Financial Risk and Financial Performance: Evidence and Insights from Commercial and Services Listed Companies in Nairobi Securities Exchange, Kenya

Abstract

1. Introduction

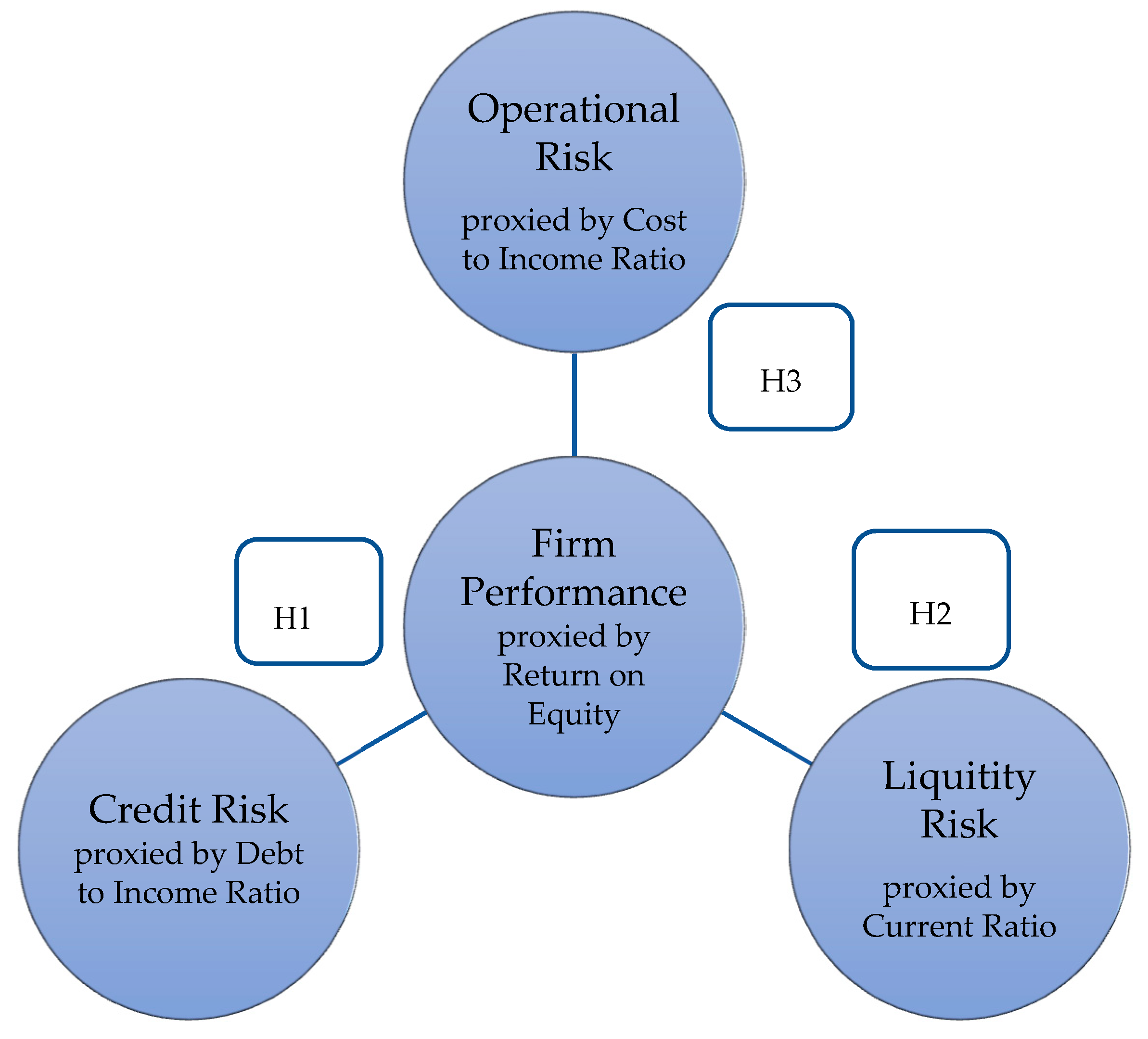

- To determine the effect of credit risks on the performance of commercial and services companies on NSE, Kenya;

- To establish the effect of liquidity risks on the performance of commercial and services companies on NSE, Kenya;

- To examine the effect of operational risks on the performance of commercial and services companies on NSE, Kenya.

2. Literature Review

3. Materials and Methods.

3.1. Target Population

3.2. Sampling Design

3.3. Research Data and Variable Construction

Total assets

income

Current liabilities

Total income

3.4. Data Analysis Method

Diagnostic Tests

4. Results

4.1. Descriptive Statistics

4.2. Hypotheses Testing Results

5. Discussion

6. Conclusions

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

References

- Agarwal, Anuj. 2011. Credit risk Management: Trends and Opportunities. Available online: http://www.capgemini.com/resources/credit-risk-management-trends-and-opportunities/ (accessed on 26 May 2017).

- Aglionby, John. 2016. Kenya Airways records country’s worst ever loss. The Financial Times. Available online: https://www.ft.com (accessed on 26 May 2017).

- Agustina, Linda, and Niswah Baroroh. 2016. The Relationship Between Enterprise Risk Management (ERM) and Firm Value Mediated Through the Financial Performance. Integrative Business and Economics Research 5: 128–38. [Google Scholar]

- Aiken, Leona S., Stephen G. West, and Raymond R. Reno. 1991. Multiple Regression: Testing and Interpreting Interactions. Newbury Park: Sage. [Google Scholar]

- Akerlof, George. 1970. The Market for “lemons”: Quality Uncertainty and the Market Mechanism. The Quarterly Journal of Economics 84: 488–500. [Google Scholar] [CrossRef]

- Andrade, Galdino, and Steven N. Kaplan. 1997. How Costly is Financial (Not Economic) Distress? Evidence from Highly Leveraged Transactions that Became Distressed. The Journal of Finance 53: 33–43. [Google Scholar]

- Arif, Ahmad, and Ahmad Showket. 2015. Relationship between financial risk and financial performance: An Insight of Indian Insurance Industry. International Journal of Science and Research 4: 1424–33. [Google Scholar]

- Armstrong, John. 2017. What Is a Commercial Company? Main Characteristics. Available online: https://www.lifepersona.com/what-is-a-commercial-company-main-characteristics (accessed on 20 January 2018).

- Auronen, Lauri. 2003. Asymmetric Information: Theory and Applications. Seminar of Strategy and International Business 116: 45–56. [Google Scholar]

- Bandalos, Deborah L. 2018. Measurement Theory and Applications for the Social Sciences. New York: The Guilford Press. [Google Scholar]

- Bansal, Arun, Robert Kaufmann, Robert Mark, and Edward Peters. 1992. Financial Risk and Financial Risk Management Technology: Issues and Advantages. Working Papers Series; New York: New York University. [Google Scholar]

- Bwire, E. 2015. Why Uchumi Collapsed and What Lessons We Can Learn from It. Available online: https://www.linkedin.com/pulse/why-uchumi-collapsed-what-les-sons-we-can-learn-from-egesa-bwire/ (accessed on 29 January 2017).

- Capgemini and Merrill Lynch Global Wealth Management. 2009. Firms Can Act to Rebuild Shaken Investor Confidence Through more Holistic Risk Management. World Wealth Report 1: 27–29. [Google Scholar]

- CMA (Capital Markets Authority). 2016. Capital Markets Soundness Report (Kenya): Mar-ket Resilience in a Persistent Bear Run. Available online: https://www.cma.or.ke (accessed on 12 May 2017).

- Collier, Paul M., and Sam Agyei-Ampomah. 2006. Management Accounting: Risk and Control Strategy. Oxford: Elsevier. [Google Scholar]

- Dey, Ripon Kumar, Syed Zabid Hossain, and Zabihollah Rezaee. 2018. Financial Risk Disclosure and Financial Attributes among Publicly Traded Manufacturing Companies: Evidence from Bangladesh. Journal of Risk and Financial Management 11: 50. [Google Scholar] [CrossRef]

- Elder, Jim. 2016. Emerging Credit Risks in 2016. Available online: https://www.spglobal.com/marketintelligence/en/news-insights/blog/emerging-credit-risks-in-2016 (accessed on 21 June 2017).

- Erasmus, Petrus Daniel. 2008. Evaluating Value Based Financial Performance Measures. Journal of Finance 6: 93–117. [Google Scholar]

- Fali, Ibrahim, Terzungwe Nyor, and Olumide Lateef Mustapha. 2020. Financial Risk and Financial Performance of listed Insurance Companies in Nigeria. European Journal of Business and Management 12: 143–53. [Google Scholar]

- Fama, Eugene. 1980. Agency Problems and the Theory of the Firm. Journal of Political Economy 88: 288–307. [Google Scholar] [CrossRef]

- Gentry, James, and John Pike. 1970. An Empirical Study of the Risk-Return Hypothesis Using Common Stock Portfolios of Life Insurance Companies. The Journal of Financial and Quantitative Analysis 5: 179–85. [Google Scholar] [CrossRef]

- Grant, Cynthia, and Azadeh Osanloo. 2014. Understanding, selecting, and integrating a theoretical framework in dissertation research: Creating the blueprint for your “house”. Administrative Issues Journal 4: 12–26. [Google Scholar] [CrossRef]

- Gujarati, Damodar. 2003. Basic Econometrics, 4th ed. New York: McGraw Hill. [Google Scholar]

- Harvey, Jasmin. 2008. Financial Risk Management, 47th ed. London: The Chartered Institute of Management Accountants. [Google Scholar]

- Holton, Glyn A. 2004. Defining risk. Financial Analysts Journal 60: 19–25. [Google Scholar] [CrossRef]

- Isiaka, Lasisi Olalekan. 2018. Effect of Liquidity Risk, Premium Growth on the Performance of Quoted Insurance Firms in Nigeria: A Panel Data Analysis. American Finance & Banking Review 2: 40–89. [Google Scholar]

- Jensen, Michael C., and William H. Meckling. 1976. Theory of the Firm: Managerial Behavior, Agency Costs and Ownership Structure. Journal of Financial Economics 3: 305–60. [Google Scholar] [CrossRef]

- Kamau, Faith, and Agnes Njeru. 2016. Effect of Liquidity Risk on Financial Performance of liquidity risk has no significant effect on return on asset. International Journal of Science and Research 5: 867–72. [Google Scholar]

- Kangethe, Kennedy. 2015. Atlas Development Closes its Kenyan Subsidiaries. Available online: https://www.capitalfm.co.ke/business (accessed on 26 November 2018).

- Kaplan, Steven N., and Jeremy C. Stein. 1993. The Evolution of Buyout Pricing and Financial Structure in the 1980s. Quarterly Journal of Economics 108: 313–57. [Google Scholar] [CrossRef]

- Kenya Airways. 2016. Annual Report & Financial Statements. Available online: https://www.kenya-airways.com (accessed on 26 November 2018).

- Kihooto, Elijah, Job Omagwa, Muturi Wachira, and Ronald Emojong. 2016. Financial Distress in Commercial and Services Companies Listed at Nairobi Securities Exchange, Kenya. European Journal of Business and Management 8: 27–48. [Google Scholar]

- Kinyua, John K., Roselyn Gakure, Mouni Gekara, and George Orwa. 2015. Effect of Risk Management on The Financial Performance Of Companies Quoted In The Nairobi Securities Exchange. International Journal of Business & Law Research 3: 26–42. [Google Scholar]

- KPMG. 2018. Retail Trends. Available online: https://home.kpmg.com/xx/en/home/insights/2018/03/2018-retail-trends.html (accessed on 3 January 2019).

- Longhorn Publishers. 2018. Investors Segment. Available online: https://longhornpublishers.com/ke/ (accessed on 28 December 2018).

- Maigua, Cecilia, and Gekara Mouni. 2016. Influence of Interest Rates Determinants on the Performance of Commercial Banks in Kenya. International Journal of Academic Research in Accounting, Finance and Management Sciences 6: 121–33. [Google Scholar] [CrossRef]

- Mathuva, David. M. 2009. Capital adequacy, cost income ratio and the performance of commercial banks: The Kenyan Scenario. The International Journal of Applied Economics and Finance 3: 35–47. [Google Scholar] [CrossRef]

- Muathe, Stephen. M. A. 2010. The Determinants of Adoption of Information and Com-munication Technology by Small and Medium Enterprises within the Health Sector in Nairobi, Kenya. Ph.D. dissertation, Kenyatta University, Nairobi, Kenya. [Google Scholar]

- Mugenda, Olive M., and Abel G. Mugenda. 2003. Research Methods: Quantitative and Qualitative Approaches. Nairobi: Acts Press. [Google Scholar]

- Munda, Constant. 2017. Hutchings Biemer and A. Baumann delisted from Nairobi bourse. Business Daily. Available online: https://www.businessdailyafrica.com (accessed on 28 November 2018).

- Muriithi, Jane Gathiga. 2016. The Effect of Financial Risk on Financial Performance of Commercial Banks in Kenya. Ph.D. dissertation, Jomo Kenyatta University of Agriculture and Technology, Juja, Kenya. [Google Scholar]

- Musau, Salome Mwongeli. 2018. Financial Inclusion and Stability of Commercial Banks In Kenya. Ph.D. dissertation, Kenyatta University, Nairobi, Kenya. [Google Scholar]

- Mutegi, Mugambi. 2017. Seven NSE-listed firms issue profit warnings on politicking. Business Daily. Available online: https://www.businessdailyafrica.com (accessed on 28 December 2018).

- Mutua, Rosemary Kasyoka. 2016. Impact of Credit risk Management on Financial Performance of Savings and Credit Co-Operative Societies in Kitui County. Master’s thesis, South Eastern Kenya University, Kitui, Kenya. [Google Scholar]

- Mwangi, Lucy Wamugo, Muathe Stephen Makau, and George Kosimbei. 2014. Relationship between Capital Structure and Performance of Nonfinancial Companies Listed in the Nairobi Securities Exchange, Kenya. Global Journal of Contemporary Research in Accounting, Auditing and Business Ethics 1: 72–90. [Google Scholar]

- NSE. 2013. Nairobi Securities Exchange Handbook 2012–2013. Available online: https://www.nse.co.ke (accessed on 13 July 2018).

- NSE. 2014. Nairobi Securities Exchange Handbook 2013–2014. Available online: https://www.nse.co.ke (accessed on 13 July 2018).

- NSE. 2015. Nairobi Securities Exchange Handbook 2014–2015. Available online: https://www.nse.co.ke (accessed on 14 July 2018).

- NSE. 2016. Nairobi Securities Exchange Handbook 2015–2016. Available online: https://www.nse.co.ke (accessed on 17 July 2018).

- NSE. 2017. Listed Companies. Available online: https://www.nse.co.ke/listed-companies/list.html (accessed on 18 July 2018).

- Nyasaka, Fredrick. 2017. The Relationship between Credit Risk Management Practices and Non- Performing Loans in Kenyan Commercial Banks: A Case Study of KCB Group Limited. Master’s thesis, United States International University—Africa, Nairobi, Kenya. Unpublished. [Google Scholar]

- Okoth, Edwin, and Vincent Achuka. 2016. Concerns raised about overall health of Kenya’s economy. Daily Nation. Available online: https://www.nation.co.ke/ (accessed on 3 June 2017).

- Oliver, Barry Rose. 2001. Issues in Financial Risk Management in Australia. Ph.D. thesis, Australian National University, Canberra, Australia. [Google Scholar]

- Omasete, Catherine. 2014. The Effect of Risk Management on Financial Performance of Insurance Companies in Kenya. Master’s thesis, University of Nairobi, Nairobi, Kenya. Unpublished. [Google Scholar]

- Park, Hun Myoung. 2011. Practical Guides to Panel Data Modeling: A Step-by-step Analysis Using Stata. Tutorial Working Paper. Niigata: Graduate School of International Relations, International University of Japan. [Google Scholar]

- Pearson, Robin. 2002. Moral Hazard and the Assessment of the Insurance Risk in the Eighteenth and Early—Nineteenth-century Britain. Business History Review 76: 1–35. [Google Scholar] [CrossRef]

- Saunders, Mark, Philip Lewis, and Adrian Thornhill. 2009. Research Methods for Business Students. New York: Pearson. [Google Scholar]

- Sisay, Daniel. 2017. The Effect of Financial Risk on Performance of Insurance Companies in Ethiopia. Ph.D. thesis, Addis Ababa University, Addis Ababa, Ethiopia. Unpublished. [Google Scholar]

- Spence, Michael. 2002. Signaling in retrospect and the informational structure of markets. American Economic Review 92: 434–59. [Google Scholar] [CrossRef]

- Stulz, Rene. 1996. Rethinking Risk Management. Journal of Applied Corporate Finance 9: 8–24. [Google Scholar] [CrossRef]

- Wang, Baolian. 2013. The cash conversion cycle spread. Journal of Financial Economics 133: 472–97. [Google Scholar] [CrossRef]

- Wangalwa, Matayo, and Willy Muturi. 2018. Effect of Financial Risk on Financial Performance of Large-Scale Supermarkets in Nairobi County, Kenya. International Journal of Social Science and Technology 4: 574–91. [Google Scholar]

- Wani, Ahmad, and Showket Ahmad. 2013. The Effect of Hedging on Firm Value and Performance: Evidence from the Nonfinancial UK Firms. Hull: Hull University Business School. [Google Scholar]

- Were, Simon. 2015. The Effect of Foreign Exchange Rate Risk Management Practices on Financial Performance of Multinational Corporations in Kenya. Master’s thesis, University of Nairobi, Nairobi, Kenya. [Google Scholar]

- Whitaker, Richard. B. 1999. The Early Stages of Financial Distress. Journal of Economics and Finance 23: 123–33. [Google Scholar] [CrossRef]

- Witkin, Belle Ruth, and James W. Altschuld. 1996. Planning and Conducting Need Assessments: A Practical Guide. New York: Sage Publications, Inc. 302p, ISBN 0-8039-5809-9. First published 1995. [Google Scholar] [CrossRef]

- Woods, Margaret, and Kevin Dowd. 2008. Financial Risk Management for Management Accountants. Oxford: Elsevier. [Google Scholar]

- Wooldridge, Jeffrey M. 2010. Econometric Analysis of Cross Section and Panel Data. Cambridge: MIT Press. [Google Scholar]

- Wruck, Karen Hopper. 1990. Financial distress, reorganization, and organizational efficiency. Journal of Financial Economics 27: 419–44. [Google Scholar] [CrossRef]

- Yan, Qicheng, and Chen Wei. 2017. Jack Ma & Alibaba: A Business and Life Biography. Shanghai: LID Publishing. [Google Scholar]

{kind=link}

| Sector\Year | 2013 | 2014 | 2015 | 2016 | 2017 |

|---|---|---|---|---|---|

| Agricultural | 18% | 27% | |||

| Automobiles & accessories | 9% | 6% | |||

| Banking | 14% | 6% | 9% | 25% | |

| Commercial & services | 43% | 55% | 39% | 18% | 25% |

| Construction & allied | 9% | 17% | 8% | ||

| Energy & petroleum | 14% | ||||

| Insurance | 17% | 18% | 8% | ||

| Investment | 6% | 9% | |||

| Investment services | 9% | ||||

| Manufacturing & allied | 29% | 9% | 11% | 9% | 33% |

| Telecommunication & technology | |||||

| Real estate investment trust | |||||

| Exchange traded fund | |||||

| Total firms issuing profit warnings per year | 7 | 11 | 18 | 11 | 12 |

| Company | Business | |

|---|---|---|

| 1 | Atlas Development and Support services | Logistics |

| 2 | Deacons (East Africa) Plc | Consumer goods |

| 3 | Eveready East Africa Limited | Power solutions |

| 4 | Express Limited | Logistics |

| 5 | Hutchings Biemer Limited | Furniture |

| 6 | Kenya Airways Limited | Transport |

| 7 | Longhorn Publishers Limited | Publishing |

| 8 | Nairobi Business Ventures Limited | Consumer goods |

| 9 | Nation Media Group | Media |

| 10 | Sameer Africa Limited | Tires |

| 11 | Standard Group Limited | Media |

| 12 | TPS Eastern Africa (Serena) Limited | Hospitality |

| 13 | Uchumi Supermarket Limited | Consumer goods |

| 14 | WPP Scangroup Limited | Marketing |

| Company | Year | ROE | Credit Risk | Liquidity Risk | Operational Risk |

|---|---|---|---|---|---|

| 1 | 2013 | 0.402342428 | 0.730440915 | 0.369036126 | 53.78240048 |

| 1 | 2014 | 0.369222029 | 0.657554119 | 0.52078737 | 40.31125172 |

| 1 | 2015 | 0.385771092 | 0.664435484 | 0.505037018 | 48.03727018 |

| 1 | 2016 | 0.318407754 | 0.557662768 | 0.79319843 | 50.60535204 |

| 1 | 2017 | 0.42481122 | 0.618833564 | 0.615943377 | 449.4766839 |

| 2 | 2013 | 0.148235428 | 0.490333986 | 1.039426246 | 2.52400779 |

| 2 | 2014 | 0.147679642 | 0.538317435 | 0.857640001 | 2.753707269 |

| 2 | 2015 | 0.210804587 | 0.431069649 | 1.319810734 | 2.418759701 |

| 2 | 2016 | 0.129799036 | 0.471311355 | 1.121739671 | 1.152987134 |

| 2 | 2017 | 0.017673087 | 0.462388778 | 1.162682242 | 0.430164698 |

| 3 | 2013 | 0.435148118 | 0.720312473 | 0.388286387 | 234.4509804 |

| 3 | 2014 | 0.413316454 | 0.734082366 | 0.362244956 | 312.4137931 |

| 3 | 2015 | 0.315310989 | 0.705198989 | 0.41803947 | 340.1445783 |

| 3 | 2016 | 0.282664399 | 0.714870093 | 0.398855554 | 1171.428571 |

| 3 | 2017 | 0.245379457 | 0.782659766 | 0.339406597 | 1169 |

| 4 | 2013 | 0.125841379 | 0.637219959 | 0.569316821 | 51.80165619 |

| 4 | 2014 | 0.106791105 | 0.643071674 | 0.555036616 | 39.26812156 |

| 4 | 2015 | 0.101725308 | 0.690080963 | 0.449105327 | 43.72856715 |

| 4 | 2016 | 0.082410574 | 0.653149863 | 0.531042196 | 62.86697844 |

| 4 | 2017 | 0.077680007 | 0.651589602 | 0.534708344 | 400.9291883 |

| 5 | 2013 | 0.088218144 | 0.679332505 | 0.472033199 | 5.485090315 |

| 5 | 2014 | 0.075139287 | 0.746994532 | 0.338697885 | 4.731330467 |

| 5 | 2015 | 0.056940838 | 0.612384514 | 0.632960953 | 1.549113074 |

| 5 | 2016 | 0.102830752 | 0.563243021 | 0.775432562 | 5.342617537 |

| 5 | 2017 | 0.028451483 | 0.617555019 | 0.619289138 | 1.890005146 |

| 6 | 2013 | 0.375796261 | 0.563292405 | 0.77527691 | 911.9937107 |

| 6 | 2014 | 0.338980475 | 0.577124186 | 0.732844446 | 189.7242268 |

| 6 | 2015 | 0.254788658 | 0.551816283 | 0.812197341 | 11.53349994 |

| 6 | 2016 | 0.146983802 | 0.507549771 | 0.970250125 | 5.570634349 |

| 6 | 2017 | 0.189432022 | 0.508790392 | 0.965445921 | 3.409141944 |

| 7 | 2013 | −0.346887116 | 0.25436037 | 2.931430036 | −5.676979549 |

| 7 | 2014 | −0.172198803 | 0.190364396 | 4.263629601 | −2.005363036 |

| 7 | 2015 | 4.982726815 | −0.032752399 | −31.53211471 | −6.276299113 |

| 7 | 2016 | 0.731740825 | −0.225149134 | −5.441500547 | −3.703561799 |

| 7 | 2017 | 0.227140154 | −0.307333862 | −4.431904709 | −1.380140693 |

| 8 | 2013 | 0.151883611 | 0.420382524 | 1.37878585 | 1.432592169 |

| 8 | 2014 | −1.13526318 | 0.234892055 | 3.257274687 | −4.390931785 |

| 8 | 2015 | −0.236494654 | 0.511689577 | 0.954309886 | −3.210953508 |

| 8 | 2016 | −0.450003905 | 0.449367661 | 1.225349276 | −3.025674331 |

| 8 | 2017 | 0.453490362 | 0.711018673 | 0.406432823 | 25.58987264 |

| 9 | 2013 | −0.008540881 | 0.413123158 | 1.420585681 | −0.211573149 |

| 9 | 2014 | −0.424151373 | 0.407803795 | 1.452159623 | −5.398431139 |

| 9 | 2015 | −0.630488885 | 0.251336229 | 2.978733997 | −4.503713639 |

| 9 | 2016 | −4.789888528 | 0.061285076 | 15.3171862 | −6.639507143 |

| 9 | 2017 | 10.80163809 | −0.009244429 | −109.173254 | −5.280334827 |

| 10 | 2013 | 0.166096946 | 0.524875694 | 0.905213009 | 30.25164986 |

| 10 | 2014 | 0.13485453 | 0.487637717 | 1.050702734 | 7.00416151 |

| 10 | 2015 | −4.751525316 | 0.117316112 | 7.523978332 | −10.46009278 |

| 10 | 2016 | 1.273732381 | −0.419289571 | −3.384986581 | −41.3288521 |

| 10 | 2017 | 0.491537747 | −0.782171992 | −2.426215729 | −4.953631638 |

| Variable | Mean | Std. Deviation. | Min | Max |

|---|---|---|---|---|

| ROE | 0.0254313 | 0.251435 | −0.567095 | 1.156945 |

| Credit risk | 0.0434844 | 0.330613 | −0.782172 | 0.782659 |

| Liquidity risk | −1.827569 | 16.39814 | −109.1733 | 15.31719 |

| Operational risk | 0.5475728 | 0.247773 | 0.0683761 | 1.48148 |

| ROE | Coefficient | Standard Error | z | p > |z| |

|---|---|---|---|---|

| Credit risk | 0.5807289 | 0.3695323 | 1.57 | 0.123 |

| Liquidity risk | −0.112057 | 0.0074164 | −15.11 | 0.000 |

| Operational risk | 0.5542459 | 0.4765494 | 1.16 | 0.251 |

| _cons | −0.503449 | 0.3168256 | −1.59 | 0.119 |

| F statistics = 78.57 Prob > chi2 = 0.0000 | ||||

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Onsongo, S.K.; Muathe, S.M.A.; Mwangi, L.W. Financial Risk and Financial Performance: Evidence and Insights from Commercial and Services Listed Companies in Nairobi Securities Exchange, Kenya. Int. J. Financial Stud. 2020, 8, 51. https://doi.org/10.3390/ijfs8030051

Onsongo SK, Muathe SMA, Mwangi LW. Financial Risk and Financial Performance: Evidence and Insights from Commercial and Services Listed Companies in Nairobi Securities Exchange, Kenya. International Journal of Financial Studies. 2020; 8(3):51. https://doi.org/10.3390/ijfs8030051

Chicago/Turabian StyleOnsongo, Susan Kerubo, Stephen M. A. Muathe, and Lucy Wamugo Mwangi. 2020. "Financial Risk and Financial Performance: Evidence and Insights from Commercial and Services Listed Companies in Nairobi Securities Exchange, Kenya" International Journal of Financial Studies 8, no. 3: 51. https://doi.org/10.3390/ijfs8030051

APA StyleOnsongo, S. K., Muathe, S. M. A., & Mwangi, L. W. (2020). Financial Risk and Financial Performance: Evidence and Insights from Commercial and Services Listed Companies in Nairobi Securities Exchange, Kenya. International Journal of Financial Studies, 8(3), 51. https://doi.org/10.3390/ijfs8030051