From Policy Mandates to Market Signals: Causal and Dynamic Effects of Carbon Information Disclosure on Firm Value

Abstract

1. Introduction

2. Literature Review and Hypothesis Development

2.1. Causal Effects of Carbon Information Disclosure: Evidence from an Environmental Policy Shock

2.2. Dynamic Effects of Carbon Information Disclosure on Firm Value

2.3. Moderating Effects of Environmental Regulation on the Relationship Between Carbon Information Disclosure and Firm Value

2.4. Summary and Research Gaps

3. Methodology

3.1. Research Design

3.2. Sample Selection and Variable Measurement

3.3. Identification Strategy and Model Specification

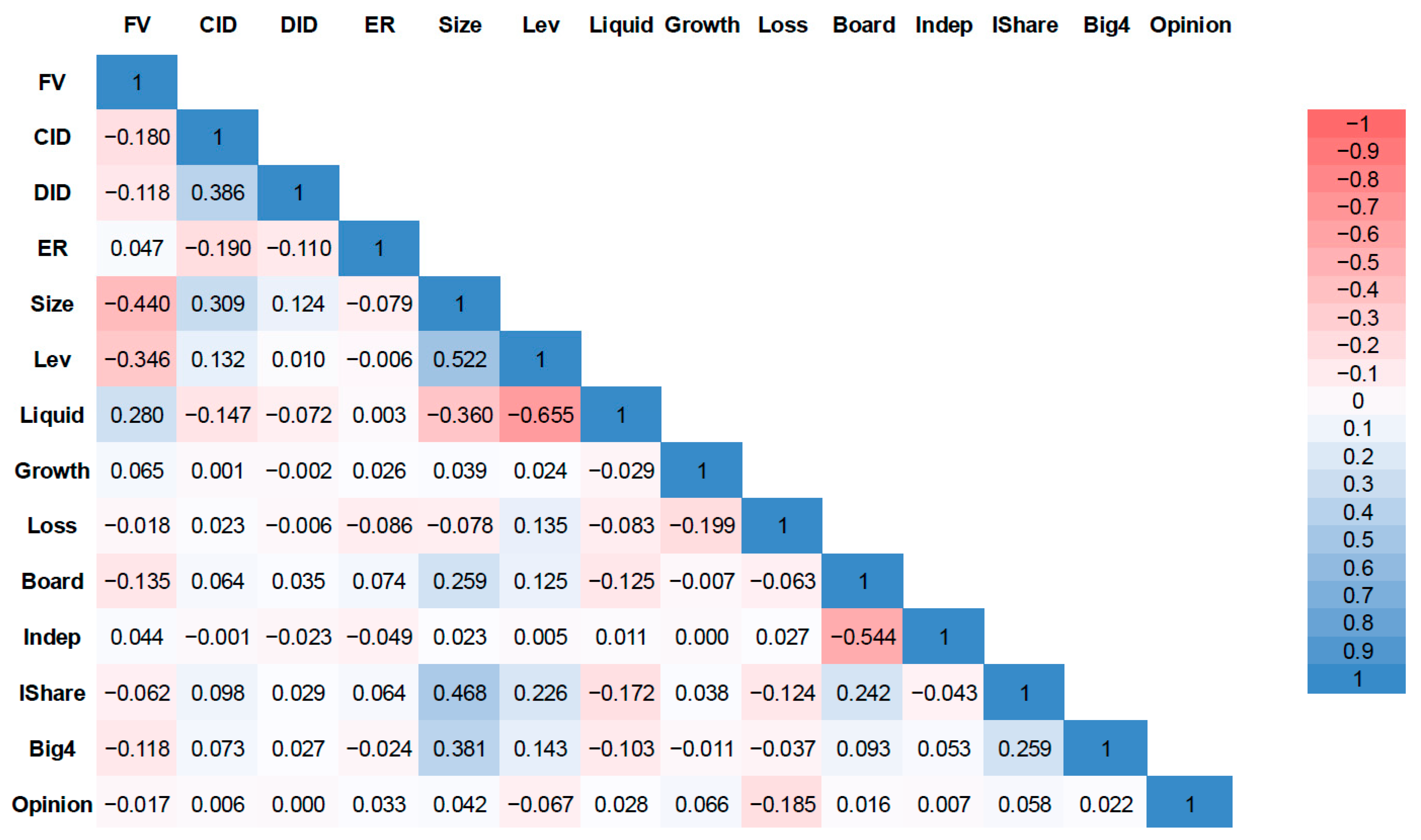

3.4. Descriptive Statistics and Correlation Analysis

4. Empirical Results

4.1. Causal Effects of Policy-Induced Carbon Information Disclosure on Firm Value

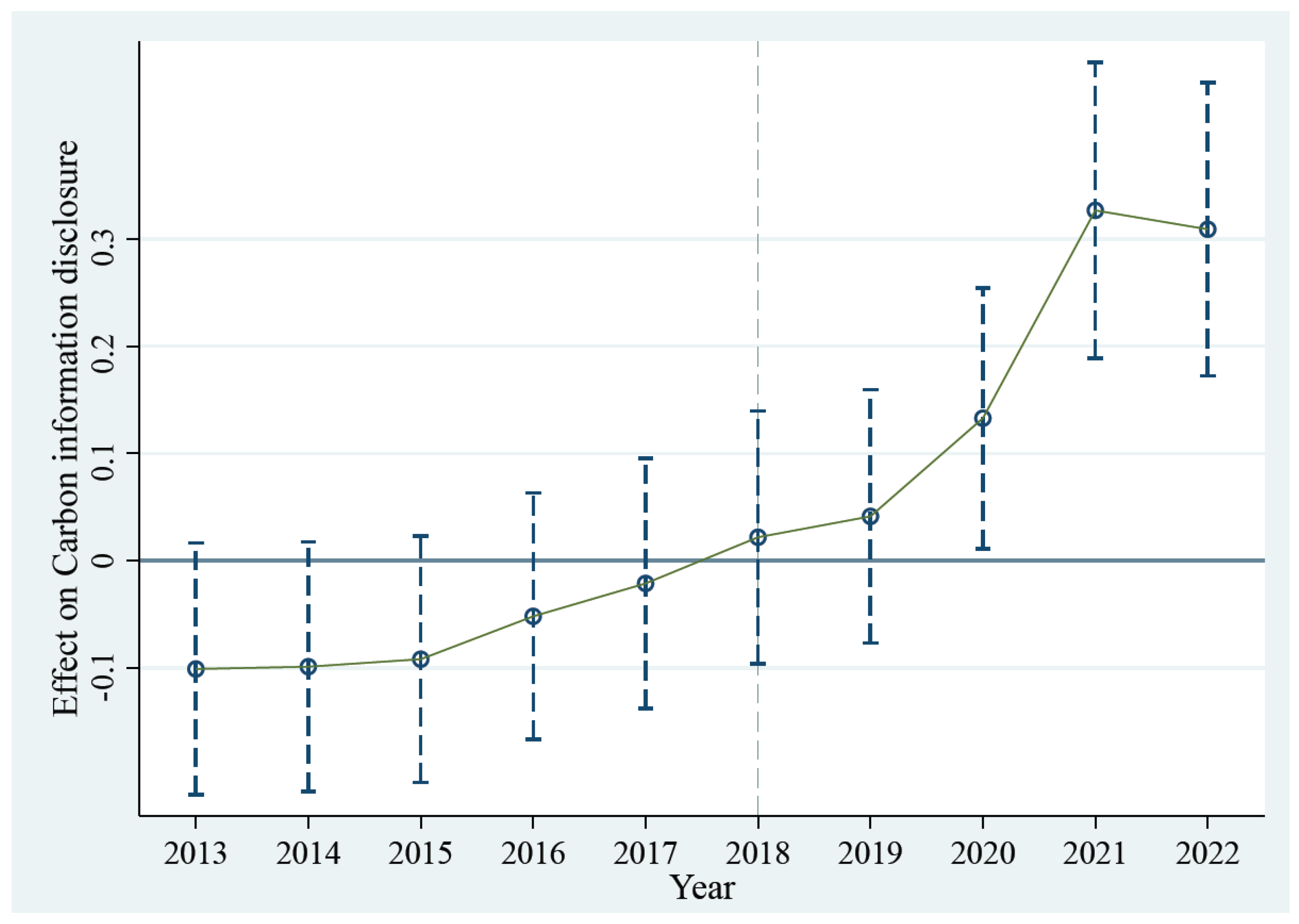

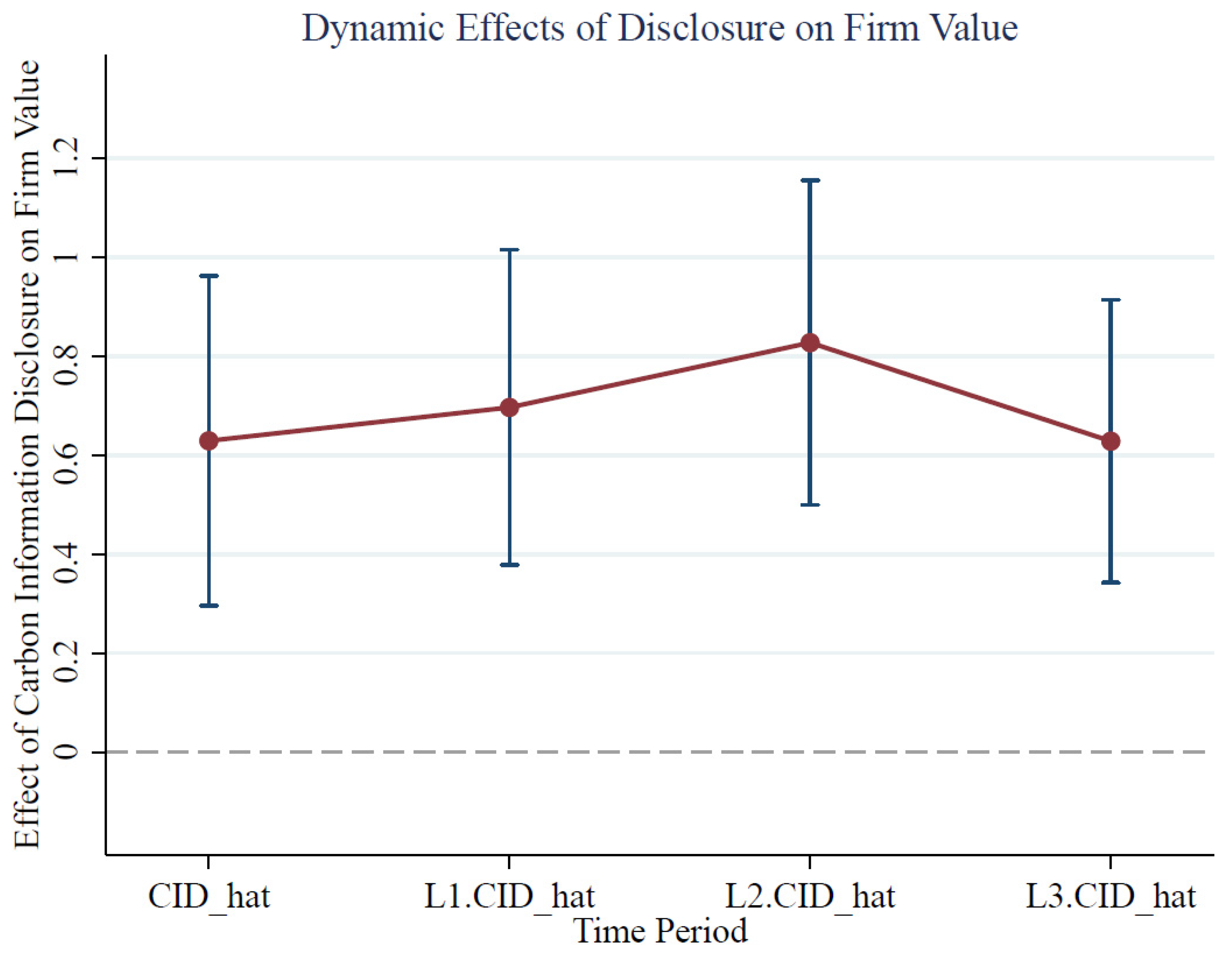

4.2. Dynamic Valuation Effects of Policy-Induced Carbon Information Disclosure

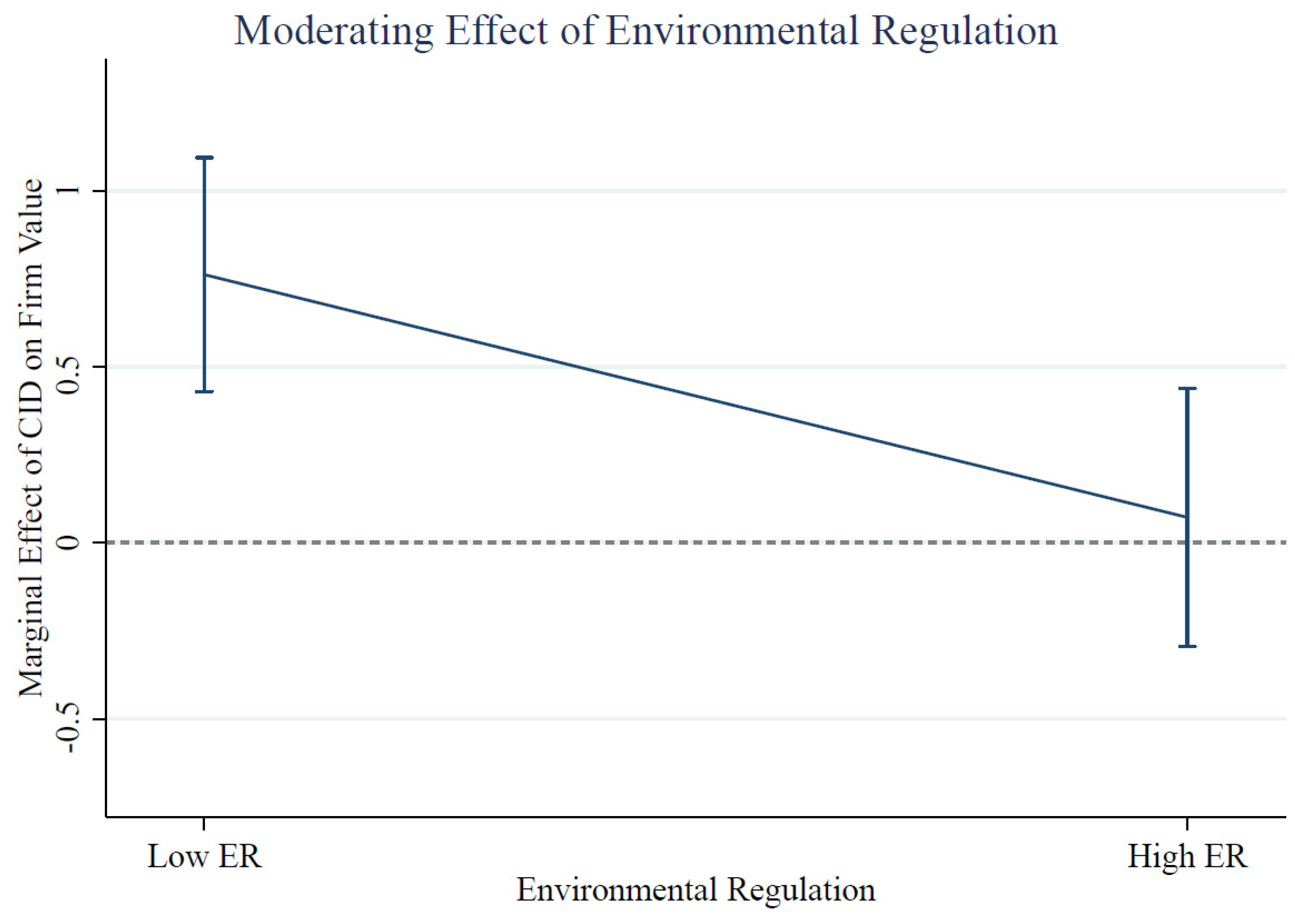

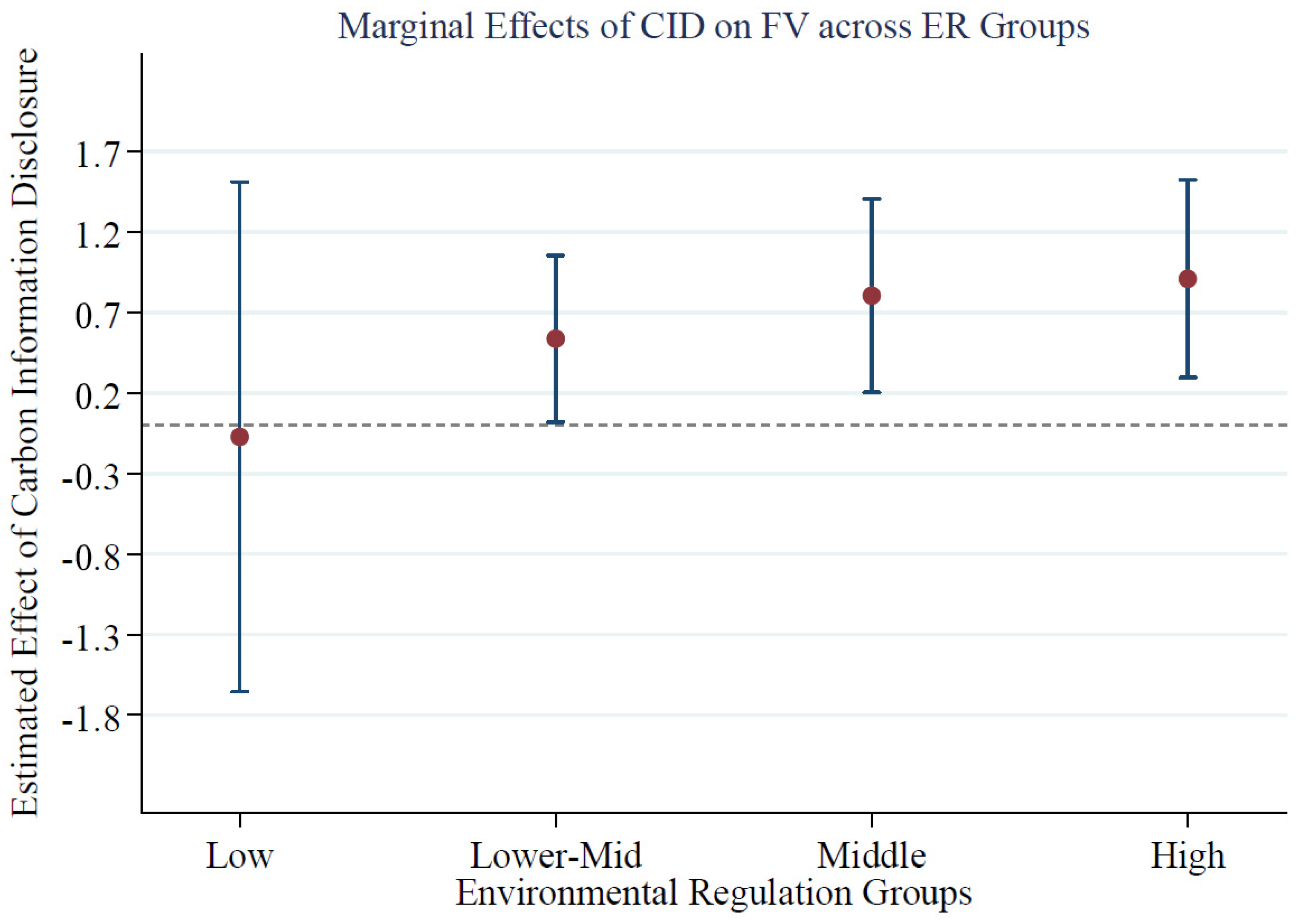

4.3. Moderating Role of Environmental Regulation

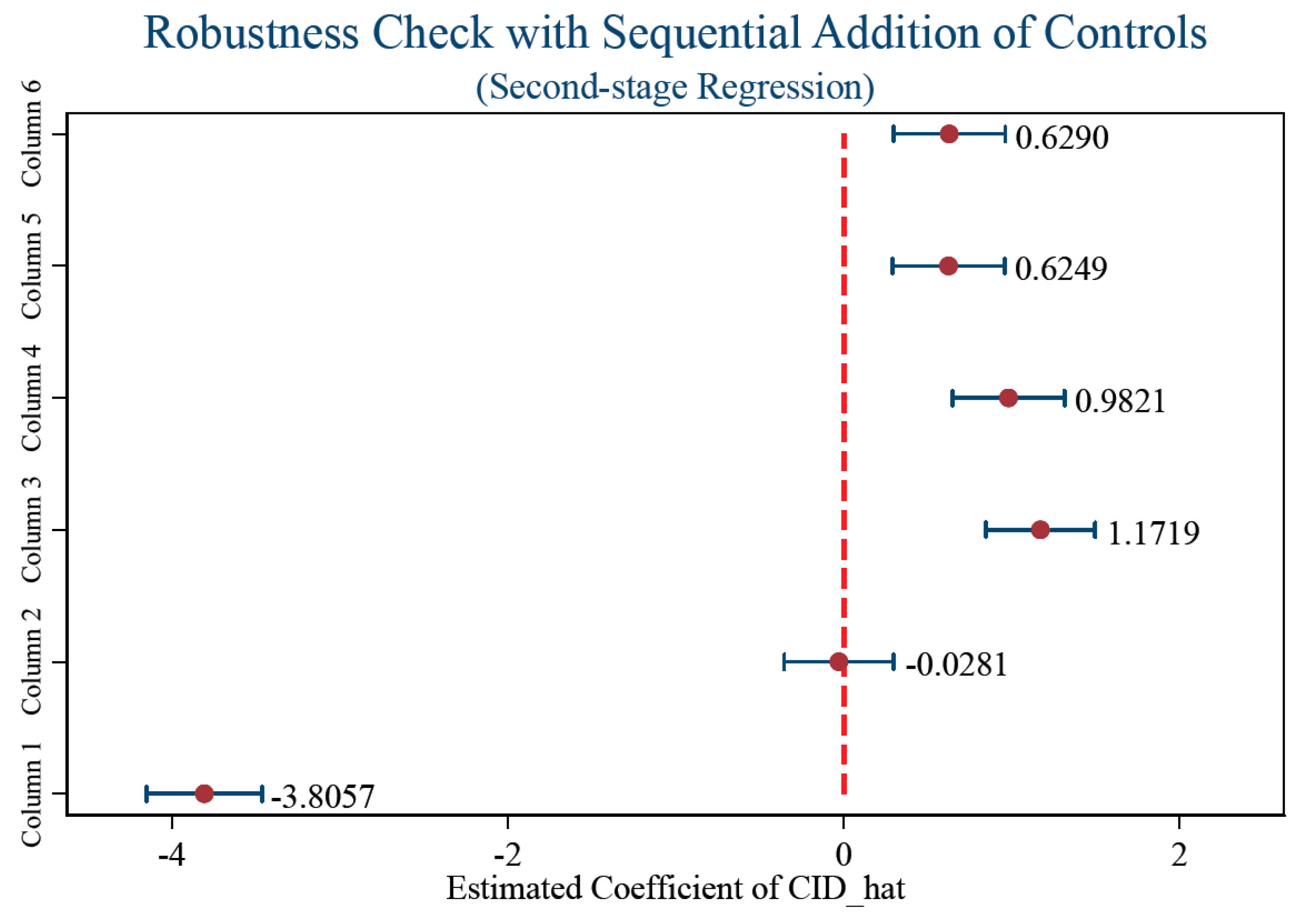

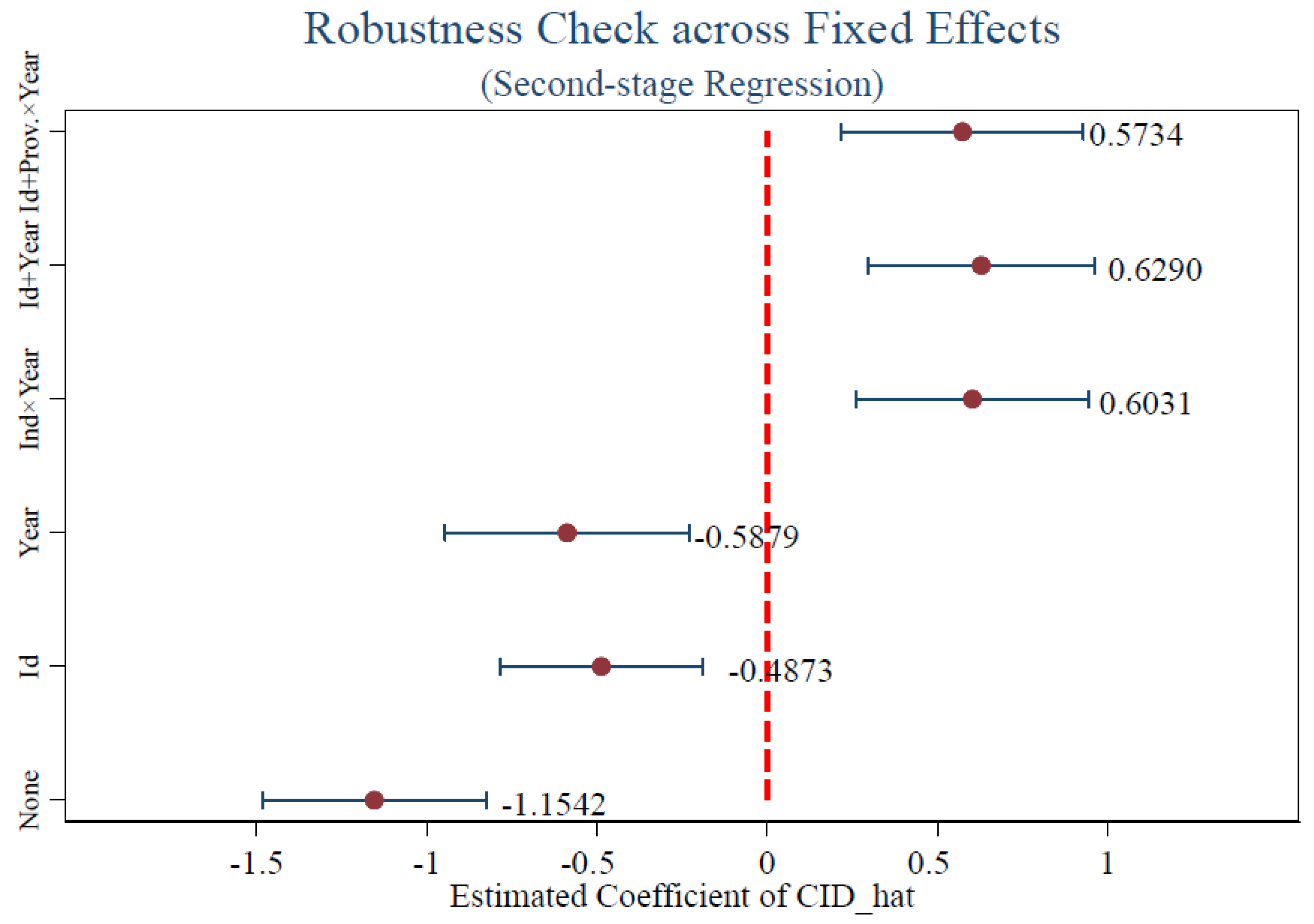

4.4. Robustness Tests

5. Conclusions and Implications

5.1. Key Findings and Contributions

5.2. Policy and Managerial Implications

5.3. Limitations and Future Research

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Abbreviations

| CID | carbon information disclosure |

| FV | firm value |

| ER | environmental regulation |

| DID | difference-in-differences |

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Variables | VIF | 1/VIF |

|---|---|---|

| Lev | 2.22 | 0.451426 |

| Size | 2.14 | 0.467208 |

| Liquid | 1.78 | 0.562632 |

| Board | 1.63 | 0.61329 |

| Indep | 1.49 | 0.671408 |

| IShare | 1.35 | 0.742063 |

| CID | 1.32 | 0.75836 |

| Big4 | 1.19 | 0.837162 |

| DID | 1.19 | 0.843196 |

| Loss | 1.14 | 0.874889 |

| ER | 1.07 | 0.935326 |

| Growth | 1.05 | 0.954768 |

| Opinion | 1.04 | 0.957739 |

| Mean VIF | 1.43 | |

References

- Ameli, N., Drummond, P., Bisaro, A., Grubb, M., & Chenet, H. (2020). Climate finance and disclosure for institutional investors: Why transparency is not enough. Climatic Change, 160, 565–589. [Google Scholar] [CrossRef]

- Aragòn-Correa, J. A., Marcus, A. A., & Vogel, D. (2020). The effects of mandatory and voluntary regulatory pressures on firms’ environmental strategies: A review and recommendations for future research. Academy of Management Annals, 14, 339–365. [Google Scholar] [CrossRef]

- Borghei, Z. (2021). Carbon disclosure: A systematic literature review. Accounting & Finance, 61, 5255–5280. [Google Scholar]

- Bu, C., Zhang, K., Shi, D., & Wang, S. (2022). Does environmental information disclosure improve energy efficiency? Energy Policy, 164, 112919. [Google Scholar] [CrossRef]

- Cao, Q., Zhou, Y., Du, H., Ren, M., & Zhen, W. (2022). Carbon information disclosure quality, greenwashing behavior, and enterprise value. Frontiers in Psychology, 13, 892415. [Google Scholar] [CrossRef] [PubMed]

- Clementino, E., & Perkins, R. (2021). How do companies respond to environmental, social and governance (ESG) ratings? Evidence from Italy. Journal of Business Ethics, 171, 379–397. [Google Scholar] [CrossRef]

- Connelly, B. L., Certo, S. T., Reutzel, C. R., DesJardine, M. R., & Zhou, Y. S. (2025). Signaling theory: State of the theory and its future. Journal of management, 51, 24–61. [Google Scholar] [CrossRef]

- Ding, D., Liu, B., & Chang, M. (2023). Carbon emissions and TCFD aligned climate-related information disclosures. Journal of Business Ethics, 182, 967–1001. [Google Scholar] [CrossRef]

- Diwan, H., & Amarayil Sreeraman, B. (2024). From financial reporting to ESG reporting: A bibliometric analysis of the evolution in corporate sustainability disclosures. Environment, Development and Sustainability, 26, 13769–13805. [Google Scholar] [CrossRef]

- Du, M., Chai, S., Wei, W., Wang, S., & Li, Z. (2022). Will environmental information disclosure affect bank credit decisions and corporate debt financing costs? Evidence from China’s heavily polluting industries. Environmental Science and Pollution Research, 29, 47661–47672. [Google Scholar] [CrossRef] [PubMed]

- Dutta, P., & Dutta, A. (2021). Impact of external assurance on corporate climate change disclosures: New evidence from Finland. Journal of Applied Accounting Research, 22, 252–285. [Google Scholar] [CrossRef]

- Flammer, C., Toffel, M. W., & Viswanathan, K. (2021). Shareholder activism and firms’ voluntary disclosure of climate change risks. Strategic Management Journal, 42, 1850–1879. [Google Scholar] [CrossRef]

- Grewal, J., Richardson, G. D., & Wang, J. (2022). Effects of mandatory carbon reporting on unrepresentative environmental disclosures. SSRN, 4166184. [Google Scholar] [CrossRef]

- Han, Y. (2020). Impact of environmental regulation policy on environmental regulation level: A quasi-natural experiment based on carbon emission trading pilot. Environmental Science and Pollution Research, 27, 23602–23615. [Google Scholar] [CrossRef] [PubMed]

- Hardiyansah, M., Agustini, A. T., & Purnamawati, I. (2021). The effect of carbon emission disclosure on firm value: Environmental performance and industrial type. The Journal of Asian Finance, Economics and Business, 8, 123–133. [Google Scholar]

- He, R., Luo, L., & Tang, Q. (2022). Usefulness of corporate carbon information for decision-making. In Information for efficient decision making: Big data, blockchain and relevance (pp. 451–476). World Scientific. [Google Scholar]

- Huang, D. Z. X. (2022). Environmental, social and governance factors and assessing firm value: Valuation, signalling and stakeholder perspectives. Accounting & Finance, 62, 1983–2010. [Google Scholar]

- Huang, H., Zou, Y., Wang, L., Wang, W., & Ren, X. (2025). Impact of carbon information disclosure on corporate financing constraints: Evidence from the Carbon Disclosure Project. Australian Journal of Management, 50, 104–131. [Google Scholar] [CrossRef]

- Kadim, A., Sunardi, N., & Husain, T. (2020). The modeling firm’s value based on financial ratios, intellectual capital and dividend policy. Accounting, 6, 859–870. [Google Scholar] [CrossRef]

- Karplus, V. J., Zhang, J., & Zhao, J. (2021). Navigating and evaluating the labyrinth of environmental regulation in China. Review of Environmental Economics and Policy, 15, 300–322. [Google Scholar] [CrossRef]

- Krueger, P., Sautner, Z., Tang, D. Y., & Zhong, R. (2024). The effects of mandatory ESG disclosure around the world. Journal of Accounting Research, 62, 1795–1847. [Google Scholar] [CrossRef]

- Liu, M., Xia, C., Lan, H., Gao, Z., Yu, X., Wang, L., Liang, X., & Wu, Y. (2024). Driving toward sustainable cities: The interplay between Chinese emerging corporate ESG performance and climate finance in achieving low-carbon development. Urban Climate, 55, 101918. [Google Scholar] [CrossRef]

- Liu, R., Rahman, M. R. C. A., & Jamil, A. H. (2025). Leveraging environmental regulation: How green innovation moderates the relationship between carbon information disclosure and firm value. Sustainability, 17, 2597. [Google Scholar] [CrossRef]

- Liu, Y., Huang, H., Mbanyele, W., Wang, F., & Liu, H. (2024). Does the issuance of green bonds nudge environmental responsibility engagements? Evidence from the Chinese green bond market. Financial Innovation, 10, 92. [Google Scholar] [CrossRef]

- Liu, Y., Li, W., Wang, L., & Meng, Q. (2023). Why greenwashing occurs and what happens afterwards? A systematic literature review and future research agenda. Environmental Science and Pollution Research, 30, 118102–118116. [Google Scholar] [CrossRef] [PubMed]

- Lo, C. W.-H., Liu, N., Pang, X., & Li, P. H. Y. (2020). Unpacking the complexity of environmental regulatory governance in a globalizing world: A critical review for research agenda setting. Journal of Environmental Policy & Planning, 22, 594–607. [Google Scholar]

- Luo, X., Zhang, R., & Liu, W. (2022). Environmental legitimacy pressure, political connection and impression management of carbon information disclosure. Carbon Management, 13, 90–104. [Google Scholar] [CrossRef]

- Lyu, Y., Ye, H., Zhao, Z., Tian, J., & Chen, L. (2020). Exploring the cost of wastewater treatment in a chemical industrial Park: Model development and application. Resources, Conservation and Recycling, 155, 104663. [Google Scholar] [CrossRef]

- Mateo-Márquez, A. J., González-González, J. M., & Zamora-Ramírez, C. (2020). Countries’ regulatory context and voluntary carbon disclosures. Sustainability Accounting, Management and Policy Journal, 11, 383–408. [Google Scholar] [CrossRef]

- Meng, J., & Zhang, Z. (2022). Corporate environmental information disclosure and investor response: Evidence from China’s capital market. Energy Economics, 108, 105886. [Google Scholar] [CrossRef]

- Ministry of Ecology and Environment. (2018). Notice on strengthening the 2018 annual carbon emission report, verification, and emission monitoring plan development work. Available online: https://www.mee.gov.cn/xxgk2018/xxgk/xxgk06/201901/t20190124_690807.html (accessed on 17 January 2019).

- Pan, L., Han, W., Li, Y., & Wu, H. (2022). Legitimacy or efficiency? Carbon emissions transfers under the pressure of environmental law enforcement. Journal of Cleaner Production, 365, 132766. [Google Scholar] [CrossRef]

- Persakis, A., Fassas, A., & Koutoupis, A. (2024). How does world economic policy uncertainty influence the carbon dioxide emission reporting and performance? Study of Fortune Global 500 firms. Environmental Science and Pollution Research, 31, 24014–24041. [Google Scholar] [CrossRef] [PubMed]

- Peters, G. F., & Romi, A. M. (2014). Does the voluntary adoption of corporate governance mechanisms improve environmental risk disclosures? Evidence from greenhouse gas emission accounting. Journal of Business Ethics, 125, 637–666. [Google Scholar] [CrossRef]

- Pitrakkos, P., & Maroun, W. (2020). Evaluating the quality of carbon disclosures. Sustainability Accounting, Management and Policy Journal, 11, 553–589. [Google Scholar] [CrossRef]

- Qian, W., & Schaltegger, S. (2017). Revisiting carbon disclosure and performance: Legitimacy and management views. The British Accounting Review, 49, 365–379. [Google Scholar] [CrossRef]

- Qian, W., Tilt, C., & Belal, A. (2021). Social and environmental accounting in developing countries: Contextual challenges and insights. Accounting, Auditing & Accountability Journal, 34, 1021–1050. [Google Scholar]

- Radu, C., Caron, M. A., & Arroyo, P. (2020). Integration of carbon and environmental strategies within corporate disclosures. Journal of cleaner Production, 244, 118681. [Google Scholar] [CrossRef]

- Runyu, L., Rahman, M. R. C. A., & Jamil, A. H. B. (2025). A systematic literature review of carbon information disclosure on value effect. Journal of Lifestyle and SDGs Review, 5, e05011. [Google Scholar] [CrossRef]

- Saka, C., & Oshika, T. (2014). Disclosure effects, carbon emissions and corporate value. Sustainability Accounting, Management and Policy Journal, 5, 22–45. [Google Scholar] [CrossRef]

- Siddique, M. A., Akhtaruzzaman, M., Rashid, A., & Hammami, H. (2021). Carbon disclosure, carbon performance and financial performance: International evidence. International Review of Financial Analysis, 75, 101734. [Google Scholar] [CrossRef]

- Steuer, S., & Tröger, T. H. (2022). The role of disclosure in green finance. Journal of Financial Regulation, 8, 1–50. [Google Scholar] [CrossRef]

- Sun, Z.-Y., Wang, S.-N., & Li, D. (2022). The impacts of carbon emissions and voluntary carbon disclosure on firm value. Environmental Science and Pollution Research, 29, 60189–60197. [Google Scholar] [CrossRef] [PubMed]

- Wang, Q. (2022). Financial effects of carbon risk and carbon disclosure: A review. Accounting & Finance, 63, 4175–4219. [Google Scholar]

- Yang, Y., Xie, S., & Qiang, M. (2025). High-temperature risk and corporate social responsibility in China. Business Ethics, the Environment & Responsibility. [Google Scholar] [CrossRef]

- Yang, Y., Zhang, J., Song, C., Wu, Y., & Zhang, B. (2025). Does environmental information disclosure make financial markets more informative? Evidence from China. Journal of Contemporary Accounting & Economics, 21, 100468. [Google Scholar] [CrossRef]

- Zhang, J., & Yang, Y. (2023). Can environmental disclosure improve price efficiency? The perspective of price delay. Finance Research Letters, 52, 103556. [Google Scholar] [CrossRef]

- Zhang, M., Wang, A., & Zhou, S. (2023). Effect of analysts’ earnings pressure on environmental information disclosure of firms: Can corporate governance alleviate the earnings obsession? Borsa Istanbul Review, 23, 495–515. [Google Scholar] [CrossRef]

- Zhang, Y.-J., & Liu, J. Y. (2020). Overview of research on carbon information disclosure. Frontiers of Engineering Management, 7, 47–62. [Google Scholar] [CrossRef]

| Variables | Symbol | Descriptions | |

|---|---|---|---|

| Dependent Variable | Firm value | FV | Tobin’s q, market value of firm/ total assets–net intangible assets–net goodwill |

| Independent Variable | Policy Shock | DID | Treat × Post, treat target carbon-intensive industries plus 1; Post years from 2018 onward plus 1 and 0 for pre-2018 years. |

| Mediator Variable | Carbon information disclosure | CID | Carbon-related keywords are identified, and their frequencies are counted for each firm-year observation |

| Moderator Variable | Environmental regulation | ER | Investment in wastewater treatment and air pollution control in location/Industrial added value |

| Control Variable | Size | Size | Take logarithm of total assets |

| Solvency | Lev | Total liabilities/total assets | |

| Liquidity | Liquid | Current assets/current liabilities | |

| Development ability | Growth | Current period net profit–last period net profit/last period net profit | |

| Loss status | Loss | The net profit of the year was less than 0 plus 1, otherwise plus 0 | |

| Size of board | Board | Take logarithm of board size | |

| Governance capability | Indep | Independent directors/total number of directors | |

| External monitoring ability | IShare | Total institutional shares/total shares outstanding | |

| Financial transparency | Big4 | Audited by one of the big four for firm-year plus 1, otherwise plus 0 | |

| Reliability | Opinion | Unqualified audit opinion for firm-year plus 1, otherwise plus 0 |

| Mean | SD | p25 | p50 | p75 | Min | Max | |

|---|---|---|---|---|---|---|---|

| FV | 1.986 | 1.226 | 1.187 | 1.584 | 2.311 | 0.828 | 7.491 |

| CID | 0.23 | 0.354 | 0 | 0.115 | 0.267 | 0 | 2.023 |

| DID | 0.084 | 0.278 | 0 | 0 | 0 | 0 | 1 |

| ER | 0.002 | 0.002 | 0.001 | 0.001 | 0.002 | 0 | 0.008 |

| Size | 22.589 | 1.298 | 21.665 | 22.416 | 23.357 | 20.193 | 26.25 |

| Lev | 0.436 | 0.196 | 0.282 | 0.431 | 0.583 | 0.064 | 0.862 |

| Liquid | 2.176 | 1.927 | 1.135 | 1.588 | 2.45 | 0.366 | 12.422 |

| Growth | 0.14 | 0.336 | −0.033 | 0.09 | 0.236 | −0.508 | 1.818 |

| Loss | 0.106 | 0.308 | 0 | 0 | 0 | 0 | 1 |

| Board | 2.13 | 0.196 | 1.946 | 2.197 | 2.197 | 1.609 | 2.639 |

| Indep | 37.699 | 5.506 | 33.33 | 36.36 | 42.86 | 33.33 | 57.14 |

| IShare | 45.803 | 23.912 | 28.212 | 47.786 | 64.565 | 0.534 | 90.973 |

| Big4 | 0.072 | 0.258 | 0 | 0 | 0 | 0 | 1 |

| Opinion | 0.978 | 0.146 | 1 | 1 | 1 | 0 | 1 |

| (1) | (2) | (3) | (4) | |

|---|---|---|---|---|

| CID | CID | FV | FV | |

| DID | 0.2403 *** | 0.2332 *** | ||

| (0.0188) | (0.0187) | |||

| CID_hat | −0.0281 | 0.6290 *** | ||

| (0.1662) | (0.1700) | |||

| Size | 0.0553 *** | −0.5961 *** | ||

| (0.0106) | (0.0396) | |||

| Lev | −0.0876 ** | 0.3682 *** | ||

| (0.0358) | (0.1366) | |||

| Liquid | 0.0030 | −0.0160 | ||

| (0.0021) | (0.0100) | |||

| Growth | 0.0079 | 0.0522 ** | ||

| (0.0065) | (0.0224) | |||

| Loss | −0.0173 ** | −0.0931 *** | ||

| (0.0080) | (0.0214) | |||

| Board | −0.0023 | 0.0466 | ||

| (0.0317) | (0.0939) | |||

| Indep | 0.0004 | 0.0060 ** | ||

| (0.0009) | (0.0026) | |||

| IShare | 0.0005 * | 0.0151 *** | ||

| (0.0003) | (0.0012) | |||

| Big4 | −0.0418 | 0.0262 | ||

| (0.0258) | (0.0822) | |||

| Opinion | 0.0257 * | 0.0064 | ||

| (0.0151) | (0.0520) | |||

| Constant | 0.2096 *** | −1.0628 *** | 1.9929 *** | 14.1587 *** |

| (0.0016) | (0.2557) | (0.0382) | (0.8805) | |

| Year FE | YES | YES | YES | YES |

| Id FE | YES | YES | YES | YES |

| N | 17,530 | 17,530 | 17,530 | 17,530 |

| Adj. R2 | 0.594 | 0.5982 | 0.6454 | 0.6748 |

| (1) | (2) | (3) | (4) | |

|---|---|---|---|---|

| FV | FV | FV | FV | |

| CID_hat | 0.6290 *** | |||

| (0.1700) | ||||

| L1.CID_hat | 0.6964 *** | |||

| (0.1627) | ||||

| L2.CID_hat | 0.8273 *** | |||

| (0.1675) | ||||

| L3.CID_hat | 0.6282 *** | |||

| (0.1459) | ||||

| Size | −0.5961 *** | −0.5956 *** | −0.6218 *** | −0.5177 *** |

| (0.0396) | (0.0454) | (0.0537) | (0.0533) | |

| Lev | 0.3682 *** | 0.2748 * | 0.1844 | 0.2085 |

| (0.1366) | (0.1454) | (0.1607) | (0.1538) | |

| Liquid | −0.0160 | −0.0055 | 0.0087 | −0.0009 |

| (0.0100) | (0.0120) | (0.0157) | (0.0149) | |

| Growth | 0.0522 ** | 0.0481 ** | 0.0553 ** | 0.0384 * |

| (0.0224) | (0.0226) | (0.0243) | (0.0220) | |

| Loss | −0.0931 *** | −0.1124 *** | −0.1026 *** | −0.0681 *** |

| (0.0214) | (0.0222) | (0.0233) | (0.0214) | |

| Board | 0.0466 | 0.0197 | −0.0128 | −0.0333 |

| (0.0939) | (0.1052) | (0.1150) | (0.1030) | |

| Indep | 0.0060 ** | 0.0065 ** | 0.0059 * | 0.0047 * |

| (0.0026) | (0.0029) | (0.0031) | (0.0027) | |

| IShare | 0.0151 *** | 0.0163 *** | 0.0187 *** | 0.0156 *** |

| (0.0012) | (0.0014) | (0.0017) | (0.0016) | |

| Big4 | 0.0262 | 0.0041 | −0.0665 | −0.0547 |

| (0.0822) | (0.0940) | (0.1044) | (0.0977) | |

| Opinion | 0.0064 | 0.0211 | 0.0184 | 0.0322 |

| (0.0520) | (0.0546) | (0.0569) | (0.0503) | |

| Constant | 14.1587 *** | 14.1879 *** | 14.7749 *** | 12.5800 *** |

| (0.8805) | −10.299 | −12.236 | −12.049 | |

| Year FE | YES | YES | YES | YES |

| Id FE | YES | YES | YES | YES |

| N | 17,530 | 15,777 | 14,024 | 12,271 |

| Adj. R2 | 0.6748 | 0.6904 | 0.7061 | 0.7274 |

| (1) | (2) | (3) | (4) | |

|---|---|---|---|---|

| FV | FV | FV | FV | |

| CID_hat | −0.0281 | 0.6290 *** | 0.6249 *** | 0.7379 *** |

| (0.1662) | (0.1700) | (0.1702) | (0.1707) | |

| ER | −36.097 | 95.2403 *** | ||

| −74.889 | −161.712 | |||

| CID_hat_ER | −4.7 × 102 *** | |||

| −642.935 | ||||

| Size | −0.5961 *** | −0.5956 *** | −0.5933 *** | |

| (0.0396) | (0.0396) | (0.0393) | ||

| Lev | 0.3682 *** | 0.3696 *** | 0.3757 *** | |

| (0.1366) | (0.1368) | (0.1357) | ||

| Liquid | −0.0160 | −0.0160 | −0.0147 | |

| (0.0100) | (0.0100) | (0.0099) | ||

| Growth | 0.0522 ** | 0.0520 ** | 0.0562 ** | |

| (0.0224) | (0.0224) | (0.0222) | ||

| Loss | −0.0931 *** | −0.0932 *** | −0.0920 *** | |

| (0.0214) | (0.0214) | (0.0214) | ||

| Board | 0.0466 | 0.0469 | 0.0444 | |

| (0.0939) | (0.0939) | (0.0928) | ||

| Indep | 0.0060 ** | 0.0060 ** | 0.0059 ** | |

| (0.0026) | (0.0026) | (0.0026) | ||

| IShare | 0.0151 *** | 0.0151 *** | 0.0154 *** | |

| (0.0012) | (0.0012) | (0.0012) | ||

| Big4 | 0.0262 | 0.0259 | 0.0130 | |

| (0.0822) | (0.0822) | (0.0815) | ||

| Opinion | 0.0064 | 0.0066 | 0.0109 | |

| (0.0520) | (0.0520) | (0.0510) | ||

| Constant | 1.9929 *** | 14.1587 *** | 14.1525 *** | 13.9811 *** |

| (0.0382) | (0.8805) | (0.8806) | (0.8752) | |

| Year FE | YES | YES | YES | YES |

| Id FE | YES | YES | YES | YES |

| N | 17,530 | 17,530 | 17,530 | 17,530 |

| Adj. R2 | 0.6454 | 0.6748 | 0.6748 | 0.6767 |

| Group | Low ER Group (Below 25th Percentile) | Lower-Middle ER Group (25th–50th Percentile) | Middle ER Group (50th–75th Percentile) | High ER Group (Above 75th Percentile) | ||||

|---|---|---|---|---|---|---|---|---|

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | |

| FV | FV | FV | FV | FV | FV | FV | FV | |

| DID | 0.2854 *** | 0.1471 *** | 0.1415 *** | 0.1208 *** | ||||

| (0.0770) | (0.0248) | (0.0241) | (0.0310) | |||||

| CID_hat | −0.0728 | 0.5366 ** | 0.8040 *** | 0.9086 *** | ||||

| (0.8074) | (0.2641) | (0.3063) | (0.3132) | |||||

| Size | 0.0827 *** | −0.7751 *** | 0.0006 | −0.8359 *** | 0.0477 *** | −0.8237 *** | 0.0187 | −0.8107 *** |

| (0.0261) | (0.1072) | (0.0146) | (0.0905) | (0.0162) | (0.0791) | (0.0143) | (0.0692) | |

| Lev | −0.1005 | 0.3296 | 0.0685 | 0.3816 | −0.0399 | 0.9539 *** | −0.0925 * | 0.9242 *** |

| (0.0893) | (0.3303) | (0.0564) | (0.3557) | (0.0538) | (0.2752) | (0.0490) | (0.2603) | |

| Liquid | 0.0087 | −0.0634 ** | 0.0027 | 0.0115 | 0.0049 * | 0.0131 | −0.0027 | −0.0073 |

| (0.0057) | (0.0288) | (0.0025) | (0.0200) | (0.0029) | (0.0248) | (0.0027) | (0.0197) | |

| Growth | 0.0330 ** | 0.1255 *** | −0.0043 | −0.0104 | −0.0055 | 0.0544 | −0.0019 | 0.0732 * |

| (0.0160) | (0.0438) | (0.0103) | (0.0524) | (0.0112) | (0.0477) | (0.0079) | (0.0389) | |

| Loss | −0.0012 | −0.0687 ** | −0.0194 | −0.0424 | −0.0124 | −0.1277 *** | 0.0050 | −0.1634 *** |

| (0.0153) | (0.0336) | (0.0118) | (0.0550) | (0.0107) | (0.0469) | (0.0127) | (0.0419) | |

| Board | −0.0810 | −0.2083 | 0.0081 | −0.3939 * | 0.0721 * | 0.2823 | 0.0167 | 0.4305 ** |

| (0.0688) | (0.2058) | (0.0437) | (0.2339) | (0.0419) | (0.1860) | (0.0388) | (0.2167) | |

| Indep | −0.0025 | 0.0012 | 0.0015 | −0.0002 | 0.0008 | 0.0058 | 0.0001 | 0.0100 * |

| (0.0020) | (0.0049) | (0.0012) | (0.0068) | (0.0013) | (0.0050) | (0.0012) | (0.0055) | |

| IShare | 0.0008 | 0.0152 *** | 0.0003 | 0.0204 *** | 0.0001 | 0.0161 *** | 0.0000 | 0.0106 *** |

| (0.0009) | (0.0034) | (0.0004) | (0.0027) | (0.0005) | (0.0022) | (0.0004) | (0.0022) | |

| Big4 | −0.0083 | −0.0636 | −0.0112 | −0.1546 | −0.0556 * | −0.1760 | 0.0153 | −0.1677 |

| (0.0453) | (0.1575) | (0.0496) | (0.1613) | (0.0298) | (0.1297) | (0.0288) | (0.1104) | |

| Opinion | −0.0498 | 0.0303 | 0.0145 | 0.0621 | 0.0067 | −0.0300 | 0.0005 | −0.2310 |

| (0.0324) | (0.0705) | (0.0153) | (0.1216) | (0.0278) | (0.1096) | (0.0232) | (0.1449) | |

| Constant | −1.2359 ** | 19.2531 *** | 0.0199 | 20.4471 *** | −1.1010 *** | 18.4055 *** | −0.2672 | 18.1197 *** |

| (0.6201) | −23,429 | (0.3313) | −21.468 | (0.3764) | −17,076 | (0.3124) | −15.456 | |

| Year FE | YES | YES | YES | YES | YES | YES | YES | YES |

| Id FE | YES | YES | YES | YES | YES | YES | YES | YES |

| N | 4178 | 4178 | 4040 | 4040 | 4126 | 4126 | 4135 | 4135 |

| Adj. R2 | 0.7391 | 0.7881 | 0.7101 | 0.7142 | 0.6721 | 0.7058 | 0.6092 | 0.718 |

| (1) | (2) | (3) | (4) | (5) | (6) | |

|---|---|---|---|---|---|---|

| FV | FV | FV | FV | FV | FV | |

| CID_hat | −3.8057 *** | −0.0281 | 1.1719 *** | 0.9821 *** | 0.6249 *** | 0.6290 *** |

| (0.1759) | (0.1662) | (0.1661) | (0.1704) | (0.1696) | (0.1700) | |

| Size | −0.5108 *** | −0.5236 *** | −0.5950 *** | −0.5961 *** | ||

| (0.0412) | (0.0414) | (0.0398) | (0.0396) | |||

| Lev | 0.2246 | 0.2858 ** | 0.3663 *** | 0.3682 *** | ||

| (0.1365) | (0.1377) | (0.1365) | (0.1366) | |||

| Liquid | −0.0162 | −0.0126 | −0.0160 | −0.0160 | ||

| (0.0099) | (0.0099) | (0.0100) | (0.0100) | |||

| Growth | 0.0957 *** | 0.0523 ** | 0.0522 ** | |||

| (0.0225) | (0.0224) | (0.0224) | ||||

| Loss | −0.0996 *** | −0.0935 *** | −0.0931 *** | |||

| (0.0215) | (0.0214) | (0.0214) | ||||

| Board | 0.0473 | 0.0466 | ||||

| (0.0938) | (0.0939) | |||||

| Indep | 0.0060 ** | 0.0060 ** | ||||

| (0.0026) | (0.0026) | |||||

| IShare | 0.0152 *** | 0.0151 *** | ||||

| (0.0012) | (0.0012) | |||||

| Big4 | 0.0262 | |||||

| (0.0822) | ||||||

| Opinion | 0.0064 | |||||

| (0.0520) | ||||||

| Constant | 2.8612 *** | 1.9929 *** | 13.1917 *** | 13.4876 *** | 14.1420 *** | 14.1587 *** |

| (0.0489) | (0.0382) | (0.8884) | (0.8919) | (0.8847) | (0.8805) | |

| Year FE | NO | YES | YES | YES | YES | YES |

| Id FE | NO | YES | YES | YES | YES | YES |

| N | 17,530 | 17,530 | 17,530 | 17,530 | 17,530 | 17,530 |

| Adj. R2 | 0.0958 | 0.6454 | 0.6622 | 0.6635 | 0.6748 | 0.6748 |

| (1) | (2) | (3) | (4) | (5) | (6) | |

|---|---|---|---|---|---|---|

| FV | FV | FV | FV | FV | FV | |

| CID_hat | −1.1542 *** | −0.4873 *** | −0.5879 *** | 0.6031 *** | 0.6290 *** | 0.5734 *** |

| (0.1673) | (0.1525) | (0.1827) | (0.1742) | (0.1700) | (0.1814) | |

| Size | −0.3551 *** | −0.4933 *** | −0.3932 *** | −0.4485 *** | −0.5961 *** | −0.6008 *** |

| (0.0272) | (0.0330) | (0.0280) | (0.0260) | (0.0396) | (0.0403) | |

| Lev | −0.7828 *** | −0.0152 | −0.6409 *** | −0.1992 | 0.3682 *** | 0.3968 *** |

| (0.1314) | (0.1399) | (0.1322) | (0.1291) | (0.1366) | (0.1385) | |

| Liquid | 0.0544 *** | −0.0307 *** | 0.0617 *** | 0.0462 *** | −0.0160 | −0.0141 |

| (0.0127) | (0.0108) | (0.0127) | (0.0125) | (0.0100) | (0.0102) | |

| Growth | 0.3107 *** | 0.0818 *** | 0.2945 *** | 0.2003 *** | 0.0522 ** | 0.0424 * |

| (0.0324) | (0.0228) | (0.0335) | (0.0323) | (0.0224) | (0.0221) | |

| Loss | −0.0126 | −0.0882 *** | −0.0158 | −0.0505 | −0.0931 *** | −0.0874 *** |

| (0.0329) | (0.0235) | (0.0329) | (0.0309) | (0.0214) | (0.0214) | |

| Board | −0.0698 | −0.1693 * | −0.0162 | 0.0062 | 0.0466 | 0.0601 |

| (0.1024) | (0.0962) | (0.1033) | (0.0963) | (0.0939) | (0.0949) | |

| Indep | 0.0122 *** | 0.0031 | 0.0132 *** | 0.0098 *** | 0.0060 ** | 0.0069 *** |

| (0.0032) | (0.0027) | (0.0032) | (0.0029) | (0.0026) | (0.0026) | |

| IShare | 0.0099 *** | 0.0162 *** | 0.0095 *** | 0.0103 *** | 0.0151 *** | 0.0152 *** |

| (0.0008) | (0.0012) | (0.0009) | (0.0008) | (0.0012) | (0.0012) | |

| Big4 | 0.0891 | −0.0361 | 0.1199 ** | 0.1667 *** | 0.0262 | 0.0055 |

| (0.0599) | (0.0827) | (0.0602) | (0.0541) | (0.0822) | (0.0807) | |

| Opinion | −0.1745 * | 0.0591 | −0.2084 ** | −0.2258 ** | 0.0064 | 0.0163 |

| (0.1046) | (0.0587) | (0.0989) | (0.0935) | (0.0520) | (0.0528) | |

| Constant | 9.8508 *** | 12.7595 *** | 10.4076 *** | 11.2997 *** | 14.1587 *** | 14.1838 *** |

| (0.6294) | (0.7694) | (0.6371) | (0.6030) | (0.8805) | (0.8957) | |

| Fixed Effect | None | Id | Year | Industry Year | Id Year | Id Province-Year |

| N | 17,530 | 17,530 | 17,530 | 17,530 | 17,530 | 17,530 |

| Adj. R2 | 0.2569 | 0.5821 | 0.3381 | 0.4105 | 0.6748 | 0.6795 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2025 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Liu, R.; Che Abdul Rahman, M.R.; Jamil, A.H. From Policy Mandates to Market Signals: Causal and Dynamic Effects of Carbon Information Disclosure on Firm Value. Int. J. Financial Stud. 2025, 13, 98. https://doi.org/10.3390/ijfs13020098

Liu R, Che Abdul Rahman MR, Jamil AH. From Policy Mandates to Market Signals: Causal and Dynamic Effects of Carbon Information Disclosure on Firm Value. International Journal of Financial Studies. 2025; 13(2):98. https://doi.org/10.3390/ijfs13020098

Chicago/Turabian StyleLiu, Runyu, Mara Ridhuan Che Abdul Rahman, and Ainul Huda Jamil. 2025. "From Policy Mandates to Market Signals: Causal and Dynamic Effects of Carbon Information Disclosure on Firm Value" International Journal of Financial Studies 13, no. 2: 98. https://doi.org/10.3390/ijfs13020098

APA StyleLiu, R., Che Abdul Rahman, M. R., & Jamil, A. H. (2025). From Policy Mandates to Market Signals: Causal and Dynamic Effects of Carbon Information Disclosure on Firm Value. International Journal of Financial Studies, 13(2), 98. https://doi.org/10.3390/ijfs13020098