Projection and Contraction Method for Pricing American Bond Options

Abstract

:1. Introduction

2. Mathematics Model

2.1. Linear Complementary Problem

- (1)

- The corresponding solution region of this model is an unbounded region;

- (2)

- The problem is complex and nonlinear, which is difficult to solved efficiently.

2.2. Simplified Model

3. Numerical Algorithm

3.1. Finite Difference Method

3.2. Numerical Method

| Algorithm 1. Projected Contraction Method |

| For set , ., . ) • , , , , , , ; • While () , update ; end • , , , , ; • If ; end • set and end end |

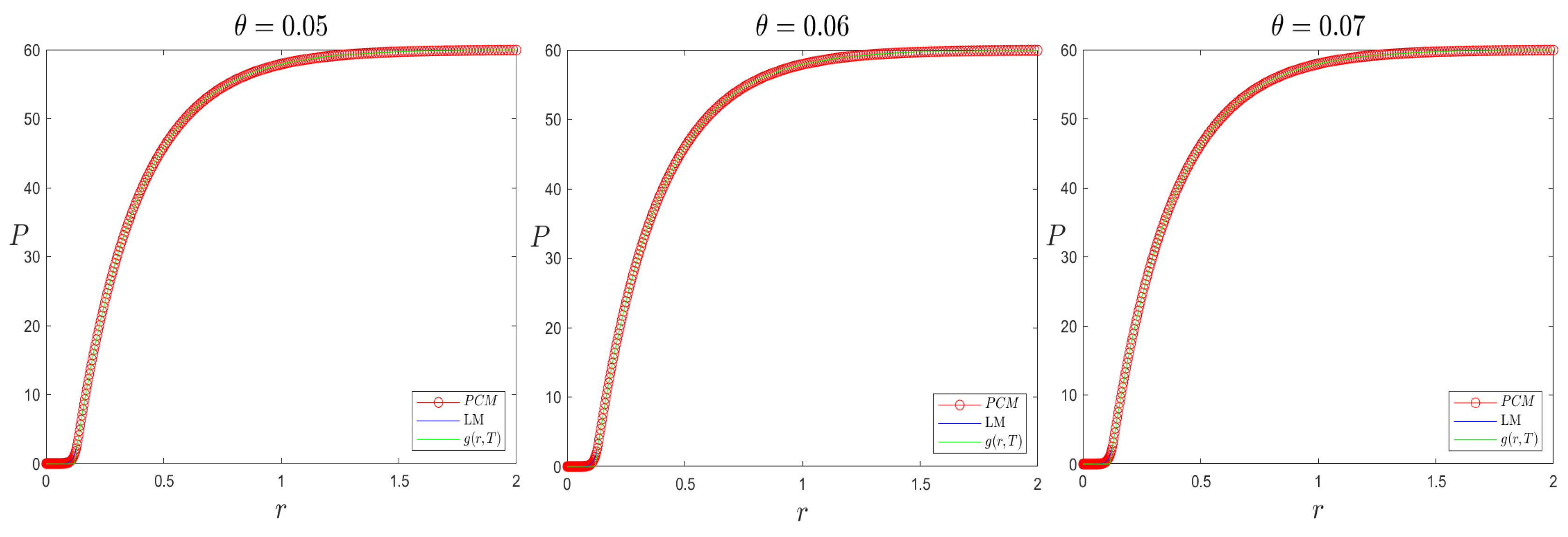

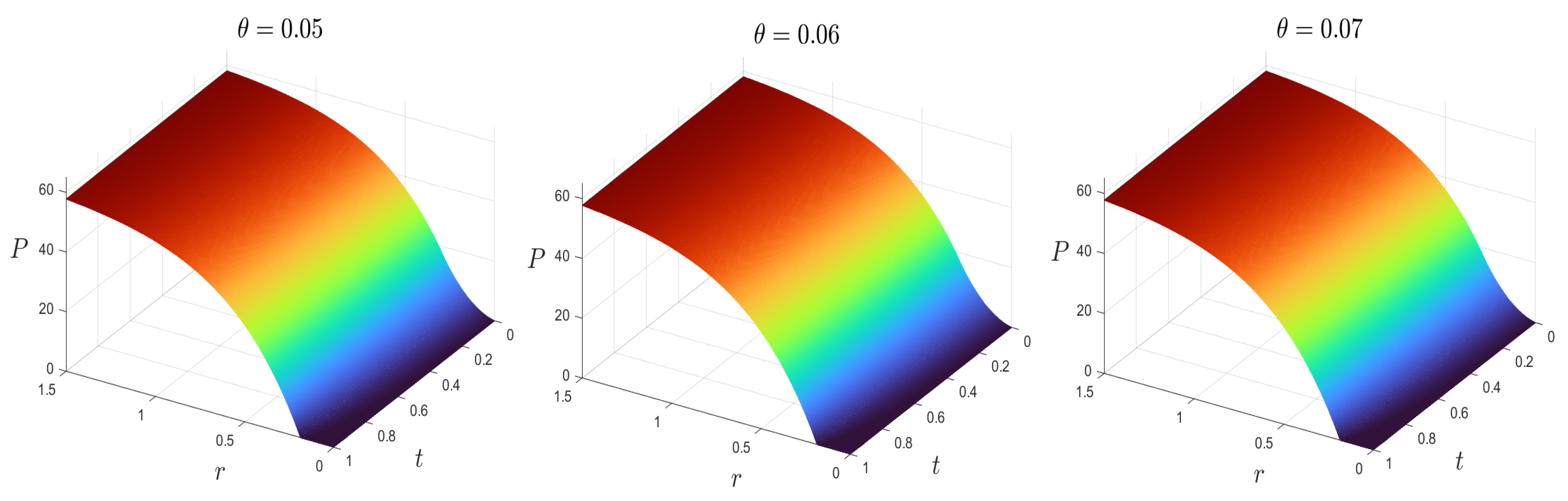

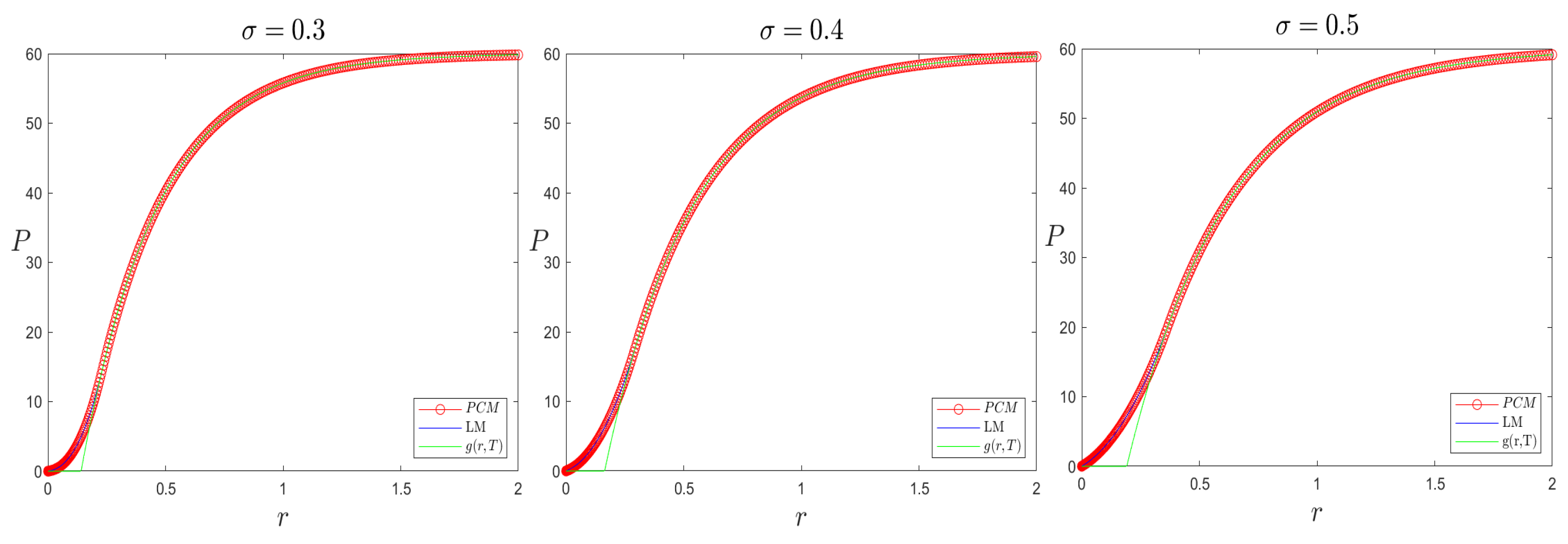

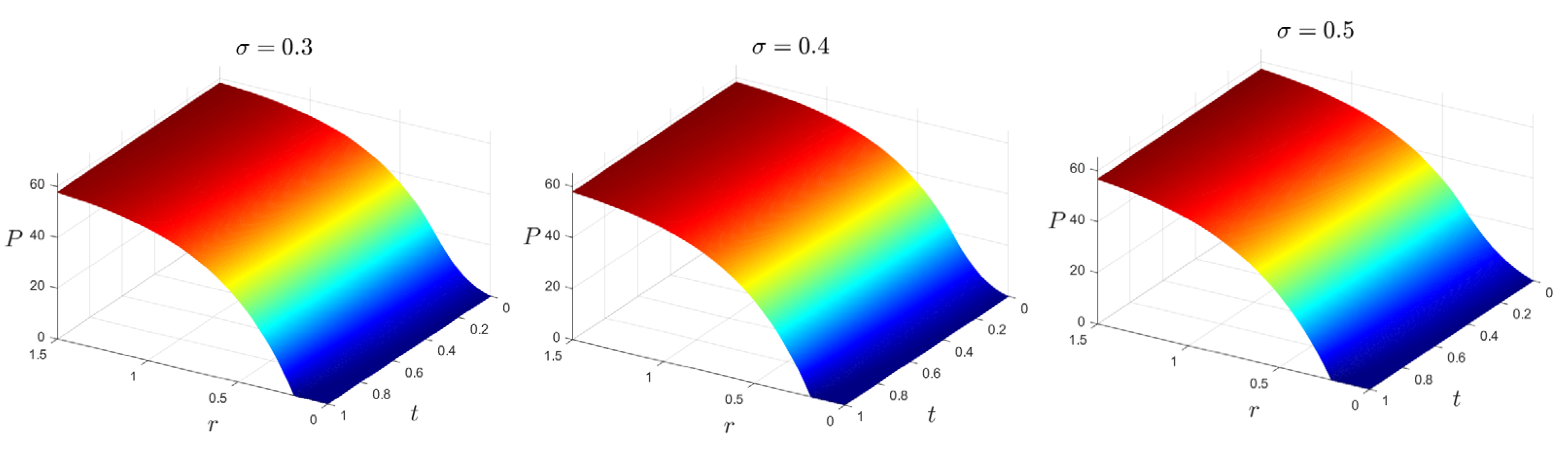

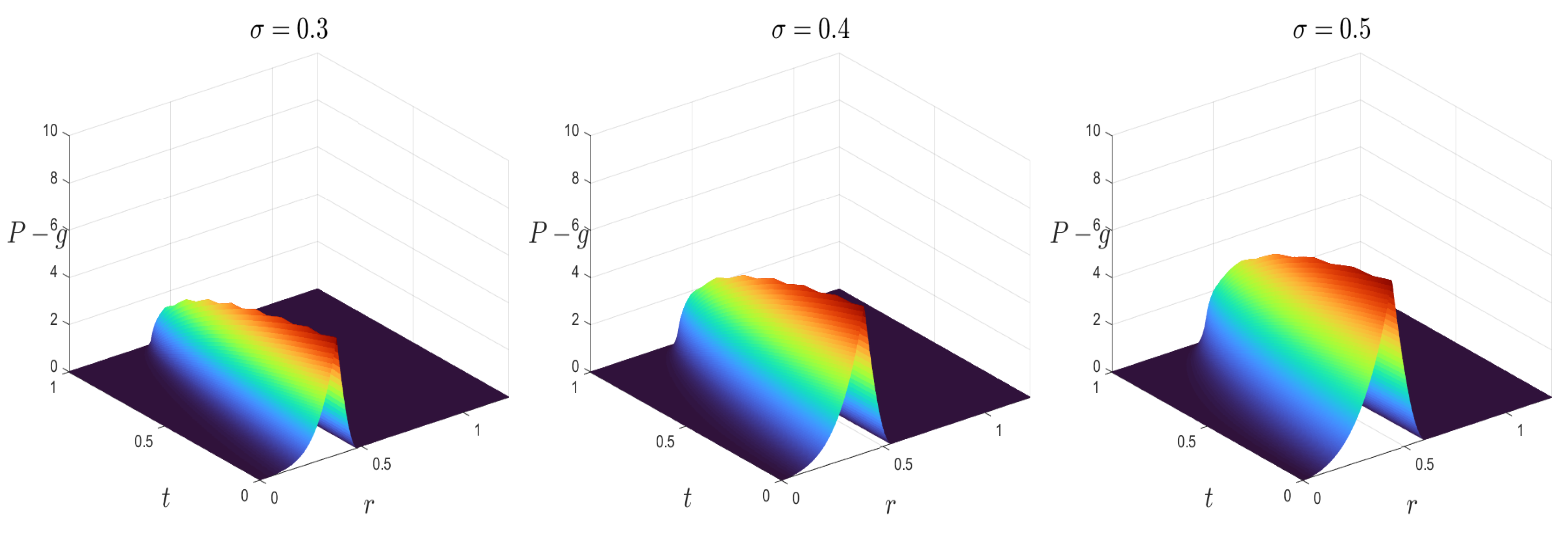

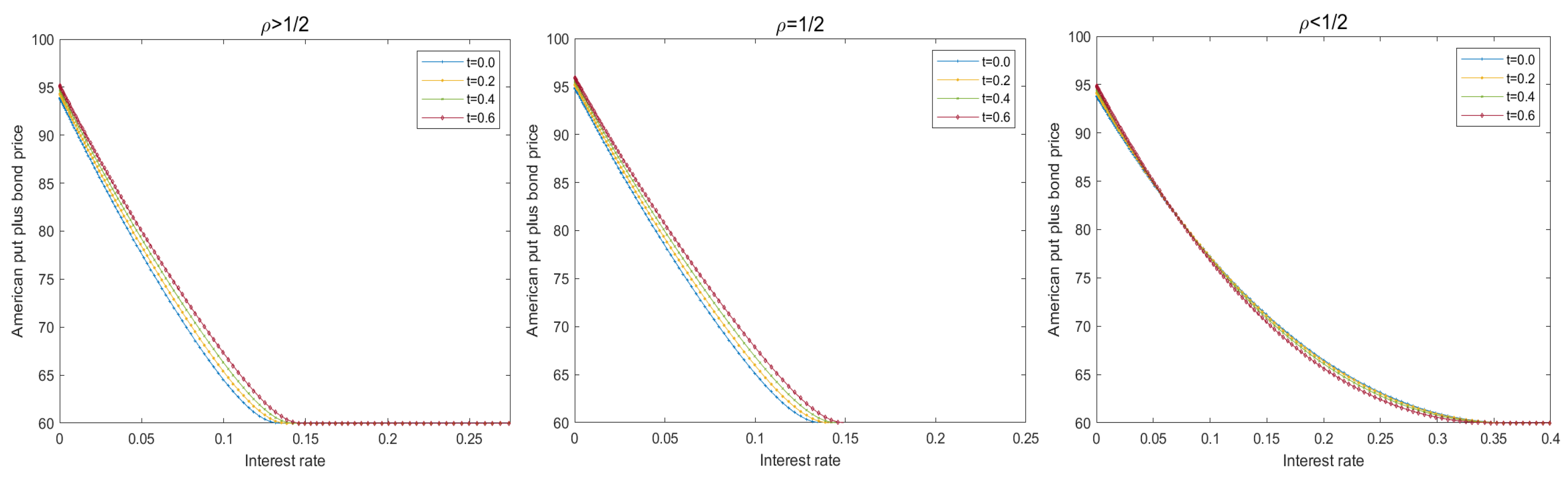

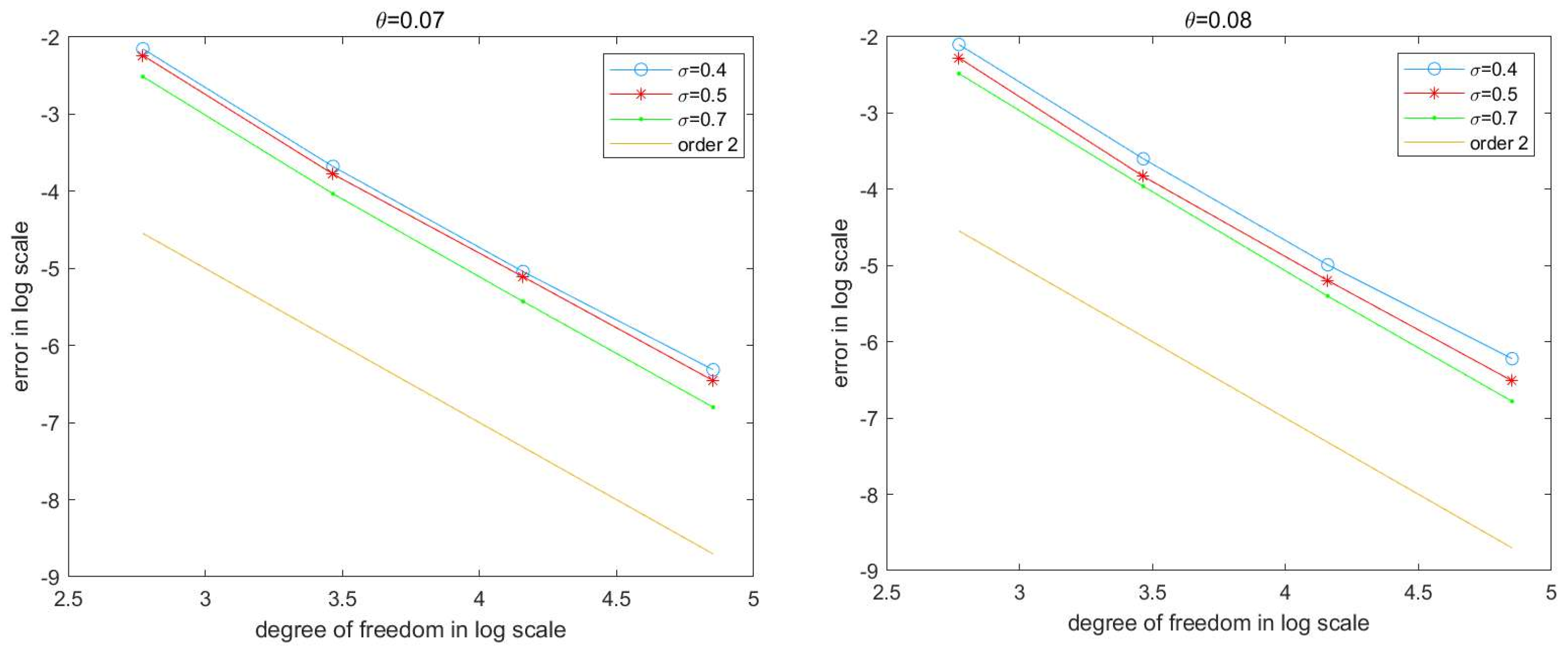

4. Numerical Simulation

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Zaevski, T.S. Pricing discounted American capped options. Chaos Solitons Fractals 2022, 156, 111833. [Google Scholar] [CrossRef]

- Zaevski, T.S. Pricing cancellable American put options on the finite time horizon. J. Futures Mark. 2022, 42, 1284–1303. [Google Scholar] [CrossRef]

- Kifer, Y. Game options. Financ. Stoch. 2000, 4, 443–463. [Google Scholar] [CrossRef]

- Zaevski, T. Perpetual cancellable American options with convertible features. Mod. Stoch. Theory Appl. 2023, 10, 367–395. [Google Scholar] [CrossRef]

- Chuang, C. Valuation of perpetual strangles: A quasi-analytical approach. J. Deriv. 2013, 21, 64–72. [Google Scholar] [CrossRef]

- Repplinger, D. Pricing of Bond Options: Unspanned Stochastic Volatility and Random Field Models; Springer Science & Business Media: Berlin/Heidelberg, Germany, 2008. [Google Scholar]

- Deng, Z.C.; Yu, J.N.; Yang, L. An inverse problem arisen in the zero-coupon bond pricing. Nonlinear Anal. Real World Appl. 2010, 11, 1278–1288. [Google Scholar] [CrossRef]

- Black, F.; Scholes, M. The pricing of options and corporate liabilities. J. Political Econ. 1973, 81, 637–654. [Google Scholar] [CrossRef]

- Magnou, G.; Mordecki, E.; Sosa, A. Pricing bond options in emerging markets: A case study. J. Dyn. Games Am. Inst. Math. Sci. 2018, 51, 21–30. [Google Scholar] [CrossRef]

- Bekaert, G.; Engstrom, E.; Ermolov, A. Macro risks and the term structure of interest rates. J. Financ. Econ. 2021, 141, 479–504. [Google Scholar] [CrossRef]

- Wang, X.; Xie, D.; Jiang, J.; Wu, X.; He, J. Value-at-Risk estimation with stochastic interest rate models for option-bond portfolios. Financ. Res. Lett. 2017, 21, 10–20. [Google Scholar] [CrossRef]

- Merton, R.C. On the pricing of corporate debt: The risk structure of interest rates. J. Financ. 1974, 29, 449–470. [Google Scholar]

- Vasicek, O. An equilibrium characterization of the term structure. J. Financ. Econ. 1977, 5, 177–188. [Google Scholar] [CrossRef]

- Cox, J.C.; Ingersoll, J.E.; Ross, S.A. A Theory of the Term Structure of Interest Rates. Econometrica 1985, 53, 385–407. [Google Scholar] [CrossRef]

- Chan, K.C.; Karolyi, G.A.; Longstaff, F.A.; Sanders, A.B. An empirical comparison of alternative models of the short-term interest rate. J. Financ. 1992, 47, 1209–1227. [Google Scholar]

- Lorig, M.; Suaysom, N. Options on bonds: Implied volatilities from affine short-rate dynamics. Ann. Financ. 2022, 18, 183–216. [Google Scholar] [CrossRef]

- Tomas, M.J.; Yu, J. An Asymptotic Solution for Call Options on Zero-Coupon Bonds. Mathematics 2021, 9, 1940. [Google Scholar] [CrossRef]

- Babbel, D.F.; Merrill, C.; Zacharias, J. Teaching Interest Rate Contingent Claims Pricing. J. Financ. Educ. 1996, 22, 41–59. [Google Scholar]

- Ho, T.S.; Stapleton, R.C.; Subrahmanyam, M.G. The valuation of American options on bonds. J. Bank. Financ. 1997, 21, 1487–1513. [Google Scholar] [CrossRef]

- Yang, H. American put options on zero-coupon bonds and a parabolic free boundary problem. Int. J. Numer. Anal. Model. 2004, 1, 203–215. [Google Scholar]

- Zhang, K.; Wang, S. Pricing American bond options using a penalty method. Automatica 2012, 48, 472–479. [Google Scholar] [CrossRef]

- Hilal, K.; Serghini, A. Pricing American bond options using a cubic spline collocation method. Bol. Soc. Parana. 2014, 32, 189–208. [Google Scholar]

- Gang, X.T.; Yi, H. A New Efficient Numerical Method for Pricing American Options on Zero-coupon Bonds. J. Eng. Math. 2021, 38, 879–900. [Google Scholar]

- Chesney, M.; Elliott, R.J.; Gibson, R. Analytical solutions for the pricing of American bond and yield options. Math. Financ. 1993, 3, 277–294. [Google Scholar] [CrossRef]

- Hao, X.N. A differential method to the American bond option pricing problem. J. Taiyuan Univ. Technol. 2008, 39, 137–144. [Google Scholar]

- He, B.S. A new method for a class of linear variational inequalities. Math. Program. 1994, 66, 137–144. [Google Scholar] [CrossRef]

- Song, H.M.; Zhang, R. Projection and contraction method for the valuation of American options. East Asian J. Appl. Math. 2015, 5, 48–60. [Google Scholar] [CrossRef]

- Tian, Y.S. A reexamination of lattice procedures for interest rate-contingent claims. Adv. Futures Options Res. 1994, 7, 87–111. [Google Scholar]

- Allegretto, W.; Lin, Y.; Yang, H. Numerical pricing of American put options on zero-coupon bonds. Appl. Numer. Math. 2003, 46, 113–134. [Google Scholar] [CrossRef]

- Wilmott, P.; Howison, S.; Dewynne, J. The Mathematics of Financial Derivatives: A Student Introduction; Cambridge University Press: Cambridge, UK, 1995. [Google Scholar]

- Wang, S. A novel fitted finite volume method for the Black–Scholes equation governing option pricing. IMA J. Numer. Anal. 2004, 24, 699–720. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| LM | 46.52 | 34.81 | 27.78 |

| PCM | 0.8139 | 1.0619 | 1.2536 |

| Error | 1.4559 | 1.3267 | 1.2596 |

| 0.04 | 0.06 | 0.08 | |||||||

|---|---|---|---|---|---|---|---|---|---|

| 0.3 | 0.4 | 0.5 | 0.3 | 0.4 | 0.5 | 0.3 | 0.4 | 0.5 | |

| FFVM Error/ | 2.06 | 1.56 | 1.36 | 2.03 | 1.64 | 1.40 | 2.24 | 1.72 | 1.44 |

| PCM Error/ | 1.74 | 1.32 | 1.27 | 1.51 | 1.46 | 1.33 | 1.83 | 1.46 | 1.33 |

| FFVM Time/s | 1.27 | 1.31 | 1.36 | 1.37 | 1.28 | 1.37 | 1.17 | 1.34 | 1.41 |

| PCM Time/s | 0.81 | 1.02 | 1.30 | 0.82 | 1.02 | 1.26 | 0.80 | 1.06 | 1.31 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Zhang, Q.; Wang, Q.; Zuo, P.; Du, H.; Wu, F. Projection and Contraction Method for Pricing American Bond Options. Mathematics 2023, 11, 4689. https://doi.org/10.3390/math11224689

Zhang Q, Wang Q, Zuo P, Du H, Wu F. Projection and Contraction Method for Pricing American Bond Options. Mathematics. 2023; 11(22):4689. https://doi.org/10.3390/math11224689

Chicago/Turabian StyleZhang, Qi, Qi Wang, Ping Zuo, Hongbo Du, and Fangfang Wu. 2023. "Projection and Contraction Method for Pricing American Bond Options" Mathematics 11, no. 22: 4689. https://doi.org/10.3390/math11224689

APA StyleZhang, Q., Wang, Q., Zuo, P., Du, H., & Wu, F. (2023). Projection and Contraction Method for Pricing American Bond Options. Mathematics, 11(22), 4689. https://doi.org/10.3390/math11224689