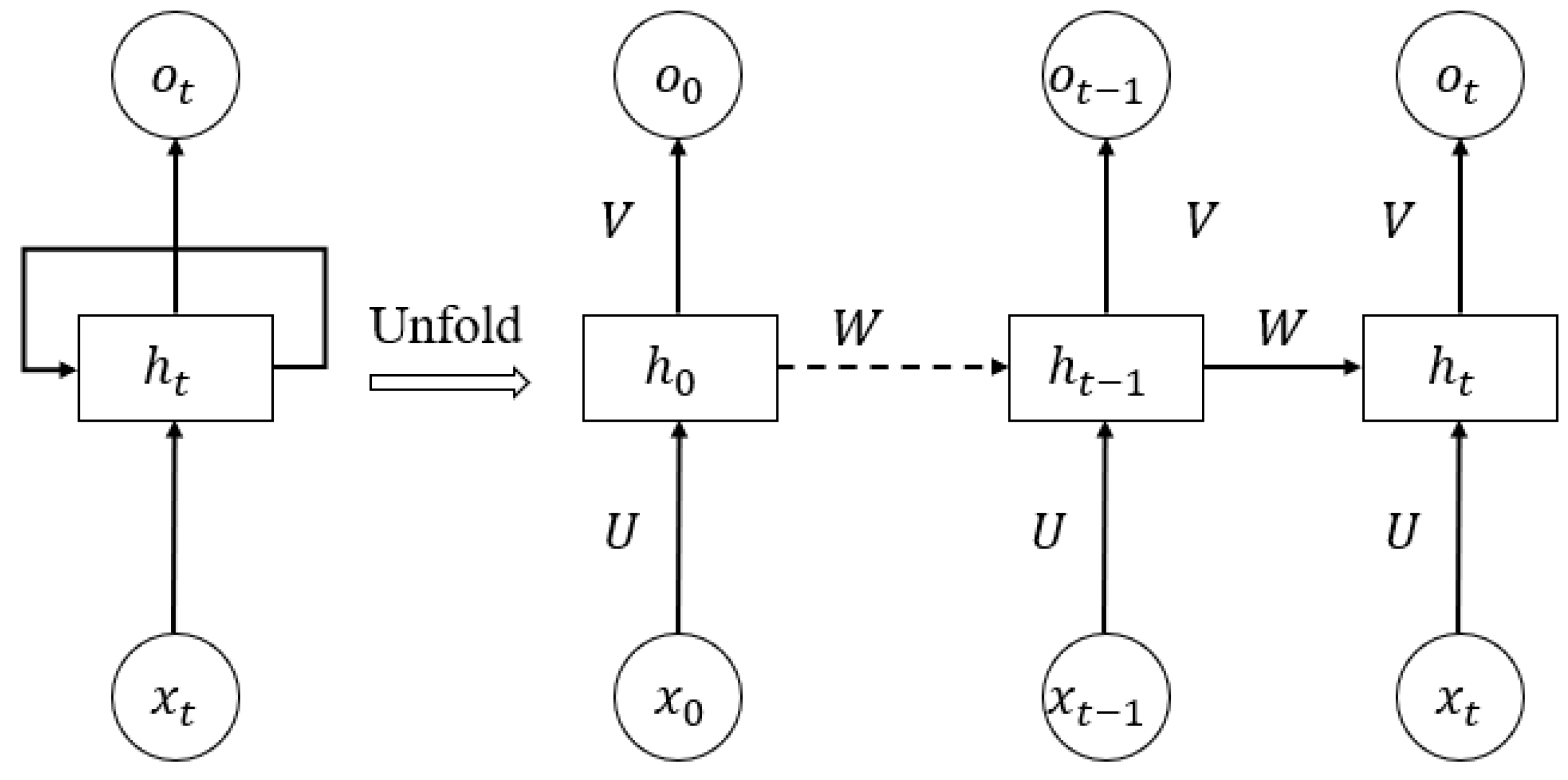

Figure 1.

The structure of a neuron of a recurrent neural network.

Figure 1.

The structure of a neuron of a recurrent neural network.

Figure 2.

The structure of neuron of LSTM.

Figure 2.

The structure of neuron of LSTM.

Figure 3.

Architecture of the LSTM model used in our paper.

Figure 3.

Architecture of the LSTM model used in our paper.

Figure 4.

The layers of LSTM model.

Figure 4.

The layers of LSTM model.

Figure 5.

The layers of the RNN model.

Figure 5.

The layers of the RNN model.

Figure 6.

The comparison of the MAPE of different models considering realized skewness and realized kurtosis.

Figure 6.

The comparison of the MAPE of different models considering realized skewness and realized kurtosis.

Figure 7.

The performance of ITM call options in different features (a) represents the LSTM with realized skewness, (b) represents the LSTM without realized skewness, (c) represents the LSTM with realized skewness and realized kurtosis.

Figure 7.

The performance of ITM call options in different features (a) represents the LSTM with realized skewness, (b) represents the LSTM without realized skewness, (c) represents the LSTM with realized skewness and realized kurtosis.

Figure 8.

The performance of ATM call options in different features (a) represents the LSTM with realized skewness, (b) represents the LSTM without realized skewness, (c) represents the LSTM with realized skewness and realized kurtosis.

Figure 8.

The performance of ATM call options in different features (a) represents the LSTM with realized skewness, (b) represents the LSTM without realized skewness, (c) represents the LSTM with realized skewness and realized kurtosis.

Figure 9.

The performance of OTM call options in different features (a) represents the LSTM with realized skewness, (b) represents the LSTM without realized skewness, (c) represents the LSTM with realized skewness and realized kurtosis.

Figure 9.

The performance of OTM call options in different features (a) represents the LSTM with realized skewness, (b) represents the LSTM without realized skewness, (c) represents the LSTM with realized skewness and realized kurtosis.

Figure 10.

The performance of ITM put options in different features (a) represents the LSTM with realized skewness, (b) represents the LSTM without realized skewness, (c) represents the LSTM with realized skewness and realized kurtosis.

Figure 10.

The performance of ITM put options in different features (a) represents the LSTM with realized skewness, (b) represents the LSTM without realized skewness, (c) represents the LSTM with realized skewness and realized kurtosis.

Figure 11.

The performance of ATM put options in different features (a) represents the LSTM with realized skewness, (b) represents the LSTM without realized skewness, (c) represents the LSTM with realized skewness and realized kurtosis.

Figure 11.

The performance of ATM put options in different features (a) represents the LSTM with realized skewness, (b) represents the LSTM without realized skewness, (c) represents the LSTM with realized skewness and realized kurtosis.

Figure 12.

The performance of OTM put options in different features (a) represents the LSTM with realized skewness, (b) represents the LSTM without realized skewness, (c) represents the LSTM with realized skewness and realized kurtosis.

Figure 12.

The performance of OTM put options in different features (a) represents the LSTM with realized skewness, (b) represents the LSTM without realized skewness, (c) represents the LSTM with realized skewness and realized kurtosis.

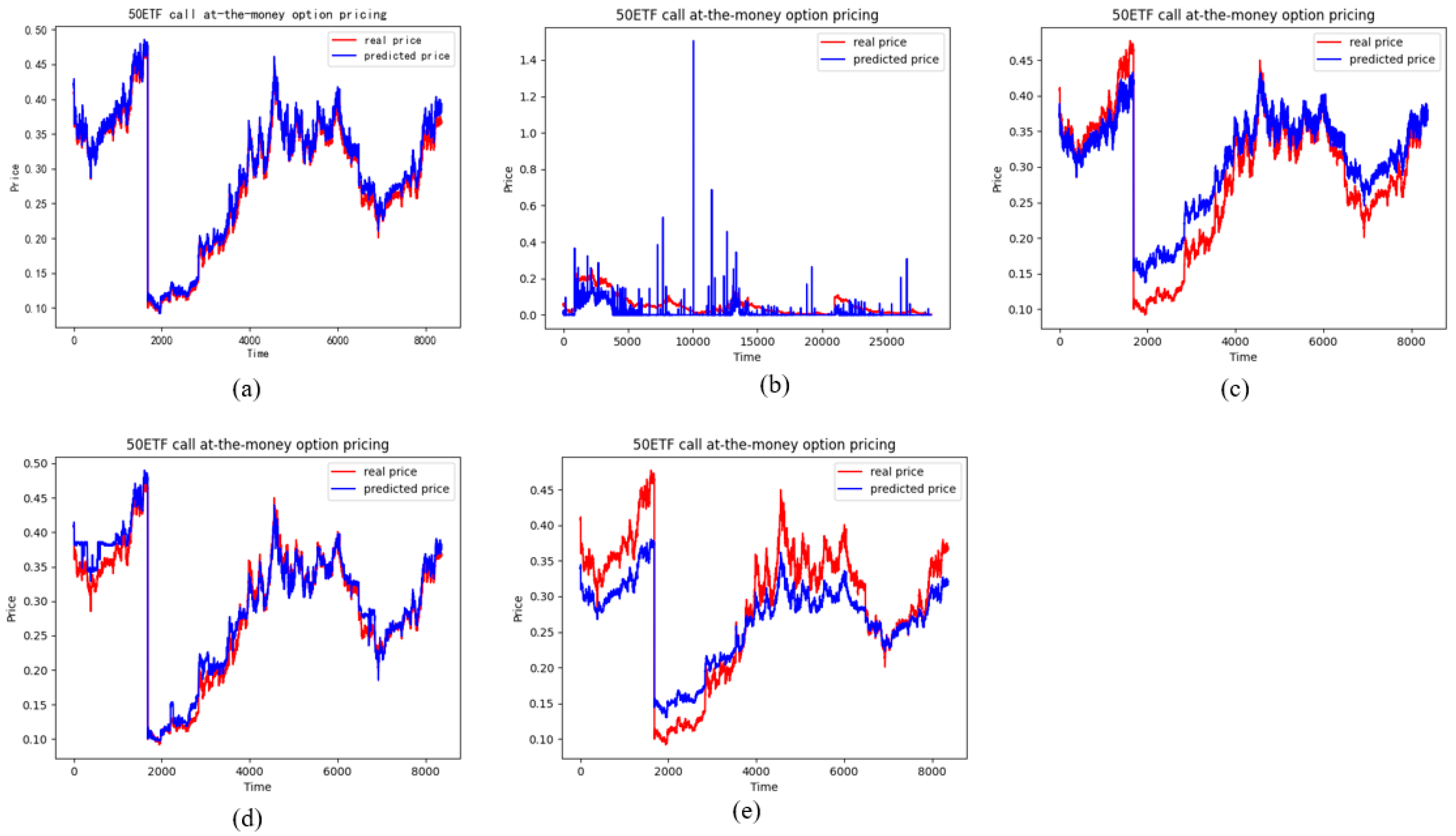

Figure 13.

The pricing performance of ITM call options on each model, (a) stands for the LSTM model, (b) stands for the BS model, (c) stands for the SVM model, (d) stands for the Ran-dom forests model, (e) stands for the RNN model.

Figure 13.

The pricing performance of ITM call options on each model, (a) stands for the LSTM model, (b) stands for the BS model, (c) stands for the SVM model, (d) stands for the Ran-dom forests model, (e) stands for the RNN model.

Figure 14.

The pricing performance of ATM call options on each model (a) stands for the LSTM model, (b) stands for the BS model, (c) stands for the SVM model, (d) stands for the Random forests model, (e) stands for the RNN model.

Figure 14.

The pricing performance of ATM call options on each model (a) stands for the LSTM model, (b) stands for the BS model, (c) stands for the SVM model, (d) stands for the Random forests model, (e) stands for the RNN model.

Figure 15.

The pricing performance of OTM call options on each model (a) stands for the LSTM model, (b) stands for the BS model, (c) stands for the SVM model, (d) stands for the Random forests model, (e) stands for the RNN model.

Figure 15.

The pricing performance of OTM call options on each model (a) stands for the LSTM model, (b) stands for the BS model, (c) stands for the SVM model, (d) stands for the Random forests model, (e) stands for the RNN model.

Figure 16.

The pricing performance of ITM put options on each model (a) stands for the LSTM model, (b) stands for the BS model, (c) stands for the SVM model, (d) stands for the Random forests model, (e) stands for the RNN model.

Figure 16.

The pricing performance of ITM put options on each model (a) stands for the LSTM model, (b) stands for the BS model, (c) stands for the SVM model, (d) stands for the Random forests model, (e) stands for the RNN model.

Figure 17.

The pricing performance of ATM put options on each model (a) stands for the LSTM model, (b) stands for the BS model, (c) stands for the SVM model, (d) stands for the Random forests model, (e) stands for the RNN model.

Figure 17.

The pricing performance of ATM put options on each model (a) stands for the LSTM model, (b) stands for the BS model, (c) stands for the SVM model, (d) stands for the Random forests model, (e) stands for the RNN model.

Figure 18.

The pricing performance of OTM put options on each model (a) stands for the LSTM model, (b) stands for the BS model, (c) stands for the SVM model, (d) stands for the Random forests model, (e) stands for the RNN model.

Figure 18.

The pricing performance of OTM put options on each model (a) stands for the LSTM model, (b) stands for the BS model, (c) stands for the SVM model, (d) stands for the Random forests model, (e) stands for the RNN model.

Table 1.

Hyperparameter of each model.

Table 1.

Hyperparameter of each model.

| | LSTM | RNN |

|---|

| Activation function | RELU | RELU |

| Loss function | MSE | MSE |

| Neurons | [200, 200, 200, 200, 200, 1] | [200, 200, 200, 200, 200, 1] |

| Learning rate | 0.001 | 0.001 |

| Optimizer | Adam | Adam |

Table 2.

Description of moneyness.

Table 2.

Description of moneyness.

| | State | Moneyness |

|---|

| Call option | ITM | >1.03 |

| ATM | 0.97~1.03 |

| OTM | <0.97 |

| Put option | ITM | <0.97 |

| ATM | 0.97~1.03 |

| OTM | >1.03 |

Table 3.

Statistics of ETF50 Call options sorted by moneyness.

Table 3.

Statistics of ETF50 Call options sorted by moneyness.

| Moneyness | | r | S | K | Maturity | Realized Volatility | Realized Skewness | Realized

Kurtosis |

|---|

| ITM | count | 70205 | 70205 | 70205 | 70205 | 70205 | 70205 | 70205 |

| mean | 0.0139 | 3.6119 | 3.2317 | 56.4780 | 0.0411 | 0.0049 | 2.2384 |

| std | 0.0059 | 0.1477 | 0.1499 | 0.1401 | 0.0948 | 1.1394 | 0.7893 |

| min | 0.0061 | 3.304 | 2.908 | 8 | 0.0006 | −2.2361 | 1 |

| max | 0.0328 | 4.096 | 3.4 | 237 | 3.9760 | 2.2361 | 5 |

| ATM | count | 83637 | 83637 | 83637 | 83637 | 83637 | 83637 | 83637 |

| mean | 0.01442 | 3.6181 | 3.4932 | 58.0846 | 0.0345 | 0.0199 | 2.2216 |

| std | 0.0063 | 0.1529 | 0.0949 | 0.1374 | 0.0771 | 1.1112 | 0.777 |

| min | 0.0061 | 3.304 | 3.253 | 8 | 0.0006 | −2.2361 | 1 |

| max | 0.0328 | 4.096 | 3.6 | 237 | 3.9760 | 2.2361 | 5 |

| OTM | count | 222532 | 222532 | 222532 | 222532 | 222532 | 222532 | 222532 |

| mean | 0.0163 | 3.6242 | 3.7427 | 69.1648 | 0.0338 | 0.0151 | 2.2193 |

| std | 0.0063 | 0.1569 | 0.122 | 0.1594 | 0.0778 | 1.1095 | 0.7772 |

| min | 0.0061 | 3.304 | 3.45 | 8 | 0.0006 | −2.2361 | 1 |

| max | 0.0328 | 4.096 | 3.9 | 237 | 3.976 | 2.2361 | 5 |

Table 4.

Statistics of ETF50 Put options sorted by moneyness.

Table 4.

Statistics of ETF50 Put options sorted by moneyness.

| Moneyness | | r | S | K | Maturity | Realized Volatility | Realized Skewness | Realized

Kurtosis |

|---|

| ITM | count | 153988 | 153988 | 153988 | 153988 | 153988 | 153988 | 153988 |

| mean | 0.0174 | 3.6841 | 3.7128 | 58.6633 | 0.0397 | 0.0071 | 2.2123 |

| std | 0.0062 | 0.1529 | 0.1344 | 0.1389 | 0.0939 | 1.1093 | 0.7664 |

| min | 0.0061 | 3.304 | 3.45 | 8 | 0.0006 | −2.2361 | 1 |

| max | 0.0328 | 4.096 | 3.9 | 237 | 3.976 | 2.2361 | 5 |

| ATM | count | 103716 | 103716 | 103716 | 103716 | 103716 | 103716 | 103716 |

| mean | 0.0154 | 3.6317 | 3.4596 | 64.8511 | 0.0346 | 0.0192 | 2.2207 |

| std | 0.0064 | 0.1576 | 0.1134 | 0.1463 | 0.0813 | 1.1099 | 0.7756 |

| min | 0.0061 | 3.304 | 3.253 | 8 | 0.0006 | −2.2361 | 1 |

| max | 0.0328 | 4.096 | 3.6 | 236 | 3.976 | 2.2361 | 5 |

| OTM | count | 145085 | 145085 | 145085 | 145085 | 145085 | 145085 | 145085 |

| mean | 0.015 | 3.5979 | 3.1774 | 77.7259 | 0.0354 | 0.0164 | 2.2283 |

| std | 0.0062 | 0.1502 | 0.1575 | 0.1671 | 0.0883 | 1.1194 | 0.7853 |

| min | 0.0061 | 3.304 | 2.908 | 8 | 0.0007 | −2.2361 | 1 |

| max | 0.0328 | 4.096 | 3.4 | 237 | 3.976 | 2.2361 | 5 |

Table 5.

Pricing error of LSTM without realized skewness.

Table 5.

Pricing error of LSTM without realized skewness.

| Metrics | Call Options | Put Options |

|---|

| | ITM | ATM | OTM | ITM | ATM | OTM |

|---|

| MSE | 0.0067 | 0.0289 | 0.0261 | 0.0442 | 0.0047 | 0.0019 |

| RMSE | 0.8197 | 1.7003 | 1.6149 | 2.1027 | 0.6876 | 0.4307 |

| MAE | 0.6437 | 1.5225 | 1.3905 | 1.8732 | 0.4064 | 0.2506 |

| MAPE | 1.1611 | 5.2866 | 28.0592 | 25.1675 | 20.1217 | 46.2594 |

Table 6.

Pricing error of LSTM with realized skewness.

Table 6.

Pricing error of LSTM with realized skewness.

| Metrics | Call Options | Put Options |

|---|

| | ITM | ATM | OTM | ITM | ATM | OTM |

|---|

| MSE | 0.0118 | 0.006 | 0.015 | 0.0207 | 0.0036 | 0.0017 |

| −76.12% | 79.24% | 42.53% | 53.17% | 23.40% | 10.53% |

| RMSE | 1.0875 | 0.7761 | 1.2257 | 1.438 | 0.6035 | 0.4113 |

| −32.67% | 54.36% | 24.10% | 31.61% | 12.23% | 4.50% |

| MAE | 0.9053 | 0.6253 | 1.0454 | 1.3198 | 0.3542 | 0.2331 |

| −40.64% | 58.96% | 24.82% | 29.54% | 12.84% | 6.98% |

| MAPE | 1.791 | 2.3868 | 19.8898 | 16.0634 | 16.7579 | 28.8013 |

| −54.25% | 54.85% | 29.11% | 36.17% | 16.72% | 37.74% |

Table 7.

Pricing error of LSTM with realized skewness and realized kurtosis.

Table 7.

Pricing error of LSTM with realized skewness and realized kurtosis.

| Metrics | Call Options | Put Options |

|---|

| | ITM | ATM | OTM | ITM | ATM | OTM |

|---|

| MSE | 0.0138 | 0.0054 | 0.0282 | 0.0305 | 0.0045 | 0.0015 |

| −16.64% | 9.31% | −87.94% | −47.46% | −24.81% | 10.70% |

| RMSE | 1.1732 | 0.7377 | 1.6790 | 1.7471 | 0.6703 | 0.3896 |

| −7.88% | 4.95% | −36.99% | −21.50% | −11.07% | 5.27% |

| MAE | 0.9242 | 0.5917 | 1.4537 | 1.5390 | 0.3751 | 0.2196 |

| −2.09% | 5.37% | −39.06% | −16.61% | −5.90% | 5.81% |

| MAPE | 1.6019 | 2.3151 | 29.0479 | 16.6420 | 16.7752 | 29.6484 |

| 10.56% | 3.01% | −46.04% | −3.60% | −0.10% | −2.94% |

Table 8.

Pricing error of ITM options estimated using different models when using realized skewness.

Table 8.

Pricing error of ITM options estimated using different models when using realized skewness.

| Models | ITM Call Options | | ITM Put Options |

|---|

| MSE | RMSE | MAE | MAPE | | MSE | RMSE | MAE | MAPE |

|---|

| BS | 33.6885 | 58.0418 | 55.9973 | 99.9041 | | 0.4037 | 6.3540 | 5.7960 | 64.2859 |

| SVM | 0.1221 | 3.4946 | 2.8661 | 5.5627 | | 0.3562 | 5.9681 | 5.7673 | 76.0187 |

| RF | 0.0209 | 1.4474 | 0.9829 | 1.8028 | | 0.0113 | 1.0631 | 0.8555 | 11.7190 |

| RNN | 0.5544 | 7.4460 | 6.2965 | 10.6978 | | 0.2093 | 4.5747 | 4.3433 | 56.2957 |

| LSTM | 0.0118 | 1.0875 | 0.9053 | 1.7910 | | 0.0207 | 1.4380 | 1.3198 | 16.0634 |

Table 9.

Pricing error of ATM options estimated using different models when using realized skewness.

Table 9.

Pricing error of ATM options estimated using different models when using realized skewness.

| Models | ATM Call Options | | ATM Put Options |

|---|

| MSE | RMSE | MAE | MAPE | | MSE | RMSE | MAE | MAPE |

|---|

| BS | 0.3303 | 5.7471 | 4.1122 | 97.2872 | | 0.1095 | 3.3095 | 2.2106 | 104.2794 |

| SVM | 0.1257 | 3.5457 | 3.0895 | 15.1358 | | 0.5718 | 7.5617 | 7.4347 | 921.8113 |

| RF | 0.0257 | 1.6023 | 1.2072 | 4.6944 | | 0.0064 | 0.7989 | 0.5151 | 30.4049 |

| RNN | 0.1764 | 4.1998 | 3.6286 | 13.8309 | | 0.0458 | 2.1405 | 2.0417 | 173.6328 |

| LSTM | 0.0060 | 0.7761 | 0.6253 | 2.3868 | | 0.0036 | 0.6035 | 0.3542 | 16.7579 |

Table 10.

Pricing error of OTM options estimated using different models when using realized skewness.

Table 10.

Pricing error of OTM options estimated using different models when using realized skewness.

| Models | OTM Call Options | | OTM Put Options |

|---|

| MSE | RMSE | MAE | MAPE | | MSE | RMSE | MAE | MAPE |

|---|

| BS | 2.2385 | 14.9615 | 12.1928 | 271.6490 | | 0.0154 | 1.2413 | 0.7371 | 107.8957 |

| SVM | 0.2772 | 5.2650 | 4.8966 | 75.7476 | | 0.8353 | 9.1395 | 9.1124 | 3293.3315 |

| RF | 0.0627 | 2.5038 | 1.8247 | 22.9774 | | 0.0023 | 0.4832 | 0.2845 | 34.4681 |

| RNN | 0.1661 | 4.0753 | 3.8056 | 72.5007 | | 0.0048 | 0.6939 | 0.6531 | 183.8504 |

| LSTM | 0.0150 | 1.2257 | 1.0454 | 19.8898 | | 0.0017 | 0.4113 | 0.2331 | 28.8013 |

Table 11.

Pricing error of ITM options estimated using different models when using realized skewness and realized kurtosis.

Table 11.

Pricing error of ITM options estimated using different models when using realized skewness and realized kurtosis.

| Models | ITM Call Options | | ITM Put Options |

|---|

| MSE | RMSE | MAE | MAPE | | MSE | RMSE | MAE | MAPE |

|---|

| BS | 33.6885 | 58.0418 | 55.9973 | 99.9041 | | 0.4037 | 6.3540 | 5.7960 | 64.2859 |

| SVM | 0.1226 | 3.5016 | 2.8688 | 5.6109 | | 0.3513 | 5.9267 | 5.7186 | 75.6203 |

| RF | 0.0208 | 1.4406 | 0.9812 | 1.7970 | | 0.0112 | 1.0576 | 0.8497 | 11.6567 |

| RNN | 0.5987 | 7.7373 | 6.5175 | 11.1190 | | 0.3030 | 5.5043 | 5.3030 | 69.5781 |

| LSTM | 0.0138 | 1.1732 | 0.9242 | 1.6019 | | 0.0305 | 1.7471 | 1.5390 | 16.6420 |

Table 12.

Pricing error of ATM options estimated using different models when using realized skewness and realized kurtosis.

Table 12.

Pricing error of ATM options estimated using different models when using realized skewness and realized kurtosis.

| Models | ATM Call Options | | ATM Put Options |

|---|

| MSE | RMSE | MAE | MAPE | | MSE | RMSE | MAE | MAPE |

|---|

| BS | 0.3303 | 5.7471 | 4.1122 | 97.2872 | | 0.1095 | 3.3095 | 2.2106 | 104.2794 |

| SVM | 0.1139 | 3.3744 | 2.9022 | 14.3229 | | 0.5596 | 7.4806 | 7.3462 | 912.8136 |

| RF | 0.0253 | 1.5915 | 1.2008 | 4.6725 | | 0.0058 | 0.7584 | 0.4925 | 29.7101 |

| RNN | 0.1815 | 4.2605 | 3.6802 | 14.1544 | | 0.0472 | 2.1731 | 2.1188 | 200.7604 |

| LSTM | 0.0054 | 0.7377 | 0.5917 | 2.3151 | | 0.0045 | 0.6703 | 0.3751 | 16.7752 |

Table 13.

Pricing error of OTM options estimated using different models when using realized skewness and realized kurtosis.

Table 13.

Pricing error of OTM options estimated using different models when using realized skewness and realized kurtosis.

| Models | OTM Call Options | | OTM Put Options |

|---|

| MSE | RMSE | MAE | MAPE | | MSE | RMSE | MAE | MAPE |

|---|

| BS | 2.2385 | 14.9615 | 12.1928 | 271.6490 | | 0.0154 | 1.2413 | 0.7371 | 107.8957 |

| SVM | 0.2856 | 5.3446 | 4.9778 | 77.0127 | | 0.8353 | 9.1395 | 9.1124 | 3293.3115 |

| RF | 0.0628 | 2.5053 | 1.8241 | 23.0268 | | 0.0024 | 0.4849 | 0.2853 | 34.4997 |

| RNN | 0.2163 | 4.6503 | 4.3962 | 83.6558 | | 0.0091 | 0.9544 | 0.8765 | 238.5260 |

| LSTM | 0.0282 | 1.6790 | 1.4537 | 29.0479 | | 0.0015 | 0.3896 | 0.2196 | 29.6484 |

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}