3.1. Analytical Techniques

We analyzed data using the maximum likelihood structural equation modeling technique based on Partial Least Squares (PLS) with the program Smart PLS 3 Professional (

Ringle et al. 2016). PLS is based on principal components analysis and orthogonal rotation, which is acceptable for determining the measurement model. Other programs, such as linear structural relations called LISREL (it is a proprietary statistical software package used in structural equation modeling), could produce similar results, despite the limited sample size. PLS application consists of a confirmatory model of structural equations that enable a model to be constructed with a system of one-way effects between two variables on a path diagram. That diagram represents the relationships between dependent and independent variables and the correlations between constructs and indicators. The objective of PLS is to provide certain values for latent variables so that predictions can be made. The model specifically defines latent variables as linear combinations of its observed measures, and the relationships between latent variables are assumed to not be interdependent. The PLS technique seeks to explain the variance in all the variables involved—both latent and observed—which results in an attempt to maximize the variance explained (

R2) in the latent variables. We selected the PLS model because all the constructs that create the structural model are measured by means of formative indicators; with six constructs, 36 indicators and 321 observations, the numbers involved are not excessively high. As the original populations from which the data were extracted do not comply with the assumptions of normality and homoscedasticity, PLS provides flexible model in line with the conditions present in social and behavioral science, so is a suitable alternative for creating structural models in the specific field of business.

Many studies (

Söllner and Leimeister 2010;

Bollen and Lennox 1991), showed that there may be potentially serious consequences if the measurement model is incorrectly specified. Inaccurate conclusions or different conclusions concerning the structural relationships between constructs may be reached.

The constructs in the model are measured by formative indicators (

Bollen and Lennox 1991) which are observed variables that act in a causal, predictive, or preceding fashion in regards the construct. In the case considered here, all the constructs are one-dimensional, i.e., first-order and formative. The same applies to the constructs that occupy exogenous positions (expectations, guarantees, and transparency) and those that occupy endogenous positions (trust, management and mutual benefit). Thus, causality flows from the ex-ante constructs (expectations, transparency, and guarantees) toward trust, and finally from management toward mutual benefit. Notably, the methods traditionally used to determine the reliability and validity of reflective measurement models are not suitable for use with constructs where the direction of causality is precisely the opposite (

Bollen and Lennox 1991). For this reason, Diamantopoulos and

Winklhofer (

2001) suggested specific procedures for measuring and assessing formative constructs. Instead, content validity should be assessed before empirically evaluating the formative measurement model to ensure that formative indicators capture all or the main facets of the construct. We applied a content specification in which the domain of the content that the indicators try to measure has been clearly specified. We provided a set of indicators that exhaustively cover the domain of each formative construct. To reinforce the justification of the operationalization of the construct as formative, we reviewed the literature and ensured a reasonable theoretical foundation, as was developed in

Section 2. In short, the validity must be tested based on theoretical reasoning and the opinion of experts

Diamantopoulos and Winklhofer (

2001). In practice, formative models are not easy to defend because the researcher must be completely sure that all the possible causes of the latent variable have been considered by the indicators

Diamantopoulos and Winklhofer (

2001). For that reason, it is absolutely essential that research includes formative measures and the PLS technique must be used to establish an acceptable level of validity of measurement before continuing with the structural analysis of relationships. Below, the measurement model is first assessed through a multicollinearity analysis in the formative measurement model, and second, by the assessment of the significance and relevance of the formative indicators. The structural model was then used to test for the hypothesized relationships.

3.3. Structural Model and Testing of Hypotheses

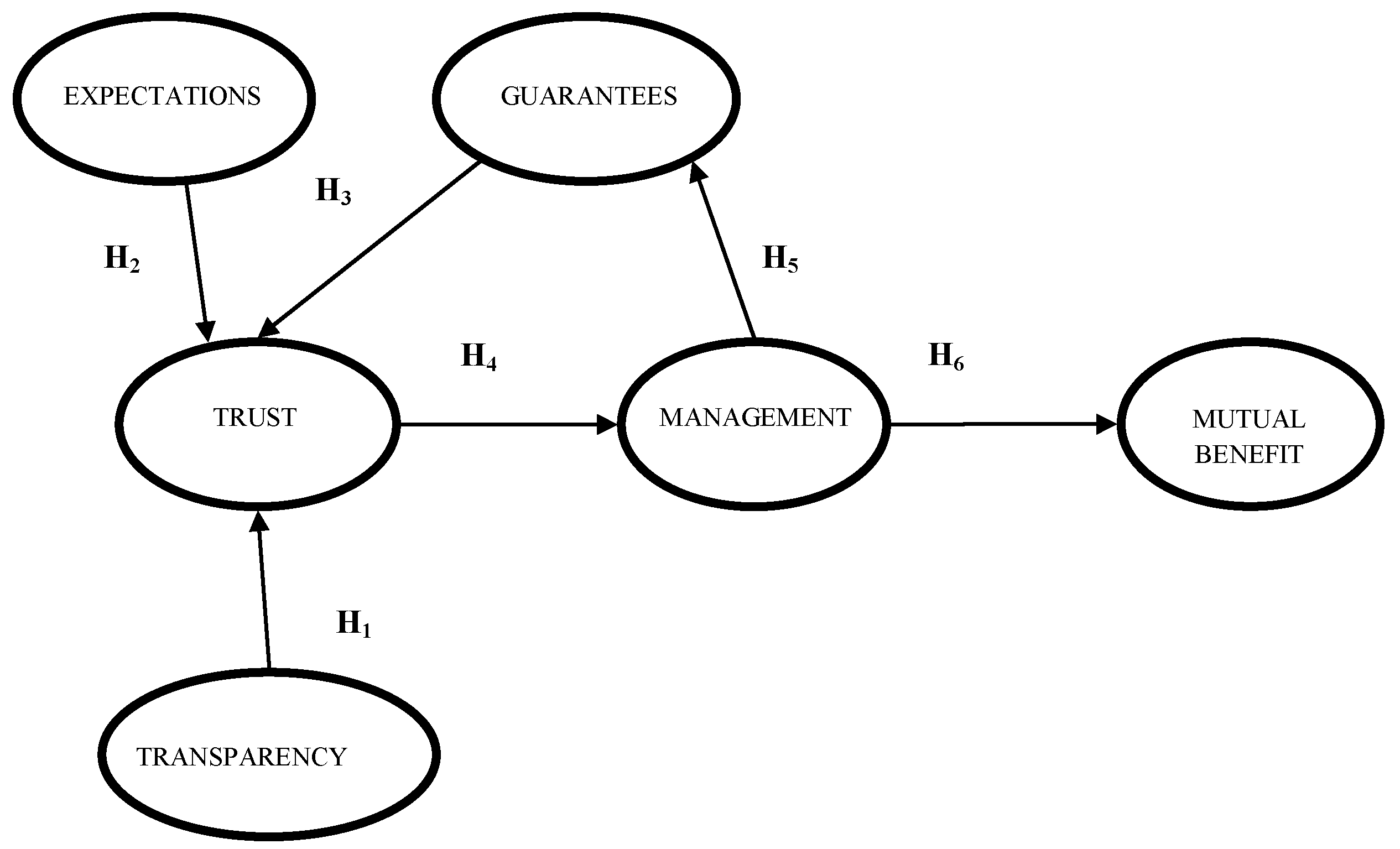

Once the measurement model was satisfactorily evaluated, the next step was to assess the structural model constructed from the relationships hypothetically established between the constructs based on the initial theoretical model. In the context of PLS, the structural model must be designed as a causal chain. Such models are known as “recursive models”, i.e., there can be no cyclical relationships in the structural model. Hence, the PLS could not be used to analyze our model as a whole, so we decided to analyze H5 separately (

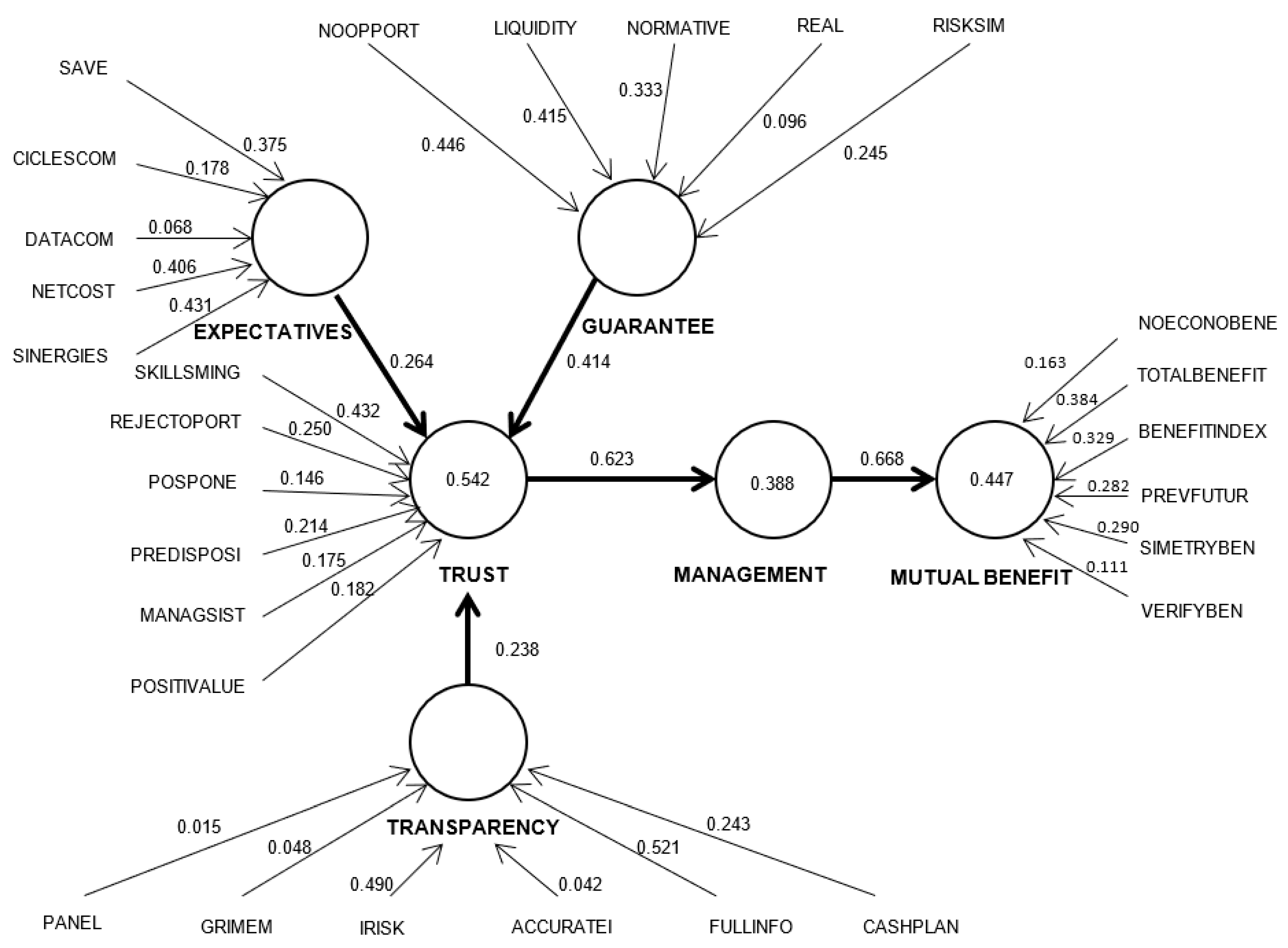

Figure 2). Our model was analyzed by aggregating the items that reflect a one-dimensional construct. The results are provided in

Table 3.

The standardized path coefficients can be said to be significant as their minimum value was 0.2 (H1 and H2), but, in most cases, they were ideal, as their values were greater than 0.3 (H3, H4, and H6).

The stability of the estimates provided by PLS was examined using the non-parametric technique known as bootstrapping (

Table 4). This process can be used to determine whether a formative indicator contributes significantly to the corresponding construct, as well as to determine the significance of the path coefficients by calculating the standard error, Student’s t-value,

ρ-value, and the confidence intervals.

It was necessary to check the significance of all the relationships established in our structural model. When results were interpreted each estimator was analyzed, though there was no need to include them all in the report on the results, since they all lead to the same conclusion. The path coefficients and, by extension, the hypotheses accepted are those that are significant: in the model, which include the five tested hypotheses (H1, H2, H3, H4, and H6). However, the goal of PLS is to identify not just which path coefficients are significant but also which of the significant relationships are most significant.

Finally, if there are mediating constructs, then their direct and indirect effects must be analyzed, which is calculated as the product of the coefficient paths along the causal line between two indirectly related variables (

Douglas and Craig 2009). The public perception of shared goods has changed substantially in the past few years. While co-owning properties has been widely accepted for a while (e.g., timeshares), the notion of sharing bikes, cars, or even rides on an on-demand basis is just now starting to gain widespread popularity. The emerging “sharing economy” is particularly interesting in the context of cities that struggle with population growth and increasing density. While sharing vehicles promises to reduce inner-city traffic, congestion, and pollution problems, the associated business models are not without problems themselves. Using agency theory, in this article we discuss existing shared mobility business models in an effort to unveil the optimal relationship between service providers (agents) and the local governments (principals) to achieve the common objective of sustainable mobility. Our findings show private or public models are fraught with conflicts, and point to a merit model as the most promising alignment of the strengths of agents and principals (

Douglas and Craig 2009).

To determine the contribution of predictive variables to the

R2 (variance explained) of the endogenous variables in the model proposed, it was necessary to calculate the absolute value of the result of multiplying the path coefficient by the correlation between each pair of constructs (

Hair et al. 2011). The result is interpreted as the variance of the endogenous construct explained by the predictive variable. We considered that the predictive variable should be able to explain at least 1.5% of the endogenous variable.

In our case, all the predictive variables explained more than 1.5% of the endogenous variable. These results confirm the conclusions reached in analyzing the path or standardized regression coefficients between the constructs.

The next step was to determine the accuracy and stability of the parameter estimates so that our hypotheses could be tested. We completed this using bootstrapping (5000 sub-samples, 321 cases, “no change in sign” as the algorithm option, significance level 0.05, and two-tailed testing), which produced the standard error, Student’s t-value, the

ρ-value, and the confidence intervals.

Table 5 shows that all the path coefficients are significant (

ρ-value < 0.05) for an error probability of 5%.

Table 6 shows the total effect of each variable on the rest and the corresponding

ρ-values. They are all significant.

Given these last results, the total effect of each variable on the rest is significant (ρ-value < 0.05), at least at the 5% level. As we had to adapt the model, eliminating the path between management and guarantees to prevent a cyclical relationship between trust-management-guarantees-trust and thus meet the requirements for PLS estimation, we cannot confirm within the structural model whether the relationship between management and guarantees is significant, or determine the sign of that relationship. However, we checked for a bivariate correlation between these two variables by estimating Spearman’s Rho coefficient using the IBM SPSS Statistics 22 software program.

Table 7 shows that the guarantees and management constructs are significantly correlated (Spearman’s Rho coefficient = 0.567 at the 0.01 level), which does not imply that there is causality between them, but simply that they are linearly related. This relationship is shown in

Figure 2 with a dotted line.

The predictive power of the model was measured via the

R2 (variance explained) for the dependent latent variables.

Hair et al. (

2011) considered a figure of 0.1 or more as a suitable value for variance explained. Lower figures indicate that the dependent latent variable in question has a lower predictive power.

As shown in

Table 8, the predictive power of the model is adequate, since all the endogenous constructs have

R2 values in excess of 0.1. Specifically, following the criteria in

Hair et al. (

2011) and

Douglas and Craig (

2009), the predictive power of the constructs is moderate in the case of trust (0.542) and close to moderate for management (0.388) and mutual benefit (0.447). In these last two cases, the

R2 are close to 0.5 or even higher, which is the level classified as moderate.

Table 9 provides our analyses of the relative explanatory power or size effect (

f2) of the model. The change in

R2 shows whether an independent variable has any substantial influence on the dependent latent variable. Following the criteria in

Cohen and Kietzmann (

2014) the size effect is considered to be approximately average in the case of the three constructs that influence trust, but large on trust itself and very large on management.

It is not possible to analyze predictive relevance by estimating the parameter Q2 and its corresponding size effect q2 because they cannot be estimated for endogenous constructs measured formatively.

The model was confirmed not only theoretically in terms of the theoretical relationships explained by each construct in itself, but also through a structural model of equations that permitted confirmation through statistics. As shown in

Figure 2, on the basis of the data obtained from the PLS, trust, management, and mutual benefit are the most important variables in this sustainable financial model. Thus, as occurs in the collaborative economy, this model shows that trust is the key factor, covering reputation assessment systems and traditional mechanisms, as a preliminary and/or supplementary step in the need for regulation. Mutual benefit arises from the social, financial, and environmental value created on the basis of the values that drive the collaborative economy, i.e., the feeling of belonging to a community and interactions between the parties involved, which are extended through the network effect.

{kind=link}

{kind=link}