Unveiling Market Connectedness: Dynamic Returns Spillovers in Asian Emerging Stock Markets

Abstract

:1. Introduction

2. Review of Related Studies

3. Materials and Methods

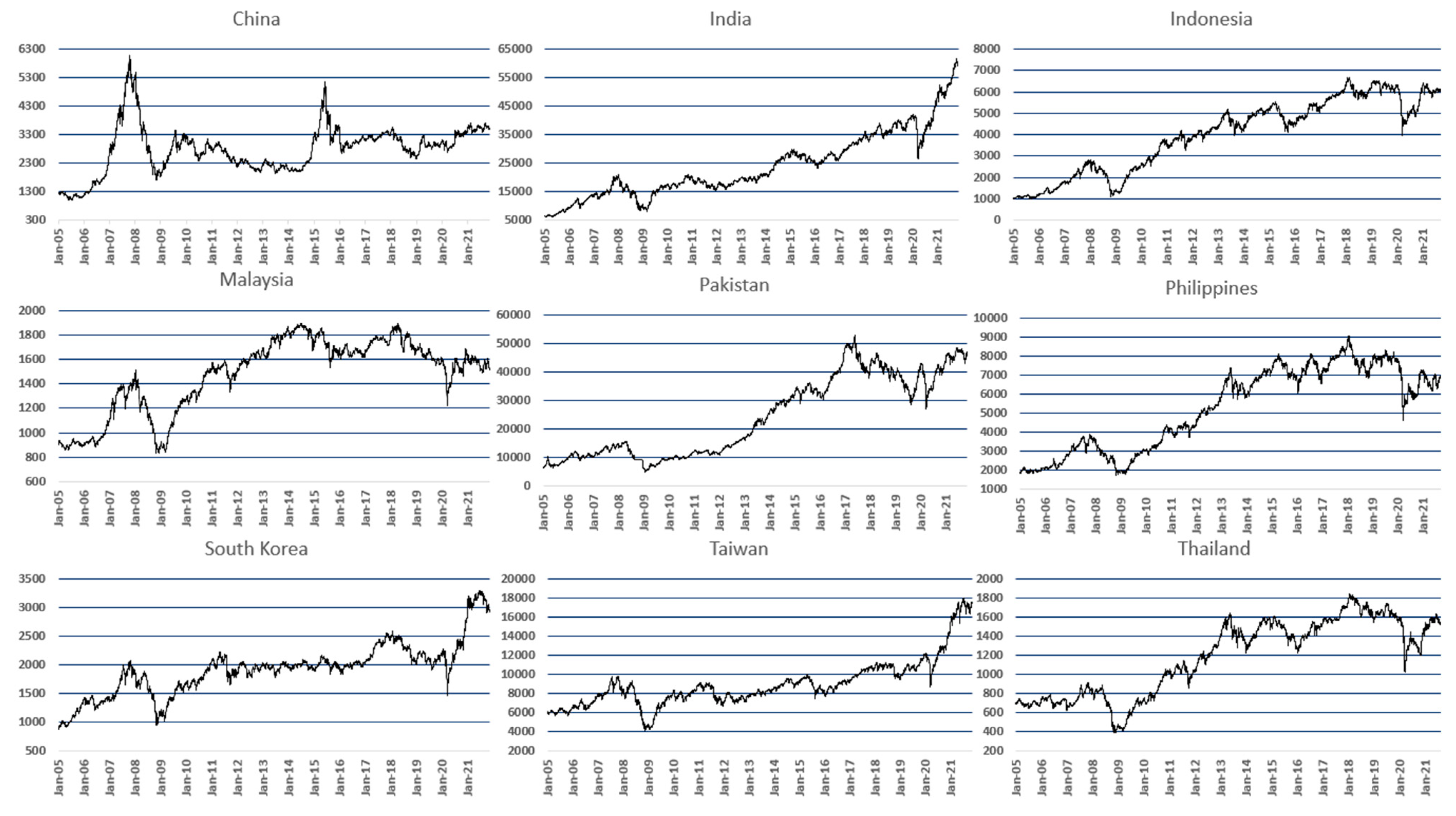

3.1. Data

3.2. Diebold and Yilmaz (2012) Spillover Framework

3.3. Baruník and Křehlík (2018) Spillover Framework

4. Results

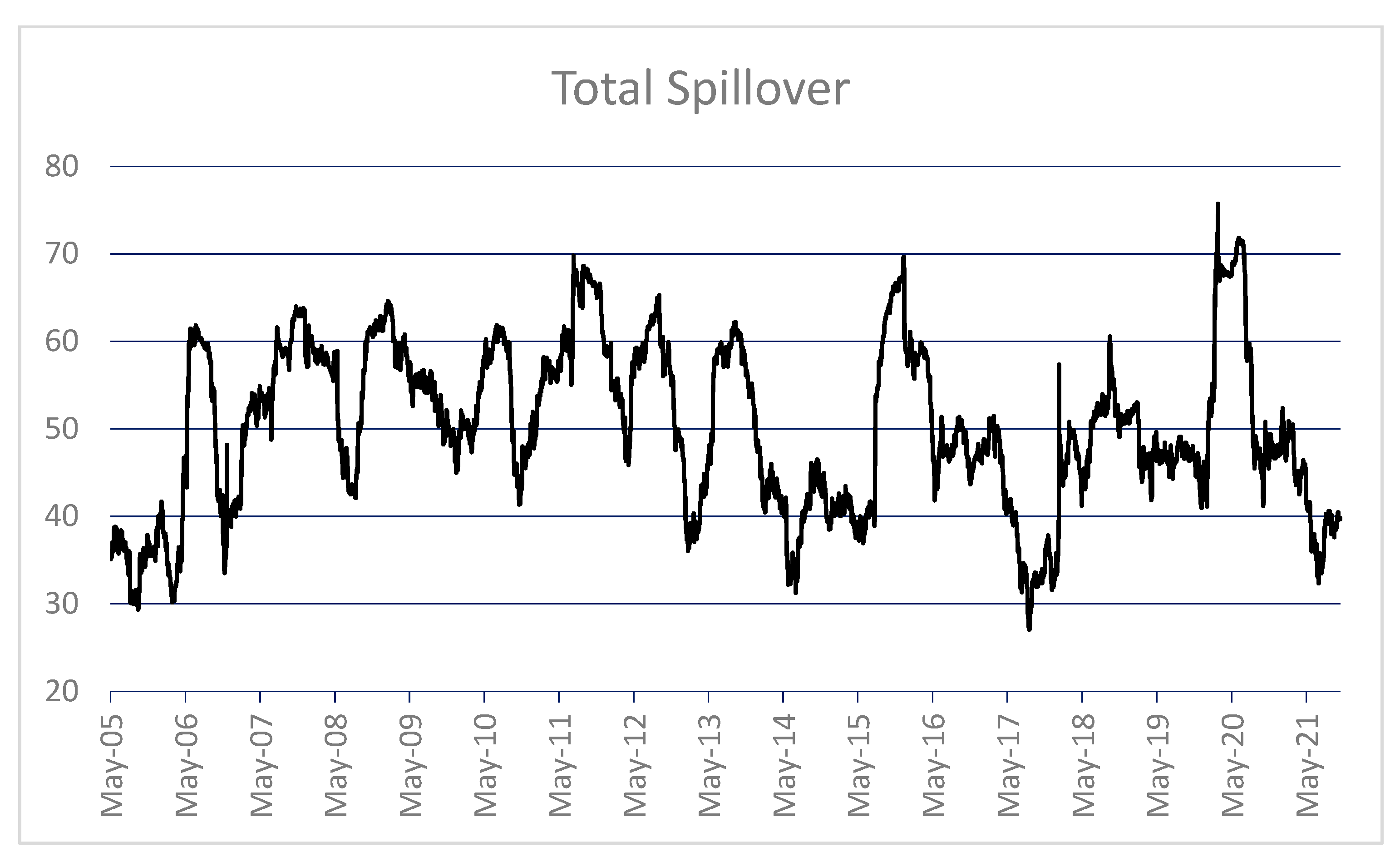

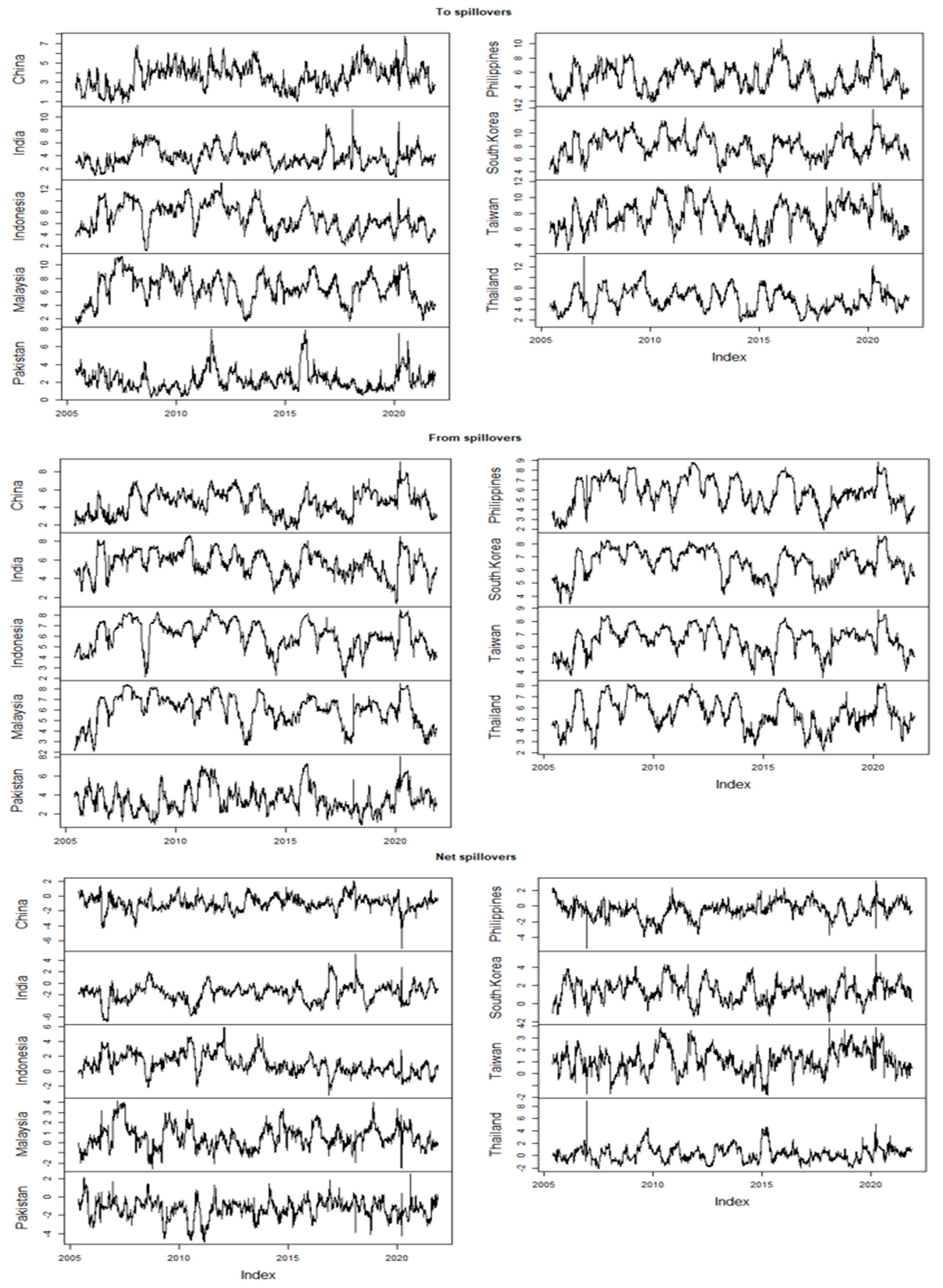

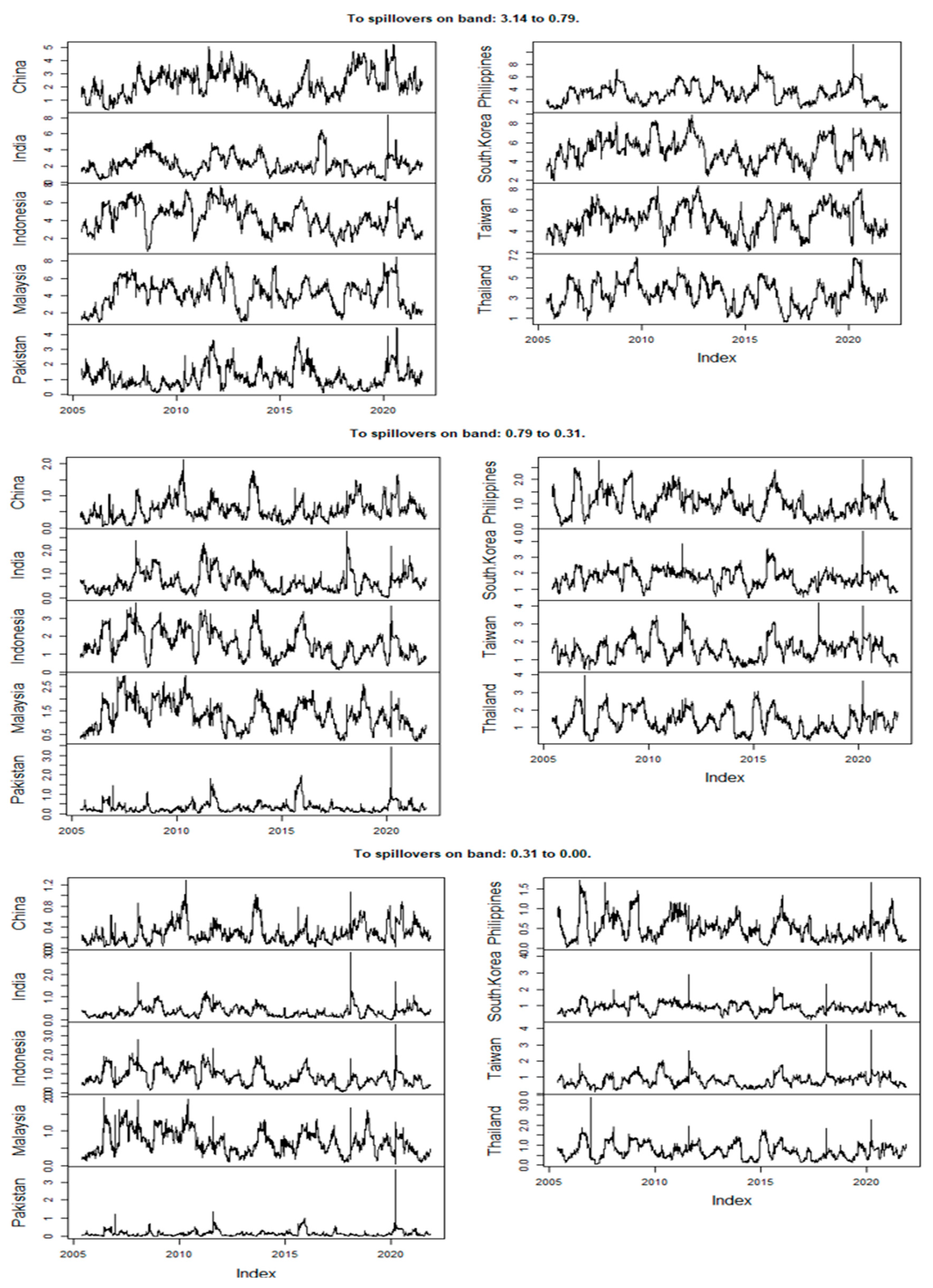

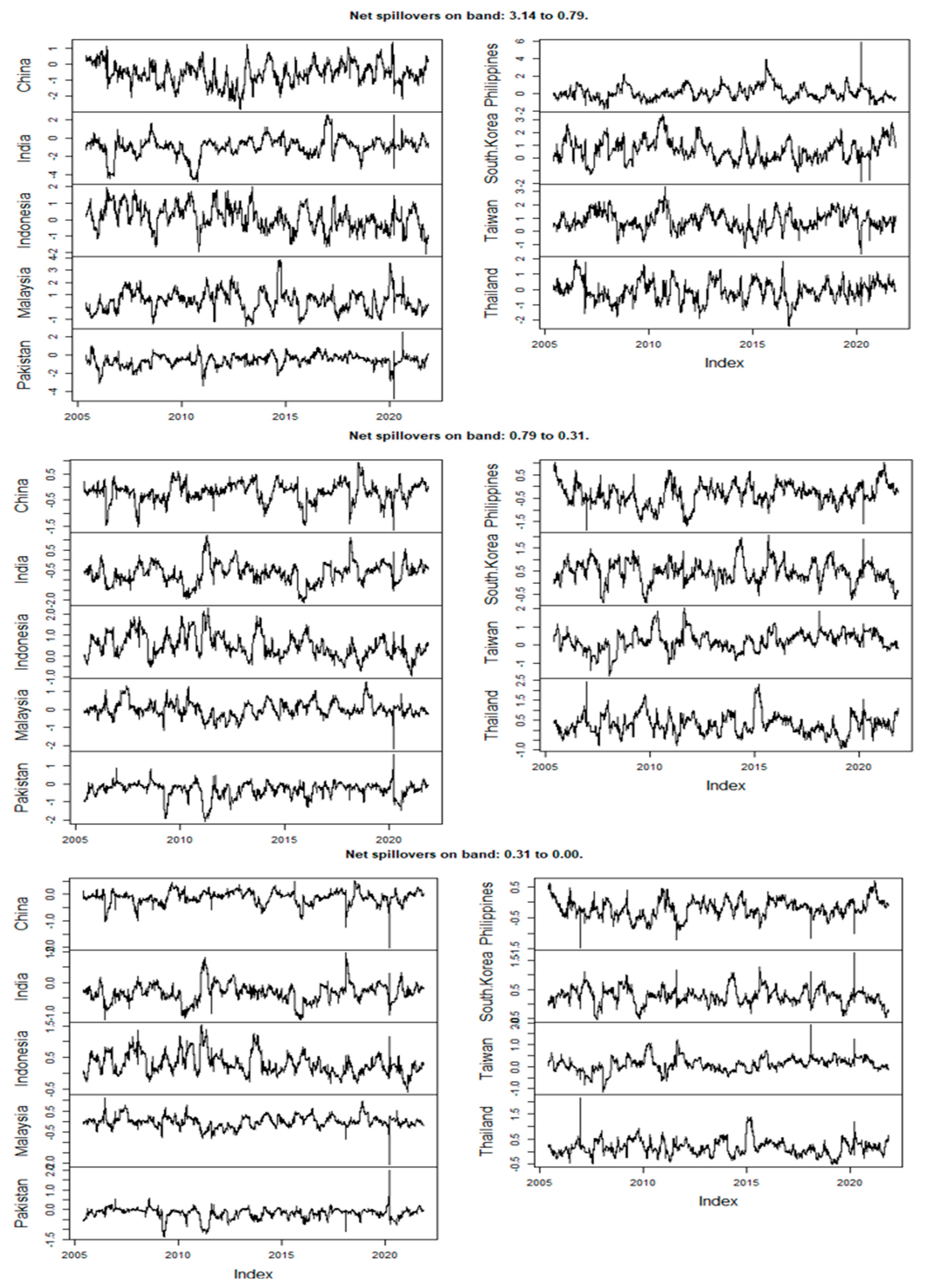

4.1. Diebold and Yilmaz (2012) Framework

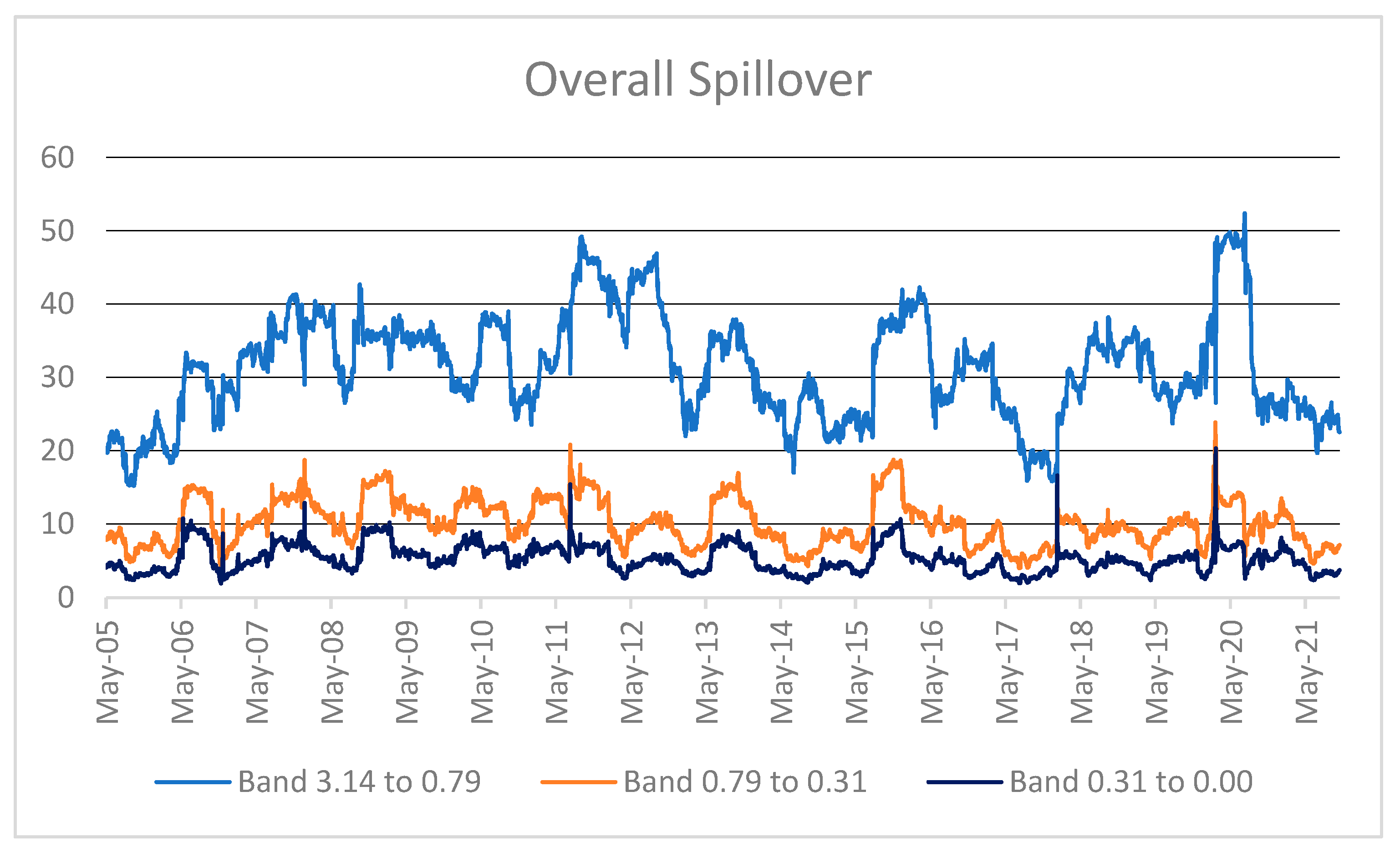

4.2. Baruník and Křehlík (2018) Method

5. Discussion and Conclusions

Author Contributions

Funding

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| China | India | Indonesia | Malaysia | Pakistan | Philippines | South Korea | Taiwan | Thailand | |

|---|---|---|---|---|---|---|---|---|---|

| China | 0 | −0.0186 | −0.1850 | −0.1524 | 0.0212 | −0.0705 | −0.3169 | −0.3217 | −0.1138 |

| India | 0.0186 | 0 | −0.4796 | −0.2167 | 0.0378 | −0.0927 | −0.4460 | −0.3595 | −0.3808 |

| Indonesia | 0.1850 | 0.4796 | 0 | 0.1224 | 0.1504 | 0.2649 | −0.1030 | −0.0423 | 0.1470 |

| Malaysia | 0.1524 | 0.2167 | −0.1224 | 0 | 0.0941 | 0.1366 | −0.1566 | −0.1087 | 0.0067 |

| Pakistan | −0.0212 | −0.0378 | −0.1504 | −0.0941 | 0 | −0.0615 | −0.1549 | −0.1185 | −0.1230 |

| Philippines | 0.0705 | 0.0927 | −0.2649 | −0.1366 | 0.0615 | 0 | −0.3127 | −0.1935 | −0.1279 |

| South Korea | 0.3169 | 0.4460 | 0.1030 | 0.1566 | 0.1549 | 0.3127 | 0 | 0.0497 | 0.2052 |

| Taiwan | 0.3217 | 0.3595 | 0.0423 | 0.1087 | 0.1185 | 0.1935 | −0.0497 | 0 | 0.1246 |

| Thailand | 0.1138 | 0.3808 | −0.1470 | −0.0067 | 0.1230 | 0.1279 | −0.2052 | −0.1246 | 0 |

| Panel I: The spillover table for the band: 3.14 to 0.79 | |||||||||

| Roughly corresponds to 1 day to 4 days (Short Term) | |||||||||

| China | India | Indonesia | Malaysia | Pakistan | Philippines | South Korea | Taiwan | Thailand | |

| China | 0 | −0.0370 | −0.0841 | −0.1181 | 0.0054 | −0.0665 | −0.1837 | −0.1988 | −0.0367 |

| India | 0.0370 | 0 | −0.1191 | −0.0674 | −0.0019 | −0.0401 | −0.0568 | −0.0522 | −0.1663 |

| Indonesia | 0.0841 | 0.1191 | 0 | −0.0883 | 0.0176 | −0.0239 | −0.0568 | −0.0927 | 0.0761 |

| Malaysia | 0.1181 | 0.0674 | 0.0883 | 0 | 0.0254 | 0.0404 | 0.0189 | −0.0306 | 0.1783 |

| Pakistan | −0.0054 | 0.0019 | −0.0176 | −0.0254 | 0 | −0.0204 | −0.0336 | −0.0151 | −0.0196 |

| Philippines | 0.0665 | 0.0401 | 0.0239 | −0.0404 | 0.0204 | 0 | −0.0073 | −0.0301 | 0.0587 |

| South Korea | 0.1837 | 0.0568 | 0.0568 | −0.0189 | 0.0336 | 0.0073 | 0 | −0.0641 | 0.1234 |

| Taiwan | 0.1988 | 0.0522 | 0.0927 | 0.0306 | 0.0151 | 0.0301 | 0.0641 | 0 | 0.1179 |

| Thailand | 0.0367 | 0.1663 | −0.0761 | −0.1783 | 0.0196 | −0.0587 | −0.1234 | −0.1179 | 0 |

| Panel II: The spillover table for the band: 0.79 to 0.31 | |||||||||

| Roughly corresponds to 4 days to 10 days. (Medium Term) | |||||||||

| China | India | Indonesia | Malaysia | Pakistan | Philippines | South Korea | Taiwan | Thailand | |

| China | 0 | 0.0128 | −0.0620 | −0.0248 | 0.0081 | −0.0003 | −0.0820 | −0.0729 | −0.0468 |

| India | −0.0128 | 0 | −0.2254 | −0.1018 | 0.0207 | −0.0328 | −0.2388 | −0.1902 | −0.1371 |

| Indonesia | 0.0620 | 0.2254 | 0 | 0.1148 | 0.0733 | 0.1747 | −0.0262 | 0.0316 | 0.0342 |

| Malaysia | 0.0248 | 0.1018 | −0.1148 | 0 | 0.0393 | 0.0713 | −0.0938 | −0.0356 | −0.0942 |

| Pakistan | −0.0081 | −0.0207 | −0.0733 | −0.0393 | 0 | −0.0208 | −0.0684 | −0.0569 | −0.0561 |

| Philippines | 0.0003 | 0.0328 | −0.1747 | −0.0713 | 0.0208 | 0 | −0.1859 | −0.0985 | −0.1173 |

| South Korea | 0.0820 | 0.2388 | 0.0262 | 0.0938 | 0.0684 | 0.1859 | 0 | 0.0676 | 0.0430 |

| Taiwan | 0.0729 | 0.1902 | −0.0316 | 0.0356 | 0.0569 | 0.0985 | −0.0676 | 0 | −0.0020 |

| Thailand | 0.0468 | 0.1371 | −0.0342 | 0.0942 | 0.0561 | 0.1173 | −0.0430 | 0.0020 | 0 |

| Panel III: The spillover table for the band: 0.31 to 0.00 | |||||||||

| Roughly corresponds to 10 days to Inf days. (Long Term) | |||||||||

| China | India | Indonesia | Malaysia | Pakistan | Philippines | South Korea | Taiwan | Thailand | |

| China | 0 | 0.0056 | −0.0389 | −0.0095 | 0.0077 | −0.0037 | −0.0512 | −0.0500 | −0.0303 |

| India | −0.0056 | 0 | −0.1351 | −0.0474 | 0.0190 | −0.0198 | −0.1504 | −0.1171 | −0.0774 |

| Indonesia | 0.0389 | 0.1351 | 0 | 0.0960 | 0.0595 | 0.1141 | −0.0200 | 0.0188 | 0.0366 |

| Malaysia | 0.0095 | 0.0474 | −0.0960 | 0 | 0.0294 | 0.0249 | −0.0818 | −0.0424 | −0.0774 |

| Pakistan | −0.0077 | −0.0190 | −0.0595 | −0.0294 | 0 | −0.0203 | −0.0529 | −0.0465 | −0.0473 |

| Philippines | 0.0037 | 0.0198 | −0.1141 | −0.0249 | 0.0203 | 0 | −0.1194 | −0.0649 | −0.0693 |

| South Korea | 0.0512 | 0.1504 | 0.0200 | 0.0818 | 0.0529 | 0.1194 | 0 | 0.0461 | 0.0389 |

| Taiwan | 0.0500 | 0.1171 | −0.0188 | 0.0424 | 0.0465 | 0.0649 | −0.0461 | 0 | 0.0088 |

| Thailand | 0.0303 | 0.0774 | −0.0366 | 0.0774 | 0.0473 | 0.0693 | −0.0389 | −0.0088 | 0 |

References

- Abbas, Ghulam, Shawkat Hammoudeh, Syed Jawad Hussain Shahzad, Shouyang Wang, and Yunjie Wei. 2019. Return and volatility connectedness between stock markets and macroeconomic factors in the G-7 countries. Journal of Systems Science and Systems Engineering 28: 1–36. [Google Scholar] [CrossRef]

- Ahmad, Nasir, Mobeen Ur Rehman, Xuan Vinh Vo, and Sang Hoon Kang. 2022. Does inter-region portfolio diversification pay more than international diversification? The Quarterly Review of Economics and Finance 83: 26–35. [Google Scholar]

- Ali, Fahad, Ahmet Sensoy, and John Goodell. 2023. Identifying diversifiers, hedges, and safe havens among Asia Pacific equity markets during COVID-19: New results for ongoing portfolio allocation. International Review of Economics & Finance 85: 744–92. [Google Scholar]

- Aslam, Faheem, Ahmed Imran Hunjra, Elie Bouri, Khurram Shahzad Mughal, and Mrestyal Khan. 2023. Dependence structure across equity sectors: Evidence from vine copulas. Borsa Istanbul Review 23: 184–202. [Google Scholar] [CrossRef]

- Aslam, Faheem, Paulo Ferreira, Khurram Shahzad Mughal, and Beenish Bashir. 2021. Intraday volatility spillovers among European financial markets during COVID-19. International Journal of Financial Studies 9: 5. [Google Scholar] [CrossRef]

- Aslam, Faheem, Yasir Tariq Mohmand, Paulo Ferreira, Bilal Ahmed Memon, Maaz Khan, and Mrestyal Khan. 2020. Network analysis of global stock markets at the beginning of the coronavirus disease (COVID-19) outbreak. Borsa Istanbul Review 20: S49–61. [Google Scholar] [CrossRef]

- Baele, Lieven. 2002. Volatility spillover effects in European equity markets: Evidence from a regime-switching model. Journal of Financial and Quantitative Analysis 40: 31–43. [Google Scholar]

- Baele, Lieven. 2005. Volatility spillover effects in European equity markets. Journal of Financial and Quantitative Analysis 40: 373–401. [Google Scholar] [CrossRef]

- Baruník, Jozef, and Tomáš Křehlík. 2018. Measuring the frequency dynamics of financial connectedness and systemic risk. Journal of Financial Econometrics 16: 271–96. [Google Scholar] [CrossRef]

- Beirne, John, Guglielmo Maria Caporale, Marianne Schulze-Ghattas, and Nicola Spagnolo. 2013. Volatility spillovers and contagion from mature to emerging stock markets. Review of International Economics 21: 1060–75. [Google Scholar] [CrossRef]

- Cooper, Richard N., Kenneth J. Arrow, Rudiger Dornbusch, Yung Chul Park, Stijin Claessens, Deon Filmer, Jeffrey S. Hammer, Lant H. Pritchett, Michael Woolcock, Deepa Narayan, and et al. 2000. The World Bank research observer 15 (2). Policy, Research Working Paper; no. WPS 2463. Available online: https://documents1.worldbank.org/curated/ru/264171468320067686/pdf/multi-page.pdf (accessed on 22 August 2023).

- Diebold, Francis X., and Kamil Yilmaz. 2009. Measuring financial asset return and volatility spillovers, with application to global equity markets. The Economic Journal 119: 158–71. [Google Scholar] [CrossRef]

- Diebold, Francis X., and Kamil Yilmaz. 2012. Better to give than to receive: Predictive directional measurement of volatility spillovers. International Journal of Forecasting 28: 57–66. [Google Scholar] [CrossRef]

- Dungey, Mardi, and Dungey Gajurel. 2014. Equity market contagion during the global financial crisis: Evidence from the world’s eight largest economies. Economic Systems 38: 161–77. [Google Scholar] [CrossRef]

- Eun, Cheol S., and Sangdal Shim. 1989. International transmission of stock market movements. Journal of Financial and Quantitative Analysis 24: 241–56. [Google Scholar] [CrossRef]

- Fang, Victor, Yee-Choon Lim, and Chien-Ting Lin. 2006. Volatility transmissions between stock and bond markets: Evidence from Japan and the US. International Journal of Information Technology 12: 120–12. [Google Scholar]

- Forbes, Kristin J., and Roberto Rigobon. 2002. No contagion, only interdependence: Measuring stock market comovements. The Journal of Finance 57: 2223–61. [Google Scholar] [CrossRef]

- Gallo, Giampiero M., and Edoardo Otranto. 2008. Volatility spillovers, interdependence and comovements: A Markov Switching approach. Computational Statistics & Data Analysis 52: 3011–26. [Google Scholar]

- Glezakos, Michalis, Anna Merika, and Haralambos Kaligosfiris. 2007. Interdependence of major world stock exchanges: How is the Athens stock exchange affected? International Research Journal of Finance and Economics 7: 24–39. [Google Scholar]

- Graham, Michael, Jarno Kiviaho, and Jussi Nikkinen. 2012. Integration of 22 emerging stock markets: A three-dimensional analysis. Global Finance Journal 23: 34–47. [Google Scholar] [CrossRef]

- Hamao, Yasushi, Ronald W. Masulis, and Victor Ng. 1990. Correlations in price changes and volatility across international stock markets. The Review of Financial Studies 3: 281–307. [Google Scholar] [CrossRef]

- Hung, Ngo Thai. 2019. Return and volatility spillover across equity markets between China and Southeast Asian countries. Journal of Economics, Finance and Administrative Science 24: 66–81. [Google Scholar] [CrossRef]

- Joshi, Prashant. 2011. Return and volatility spillovers among Asian stock markets. Sage Open 1: 2158244011413474. [Google Scholar] [CrossRef]

- Kanas, Angelos. 1998. Volatility spillovers across equity markets: European evidence. Applied Financial Economics 8: 245–56. [Google Scholar] [CrossRef]

- Kao, Wei-Shun, Tzu-Chuan Kao, Chang-Cheng Changchien, Li-Hsun Wang, and Kuei-Tzu Yeh. 2018. Contagion in international stock markets after the subprime mortgage crisis. The Chinese Economy 51: 130–53. [Google Scholar] [CrossRef]

- Khan, Mrestyal, and Maaz Khan. 2021. Cryptomarket Volatility in Times of COVID-19 Pandemic: Application of GARCH Models. Economic Research Guardian 11: 170–81. [Google Scholar]

- Korinek, Anton. 2018. Regulating capital flows to emerging markets: An externality view. Journal of International Economics 111: 61–80. [Google Scholar] [CrossRef]

- Li, Yanshuang, Yujie Shi, Yongdong Shi, Shangkun Yi, and Weiping Zhang. 2023. COVID-19 vaccinations and risk spillovers: Evidence from Asia-Pacific stock markets. Pacific-Basin Finance Journal 79: 102004. [Google Scholar] [CrossRef]

- Markowitz, Harry Max. 1952. Portfolio Selection. London: Yale University Press. [Google Scholar]

- Ng, Angela. 2000. Volatility spillover effects from Japan and the US to the Pacific–Basin. Journal of International Money and Finance 19: 207–33. [Google Scholar] [CrossRef]

- Malik, Preeti, Urvish Patel, Deep Mehtab, Nidhai Patel, Reveena Kelkar, Muhammad Akrmah, Janice L. Gabrilove, and Henry Sacks. 2021. Biomarkers and outcomes of COVID-19 hospitalisations: Systematic review and meta-analysis. BMJ Evidence-Based Medicine 26: 107–8. [Google Scholar] [CrossRef] [PubMed]

- Panda, Ajaya. Kumar, Pradiptarathi Panda, Swagatika Nanda, and Atul Parad. 2021. Information bias and its spillover effect on return volatility: A study on stock markets in the Asia-Pacific region. Pacific-Basin Finance Journal 69: 101653. [Google Scholar] [CrossRef]

- Pete, Engardio. 2006. India Are Revolutionizing Global Business. New York: McGraw-Hill. [Google Scholar]

- Pretorius, Elna. 2002. Economic determinants of emerging stock market interdependence. Emerging Markets Review 3: 84–105. [Google Scholar] [CrossRef]

- Savva, Christos S., Denise R. Osborn, and Len Gill. 2004. Volatility, Spillover Effects and Correlations in US and Major European Markets. Manchester: University of Manchester. [Google Scholar]

- Sharpe, Willian Forsyth. 1963. A simplified model for portfolio analysis. Management Science 9: 277–93. [Google Scholar] [CrossRef]

- Thomas, Nisha Mary, Smita Kashiramka, Surendra Singh Yadav, and Justin Paul. 2022. Role of emerging markets vis-à-vis frontier markets in improving portfolio diversification benefits. International Review of Economics & Finance 78: 95–121. [Google Scholar]

- Wagner, Niklas, and Alexander Szimayer. 2004. Local and spillover shocks in implied market volatility: Evidence for the US and Germany. Research in International Business and Finance 18: 237–51. [Google Scholar] [CrossRef]

- Zhang, Hua, Jinyu Chen, and Liuguo Shao. 2021. Dynamic spillovers between energy and stock markets and their implications in the context of COVID-19. International Review of Financial Analysis 77: 101828. [Google Scholar] [CrossRef] [PubMed]

| China | India | Indonesia | Malaysia | Pakistan | Philippines | South Korea | Taiwan | Thailand | |

|---|---|---|---|---|---|---|---|---|---|

| Mean | 0.024% | 0.051% | 0.044% | 0.012% | 0.046% | 0.032% | 0.028% | 0.025% | 0.020% |

| Std.Dev. | 1.540% | 1.443% | 1.265% | 0.733% | 1.240% | 1.278% | 1.221% | 1.116% | 1.194% |

| Kurtosis | 5.26154 | 9.33308 | 8.61167 | 14.18593 | 4.55860 | 11.63273 | 9.64224 | 4.82645 | 19.1970 |

| Skewness | −0.5649 | −0.4623 | −0.5748 | −0.8511 | −0.5255 | −0.9905 | −0.5293 | −0.4848 | −1.2612 |

| Minimum | −0.0925 | −0.1138 | −0.1095 | −0.0997 | −0.1009 | −0.1432 | −0.1117 | −0.0673 | −0.1606 |

| Maximum | 0.09034 | 0.120 | 0.09704 | 0.06626 | 0.08255 | 0.09365 | 0.11284 | 0.06525 | 0.10577 |

| Jarqua Bera Test | 5187.7 | 15,759 | 13,523 | 36,577 | 3920.2 | 24,949 | 16,858 | 4341 | 67,176 |

| ADF test | −46.761 *** | −46.995 *** | −43.904 *** | −43.241 *** | −42.453 *** | −45.132 *** | −44.959 *** | −44.131 *** | −44.061 *** |

| Count | 4311 | 4311 | 4311 | 4311 | 4311 | 4311 | 4311 | 4311 | 4311 |

| China | India | Indonesia | Malaysia | Pakistan | Philippines | South Korea | Taiwan | Thailand | From | |

|---|---|---|---|---|---|---|---|---|---|---|

| China | 70.52 | 2.17 | 4 | 3.84 | 0.37 | 2.38 | 6.75 | 6.61 | 3.36 | 29.48 |

| India | 2 | 53.81 | 8.33 | 5.53 | 0.49 | 5.94 | 9.53 | 8.31 | 6.04 | 46.17 |

| Indonesia | 2.34 | 4.02 | 43.87 | 10.23 | 0.8 | 8.24 | 10.47 | 9.78 | 10.25 | 56.13 |

| Malaysia | 2.47 | 3.58 | 11.33 | 44.52 | 0.6 | 8.22 | 10.2 | 10.01 | 9.07 | 55.48 |

| Pakistan | 0.56 | 0.83 | 2.16 | 1.44 | 88.66 | 1.05 | 1.86 | 1.53 | 1.9 | 11.33 |

| Philippines | 1.74 | 5.11 | 10.62 | 9.45 | 0.49 | 47.18 | 9.18 | 8.38 | 7.84 | 52.81 |

| South Korea | 3.9 | 5.52 | 9.55 | 8.79 | 0.47 | 6.37 | 39.84 | 17.67 | 7.9 | 60.17 |

| Taiwan | 3.71 | 5.08 | 9.4 | 9.03 | 0.47 | 6.64 | 18.12 | 40.42 | 7.13 | 59.58 |

| Thailand | 2.34 | 2.62 | 11.57 | 9.13 | 0.79 | 6.68 | 9.75 | 8.25 | 48.87 | 51.13 |

| Directional to Others | 19.06 | 28.93 | 66.96 | 57.44 | 4.48 | 45.52 | 75.86 | 70.54 | 53.49 | 422.28 |

| Directional Including Own | 89.58 | 82.74 | 110.83 | 101.96 | 93.14 | 92.7 | 115.7 | 110.96 | 102.36 | 46.92% |

| Net Directional Connectedness | −10.42 | −17.24 | 10.83 | 1.96 | −6.85 | −7.29 | 15.69 | 10.96 | 2.36 |

| Panel I: The spillover table for the band: 3.14 to 0.79. Roughly corresponds to 1 day to 4 days (Short Term) | ||||||||||

| China | India | Indonesia | Malaysia | Pakistan | Philippines | South Korea | Taiwan | Thailand | From | |

| China | 51.22 | 1.42 | 2.38 | 2.62 | 0.21 | 1.59 | 4.61 | 4.44 | 2.14 | 19.41 |

| India | 1.09 | 40.47 | 3.64 | 2.72 | 0.33 | 3.34 | 4.26 | 3.81 | 2.86 | 22.05 |

| Indonesia | 1.63 | 2.56 | 29.67 | 6.86 | 0.64 | 5.3 | 6.4 | 6.32 | 6.2 | 35.91 |

| Malaysia | 1.56 | 2.11 | 6.07 | 30.3 | 0.37 | 5.04 | 6.04 | 6.25 | 4.83 | 32.27 |

| Pakistan | 0.25 | 0.31 | 0.8 | 0.6 | 57.88 | 0.44 | 0.6 | 0.43 | 0.77 | 4.2 |

| Philippines | 0.99 | 2.97 | 5.09 | 5.4 | 0.26 | 33.02 | 4.37 | 4.49 | 3.82 | 27.39 |

| South Korea | 2.96 | 3.75 | 5.89 | 6.21 | 0.3 | 4.3 | 28.45 | 12.39 | 4.79 | 40.59 |

| Taiwan | 2.65 | 3.34 | 5.49 | 5.98 | 0.29 | 4.22 | 11.81 | 28.17 | 4.09 | 37.87 |

| Thailand | 2.21 | 1.36 | 6.88 | 6.44 | 0.59 | 4.34 | 5.9 | 5.15 | 35.12 | 32.87 |

| Contribution To | 13.34 | 17.82 | 36.24 | 36.83 | 2.99 | 28.57 | 43.99 | 43.28 | 29.5 | 252.56 |

| Contribution Including Own | 64.56 | 58.29 | 65.91 | 67.13 | 60.87 | 61.59 | 72.44 | 71.45 | 64.62 | 43.04% |

| Net Spillover | −6.07 | −4.23 | 0.33 | 4.56 | −1.21 | 1.18 | 3.4 | 5.41 | −3.37 | |

| Panel II: The spillover for the band: 0.79 to 0.31. Roughly corresponds to 4 days to 10 days. (Medium Term) | ||||||||||

| China | India | Indonesia | Malaysia | Pakistan | Philippines | South Korea | Taiwan | Thailand | From | |

| China | 12.9 | 0.47 | 1.02 | 0.79 | 0.11 | 0.48 | 1.34 | 1.35 | 0.76 | 6.32 |

| India | 0.58 | 8.7 | 2.93 | 1.8 | 0.11 | 1.61 | 3.25 | 2.79 | 1.99 | 15.06 |

| Indonesia | 0.46 | 0.9 | 9.19 | 2.18 | 0.11 | 1.86 | 2.52 | 2.16 | 2.56 | 12.75 |

| Malaysia | 0.57 | 0.88 | 3.22 | 9.22 | 0.15 | 1.96 | 2.52 | 2.3 | 2.58 | 14.18 |

| Pakistan | 0.18 | 0.3 | 0.77 | 0.5 | 19.98 | 0.34 | 0.73 | 0.63 | 0.63 | 4.08 |

| Philippines | 0.48 | 1.31 | 3.43 | 2.6 | 0.15 | 9.22 | 2.97 | 2.4 | 2.49 | 15.83 |

| South Korea | 0.6 | 1.1 | 2.28 | 1.68 | 0.11 | 1.29 | 7.34 | 3.37 | 1.94 | 12.37 |

| Taiwan | 0.7 | 1.08 | 2.45 | 1.98 | 0.12 | 1.51 | 3.98 | 7.92 | 1.91 | 13.73 |

| Thailand | 0.34 | 0.76 | 2.87 | 1.73 | 0.13 | 1.44 | 2.33 | 1.89 | 8.83 | 11.49 |

| Contribution To | 3.91 | 6.8 | 18.97 | 13.26 | 0.99 | 10.49 | 19.64 | 16.89 | 14.86 | 105.81 |

| Contribution Including Own | 16.81 | 15.5 | 28.16 | 22.48 | 20.97 | 19.71 | 26.98 | 24.81 | 23.69 | 53.14% |

| Net Spillover | −2.41 | −8.26 | 6.22 | −0.92 | −3.09 | −5.34 | 7.27 | 3.16 | 3.37 | |

| Panel III: The spillover for the band: 0.31 to 0.00. Roughly corresponds to 10 days to Inf days. (Long Term) | ||||||||||

| China | India | Indonesia | Malaysia | Pakistan | Philippines | South Korea | Taiwan | Thailand | From | |

| China | 6.41 | 0.27 | 0.6 | 0.43 | 0.06 | 0.31 | 0.8 | 0.82 | 0.46 | 3.75 |

| India | 0.32 | 4.64 | 1.77 | 1.02 | 0.05 | 1 | 2.02 | 1.71 | 1.19 | 9.08 |

| Indonesia | 0.25 | 0.55 | 5 | 1.19 | 0.05 | 1.08 | 1.55 | 1.3 | 1.49 | 7.46 |

| Malaysia | 0.34 | 0.59 | 2.05 | 5 | 0.08 | 1.22 | 1.64 | 1.46 | 1.66 | 9.04 |

| Pakistan | 0.13 | 0.22 | 0.59 | 0.35 | 10.8 | 0.27 | 0.54 | 0.48 | 0.49 | 3.07 |

| Philippines | 0.27 | 0.82 | 2.11 | 1.45 | 0.09 | 4.94 | 1.85 | 1.49 | 1.53 | 9.61 |

| South Korea | 0.34 | 0.66 | 1.37 | 0.91 | 0.06 | 0.78 | 4.05 | 1.91 | 1.17 | 7.2 |

| Taiwan | 0.37 | 0.66 | 1.47 | 1.07 | 0.06 | 0.9 | 2.33 | 4.33 | 1.13 | 7.99 |

| Thailand | 0.19 | 0.5 | 1.82 | 0.97 | 0.07 | 0.9 | 1.52 | 1.21 | 4.91 | 7.18 |

| Contribution To | 2.21 | 4.27 | 11.78 | 7.39 | 0.52 | 6.46 | 12.25 | 10.38 | 9.12 | 64.38 |

| Contribution Including Own | 8.62 | 8.91 | 16.78 | 12.39 | 11.32 | 11.4 | 16.3 | 14.71 | 14.03 | 56.25% |

| Net Spillover | −1.54 | −4.81 | 4.32 | −1.65 | −2.55 | −3.15 | 5.05 | 2.39 | 1.94 | |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Khan, M.; Khan, M.; Kayani, U.N.; Mughal, K.S.; Mumtaz, R. Unveiling Market Connectedness: Dynamic Returns Spillovers in Asian Emerging Stock Markets. Int. J. Financial Stud. 2023, 11, 112. https://doi.org/10.3390/ijfs11030112

Khan M, Khan M, Kayani UN, Mughal KS, Mumtaz R. Unveiling Market Connectedness: Dynamic Returns Spillovers in Asian Emerging Stock Markets. International Journal of Financial Studies. 2023; 11(3):112. https://doi.org/10.3390/ijfs11030112

Chicago/Turabian StyleKhan, Maaz, Mrestyal Khan, Umar Nawaz Kayani, Khurrum Shahzad Mughal, and Roohi Mumtaz. 2023. "Unveiling Market Connectedness: Dynamic Returns Spillovers in Asian Emerging Stock Markets" International Journal of Financial Studies 11, no. 3: 112. https://doi.org/10.3390/ijfs11030112

APA StyleKhan, M., Khan, M., Kayani, U. N., Mughal, K. S., & Mumtaz, R. (2023). Unveiling Market Connectedness: Dynamic Returns Spillovers in Asian Emerging Stock Markets. International Journal of Financial Studies, 11(3), 112. https://doi.org/10.3390/ijfs11030112