The Impact of COVID-19 on the Connectedness of Stock Index in ASEAN+3 Economies

Abstract

:1. Introduction

2. Literature Review

3. Method

3.1. Diebold and Yilmaz (DY12) Time Domain Approach

3.2. Baruník and Křehlík (BK18) Frequency Domain Approach

3.3. Wavelet-Based Method

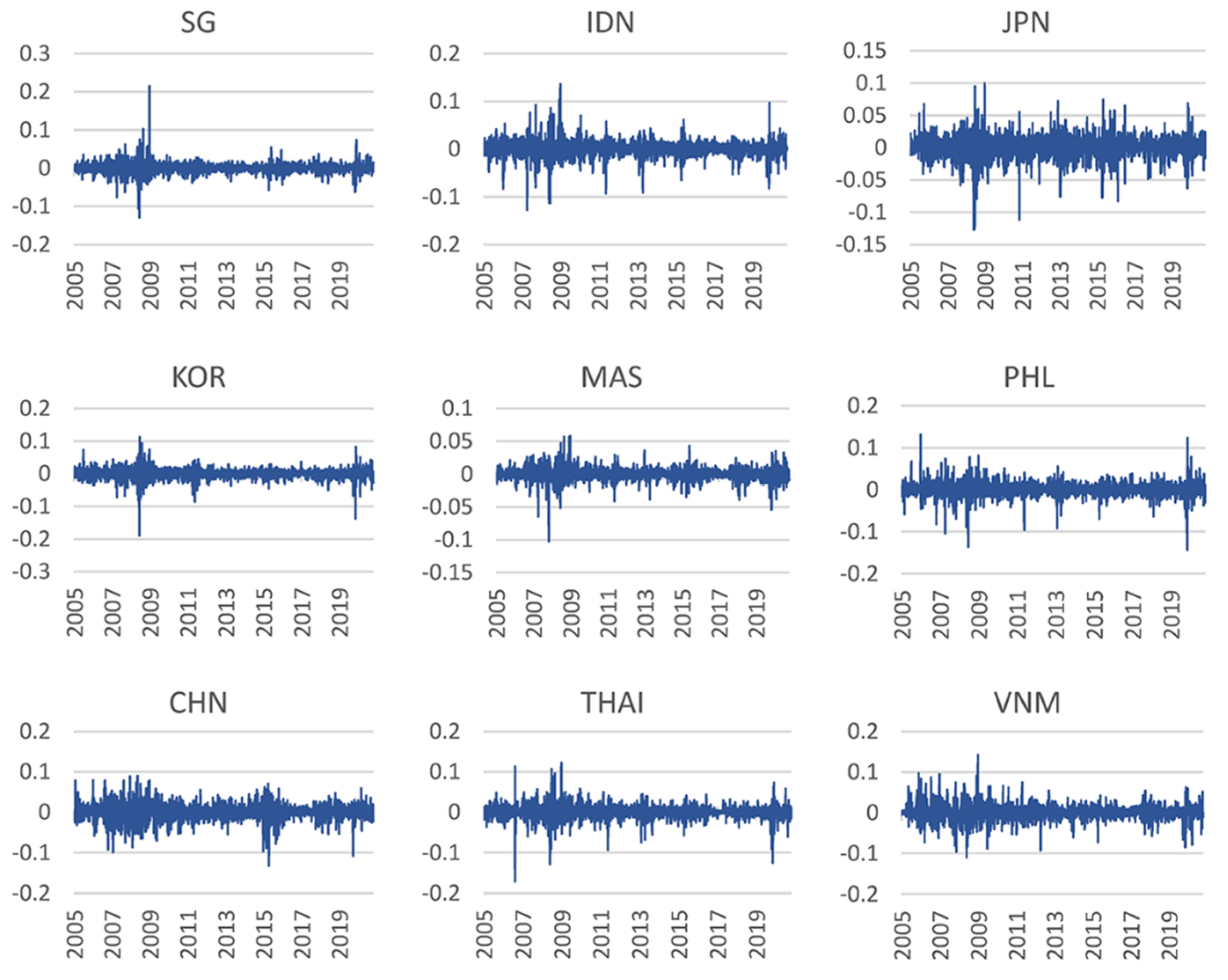

3.4. Data and Variables

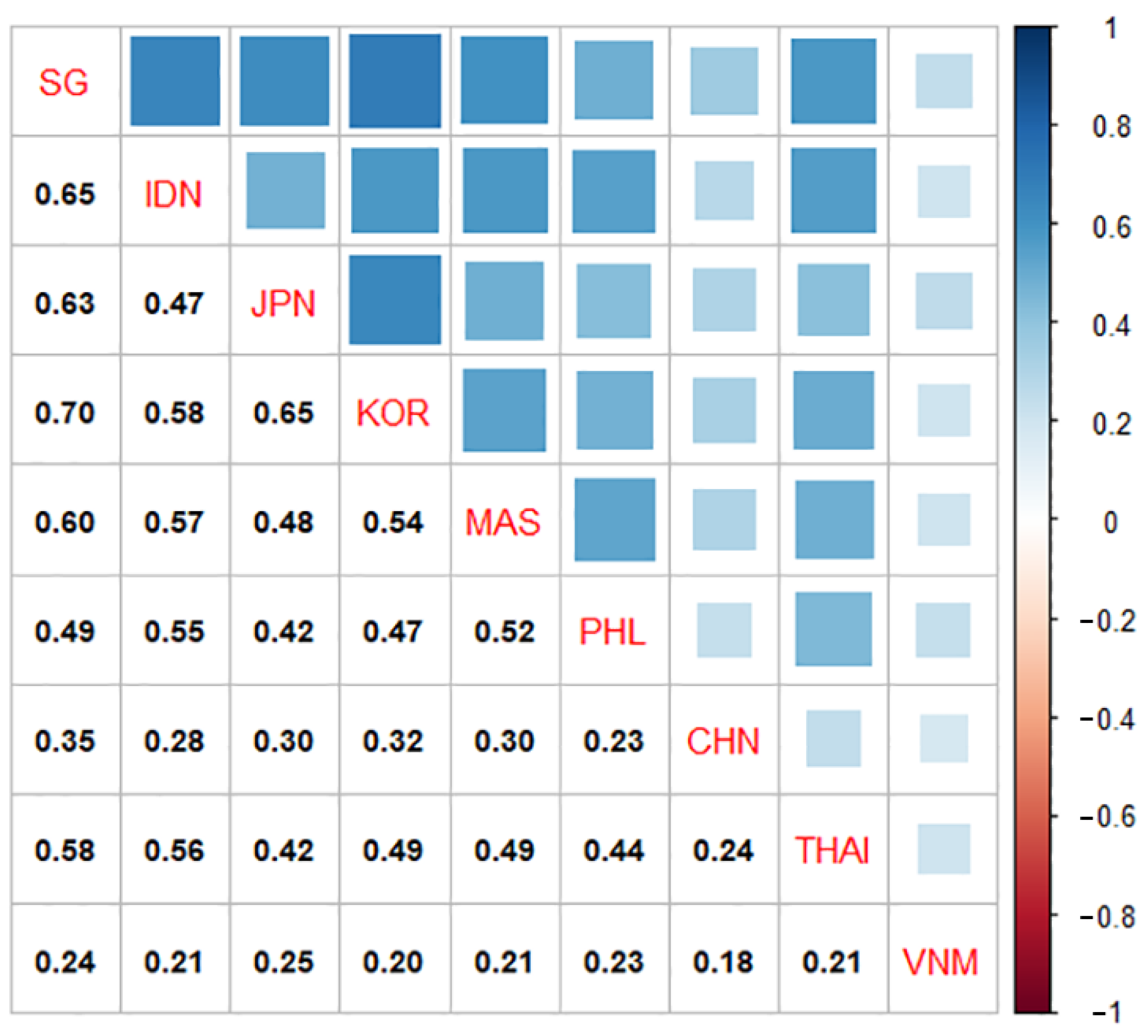

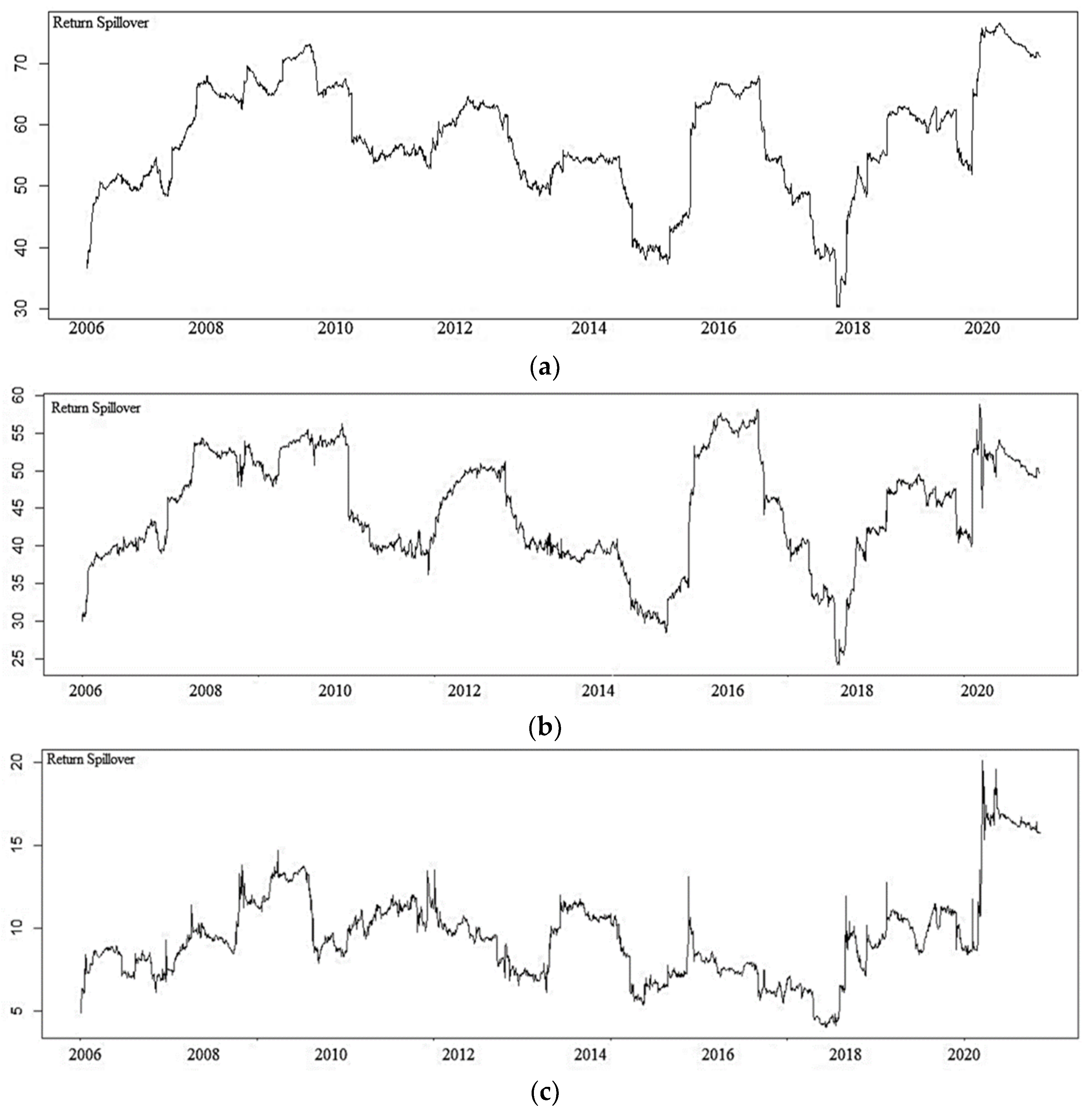

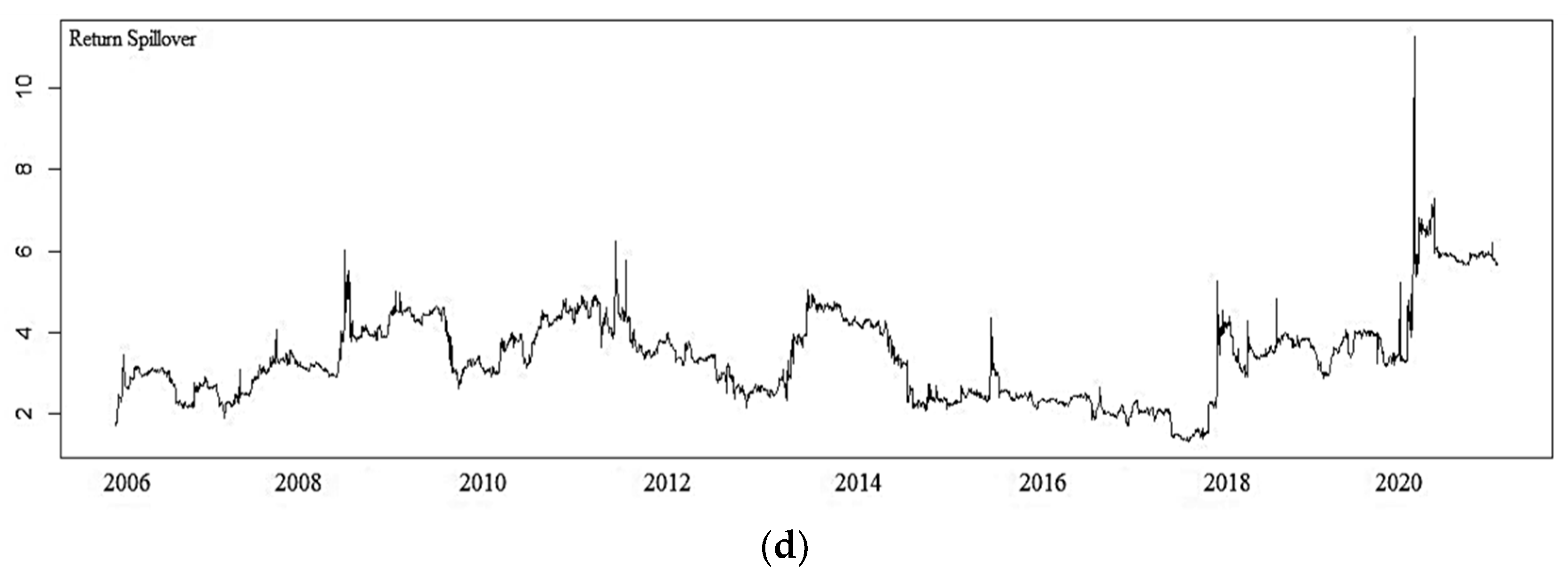

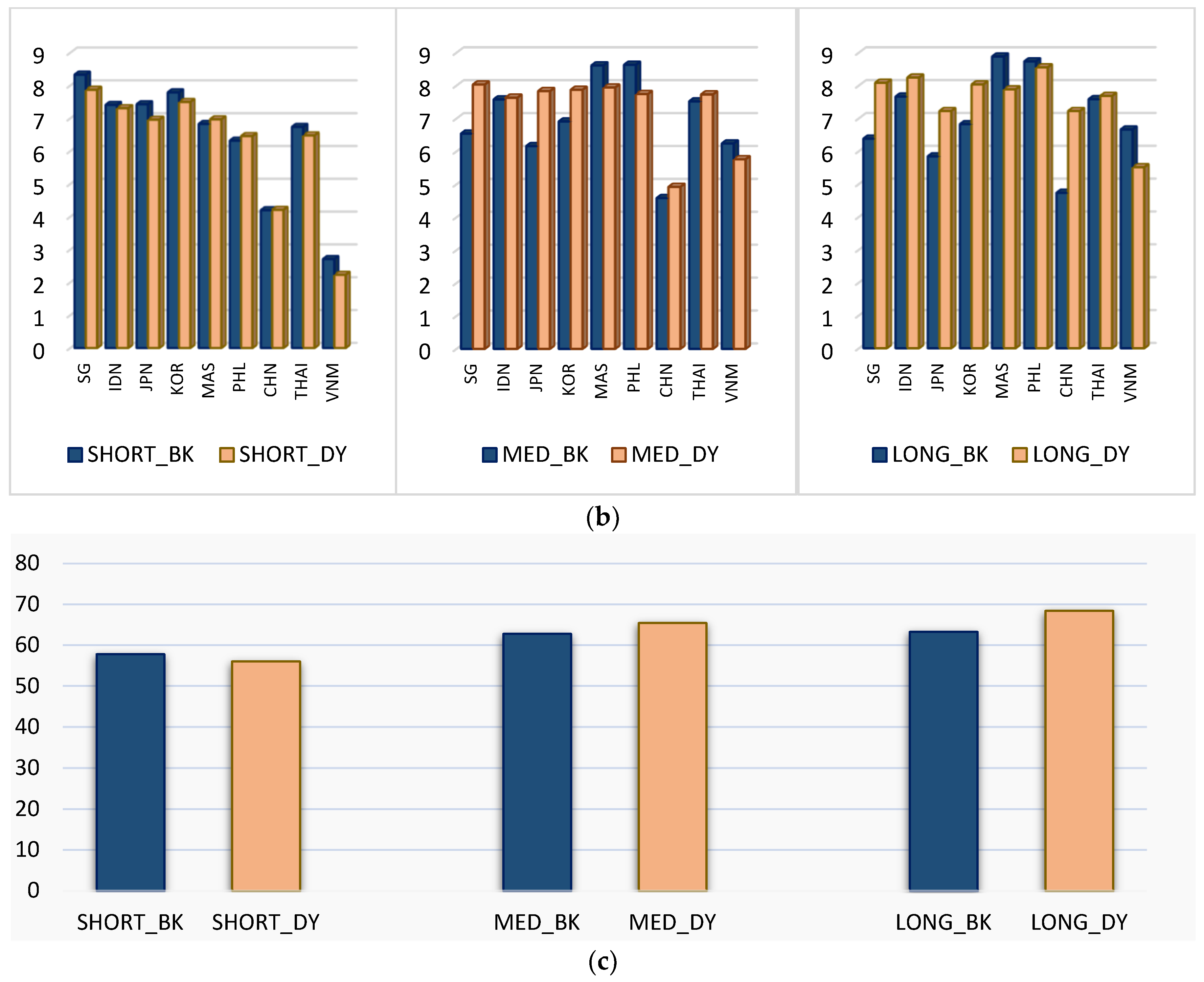

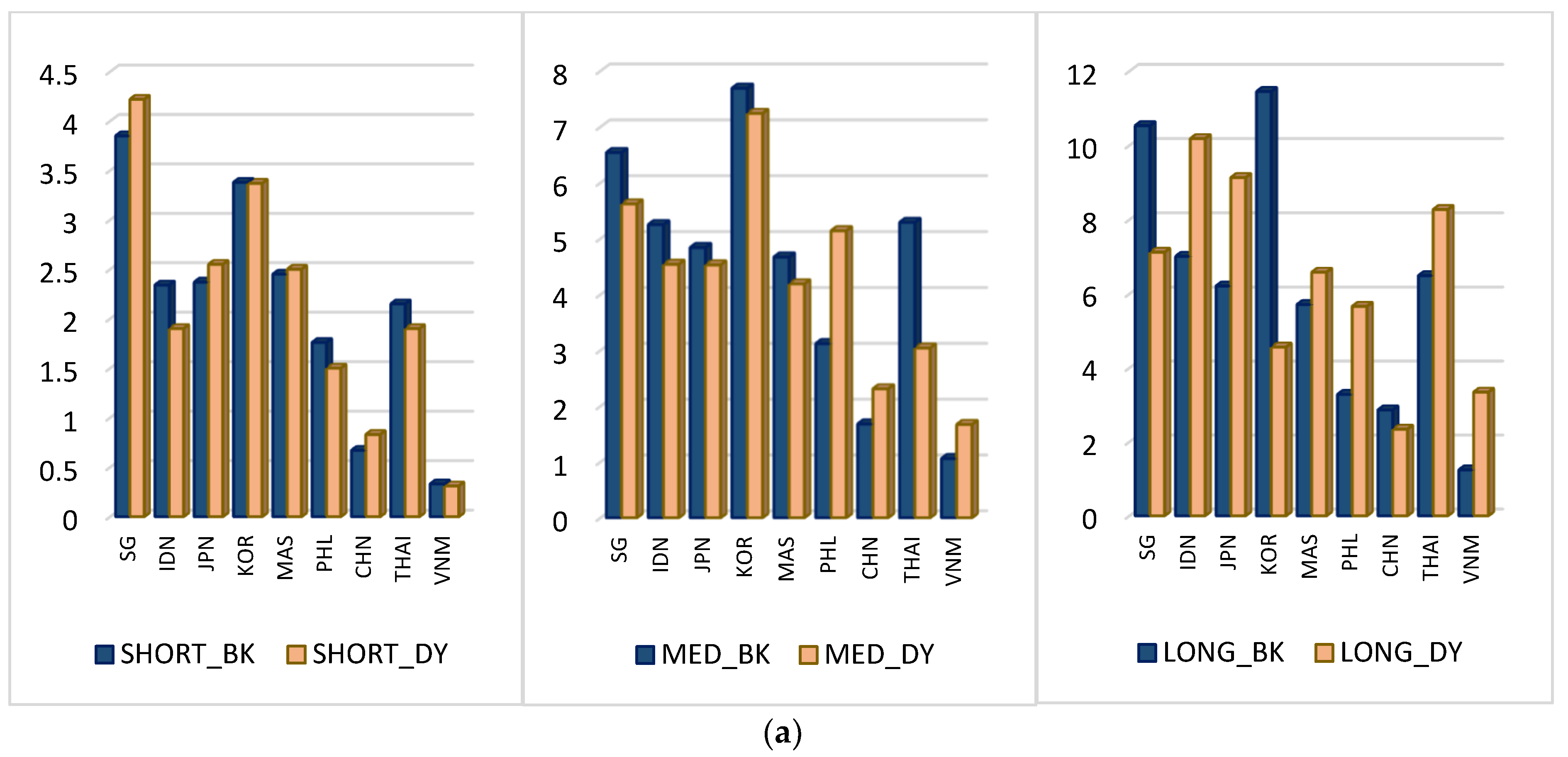

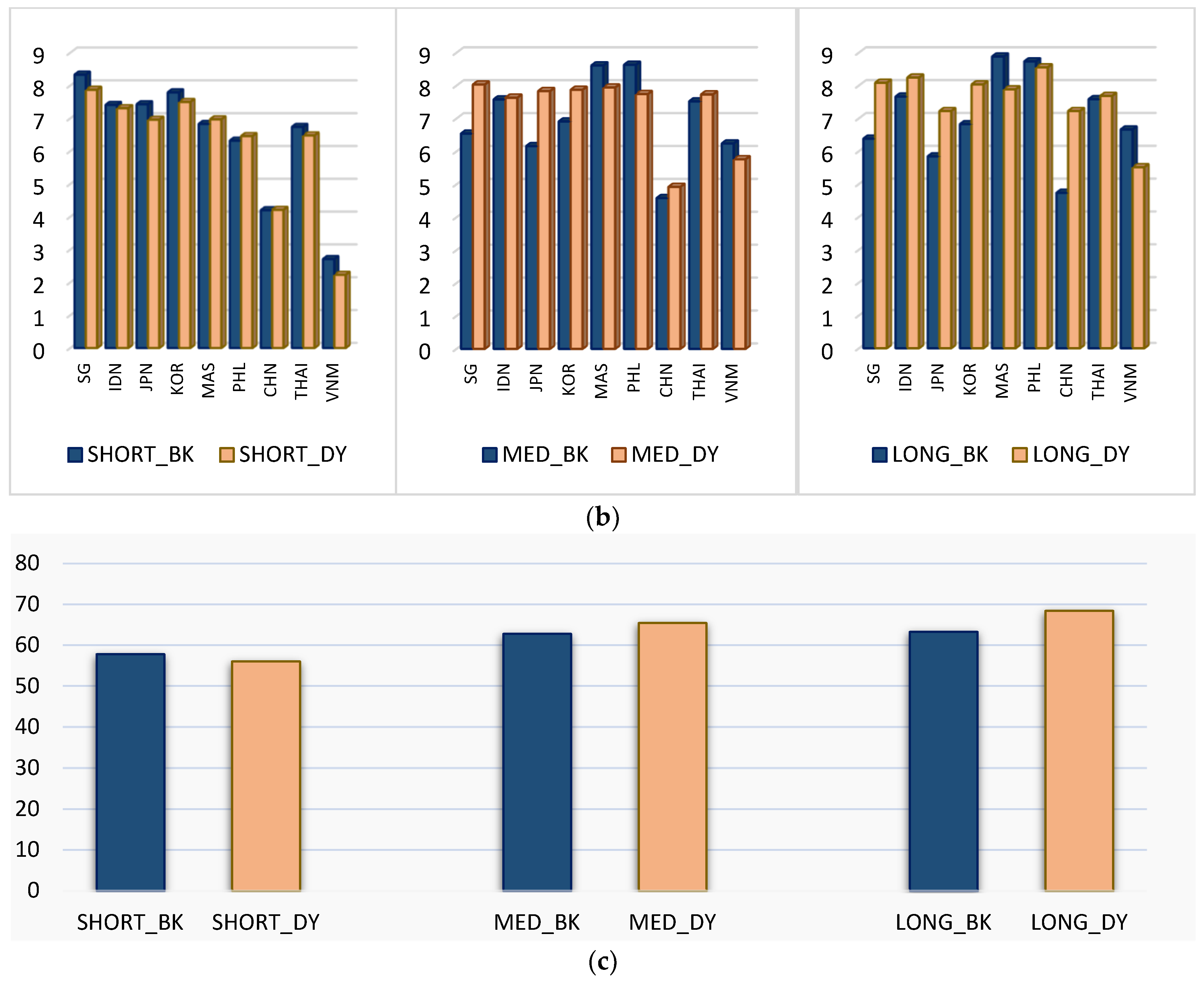

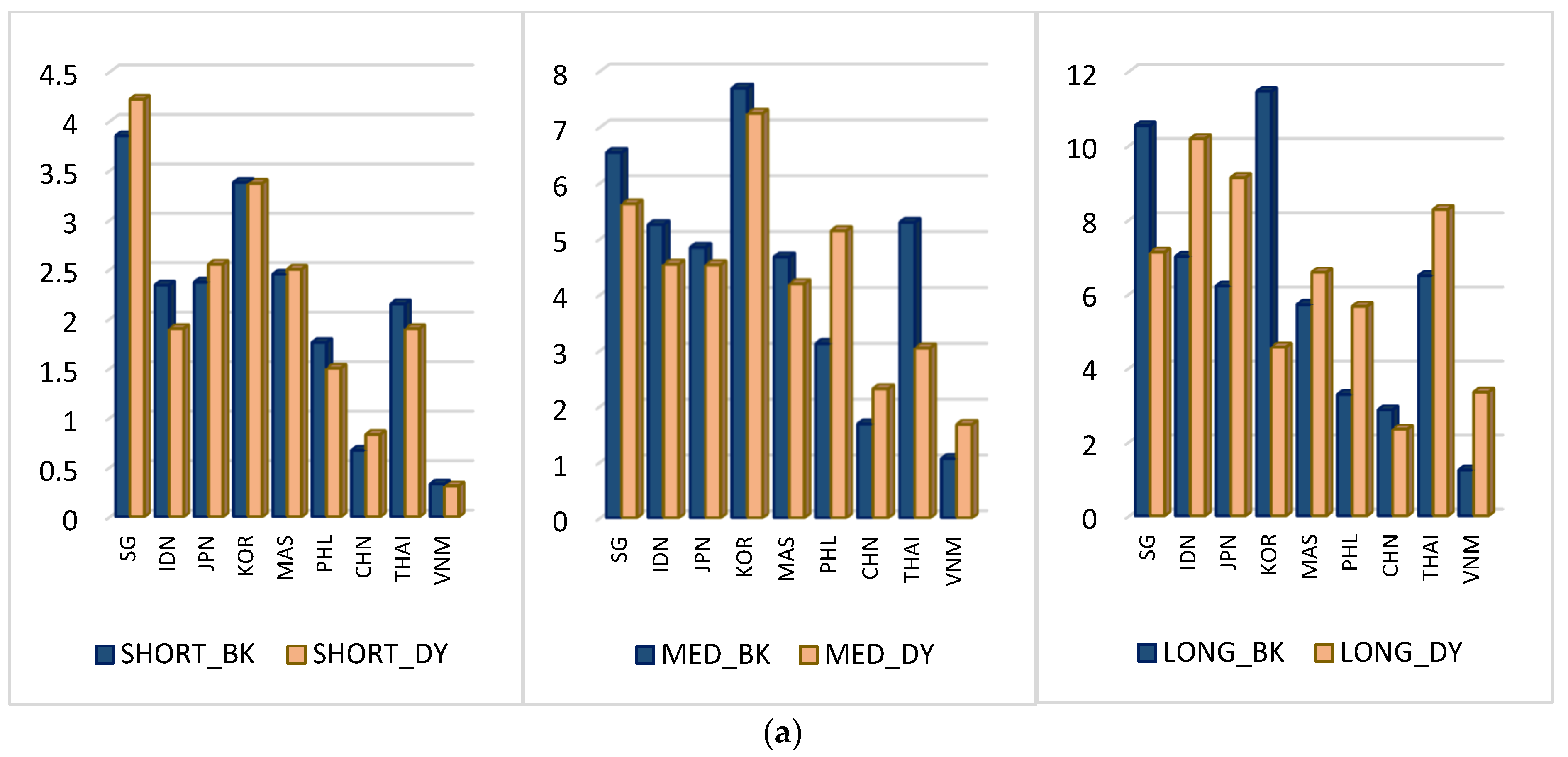

4. Empirical Results

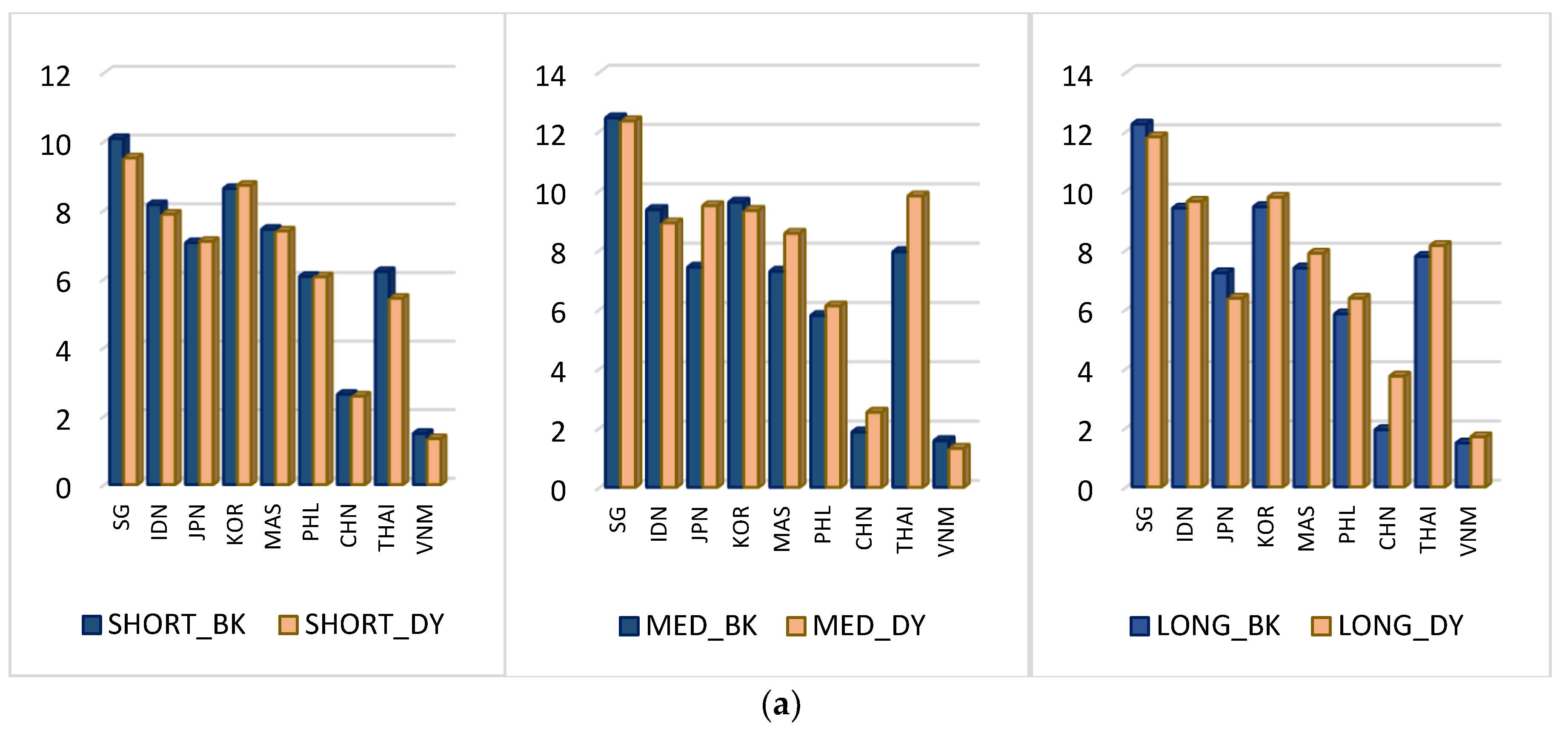

4.1. Static Connectedness

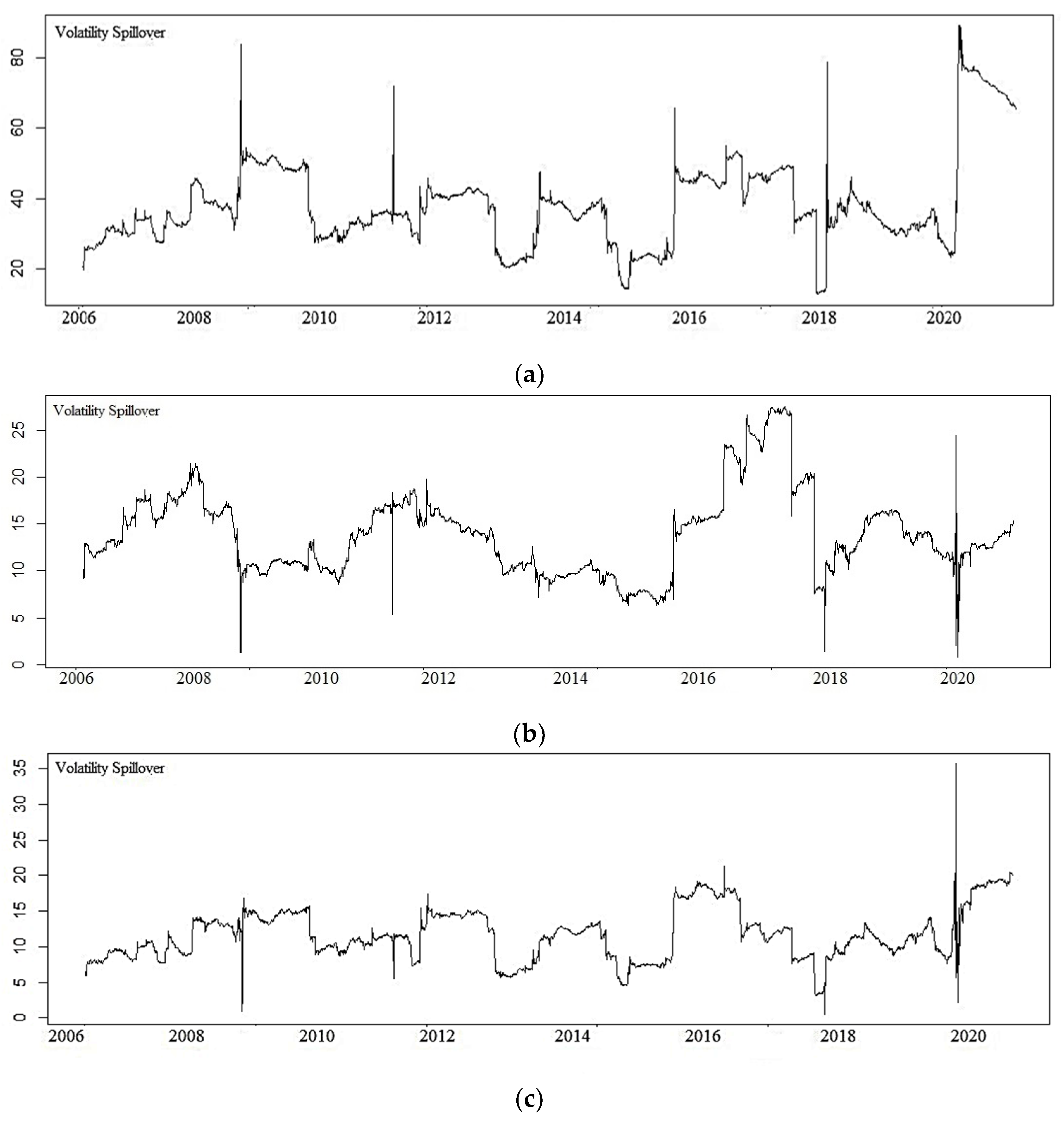

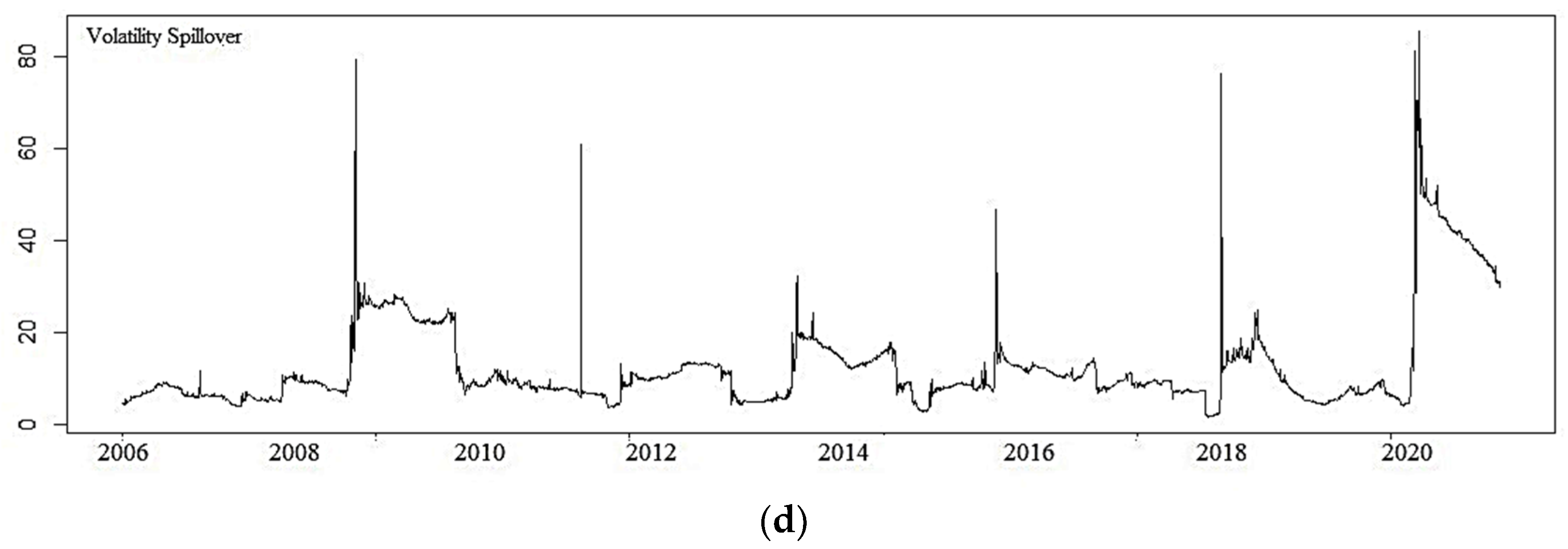

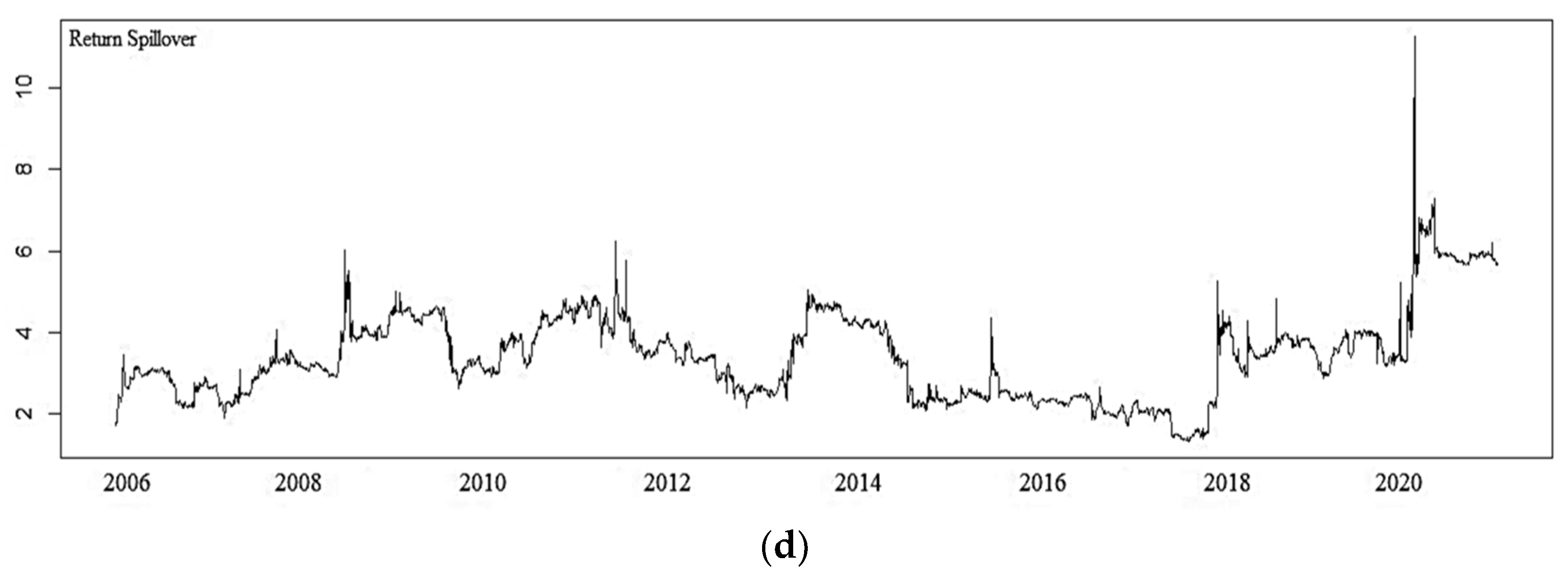

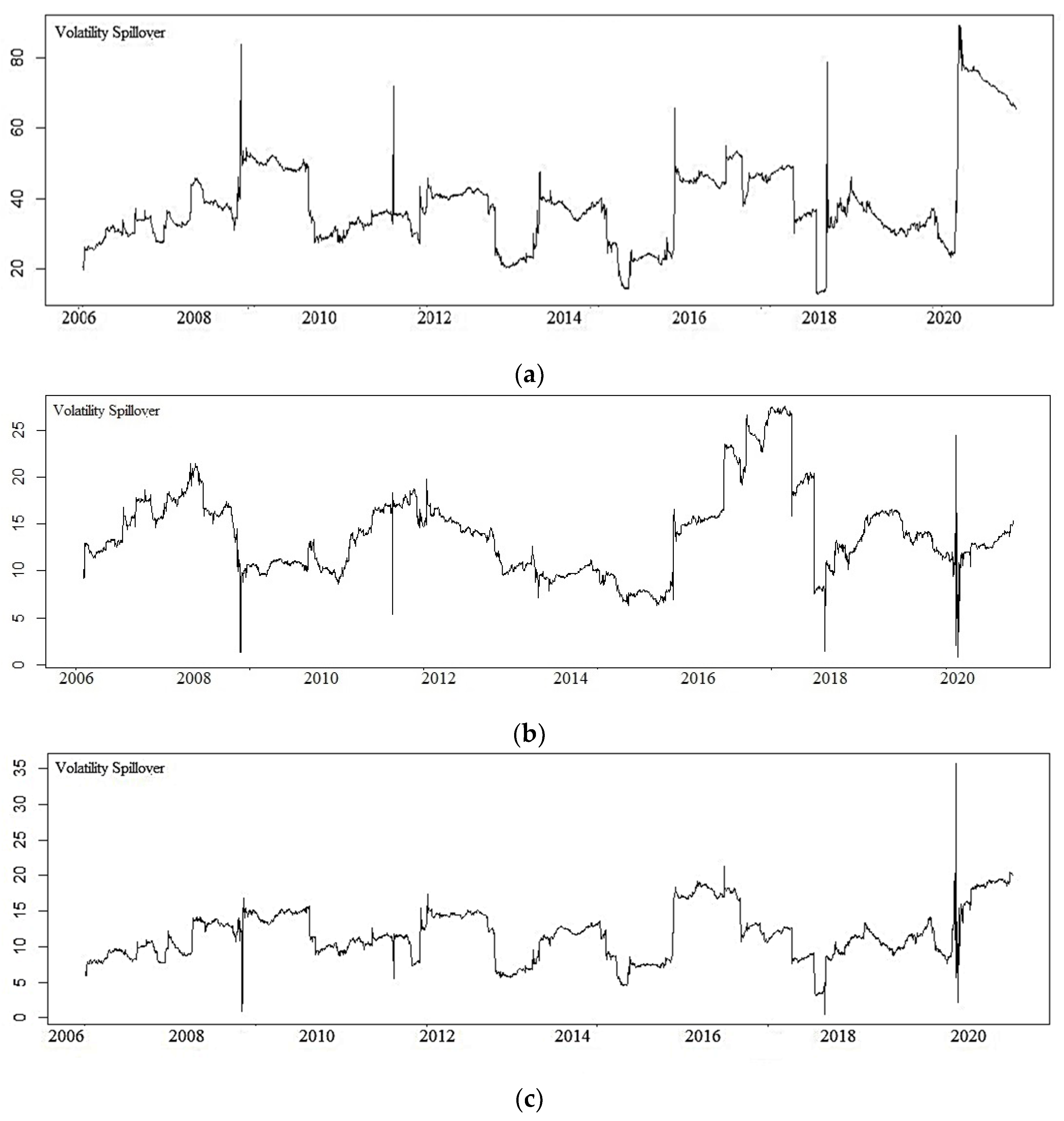

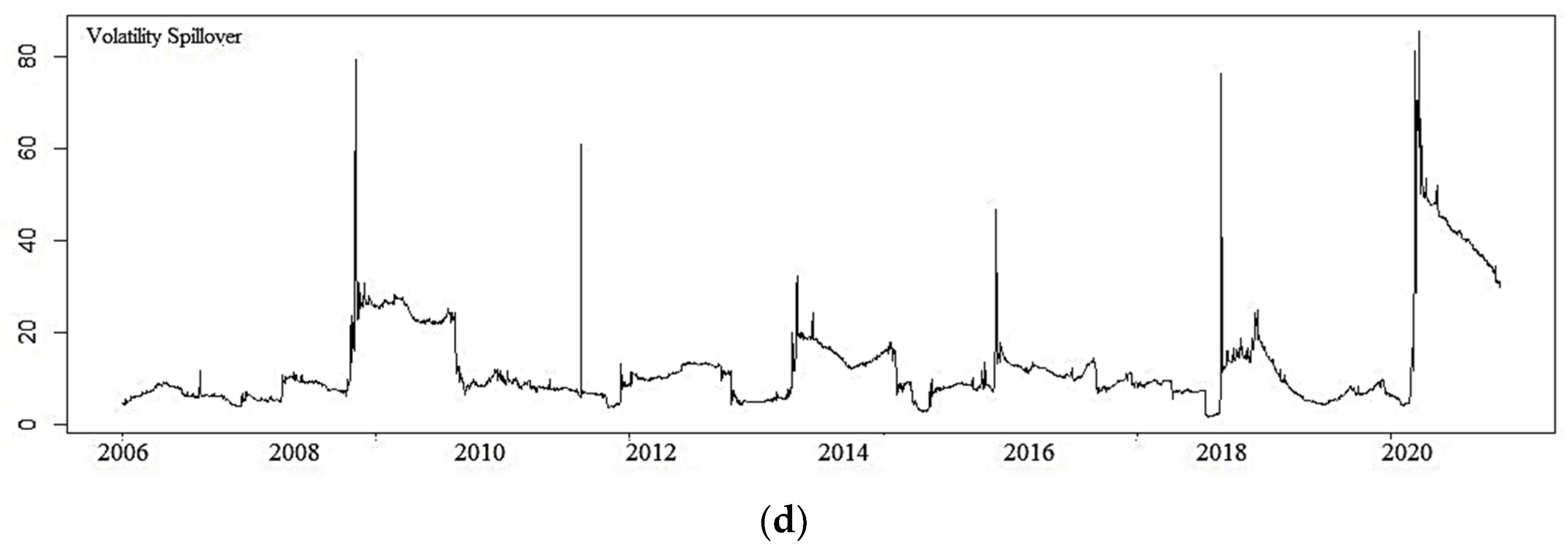

4.2. Dynamic Rolling Connectedness

4.3. Robustness

5. Conclusions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- Dias, R.; Da Silva, J.V.; Dionísio, A. Financial markets of the LAC region: Does the crisis influence the financial integration? Int. Rev. Financ. Anal. 2019, 63, 160–173. [Google Scholar] [CrossRef]

- Jondeau, E.; Rockinger, M. The Copula-GARCH model of conditional dependencies: An international stock market application. J. Int. Money Financ. 2006, 25, 827–853. [Google Scholar] [CrossRef] [Green Version]

- Mokni, K.; Mansouri, F. Conditional dependence between international stock markets: A long-memory GARCH copula model approach. J. Multinatl. Financ. Manag. 2017, 42–43, 116–131. [Google Scholar] [CrossRef]

- Azimili, A. The impact of COVID-19 on the degree of dependence and structure of risk return relationship: A quintile regression approach. Financ. Res. Lett. 2020, 36, 101648. [Google Scholar] [CrossRef] [PubMed]

- Cepoi, C.O. Asymmetric dependence between stock market returns and news during COVID-19 financial turmoil. Financ. Res. Lett. 2020, 36, 101658. [Google Scholar] [CrossRef] [PubMed]

- Topcu, M.; Gulal, O.S. The impact of COVID-19 on emerging stock markets. Financ. Res. Lett. 2020, 36, 101691. [Google Scholar] [CrossRef]

- Sharif, A.; Aloui, C.; Yarovaya, L. COVID-19 pandemic, oil prices, stock market, geopolitical risk and policy uncertainty nexus in the U.S. economy: Fresh evidence from the wavelet-based approach. Int. Rev. Financ. Anal. 2020, 70, 101496. [Google Scholar] [CrossRef]

- Yarovaya, L.; Ahmed, H.E.; Shawkat, M.H. Searching for Safe Havens during the COVID-19 Pandemic: Determinants of Spillovers between Islamic and Conventional Financial Markets. 2020. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3634114 (accessed on 15 July 2021).

- Anh, D.L.T.; Gan, C. The impact of the COVID-19 lockdown on stock market performance: Evidence from Vietnam. J. Econ. Stud. 2021, 48, 836–851. [Google Scholar] [CrossRef]

- Kamaludin, K.; Sundarasen, S.; Ibrahim, I. COVID-19, Dow Jones and equity market movement in ASEAN-5 countries: Evidence from wavelet analyses. Heliyon 2021, 7, e05851. [Google Scholar] [CrossRef]

- Baker, S.R.; Bloom, N.; Davis, S.J.; Kost, K.; Sammon, M.; Viratyosin, T. The unprecedented stock market reaction to COVID-19. Rev. Asset Pricing Stud. 2020, 10, 742–758. [Google Scholar] [CrossRef]

- Ammy-Driss, A.; Garcin, M. Efficiency of the financial markets during the COVID-19 crisis: Time-varying parameters of fractional stable dynamics. arXiv 2020, arXiv:2007.10727. [Google Scholar]

- Hung, N.T. Dynamic spillover effects between oil prices and stock markets: New evidence from pre and during COVID-19 outbreak. AIMS Energy 2020, 8, 819–834. [Google Scholar] [CrossRef]

- McKibbin, W.J.; Vines, D. Global macroeconomic cooperation in response to the COVID-19 pandemic: A roadmap for the G20 and the IMF. Oxf. Rev. Econ. Policy 2020, 36, S297–S337. [Google Scholar] [CrossRef]

- Ali, M.; Nafis, A.; Rizvi, S.A.R. Coronavirus (COVID-19)—An epidemic or pandemic for financial markets. J. Behav. Exp. Financ. 2020, 27, 100341. [Google Scholar] [CrossRef] [PubMed]

- Barro, R.J.; José, F.U.; Joanna, W. The Coronavirus and the Great Influenza Pandemic: Lessons from the “Spanish flu” for the Coronavirus’s Potential Effects on Mortality and Economic Activity; NBER Working Paper No. 26866; National Bureau of Economic Research: Cambridge, MA, USA, 2020. [Google Scholar]

- Zhang, D.; Min, H.; Qiang, J. Financial markets under the global pandemic of COVID-19. Financ. Res. Lett. 2020, 36, 101528. [Google Scholar] [CrossRef] [PubMed]

- King, M.; Sentana, E.; Wadhwani, S. Volatility and links between national stock markets. Econometrica 1994, 62, 901–933. [Google Scholar] [CrossRef]

- Forbes, K.J.; Rigobon, R. No contagion, only interdependence: Measuring stock market comovements. J. Financ. 2002, 57, 223–261. [Google Scholar] [CrossRef]

- Berben, R.P.; Jansen, W.J. Comovement in international equity markets: A sectoral view. J. Int. Money Financ. 2005, 24, 832–857. [Google Scholar] [CrossRef] [Green Version]

- Bartram, S.M.; Taylor, S.J.; Wang, Y.-H. The Euro and European financial market dependence. J. Bank. Financ. 2007, 31, 1461–1481. [Google Scholar] [CrossRef]

- Kasa, K. Common stochastic trends in international stock markets. J. Monet. Econ. 1992, 29, 95–124. [Google Scholar] [CrossRef]

- Manopimoke, P.; Prukumpai, S.; Sethapramote, Y. Dynamic Connectedness in Emerging Asian Equity Markets. In Banking and Finance Issues in Emerging Markets; Barnett, W.A., Sergi, B.S., Eds.; Emerald Publishing Limited: Bingley, UK, 2018; pp. 51–84. [Google Scholar]

- Jiang, Y.; Yu, M.; Hashmi, S.M. The financial crisis and co-movement of global stock markets—A case of six major economies. Sustainability 2017, 9, 260. [Google Scholar] [CrossRef] [Green Version]

- Madaleno, M.; Pinho, C. International stock market indices comovements: A new look. Int. J. Financ. Econ. 2012, 17, 89–102. [Google Scholar] [CrossRef]

- Diebold, F.X.; Yilmaz, K. Measuring financial asset return and volatility spillovers, with application to global equity markets. Econ. J. 2009, 119, 158–171. [Google Scholar] [CrossRef] [Green Version]

- Diebold, F.X.; Yilmaz, K. Better to give than to receive: Predictive directional measurement of volatility spillovers. Int. J. Forecast. 2012, 28, 57–66. [Google Scholar] [CrossRef] [Green Version]

- Diebold, F.X.; Yilmaz, K. On the network topology of variance decompositions: Measuring the connectedness of financial firms. J. Econom. 2014, 182, 119–134. [Google Scholar] [CrossRef] [Green Version]

- Maghyereh, A.I.; Awartani, B.; Al Hilu, K. Dynamic transmissions between the US and equity markets in the MENA countries: New evidence from pre-and post-global financial crisis. Q. Rev. Econ. Financ. 2015, 56, 123–138. [Google Scholar] [CrossRef] [Green Version]

- Mensi, W.; Boubaker, F.Z.; Al-Yahyaee, K.H.; Kang, S.H. Dynamic volatility spillovers and connectedness between global, regional, and GIPSI stock markets. Financ. Res. Lett. 2018, 25, 230–238. [Google Scholar] [CrossRef]

- Kang, S.H.; Uddin, G.S.; Troster, V.; Yoon, S.-M. Directional spillover effects between ASEAN and world stock markets. J. Multinatl. Financ. Manag. 2019, 52, 100592. [Google Scholar] [CrossRef]

- Koop, G.; Pesaran, M.H.; Potter, S.M. Impulse response analysis in non-linear multivariate models. J. Econom. 1996, 74, 119–147. [Google Scholar] [CrossRef]

- Pesaran, M.H.; Shin, Y. Generalized impulse response analysis in linear multivariate models. Econ. Lett. 1998, 58, 17–29. [Google Scholar] [CrossRef]

- Baruník, J.; Křehlík, T. Measuring the frequency dynamics of financial connectedness and systemic risk. J. Financ. Econom. 2018, 16, 271–296. [Google Scholar] [CrossRef]

- Tiwari, A.K.; Cunado, J.; Gupta, R.; Wohar, M.E. Volatility spillovers across global asset classes: Evidence from time and frequency domains. Q. Rev. Econ. Financ. 2018, 70, 194–202. [Google Scholar] [CrossRef]

- Ferrer, R.; Shahzad, S.J.H.; López, R.; Jareño, F. Time and frequency dynamics of connectedness between renewable energy stocks and crude oil prices. Energy Econ. 2018, 76, 1–20. [Google Scholar] [CrossRef]

- Mensi, W.; Hernandez, J.A.; Yoon, S.M.; Vo, X.V.; Kang, S.H. Spillovers and connectedness between major precious metals and major currency markets: The role of frequency factor. Int. Rev. Financ. Anal. 2021, 74, 101672. [Google Scholar] [CrossRef]

- Liao, T.G.; Diaz, J.F. Real GDP growth rates of the ASEAN region: Evidence of spillovers and asymmetric volatility effects. Labu. Bull. Int. Bus. Financ. 2019, 18, 39–61. [Google Scholar]

- Giang, N.K.; Yap, L. Vietnam Is Asia’s Best Stock Market Performer in May. 2020. Available online: https://www.bloomberg.com/news/articles/2020-05-27/inside-asia-s-best-stock-rally-in-may-vietnam-markets-primer (accessed on 3 March 2021).

- Wu, F. Stock market integration in East and South East Asia: The role of global factor. Int. Rev. Financ. Anal. 2020, 67, 101406. [Google Scholar] [CrossRef]

- Karkowska, R.; Urjasz, S. Connectedness structures of sovereign bond markets in Central and Eastern Europe. Int. Rev. Financ. Anal. 2021, 74, 101644. [Google Scholar] [CrossRef]

- Zhang, W.; Hamori, S. Crude oil market and stock markets during the COVID-19 pandemic: Evidence from the US, Japan, and Germany. Int. Rev. Financ. Anal. 2021, 74, 101702. [Google Scholar] [CrossRef]

- The Economist. Spread and Stutter. 2020. Available online: https://www.economist.com/finance-and-economics/2020/02/27/markets-wake-up-with-a-jolt-to-the-implications-of-covid-19 (accessed on 4 March 2021).

- Aslam, F.; Saqib, A.; Duc, K.N.; Khurrum, S.M.; Maaz, K. On the efficiency of foreign exchange markets in times of the COVID-19 pandemic. Technol. Forecast. Soc. Chang. 2020, 161, 120261. [Google Scholar] [CrossRef]

- Lin, W.-L.; Engle, R.F.; Ito, T. Do bulls and bears move across borders? International transmission of stock returns and volatility. Rev. Financ. Stud. 1994, 7, 507–538. [Google Scholar] [CrossRef]

- Onali, E. COVID-19 and Stock Market Volatility. 2020. Available online: https://ssrn.com/abstract=3571453 (accessed on 24 April 2021).

- Al-Awadhi, A.M.; Al-Saifi, K.; Al-Awadhi, A.; Alhammadi, S. Death and contagious infectious diseases: Impact of the COVID-19 virus on stock market returns. J. Behav. Exp. Financ. 2020, 27, 100326. [Google Scholar] [CrossRef] [PubMed]

- Papadamous, S.; Fassas, A.; Kenourgios, D.; Dimitrious, D. Direct and Indirect Effects of COVID-19 Pandemic on Implied Stock Market Volatility: Evidence from Panel Data Analysis. MPRA Paper 100020. 2020. Available online: https://mpra.ub.uni-muenchen.de/100020/1/MPRA_paper_100020.pdf (accessed on 21 May 2021).

- Kwapień, J.; Wątorek, M.; Drożdż, S. Cryptocurrency market consolidation in 2020–2021. Entropy 2021, 23, 1674. [Google Scholar] [CrossRef] [PubMed]

- ASEAN. Overview of ASEAN Plus Three Cooperation, ASEAN Secretariat Information Paper. April 2020. Available online: https://asean.org/storage/2016/01/APT-Overview-Paper-24-Apr-2020.pdf (accessed on 31 December 2020).

- Dias, R.; Pardal, P.; Teixeira, N.; Machoca, V. Financial market integration of ASEAN-5 with China. Littera Scr. 2020, 13, 46–63. [Google Scholar] [CrossRef]

- Pradhan, R.P.; Arvin, B.M.; Norman, N.R.; Nair, M.; Hall, J.H. Insurance penetration and economic growth nexus: Cross-country evidence from ASEAN. Res. Int. Bus. Financ. 2016, 36, 447–458. [Google Scholar] [CrossRef]

- Gulzar, S.; Kayani, G.M.; Feng, H.X.; Ayub, U.; Rafique, A. Financial cointegration and spillover effect of global financial crisis: A study of emerging Asian financial markets. Econ. Res.-Ekon. Istraživanja 2019, 32, 217–318. [Google Scholar] [CrossRef] [Green Version]

- Daubechies, I. Orthonormal bases of compactly supported wavelets. Commun. Pure Appl. Math. 1988, 41, 909–996. [Google Scholar] [CrossRef] [Green Version]

- Daubechies, I. Ten Lectures on Wavelets; Society for Industrial and Applied Mathematics: Philadelphia, PA, USA, 1992. [Google Scholar]

- Toyoshima, Y.; Hamori, S. Measuring the time-frequency dynamics of return and volatility connectedness in global crude oil markets. Energies 2018, 11, 2893. [Google Scholar] [CrossRef] [Green Version]

- Lovcha, Y.; Perez-Laborda, A. Dynamic frequency connectedness between oil and natural gas volatilities. Econ. Model. 2020, 84, 181–189. [Google Scholar] [CrossRef]

- Wahyudi, S.; Najmudin, L.R.; Rachmawati, R. Assessing the contagion effect on herding behaviour under segmented and integrated stock markets circumstances in the USA, China, and ASEAN-5. Econ. Ann.-XXI 2018, 169, 15–20. [Google Scholar] [CrossRef] [Green Version]

- Liu, T.; Hamori, S. Spillovers to renewable energy stocks in the US and Europe: Are they different? Energies 2020, 13, 3162. [Google Scholar] [CrossRef]

- Wang, X.; Wang, Y. Volatility spillovers between crude oil and Chinese sectoral equity markets: Evidence from a frequency dynamics perspective. Energy Econ. 2019, 80, 995–1009. [Google Scholar] [CrossRef]

- Maghyereh, A.I.; Abdoh, H.; Awartani, B. Connectedness and hedging between gold and Islamic securities: A new evidence from time-frequency domain approaches. Pac. Basin Financ. J. 2019, 54, 13–28. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| CTY | Mean | Max | Min | SD | Skew | Kurt | JB | ADF | KPSS | |

|---|---|---|---|---|---|---|---|---|---|---|

| Singapore | SG | 0.0001 | 0.2147 | −0.1293 | 0.0132 | 1.027 | 35.72 | 130,482 * | −53.96 * | a 0.034 |

| Indonesia | IDN | 0.0006 | 0.1362 | −0.1277 | 0.0156 | −0.529 | 14.75 | 16,886 * | −50.27 * | a 0.196 |

| Japan | JPN | 0.0003 | 0.0999 | −0.1272 | 0.0167 | −0.666 | 10.03 | 6215 * | −55.36 * | a 0.160 |

| Korea | KOR | 0.0004 | 0.1128 | −0.1895 | 0.0148 | −1.187 | 20.33 | 37,132 * | −54.92 * | a 0.081 |

| Malaysia | MAS | 0.0002 | 0.0581 | −0.1024 | 0.0089 | −0.778 | 15.25 | 18,516 * | −49.89 * | a 0.218 |

| Philippine | PHL | 0.0004 | 0.1313 | −0.1432 | 0.0157 | −0.563 | 15.12 | 17,970 * | −54.38 * | a 0.171 |

| China | CHN | 0.0004 | 0.0903 | −0.1324 | 0.0186 | −0.491 | 7.87 | 2996 * | −52.18 * | a 0.174 |

| Thailand | THAI | 0.0002 | 0.1224 | −0.1709 | 0.0158 | −0.757 | 17.09 | 24,379 * | −53.16 * | a 0.079 |

| Vietnam | VNM | 0.0005 | 0.1419 | −0.1093 | 0.0179 | −0.03 | 8.27 | 3376 * | −45.98 * | a 0.092 |

| Panel A. Diebold–Yilmaz Method (2012) | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| SG | IDN | JPN | KOR | MAS | PHL | CHN | THAI | VNM | FROM_ABS | ||

| SG | 28.81 | 12.34 | 11.51 | 13.95 | 10.65 | 7.24 | 3.74 | 9.84 | 1.91 | 7.91 | |

| IDN | 14.20 | 32.92 | 7.22 | 11.06 | 10.58 | 9.85 | 2.46 | 10.32 | 1.40 | 7.45 | |

| JPN | 14.56 | 8.02 | 35.95 | 14.91 | 8.10 | 6.28 | 3.26 | 6.68 | 2.25 | 7.12 | |

| KOR | 15.44 | 10.62 | 13.19 | 31.73 | 8.93 | 7.28 | 3.27 | 8.14 | 1.39 | 7.59 | |

| MAS | 13.27 | 11.75 | 7.83 | 10.02 | 34.70 | 9.31 | 3.03 | 8.78 | 1.30 | 7.26 | |

| PHL | 10.59 | 12.14 | 6.99 | 9.42 | 10.52 | 38.28 | 2.06 | 8.24 | 1.76 | 6.86 | |

| CHN | 7.99 | 4.76 | 5.47 | 6.25 | 5.39 | 3.16 | 61.36 | 3.72 | 1.90 | 4.29 | |

| THAI | 13.07 | 12.00 | 7.06 | 9.81 | 9.00 | 7.60 | 2.24 | 37.69 | 1.53 | 6.92 | |

| VNM | 6.24 | 4.37 | 4.63 | 4.05 | 3.60 | 3.39 | 2.13 | 3.53 | 68.06 | 3.55 | |

| TO | 10.60 | 8.44 | 7.10 | 8.83 | 7.42 | 6.01 | 2.47 | 6.58 | 1.49 | 58.94 | |

| NET_ABS | 2.69 | 0.99 | −0.02 | 1.25 | 0.16 | −0.85 | −1.83 | −0.34 | −2.06 | ||

| Panel B. Baruník–Křehlík method (2018)—Spillover for band 3.14 to 0.63 (roughly to 1 day to 5 days). | |||||||||||

| SG | IDN | JPN | KOR | MAS | PHL | CHN | THAI | VNM | FROM_ABS | FROM_WTH | |

| SG | 23.43 | 9.99 | 9.38 | 11.31 | 8.69 | 5.8 | 3.25 | 7.79 | 1.51 | 6.41 | 8.33 |

| IDN | 10.67 | 26.02 | 5.58 | 8.23 | 8.2 | 7.74 | 2.03 | 7.79 | 1.09 | 5.7 | 7.41 |

| JPN | 11.31 | 6.42 | 29.6 | 12.14 | 6.6 | 5.3 | 2.83 | 5.01 | 1.84 | 5.72 | 7.43 |

| KOR | 11.99 | 8.45 | 10.69 | 25.76 | 7.12 | 5.83 | 2.75 | 6.05 | 1.11 | 6 | 7.79 |

| MAS | 9.46 | 8.42 | 5.86 | 7.21 | 26.76 | 6.91 | 2.39 | 6.05 | 0.98 | 5.25 | 6.83 |

| PHL | 7.26 | 8.65 | 4.9 | 6.66 | 7.65 | 30.73 | 1.6 | 5.7 | 1.35 | 4.86 | 6.32 |

| CHN | 5.89 | 3.42 | 4.3 | 4.87 | 4.17 | 2.36 | 49.77 | 2.71 | 1.35 | 3.23 | 4.2 |

| THAI | 9.8 | 8.87 | 5.13 | 7.06 | 6.97 | 5.85 | 1.91 | 29.94 | 1.09 | 5.19 | 6.74 |

| VNM | 3.46 | 2.3 | 2.98 | 2.28 | 2.11 | 2.23 | 1.48 | 1.93 | 50.59 | 2.09 | 2.71 |

| TO_ABS | 7.76 | 6.28 | 5.42 | 6.64 | 5.72 | 4.67 | 2.03 | 4.78 | 1.14 | 44.45 | |

| TO_WTH | 10.08 | 8.16 | 7.05 | 8.63 | 7.44 | 6.07 | 2.63 | 6.21 | 1.49 | 57.76 | |

| NET ABS | 1.35 | 0.58 | −0.3 | 0.64 | 0.47 | −0.19 | −1.2 | −0.41 | −0.95 | ||

| Panel C. Baruník–Křehlík method (2018)—Spillover for band 0.63 to 0.15 (roughly 6 days to 21 days). | |||||||||||

| SG | IDN | JPN | KOR | MAS | PHL | CHN | THAI | VNM | FROM_ABS | FROM_WTH | |

| SG | 3.96 | 1.74 | 1.56 | 1.94 | 1.45 | 1.06 | 0.37 | 1.5 | 0.29 | 1.1 | 6.54 |

| IDN | 2.57 | 5.08 | 1.19 | 2.05 | 1.74 | 1.55 | 0.32 | 1.84 | 0.22 | 1.28 | 7.58 |

| JPN | 2.39 | 1.19 | 4.69 | 2.05 | 1.12 | 0.73 | 0.32 | 1.23 | 0.3 | 1.04 | 6.16 |

| KOR | 2.52 | 1.61 | 1.83 | 4.39 | 1.33 | 1.07 | 0.38 | 1.53 | 0.2 | 1.16 | 6.91 |

| MAS | 2.76 | 2.43 | 1.43 | 2.03 | 5.81 | 1.74 | 0.46 | 1.97 | 0.23 | 1.45 | 8.61 |

| PHL | 2.42 | 2.55 | 1.52 | 2.01 | 2.1 | 5.54 | 0.35 | 1.84 | 0.3 | 1.45 | 8.63 |

| CHN | 1.52 | 0.97 | 0.85 | 1 | 0.89 | 0.58 | 8.57 | 0.73 | 0.39 | 0.77 | 4.58 |

| THAI | 2.37 | 2.29 | 1.39 | 2 | 1.49 | 1.28 | 0.25 | 5.67 | 0.32 | 1.27 | 7.52 |

| VNM | 2 | 1.48 | 1.18 | 1.26 | 1.08 | 0.84 | 0.47 | 1.14 | 12.7 | 1.05 | 6.24 |

| TO_ABS | 2.06 | 1.58 | 1.22 | 1.59 | 1.24 | 0.98 | 0.32 | 1.31 | 0.25 | 10.57 | |

| TO_WTH | 12.25 | 9.41 | 7.23 | 9.46 | 7.39 | 5.84 | 1.93 | 7.78 | 1.48 | 62.77 | |

| NET ABS | 0.96 | 0.3 | 0.18 | 0.43 | −0.21 | −0.47 | −0.45 | 0.04 | −0.8 | ||

| Panel D. Baruník–Křehlík method (2018)—Spillover for band 0.15 to 0 (roughly 21 days to infinity). | |||||||||||

| SG | IDN | JPN | KOR | MAS | PHL | CHN | THAI | VNM | FROM_ABS | FROM_WTH | |

| SG | 1.42 | 0.62 | 0.57 | 0.7 | 0.51 | 0.38 | 0.13 | 0.55 | 0.11 | 0.4 | 6.38 |

| IDN | 0.96 | 1.82 | 0.45 | 0.77 | 0.64 | 0.57 | 0.11 | 0.69 | 0.09 | 0.48 | 7.66 |

| JPN | 0.85 | 0.41 | 1.66 | 0.72 | 0.38 | 0.24 | 0.11 | 0.44 | 0.11 | 0.36 | 5.84 |

| KOR | 0.93 | 0.57 | 0.67 | 1.59 | 0.48 | 0.38 | 0.14 | 0.57 | 0.08 | 0.42 | 6.82 |

| MAS | 1.05 | 0.9 | 0.55 | 0.78 | 2.14 | 0.66 | 0.17 | 0.76 | 0.09 | 0.55 | 8.88 |

| PHL | 0.91 | 0.94 | 0.58 | 0.75 | 0.77 | 2.01 | 0.12 | 0.7 | 0.11 | 0.54 | 8.73 |

| CHN | 0.58 | 0.37 | 0.32 | 0.38 | 0.33 | 0.22 | 3.02 | 0.28 | 0.16 | 0.29 | 4.73 |

| THAI | 0.9 | 0.84 | 0.53 | 0.76 | 0.54 | 0.46 | 0.09 | 2.08 | 0.12 | 0.47 | 7.58 |

| VNM | 0.79 | 0.58 | 0.47 | 0.51 | 0.41 | 0.32 | 0.18 | 0.46 | 4.77 | 0.41 | 6.66 |

| TO_ABS | 0.77 | 0.58 | 0.46 | 0.6 | 0.45 | 0.36 | 0.12 | 0.49 | 0.1 | 3.93 | |

| TO_WTH | 12.45 | 9.36 | 7.42 | 9.61 | 7.28 | 5.79 | 1.86 | 7.94 | 1.57 | 63.29 | |

| NET ABS | 0.37 | 0.1 | 0.1 | 0.18 | −0.1 | −0.18 | −0.17 | 0.02 | −0.31 | ||

| Panel A. Diebold–Yilmaz method (2012) | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| SG | IDN | JPN | KOR | MAS | PHL | CHN | THAI | VNM | FROM | ||

| SG | 65.30 | 5.47 | 4.42 | 11.55 | 5.00 | 2.13 | 2.34 | 3.43 | 0.34 | 3.86 | |

| IDN | 9.49 | 51.69 | 5.34 | 11.00 | 6.64 | 4.65 | 1.95 | 7.99 | 1.26 | 5.37 | |

| JPN | 8.77 | 5.63 | 53.25 | 15.27 | 3.95 | 2.82 | 2.54 | 6.21 | 1.56 | 5.19 | |

| KOR | 14.58 | 7.41 | 10.75 | 48.15 | 5.73 | 2.80 | 2.57 | 6.96 | 1.05 | 5.76 | |

| MAS | 10.35 | 7.31 | 4.50 | 9.24 | 52.27 | 4.97 | 3.59 | 6.87 | 0.90 | 5.30 | |

| PHL | 5.71 | 6.84 | 4.97 | 6.94 | 6.47 | 59.93 | 1.03 | 6.76 | 1.35 | 4.45 | |

| CHN | 8.01 | 2.43 | 2.83 | 4.11 | 4.01 | 0.65 | 75.80 | 1.87 | 0.28 | 2.69 | |

| THAI | 8.32 | 8.49 | 5.48 | 9.80 | 5.75 | 5.47 | 1.75 | 53.57 | 1.37 | 5.16 | |

| VNM | 0.45 | 1.75 | 3.21 | 2.68 | 1.95 | 1.32 | 0.77 | 2.92 | 84.95 | 1.67 | |

| TO | 7.30 | 5.04 | 4.61 | 7.84 | 4.39 | 2.76 | 1.84 | 4.78 | 0.90 | 39.45 | |

| NET_ABS | 3.44 | −0.33 | −0.58 | 2.08 | −0.92 | −1.70 | −0.85 | −0.38 | −0.77 | ||

| Panel B. Baruník–Křehlík method (2018)—Spillover for band 3.14 to 0.63 (roughly to 1 day to 5 days). | |||||||||||

| SG | IDN | JPN | KOR | MAS | PHL | CHN | THAI | VNM | FROM_ABS | FROM_WTH | |

| SG | 10.93 | 0.83 | 0.96 | 1.55 | 1.18 | 0.47 | 0.37 | 0.81 | 0.03 | 0.69 | 2.18 |

| IDN | 1.51 | 22.02 | 0.54 | 0.84 | 1.17 | 1 | 0.18 | 1.06 | 0.06 | 0.71 | 2.24 |

| JPN | 1.58 | 0.6 | 22.32 | 3.19 | 0.72 | 0.44 | 0.26 | 0.64 | 0.3 | 0.86 | 2.72 |

| KOR | 1.89 | 0.59 | 2.24 | 14.74 | 0.7 | 0.62 | 0.23 | 0.54 | 0.09 | 0.77 | 2.43 |

| MAS | 2.34 | 1.29 | 0.78 | 1.13 | 25.46 | 0.89 | 0.4 | 1.27 | 0.1 | 0.91 | 2.89 |

| PHL | 1.2 | 1.68 | 0.69 | 1.39 | 1.16 | 35.53 | 0.12 | 1.35 | 0.16 | 0.86 | 2.73 |

| CHN | 0.85 | 0.3 | 0.34 | 0.44 | 0.5 | 0.1 | 28.58 | 0.24 | 0.07 | 0.32 | 1 |

| THAI | 1.53 | 1.28 | 0.65 | 0.84 | 1.35 | 1.3 | 0.2 | 26.38 | 0.11 | 0.81 | 2.56 |

| VNM | 0.05 | 0.1 | 0.51 | 0.23 | 0.18 | 0.18 | 0.14 | 0.18 | 43.26 | 0.17 | 0.55 |

| TO_ABS | 1.22 | 0.74 | 0.75 | 1.07 | 0.77 | 0.56 | 0.21 | 0.68 | 0.1 | 6.09 | |

| TO_WTH | 3.85 | 2.34 | 2.37 | 3.38 | 2.45 | 1.76 | 0.67 | 2.15 | 0.33 | 19.3 | |

| NET ABS | 0.53 | 0.03 | −0.11 | 0.3 | −0.14 | −0.3 | −0.11 | −0.13 | −0.07 | ||

| Panel C. Baruník–Křehlík method (2018)—Spillover for band 0.63 to 0.15 (roughly 6 days to 21 days). | |||||||||||

| SG | IDN | JPN | KOR | MAS | PHL | CHN | THAI | VNM | FROM_ABS | FROM_WTH | |

| SG | 14.45 | 1.36 | 1.32 | 2.88 | 1.27 | 0.62 | 0.5 | 0.99 | 0.06 | 1 | 3.55 |

| IDN | 2.49 | 14.82 | 1.53 | 3.13 | 1.97 | 1.45 | 0.47 | 2.47 | 0.43 | 1.55 | 5.49 |

| JPN | 2.21 | 1.67 | 15.91 | 4.29 | 1.03 | 0.9 | 0.68 | 2.02 | 0.49 | 1.48 | 5.24 |

| KOR | 3.43 | 2.07 | 3.07 | 13.56 | 1.6 | 0.67 | 0.6 | 2.12 | 0.34 | 1.54 | 5.47 |

| MAS | 2.74 | 2.2 | 1.21 | 2.64 | 14.59 | 1.82 | 1.13 | 2.09 | 0.28 | 1.57 | 5.56 |

| PHL | 1.61 | 2.08 | 1.68 | 1.86 | 2.37 | 14.91 | 0.25 | 2.25 | 0.5 | 1.4 | 4.97 |

| CHN | 1.91 | 0.64 | 0.86 | 1.02 | 1.32 | 0.15 | 24.74 | 0.51 | 0.1 | 0.72 | 2.57 |

| THAI | 2.13 | 2.71 | 1.67 | 2.89 | 1.6 | 1.88 | 0.43 | 14.54 | 0.49 | 1.53 | 5.44 |

| VNM | 0.08 | 0.58 | 0.94 | 0.82 | 0.69 | 0.43 | 0.22 | 0.97 | 24.39 | 0.52 | 1.86 |

| TO_ABS | 1.85 | 1.48 | 1.37 | 2.17 | 1.32 | 0.88 | 0.48 | 1.49 | 0.3 | 11.32 | |

| TO_WTH | 6.54 | 5.25 | 4.84 | 7.69 | 4.67 | 3.12 | 1.68 | 5.29 | 1.06 | 40.15 | |

| NET ABS | 0.85 | −0.07 | −0.11 | 0.63 | −0.25 | −0.52 | −0.24 | −0.04 | −0.22 | ||

| Panel D. Baruník–Křehlík method (2018)—Spillover for band 0.15 to 0 (roughly 21 days to infinity). | |||||||||||

| SG | IDN | JPN | KOR | MAS | PHL | CHN | THAI | VNM | FROM_ABS | FROM_WTH | |

| SG | 39.93 | 3.28 | 2.14 | 7.12 | 2.55 | 1.03 | 1.48 | 1.64 | 0.25 | 2.17 | 5.38 |

| IDN | 5.49 | 14.85 | 3.27 | 7.03 | 3.49 | 2.19 | 1.3 | 4.46 | 0.77 | 3.11 | 7.73 |

| JPN | 4.98 | 3.36 | 15.03 | 7.8 | 2.19 | 1.48 | 1.59 | 3.54 | 0.77 | 2.86 | 7.1 |

| KOR | 9.25 | 4.75 | 5.44 | 19.84 | 3.44 | 1.51 | 1.74 | 4.3 | 0.61 | 3.45 | 8.57 |

| MAS | 5.27 | 3.82 | 2.5 | 5.47 | 12.22 | 2.26 | 2.06 | 3.51 | 0.51 | 2.82 | 7.02 |

| PHL | 2.89 | 3.09 | 2.59 | 3.69 | 2.93 | 9.49 | 0.66 | 3.15 | 0.69 | 2.19 | 5.44 |

| CHN | 5.25 | 1.49 | 1.63 | 2.65 | 2.19 | 0.4 | 22.49 | 1.12 | 0.11 | 1.65 | 4.1 |

| THAI | 4.66 | 4.49 | 3.16 | 6.07 | 2.81 | 2.29 | 1.12 | 12.64 | 0.77 | 2.82 | 7 |

| VNM | 0.33 | 1.08 | 1.76 | 1.64 | 1.08 | 0.71 | 0.42 | 1.77 | 17.29 | 0.97 | 2.42 |

| TO_ABS | 4.24 | 2.82 | 2.5 | 4.61 | 2.3 | 1.32 | 1.15 | 2.61 | 0.5 | 22.04 | |

| TO_WTH | 10.53 | 7.01 | 6.21 | 11.45 | 5.71 | 3.28 | 2.86 | 6.49 | 1.24 | 54.77 | |

| NET ABS | 2.07 | −0.29 | −0.36 | 1.16 | −0.52 | −0.87 | −0.5 | −0.21 | −0.47 | ||

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Aziz, M.I.A.; Ahmad, N.; Zichu, J.; Nor, S.M. The Impact of COVID-19 on the Connectedness of Stock Index in ASEAN+3 Economies. Mathematics 2022, 10, 1417. https://doi.org/10.3390/math10091417

Aziz MIA, Ahmad N, Zichu J, Nor SM. The Impact of COVID-19 on the Connectedness of Stock Index in ASEAN+3 Economies. Mathematics. 2022; 10(9):1417. https://doi.org/10.3390/math10091417

Chicago/Turabian StyleAziz, Mukhriz Izraf Azman, Norzalina Ahmad, Jin Zichu, and Safwan Mohd Nor. 2022. "The Impact of COVID-19 on the Connectedness of Stock Index in ASEAN+3 Economies" Mathematics 10, no. 9: 1417. https://doi.org/10.3390/math10091417

APA StyleAziz, M. I. A., Ahmad, N., Zichu, J., & Nor, S. M. (2022). The Impact of COVID-19 on the Connectedness of Stock Index in ASEAN+3 Economies. Mathematics, 10(9), 1417. https://doi.org/10.3390/math10091417