BREXIT and Foreign Direct Investment: Key Issues and New Empirical Findings

Abstract

:1. Introduction

2. Literature Review

2.1. Selected BREXIT FDI Aspects

- British FDI outflows will reduce in the EU and this should dampen knowledge accumulation in EU27 countries;

- Taking additionally into account the arguments of Froot and Stein (1991), British FDI outflows—with an emphasis on international M&As (Mergers and Acquisitions)—will particularly reduce to those EU27 countries where the real appreciation (a mirror of pound depreciation) is rather high. One may assume that the Eurozone’s appreciation rate will be higher than that of other EU countries to the extent that BREXIT itself will create nervous markets for some time and thus could reinforce the role of Germany, France, the Netherlands, and Luxembourg as typical safe-haven countries in the Eurozone. Thus, one should consider real exchange rate effects and control for them in FDI gravity models, especially in the case of drastic policy changes such as BREXIT.

2.2. FDI Dynamics within the EU

- To the extent that trade reinforces specialization and that, in turn, specialization gains raise factor productivity, there will be enhanced investment opportunities, particularly in those countries where technology-intensive Schumpeterian sector production has increased. Jungmittag and Welfens (2016) has shown in an empirical analysis for the EU15 (all EU-members previous 2004) that output in those EU countries which have achieved more high-technology specialization is raised through trade. According to the theory of asset-seeking foreign direct investment (e.g., Makino et al. 2002; Ivarsson and Jonsson 2003), such a specialization pattern will attract higher FDI inflows as foreign investors seek to acquire firms with technological advantages that are complementary to the respective foreign firm’s core research and production activities.

- The combination of regional free trade and free capital flows implies that there are particular opportunities for regional production networks in the EU. As offshoring (i.e., imports of intermediate products as intra-MNC (Multinational Companies) trade) and international/interregional (intra-EU) and regional outsourcing is reinforcing the international competitiveness of multinational firms, such firms, following the OLI (Ownership-, Location- and Internalization Advantages) approach of Dunning (Dunning 2001), should increase production abroad. In the case of EU countries, this implies that FDI outflows to third countries (e.g., to the US) should increase.

- As trade-related specialization gains raise per capita income, demand for differentiated products will increase and those products in turn stand for technology-intensive and knowledge-intensive goods that are typically produced by multinational companies. If the economic logic of production suggests that producers should have production in geographic proximity to markets (e.g., Raff and Von der Ruhr 2001), it is obvious that multinational production would expand in a way that enhances FDI. This points to a positive reciprocal link between trade and FDI.

- The single market enhances trade in intermediate products which will raise the productivity of internationalized firms in a way that will contribute to more exports as more productive firms can benefit through higher export shares (Melitz 2003). Hence, there is a reciprocal link between FDI and trade in this respect.

- Another reciprocal link between trade and FDI comes from the fact that FDI inflows go along with international technology transfer for the host country—and in the case of greenfield investment, with a higher capital stock in the host country—so that output and gross national income, respectively, are raised. Therefore, imports will be raised and, following the logic of the trade gravity model, both imports and exports would increase. Hence, trade will be raised as well so that there is a positive reciprocal link between FDI and trade.

2.3. Gravity FDI Flow/Stock Studies Targeting the EU

- EU (EU single market) membership of target and origin country will increase FDI flows.

- Trade openness will increase FDI flows.

- Corporate tax level constrains FDI flows.

- A higher relative FDI stock will attract more FDI flows. The FDI stock variable is considered relative to the total capital stock that may be assumed to implicitly reflect some path dependency as well as reinvestment of profitable subsidiaries abroad (as we want to explain, FDI inflows endogeneity might be a potential problem; this is addressed by lagging this variable by one period).7

- A low real exchange rate (to USD) will attract more FDI flows—depreciation of the home currency stimulates higher FDI inflows.

3. Econometric Specification and Data

3.1. Theoretical Foundation of the Gravity Model

- —regression constant (—regression estimators respectively),

- —characteristics of the origin country (GDP, GDP/capita, EU membership),

- —characteristics of the target country (GDP, GDP/capita, EU membership, openness, R&D (Research and Development) investment, ICT (Information and Communication Technology) investment, corporate tax level, relative FDI stock),

- —characteristics of the relationship between country pairs (distance, cultural and historical differences, etc.),

- —dyadic fixed effects, i.e., one dummy variable for each possible set of partner countries, controls for all unobservables and satisfies the multilateral resistance requirement),

- —time fixed effects, i.e., one dummy variable for each year,

- —error term.

3.2. Data

3.2.1. Definition and Sources

3.2.2. Treating Missing Values

3.2.3. Treating Negative Values

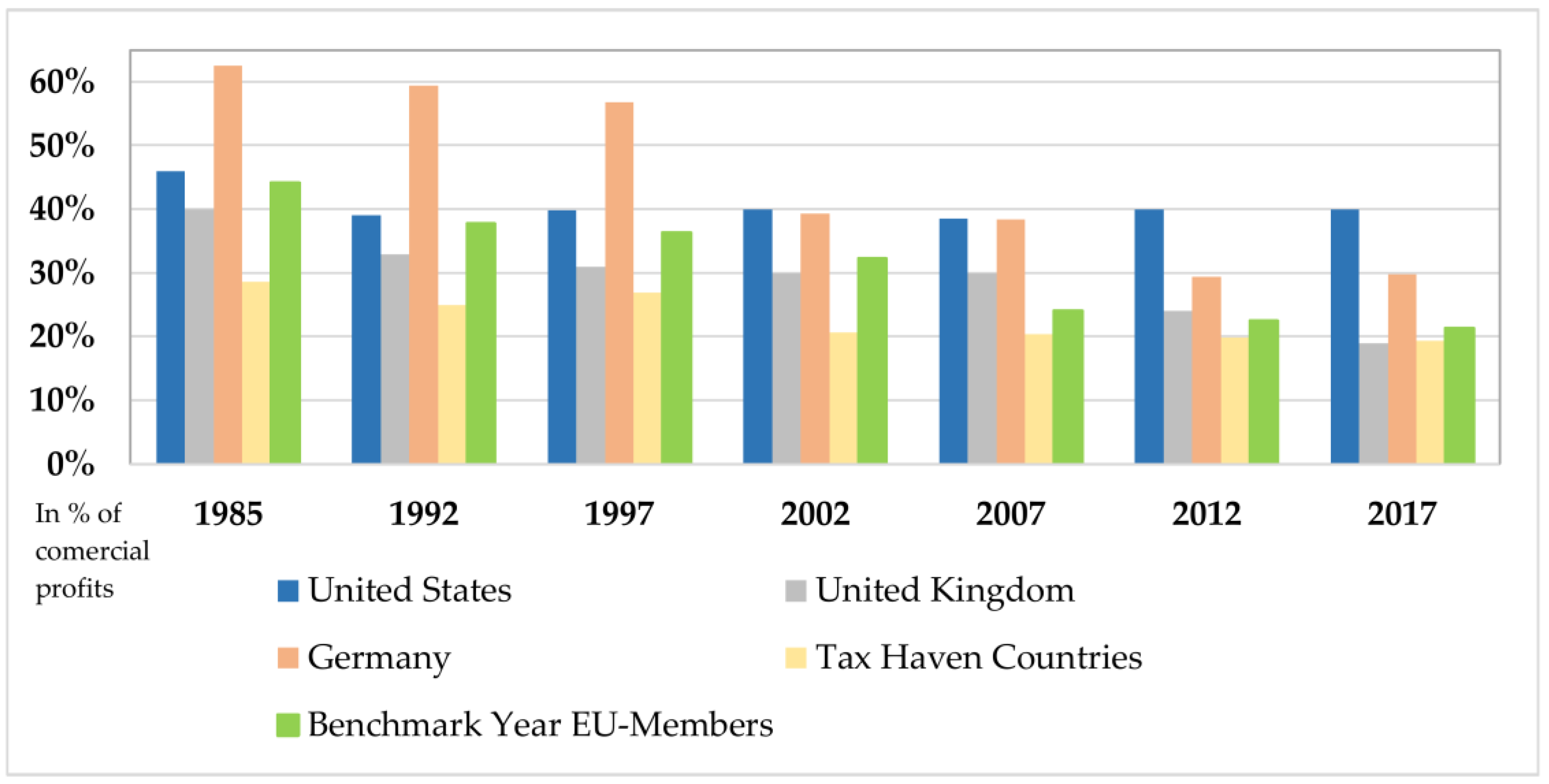

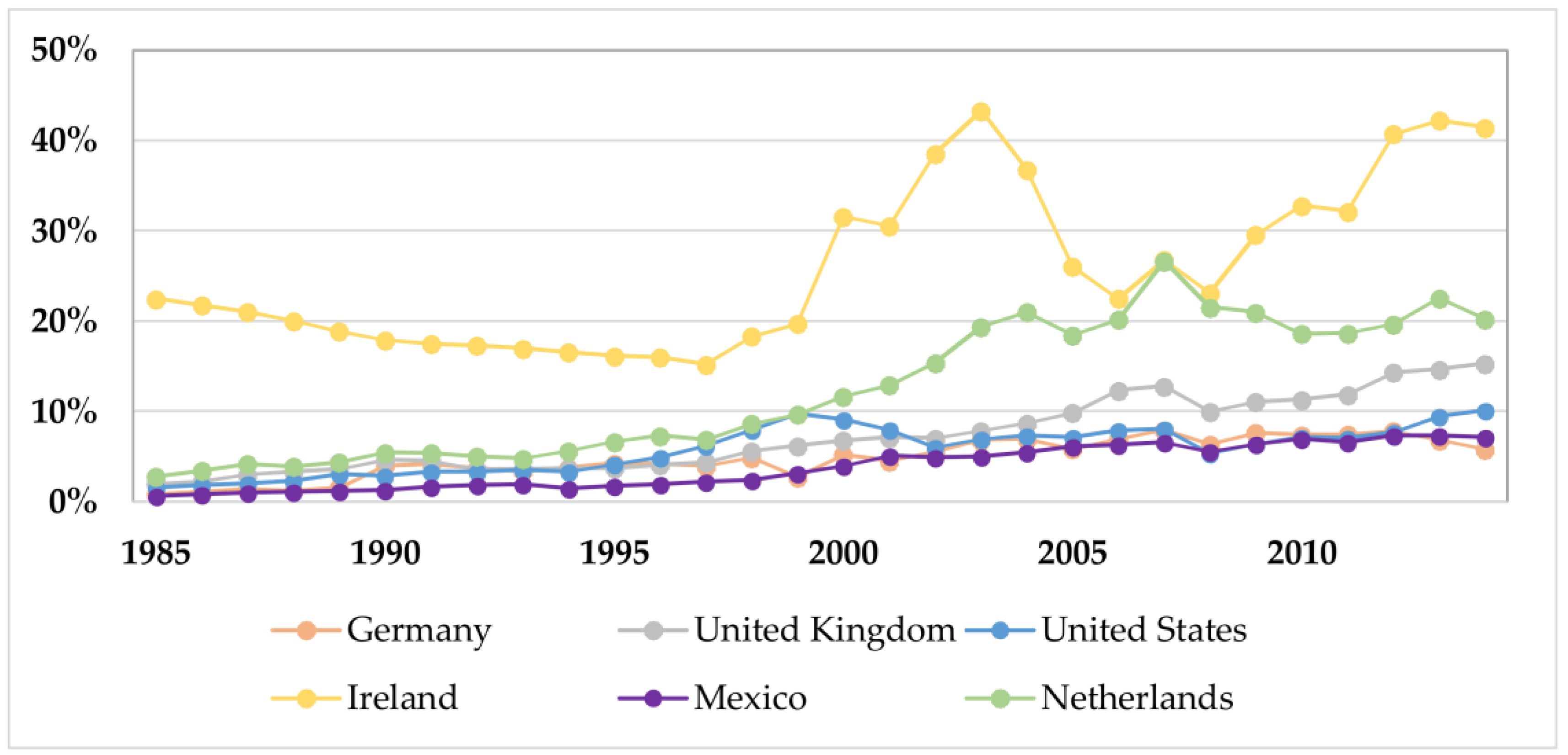

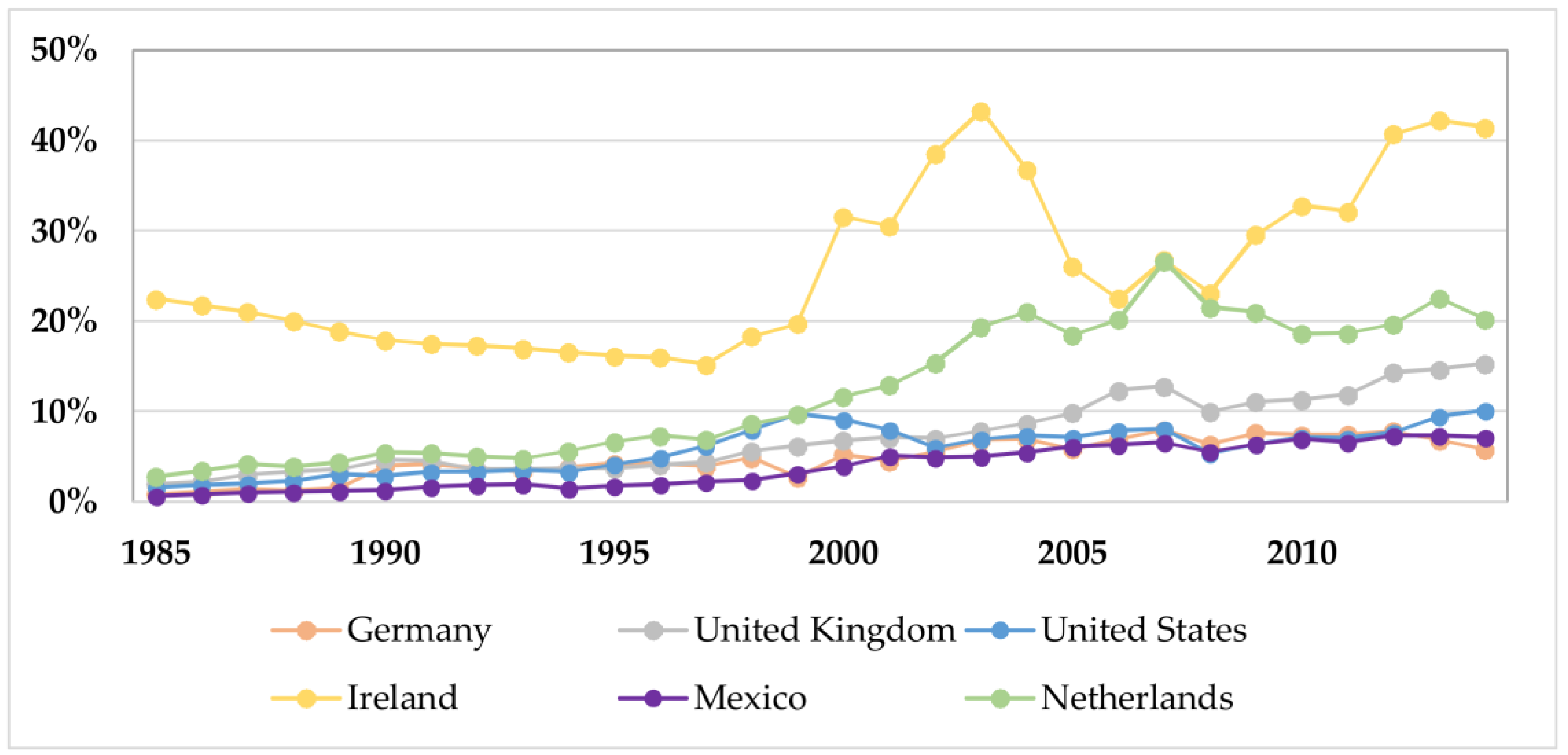

3.2.4. Special Role of UK in Descriptive Data

4. Empirical Findings

4.1. PPML Dyadic Fixed Estimations

4.2. Results

- The EU membership of the origin country has a significant impact on FDI flows, namely +62% if the origin country is an EU member. No significant impact on FDI flow concerning the target country and EU membership is found. This contradicts previous studies, especially Bruno et al. (2016), as they also use OECD flow data. We ascribe the different results to not controlling for negative flows, as we get similar results to Bruno et al. (2016) when we do not control for them. FDI origin country and EU membership findings mirror those in literature.When controlling for single market instead of pure membership, we find a highly significant impact of both origin and target country having access to it. Interpreting model (8), which includes the total set of variables of interest, a country attracts +42% FDI inflows and sends +83% FDI outflows if it has access to the EU single market. While this number seems very high, it mirrors previous findings (see Table 1).

- Hypothesis 1 is therefore accepted, indicating that access to the single market results in considerably higher FDI in- and outflows.

- Trade openness has a significant impact on FDI flows, with a 1% increase in openness leading to a 0.6% increase in FDI flows (model 7). When controlling for the share of foreign ownership of a country’s capital stock, the effect vanishes, as both variables correlate strongly (see Table A1 and Table A2 in the Appendix A). To the extent that there is an FDI stock endogeneity problem, one would take model (3) as the preferred version, which clearly indicates the strong relevance of trade intensity. If this network should be damaged through a modest EU–UK free trade agreement, serious negative post-BREXIT effects on FDI should be expected.

- Hypothesis 2 is neither accepted nor rejected. While many studies prove the significant impact of the classical openness indicator, we show that it is important to focus attention on other variables, especially the share of already existing foreign capital within a country. Further research concerning trade and FDI is needed (keywords: production to market, supply chain analysis, etc.), and will be discussed to some extent in the conclusion.

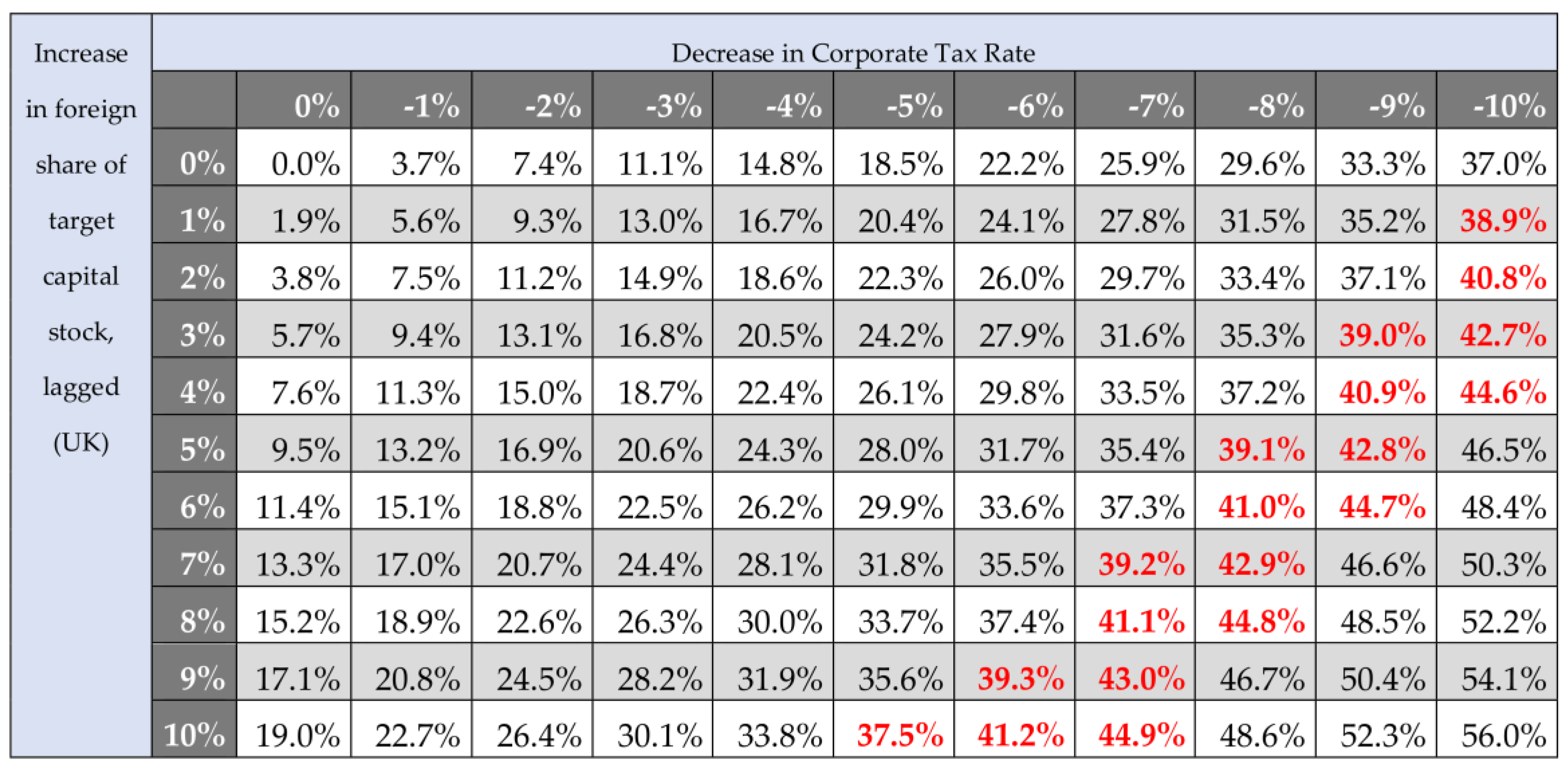

- The corporate tax level has a negative impact on FDI flows, with a 1% increase in the statutory corporate tax level leading to an almost 4% decrease in FDI flows, and therefore results are in line with Folfas (2011). This will have different implications on greenfield and brownfield investments, mainly impacting decisions on where to construct new production plants. In addition, this should be considered in the context of tax havens.

- Hypothesis 3 is accepted. High corporate tax levels in home countries constrain FDI inflows.

- If the foreign-owned share of a country’s capital stock (namely inward stock over capital stock, lagged by one year to control for annual inflow) increases by 1%, the FDI inflow will increase by 1.9%. On one hand, with an annually rising FDI stock by aggregated inflow, depreciated and growth-considered, the stock-flow relationship is straightforward. On the other hand, we are interested in the cluster and spillover effects which pre-existing investment has on further investment. By lagging stocks we neutralize the direct inflow effect, leaving only the cluster effect.These findings are assessed to have strong implications, especially when considering policy changes such as an exit from the EU. To mirror this effect more clearly, an intertemporal gravity model could be altered, which we suggest for future research in the field of FDI flows but especially stocks.

- Hypothesis 4, that the relative foreign share of the capital stock of a country attracts increasing FDI, is accepted.

- According to Barrell et al. (2017), we would suspect that a low real exchange rate vis-à-vis USD will attract a higher FDI inward flow. However, the real exchange rate of home country to USD does not significantly impact FDI inward flows. However, this variable may not be compiled in an optimal way and further research needs to be done.

- Hypothesis 5 is rejected.

5. Policy Implications and Future Research

Author Contributions

Acknowledgments

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Var_List | Ln_Target_Rer | Target_Corporate_Taxrate | Target_Openness | Foreign_Capstock_Share_Lagged |

|---|---|---|---|---|

| ln_target_rer | 1 | - | - | - |

| target_corporate_taxrate | −0.2153 | 1 | - | - |

| target_openness | −0.057 | −0.4553 | 1 | - |

| foreign_capstock_share_lagged | −0.1741 | −0.3248 | 0.7546 | 1 |

| Var_List | Target_Eu | Origin_Eu | Ln_Target_Gdp | Ln_Origin_Gdp | Ln_Target_Gdp_Per_Capita | Ln_Origin_Gdp_Per_Capita | Ln_Target_Rer | Target_Corporate_Taxrate | Target_Openness | Foreign_Capstock_Share_Lagged |

|---|---|---|---|---|---|---|---|---|---|---|

| target_eu | 1.0000 | - | - | - | - | - | - | - | - | - |

| origin_eu | 0.0167 | 1.0000 | - | - | - | - | - | - | - | - |

| ln_target_gdp | 0.0058 | -0.0148 | 1.0000 | - | - | - | - | - | - | - |

| ln_origin_gdp | −0.0079 | 0.0185 | −0.0346 | 1.0000 | - | - | - | - | - | - |

| ln_target_gdp_per_capita | 0.2972 | 0.0740 | 0.1925 | 0.0975 | 1.0000 | - | - | - | - | - |

| ln_origin_gdp_per_capita | 0.0518 | 0.2402 | −0.0281 | 0.3412 | 0.1777 | 1.0000 | - | - | - | - |

| ln_target_rer | −0.5343 | 0.0087 | −0.2104 | −0.0135 | −0.3051 | 0.0086 | 1.0000 | - | - | - |

| target_corporate_taxrate | −0.0426 | −0.1133 | 0.4799 | −0.1279 | −0.0479 | −0.2857 | −0.2153 | 1.0000 | - | - |

| target_openness | 0.3743 | 0.0674 | −0.4962 | 0.0744 | 0.2509 | 0.1698 | −0.0570 | −0.4553 | 1.0000 | - |

| foreign_capstock_share_lagged | 0.2622 | 0.0748 | −0.2341 | 0.0946 | 0.4953 | 0.1949 | −0.1741 | −0.3248 | 0.7546 | 1.0000 |

References

- Anderson, James E. 2011. The Gravity Model. Annual Review of Economics 3: 133–60. [Google Scholar] [CrossRef]

- Anderson, James E., and Eric Van Wincoop. 2003. Gravity with Gravitas: A Solution to the Border Puzzle. American Economic Review 93: 170–92. [Google Scholar] [CrossRef]

- Baldwin, Richard, and Daria Taglioni. 2007. Gravity for Dummies and Dummies for Gravity Equations. NBER Working Paper No. 12516. Cambridge: National Bureau of Economic Research. [Google Scholar]

- Bank of England. 2018. Inflation Report. London: Bank of England. [Google Scholar]

- Barrell, Ray, and Nigel Pain. 1997. Foreign Direct Investment, Technological Change, and Economic Growth within Europe. The Economic Journal 107: 1770–86. [Google Scholar] [CrossRef]

- Barrell, Ray, Abdulkader Nahhas, and John Hunter. 2017. Exchange Rates and Bilateral FDI: Gravity Models of Bilateral FDI in High Income Economies. Economics and Finance Working Paper Series, No. 17-07; London: Brunel University London. [Google Scholar]

- Blomström, Magnus, and Ari Kokko. 1998. Multinational Corporations and Spillovers. Journal of Economic Surveys 12: 247–77. [Google Scholar] [CrossRef]

- Blomstrom, Magnus, Ari Kokko, and Mario Zejan. 2000. Foreign Direct Investment: Firm and Host Country Strategies. Basingstoke: Palgrave Macmillan UK. [Google Scholar]

- Brenton, Paul, Francesca Di Mauro, and Matthias Lücke. 1999. Economic Integration and FDI: An Empirical Analysis of Foreign Investment in the EU and in Central and Eastern Europe. Empirica 26: 95–121. [Google Scholar] [CrossRef]

- Bruno, Randolph, Nauro Campos, Saul Estrin, and Meng Tian. 2016. Technical Appendix to ‘The Impact of Brexit on Foreign Investment in the UK’. Gravitating Towards Europe: An Econometric Analysis of the FDI Effects of EU Membership. London: Center for Economic Performance, London School of Economics and Political Science. [Google Scholar]

- De Benedictis, Luca, and Daria Taglioni. 2011. The Gravity Model in International Trade. In The Trade Impact of European Union Preferential Policies: An Analysis through Gravity Models. Edited by Luca De Benedictis and Luca Salvatici. Berlin: Springer. [Google Scholar]

- Dunning, John H. 1998. Location and the Multinational Enterprise—A Neglected Factor? Journal of International Business Studies 29: 45–66. [Google Scholar] [CrossRef]

- Dunning, John H. 2001. The Eclectric (OLI) Paradigm of International Production: Past, Present and Future. International Journal of the Econometrics of Business 8: 173–90. [Google Scholar] [CrossRef]

- Egger, Peter, and Michael Pfaffermayr. 2004. Foreign Direct Investment and European Integration in the 1990s. The World Economy 27: 99–110. [Google Scholar] [CrossRef]

- Erken, Hugo. 2017. The Permanent Damage of Brexit. Rabobank Special. Utrecht: Rabobank/Raboresearch. [Google Scholar]

- EY. 2018. Signs of a Brexit Impact on UK Foreign Direct Investment. Available online: http://www.ey.com/uk/en/newsroom/news-releases/18-03-29-signs-of-a-brexit-impact-on-uk-foreign-direct-investment (accessed on 12 April 2018).

- Feenstra, Robert C., Robert Inklaar, and Marcel P. Timmer. 2015. The Next Generation of the Penn World Table. American Economic Review 105: 3150–82. [Google Scholar] [CrossRef]

- Folfas, Paweł. 2011. FDI between EU Member States: Gravity Model and Taxes. ETSG 2011 Conference Paper. Warsaw: Warsaw School of Economics, Institute of International Economics. [Google Scholar]

- Fournier, Jean-Marc, Aurore Domps, Yaëlle Gorin, Xavier Guillet, and Délia Morchoisne. 2015. Implicit Regulatory Barriers in the EU Single Market: New Empirical Evidence from Gravity Models. OECD Economics Department Working Papers, No. 1181. Paris: OECD Publishing. [Google Scholar]

- Francois, Joseph, Miriam Manchin, Hanna Norberg, Olga Pindyuk, and Patrick Tomberger. 2013. Reducing Transatlantic Barriers to Trade and Investment. London: CEPR (for the European Commission). [Google Scholar]

- Froot, Kenneth, and Jeremy Stein. 1991. Exchange Rates and Foreign Direct Investments. Quarterly Journal of Economics 106: 1191–217. [Google Scholar] [CrossRef]

- Hayashi, Fumio. 2000. Econometrics. Princeton: Princeton University Press, pp. 233–34. [Google Scholar]

- Head, Keith, and Thierry Mayer. 2014. Gravity Equations: Workhorse, Toolkit and Cookbook. In Handbook of International Economics. Edited by Gene M. Grossman and Kenneth S. Rogoff. New York: Elsevier, vol. 4, chp. 3. pp. 131–95. [Google Scholar]

- Herrmann, Heinz, and Robert E. Lipsey. 2003. Foreign Direct Investment in the Real and Financial Sector of Industrial Countries. Berlin: Springer. [Google Scholar]

- HM Government. 2016. HM Treasury Analysis: The Long-Term Economic Impact of EU Membership and the Alternatives; London: HM Government.

- Ivarsson, Inge, and Thommy Jonsson. 2003. Local technological competence and asset-seeking FDI: An empirical study of manufacturing and wholesale affiliates in Sweden. International Business Review 12: 369–86. [Google Scholar] [CrossRef]

- Jungmittag, Andre, and Paul J. J. Welfens. 2016. Beyond EU-US Trade Dynamics: TTIP Effects Related to Foreign Direct Investment and Innovation. EIIW Discussion Paper No. 212. Bonn: Institute of Labor Economics. [Google Scholar]

- Kareem, Fatima Olanike, I. Martínez-Zarzoso, and B. Bruemmer. 2016. Fitting the Gravity Model If Zero Trade Flows Are Frequent: A Comparison of Estimation Techniques Using Africa’s Trade Data. Global Food Discussion Paper No. 77. Göttingen: Georg-August University Göttingen. [Google Scholar]

- Knickerbocker, Frederick T. 1973. Oligopolistic Reaction and Multinational Enterprises. Boston: Harvard University. [Google Scholar]

- Köhler, Matthias. 2018. An Analysis of Non-Traditional Activities at German Savings Banks—Does the Type of Fee and Commission Income Matter? Discussion Paper No. 01/2018. Frankfurt: Deutsche Bundesbank. [Google Scholar]

- KPMG. 2017. KPMG Corporate Tax Rates Table. Available online: https://home.kpmg.com/xx/en/home/services/tax/tax-tools-and-resources/tax-rates-online/corporate-tax-rates-table.html (accessed on 23 April 2018).

- Lawless, Martina, and Edgar L. W. Morgenroth. 2016. The Product and Sector Level Impact of a Hard Brexit across the EU. ESRI Working Paper No. 550. Tokyo: Economic and Social Research Institute. [Google Scholar]

- Makino, Shige, Chung-Ming Lau, and Rhy-Song Yeh. 2002. Asset-Exploitation versus Asset-Seeking: Implications for Location Choice of Foreign Direct Investment from Newly Industrialized Economies. Journal of International Business Studies 33: 403–21. [Google Scholar] [CrossRef]

- McGrattan, Ellen R., and Andrea Waddle. 2017. The Impact of Brexit on Foreign Investment and Production. Federal Reserve Bank of Minneapolis Research Department Staff Report 542 and NBER Paper w23217. Cambridge: National Bureau of Economic Research. [Google Scholar]

- Melitz, Marc J. 2003. The Impact of Trade on Intra-Industry Reallocations and Aggregate Industry Productivity. Econometrica 71: 1695–725. [Google Scholar] [CrossRef]

- Mintz, Jack, and Alfons Weichenrieder. 2010. The Indirect Side of Direct Investment—Multinational Company Finance and Taxation. CESifo Book Series; Cambridge: MIT Press. [Google Scholar]

- Raff, Horst, and Marc Von der Ruhr. 2001. Foreign Direct Investment in Producer Services: Theory and Empirical Evidence. CESifo Working Paper No. 598. Munich: CESifo Group Munich. [Google Scholar]

- Shepherd, Ben. 2016. The Gravity Model of International Trade: A User Guide. Herndon: United Nations Publication. [Google Scholar]

- Silva, J. M. C. Santos, and Silvana Tenreyro. 2006. The Log of Gravity. The Review of Economics and Statistics 88: 641–58. [Google Scholar] [CrossRef]

- Silva, J. M. C. Santos, and Silvana Tenreyro. 2011. Further Simulation Evidence on the Performance of the Poisson Pseudo-Maximum Likelihood Estimator. Economics Letters 112: 220–22. [Google Scholar] [CrossRef]

- Stammann, Amrei. 2017. Fast and Feasible Estimation of Generalized Linear Models with Many Two-Way Fixed Effects. Düsseldorf Working Paper. Düsseldorf: Heinrich Heine University. [Google Scholar]

- Straathof, Bas, Gert Jan Linders, Arjan Lejour, and M. Ã. Jan. 2008. The Internal Market and the Dutch Economy. Implications for Trade and Economic Growth. CPB Document No. 168. The Hague: CPB. [Google Scholar]

- Welfens, Paul J. J. 2017a. An Accidental BREXIT. London: Palgrave Macmillan. [Google Scholar]

- Welfens, Paul J. J. 2017b. The True Cost of BREXIT for the UK: A Research Note. EIIW Discussion Paper No. 234. Wuppertal: Universitätsbibliothek Wuppertal, University Library. [Google Scholar]

- Whyman, Philip B., and Alina I. Petrescu. 2017. The Economics of Brexit. A Cost-Benefit Analysis of the UK’s Economic Relationship with the EU. Berlin: Palgrave Macmillan, Springer International Publishing AG. [Google Scholar]

- Wojciechowski, Liwiusz. 2013. The Determinants of FDI Flows from the EU-15 to the Visegrad Group Countries—A Panel Gravity Model Approach. Entrepreneur Business and Economics Review 1: 7–22. [Google Scholar] [CrossRef]

- Wyman, Oliver. 2017. One Year on from the Brexit Vote—A Briefing for Wholesale Banks. London: TheCityUK. [Google Scholar]

| 1 | Some variables, such as distance, might lose importance with falling transport costs. Others, such as digitalization and innovation, gain due to globalization. |

| 2 | Therefore, they ran two models, 1981–2005 and 1994–2004. They did not find significant differences. |

| 3 | What is the decisive connection between an EU dropout and FDI flow/stock and to what extent; for example, currency union, policy union, migration, free trade areas, etc. |

| 4 | They use a two-step system Generalized Method of Moments (GMM) estimator for their gravity model. |

| 5 | Direction matters. |

| 6 | This is a workaround to more commonly used panel estimations with OLS in Stata, enabling calculation of panel-estimations with PPML. |

| 7 | The methodology of lagging endogenous variables with respect to time in order to mitigate potential endogeneity problems has become more popular in recent literature; in this regard we follow Köhler (2018). We also use cluster robust standard errors, clustered by country pair, and check the adequacy of the methodology via a Durbin–Wu–Hausman test. |

| 8 | Utilization of the model in economic research is described by De Benedictis and Taglioni (2011). |

| 9 | Outward and inward resistance: exports from country i to country j depend on trade costs of all possible export markets (outward resistance); imports into country i from j depend on trade costs of all possible import markets. |

| 10 | Controlling for EU membership in an era without entries or exits in a country fixed effects setting will not work (due to omitted variable bias). Bilateral dummies are constructed: (1) member exports to member; (2) nonmember exports to member; (3) member exports to nonmember; the non-non case acts as a baseline for interpretation. |

| 11 | Regressions were run separately just for the purpose of validation of variable exogeneity, with FDI inflow as a dependent variable and EU-membership and FDI capital stock share (lagged) as explanatory variables, using the xtivreg2 Stata command, see Hayashi (2000), as there is no endogeneity test implementable within the PPML. |

| 12 | Setting the smallest equal to zero and adding up. |

| 13 | In previous literature, this problem was not addressed in detail, although Fournier et al. (2015) and Bruno et al. (2016) seemed to have assigned zeroes (which then convert to one, in order to be able to also utilize OLS) to negatives instead of dropping them. Comparing their datasets and nondropped observations lead to this conclusion. |

| 14 | Countries with the lowest corporate tax levels include Ireland, Switzerland, Slovenia, Chile, the Czech Republic, Poland and Hungary. |

| 15 | For example, one dummy for Australia-Austria, but also one dummy for Austria-Australia. |

| 16 | |

| 17 | The variables target_openness and foreign_capstock_share_lagged show a correlation coefficient of 0.75, indicating that the capital stock variable swallows the explanatory power of trade openness; see Table A1 and Table A2 in the Appendix A. |

| 18 | Barrell et al. (2017) were the first to take on a different modelling approach. Their findings are quite similar to ours, however they did not use fixed effects and as well FDI stocks rather than FDI flows. |

| Study | Data | Model | OLS Results | PPML Results |

|---|---|---|---|---|

| Straathof et al. (2008) | OECD stock (1981–2005) | OLS dyadic fixed | +14% (from EU outsiders), +28% (from EU insiders) | |

| Fournier et al. (2015) | OECD flow (mid-1990s–2011) | OLS country fixed, ppml country fixed | +57% (if target is EU), +48% (if origin is EU) | +48% (if target is EU), +58% (if origin is EU) |

| Bruno et al. (2016) | OECD flow (1985–2012) | OLS dyadic fixed, ppml dyadic fixed, Heckmann Sample Selection | +33% (if target is EU) | +38% (if target is EU), +129% (if origin is EU) |

| Variables | Definition | Source |

|---|---|---|

| inflow | Inward FDI flows (origin to target), in current USD | OECD database |

| target_gdp | GDP of FDI target country, in current USD | World Bank |

| origin_gdp | GDP of FDI origin country, in current USD | World Bank |

| target_gdp_per_capita | GDP per capita of FDI target country, in current USD | World Bank |

| origin_gdp_per_capita | GDP per capita of FDI origin country, in current USD | World Bank |

| target_openness | Total imports plus total exports of FDI target country, divided by its GDP | World Bank |

| foreign_capstock_share_lagged | Total FDI inward stock in the target country (in current USD) by total inward capital stock (converted from constant 2011 national prices into current USD); lagged by one year | OECD database; Feenstra et al. (2015) for conversion methodology |

| target_corporate_taxrate | General corporate tax rates, including average/typical local taxes | Mintz and Weichenrieder (2010); KPMG (2017) |

| target_rer | Nominal exchange rates (target country to USD) multiplied by US consumer price index, divided by home consumer price index | OECD database |

| (1) | (2) | (3) | (4) | |

|---|---|---|---|---|

| Variables | Inflow | Inflow | Inflow | Inflow |

| target_eu | 0.235 | 0.135 | 0.0378 | 0.124 |

| (0.152) | (0.151) | (0.157) | (0.161) | |

| origin_eu | 0.589 *** | 0.504 *** | 0.511 *** | 0.480 *** |

| (0.205) | (0.184) | (0.184) | (0.181) | |

| ln_target_gdp | 1.346 | 3.958 ** | 3.859 ** | 3.204 * |

| (1.519) | (1.966) | (1.907) | (1.700) | |

| ln_origin_gdp | 1.766 * | 1.269 | 1.302 | 1.178 |

| (1.073) | (1.083) | (1.068) | (1.017) | |

| ln_target_gdp_per_capita | 0.185 | −2.233 | −2.216 | −1.972 |

| (1.642) | (1.880) | (1.829) | (1.684) | |

| ln_origin_gdp_per_capita | −1.104 | −0.529 | −0.580 | −0.431 |

| (1.132) | (1.156) | (1.135) | (1.097) | |

| ln_target_rer | 0.819 | 1.305 * | 1.177 * | 1.004 |

| (0.629) | (0.716) | (0.709) | (0.674) | |

| target_corporate_taxrate | −4.077 *** | −3.775 *** | −3.804 *** | |

| (1.165) | (1.136) | (1.096) | ||

| target_openness | 0.634 ** | 0.161 | ||

| (0.290) | (0.324) | |||

| foreign_capstock_share_lagged | 2.092 *** | |||

| (0.795) | ||||

| Observations | 15,359 | 15,359 | 15,359 | 15,359 |

| R-squared | 0.639 | 0.648 | 0.655 | 0.657 |

| (5) | (6) | (7) | (8) | |

|---|---|---|---|---|

| VARIABLES | Inflow | Inflow | Inflow | Inflow |

| target_eu_singlemarket | 0.545 ** | 0.468 ** | 0.408 ** | 0.349 * |

| (0.215) | (0.196) | (0.204) | (0.190) | |

| origin_eu_singlemarket | 0.634 *** | 0.618 *** | 0.626 *** | 0.602 *** |

| (0.216) | (0.204) | (0.199) | (0.198) | |

| ln_target_gdp | 2.958 | 5.280 ** | 5.078 ** | 4.276 ** |

| (1.854) | (2.201) | (2.165) | (1.954) | |

| ln_origin_gdp | 2.562 ** | 2.096 * | 2.152 ** | 2.000 * |

| (1.079) | (1.097) | (1.088) | (1.048) | |

| ln_target_gdp_per_capita | −1.704 | −3.841 * | −3.703 * | −3.203 |

| (1.996) | (2.194) | (2.157) | (1.986) | |

| ln_origin_gdp_per_capita | −2.003 * | −1.463 | −1.539 | −1.359 |

| (1.163) | (1.195) | (1.180) | (1.154) | |

| ln_target_rer | 0.558 | 1.022 | 0.920 | 0.834 |

| (0.562) | (0.642) | (0.639) | (0.612) | |

| target_corporate_taxrate | −3.936 *** | −3.653 *** | −3.720 *** | |

| (1.080) | (1.076) | (1.040) | ||

| target_openness | 0.576 * | 0.157 | ||

| (0.304) | (0.329) | |||

| foreign_capstock_share_lagged | 1.945 ** | |||

| (0.780) | ||||

| Observations | 15,359 | 15,359 | 15,359 | 15,359 |

| R-squared | 0.645 | 0.654 | 0.659 | 0.661 |

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Welfens, P.J.J.; Baier, F.J. BREXIT and Foreign Direct Investment: Key Issues and New Empirical Findings. Int. J. Financial Stud. 2018, 6, 46. https://doi.org/10.3390/ijfs6020046

Welfens PJJ, Baier FJ. BREXIT and Foreign Direct Investment: Key Issues and New Empirical Findings. International Journal of Financial Studies. 2018; 6(2):46. https://doi.org/10.3390/ijfs6020046

Chicago/Turabian StyleWelfens, Paul J. J., and Fabian J. Baier. 2018. "BREXIT and Foreign Direct Investment: Key Issues and New Empirical Findings" International Journal of Financial Studies 6, no. 2: 46. https://doi.org/10.3390/ijfs6020046

APA StyleWelfens, P. J. J., & Baier, F. J. (2018). BREXIT and Foreign Direct Investment: Key Issues and New Empirical Findings. International Journal of Financial Studies, 6(2), 46. https://doi.org/10.3390/ijfs6020046