1. Introduction

The impacts of international trade on economic growth remain the prominent issues in both theoretical and policy context. The nexus of trade and economic growth has gained even more attention in recent years, considering the persistent and widespread differences in economic performance among countries, especially among developing countries in the wake of growing international trade integration (

Silajdzic and Mehic 2018). However, the empirical analyses are as inconclusive as the theoretical perspectives. For example, the study by

Chang et al. (

2009) and

Zahonogo (

2016) indicate that the effects of foreign trade on economic growth are conditional to the different structural characteristics of the economy.

However, according to a study by

Kim (

2011), foreign trade has significant adverse effects on developing countries. Furthermore,

Baliamoune-Lutz (

2011) and

Matthew and Folasade (

2014) found that international trade only had little significance on economic growth and implied that the domestic institutions’ weakness is responsible for enhancing the growth effect of international trade.

Likewise, the impact of foreign direct investment (FDI) on economic growth is inconclusive. The FDI spillover to the host economy is significantly determined by the economy’s ability to benefit from FDI. Absorptive capacity indicates an economy’s capacity to absorb the opportunities spilled over by the FDI inflow (

Khordagui and Saleh 2013). Hence, the role of FDI to enhance economic growth will depend on the domestic absorptive capacity of FDI-receiving countries (

Khordagui and Saleh 2013;

Jyun-Yi and Chih-Chiang 2008;

Jude and Levieuge 2016;

Ali et al. 2010).

The increasing China–Africa economic relations received much attention and debate among scholars. It is revealed by the China–Africa trade, and the FDI flow from China to African countries. The literature on the China–Africa relationship often falls under two broad categories. Some argue that the relationship is a win–win for African countries and China. However, some others view the relationship as a new form of imperialism, especially concerning the issue of African countries’ resource exploitation (

Adisu et al. 2010;

Foster et al. 2008;

Kolstad and Wiig 2011).

More particularly, a study by

He (

2013), using manufactured goods exports of sub-Saharan Africa to represent the production of countries, reveals that Africa’s trade relation with China has a positive and significant effect on the economic development of African countries. However, the benefit in terms of trade effect is limited to those African economies that export natural resources (

Busse et al. 2016). On the other hand, for other scholars, the trade between Africa and China has an insignificant or a negative effect on the economic growth of African countries and is more dominated by China’s economic interests, namely the access to critical resources (

Foster et al. 2008;

Adisu et al. 2010;

Busse et al. 2016). Moreover, as it is clearly maintained, some researchers argue that Africa’s trade with China is centered on China’s interest in Africa and deteriorating effect on the African economy.

Similarly, the impact of Chinese FDI on the economic growth of African countries is controversial. According to

Foster et al. (

2008),

Adisu et al. (

2010) and

Busse et al. (

2016), FDI flows from China to African countries seem to play no major role in African countries’ economic growth and are perceived to follow the state-driven strategy of giving infrastructure and taking natural resources. On the other hand, the Chinese foreign direct investment flow indicates China’s significant role in African countries’ economic performance. For example, the study by

Pigato and Tang (

2015) shows those African countries which have benefited from the China–Africa economic relationship, though the bulk of Chinese investment is focused on a few resource-rich countries. Furthermore,

Whalley and Weisbrod (

2012) and

Doku et al. (

2017) indicated that an increase in China’s FDI stock and flow into African countries has a positive effect on African countries’ economic growth.

These studies, however, are not sufficient, not without limitations, and no study was conducted using appropriate econometric specifications and considering the domestic capabilities of African countries to reap growth effect of the China–Africa economic relations. As a result, we can find different empirical literature that reveals that the effects of the China–Africa trade and Chinese FDI on the economic growth of African countries are mixed at best. Furthermore, it is interesting to note that no attempts have been made to investigate the impact of Chinese FDI and China–Africa trade on African countries’ economic growth from the perspective of institutional quality and their role in mediating the relationship. Thus, this study’s unique contribution towards the body of knowledge is that it has extended the classical economic model to capture the moderating role of institutional quality in the nexus of the China–Africa economic relationship (China–Africa trade and Chinese FDI) and economic growth of African countries.

Therefore, the major aim of this study is to analyze the impacts of the China–Africa trade and Chinese FDI on the economic growth of the African countries, controlling the mediating role of the institutional quality of African countries.

The rest part of this paper is organized as follows. Part two discusses the stylized facts of Chinese FDI and the China–Africa trade, the institutional environment and economic performance of African countries. Part three presents the literature review and hypothesis. Part four explains the data and methodology of the study. Part five presents the results and findings of the study. Part six presents a detailed discussion of the study, and part seven gives conclusions based on the findings.

2. Chinese FDI and China–Africa Trade, Institutional Quality and Economic Growth of African Countries

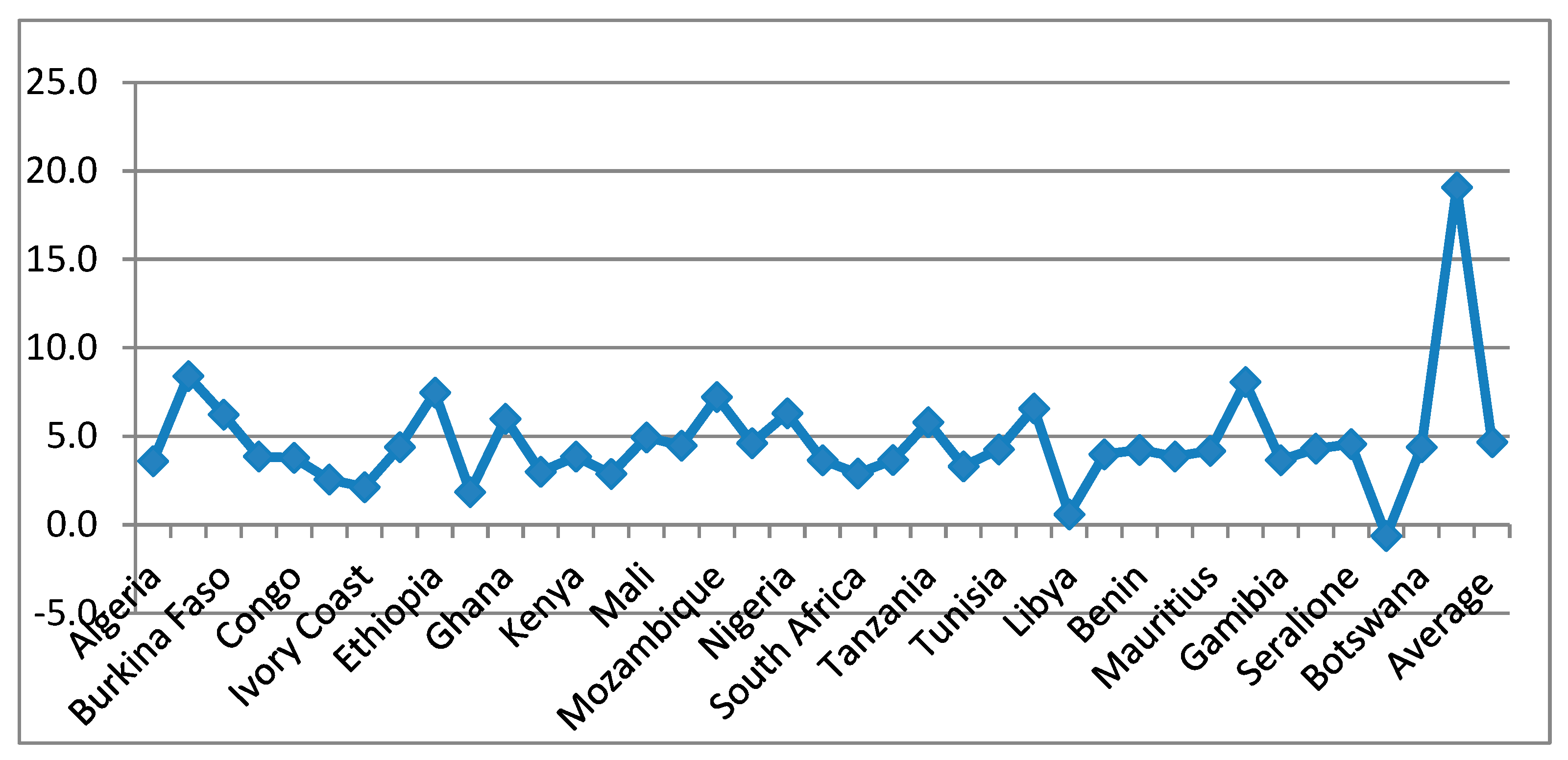

In the last two decades, Africa registered a period of sustainable and impressive economic growth. Some of the countries can be included among the fastest-growing economies in the world. Most African countries have registered a sustainable economic growth with an economic growth rate exceeding 5% per year over the past 15 years. The average growth rate of the sample African countries is presented in

Appendix F. The growth registered in this period was supported by favorable external conditions, especially high commodity prices boom as a result of high international demand for commodities, and the increase in investment money and FDI flow in search of new economic opportunities at the global level have played a significant role (

Zamfir 2016). Among external factors, a vital change that took place in Africa was the rise of Brazil, Russia, India, China and South Africa (BRICS countries) and their strengthening economic and trade relationships with African countries. While one should be careful in establishing a relationship between the emergence of the BRICS economies in Africa and Africa’s recent impressive economic growth record, the BRICS have certainly contributed to changing perceptions of Africa’s economic fortunes among the international donor community. The most important emerging player from the BRICS group on African soil is China because China provides the largest share of foreign finance for Africa from the South–South cooperation (

Woods 2008).

China has a long trade relationship with African countries. However, the fastest growth of the trade between African countries and China was registered in the last two decades. According to trade data from the Global Trade Atlas, trade between China and Africa has increased at the fastest rate since 2000. The total trade between Africa and China has registered a compound growth rate of 24.7% in the last two decades. It also implies that the trade in goods and services has grown at 26.7% annually on average for the past two decades (

Borojo and Yushi 2016).

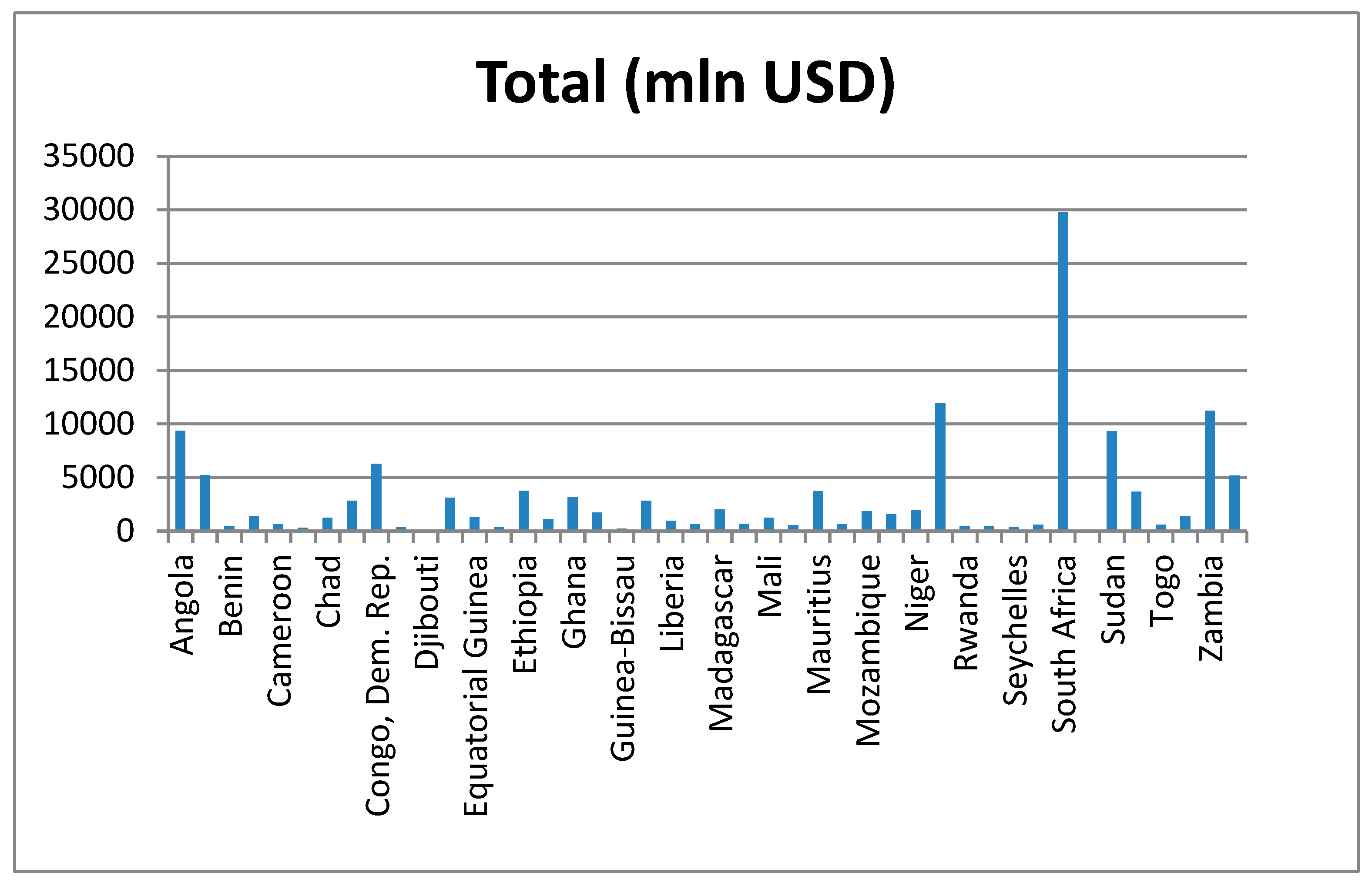

Furthermore, Chinese FDI is distributed in almost all African countries. This reveals that Chinese outward FDI to African countries plays a prominent role in China’s economic interaction with many African countries (

Miao et al. 2020). The distribution of Chinese FDI in sample African countries is reported in the

Appendix D.

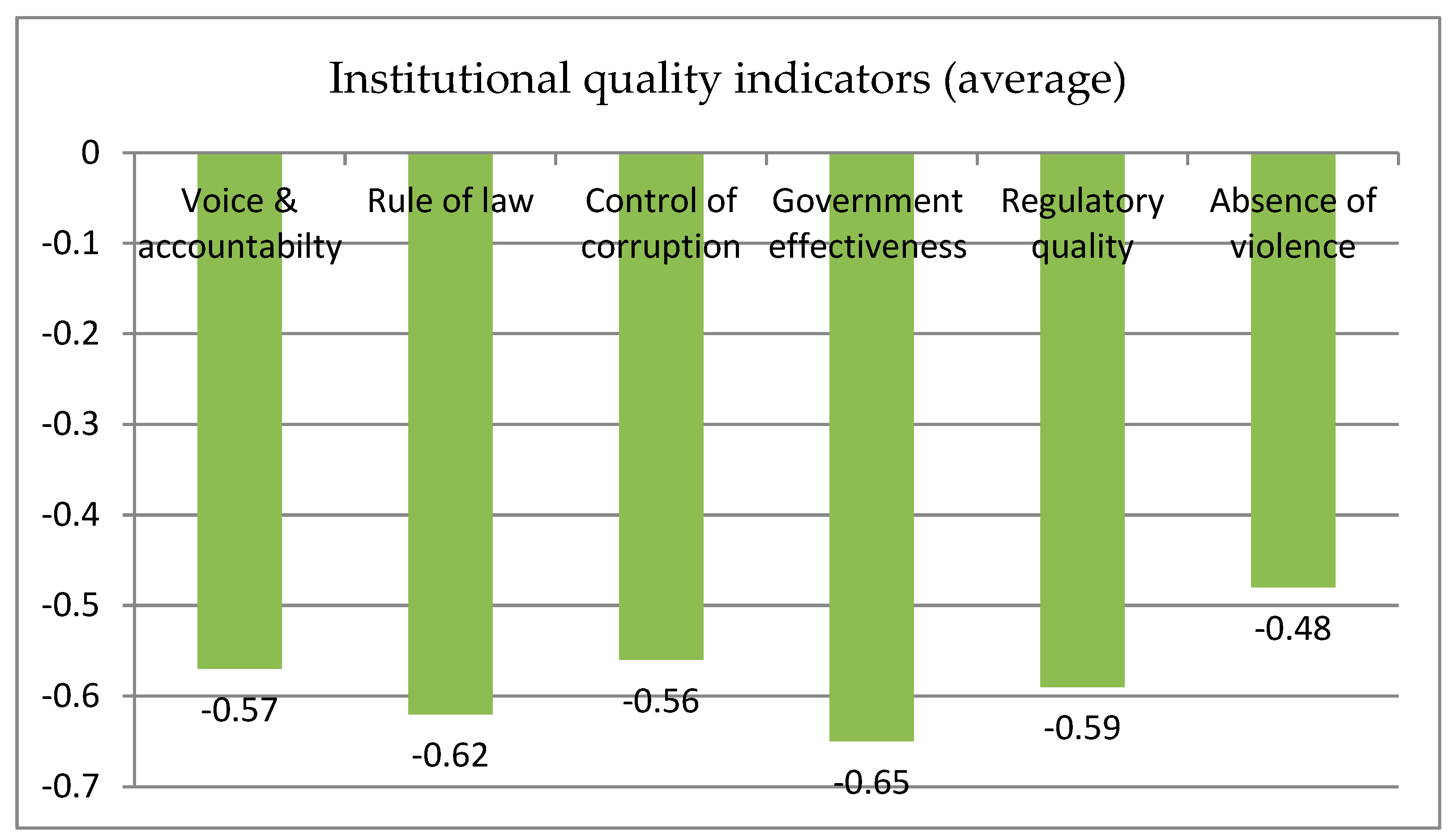

Additionally, the institutional environment of African countries is weaker and needs improvement. The mean score of the sample African countries’ institutional quality indicators indicates that the African countries continue to score below expectations with the negative scores outweighing the positive ones. For instance, the reports in

Appendix E suggest that, on average, the political environment (−0.478) across the sample is quite unstable. This indicates that there is still political instability and violence, which taints the democratic atmosphere of the countries. The worst performer on the scale, which has proven resistant to change, is government effectiveness, which is still lagging behind with an average score of negative 0.651. Thus, the governments’ ability to offer quality public services and to formulate and implement policies that are indicative of government effectiveness is low. This is closely followed by a rule of law with the average score of negative 0.621. Furthermore, the regulatory quality and control of corruption, which are under the due attention of international organizations, has recorded the average negative score of 0.565 and 0.562, respectively (see

Appendix E). Therefore, the scores of the institutional quality of African countries indicate that the countries’ performance in the institutional environment is weak and needs policy attention.

4. Methodology and Data

This section discusses the strategy used to examine the impacts of the China–Africa trade and Chinese FDI on the economic growth of African countries and the data used for the exercise.

4.1. Method of Analysis

This part mainly focuses on the discussion of the strategy to analyze the effects of the China–Africa trade and Chinese FDI on African countries’ economic growth. To this end, a dynamic panel data model was employed to analyze the impacts of the China–Africa trade, Chinese FDI flow on the African economy, extending the neoclassical augmented growth model developed by

Mankiw et al. (

1992) that relates growth with different explanatory variables. The following part briefly describes the functional specification of the empirical models that are used to analyze the impact of trade between Africa and China and Chinese FDI flow from China to Africa on the economic growth of African countries.

The analysis of the effect of the China–Africa trade and Chinese FDI flow on African countries’ economic growth was based on a pooled data set of cross-country and time-series observations, using a sample of 44 African countries for the period of 2003–2017. Hence, this is one of the reasons to use the two-step system GMM estimator of

Arellano and Bover (

1995), employed to examine the impacts of the China–Africa trade and FDI flow on the economic growth of African countries.

There are several reasons to use a dynamic panel data model (the two-step system GMM model) to exercise the growth equation. First, the two-step system GMM system estimator is employed for the estimation of the effect of the trade openness of China–Africa and the inflow of Chinese FDI and aid to Africa on the economic growth of African countries because our analysis is based on a pooled data set of cross-country and time-series observations.

Second, the economic growth by itself is a dynamic phenomenon that can be captured by dynamic panel models. Hence, to determine this dynamic phenomenon, the system GMM model is suitable. Third, the two-step system GMM model can address the endogeneity problem and gives consistent estimates, even in the presence of measurement error. Fourth, this model provides asymptotically efficient inference, assuming a minimal set of statistical assumptions (

Arellano and Bover 1995;

Blundell and Bond 1998).

In general, the system GMM is an estimator designed for conditions with small time (T) and large panels (N). It is a systematic method with a few periods and many individual units with a linear functional relationship, one left-hand variable that is dynamic, depending on its past realizations, and right-hand side variables that are not strictly exogenous; associated with past and possibly current realizations of the error fixed individual effects, implying unobserved heterogeneity (heteroskedasticity) and autocorrelation within individual units’ errors, but not across them.

In the two-step system GMM model, the China–Africa trade, Chinese FDI and financial aid variables are considered as endogenous because there will be a reverse causality problem between economic growth and China–Africa trade, and economic growth and financial aid and economic growth and FDI inflow from China to African countries.

Therefore, using this dynamic model helps us by providing an important robustness check on the statistical inferences and yield accurate estimates. It is sufficient to exploit the full use of the information contained within the data set. Based on the above information, the econometric equation that relates the dependent variable (real gross domestic product (real GDP) per capita growth for African countries) to China–Africa trade, Chinese FDI inflow to Africa and control variables is specified in the following equation:

where

g-denotes the per capita real GDP growth of African countries,

Xit represents the control variables such as the lag of per capita GDP growth of the countries, physical capital, the inflation rate of African countries, health expenditure of African countries and the institutional quality of African countries.

Iit is a Chinese FDI in African countries.

Tit is trade between China and African countries.

INit represents the interaction terms among institutional quality and the China–Africa trade, institutional quality and Chinese FDI, and China–Africa trade and Chinese FDI.

εit indicates the stochastic term.

The logarithm-linear transformation of Equation (1) is:

In this model, one of the innovations of this study is the inclusion of the conditional effect of the China–Africa economic relationship on the economic growth of African countries in which the previous empirical studies lack. The conditional effect of the China–Africa trade and Chinese FDI to the domestic absorptive capacity of African countries on economic growth was incorporated in the model. Hence, the interaction terms of the China–Africa trade, Chinese FDI as the Chinese foreign trade, Chinese FDI, foreign aid, service contracts and labor cooperation were closely mixed and combined. Hence, the impact channels of Chinese trade, FDI and aid overlap (

McCormick 2008).

To see the interaction, for example, consider the Chinese FDI in the mining and construction sectors. These types of FDI were often accompanied by loans from the Chinese government to African governments, which in turn contract Chinese firms to extract resources or build infrastructure. In turn, the repayment of these loans is often tied to commodity exports from African borrowers to China. As a result, the interaction term is included in the model specification.

4.2. The Data

This study used data for the period 2003–2017 based on the data availability for 44 African countries. The sample countries included in this study are reported in

Appendix C. Trade data between African countries and China were taken from the tralac database. The GDP of African countries, gross fixed capital formation, inflation, the domestic credit to private sector per GDP, mobile subscription rate and health expenditure were compiled from World Development Indicators (WDI). Chinese FDI to Africa data were compiled from United Nations Com Trade (UNCTAD) bilateral FDI Statistics and the China Statistical Yearbook by the Johns Hopkins China–Africa Research Institute. Financial aid data from China to African countries were obtained from the AidData website.

Institutional quality indicators such as the control of corruption, absence of violence and security, rule of law, government effectiveness, voice and accountability and regulatory quality of African countries were collected from Worldwide Governance Indicators (WGI) World Bank Group website. They feature the scores for various dimensions of institutional quality by combining information from several independent sources. They extract information from all these sources, transform their scales so that every indicator is constructed as a normally distributed random variable with a zero mean, unit standard deviation, and ranging approximately from −2.5 to 2.5 with higher values showing better institutions. Using these six indicators of the institutional quality of African countries, we derived a single composite indicator using principal component analysis. From

Table A2, the eigenvalues of the first principal component of governance and institutional quality is greater than 1 (4.725 > 1). However, none of the other components have eigenvalues more than 1. Since the first component explains 78.8% of the original variables’ variation, the study uses the eigenvectors of the first principal component as weights in constructing an institutional and governance index (see

Appendix B).

5. Results and Findings

This section mainly focuses on the impacts of the China–Africa trade and Chinese FDI to African countries on the economic growth of African countries. It provides the results and findings of the study. The summary statistics of the major variables are reported in

Appendix A.

Table 1 presents the two-step system GMM estimates of the effects of the China–Africa trade and Chinese FDI on the growth of African countries.

The regression command (xtabond2) of a

Roodman (

2009) dynamic panel data model is applied because it can do everything xtabond does and has many extra characteristics. The second lag is used in the specification because the second lag is not correlated with the current error term, but the first lag is correlated with the current error term. In addition, it is suggested to use second or deeper lags to get a good instrument, but using deeper lags can decrease the sample size. The conventional covariance matrix is robust in a two-step system GMM estimation of panel-specific auto-correlation and heteroskedasticity, but the standard errors are biased downwards (

Roodman 2009). STATA 13 is used to exercise the regression.

The institutional quality index is derived using the governance quality index derived from six governance indicators (control of corruption, absence of violence and instability, government effectiveness, regulatory quality, rule of law, voice and accountability) using principal component analysis. Additionally, the diagnostic test of the model was conducted to evaluate the robustness of the model. Thus, the Hansen test is conducted for the over-identification issue. We fail to reject insignificant statistics for the Hansen test for the two-step system GMM in

Table 1. Therefore, it confirms that the instruments satisfy the orthogonality condition, or all instruments are valid in the model. Similarly, the Wald test for the joint significance of the variables is conducted and does not reject our model specification. The serial correlation test of the Arellano and Bond test is applied and does not reject the null that there is no second-order serial correlation. These diagnostic tests, therefore, validate the use of the two-step system GMM model to analyze the impacts of the China–Africa trade and Chinese FDI flow on the growth of African countries.

Among the traditional determinants of growth, physical capital and institutional quality are significant determinants of growth in African countries. Their coefficients are positive and statistically significant. The accumulation of physical capital, therefore, enables economic growth for African countries. In the development process, thus, physical capital accumulation can be a primary engine for economic growth. On the other hand, the coefficients of inflation and health expenditure are negative and statistically significant. Maintaining price stability by controlling inflation is a robust factor for economic growth. However, the coefficient of credit to the private sector has a negative and significant effect on the GDP per capita growth of African countries. Furthermore, the coefficient of the lag of per capita GDP is negative and statistically significant.

Among the variables of interest, the results in

Table 1 indicate that trade between China and African countries has an insignificant effect on the GDP per capita growth of African countries when controlled individually in Column (I) (

Table 1).

On the other hand, the coefficient of Chinese FDI is negative and statistically significant, indicating a negative association between Chinese FDI and GDP per capita growth when we consider it individually. This might be because the growth effect of FDI should be backed by the domestic adaptive capacity to use the benefit of Chinese FDI to excel in economic growth. That is, Chinese FDI flow to African countries alone is not sufficient for African countries to reap the benefits of FDI. The positive impacts of FDI on host countries’ economic growth depends on whether certain factors exist or not in those countries, such as the degree of openness of its economy, political stability, the absence of violence or domestic institutional quality (

Asheghian 2004;

Hansen and Rand 2006). Furthermore, in a recent empirical investigation,

McCloud and Kumbhakar (

2011) noted the existence of a heterogeneous relationship between FDI and economic growth across developing countries. They argued that, across countries, differences in institutional quality were correlated with heterogeneous absorptive capacities and hence, a heterogeneous FDI–growth relationship. Hence, the role of FDI to enhance economic growth will depend on the domestic absorptive capacity of FDI-receiving countries. It is based on this that we further examined the conditional effect of FDI on domestic institutional quality.

Therefore, based on the justification, we extended our analysis to the conditional effects of FDI and China–Africa trade with institutional quality because different variables can complement the growth effect of FDI flow. As a result, we used the interaction terms of FDI to the institutional quality of African countries to determine its conditional impact as the improvement in institutional quality complements FDI flow and the China–Africa trade in enhancing economic growth.

Furthermore, Chinese FDI flow can also be affected by trade between China and African countries. We include the interaction terms of China–Africa trade and FDI as the Chinese foreign trade and FDI have been closely mixed and combined. The impact channels of Chinese trade, FDI and aid overlap affect each other (

McCormick 2008). Hence, we control the interaction terms of China–Africa trade and Chinese FDI in our specification. Because of the high correlation among the interaction terms, we separately control the interaction terms from Column (II) to Column (IV).

Accordingly, the conditional effect of Chinese FDI flow to African countries and China–Africa trade to domestic institutional quality is strongly positive. Therefore, the results are in line with the hypotheses (H1 and H2A) (see

Table 2). This result implies that institutional reforms can promote the marginal effects of Chinese FDI and China–Africa trade as institutional complementarities may lead to an incremental effect on growth. To benefit from FDI-led growth and the China–Africa trade, therefore, institutional reforms should precede FDI attraction and trade policies. This result is supported by some literature such as

Khordagui and Saleh (

2013) and

Jude and Levieuge (

2016) that reveal FDI spillovers exist in different economies, yet that they are more evident when controlling for the domestic absorptive capacities of countries.

Furthermore, the China–Africa trade has a growth-enhancing effect on Chinese FDI and the growth nexus of African countries. This result indicates that trade openness can play a role in facilitating the spillover of FDI benefits to the host country. The findings are in line with the FDI literature that argues that FDI and trade openness can be complementary for economic growth and that an economy promoting more open trade policies, especially export promotion policies, are more likely to benefit from FDI spillovers (

Nobakht and Madani 2014). Therefore, the China–Africa trade openness can be a mediating factor in the impacts of Chinese FDI flow on African countries’ economic growth. Thus, the result supported the acceptance of our hypotheses (H2B).

Furthermore, we run for other African countries excluding South Africa, Nigeria, Zambia and Sudan to partly reduce reverse causality issues and to look at if the China–Africa trade and Chinese FDI have the same relationship with the whole sample. South Africa is one of the largest hubs for Chinese FDI. The volume of trade, FDI and financial aid allocation from China to these countries is larger than the rest of African countries. South Africa is the largest trading partner for China in Africa, while China has been the country’s biggest trading partner accounting for a quarter to a third of the China–Africa overall trade. It is the top country exporting to China and importing from China. According to FDI Markets, South Africa is the first destination for Chinese direct investment. Similarly, Nigeria, Sudan, Zambia and Algeria are the top destinations of Chinese FDI next to South Africa. About 60% of Chinese FDI stock in Africa was allocated to these countries (see

Appendix D). Furthermore, these countries have a big share of trade with China. Therefore, the exclusion of these countries helps analyze the sensitivity of the results. The results are reported in

Table 3 below.

We find almost the same results. The signs of coefficients and their level of significance are almost the same except minor differences in the magnitude and significance of the coefficients of some control variables. The conditional effects of Chinese FDI and the China–Africa trade on the institutional quality of African countries are positive and statistically significant. Likewise, the interaction terms of all China–Africa trade and Chinese FDI is robustly positive. That is the interaction of China–Africa trade openness and FDI to positive and statistically significant, revealing that trade openness between China and African countries fuels the growth effect of Chinese FDI to African countries.

6. Discussions

The relationship between foreign trade and economic growth has been theoretically and empirically controversial. While conventional insight predicts a growth-enhancing effect of trade, recent developments suggest that foreign trade is not always beneficial for economic growth.

The results and findings of this study indicate that the China–Africa trade relationship has a robust positive effect on the economic growth of African countries subject to institutional quality. This result on the impact of the China–Africa trade on the economic growth of African countries is inconsistent with some earlier literature, such as

Yin and Vaschetto (

2011) and

He (

2013) that have provided evidence that China’s increasing trade with Africa is helpful to African sustainable economic growth and development. However, this result is inconsistent with the findings of

Ademola et al. (

2009),

Chemingui and Bchir (

2010) and

Elu and Price (

2010) that reveal for many African countries, the adverse effects of China trade may be greater than the positive ones. Thus, many countries that suffer from insufficient productive capacity and limited economic diversification will not significantly improve, suggesting that trade with China is not a long-term or viable source of development for many African countries.

Despite the theoretical justification that FDI can have a positive impact on the economic growth of host economies through increasing capital accumulation (

Solow 1957;

Titarenko 2005;

Mahembe and Odhiambo 2014), a number of empirical studies found controversial results regarding the effect of FDI on economic growth. More specifically, the empirical studies on the impacts of Chinese FDI on the economic growth of African countries found an unresolved empirical puzzle some with a positive effect (

Whalley and Weisbrod 2012;

Pigato and Tang 2015;

Doku et al. 2017) and others with adverse effects (

Foster et al. 2008;

Adisu et al. 2010;

Busse et al. 2016). Thus, The practical significance of this study, regarding the Chinese FDI–growth nexus, comes at the crossroad of these findings, because examining the effects of FDI on economic growth without incorporating the domestic absorptive capacity of FDI-receiving countries does not provide the full conclusion of the nexus of FDI and economic growth, which means that institutional quality complements Chinese FDI in enhancing the economic growth of African countries. Indeed, the literature has shown that the positive effects of FDI on economic growth are conditioned by the quality of institutions (

Ali et al. 2010;

Khordagui and Saleh 2013;

Jude and Levieuge 2016).

The results of this study further indicate that the growth-effect of Chinese FDI to African countries is negative and statistically significant. However, this finding does not support some previous studies by

Doku et al. (

2017) and

Whalley and Weisbrod (

2012), who examined the effect of Chinese FDI on economic growth in Africa and found that the increase in China’s FDI into African countries enhances economic growth for African countries. Similarly, the findings of this study do not support the findings of

Busse et al. (

2016), who find that neither total net FDI inflows nor inflows from China alone have a significant impact on African growth.

This finding on the nexus of Chinese FDI and the economic growth of African countries is not surprising because a number of studies on the FDI–growth nexus came with inconclusive findings. For example, a study by

Bruno and Campos (

2018) shows that 11% of empirical studies show that FDI has a negative effect on growth, 39% find growth to be independent of FDI and 50% of empirical studies report a significantly positive effect of FDI on growth. Thus, it seems that FDI plays an ambiguous role in generating economic growth, with little support for an independent, positive effect.

One of the reasons for the controversial outcomes of previous studies might be that previous studies investigated the direct effect of Chinese FDI on economic growth without considering institutional and policy environments of Chinese FDI-hosting African countries. Here, in this analysis, we investigated not only the direct but also the conditional impact of Chinese FDI on the economic growth of African countries that will help observe the full impact of FDI flow.

As a result, as

Table 1 indicates, the interaction term of Chinese FDI and institutional quality has a strongly positive effect on the economic growth of African countries. The empirics of this result critically refer that the institutional quality level of a country does help in enhancing the growth effect of Chinese FDI flow to African countries. The positive impacts of Chinese FDI on African countries’ economic growth depend on institutional factors such as political stability, the absence of violence, rule of law, regulatory quality and the effectiveness of the government (

Asheghian 2004;

Hansen and Rand 2006). Furthermore, the finding of this study is consistent with the findings of

Adams and OseiOpoku (

2015) that the effects of FDI on economic growth is a positive and significant subject to the level of regulations in the FDI host countries. This reveals that the growth effect of FDI is stimulated in the presence of efficient and quality institutions.

These results highlight important potential channels through which FDI may affect growth and are broadly consistent with previous findings on absorptive capacity requirements. Therefore, the findings of this study highlight the complementarity between Chinese FDI to African countries and institutional quality where the impact of FDI on economic growth actually depends on the quality of institutions in the African countries. The findings sum up that the growth-enhancing effect of Chinese FDI on African countries is conditional on the African countries’ institutional environment.

From the theoretical point of view, it is stated that FDI can impact the host economies through capital accumulation (

Titarenko 2005). For example, one of the neo-classical economic models, the exogenous growth model of

Solow (

1956,

1957), indicates that economic growth is a function of the labor force and capital, keeping technology exogenous. According to this model, capital accumulation contributes to the economic growth of countries and FDI can contribute to economic growth directly through capital accumulation and expand economic growth (

Mahembe and Odhiambo 2014). This study, in this regard, extended this theory to include the mediating role of the domestic institutional quality of African countries in the Chinese FDI and China–Africa trade and economic growth of African countries’ relationship. Furthermore, to clearly examine the impact of the China–Africa trade and Chinese FDI, it is better to understand the nature of the economic relationship instruments of China–Africa economic relations. This implies that focusing on the individual pillar of the China–Africa economic relationship cannot explain the full impact of the relationship. Additionally, a policy analysis of the economic relationship between African countries and China should also consider the local institutional environment of African countries.

7. Conclusions

This study has examined the impacts of the China–Africa trade and FDI on the economic growth of African countries extending the economic growth model of

Mankiw et al. (

1992) to include different determinants of economic growth and control China–Africa economic relation indicators. The two-step system GMM model is employed using data for 44 African countries for the periods 2003–2017. The novel part of this study, in this regard, is considering the conditional effect of China–Africa trade and FDI on the economic growth of African countries extending economic relationship theories to include the mediating role of the institutional environment of African countries.

The results of the study reveal that the interaction of Chinese FDI with the institutional quality variable has a significant positive effect on the GDP per capita growth of African countries, indicating the conditional effect of the China–Africa economic relationship on the economic growth of African countries. Likewise, the conditional effect of China–Africa trade of domestic absorptive capacity on the economic growth of African countries is positive and statistically significant.

Our main conclusion is that institutional quality complements the impacts of China–Africa trade and Chinese FDI on economic growth in African countries. Thus, the results show that Chinese FDI and China–Africa trade alone have no significant positive effect on economic growth in African countries, while a better institutional environment encourages a growth-enhancing effect of Chinese FDI and China–Africa trade to African countries. Thus, the host countries’ governments have a crucial role in creating the conditions through improving the level of domestic institutions that consent for the leverage of the helpful effects or for the reduction of the adverse effects of Chinese FDI and China–Africa trade on African countries’ economic growth. Therefore, to reap the full benefits from the China–Africa trade and Chinese FDI, considerable improvements in the institutional quality of African economies are required.

{kind=link}

{kind=link}

{kind=link}