Understanding German FDI in Latin America and Asia: A Comparison of GLM Estimators

Abstract

1. Introduction

2. Literature Review

2.1. Literature Review on Gravity Model Estimation

2.2. Related Literature

3. Methodology and Data

4. Results

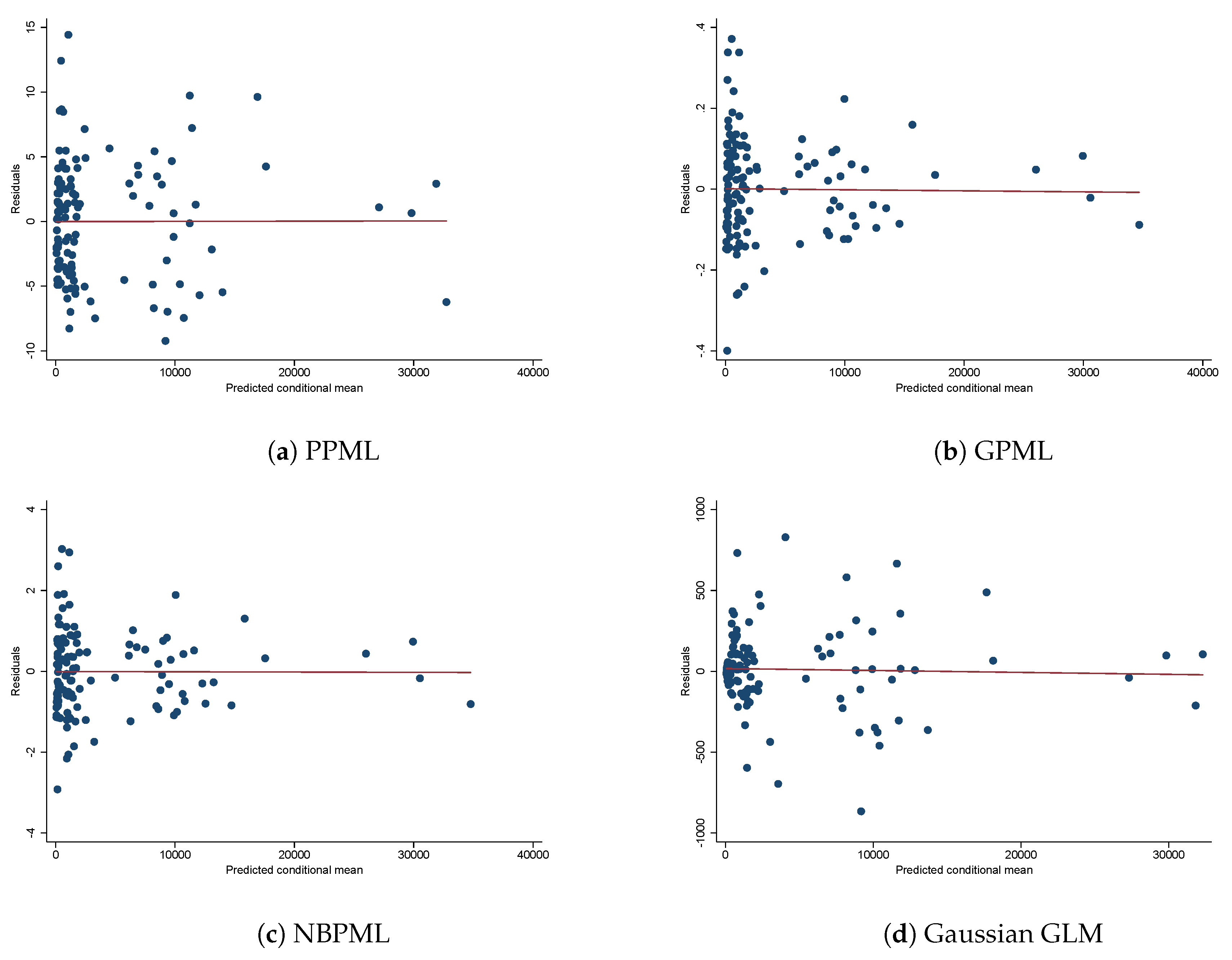

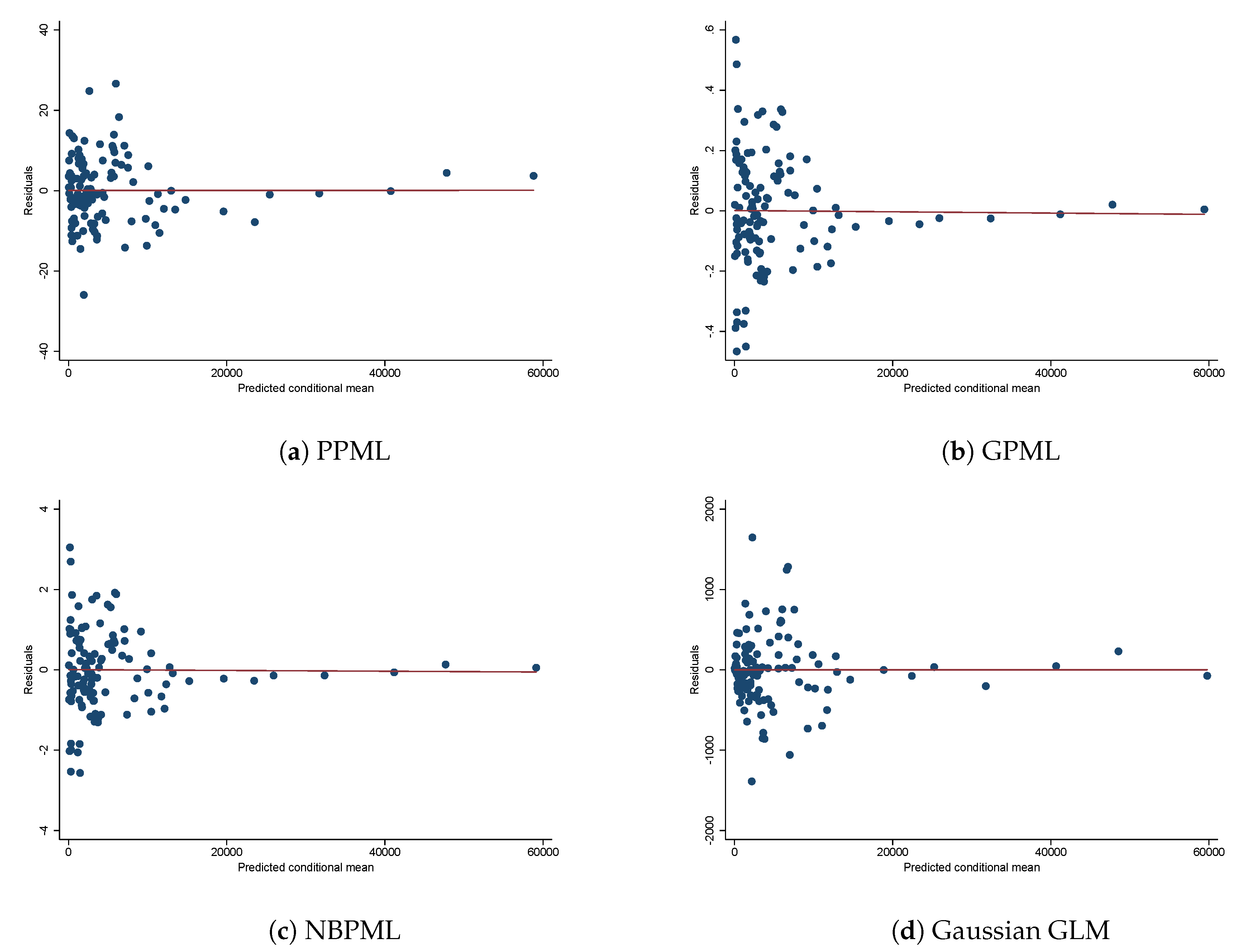

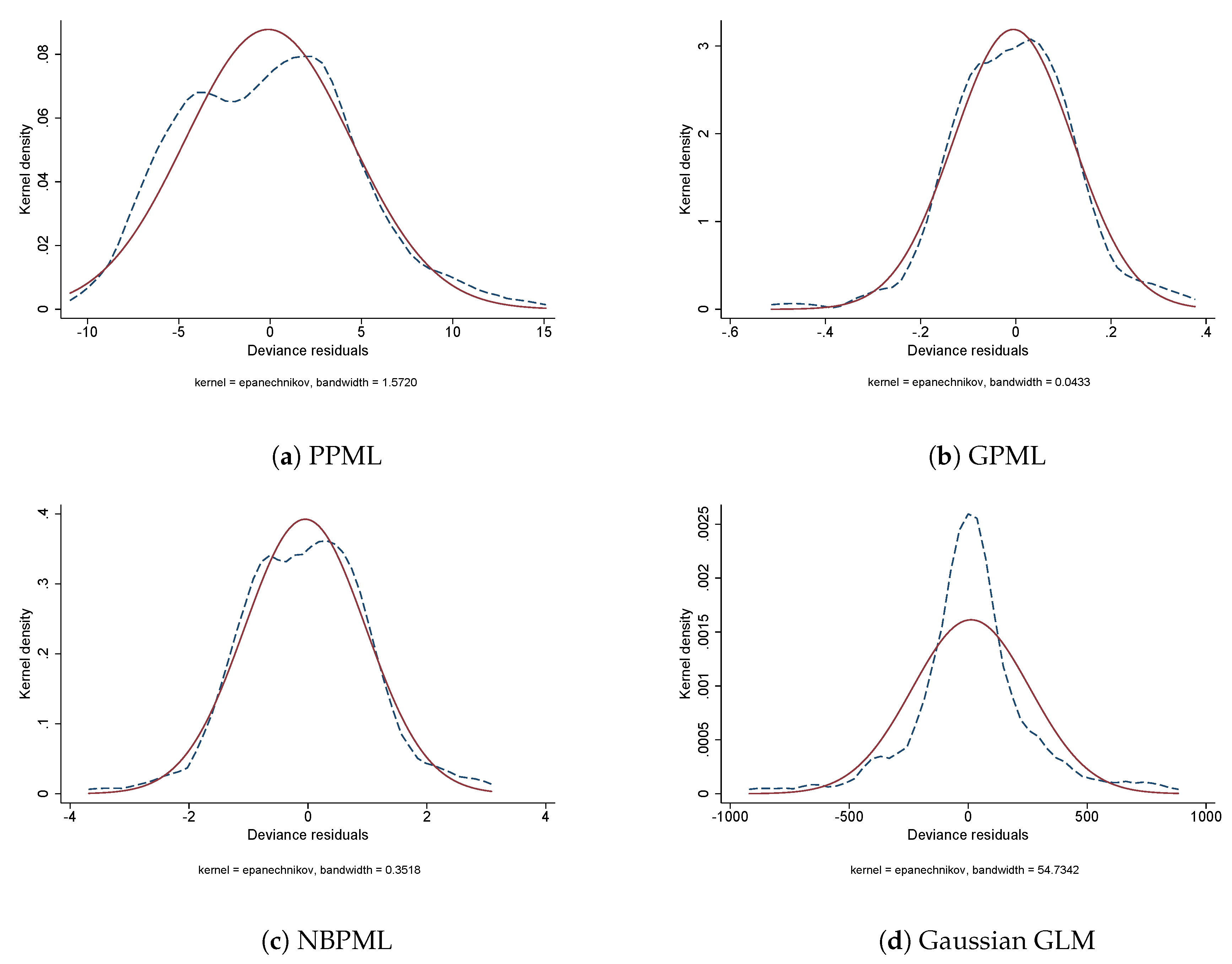

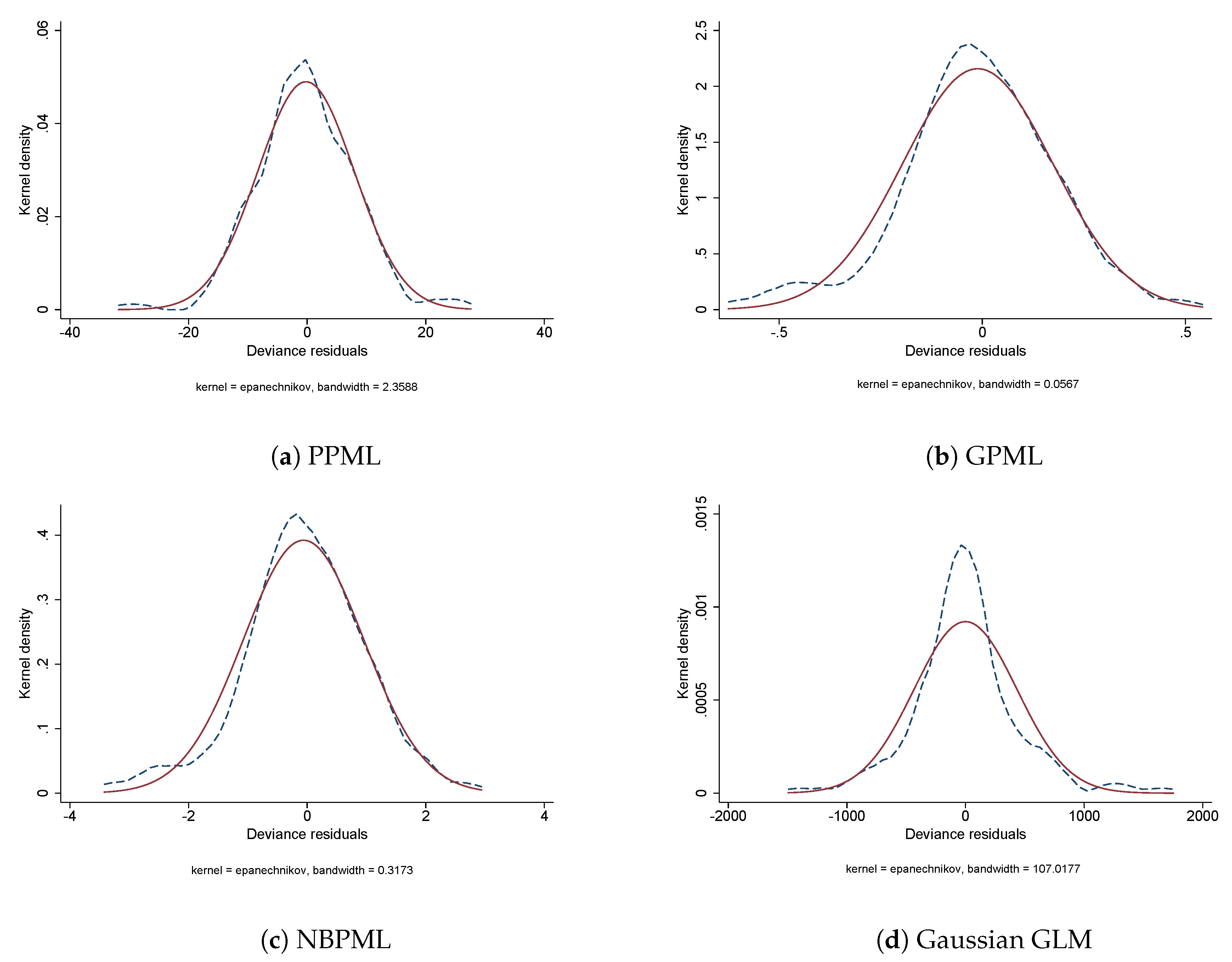

4.1. A Comparison of GLM Estimators

4.2. German FDI in Developing Countries

4.2.1. German FDI in Latin American Countries

4.2.2. German FDI in Asian Countries

5. Conclusions

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Variable Name | Description | Source |

|---|---|---|

| FDI stock | Log of bilateral outward FDI stock in millions (constant 2010 US$) | UNCTADBilateral FDI database |

| GDP and Population Measures | ||

| Sum of HOST and PARENT real GDP | Log of sum of HOST and PARENT real GDP | World Development Indicators, World Bank |

| Similarity of HOST and PARENT real GDP | Log of share of HOST real GDP in the sum of HOST and PARENT GDP * Share of PARENT real GDP in the sum of HOST and PARENT GDP | World Development Indicators, World Bank |

| Squared GDP difference | Log of squared real GDP difference between HOST and PARENT country | World Development Indicators, World Bank |

| HOST population | Log of HOST population, total in mn | Gravity database from CEPII |

| HOST GDP per capita | Log of HOST GDP per capita in trillions (constant 2010 US$) | World Development Indicators, World Bank |

| Distance and other geography measures | ||

| Time zone differences | No. of hours difference between PARENT and HOST | Gravity database from CEPII |

| HOST landlocked | 1 if HOST is landlocked | GeoDistdatabase from CEPII |

| Factor endowments/productivity | ||

| HOST land area | Log of land area (km) in HOST country | Gravity database from CEPII |

| Interaction of GDP differences with skill differences | Log(sq_gdp_diff * sq_skill_diff) | ILOSTAT, World Development Indicators |

| HOST education level | Log of average years of schooling in the population aged 25 years and older, HOST country | PWT 9.0 |

| Exchange Rate/Monetary policy | ||

| Exchange rate | Log of real exchange rate in host country, national currency/USD | PWT9.0 |

| Trade openness | ||

| HOST trade openness | Trade (% of GDP) | World Development Indicators, World Bank |

| Infrastructure | ||

| HOST Internet users | Log of Internet users (per 100 people) in HOST country | World Development Indicators, World Bank |

| HOST telephones | Log of fixed telephone subscriptions (per 100 people) in HOST country | World Development Indicators, World Bank |

| Institutions | ||

| HOST political rights | Political rights index for HOST country (Ranges from 1 to 7 with the highest score indicating the lowest level of freedom) | Freedom House |

| HOST civil liberties | Civil liberties index for HOST country (Ranges from 1 to 7 with highest score indicating the lowest level of freedom) | Freedom House |

| HOST voice and accountability | Voice and accountability, in percentile rank (Ranges from 0 (lowest) to 100 (highest)) | World Governance Indicators (WGI), World Bank |

| HOST Political Stability | Political stability and absence of violence/terrorism, in percentile rank (Ranges from 0 (lowest) to 100 (highest)) | World Governance Indicators (WGI), World Bank |

| Variable | Mean | Std. dev. | Min. | Max. |

|---|---|---|---|---|

| Latin American | ||||

| FDI stock | 4032.01 | 6473.842 | 46.35457 | 32,412.2 |

| Similarity of HOST and PARENT real GDP | −2.19556 | 1.072832 | −4.109496 | −0.7367529 |

| Squared GDP difference | 1.934415 | 0.5549258 | 0.3783011 | 2.514491 |

| HOST population | 3.356185 | 1.255794 | 1.177912 | 5.291575 |

| Interaction of GDP differences with skill differences | −1.163627 | 0.6811084 | −2.618729 | 0.0771762 |

| HOST education level | 2.025653 | 0.153896 | 1.615327 | 2.342417 |

| HOST trade openness | 0.4764379 | 0.1449892 | 0.1563556 | 0.8078977 |

| HOST telephones | 2.829999 | 0.3449711 | 1.935676 | 3.409637 |

| HOST Internet users | 2.162613 | 1.577725 | −2.451535 | 4.008242 |

| HOST political rights | 2.445378 | 1.071175 | 1 | 5 |

| HOST voice and accountability | 56.15861 | 17.81786 | 20.65728 | 89.42308 |

| HOST political stability | 37.21707 | 23.9505 | 1.005025 | 84.65608 |

| Asian | ||||

| FDI stock | 5361.678 | 8878.998 | 54.2917 | 59,695.39 |

| Sum of HOST and PARENT real GDP | 1.397719 | 0.2621594 | 1.072826 | 2.376484 |

| HOST GDP per capita | −19.29271 | 0.9122447 | −21.1438 | −17.58241 |

| HOST education level | 2.051156 | 0.3046183 | 1.306478 | 2.543428 |

| Exchange rate | 4.495245 | 2.540779 | 0.9226475 | 9.248593 |

| HOST Internet users | 1.685045 | 2.103335 | −4.336542 | 4.43165 |

| HOST civil liberties | 3.957983 | 1.317387 | 1.317387 | 7 |

| HOST voice and accountability | 39.80298 | 21.48534 | 4.694836 | 72.11539 |

References

- Adam, Antonis, and Fragkiskos Filippaios. 2007. Foreign direct investment and civil liberties: A new perspective. European Journal of Political Economy 23: 1038–52. [Google Scholar] [CrossRef]

- Antonakakis, Nikolaos, and Gabriele Tondl. 2015. Robust determinants of OECD FDI in developing countries: Insights from bayesian model averaging. Cogent Economics and Finance 3: 1–25. [Google Scholar] [CrossRef]

- Baltagi, Badi H., Peter Egger, and Michael Pfaffermayr. 2007. Estimating models of complex FDI: Are there third-country effects? Journal of Econometrics 140: 260–81. [Google Scholar] [CrossRef]

- Baltagi, Badi H., Peter Egger, and Michael Pfaffermayr. 2014. Panel Data Gravity Models of International Trade. In The Oxford Handbook of Panel Data. Oxford: Oxford University Press, chp. 20, pp. 608–42. [Google Scholar] [CrossRef]

- Basile, Roberto, Davide Castellani, and Antonello Zanfei. 2008. Location choices of multinational firms in Europe: The role of EU cohesion policy. Journal of International Economics 74: 328–40. [Google Scholar] [CrossRef]

- Berden, Koen, Jeffrey H. Bergstrand, and Eva van Etten. 2012. Governance, Globalization, and Selection into Foreign Direct Investment. Available online: http://www3.nd.edu/~jbergstr/Working_Papers/Governance.pdf (accessed on 22 May 2013).

- Bergstrand, Jeffrey H., and Peter Egger. 2007. A knowledge-and-physical-capital model of international trade flows, foreign direct investment, and multinational enterprises. Journal of International Economics 73: 278–308. [Google Scholar] [CrossRef]

- Blonigen, Bruce A., Ronald B. Davies, and Keith Head. 2003. Estimating the Knowledge-Capital Model of the Multinational Enterprise: Comment. American Economic Review 93: 980–94. [Google Scholar] [CrossRef]

- Brainard, S. Lael. 1997. An Empirical Assessment of the Proximity-Concentration Trade-off Between Multinational Sales and Trade. American Economic Review 87: 520–44. [Google Scholar]

- Brenton, Paul, and Francesca Di Mauro. 1999. Economic Integration and FDI: An Empirical Analysis of Foreign Investment in the EU and in Central and Eastern Europe. Empirica 26: 95–121. [Google Scholar] [CrossRef]

- Buch, Claudia, Jörn Kleinert, and Farid Toubal. 2003. Determinants of German FDI: New Evidence from Micro-Data. Discussion Paper 09/03. Frankfurt am Main: Economic Research Centre of the Deutsche Bundesbank. [Google Scholar] [CrossRef]

- Burger, Martijn, Frank Van Oort, and Gert-Jan Linders. 2009. On the specification of the gravity model of trade: Zeros, excess zeros and zero-inflated estimation. Spatial Economic Analysis 4: 167–90. [Google Scholar] [CrossRef]

- Büthe, Tim, and Helen V. Milner. 2008. The politics of foreign direct investment into developing countries: Increasing FDI through international trade agreements? American Journal of Political Science 52: 741–62. [Google Scholar] [CrossRef]

- Camarero, Mariam, Inmaculada Martínez-Zarzoso, Felicitas Nowak-Lehmann D, and Cecilio Tamarit. 2016. Trade Openness and Income: A Tale of Two Regions. World Economy 39: 386–408. [Google Scholar] [CrossRef]

- Camarero, Mariam, Laura Montolio, and Cecilio Tamarit. 2019a. Alternative Estimators for the FDI Gravity Model: An Application to German Outward FDI. Working Papers 1907. Valencia: Department of Applied Economics II, Universidad de Valencia. [Google Scholar]

- Camarero, Mariam, Laura Montolio, and Cecilio Tamarit. 2019b. What drives German foreign direct investment? New evidence using Bayesian statistical techniques. Economic Modelling 83: 326–45. [Google Scholar] [CrossRef]

- Cameron, Colin A., and Pravin K. Trivedi. 2009. Microeconometrics Using Stata. College Station: Stata Press. [Google Scholar]

- Carr, David L., James R. Markusen, and Keith E. Maskus. 2001. Estimating the Knowledge-Capital Model of the Multinational Enterprise. American Economic Review 91: 693–708. [Google Scholar] [CrossRef]

- Cherif, Mondher, and Christian Dreger. 2018. Do regional trade agreements stimulate FDI? Evidence for the Agadir, MERCOSUR and AFTA regions. Review of Development Economics. [Google Scholar] [CrossRef]

- Deininger, Klaus, Derek Byerlee, Jonathan Lindsay, Andrew Norton, Harris Selod, and Mercedes Stickler. 2011. Rising Global Interest in Farmland: Can It Yield Sustainable and Equitable Benefits? Washington: The World Bank. [Google Scholar] [CrossRef]

- Dixon, Jay, and Paul Alexander Haslam. 2015. Does the Quality of Investment Protection Affect FDI Flows to Developing Countries? Evidence from Latin America. World Economy, 1080–108. [Google Scholar] [CrossRef]

- Egger, Peter H., and Kevin E. Staub. 2016. GLM estimation of trade gravity models with fixed effects. Empirical Economics 50: 137–75. [Google Scholar] [CrossRef]

- Faeth, Isabel. 2009. Determinants of foreign direct investment—A tale of nine theoretical models. Journal of Economic Surveys 23: 165–96. [Google Scholar] [CrossRef]

- Gómez-Herrera, Estrella. 2013. Comparing alternative methods to estimate gravity models of bilateral trade. Empirical Economics 44: 1087–111. [Google Scholar] [CrossRef]

- Gutiérrez-Portilla, Paula, Adolfo Maza, and José Villaverde. 2019. Has the crisis affected Spanish investment strategy abroad? A spatial panel data approach. World Economy 42: 1032–56. [Google Scholar] [CrossRef]

- Hauge, Jostein. 2020. Industrial policy in the era of global value chains: Towards a developmentalist perspective drawing on the industrialisation experiences of South Korea and Taiwan. The World Economy, 1–23. [Google Scholar] [CrossRef]

- Head, Keith, and Thierry Mayer. 2014. Gravity Equations: Workhorse, Toolkit, and Cookbook. In Handbook of International Economics. Amsterdam: Elsevier, Volume 4, pp. 131–95. [Google Scholar] [CrossRef]

- Head, Keith, and John Ries. 2008. FDI as an outcome of the market for corporate control: Theory and evidence. Journal of International Economics 74: 2–20. [Google Scholar] [CrossRef]

- Herzer, Dierk, Stephan Klasen, and Felicitas Nowak-Lehmann D. 2008. In search of FDI-led growth in developing countries: The way forward. Economic Modelling 25: 793–810. [Google Scholar] [CrossRef]

- Huang, Chao Hsi, Kai Fang Teng, and Pan Long Tsai. 2010. Inward and outward foreign direct investment and poverty: East Asia vs. Latin America. Review of World Economics 146: 763–79. [Google Scholar] [CrossRef]

- Qamar, Shahzadeh. 2014. A Review of the Economic Applications of the Gravity Model on FDI. International Journal of Applied Research 3: 30–45. [Google Scholar]

- Kleinert, Jörn, and Farid Toubal. 2010. Gravity for FDI. Review of International Economics 18: 1–13. [Google Scholar] [CrossRef]

- Li, Quan, and Adam Resnick. 2003. Reversal of fortunes: Democratic institutions and foreign direct investment inflows to developing countries. International Organization 57: 175–211. [Google Scholar] [CrossRef]

- Li, Quan, and Rafael Reuveny. 2003. Economic globalization and democracy: An empirical analysis. British Journal of Political Science 33: 29–54. [Google Scholar] [CrossRef]

- Liargovas, Panagiotis G., and Konstantinos S. Skandalis. 2012. Foreign Direct Investment and Trade Openness: The Case of Developing Economies. Social Indicators Research 106: 323–31. [Google Scholar] [CrossRef]

- Markusen, James R., and Keith E. Maskus. 2001. Reconciling Theory and Evidence. In Topics in Empirical International Economics: A Festschrift in Honor of Robert E. Lipsey. Chicago: University of Chicago Press, pp. 71–98. [Google Scholar]

- Martin, Will, and Cong S. Pham. 2008. Estimating the Gravity Equation When Zero Trade Flows are Frequent. MPRA Paper 9453. Munich: University Library of Munich. [Google Scholar]

- Martínez-San Román, Valeriano, Marta Bengoa, and Blanca Sánchez-Robles. 2016. Foreign direct investment, trade integration and the home bias: evidence from the European Union. Empirical Economics 50: 197–229. [Google Scholar] [CrossRef]

- Martínez-Zarzoso, Inmaculada. 2013. The log of gravity revisited. Applied Economics 45: 311–27. [Google Scholar] [CrossRef]

- Matyas, Laszlo. 2017. The Econometrics of Multi-Dimensional Panels. Berlin: Springer. [Google Scholar] [CrossRef]

- McCullagh, P., and J.A. Nelder. 1989. Generalized Linear Models, 2nd ed. London: Chapman and Hall. [Google Scholar]

- Ramsey, J.B. 1969. Testing for Specification Errors in Classical Linear Least-Squares Regression Analysis. Journal of the Royal Statistical Society. Series B (Methodological) 31: 350–71. [Google Scholar] [CrossRef]

- Santos Silva, J.M.C., and Silvana Tenreyro. 2006. The log of gravity. The Review of Economics and Statistics 88: 641–58. [Google Scholar] [CrossRef]

- Santos Silva, J.M.C., and Silvana Tenreyro. 2011. Further simulation evidence on the performance of the Poisson pseudo-maximum likelihood estimator. Economics Letters 112: 220–22. [Google Scholar] [CrossRef]

- UNCTAD. 1998. World Investment Report 1998: Trends and Determinants. Geneva: United Nations Publication. [Google Scholar] [CrossRef]

- Wölwer, Anna-Lena, Martin Breßlein, and Jan Pablo Burgard. 2018. Gravity Models in R. Austrian Journal of Statistics 47: 16–35. [Google Scholar] [CrossRef]

- Zhang, Kevin H. 2001. Does Foreign Direct Investment Promote Economic Growth? Evidence from East Asia and Latin America. Contemporary Economic Policy 19: 175–85. [Google Scholar] [CrossRef]

| 1 | Own elaboration based on the UNCTAD’s Bilateral FDI Statistics database. |

| 2 | Notice that the choice of countries was somewhat restricted by the availability of data concerning the large set of potential explanatory variables included in the dataset of Camarero et al. (2019a), the one used in the present study. Furthermore, Argentina is not included in the Latin American countries’ group because German FDI shrank sharply in the year 2000 due to the economic depression that hit the country. |

| 3 | The Tobit estimator assumes dependence among the selection and outcome equations. |

| 4 | The dataset from Camarero et al. (2019) covered bilateral FDI stock between Germany and 59 destination countries from 1996 to 2012. Notice that the dataset was strongly balanced, given the interest of the researchers in addressing the variable selection problem faced in the modelization of FDI. The FDI dataset included 61 explanatory variables and had 1.105 total observations. Due to missing data for some of the explanatory variables, they had to cope with a somewhat limited number of observations. For the purpose of our study, we focused only on a subset of this dataset considering 14 developing destination countries (seven Latin American and seven Asian). Thereby, the total number of observations for each of our subsamples was 119. Despite the potential limitation of the number of observations, we considered that our analysis offered room for policy implications. |

| 5 | UNCTAD FDI statistics incorporate international guidelines in the compilation of FDI data (the IMF’s Balance of Payments and International Investment Position Manual (BPM6) and the fourth edition of OECD’s Benchmark Definition of Foreign Direct Investment (BD4)) to guarantee their quality, yet it might still be somewhat distortive due to differences in corporate accounting practices and valuation methods across countries. |

| 6 | Results remained stable when applying a stepwise backward selection procedure. |

| 7 | An important limitation of these estimations was that by including host country fixed effects, the researcher could no longer estimate those variables with low or no time variability (such as distance, population, or land area, among others), as they were perfectly collinear with the fixed effects (see Baltagi et al. (2014)). Accordingly, we also performed a robustness check by replicating the estimations without host country fixed effects.The findings confirmed that NBPML and GPML were the best performing estimators. Both estimators yielded the same results with similar estimated coefficients and signs. As opposed to the results in Section 4.2.1 and Section 4.2.2, host population, land area, and time zone difference appeared to be significant and with the expected sign for Latin American countries; whereas for Asian countries, landlocked was found to be significant and exerted the expected sign. Results are available upon request. |

| 8 | For readability, we depict the kernel density of deviance residuals (illustrated by the black dashed curve) together with a normal density plot based on the same variance along the lines of Egger and Staub (2016). |

| 9 | Note, however, that Carr et al. (2001) predicted a negative impact of the interaction of skill differences with GDP differences on FDI. Nonetheless, the work in Blonigen et al. (2003) conferred this negative prediction to a misspecification of the skill differences variable used by Carr et al. (2001). Once corrected, the authors confirmed a positive association between the interaction of skill differences with GDP differences and FDI. |

| Destination Countries | ||||

|---|---|---|---|---|

| Developing | ||||

| Latin American | ||||

| Brazil | Colombia | Mexico | Venezuela | |

| Chile | Ecuador | Uruguay | ||

| Asian | ||||

| China | Indonesia | Korea, Republic of | Thailand | |

| India | Kazakhstan | Malaysia |

| GLMs | ||||

|---|---|---|---|---|

| PPML | GPML | NBPML | Gaussian GLM | |

| Similarity of HOST and PARENT real GDP | 1.017 ** | 0.970 *** | 0.915 *** | 2.241 *** |

| (0.42) | (0.37) | (0.34) | (0.60) | |

| Squared GDP difference | −2.277 *** | −2.076 *** | −2.010 *** | −2.501 *** |

| (0.17) | (0.30) | (0.28) | (0.15) | |

| HOST population | −5.424 *** | −5.310 *** | ||

| (1.00) | (1.06) | |||

| Interaction of GDP differences with skill differences | 0.445 *** | 0.488 *** | 0.485 *** | 0.346 *** |

| (0.10) | (0.05) | (0.04) | (0.13) | |

| HOST education level | −2.868 *** | −2.607 *** | −2.406 *** | −3.662 *** |

| (0.42) | (0.83) | (0.77) | (0.37) | |

| HOST trade openness | −2.413 *** | −2.394 *** | −2.402 *** | −2.220 *** |

| (0.26) | (0.24) | (0.26) | (0.21) | |

| HOST telephones | −0.677 *** | −0.713 *** | −0.711 *** | −0.462 *** |

| (0.16) | (0.06) | (0.07) | (0.13) | |

| HOST Internet users | 0.237 *** | 0.390 *** | 0.374 *** | 0.321 *** |

| (0.07) | (0.08) | (0.08) | (0.05) | |

| HOST political rights | 0.159 *** | 0.132 *** | 0.127 *** | 0.246 *** |

| (0.03) | (0.02) | (0.02) | (0.03) | |

| HOST voice and accountability | −0.015 *** | −0.030 *** | −0.029 *** | |

| (0.00) | (0.00) | (0.00) | ||

| HOST political stability | 0.007 *** | 0.007 *** | 0.007 *** | 0.004 *** |

| (0.00) | (0.00) | (0.00) | (0.00) | |

| Host country FE | ||||

| Year FE | ||||

| Observations | 119 | 119 | 119 | 119 |

| test p-values | 0.6125 | 0.0040 | 0.0152 | 0.0000 |

| 29.54138 | 16.37211 | 13.00016 | 13.954 | |

| 1896.413 | −538.1903 | −417.8303 | 7,234,199 | |

| 2436.454031 | 1.85062599 | 122.2106144 | 7,234,738.776 | |

| 21.56154 | 0.0163772 | 1.08151 | 64,024.24 | |

| 0.0185131 | 0.0077757 | 0.010164 | −0.0065372 | |

| 0.0274735 | 0.0158241 | 0.01605 | 0.0415093 | |

| 0.122962 | 0.0977254 | 0.0996833 | 0.1420331 | |

| GLMs | ||||

|---|---|---|---|---|

| PPML | GPML | NBPML | Gaussian GLM | |

| Sum of HOST and PARENT real GDP | 1.763 *** | 1.757 *** | ||

| (0.08) | (0.08) | |||

| HOST GDP per capita | 1.758 *** | 1.928 *** | ||

| (0.17) | (0.14) | |||

| HOST education level | 4.360 *** | 2.820 *** | 2.848 *** | 6.618 *** |

| (0.50) | (0.69) | (0.67) | (0.78) | |

| Exchange rate | −0.502 *** | |||

| (0.10) | ||||

| HOST Internet users | 0.079 *** | 0.080 *** | ||

| (0.03) | (0.03) | |||

| HOST civil liberties | 0.280 ** | 0.277 ** | ||

| (0.11) | (0.12) | |||

| HOST voice and accountability | 0.017 *** | 0.027 *** | 0.027 *** | 0.022 *** |

| (0.00) | (0.01) | (0.01) | (0.01) | |

| Host country FE | ||||

| Year FE | ||||

| Observations | 119 | 119 | 119 | 119 |

| test | 0.1819 | 0.9395 | 0.9422 | 0.9166 |

| 75.4968 | 17.59368 | 14.99792 | 15.07193 | |

| 7293.547 | −535.9904 | −417.5759 | 2.21 | |

| 7833.587578 | 4.050531479 | 122.4650283 | 22,127,650.53 | |

| 69.32378 | 0.0358454 | 1.083761 | 195,819.9 | |

| 0.0119449 | 0.0170187 | 0.0170236 | 0.0123652 | |

| 0.0586087 | 0.0355448 | 0.0355855 | 0.0804531 | |

| 0.1591156 | 0.1410872 | 0.1405214 | 0.1735322 | |

| Latin American | Asian | |

|---|---|---|

| RESET test (5%) | PPML | All of them |

| AIC | NBPML | NBPML |

| BIC | GPML | GPML |

| Deviance | GPML | GPML |

| Dispersion | GPML | GPML |

| Bias | Gaussian GLM | PPML |

| MSE | GPML/NBPML | GPML/NBPML |

| Error loss | GPML/NBPML | NBPML/GPML |

| Pearson residuals | NBPML/GPML | NBPML/GPML |

| Deviance residuals | NBPML/GPML | PPML/NBPML |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Camarero, M.; Montolio, L.; Tamarit, C. Understanding German FDI in Latin America and Asia: A Comparison of GLM Estimators. Economies 2020, 8, 19. https://doi.org/10.3390/economies8010019

Camarero M, Montolio L, Tamarit C. Understanding German FDI in Latin America and Asia: A Comparison of GLM Estimators. Economies. 2020; 8(1):19. https://doi.org/10.3390/economies8010019

Chicago/Turabian StyleCamarero, Mariam, Laura Montolio, and Cecilio Tamarit. 2020. "Understanding German FDI in Latin America and Asia: A Comparison of GLM Estimators" Economies 8, no. 1: 19. https://doi.org/10.3390/economies8010019

APA StyleCamarero, M., Montolio, L., & Tamarit, C. (2020). Understanding German FDI in Latin America and Asia: A Comparison of GLM Estimators. Economies, 8(1), 19. https://doi.org/10.3390/economies8010019