1. Introduction

Modern mathematical game theory solves problems of modeling, research and analysis of various conflict-controlled processes. Of particular interest are the processes developing over time [

1]. Differential games allow us to describe such dynamic processes in the sense of a conflict.

In a differential game of extraction, the standard scenario involves a dynamic competition among players (or, more precisely, companies) which exert effort aimed at extracting a natural resource. If the resource does not regenerate over time, such as natural gas or earth minerals, it is called exhaustible or nonrenewable.

Economic literature has been dealing with effects and characteristics of exhaustible resource extraction since 1817, when Ricardo [

2] addressed the issue in his essay

The principles of political economy and taxation. In the 20th century, the debate was relaunched by Hotelling [

3], and then subsequently a vast stream of static and dynamic models was conceived and developed over the years (see, for example [

4]).

If we only focus on models described through differential games, the basic framework includes a population of companies extracting the same resource, having the extraction effort levels as their strategic variables, which directly affect their respective payoffs, which increase as the extracted quantity increases. On the other hand, the state variables represent the stocks of resources, which are depleted over time by extraction. In the easiest representation, there is a unique resource and all companies aim to pick it up as much as possible. To describe a more realistic economic behavior, a key element was introduced in economic literature: the random duration of the game.

The seminal paper on this extension of the standard optimal control problem is due to Yaari [

5] in 1965. At the same time, in Russia, in 1966, Petrosyan and Murzov [

6] first studied differential zero-sum games with terminal payoff at random time horizon. Subsequently, further studies have been provided: in the work of Boukas et al. [

7] in 1990, an optimal control problem with random duration was studied in general terms. Cooperative differential games with random time horizon were first studied by Petrosyan and Shevkoplyas [

8] in 2000, whereas the concept of time consistency in differential games with prescribed duration was introduced in [

9].

Such a concept is particularly relevant because most literature treats stability of the cooperative solutions in static cooperative settings. On the other hand, stable cooperation in the problem is a key requirement when the scenario is dynamic as well. In cooperative differential games, cooperating players wish to establish a dynamically stable (time-consistent) cooperative agreement (e.g., the dynamic versions of the Shapley Value, core, etc.).

Time consistency implies that, as cooperation evolves, cooperating partners are guided by the same optimality principle at each instant of time and hence do not have any incentive to deviate from the previously adopted cooperative behavior.

After Petrosyan’s seminal paper in 1977, such topic was actively developed by a number of researchers. In a paper by Jorgensen et al. [

10], the problem of time-consistency and agreeability of the solution in linear-state class of differential games was investigated. In a paper by Petrosjan and Zaccour [

11], a similar problem of ecological management was studied as well as in the more recent paper by Zaccour [

12] and book by Petrosyan and Yeung [

13]. Recently, the notion of time consistency was extended to the case of discrete games (see, e.g., [

14]). An extension of the time consistency problem to the case of differential games with random duration was first undertaken in [

8], subsequently further investigation and results were accomplished in [

15,

16,

17,

18,

19]. In [

20], a random time horizon hybrid (see also [

21] for a general treatment of hybrid differential games) differential game was considered such that the probability distribution can change over time. Differential games with discrete random variable of time horizon and corresponding time-consistency problem were considered recently in [

22]. Time-consistency notation for multistage games with vector payoffs was introduced in [

23]. The regularization of a cooperative solution for the case of Core and the Shapley value had been done for a multistage game with random time horizon in [

24]. The present contribution locates itself in this line of research.

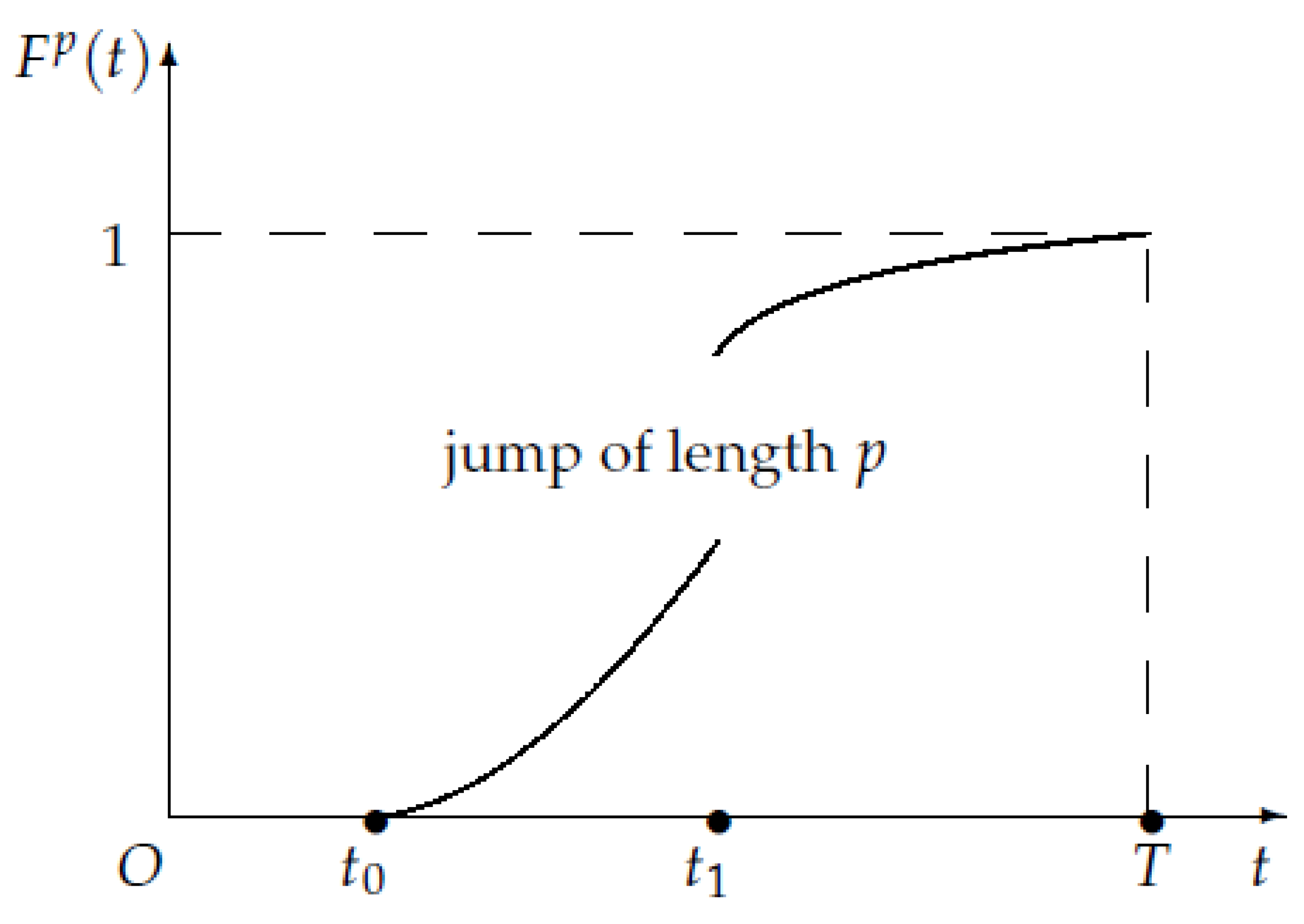

In this paper, we intend to propose a description and an analysis of a scenario which differs from the previous treatments: the random variable which indicates the stopping time of extraction has a c.d.f. which is not continuous over the whole time interval. Specifically, we assume that there is a jump at an internal point, and we carry out an analysis which is differentiated based on the initial time of the game, i.e., before or after the jump. This formulation can represent any situation in which the distribution of the random variable is affected by external factors such as a Parliament bill which makes an extraction technique illegal. An example may be provided by the controversial fracking process for gas extraction.

In this setting, standard models take into account an oligopolistic competition among firms, where each firm aims to maximize its own profit. However, there exist some different approaches in the literature which also involve the possibility of cooperation among agents.

Because of the depletion of oil and gas resources on the mainland, the active development of oil-and-gas fields on continental shelves is to begin in the near future. Today, there are about seventy developing and potential oil-and-gas fields on continental shelves of Azerbaijan, Canada, Kazakhstan, Mexico, Norway, Russia, Saudi Arabia, the USA, etc. For example, today the firms which are involved in the development of Sakhalin oil-and-gas fields (Russia) are Gazprom, Shell, Mitsui, and Mitsubishi.

Moreover, the task of oil and gas exploitation in the Arctic is a key issue nowadays, especially relevant for Canada, Denmark, Norway, Russia and the USA. We believe that the source of economic success of the development of pool in Arctic should bring about a cooperative collaboration of participating countries. Collaboration in the Arctic is important at least in the sense that an accident at one borehole could lead to serious problems or complete stoppage of resource exploitation for all neighbors. Thus, the involved countries have to collaborate to provide security for oil and gas exploitation in the Arctic, otherwise environmental disasters and huge economic losses for all participants might occur. This is the main motivation to consider the cooperative form of the non-renewable resource extraction game.

However, despite all the above, the oil and gas extraction on a continental shelf is a high-risk economic activity and reconsideration of existing models of non-renewable resource extraction is required. Stochastic framework may be useful in the sense that it increases the validity of models (see, for example, [

25]). As usual, game-theoretical models with infinite or fixed time horizon are used for modeling of renewable or exhausted resource exploitation. Although they provide numerous insights for equilibrium and stability, such an approach is not very realistic. Namely, the contract date is never equal to the real period of field exploitation, because either exploitation is prematurely finished by accident or unprofitability or the period of exploitation is extended.

Here, we specifically consider the occurrence of a cooperative game structure, where companies agree on a collective strategy to maximize the aggregate payoff. The agreement establishes that, after maximization, the total payoff is supposed to be redistributed among the cooperating firms. As in standard theory of cooperative games, the distribution of the total worth is the problem to be addressed (see, for example, [

8]). In a differential game, the total worth simply corresponds to the sum of the integral payoffs of all players, and the distribution of the total worth has to be implemented by using a suitable solution concept. Our main focus is on the cooperative setup, where we describe the determination of an IDP (imputation distribution procedure, which was first introduced by Petrosyan in [

9]), which is a dynamic way to attribute players their respective shares gained in the game. We also determine the relations to explicitly calculate IDPs in the above different cases, also discussing the issue of time consistency. Finally, we outline a complete example where

N companies compete over extraction of a unique exhaustible resource, comparing the results in the non-cooperative and cooperative scenarios.

The paper is organized as follows.

Section 2 introduces the notation of the game, whose non-cooperative setup is exposed. The cooperative setup is proposed in

Section 3, where the main findings, including a theorem which establishes the existence of a time-consistent imputation, are laid out in detail. In

Section 4, we propose a model to employ the above-mentioned procedure.

Section 5 concludes and proposes some possible future developments.

3. Main Results in the Cooperative Setup

Suppose that the game

is played in a cooperative scenario. Generally speaking, cooperation means that a group of companies agree to form a coalition before starting the game. In this case, we assume that such a group is the

grand coalition, i.e., the totality of the involved players. Clearly, any dynamic model in which players form coalitions that are subgroups of the grand coalition deserves a special attention as well, but it is outside the scope of this paper (for the construction of the value functions in cooperative games, see, for example, [

27,

28] for cooperative differential games).

From now on, to simplify the notation and to reconcile the ongoing discussion with a standard case, we assume a unique exhaustible resource, which is extracted by

N different companies, hence

and

are the effort levels. The cooperating players decide to use optimal strategies

, which are defined as the strategies maximizing the sum of all payoffs, i.e.,

As is standard in cooperative games, all players in the coalition jointly agree on a distribution method to share the total payoff. It is possible that, in some instant, the solution of the current game is not optimal according to the optimality principle which was initially selected, meaning that the optimality principle may lose time-consistency. Because we are investigating a dynamic setting, it is necessary to define and to determine an imputation distribution procedure which is supposed to be compliant with the payoff in the form of Equation (

4).

Before proceeding, we briefly recall the notion of imputation: in an

N-players cooperative game, an

imputation is a distribution

among players such that the sum of its coordinates is equal to the value of the grand coalition and each

assigns to the

i-th player a quantity which is not smaller than the one she would achieve by playing as a singleton. In other words, if

N is the set of players and

is the characteristic function of the game,

is an imputation if

and

for all

. The first property is called

efficiency and guarantees that the imputation is a method of distribution of the total gain among all players (for an exhaustive overview on cooperative games, see [

29]). Different imputations are usually employed in cooperative games, because not all solution concepts fit all models. However, the most useful one seems to be the

Shapley value, first introduced by Nobel laureate L.S. Shapley in [

30] in 1953, and which has been utilized in a huge number of economic and financial applications. (An extensive treatment of the Shapley value and of other relevant solution concepts can be found in [

29].)

Definition 2. Given an imputation in a game , such that for all we have that:then the vector function is called an imputation distribution procedure (IDP). The next Definition intends to expose the property of time-consistency for imputations.

Definition 3. An imputation in a game is time-consistent if there exists an IDP such that:

- 1.

for all the vector , wherefor all , belongs to the same optimality principle in the subgame , i.e., is an imputation in ; - 2.

for all the vector wherefor all , belongs to the same optimality principle in the subgame , i.e., is an imputation in .

The next step consists in the determination of a relation between and . In addition, in this case, we have to distinguish the cases when the subgame starts before or after the jump at instant . Firstly, we prove a lemma which is helpful to reformulate imputation . The subsequent Proposition intend to explicitly outline the forms for the IDPs of the game.

Lemma 1. If , for all , the coordinates of imputation ξ can be written as follows: Proof. We can write the following:

and finally Equation (

6).

For the second case, we can write the following:

and finally Equation (

7). ☐

Proposition 3. If , then for all , the i-th coordinate of the IDP is given by: If , then for all , the i-th coordinate of the IDP is given by: Proof. When

, we can differentiate Equation (

6) with respect to

, thus obtaining:

Then, solving for

yields:

When

, we can differentiate Equation (

7) with respect to

, thus obtaining:

Then, solving for

yields:

☐

The above results can be collected as follows:

Theorem 1. Let the imputation of the game be an absolutely continuous function of t, . If the IDP has one of the following forms:

then is a time-consistent imputation with IDP given by either Equation (10) or (11). The problem of stable cooperation in differential games with random duration where c.d.f. is continuous ( without any breaks) was studied by in [

8,

16,

18]. Assuming in our model

p is equal to zero, the obtained results coincide with the results in the above-mentioned work. Moreover, new results cover the framework for a fully deterministic models. Namely, for the problem with prescribed duration for

in Equations (

10) and (

11), we obtain the results published in [

9]. For the problem with constant discounting, see work [

11] and Equation (

10) with

.

4. An Example

We are going to consider a simple model of common-property nonrenewable resource extraction published in [

31] in 2000, and then further investigated in successive papers (e.g., [

15,

32]).

In addition, in this case,

, that is we have a unique state variable

indicating the stock of a nonrenewable resource at time

t. The companies’ strategic variables

, for

denote the rates of extraction, or extraction efforts, at time

t. The state equation has the form:

the initial condition, i.e., the amount of resource at time

is

The differential Equation (

12) is the most standard and simple dynamics in nonrenewable resource extraction games, where all players concur to extract and deplete the resource with the same intensity. When the involved resource is renewable, it also regenerates at a growth rate

, hence a positive linear term in the state variable also appears in Equation (

12), and the model must be treated differently (see for example [

33] or the survey [

34]).

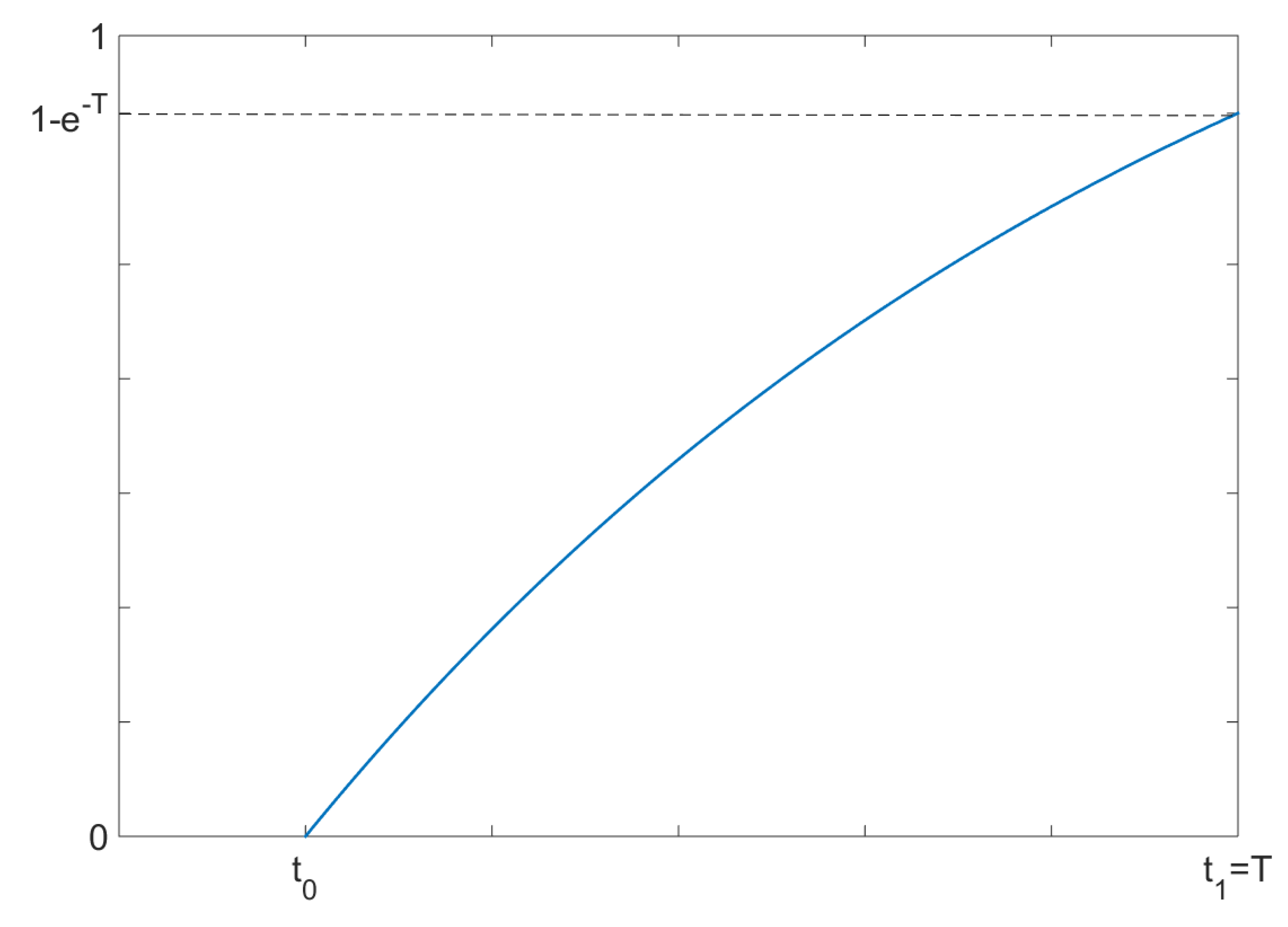

Back to the model, we suppose that the game ends at the random time instant

t, a random variable having exponential distribution

on the interval

(

Figure 2), i.e., we are investigating the first case, before the jump in the distribution. We also assume that the jump takes place in the end of the interval

, i.e.,

. Hence, the discontinuity occurs at the terminal time. The c.d.f. of the random variable

t is given by:

which turns into

for

. From now on, we consider this case, i.e.,

.

Note that we can provide the complete formulation of the discontinuous c.d.f. as in the previous section:

meaning that, in this case,

.

In this game, each player

i has a utility function

where

and

are positive constants depending on the specific scenario and on the companies’ characteristics.

The expected integral payoff of player (to lighten the notation, we omit redundant arguments whenever possible):

We are going to find

noncooperative open-loop optimal trajectories of state and controls in relation to the noncooperative form of the game using Pontryagin’s maximum principle, which is one of the two major procedures for equilibrium structure in differential games [

31]. In this model, this method is suitable, because the open-loop trajectories are easily visualized in

. Each company aims to solve the following problem:

Each player has a Hamiltonian function of the form:

where

is the

i-th adjoint variable attached by company

i to the resource dynamics or, in line with a standard economic interpretation, the related shadow price.

Differentiating each Hamiltonian with respect to

and then equating to 0 yields the first order conditions:

then, solving for

, we obtain:

The second order conditions hold, because for all

:

The adjoint equations and the related transversality conditions read as:

hence the optimal costates are

, for all

.

Plugging

into the FOCs yields the optimal controls, i.e.,

To determine the optimal state

, it suffices to substitute Equation (

14) into the state dynamics in Equation (

12) and subsequently integrate both sides, employing the initial condition:

so the optimal stock of resource amounts to:

Now, we are going to take into account a cooperative version of the game, that is a scenario where all companies agree to play strategies such that their aggregate payoff is maximized. The sum of all payoffs is:

The approach for the determination of the open-loop equilibrium structure is analogous to the one adopted in the noncooperative case. From now on, we are going to use the notation

,

to avoid confusion with the previous quantities.

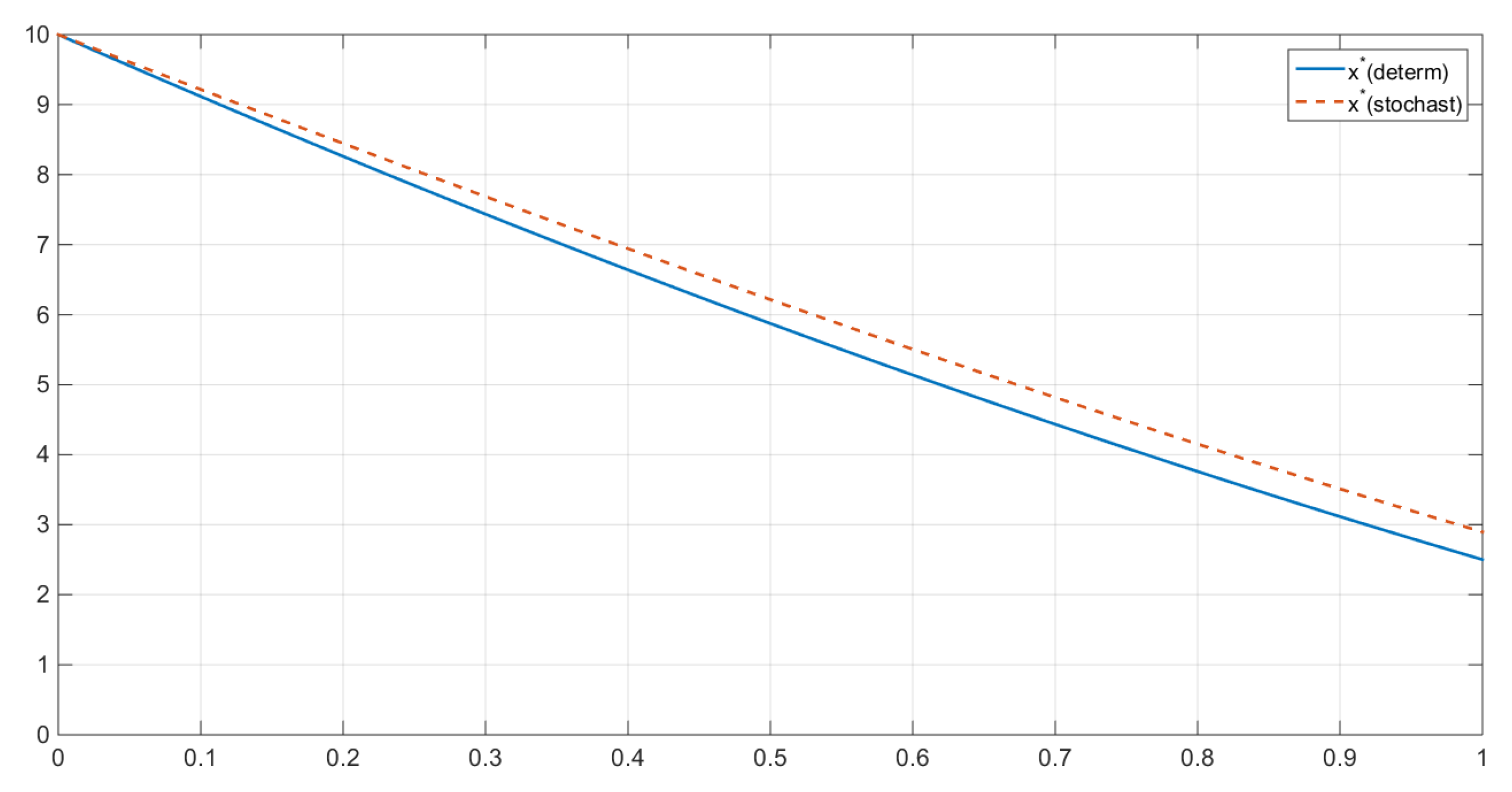

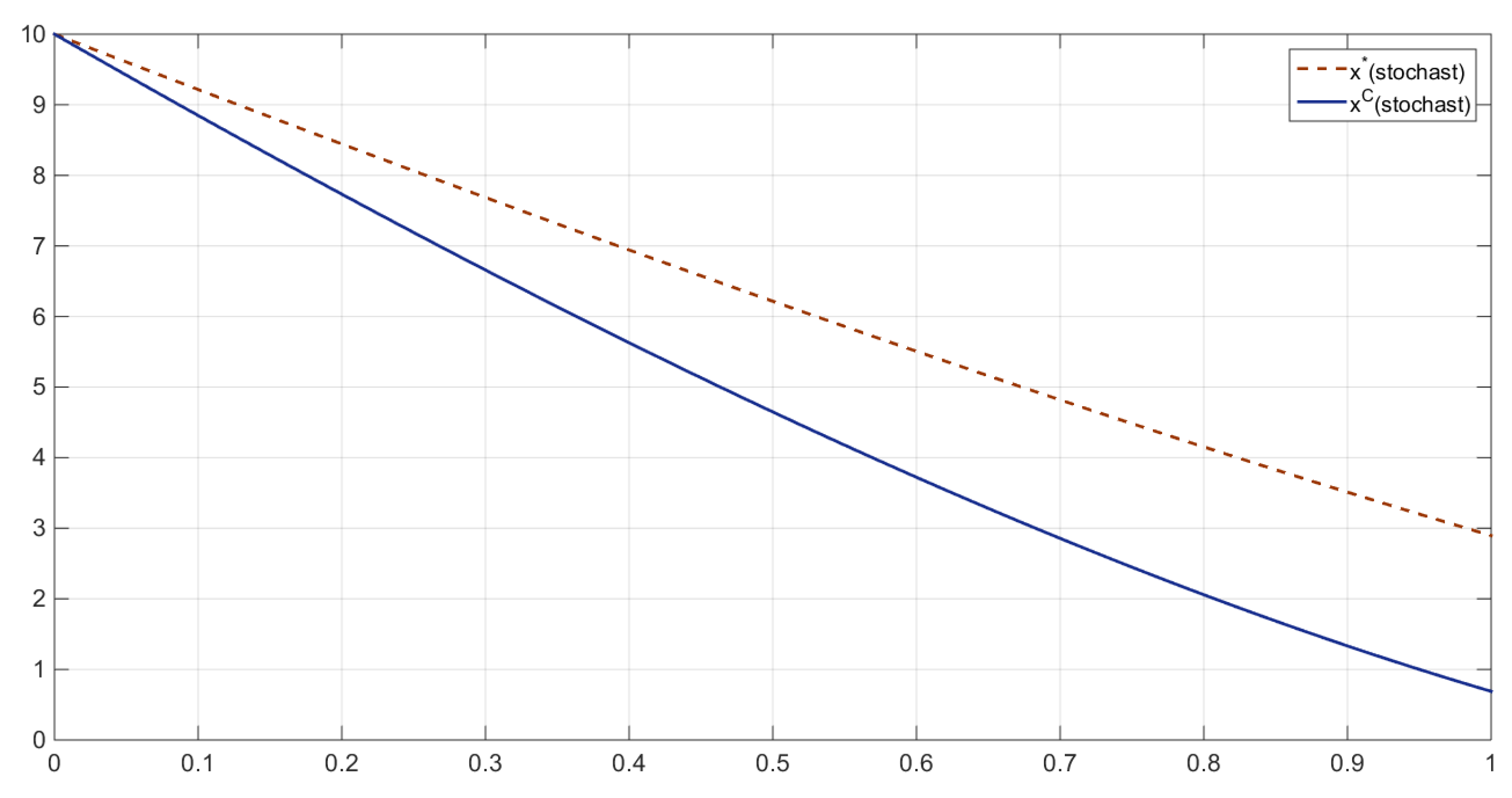

The comparison between the resource stocks in the two scenarios can be illustrated by a simple inequality, highlighting that the noncooperative resource stock exceeds the cooperative one (

Figure 3 and

Figure 4). Namely, at all

, we have that:

Such an estimate always holds for

, because

An investigation of a suitable IDP requires the definition of an imputation in this model. If we choose an egalitarian distribution, we can define the shares of the imputation as fractions of the total payoff equally divided by the number of players, i.e.,

The case we are taking into account is the first one in the previous section, i.e.,

, where constant

. Furthermore, the exponential c.d.f. at hand has a relevant property: since

, the ratio

, hence Equation (

8) for IDP takes the form:

Evaluating

at the optimal controls and states amount to:

By employing

in

, we can determine the expression of the expected integral payoff of company

i for a subgame starting at

:

Subsequently, we have to determine

, by a simple differentiation:

Finally, employing the found forms for

and

, we get:

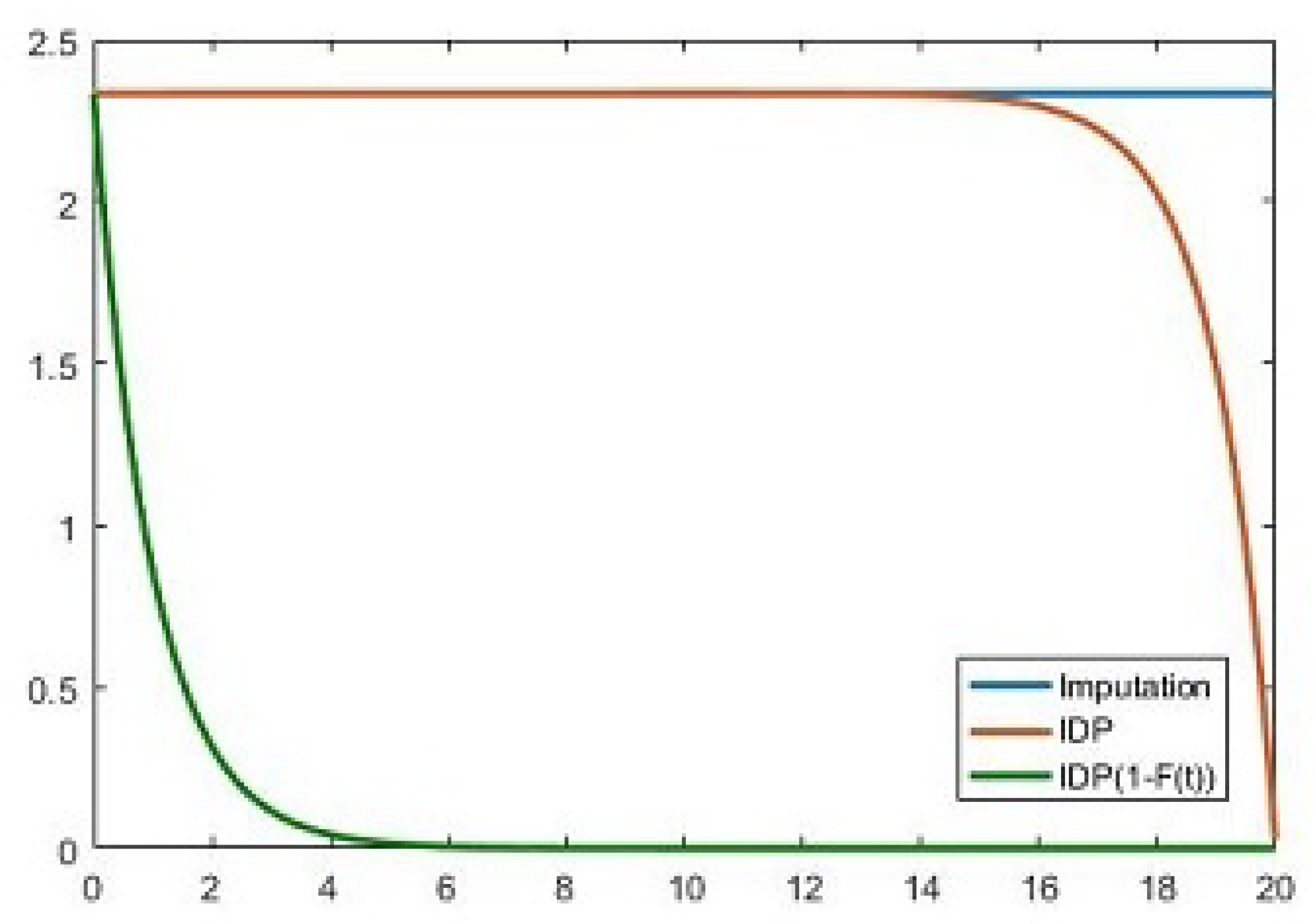

Figure 5, which was created with Matlab R2016a, portrays a sketch of the behavior of the imputation and of the IDP over time. The numerical simulation was performed for the following parameters:

,

,

,

,

, and

.

On this figure, we can see that the amount of imputation is equal to the integral of IDP multiplied by discount probability factor.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}