2.1. Stochastic Dynamic Mortality Modeling and Life Expectancy

In the reform of social security systems in developed countries, the life expectancy of the population is an important reference factor in delaying the mandatory retirement age. The life table approach to estimating future life expectancy using historical mortality rates may lead to an underestimation of pension expenditure. In contrast, stochastic dynamic mortality models can portray the time-varying and stochastic nature of population mortality changes and can more accurately predict future life expectancy. Currently, there are a variety of classical stochastic mortality models. Wang and Lu [

9] showed that the CBD mortality model [

10,

11,

12] is more suitable for capturing the dynamic and uncertainty of China’s population mortality model than the Lee Carter model and Bayesian hierarchical model. Thus, this paper employed the CBD mortality model to predict the life expectancy of the population. The specific form of the function is as follows:

where

is the probability of dying within one year for a person

years old living in

period. The survival probability is represented by

.

and

denote two stochastic processes, in which

represents the mortality improvement over time for all ages, and

represents that the mortality rate improves less in the older age group than in the younger age group.

is the sample age mean, derived from the age-weighted average of the ages in the sample, where the weight of each age is the proportion of the population of that age in the total population.

. The CBD model does not suffer from variable identification problems and, therefore, does not need to add any constraints. We used Farlle’s method to calculate the probability of death, which corresponds to a life expectancy of:

where

is the remaining lifetime of an individual with age

at time

, and

is the maximum lifespan.

2.4. The Income and Expenditure of the Pension Insurance Fund

The employees’ pension fund in China consists of two parts: the integrated account and the individual account. In terms of ownership, the former is a public pension and the latter is a private pension. In terms of sources of funding, the integrated account is financed by enterprises’ contributions to pension insurance premiums based on a certain percentage of the employee’s salary, while the individual account is financed by a certain percentage of the employee’s salary. In terms of financial systems, the integrated account adopts a pay-as-you-go financial system, while the individual account adopts a fund accumulation system. In terms of liability, the integrated account adopts a defined benefit (DB), while the individual account adopts a defined contribution (DC). Retired workers receive a pension that consists of a basic pension from the integrated account plus a pension from the individual account. However, due to disorganized management, individual accounts have been diverted to the payment of pensions from the integrated account. Individual accounts have essentially become notional accounts.

The income part of the integrated account depends on the statutory contribution base, enterprise contribution rate, number of insured persons, and actual collection rate. The income part of the individual account depends on the statutory contribution base, individual contribution rate, number of insured persons, and actual collection rate. Let

be the income of the integrated account under retirement scheme

with retirement age

. Let

be the income of an individual account under a retirement scheme with retirement age

. The specific formulas are as follows:

where

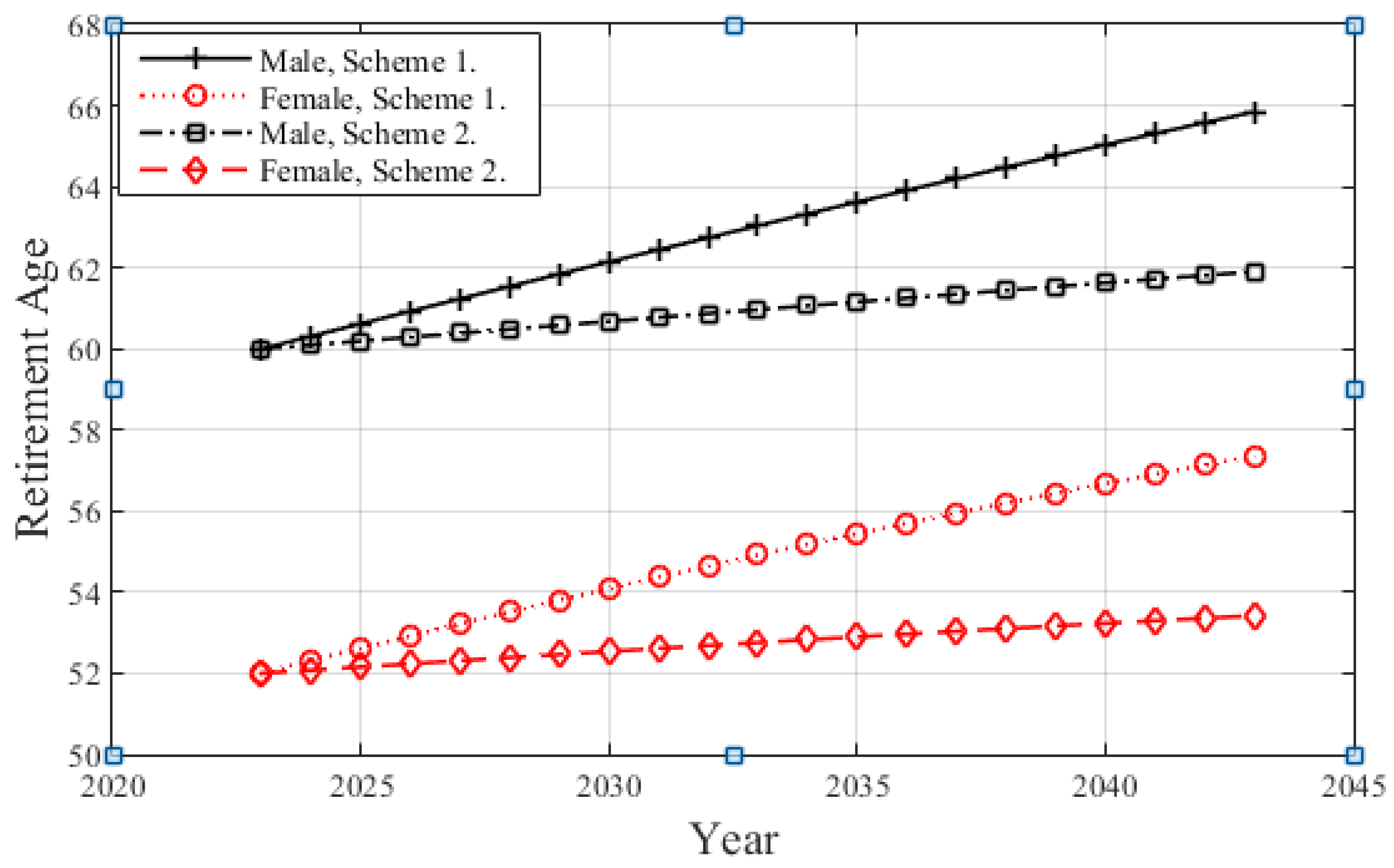

represents the scheme with a fixed retirement residual life, and

represents the scheme with a fixed life burden rate.

is the statutory contribution rate for enterprises,

is the statutory contribution rate for individuals,

is the urban employment rate,

is the participation rate of urban active workers,

is the proportion of insured workers in enterprises to insured workers,

is the actual contribution rate, and

(

t) is the statutory contribution base of a salary.

The total income of the pension fund of employees is:

In 1997, the government carried out a reform of the pension insurance system, establishing a unified basic pension insurance system for enterprise employees. Prior to the reform, employees were not required to pay pension insurance premiums, and the company or the government would pay their pensions after retirement. After the reform, enterprise employees were required to bear pension insurance premiums. Therefore, the government categorizes employees who participate in pension insurance into “old people”, “middle people”, and “new people”. The “old people” are those who retired before 1997. The “new people” are those who joined the workforce after 1997. The “middle people” are those who joined the workforce before 1997 and retired after 1997. Pensions are paid by the pension fund in different ways for different types of retirees. The expenses of an integrated pension insurance account consist of the basic pension for “new people”, the basic pension and transitional pension for “middle people”, and the basic pension for “old people”. Individual account expenses consist of “newcomer” individual account pension expenses and “middle-aged” individual account pension expenses. We established the actuarial model of pension fund expenditure.

The pension benefits for “new people” include a basic pension from the integrated account and a pension from the individual account. Therefore, the expenditure of the pension fund, which is used to pay the pensions of “new people”, also includes two corresponding parts.

The expenditure of “new people” for the integrated account,

, is as follows:

where

where

is the employment rate for “new people”

is the participation rate of urban retirees for “new people”

is basic pension expenditure for “new people”;

is the annual pension growth rate;

is the actual contribution salary of the insured person;

is the index of the average contribution salary of the participant;

is the index of contributions; and

is the actual average contribution index, and

.

Let

be the expenditure on the individual account of the “new people” under retirement age

:

where

is the amount of individual accounts by gender,

,

is the interest rate of individual account bookings for the year, and

is the number of months of payment by gender

.

The expenditure of “middle people” is more complex, comprising the expenditure on the integrated account and the expenditure on the individual account. Let

be the expenditure of the integrated account for “middle people”:

where

is the basic pension for “middle people”, is the transitional pension of “middle person”, and is the transition coefficient.

Let

be the individual account expenditure of “middle people”; then:

The pensions of “old people” are paid according to the original policy. Let

be the basic pension expenditure for “old people” with a retirement age of

; then:

where

,

denotes the basic pension expenditure of the “old people” denotes the growth rate of retiree pensions with age, denotes the replacement rate of pensions for urban enterprise workers in 2007, and denotes the growth rate of wages before retirement.

The total expenditure of pension fund

is:

The balance of the pension insurance fund,

, is as follows:

2.5. The Pension Wealth of Employees

Regarding delaying the retirement age, employees are worried about whether delaying the retirement age will lead to a reduction in pension benefits during the whole retirement period. The total pension benefit of retirees comprises the discounted sum of pension benefits received during the whole retirement period, which is defined as pension wealth. According to the policy of pensions, the pension received by retirees is equal to the basic pension from the integrated account plus the individual pension from the individual account. The individual account pension at each month is calculated using the accumulated savings amount of the individual account divided by the number of months of accrual corresponding to the retirement age. To assess the impact of delaying the retirement age on the pension benefits of retirees, we constructed a gain-and-loss index for pension wealth as follows. Let

be the gender-specific pension benefit at the first year of retirement.

denotes the gender-specific pension wealth, which is the sum of the present value of the pension benefits at retirement:

where

is the average growth rate of wages before retirement,

denotes the growth rate of pensions, and

is the interest rate.

Let

be the pensions paid by individual accounts in the first year after retirement.

denotes the accumulated wealth from an individual account pension:

Therefore, the pension wealth,

, under delay retirement scheme

is:

Then, the gain/loss coefficient of pension wealth,

, for delaying retirement age schemes is as follows:

where

is the pension wealth under the constant retirement age

(present retirement age). When

, it indicates that delayed retirement age leads to a reduction in employee pension wealth, and there is a negative incentive for delayed retirement. When

, it indicates that delayed retirement age increases employee pension wealth and has positive incentives for delayed retirement.

Moreover, delaying the retirement age may have positive and negative effects on employee pension wealth. The employee’s pension wealth mainly depends on the initial pension entitlement (i.e., pension benefit at the first year of retirement) and the time length of the pension receipt. According to China’s policy, the initial pension entitlement has a positive relationship with the time length of the contribution. Delaying the retirement age will increase the time length of the contribution, further increase the initial pension entitlement and have a positive effect on the employee’s pension wealth. At the same time, the change in the time length of receiving pension benefits depends on the speed of delaying the retirement age and the growth rate of life expectancy. When the speed of delaying the retirement age is greater than the growth rate of life expectancy, the length of receiving pension benefits decreases over time, and there is a negative effect of delaying the retirement age on employee pension wealth, and vice versa. If the retirement age is delayed too quickly, it will have a negative impact through a reduction in the time length of receiving pension benefits, and when the intensity of this negative impact is greater than the intensity of the positive impact through an increase in the initial pension entitlement, it will produce a negative net impact on employee pension wealth. It follows that there is a certain threshold value for the speed of delaying the retirement age, below which delaying the retirement age increases the level of pension wealth. This threshold value for the speed of retirement age delay depends on the growth rate of life expectancy.

{kind=link}