An Efficient Localized RBF-FD Method to Simulate the Heston–Hull–White PDE in Finance

Abstract

1. Introduction

2. Mesh Generation

3. Constructing the RBF-FD Weights

- In fact, the weights we obtained by now are used in an initial step by considering three points of the stencil. Each time, three interior points of the stencil are considered (in a loop), and the weights are computed.

- These values along with the weights corresponding to the first and last nodes are grouped together in a matrix, which we call the differentiation matrix in the next section.

- Note that after computing the matrices, the final matrix will not be changed during the time stepping process, as we discuss in the next section as well.

- The computed weights change only when the three adjacent nodes of the stencil or their spacings (h or w) change.

4. Numerical Method

5. Stability

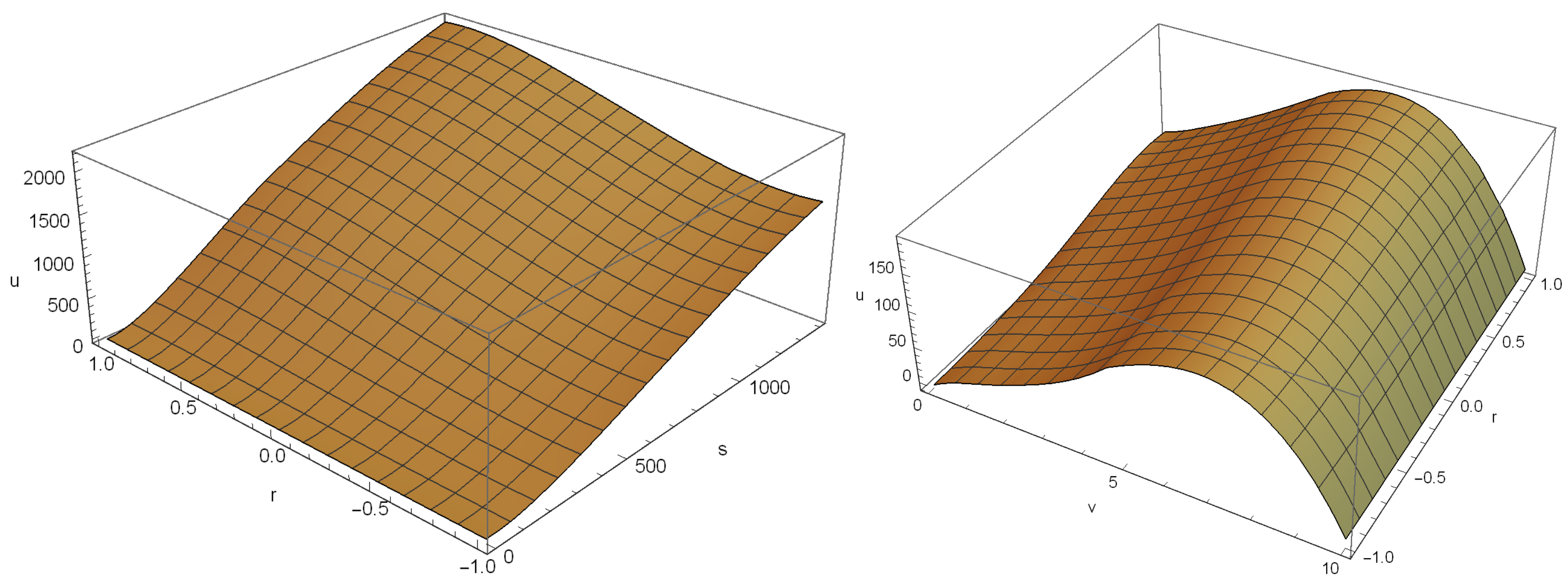

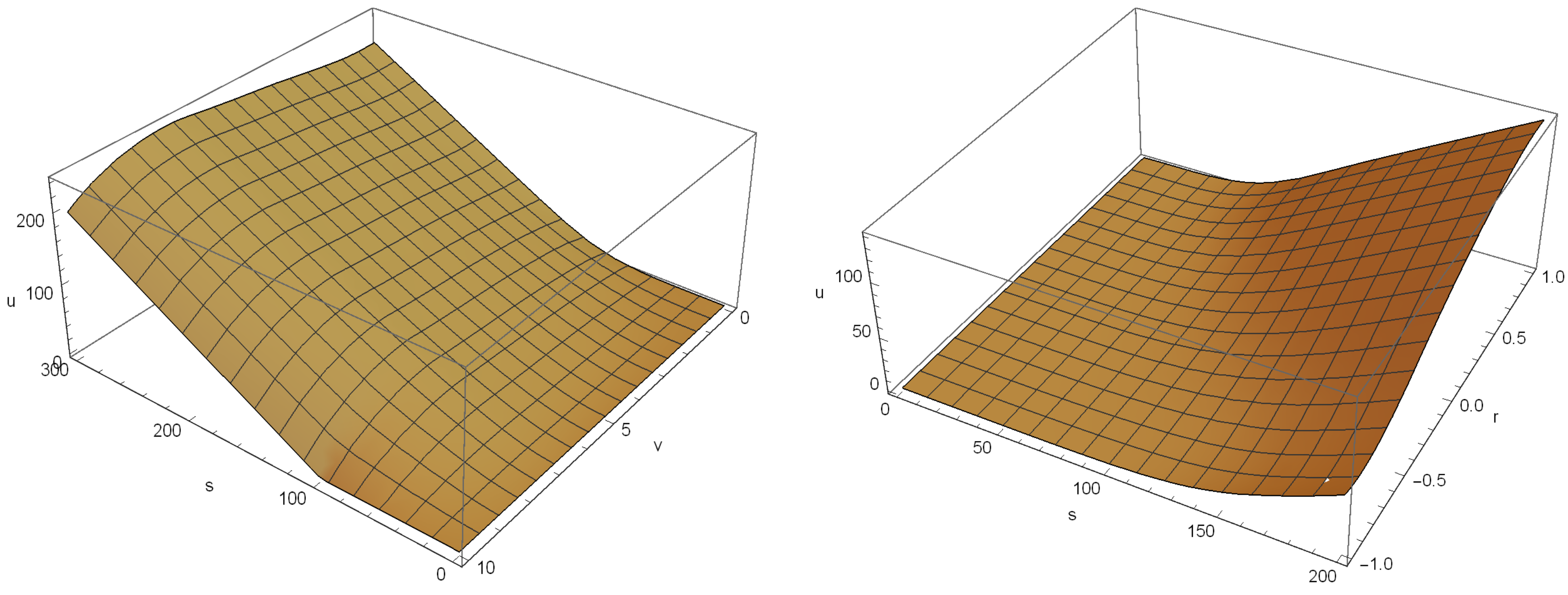

6. Simulation Results

- The second-order FD method with uniform node distribution along space and the explicit first-order Euler’s method shown by FD, see e.g., [10],

7. Summary

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Heston, S.L. A closed-form solution for options with stochastic volatility with applications to bond and currency options. Rev. Financ. Stud. 1993, 6, 327–343. [Google Scholar] [CrossRef]

- Adhikari, R. Foundations of Computational Finance. Math. J. 2020, 22, 1–59. [Google Scholar] [CrossRef]

- Cox, J.C.; Ingersoll, J.E.; Ross, S.A. A theory of the term structure of interest rates. Econometrica 1985, 53, 385–407. [Google Scholar] [CrossRef]

- Hull, J.; White, A. Using Hull-White interest rate trees. J. Deriv. 1996, 4, 26–36. [Google Scholar] [CrossRef]

- Cao, J.; Lian, G.; Roslan, T.R.N. Pricing variance swaps under stochastic volatility and stochastic interest rate. Appl. Math. Comput. 2016, 277, 72–81. [Google Scholar] [CrossRef]

- Hull, J.; White, A. The general Hull-White model and supercalibration. Financ. Anal. J. 2001, 57, 34–43. [Google Scholar] [CrossRef]

- Stein, J.C.; Stein, E.M. Stock price distributions with stochastic volatility: An analytic approach. Rev. Financ. Stud. 1991, 4, 727–752. [Google Scholar] [CrossRef]

- Djeutcha, E.; Aime Fono, L. Pricing for options in a Hull-White-Vasicek volatility and interest rate model. Appl. Math. Sci. 2021, 15, 377–384. [Google Scholar] [CrossRef]

- Grzelak, L.A.; Oosterlee, C.W. On the Heston model with stochastic interest rates. SIAM J. Financ. Math. 2011, 2, 255–286. [Google Scholar] [CrossRef]

- Ullah, M.Z. Numerical solution of Heston-Hull-White three-dimensional PDE with a high order FD scheme. Mathematics 2019, 7, 704. [Google Scholar] [CrossRef]

- Wong, H.Y.; Zhao, J. An artificial boundary method for the Hull-White model of American interest rate derivatives. Appl. Math. Comput. 2011, 217, 4627–4643. [Google Scholar] [CrossRef]

- Fornberg, B. A Practical Guide to Pseudospectral Methods; Cambridge University Press: Cambridge, UK, 1996. [Google Scholar]

- Soleymani, F.; Zhu, S. On a high-order Gaussian radial basis function generated Hermite finite difference method and its application. Calcolo 2021, 58, 50. [Google Scholar] [CrossRef]

- Kadalbajoo, M.K.; Kumar, A.; Pati Tripathi, L. Application of the local radial basis function-based finite difference method for pricing American options. Int. J. Comput. Math. 2015, 92, 1608–1624. [Google Scholar] [CrossRef]

- Yousuf, M.; Khaliq, A.Q.M. Partial differential integral equation model for pricing American option under multi state regime switching with jumps. Numer. Meth. Part. Diff. Equ. 2023, 39, 890–912. [Google Scholar] [CrossRef]

- Milovanović, S.; von Sydow, L. Radial basis function generated finite differences for option pricing problems. Comput. Math. Appl. 2018, 75, 1462–1481. [Google Scholar] [CrossRef]

- Milovanović, S.; von Sydow, L. A high order method for pricing of financial derivatives using radial basis function generated finite differences. Math. Comput. Simul. 2020, 174, 205–217. [Google Scholar] [CrossRef]

- Soleymani, F. Finding an efficient machine learning predictor for lesser liquid credit default swaps in equity markets. Iran. J. Numer. Anal. Optim. 2023, 13, 19–38. [Google Scholar]

- Kluge, T. Pricing Derivatives in Stochastic Volatility Models Using the Finite Difference Method. Ph.D. Thesis, TU Chemnitz, Chemnitz, Germany, 2002. [Google Scholar]

- Soleymani, F.; Saray, B.N. Pricing the financial Heston-Hull-White model with arbitrary correlation factors via an adaptive FDM. Comput. Math. Appl. 2019, 77, 1107–1123. [Google Scholar] [CrossRef]

- Haentjens, T.; in’t Hout, K.J. Alternating direction implicit finite difference schemes for the Heston-Hull-White partial differential equation. J. Comput. Financ. 2012, 16, 83–110. [Google Scholar] [CrossRef]

- Fasshauer, G.E. Meshfree Approximation Methods with MATLAB; World Scientific Publishing Co.: Singapore, 2007. [Google Scholar]

- Rahimi, A.; Shivanian, E.; Abbasbandy, S. Analysis of new RBF-FD weights, calculated based on inverse quadratic functions. J. Math. 2022, 2022, 3718132. [Google Scholar] [CrossRef]

- Soleymani, F. An efficient numerical scheme for the solution of a stochastic volatility model including contemporaneous jumps in finance. Int. J. Comput. Methods 2022, 19, 2141021. [Google Scholar] [CrossRef]

- Platte, R.B. How fast do radial basis function interpolants of analytic functions converge? IMA J. Numer. Anal. 2011, 31, 1578–1597. [Google Scholar] [CrossRef]

- Wright, G.B.; Fornberg, B. Scattered node compact finite difference-type formulas generated from radial basis functions. J. Comput. Phys. 2006, 212, 99–123. [Google Scholar] [CrossRef]

- Knapp, R. A method of lines framework in Mathematica. J. Numer. Anal. Indust. Appl. Math. 2008, 3, 43–59. [Google Scholar]

- Meyer, G.H. The Time-Discrete Method of Lines for Options and Bonds: A PDE Approach; World Scientific Publishing: Hackensack, NJ, USA, 2015. [Google Scholar]

- Soleymani, F.; Akgül, A.; Karatas Akgül, E. On an improved computational solution for the 3D HCIR PDE in finance. An. Stiintifice Ale Univ. Ovidius Constanta—Ser. Mat. 2019, 27, 207–230. [Google Scholar] [CrossRef]

- Sofroniou, M.; Knapp, R. Advanced Numerical Differential Equation Solving in Mathematica; Wolfram Mathematica, Tutorial Collection: Champaign, IL, USA, 2008. [Google Scholar]

- Butcher, J.C. Numerical Methods for Ordinary Differential Equations, 2nd ed.; Wiley: Oxford, UK, 2008. [Google Scholar]

- Wellin, P.R.; Gaylord, R.J.; Kamin, S.N. An Introduction to Programming with Mathematica; Cambridge University Press: Cambridge, UK, 2005. [Google Scholar]

- Schöbel, R.; Zhu, J. Stochasic volatility with an Ornstein-Uhlenbeck process: An extension. Eur. Financ. Rev. 1999, 3, 23–46. [Google Scholar] [CrossRef]

- Grzelak, L.A.; Oosterlee, C.W.; Van Weeren, S. Extension of stochastic volatility equity models with the Hull-White interest rate process. Quant. Finance 2012, 12, 89–105. [Google Scholar] [CrossRef]

- van Haastrecht, A.; Lord, R.; Pelsser, A.; Schrager, D. Pricing long-maturity equity and FX derivatives with stochastic interest rates and stochastic volatility. Insur. Math. Econ. 2009, 45, 436–448. [Google Scholar] [CrossRef]

- Guo, S.; Grzelak, L.; Oosterlee, C.W. Analysis of an affine version of the Heston-Hull-White option pricing partial differential equation. Appl. Numer. Math. 2013, 72, 143–159. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Solver | m | n | o | N | Time | |||

|---|---|---|---|---|---|---|---|---|

| FD | ||||||||

| 10 | 8 | 6 | 480 | 0.002 | 25.492 | 5.7 | 0.47 | |

| 14 | 10 | 10 | 1400 | 0.001 | 11.098 | 3.1 | 0.79 | |

| 18 | 12 | 12 | 2592 | 0.0005 | 17.203 | 6.3 | 1.31 | |

| 24 | 14 | 14 | 4704 | 0.00025 | 18.731 | 1.5 | 3.67 | |

| 28 | 16 | 16 | 7168 | 0.0002 | 13.329 | 1.7 | 7.26 | |

| 45 | 22 | 22 | 21,780 | 0.00005 | 14.636 | 9.4 | 72.65 | |

| HM | ||||||||

| 10 | 8 | 6 | 480 | 0.001 | 14.472 | 1.0 | 0.56 | |

| 14 | 10 | 10 | 1400 | 0.0005 | 15.300 | 5.3 | 1.03 | |

| 18 | 12 | 12 | 2592 | 0.00025 | 15.615 | 3.4 | 2.76 | |

| 24 | 14 | 14 | 4704 | 0.0001 | 15.806 | 2.2 | 9.64 | |

| 28 | 16 | 16 | 7168 | 0.0001 | 15.871 | 1.8 | 12.69 | |

| 50 | 22 | 22 | 24,200 | 0.000025 | 16.006 | 5.9 | 188.58 | |

| RBF-FDM | ||||||||

| 10 | 8 | 6 | 480 | 0.004 | 15.237 | 5.8 | 0.75 | |

| 14 | 10 | 10 | 1400 | 0.0025 | 16.002 | 1.0 | 1.31 | |

| 18 | 12 | 12 | 2592 | 0.002 | 16.029 | 9.0 | 3.26 | |

| 24 | 14 | 14 | 4704 | 0.0005 | 16.292 | 7.1 | 7.49 | |

| 28 | 16 | 16 | 7168 | 0.0004 | 16.246 | 4.3 | 11.29 | |

| 50 | 22 | 22 | 24,200 | 0.0002 | 16.191 | 9.2 | 123.47 |

| Solver | m | n | o | N | Time | |||

|---|---|---|---|---|---|---|---|---|

| 20 | 10 | 10 | 2000 | 0.00025 | 22.022 | 4.9 | 1.89 | |

| 24 | 12 | 12 | 3456 | 0.0002 | 21.436 | 2.1 | 4.12 | |

| 26 | 14 | 14 | 5096 | 0.0001 | 19.678 | 6.1 | 9.69 | |

| 28 | 16 | 16 | 7168 | 0.0001 | 17.376 | 1.7 | 12.59 | |

| 30 | 18 | 18 | 9720 | 0.00005 | 17.404 | 1.7 | 37.65 | |

| 36 | 20 | 20 | 14,400 | 0.000025 | 20.510 | 2.2 | 109.47 | |

| 38 | 22 | 22 | 18,392 | 0.000025 | 20.275 | 3.3 | 164.28 | |

| 42 | 22 | 22 | 20,328 | 0.00002 | 18.370 | 1.2 | 231.74 | |

| HM | ||||||||

| 20 | 10 | 10 | 2000 | 0.00025 | 20.631 | 1.6 | 2.14 | |

| 24 | 12 | 12 | 3456 | 0.0002 | 20.709 | 1.2 | 4.31 | |

| 26 | 14 | 14 | 5096 | 0.0001 | 20.729 | 1.1 | 9.17 | |

| 28 | 16 | 16 | 7168 | 0.0001 | 20.748 | 1.0 | 13.65 | |

| 30 | 18 | 18 | 9720 | 0.00005 | 20.767 | 9.9 | 38.12 | |

| 36 | 20 | 20 | 14,400 | 0.000025 | 20.810 | 7.8 | 110.92 | |

| 38 | 22 | 22 | 18,392 | 0.000025 | 20.818 | 7.5 | 170.31 | |

| 42 | 22 | 22 | 20,328 | 0.00002 | 20.833 | 6.7 | 253.64 | |

| RBF-FDM | ||||||||

| 20 | 10 | 10 | 2000 | 0.004 | 20.859, | 6.4 | 2.54 | |

| 24 | 12 | 12 | 3456 | 0.002 | 20.901, | 4.4 | 5.01 | |

| 26 | 14 | 14 | 5096 | 0.001 | 20.931, | 3.0 | 7.58 | |

| 28 | 16 | 16 | 7168 | 0.0005 | 20.943, | 2.4 | 14.69 | |

| 30 | 18 | 18 | 9720 | 0.0004 | 20.956, | 1.8 | 37.61 | |

| 36 | 20 | 20 | 14,400 | 0.0002 | 20.967, | 1.2 | 103.91 | |

| 38 | 22 | 22 | 18,392 | 0.0001 | 20.980, | 6.6 | 172.66 | |

| 42 | 22 | 22 | 20,328 | 0.00005 | 20.982 | 5.7 | 259.37 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Liu, T.; Ullah, M.Z.; Shateyi, S.; Liu, C.; Yang, Y. An Efficient Localized RBF-FD Method to Simulate the Heston–Hull–White PDE in Finance. Mathematics 2023, 11, 833. https://doi.org/10.3390/math11040833

Liu T, Ullah MZ, Shateyi S, Liu C, Yang Y. An Efficient Localized RBF-FD Method to Simulate the Heston–Hull–White PDE in Finance. Mathematics. 2023; 11(4):833. https://doi.org/10.3390/math11040833

Chicago/Turabian StyleLiu, Tao, Malik Zaka Ullah, Stanford Shateyi, Chao Liu, and Yanxiong Yang. 2023. "An Efficient Localized RBF-FD Method to Simulate the Heston–Hull–White PDE in Finance" Mathematics 11, no. 4: 833. https://doi.org/10.3390/math11040833

APA StyleLiu, T., Ullah, M. Z., Shateyi, S., Liu, C., & Yang, Y. (2023). An Efficient Localized RBF-FD Method to Simulate the Heston–Hull–White PDE in Finance. Mathematics, 11(4), 833. https://doi.org/10.3390/math11040833