Fractality of Borsa Istanbul during the COVID-19 Pandemic

,

,  , , and

, , and

Abstract

1. Introduction

2. Literature Review

3. Materials and Methods

3.1. Dataset

3.2. Fractal Dimension Estimation Methodology

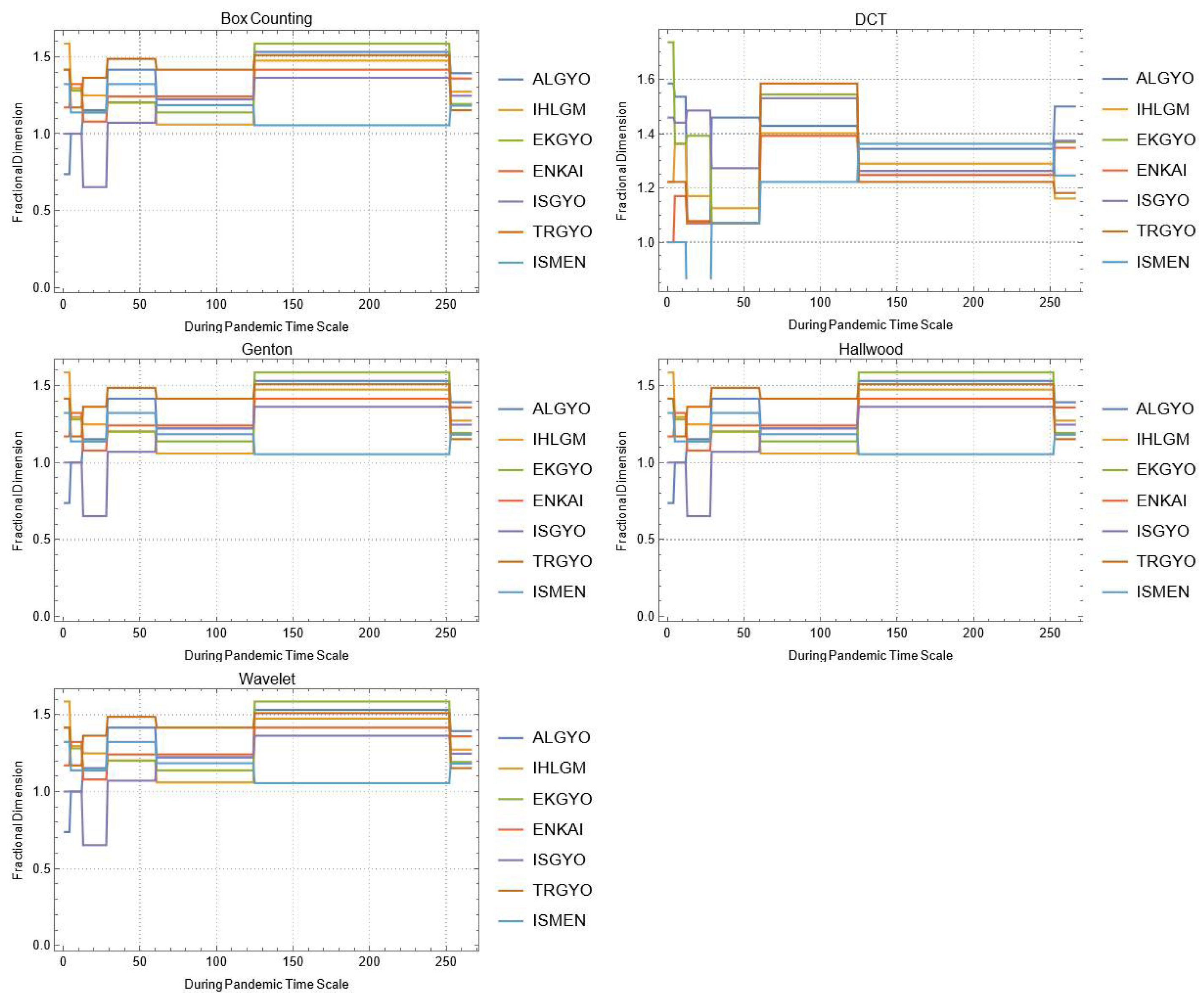

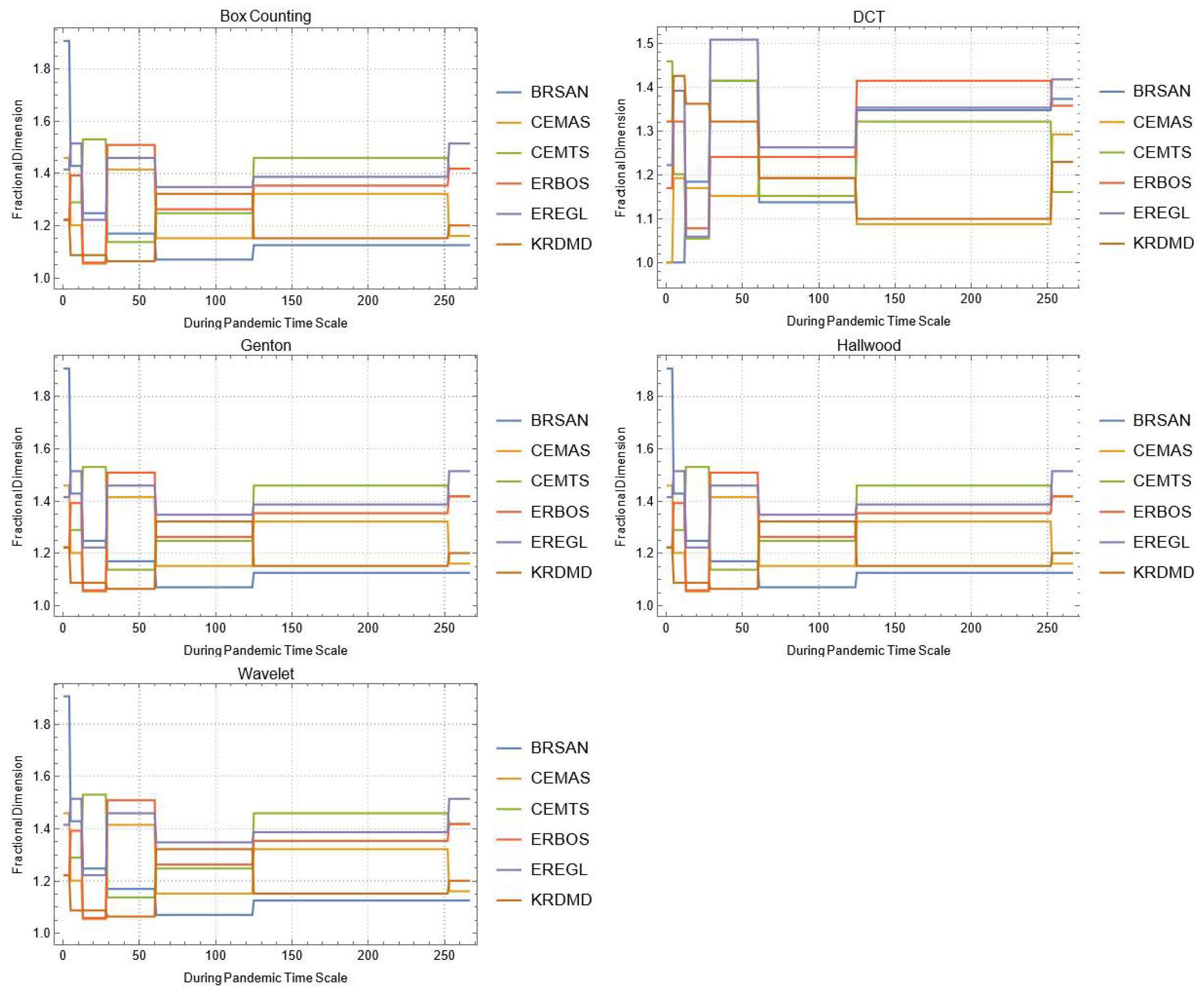

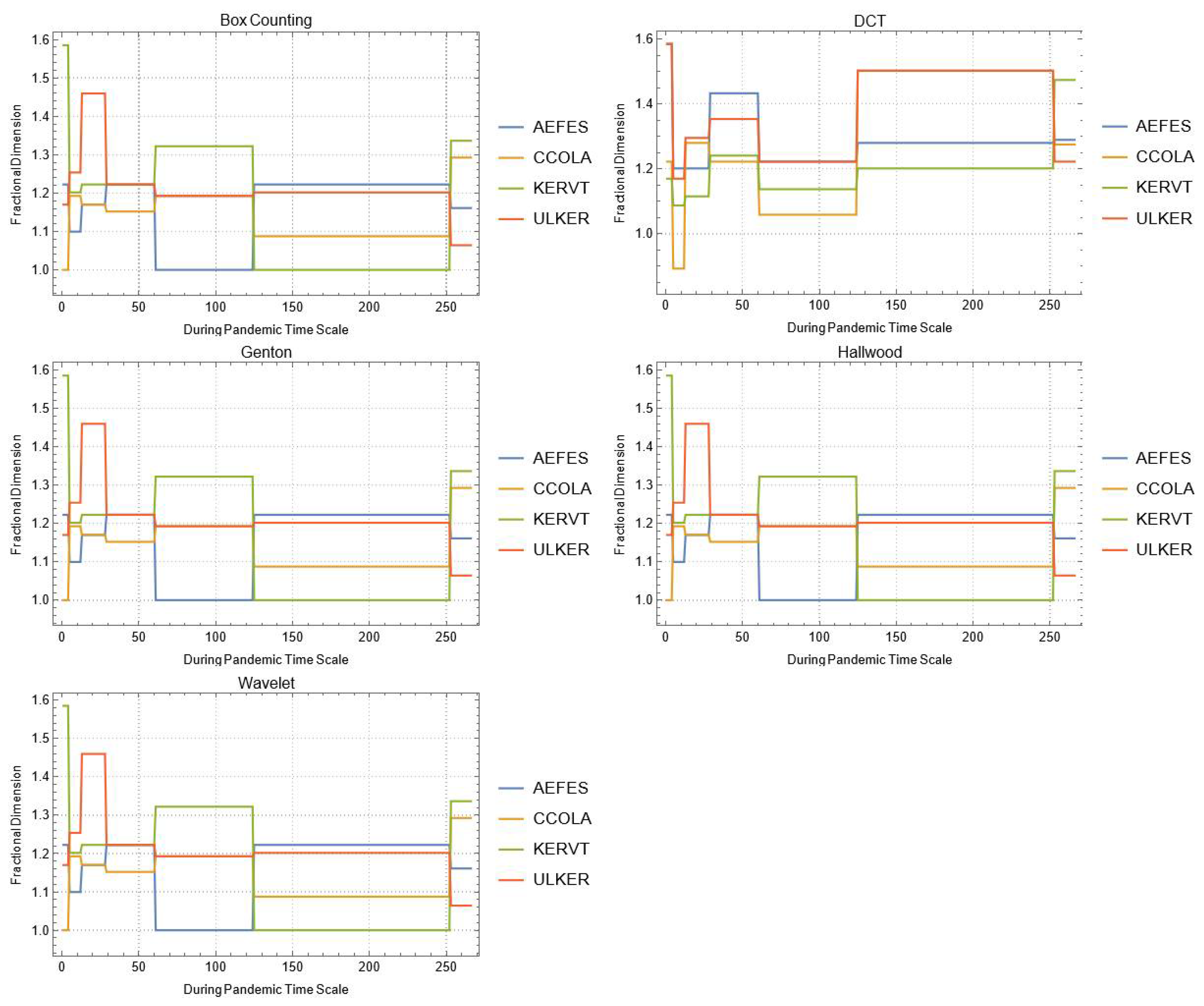

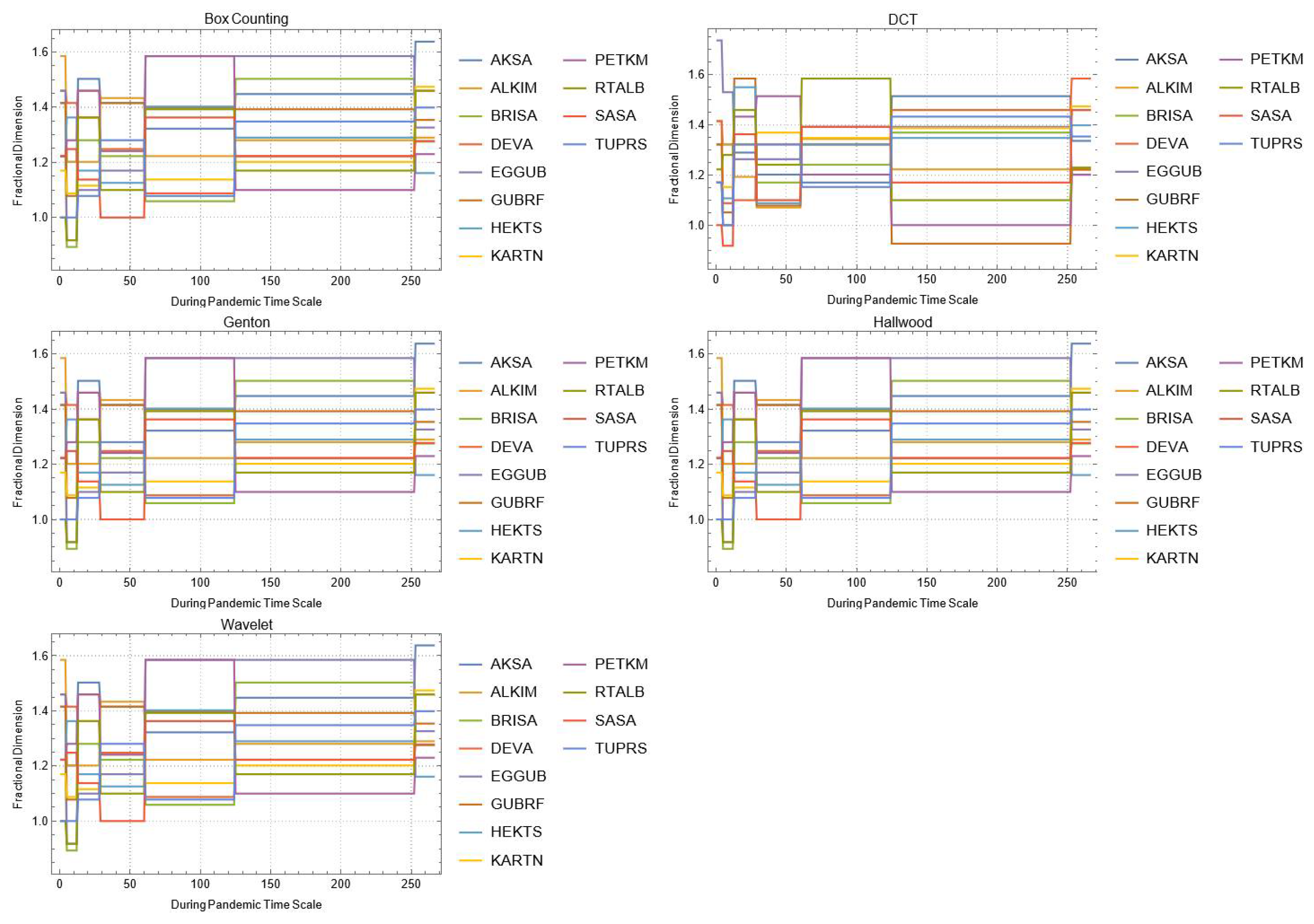

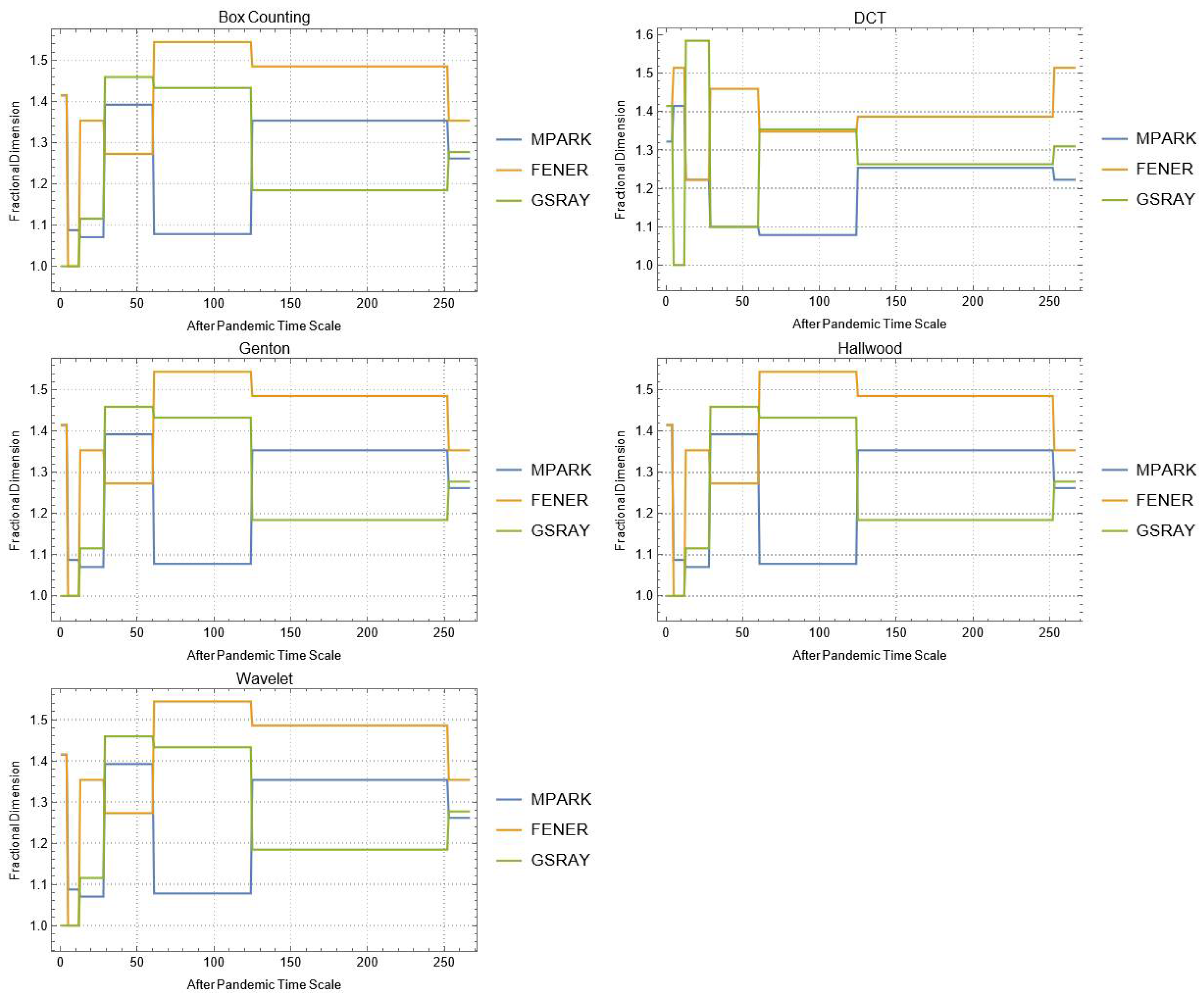

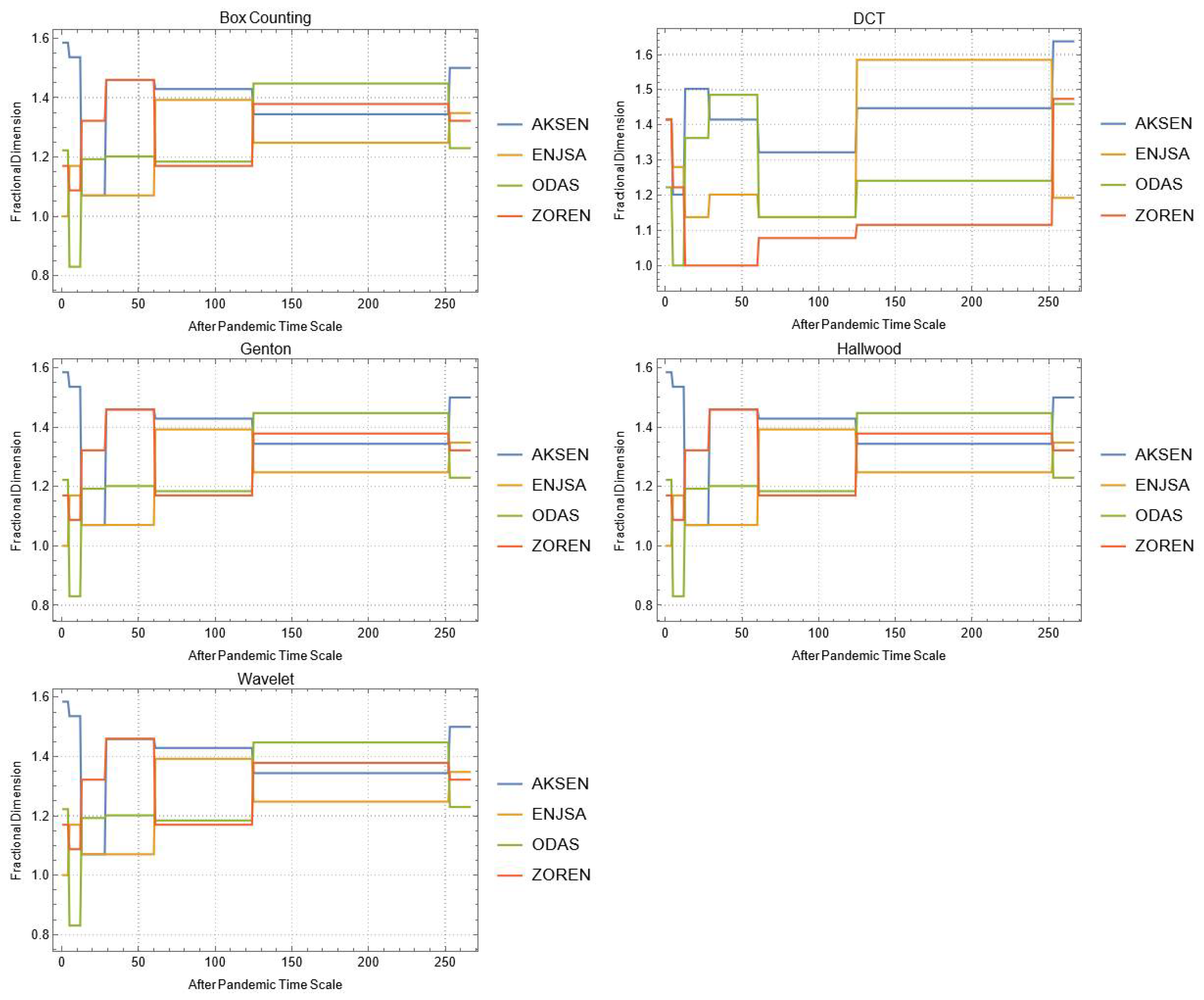

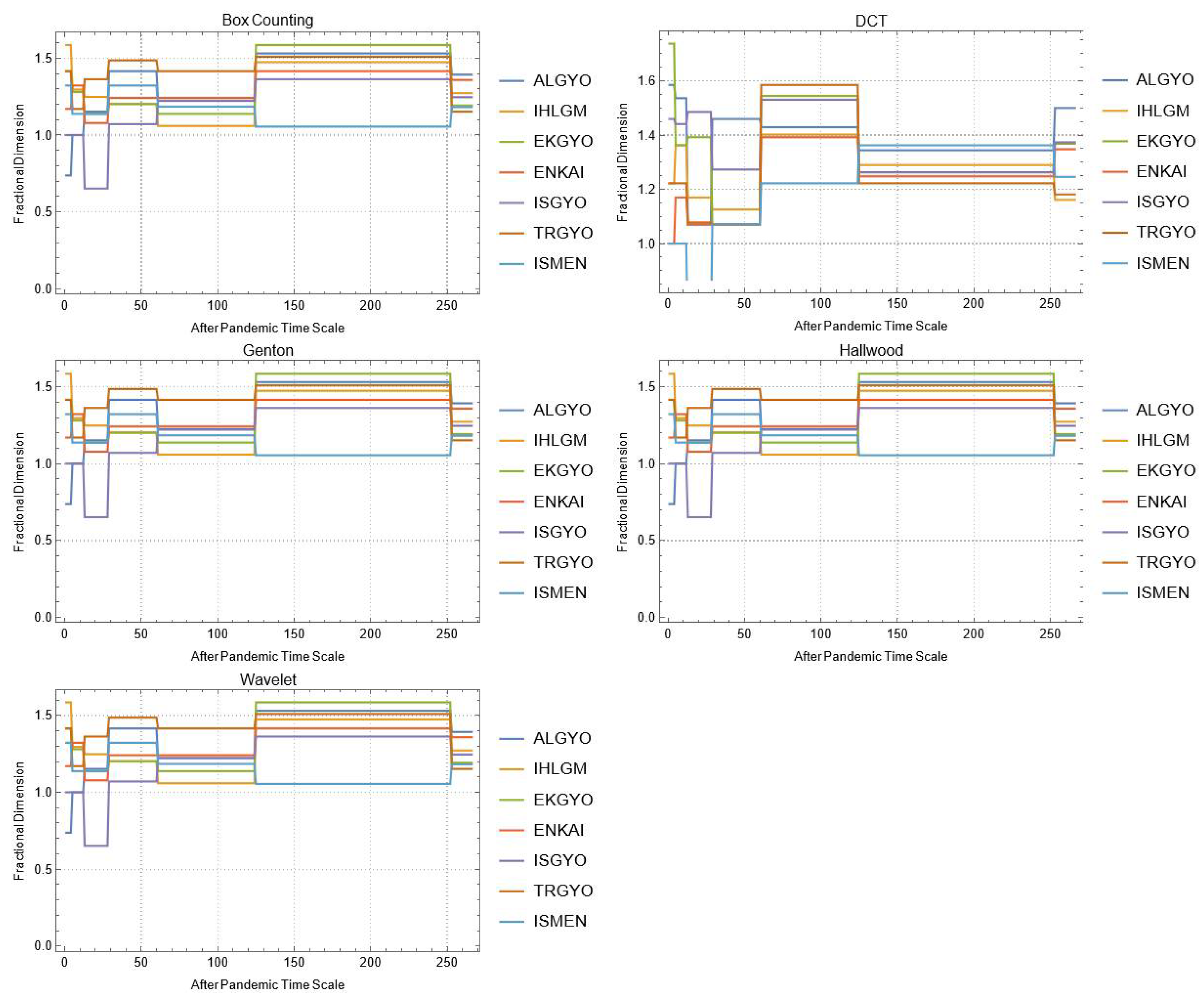

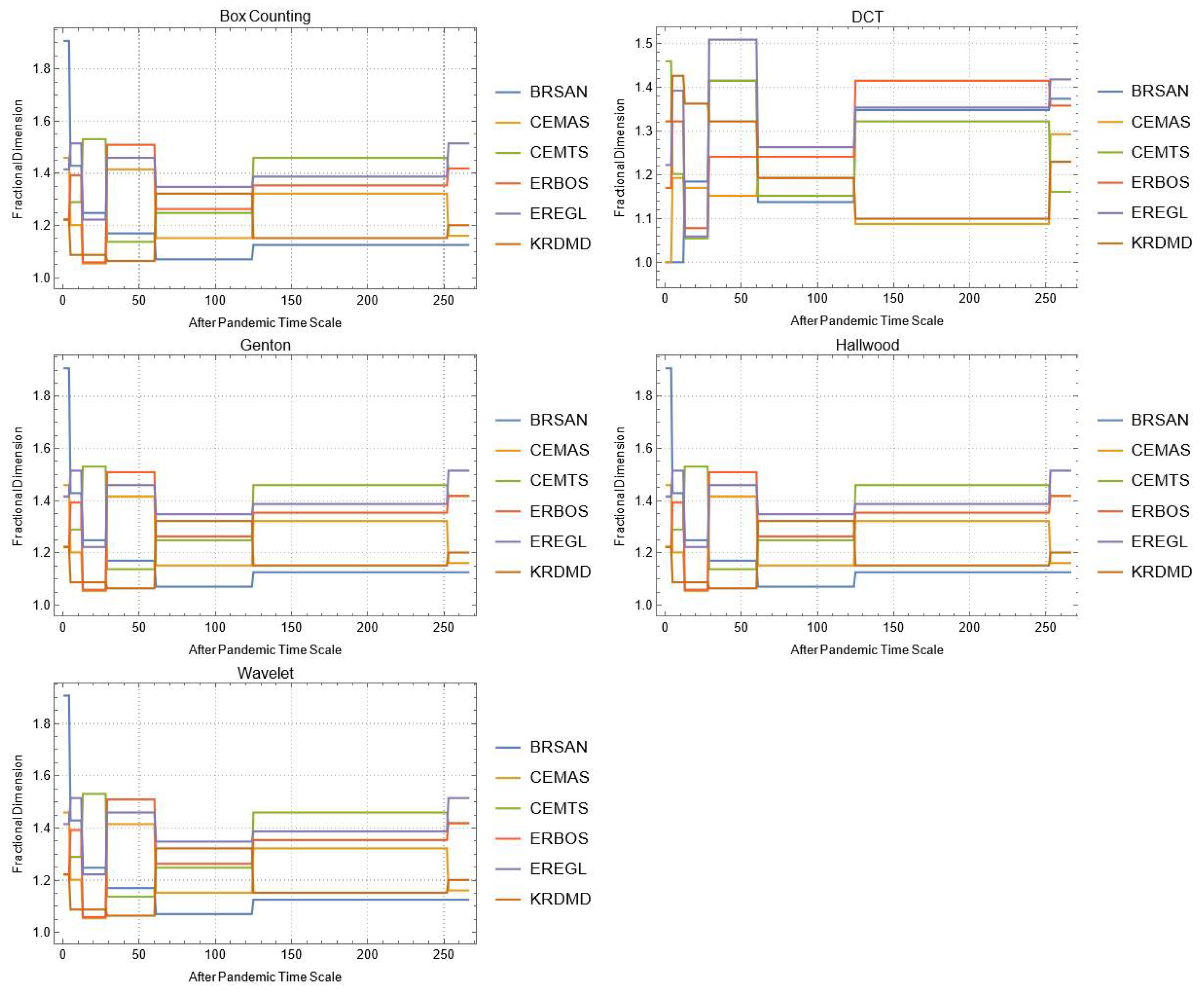

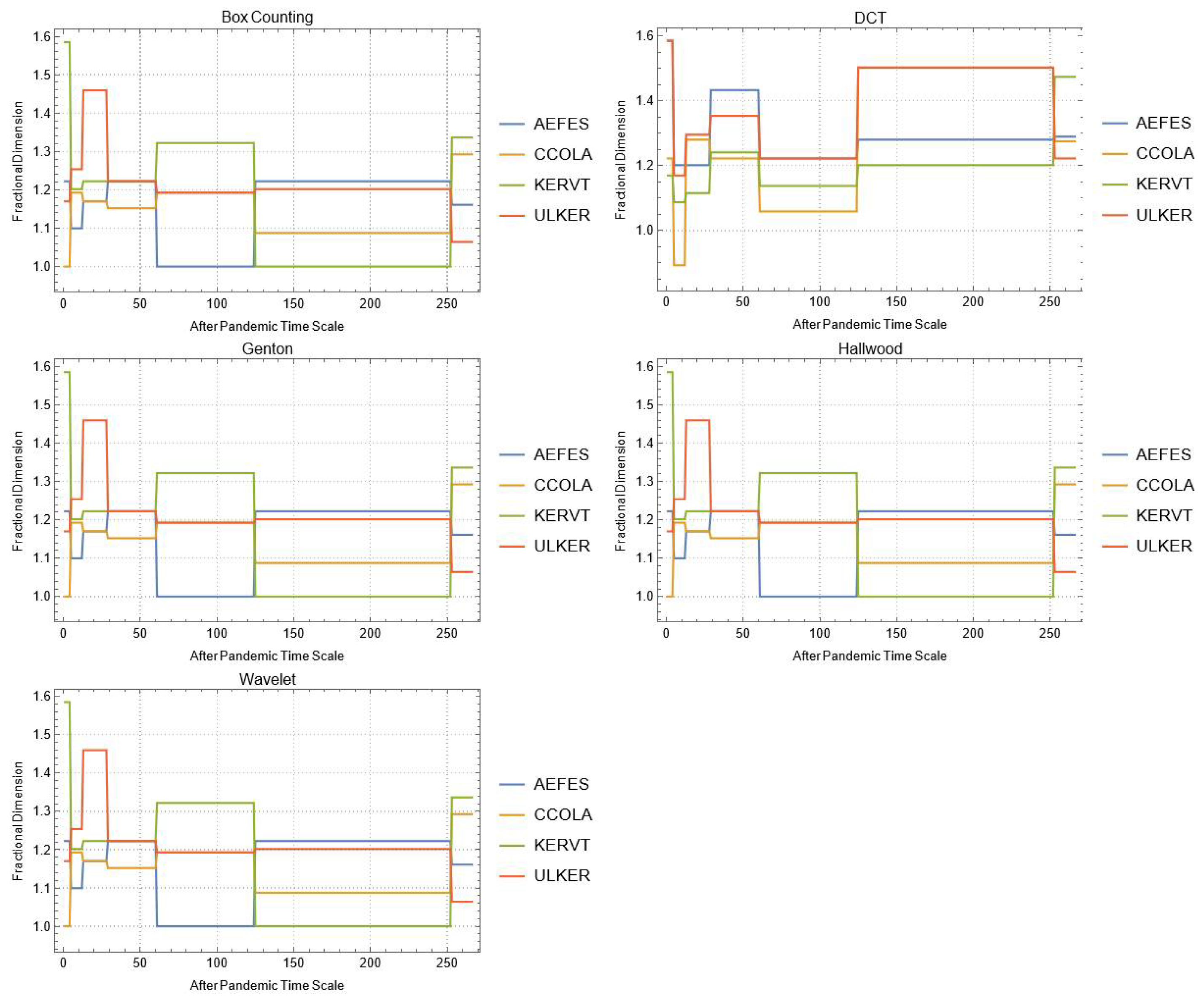

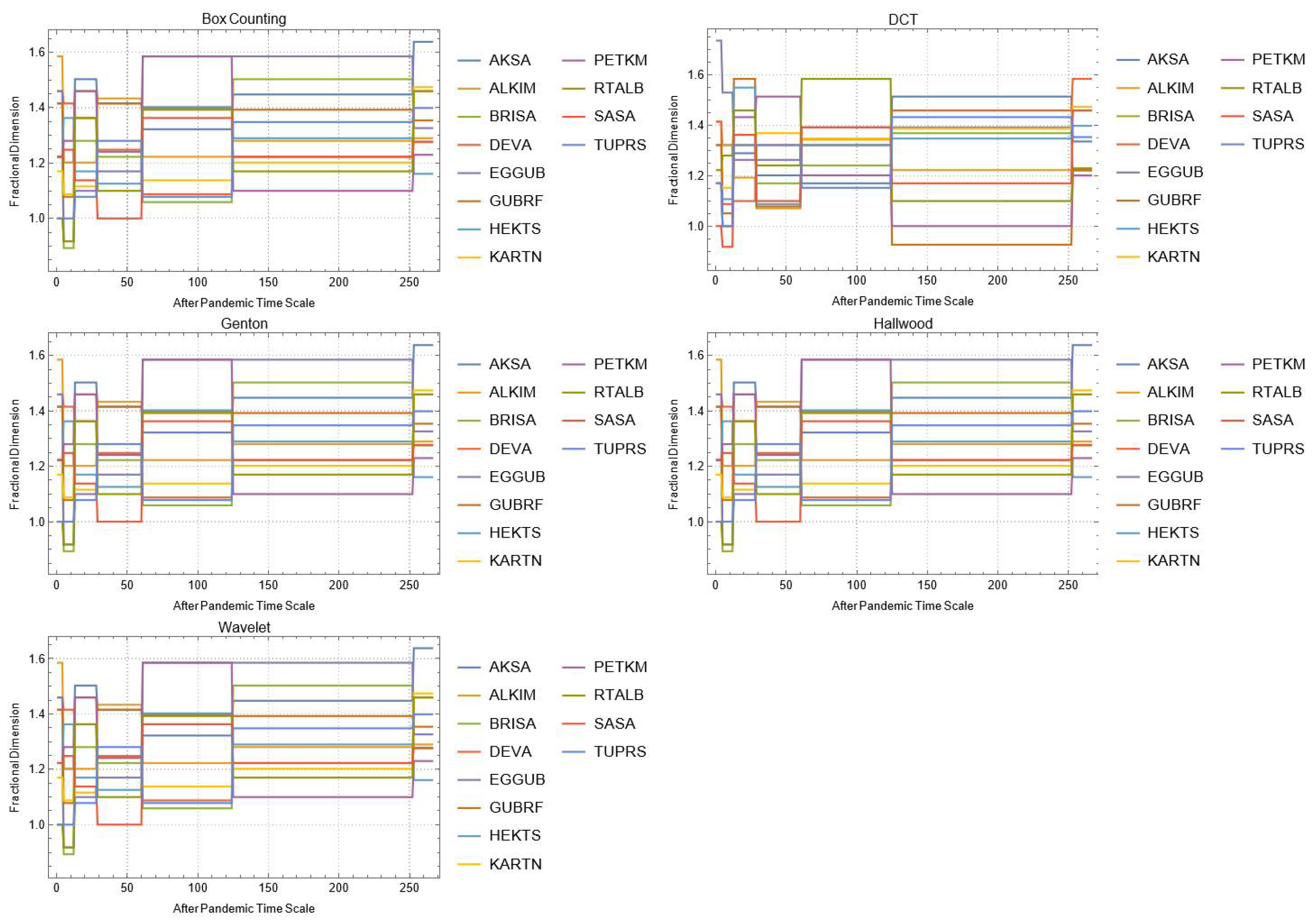

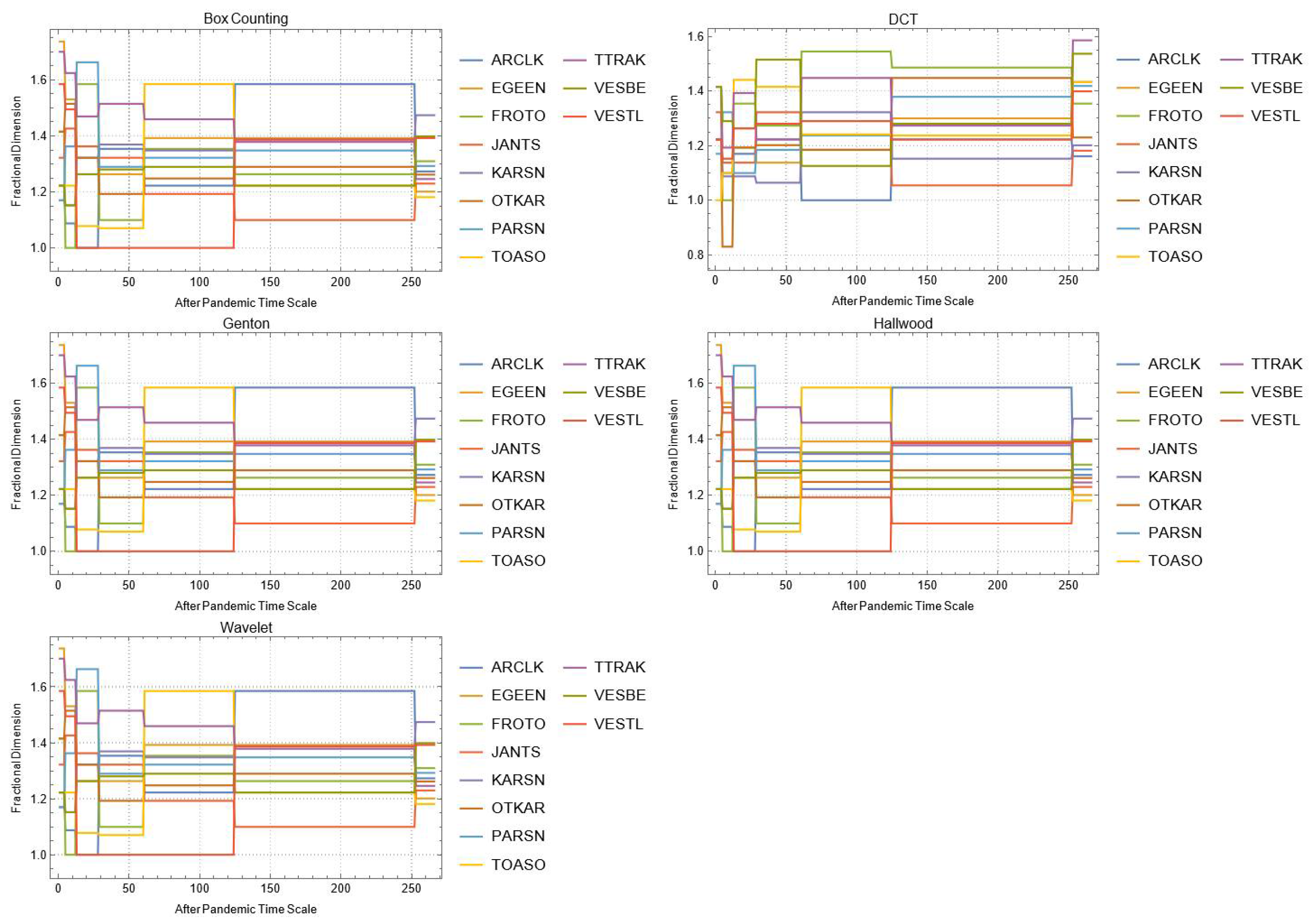

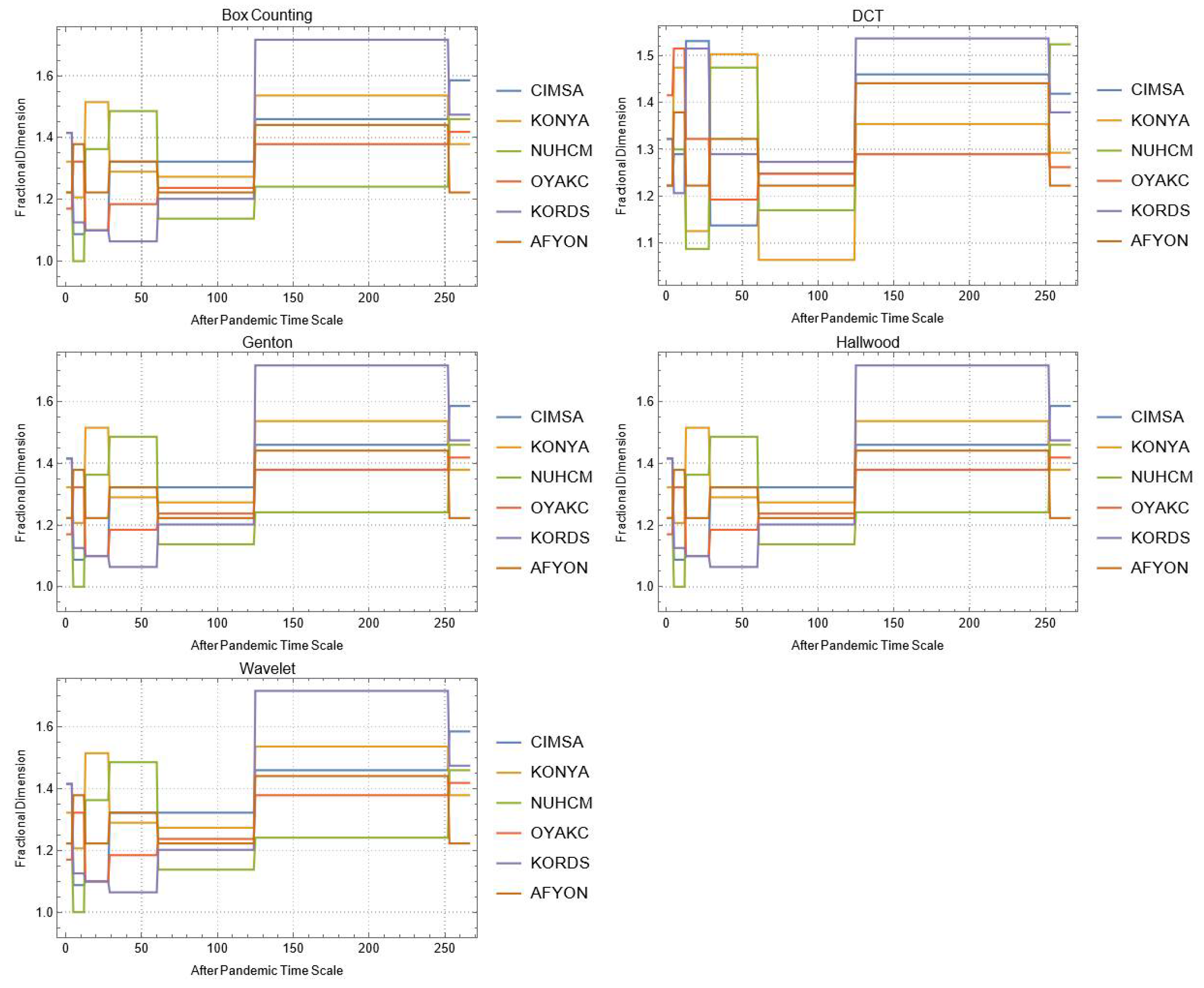

4. Results

5. Conclusions and Discussion

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A

Appendix B

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Company | ||||

|---|---|---|---|---|

| MPARK | FENER | GSRAY | ||

| During COVID-19 Pandemic | Box | 1.37851 | 1.30946 | 1.24593 |

| DCT | 1.57274 | 1.41248 | 1.54889 | |

| Genton | 1.42786 | 1.59779 | 1.42786 | |

| Hall-Wood | 1.48638 | 1.58955 | 1.58954 | |

| Wavelet | 1.65934 | 1.53477 | 1.60411 | |

| After COVID-19 Pandemic | Box | 1.1375 | 1.30736 | 1.32193 |

| DCT | 1.58383 | 1.39918 | 1.52539 | |

| Genton | 1.72322 | 1.29026 | 1.33466 | |

| Hall-Wood | 1.69452 | 1.44479 | 1.55843 | |

| Wavelet | 1.64103 | 1.47871 | 1.56843 | |

| Company | ||||||

|---|---|---|---|---|---|---|

| AKSEN | ENJSA | GSRAY | ODAS | ZOREN | ||

| During COVID-19 Pandemic | Box | 1.39232 | 1.3581 | 1.24593 | 1.26178 | 1.32193 |

| DCT | 1.52748 | 1.51357 | 1.54889 | 1.54157 | 1.4914 | |

| Genton | 1.59779 | 1.6909 | 1.42786 | 1.06529 | 1.01282 | |

| Hall-Wood | 1.43438 | 1.5037 | 1.58954 | 1.47734 | 1.51174 | |

| Wavelet | 1.55901 | 1.58398 | 1.60411 | 1.56638 | 1.5802 | |

| After COVID-19 Pandemic | Box | 1.35022 | 1.2751 | 1.32193 | 1.24593 | 1.22239 |

| DCT | 1.44307 | 1.66975 | 1.52539 | 1.65137 | 1.52778 | |

| Genton | 1.59769 | 1.5533 | 1.33466 | 1.6908 | 1.01273 | |

| Hall-Wood | 1.51203 | 1.48514 | 1.55843 | 1.63719 | 1.56331 | |

| Wavelet | 1.54996 | 1.60942 | 1.56843 | 1.61333 | 1.57025 | |

| Company | ||||||||

|---|---|---|---|---|---|---|---|---|

| ALGYO | IHLGM | EKGYO | ISGYO | TRGYO | ISMEN | ENKAI | ||

| During COVID-19 Pandemic | Box | 1.20105 | 1.37851 | 1.34792 | 1.18129 | 1.35364 | 1.22972 | 1.41825 |

| DCT | 1.50116 | 1.49181 | 1.36077 | 1.40249 | 1.35799 | 1.30878 | 1.59954 | |

| Genton | 1.36075 | 1.1.0952 | 1.08682 | 1.01282 | 1.42786 | 1.45643 | 1.64509 | |

| Hall-Wood | 1.30956 | 1.37466 | 1.42515 | 1.34385 | 1.3838 | 1.50026 | 1.55391 | |

| Wavelet | 1.564 | 1.65747 | 1.51016 | 1.49364 | 1.51121 | 1.50724 | 1.6693 | |

| After COVID-19 Pandemic | Box | 1.30946 | 1.35364 | 1.22239 | 1.33621 | 1.39232 | 1.18462 | 1.44057 |

| DCT | 1.53015 | 1.58646 | 1.55705 | 1.59204 | 1.47999 | 1.2965 | 1.8313 | |

| Genton | 1.49816 | 1.57663 | 1.42777 | 1.42777 | 1.42777 | 1.67975 | 1.37951 | |

| Hall-Wood | 1.57801 | 1.57213 | 1.52622 | 1.6234 | 1.44053 | 1.55901 | 1.55809 | |

| Wavelet | 1.56808 | 1.61339 | 1.54428 | 1.60193 | 1.52894 | 1.43918 | 1.74153 | |

| Company | |||||||

|---|---|---|---|---|---|---|---|

| BRSAN | CEMAS | CEMTS | ERBOS | EREGL | KRDMD | ||

| During COVID-19 Pandemic | Box | 1.45943 | 1.41825 | 1.58496 | 1.51457 | 1.35364 | 1.47393 |

| DCT | 1.69528 | 1.5268 | 1.31213 | 1.40179 | 1.47164 | 1.53113 | |

| Genton | 1.31238 | 2.01282 | 1.39507 | 1.39615 | 1.48231 | 1.40514 | |

| Hall-Wood | 1.25374 | 1.5827 | 1.45416 | 1.50027 | 1.50255 | 1.39094 | |

| Wavelet | 1.65178 | 1.61258 | 1.48435 | 1.54503 | 1.56887 | 1.60426 | |

| After COVID-19 Pandemic | Box | 1.27216 | 1.26178 | 1.3581 | 1.14005 | 1.23902 | 1.27216 |

| DCT | 1.48449 | 1.47841 | 1.6488 | 1.58219 | 1.8281 | 1.50982 | |

| Genton | 1.42777 | 1.42777 | 1.6273 | 1.46171 | 1.50177 | 1.7497 | |

| Hall-Wood | 1.62374 | 1.44228 | 1.63716 | 1.53733 | 1.49404 | 1.65949 | |

| Wavelet | 1.51227 | 1.56394 | 1.61972 | 1.54408 | 1.5628 | 1.50406 | |

| Company | |||||

|---|---|---|---|---|---|

| AEFES | CCOLA | KERVT | ULKER | ||

| During COVID-19 Pandemic | Box | 1.27302 | 1.16096 | 1.29248 | 1.53605 |

| DCT | 1.59562 | 1.54606 | 1.62966 | 1.56977 | |

| Genton | 1.42786 | 1.31622 | 1.01282 | 1.4534 | |

| Hall-Wood | 1.54644 | 1.38652 | 1.51887 | 1.46041 | |

| Wavelet | 1.64823 | 1.5565 | 1.6376 | 1.64383 | |

| After COVID-19 Pandemic | Box | 1.24793 | 1.42065 | 1.39232 | 1.34792 |

| DCT | 1.55635 | 1.50977 | 1.62563 | 1.6106 | |

| Genton | 1.42777 | 1.44638 | 1.49816 | 1.5273 | |

| Hall-Wood | 1.54899 | 1.51059 | 1.43155 | 1.45563 | |

| Wavelet | 1.61962 | 1.57293 | 1.61228 | 1.62522 | |

| Company | |||||||

|---|---|---|---|---|---|---|---|

| AKSA | ALKIM | BRISA | EGGUB | GUBRF | HEKTS | ||

| During COVID-19 Pandemic | Box | 1.5 | 1.16096 | 1.29248 | 1.36848 | 1.02531 | 1.27216 |

| DCT | 1.52271 | 1.44591 | 1.43384 | 1.41048 | 1.23891 | 1.31219 | |

| Genton | 1.42786 | 1.59779 | 1.33475 | 1.287 | 1.33475 | 1.46028 | |

| Hall-Wood | 1.34021 | 1.36346 | 1.40891 | 1.41459 | 1.35553 | 1.3785 | |

| Wavelet | 1.55739 | 1.50529 | 1.48497 | 1.51245 | 1.37953 | 1.49638 | |

| After COVID-19 Pandemic | Box | 1.22972 | 1.41825 | 1.14005 | 1.35022 | 1.20105 | 1.06464 |

| DCT | 1.59267 | 1.61159 | 1.48936 | 1.55797 | 1.51079 | 1.61711 | |

| Genton | 1.59769 | 1.42777 | 1.56022 | 1.52853 | 1.41654 | 1.39975 | |

| Hall-Wood | 1.68157 | 1.48911 | 1.63717 | 1.54632 | 1.54637 | 1.49217 | |

| Wavelet | 1.5747 | 1.5665 | 1.59737 | 1.54603 | 1.53512 | 1.53014 | |

| KARTN | PETKM | RTALB | SASA | TUPRS | DEVA | ||

| During COVID-19 Pandemic | Box | 1.33621 | 1.45943 | 1.27729 | 1.41825 | 1.58496 | 1.27216 |

| DCT | 1.37973 | 1.49943 | 1.36019 | 1.43944 | 1.62698 | 1.54888 | |

| Genton | 1.48231 | 1.56922 | 1.01282 | 1.43859 | 1.42786 | 1.64562 | |

| Hall-Wood | 1.42035 | 1.36165 | 1.4537 | 1.44567 | 1.49677 | 1.5171 | |

| Wavelet | 1.54535 | 1.56379 | 1.4911 | 1.57521 | 1.61367 | 1.4928 | |

| After COVID-19 Pandemic | Box | 1.16096 | 1.43724 | 0.8625 | 1.20752 | 1.29546 | 1.19616 |

| DCT | 1.38873 | 1.52578 | 1.45971 | 1.51255 | 1.5749 | 1.51234 | |

| Genton | 1.46959 | 1.54707 | 1.51796 | 1.58292 | 1.48917 | 1.49526 | |

| Hall-Wood | 1.36295 | 1.71527 | 1.40161 | 1.66586 | 1.56172 | 1.58273 | |

| Wavelet | 1.43129 | 1.59343 | 1.47861 | 1.51861 | 1.58164 | 1.62658 | |

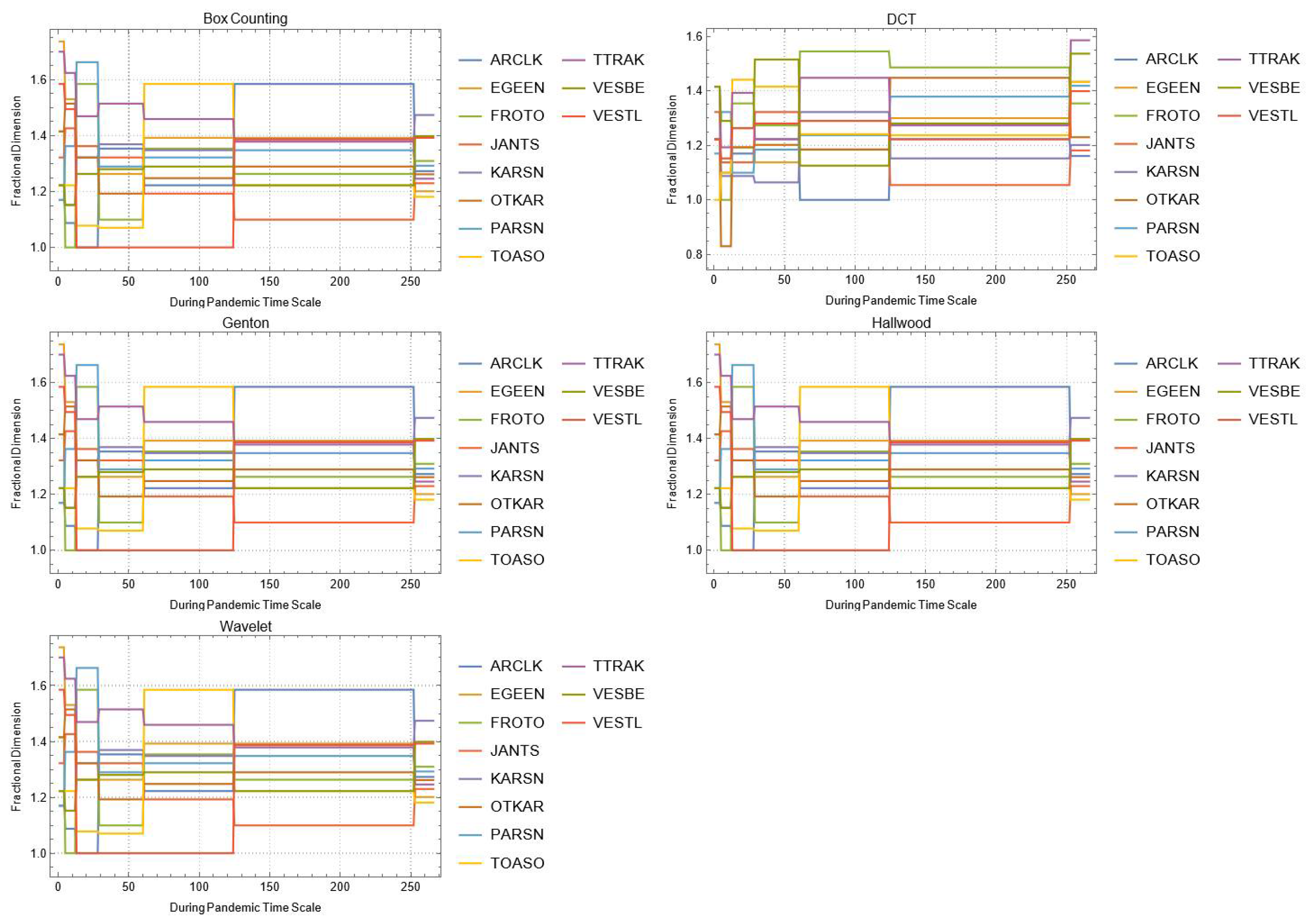

| Company | |||||||

|---|---|---|---|---|---|---|---|

| ARCLK | EGEEN | FROTO | JANTS | KARSN | OTKAR | ||

| During COVID-19 Pandemic | Box | 1.54432 | 1.32604 | 1.27729 | 1.20105 | 1.47393 | 1.41825 |

| DCT | 1.46293 | 1.42102 | 1.5705 | 1.5358 | 1.70412 | 1.45764 | |

| Genton | 1.48926 | 1.50173 | 1.4703 | 1.42786 | 1.22433 | 1.51806 | |

| Hall-Wood | 1.44664 | 1.49985 | 1.56409 | 1.4205 | 1.3637 | 1.4337 | |

| Wavelet | 1.59237 | 1.50315 | 1.61418 | 1.51549 | 1.62626 | 1.56887 | |

| After COVID-19 Pandemic | Box | 1.22029 | 1.3863 | 1.29248 | 1.31225 | 1.22972 | 1.23902 |

| DCT | 1.85999 | 1.67799 | 1.52389 | 1.35321 | 1.54756 | 1.63595 | |

| Genton | 1.42777 | 1.47814 | 1.59769 | 1.51257 | 1.42777 | 1.56325 | |

| Hall-Wood | 1.50839 | 1.5015 | 1.58748 | 1.52693 | 1.55525 | 1.65497 | |

| Wavelet | 1.61282 | 1.57105 | 1.63225 | 1.42554 | 1.5453 | 1.54648 | |

| PARSN | TOASO | TTRAK | VESBE | VESTL | |||

| During COVID-19 Pandemic | Box | 1.20163 | 1.152 | 1.1427 | 1.39232 | 1.47393 | |

| DCT | 1.50052 | 1.46573 | 1.47848 | 1.40889 | 1.33578 | ||

| Genton | 1.27586 | 1.39615 | 1.34724 | 1.46195 | 1.39615 | ||

| Hall-Wood | 1.30441 | 1.37369 | 1.3862 | 1.3647 | 1.38722 | ||

| Wavelet | 1.53666 | 1.571 | 1.54132 | 1.47231 | 1.50764 | ||

| After COVID-19 Pandemic | Box | 1.29248 | 1.3581 | 1.22972 | 1.11852 | 1.25125 | |

| DCT | 1.52648 | 1.55559 | 1.58801 | 1.58967 | 1.41387 | ||

| Genton | 1.46019 | 1.48221 | 1.4882 | 1.32336 | 1.42777 | ||

| Hall-Wood | 1.51478 | 1.52797 | 1.51241 | 1.49605 | 1.59371 | ||

| Wavelet | 1.59759 | 1.59814 | 1.54897 | 1.54547 | 1.51057 | ||

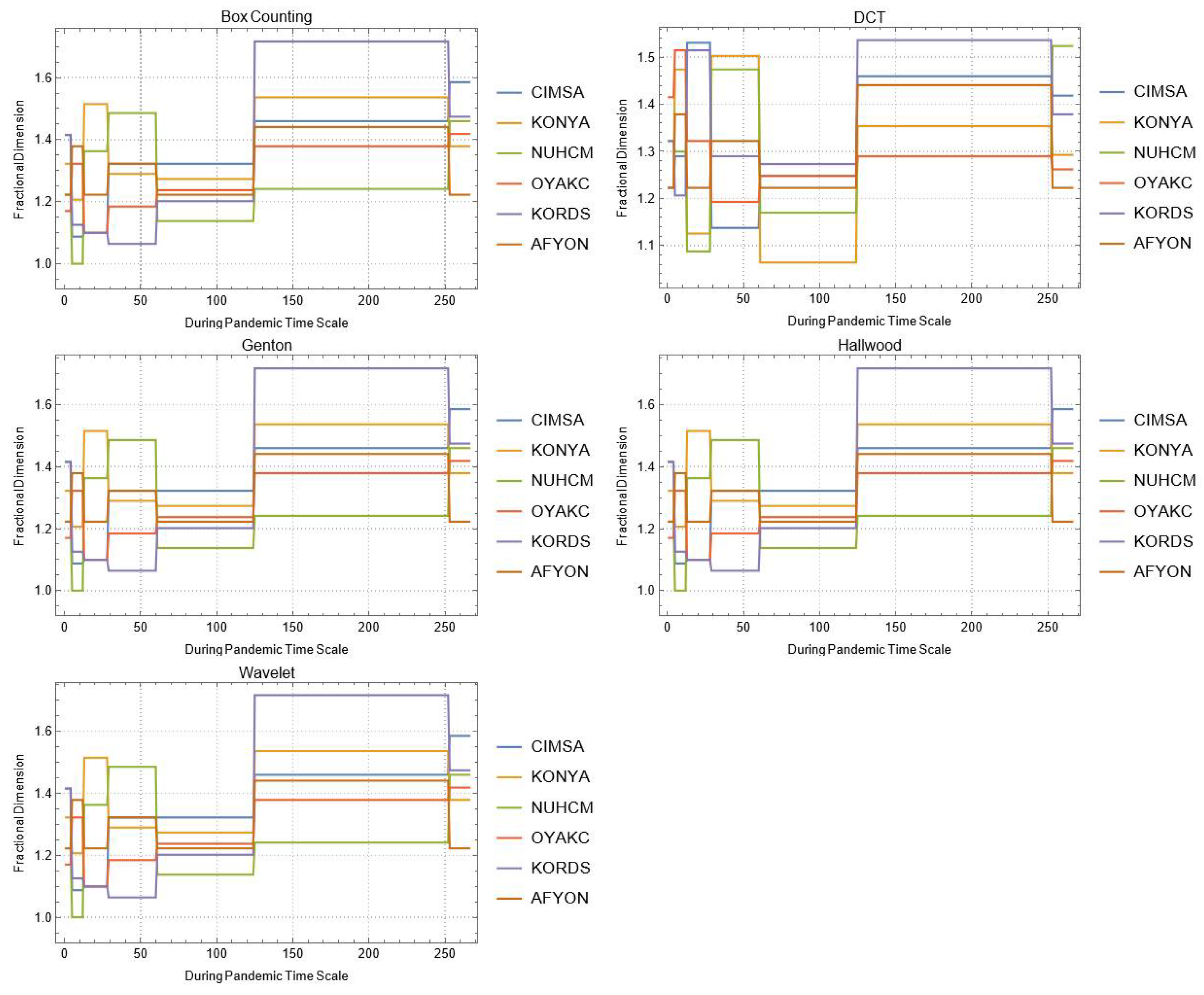

| Company | |||||||

|---|---|---|---|---|---|---|---|

| CIMSA | KONYA | NUHCM | OYAKC | KORDS | AFYON | ||

| During COVID-19 Pandemic | Box | 1.45943 | 1.47393 | 1.22972 | 1.29248 | 1.1375 | 1.33621 |

| DCT | 1.44766 | 1.62888 | 1.43918 | 1.59801 | 1.53645 | 1.67943 | |

| Genton | 1.42786 | 1.42786 | 1.42786 | 1.59779 | 1.37539 | 1.42786 | |

| Hall-Wood | 1.4666 | 1.42647 | 1.42647 | 1.46293 | 1.37825 | 1.3729 | |

| Wavelet | 1.5538 | 1.67507 | 1.67507 | 1.52817 | 1.54816 | 1.64333 | |

| After COVID-19 Pandemic | Box | 1.33148 | 1.36848 | 1.36848 | 1.28951 | 1.22971 | 1.29248 |

| DCT | 1.46268 | 1.52558 | 1.52558 | 1.59013 | 1.56263 | 1.53319 | |

| Genton | 1.59769 | 1.56074 | 1.56074 | 1.49816 | 1.48917 | 1.5273 | |

| Hall-Wood | 1.70257 | 1.48939 | 1.48939 | 1.61519 | 1.65369 | 1.52839 | |

| Wavelet | 1.59858 | 1.50925 | 1.50925 | 1.61267 | 1.57949 | 1.57245 | |

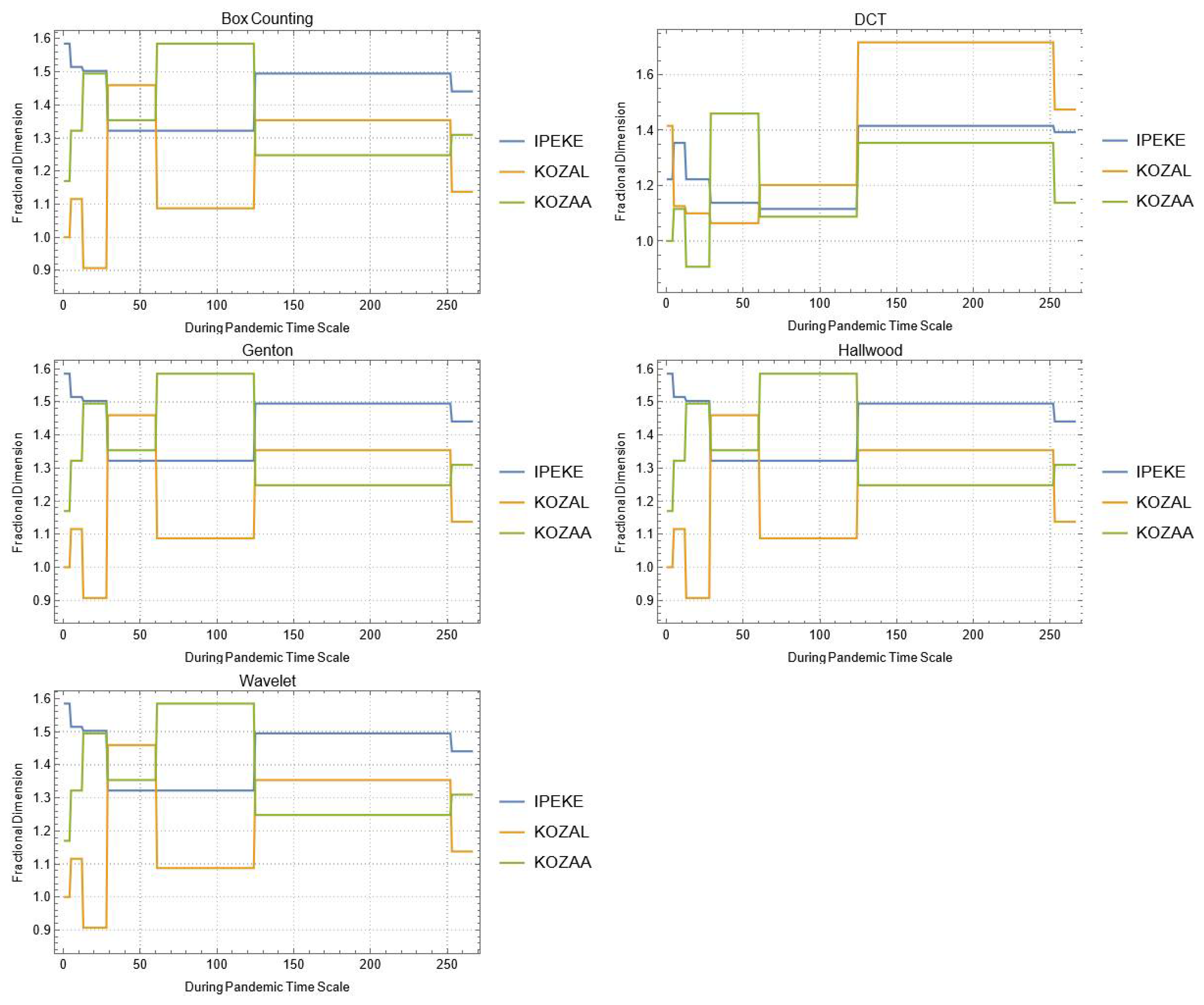

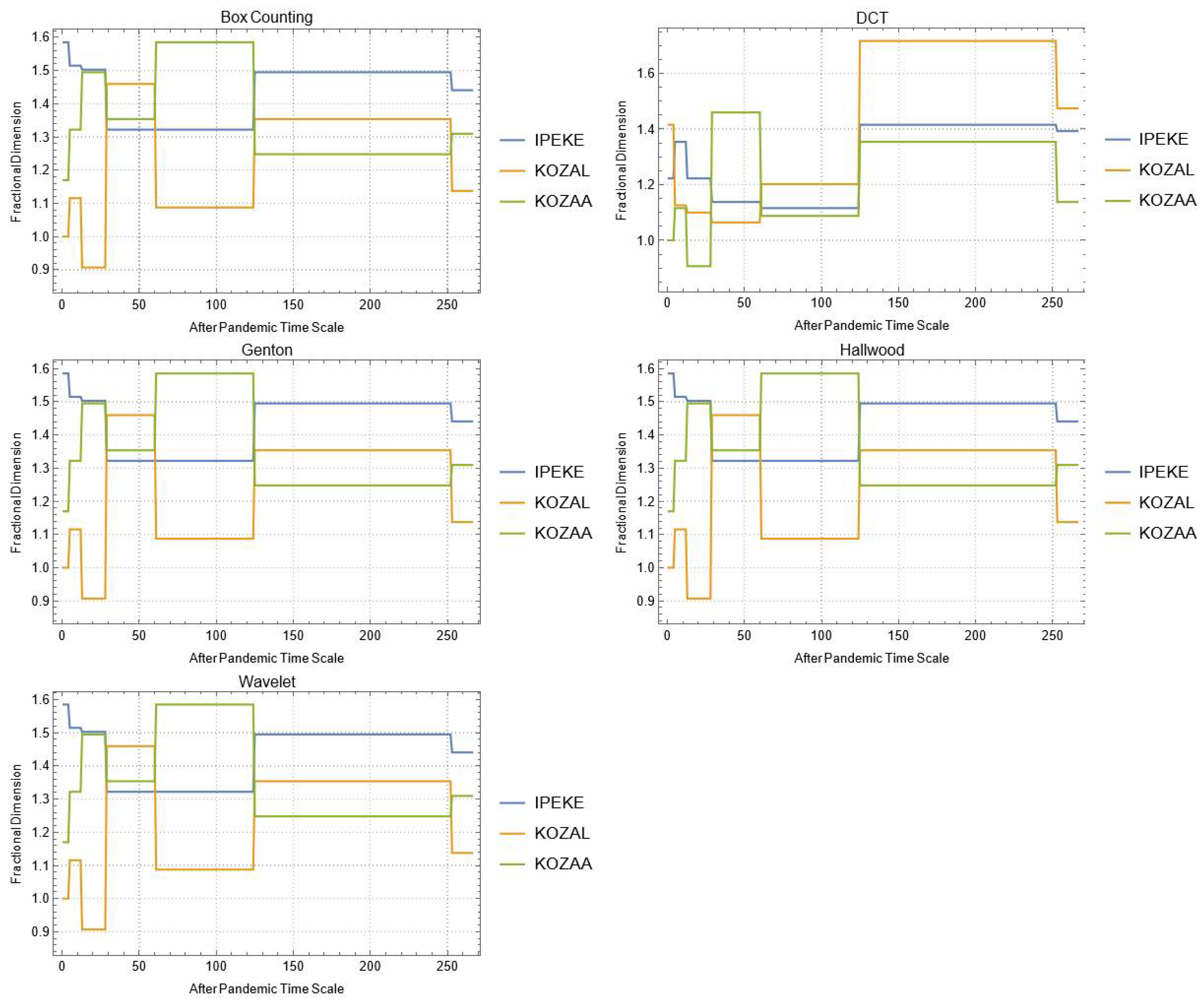

| Company | ||||

|---|---|---|---|---|

| IPEKE | KOZAL | KOZAA | ||

| During COVID-19 Pandemic | Box | 1.37362 | 1.30946 | 1.24793 |

| DCT | 1.49956 | 1.59903 | 1.39995 | |

| Genton | 1.49825 | 1.56536 | 1.5979 | |

| Hall-Wood | 1.58478 | 1.64702 | 1.69209 | |

| Wavelet | 1.61985 | 1.6039 | 1.60488 | |

| After COVID-19 Pandemic | Box | 1.35364 | 1.23902 | 1.40368 |

| DCT | 1.56465 | 1.52856 | 1.53189 | |

| Genton | 1.5533 | 1.48221 | 1.5533 | |

| Hall-Wood | 1.5842 | 1.47435 | 1.511276 | |

| Wavelet | 1.5942 | 1.54517 | 1.57928 | |

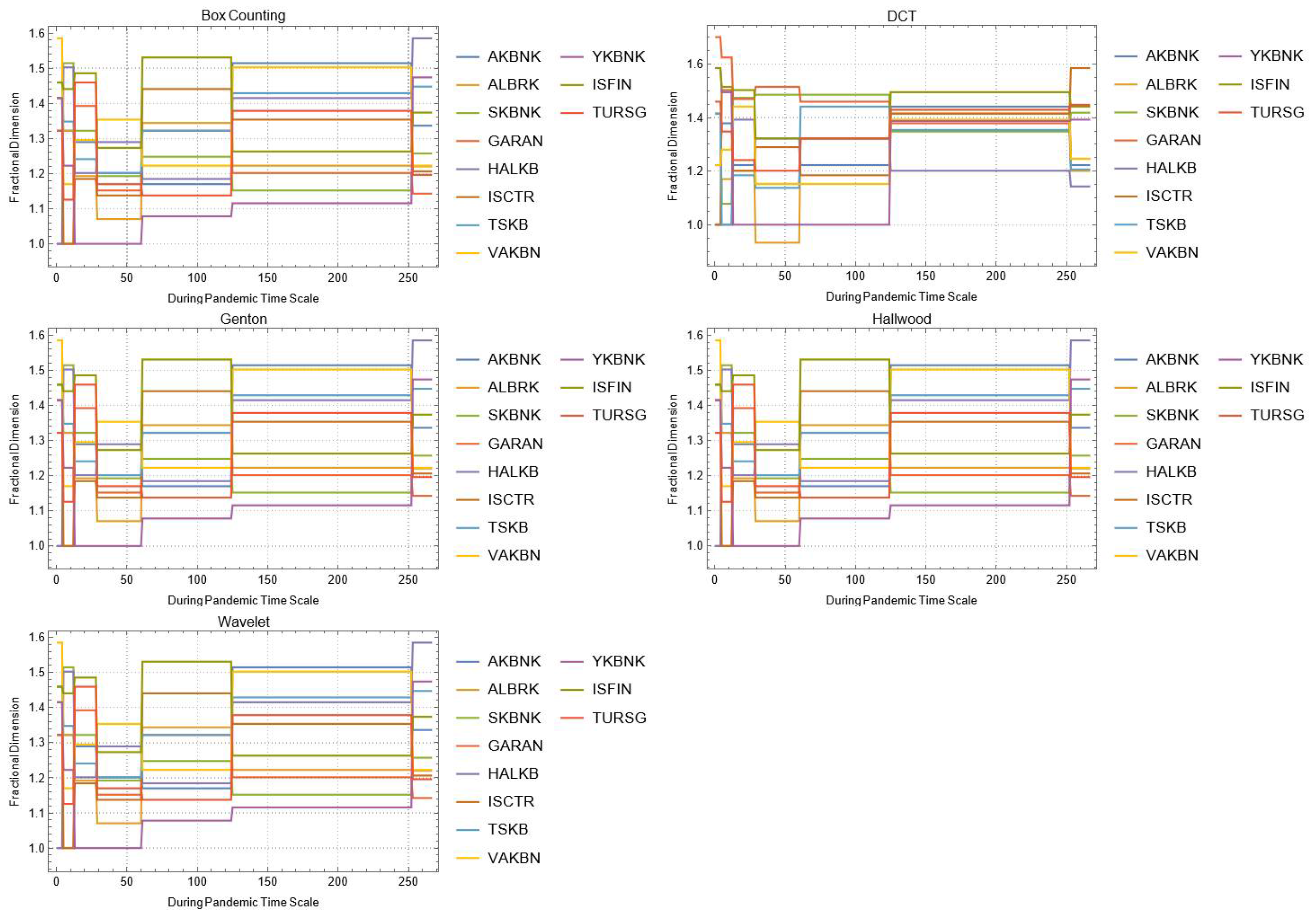

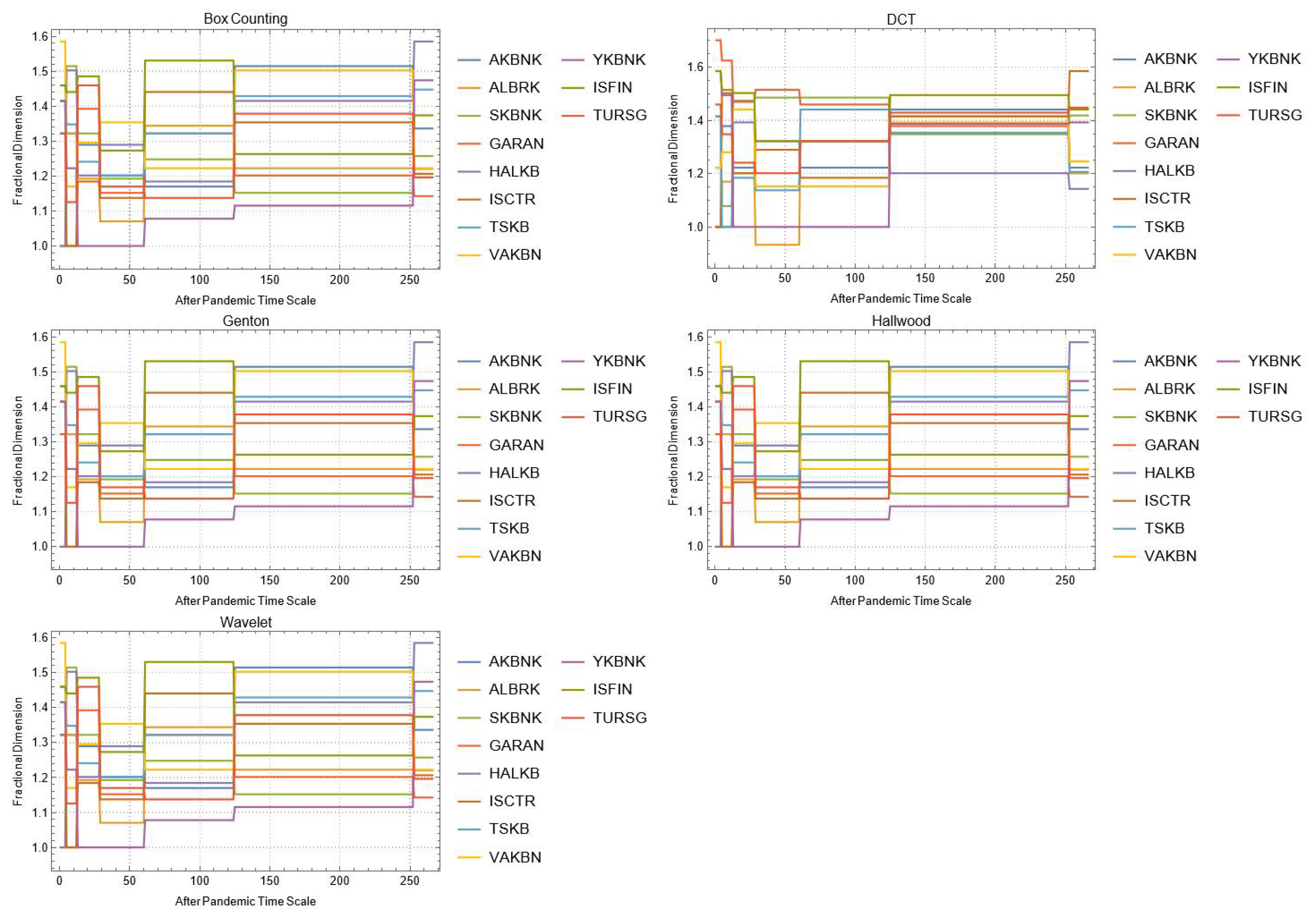

| Company | |||||||

|---|---|---|---|---|---|---|---|

| AKBNK | ALBRK | SKBNK | GARAN | HALKB | ISCTR | ||

| During COVID-19 Pandemic | Box | 1.63743 | 1.28951 | 1.26303 | 1.58496 | 1.20645 | 1.44746 |

| DCT | 1.66071 | 1.54484 | 1.499552 | 1.56425 | 1.59563 | 1.57338 | |

| Genton | 1.49825 | 1.16483 | 1.8429 | 1.37539 | 1.42786 | 1.42786 | |

| Hall-Wood | 1.44471 | 1.38983 | 1.41475 | 1.46153 | 1.35285 | 1.41877 | |

| Wavelet | 1.6183 | 1.6112 | 1.5655 | 1.59767 | 1.5329 | 1.57249 | |

| After COVID-19 Pandemic | Box | 1.24101 | 1.27729 | 1.32193 | 1.43296 | 1.32193 | 1.32193 |

| DCT | 1.51264 | 1.55073 | 1.69709 | 1.54787 | 1.6602 | 1.54623 | |

| Genton | 1.5273 | 2.01273 | 1.6908 | 1.42777 | 1.42777 | 1.53998 | |

| Hall-Wood | 1.52238 | 1.5544 | 1.57661 | 1.4985 | 1.5982 | 1.59875 | |

| Wavelet | 1.55175 | 1.60458 | 1.61689 | 1.54232 | 1.66689 | 1.5741 | |

| TSKB | VAKBN | YKBNK | ISFIN | TURSG | |||

| During COVID-19 Pandemic | Box | 1.19616 | 1.06413 | 1.32193 | 1.24593 | 1.24593 | |

| DCT | 1.49153 | 1.44874 | 1.55714 | 1.44361 | 1.57191 | ||

| Genton | 2.01282 | 1.33475 | 1.42786 | 1.33475 | 1.42786 | ||

| Hall-Wood | 1.39007 | 1.43632 | 1.47457 | 1.27023 | 1.36196 | ||

| Wavelet | 1.51943 | 1.51543 | 1.54846 | 1.4385 | 1.60278 | ||

| After COVID-19 Pandemic | Box | 1.40368 | 1.36923 | 1.1375 | 1.1375 | 1.48481 | |

| DCT | 1.31273 | 1.59096 | 1.68012 | 1.56347 | 1.57141 | ||

| Genton | 1.15023 | 1.42777 | 1.42777 | 1.42777 | 1.62571 | ||

| Hall-Wood | 1.4476 | 1.55096 | 1.55096 | 1.61039 | 1.56522 | ||

| Wavelet | 1.44179 | 1.5469 | 1.5496 | 1.65673 | 1.57786 | ||

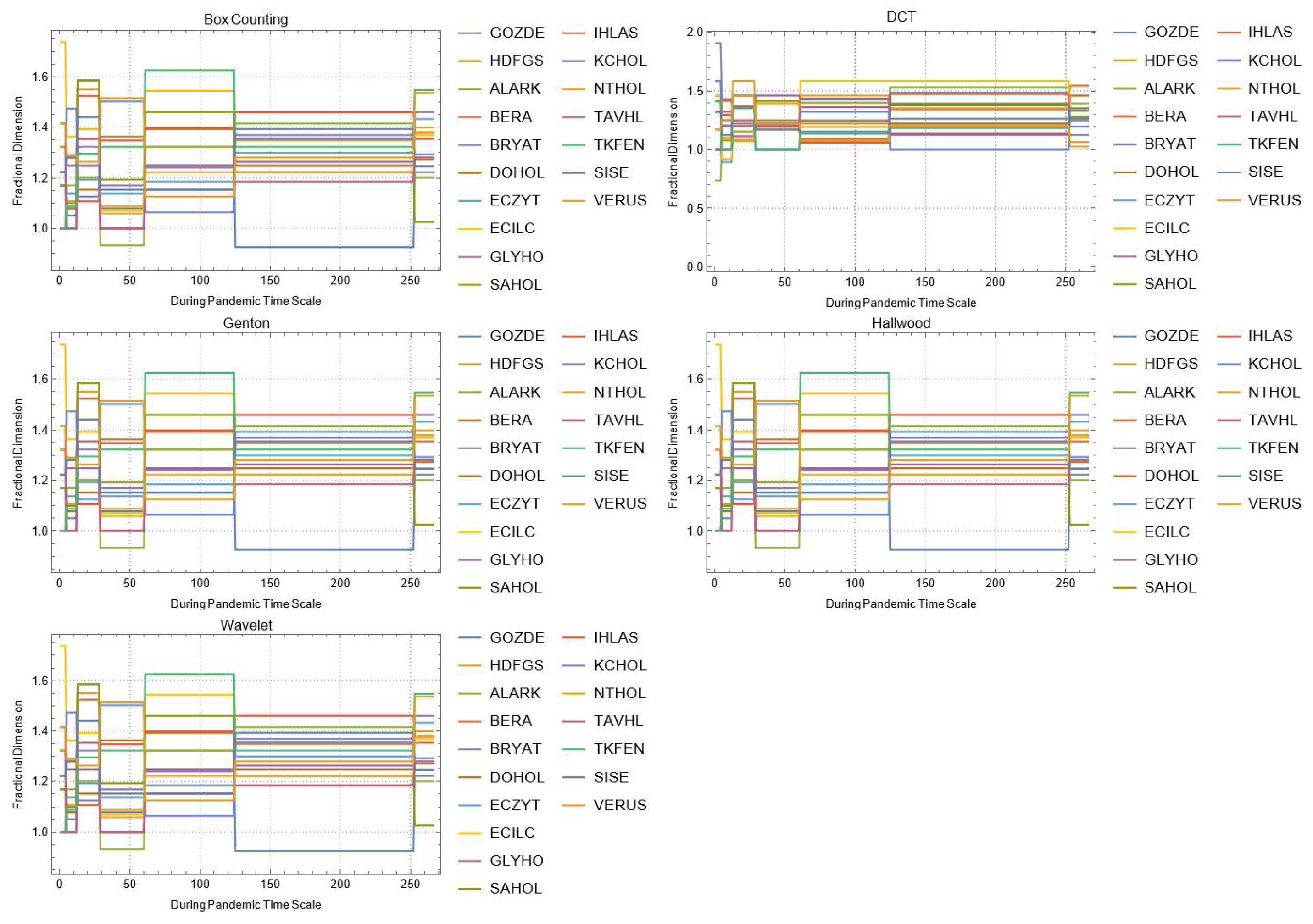

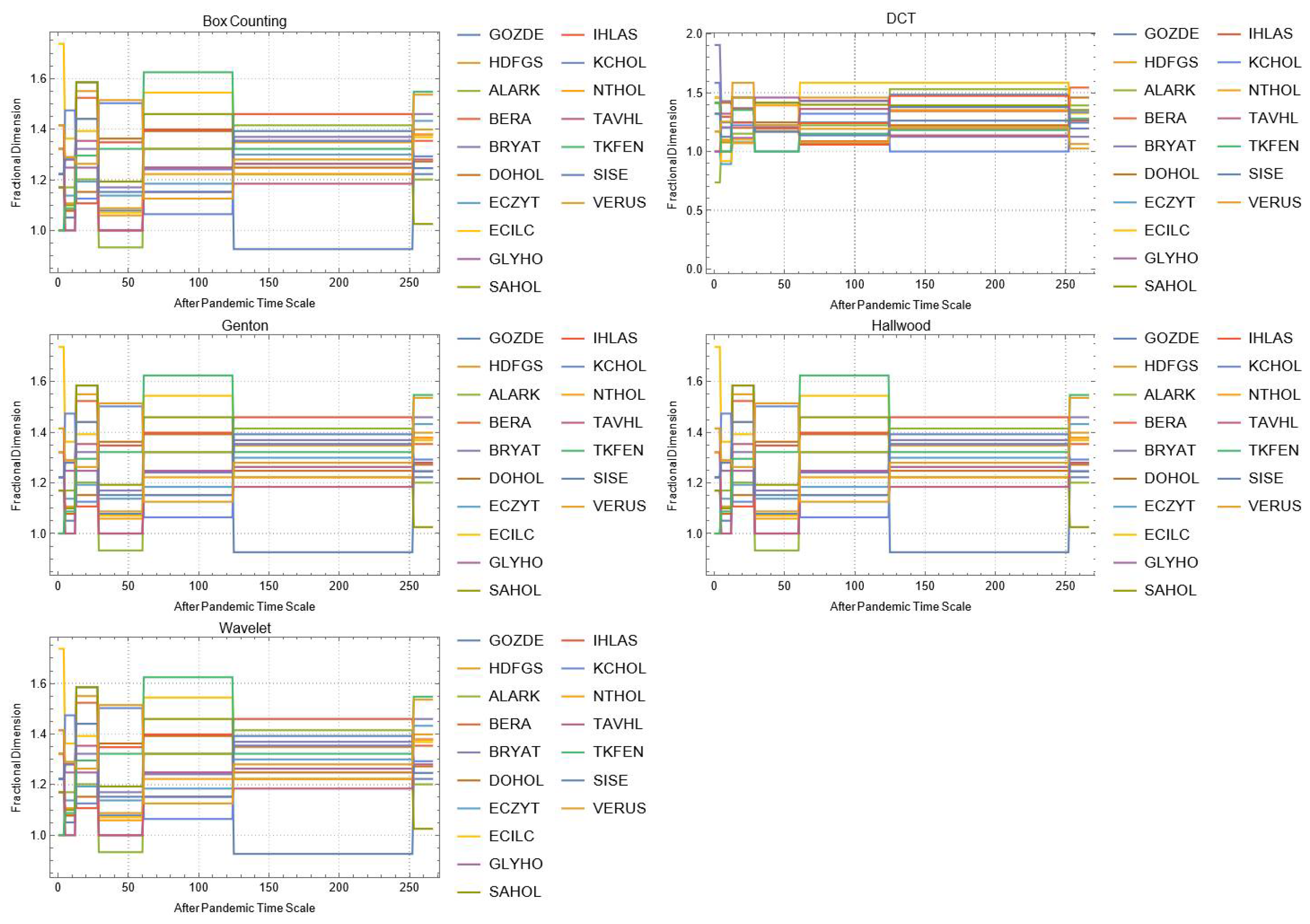

| Company | |||||||

|---|---|---|---|---|---|---|---|

| GOZDE | HDFGS | ALARK | BERA | BRYAT | DOHOL | ||

| During COVID-19 Pandemic | Box | 1.35364 | 1.16096 | 1.22029 | 1.37362 | 1.2751 | 1.320604 |

| DCT | 1.47725 | 1.43632 | 1.45664 | 1.41202 | 1.54647 | 1.497 | |

| Genton | 1.42786 | 1.74979 | 1.49087 | 1.59779 | 1.28584 | 1.08682 | |

| Hall-Wood | 1.34344 | 1.44842 | 1.50356 | 1.42336 | 1.38412 | 1.45422 | |

| Wavelet | 1.49981 | 1.43171 | 1.48553 | 1.54662 | 1.55072 | 1.52969 | |

| After COVID-19 Pandemic | Box | 1.37362 | 1.27216 | 1.22972 | 1.22029 | 1.20105 | 1.29248 |

| DCT | 1.6002 | 1.56201 | 1.51067 | 1.45444 | 1.35748 | 1.59235 | |

| Genton | 1.48221 | 1.70239 | 1.47891 | 1.39975 | 1.39783 | 1.62278 | |

| Hall-Wood | 1.49163 | 1.53124 | 1.52274 | 1.44065 | 1.49297 | 1.648 | |

| Wavelet | 1.63653 | 1.49604 | 1.51656 | 1.49968 | 1.49047 | 1.59659 | |

| ECZYT | ECILC | GLYHO | SAHOL | IHLAS | KCHOL | ||

| During COVID-19 Pandemic | Box | 1.20105 | 1.19233 | 1.22239 | 1.39855 | 1.39232 | 1.37851 |

| DCT | 1.42554 | 1.59824 | 1.46271 | 1.65878 | 1.59021 | 1.50579 | |

| Genton | 1.33475 | 1.38833 | 1.27586 | 1.49825 | 2.01282 | 1.46534 | |

| Hall-Wood | 1.4653 | 1.45421 | 1.43999 | 1.53787 | 1.55502 | 1.42767 | |

| Wavelet | 1.51942 | 1.56661 | 1.50633 | 1.6205 | 1.64907 | 1.61186 | |

| After COVID-19 Pandemic | Box | 1.12462 | 1.41825 | 1.39232 | 1.28951 | 1.30736 | 1.152 |

| DCT | 1.38873 | 1.61058 | 1.60024 | 1.65413 | 1.53119 | 1.5816 | |

| Genton | 1.39382 | 1.49816 | 1.65016 | 1.49816 | 1.16473 | 1.48917 | |

| Hall-Wood | 1.49367 | 1.55717 | 1.57341 | 1.49305 | 1.59042 | 1.61307 | |

| Wavelet | 1.49483 | 1.65927 | 1.58808 | 1.52649 | 1.58222 | 1.54236 | |

| NTHOL | TAVHL | TKFEN | VERUS | SISE | |||

| During COVID-19 Pandemic | Box | 1.52356 | 1.54749 | 1.43296 | 1.39855 | 1.22239 | |

| DCT | 1.25355 | 1.50715 | 1.49315 | 1.51997 | 1.64314 | ||

| Genton | 1.01282 | 1.49825 | 1.40514 | 1.01282 | 1.5225 | ||

| Hall-Wood | 1.27592 | 1.57447 | 1.4897 | 1.24081 | 1.46576 | ||

| Wavelet | 1.49223 | 1.5605 | 1.57421 | 1.54008 | 1.59263 | ||

| After COVID-19 Pandemic | Box | 1.06464 | 1.43296 | 1.48543 | 1.11852 | 1.3888 | |

| DCT | 1.51917 | 1.51042 | 1.48723 | 1.57742 | 1.62597 | ||

| Genton | 1.42777 | 1.47668 | 1.5273 | 1.40392 | 1.58531 | ||

| Hall-Wood | 1.5423 | 1.52508 | 1.65222 | 1.4892 | 1.56705 | ||

| Wavelet | 1.57562 | 1.56515 | 1.58128 | 1.56462 | 1.65136 | ||

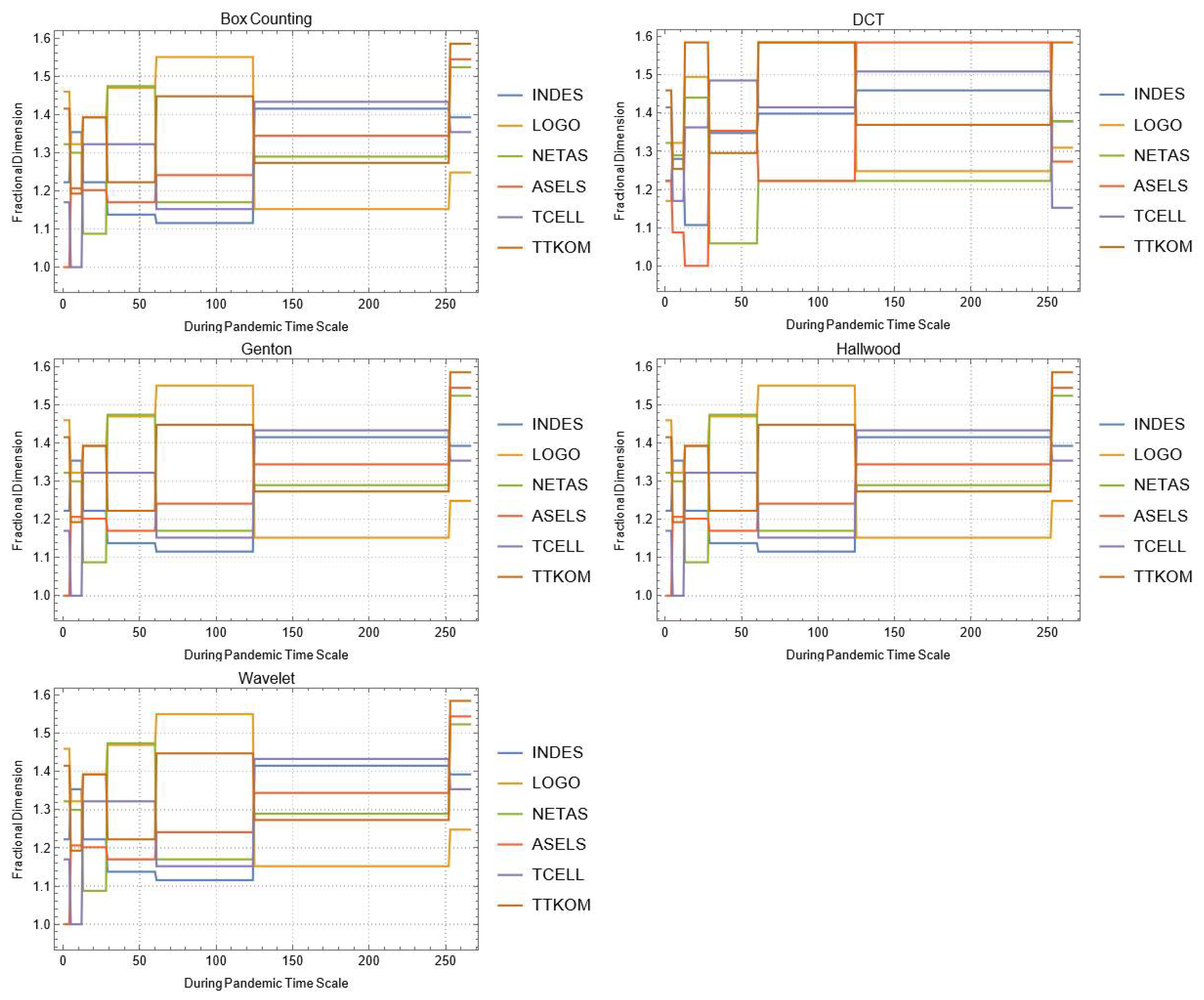

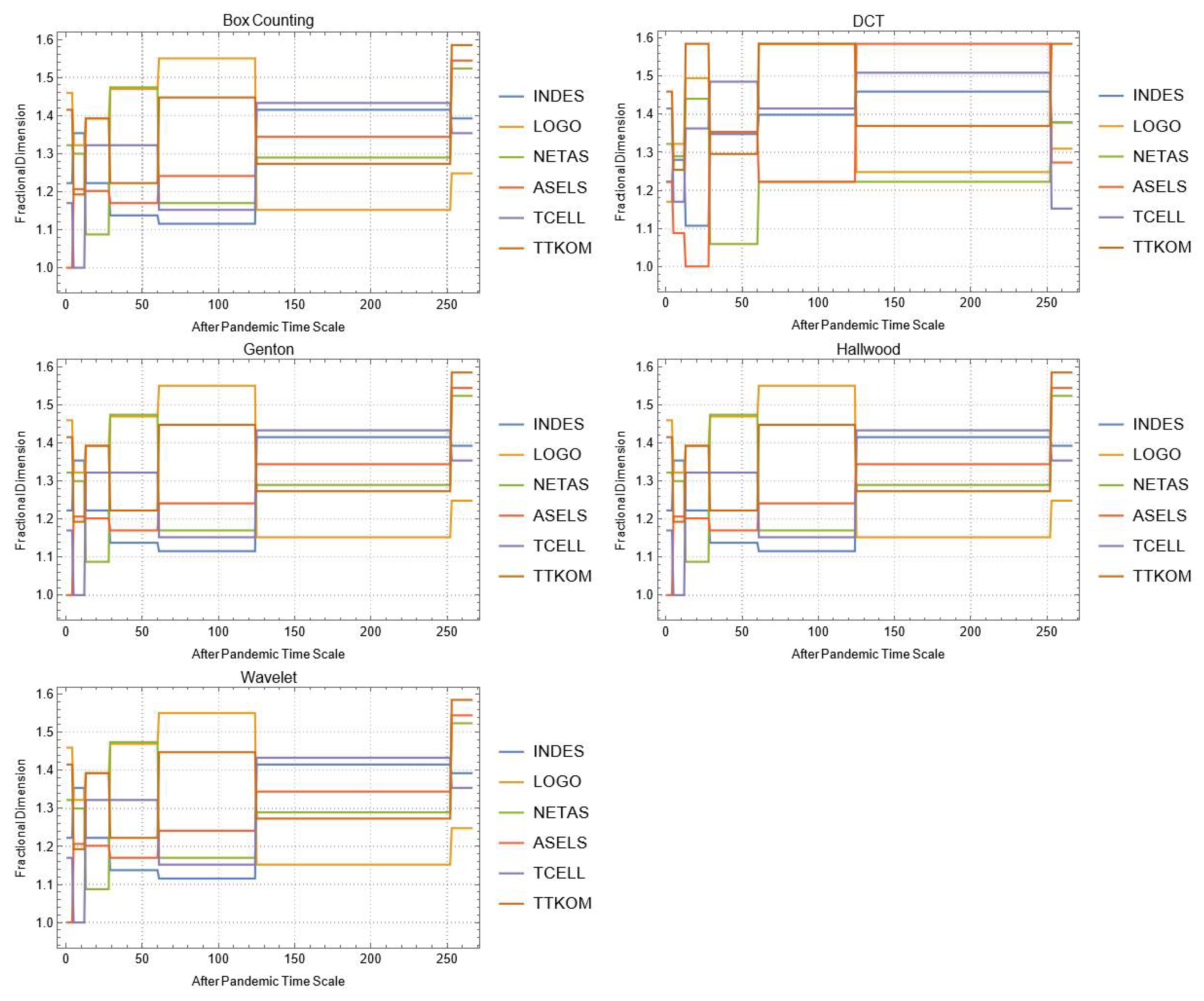

| Company | |||||||

|---|---|---|---|---|---|---|---|

| INDES | LOGO | NETAS | ASELS | TCELL | TTKOM | ||

| During COVID-19 Pandemic | Box | 1.44057 | 1.22239 | 1.45943 | 1.35364 | 1.39855 | 1.24593 |

| DCT | 1.39189 | 1.4589 | 1.63822 | 1.48452 | 1.56951 | 1.56672 | |

| Genton | 1.45095 | 1.30795 | 1.34986 | 1.5274 | 1.5274 | 1.59779 | |

| Hall-Wood | 1.38627 | 1.31053 | 1.40739 | 1.49313 | 1.48876 | 1.5099 | |

| Wavelet | 1.43944 | 1.45426 | 1.6154 | 1.56521 | 1.65928 | 1.59563 | |

| After COVID-19 Pandemic | Box | 1.25125 | 1.44376 | 1.32604 | 1.22239 | 1.58496 | 1.43296 |

| DCT | 1.25967 | 1.61606 | 1.51304 | 1.60297 | 1.64814 | 1.78624 | |

| Genton | 1.51892 | 1.38781 | 1.47839 | 1.62571 | 1.59769 | 1.62016 | |

| Hall-Wood | 1.51808 | 1.4335 | 1.63836 | 1.71768 | 1.528 | 1.57942 | |

| Wavelet | 1.50682 | 1.60631 | 1.56389 | 1.65715 | 1.66324 | 1.64097 | |

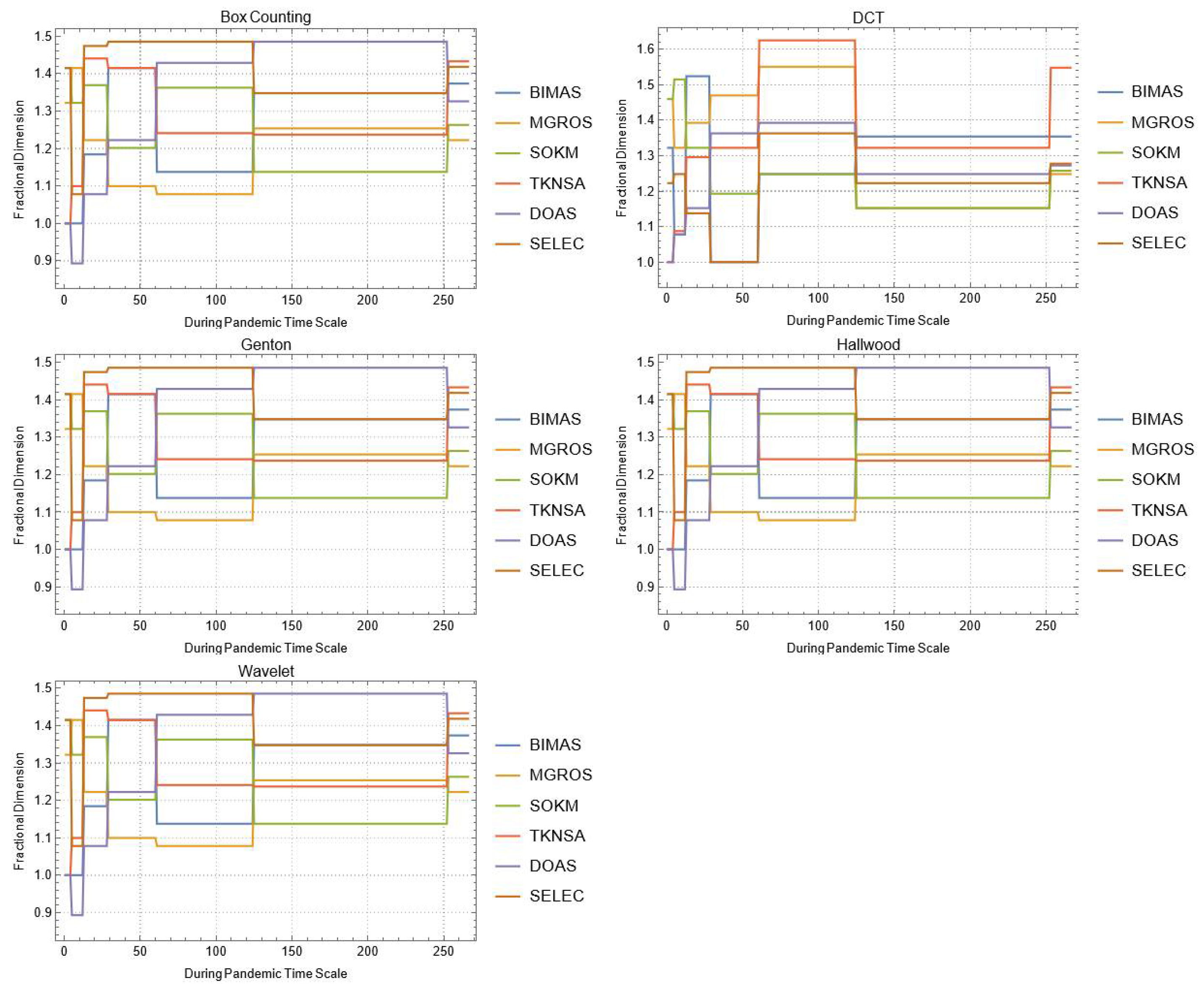

| Company | |||||||

|---|---|---|---|---|---|---|---|

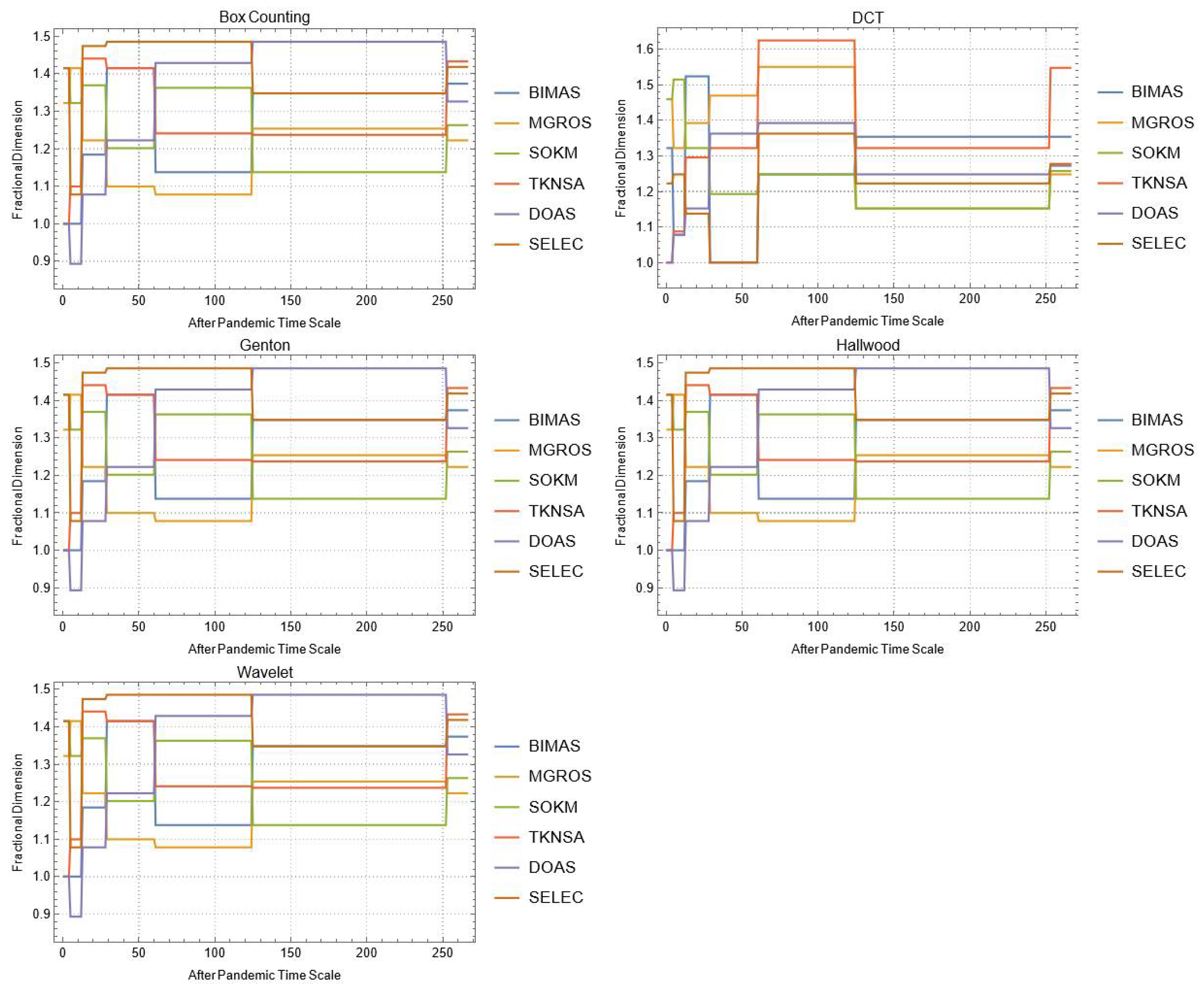

| BIMAS | MGROS | SOKM | TKNSA | DOAS | SELEC | ||

| During COVID-19 Pandemic | Box | 1.12553 | 1.26178 | 1.28011 | 1.18129 | 1.43254 | 1.25729 |

| DCT | 1.51763 | 1.52327 | 1.44471 | 1.47045 | 1.48424 | 1.47474 | |

| Genton | 1.5854 | 1.42786 | 1.48231 | 1.41016 | 1.2352 | 1.44025 | |

| Hall-Wood | 1.57925 | 1.46885 | 1.51494 | 1.31223 | 1.43009 | 1.48644 | |

| Wavelet | 1.59938 | 1.5454 | 1.49183 | 1.57079 | 1.563861 | 1.54858 | |

| After COVID-19 Pandemic | Box | 1.39232 | 1.21313 | 1.48393 | 1.17878 | 1.12396 | 1.17682 |

| DCT | 1.5598 | 1.59184 | 1.55517 | 1.33769 | 1.39599 | 1.48681 | |

| Genton | 1.53541 | 1.5388 | 1.46524 | 1.60775 | 1.66126 | 1.64316 | |

| Hall-Wood | 1.5162 | 1.48675 | 1.43324 | 1.54968 | 1.67103 | 1.50934 | |

| Wavelet | 1.62423 | 1.58672 | 1.62185 | 1.54931 | 1.55305 | 1.53892 | |

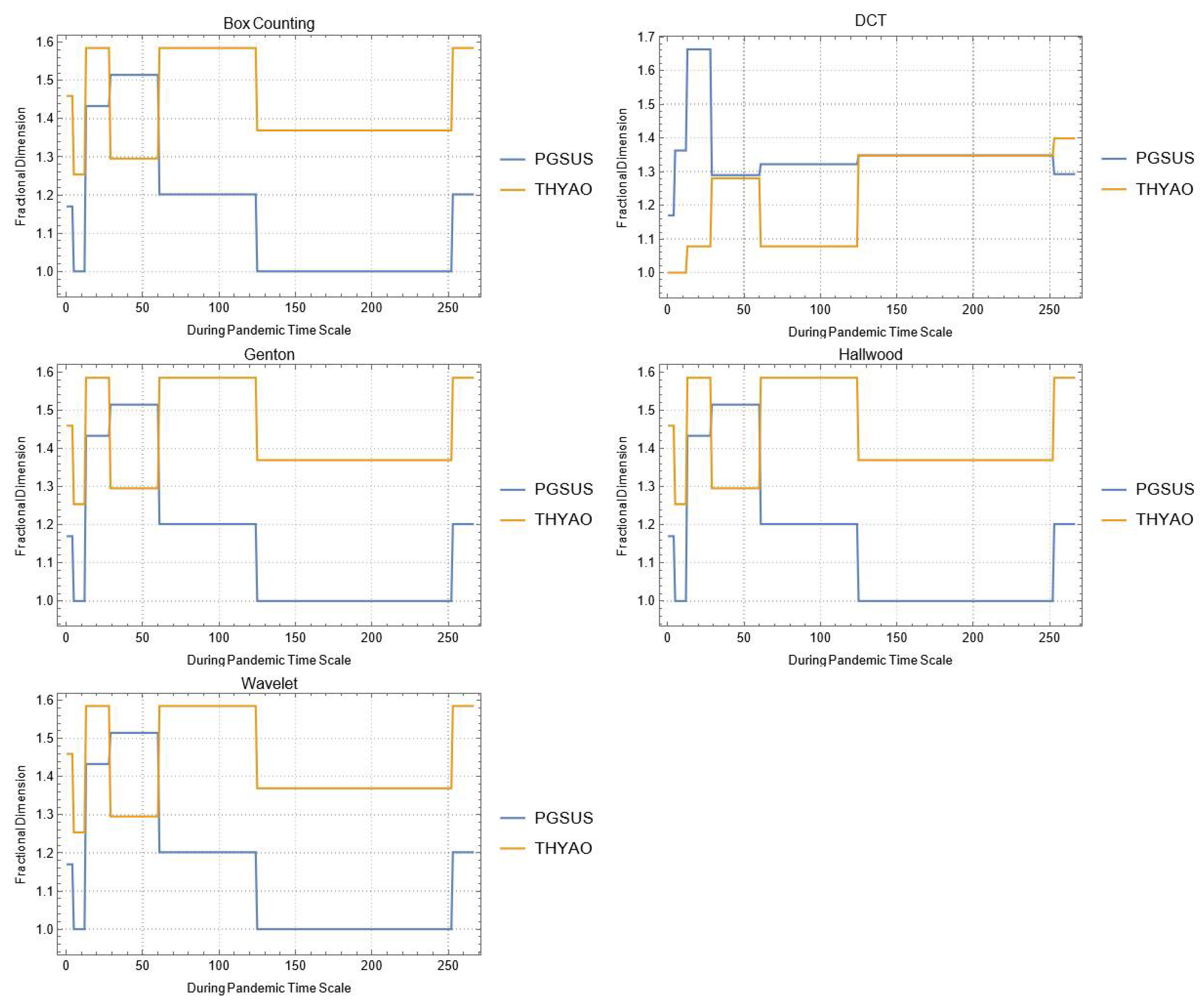

| Company | |||

|---|---|---|---|

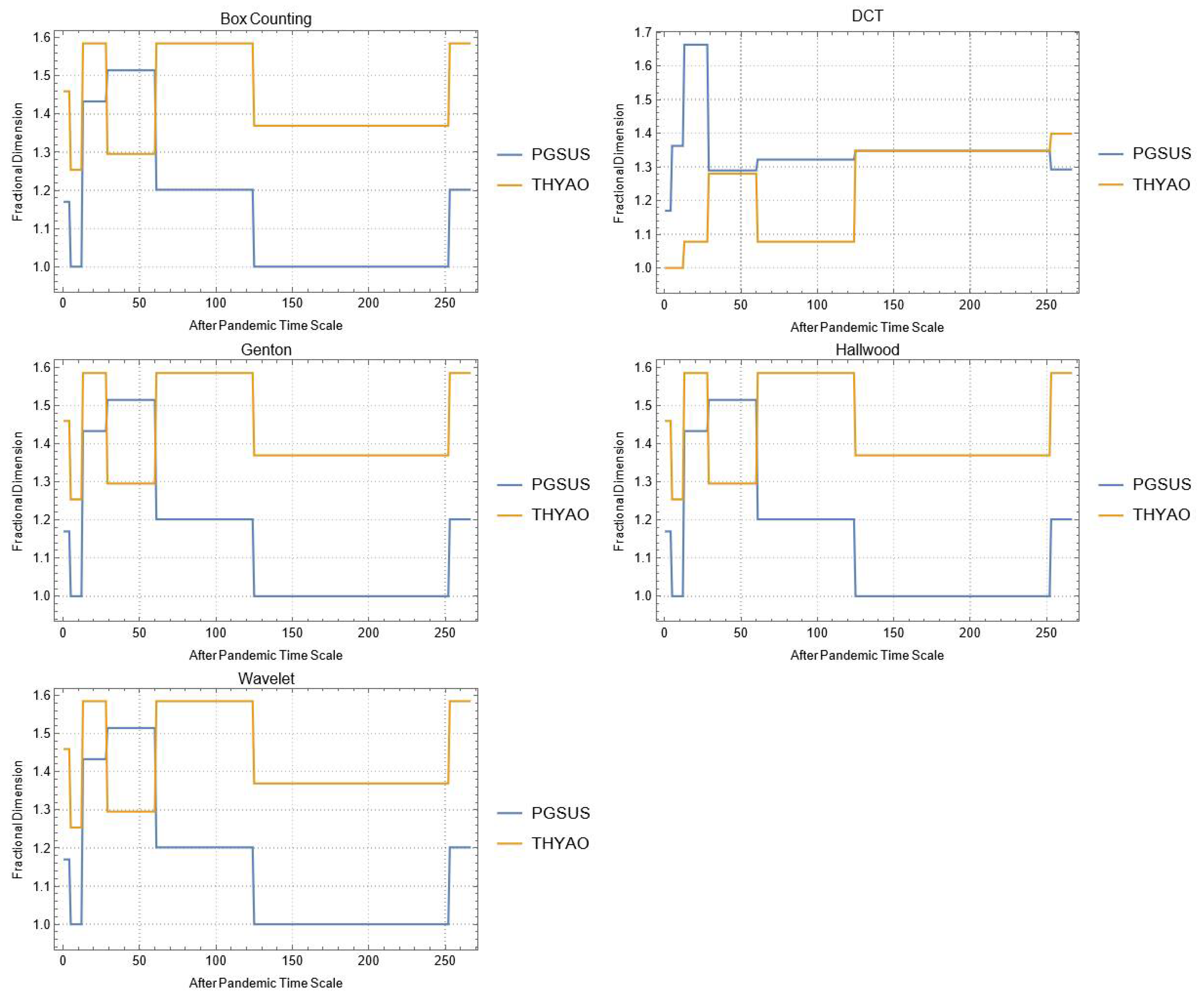

| PGSUS | THYAO | ||

| During COVID-19 Pandemic | Box | 1.22972 | 1.58496 |

| DCT | 1.34049 | 1.49706 | |

| Genton | 1.41336 | 1.57225 | |

| Hall-Wood | 1.33551 | 1.44832 | |

| Wavelet | 1.46605 | 1.59804 | |

| After COVID-19 Pandemic | Box | 1.16096 | 1.26303 |

| DCT | 1.35076 | 1.47095 | |

| Genton | 1.59302 | 1.63422 | |

| Hall-Wood | 1.6529 | 1.61102 | |

| Wavelet | 1.54537 | 1.56825 | |

| During COVID-19 Pandemic | |||||

|---|---|---|---|---|---|

| Box Counting | DCT | Genton | Hall-Wood | Wavelet | |

| Social | 26.7048 | 21.5063 | 26.7048 | 26.7048 | 26.7048 |

| Energy | 19.1639 | 28.6129 | 19.1639 | 19.1639 | 19.1639 |

| Real Estate | 32.6589 | 23.3409 | 32.6589 | 32.6589 | 32.6589 |

| Metal Industry | 31.2604 | 21.7374 | 31.2604 | 31.2604 | 31.2604 |

| Food/Beverage/Tobacco | 17.4989 | 18.602 | 17.4989 | 17.4989 | 17.4989 |

| Chemicals | 31.0055 | 34.924 | 31.0055 | 31.0055 | 31.0055 |

| Machineries | 30.4641 | 27.979 | 30.4641 | 30.4641 | 30.4641 |

| Stone-Soil based Manufacturing | 26.2005 | 21.6834 | 26.2005 | 26.2005 | 26.2005 |

| Mining | 30.567 | 33.2015 | 30.567 | 30.567 | 30.567 |

| Financials | 26.6369 | 25.2572 | 26.6369 | 26.6369 | 26.6369 |

| Holdings Investment Companies | 28.7737 | 34.2268 | 28.7737 | 28.7737 | 28.7737 |

| Technology | 24.9548 | 24.934 | 24.9548 | 24.9548 | 24.9548 |

| Wholesale Retail | 25.4617 | 272.803 | 25.4617 | 25.4617 | 25.4617 |

| Transportation | 38.9401 | 11.5473 | 38.9401 | 38.9401 | 38.9401 |

| After COVID-19 Pandemic | |||||

| Box Counting | DCT | Genton | Hall-Wood | Wavelet | |

| Social | 26.7048 | 21.5063 | 26.7048 | 26.7048 | 26.7048 |

| Energy | 19.1639 | 28.6129 | 19.1639 | 19.1639 | 19.1639 |

| Real Estate | 32.6589 | 23.3409 | 32.6589 | 32.6589 | 32.6589 |

| Metal Industry | 31.2604 | 21.7374 | 31.2604 | 31.2604 | 31.2604 |

| Food/Beverage/Tobacco | 17.4989 | 18.602 | 17.4989 | 17.4989 | 17.4989 |

| Chemicals | 31.0055 | 34.924 | 31.0055 | 31.0055 | 31.0055 |

| Machineries | 30.4641 | 27.979 | 30.4641 | 30.4641 | 30.4641 |

| Stone-Soil based Manufacturing | 26.2005 | 21.6834 | 26.2005 | 26.2005 | 26.2005 |

| Mining | 30.567 | 33.2015 | 30.567 | 30.567 | 30.567 |

| Financials | 26.6369 | 25.2572 | 26.6369 | 26.6369 | 26.6369 |

| Holdings Investment Companies | 28.7737 | 34.2268 | 28.7737 | 28.7737 | 28.7737 |

| Technology | 24.9548 | 24.934 | 24.9548 | 24.9548 | 24.9548 |

| Wholesale Retail | 25.4617 | 27.2803 | 25.4617 | 25.4617 | 25.4617 |

| Transportation | 38.9401 | 11.5473 | 38.9401 | 38.9401 | 38.9401 |

References

- Mantegna, R.N.; Stanley, H.E. Scaling behaviour in the dynamics of an economic index. Nature 1995, 376, 46–49. [Google Scholar] [CrossRef]

- Mantegna, R.N.; Stanley, H.E. Turbulence and financial markets. Nature 1996, 383, 587–588. [Google Scholar] [CrossRef]

- Mantegna, R.N.; Stanley, H.E. Stock market dynamics and turbulence: Parallel analysis of fluctuation phenomena. Phys. A Stat. Mech. Appl. 1997, 239, 255–266. [Google Scholar] [CrossRef]

- Mantegna, R.N.; Stanley, H.E. Physics investigation of financial markets. In Proceedings of the International School of Physics “Enrico Fermi”, Course CXXXIV; Mallamace, F., Stanley, H.E., Eds.; IOS Press: Amsterdam, The Netherlands, 2004; pp. 473–489. [Google Scholar]

- Mantegna, R.N.; Stanley, H.E. An Introduction to Econophysics Correlations and Complexity in Finance; Cambridge University Press: Cambridge, UK, 2000. [Google Scholar]

- Calvet, L.; Fisher, A. Multifractality in asset returns: Theory and evidence. Rev. Econ. Stat. 2002, 84, 381–406. [Google Scholar] [CrossRef]

- Bachelier, L. The theory of speculation. In Random Character of Stock Market Prices; Cootner, P.H., Ed.; Cambridge University Press: Cambridge, UK, 1964. [Google Scholar]

- Andersen, T.G. Stochastic autoregressive volatility: A framework for volatility modeling. Math. Financ. 1994, 4, 75–102. [Google Scholar]

- Andersen, T.G.; Bollerslev, T. Heterogeneous information arrivals and return volatility dynamics: Uncovering the long-run in high frequency returns. J. Financ. 1997, 52, 975–1005. [Google Scholar] [CrossRef]

- Andersen, T.G.; Lund, J. Estimating continuous-time stochastic volatility models of the short-term interest rate. J. Econ. 1997, 77, 343–377. [Google Scholar] [CrossRef]

- Andersen, T.G.; Chung, H.J.; Sørensen, B.E. Efficient method of moments estimation of a stochastic volatility model: A Monte Carlo study. J. Econ. 1999, 91, 61–87. [Google Scholar] [CrossRef]

- Bollerslev, T.; Mikkelsen, H.O. Modeling and pricing long memory in stock market volatility. J. Econ. 1996, 73, 151–184. [Google Scholar] [CrossRef]

- Bates, D.S. Jumps and stochastic volatility: Exchange rate processes implicit in Deutsche mark options. Rev. Financ. Stud. 1996, 9, 69–107. [Google Scholar] [CrossRef]

- Fouque, J.P.; Papanicolaou, G.; Sircar, K.R. Mean-reverting stochastic volatility. Int. J. Theor. Appl. Financ. 2000, 3, 101–142. [Google Scholar] [CrossRef]

- Gallant, A.R.; Hsu, C.T.; Tauchen, G. Using daily range data to calibrate volatility diffusions and extract the forward integrated variance. Rev. Econ. Stat. 1999, 81, 617–631. [Google Scholar] [CrossRef]

- Fama, E.F. Efficient capital markets: A review of theory and empirical work. J. Financ. 1970, 25, 383–417. [Google Scholar] [CrossRef]

- Mandelbrot, B.B. Fractals and Scaling in Finance; Springer: New York, NY, USA, 1997. [Google Scholar]

- Mandelbrot, B.B. Scaling in financial prices: IV. Multifractal concentration. Quant. Financ. 2001, 1, 641. [Google Scholar] [CrossRef]

- Mandelbrot, B.B.; Van Ness, J.W. Fractional Brownian motions, fractional noises and applications. SIAM Rev. 1968, 10, 422–437. [Google Scholar] [CrossRef]

- Mandelbrot, B.B.; Wallis, J.R. Noah, Joseph, and operational hydrology. Water Resour. Res. 1968, 4, 909–918. [Google Scholar] [CrossRef]

- Mandelbrot, B.B.; Evertsz, C.J.; Gutzwiller, M.C. Fractals and Chaos: The Mandelbrot Set and Beyond; Springer: New York, NY, USA, 2004; Volume 3. [Google Scholar]

- Lo, A.W. Long-term memory in stock market prices. Econometrica 1991, 59, 1279–1313. [Google Scholar] [CrossRef]

- Evertsz, C.J. Fractal geometry of financial time series. Fractals 1995, 3, 609–616. [Google Scholar] [CrossRef]

- Peters, E.E. Chaos and Order in the Capital Markets: A New View of Cycles, Prices, and Market Volatility; John Wiley & Sons: New York, NY, USA, 1996. [Google Scholar]

- Gayathri, M.; Murugesan, S.; Gayathri, J. Persistence and long range dependence in Indian stock market returns. Int. J. Manag. Bus. Stud. 2012, 2, 72–77. [Google Scholar]

- Mahalingam, G.; Selvam, M. Fractal Analysis in the Indian Stock Market with Special Reference to CNX 500 Index Returns. 2013. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2325334 (accessed on 1 June 2022).

- Kapecka, A. Fractal analysis of financial time series using fractal dimension and pointwise Hölder exponents. Dyn. Econ. Mod. 2013, 13, 107–126. [Google Scholar]

- Agarwal, S.; Vats, A. A comparative study of financial crises: Fractal dissection of investor rationality. Vis. J. Bus. Perspect. 2021. [Google Scholar] [CrossRef]

- Sensoy, A. Generalized Hurst exponent approach to efficiency in MENA markets. Phys. A Stat. Mech. Appl. 2013, 392, 5019–5026. [Google Scholar] [CrossRef]

- Ciaian, P.; Rajcaniova, M.; Kancs, D.A. The economics of Bitcoin price formation. Appl. Econ. 2016, 48, 1799–1815. [Google Scholar] [CrossRef]

- Kim, T.Y.; Oh, K.J.; Kim, C.; Do, J.D. Artificial neural networks for non-stationary time series. Neurocomputing 2004, 61, 439–447. [Google Scholar] [CrossRef]

- Bhatt, B.J.; Dedania, H.V.; Shah, V.R. Fractional Brownian motion and predictability index in financial market. Glob. J. Math. Sci. Theory Pract. 2013, 5, 197–203. [Google Scholar]

- Yu, L.; Zhang, D.; Wang, K.; Yang, W. Coarse iris classification using box-counting to estimate fractal dimensions. Pattern Recognit. 2005, 38, 1791–1798. [Google Scholar] [CrossRef]

- Peitgen, H.O.; Jürgens, H.; Saupe, D.; Feigenbaum, M.J. Chaos and Fractals: New Frontiers of Science; Springer: New York, NY, USA, 1992; Volume 7. [Google Scholar]

- Gagnepain, J.J.; Roques-Carmes, C. Fractal approach to two-dimensional and three-dimensional surface roughness. Wear 1986, 109, 119–126. [Google Scholar] [CrossRef]

- Xu, S.; Weng, Y. A new approach to estimate fractal dimensions of corrosion images. Pattern Recognit. Lett. 2006, 27, 1942–1947. [Google Scholar] [CrossRef]

- Sarkar, N.; Chaudhuri, B.B. An efficient differential box-counting approach to compute fractal dimension of image. IEEE Trans. Syst. Man Cybern. 1994, 24, 115–120. [Google Scholar] [CrossRef]

- Peleg, S.; Naor, J.; Hartley, R.; Avnir, D. Multiple resolution texture analysis and classification. IEEE Trans. Pattern Analys. Mach. Intell. 1984, 6, 518–523. [Google Scholar] [CrossRef]

- Pentland, A.P. Fractal-based description of natural scenes. IEEE Trans. Pattern Analys. Mach. Intell. 1984, 6, 661–674. [Google Scholar] [CrossRef]

- Keller, J.M.; Chen, S.; Crownover, R.M. Texture description and segmentation through fractal geometry. Comput. Vis. Graph. Image Process. 1989, 45, 150–166. [Google Scholar] [CrossRef]

- Chen, W.S.; Yuan, S.Y.; Hsieh, C.M. Two algorithms to estimate fractal dimension of gray-level images. Opt. Eng. 2003, 42, 2452–2464. [Google Scholar] [CrossRef]

- Arneodo, A.; Audit, B.; Bacry, E.; Manneville, S.; Muzy, J.F.; Roux, S.G. Thermodynamics of fractal signals based on wavelet analysis: Application to fully developed turbulence data and DNA sequences. Phys. A Stat. Mech. Appl. 1998, 254, 24–45. [Google Scholar] [CrossRef][Green Version]

- Bekiros, S.D. Timescale analysis with an entropy-based shift-invariant discrete wavelet transform. Comput. Econ. 2014, 44, 231–251. [Google Scholar] [CrossRef]

- Parisi, F.; Caldarelli, G.; Squartini, T. Entropy-based approach to missing-links prediction. Appl. Netw. Sci. 2018, 3, 17. [Google Scholar] [CrossRef]

- Pele, D.T.; Lazar, E.; Dufour, A. Information entropy and measures of market risk. Entropy 2017, 19, 226. [Google Scholar] [CrossRef]

- Wang, J.Z.; Wang, J.J.; Zhang, Z.G.; Guo, S.P. Forecasting stock indices with back propagation neural network. Expert Syst. Appl. 2011, 38, 14346–14355. [Google Scholar] [CrossRef]

- Zhang, Y.; Wang, S.; Sun, P.; Phillips, P. Pathological brain detection based on wavelet entropy and Hu moment invariants. Bio-Med. Mater. Eng. 2015, 26, S1283–S1290. [Google Scholar] [CrossRef]

- Cajueiro, D.O.; Gogas, P.; Tabak, B.M. Does financial market liberalization increase the degree of market efficiency? The case of the Athens Stock Exchange. Int. Rev. Financ. Analys. 2009, 18, 50–57. [Google Scholar] [CrossRef]

- Wang, Y.; Liu, L.; Gu, R. Analysis of efficiency for Shenzhen stock market based on multifractal detrended fluctuation analysis. Int. Rev. Financ. Analys. 2009, 18, 271–276. [Google Scholar] [CrossRef]

- Neto, J.N.D.M.; Fávero, L.P.L.; Takamatsu, R.T. Hurst exponent, fractals and neural networks for forecasting financial asset returns in Brazil. Int. J. Data Sci. 2018, 3, 29–49. [Google Scholar]

- Gayathri, M.; Selvam, M. Efficiency of fractal market hypothesis in the Indian stock market. In Proceedings of the HIS Publications: International Conference on Changing Perspectives of Management, Kathmandu, Nepal, 10–12 March 2011; pp. 186–192. [Google Scholar]

- Krištoufek, L. Rescaled range analysis and detrended fluctuation analysis: Finite sample properties and confidence intervals. Czech Econ. Rev. 2010, 4, 315–329. [Google Scholar]

- Sensoy, A. The inefficiency of Bitcoin revisited: A high-frequency analysis with alternative currencies. Financ. Res. Lett. 2019, 28, 68–73. [Google Scholar] [CrossRef]

- Sakalauskas, V.; Kriksciuniene, D. Tracing of stock market long term trend by information efficiency measures. Neurocomputing 2013, 109, 105–113. [Google Scholar] [CrossRef]

- Lepot, M.; Aubin, J.B.; Clemens, F.H. Interpolation in time series: An introductive overview of existing methods, their performance criteria and uncertainty assessment. Water 2017, 9, 796. [Google Scholar] [CrossRef]

- Sirlantzis, K.; Siriopoulos, C. Deterministic chaos in stock markets: Empirical results from monthly returns. Neural Netw. World 1993, 3, 855–864. [Google Scholar]

- Siriopoulos, C. Investigating the behaviour of mature and emerging capital markets. Indian J. Quant. Econ. 1996, 11, 76–98. [Google Scholar]

- Mills, T. Is there long-memory in UK stock returns? Appl. Financ. Econ. 1993, 3, 303–306. [Google Scholar] [CrossRef]

- Panagiotidis, T. Market capitalization and efficiency. Does it matter? Evidence from the Athens Stock Exchange. Appl. Financ. Econ. 2005, 15, 707–713. [Google Scholar] [CrossRef]

- Panagiotidis, T. Market efficiency and the Euro: The case of the Athens Stock Exchange. Empirica 2010, 37, 237–251. [Google Scholar] [CrossRef]

- Inglada-Perez, L. A comprehensive framework for uncovering non-linearity and Chaos in financial markets: Empirical evidence for four major stock market indices. Entropy 2020, 22, 1435. [Google Scholar] [CrossRef] [PubMed]

- Siriopoulos, C.; Skaperda, M. Investing in mutual funds: Are you paying for performance or for the ties of the manager? Bull. Appl. Econ. 2020, 7, 153. [Google Scholar] [CrossRef]

- IMF. World Economic Outlook; IMF: Washington, WA, USA, 2020; Available online: https://www.imf.org/en/Publications/WEO (accessed on 1 June 2022).

- Batrancea, I.; Moscviciov, A.; Sabau, C.; Batrancea, L.M. Banking crisis: Causes, Characteristic and solution. Economics 2013, 1, 16–29. [Google Scholar]

- Ramelli, S.; Wagner, A.F. Feverish stock price reactions to COVID-19. Rev. Corp. Financ. Stud. 2020, 9, 622–655. [Google Scholar] [CrossRef]

- David, S.A.; Inácio, C.M., Jr.; Machado, J.A.T. The recovery of global stock markets indices after impacts due to pandemics. Res. Int. Bus. Financ. 2021, 55, 101335. [Google Scholar] [CrossRef]

- Khan, K.; Zhao, H.; Zhang, H.; Yang, H.; Shah, M.H.; Jahanger, A. The impact of COVID-19 pandemic on stock markets: An empirical analysis of world major stock indices. J. Asian Financ. Econ. Bus. 2020, 7, 463–474. [Google Scholar] [CrossRef]

- Topcu, M.; Gulal, O.S. The impact of COVID-19 on emerging stock markets. Fin. Res. Lett. 2020, 36, 101691. [Google Scholar] [CrossRef]

- Yilmazkuday, H. COVID-19 effects on the S&P 500 index. Appl. Econ. Lett. 2021, 1–7. [Google Scholar] [CrossRef]

- Zhang, D.; Hu, M.; Ji, Q. Financial markets under the global pandemic of COVID-19. Financ. Res. Lett. 2020, 36, 101528. [Google Scholar] [CrossRef]

- Sansa, N.A. The impact of the COVID-19 on the financial markets: Evidence from China and USA. Electron. Res. J. Soc. Sci. Humanit. 2020, 2, 1–26. [Google Scholar]

- Toda, A.A. Susceptible-Infected-Recovered (SIR) Dynamics of COVID-19 and Economic Impact. 2020. Available online: https://econpapers.repec.org/paper/arxpapers/2003.11221.htm (accessed on 1 June 2022).

- Alfaro, L.; Chari, A.; Greenland, A.N.; Schott, P.K. Aggregate and Firm-Level Stock Returns during Pandemics, in Real Time; National Bureau of Economic Research: Cambridge, MA, USA, 2020. [Google Scholar]

- Ru, H.; Yang, E.; Zou, K. What Do We Learn from SARS-CoV-1 to SARS-CoV-2: Evidence from Global Stock Markets. 2020. Available online: https://www.economicsobservatory.com/ongoing-research/what-do-we-learn-from-sars-cov-1-to-sars-cov-2-evidence-from-global-stock-markets (accessed on 1 June 2022).

- Gerding, F.; Martin, T.; Nagler, F. The Value of Fiscal Capacity in the Face of a Rare Disaster. 2020. Available online: https://www.semanticscholar.org/paper/The-Value-of-Fiscal-Capacity-in-the-Face-of-a-Rare-Gerding-Martin/4de59adeae67c820ed08ed25a74761ec37bee4ae (accessed on 1 June 2022).

- Ozili, P.K.; Arun, T. Spillover of COVID-19: Impact on the Global Economy. 2020. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3562570 (accessed on 1 June 2022).

- Cookson, J.A.; Engelberg, J.E.; Mullins, W. Does partisanship shape investor beliefs? Evidence from the COVID-19 pandemic. Rev. Asset Pricing Stud. 2020, 10, 863–893. [Google Scholar] [CrossRef]

- McKibbin, W.; Fernando, R. The global macroeconomic impacts of COVID-19: Seven scenarios. Asian Econ. Pap. 2021, 20, 1–30. [Google Scholar] [CrossRef]

- Xinhua, H. China Financial Markets Remains Stable Amid COVID-19 Impact. China Daily-Hong Kong, 22 March 2020. [Google Scholar]

- Hall, P.; Wood, A. On the performance of box-counting estimators of fractal dimension. Biometrika 1993, 80, 246–251. [Google Scholar] [CrossRef]

- Genton, M.G. Highly robust variogram estimation. Math. Geol. 1998, 30, 213–221. [Google Scholar] [CrossRef]

- Gneiting, T.; Schlather, M. Stochastic models that separate fractal dimension and the Hurst effect. SIAM Rev. 2004, 46, 269–282. [Google Scholar] [CrossRef]

- Gneiting, T.; Ševčíková, H.; Percival, D.B. Estimators of fractal dimension: Assessing the roughness of time series and spatial data. Stat. Sci. 2012, 27, 247–277. [Google Scholar] [CrossRef]

- Müller, M. Dynamic time warping. In Information Retrieval for Music and Motion; Springer: Berlin/Heidelberg, Germany, 2007; pp. 69–84. [Google Scholar]

- Blackledge, J.; Lamphiere, M. A review of the fractal market hypothesis for trading and market price prediction. Mathematics 2021, 10, 117. [Google Scholar] [CrossRef]

- Batrancea, L. The influence of liquidity and solvency on performance within the healthcare industry: Evidence from publicly listed companies. Mathematics 2021, 9, 2231. [Google Scholar] [CrossRef]

- Batrancea, L.M. An econometric approach on performance, assets, and liabilities in a sample of banks from Europe, Israel, United States of America, and Canada. Mathematics 2021, 9, 3178. [Google Scholar] [CrossRef]

- Batrancea, L.; Batrancea, I.; Moscviciov, A. The analysis of the entity’s liquidity—A means of evaluating cash flow. J. Int. Financ. Econ. 2009, 9, 92–98. [Google Scholar]

| Sector | Box Counting | DCT | Genton | Hall-Wood | Wavelet |

|---|---|---|---|---|---|

| Social | −0.0384787 | −0.005845 | −0.016962 | 0.00979677 | −0.023266 |

| Energy | −0.0448036 | 0.0358862 | 0.126412 | 0.0460285 | 0.0084825 |

| Real Estate | 0.0168396 | 0.0839297 | 0.0793312 | 0.10149 | 0.0115641 |

| Metal Industry | −0.141769 | 0.076255 | 0.0448354 | 0.0907244 | −0.015062 |

| Food/Beverage/Tobacco | 0.0396851 | −0.006135 | 0.157217 | 0.00759142 | −0.008396 |

| Chemicals | −0.0786395 | 0.0706746 | 0.0776561 | 0.104998 | 0.0213005 |

| Machineries | −0.0335492 | 0.0538419 | 0.0476538 | 0.0943814 | 0.0053354 |

| Stone-Soil based Manufacturing | −0.0369419 | −0.005562 | 0.0605334 | 0.125544 | −0.007214 |

| Mining | 0.0188247 | 0.0311941 | −0.014740 | −0.0703955 | −0.022804 |

| Financials | 0.0121408 | 0.0247008 | 0.0573303 | 0.113841 | 0.0208023 |

| Holdings Investment Companies | −0.0275258 | 0.0295971 | 0.0812037 | 0.0687147 | 0.0079427 |

| Technology | 0.0241203 | 0.0347521 | 0.0577145 | 0.09597 | 0.0323409 |

| Wholesale Retail | 0.0113931 | 0.001284 | 0.110093 | 0.0471959 | 0.0084337 |

| Transportation | −0.129512 | −0.004891 | 0.0832621 | 0.174997 | 0.0173918 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Balcı, M.A.; Batrancea, L.M.; Akgüller, Ö.; Gaban, L.; Rus, M.-I.; Tulai, H. Fractality of Borsa Istanbul during the COVID-19 Pandemic. Mathematics 2022, 10, 2503. https://doi.org/10.3390/math10142503

Balcı MA, Batrancea LM, Akgüller Ö, Gaban L, Rus M-I, Tulai H. Fractality of Borsa Istanbul during the COVID-19 Pandemic. Mathematics. 2022; 10(14):2503. https://doi.org/10.3390/math10142503

Chicago/Turabian StyleBalcı, Mehmet Ali, Larissa M. Batrancea, Ömer Akgüller, Lucian Gaban, Mircea-Iosif Rus, and Horia Tulai. 2022. "Fractality of Borsa Istanbul during the COVID-19 Pandemic" Mathematics 10, no. 14: 2503. https://doi.org/10.3390/math10142503

APA StyleBalcı, M. A., Batrancea, L. M., Akgüller, Ö., Gaban, L., Rus, M.-I., & Tulai, H. (2022). Fractality of Borsa Istanbul during the COVID-19 Pandemic. Mathematics, 10(14), 2503. https://doi.org/10.3390/math10142503