Emerging Countries and the Effects of the Trade War between US and China

Abstract

1. Introduction

2. Methodology

2.1. GTAP Overview

2.2. Regional and Sector Aggregation and Simulations

- (a)

- US additional 25% import duty on steel from China, India, Russia, EU and other countries;

- (b)

- Additional 10% US import tariff on aluminum from China, India, Russia, EU and other countries;

- (c)

- An additional 25% charge on Chinese products listed by the US.

- (a)

- An additional 25% tariff on the US products listed by China.

3. Results

3.1. Production

3.2. Imports, Exports, and Trade Balance

3.3. Welfare

3.4. Sensitivity Analysis

4. Discussion

5. Conclusions

Author Contributions

Funding

Conflicts of Interest

Appendix A

{kind=link}

| GTAP Sector | ESUBD 1 | ESUBM 2 | ESUBVA 3 |

|---|---|---|---|

| Iron & Steel | 2.95 | 5.90 | 1.26 |

| Aluminum | 4.20 | 8.40 | 1.26 |

| Soybeans | 2.45 | 4.90 | 0.26 |

| Primary products | 2.78 | 5.88 | 0.38 |

| Other not industrialized | 4.85 | 11.41 | 0.21 |

| Other industrialized | 3.40 | 7.04 | 1.26 |

| Dairy products | 3.65 | 7.30 | 1.12 |

| Processed Rice | 2.60 | 5.20 | 1.12 |

| Other Food | 2.00 | 4.00 | 1.12 |

| Beverages & Tobacco | 1.15 | 2.30 | 1.12 |

| Petroleum & Coke | 2.10 | 4.20 | 1.26 |

| Chemicals | 3.30 | 6.60 | 1.26 |

| Motor vehicles and parts | 2.80 | 5.60 | 1.26 |

| Other Transport Equipment | 4.30 | 8.60 | 1.26 |

| Electronic Equipment | 4.40 | 8.80 | 1.26 |

| Other Machinery | 4.05 | 8.10 | 1.26 |

| Other Manufacturing | 3.75 | 7.50 | 1.26 |

| Services | 1.94 | 3.85 | 1.36 |

Appendix B

| Initials | Product | Sector Aggregation |

|---|---|---|

| i_s | Ferrous metals | Iron & Steel |

| nfm | Metals nec | Aluminum |

| osd | Oil seeds | Soybeans |

| pdr | Paddy rice | Primary products |

| wht | Wheat | |

| gro | Cereal grains nec | |

| v_f | Vegetables, fruit, nuts | |

| pfb | Plant-based fibers | |

| ocr | Crops nec | |

| oap | Animal products nec | |

| fsh | Fishing | |

| omt | Meat products nec | |

| vol | Vegetable oils and fats | |

| c_b | Sugar cane, sugar beet | Other not industrialized |

| ctl | Cattle, sheep, goats, horses | |

| rmk | Raw milk | |

| wol | Wool, silk-worm cocoons | |

| frs | Forestry | |

| coa | Coal | |

| oil | Oil | |

| gas | Gas | |

| omn | Minerals nec | |

| sgr | Sugar | Other industrialized |

| tex | Textiles | |

| wap | Wearing apparel | |

| lea | Leather products | |

| lum | Wood products | |

| ppp | Paper products, publishing | |

| nmm | Mineral products nec | |

| fmp | Metal products | |

| mil | Dairy products | Dairy products |

| pcr | Processed rice | Processed Rice |

| ofd | Food products nec | Other Food |

| b_t | Beverages and tobacco products | Beverages & Tobacco |

| p_c | Petroleum, coal products | Petroleum & Coke |

| crp | Chemical,rubber,plastic prods | Chemicals |

| mvh | Motor vehicles and parts | Motor vehicles and parts |

| otn | Transport equipment nec | Other Transport Equipment |

| ele | Electronic equipment | Electronic Equipment |

| ome | Machinery and equipment nec | Other Machinery |

| omf | Manufactures nec | Other Manufacturing |

| ely | Electricity | Services |

| gdt | Gas manufacture, distribution | |

| wtr | Water | |

| cns | Construction | |

| trd | Trade | |

| otp | Transport nec | |

| wtp | Sea transport | |

| atp | Air transport | |

| cmn | Communication | |

| ofi | Financial services nec | |

| isr | Insurance | |

| obs | Business services nec | |

| ros | Recreation and other services | |

| osg | PubAdmin/Defence/Health/Educat | |

| dwe | Dwellings |

Appendix C

| N° | GTAP Sector | GTAP Code | GTA Description | OECD Classification | Tariff Increased by US | Tariff Increased by China |

|---|---|---|---|---|---|---|

| 1 | Iron & Steel | 35 | Iron & Steel: basic production and casting | medium-low-technology industries | Yes | No |

| 2 | Aluminum | 36 | Non-Ferrous Metals: production and casting of copper, aluminum, zinc, lead, gold, and silver | medium-low-technology industries | Yes | No |

| 3 | Soybeans | 5 | Oil Seeds: oil seeds and oleaginous fruit; soy beans, copra | Primary products | No | No |

| 4 | Primary products | 1/2/3/4/7/8/10/14/19/20/21 | Not Industrialized products which were target of import tariffs | Primary products | No | Yes |

| 5 | Other not industrialized | 6/9/11/12/13/15/16/17/18 | Not Industrialized products which were not target of import tariffs | Primary products | No | No |

| 6 | Other industrialized | 24/27/28/29/30/31/34/37 | Industrialized products which were not target of import tariffs | low, medium-low and high technology industries | No | No |

| 7 | Dairy products | 22 | Milk: dairy products | low-technology industries | No | Yes |

| 8 | Processed Rice | 23 | Processed Rice: rice, semi- or wholly milled | low-technology industries | No | Yes |

| 9 | Other Food | 25 | Other Food: prepared and preserved fish or vegetables, fruit juices and vegetable juices, prepared and preserved fruit and nuts, all cereal flours, food products n.e.c. | low-technology industries | No | Yes |

| 10 | Beverages & Tobacco | 26 | Beverages and Tobacco products | low-technology industries | No | Yes |

| 11 | Petroleum & Coke | 32 | Petroleum & Coke: coke oven products, refined petroleum products, processing of nuclear fuel | medium-low-technology industries | Yes | No |

| 12 | Chemicals | 33 | Chemical Rubber Products: basic chemicals, other chemical products, rubber and plastics products | medium-high-technology industries | No | No |

| 13 | Motor vehicles and parts | 38 | Motor vehicles and parts: cars, lorries, trailers and semi-trailers | medium-high-technology industries | Yes | Yes |

| 14 | Other Transport Equipment | 39 | Other Transport Equipment: Manufacture of other transport equipment | medium-high-technology industries | Yes | No |

| 15 | Electronic Equipment | 40 | Electronic Equipment: office, accounting and computing machinery, radio, television and communication equipment and apparatus | high-technology industries | Yes | No |

| 16 | Other Machinery | 41 | Other Machinery & Equipment: electrical machinery and apparatus n.e.c., medical, precision and optical instruments, watches and clocks | high-technology industries | Yes | No |

| 17 | Other Manufacturing | 42 | Other Manufacturing: includes recycling | high-technology industries | Yes | No |

| 18 | Services | 43–57 | Services | Services | No | No |

References

- Bollen, Johannes, and Hugo Rojas-Romagosa. 2018. Trade Wars: Economic Impacts of US Tariff Increases and Retaliations. An International Perspective. CPB Netherlands Bureau for Economic Policy Analysis. Available online: https://www.cpb.nl/sites/default/files/omnidownload/CPB-Background-Document-November2018-Trade-Wars-update.pdf (accessed on 20 December 2018).

- Burfisher, Mary E. 2011. Introduction to Computable General Equilibrium Models. Cambridge: Cambridge University Press. [Google Scholar]

- Ciuriak, Dan, and Jingliang Xiao. 2018. Quantifying the Impacts of the US Section 232 Steel and Aluminum Tariffs. C.D. Howe Institute Working Paper. Available online: https://www.cdhowe.org/sites/default/files/attachments/research_papers/mixed/Working%20Paper%200612web.pdf (accessed on 10 December 2018).

- Comtrade. 2018. United Nations Commodity Trade Statistics Database Statistics Division. Available online: http://comtrade.un.org (accessed on 15 June 2018).

- Domingues, Edson P., Eduardo A. Haddad, and Geoffrey Hewings. 2008. Sensitivity analysis in applied general equilibrium models: An empirical assessment for MERCOSUR free trade areas agreements. The Quarterly Review of Economics and Finance 48: 287–306. [Google Scholar] [CrossRef]

- Hertel, Thomas Warren, ed. 1997. Global Trade Analysis: Modeling and Applications. New York: Cambridge University Press. [Google Scholar]

- IMF. 2018. G-20 Surveillance Note, G-20 Finance Ministers and Central Bank Governors’ Meetings. Buenos Aires (Argentina). Available online: https://www.imf.org/external/np/g20/pdf/2018/071818.pdf (accessed on 28 April 2019).

- Li, Chunding, Chuantian He, and Chuangwei Lin. 2018. Economic Impacts of the Possible China-US Trade War. Emerging Markets Finance and Trade 54: 1557–77. [Google Scholar] [CrossRef]

- McDougall, Robert. 1993. Two small extensions to Salter. Salter Working Paper No. 12. Melbourne, Australia: Industry Commission. [Google Scholar]

- MOFCOM. 2018. Ministry of Commerce of the People’s Republic of China. Available online: http://english.mofcom.gov.cn/article/newsrelease/significantnews/201806/20180602757681.shtml (accessed on 30 June 2018).

- Monte, Edson Zambon, and Erly Cardoso Teixeira. 2007. Impactos da Área de Livre Comércio das Américas (Alca), com gradual desgravação tarifária, na economia brasileira. Nova Economia 17: 37–63. [Google Scholar] [CrossRef][Green Version]

- Taheripour, Farzad, and Wallace E. Tyner. 2018. Impacts of Possible Chinese 25% Tariff on U.S. Soybeans and Other Agricultural Commodities. Choices 33: 1–7. Available online: http://www.choicesmagazine.org/choices-magazine/theme-articles/US–China-trade-dispute-and-potential-impacts-to-agriculture/impacts-of-possible-chinese-25-tariff-on-us-soybeans-and-other-agricultural-commodities (accessed on 25 April 2019).

- Tyner, Wallace E., Maksym Chepeliev, and Dominique van der Mensbrugghe. 2018. How U.S. Agriculture Will Fare under the USMCA and Retaliatory Tariffs. GTAP Working Paper No. 84. Oak Brook, IL, USA: Farm Foundation. [Google Scholar]

- USTR. 2018. Office of the United States Trade Representative. Available online: https://ustr.gov/about-us/policy-offices/press-office/press-releases/2018/june/ustr-issues-tariffs-chinese-products (accessed on 30 June 2018).

- Wigle, Randall M. 1991. The Pagan-Shannon approximation: Unconditional systematic sensitivity in minutes. Empirical Economics 16: 35–49. [Google Scholar] [CrossRef]

| 1 | The USTR report (USTR 2018) found that the current quantities of steel and aluminum imports in the circumstances of global overcapacity of these products would be “weakening the domestic economy”, resulting in the persistent threat of further closures of production facilities of domestic steel and aluminum and thereby reducing the ability to meet national security production requirements on a national emergency scale. |

| 2 | In June 2018, the EU followed the same path and reported its retaliatory measures to the WTO. |

| 3 | Primary factors of production comprise capital, skilled and non-skilled labor, which are mobile between commodity groups that maintain invariant prices. Land and natural resources are sluggish. The degree of factor mobility is governed by a constant elasticity of transformation. |

| 4 | The values of the elasticity of substitution between primary factors (ESUBVA), between domestic and imported goods in the Armington aggregation structure (ESUBD) and between imports from different sources (ESUBM) are provided in Appendix A. |

| 5 | The model also includes a global bank that intermediates between global savings and regional investments, selling saving goods to each regional household to satisfy their demand for savings and buying shares in a portfolio of regional investment (Hertel 1997). Savings is an argument in regional household utility function and constrained optimization leads to a demand for homogeneous saving goods, which as any other good depends on income of the household and its relative price. Once the global bank assembled all regional savings, there are two approaches by which the global bank can allocate regional investments. The first, so-called ‘fixed regional composition’ (which is used in all simulations in this paper), assumes that regional composition of global capital stocks is left unaltered in the simulation. Therefore, regional and global investments move together and the rates of return in each region will differ. The second mechanism (rate of return component) is an alternative investment approach, in which the rates of return are the same in all regions. Investment depends on expected rate of return in the next period, which declines as capital stock increases. |

| 6 | The equations were obtained from AnalyseGE, which uses TABmate and ViewHAR written by Mark Horridge and is available from the RunGTAP software. |

| 7 | The higher is the share of region in the countries imports of product i, the higher would be the impact on aggregate prices of imports of this product. |

| 8 | Where qo is output of sector i in country s (% change); SHRDM is the share of domestic sales of sector i in the country s; qds is the domestic sales of i in region s; SHRST is the share of sales of i to global transportation services in s; qst is the sales of sector i to international transport sector; SHRXMD is the share of export sales of product i provided by country r to region s; and qxs are the exports of i from country r to region s (% variation). |

| 9 | The economic impact of the tariff shock is reflected by the change in value of the endogenous variables pms, qxs, qo, qds and pim, comparing its initial value and that obtained in the new equilibrium after the simulation. |

| 10 | The detailed sectoral aggregation, according to the GTAP sectors, and their corresponding OECD classification, is given in Appendix B and Appendix C, respectively. |

| 11 | The results were obtained from RunGTAP, which allows the user to run simulations interactively in a Windows environment using the GTAP general equilibrium model. |

| 12 | The regional household’s EV reflects the difference between the expenditure required to obtain the new level of utility at initial prices (YEV) and that level of utility available at the initial equilibrium (Y), that is to say EV = YEV-Y. According to Burfisher (2011), EV is a money metric measure which compares the cost of pre and post-shock levels of consumer utility, valued at base year prices. As a CGE model has a utility function, it is simple to calculate the utility obtained from different baskets of goods. For example, a tariff reduction in some good would cause a price change that allows the consumer to afford a new basket of goods that increases their utility. The EV measures the change in expenditure that consumers would have to get to afford the new level of utility at pre-shock prices. |

| 13 | The terms of trade (TOT) are defined as the ratio of the price received for tradeables to the price paid for them. McDougall (1993) shows that the change in terms of trade can be decomposed into three terms representing the contribution of world price indexes of all sectors, regional export and import prices. The impact on welfare, derived from the investment-savings component (I-S) depends on price of savings and investment and whether the region is either a net supplier or a net receiver of savings. The regions that are net suppliers of savings to the global bank benefit from an increase in price of savings relative to investment goods, while net receivers lose. |

| 14 | Other studies based on CGE models, such as The International Monetary Fund (IMF 2018), Taheripour and Tyner (2018) and Li et al. (2018), also found that US and China would face losses due to the trade war, in terms of both GDP and welfare. |

| Regional Aggregation | Sectoral Aggregation |

|---|---|

| China | Iron & Steel |

| US | Aluminum |

| Brazil | Soybeans |

| Argentina | Primary products |

| India | Other not industrialized |

| Canada | Other industrialized |

| Russia | Dairy products |

| Mexico | Processed Rice |

| EU | Other Food |

| Other Countries | Beverages & Tobacco |

| Petroleum & Coke | |

| Chemicals | |

| Motor vehicles and parts | |

| Other Transport Equipment | |

| Electronic Equipment | |

| Other Machinery | |

| Other Manufacturing | |

| Services |

| Products | Country Adopting the Measures | Ad Valorem Import Tariff | Countries Targeted |

|---|---|---|---|

| Iron & Steel | US | 25% | China, India, Russia, EU and other countries |

| Aluminum | US | 10% | China, India, Russia, EU and other countries |

| US list with 818 Chinese products | US | 25% | China |

| list of China with 818 Chinese products | China | 25% | US |

| Sectors | China | US | Brazil | Argentina | India | Canada | Russia | Mexico | EU | Other |

|---|---|---|---|---|---|---|---|---|---|---|

| Scenario 1 | ||||||||||

| Iron & Steel | 0.73 | 5.71 | 2.49 | 2.91 | −1.27 | 11.20 | −1.78 | 1.50 | −1.68 | −2.02 |

| Aluminum | 1.11 | 2.88 | 1.00 | 3.58 | −1.24 | 9.26 | −2.36 | 4.22 | −1.32 | −2.10 |

| Soybeans | 1.91 | 0.04 | −0.47 | −0.36 | −0.01 | −1.74 | 0.08 | −2.48 | 0.05 | −0.03 |

| Primary products | 0.62 | 0.04 | −0.35 | −0.46 | −0.04 | −1.49 | 0.09 | −1.51 | 0.00 | −0.06 |

| Other not industrialized | 1.64 | 0.01 | −0.53 | −0.26 | −0.18 | −0.56 | 0.01 | −2.03 | −0.15 | −0.12 |

| Other industrialized | 2.49 | −0.54 | −0.68 | −0.57 | −0.65 | −2.39 | −0.49 | −4.94 | −0.72 | −0.91 |

| Dairy products | 0.03 | 0.01 | 0.09 | −0.13 | 0.07 | −0.03 | 0.09 | −0.52 | 0.05 | −0.02 |

| Processed Rice | 0.36 | −0.07 | −0.06 | −0.26 | 0.04 | −0.09 | 0.15 | −0.68 | 0.02 | 0.03 |

| Other Food | 0.55 | 0.00 | −0.15 | −0.25 | 0.01 | −0.97 | −0.04 | −0.84 | −0.04 | −0.10 |

| Beverages & Tobacco | −0.13 | 0.00 | 0.03 | 0.02 | 0.06 | −0.13 | 0.07 | −0.42 | 0.03 | 0.05 |

| Petroleum & Coke | 0.15 | 0.10 | 0.02 | −0.06 | −0.03 | −0.05 | 0.11 | −1.12 | 0.05 | −0.08 |

| Chemicals | 0.38 | 0.84 | −0.41 | −0.71 | −0.11 | −0.24 | 0.18 | −3.92 | 0.17 | −0.35 |

| Motor vehicles and parts | −0.11 | −0.47 | 0.24 | −0.13 | 0.16 | −0.09 | 0.30 | −4.98 | 0.20 | 0.27 |

| Other Transport Equipment | 1.98 | −1.29 | −0.83 | −0.37 | −0.26 | −3.29 | 0.55 | −4.94 | 0.07 | −0.34 |

| Electronic Equipment | −8.09 | 5.78 | −0.19 | −1.30 | −0.26 | 7.66 | −1.05 | 17.78 | −0.38 | 2.63 |

| Other Machinery | −0.61 | 0.93 | −0.40 | −1.32 | −0.16 | 1.79 | 0.06 | −0.88 | 0.22 | −0.07 |

| Other Manufacturing | −4.07 | 4.11 | 0.23 | 0.05 | 2.54 | 1.08 | 0.17 | 0.46 | 0.59 | 1.86 |

| Services | −0.21 | −0.12 | 0.11 | 0.10 | 0.04 | 0.02 | 0.07 | 0.16 | 0.06 | 0.07 |

| Scenario 2 | ||||||||||

| Iron & Steel | 0.73 | 6.00 | 1.90 | 2.14 | −1.29 | 11.12 | −1.83 | 1.49 | −1.68 | −2.06 |

| Aluminum | 1.12 | 3.40 | −0.28 | 2.17 | −1.28 | 9.26 | −2.48 | 4.31 | −1.36 | −2.17 |

| Soybeans | 6.43 | −13.92 | 9.30 | 4.47 | 0.01 | −0.06 | 0.16 | −4.15 | 0.09 | 0.24 |

| Primary products | 0.81 | −0.21 | −0.95 | −2.13 | 0.03 | −1.58 | 0.11 | −1.63 | 0.09 | 0.02 |

| Other not industrialized | 1.61 | 0.18 | −1.15 | −0.72 | −0.21 | −0.57 | 0.01 | −1.99 | −0.15 | −0.12 |

| Other industrialized | 2.39 | −0.40 | −0.98 | −0.80 | −0.66 | −2.45 | −0.49 | −4.95 | −0.71 | −0.91 |

| Dairy products | 0.36 | −0.27 | 0.13 | −0.24 | 0.06 | −0.03 | 0.09 | −0.52 | 0.06 | 0.04 |

| Processed Rice | 0.28 | 0.19 | −0.14 | −1.16 | 0.04 | 0.04 | 0.18 | −0.68 | 0.03 | 0.04 |

| Other Food | 0.52 | −0.15 | −0.30 | −0.54 | 0.01 | −0.96 | 0.13 | −0.80 | −0.01 | −0.02 |

| Beverages & Tobacco | −0.13 | −0.12 | −0.01 | −0.02 | 0.06 | −0.13 | 0.07 | −0.41 | 0.05 | 0.06 |

| Petroleum & Coke | 0.12 | 0.11 | −0.06 | −0.05 | −0.04 | −0.05 | 0.09 | −1.12 | 0.04 | −0.10 |

| Chemicals | 0.32 | 1.09 | −0.61 | −1.02 | −0.14 | −0.33 | 0.13 | −3.94 | 0.12 | −0.40 |

| Motor vehicles and parts | 0.38 | −1.13 | 0.15 | −0.51 | 0.18 | −0.26 | 0.29 | −5.04 | 0.37 | 0.40 |

| Other Transport Equipment | 1.92 | −0.89 | −1.57 | −0.64 | −0.31 | −3.38 | 0.42 | −4.96 | −0.06 | −0.46 |

| Electronic Equipment | −8.06 | 6.14 | −0.26 | −1.69 | −0.32 | 7.56 | −1.13 | 17.71 | −0.45 | 2.50 |

| Other Machinery | −0.62 | 1.26 | −1.03 | −2.06 | −0.20 | 1.60 | 0.02 | −1.01 | 0.15 | −0.19 |

| Other Manufacturing | −4.11 | 4.41 | 0.24 | 0.07 | 2.47 | 1.06 | 0.14 | 0.46 | 0.55 | 1.81 |

| Services | −0.26 | −0.12 | 0.12 | 0.12 | 0.03 | 0.04 | 0.08 | 0.17 | 0.06 | 0.07 |

| Sectors | US Import Tariffs on China’s Exports (%) | US Import Prices of Product i from China | US imports from China | US Aggregate Prices of Imports | US Aggregate Imports |

|---|---|---|---|---|---|

| Scenario 1 | |||||

| Iron & Steel | 26.03 | 23.23 | −53.62 | 13.21 | −23.48 |

| Aluminum | 13.19 | 8.36 | −30.02 | 4.83 | −7.55 |

| Soybeans | 0.01 | −0.99 | 6.67 | 0.40 | −0.36 |

| Primary products | 1.12 | −1.38 | 10.50 | 0.40 | −0.55 |

| Other not industrialized | 0.31 | −0.36 | 6.41 | 0.16 | 0.22 |

| Other industrialized | 7.57 | −1.51 | 10.28 | −0.36 | 1.61 |

| Dairy products | 5.94 | −1.15 | 10.49 | 0.26 | −0.35 |

| Processed Rice | 4.36 | −1.42 | 9.00 | 0.20 | 0.15 |

| Other Food | 2.76 | −1.48 | 7.07 | 0.29 | −0.30 |

| Beverages & Tobacco | 4.10 | −1.72 | 4.86 | 0.49 | −0.38 |

| Petroleum & Coke | 25.17 | 24.47 | −59.52 | 0.43 | −0.30 |

| Chemicals | 27.75 | 22.56 | −71.56 | 1.85 | −3.55 |

| Motor vehicles and parts | 25.86 | 22.94 | −67.04 | 1.26 | −2.31 |

| Other Transport Equipment | 28.43 | 22.25 | −81.09 | 1.11 | −3.20 |

| Electronic Equipment | 25.25 | 23.10 | −75.05 | 6.78 | −12.78 |

| Other Machinery | 26.47 | 22.76 | −77.31 | 3.27 | −7.99 |

| Other Manufacturing | 26.52 | 22.50 | −70.06 | 5.93 | −10.98 |

| Services | 0.00 | −1.97 | 8.79 | 0.25 | −0.24 |

| Scenario 2 | |||||

| Iron & Steel | 26.03 | 23.25 | −53.59 | 13.28 | −23.67 |

| Aluminum | 13.19 | 8.37 | −29.97 | 4.86 | −7.59 |

| Soybeans | 0.01 | 0.00 | −4.37 | 0.62 | −7.21 |

| Primary products | 1.12 | −0.96 | 6.50 | 0.46 | −2.07 |

| Other not industrialized | 0.31 | −0.33 | 6.16 | 0.19 | 0.05 |

| Other industrialized | 7.57 | −1.45 | 9.68 | −0.32 | 1.17 |

| Dairy products | 5.94 | −1.03 | 9.09 | 0.29 | −0.94 |

| Processed Rice | 4.36 | −0.85 | 5.62 | 0.26 | −0.31 |

| Other Food | 2.76 | −1.06 | 5.05 | 0.37 | −0.82 |

| Beverages & Tobacco | 4.11 | −1.52 | 4.23 | 0.53 | −0.60 |

| Petroleum & Coke | 25.17 | 24.51 | −59.54 | 0.46 | −0.38 |

| Chemicals | 27.75 | 22.62 | −71.70 | 1.88 | −3.85 |

| Motor vehicles and parts | 25.86 | 23.05 | −67.32 | 1.27 | −2.70 |

| Other Transport Equipment | 28.43 | 22.25 | −81.10 | 1.13 | −3.51 |

| Electronic Equipment | 25.25 | 23.10 | −75.08 | 6.80 | −13.00 |

| Other Machinery | 26.47 | 22.76 | −77.37 | 3.29 | −8.36 |

| Other Manufacturing | 26.52 | 22.53 | −70.15 | 5.96 | −11.28 |

| Services | 0.00 | −1.97 | 8.59 | 0.29 | −0.54 |

| Sectors | China’s Import Tariffs on US Exports (%) | China Import Prices of Product i from US | China Imports from US | China Aggregate Prices of Imports | China Aggregate Imports |

|---|---|---|---|---|---|

| Scenario 1 | |||||

| Iron & Steel | 2.29 | 0.83 | −7.20 | 0.25 | −3.95 |

| Aluminum | 0.95 | 1.03 | −11.42 | 0.28 | −5.69 |

| Soybeans | 2.42 | 0.17 | 0.21 | 0.25 | −0.17 |

| Primary products | 6.94 | 0.16 | −3.41 | 0.23 | −3.80 |

| Other not industrialized | 0.25 | 0.17 | −1.71 | 0.10 | −1.00 |

| Other industrialized | 4.26 | 0.28 | −5.45 | 0.23 | −5.12 |

| Dairy products | 6.29 | 0.16 | −4.62 | 0.19 | −4.81 |

| Processed Rice | 1.00 | 0.26 | −4.47 | 0.21 | −4.21 |

| Other Food | 10.82 | 0.15 | −3.10 | 0.21 | −3.34 |

| Beverages & Tobacco | 6.06 | 0.16 | −2.35 | 0.20 | −2.44 |

| Petroleum & Coke | 3.87 | 0.17 | −1.23 | 0.11 | −0.99 |

| Chemicals | 6.05 | 0.28 | −5.27 | 0.20 | −4.77 |

| Motor vehicles and parts | 22.43 | 0.54 | −6.28 | 0.25 | −4.77 |

| Other Transport Equipment | 2.55 | 0.45 | −8.72 | 0.29 | −7.45 |

| Electronic Equipment | 0.72 | 1.41 | −19.26 | 0.20 | −10.25 |

| Other Machinery | 4.83 | 0.53 | −8.82 | 0.22 | −6.47 |

| Other Manufacturing | 14.48 | 0.63 | −10.06 | 0.25 | −7.44 |

| Services | 0.00 | 0.13 | −3.99 | 0.28 | −4.53 |

| Scenario 2 | |||||

| Iron & Steel | 2.29 | 0.73 | −6.56 | 0.27 | −4.00 |

| Aluminum | 0.95 | 0.94 | −10.64 | 0.30 | −5.74 |

| Soybeans | 27.42 | 21.69 | −47.43 | 7.54 | −3.67 |

| Primary products | 31.94 | 22.86 | −67.78 | 3.13 | −9.74 |

| Other not industrialized | 0.25 | 0.12 | −0.80 | 0.15 | −1.03 |

| Other industrialized | 4.26 | 0.18 | −4.55 | 0.26 | −5.06 |

| Dairy products | 31.29 | 23.60 | −78.04 | 1.79 | −9.44 |

| Processed Rice | 26.00 | 24.91 | −69.01 | 0.27 | −2.86 |

| Other Food | 35.82 | 22.51 | −53.73 | 3.09 | −7.71 |

| Beverages & Tobacco | 31.06 | 23.61 | −37.59 | 3.18 | −5.44 |

| Petroleum & Coke | 3.87 | 0.16 | −1.06 | 0.14 | −1.02 |

| Chemicals | 6.05 | 0.18 | −4.50 | 0.21 | −4.69 |

| Motor vehicles and parts | 47.43 | 20.95 | −65.20 | 1.55 | −7.37 |

| Other Transport Equipment | 2.55 | 0.35 | −8.04 | 0.28 | −7.48 |

| Electronic Equipment | 0.72 | 1.32 | −18.53 | 0.22 | −10.30 |

| Other Machinery | 4.83 | 0.43 | −7.98 | 0.23 | −6.54 |

| Other Manufacturing | 14.48 | 0.53 | −9.27 | 0.26 | −7.45 |

| Services | 0.00 | 0.00 | −3.52 | 0.30 | −4.61 |

| Scenario 1 | Scenario 2 | ||

|---|---|---|---|

| China | 7.624 | China | 10.678 |

| US | 48.402 | US | 52.155 |

| Brazil | −4.528 | Brazil | −6.457 |

| Argentina | −0.913 | Argentina | −1.120 |

| India | −1.954 | India | −2.092 |

| Canada | −2.979 | Canada | −3.268 |

| Russia | −1.656 | Russia | −1.864 |

| Mexico | −3.099 | Mexico | −3.231 |

| EU | −19.280 | EU | −21.302 |

| Other | −21.612 | Other | −23.497 |

| Sectors | China | US | Brazil | Argentina | India | Canada | Russia | Mexico | EU | Other |

|---|---|---|---|---|---|---|---|---|---|---|

| Scenario 1 | ||||||||||

| Iron & Steel | 2.388 | 7.820 | 1.729 | 0.146 | −0.948 | 2.821 | −1.084 | 0.771 | −4.647 | −8.473 |

| Aluminum | 6.022 | 1.546 | 0.236 | 0.205 | −0.108 | 3.544 | −0.942 | 1.125 | −2.569 | −8.989 |

| Soybeans | 0.015 | 0.047 | −0.032 | 0.006 | 0.002 | −0.080 | 0.000 | 0.043 | −0.011 | 0.024 |

| Primary products | 2.945 | 0.262 | −0.456 | −0.164 | −0.139 | −0.639 | 0.043 | −0.592 | −0.175 | −0.998 |

| Other not industrialized | 4.104 | −1.446 | −1.049 | −0.074 | −0.442 | −1.615 | 0.419 | −1.414 | −0.323 | 2.368 |

| Other industrialized | 47.152 | −5.526 | −1.808 | −0.229 | −1.552 | −3.928 | −0.423 | −3.916 | −14.521 | −16.894 |

| Dairy products | 0.159 | 0.080 | −0.008 | −0.013 | −0.002 | −0.022 | 0.007 | −0.137 | 0.028 | −0.096 |

| Processed Rice | 0.036 | 0.000 | −0.008 | 0.000 | 0.005 | 0.001 | 0.000 | −0.003 | −0.001 | −0.032 |

| Other Food | 2.020 | 0.149 | −0.074 | −0.043 | −0.017 | −0.369 | −0.035 | −0.535 | −0.342 | −0.841 |

| Beverages & Tobacco | 0.120 | 0.039 | −0.014 | 0.000 | 0.000 | −0.069 | 0.001 | −0.100 | 0.085 | −0.065 |

| Petroleum & Coke | 0.307 | 0.324 | −0.077 | −0.009 | 0.052 | −0.156 | 0.280 | −0.494 | −0.039 | −0.227 |

| Chemicals | 0.290 | 4.648 | −0.563 | −0.146 | 0.090 | 0.162 | 0.199 | −2.122 | 3.206 | −4.556 |

| Motor vehicles and parts | 0.475 | 2.702 | −0.122 | −0.131 | 0.000 | −0.389 | −0.078 | −3.153 | 0.600 | 0.415 |

| Other Transport Equipment | 4.161 | −1.290 | −0.191 | −0.018 | −0.057 | −0.558 | −0.002 | −0.428 | −0.415 | −1.181 |

| Electronic Equipment | −48.810 | 17.819 | −0.452 | −0.045 | −0.031 | 1.223 | −0.069 | 10.430 | −1.308 | 21.695 |

| Other Machinery | −10.158 | 13.149 | −0.848 | −0.164 | −0.257 | 0.601 | −0.234 | −0.399 | 1.993 | −2.645 |

| Other Manufacturing | −15.924 | 6.072 | −0.014 | −0.018 | 2.098 | 0.136 | 0.079 | −0.007 | 2.163 | 6.105 |

| Services | 12.322 | 2.017 | −0.778 | −0.217 | −0.650 | −3.641 | 0.182 | −2.167 | −3.005 | −7.226 |

| Total | 7.624 | 48.412 | −4.528 | −0.913 | −1.955 | −2.979 | −1.656 | −3.099 | −19.281 | −21.616 |

| Scenario 2 | ||||||||||

| Iron & Steel | 2.437 | 8.022 | 1.560 | 0.129 | −0.952 | 2.830 | −1.101 | 0.780 | −4.661 | −8.520 |

| Aluminum | 6.056 | 1.945 | 0.076 | 0.147 | −0.117 | 3.562 | −0.977 | 1.155 | −2.652 | −9.126 |

| Soybeans | 0.570 | −5.388 | 3.241 | 1.225 | 0.001 | 0.100 | 0.000 | 0.096 | −0.028 | 0.361 |

| Primary products | 4.575 | −1.799 | −1.194 | −0.856 | 0.117 | −0.637 | 0.038 | −0.632 | 0.245 | 0.438 |

| Other not industrialized | 4.072 | −0.672 | −1.987 | −0.110 | −0.531 | −1.601 | 0.528 | −1.380 | −0.486 | 2.739 |

| Other industrialized | 46.028 | −3.480 | −2.464 | −0.310 | −1.566 | −4.000 | −0.449 | −3.929 | −14.353 | −17.035 |

| Dairy products | 0.273 | −0.136 | −0.015 | −0.025 | −0.002 | −0.022 | 0.005 | −0.140 | 0.057 | 0.012 |

| Processed Rice | 0.024 | 0.013 | −0.016 | −0.003 | 0.007 | 0.001 | 0.000 | −0.003 | −0.001 | −0.027 |

| Other Food | 2.050 | −0.452 | −0.134 | −0.070 | −0.012 | −0.366 | 0.042 | −0.527 | −0.187 | −0.385 |

| Beverages & Tobacco | 0.221 | −0.099 | −0.030 | −0.004 | 0.000 | −0.071 | 0.000 | −0.102 | 0.142 | −0.052 |

| Petroleum & Coke | 0.314 | 0.534 | −0.121 | −0.023 | 0.053 | −0.156 | 0.277 | −0.494 | −0.111 | −0.324 |

| Chemicals | −0.148 | 6.986 | −1.110 | −0.272 | 0.047 | 0.101 | 0.158 | −2.109 | 2.603 | −5.063 |

| Motor vehicles and parts | 1.798 | −0.227 | −0.320 | −0.214 | 0.002 | −0.512 | −0.103 | −3.208 | 2.013 | 1.122 |

| Other Transport Equipment | 4.202 | −0.415 | −0.327 | −0.030 | −0.070 | −0.574 | −0.021 | −0.431 | −0.790 | −1.520 |

| Electronic Equipment | −48.517 | 19.123 | −0.651 | −0.065 | −0.050 | 1.202 | −0.084 | 10.387 | −1.603 | 20.714 |

| Other Machinery | −9.726 | 16.800 | −1.568 | −0.243 | −0.316 | 0.502 | −0.329 | −0.503 | 0.700 | −4.276 |

| Other Manufacturing | −15.945 | 6.496 | −0.047 | −0.024 | 2.053 | 0.127 | 0.070 | −0.009 | 2.047 | 5.924 |

| Services | 12.395 | 4.912 | −1.349 | −0.371 | −0.756 | −3.750 | 0.081 | −2.183 | −4.241 | −8.483 |

| Total | 10.678 | 52.162 | −6.457 | −1.120 | −2.092 | −3.268 | −1.864 | −3.233 | −21.306 | −23.501 |

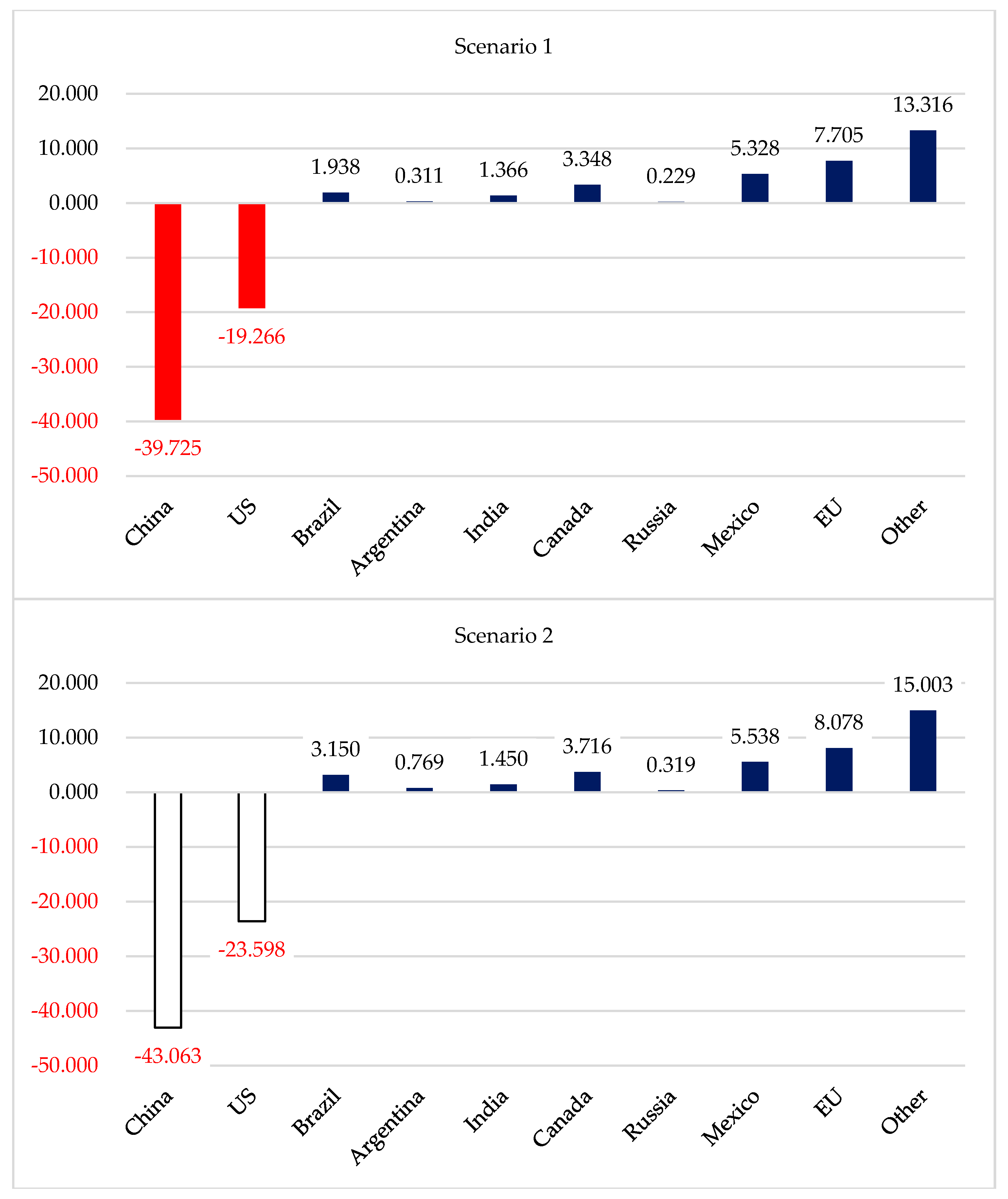

| Regions | Allocative Effects | Terms of Trade Effect | I-S Effect | Total |

|---|---|---|---|---|

| Scenario 1 | ||||

| China | −7.778 | −34.326 | 2.380 | −39.725 |

| US | −26.580 | 3.052 | 4.265 | −19.263 |

| Brazil | 1.025 | 1.071 | −0.158 | 1.938 |

| Argentina | 0.130 | 0.285 | −0.103 | 0.311 |

| India | 0.439 | 1.082 | −0.155 | 1.366 |

| Canada | 0.886 | 2.734 | −0.272 | 3.348 |

| Russia | 0.178 | 0.369 | −0.318 | 0.229 |

| Mexico | 0.276 | 5.727 | −0.675 | 5.328 |

| EU | 2.282 | 6.400 | −0.977 | 7.705 |

| Other | 4.070 | 13.202 | −3.956 | 13.316 |

| Total | −25.072 | −0.404 | 0.030 | −25.446 |

| Scenario 2 | ||||

| China | −11.812 | −33.975 | 2.724 | −43.063 |

| US | −26.423 | −0.504 | 3.332 | −23.595 |

| Brazil | 1.209 | 2.089 | −0.147 | 3.150 |

| Argentina | 0.226 | 0.673 | −0.130 | 0.769 |

| India | 0.435 | 1.118 | −0.103 | 1.450 |

| Canada | 0.928 | 3.029 | −0.242 | 3.716 |

| Russia | 0.195 | 0.433 | −0.308 | 0.319 |

| Mexico | 0.276 | 5.907 | −0.645 | 5.538 |

| EU | 2.197 | 6.719 | −0.837 | 8.078 |

| Other | 4.505 | 14.105 | −3.607 | 15.003 |

| Total | −28.263 | −0.406 | 0.036 | −28.634 |

| Sectors | China | US | Brazil | Argentina | India | Canada | Russia | Mexico | EU | Other | Total |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Scenario 1 | |||||||||||

| Iron & Steel | 0.018 | −1.583 | 0.098 | −0.029 | −0.095 | 0.032 | −0.055 | 0.009 | −0.118 | −0.173 | −1.897 |

| Aluminum | 0.040 | −0.673 | 0.013 | −0.038 | −0.040 | 0.046 | −0.055 | 0.021 | −0.062 | −0.077 | −0.824 |

| Soybeans | −0.003 | 0.000 | 0.001 | −0.004 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.049 | 0.043 |

| Primary products | −0.258 | −0.004 | 0.012 | −0.003 | 0.014 | 0.007 | −0.013 | 0.022 | 0.007 | 0.047 | −0.169 |

| Other not industrialized | 0.050 | 0.003 | −0.016 | −0.007 | −0.009 | −0.004 | 0.049 | −0.688 | −0.004 | −0.066 | −0.692 |

| Other industrialized | 3.501 | 0.718 | 0.110 | 0.029 | 0.020 | 0.143 | 0.076 | 0.175 | 0.491 | 1.471 | 6.734 |

| Dairy products | −0.038 | −0.001 | 0.004 | 0.002 | 0.002 | 0.023 | 0.000 | 0.015 | 0.016 | 0.009 | 0.033 |

| Processed Rice | −0.004 | 0.000 | 0.000 | 0.000 | −0.003 | 0.000 | 0.000 | 0.000 | 0.000 | 0.006 | 0.000 |

| Other Food | −0.129 | −0.002 | 0.010 | 0.001 | 0.003 | 0.020 | 0.003 | 0.029 | 0.040 | 0.138 | 0.114 |

| Beverages & Tobacco | −0.117 | −0.024 | 0.010 | 0.004 | 0.005 | 0.069 | 0.000 | 0.033 | 0.047 | 0.078 | 0.105 |

| Petroleum & Coke | −0.119 | −0.007 | 0.037 | 0.002 | 0.000 | 0.086 | 0.044 | 0.050 | 0.359 | −0.106 | 0.345 |

| Chemicals | −0.911 | −2.740 | 0.056 | 0.002 | 0.063 | 0.032 | 0.015 | 0.055 | 0.285 | 0.145 | −2.998 |

| Motor vehicles and parts | −1.319 | −0.842 | 0.134 | 0.033 | 0.041 | 0.067 | −0.007 | 0.083 | 0.163 | 0.326 | −1.321 |

| Other Transport Equipment | −0.173 | −0.388 | 0.015 | 0.011 | 0.038 | 0.008 | 0.008 | 0.021 | 0.039 | 0.255 | −0.165 |

| Electronic Equipment | −1.866 | −10.480 | 0.116 | 0.016 | 0.030 | 0.030 | 0.005 | 0.119 | 0.088 | 0.411 | −11.531 |

| Other Machinery | −3.544 | −6.858 | 0.237 | 0.036 | 0.221 | 0.046 | 0.065 | 0.129 | 0.427 | 0.484 | −8.756 |

| Other Manufacturing | −0.654 | −3.047 | 0.040 | 0.008 | 0.134 | 0.030 | 0.014 | 0.061 | 0.239 | 0.192 | −2.983 |

| Services | −2.070 | −0.663 | 0.136 | 0.067 | 0.013 | 0.221 | 0.031 | 0.085 | 0.277 | 0.768 | −1.134 |

| Total | −7.778 | −26.593 | 1.025 | 0.130 | 0.439 | 0.886 | 0.178 | 0.276 | 2.283 | 4.070 | −25.085 |

| Scenario 2 | |||||||||||

| Iron & Steel | 0.018 | −1.577 | 0.088 | −0.021 | −0.095 | 0.032 | −0.056 | 0.008 | −0.118 | −0.176 | −1.897 |

| Aluminum | 0.040 | −0.664 | 0.006 | −0.022 | −0.042 | 0.046 | −0.057 | 0.021 | −0.062 | −0.081 | −0.814 |

| Soybeans | −0.816 | 0.013 | −0.014 | 0.046 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.092 | −0.679 |

| Primary products | −1.158 | −0.010 | 0.014 | −0.037 | 0.015 | 0.019 | −0.008 | 0.019 | −0.017 | 0.439 | −0.725 |

| Other not industrialized | 0.041 | 0.041 | −0.036 | −0.019 | −0.010 | −0.005 | 0.052 | −0.675 | −0.005 | −0.069 | −0.684 |

| Other industrialized | 3.339 | 0.615 | 0.123 | 0.032 | 0.017 | 0.137 | 0.072 | 0.168 | 0.473 | 1.439 | 6.417 |

| Dairy products | −0.091 | −0.005 | 0.006 | 0.003 | 0.002 | 0.025 | 0.000 | 0.014 | 0.015 | 0.013 | −0.017 |

| Processed Rice | −0.004 | 0.000 | 0.000 | −0.001 | −0.003 | 0.000 | 0.000 | 0.000 | 0.000 | 0.013 | 0.005 |

| Other Food | −0.390 | −0.013 | 0.012 | 0.001 | 0.003 | 0.024 | 0.003 | 0.028 | 0.034 | 0.123 | −0.175 |

| Beverages & Tobacco | −0.169 | −0.034 | 0.016 | 0.007 | 0.005 | 0.074 | 0.000 | 0.034 | 0.051 | 0.082 | 0.067 |

| Petroleum & Coke | −0.143 | −0.042 | 0.054 | 0.009 | −0.004 | 0.088 | 0.040 | 0.051 | 0.318 | −0.117 | 0.252 |

| Chemicals | −0.919 | −2.710 | 0.067 | 0.004 | 0.059 | 0.032 | 0.015 | 0.054 | 0.263 | 0.141 | −2.994 |

| Motor vehicles and parts | −2.484 | −0.899 | 0.176 | 0.044 | 0.043 | 0.069 | −0.002 | 0.080 | 0.267 | 0.363 | −2.343 |

| Other Transport Equipment | −0.182 | −0.383 | 0.015 | 0.013 | 0.040 | 0.008 | 0.009 | 0.020 | 0.036 | 0.251 | −0.173 |

| Electronic Equipment | −1.885 | −10.478 | 0.157 | 0.019 | 0.030 | 0.031 | 0.006 | 0.119 | 0.073 | 0.404 | −11.524 |

| Other Machinery | −3.632 | −6.842 | 0.308 | 0.044 | 0.227 | 0.047 | 0.071 | 0.125 | 0.407 | 0.490 | −8.755 |

| Other Manufacturing | −0.661 | −3.061 | 0.052 | 0.010 | 0.133 | 0.030 | 0.014 | 0.061 | 0.235 | 0.193 | −2.993 |

| Services | −2.310 | −0.639 | 0.178 | 0.095 | 0.014 | 0.243 | 0.038 | 0.089 | 0.286 | 0.830 | −1.177 |

| Total | −11.812 | −26.437 | 1.209 | 0.226 | 0.435 | 0.928 | 0.195 | 0.276 | 2.197 | 4.505 | −28.276 |

| Sectors | China | US | Brazil | Argentina | India | Canada | Russia | Mexico | EU | Other | Total |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Scenario 1 | |||||||||||

| Iron & Steel | −0.723 | 0.095 | 0.053 | 0.002 | 0.034 | 0.032 | 0.006 | 0.081 | 0.089 | 0.336 | 0.004 |

| Aluminum | −0.514 | 0.171 | 0.022 | 0.013 | −0.028 | 0.198 | −0.001 | 0.284 | −0.192 | 0.077 | 0.029 |

| Soybeans | −0.092 | 0.019 | 0.051 | 0.012 | 0.002 | 0.033 | −0.001 | −0.007 | −0.014 | −0.021 | −0.018 |

| Primary products | −0.387 | −0.043 | 0.130 | 0.078 | 0.014 | 0.138 | −0.021 | 0.120 | −0.048 | 0.067 | 0.047 |

| Other not industrialized | −0.210 | −0.154 | 0.094 | 0.005 | −0.018 | 0.185 | 0.010 | 0.170 | −0.122 | 0.134 | 0.095 |

| Other industrialized | −9.229 | 0.931 | 0.243 | 0.034 | 0.218 | 0.461 | 0.204 | 0.478 | 2.003 | 4.095 | −0.563 |

| Dairy products | −0.007 | 0.001 | −0.001 | 0.006 | 0.000 | 0.002 | −0.003 | 0.000 | 0.011 | −0.009 | −0.001 |

| Processed Rice | −0.005 | 0.002 | 0.002 | 0.001 | 0.008 | 0.000 | 0.000 | 0.000 | −0.001 | −0.008 | −0.001 |

| Other Food | −0.590 | −0.041 | 0.022 | 0.020 | 0.014 | 0.097 | 0.006 | 0.129 | 0.071 | 0.313 | 0.042 |

| Beverages & Tobacco | −0.033 | −0.044 | 0.006 | 0.005 | 0.001 | 0.007 | −0.003 | 0.074 | 0.031 | −0.008 | 0.036 |

| Petroleum & Coke | −0.210 | 0.036 | −0.001 | 0.000 | 0.036 | 0.037 | 0.004 | 0.042 | −0.031 | 0.106 | 0.019 |

| Chemicals | −2.936 | 0.264 | 0.050 | 0.022 | 0.162 | 0.323 | 0.013 | 0.286 | 0.526 | 1.251 | −0.039 |

| Motor vehicles and parts | −0.786 | −0.324 | −0.002 | −0.028 | 0.017 | 0.116 | −0.021 | 1.138 | 0.121 | 0.194 | 0.425 |

| Other Transport Equipment | −0.796 | 0.204 | 0.012 | 0.006 | 0.022 | 0.098 | −0.002 | 0.062 | 0.072 | 0.299 | −0.023 |

| Electronic Equipment | −6.314 | 1.117 | 0.092 | 0.021 | 0.133 | 0.058 | 0.103 | 1.182 | 1.214 | 1.982 | −0.412 |

| Other Machinery | −6.239 | 0.736 | 0.161 | 0.026 | 0.171 | 0.126 | 0.086 | 1.179 | 1.248 | 2.434 | −0.072 |

| Other Manufacturing | −1.590 | 0.271 | 0.020 | 0.009 | 0.079 | 0.051 | 0.032 | 0.060 | 0.497 | 0.425 | −0.147 |

| Services | −3.665 | −0.188 | 0.117 | 0.053 | 0.216 | 0.774 | −0.044 | 0.451 | 0.925 | 1.536 | 0.175 |

| Total | −34.328 | 3.053 | 1.071 | 0.285 | 1.083 | 2.734 | 0.369 | 5.729 | 6.400 | 13.202 | −0.403 |

| Scenario 2 | |||||||||||

| Iron & Steel | −0.730 | −0.103 | 0.085 | 0.003 | 0.034 | 0.038 | 0.009 | 0.084 | 0.089 | 0.343 | −0.148 |

| Aluminum | −0.517 | −0.218 | 0.041 | 0.020 | −0.030 | 0.196 | 0.002 | 0.284 | −0.182 | 0.099 | −0.305 |

| Soybeans | −0.102 | 0.740 | 0.335 | 0.118 | 0.004 | 0.055 | −0.003 | 0.048 | −0.018 | 0.097 | 1.274 |

| Primary products | −0.301 | 0.861 | 0.320 | 0.275 | 0.021 | 0.191 | −0.037 | 0.179 | −0.132 | 0.162 | 1.540 |

| Other not industrialized | −0.314 | 0.337 | 0.201 | 0.008 | −0.032 | 0.187 | 0.040 | 0.169 | −0.200 | 0.216 | 0.613 |

| Other industrialized | −8.992 | −1.331 | 0.340 | 0.035 | 0.220 | 0.483 | 0.209 | 0.491 | 1.957 | 4.006 | −2.582 |

| Dairy products | −0.007 | 0.006 | −0.002 | 0.009 | 0.000 | 0.002 | −0.003 | 0.002 | 0.012 | −0.009 | 0.010 |

| Processed Rice | −0.003 | 0.001 | 0.004 | 0.002 | 0.010 | 0.000 | 0.000 | 0.000 | −0.001 | −0.011 | 0.000 |

| Other Food | −0.437 | 0.192 | 0.037 | 0.036 | 0.018 | 0.108 | 0.002 | 0.129 | 0.048 | 0.238 | 0.371 |

| Beverages & Tobacco | −0.030 | 0.104 | 0.013 | 0.010 | 0.001 | 0.010 | −0.004 | 0.073 | 0.037 | −0.010 | 0.205 |

| Petroleum & Coke | −0.210 | 0.017 | 0.006 | 0.002 | 0.044 | 0.041 | 0.012 | 0.049 | −0.027 | 0.121 | 0.055 |

| Chemicals | −2.867 | 0.009 | 0.099 | 0.032 | 0.164 | 0.356 | 0.017 | 0.317 | 0.601 | 1.325 | 0.053 |

| Motor vehicles and parts | −0.745 | 0.740 | 0.023 | −0.033 | 0.017 | 0.153 | −0.024 | 1.134 | 0.136 | 0.206 | 1.608 |

| Other Transport Equipment | −0.797 | −0.197 | 0.027 | 0.006 | 0.023 | 0.104 | −0.001 | 0.062 | 0.113 | 0.353 | −0.307 |

| Electronic Equipment | −6.374 | −1.815 | 0.098 | 0.021 | 0.135 | 0.065 | 0.114 | 1.174 | 1.248 | 2.082 | −3.253 |

| Other Machinery | −6.275 | −0.736 | 0.212 | 0.027 | 0.175 | 0.178 | 0.100 | 1.198 | 1.351 | 2.632 | −1.139 |

| Other Manufacturing | −1.583 | −0.420 | 0.022 | 0.009 | 0.083 | 0.054 | 0.035 | 0.061 | 0.506 | 0.436 | −0.798 |

| Services | −3.693 | 1.311 | 0.227 | 0.092 | 0.231 | 0.810 | −0.034 | 0.456 | 1.181 | 1.819 | 2.400 |

| Total | −33.977 | −0.504 | 2.089 | 0.674 | 1.118 | 3.030 | 0.433 | 5.909 | 6.719 | 14.106 | −0.404 |

| Region | Scenario 1 | Scenario 2 | ||||||

|---|---|---|---|---|---|---|---|---|

| Mean | Standard Deviation | 93.75 Confidence Interval | Mean | Standard Deviation | 93.75 Confidence Interval | |||

| China | −39.394 | 2.887 | −50.942 | −27.846 | −42.703 | 2.828 | −54.014 | −31.392 |

| US | −19.066 | 0.533 | −21.197 | −16.936 | −23.403 | 0.685 | −26.144 | −20.661 |

| Brazil | 1.957 | 0.183 | 1.227 | 2.687 | 3.177 | 0.297 | 1.988 | 4.365 |

| Argentina | 0.317 | 0.043 | 0.146 | 0.487 | 0.779 | 0.103 | 0.367 | 1.191 |

| India | 1.357 | 0.143 | 0.786 | 1.927 | 1.441 | 0.145 | 0.861 | 2.021 |

| Canada | 3.354 | 0.340 | 1.996 | 4.713 | 3.723 | 0.368 | 2.252 | 5.194 |

| Russia | 0.234 | 0.059 | −0.002 | 0.469 | 0.325 | 0.068 | 0.054 | 0.596 |

| Mexico | 5.288 | 0.304 | 4.071 | 6.505 | 5.499 | 0.318 | 4.228 | 6.769 |

| EU | 7.658 | 0.616 | 5.194 | 10.122 | 8.036 | 0.665 | 5.378 | 10.694 |

| Other Countries | 13.249 | 1.033 | 9.116 | 17.382 | 14.944 | 1.151 | 10.340 | 19.549 |

| Total | −25.046 | 6.140 | −49.606 | −0.486 | −28.182 | 6.627 | −54.690 | −1.674 |

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Carvalho, M.; Azevedo, A.; Massuquetti, A. Emerging Countries and the Effects of the Trade War between US and China. Economies 2019, 7, 45. https://doi.org/10.3390/economies7020045

Carvalho M, Azevedo A, Massuquetti A. Emerging Countries and the Effects of the Trade War between US and China. Economies. 2019; 7(2):45. https://doi.org/10.3390/economies7020045

Chicago/Turabian StyleCarvalho, Monique, André Azevedo, and Angélica Massuquetti. 2019. "Emerging Countries and the Effects of the Trade War between US and China" Economies 7, no. 2: 45. https://doi.org/10.3390/economies7020045

APA StyleCarvalho, M., Azevedo, A., & Massuquetti, A. (2019). Emerging Countries and the Effects of the Trade War between US and China. Economies, 7(2), 45. https://doi.org/10.3390/economies7020045