Reasons Fostering or Discouraging the Implementation of Central Bank-Backed Digital Currency: A Review

,

,  ,

,

Abstract

1. Introduction

2. CBDC: Characteristics, Safety and Sustainability

3. Methodology

4. Analysis of the Arguments of Countries Defending the Establishment of CBDC

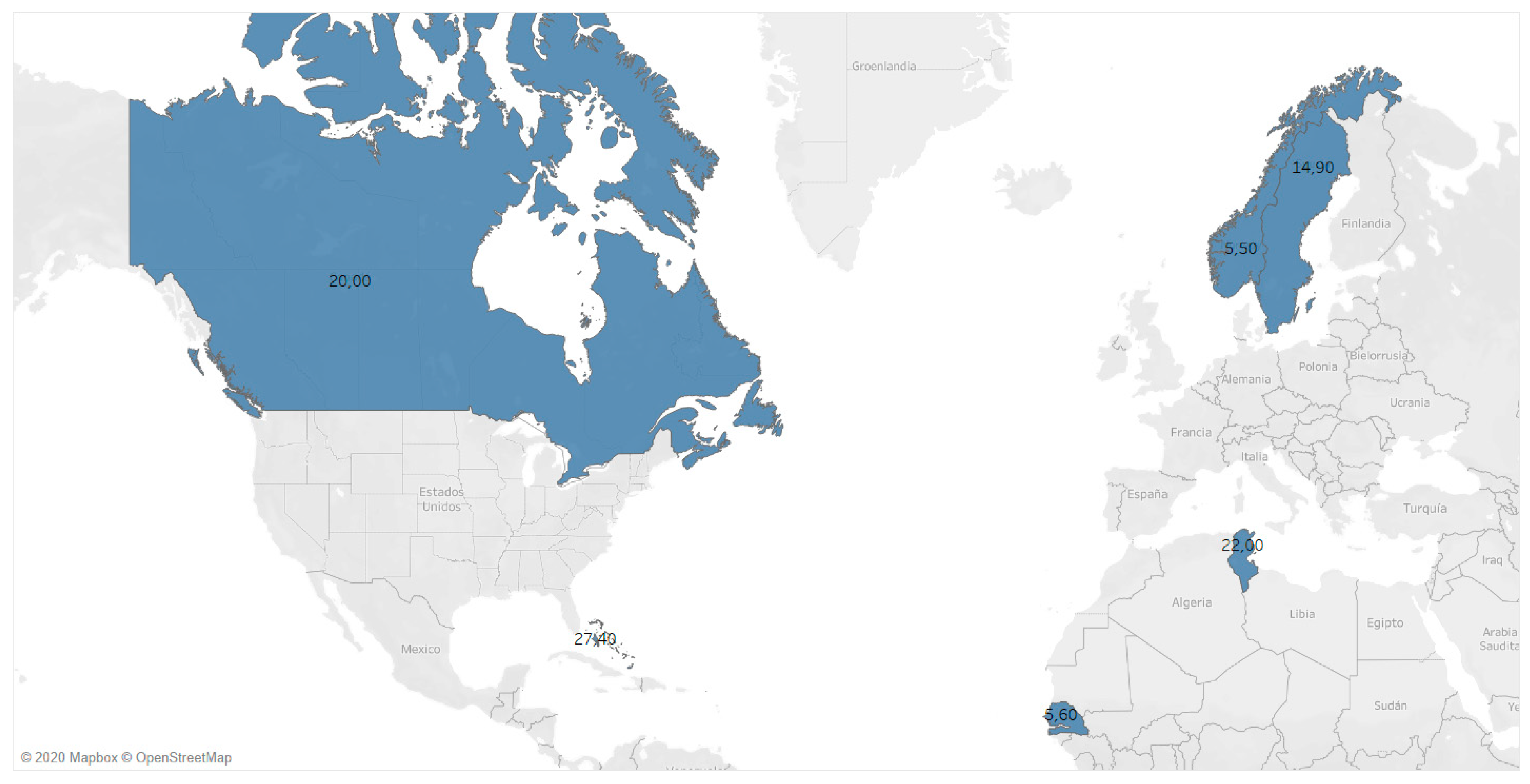

4.1. Geographic Dispersion and Access to Financial Services

4.2. Increased Bank Penetration Rate and Access to Financial Services

4.3. The Financial Sector Is Not Obsolete

4.4. Security Reasons: Avoid Money Laundering and Terrorist Financing

4.5. Consumer Protection

4.6. Maintaining Control over Monetary and Macroeconomic Policy

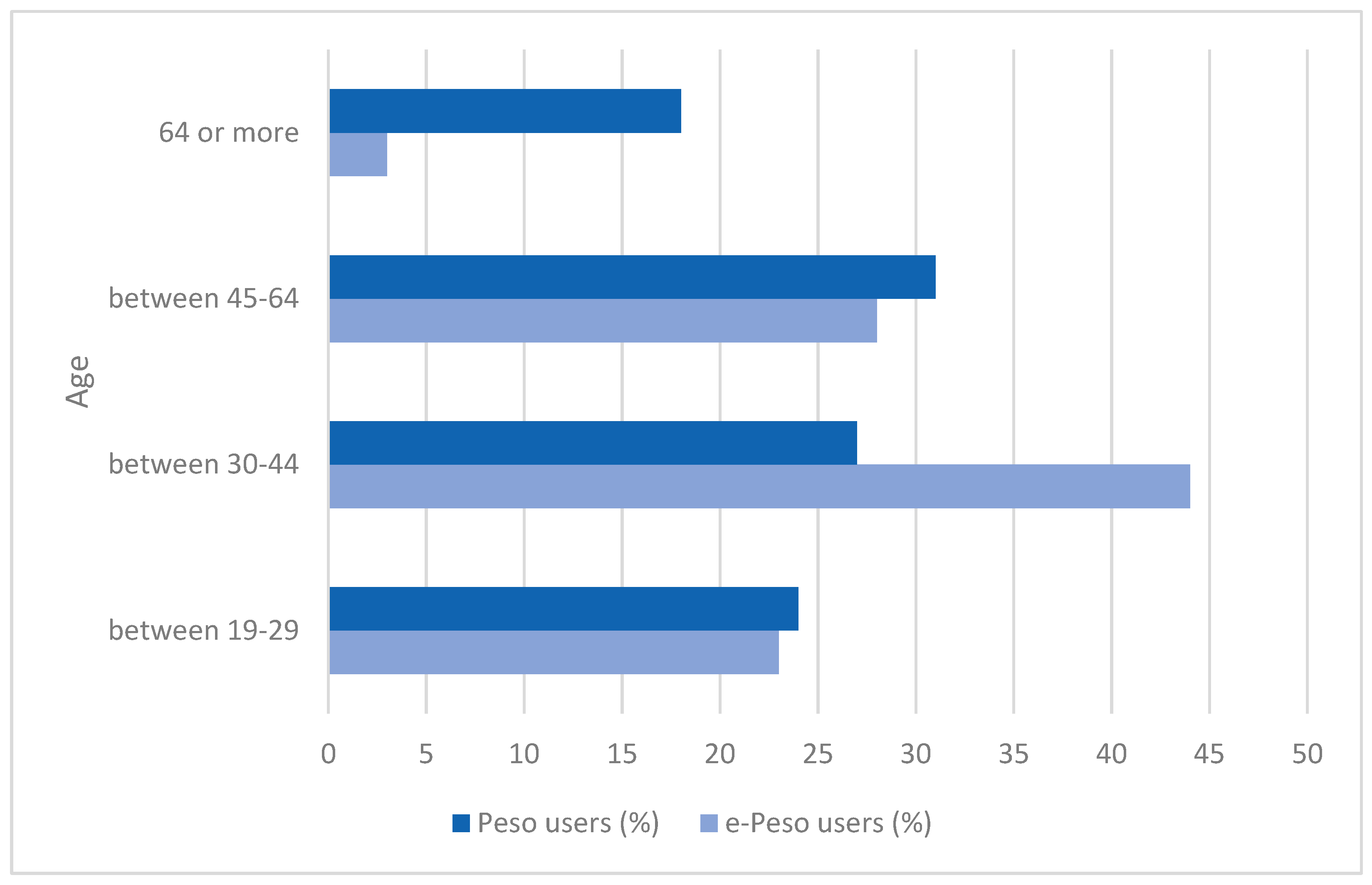

4.7. Drop in Use of Cash (Alternative)

4.8. Lower Costs and Greater Efficiency of the Banking System

5. Analysis of Reasons for Not Establishing a CBDC

5.1. Preference for Private Virtual Currency

5.2. Lack of Demand/Inability to function

5.3. Failed Test/Need for More Security and Investigation

5.4. There Is No Advantage over Electronic Payment

6. Conclusions

Author Contributions

Funding

Conflicts of Interest

Appendix A

References

- Amamiya, Masayoshi. 2019. Should The Bank of Japan Issue a Digital Currency? Speech at a Reuters Newsmaker Event in Tokyo, Speech. Tokyo, Japan, July 5; Available online: https://www.boj.or.jp/en/announcements/press/koen_2019/ko190712a.htm/ (accessed on 18 March 2020).

- Auer, Raphael, and Rainer Böhme. 2020. The Technology of Retail Central Bank Digital Currency. BIS Quarterly Review. Bank for International Settlements. Available online: https://www.bis.org/publ/qtrpdf/r_qt2003j.pdf (accessed on 16 March 2020).

- Banco Central del Uruguay. 2019. The Cost of Using Cash and Checks in Uruguay. Documentos De Trabajo Del Banco Central Del Uruguay. Montevideo: Banco Central del Uruguay. Available online: https://www.bcu.gub.uy/Estadisticas-e-Indicadores/Documentos%20de%20Trabajo/4.2019.pdf#search=e%2DPeso (accessed on 3 March 2020).

- Bank of China. 2017. 2016 Annual Report: Serving Society, Delivering Excellence. Annual Report. Beijing: Bank of China Limited. Available online: https://pic.bankofchina.com/bocappd/report/201704/P020170427553394747733.pdf (accessed on 5 March 2020).

- Bank of England. 2020. Discussion Paper Central Bank Digital Currency: Opportunities, Challenges and Design. Discussion Paper: Future of Money. London: Bank of England. Available online: https://www.bankofengland.co.uk/-/media/boe/files/paper/2020/central-bank-digital-currency-opportunities-challenges-and-design.pdf?la=en&hash=DFAD18646A77C00772AF1C5B18E63E71F68E4593 (accessed on 6 March 2020).

- Bank of Israel. 2018. Report of the Team to Examine the Issue of Central Bank Digital Currencies. Tel Aviv: Bank of Israel (BoI). Available online: https://www.boi.org.il/en/NewsAndPublications/PressReleases/Documents/Digital%20currency.pdf (accessed on 2 March 2020).

- Bank of Lithuania. 2019. In an Effort to Boost Debate on CBDC, The Bank of Lithuania Publishes an In-Depth Analysis. Available online: https://www.lb.lt/en/news/in-an-effort-to-boost-debate-on-cbdc-the-bank-of-lithuania-publishes-an-in-depth-analysis (accessed on 10 February 2020).

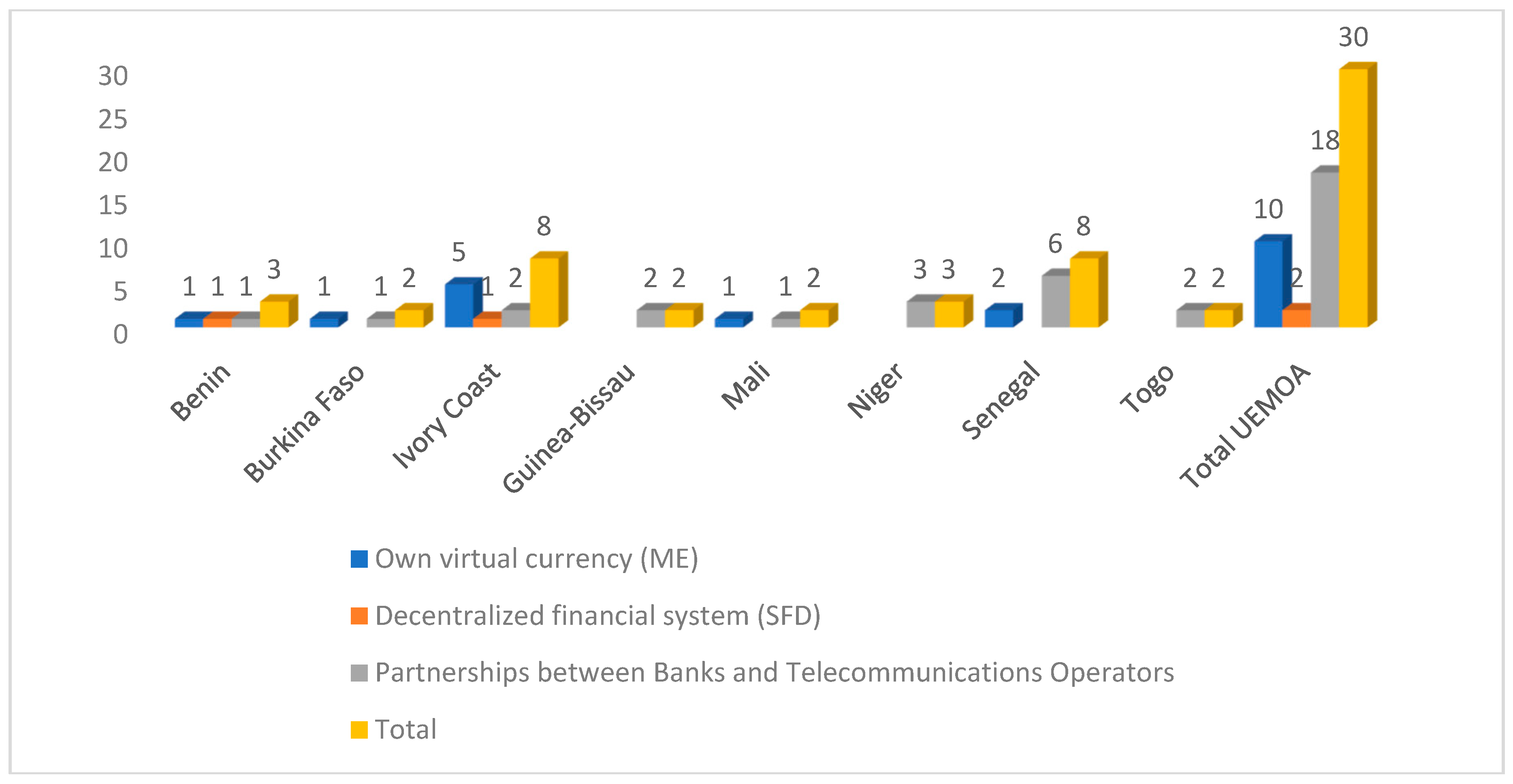

- Banque Centrale des Etats de l’Afrique de l’Ouest (BCEAO). 2020. Bceao.Int. Available online: https://www.bceao.int/fr/content/etablissements-de-monnaie-electronique (accessed on 16 January 2020).

- Berkmen, Pelin, Kimberly Beaton, Dmitry Gershenson, Javier Arze del Granado, Kotaro Ishi, Marie Kim, Emanuel Kopp, and Marina Rousset. 2019. Fintech in Latin America and the Caribbean: Stocktaking. IMF Working Papers 19: 1. [Google Scholar] [CrossRef]

- Bitcoin News. 2020. Central Banks Worldwide Testing Their Own Digital Currencies. Bitcoin News. Available online: https://news.bitcoin.com/central-banks-testing-digital-currencies/ (accessed on 12 January 2020).

- Bjerg, Ole, and Rasmus Hougaard Nielsen. 2018. Who Should Make Kroner?—A Review of Danmarks Nationalbank’s Analysis of CBDC. SSRN Electronic Journal, 22–24. [Google Scholar] [CrossRef]

- Blanc, Jérome. 2009. Beyond the Competition Approach to Money: A Conceptual Framework applied to the Early Modern France. Paper presented at the XVth World Economic History Congress, Utrecht, The Netherlands, August 3–7; Available online: https://halshs.archives-ouvertes.fr/halshs-00414496/document (accessed on 2 May 2020).

- Boar, Codruta, Henry Holden, and Amber Wadsworth. 2020. Impending Arrival—A Sequel to the Survey on Central Bank Digital Currency. BIS Papers. Basel: Bank for International Settlements. Available online: https://www.bis.org/publ/bppdf/bispap107.pdf (accessed on 10 January 2020).

- Bordo, Michael D., and Andrew T. Levin. 2017. Central Bank Digital Currency and the Future of Monetary Policy. NBER Working Papers. National Bureau of Economic Research, Cambridge, MA, USA. Available online: http://www.nber.org/papers/w23711 (accessed on 10 December 2019).

- Brainard, Lael. 2018. Cryptocurrencies, Digital Currencies, and Distributed Ledger Technologies: What Are We Learning? Governor Lael Brainard at The Decoding Digital Currency Conference Sponsored by The Federal Reserve Bank of San Francisco. Presentation, San Francisco, CA, USA, May 15. Available online: https://www.federalreserve.gov/newsevents/speech/brainard20180515a.htm (accessed on 22 December 2019).

- Brainard, Lael. 2019. Delivering Fast Payments for All. Remarks by Lael Brainard Member Board of Governors of the Federal Reserve System. Presentation, Federal Reserve Bank of Kansas City Town Hall, Kansas City, MI, USA, August 5. Available online: https://www.federalreserve.gov/newsevents/speech/files/brainard20190805a.pdf (accessed on 24 December 2019).

- Brainard, Lael. 2020. The Digitalization of Payments and Currency: Some Issues for Consideration. Remarks by Lael Brainard Member Board of Governors of The Federal Reserve System. Symposium on the Future of Payments. Speech, Stanford Graduate School of Business, Stanford, CA, USA, February 5. Available online: https://www.federalreserve.gov/newsevents/speech/files/brainard20200205a.pdf (accessed on 24 December 2019).

- Burleson, Joseph. 2013. Bitcoin: The Legal Implications of A Novel Currency. EV. BANKING & FIN. L. Available online: https://www.bu.edu/rbfl/files/2014/03/RBFL-V.-33_1_Burleson.pdf (accessed on 2 November 2019).

- Campbell-Verduyn, Malcolm. 2018. Bitcoin, Crypto-Coins, and Global Anti-Money Laundering Governance. Crime, Law and Social Change 69: 283–305. [Google Scholar] [CrossRef]

- Campuzano, Vásquez, John Alexander, Gonzalo Junior Chávez Cruz, and José Maza Iñiguez. 2018. El fracaso del dinero electrónico en ecuador. 3C Empresa: Investigación Y Pensamiento Crítico 7: 82–101. [Google Scholar] [CrossRef]

- Banco Central del Uruguay. 2018. Autorización Prueba Piloto Para La Transformación De Dinero En Billete Electrónico. Bcu.Gub.Uy. Available online: https://www.bcu.gub.uy/Acerca-de-BCU/Resoluciones%20de%20Directorio/RD_282_2017.pdf#search=Billete%20electr%C3%B3nico (accessed on 17 January 2020).

- Centrale Bank van Curaçao en Sint Maarten. 2018. Central Banks Should Emerge as Innovation Leaders. Available online: https://cbcs.spin-cdn.com/media/speeches_2018_2019/20190330_opening_speech_l_matroos_lasten_june_29th_2018.pdf (accessed on 10 November 2019).

- Chan, Norman T. L. 2018. Keynote Speech at Treasury Markets Summit 2018: Crypto-Assets and Money. Norman T. L. Chan, Chief Executive. Hong Kong Monetary Authority Speech, Hong Kong, September 21. Available online: https://www.hkma.gov.hk/eng/news-and-media/speeches/2018/09/20180921-1/ (accessed on 13 February 2020).

- Chapman, James, Rodney Garratt, Scott Hendry, Andrew McCormack, and Wade McMahon. 2017. Project Jasper: Are Distributed Wholesale Payment Systems Feasible Yet? Ebook. Ottawa: Bank of Canada. Available online: https://www.bankofcanada.ca/wp-content/uploads/2017/05/fsr-june-2017-chapman.pdf (accessed on 3 January 2020).

- Chehade, Nadine. 2015. Financial Inclusion in Tunisialow-Income Households and Micro-Enterprises. Ebook. Washington, DC: World Bank. Available online: https://openknowledge.worldbank.org/bitstream/handle/10986/22940/Snapshot000fin0nd0micro0enterprises.pdf?sequence=1&isAllowed=y (accessed on 6 November 2019).

- China Banking News. 2020. 15 Companies Reportedly Participating in Development of China’s Central Bank Digital Currency. Chinabankingnews.Com. Available online: http://www.chinabankingnews.com/2020/01/02/15-companies-reportedly-participating-in-development-of-chinas-central-bank-digital-currency/ (accessed on 12 March 2020).

- Chong Tee, Ong. 2018. The Post-Crisis Financial Landscape: What Next?—Remarks by Mr. Ong Chong Tee, Deputy Managing Director, Monetary Authority of Singapore, at Society for Financial Studies Cavalcade Asia-Pacific Conference’s. Lecture, December 13. Available online: https://www.mas.gov.sg/news/speeches/2018/the-postcrisis-financial-landscape-what-next (accessed on 26 November 2019).

- Choo, Kim-Kwang Raymond. 2015. Cryptocurrency and Virtual Currency: Corruption and Money Laundering/Terrorism Financing Risks? In Handbook of Digital Currency. Cambridge: Academic Press, pp. 283–307. [Google Scholar]

- Cull, Robert, Tilman Ehrbeck, and Nina Holle. 2014. La Inclusión Financiera Y El Desarrollo: Pruebas Recientes De Su Impacto. Ebook. Washington, DC: World Bank. Available online: https://www.cgap.org/sites/default/files/FocusNote-Financial-Inclusion-and-Deelopment-April-2014-Spanish.pdf (accessed on 8 November 2019).

- Danmarks Nationalbank. 2017. Central Bank Digital Currency in Denmark? Analysis. Copenhaguen: Danmarks Nationalbank. Available online: https://www.nationalbanken.dk/en/publications/Documents/2017/12/Analysis%20-%20Central%20bank%20digital%20currency%20in%20Denmark.pdf (accessed on 12 November 2019).

- Diariobitcoin. 2016. Canadá Experimenta Con La Primera Moneda Digital De Curso Legal De La Historia: CAD-COIN. Available online: https://www.diariobitcoin.com/index.php/2016/06/19/canada-experimenta-con-la-primera-moneda-digital-de-curso-legal-de-la-historia-cad-coin/ (accessed on 24 December 2019).

- Digital Currencies and Fintech. 2020. Bankofcanada.Ca. Available online: https://www.bankofcanada.ca/research/digital-currencies-and-fintech/ (accessed on 26 November 2019).

- Digital Economy and Society Index (DESI). 2017. Shaping Europe’S Digital Future—European Commission. Available online: https://ec.europa.eu/digital-single-market/en/news/digital-economy-and-society-index-desi-2017 (accessed on 3 December 2019).

- Dolader Retamal, Carlos, Joan Bel Roig, and José Luis Muñoz Tapia. 2017. La Blockchain: Fundamentos, Aplicaciones Y Relación Con Otras Tecnologías Disruptivas. Economía Industrial 405: 33–40. Available online: https://www.mincotur.gob.es/Publicaciones/Publicacionesperiodicas/EconomiaIndustrial/RevistaEconomiaIndustrial/405/DOLADER,%20BEL%20Y%20MU%C3%91OZ.pdf (accessed on 23 January 2020).

- Ducas, Evangeline, and Alex Wilner. 2017. The Security and Financial Implications of Blockchain Technologies: Regulating Emerging Technologies in Canada. International Journal: Canada’s Journal of Global Policy Analysis 72: 538–562. [Google Scholar] [CrossRef]

- Echarte-Fernández, Miguel Àngel. 2019. La Dolarización En América Latina, 1st ed. Madrid: Unión Editorial. [Google Scholar]

- Engert, Walter, Ben Fung, and Scott Hendry. 2018. Is A Cashless Society Problematic? Ottawa: Bank of Canada. Available online: https://www.bankofcanada.ca/wp-content/uploads/2018/10/sdp2018-12.pdf (accessed on 23 December 2019).

- Ernst and Young. 2019. EY Fintech Australia Census 2019 Profiling and Defining the Fintech Sector. Ernst & Young. Available online: https://fintechauscensus.ey.com/2019/Documents/EY%20FinTech%20Australia%20Census%202019.pdf (accessed on 2 November 2019).

- EY Fintech Adoption Index: Canadian Findings. 2017. Ebook. Ernst & Young. Available online: http://www.ey.com/ca/en/services/advisory/advisory-for-financial-services/ey-fintech-adoption-index-canadian-findings,2016 (accessed on 12 November 2019).

- Fabris, Nikola. 2019. Cashless Society—The Future of Money Or A Utopia? Journal of Central Banking Theory and Practice 8: 53–66. [Google Scholar] [CrossRef]

- Federal Reserve Bank of St. Louis (Switzerland). 2018. Assessing the Impact of Central Bank Digital currency on Private Banks. Federal Reserve Bank of St. Louis. Available online: https://www.snb.ch/n/mmr/reference/sem_2019_05_31_andolfatto/source/sem_2019_05_31_andolfatto.n.pdf (accessed on 5 February 2020).

- Fernández de Lis, Santiago, and Olga Gouveia. 2019. Monedas Digitales Emitidas Por Bancos Centrales: Características, Opciones, Ventajas Y Desventajas. Documento De Trabajo. Madrid: BBVA Research. Available online: https://www.bbvaresearch.com/wp-content/uploads/2019/03/WP_Monedas-digitales-emitidas-por-bancos-centrales-ICO.pdf (accessed on 28 January 2020).

- Fintech in Canada: Towards Leading the Global Financial Technology Transition. 2016. Ebook. Digital Finance Institute, McCarthy Tétrault LLP. Available online: http://www.digitalfinanceinstitute.org/wp-content/uploads/2017/02/Digital-Finance-Institute-FinTech-Report-1.pdf (accessed on 12 January 2020).

- Ghalib, Asad Kamran, and Degol Hailu. 2008. Bancarización De Los No Bancarizados: Mejorar El Acceso A Servicios Financieros. Ebook. Brasília: International Policy, Centre for Inclusive Grotwth. Available online: https://ipcig.org/pub/esp/IPCPolicyResearchBrief9.pdf (accessed on 28 October 2019).

- Gómez-Fernández, Nerea, and Juan-Francisco Albert. 2019. ¿Es La Eurozona Un Área Óptima Para Suprimir El Efectivo? Un Análisis Sobre La Inclusión Financiera Y El Uso De Efectivo. Cuadernos De Economía 43. [Google Scholar] [CrossRef]

- Grym, Aleksi, Päivi Heikkinen, Karlo Kauko, and Kari Takala. 2017. Central Bank Digital Currency. Bof Economics Review. Helsinki: Bank of Finland. Available online: https://pdfs.semanticscholar.org/9fa6/e095fa409d199e7aec8b50b657a7075fbe9e.pdf (accessed on 16 December 2019).

- Hayashi, Kenji, Hiroyuki Takano, Makoto Chiba, and Yasuhiro Takamoto. 2019. (Research Lab) Summary of The Report of The Study Group on Legal Issues Regarding Central Bank Digital Currency: Bank of Japan. Available online: https://www.boj.or.jp/en/research/wps_rev/lab/lab19e03.htm/ (accessed on 1 February 2020).

- Huillet, Marie. 2019. Jefe Del Banco Central De Rusia: Estamos Considerando Una CBDC, Pero No Para El Futuro Cercano. Cointelegraph. Available online: https://es.cointelegraph.com/news/russian-central-bank-head-cbdc-under-consideration-but-not-for-near-future (accessed on 1 March 2020).

- Jinze, Etienne. 2019. First Look: China’s Central Bank Digital Currency. Binance Research. Available online: https://research.binance.com/analysis/china-cbdc (accessed on 22 October 2019).

- Johan, Sofia A., and Anshum Pant. 2018. Regulation of The Crypto-Economy: Securitization of The Digital Security. SSRN Electronic Journal. [Google Scholar] [CrossRef]

- Johnson, Grahame, and Lukasz Pomorski. 2014. Briefing on Digital Currencies. Ebook. Ottawa: Bank of Canada. Available online: https://www.bankofcanada.ca/wp-content/uploads/2014/04/Senate_statement.pdf (accessed on 29 October 2019).

- Juškaitė, Aistė, Sigitas Šiaudinis, and Tomas Reichenbachas. 2019. CBDC—In A Whirlpool of Discussion. Occasional Paper Series; Vilnius: Bank of Lithuania. Available online: https://www.lb.lt/en/publications/no-29-aiste-juskaite-sigitas-siaudinis-tomas-reichenbachas-cbdc-in-the-whirpool-of-discussion (accessed on 22 January 2020).

- Kganyago, Lesetja. 2018. Governor Speech at the Nelson Mandela Commemorative Banknotes and R5 Circulation Coin Launch. Speech, Freedom Park, Pretoria, July 13. Available online: https://www.resbank.co.za/SiteAssets/Lists/Speeches/NewForm/Governor’s%20address%20Commemorative%20Banknotes%20and%20coin%20launch.pdf (accessed on 1 March 2020).

- Kumhof, Michael, and Clare Noone. 2018. Ccentral Bank Digital Currencies—Design Principles and Balance Sheet Implications. Working Paper. Bank of England, London, UK. Available online: https://www.bankofengland.co.uk/working-paper/2018/central-bank-digital-currencies---design-principles-and-balance-sheet-implications (accessed on 24 November 2019).

- Kuroda, Akinobu. 2008. What Is The Complementarity Among Monies? An Introductory Note. Financial History Review 15: 7–15. [Google Scholar] [CrossRef]

- Licandro, Gerardo. 2018. Uruguayan E-Peso on the Context of Financial Inclusion. Lecture, Basel, November 16. Available online: https://www.bis.org/events/eopix_1810/licandro_pres.pdf (accessed on 18 December 2019).

- Loh, Jacqueline. 2018. E-Payments in Asia: Regulating Innovation and Innovative Regulation—Keynote Address by Ms. Jacqueline Loh, Deputy Managing Director, Monetary Authority of Singapore, at The Central Bank Payments. Speech, Singapore, June 26. Available online: https://www.mas.gov.sg/news/speeches/2018/epayments-in-asia (accessed on 7 December 2019).

- Lowe, Philip. 2017. An Eaud? Sydney: Reserve Bank of Australia. Available online: https://www.rba.gov.au/speeches/2017/pdf/sp-gov-2017-12-13.pdf (accessed on 12 December 2019).

- Mancini-Griffoli, Tommaso, Maria Soledad Martinez Peria, Itai Agur, Anil Ari, John Kiff, Adina Popescu, and Celine Rochon. 2018. Casting Light on Central Bank Digital Currencies. Ebook. Washington, DC: International Monetary Fund. Available online: https://www.imf.org/~/media/Files/Publications/SDN/2018/SDN1808.ashx (accessed on 28 October 2019).

- Möser, Malte, Rainer Böhme, and Dominic Breuker. 2014. Towards Risk Scoring of Bitcoin Transactions. Paper presented at the International Conference on Financial Cryptography and Data Security FC 2014: Financial Cryptography and Data Security, Christ Church, Barbados, March 3–7; Lecture. pp. 16–32. [Google Scholar]

- Náñez Alonso, Sergio Luis. 2019. Activities and Operations with Cryptocurrencies and Their Taxation Implications: The Spanish Case. Laws 8: 16. [Google Scholar] [CrossRef]

- Navas Navarro, Susana. 2015. Un Mercado Financiero Floreciente: El Del Dinero Virtual No Regulado (Especial Atención a Los Bitcoins). Revista CESCO De Derecho De Consumo 13: 79–115. Available online: http://www.revista.uclm.es/index.php/cesco (accessed on 9 November 2019).

- Niepelt, Dirk. 2018. Reserves for All? Central Bank Digital Currency, Deposits, and Their (Non)-Equivalence. Cesifo Working Papers. Munich Society for the Promotion of Economic Research–CESifo GmbH, Munich, Germany. Available online: http://www.CESifo-group.org/wp (accessed on 11 October 2019).

- Norges Bank. 2018. Central Bank Digital Currencies. Norges Bank Papers. Oslo: Norges Bank. Available online: https://static.norges-bank.no/contentassets/166efadb3d73419c8c50f9471be26402/nbpapers-1-2018-centralbankdigitalcurrencies.pdf?v=05/18/2018121950&ft=.pdf (accessed on 17 November 2019).

- Norges Bank. 2019. Central Bank Digital Currencies Nº2. Norges Bank Papers. Oslo: Norges Bank. Available online: https://static.norges-bank.no/contentassets/79181f38077a48b59f6fbdd113c34d2c/nb_papers_2_19_cbdc.pdf?v=06/27/2019121511&ft=.pdf (accessed on 18 November 2019).

- Novoa, Jaime. 2020. Noruega Afirma Que Bitcoin No Es Una Moneda O Divisa. Genbeta.Com. Available online: https://www.genbeta.com/web/noruega-afirma-que-bitcoin-no-es-una-moneda-o-divisa (accessed on 26 February 2020).

- Nuño, Galo. 2018. Implicaciones De Política Monetaria De La Emisión De Dinero Digital Por Parte De Los Bancos Centrales. Madrid: Banco de España. [Google Scholar]

- Observatorio Económico Legislativo de CEDICE Libertad. 2015. La Dolarización Como Opción De Política Monetaria En Venezuela: Aproximación Desde Un Análisis Costo-Beneficio. ACB: Análisis Costo Beneficio. CEDICE. Available online: http://cedice.org.ve/observatoriolegislativo/wp-content/uploads/2015/08/ACB-Dolarizacion-OT-Agosto-2015.pdf (accessed on 3 January 2020).

- Pankki, Suomen. 2018. Central Bank Issued Digital Cash—Justification and Mandate Seminar. Suomen Pankki. Available online: ttps://www.suomenpankki.fi/en/financial-stability/events/money-in-the-digital-age/central-bank-issued-digital-cash/ (accessed on 20 December 2019).

- Partz, Helen. 2019. El Banco Central De Rusia Ya Está Probando Stablecoins Vinculadas A Activos Reales. Cointelegraph. Available online: https://es.cointelegraph.com/news/russias-central-bank-is-now-testing-real-asset-pegged-stablecoins (accessed on 15 January 2020).

- Ponsford, Matthew. 2015. A Comparative Analysis of Bitcoin and Other Decentralized Virtual Currencies: Legal Regulation in The People’s Republic of China, Canada, and The United States. SSRN Electronic Journal, 30–31. [Google Scholar] [CrossRef]

- Raskin, Max, and David Yermack. 2016. Digital Currencies, Decentralized Ledgers, and The Future of Central Banking. NBER Working Paper Series. National Bureau of Economic Research, Cambridge, MA, USA. Available online: http://www.nber.org/papers/w22238 (accessed on 4 January 2020).

- Reserve Bank of Australia. 2019. Submission To Thesenate Select Committee on Financial Technology and Regulatory Technology; Sydney: Reserve Bank of Australia. Available online: https://www.rba.gov.au/publications/submissions/payments-system/financial-and-regulatory-technology/pdf/financial-and-regulatory-technology.pdf (accessed on 12 February 2020).

- Reserve Bank of India. 2020. Distributed Ledger Technology, Blockchain and Central Banks. RBI Bulletin. Assam: The Reserve Bank of India. Available online: https://rbidocs.rbi.org.in/rdocs/Bulletin/PDFs/03AR_11022020510886F328EB418FB8013FBB684BB5BC.PDF (accessed on 17 February 2020).

- Reserve Bank of New Zealand. 2018. The Future of Cash in New Zealand Internal Project Research Report; Wellington: Reserve Bank of New Zealand. Available online: https://www.rbnz.govt.nz/-/media/ReserveBank/Files/Notes%20and%20coins/future-of-cash/Future-of-cash-internal-research-report-June-2018.pdf?revision=6c258e72-e57d-4479-a251-0c5ded245311 (accessed on 18 February 2020).

- Sánchez-Cano, Julieta Evangelina. 2019. El Bitcoin Y Su Demanda Exponencial De Energía. Panorama Económico 14: 85. [Google Scholar] [CrossRef]

- Sik Kim, Young, and Ohik Kwon. 2019. Central Bank Digital Currency and Financial Stability. BOK Working Paper No. 2019-6, Economic Research Institute-Bank of Korea, Seoul, Korea. Available online: http://www.bok.or.kr/ucms/cmmn/file/fileDown.do?menuNo=600342&atchFileId=FILE_000000000008900&fileSn=1 (accessed on 8 January 2020).

- Slattery, Thomas. 2014. Taking a Bit out of Crime: Bitcoin and Cross-Border Tax Evasion. Brooklyn Journal of International Law 39: 829–60. [Google Scholar]

- South African Reserve Bank. 2018. Review of The National Payment System Act 78 of 1999. Policy Paper. South African Reserve Bank. Available online: https://www.resbank.co.za/RegulationAndSupervision/NationalPaymentSystem(NPS)/Legal/Documents/Documents%20for%20Comment/NPS%20Act%20Review%20Policy%20Paper%20-%20final%20version%20-%2013%20September%202018.pdf (accessed on 4 February 2020).

- Sveriges Riksbank. 2018. The Riksbank’S E-Krona Projectreport 2. Stockholm: Sveriges Riksbank. Available online: https://www.riksbank.se/globalassets/media/rapporter/e-krona/2018/the-riksbanks-e-krona-project-report-2.pdf (accessed on 17 November 2019).

- Swiss Financial Market Supervisory Authority. 2019. FINMA Guidance: Stringent Approach to Combating Money Laundering on the Blockchain. Available online: https://www.finma.ch/en/news/2019/08/20190826-mm-kryptogwg/ (accessed on 21 November 2019).

- Swiss National Bank. 2019. The Evolution of Payment Systems in the Digital Age: A Central Bank Perspective. Zurich: Swiss National Bank. Available online: https://www.snb.ch/en/mmr/speeches/id/ref_20190328_amrtmo/source/ref_20190328_amrtmo.en.pdf (accessed on 22 November2019).

- Swiss National Bank. 2020. Central Bank Group to Assess Potential Cases for Central Bank Digital Currencies. Available online: https://www.snb.ch/en/mmr/reference/pre_20200121/source/pre_20200121.en.pdf (accessed on 4 March 2020).

- The Central Bank of the Bahamas. 2019a. Project Sand Dollar: A Bahamian Payments Systems Modernization Initiative. Available online: https://www.centralbankbahamas.com/news.php?cmd=view&id=16660 (accessed on 23 October 2019).

- The Central Bank of the Bahamas. 2019b. Project Sand Dollar: A Bahamas payments System Modernisation Initiative-2. Nassau: The Central Bank of the Bahamas. Available online: https://www.centralbankbahamas.com/download/022598600.pdf (accessed on 23 October 2019).

- The Hong Kong Monetary Authority. 2020. The Outcomes and Findings of Project Inthanon-Lionrock and the Next Steps. Available online: https://www.hkma.gov.hk/eng/news-and-media/press-releases/2020/01/20200122-4/ (accessed on 26 February 2020).

- The Nassau Guardian. 2020. Central Bank to Sign Contract for Digital Currency System. The Nassau Guardian. Available online: https://thenassauguardian.com/2019/05/29/central-bank-to-sign-contract-for-digital-currency-system/ (accessed on 2 March 2020).

- The Road to Digital Money. 2020. Bankofcanada.Ca. Available online: https://www.bankofcanada.ca/2019/04/the-road-to-digital-money/ (accessed on 17 January 2020).

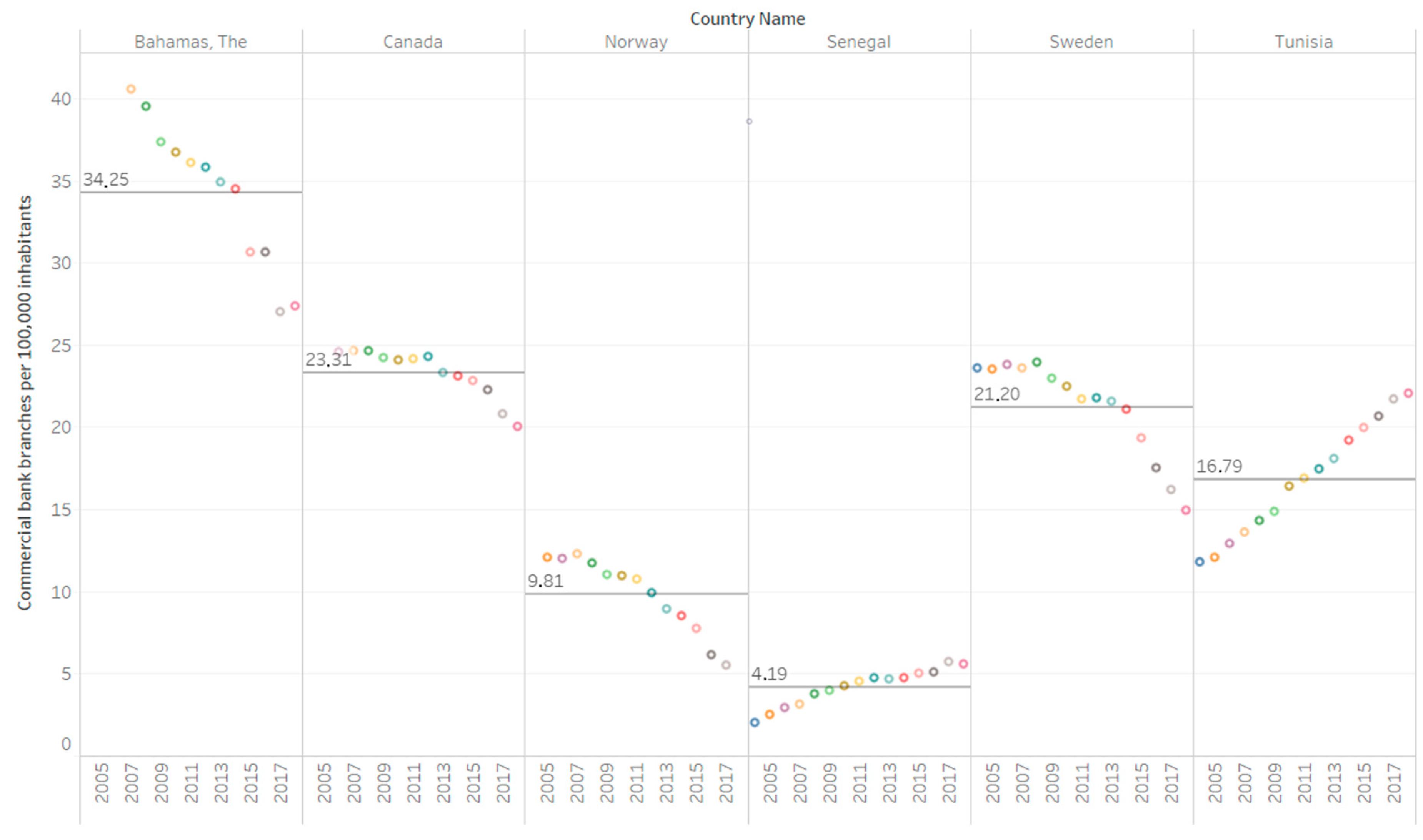

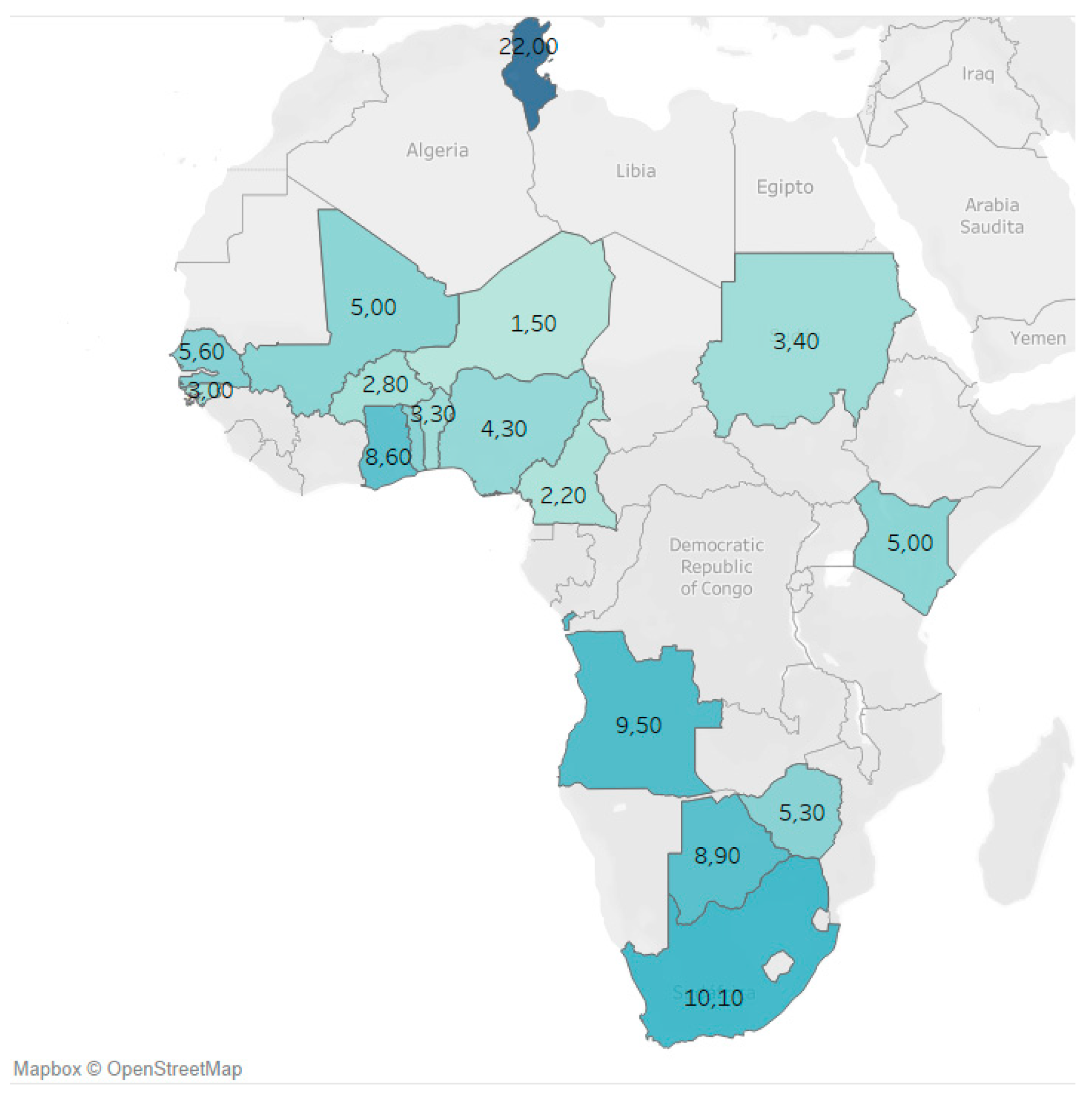

- The World Bank. 2020a. Commercial Bank Branches (per 100,000 Adults) in Senegal, Tunisia, Kenya, South Africa, Ghana, Niger, Nigeria, Mali, Guinea-Bissau, Togo, Benin, Burkina Faso, Angola, Zimbabwe, Cameroon, Tanzania, Sudan and Botswana. Available online: https://data.worldbank.org/indicator/FB.CBK.BRCH.P5?end=2018&locations=SN-TN-KE-ZA-GH-NE-NG-ML-GW-TG-BJ-BF-AO-ZW-CM-TZ-SD-BW&start=2018&view=bar (accessed on 12 April 2020).

- The World Bank. 2020b. Commercial Bank Branches per 100,000 Inhabitants: Canada, Bahamas, Sweden, Norway, Tunisia and Senegal, 2004–2018 Data. Datos.Bancomundial.Org. Available online: https://datos.bancomundial.org/indicador/FB.CBK.BRCH.P5?end=2018&locations=CA-BS-SE-NO-SN-TN&start=2004&view=chart (accessed on 1 February 2020).

- The World Bank. 2020c. Country, Year, Number of ATMs per 100,000 Inhabitants and Trend. Available online: https://databank.worldbank.org/reports.aspx?source=2&series=FB.ATM.TOTL.P5&country=CAN,BHS,SWE,NOR,SEN,TUN (accessed on 2 February 2020).

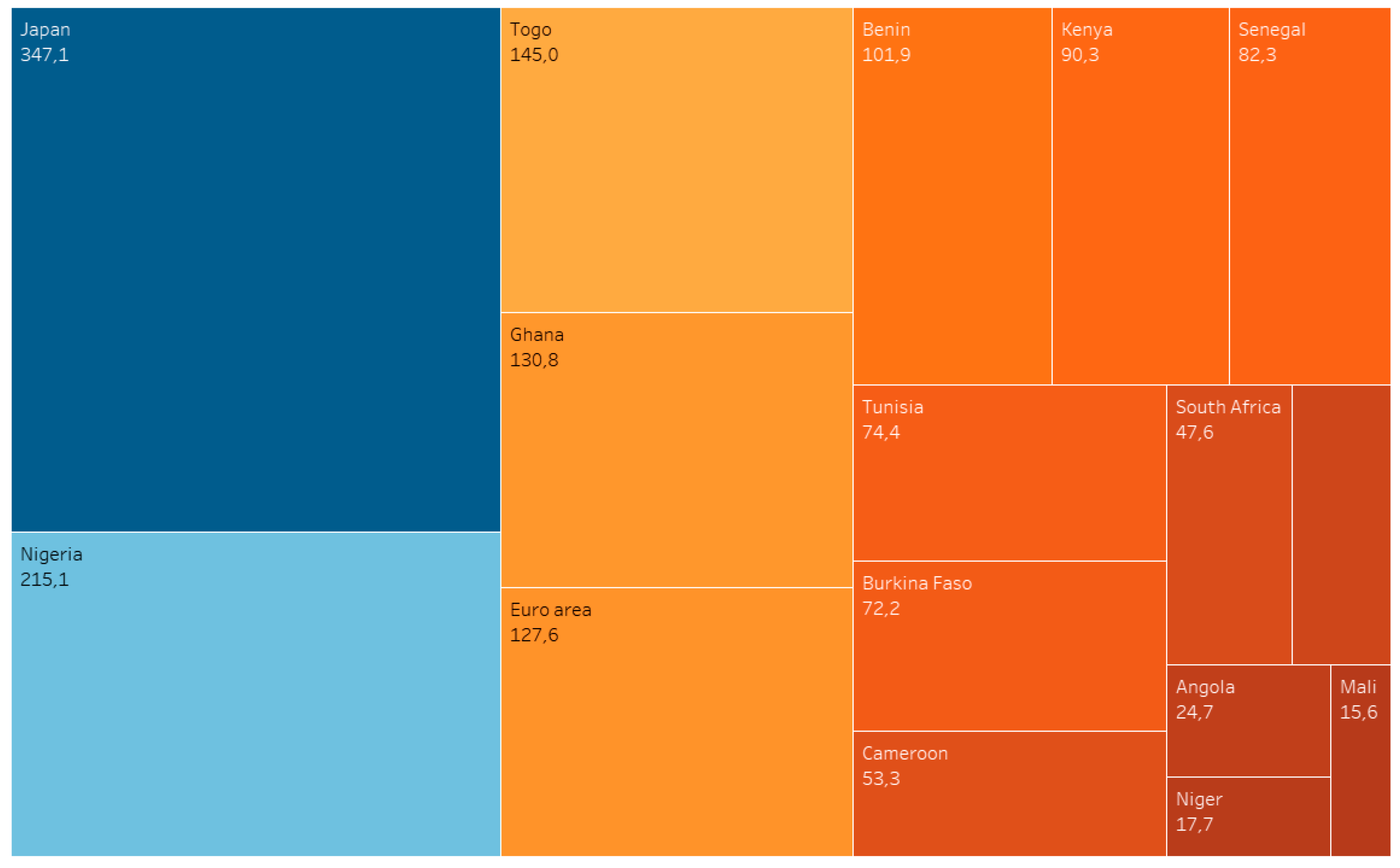

- The World Bank. 2020d. Population Density (People per sq. km of Land Area) of South Africa, Tunisia, Angola, Ghana, Senegal, Zimbabwe, Togo, Kenya, Mali, Nigeria, Benin, Burkina Faso, Cameroon, Niger, Japan and the Euro area. Available online: https://data.worldbank.org/indicator/EN.POP.DNST?end=2018&locations=ZA-TN-AO-GH-SN-ZW-TG-KE-ML-NG-BJ-BF-CM-NE-JP-XC&start=2018&view=bar (accessed on 4 March 2020).

- The World Bank. 2020e. Population Density (People per sq. km of Land Area)—Canada, Norway, Tunisia, Senegal. Available online: https://databank.worldbank.org/reports.aspx?source=2&series=EN.POP.DNST&country=CAN,NOR,TUN,SEN (accessed on 1 March 2020).

- Van Wegberg, Rolf, Jan-Jaap Oerlemans, and Oskar van Deventer. 2018. Bitcoin Money Laundering: Mixed Results? An Explorative Study on Money Laundering of Cybercrime Proceeds Using Bitcoin. Journal of Financial Crime 25: 419–35. [Google Scholar] [CrossRef]

- Wilson, Maria Paz. 2018. El Billete Electrónico Emitido Por El BCU: Avance En Su Aplicación. Lecture, VII Jornadas de Derecho Bancocentralista. Disponible en. Available online: https://www.bcu.gub.uy/Comunicaciones/DraMariaPazWilson.ppt2018 (accessed on 4 December 2019).

- Wu, Chen Y., and Vivek K. Pandey. 2014. The Value of Bitcoin in Enhancing the Efficiency of an Investor’s Portfolio. Journal of Financial Planning 27: 44–52. [Google Scholar]

| 1 | However, both systems can fulfill the classic functions of money: medium of exchange, unit of accounting and store of value. |

| 2 | To do this, FINMA published a guide on the applicable regulations to prevent money laundering through this technology, which can be found at: https://www.finma.ch/en/~/media/finma/dokumente/dokumentencenter/myfinma/4dokumentation/finma-aufsichtsmitteilungen/20190826-finma-aufsichtsmitteilung-02–2019.pdf?la=en. |

| 3 | Continuing with the issue related to consumer protection, and as a curiosity, we point out the initiative carried out in Liberstad, a private anarcho-capitalist city in Norway. This city has implemented a native virtual currency called City Coin on its Smart City platform, which is powered by blockchain technology (Norway: An Anarcho-capitalist Smart City Adopts Crypto as the Only Recognized Means of Exchange 2020). City Coin was established as the only official means of exchange. Founded in 2015, the city is the result of the Liberstad project, administered by the non-profit Liberstad Drift Association, which aims to create a city-society autonomous from government interference. City parcels were first sold for Bitcoin (BTC) and NOK in 2017. Around 100 individuals had purchased parcels from the project in April 2018. |

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

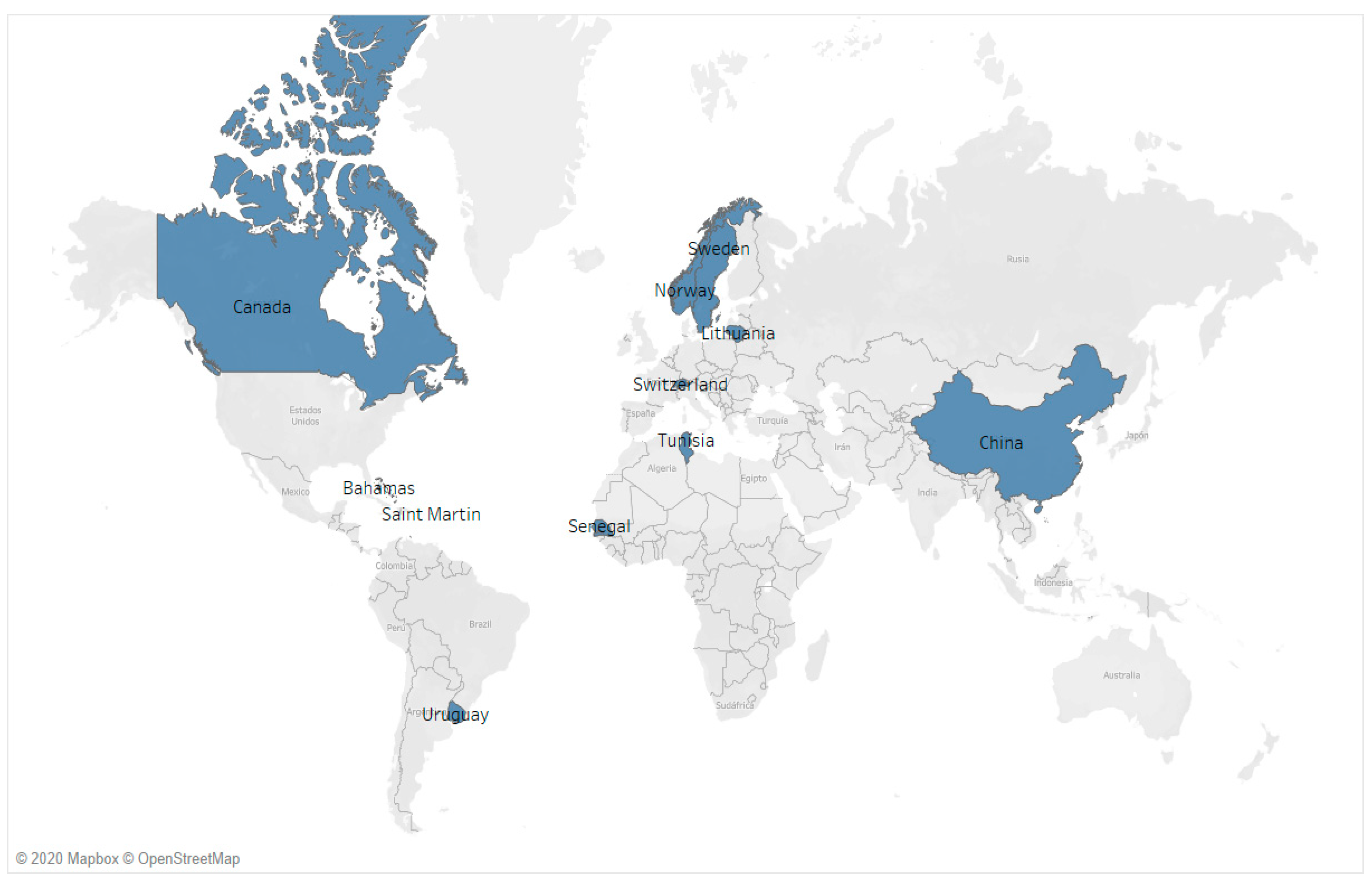

| Country/Reason for Establishing CBDC | Geographic Dispersion/Access to Financial Services | Increased Rate of Bank Penetration | Avoid Obsolescence of Financial Sector | Avoid Money Laundering and Terrorist Financing | Consumer Protection | Maintain Control Over Monetary and Macroeconomic Policy | Drop in Cash Use (Alternative) | Lower Costs and Greater Efficiency of Banking System |

|---|---|---|---|---|---|---|---|---|

| Canada | x | x | x | x | x | |||

| Senegal | x | x | ||||||

| Tunisia | x | x | ||||||

| Norway | x | x | x | x | ||||

| Saint Martin | x | x | x | x | ||||

| Curacao | x | x | x | x | ||||

| Bahamas | x | x | x | x | ||||

| Sweden | x | x | ||||||

| Uruguay | x | |||||||

| Switzerland | x | x | x | x | ||||

| China | x | x | ||||||

| Lithuania | x | x |

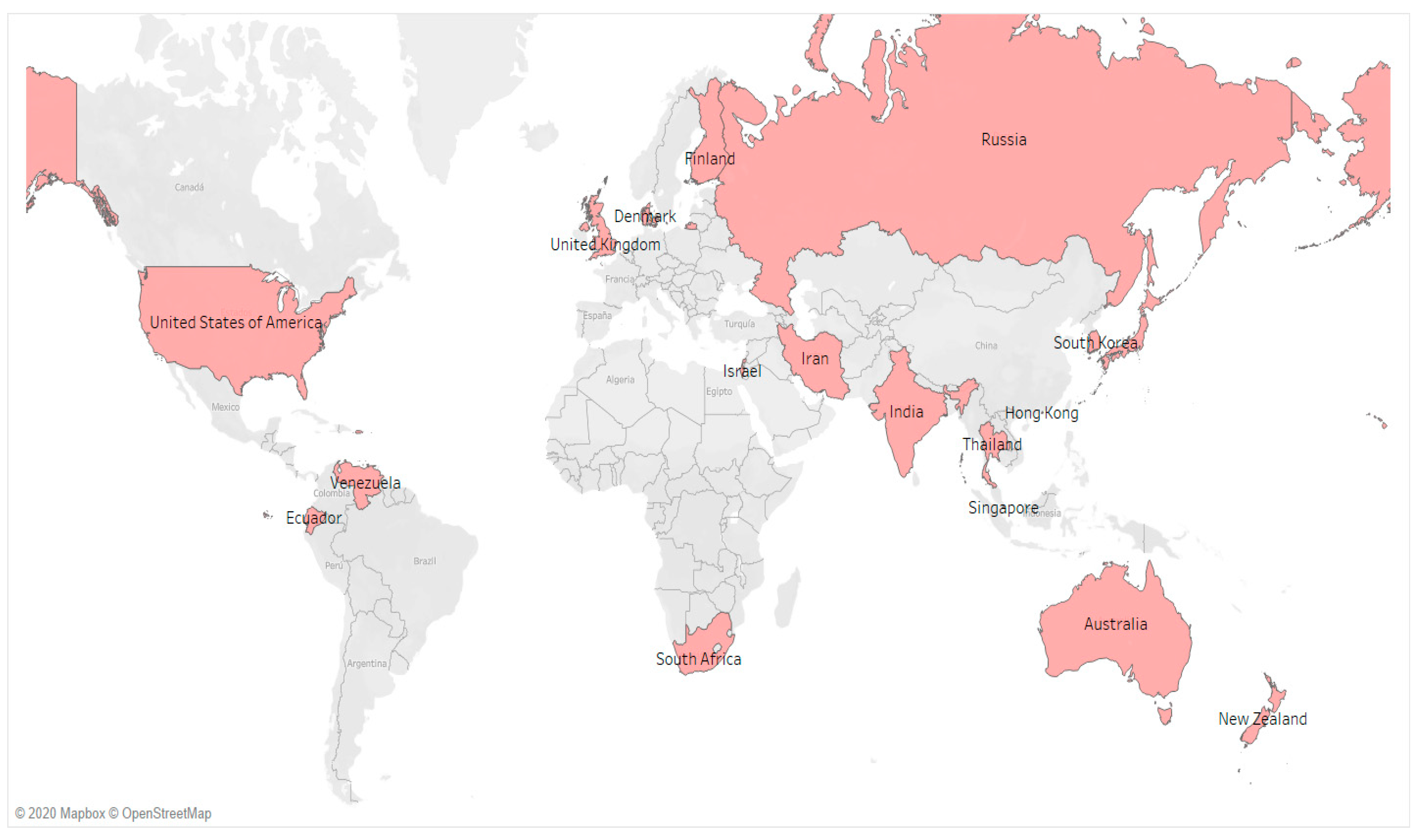

| Country/Reason for Not Establishing CBDC | Preference for Private Virtual Currency | Lack of Demand/Inability to Operate | Failed Test/Need More Security or Investigation | No Advantage Over Electronic Payments |

|---|---|---|---|---|

| Venezuela | x | |||

| Ecuador | x | |||

| Australia | x | |||

| Denmark | x | |||

| Israel | x | |||

| Finland | x | |||

| Hong Kong | x | |||

| Thailand | x | |||

| India | x | |||

| Iran | x | |||

| New Zealand | x | |||

| Japan | x | x | ||

| Russia | x | |||

| Singapore | x | x | ||

| South Africa | x | |||

| South Korea | x | |||

| United States of America | x | x | ||

| United Kingdom | x | x |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Náñez Alonso, S.L.; Echarte Fernández, M.Á.; Sanz Bas, D.; Kaczmarek, J. Reasons Fostering or Discouraging the Implementation of Central Bank-Backed Digital Currency: A Review. Economies 2020, 8, 41. https://doi.org/10.3390/economies8020041

Náñez Alonso SL, Echarte Fernández MÁ, Sanz Bas D, Kaczmarek J. Reasons Fostering or Discouraging the Implementation of Central Bank-Backed Digital Currency: A Review. Economies. 2020; 8(2):41. https://doi.org/10.3390/economies8020041

Chicago/Turabian StyleNáñez Alonso, Sergio Luis, Miguel Ángel Echarte Fernández, David Sanz Bas, and Jarosław Kaczmarek. 2020. "Reasons Fostering or Discouraging the Implementation of Central Bank-Backed Digital Currency: A Review" Economies 8, no. 2: 41. https://doi.org/10.3390/economies8020041

APA StyleNáñez Alonso, S. L., Echarte Fernández, M. Á., Sanz Bas, D., & Kaczmarek, J. (2020). Reasons Fostering or Discouraging the Implementation of Central Bank-Backed Digital Currency: A Review. Economies, 8(2), 41. https://doi.org/10.3390/economies8020041