Thailand Sustainability Investment Performance on Thailand’s Stock Market and Financial Assets

, ,

, ,

Abstract

1. Introduction

2. Literature Review

3. Data and Research Method

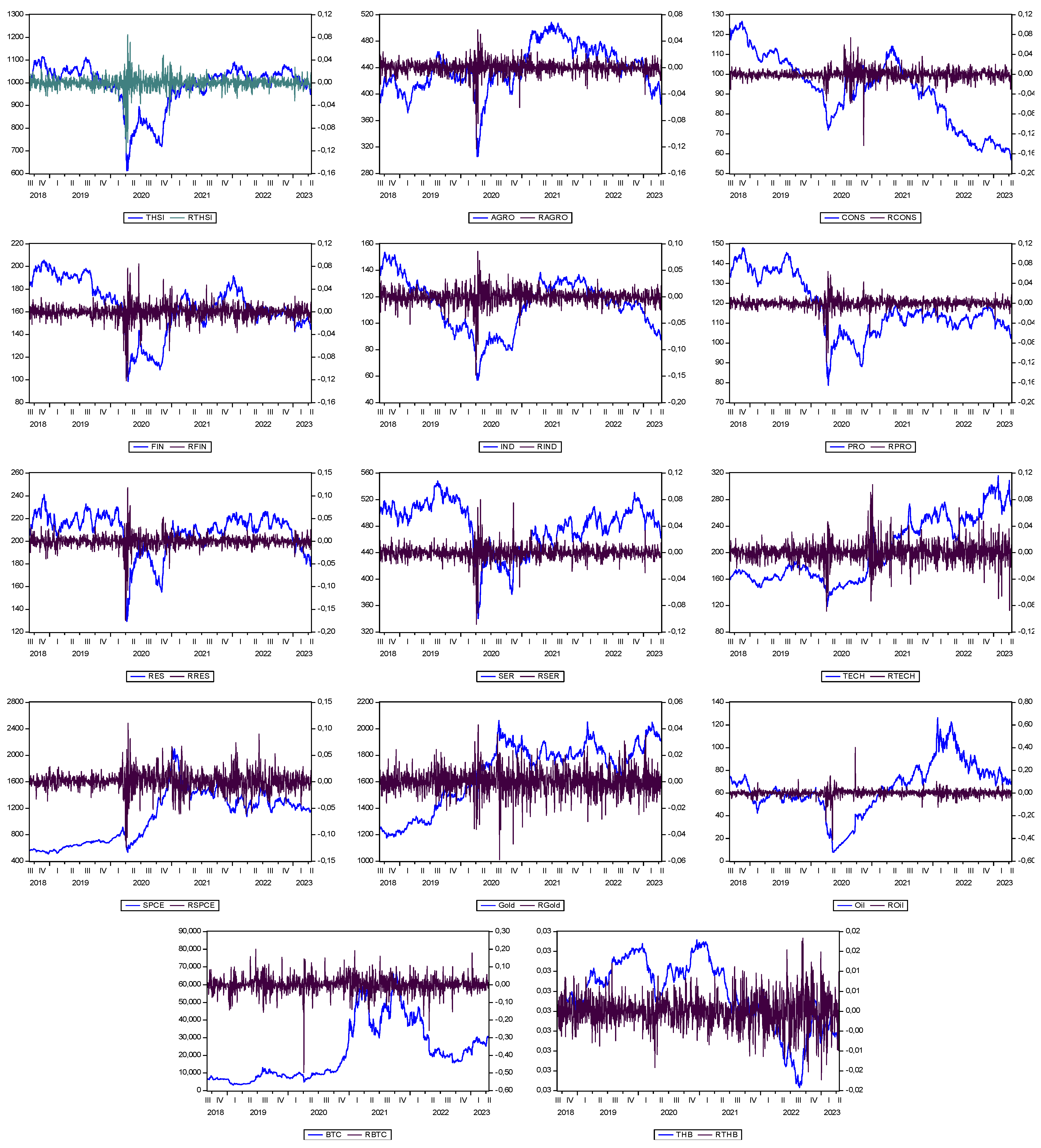

3.1. Data

3.2. Research Method

4. Results and Discussion

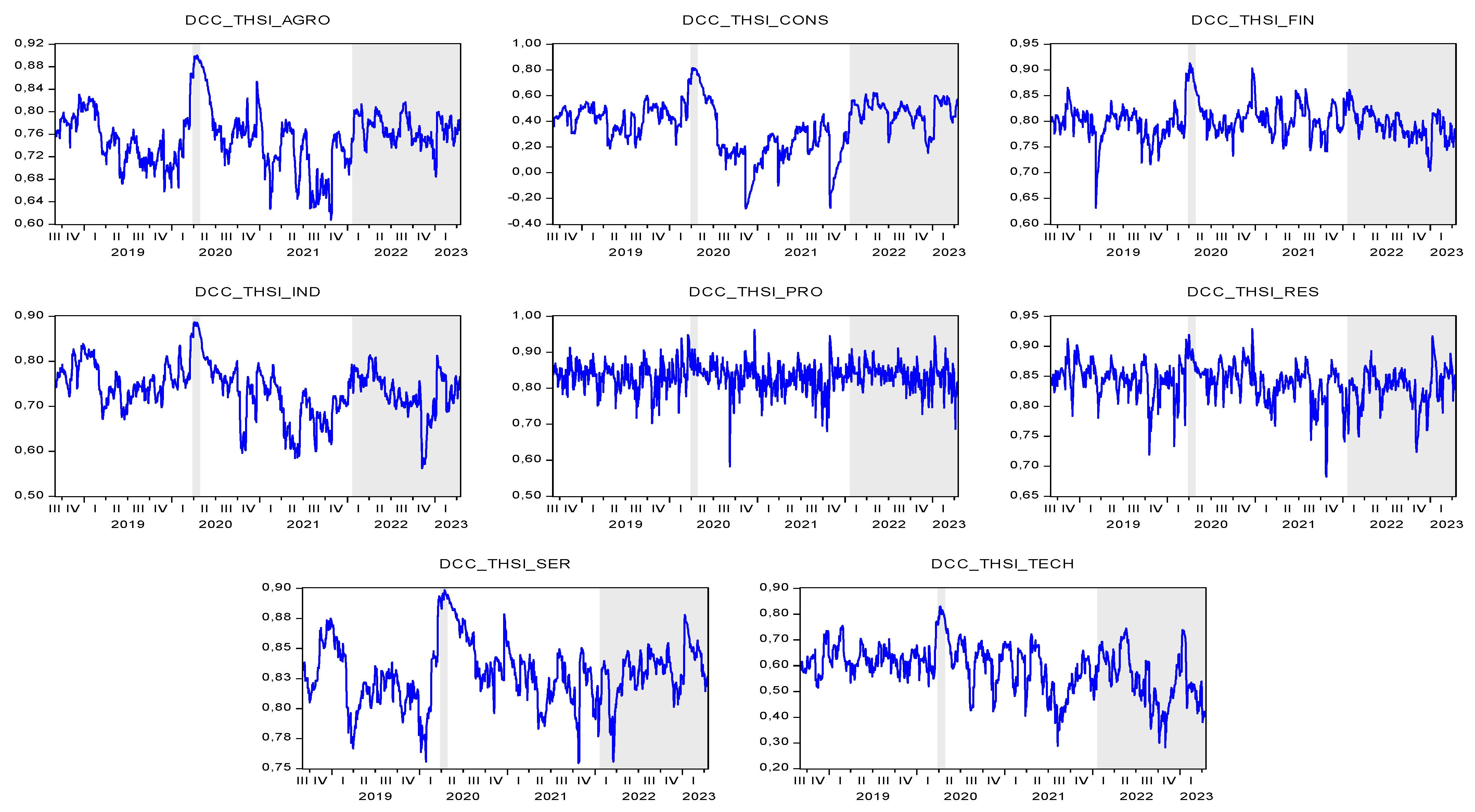

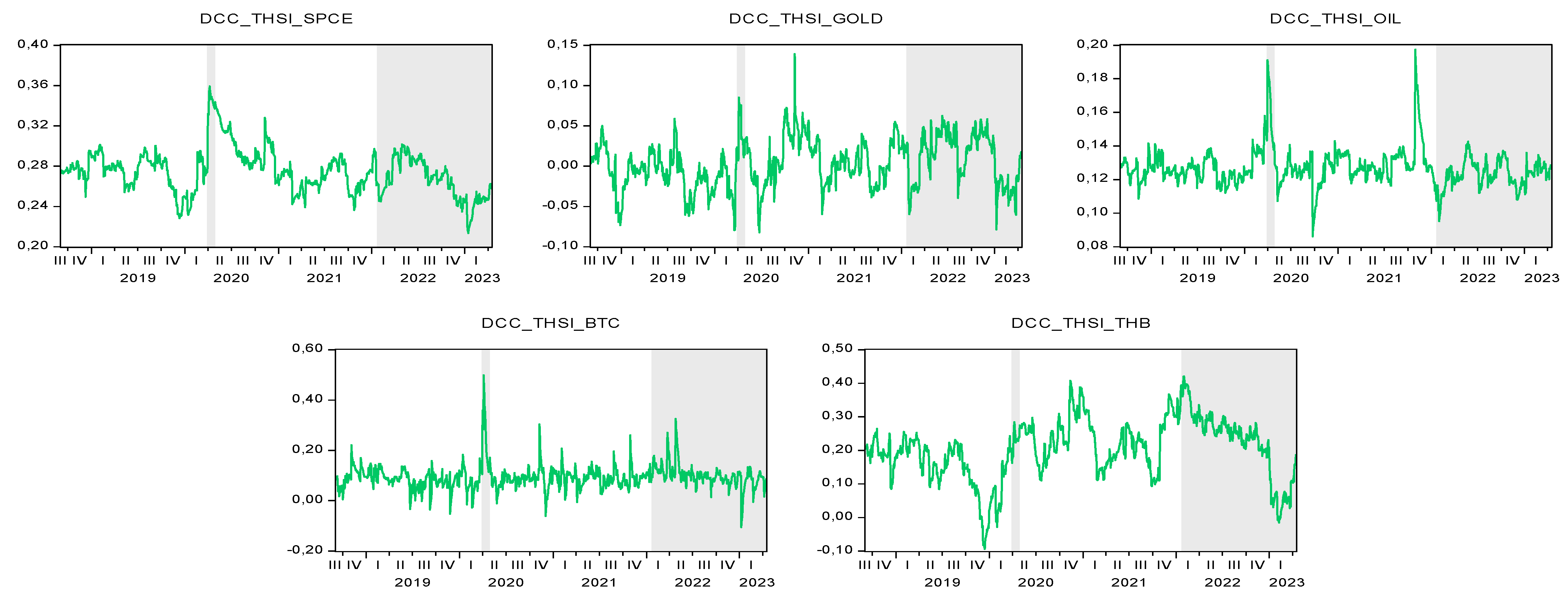

4.1. Dynamic Conditional Correlation Analysis

4.2. Hedge and Safe-Haven Analysis

4.3. Granger Causality Test

5. Conclusions and Future Directions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

| Lags | Loglikelihood | LR | AIC | SIC | HQC |

|---|---|---|---|---|---|

| 0 | 54,399.880 | NA | −90.794 | −90.735 * | −90.772 * |

| 1 | 54,645.070 | 484.251 | −90.877 * | −89.985 | −90.541 |

| 2 | 54,818.100 | 337.682 | −90.838 | −89.114 | −90.189 |

| 3 | 54,994.470 | 340.077 | −90.805 | −88.249 | −89.842 |

| 4 | 55,148.490 | 293.389 | −90.735 | −87.346 | −89.459 |

| 5 | 55,316.850 | 316.763 | −90.689 | −86.467 | −89.099 |

| 6 | 55,484.260 | 311.049 | −90.642 | −85.587 | −88.737 |

| 7 | 55,633.830 | 274.435 | −90.564 | −84.677 | −88.346 |

| 8 | 55,775.100 | 255.878 | −90.473 | −83.753 | −87.941 |

| Variables | Mean Equation | Variance Equation | Diagnostic Test | |||

|---|---|---|---|---|---|---|

| Q2(5) | Q2(10) | |||||

| THSI | −1.26 × 10−5 | 2.88 × 10−6 a | 0.109 a | 0.865 a | 8.499 [0.131] | 11.477 [0.386] |

| AGRO | −3.01 × 10−5 | 2.61 × 10−6 a | 0.092 a | 0.884 a | 4.238 [0.516] | 7.962 [0.633] |

| CONS | −7.93 × 10−4 a | 2.02 × 10−7 c | 0.053 a | 0.950 a | 9.548 [0.089] | 9.860 [0.453] |

| FIN | −1.66 × 10−4 | 1.27 × 10−6 a | 0.085 a | 0.912 a | 4.213 [0.519] | 7.263 [0.700] |

| IND | −5.10 × 10−4 | 2.64 × 10−6 a | 0.070 a | 0.917 a | 5.231 [0.388] | 14.207 [0.164] |

| PRO | −1.65 × 10−4 | 1.61 × 10−6 a | 0.083 a | 0.901 a | 7.464 [0.188] | 9.247 [0.509] |

| RES | −4.16 × 10−5 | 3.23 × 10−6 a | 0.102 a | 0.881 a | 2.840 [0.725] | 16.180 [0.104] |

| SER | 4.32 × 10−5 | 2.57 × 10−6 a | 0.086 a | 0.888 a | 3.176 [0.673] | 4.822 [0.903] |

| TECH | 4.25 × 10−4 | 1.30 × 10−5 a | 0.173 a | 0.783 a | 4.244 [0.515] | 10.668 [0.384] |

| SPCE | 8.62 × 10−4 b | 2.90 × 10−6 a | 0.116 a | 0.883 a | 1.684 [0.891] | 5.513 [0.854] |

| Gold | 2.01 × 10−4 | 5.31 × 10−6 a | 0.097 a | 0.844 a | 0.653 [0.985] | 10.709 [0.381] |

| Oil | 1.24 × 10−3 b | 4.72 × 10−5 a | 0.254 a | 0.740 a | 1.506 [0.912] | 6.046 [0.811] |

| BTC | 1.61 × 10−3 | 3.13 × 10−4 a | 0.144 a | 0.722 a | 9.100 [0.105] | 10.487 [0.399] |

| THB | −2.41 × 10−6 | 9.87 × 10−8 b | 0.041 a | 0.953 a | 8.858 [0.115] | 11.262 [0.337] |

| 1 | Based on S&P Goldman Sachs commodity index (GSCI) returns at the end of 2021 compared to the end of 2022. |

| 2 | Based on S&P 500 ESG index returns at the end of 2021 compared to the end of 2022. |

References

- Ahad, M., Imran, Z. A., & Shahzad, K. (2024). Safe haven between European ESG and energy sector under Russian-Ukraine war: Role of sustainable investments for portfolio diversification. Energy Economics, 138, 107853. [Google Scholar] [CrossRef]

- Al-Nassar, N. S., Boubaker, S., Chaibi, A., & Makram, B. (2023). In search of hedges and safe havens during the COVID-19 pandemic: Gold versus Bitcoin, oil, and oil uncertainty. Quarterly Review of Economics and Finance, 90, 318–332. [Google Scholar] [CrossRef] [PubMed]

- Andersson, E., Hoque, M., Rahman, M. L., Uddin, G. S., & Jayasekera, R. (2022). ESG investment: What do we learn from its interaction with stock, currency and commodity markets? International Journal of Finance and Economics, 27(3), 3623–3639. [Google Scholar] [CrossRef]

- Asvathitanont, C., & Tangjitprom, N. (2020). The performance of environmental, social, and governance investment in Thailand. International Journal of Financial Research, 11(6), 253–261. [Google Scholar] [CrossRef]

- Bal, G. R., & Maharana, A. K. (2023). Can equity market risk be diversified with the help of ESG investment and commodities? Global Business Review. in press. [Google Scholar] [CrossRef]

- Barson, Z., Ofori, K. S., Junior, P. O., Boakye, K. G., & Ampong, G. O. A. (2024). Time-varying connectedness between ESG stocks and BRVM traditional stocks. Journal of Emerging Market Finance, 23(3), 306–335. [Google Scholar] [CrossRef]

- Basher, S. A., & Sadorsky, P. (2022). Forecasting bitcoin price direction with random forests: How important are interest rates, inflation, and market volatility? Machine Learning with Applications, 9, 100355. [Google Scholar] [CrossRef]

- Baur, D. G., & Lucey, B. M. (2010). Is gold a hedge or a safe haven? An analysis of stocks, bonds and gold. Financial Review, 45, 217–229. [Google Scholar] [CrossRef]

- Baur, D. G., & McDermott, T. K. (2010). Is gold a safe haven? International evidence. Journal of Banking & Finance, 34, 1886–1898. [Google Scholar] [CrossRef]

- Bloomberg Intelligence. (2022). ESG may surpass $41 trillion assets in 2022, but not without challenges. Available online: https://www.bloomberg.com/company/press/esg-may-surpass-41-trillion-assets-in-2022-but-not-without-challenges-finds-bloomberg-intelligence/ (accessed on 30 July 2023).

- Bunnun, W., & Chancharat, N. (2023). The mediating role of dividend policy in the relationship between ownership structure and firm performance of Thai listed companies. International Journal of Trade and Global Markets, 17(3–4), 340–347. [Google Scholar] [CrossRef]

- Cagli, E. C. C., Mandaci, P. E., & Taşkın, D. (2023). Environmental, social, and governance (ESG) investing and commodities: Dynamic connectedness and risk management strategies. Sustainability Accounting, Management and Policy Journal, 14(5), 1052–1074. [Google Scholar] [CrossRef]

- Chen, M., & Mussalli, G. (2020). An integrated approach to quantitative ESG investing. The Journal of Portfolio Management, 46(3), 65–74. [Google Scholar] [CrossRef]

- Döttling, R., & Kim, S. (2024). Sustainability preferences under stress: Evidence from COVID-19. Journal of Financial and Quantitative Analysis, 59(2), 435–473. [Google Scholar] [CrossRef]

- Engle, R. F. (2002). Dynamic conditional correlation: A simple class of multivariate GARCH models. Journal of Business & Economic Statistics, 20(3), 339–350. [Google Scholar] [CrossRef]

- Ferriani, F., & Natoli, F. (2021). ESG risks in times of COVID-19. Applied Economics Letters, 28(18), 1537–1541. [Google Scholar] [CrossRef]

- Harnphattananusorn, S. (2019). Analysis of relationship and volatilities between foreign exchange market and stock market of Thailand and selected Asian countries. Kasetsart Journal of Social Sciences, 40(1), 262–269. [Google Scholar] [CrossRef]

- Hasan, M. B., Rashid, M. M., Hossain, M. N., Rahman, M. M., & Amin, M. R. (2023). Using green and ESG assets to achieve post-COVID-19 environmental sustainability. Fulbright Review of Economics and Policy, 3(1), 25–48. [Google Scholar] [CrossRef]

- Iglesias-Casal, A., López-Penabad, M. C., López-Andión, C., & Maside-Sanfiz, J. M. (2020). Diversification and optimal hedges for socially responsible investment in Brazil. Economic Modelling, 85, 106–118. [Google Scholar] [CrossRef]

- Imran, Z. A., Ahad, M., Shahzad, K., Ahmad, M., & Hameed, I. (2024). Safe haven properties of industrial stocks against ESG in the United States: Portfolio implication for sustainable investments. Energy Economics, 136, 107712. [Google Scholar] [CrossRef]

- Katsampoxakis, I., Xanthopoulos, S., Basdekis, C., & Christopoulos, A. G. (2024). Can ESG stocks be a safe haven during global crises? Evidence from the COVID-19 pandemic and the Russia-Ukraine war with time-frequency wavelet analysis. Economies, 12(4), 89. [Google Scholar] [CrossRef]

- Lei, H., Xue, M., Liu, H., & Ye, J. (2023). Precious metal as a safe haven for global ESG stocks: Portfolio implications for socially responsible investing. Resources Policy, 80, 103170. [Google Scholar] [CrossRef]

- Markowitz, H. (1952). Portfolio selection. The Journal of Finance, 7(1), 77–91. [Google Scholar] [CrossRef]

- Mousa, M., Saleem, A., & Sági, J. (2022). Are ESG shares a safe haven during COVID-19? Evidence from the Arab region. Sustainability, 14, 208. [Google Scholar] [CrossRef]

- Naeem, M. A., & Karim, S. (2021). Tail dependence between bitcoin and green financial assets. Economics Letters, 208, 110068. [Google Scholar] [CrossRef]

- Naeem, M. A., Karim, S., Uddin, G. S., & Junttila, J. (2022). Small fish in big ponds: Connections of green finance assets to commodity and sectoral stock markets. International Review of Financial Analysis, 83, 102283. [Google Scholar] [CrossRef]

- Naeem, M. A., Rabbani, M. R., Karim, S., & Billah, S. M. (2023). Religion vs. ethics: Hedge and safe haven properties of Sukuk and green bonds for stock markets pre-and during COVID-19. International Journal of Islamic and Middle Eastern Finance and Management, 16(2), 234–252. [Google Scholar] [CrossRef]

- Nittayakamolphun, P., Bejrananda, T., & Pholkerd, P. (2022). Stablecoins as safe haven or hedging asset for cryptocurrencies. Applied Economics Journal, 29(2), 45–70. Available online: https://so01.tci-thaijo.org/index.php/AEJ/article/view/260150 (accessed on 30 July 2023).

- Nittayakamolphun, P., Bejrananda, T., & Pholkerd, P. (2024a). Green bonds and ESG stocks as safe haven or hedging asset for other financial assets. Kasetsart Journal of Social Sciences, 45(4), 1307–1318. [Google Scholar] [CrossRef]

- Nittayakamolphun, P., Bejrananda, T., & Pholkerd, P. (2024b). Asymmetric effects of uncertainty and commodity markets on sustainable stock in seven emerging markets. Journal of Risk and Financial Management, 17(4), 155. [Google Scholar] [CrossRef]

- Omura, A., Roca, E., & Nakai, M. (2021). Does responsible investing pay during economic downturns: Evidence from the COVID-19 pandemic. Finance Research Letters, 42, 101914. [Google Scholar] [CrossRef]

- Pedini, L., & Severini, S. (2022). Exploring the hedge, diversifier and safe haven properties of ESG investments: A cross-quantilogram analysis. Available online: https://mpra.ub.uni-muenchen.de/112339/1/MPRA_paper_112339.pdf (accessed on 30 July 2023).

- Piserà, S., & Chiappini, H. (2024). Are ESG indexes a safe-haven or hedging asset? Evidence from the COVID-19 pandemic in China. International Journal of Emerging Markets, 19(1), 56–75. [Google Scholar] [CrossRef]

- Prinyapon, Y., Nittayagasetwat, A., & Nittayagasetwat, W. (2022). Performance of ESG stocks: Case of stock exchange of Thailand. NIDA Business Journal, 31, 42–60. Available online: https://so10.tci-thaijo.org/index.php/NIDABJ/article/view/89 (accessed on 30 July 2023).

- Ratner, M., & Chiu, C. C. (2013). Hedging stock sector risk with credit default swaps. International Review of Financial Analysis, 30, 18–25. [Google Scholar] [CrossRef]

- Rubbaniy, G., Khalid, A. A., Rizwan, M. F., & Ali, S. (2022). Are ESG stocks safe-haven during COVID-19? Studies in Economics and Finance, 39(2), 239–255. [Google Scholar] [CrossRef]

- Sharma, I., Bamba, M., Verma, B., & Verma, B. (2024). Dynamic connectedness and investment strategies between commodities and ESG stocks: Evidence from India. Australasian Accounting, Business and Finance Journal, 18(3), 67–84. [Google Scholar] [CrossRef]

- Sharpe, W. F. (1964). Capital asset prices: A theory of market equilibrium under conditions of risk. The Journal of Finance, 19(3), 425–442. [Google Scholar] [CrossRef]

- Singh, A. (2020). COVID-19 and safer investment bets. Finance Research Letters, 36, 101729. [Google Scholar] [CrossRef]

- Sinlapates, P., & Chancharat, S. (2022). Contrarian profits in Thailand sustainability investment-listed versus in stock exchange of Thailand-listed companies. Risks, 10, 229. [Google Scholar] [CrossRef]

- Suttipun, M. (2023). ESG performance and corporate financial risk of the alternative capital market in Thailand. Cogent Business & Management, 10, 2168290. [Google Scholar] [CrossRef]

- Suttipun, M., Khunkaew, R., & Wichianrak, J. (2023). The impact of environmental, social and governance (ESG) reporting and female board members on financial performance: Evidence from Thailand. Journal of Accounting Profession, 19(61), 89–111. [Google Scholar] [CrossRef]

- The Stock Exchange of Thailand. (2023a). SETTHSI index. Available online: https://www.set.or.th/en/market/index/setthsi/overview (accessed on 30 July 2023).

- The Stock Exchange of Thailand. (2023b). List of Thailand sustainability investment in 2022. Available online: https://www.setsustainability.com/libraries/710/item/thailand-sustainability-investment-lists (accessed on 30 July 2023).

- Umar, Z., Kenourgio, D., & Papathanasiou, S. (2020). The static and dynamic connectedness of environmental, social, and governance investments: International evidence. Economic Modelling, 93, 112–124. [Google Scholar] [CrossRef]

- Umar, Z., Polat, O., Choi, S. Y., & Teplova, T. (2022). The impact of the Russia-Ukraine conflict on the connectedness of financial markets. Finance Research Letters, 48, 102976. [Google Scholar] [CrossRef]

| Variables | Symbol | Definition |

|---|---|---|

| Thailand sustainability investment | THSI | Thailand sustainability investment index |

| Thailand’s stock market | AGRO | Agro and food industry stocks: Agro and food industry group index |

| CONS | Consumer products stocks: Consumer products group index | |

| FIN | Financials stocks: Financials group index | |

| IND | Industrials stocks: Industrials group index | |

| PRO | Property and construction stocks: Property and construction group index | |

| RES | Resources stocks: Resources group index | |

| SER | Services stocks: Services group index | |

| TECH | Technology stocks: Technology group index | |

| Financial assets | SPCE | Clean energy: S&P Global clean energy index |

| Gold | Gold: Gold price (USD per ounce) | |

| Oil | Crude oil: West Texas intermediate crude oil price (USD per barrel) | |

| BTC | Bitcoin: Bitcoin price (USD) | |

| THB | Thai baht: Exchange rate (1 Thai baht to US dollars) |

| Variables | Average (%) | S.D. (%) | Max (%) | Min (%) | Skewness | Kurtosis | J-B | ADF | PP | ARCH (5) | Corr-THSI |

|---|---|---|---|---|---|---|---|---|---|---|---|

| THSI | −0.003 | 1.194 | 8.479 | −12.322 | −1.733 | 26.688 | 28,800 a | −8.647 a | −37.070 a | 176.441 a | 1.000 |

| AGRO | 0.000 | 1.088 | 5.744 | −12.248 | −2.055 | 23.649 | 22,274 a | −37.125 a | −37.039 a | 132.408 a | 0.825 a |

| CONS | −0.062 | 1.166 | 7.404 | −14.344 | −1.432 | 25.943 | 26,863 a | −33.115 a | −33.098 a | 22.594 a | 0.297 a |

| FIN | −0.017 | 1.352 | 8.489 | −12.156 | −1.191 | 18.309 | 12,062 a | −12.450 a | −35.469 a | 124.197 a | 0.852 a |

| IND | −0.035 | 1.453 | 8.571 | −14.817 | −1.465 | 18.999 | 13,293 a | −12.881 a | −35.830 a | 178.127 a | 0.809 a |

| PRO | −0.020 | 1.032 | 6.430 | −11.910 | −2.179 | 30.588 | 39,199 a | −34.760 a | −35.087 a | 126.927 a | 0.887 a |

| RES | −0.010 | 1.435 | 11.782 | −17.470 | −1.843 | 34.273 | 49,826 a | −13.479 a | −36.324 a | 157.477 a | 0.894 a |

| SER | −0.005 | 1.092 | 8.037 | −10.818 | −0.856 | 22.650 | 19,549 a | −37.567 a | −37.463 a | 109.332 a | 0.882 a |

| TECH | 0.045 | 1.593 | 10.244 | −8.858 | 0.138 | 9.829 | 2347.0 a | −35.276 a | −35.384 a | 185.610 a | 0.587 a |

| SPCE | 0.061 | 1.858 | 11.033 | −12.497 | −0.356 | 9.683 | 2270.0 a | −31.456 a | −31.646 a | 249.771 a | 0.365 a |

| Gold | 0.036 | 0.940 | 4.297 | −5.898 | −0.333 | 6.287 | 565.101 a | −34.077 a | −34.134 a | 59.249 a | 0.022 |

| Oil | −0.004 | 3.559 | 40.352 | −41.765 | −1.766 | 48.214 | 103,353 a | −30.003 a | −30.321 a | 161.406 a | 0.092 a |

| BTC | 0.127 | 4.555 | 20.079 | −49.728 | −1.205 | 17.253 | 10,500 a | −35.952 a | −35.940 a | 17.211 a | 0.155 a |

| THB | −0.005 | 0.402 | 1.835 | −1.726 | 0.042 | 4.637 | 134.945 a | −33.592 a | −34.233 a | 77.651 a | 0.184 a |

| Variables | AGRO | CONS | FIN | IND | PRO | RES | SER | TECH | SPCE | Gold | Oil | BTC | THB |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Average DCC | 0.754 | 0.370 | 0.799 | 0.737 | 0.833 | 0.840 | 0.829 | 0.588 | 0.275 | 0.003 | 0.127 | 0.093 | 0.203 |

| 0.025 a | 0.039 a | 0.032 c | 0.028 a | 0.099 a | 0.048 a | 0.018 a | 0.044 b | 0.004 | 0.009 c | 0.003 | 0.023 | 0.018 b | |

| 0.955 a | 0.946 a | 0.906 a | 0.941 a | 0.589 a | 0.832 a | 0.959 a | 0.927 a | 0.971 a | 0.941 a | 0.916 a | 0.793 a | 0.963 a |

| Variables | Safe-Haven | |||

|---|---|---|---|---|

| AGRO | 0.753 a | 0.005 | 0.010 | 0.046 a |

| CONS | 0.373 a | 0.002 | −0.044 | −0.073 |

| FIN | 0.798 a | 0.003 | 0.015 a | 0.052 a |

| IND | 0.734 a | 0.009 | 0.025 a | 0.067 a |

| PRO | 0.833 a | 0.003 | 0.005 | 0.029 a |

| RES | 0.839 a | −0.005 | 0.003 | 0.017 c |

| SER | 0.828 a | 0.001 | 0.009 b | 0.025 a |

| TECH | 0.589 a | −0.005 | −0.008 | 0.047 c |

| SPCE | 0.274 a | 0.001 | −0.001 | 0.022 a |

| Gold | 0.002 b | −0.000 | 0.006 | 0.015 c |

| Oil | 0.127 a | −0.001 | 0.001 | 0.016 a |

| BTC | 0.092 a | 0.000 | 0.006 | 0.013 |

| THB | 0.201 a | 0.015 | 0.017 | 0.013 |

| Variables | COVID-19 | Russia–Ukraine War | ||

|---|---|---|---|---|

| AGRO | 0.757 a | −0.008 a | 0.748 a | 0.020 a |

| CONS | 0.444 a | −0.181 a | 0.332 a | 0.140 a |

| FIN | 0.792 a | 0.017 a | 0.802 a | −0.011 a |

| IND | 0.744 a | −0.018 a | 0.739 a | −0.010 a |

| PRO | 0.834 a | −0.001 | 0.832 a | 0.004 c |

| RES | 0.838 a | 0.003 | 0.842 a | −0.010 a |

| SER | 0.824 a | 0.011 a | 0.829 a | 0.002 |

| TECH | 0.586 a | 0.007 | 0.606 a | −0.065 a |

| SPCE | 0.269 a | 0.013 a | 0.278 a | −0.013 a |

| Gold | 0.000 | 0.007 a | 0.000 | 0.010 a |

| Oil | 0.124 a | 0.006 a | 0.128 a | −0.005 a |

| BTC | 0.091 a | 0.004 | 0.091 a | 0.007 b |

| THB | 0.183 a | 0.047 a | 0.195 a | 0.029 a |

| Variables | AGRO | CONS | FIN | IND | PRO | RES | SER | TECH | SPCE | Gold | Oil | BTC | THB |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| b | a | b | |||||||||||

| b | c | b | a | a | b |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2025 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Nittayakamolphun, P.; Bunnun, W.; Phong-a-ran, N.; Uttarin, R.; Pholkerd, P. Thailand Sustainability Investment Performance on Thailand’s Stock Market and Financial Assets. Int. J. Financial Stud. 2025, 13, 71. https://doi.org/10.3390/ijfs13020071

Nittayakamolphun P, Bunnun W, Phong-a-ran N, Uttarin R, Pholkerd P. Thailand Sustainability Investment Performance on Thailand’s Stock Market and Financial Assets. International Journal of Financial Studies. 2025; 13(2):71. https://doi.org/10.3390/ijfs13020071

Chicago/Turabian StyleNittayakamolphun, Pitipat, Wiwatwong Bunnun, Nathaporn Phong-a-ran, Raweepan Uttarin, and Panjamapon Pholkerd. 2025. "Thailand Sustainability Investment Performance on Thailand’s Stock Market and Financial Assets" International Journal of Financial Studies 13, no. 2: 71. https://doi.org/10.3390/ijfs13020071

APA StyleNittayakamolphun, P., Bunnun, W., Phong-a-ran, N., Uttarin, R., & Pholkerd, P. (2025). Thailand Sustainability Investment Performance on Thailand’s Stock Market and Financial Assets. International Journal of Financial Studies, 13(2), 71. https://doi.org/10.3390/ijfs13020071