; For future research, it would be interesting to include other types of documents, such as books or conference documents, to analyze the variation in the findings.

- Delve into different fields of this discipline, for more specific research on some of the topics related to these topics.

4. Results and Discussion

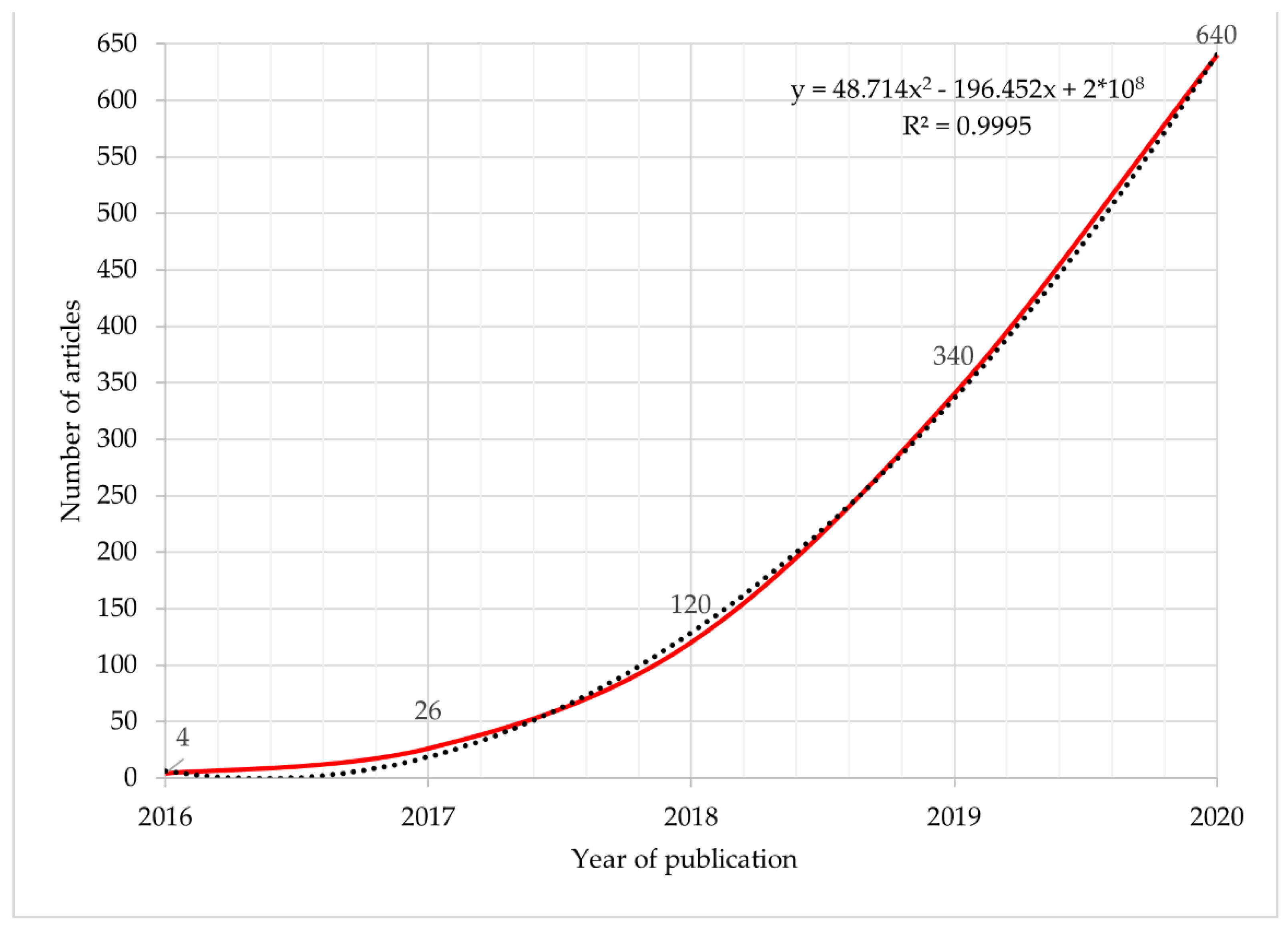

4.1. Temporal Evolution of Scientific Production (2016–2020)

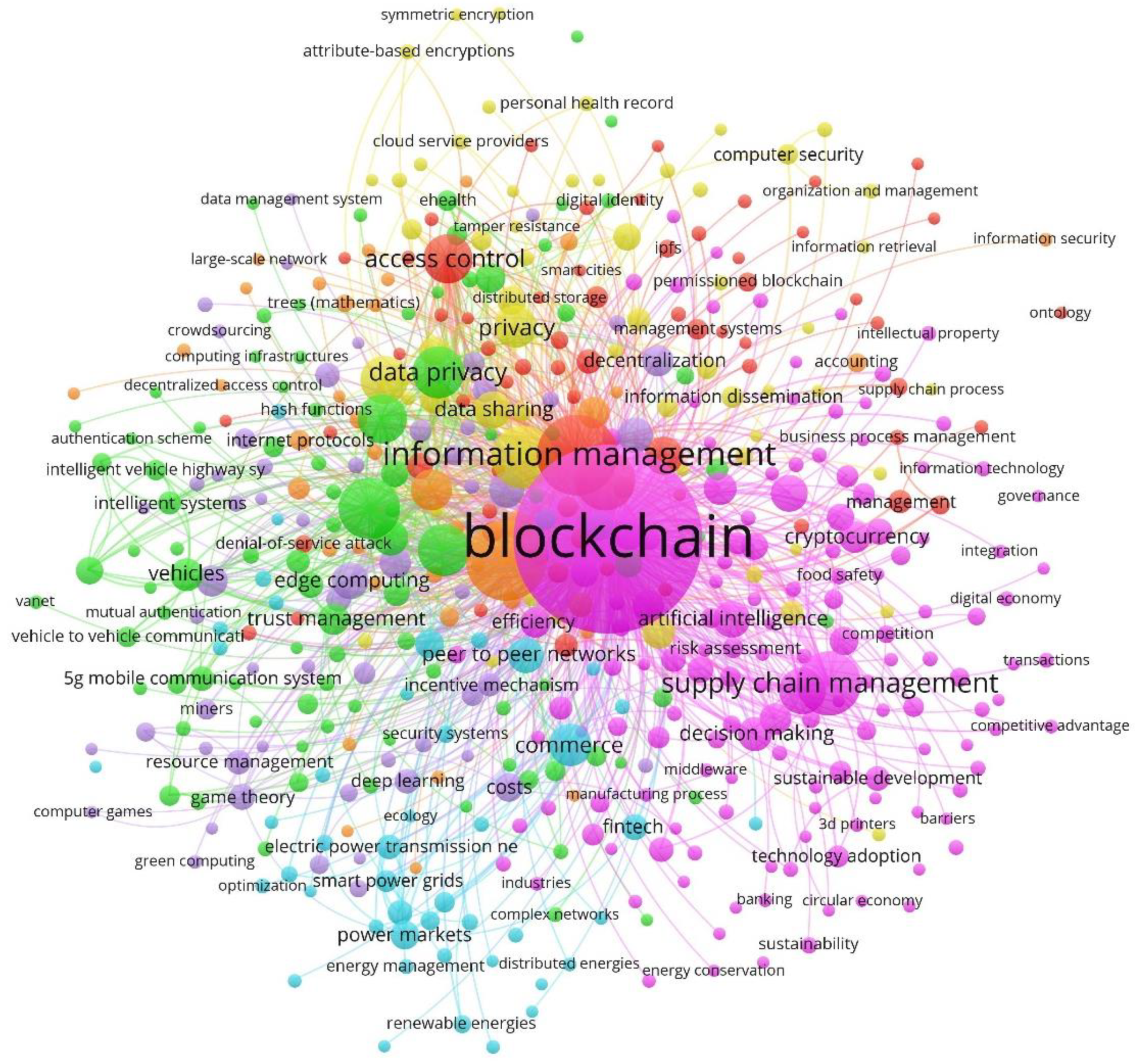

4.2. Keyword Analysis: Identification of Current Lines of Research

4.3. Future Directions of Research

4.3.1. Credit Value Evaluation Mechanism

4.3.2. Enabled Payment Gateway

4.3.3. Unstructured Supplementary Service Data Message

4.3.4. Consolidated Identity Management

4.3.5. Hyperledger Sawtooth

4.3.6. Hierarchical Lightweight High Throughput Blockchain

4.3.7. BGP Security Infrastructure

4.3.8. Global Supply Chain Risk Analysis

4.3.9. Extensible Permissioned Blockchain Platform

4.3.10. Centralized Authentication Authorization Auditing

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Kiviat, T.I. Beyond Bitcoin: Issues in Regulating Blockchain Transactions. Duke Law J. 2015, 65, 569–608. [Google Scholar]

- Alabi, K. Digital Blockchain Networks Appear to Be Following Metcalfe’s Law. Electron. Commer. Res. Appl. 2017, 24, 23–29. [Google Scholar] [CrossRef]

- ALSaqa, Z.H.; Hussein, A.I.; Mahmood, S.M. The Impact of Blockchain on Accounting Information Systems. J. Inf. Technol. Manag. 2019, 11, 62–80. [Google Scholar] [CrossRef]

- Rîndaşu, S.-M. Blockchain in Accounting: Trick or Treat? Qual. Access Success 2019, 20, 143–147. [Google Scholar]

- Wang, P.; Qiao, S. Emerging Applications of Blockchain Technology on a Virtual Platform for English Teaching and Learning. Wirel. Commun. Mob. Comput. 2020, 2020. [Google Scholar] [CrossRef]

- Alexander, A.; McGill, M.; Tarasova, A.; Ferreira, C.; Zurkiya, D. Scanning the Future of Medical Imaging. J. Am. Coll. Radiol. 2019, 16, 501–507. [Google Scholar] [CrossRef] [PubMed]

- Tso, R.; Liu, Z.-Y.; Hsiao, J.-H. Distributed E-Voting and E-Bidding Systems Based on Smart Contract. Electronics 2019, 8, 422. [Google Scholar] [CrossRef]

- Papagiannidis, S.; Bourlakis, M.; See-To, E. Social Media in Supply Chains and Logistics: Contemporary Trends and Themes. Int. J. Bus. Sci. Appl. Manag. 2019, 14, 17–34. [Google Scholar]

- Efimova, L.G. The Mechanism of Credit Transfers via the Blockchain. Int. Account. 2020, 23, 567–584. [Google Scholar] [CrossRef]

- Griggs, D.; Smith, M.S.; Rockström, J.; Öhman, M.C.; Gaffney, O.; Glaser, G.; Kanie, N.; Noble, I.; Steffen, W.; Shyamsundar, P. An Integrated Framework for Sustainable Development Goals. Ecol. Soc. 2014, 19. [Google Scholar] [CrossRef]

- Perdana, A.; Robb, A.; Balachandran, V.; Rohde, F. Distributed Ledger Technology: Its Evolutionary Path and the Road Ahead. Inf. Manag. 2021, 58, 103316. [Google Scholar] [CrossRef]

- Bonyuet, D. Overview and Impact of Blockchain on Auditing. Int. J. Digit. Account. Res. 2020, 20, 31–43. [Google Scholar] [CrossRef]

- Coyne, J.G.J.G.; McMickle, P.L.P.L. Can Blockchains Serve an Accounting Purpose? J. Emerg. Technol. Account. 2017, 14, 101–111. [Google Scholar] [CrossRef]

- Church, K.S.; Stein Smith, S.; Kinory, E. Accounting Implications of Blockchain-A Hyperledger Composer Use Case for Intangible Assets. J. Emerg. Technol. Account. 2020. [Google Scholar] [CrossRef]

- Christidis, K.; Devetsikiotis, M. Blockchains and Smart Contracts for the Internet of Things. IEEE Access 2016, 4, 2292–2303. [Google Scholar] [CrossRef]

- Lemieux, V.L. Trusting Records: Is Blockchain Technology the Answer? Rec. Manag. J. 2016, 26, 110–139. [Google Scholar] [CrossRef]

- Cai, Y.; Zhu, D. Fraud Detections for Online Businesses: A Perspective from Blockchain Technology. Financ. Innov. 2016, 2, 1–10. [Google Scholar] [CrossRef]

- Egelund-Müller, B.; Elsman, M.; Henglein, F.; Ross, O. Automated Execution of Financial Contracts on Blockchains. Bus. Inf. Syst. Eng. 2017, 59, 457–467. [Google Scholar] [CrossRef]

- Dai, J.; Vasarhelyi, M.A.M.A. Toward Blockchain-Based Accounting and Assurance. J. Inf. Syst. 2017, 31, 5–21. [Google Scholar] [CrossRef]

- Rozario, A.M.; Thomas, C. Reengineering the Audit with Blockchain and Smart Contracts. J. Emerg. Technol. Account. 2019, 16, 21–35. [Google Scholar] [CrossRef]

- Procházka, D. Accounting for Bitcoin and Other Cryptocurrencies under IFRS: A Comparison and Assessment of Competing Models. Int. J. Digit. Account. Res. 2018, 18, 161–188. [Google Scholar] [CrossRef]

- Wang, Y.; Kogan, A. Designing Confidentiality-Preserving Blockchain-Based Transaction Processing Systems. Int. J. Account. Inf. Syst. 2018, 30, 1–18. [Google Scholar] [CrossRef]

- Gießmann, S. Money, Credit, and Digital Payment 1971/2014: From the Credit Card to Apple Pay. Adm. Soc. 2018, 50, 1259–1279. [Google Scholar] [CrossRef]

- de Graaf, T.J. From Old to New: From Internet to Smart Contracts and from People to Smart Contracts. Comput. Law Secur. Rev. 2019, 35, 105322. [Google Scholar] [CrossRef]

- Ionescu, L. Big Data, Blockchain, and Artificial Intelligence in Cloud-Based Accounting Information Systems. Anal. Metaphys. 2019, 18, 44–49. [Google Scholar] [CrossRef]

- McAliney, P.J.P.J.; Ang, B. Blockchain: Business’ next New “It” Technology—a Comparison of Blockchain, Relational Databases, and Google Sheets. Int. J. Discl. Gov. 2019, 16, 163–173. [Google Scholar] [CrossRef]

- Smith, S.S.; Castonguay, J.J. Blockchain and Accounting Governance: Emerging Issues and Considerations for Accounting and Assurance Professionals. J. Emerg. Technol. Account. 2020, 17, 119–131. [Google Scholar] [CrossRef]

- Mosteanu, N.R.; Faccia, A. Digital Systems and New Challenges of Financial Management – Fintech, XBRL, Blockchain and Cryptocurrencies. Qual. Access Success 2020, 21, 159–166. [Google Scholar]

- Demirkan, S.; Demirkan, I.; McKee, A. Blockchain Technology in the Future of Business Cyber Security and Accounting. J. Manag. Anal. 2020, 7, 189–208. [Google Scholar] [CrossRef]

- Tapscott, D.; Kirkland, R. How Blockchains Could Change the World. McKinsey Q. 2016, 2016, 110–113. [Google Scholar]

- Xu, J.J. Are Blockchains Immune to All Malicious Attacks? Financ. Innov. 2016, 2, 25. [Google Scholar] [CrossRef]

- Abou Jaoude, J.; George Saade, R. Blockchain Applications - Usage in Different Domains. IEEE Access 2019, 7, 45360–45381. [Google Scholar] [CrossRef]

- Yuan, Y.; Wang, F.Y. Blockchain: The State of the Art and Future Trends. Zidonghua Xuebao/Acta Autom. Sin. 2016, 42, 481–494. [Google Scholar] [CrossRef]

- He, W.; Zhang, Z.J.; Li, W. Information Technology Solutions, Challenges, and Suggestions for Tackling the COVID-19 Pandemic. Int. J. Inf. Manag. 2021, 57, 102287. [Google Scholar] [CrossRef] [PubMed]

- Minakova, I.; Nosachevsky, K. Management Control in the Big Companies: New Approaches. Econ. Ann. XXI 2019, 180, 130–137. [Google Scholar] [CrossRef]

- Nakamoto, S. Bitcoin: A Peer-to-Peer Electronic Cash System. 2019, pp. 1–11. Available online: www.bitcoin.org (accessed on 20 June 2021). [CrossRef]

- Haber, S.; Stornetta, W.S. How to Time-Stamp a Digital Document. In Advances in Cryptology-CRYPT0’ 90; Springer: Berlin/Heidelberg, Germany, 1991; Volume 537 LNCS, pp. 437–455. [Google Scholar]

- Huerta, E.; Jensen, S. An Accounting Information Systems Perspective on Data Analytics and Big Data. J. Inf. Syst. 2017, 31, 101–114. [Google Scholar] [CrossRef]

- Dunk, A.S. Product Life Cycle Cost Analysis: The Impact of Customer Profiling, Competitive Advantage, and Quality of IS Information. Manag. Account. Res. 2004, 15, 401–414. [Google Scholar] [CrossRef]

- Hayes, A. The Socio-Technological Lives of Bitcoin. Theory Cult. Soc. 2019, 36, 49–72. [Google Scholar] [CrossRef]

- O’Connor, N.G.; Martinsons, M.G. Management of Information Systems: Insights from Accounting Research. Inf. Manag. 2006, 43, 1014–1024. [Google Scholar] [CrossRef]

- Tauscher, L.; Greenberg, S. How People Revisit Web Pages: Empirical Findings and Implications for the Design of History Systems. Int. J. Hum. Comput. Stud. 1997, 47, 97–137. [Google Scholar] [CrossRef]

- Shi, L.; Li, X.; Gao, Z.; Duan, P.; Liu, N.; Chen, H. Worm Computing: A Blockchain-Based Resource Sharing and Cybersecurity Framework. J. Netw. Comput. Appl. 2021, 185, 103081. [Google Scholar] [CrossRef]

- Thomson, G. BYOD: Enabling the Chaos. Netw. Secur. 2012, 2012, 5–8. [Google Scholar] [CrossRef]

- Zahadat, N.; Blessner, P.; Blackburn, T.; Olson, B.A. BYOD Security Engineering: A Framework and Its Analysis. Comput. Secur. 2015, 55, 81–99. [Google Scholar] [CrossRef]

- Ebrahim, S.H.; Ahmed, Q.A.; Gozzer, E.; Schlagenhauf, P.; Memish, Z.A. Covid-19 and Community Mitigation Strategies in a Pandemic. BMJ 2020, 368, m1066. [Google Scholar] [CrossRef] [PubMed]

- Brincat, A.A.; Lombardo, A.; Morabito, G.; Quattropani, S. On the Use of Blockchain Technologies in WiFi Networks. Comput. Netw. 2019, 162, 106855. [Google Scholar] [CrossRef]

- Hu, D.; Li, Y.; Pan, L.; Li, M.; Zheng, S. A Blockchain-Based Trading System for Big Data. Comput. Netw. 2021, 191, 107994. [Google Scholar] [CrossRef]

- Chen, Y.; Chen, S.; Liang, J.; Feagan, L.W.; Han, W.; Huang, S.; Wang, X.S. Decentralized Data Access Control over Consortium Blockchains. Inf. Syst. 2020, 94, 101590. [Google Scholar] [CrossRef]

- O’Leary, D.E. Some Issues in Blockchain for Accounting and the Supply Chain, with an Application of Distributed Databases to Virtual Organizations. Intell. Syst. Account. Financ. Manag. 2019, 26, 137–149. [Google Scholar] [CrossRef]

- Calderón, J.; Stratopoulos, T.C. What Accountants Need to Know about Blockchain*. Account. Perspect. 2020, 19, 303–323. [Google Scholar] [CrossRef]

- Musante, S. Learning How to Ask Research Questions. BioScience 2010, 60, 266. [Google Scholar] [CrossRef][Green Version]

- Abramo, G. Revisiting the Scientometric Conceptualization of Impact and Its Measurement. J. Informetr. 2018, 12, 590–597. [Google Scholar] [CrossRef]

- Abad-Segura, E.; González-Zamar, M.D.; López-Meneses, E.; Vázquez-Cano, E. Financial Technology: Review of Trends, Approaches and Management. Mathematics 2020, 8, 951. [Google Scholar] [CrossRef]

- Abad-Segura, E.; González-Zamar, M.-D.D. Research Analysis on Emerging Technologies in Corporate Accounting. Mathematics 2020, 8, 1589. [Google Scholar] [CrossRef]

- Abad-Segura, E.; González-Zamar, M.D. Global Research Trends in Financial Transactions. Mathematics 2020, 8, 614. [Google Scholar] [CrossRef]

- Mongeon, P.; Paul-Hus, A. The Journal Coverage of Web of Science and Scopus: A Comparative Analysis. Scientometrics 2016, 106, 213–228. [Google Scholar] [CrossRef]

- Moher, D.; Liberati, A.; Tetzlaff, J.; Altman, D.G.; Altman, D.G.; Antes, G.; Atkins, D.; Barbour, V.; Barrowman, N.; Berlin, J.A.; et al. Preferred Reporting Items for Systematic Reviews and Meta-Analyses: The PRISMA Statement. PLoS Med. 2009, 6, 1–6. [Google Scholar] [CrossRef] [PubMed]

- Ding, Y.; Chowdhury, G.G.; Foo, S. Bibliometric Cartography of Information Retrieval Research by Using Co-Word Analysis. Inf. Process. Manag. 2001, 37, 817–842. [Google Scholar] [CrossRef]

- van Eck, N.J.; Waltman, L. Visualizing Bibliometric Networks. In Measuring Scholarly Impact; Springer International Publishing: Cham, Switzerland, 2014; pp. 285–320. [Google Scholar]

- Van Eck, N.J.; Waltman, L. How to Normalize Cooccurrence Data? An Analysis of Some Well-Known Similarity Measures. J. Am. Soc. Inf. Sci. Technol. 2009, 60, 1635–1651. [Google Scholar] [CrossRef]

- van Eck, N.J.; Waltman, L. Software Survey: VOSviewer, a Computer Program for Bibliometric Mapping. Scientometrics 2010, 84, 523–538. [Google Scholar] [CrossRef]

- Waltman, L.; Van Eck, N.J. A New Methodology for Constructing a Publication-Level Classification System of Science. J. Am. Soc. Inf. Sci. Technol. 2012, 63, 2378–2392. [Google Scholar] [CrossRef]

- Van Eck, N.; Waltman, L.; Den Berg, J.; Kaymak, U. Visualizing the Computational Intelligence Field. IEEE Comput. Intell. Mag. 2006, 1, 6–10. [Google Scholar] [CrossRef]

- Sockin, M.; Xiong, W. A Model of Cryptocurrencies. NBER Work. Pap. Series 2020, 1–57. [Google Scholar] [CrossRef]

- Queiroz, M.M.; Telles, R.; Bonilla, S.H. Blockchain and supply chain management integration: A systematic review of the literature. Supply Chain Manag. 2019, 25, 241–254. [Google Scholar] [CrossRef]

- Kim, T.H.; Kumar, G.; Saha, R.; Rai, M.K.; Buchanan, W.J.; Thomas, R.; Alazab, M. A Privacy Preserving Distributed Ledger Framework for Global Human Resource Record Management: The Blockchain Aspect. IEEE Access 2020, 8, 96455–96467. [Google Scholar] [CrossRef]

- Nygard, K.E.; Bugalwi, A.; Alruwaythi, M.; Rastogi, A.; Kambhampaty, K.; Kotala, P. Situational Trust and Reputation in Cyberspace. Int. J. Comput. Appl. 2019, 26, 154–163. [Google Scholar]

- Ren, Y.; Zhu, F.; Qi, J.; Wang, J.; Sangaiah, A.K. Identity Management and Access Control Based on Blockchain under Edge Computing for the Industrial Internet of Things. Appl. Sci. 2019, 9, 2058. [Google Scholar] [CrossRef]

- Munn, L.; Hristova, T.; Magee, L. Clouded Data: Privacy and the Promise of Encryption. Big Data Soc. 2019, 6, 205395171984878. [Google Scholar] [CrossRef]

- Paech, P. Securities, Intermediation and the Blockchain: An Inevitable Choice between Liquidity and Legal Certainty? Unif. Law Rev. 2016, 21, 612–639. [Google Scholar] [CrossRef]

- Kshetri, N. Can Blockchain Strengthen the Internet of Things? IT Prof. 2017, 19, 68–72. [Google Scholar] [CrossRef]

- Yeoh, P. Regulatory Issues in Blockchain Technology. J. Financ. Regul. Compliance 2017, 25, 196–208. [Google Scholar] [CrossRef]

- Xiong, Z.; Zhang, Y.; Niyato, D.; Wang, P.; Han, Z. When Mobile Blockchain Meets Edge Computing. IEEE Commun. Mag. 2018, 56, 33–39. [Google Scholar] [CrossRef]

- Dwivedi, S.K.; Amin, R.; Vollala, S. Blockchain Based Secured Information Sharing Protocol in Supply Chain Management System with Key Distribution Mechanism. J. Inf. Secur. Appl. 2020, 54, 102554. [Google Scholar] [CrossRef]

- Lee, S.Y. PHR System Using Blockchain Technology. Int. J. Adv. Trends Comput. Sci. Eng. 2019, 8, 3188–3193. [Google Scholar] [CrossRef]

- Di Francesco Maesa, D.; Mori, P. Blockchain 3.0 Applications Survey. J. Parallel Distrib. Comput. 2020, 138, 99–114. [Google Scholar] [CrossRef]

- Francisco, K.; Swanson, D. The Supply Chain Has No Clothes: Technology Adoption of Blockchain for Supply Chain Transparency. Logistics 2018, 2, 2. [Google Scholar] [CrossRef]

- Katyayani, J.; Varalakshmi, C. Cognitive Computational Model for Evaluation of Fintech Products and Services with Respect to Vijayawada City, Ap. Int. J. Innov. Technol. Explor. Eng. 2019, 8, 1733–1736. [Google Scholar] [CrossRef]

- Yu, F.R.; Liu, J.; He, Y.; Si, P.; Zhang, Y. Virtualization for Distributed Ledger Technology (VDLT). IEEE Access 2018, 6, 25019–25028. [Google Scholar] [CrossRef]

- Ar, I.M.; Erol, I.; Peker, I.; Ozdemir, A.I.; Medeni, T.D.; Medeni, I.T. Evaluating the Feasibility of Blockchain in Logistics Operations: A Decision Framework. Expert Syst. Appl. 2020, 158, 113543. [Google Scholar] [CrossRef]

- Chen, J.; Lv, Z.; Song, H. Design of Personnel Big Data Management System Based on Blockchain. Future Gener. Comput. Syst. 2019, 101, 1122–1129. [Google Scholar] [CrossRef]

- Buocz, T.; Ehrke-Rabel, T.; Hödl, E.; Eisenberger, I. Bitcoin and the GDPR: Allocating Responsibility in Distributed Networks. Comput. Law Secur. Rev. 2019, 35, 182–198. [Google Scholar] [CrossRef]

- Tang, C.S.; Veelenturf, L.P. The Strategic Role of Logistics in the Industry 4.0 Era. Transp. Res. Part E Logist. Transp. Rev. 2019, 129, 1–11. [Google Scholar] [CrossRef]

- Sebastião, H.; Godinho, P. Forecasting and Trading Cryptocurrencies with Machine Learning under Changing Market Conditions. Financ. Innov. 2021, 7, 1–30. [Google Scholar] [CrossRef]

- Weiss, M.B.H.; Werbach, K.; Sicker, D.C.; Bastidas, C.E.C. On the Application of Blockchains to Spectrum Management. IEEE Trans. Cogn. Commun. Netw. 2019, 5, 193–205. [Google Scholar] [CrossRef]

- Yin, H.; Guo, D.; Wang, K.; Jiang, Z.; Lyu, Y.; Xing, J. Hyperconnected Network: A Decentralized Trusted Computing and Networking Paradigm. IEEE Netw. 2018, 32, 112–117. [Google Scholar] [CrossRef]

- Schmidt, C.G.; Wagner, S.M. Blockchain and Supply Chain Relations: A Transaction Cost Theory Perspective. J. Purch. Supply Manag. 2019, 25, 100552. [Google Scholar] [CrossRef]

- Kaya, Y. Analysis of Cryptocurrency Market and Drivers of the Bitcoin Price: Understanding the Price Drivers of Bitcoinunder Speculative Environment. 2018. Available online: http://www.diva-portal.org/smash/record.jsf?pid=diva2%3A1295584&dswid=-2630 (accessed on 7 July 2021).

- Ahmad, F.; Kerrache, C.A.; Kurugollu, F.; Hussain, R. Realization of Blockchain in Named Data Networking-Based Internet-of-Vehicles. IT Prof. 2019, 21, 41–47. [Google Scholar] [CrossRef]

- Potts, M. The State of Information Security. Netw. Secur. 2012, 2012, 9–11. [Google Scholar] [CrossRef]

- Sullivan, C.; Burger, E. E-Residency and Blockchain. Comput. Law Secur. Rev. 2017, 33, 470–481. [Google Scholar] [CrossRef]

- Hassan, M.A.; Shukur, Z.; Hasan, M.K. An Efficient Secure Electronic Payment System for E-Commerce. Computers 2020, 9, 66. [Google Scholar] [CrossRef]

- Channgam, S.; Nilsook, P.; Wannapiroon, P. Intelligent Information Management with Digitization Workflow. Int. J. Mach. Learn. Comput. 2019, 9, 886–892. [Google Scholar] [CrossRef]

- Messina, D.; Barros, A.C.; Soares, A.L.; Matopoulos, A. An Information Management Approach for Supply Chain Disruption Recovery. Int. J. Logist. Manag. 2020, 31, 489–519. [Google Scholar] [CrossRef]

- Yue, G. Design of Information Management System for Structural Monitoring Based on Network Fragmentation. Int. J. Internet Protoc. Technol. 2020, 13, 202–210. [Google Scholar] [CrossRef]

- Coughlin, T. Digital Storage in File-Based Workflows. SMPTE Motion Imaging J. 2012, 121, 77–82. [Google Scholar] [CrossRef]

- Ren, Y.; Leng, Y.; Qi, J.; Sharma, P.K.; Wang, J.; Almakhadmeh, Z.; Tolba, A. Multiple Cloud Storage Mechanism Based on Blockchain in Smart Homes. Future Gener. Comput. Syst. 2021, 115, 304–313. [Google Scholar] [CrossRef]

- Cai, Z.; Lin, J.; Liu, F. Blockchain Storage: Technologies and Challenges. Chin. J. Netw. Inf. Secur. 2020, 6, 11–20. [Google Scholar] [CrossRef]

- Mohanta, B.K.; Jena, D.; Satapathy, U. Trust Management in IOT Enable Healthcare System Using Ethereum Based Smart Contract. Int. J. Sci. Technol. Res. 2019, 8, 758–763. [Google Scholar]

- Rawat, D.B. Fusion of Software Defined Networking, Edge Computing, and Blockchain Technology for Wireless Network Virtualization. IEEE Commun. Mag. 2019, 57, 50–55. [Google Scholar] [CrossRef]

- Li, Z.; Wang, W.M.M.; Liu, G.; Liu, L.; He, J.; Huang, G.Q.Q. Toward Open Manufacturing a Cross-Enterprises Knowledge and Services Exchange Framework Based on Blockchain and Edge Computing. Ind. Manag. Data Syst. 2018, 118, 303–320. [Google Scholar] [CrossRef]

- Wang, Y.; Chen, C.-R.; Huang, P.-Q.; Wang, K. A New Differential Evolution Algorithm for Joint Mining Decision and Resource Allocation in a MEC-Enabled Wireless Blockchain Network. Comput. Ind. Eng. 2021, 155, 107186. [Google Scholar] [CrossRef]

- Kang, J.; Yu, R.; Huang, X.; Wu, M.; Maharjan, S.; Xie, S.; Zhang, Y. Blockchain for Secure and Efficient Data Sharing in Vehicular Edge Computing and Networks. IEEE Internet Things J. 2019, 6, 4660–4670. [Google Scholar] [CrossRef]

- Cebrián-Hernández, Á.; Jiménez-Rodríguez, E. Modeling of the Bitcoin Volatility through Key Financial Environment Variables: An Application of Conditional Correlation MGARCH Models. Mathematics 2021, 9, 267. [Google Scholar] [CrossRef]

- Kumar, G.; Saha, R.; Buchanan, W.J.; Geetha, G.; Thomas, R.; Rai, M.K.; Kim, T.-H.H.; Alazab, M. Decentralized Accessibility of E-Commerce Products through Blockchain Technology. Sustain. Cities Soc. 2020, 62, 102361. [Google Scholar] [CrossRef]

- Angelis, J.; Ribeiro da Silva, E. Blockchain Adoption: A Value Driver Perspective. Bus. Horiz. 2019, 62, 307–314. [Google Scholar] [CrossRef]

- Fiergbor, D.D. Blockchain Technology in Fund Management. In Communications in Computer and Information Science; Springer Nature Switzerland AG: Cham, Switzerland, 2018; Volume 899, pp. 310–319. [Google Scholar]

- Cocco, L.; Concas, G.; Marchesi, M. Using an Artificial Financial Market for Studying a Cryptocurrency Market. J. Econ. Interact. Coord. 2017, 12, 345–365. [Google Scholar] [CrossRef]

- Ali, M.S.; Vecchio, M.; Pincheira, M.; Dolui, K.; Antonelli, F.; Rehmani, M.H. Applications of Blockchains in the Internet of Things: A Comprehensive Survey. IEEE Commun. Surv. Tutor. 2019, 21, 1676–1717. [Google Scholar] [CrossRef]

- Novo, O. Blockchain Meets IoT: An Architecture for Scalable Access Management in IoT. IEEE Internet Things J. 2018, 5, 1184–1195. [Google Scholar] [CrossRef]

- Mazzei, D.; Baldi, G.; Fantoni, G.; Montelisciani, G.; Pitasi, A.; Ricci, L.; Rizzello, L. A Blockchain Tokenizer for Industrial IOT Trustless Applications. Future Gener. Comput. Syst. 2020, 105, 432–445. [Google Scholar] [CrossRef]

- Xu, L.D.; Xu, E.L.; Li, L. Industry 4.0: State of the Art and Future Trends. Int. J. Prod. Res. 2018, 56, 2941–2962. [Google Scholar] [CrossRef]

- Younan, M.; Houssein, E.H.; Elhoseny, M.; Ali, A.A. Challenges and Recommended Technologies for the Industrial Internet of Things: A Comprehensive Review. Measurement 2020, 151, 107198. [Google Scholar] [CrossRef]

- Hu, W.; Li, H. A Blockchain-Based Secure Transaction Model for Distributed Energy in Industrial Internet of Things. Alex. Eng. J. 2021, 60, 491–500. [Google Scholar] [CrossRef]

- Hu, Y.; Manzoor, A.; Ekparinya, P.; Liyanage, M.; Thilakarathna, K.; Jourjon, G.; Seneviratne, A. A Delay-Tolerant Payment Scheme Based on the Ethereum Blockchain. IEEE Access 2019, 7, 33159–33172. [Google Scholar] [CrossRef]

- Chen, C.-L.; Tsai, W.-C.; Chen, Y.-Y.; Tsaur, W.-J. Using a Stored-Value Card to Provide an Added-Value Service of Payment Protocol in VANET. Inf. Technol. Control 2013, 42, 369–372. [Google Scholar] [CrossRef]

- Daskapan, S.; Van Den Berg, J.; Ali-Eldin, A. Towards a Trustworthy Short-Range Mobile Payment System. Int. J. Inf. Technol. Manag. 2010, 9, 317–336. [Google Scholar] [CrossRef]

- Agbezoutsi, K.E.; Urien, P.; Dandjinou, T.M. Mobile Money Traceability and Federation Using Blockchain Services. Ann. Des Telecommun. Ann. Telecommun. 2021, 76, 223–233. [Google Scholar] [CrossRef]

- Cai, T.; Cai, H.J.; Wang, H.; Cheng, X.; Wang, L. Analysis of Blockchain System With Token-Based Bookkeeping Method. IEEE Access 2019, 7, 50823–50832. [Google Scholar] [CrossRef]

- Serrano, W. The Blockchain Random Neural Network for Cybersecure IoT and 5G Infrastructure in Smart Cities. J. Netw. Comput. Appl. 2021, 175, 102909. [Google Scholar] [CrossRef]

- Yoon, W.; Im, J.; Choi, I.; Kim, D. Blockchain-Based Object Name Service with Tokenized Authority. IEEE Trans. Serv. Comput. 2019, 13, 1. [Google Scholar] [CrossRef]

- Zhao, K.K.; Tang, S.; Zhao, B.; Wu, Y. Dynamic and Privacy-Preserving Reputation Management for Blockchain-Based Mobile Crowdsensing. IEEE Access 2019, 7, 74694–74710. [Google Scholar] [CrossRef]

- Siris, V.A.; Dimopoulos, D.; Fotiou, N.; Voulgaris, S.; Polyzos, G.C. Decentralized Authorization in Constrained IoT Environments Exploiting Interledger Mechanisms. Comput. Commun. 2020, 152, 243–251. [Google Scholar] [CrossRef]

- Bragadeesh, S.A.; Umamakeswari, A. Role of Blockchain in the Internet-of-Things (IoT). Int. J. Eng. Technol. 2018, 7, 109–112. [Google Scholar] [CrossRef][Green Version]

- Sanka, A.I.; Irfan, M.; Huang, I.; Cheung, R.C.C. A Survey of Breakthrough in Blockchain Technology: Adoptions, Applications, Challenges and Future Research. Comput. Commun. 2021, 169, 179–201. [Google Scholar] [CrossRef]

- Wu, J.; Xiong, F.; Li, C. Application of Internet of Things and Blockchain Technologies to Improve Accounting Information Quality. IEEE Access 2019, 7, 100090–100098. [Google Scholar] [CrossRef]

- Zhao, L.Q.; Song, Y.B.; Zhang, K.L.; Hu, A.Q.; Luo, J. Logistics Information Privacy Protection Based on Blockchain and Hierarchical Encryption. Yingyong Kexue Xuebao/J. Appl. Sci. 2019, 37, 224–234. [Google Scholar] [CrossRef]

- Butler, K.; Farley, T.R.; McDaniel, P.; Rexford, J. A Survey of BGP Security Issues and Solutions. Proc. IEEE 2010, 98, 100–122. [Google Scholar] [CrossRef]

- Xing, Q.; Wang, B.; Wang, X. BGPcoin: Blockchain-Based Internet Number Resource Authority and BGP Security Solution. Symmetry 2018, 10, 408. [Google Scholar] [CrossRef]

- Shao, W.; Jia, C.; Xu, Y.; Qiu, K.; Gao, Y.; He, Y. AttriChain: Decentralized Traceable Anonymous Identities in Privacy-Preserving Permissioned Blockchain. Comput. Secur. 2020, 99. [Google Scholar] [CrossRef]

- Yadav, G.; Kumar, A.; Luthra, S.; Garza-Reyes, J.A.; Kumar, V.; Batista, L. A Framework to Achieve Sustainability in Manufacturing Organisations of Developing Economies Using Industry 4.0 Technologies’ Enablers. Comput. Ind. 2020, 122, 103280. [Google Scholar] [CrossRef]

- Cole, R.; Stevenson, M.; Aitken, J. Blockchain Technology: Implications for Operations and Supply Chain Management. Supply Chain Manag. 2019, 24, 469–483. [Google Scholar] [CrossRef]

- Prause, G. Smart Contracts for Smart Supply Chains. IFAC-Pap. 2019, 52, 2501–2506. [Google Scholar] [CrossRef]

- Nam, J.-H.; Lee, S.-J.; Lee, I.-G. IP DLedger: Decentralized Ledger for Intellectual Property. J. Adv. Res. Dyn. Control Syst. 2018, 10, 271–280. [Google Scholar]

- Onik, M.M.H.; Kim, C.-S.; Lee, N.-Y.; Yang, J. Privacy-Aware Blockchain for Personal Data Sharing and Tracking. Open Comput. Sci. 2019, 9, 80–91. [Google Scholar] [CrossRef]

- Eenmaa-Dimitrieva, H.; Schmidt-Kessen, M.J. Creating Markets in No-Trust Environments: The Law and Economics of Smart Contracts. Comput. Law Secur. Rev. 2019, 35, 69–88. [Google Scholar] [CrossRef]

- Kim, S.-K.; Kim, U.-M.; Huh, J.-H. A Study on Improvement of Blockchain Application to Overcome Vulnerability of IoT Multiplatform Security. Energies 2019, 12, 402. [Google Scholar] [CrossRef]

- Baev, A.A.; Levina, V.S.; Reut, A.V.; Svidler, A.A.; Kharitonov, I.A.; Grigor’ev, V.V. Blockchain Technology in Accounting and Auditing. Accounting. Analysis. Audit. 2020, 7, 69–79. [Google Scholar] [CrossRef]

- Appelbaum, D.; Nehmer, R.A. Auditing Cloud-Based Blockchain Accounting Systems. J. Inf. Syst. 2020, 34, 5–21. [Google Scholar] [CrossRef]

- Hussien, H.M.; Yasin, S.M.; Udzir, N.I.; Ninggal, M.I.H.; Salman, S. Blockchain Technology in the Healthcare Industry: Trends and Opportunities. J. Ind. Inf. Integr. 2021, 22. [Google Scholar] [CrossRef]

- Merediz-Solà, I.; Bariviera, A.F. A Bibliometric Analysis of Bitcoin Scientific Production. Res. Int. Bus. Financ. 2019, 50, 294–305. [Google Scholar] [CrossRef]

- Rouzbahani, H.M.; Karimipour, H.; Dehghantanha, A.; Parizi, R.M. Blockchain Applications in Power Systems: A Bibliometric Analysis. In Advances in Information Security; Springer Nature Switzerland AG: Cham, Switzerland, 2020; Volume 79, pp. 129–145. [Google Scholar]

- Bodkhe, U.; Tanwar, S.; Parekh, K.; Khanpara, P.; Tyagi, S.; Kumar, N.; Alazab, M. Blockchain for Industry 4.0: A Comprehensive Review. IEEE Access 2020, 8, 79764–79800. [Google Scholar] [CrossRef]

- Dabbagh, M.; Sookhak, M.; Safa, N.S. The Evolution of Blockchain: A Bibliometric Study. IEEE Access 2019, 7, 19212–19221. [Google Scholar] [CrossRef]

- Firdaus, A.; Razak, M.F.A.; Feizollah, A.; Hashem, I.A.T.; Hazim, M.; Anuar, N.B. The Rise of “Blockchain”: Bibliometric Analysis of Blockchain Study. Scientometrics 2019, 120, 1289–1331. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

| R | Year | Article Title | Author(s) | Journal | SA | AT |

|---|---|---|---|---|---|---|

| [15] | 2016 | Blockchains and Smart Contracts for the Internet of Things | Christidis, K.; Devetsikiotis, M. | IEEE Access | E-CS | B-A-M |

| [16] | 2016 | Trusting Records: Is Blockchain Technology the Answer? | Lemieux, V.L. | Records Management Journal | SS-BMA | B |

| [17] | 2016 | Fraud detections for online businesses: a perspective from blockchain technology | Cai, Y.; Zhu, D. | Financial Innovation | EEF-BMA | B-A-M |

| [18] | 2017 | Automated Execution of Financial Contracts on Blockchains | Egelund-Müller, B.; Elsman, M.; Henglein, F.; Ross, O. | Business and Information Systems Engineering | CS | B-A |

| [19] | 2017 | Toward blockchain-based accounting and assurance | Dai, J.; Vasarhelyi, M.A. | Journal of Information Systems | BMA | B-A |

| [20] | 2017 | Can Blockchains Serve an Accounting Purpose? | Coyne, J.G.; McMickle, P.L. | Journal of Emerging Technologies in Accounting | BMA-CS | B-A |

| [21] | 2018 | Accounting for Bitcoin and Other Cryptocurrencies under IFRS: A Comparison and Assessment of Competing Models | Procházka, D. | International Journal of Digital Accounting Research | EEF-DS-BMA | B-A |

| [22] | 2018 | Designing confidentiality-preserving Blockchain-based transaction processing systems | Wang, Y.; Kogan, A. | International Journal of Accounting Information Systems | EEF-BMA-DS | B-M |

| [23] | 2018 | Money, Credit, and Digital Payment 1971/2014: From the Credit Card to Apple Pay. | Gießmann, S. | Administration and Society | SS-BMA | B-A-M |

| [24] | 2019 | From Old to New: From Internet to Smart Contracts and from People to Smart Contracts | de Graaf, T.J. | Computer Law and Security Review | SS-BMA-CS | B-A-M |

| [25] | 2019 | Big Data, Blockchain, and Artificial Intelligence in Cloud-Based Accounting Information Systems | Ionescu, L. | Analysis and Metaphysics | AH | B-A |

| [26] | 2019 | Blockchain: Business’ next New “It” Technology—a Comparison of Blockchain, Relational Databases, and Google Sheets | McAliney, P.J.; Ang, B. | International Journal of Disclosure and Governance | EEF-BMA | B-A-M |

| [27] | 2020 | Blockchain and accounting governance: emerging issues and considerations for accounting and assurance professionals | Smith, S.S.; Castonguay, J.J. | Journal of Emerging Technologies in Accounting | BMA-CS | B-A |

| [28] | 2020 | Digital systems and new challenges of financial management—fintech, XBRL, blockchain and cryptocurrencies | Mosteanu, N.R.; Faccia, A. | Quality—Access to Success | BMA | B-A-M |

| [29] | 2020 | Blockchain Technology in the Future of Business Cyber Security and Accounting. | Demirkan, S.; Demirkan, I.; McKee, A. | Journal of Management Analytics | BMA-M-DS | B-A |

| R | 2016 | 2017 | 2018 | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Keyword | L | TLS | O | % | Keyword | L | TLS | O | % | Keyword | L | TLS | O | % | |

| 1 | Blockchain | 36 | 37 | 3 | 75% | Blockchain | 197 | 245 | 22 | 84.62% | Blockchain | 860 | 1185 | 94 | 78.33% |

| 2 | Privacy | 31 | 32 | 2 | 50% | Bitcoin | 35 | 41 | 4 | 15.38% | Information Management | 355 | 434 | 25 | 20.83% |

| 3 | Access Control | 14 | 14 | 1 | 25% | Cloud Computing | 52 | 64 | 4 | 15.38% | Internet of Things | 217 | 284 | 19 | 15.83% |

| 4 | Authenticity | 5 | 5 | 1 | 25% | Electronic Money | 51 | 55 | 4 | 15.38% | Digital Storage | 223 | 279 | 15 | 12.50% |

| 5 | Authorization Management | 14 | 14 | 1 | 25% | Internet Of Things | 61 | 81 | 4 | 15.38% | Network Security | 166 | 211 | 12 | 10.00% |

| 6 | Bitcoin | 14 | 14 | 1 | 25% | Supply Chains | 57 | 72 | 4 | 15.38% | Cryptography | 149 | 170 | 11 | 9.17% |

| 7 | Computer Security | 18 | 18 | 1 | 25% | Data Privacy | 57 | 61 | 3 | 11.54% | Data Privacy | 140 | 178 | 11 | 9.17% |

| 8 | Confidentiality | 18 | 18 | 1 | 25% | Information Management | 46 | 47 | 3 | 11.54% | Smart Contracts | 135 | 156 | 11 | 9.17% |

| 9 | Copyrights | 14 | 14 | 1 | 25% | Intelligent Systems | 50 | 59 | 3 | 11.54% | Authentication | 136 | 164 | 10 | 8.33% |

| 10 | Data Privacy | 14 | 14 | 1 | 25% | Security | 43 | 46 | 3 | 11.54% | Bitcoin | 60 | 68 | 8 | 6.67% |

| 11 | Decentralized Access Control | 14 | 14 | 1 | 25% | Commerce | 31 | 32 | 2 | 7.69% | Commerce | 112 | 127 | 8 | 6.67% |

| 12 | Digital Preservation | 5 | 5 | 1 | 25% | Computation Theory | 25 | 27 | 2 | 7.69% | Access Control | 98 | 111 | 7 | 5.83% |

| 13 | Electronic Money | 14 | 14 | 1 | 25% | Cybersecurity | 25 | 35 | 2 | 7.69% | Electronic Money | 76 | 88 | 7 | 5.83% |

| 14 | Indicator-Centric Schema | 18 | 18 | 1 | 25% | Distributed Computer Systems | 31 | 33 | 2 | 7.69% | Privacy | 112 | 129 | 7 | 5.83% |

| 15 | Information Dissemination | 18 | 18 | 1 | 25% | Distributed Ledger | 6 | 7 | 2 | 7.69% | Cloud Computing | 91 | 113 | 6 | 5.00% |

| R | 2019 | 2020 | 2016–2020 | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Keyword | L | TLS | O | % | Keyword | L | TLS | O | % | Keyword | L | TLS | O | % | |

| 1 | Blockchain | 1885 | 3122 | 267 | 78.53% | Blockchain | 4120 | 7501 | 556 | 86.88% | Blockchain | 5748 | 12090 | 942 | 83.36% |

| 2 | Internet of Things | 547 | 789 | 54 | 15.88% | Information Management | 1160 | 1703 | 97 | 15.16% | Information Management | 1798 | 2944 | 174 | 15.40% |

| 3 | Information Management | 550 | 760 | 49 | 14.41% | Internet of Things | 952 | 1453 | 93 | 14.53% | Internet of Things | 1506 | 2621 | 171 | 15.13% |

| 4 | Digital Storage | 407 | 552 | 34 | 10.00% | Supply Chain Management | 757 | 1101 | 74 | 11.56% | Supply Chain Management | 947 | 1465 | 108 | 9.56% |

| 5 | Smart Contract | 307 | 409 | 32 | 9.41% | Digital Storage | 714 | 1061 | 58 | 9.06% | Digital Storage | 1140 | 1892 | 107 | 9.47% |

| 6 | Supply Chain Management | 251 | 315 | 30 | 8.82% | Network Security | 718 | 1042 | 58 | 9.06% | Network Security | 1055 | 1739 | 99 | 8.76% |

| 7 | Smart Contracts | 262 | 339 | 29 | 8.53% | Smart Contract | 577 | 724 | 56 | 8.75% | Smart Contract | 910 | 1268 | 98 | 8.67% |

| 8 | Data Privacy | 314 | 441 | 27 | 7.94% | Authentication | 455 | 630 | 43 | 6.72% | Data Privacy | 744 | 1218 | 72 | 6.37% |

| 9 | Network Security | 328 | 440 | 27 | 7.94% | Security | 494 | 684 | 41 | 6.41% | Security | 698 | 1081 | 71 | 6.28% |

| 10 | Ethereum | 187 | 237 | 20 | 5.88% | Access Control | 429 | 617 | 38 | 5.94% | Access Control | 623 | 1025 | 66 | 5.84% |

| 11 | Security | 187 | 238 | 20 | 5.88% | Supply Chains | 461 | 621 | 37 | 5.78% | Authentication | 639 | 956 | 65 | 5.75% |

| 12 | Access Control | 201 | 273 | 19 | 5.59% | Cryptography | 454 | 619 | 36 | 5.63% | Cryptography | 690 | 1043 | 63 | 5.58% |

| 13 | Commerce | 266 | 331 | 19 | 5.59% | Data Sharing | 416 | 558 | 32 | 5.00% | Supply Chains | 685 | 987 | 59 | 5.22% |

| 14 | Cryptography | 171 | 228 | 15 | 4.41% | Data Privacy | 386 | 524 | 30 | 4.69% | Privacy | 500 | 753 | 49 | 4.34% |

| 15 | Big Data | 140 | 173 | 14 | 4.12% | Network Architecture | 384 | 524 | 30 | 4.69% | Commerce | 615 | 823 | 47 | 4.16% |

| Cluster 1 (Pink, 29%) | ||||

|---|---|---|---|---|

| Rank | Keyword | Weight Links | Weight Total Link Strength | Weight Occurrences |

| 1 | Blockchain (*) | 511 | 5077 | 942 |

| 2 | Supply Chain Management | 206 | 591 | 108 |

| 3 | Supply Chains | 196 | 437 | 59 |

| 4 | Artificial Intelligence | 117 | 191 | 37 |

| 5 | Distributed Ledger | 108 | 185 | 37 |

| 6 | Decision Making | 126 | 221 | 31 |

| 7 | Big Data | 131 | 212 | 30 |

| 8 | Cryptocurrency | 70 | 128 | 28 |

| 9 | Trust | 106 | 189 | 28 |

| 10 | Industry 4.0 | 114 | 216 | 26 |

| Cluster 2 (Green, 18%) | ||||

|---|---|---|---|---|

| Rank | Keyword | Weight Links | Weight Total Link Strength | Weight Occurrences |

| 1 | Network Security (*) | 294 | 886 | 99 |

| 2 | Data Privacy | 226 | 623 | 72 |

| 3 | Security | 229 | 545 | 71 |

| 4 | Authentication | 198 | 464 | 65 |

| 5 | Security and Privacy | 156 | 316 | 33 |

| 6 | Trust Management | 113 | 208 | 28 |

| 7 | Identity Management | 76 | 136 | 25 |

| 8 | Security Analysis | 116 | 204 | 21 |

| 9 | Vehicular ad hoc Networks | 86 | 190 | 21 |

| 10 | Mobile Telecommunication Systems | 103 | 156 | 19 |

| Cluster 3 (Red, 13%) | ||||

|---|---|---|---|---|

| Rank | Keyword | Weight Links | Weight Total Link Strength | Weight Occurrences |

| 1 | Information Management (*) | 378 | 1338 | 174 |

| 2 | Smart Contract | 259 | 577 | 98 |

| 3 | Access Control | 190 | 516 | 66 |

| 4 | Ethereum | 115 | 227 | 40 |

| 5 | Proposed Architectures | 93 | 157 | 19 |

| 6 | Trusted Third Parties | 83 | 134 | 17 |

| 7 | Embedded Systems | 90 | 140 | 15 |

| 8 | Management | 29 | 45 | 15 |

| 9 | Hyperledger Fabric | 38 | 62 | 14 |

| 10 | Crime | 55 | 87 | 12 |

| Cluster 4 (Yellow, 12%) | ||||

|---|---|---|---|---|

| Rank | Keyword | Weight Links | Weight Total Link Strength | Weight Occurrences |

| 1 | Digital Storage (*) | 306 | 924 | 107 |

| 2 | Cryptography | 197 | 490 | 63 |

| 3 | Privacy | 174 | 374 | 49 |

| 4 | Data Sharing | 145 | 294 | 37 |

| 5 | Distributed Ledger Technology | 89 | 138 | 29 |

| 6 | Trusted Computing | 114 | 210 | 25 |

| 7 | Privacy Preserving | 108 | 191 | 23 |

| 8 | Public Key Cryptography | 95 | 157 | 22 |

| 9 | Records Management | 72 | 138 | 21 |

| 10 | Electronic Document Exchange | 69 | 121 | 15 |

| Cluster 5 (Cyan, 11%) | ||||

|---|---|---|---|---|

| Rank | Keyword | Weight Links | Weight Total Link Strength | Weight Occurrences |

| 1 | Edge Computing (*) | 151 | 303 | 36 |

| 2 | Bitcoin | 93 | 167 | 34 |

| 3 | Cloud Computing | 141 | 283 | 33 |

| 4 | Decentralization | 97 | 162 | 26 |

| 5 | Distributed Computer Systems | 139 | 242 | 26 |

| 6 | Fog Computing | 97 | 192 | 26 |

| 7 | Electronic Money | 113 | 185 | 25 |

| 8 | Costs | 108 | 194 | 22 |

| 9 | Game Theory | 87 | 155 | 18 |

| 10 | Deep Learning | 71 | 108 | 17 |

| Cluster 6 (Purple, 9%) | ||||

|---|---|---|---|---|

| Rank | Keyword | Weight Links | Weight Total Link Strength | Weight Occurrences |

| 1 | Commerce (*) | 166 | 343 | 47 |

| 2 | Peer to Peer Networks | 146 | 256 | 34 |

| 3 | Power Markets | 98 | 205 | 23 |

| 4 | Smart City | 128 | 210 | 23 |

| 5 | Fintech | 76 | 119 | 19 |

| 6 | Smart Grid | 90 | 153 | 16 |

| 7 | Smart Power Grids | 85 | 155 | 14 |

| 8 | Microgrids | 54 | 78 | 10 |

| 9 | Security Systems | 61 | 82 | 9 |

| 10 | Personal Computing | 58 | 77 | 8 |

| Cluster 7 (Orange, 8%) | ||||

|---|---|---|---|---|

| Rank | Keyword | Weight Links | Weight Total Link Strength | Weight Occurrences |

| 1 | Internet of Things (*) | 352 | 1202 | 171 |

| 2 | Network Architecture | 191 | 410 | 44 |

| 3 | Security of Data | 103 | 181 | 26 |

| 4 | Consensus Algorithms | 117 | 173 | 22 |

| 5 | Automation | 67 | 113 | 16 |

| 6 | Consortium Blockchain | 75 | 106 | 13 |

| 7 | Internet Protocols | 71 | 103 | 12 |

| 8 | Accounting | 15 | 25 | 10 |

| 9 | Data Transfer | 54 | 86 | 10 |

| 10 | Centralized Management | 52 | 67 | 9 |

| Rank | Future Direction of Research | Relevance Score (*) |

|---|---|---|

| 1 | Credit Value Evaluation Mechanism | 21.833 |

| 2 | Enabled Payment Gateway | 20.191 |

| 3 | Unstructured Supplementary Service Data Message | 20.191 |

| 4 | Consolidated Identity Management | 20.027 |

| 5 | Hyperledger Sawtooth | 19.425 |

| 6 | Hierarchical Lightweight High Throughput Blockchain | 19.215 |

| 7 | BGP Security Infrastructure | 18.502 |

| 8 | Global Supply Chain Risk Analysis | 17.201 |

| 9 | Extensible Permissioned Blockchain Platform | 17.101 |

| 10 | Centralized Authentication Authorization Auditing | 12.217 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Abad-Segura, E.; Infante-Moro, A.; González-Zamar, M.-D.; López-Meneses, E. Blockchain Technology for Secure Accounting Management: Research Trends Analysis. Mathematics 2021, 9, 1631. https://doi.org/10.3390/math9141631

Abad-Segura E, Infante-Moro A, González-Zamar M-D, López-Meneses E. Blockchain Technology for Secure Accounting Management: Research Trends Analysis. Mathematics. 2021; 9(14):1631. https://doi.org/10.3390/math9141631

Chicago/Turabian StyleAbad-Segura, Emilio, Alfonso Infante-Moro, Mariana-Daniela González-Zamar, and Eloy López-Meneses. 2021. "Blockchain Technology for Secure Accounting Management: Research Trends Analysis" Mathematics 9, no. 14: 1631. https://doi.org/10.3390/math9141631

APA StyleAbad-Segura, E., Infante-Moro, A., González-Zamar, M.-D., & López-Meneses, E. (2021). Blockchain Technology for Secure Accounting Management: Research Trends Analysis. Mathematics, 9(14), 1631. https://doi.org/10.3390/math9141631