Abstract

We examine the nonlinear relationship between interest rates on bank risk-taking behavior in South Africa between 2008:q1 and 2022:q3 using nonlinear autoregressive distributive lag (NARDL) and quantile autoregressive distributive lag (QARDL) models. Whilst the preliminary estimates from linear ARDL produce results adhering to conventional theory, the NARDL and QARDL analysis shows that the relationship between the variables is more complex. On one hand, the NARDL model shows that the phase of monetary policy (cyclical asymmetries) is important in determining the pass-through effects of interest rates on bank risk behavior. We find that both contractionary and expansionary monetary policy increases long-term risk through decreased liquidity for the former and increased non-performing loans for the latter. On the other hand, the QARDL model shows that the level of bank risk behavior (location asymmetries) is also important in determining the impact of interest rates on bank risk behavior. We find that interest rates affect bank risk behavior in ‘medium-to-high risk environments’ for unsecured loans and lending and in ‘medium-to-low risk environments’ for liquidity. Overall, these results enable us to recommend ways in which the SARB can strengthen its monitoring mechanisms given the multifaceted impact of interest rates on bank risk-taking.

1. Introduction

The global economy has witnessed sharp increases in inflation rates since 2022, leading to a proactive response from central banks worldwide. To combat rising inflation, major central banks have raised their policy rates, marking a departure from the low-interest-rate environments observed prior to the ongoing Ukraine–Russia conflict. Notably, the South African Reserve Bank (SARB) raised its policy rate from 3.5% in July 2020 to 7.25% in January 2023, with projections indicating a continued interest rate hiking cycle due to persistent high inflation (Majola 2023). This shift in policy has sparked debates regarding the influence of interest rates on bank risk-taking, particularly in an economic environment characterized by elevated inflation and subdued economic activity. These discussions have been further fueled by the recent collapses of Silicon Valley Bank (SVB) and Signature Bank in the United States.

Given the inherent operational structure of banks, which involves short-term borrowing and long-term lending (Bednar and Elamin 2014), knowing the impact of rising interest rates on risk-taking behavior for South African banks is of concern considering the surge in government securities holdings by commercial banks since the 2008/2009 global financial crisis which exposes these banks to financial risks (Hesse and Miyajima 2022). Further considering that the SARB has included macroprudential policies amongst its monetary policy toolbox, knowing whether these policies are achieving their purpose of safeguarding financial stability in the banking sector amidst the changes in interest rates, is important for policymakers, regulators and market participants.

However, the current academic literature gives contradicting insights into the relationship between higher interest rates and bank risk-taking behavior. On one hand, some authors argue that an increase in interest rates increases banking risks via its negative effects on the balance sheets and income statements of banks, as liabilities rise while the value of assets declines (Porcellacchia 2020). On the other hand, others argue that increased interest rates lead to higher bank revenues and expected net returns on safe assets (such as government bonds) which could minimize investments in riskier assets (De Nicolò et al. 2010; Claessens et al. 2018). Moreover, the existing empirical literature mostly focuses on the impact of low-interest-rate environments on bank risk-taking behavior in advanced economies that have implemented zero-interest-rate policies (ZIRPs). Notably, these studies use linear econometric tools in their empirical analysis despite evidence of the impact of interest rates on bank risk-taking varying between different monetary policy stances and levels of bank capitalization or leverage effects (Dell’Ariccia and Marquez 2013; Dell’Ariccia et al. 2014; Buch et al. 2014; Jiménez et al. 2014; Özşuca and Akbostancı 2016; Chen et al. 2017; Bonfim and Soares 2018; Brana et al. 2019; Bubeck et al. 2020).

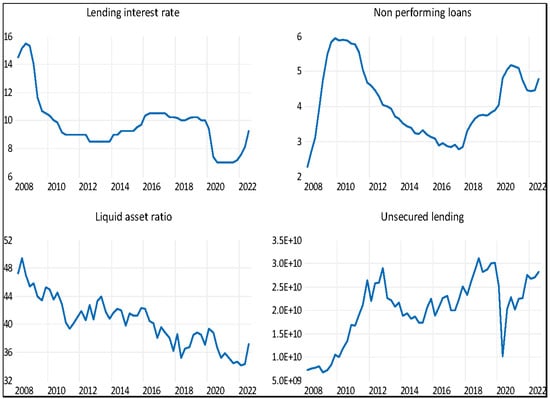

Our study investigates the nonlinear relationship between interest rates and bank risk-taking in South Africa, an emerging market economy that has not implemented a ZIRP (zero-interest-rate policy) and lacks empirical research on the subject for the country. To motivate our study, Figure 1 shows the trends in the lending rate (proxy for interest rates) and non-performing loans, liquid asset as a ratio of short-term liabilities and unsecured lending which are bank risk-taking indicators. Although we observe that liquid asset ratios (non-performing loans and unsecured lending) have generally decreased (increased) between the GFC and the more recent COVID-19, which indicates an increase in bank risk-taking behavior, we observe some asymmetric properties in the data that require empirical attention. Firstly, we observe outliers in the data, particularly during periods of crisis, which are indicative of location asymmetries. Secondly, we observe different cyclical patterns in the data, with liquid asset ratios and non-performing loans (unsecured lending) having sharper and shorter (smoother and longer) cycles. Therefore, accounting for location and cyclical asymmetries is crucial when investigating the impact of interest rates on bank risk-taking behavior.

Figure 1.

Times-series plot of interest rates and bank risk-taking measures.

To explore the nonlinear effects of interest rates on bank risk-taking in South Africa, we use two econometric models that capture different forms of asymmetries. Firstly, we use the nonlinear ARDL (NARDL) technique proposed by Shin et al. (2014). This technique allows for the decomposition of the independent variable of interest (interest rates, in this case) into positive and negative components, enabling an investigation of the impact of declining and rising interest rates on bank risk-taking, i.e., cyclical asymmetries. Secondly, the quantile ARDL (QARDL) of Cho et al. (2015) is employed to capture the differential impact of interest rates on various levels of risk-taking, recognizing the variations in risk-taking environments, i.e., location asymmetries. Notably, these nonlinear econometric models are preferred over other existing nonlinear models in that they are compatible with both stationary and non-stationary data as well as address endogeneity concerns such as simultaneity and reverse causality.

To the best of our knowledge, our study is the first to investigate the influence of cyclical and location asymmetries on the interest-rate–bank-risk-taking relationship. Our analysis serves to enlighten South African monetary policymakers on whether their current path of raising interest rates in an already high-risk environment poses a threat to the financial system through excessive bank risk-taking behavior. Financial regulators would also be interested in knowing the extent to which macroprudential policies have protected the banking sector against the risk inherent to changes in interest rates. Investors and fund managers could also use our results to make more informed decisions concerning risk management and diversification strategies.

2. Literature Review

2.1. Theoretical Literature

Banks operate on a short-term borrowing and long-term lending model, handling demand deposits that are short-term and providing long-term loans to individuals and businesses. This necessitates aligning the returns on their assets and liabilities. Central Banks are concerned with risk transmitted to commercial banks via changes in interest rates, i.e., the ‘interest rate channel’ of monetary policy. The dynamics of these transmissions are outlined in the works of Rajan (2006), De Nicolò et al. (2010), Dell’Ariccia and Marquez (2013), Dell’Ariccia et al. (2014) and Valencia (2014) which we discuss below.

Rajan (2006) introduced a ‘search for yield’ theory, in which high interest rates result in higher returns on risk-free assets, limiting investments in riskier assets. Conversely, low interest rates decrease revenue on safe assets, prompting banks to invest in riskier assets—an idea supported by the asset substitution theory (De Nicolò et al. 2010).

Valencia (2014) developed a dynamic model linking an exogenous change in monetary policy (risk-free rate) to bank risk-taking. The model, considering monopolistic banks, limited liability, equity issuance and profit maximization, indicates that expansionary monetary policy enhances bank profitability through reduced funding costs, leading to increased lending and leverage. Limited liability exacerbates profitability and encourages risk-taking. However, under certain conditions, a lower policy rate may reduce risk-taking, especially when banks adjust lending by decreasing dividends.

Models by Dell’Ariccia and Marquez (2013) and Dell’Ariccia et al. (2014) model the connection between monetary policy, bank risk-taking and leverage. The former proposes that an increase in interest rates leads to heightened monitoring by banks, potentially reducing risk-taking. The latter suggests that the impact of low interest rates on bank risk-taking depends on the degree of leverage, with well-capitalized banks increasing risk-taking and highly leveraged banks decreasing it.

De Nicolò et al.’s (2010) risk-shifting model contends that the effect of expansionary monetary policy on bank risk-taking is ambiguous with positive interest rates. Lower interest rates may decrease deposit rates, not fully passed on to customers, leading to higher expected net returns on safer assets and minimized investments in riskier assets. However, lower interest rates may also reduce the yield on safe assets, encouraging banks to invest in riskier assets, aligning with the search for yield hypothesis.

2.2. Empirical Literature

This section conducts an empirical literature review to identify gaps in existing studies, reviewing 18 relevant studies conducted post the 2008/2009 global financial crisis, a period marked by increased interest in the impact of interest rates on bank risk-taking due to unconventional monetary policies in developed economies. Table 1 summarizes the reviewed literature.

Table 1.

A summary of the empirical literature.

Numerous studies indicate that low or negative interest rates correlate with increased bank risk-taking. Gambacorta (2009) notes heightened default risks during prolonged low-interest periods, while Altunbas et al. (2010) and De Nicolò et al. (2010) link low rates to increased risk-taking for US and European banks. Andries et al. (2015) find that European banks lower lending standards during low-interest periods, and similar findings are observed in Asian and Bolivian banks by Ramayandi et al. (2014) and Ioannidou et al. (2015).

Studies examining unconventional monetary policy periods reveal increased bank risk-taking following policy easing. Dang and Dang (2020) observe heightened risk-taking in Vietnamese banks due to central bank asset purchases, while Schmidt (2018), Kabundi and De Simone (2020) and Nakashima et al. (2020) show contributions from both conventional and unconventional policies to risk-taking in Euro area and Japanese banks.

Differential impacts based on bank size and capitalization are noted. Delis and Kouretas (2011), Buch et al. (2014), Jiménez et al. (2014), Özşuca and Akbostancı (2016) and Brana et al. (2019) find that low interest rates affect risk-taking more significantly for less-capitalized banks. Bubeck et al. (2020) report that negative interest rates encourage riskier investments by European banks, especially those less capitalized. Bonfim and Soares (2018) and Chen et al. (2017) note similar effects in Portuguese and emerging economy banks.

Contrary findings suggest lower interest rates may reduce or not impact risk-taking. Nucera et al. (2017) find negative interest rates reduce risk-taking for large European banks but enhance it for smaller banks. Paligorova and Santos (2017) observe reduced loan spreads during expansionary policy in US banks, indicating lower risk-taking. Bikker and Vervliet (2018) show the negative effects of low interest rates on bank performance and net interest margins, without evidence of increased risk-taking. Matthys et al. (2020) find no evidence of higher bank risk-taking during unconventional policy periods in the US.

Overall, most previous literature supports the idea that loose or expansionary monetary policy enhances bank risk-taking, especially for banks with lower capitalization levels. Nonetheless, we identify two gaps in the empirical literature. Firstly, most previous studies have focused on industrialized economies (Gambacorta 2009; Altunbas et al. 2010; De Nicolò et al. 2010; Delis and Kouretas 2011; Buch et al. 2014; Özşuca and Akbostancı 2016; Nucera et al. 2017; Paligorova and Santos 2017; Bonfim and Soares 2018; Kabundi and De Simone 2020; Dang and Dang 2020) with very few studies conducted for emerging economies (Ramayandi et al. 2014; Özşuca and Akbostancı 2016; Chen et al. 2017; Hussain et al. 2021). Moreover, previous studies have relied on linear econometric estimators and focused on the impact of low-interest-rate environments on bank risk-taking behavior. In light of recent changes in interest rate environments, it would be more beneficial to make use of nonlinear econometric tools to capture the impact of both contractionary and expansionary monetary policies on bank risk-taking behavior.

Against these identified gaps, we contribute to the literature by making a case study for South Africa, of which there exists no previous literature on the country or any other African nation. To account for asymmetries in the interest rate and bank risk-taking relationship we make use of two econometric models. The first is the NARDL which accounts for cyclical asymmetries; that is, it distinguishes periods of raising interest rates or those of falling interest rates. The second is the QARDL model which accounts for location asymmetries which is analogous to capturing the impact of interest rates on bank risk at different levels of risk or bank capitalization (Delis and Kouretas 2011; Buch et al. 2014; Jiménez et al. 2014; Özşuca and Akbostancı 2016; Chen et al. 2017; Bonfim and Soares 2018; Brana et al. 2019; Bubeck et al. 2020). These methods are discussed in detail in the following section.

3. Methodology

3.1. Baseline Regression

Our baseline regression is structured as follows:

RISK = f(INT, INF, GDP, ROE)

The dependent variable, RISK, serves as a measure of risk-taking, encompassing three proxies. Firstly, the liquidity ratio is utilized, where a lower liquidity ratio indicates heightened risk-taking activities in a bank (Jiang et al. 2020). Secondly, non-performing loans gauge the bank’s exposure to default risk (Ramayandi et al. 2014; Delis and Kouretas 2011). Lastly, unsecured lending is employed as a measure of risk-taking, reflecting the extent to which a bank is willing to engage with riskier clients by providing loans without collateral (Paligorova and Santos 2017). The main independent variable, INT, represents the interest rate and is proxied by the lending rate.

The controls in regression (1) include the inflation rate (INF) whose effect on bank risk-taking is twofold. On one hand, increased inflation rates lead to a reduction in the volume of bank assets and, subsequently, a decline in the amount of credit extended (Bohachova 2008). On the other hand, the impact of higher inflation can also negatively affect the earnings of borrowers who already have loans. This, in turn, can undermine the quality of previously issued loans. If the credit rationing effect is more pronounced, all else being equal, banks may opt to take on fewer risks in their financial portfolios as a response to higher inflation rates. Another control variable we use is economic growth (GDP) which is expected to lead to higher credit risk (De Nicolò et al. 2010). Furthermore, periods of low economic activity often lead to higher non-performing loans. The last control variable is the return on equity (ROE) in the banking sector which captures bank profitability. Lower profits may encourage banks to take more risk in their lending.

Regression (1) is estimated using a family of ARDL models, consisting of the conventional ARDL, the NARDL and the QARDL models. Notably, the ARDL framework offers several empirical advantages over competing models, including flexibility in accommodating a mix of I(0) and I(1) variables, suitability for small sample sizes and unbiased estimates of long-run coefficients even when some regressors are endogenous (Pesaran et al. 2001; Shin et al. 2014). Moreover, the nonlinear variants of the model capture cyclical (NARDL) and location (QARDL) asymmetries. These estimators are detailed in the following section.

3.2. ARDL Regression

Firstly, we specify the following baseline ARDL model:

where is a difference operator, θ and α are the regression coefficients, and is a well-behaved error term. To test for the cointegration effect, we follow Pesaran et al. (2001) and test the following null hypothesis:

against the alternative of

H0: θ1 ≠ θ2 ≠ θ3 ≠ θ4 ≠ θ5 ≠ 0

H1: θ1 = θ2 = θ3 = θ4 = θ5 = 0

And we evaluate the test using an F-test applied to critical values derived from Pesaran et al. (2001). Once cointegration effects are confirmed, the long-run regression coefficients are computed as β1 = −θ2/θ1, β2 = −θ3/θ1, β3 = −θ4/θ1 and β4 = −θ5/θ1, and the corresponding error correction model is

where ECT is an error correction term that measures the speed of equilibrium reversion following a shock. It is assumed to be negative and statistically significant. Additionally, Pesaran et al. (2001) consider the t-statistics of the ECT as an additional test for cointegration in the ARDL model.

3.3. NARDL Regression

To account for cyclical asymmetries, we use the NARDL model of Shin et al. (2014) which decomposes the independent variable of interest into positive and negative partitions defined as

with the baseline NARDL regression specified as

where π+ and π− are the coefficients of the positive and negative portions of the interest rate variable, respectively. As in the case of the linear cointegration model, the bounds test for cointegration in the NARDL model is applied to test the following null and alternative hypotheses:

H0: π+ = π− = θ1 = θ2 = θ3 = θ4 = θ5 ≠ 0

H1: π+ ≠ π− ≠ θ1 ≠ θ2 ≠ θ3 ≠ θ4 ≠ θ5 ≠ 0

And once bounds cointegration effects are confirmed, the long-run regression estimates are computed as Ψ+ = = −π+/θ1, Ψ− = = −π−/θ1, β1 = −θ2/θ1, β2 = −θ3/θ1, β3 = −θ4/θ1 and β4 = −θ5/θ1, and the associated error correction model is given as

where ECT is the error correction term. Shin et al. (2014) propose two tests for long-run and short-run asymmetric effects. The first tests the null hypothesis that the long-run coefficients are equivalent (i.e., π+ = π+) whilst the second tests the null hypothesis that the short-run coefficients are not different from each other (η+ = η+).

3.4. QARDL Regression

Lastly, we use the QARDL estimators of Cho et al. (2015). We induce locational asymmetries by integrating the quantile regression of Koenker and Bassett (1978) into the ARDL framework. The baseline QARDL model is specified as

where Xt is the compact set of distributive lag covariates. The conditional mean function is given as

where 0 < θ < 1 denotes any solution to the minimizing problem, and represents the solution from which the θth conditional quantile . After deriving the estimates from the baseline QARDL regression, we can compute the long-run estimator as

Furthermore, the short-run and error correction models are estimated as

where is the quantile error correction term.

4. Data and Empirical Results

4.1. Data Sources

The time-series variables used in our study are collected from three sources: (i) the International Monetary Fund (IMF) financial soundness database, (ii) the South African Reserve Bank (SARB) online database and (iii) the South African National Credit Regulator (NCR) online database. Table 2 links each variable used in the study to its source. All time-series data were collected at a quarterly frequency, spanning the period from 2008:q1 to 2022:q3.

Table 2.

Description of the variables.

4.2. Descriptive Statistics, Correlation Matrix and Unit Root Tests

Table 3 reports the descriptive statistics of bank risk-taking measures and the regressors. Non-performing loans average 4.11% as a percentage of GDP which is lower than the 5% that is regarded as elevated by the International Monetary Fund (IMF). However, it should be noted that during periods of economic crises, non-performing loans reached elevated levels. Liquid assets average 40.37%; however, a decline was observed since 2008. Standard deviations of most of the variables (except for unsecured lending) are low, implying minimal variability in the data.

Table 3.

Descriptive statistics.

Table 4 presents the correlation matrix to show the degree of linear association between the variables and to detect severe multicollinearity. The lending rate is positively and significantly correlated with liquid assets, while its relationship with non-performing loans and unsecured lending is negative and significant. The implication is that higher interest rates are associated with lower risk-taking. The correlations between the regressors are less than 0.8 which is an indication of the absence of severe multicollinearity.

Table 4.

Correlation matrix.

Table 5 presents the results of the ADF, PP and DF-GLS unit root test performed with an intercept (Panel A) and with an intercept and trend (Panel B). Notably, the risk-taking variables (LOANS, LENDING, LIQUID) fail to reject the unit root hypothesis when the test is performed with an intercept (Panel A), whereas the independent variables generally confirm stationary at an I(0) level. However, when the unit root tests are performed using first differences, all series confirm the I(1) process with the exception of the LIQUID variables when the DF-GLS test is performed with an intercept only. Our overall findings suggest that none of the variables is integrated with I(2) which is a crucial condition for ensuring the compatibility of the time series with our ARDL, NARDL and QARDL models.

Table 5.

Unit root tests.

4.3. ARDL Results

We start our empirical analysis with the estimation of linear ARDL models across three regressions, each using a distinct bank risk measure as the dependent variable, as reported in Table 6.

Table 6.

Linear ARDL results.

In the non-performing loans model, the long-run coefficient for the interest rate variable attains significance, with a positive indication that higher (lower) interest rates correspond to increased (decreased) bank risk-taking. Control variable estimates suggest a positive influence of GDP (ROE) on non-performing loans (unsecured loans), while the pandemic exacerbates bank illiquidity and unsecured lending. Conversely, in the short run, the interest rate variable’s significance is confined to the LIQUID variable, with a positive coefficient indicating that higher (lower) interest rates reduce (increase) bank risk-taking by minimizing (augmenting) the asset–liability mismatch.

The observed results theoretically align with Rajan’s (2006) ‘search for yield’ hypothesis, proposing that expansionary (contractionary) policies encourage (discourage) banks to engage in riskier assets. Additionally, our findings resonate with prior empirical evidence in both emerging economies (Özşuca and Akbostancı 2016; Chen et al. 2017; Hussain et al. 2021) and advanced nations (Gambacorta 2009; Altunbas et al. 2010; Delis and Kouretas 2011; Özşuca and Akbostancı 2016; Nucera et al. 2017; Paligorova and Santos 2017; Bonfim and Soares 2018; Kabundi and De Simone 2020; Dang and Dang 2020). The robustness of our results is confirmed by the significance of F-statistics for bounds cointegration and the absence of non-normality, serial correlation and heteroscedasticity in regression error terms.

4.4. NARDL Results

Next, we examine the results from the NARDL models, specifically segregating the impact of increasing interest rates (contractionary monetary policy) from decreasing interest rates (expansionary monetary policy) on bank risk-taking behavior. The NARDL estimates are reported in Table 7.

Table 7.

NARDL results.

In the long term, the coefficients reveal cyclical asymmetries in the associations between interest rates and bank risk, while the estimates on the other control variables remain consistent with those in Table 6 for linear ARDL estimates. The INT+ coefficient is only significant for the LIQUID regression, indicating that raising interest rates (contractionary monetary policy) heightens bank risk-taking. Conversely, the INT- coefficient is only significant for the LOANS and LENDING regressions, with positive (negative) estimates for the former (latter). Overall, our findings suggest that both contractionary and expansionary monetary policies escalate bank risk-taking by exacerbating bank liquidity (i.e., ‘search-for-yield’ effects of Rajan (2006)) and non-performing loans (i.e., ‘risk-shifting’ effects of De Nicolò et al. (2010)), respectively.

In the short run, both contractionary and expansionary policies are found to exacerbate bank risk-taking, except that contractionary (expansionary) policy exacerbates non-performing loans (bank liquidity). The negative and significant error correction terms in all three models confirm that short-run dynamics transition into long-term effects. Additionally, our bounds test for asymmetric cointegration, along with tests for long-run and short-run asymmetries (except for the unsecured loans variable), verifies significant cyclical asymmetries between interest rates and bank risk-taking behavior. Diagnostic tests further validate that the estimated nonlinear regression adheres to classical regression assumptions.

4.5. QARDL Results

Lastly, we examine the results from the QARDL regressions to identify location asymmetries, that is, to see if the behavior of interest rates on bank risk-taking behavior differs between ‘high-risk’, ‘medium-risk’ and ‘low-risk’ environments. The percentiles chosen for this study are the 10th, 25th, 50th, 75th and 90th. Table 8 and Table 9 show the results of the long-run and short-run coefficients of the QARDL regressions, respectively.

Table 8.

Quantile ARDL: long-run estimates.

Table 9.

Quantile ARDL: short-run estimates.

The findings reveal several key observations. Firstly, in the LIQUID regressions, a positively significant coefficient on the interest rates variable is evident at the 50th quantile and above. This implies that higher (lower) interest rates diminish (boost) risk during periods characterized by medium-to-high levels of capital liquidity. Secondly, negative and significant estimates on the interest rates variable are observed in the LOANS regressions at the 10th and 75th quantiles. This suggests that higher (lower) interest rates reduce (increase) risk during periods featuring moderately high and extremely low levels of non-performing loans. Thirdly, negative and significant estimates also appear in the interest rate variable for the LEND regressions at the 50th quantile and below, indicating that higher (lower) interest rates reduce (increase) risk during periods with moderate- to low-risk levels of unsecured lending. Lastly, the short-term estimates generally mirror those of the long-term, with negative and significant error correction terms (ECTs) verifying cointegration effects at different quantiles. The relationships between the variables are ‘more solid’ over the long run than short run. Furthermore, the results suggest that banks alter their lending behavior in response to macroeconomic variables in the long run compared to the short run mostly in response to changes in profit levels.

In summary, our QARDL regression results propose that higher interest rates mitigate risk, particularly for banks with relatively high levels of capital liquidity and low levels of non-performing loans/unsecured lending. These findings align with the theoretical assumptions of Dell’Ariccia et al. (2014), emphasizing the dependence of interest rates on bank risk based on the level of bank capitalization and leverage effects. Contrary to the prior empirical findings of Delis and Kouretas (2011), Buch et al. (2014), Jiménez et al. (2014), Özşuca and Akbostancı (2016), Chen et al. (2017), Bonfim and Soares (2018), Brana et al. (2019) and Bubeck et al. (2020), we observe that the impact of interest rates on risk-taking activity is more prominent during periods when banks are more capitalized or less risky, challenging previous assertions. Following Dell’Ariccia and Marquez (2013), we attribute this to less (more) risky banks or environments being less (more) monitored by financial regulators, allowing less (more) risky banks to engage in more (less) risky investments.

5. Conclusions and Recommendations

We examine the nonlinear relationship between interest rates on bank risk-taking behavior in South Africa between 2008:q1 and 2022:q3 using a family of ARDL models, i.e., linear ARDL, NARDL and QARDL models. Firstly, we estimate a linear ARDL model and find a positive long-run relationship between interest rates and non-performing loans, whereas positive short-run relations are only observed between interest rates and bank liquidity/unsecured lending. Next, we estimate NARDL models to give further information on the different relationships during upswings or downswings of the interest rate variable, and we find that falling (rising) interest rates decreased non-performing loans and yet increased unsecured lending (decreased bank liquidity). Lastly, we estimate QARDL models to segregate the effects of interest rates on bank risk at different levels of risk and find that the relationship is stronger in ‘medium-to-high’ risk environments for non-performing loans and unsecured lending and in ‘medium-to-low’ risk environments for liquidity.

Given South Africa’s current environment characterized by increasing interest rates and elevated risk levels since the COVID-19 period, our findings imply that contractionary policies may heighten financial risk by encouraging banks to invest in more illiquid assets. Conversely, a shift to decreasing interest rates or implementing expansionary monetary policy could elevate unsecured lending. Moreover, the QARDL results suggest that the Reserve Bank can effectively mitigate risk only when risk levels are moderate or low, becoming less effective at higher risk levels, a crucial observation given the sustained high levels of bank risk-taking in South Africa post-COVID-19.

Altogether, our results suggest that SARB cannot use its policy rate in isolation to curb the already high levels of bank risk-taking behavior. We therefore provide the following recommendations based on these observations. Firstly, the Central Bank should reassess its macroprudential toolkit, considering modifications to capital buffers, loan-to-value ratios and countercyclical capital requirements. Macroprudential regulation should be centered around limiting sovereign risk which can impact negatively the profitability of banks in the event of a decline in government bond yields, thus encouraging risk-taking. Secondly, enhancing communication channels through forward guidance measures could help shape bank sector expectations. Lastly, intensifying supervision and monitoring functions, including more frequent stress tests on the banking sector, is essential to effectively manage and curb heightened levels of bank risk-taking behavior.

The limitations/delimitations of the study are as follows: Firstly, the sample period chosen for the analysis was 2008:q1 to 2023:q3 which coincided with the 2008/09 global financial crisis. Data for the period prior to the global financial crisis was not employed as the impact of interest rates on bank risk-taking had not gained traction. Secondly, the study focused on the entire banking sector in South Africa due to the unavailability of data. Aggregated data prevent the analysis of the effect of interest rates on individual banks. Future research studies should focus on the impact of interest rates on individual banks. This will highlight the impact of rising and declining interest rates on risk-taking in banks of different sizes.

Author Contributions

Conceptualization, C.M.; methodology, C.M. and A.P.; software, C.M. and A.P.; validation, A.P.; formal analysis, C.M.; investigation, A.P.; resources, A.P.; data curation, C.M. and A.P.; writing—original draft preparation, C.M.; writing—review and editing, A.P.; visualization, C.M.; supervision, A.P.; project administration, A.P.; funding acquisition, A.P. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Data Availability Statement

The data presented in this study are openly available at the following repository: https://doi.org/10.7910/DVN/H0OTTP.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Altunbas, Yener, Leonardo Gambacorta, and David Marques-Ibanez. 2010. Does monetary policy affect bank risk-taking? International Journal of Central Banking 10: 95–135. [Google Scholar]

- Andries, Alin Marius, Vasile Cocris, and Ioana Plescau. 2015. Low interest rates and bank risk-taking: Has the crisis changed anything? Evidence from the Eurozone. Review of Economic and Business Studies 8: 125–48. [Google Scholar] [CrossRef]

- Bednar, William, and Mahmoud Elamin. 2014. Rising Interest Rate Risk at US Banks. Economic Commentary. Available online: https://www.clevelandfed.org/publications/economic-commentary/ec-201412-rising-interest-rate-risk-at-us-banks (accessed on 20 August 2023).

- Bikker, Jacob A., and Tobias M. Vervliet. 2018. Bank profitability and risk-taking under low interest rates. International Journal of Finance & Economics 23: 3–18. [Google Scholar]

- Bohachova, Olga. 2008. The Impact of Macroeconomic Factors on Risks in the Banking Sector: A Cross-Country Empirical Assessment. IAW Diskussionspapiere. Available online: https://www.econstor.eu/bitstream/10419/36633/1/584116233.PDF (accessed on 18 July 2023).

- Bonfim, Diana, and Carla Soares. 2018. The risk-taking channel of monetary policy: Exploring all avenues. Journal of Money, Credit and Banking 50: 1507–41. [Google Scholar] [CrossRef]

- Brana, Sophie, Alexandra Campmas, and Ion Lapteacru. 2019. (Un) Conventional monetary policy and bank risk-taking: A nonlinear relationship. Economic Modelling 81: 576–93. [Google Scholar] [CrossRef]

- Bubeck, Johannes, Angela Maddaloni, and JoséLuis Peydró. 2020. Negative monetary policy rates and systemic banks’ risk-taking: Evidence from the euro area securities register. Journal of Money, Credit and Banking 52: 197–231. [Google Scholar] [CrossRef]

- Buch, Claudia M., Sandra Eickmeier, and Esteban Prieto. 2014. In search for yield? Survey-based evidence on bank risk taking. Journal of Economic Dynamics and Control 43: 12–30. [Google Scholar] [CrossRef]

- Chen, Minghua, Ji Wu, Bang N. Jeon, and Rui Wang. 2017. Monetary policy and bank risk-taking: Evidence from emerging economies. Emerging Markets Review 31: 116–40. [Google Scholar] [CrossRef]

- Cho, Jin S., Tae-Hwan Kim, and Yongcheol Shin. 2015. Quantile cointegration in the autoregressive distributed-lag modeling framework. Journal of Econometrics 188: 281–300. [Google Scholar] [CrossRef]

- Claessens, Stijn, Nicholas Coleman, and Michael Donnelly. 2018. “Low-For-Long” interest rates and banks’ interest margins and profitability: Cross-country evidence. Journal of Financial Intermediation 35: 1–16. [Google Scholar] [CrossRef]

- Colletaz, Gilbert, Grégory Levieuge, and Alexandra Popescu. 2018. Monetary policy and long-run systemic risk-taking. Journal of Economic Dynamics and Control 86: 165–84. [Google Scholar] [CrossRef]

- Dang, Van D., and Van C. Dang. 2020. The conditioning role of performance on the bank risk-taking channel of monetary policy: Evidence from a multiple-tool regime. Research in International Business and Finance 54: 101301. [Google Scholar] [CrossRef]

- De Nicolò, Gianni, Giovanni Dell’ariccia, Luc Laeven, and Fabián Valencia. 2010. Monetary Policy and Bank Risk Taking. Available online: https://papers.ssrn.com/sol3/Delivery.cfm/SSRN_ID1654582_code261593.pdf?abstractid=1654582&mirid=1 (accessed on 20 October 2023).

- Delis, Manthos D., and Georgios P. Kouretas. 2011. Interest rates and bank risk-taking. Journal of Banking & Finance 35: 840–55. [Google Scholar]

- Dell’Ariccia, Giovanni, and Robert Marquez. 2013. Interest rates and the bank risk-taking channel. Annual Review of Financial Economics 5: 123–41. [Google Scholar] [CrossRef]

- Dell’Ariccia, Giovanni, Luc Laeven, and Robert Marquez. 2014. Real interest rates, leverage, and bank risk-taking. Journal of Economic Theory 149: 65–99. [Google Scholar] [CrossRef]

- Gambacorta, Leonardo. 2009. Monetary Policy and the Risk-Taking Channel. BIS Quarterly Review December. Available online: https://www.bis.org/publ/qtrpdf/r_qt0912f.pdf (accessed on 1 February 2024).

- Hesse, Heiko, and Ken Miyajima. 2022. South Africa: The Financial Sector-Sovereign Nexus. Washington, DC: International Monetary Fund. [Google Scholar]

- Hussain, Muntazir, Usman Bashir, and Ahmad R. Bilal. 2021. Effect of monetary policy on bank risk: Does market structure matter? International Journal of Emerging Markets 16: 696–725. [Google Scholar] [CrossRef]

- Ioannidou, Vasso, Steven Ongena, and José-Luis Peydró. 2015. Monetary policy, risk-taking, and pricing: Evidence from a quasi-natural experiment. Review of Finance 19: 95–144. [Google Scholar] [CrossRef]

- Jiang, Hai, Jinyi Zhang, and Chen Sun. 2020. How does capital buffer affect bank risk-taking? New evidence from China using quantile regression. China Economic Review 60: 101300. [Google Scholar] [CrossRef]

- Jiménez, Gabriel, Steven Ongena, José-Luis Peydró, and Jesús Saurina. 2014. Hazardous times for monetary policy: What do twenty-three million bank loans say about the effects of monetary policy on credit risk-taking? Econometrica 82: 463–505. [Google Scholar]

- Kabundi, Alain, and Francisco N. De Simone. 2020. Monetary policy and systemic risk-taking in the euro area banking sector. Economic Modelling 91: 736–58. [Google Scholar] [CrossRef]

- Koenker, Roger, and Gilbert Bassett. 1978. Regression quantiles. Econometrica 40: 33–50. [Google Scholar] [CrossRef]

- Majola, Given. 2023. SARB Expected to Increase Repo Rate at Next MPC Meeting. Available online: https://www.iol.co.za/business-report/economy/sarb-expected-to-increase-repo-rate-at-next-mpc-meeting-e4cccfeb-6cea-41b3-aa58–87842e02eebc (accessed on 30 March 2023).

- Matthys, Thomas, Elien Meuleman, and Rudi Vander Vennet. 2020. Unconventional monetary policy and bank risk taking. Journal of International Money and Finance 109: 102233. [Google Scholar] [CrossRef]

- Nakashima, Kiyotaka, Masahiko Shibamoto, and Koji Takahashi. 2020. Risk-Taking Channel of Unconventional Monetary Policies in Bank Lending. Available online: https://papers.ssrn.com/sol3/Delivery.cfm/SSRN_ID3534626_code1549748.pdf?abstractid=3044582&mirid=1 (accessed on 20 June 2023).

- Nucera, Federico, André Lucas, Julia Schaumburg, and Bernd Schwaab. 2017. Do negative interest rates make banks less safe? Economics Letters 159: 112–15. [Google Scholar] [CrossRef]

- Özşuca, Ekin A., and Elif Akbostancı. 2016. An empirical analysis of the risk-taking channel of monetary policy in Turkey. Emerging Markets Finance and Trade 52: 589–609. [Google Scholar] [CrossRef]

- Paligorova, Teodora, and João A. C. Santos. 2017. Monetary policy and bank risk-taking: Evidence from the corporate loan market. Journal of Financial Intermediation 30: 35–49. [Google Scholar] [CrossRef]

- Pesaran, M. Hashem, Yongcheol Shin, and Richard J. Smith. 2001. Bounds testing approaches to the analysis of level relationships. Journal of Applied Econometrics 16: 289–326. [Google Scholar] [CrossRef]

- Porcellacchia, Davide. 2020. What Is the Tipping Point? Low Rates and Financial Stability. Available online: https://papers.ssrn.com/sol3/Delivery.cfm/RePEc_ecb_ecbwps_20202447.pdf?abstractid=3657086&mirid=1 (accessed on 15 July 2023).

- Rajan, Raghuram G. 2006. Has finance made the world riskier? European Financial Management 12: 499–533. [Google Scholar] [CrossRef]

- Ramayandi, Arief, Umang Rawat, and Hsiao C. Tang. 2014. Can Low Interest Rates be Harmful: An Assessment of the Bank Risk-Taking Channel in Asia. Available online: http://hdl.handle.net/11540/4188 (accessed on 23 November 2023).

- Schmidt, Jörg. 2018. Unconventional Monetary Policy and Bank Risk-Taking in the Euro Area. MAGKS Joint Discussion Paper Series in Economics; Available online: https://www.econstor.eu/bitstream/10419/200680/1/24-2018_schmidt.pdf (accessed on 18 August 2023).

- Shin, Yongcheol, Byungchul Yu, and Matthew Greenwood-Nimmo. 2014. Modelling asymmetric cointegration and dynamic multipliers in a nonlinear ARDL framework. In Festschrift in Honor of Peter Schmidt. New York: Springer. [Google Scholar] [CrossRef]

- Valencia, Fabián. 2014. Monetary policy, bank leverage, and financial stability. Journal of Economic Dynamics and Control 47: 20–38. [Google Scholar] [CrossRef]

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).