2.1. Industry and Porter’s Five Forces

Porter’s five forces model sets an analytical framework for understanding the influence of an industry’s structure on the profit potential of the firms within the industry. This framework is one of the most significant contributions to the strategic field using industrial organisation economic logic (

Bridoux 2004) since, as stated by

Hawawini et al. (

2003), the structural characteristics of industries are the primary determinants of performance.

It builds on the structure-conduct-performance (SCP) paradigm from industrial organisation economics. The SCP paradigm argues that performance is determined by the conduct of the firms, which in turn is determined by the structural characteristics of the market (

Clark 1998).

According to

Porter (

1979) the state of competition in an industry depends on five basic forces: the threat of new entrants, the bargaining power of customers, the bargaining power of suppliers, the threat of substitute products or services, and the rivalry among current contestants. The combined strength of these forces defines the ultimate profit potential of an industry. Specifically, when the industrial rivalry is not strong, companies have the ability to raise prices and hence earn higher profits. Likewise, the larger the bargaining power of customers/suppliers and the larger the threat of new entrants, the lower the firm’s profitability. Finally, if the substitution of a company’s products or services is fairly easy and of low cost, then the company’s power can be weakened, and the firm’s profitability can be reduced. Awareness of these forces can help the company take a position in its industry that is less vulnerable to attack. As noted by

Grigore (

2014), the industry’s structure, manifested in the competitive forces, sets industry profitability in the medium and long term.

The ultimate function of Porter’s competitive strategy is to explain the sustainability of profits against bargaining and against direct and indirect competition (

Porter 1991).

Huang et al. (

2015) tried to integrate both industrial organisation theory (IO) and the resource-based view of the firm (RBV) in order to clarify the conceptual distinction between two types of competitive advantage—the temporary and the sustainable competitive advantage. The results supported the IO theorists’ proposition that a firm’s temporary competitive advantage can be gained via strengthening its market position in an industry. However, further testing suggested that a firm’s market position in an industry had no influence on the firm’s sustainable competitive advantage outcomes, supporting an argument that the competitive advantage resulting from entry barriers or market concentration is temporary. Similarly,

Rivard et al. (

2006) tested an integrated model (including both a resource-based view and competitive strategy) of the contribution of IT to the firm’s performance since, as stated by

Porter and Millar (

1985), IT is seen as a means by which firms can gain competitive advantage by altering the competitive forces that collectively determine the industry’s profitability. The relationship between industry forces and performance suggests that greater environmental hostility is somewhat associated with lower performance in terms of market performance, but not in terms of profitability.

Spanos and Lioukas (

2001) have investigated the relative impact of industry- and firm-specific factors on sustainable competitive advantage, referring also to both Porter’s framework of competitive strategy and the resource-based view of the firm.

Espallardo and Ballester (

2009) studied whether the effectiveness of innovation in improving a firm’s performance varies in different competitive situations, and analysed whether the competitive forces act as a motivator or as an inhibitor, finding that small firms must invest in innovation, preferably when competitive forces are more intense. Furthermore,

Pecotich et al. (

1999) developed an industruct, an instrument designed to measure perceptions of industry structure based on Porter’s five competitive forces formulation finding that rivalry and entry were the highest forces.

However, Porter’s work has been widely criticised and, as stated by

Dobbs (

2014), has laid the groundwork for an unnecessary and unfortunate battle for paradigm dominance between Porter’s five forces and the resource-based view of the firm. Despite this, Porter’s five forces model has been widely exploited and applied. For example,

Lüttgens and Diener (

2016) have adopted Porter’s five forces in order to analyse different threats to a business model, as well as to evaluate different business model patterns and rate them according to their impact on each of Porter’s forces.

Sutherland (

2014) has extended Porter’s five forces model to include nonmarket actions in the telecommunications sector, finding it a useful tool for analysing advocacy, lobbying and litigation by players in this heavily regulated market. Furthermore,

Wu and Yang (

2014) have applied Porter’s five forces model to gain insight into the competitive landscape of the shale gas market in China.

Taking into account all of the factors stated above, the five forces framework and the resource-based view of the firm can be considered complementary perspectives rather than adversarial, as is commonly the case (

Dobbs 2014 citing (

Makhija 2012;

Ronda-Pupo and Guerras-Martin 2012)). Specifically, linking five forces assessments to opportunities and threats can help strategic thinkers develop powerful responses to industry pressures in order to improve competitiveness and increase profit.

With the aforementioned in mind, we formulate the following hypothesis:

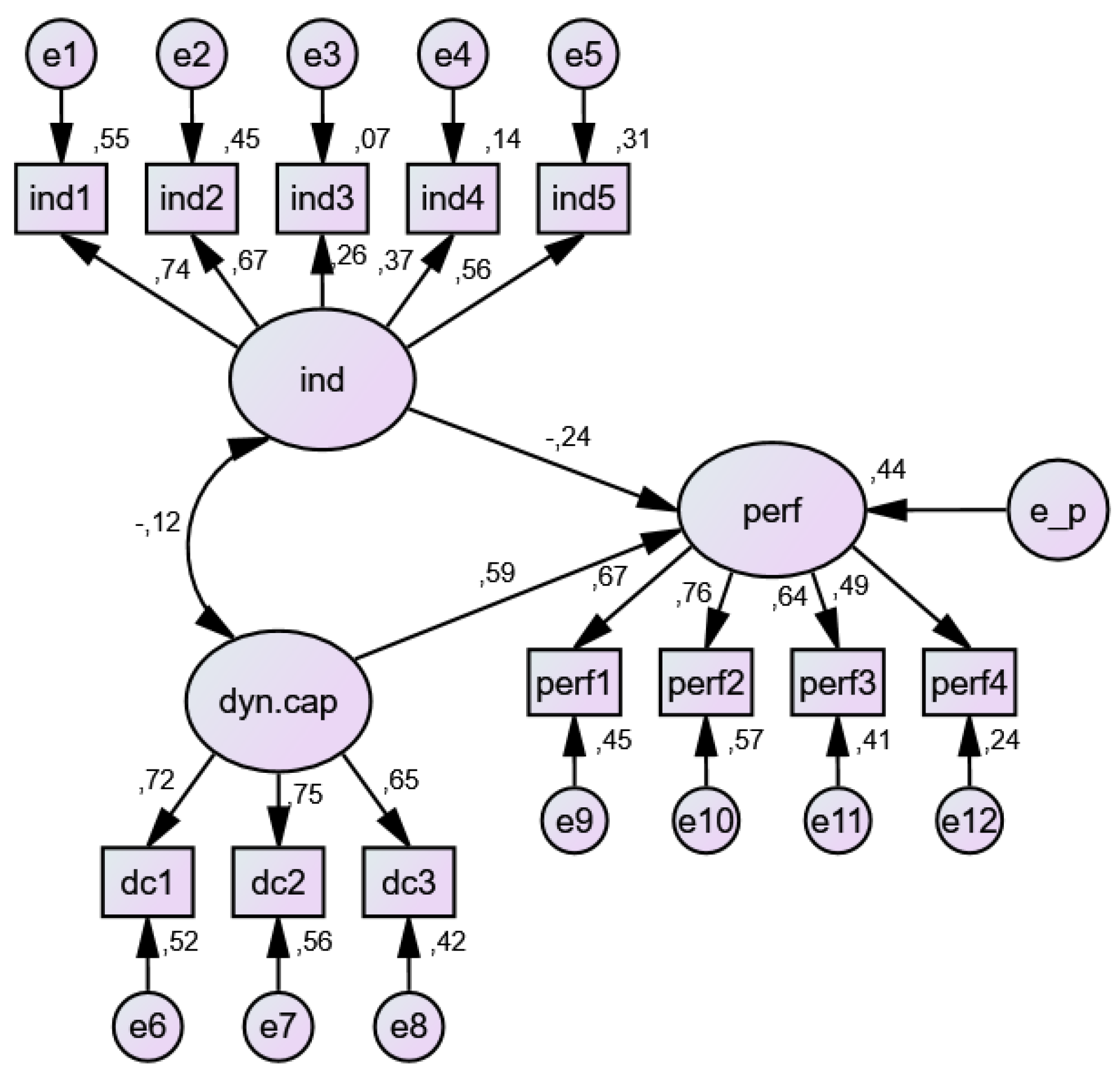

H1. The industry within which a firm operates significantly influences the firm’s performance.

2.2. Dynamic Capabilities

Alongside the external orientation, especially since the 1980s, the resource-based view has been advanced as an explanation of the determinants of a company’s success. Although the importance of the internal factors for the firm’s competitive advantage and performance was highlighted in Penrose’s theory of firm growth in the 1950s, the resource-based view has developed with the works of

Wernerfelt (

1984),

Rumelt (

1984) and, particularly, those of

Barney (

1986,

1991). Reviews of the empirical research in the field have been given by

Barney and Arikan (

2001),

Crook et al. (

2008), and

Newbert (

2008).

Resources include “all assets, capabilities, organizational processes, firm attributes, information, knowledge, etc. controlled by a firm that enabled the firm to conceive of and implement strategies that improve its efficiency and effectiveness” (

Barney 1991). They encompass financial, physical, human, organisational assets (

Barney 1991), as well as intellectual resources (

Newbert 2008).

The resource-based theory is founded on two important assumptions: heterogeneity and immobility of resources between the firms (

Barney 1991). The first assumption implies differences in resources and strategies to compete among companies that could result in competitive advantage. Immobility means that resources do not transfer from company to company, or that companies are not able to replicate resources of other companies or to implement the same strategies. In order to produce competitive advantage, the resources have to be valuable, rare, inimitable, and non-substitutable (

Barney 1991). These features of resources are implemented in the widely known VRIN framework.

As an extension of the resource-based view, pioneered by the works of

Teece and Pisano (

1994),

Teece et al. (

1997),

Eisenhardt and Martin (

2000), and

Zollo and Winter (

2002),

Winter (

2003), and continuing with the studies of

Helfat et al. (

2007),

Teece (

2007),

Wang and Ahmed (

2007),

Augier and Teece (

2009),

Teece (

2014),

Wang et al. (

2015),

Teece (

2017), and many others, the concept of dynamic capabilities has advanced in order to provide additional explanation for the firm’s performance from an internal perspective. This theoretical approach tries to explain how valuable, rare, inimitable, and non-substitutable resources can be created, as well as how the resources can be restored in changing environment in which the company operates in order to generate and sustain competitive advantage (

Ambrosini and Bowman 2009) and improve the firm’s performance.

According to the dynamic capabilities approach, possessing valuable, rare, inimitable, and non-substitutable resources without dynamic capabilities does not enable the firm to sustain a competitive advantage and performance. In a changing environment, resources cannot remain static and still be valuable; on the contrary, dynamic capabilities are needed to regenerate the resources (

Ambrosini and Bowman 2009). With the shift from external to internal orientation in the field of strategic management, particular attention has been paid to the cognitive and behavioural processes that are important for capabilities that influence the firm’s performance (

Hodgkinson and Healey 2011, p. 501).

The dynamic capabilities approach has been developed on the basis of many contributions, both theoretically and empirically. However, the concept is characterised by its fragmentation. This is true for both definitions and conceptualisations of dynamic capabilities, which has an impact on empirical research (

Arend and Bromiley 2009;

Vogel and Güttel 2013;

Burisch and Wohlgemuth 2016).

According to

Teece et al. (

1997), dynamic capability is “the firm’s ability to integrate, build, and reconfigure internal and external competences to address rapidly changing environments.” Many other supporters of the dynamic capabilities perspective provide their own definitions of capabilities.

Eisenhardt and Martin (

2000) state that dynamic capabilities are “the firm’s processes that use resources—specifically the processes to integrate, reconfigure, gain and release resources—to match and even create market change. Dynamic capabilities are thus the organizational and strategic routines by which firms achieve new resource configurations as markets emerge, collide, split, evolve, and die”.

According to

Zahra et al. (

2006), dynamic capabilities are “abilities to reconfigure a firm’s resources and routines in the manner envisioned and deemed appropriate by its principal decision-maker”.

Helfat et al. (

2007) define dynamic capability as “the capacity of an organization to purposefully create, extend or modify its resource base”. According to

Wang and Ahmed (

2007) dynamic capability is “a firm’s behavioural orientation constantly to integrate, reconfigure, renew and recreate its resources and capabilities and, most importantly, upgrade and reconstruct its core capabilities in response to the changing environment to attain and sustain competitive advantage.”

Despite numerous approaches to defining dynamic capabilities, it is possible to isolate a common feature; namely, that dynamic capabilities are a firm’s processes that adopt resources in accordance with changes of environment. There are two levels of capabilities: ordinary and dynamic (

Winter 2003). In comparison to operational and other ordinary capabilities that are important for the firm’s current activities, dynamic capabilities enable a change of resources and ordinary capabilities (

Cepeda and Vera 2007). Hence, dynamic capabilities use the existing resources and create new resources and capabilities, aligning the organisation to the change in the environment. According to

Wang and Ahmed (

2007), there are three main components of dynamic capabilities: adaptive capability, absorptive capability, and innovative capability. The first one refers to the capability of the firm to identify and take the advantage of the market opportunities. The capability to identify new information, and to assimilate and exploit it is denoted as absorptive capability.

Zahra and George (

2002) define absorptive capacity as “a dynamic capability that influences the firm’s ability to create and deploy the knowledge necessary to build other organizational capabilities”. Innovative capability describes the capability of developing new products and/or markets.

According to Teece’s approach (2007), which is followed in this study, dynamic capabilities are divided into three components. The first one is the capacity to sense and shape opportunities and threats, implying “scanning, creation, learning, and interpretive activities” (

Teece 2007). These opportunities are primarily related to markets and technologies. The processes include analysing customers (the changes of their needs and innovations), suppliers and competitors, processes aimed at directing internal research and development, and processes aimed at tapping developments in technology. Moreover, in comparison to the industrial perspective, the dynamic capabilities approach includes a more comprehensive view of the environment in which the firm operates. It encompasses the business “ecosystem”—the community of individuals and organisations, including buyers, complementors, suppliers, labour market, educational and research institutions, financial institutions, regulatory authorities, and the legal system (

Teece 2007). Thus, in addition to exploring the market and technology, it is important to scan other elements of the “ecosystem”, as well. Without these activities, the firms would not be able to recognize the opportunities that could be visible to other firms (

Teece 2007).

The second one is the capability to seize opportunities, which involves addressing sensed opportunities through new products, services or processes, which requires a mobilisation of resources (e.g., financial, human), investment in development, and commercialisation (

Teece 2007). According to

O’Reilly and Tushman (

2008), this is the ability to make the right decisions and execute them, while from the organisational perspective, “this requires leaders who can craft a vision and strategy, ensure the proper organizational alignments (whether it is for exploitation or exploration), assemble complementary assets, and decide on resource allocation and timing.”

The third component refers to the capability of keeping competitiveness through enhancing, combining, protecting, and reconfiguring the company’s assets, both intangible and tangible, as well as operating capabilities. It may encompass a change in business model, mergers, acquisitions and divestments (

Teece 2007). According to

Helfat and Peteraf (2003), there are two forms of capability redeployment: sharing of a capability between the old and the new market, and inter-temporal transfer of capabilities from one market to another. There are numerous ways dynamic capabilities can influence the firm’s performance. Successful recognition and assessment of opportunities related to markets and technologies, as well as the design of new products and business models, can result in a competitive advantage and profitability (

Teece 2007). Adapting the resource base to the changes in the business “ecosystem,” as well as shaping it (creating market change), may enhance profitability. Moreover, dynamic capabilities could improve the efficiency of the firm’s reaction to environmental dynamism, which positively affects performance. Dynamic capabilities may enhance inter-firm performance. They provide new decision options that could generate higher profitability (

Wilden et al. 2013). Dynamic capabilities allow “the firm to take advantage of revenue enhancing opportunities and adjust its operations to reduce costs” (

Drnevich and Kriauciunas 2011).

According to

Eisenhardt and Martin (

2000), dynamic capabilities do not necessarily result in increased performance, since performance is not directly related to dynamic capabilities but to the configuration of resources affected by dynamic capabilities. Some other researchers also argue that the effect of dynamic capabilities on performance is indirect, with a mediating role of the firm’s operational capabilities (

Helfat and Peteraf 2003;

Zahra et al. 2006;

Pavlou and El Sawy 2011). Moreover, there are costs associated with dynamic capabilities that could have negative effects on the firm’s performance (

Zollo and Winter 2002;

Winter 2003).

Zott (

2003) shows that differences in performance among firms are related to the costs of dynamic capabilities.

Considering the empirical validation of the concept of dynamic capabilities,

Ambrosini and Bowman (

2009), and

Arend and Bromiley (

2009) highlight limited empirical support.

Vogel and Güttel (

2013) state that “the dynamic capability view still lacks consensual concepts that allow comparisons of empirical studies”. Some studies find empirical support of the dynamic capabilities approach (e.g.,

Zott 2003;

Fang and Zou 2009;

Drnevich and Kriauciunas 2011), while some papers confirm that the effect of dynamic capabilities on a firm’s competitive advantage/performance is contingent on specific factors, such as the firm’s organisational structure and the intensity of competition the firm faces (

Wilden et al. 2013), or the degree of dynamism of the firm’s external environment, showing a weaker effect in the context of high and low environmental dynamism in comparison to in the context of a moderate one (

Schilke 2014). In the assessment of empirical research on the relationship between dynamic capabilities and performance,

Pezeshkan et al. (

2015) found that the dynamic capabilities approach is confirmed empirically in 60 percent of studies. The differences in empirical support result from the type and nature of dynamic capabilities, the type of performance measures used in the analyses, whether dynamic capabilities are analysed independently or in interaction with other variables (contextual or organisational), as well as from the research design features (

Pezeshkan et al. 2015).

With respect to the above-stated theoretical considerations and the results of empirical research, we formulate the second hypothesis of the present research:

H2. Dynamic capabilities positively influence the firm’s performance.

Although supporters of both external and internal orientation approaches for explaining a firm’s performance have found empirical validation of their views, some researchers hold that an integrated view could better explain the sources of a firm’s performance (

Hansen and Wernerfelt 1989;

Henderson and Mitchell 1997;

Hoskisson et al. 1999;

Spanos and Lioukas 2001). Following this approach, in the subsequent section of the study, we empirically analyse the importance of both external or industry factors, and of dynamic capabilities, as internal factors for the firm’s success.

{kind=link}