Do Geopolitical Tensions and Economic Policy Uncertainties Reorient Mineral Imports in the USA? A Fat-Tailed Data Analysis Using Novel Quantile Approaches

Abstract

1. Introduction

2. Literature Review and Background Works

3. Materials and Methods

3.1. Data and Sources

3.2. Unit-Root Test for Nonlinear Data Property

3.3. Cross-Quantilogram (CQ) Technique

3.4. Quantile-on-Quantile (QQ) Approach

4. Empirical Findings and Discussions

4.1. Findings from the Descriptive Analysis

4.2. Findings from the KSS Unit-Root Test for Nonlinearity

4.3. Findings from the Cross-Quantilogram (CQ) Technique

4.3.1. USA’s Geopolitical Risk (UGPR) and Mineral Import (MI)

4.3.2. Global Geopolitical Risk (GGPR) to Mineral Import (MI)

4.3.3. USA’s Economic Policy Uncertainty (UEPU) to Mineral Import (MI)

4.3.4. Global Economic Policy Uncertainty (GEPU) to Mineral Import (MI)

4.4. Findings from the Quantile-on-Quantile (QQ) Technique

4.4.1. USA’s Geopolitical Risk (UGPR) and Mineral Import (MI)

4.4.2. Global Geopolitical Risk (GGPR) and Mineral Import (MI)

4.4.3. USA’s Economic Policy Uncertainty (UEPU) and Mineral Import (MI)

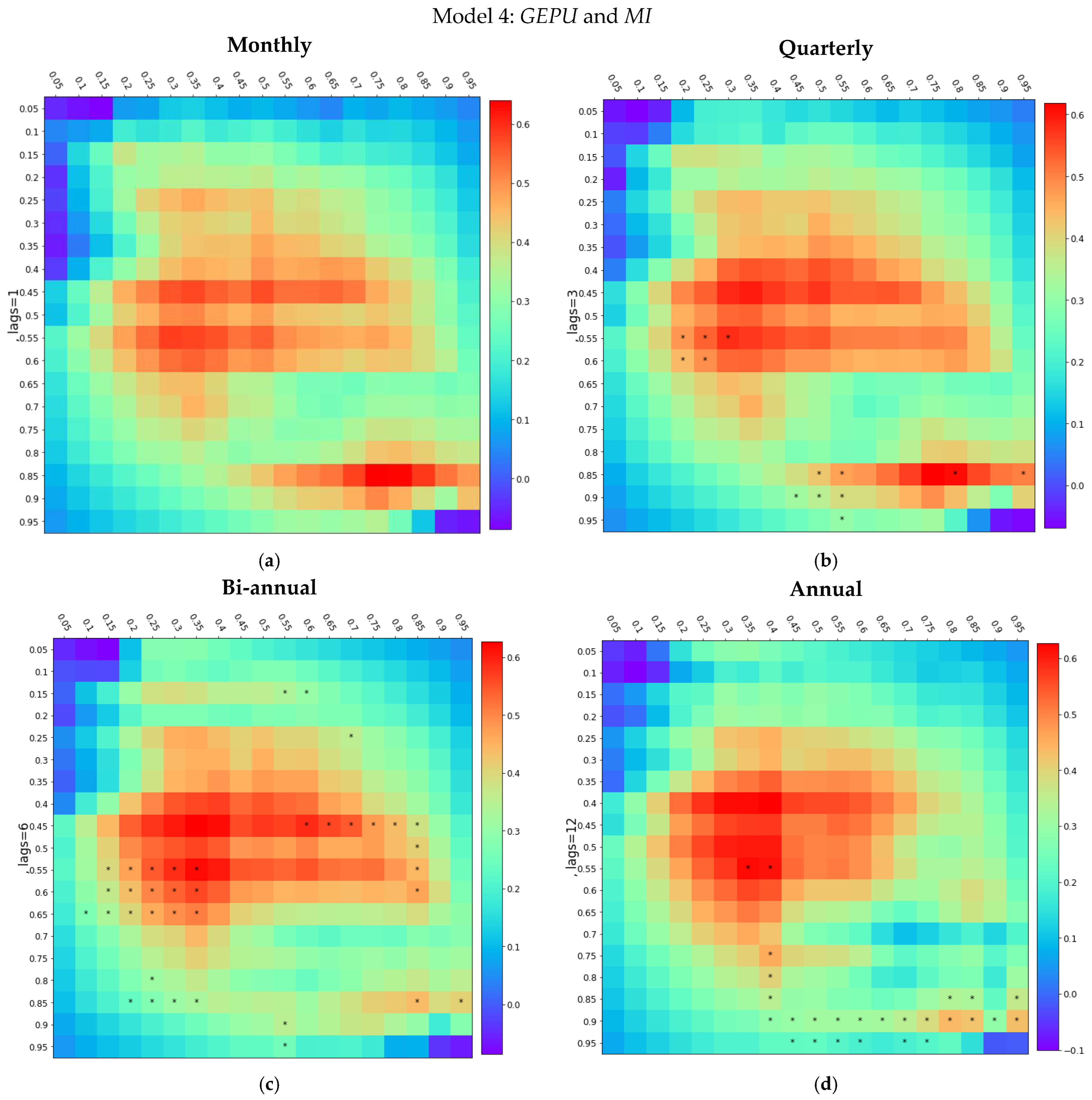

4.4.4. Global Economic Policy Uncertainty (GEPU) and Mineral Import (MI)

5. Conclusions and Policy Implications

Author Contributions

Funding

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Azapagic, A. Developing a framework for sustainable development indicators for the mining and minerals industry. J. Clean. Prod. 2004, 1, 639–662. [Google Scholar] [CrossRef]

- Islam, M.M.; Sohag, K.; Hammoudeh, S.; Mariev, O.; Samargandi, N. Minerals import demands and clean energy transitions: A disaggregated analysis. Energy Econ. 2022, 113, 106205. [Google Scholar] [CrossRef]

- World Bank. Mineral Production to Soar as Demand for Clean Energy Increases. World Bank. 2020. Available online: https://www.worldbank.org/en/news/press-release/2020/05/11/mineral-production-to-soar-as-demand-for-clean-energy-increases (accessed on 12 April 2022).

- Li, J.; Lv, L.; Zhou, G.; Li, X. Mechanism of a microscale flat plate heat pipe with extremely high nominal thermal conductivity for cooling high-end smartphone chips. Energy Convers. Manag. 2019, 201, 112202. [Google Scholar] [CrossRef]

- Chapman, B. The geopolitics of rare earth elements: Emerging challenge for US National Security and Economics. J. Self-Gov. Manag. Econ. 2018, 6, 50–91. [Google Scholar]

- Eckes, A.E., Jr. The United States and the Global Struggle for Minerals; University of Texas Press: Austin, TX, USA, 1979. [Google Scholar]

- Lee, A. Strategic and Critical Minerals: What They Are Why They Matter. BIG ROCK Exploration. 2019. Available online: https://bigrockexploration.com/2019/04/what-makes-minerals-strategic-critical/ (accessed on 26 July 2022).

- Amzallag, N. From metallurgy to bronze age civilizations: The synthetic theory. Am. J. Archaeol. 2009, 113, 497–519. [Google Scholar] [CrossRef]

- Bortnikov, N.S.; Volkov, A.V.; Galyamov, A.L.; Vikent’ev, I.V.; Aristov, V.V.; Lalomov, A.V.; Murashov, K.Y. Mineral resources of high-tech metals in Russia: State of the art and outlook. Geol. Ore Depos. 2016, 58, 83–103. [Google Scholar] [CrossRef]

- Sonnemann, G.; Gemechu, E.D.; Adibi, N.; De Bruille, V.; Bulle, C. From a critical review to a conceptual framework for integrating the criticality of resources into Life Cycle Sustainability Assessment. J. Clean. Prod. 2015, 94, 20–34. [Google Scholar] [CrossRef]

- Da Silva Lima, L.; Quartier, M.; Buchmayr, A.; Sanjuan-Delmás, D.; Laget, H.; Corbisier, D.; Mertens, J.; Dewulf, J. Life cycle assessment of lithium-ion batteries and vanadium redox flow batteries-based renewable energy storage systems. Sustain. Energy Technol. Assess. 2021, 46, 101286. [Google Scholar] [CrossRef]

- Omodara, L.; Pitkäaho, S.; Turpeinen, E.-M.; Saavalainen, P.; Oravisjärvi, K.; Keiski, R.L. Recycling and substitution of light rare earth elements, cerium, lanthanum, neodymium, and praseodymium from end-of-life applications-A review. J. Clean. Prod. 2019, 236, 117573. [Google Scholar] [CrossRef]

- USGS. Facts About Nickel Nickel Uses, Resources, Supply, Demand, and Production Information. Geoscience News and Information: Geology.com. 2021. Available online: https://geology.com/usgs/uses-of-nickel/ (accessed on 20 April 2022).

- Albulescu, C.T.; Demirer, R.; Raheem, I.D.; Tiwari, A.K. Does the US economic policy uncertainty connect financial markets? Evidence from oil and commodity currencies. Energy Econ. 2019, 83, 375–388. [Google Scholar] [CrossRef]

- Brzezinski, Z. The Geostrategic Triad: Living with China, Europe, and Russia; CSIS: Washington, DC, USA, 2001; Volume 23. [Google Scholar]

- Spykman, N.J. America’s Strategy in World Politics: The United States and the Balance of Power; Routledge: Abingdon, UK, 2017. [Google Scholar]

- Massari, S.; Ruberti, M. Rare earth elements as critical raw materials: Focus on international markets and future strategies. Resour Policy 2013, 38, 36–43. [Google Scholar] [CrossRef]

- Harff, B.; Gurr, T.R. Ethnic Conflict in World Politics; Routledge: Abingdon, UK, 2018. [Google Scholar]

- Gordon, T.; Webber, J.R. Blood of Extraction: Canadian Imperialism in Latin America; Fernwood Publishing: Black Point, NS, Canada, 2016. [Google Scholar]

- Davis, G.A.; Tilton, J.E. The resource curse. In Natural Resources Forum; Wiley Online Library: Hoboken, NJ, USA, 2005; pp. 233–242. [Google Scholar]

- Islam, M.M.; Sohag, K.; Alam, M.M. Mineral import demand and clean energy transitions in the top mineral-importing countries. Resour. Policy 2022, 78, 102893. [Google Scholar] [CrossRef]

- Hamilton, J.D. Understanding crude oil prices. Energy J. 2009, 30, 56–78. [Google Scholar] [CrossRef]

- Kilian, L.; Murphy, D.P. The role of inventories and speculative trading in the global market for crude oil. J. Appl. Econom. 2014, 29, 454–478. [Google Scholar] [CrossRef]

- Jourdan, P. Toward a resource-based African industrialization strategy. In The Industrial Policy Revolution II; Springer: Berlin/Heidelberg, Germany, 2013; pp. 364–385. [Google Scholar]

- Stuermer, M. Industrialization and the demand for mineral commodities. J. Int. Money Finance 2017, 76, 16–27. [Google Scholar] [CrossRef]

- Henckens, M.; Biermann, F.H.B.; Driessen, P.P.J. Mineral resources governance: A call for the establishment of an International Competence Center on Mineral Resources Management. Resour. Conserv. Recycl. 2019, 141, 255–263. [Google Scholar] [CrossRef]

- Valero, A.; Valero, A.; Calvo, G.; Ortego, A. Material bottlenecks in the future development of green technologies. Renew. Sustain. Energy Rev. 2018, 93, 178–200. [Google Scholar] [CrossRef]

- Jiskani, I.M.; Moreno-Cabezali, B.M.; Rehman, A.U.; Fernandez-Crehuet, J.M.; Uddin, S. Implications to secure mineral supply for clean energy technologies for developing countries: A fuzzy based risk analysis for mining projects. J. Clean. Prod. 2022, 358, 132055. [Google Scholar] [CrossRef]

- Nygaard, A. The Geopolitical Risk and Strategic Uncertainty of Green Growth after the Ukraine Invasion: How the Circular Economy Can Decrease the Market Power of and Resource Dependency on Critical Minerals. Circ. Econ. Sustain. 2022, 1–28. [Google Scholar] [CrossRef]

- Daniel, P. Economic policy in mineral-exporting countries: What have we learned? In Mineral Wealth and Economic Development; Routledge: Abingdon, UK, 2015; pp. 81–121. [Google Scholar]

- Elshkaki, A. Materials, energy, water, and emissions nexus impacts on the future contribution of PV solar technologies to global energy scenarios. Sci. Rep. 2019, 9, 19238. [Google Scholar] [CrossRef]

- Zhou, T.; Li, K.; Yang, S.L. Remanufacturing with material restrictions in monopoly and duopoly. Eur. J. Ind. Eng. 2022, 16, 556–583. [Google Scholar] [CrossRef]

- Sohn, I. Long-term projections of non-fuel minerals: We were wrong, but why? Resour. Policy 2005, 30, 259–284. [Google Scholar] [CrossRef]

- Seck, G.S.; Hache, E.; Barnet, C. Potential bottleneck in the energy transition: The case of cobalt in an accelerating electro-mobility world. Resour. Policy 2022, 75, 102516. [Google Scholar] [CrossRef]

- Calvo, G.; Valero, A. Strategic mineral resources: Availability and future estimations for the renewable energy sector. Environ. Dev. 2022, 41, 100640. [Google Scholar] [CrossRef]

- Li, Y.; Huang, J.; Zhang, H. The impact of country risks on cobalt trade patterns from the perspective of the industrial chain. Resour. Policy 2022, 77, 102641. [Google Scholar] [CrossRef]

- Fernandez, V. Price and income elasticity of demand for mineral commodities. Resour. Policy 2018, 59, 160–183. [Google Scholar] [CrossRef]

- Redlinger, M.; Eggert, R. Volatility of by-product metal and mineral prices. Resour. Policy 2016, 47, 69–77. [Google Scholar] [CrossRef]

- García, D.; Guzmán, J.I. Short-term price volatility and reversion rate in mineral commodity markets. Miner. Econ. 2020, 33, 217–229. [Google Scholar] [CrossRef]

- Hu, Y.; Zhang, Y.; Bao, S.; Liu, T. Effects of the mineral phase and valence of vanadium on vanadium extraction from stone coal. Int. J. Miner. Metall. Mater. 2012, 19, 893–898. [Google Scholar] [CrossRef]

- Aldakhil, A.M.; Nassani, A.A.; Zaman, K. The role of technical cooperation grants in mineral resource extraction: Evidence from a panel of 12 abundant resource economies. Resour. Policy 2020, 69, 101822. [Google Scholar] [CrossRef]

- Church, C.; Crawford, A. Minerals and the metals for the energy transition: Exploring the conflict implications for mineral-rich, fragile states. In The Geopolitics of the Global Energy Transition; Springer: Berlin/Heidelberg, Germany, 2020; pp. 279–304. [Google Scholar]

- Bazilian, M.D. The mineral foundation of the energy transition. Extr. Ind. Soc. 2018, 5, 93–97. [Google Scholar] [CrossRef]

- Tokimatsu, K.; Höök, M.; McLellan, B.; Wachtmeister, H.; Murakami, S.; Yasuoka, R.; Nishio, M. Energy modeling approach to the global energy-mineral nexus: Exploring metal requirements and the well-below 2 C target with 100 percent renewable energy. Appl. Energy 2018, 225, 1158–1175. [Google Scholar] [CrossRef]

- Hanai, K. Conflict minerals regulation and mechanism changes in the DR Congo. Resour. Policy 2021, 74, 102394. [Google Scholar] [CrossRef]

- British Geological Survey (BGS). MineralsUK. British Geological Survey (BGS), Center for Sustainable Mineral Development. 2022. Available online: https://www2.bgs.ac.uk/mineralsuk/statistics/UKStatistics.html (accessed on 26 February 2022).

- Caldara, D.; Iacoviello, M. Measuring geopolitical risk. Am. Econ. Rev. 2022, 112, 1194–1225. [Google Scholar] [CrossRef]

- EPU. Economic Policy Uncertainty Index. Research on Economic Policy Uncertainty. 2022. Available online: https://www.policyuncertainty.com/index.html (accessed on 10 December 2022).

- Baker, S.R.; Bloom, N.; Davis, S.J. Measuring economic policy uncertainty. Q. J. Econ. 2016, 131, 1593–1636. [Google Scholar] [CrossRef]

- Jaber, J.O.; Elkarmi, F.; Alasis, E.; Kostas, A. Employment of renewable energy in Jordan: Current status, SWOT and problem analysis. Renew. Sustain. Energy Rev. 2015, 49, 490–499. [Google Scholar] [CrossRef]

- Vakulchuk, R.; Overland, I.; Scholten, D. Renewable energy and geopolitics: A review. Renew. Sustain. Energy Rev. 2020, 122, 109547. [Google Scholar] [CrossRef]

- Li, F.; Yang, C.; Li, Z.; Failler, P. Does geopolitics have an impact on energy trade? Empirical research on emerging countries. Sustainability 2021, 13, 5199. [Google Scholar] [CrossRef]

- Kapetanios, G.; Shin, Y.; Snell, A. Testing for a unit root in the nonlinear STAR framework. J. Econom. 2003, 112, 359–379. [Google Scholar] [CrossRef]

- Han, H.; Linton, O.; Oka, T.; Whang, Y.-J. The cross-quantilogram: Measuring quantile dependence and testing directional predictability between time series. J. Econom. 2016, 193, 251–270. [Google Scholar] [CrossRef]

- Cho, D.; Han, H. The tail behavior of safe haven currencies: A cross-quantilogram analysis. J. Int. Financ. Mark. Inst. Money 2021, 70, 101257. [Google Scholar] [CrossRef]

- Sohag, K.; Hammoudeh, S.; Elsayed, A.H.; Mariev, O.; Safonova, Y. Do geopolitical events transmit opportunity or threat to green markets? Decomposed measures of geopolitical risks. Energy Econ. 2022, 111, 106068. [Google Scholar] [CrossRef]

- Sim, N.; Zhou, H. Oil prices, US stock return, and the dependence between their quantiles. J. Bank. Financ. 2015, 55, 1–8. [Google Scholar] [CrossRef]

- Bouoiyour, J.; Selmi, R.; Wohar, M.E. Measuring the response of gold prices to uncertainty: An analysis beyond the mean. Econ. Model. 2018, 75, 105–116. [Google Scholar] [CrossRef]

- Fatima, T.; Karim, M.Z.a.; Meo, M.S. Sectoral CO2 emissions in China: Asymmetric and time-varying analysis. J. Environ. Plan. Manag. 2021, 64, 581–610. [Google Scholar] [CrossRef]

- Auxier, B. 64% of Americans Say Social Media Have a Mostly Negative Effect on the Way Things Are Going in the U.S. Today. Pew Research Center. 2020. Available online: https://www.pewresearch.org/fact-tank/2020/10/15/64-of-americans-say-social-media-have-a-mostly-negative-effect-on-the-way-things-are-going-in-the-u-s-today/ (accessed on 24 July 2022).

- Amaded, K.U.S. Military Budget, Its Components, Challenges, and Growth. The Balance. 2022. Available online: https://www.thebalance.com/u-s-military-budget-components-challenges-growth-3306320 (accessed on 24 July 2022).

- NSC. National Strategy for Counterterrorism of the United States of America [Internet]. Office of the Director of National Intelligence; 2018. Available online: https://www.dni.gov/index.php/features/national-strategy-for-counterterrorism (accessed on 24 July 2022).

- Davis, M. The Impact of 9/11 on Business. Investopedia. 2022. Available online: https://www.investopedia.com/financial-edge/0911/the-impact-of-september-11-on-business.aspx (accessed on 20 September 2022).

- Su, C.-W.; Khan, K.; Umar, M.; Zhang, W. Does renewable energy redefine geopolitical risks? Energy Policy 2021, 158, 112566. [Google Scholar] [CrossRef]

- Cheng, C.H.J.; Chiu, C.-W.J. How important are global geopolitical risks to emerging countries? Int. Econ. 2018, 156, 305–325. [Google Scholar] [CrossRef]

- Santillán-Saldivar, J.; Cimprich, A.; Shaikh, N.; Laratte, B.; Young, S.B.; Sonnemann, G. How recycling mitigates supply risks of critical raw materials: Extension of the geopolitical supply risk methodology applied to information and communication technologies in the European Union. Resour. Conserv. Recycl. 2021, 164, 105108. [Google Scholar] [CrossRef]

- Lee, J. The world stock markets under geopolitical risks: Dependence structure. World Econ. 2019, 42, 1898–1930. [Google Scholar] [CrossRef]

- Bilgin, M.H.; Gozgor, G.; Karabulut, G. How do geopolitical risks affect government investment? An empirical investigation. Def. Peace Econ. 2020, 31, 550–564. [Google Scholar] [CrossRef]

- Amadeo, K. How the Federal Reserve Controls Inflation. The Balance. 2022. Available online: https://www.thebalance.com/what-is-being-done-to-control-inflation-3306095 (accessed on 15 August 2022).

- Dotsey, M.; Sarte, P.D. Inflation uncertainty and growth in a cash-in-advance economy. J. Monet. Econ. 2000, 45, 631–655. [Google Scholar] [CrossRef]

- Barro, R.J. Inflation and economic growth. Ann. Econ. Financ. 2013, 14, 85–109. [Google Scholar]

- Friedman, M. Nobel lecture: Inflation and unemployment. J. Political Econ. 1977, 85, 451–472. [Google Scholar] [CrossRef]

- Kim, W. Government spending policy uncertainty and economic activity: US time series evidence. J. Macroecon. 2019, 61, 103124. [Google Scholar] [CrossRef]

- Bloom, N. The impact of uncertainty shocks. Econometrica 2009, 77, 623–685. [Google Scholar]

- Rubio-Ramírez, J.F.; Fernández-Villaverde, J.; Kuester, K.; Guerron-Quintana, P.A. Fiscal Volatility Shocks and Economic Activity. Am. Econ. Rev. 2011, 105, 3352–3384. [Google Scholar]

- Born, B.; Pfeifer, J. Policy risk and the business cycle. J. Monet. Econ. 2014, 68, 68–85. [Google Scholar] [CrossRef]

- Baunsgaard, T.; Keen, M. Tax revenue and (or?) trade liberalization. J. Public Econ. 2010, 94, 563–577. [Google Scholar] [CrossRef]

- Teera, J.M.; Hudson, J. Tax performance: A comparative study. J. Int. Dev. 2004, 16, 785–802. [Google Scholar] [CrossRef]

- Bikas, E.; Andruskaite, E. Factors affecting value added tax revenue. Eur. Sci. J. 2013, 9, 8–19. [Google Scholar]

- Matschke, X. Costly revenue-raising and the case for favoring import-competing industries. J. Int. Econ. 2008, 74, 143–157. [Google Scholar] [CrossRef][Green Version]

- Chou, W.L.; Shih, Y.C. The equilibrium exchange rate of the Chinese Renminbi. J. Comp. Econ. 1998, 26, 165–174. [Google Scholar] [CrossRef]

- Danmola, R.A. The impact of exchange rate volatility on the macro economic variables in Nigeria. Eur. Sci. J. 2013, 9, 152–165. [Google Scholar]

- Tam, P.S. Global trade flows and economic policy uncertainty. Appl. Econ. 2018, 50, 3718–3734. [Google Scholar] [CrossRef]

- Sharma, C.; Paramati, S.R. Does economic policy uncertainty dampen imports? Commodity-level evidence from India. Econ. Model. 2021, 94, 139–149. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Code | Description | Measurement | Sources |

|---|---|---|---|

| Dependent variable | |||

| MI | Mineral imports | Total mineral imports volume in metric ton (measured in thousands) | British Geological Survey [46] |

| Independent variables | |||

| UGPR | USA’s geopolitical risk index | Three USA-based newspapers include “The New York Times, Washington Post, and Chicago Tribune,” whose electronic archives are the sources of the USA’s geopolitical risk (GPR) index. This index is shown as a percentage of the monthly newspaper writings. Mainly, the generated index reflects how the United States views the risks that affect the concerned countries. | Caldara & Iacoviello [47] |

| GGPR | Global geopolitical risk index | The global geopolitical risks index highlights the monthly news articles from 11 renowned dailies covering six aspects of geopolitical events. In addition, this index distinguishes between the threats of geopolitical risks and the direct adverse effects of geopolitical events. | |

| UEPU | USA’s economic policy uncertainty index | The newspaper-based index of the USA’s economic policy uncertainty is the product of the search results from 10 prominent newspapers. A normalized index is devised based on the number of news items on economic policy uncertainty. Moreover, the uncertainty index about the policy-related macroeconomic variables is a dispersion measure of forecasts made by different predictors regarding future levels of the Consumer Price Index, Federal Expenditures, and State and Local Expenditures. | EPU [48] |

| GEPU | Global economic policy uncertainty index | Global economic policy uncertainty is an index congregating mainly two underlying components, purchasing power parity (PPP) and exchange rate, to gauge policy-related volatility on these macroeconomic determinants. Therefore, quantifying media coverage of policy-related economic uncertainty is the most adaptable part of covering the perspectives of the globe, countries and regions. | |

| MI | UGPR | GGPR | UEPU | GEPU | |

|---|---|---|---|---|---|

| Mean | 15.6446 | 0.9339 | 4.5041 | 4.7474 | 4.7535 |

| Median | 15.8755 | 0.9334 | 4.4714 | 4.6971 | 4.7056 |

| Maximum | 16.1880 | 2.3844 | 6.2393 | 6.2225 | 6.0641 |

| Minimum | 14.8810 | −0.0483 | 3.6647 | 3.8018 | 3.8911 |

| Std. Dev. | 1.5200 | 0.3519 | 0.3580 | 0.4291 | 0.4671 |

| Skewness | −0.3770 | 0.3671 | 1.1326 | 0.5447 | 0.4296 |

| Kurtosis | 1.3780 | 4.9817 | 6.8394 | 3.2926 | 2.4977 |

| Jarque-Bera | 39.9934 | 55.8289 | 48.4129 | 15.9072 | 12.3847 |

| Prob. | 0.0000 | 0.0000 | 0.0000 | 0.0003 | 0.0020 |

| Obs. | 300 | 300 | 300 | 300 | 300 |

| Series | KSS Estimated Values | Significance at 10% Level |

|---|---|---|

| MI | −4.68 | −2.66 |

| UGPR | −3.74 | −2.66 |

| GGPR | −3.89 | −2.66 |

| UEPU | −2.78 | −2.66 |

| GEPU | −3.54 | −2.66 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Islam, M.M.; Sohag, K.; Rehman, F.u. Do Geopolitical Tensions and Economic Policy Uncertainties Reorient Mineral Imports in the USA? A Fat-Tailed Data Analysis Using Novel Quantile Approaches. Mathematics 2023, 11, 180. https://doi.org/10.3390/math11010180

Islam MM, Sohag K, Rehman Fu. Do Geopolitical Tensions and Economic Policy Uncertainties Reorient Mineral Imports in the USA? A Fat-Tailed Data Analysis Using Novel Quantile Approaches. Mathematics. 2023; 11(1):180. https://doi.org/10.3390/math11010180

Chicago/Turabian StyleIslam, Md. Monirul, Kazi Sohag, and Faheem ur Rehman. 2023. "Do Geopolitical Tensions and Economic Policy Uncertainties Reorient Mineral Imports in the USA? A Fat-Tailed Data Analysis Using Novel Quantile Approaches" Mathematics 11, no. 1: 180. https://doi.org/10.3390/math11010180

APA StyleIslam, M. M., Sohag, K., & Rehman, F. u. (2023). Do Geopolitical Tensions and Economic Policy Uncertainties Reorient Mineral Imports in the USA? A Fat-Tailed Data Analysis Using Novel Quantile Approaches. Mathematics, 11(1), 180. https://doi.org/10.3390/math11010180