1. Introduction

Trading in the financial markets is complex and chaotic because of the large number of influential factors from the economic and psychological surroundings. The field is also characterized by the high speed of information inflows that affects trade profitability within seconds. For these reasons, researchers and practitioners have tried to use Artificial Intelligence (AI) that can help the individual investor make trading decisions or automatically conduct the entire trading process. The aim of the following paper is to review the most recent advances in algorithmic trading systems that are based on AI and to evaluate their future evolutions. Moreover, unlike other papers that concentrate on a single methodology or data set, in this paper we took a more holistic approach that integrates different methodology or data sources into a single decision-making process aimed at detecting financial asset price trend shifts. In our view, the analysis of combined information that is collected from different sources can better forecast financial asset price movement. The data are collected from technical and fundamental analysis and investor sentiment derived from social media. Moreover, we report research on different financial assets such as stocks, ETFs and cryptocurrencies, and precious metals on different trading time frames that can be used by a wide range of traders, including swing and intraday.

A typical algorithmic trading system can accurately analyze various data sets from different sources, produces buy/sell signals through machine learning (ML) or deep learning (DL) artificial neural networks (ANN), and can transact a large number of orders with high-frequency trading (HFT) in a fraction of a second. For that reason, many institutional traders are developing trading systems, which allow them to perform a large number of financial transactions in a short period. HFT algorithm can also be useful to perform arbitrage trading that takes advantage of the existence of different prices for the same commodity. For such strategies, HFT firms need fluent non delayed data and will be willing to pay a lot of money to acquire a fast and fluent data stream that will provide them with reliable data before their competitors. According to authors of [

1] traders often hold their positions for short periods of time and profit from tiny gains in each trade. Furthermore, the volume of HFT trading has been growing rapidly since the beginning of the 21st century to approximately 70% at its peak. Ref. [

2] offered agent-based simulation that will be able to replicate several characteristics of financial markets including the presence of extreme price events, long memory in order flow, the autocorrelation of returns, concave price impact, and clustered volatility. Ref. [

3] examined the effect of high-frequency trading on market quality by examining limit orders. They argued that HFT traders impose a welfare externality by gathering the most profitable limit orders and creating order book imbalance. They concluded that HFT traders demand liquidity from the thin side of the order book and supply liquidity on the thick side. This strategy in their view is more pronounced during the volatile periods when trading speed increases. Ref. [

4] argued that the use of HFT strategies combined with machine learning methods has significantly improved the capability of financial time series forecasts. They proposed an effective and robust automatic HFT grid trading system for the FOREX markets that reduced trade drawdown. Ref. [

5] investigated the predictability of various machine learning models for high-frequency trading of Bitcoin and concluded that they had long memory traits, high levels of stochasticity, and topological complexity. They showed that the superiority of the artificial neural networks is sourced by the parallel processing methods that emulate human decision-making in the presence of underlying nonlinear input–output relationships in noisy signal environments and that the Bayesian regularization renders an outstanding accuracy in forecasting.

AI Trading systems are usually based on several of the following data sources and methodologies: 1. Technical analysis, which is a set of strategies that are derived from past behavior of a financial assets price and volumes of trade. This methodology generates trading signals of different financial assets, such as stocks, currencies, EFTs (EFT = Exchange Trade Fund), and commodities. 2. Fundamental analysis which evaluates the impact of corporate economic news on stock prices. 3. Investors sentiment implies investors’ emotions which are gathered from social media. This paper will review the most advanced research papers in the field of algorithmic trading that combine the described data sources and methodologies into an integrated system. Moreover, the paper will show which methodology combinations helped improve trading results and which proved nonfertile in improving trading performances. Moreover, we report the results of recent research that combines technical analysis and pattern recognition with more traditional forecasting methods such as linear regression.

Technical analysis has been developed enormously during past decades and gained popularity among novice and professional trades because of its relative simplicity and ease of performance. Furthermore, the AI revolution has emphasized the advantage of such analysis when it is conducted by machines rather than by human traders. Machines can wait for market entry or exit for a long period without getting tired and they are not subject to human bias and emotions that sometimes lead human traders to bad investment decisions. Ref. [

6] found that whether algorithm traders earn more profit than human traders depends on the market environment and the fundamental value of a financial asset. Ref. [

7] found evidence of an inverse relationship between algorithmic trading efficiency and trade size.

DL methodology is an algorithm composed of multiple ANN layers. The procedure sets multiple feature layers to obtain higher-dimensional classification and it is being used to analyze an unbounded number of layers of information. Learning could be supervised, semi-supervised, or unsupervised. This methodology can be used to identify correlations between asset returns by examining an infinite number of past data and producing future returns predictions according to the occurrence of identified past conditions. For example, DL can integrate past commodity prices with interest rates, currencies, inflation data, and returns of specific stocks or ETFs to produce future return probabilities of any of the observed assets.

Another field of knowledge that gains popularity in recent years is the use of AI to track investment emotions towards a particular financial asset through internet word tracking in general with emphasis on social networks. Those emotional recognitions are gathered and filtered and then are used to produce a ratio of positive divided by negative emotions that are generated in the decision-making system as another source of information that can strengthen or weaken other inputs before predicting a financial asset’s price direction.

Advanced algorithmic trading systems can perform actual trading according to AI and report the trading results including, for example, price slippage and brokers fees. Moreover, those systems often report three performance measurements: Net Profit (NP), Percent of Profitable trades of all trades (PP), the Profit Factor (PF), and Maximum Drawdown (MDD). NP is the total net profit generated by the trading system. The PP is the percentage of winning trades of all trades generated by the system and the PF is the gross profits divided by gross losses and MDD measures the maximum loss generated by a single trade. Each investor can pick the trading algorithm that produces the best back-testing trading results according to his/her risk preferences. A more risk-averse investor will prefer an algorithmic setup that produced low MDD while a less risk-averse investor may prefer an algorithm that produces the highest NP or PF. The purpose of this paper is to review the most advanced methodologies that are used for AI financial market analysis and trading.

Trading systems that use AI have been developed dramatically in recent years. Those systems seek to improve predictions of financial asset price trends and as a result of that improve trading performances. The evolutions of those systems led them to seek as many inputs as possible derived from a variety of sources that can contribute to that task. A successful trading system integrates a variety of information analyzed with a predesigned system that understands the importance of each piece of information and its use in the prediction process. Such a procedure is complicated and challenging and demands careful algorithm selection and design.

Algorithmic trading has its merits; however, they are also associated with risks and costs that are unique to computational ML systems. For example, systems that are based on algorithms may interpret a momentarily trading disruption caused by an external problem as a market crash and enhance the price fall causing major losses to investors. Another example is the system can interpret one extreme price wrongly generated by a single trader as a signal of an upcoming trend shift in the financial assets price. Those examples demonstrate that the system’s need for a fast reaction to market new information may result in a wrong interpretation of the news and substantial losses. Ref. [

8] stated that risk arises from the choice of the algorithms, bias, and non-representative data sets and from human decisions that are based on their AI interpretations. They added that the reduction in risks requires a vigilant division of work between AI and humans. Costs of trading may also be a problem to algorithmic trading systems that usually perform many trades in a short period of time. That system must have a rebate arrangement that reduces its costs in order to maximize profits.

2. Material and Methods

This paper reviews recent techniques and methodologies utilized to construct algorithmic trading systems using AI and DL capabilities. The papers were chosen according to their originality and importance to the field. The publication date and the journal they were published in were also taken into consideration. The papers that are cited in this study use different methodologies to forecast financial asset trends. They all have something in common: they use past information to predict the future and show that DL and ML can be used to process that data to produce successful trading performances. Combining traditional methods such as technical analysis, pattern recognition, and investor sentiment analysis with advanced DL algorithm have been proven to be able to improve financial forecasting and trading profitability. Moreover, integrating investors’ psychology and biases into trading systems has become more and more popular in recent years following the iconic work of Kahneman and Tversky’s prospect theory (Ref. [

9]).

This paper discusses the fuzzy logic that guides algorithmic trading systems. That logic analyses data from different sources such as past price movements of financial assets and correlations, volumes of trade, economic surroundings, firms’ fundamental reporting, and investors’ sentiments. Such a vast amount of information sometimes diverts or delays the system from achieving the correct and on-time trading decisions. In order to cope with these challenges, an optimal number of rules and a “forget” mechanism that excretes unnecessary information, should be used. A recent publication, for example, found that adding more indicators and trading rules does not necessarily improve the trading results [

10]. They documented that the optimal number of technical indicators for trading daily bars of major cryptocurrencies is one or two.

The paper structure is as follows: Chapter 3 discusses artificial neural networks use in financial assets price predictions, including

Section 3.1 on support vector machine, Section on 3.2 long short-term memory, and Section on 3.3 fuzzy systems. Chapter 4 discusses the important role of investors’ sentiment and social media impact on financial asset price predictions and how these information pieces are integrated into autonomous trading systems. Recent publications have pointed out that social media sentiment measurement can contribute information that other sources of row data cannot and therefore they can be used to improve price predictions and trading performance. Chapter 5 discusses pattern recognitions and their contributions to financial assets price forecasting and trading. These patterns have been used for many years by professional traders, and they are often being integrated into prediction systems in finance. Chapter 6 summarizes and concludes this paper.

3. Artificial Neural Network (ANN)

Artificial neural networks (ANN) are known to be able to provide an abnormal return by using technical indicators as predictors in stock markets [

11]. Ref. [

12] achieved excess returns by using deep learning techniques and technical indicators to analyze open-high-low-close prices and volume in the Korean stock market. The ANN, as a DL technique is used to recognize patterns or images by imitating the visual processing of living organisms. Ref. [

13] predicted cryptocurrency prices using a stochastic model that induces layer-wise randomness into the observed feature activations of NN. They achieved in their best-case experiment, only 5% improvement in Mean Absolute Percentage Error (MAPE) with 23 features of a 7-day window size. Ref. [

14] offered cryptocurrency prices forecasting methodology using a DL algorithm and blockchain information. They concluded that prediction performance is high for both currencies when the blockchain data are used together with Bitcoin and Ethereum prices. Moreover, they documented that the Ethereum currency has the highest percentage of prediction accuracy and the lowest error rate compared to Bitcoin. NN uses learning filters that are generated in each of the network layers to detect a predetermined signal at any given layer and to send real-time information to the system that performs automated trading decisions.

3.1. Support Vector Machine (SVM)

Support vector machine (SVM) is a supervised learning method aimed to predict and classify items using linear or nonlinear processes [

15]. The process allows error within the training data resulting in a significantly reduced error in the tested data. Ref. [

16] combined a cumulative auto-regressive moving average with a least squares SVM model to make basic predictions for the stock market. They concluded that their model is more suitable for stock price forecasting than the single forecasting model. Ref. [

17] tested the predictability of the NIKKEI 225 index weekly movement direction with the SVM forecasting model and proved that SVM outperforms other classification methods. Furthermore, they offered an improved model that combines SVM with the other classification methods. Ref. [

18] used the SVM algorithm to make automated transaction decisions on the Forex market and proved the system’s contribution to successful trading. Ref. [

19] examined the predictability of the 12 cryptocurrency prices using SVM and concluded at the daily or minute level frequencies, ML classification algorithms reach about 55–65% of predictive accuracy. Ref. [

20] used SVM kernel functions to predict the price directions of cryptocurrency and foreign exchange. They showed that the Radial Basis Gaussian (RBG) SVM forecasting model outperformed other SVM-kernel models.

SVM-based systems are widely used to predict financial asset price trends. Those systems use different models that filter past financial data and produce predictions. They all assume that future price trends can be forecasted by analyzing past correlations between financial assets and that economic conditions are repetitive. Such assumptions are correct under normal market conditions; however, they prove infertile under “Black Swan” conditions that surprise the market from time to time.

3.2. Long Short-Term Memory (LSTM)

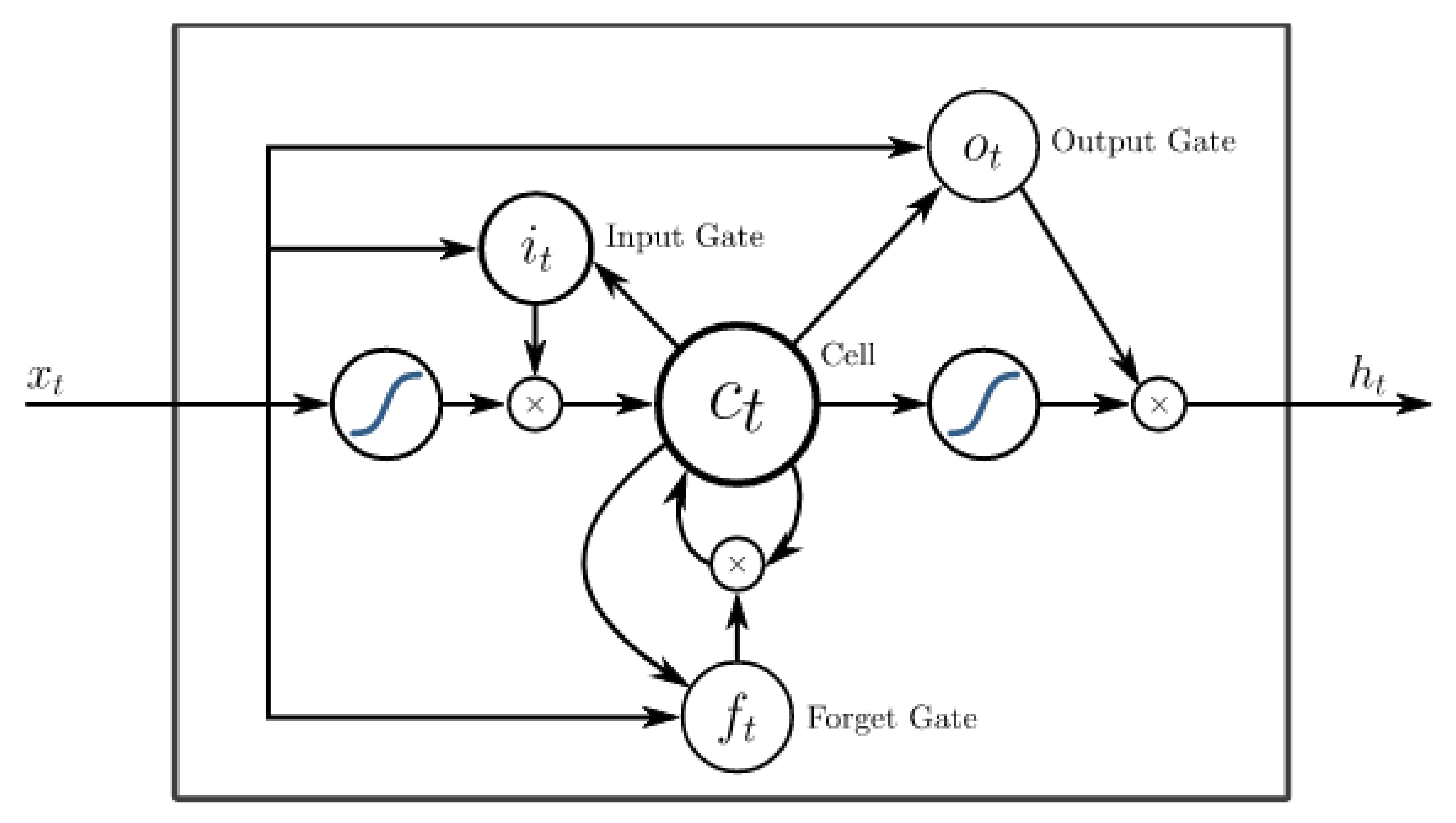

LSTM is an artificial recurrent neural network (RNN) used in the fields of AI and DL. The procedure can process sequences of data simultaneously and it is useful for classifying, processing, and making predictions on time serious data, making it an ideal tool for financial assets price predictions. LSTM includes a cell, input and output gates, and a forget gate (see

Figure 1). The cell remembers values while the other three gates control the information flow into and out of the cell.

in

Figure 1 is the Cell in which the main processes are conducted, and

,

and

are the input, output, and the forget gates. The mathematical process is described in Equations (1)–(5).

where:

is the forget gate activiation vector,

is the input gte activiation vector,

is the output gate activiation vector,

is the cell vector,

is the output vector,

= sigmoid function,

= hyperbolic tangent functions,

is the weight matrix, and

is the bias vector that are learned by training.

The major difference between LSTMs over traditional ANN is that they can learn selectively by remembering and forgetting the required historical data. This can be very useful for the financial assets trading system by setting a specific range of data that the designer wants the algorithm to perform predictions while at the same time, deciding upon the range and scope of data that the system should forget in order not to be destructed by irrelevant data. Ref. [

23] ensembled an LSTM model that uses many technical indicators as the network inputs for predicting intraday stock movements of U.S. large-cap stocks. They concluded that the model performed better than benchmark models with lasso and ridge logistic classifiers or equally weighted ensembles. Ref. [

24] used LSTM networks with technical analysis indicators to predict future stock prices. Results showed an average of 55.9% accuracy in predicting stock price trend shifts. Ref. [

25] compared deep learning methods such as a deep neural network (DNN), a convolutional NN, and a deep residual network, for Bitcoin price prediction. They showed that DNN-based models were the best for price trend prediction of Bitcoin. Moreover, they found that the classification model was more effective than regression models for algorithmic trading. Ref. [

26] tested forecasting models using daily cryptocurrency prices. For each cryptocurrency, they used different LSTM models and concluded that the model that is based on 50 days of data performed the best since it has the capability to capture long-term dependencies. Ref. [

27] used LSTM for swing traders to predict future stock values. Their system reported the predicted values of the company stock price in the Indian stock market for 30 days. Their system was based on technical indicators such as Support and Resistance levels, Fibonacci retracement levels, MFI, RSI, and the MACD (Support and Resistance levels, Fibonacci retracement levels, MFI, RSI, and the MACD are technical indicators). The results achieved by the proposed model establish the efficacy of the proposed technique. Ref. [

28] employs random forests and LSTM networks as training methodologies to forecast the movement of the S&P500 stocks from January 1993 until December 2018 for intraday trading. On each trading day, they bought 10 stocks with the highest probability to outperform the market and sell short 10 stocks with the lowest probability to do it. They showed that a multi-feature setting provided a daily return of 0.64% using LSTM networks. Ref. [

29] conducted their research on China’s stock market; their data included opening price, closing price, lowest price, highest price, and daily trading volume of stocks. Their results showed that the LSTM neural network model can predict stock prices with limitations such as time lag of prediction. Moreover, to predict stock price trends, the model should explore internal rules through the selective memory advanced deep learning function of the LSTM neural network model.

The advantage of an LSTM in financial price forecasting is its ability to forget information that the system designer evaluates their relevance and therefore should be ignored after some time to enable correct predictions. This is a delicate task that can damage the system’s prediction ability since the financial markets are very dynamic and the relevancy of any specific data pieces to predictions may change over time.

3.3. Fuzzy Systems

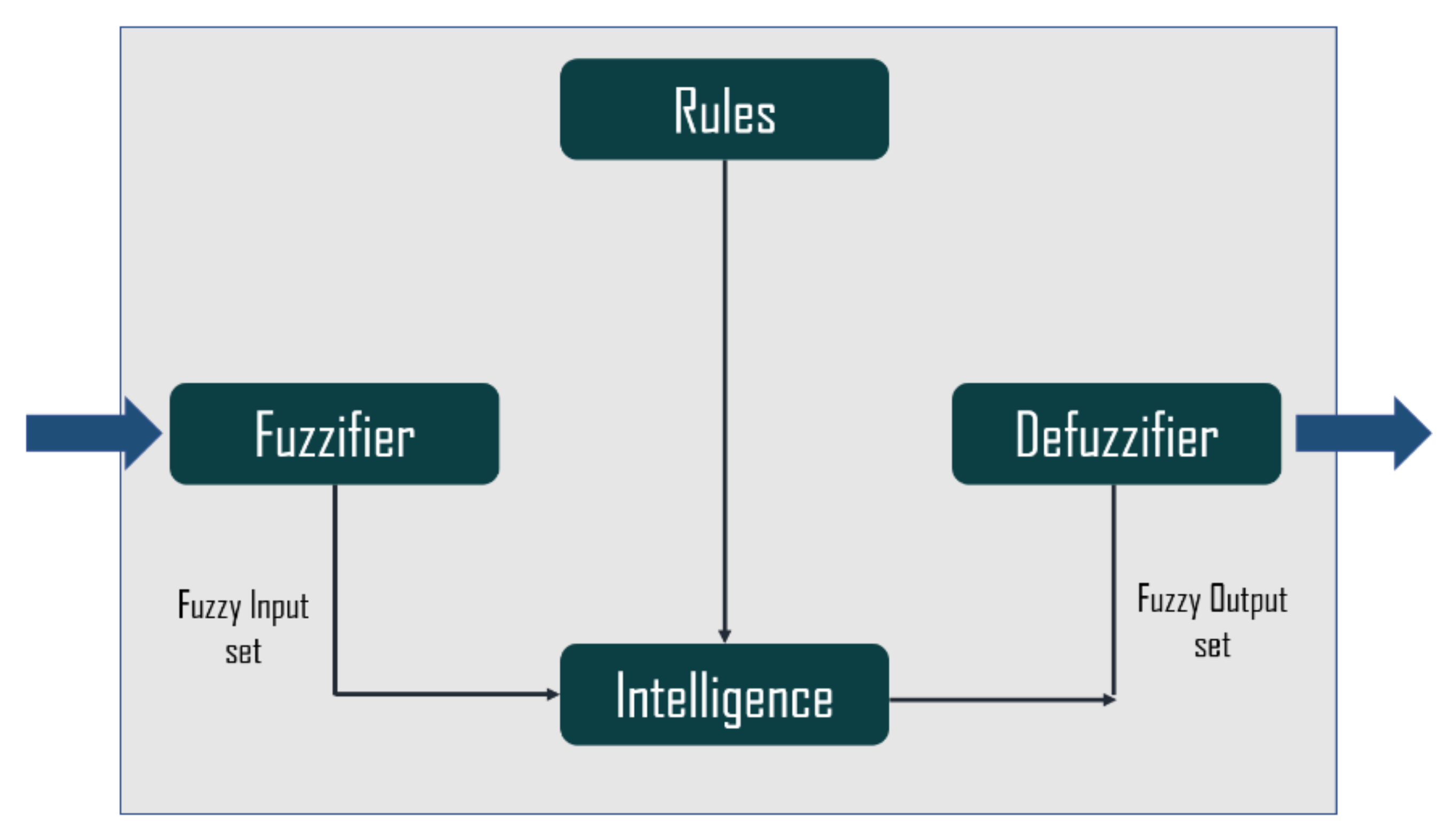

A fuzzy system is a distinguished formation characterized as a set of interacting components with a well-defined structure. The uniqueness of fuzzy techniques is that they can process information, whereas classical theory or binary logic is impossible. fuzzy systems can model complex and often vague real problems. The inputs of fuzzy systems are sets of data with some degree of classified membership between 0 and 1 representing the strength of belonging to a specific fuzzy set. Fuzzy logic is a method of reasoning that resembles how humans perform decision-making. The fuzzy logic process consists of four main parts, as demonstrated in

Figure 2.

Rules are the conditions offered by experts behind the algorithm. The Fuzzifier converts inputs into fuzzy classification sets. The Intelligence determines the degree of match between fuzzy inputs and the set of rules. At this stage, the system can also decide on the set of rules that do not improve prediction and should be dismissed. The final stage is Defuzzification in which the system converts the fuzzy sets into values that can be translated into action orders such as buying or selling a financial asset.

Fuzzy systems are often used in financial forecasting when traditional models have limited prediction power because of nonlinearity and nonstationary often characterizing financial phenomena. Ref. [

30] used technical analysis to construct a fuzzy system that is able to perform medium-term optimal financial asset allocation. They showed that their model has outperformed the Buy and Hold (B&H) strategy between 1997 and 2012 for ASE (ASE = Athens Stock Exchange). Refs. [

31,

32] used a clustering genetic fuzzy system to predict daily stock prices. They used steps models that included stepwise regression analysis, data clustering, and a genetic fuzzy system for stock price prediction and concluded that their model has better forecasting accuracy of short-term stock price than alternative models. Ref. [

33] studied the ability of a multi-objective fuzzy system to predict a bull signal or a bear signal in the cryptocurrency market. The fuzzy sets were partitioned as very low, low, medium, high, and very high, later to be used to signal whether a cryptocurrency is bearish or bullish on a specific day. They reported that the system yields a 53% accuracy with 25 days rule length. Ref. [

34] proposed a clustering-based adaptive neuro-fuzzy system for predicting apple stock daily price. He used four technical indicators in his study: 1 and 2 weeks simple moving average, 14 days disparity (the disparity index measures the relative position of an asset’s most recent closing price to a selected moving average and reports the value as a percentage) and Larry Williams percent range (the Williams percent range is a momentum indicator that moves between 0 and −100 and measures oversold and overbought levels). The simulation results indicated that the average subtractive clustering-based neuro-fuzzy networks were better than other networks. Ref. [

35] boosted the profitability of technical analysis for currency trading using a multivariate fuzzy logic. Their approach yielded consistently higher Sharp ratios (Sharp ratio measures the risk return ratio) for all investigated currencies. Ref. [

36] suggests evolving possibilistic fuzzy modeling to forecast realized volatility with jumps. Adding or removing clusters was allowed using statistical distance-like criteria to update the model. The data consisted of global major market indexes (S&P500 and Nasdaq, FTSE, DAX, IBEX, and Ibovespa). Their results show that the possibilistic fuzzy model is highly efficient to model index volatility with jumps in terms of forecasting accuracy. Ref. [

37] proposed a hybrid neuro-fuzzy controller to forecast the direction of the daily price of Bitcoin. Their system investment returns were 71.21% higher than the B&H strategy. Ref. [

38] used fuzzy if–then rules for their stock trading system. They used three linguistic variables as inputs for the rules: view from the expert, earning-per-share, and price-to-earnings ratio. They concluded that using this fuzzy logic can improve trading results. Ref. [

39] tested whether the occurrence of technical patterns along with a membership value is able to signal the future returns of stocks. They matched 1450 U.S. companies with control companies on the basis of market value and previous years’ returns and found that stocks with certain technical patterns can generate abnormal returns after pattern occurrence for up to 120 days. Ref. [

40] combined technical analysis and fundamental analysis within a fuzzy system that utilizes 677 stocks from the Indonesian stock market exchange. They concluded that the Fuzzy technique combined with three candlesticks momentum entry buy/sell signals can make trading more rewarding. The use of any trading rule depends on the time frame preferences of the individual trader. Swing traders for example analyze daily and weekly bars (a trading bar contains information about the opening/closing prices along with the high/low levels of a specific time frame) while day traders analyze shorter periods such as an hour or even a few minutes bars and base their decision upon a short period’s momentums. Ref. [

41] examined the intraday algorithmic system for trading precious metals futures and found that an RSI-based system produced above the B&H returns of 326.3%, 106.2%, 63.7%, and 22.4%, for palladium, gold, silver, and platinum, respectively, for the examined period. They also recommended that 60 min bars should be used for trading precious metal futures. These results can be useful for intraday traders both manual and algorithmic by implementing the most efficient trading rules and time frames for each of the precious metals futures.

The advantage of the fuzzy systems in predicting financial asset price trends is their relative simplicity and their ability to integrate different sources of information. The problem with such systems is their inability to adjust to changing financial conditions and relaxing predetermined rules that should be changed accordingly.

4. Investors Sentiments and Social Media

Social media has been growing in popularity among financial analysts because of its ability to examine human sentiments towards various issues and not just raw data. The idea is that “herd behavior” that exists in many life aspects also characterizes investment behavior [

42,

43]. The use of investor sentiment analysis to predict stock return in the financial literature sometimes appears as sole predicting information or as an addition to other market data sources. Ref. [

44] investigated the impact of social media on various global financial markets using a firm’s Twitter sentiment and found that Twitter activity and investor’s sentiment are associated with trading volume and returns. Ref. [

45] predicted changes in Bitcoin and Ethereum prices using Twitter and Google Trends data. They found that tweet volume is a good predictor of price direction rather than tweet sentiment. They formed a linear model that uses tweets and Google trends to accurately predict the direction of price changes of cryptocurrencies.

Ref. [

46] based on a large dataset of 84 million tweets and 8 years of stock data for 407 companies from the S&P 500 index, tested whether social media has differential impacts on stock performance. They found that while consumers’ negative sentiment significantly impacts stock prices, consumers’ positive sentiment does not play a significant role in stock performance. Ref. [

47] argued that social media simultaneously encourages and biases trading decisions creating a new class of self-directed online traders. Ref. [

48] combined indicators of technical analysis and investor sentiment derived from news articles to construct a predictive model that can forecast trends of the twenty most capitalized companies listed in the NASDAQ100 index. Ref. [

49] argued that cryptocurrency price fluctuations depend heavily on web search analytics tools such as Google Trends and on social media sentiment. They also found that Twitter sentiments tend to be positive for cryptocurrencies even if their prices go down.

Ref. [

50] applied several NN models to stock market opinions posted in twits and documented that the deep learning model can be used effectively for financial sentiment analysis and a that the convolutional neural network is the best model to predict the sentiment out of stock twit’s dataset. Ref. [

51] tried to predict Bitcoin’s trends by extracting keywords from Bitcoin-related comments posted on online forums. They claimed that user opinions on online forums are conducive to understanding a range of cryptocurrency price trends. Ref. [

52] proposed the usage of ML tools and social media data for predicting the price movement of Bitcoin, Ethereum, Ripple, and Litecoin. Their results indicate that machine learning and sentiment analysis can predict cryptocurrency market trends. Moreover, they concluded that Twitter data by itself can be used to predict certain cryptocurrencies’ prices. Ref. [

53] integrated sentiment analysis into a machine learning method and demonstrated that the forecasting accuracy of the direction of the SSE50 (SSE50 is an index representing 50 top companies listed on the Shanghai Stock exchange) index is 89.93% with a rise of 18.6% after introducing sentiment variables. Their findings also imply that sentiment probably contains precious information about the asset’s fundamental values. Ref. [

54] used text mining technology to quantify the social media opinions on stock-related news compiled into logistic regression proposing an improved prediction model.

Social media and investors’ sentiments have been important in recent years as additions to financial price prediction processes. The understanding that row data alone has limited prediction power is widely accepted now by researchers. However, investors’ mood is easily altered by false rumors and fake news and therefore can be sometimes unreliable and should be carefully analyzed. This is especially true for young or inexperienced investors who rely heavily on social media to shape their personal views. In order to reduce that phenomenon and still use social media as a source of information, the system designer should verify investors’ sentiments from various outlets before integrating them into the trading system.

5. Patterns Recognitions

One of the most promising areas of AI is pattern recognition which is a DL method applied to analyze pictures and photos in a variety of fields such as medicine, biology, and chemistry. In recent years, this methodology has gained popularity among designers of algorithmic trading systems and market forecasters. Years of trading experience have led to the conclusion that certain price patterns are repeated in different financial markets and financial assets. Those patterns are sourced by human behavior and biases. Since some AI trading algorithms imitate human behavior and their intelligence is based on human knowledge and experience, the pattern’s repeatability is getting stronger. The most basic patterns recognition is “candlesticks” (candlestick is a formation representing the open, close, high, and low price of a financial asset in a predetermined time frame) formations and “Support and Resistance” levels for example [

55,

56]. Ref. [

57] examined the ability of “candlestick” patterns to predict Bitcoin’s trends shifts and found that the “Engulfing” pattern can timely produce correct predictions of Bitcoin price shifts resulting in a 3.54 profit factor that indicates that profits were 3.54 times the losses of the algorithmic trading system during the beginning of 2012 till the end of July 2020. The result of this study can be used in practice both by human traders and trading systems. A human trader can identify the daily “Engulfing” buy/sell signals simply by examining the chart or using pattern recognition systems and then performing the trading order manually. An automated trading system can identify the pattern and produce trading orders accordingly.

Other researchers have tried to characterize financial asset price movement by Linear Regression, Box formations, and dynamic channels such as Bollinger Bands (BB) and Keltner channels (Keltner channels are volatility-based bands invented by Chester Keltner that can aid in determining the direction of a trend). According to this trading strategy, a breakout of the form implies the strength of the asset’s price momentum and can be used to achieve abnormal returns. Ref. [

58] used ML to design a trading system that is based on three methodologies: Bollinger Bands (BB), Linear Regression, and Darvas boxes (Darvas boxes are box formations developed by Nicolas Darvas). The data in this study consist of 20 years of daily price data of five precious future metals: gold, silver, copper, platinum, and palladium. Results show that linear regression is the best technique for forecasting silver and gold prices, while the Bollinger Band technique best fits palladium prices. Ref. [

59] proposed an algorithmic system that is based on three fuzzy logic controllers such as candlestick patterns and BB which were used for producing buy, hold, and sell signals. Ref. [

60] traded stocks of Taiwan 50 using BB methodology. Results reveal that investors might beat the market by entering a long position when the price touches the lower band and a short position when it touches the upper band.

Pattern recognition is traditionally used in forecasting systems in a variety of fields. In finance predictions, they use the human psychological ability to examine chaotic environments with structures and formations. The assumption that leads systems designers to use those patterns is that those patterns that appeared in the past will also appear in the future. The problem with such an assumption is that patterns may change in their frequency of appearance over time, and they differ from one financial asset to another.

6. Summary and Conclusions

This paper reviewed the most advanced systems that were designed to forecast and trade financial assets. The paper’s main contribution is that it covers the most important methodologies that are integrated into algorithmic trading systems. It also points to the advantages and disadvantages of each methodology. The financial markets are complex and dynamic, making forecasting a very difficult task. However, this paper shows that predictions can be formed using AI and careful design producing profits that outperform the B&H returns.

In recent years, researchers, institutional traders, and funders have become aware of the advantages of using ANN for designing and operating trading systems. The advantages that are inherent in such a system over human traders are enormous. An ANN system can analyze a large amount of data from different sources in a fraction of a section. Moreover, it can use fuzzy logic that imitates human behavior without the biases involved with human trading. DL procedures can vaguely explore, though not intuitively, the correlation between assets value and market economic conditions and use that for the price prediction of stocks, ETFs currencies, and commodities. Algorithms can not only make accurate predictions and perform real trading, they can also report various back-testing results that may suit different risk-averse levels of investors. SVM can gather information from various sources from financial exchanges, global economies, and social media. The latter source of information was documented to improve the system’s prediction accuracy. Another important contribution of AI to trading is pattern recognition and breakout signaling. In this area of expertise, the system is set to recognize well-known patterns and to decide accordingly when to enter or exit a trade. Candlestick patterns, boxes, and channel formations are found to be useful in predicting the price trend of various financial assets. Trading systems seek to improve predictions of financial asset price trends and as a result of that to improve trading performances. The evolutions of those systems led them to seek as many relevant inputs as possible derived from a variety of sources that can contribute to that task. A successful trading system integrates a variety of information analyzed with a predesigned system that understands the importance of each piece of information and its use in the prediction process. Such a procedure is complicated and challenging and demands careful algorithm selection and design. An important practical implementation of this study is that each financial asset behaves differently and therefore should be traded according to a different set of rules and methodology. Moreover, the system designers must consider that market conditions change frequently and change their systems accordingly.

The paper covered various methodologies that guide designers of algorithmic trading systems. Most of the cited papers have proven fertile in achieving the above index profitability. Those suggested techniques must be modified in real life to a specific market condition and to a specific financial asset. Moreover, real-life traders must take into consideration the risks involved in algorithmic trading and their associated costs before they are engaged in such a venture. Unlike past papers, the current paper utilized a holistic methodology towards trading taking into consideration human behavior and sentiments that were collected from social media that can add insights about future price movements of financial assets that cannot be revealed from past raw data derived from the financial markets. Moreover, we provided practical suggestions for manual traders and algorithmic traders.

The future of algorithmic trading systems is exciting. We estimate that new techniques will be developed using an even larger amount of data sets that would be analyzed simultaneously using quantum computers producing faster and more accurate price predictions. New devices such as brain scanners and eye trackers will provide the systems with a full human emotion profile that will derive prediction accuracy even further. Deepening algorithmic trading system entrenchment in the finance sector might enhance the human–computer conflict. Ref. [

61], for example, showed that people perceive AI as more capable of impartiality than humans. The human–machine interface should be carefully balanced in the future to ensure that the advantages of both machines and humans can be incorporated successfully.

{kind=link}

{kind=link}