Abstract

This study aims to systematically analyze and synthesize the literature produced thus far on cryptocurrency investment. We use a systematic review process supported by VOSviewer bibliographic coupling to review 482 papers published in the ABS 2021 journal list, considering all different areas of knowledge. This paper contributes an in-depth systematic analysis on the unconsolidated topic of cryptocurrency investment through the use of a cluster-based approach grounded in a bibliographic coupling analysis, revealing complex network associations within each cluster. Four literature clusters emerge from the cryptocurrency investment literature, namely, investigating investor behavior, portfolio diversification, cryptocurrency market microstructure, and risk management in cryptocurrency investment. Additionally, the study delivers a qualitative analysis that reveals the main conclusions and future research venues by cluster. The findings provide researchers with cluster-based information and structured networking for research outlets and literature strands.

1. Introduction

The first stone in the creation of the cryptocurrency market was the white paper published by Nakamoto (2008) explaining the creation and operation of a new digital currency which has the particularity of being decentralized and does not require the intermediation of any financial institution.

Although used as means of payment, cryptocurrencies tend to be explored more as investment assets (Almeida 2021; Almeida and Gonçalves 2023b; Blau 2017; Li et al. 2021). Cryptocurrencies have become a popular asset class in global financial markets, with their market experiencing rapid development that has spread to the four corners of the world, including both developed and developing countries, as one of the world’s fastest growing financial markets (Białkowski 2020; Fang et al. 2021). The emergence of this new market, along with the creation of investment platforms, has brought investment opportunities with the dream of high and easy profits closer to regular people (many of them without any financial knowledge). This has led to a flood of new, non-institutional investors seeking to be millionaires in this highly volatile market. Some have made it, and some have lost everything. Thus, unsurprisingly, the cryptocurrency market has received significant attention from everyone: the media, regulators, and individual and institutional investors. It is also a current and important topic in academic research (Angerer et al. 2020; Li et al. 2021).

Due to the increasing popularity of cryptocurrencies, new empirical evidence is being produced very quickly; therefore, there is a great need to aggregate and synthesize the existing knowledge on cryptocurrency investments and to identify gaps in the literature (Angerer et al. 2020; Corbet et al. 2019). Therefore, in this study, we aggregate and synthesize what is currently known in the cryptocurrency investment literature, providing important insights for investors to better assess their investment by maximizing returns and minimizing the risks, and helping researchers to better study the complexities of the cryptocurrency market.

In this regard, following the call of Angerer et al. (2020) and Corbet et al. (2019), we develop a bibliometric analysis of cryptocurrency investment with a threefold objective: to consolidate and map the knowledge of the growing academic literature on cryptocurrency investment; to facilitate future research by identifying gaps in the literature; and to provide useful research findings for investors, academics, professionals, and policymakers.

This paper contributes a cluster-based systematic analysis on the important and unconsolidated topic of cryptocurrency investment. We provide a more in-depth analysis than previous research (Aysan et al. 2021; Bariviera and Merediz-Solà 2021; García-Corral et al. 2022; Jalal et al. 2021; Liang et al. 2016; Merediz-Solá and Bariviera 2019) by using a cluster-based approach grounded in a bibliographic coupling analysis, revealing complex network associations within each cluster. A cluster analysis highlights time trends and topic networking and provides specific cluster-based authors and research outlets that provide guidance for academics and practitioners alike on specific strands of the literature. Furthermore, the use of more broad keywords in our search enables the possible contribution of more borderline studies on cryptocurrency investment. In addition, our study delivers a qualitative analysis, revealing the main conclusions and future research venues by cluster.

A study with these significant contributions is of the utmost importance for researchers, investors, regulators, and academics in general. Our findings provide researchers with valuable information for their future studies on cryptocurrency investment. In addition, it provides insights for regulators to effectively regulate cryptocurrencies.

2. Data and Methodology

Similar to the extant literature, we sampled the Web of Science Core Collection database (WoS) (Jiang et al. 2021; Liang et al. 2016; Milian et al. 2019; Yue et al. 2021).

As the initial landmark in cryptocurrency literature was published in 2008 by Satoshi Nakamoto, we decided to take the year 2009 as the starting date of our search. Thus, we searched for academic journals between 1 January 2009 and 11 April 2021.

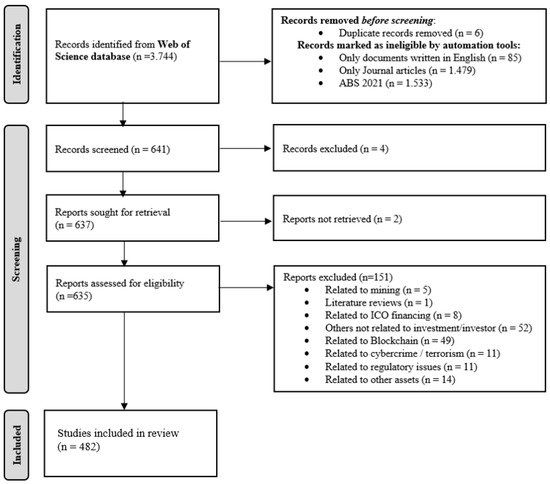

In order to perform the search, we selected the keywords “cryptocurrenc*”, “Bitcoin”, “Portfolio diversification”, “invest*”, and “Alternative investment”. The initial search results returned 3.744 articles. However, we only considered articles that addressed our research objective, that is, the articles needed to address the subject of cryptocurrency as an investment, providing any knowledge that might be of interest from the investment/investor perspective. Additionally, as a quality criterion, we decided to only select journal articles written in English and that belonged to the Academic Journal Guide ABS (Association of Business Schools) list of 2021, regardless of their field of knowledge. With the use of the ABS journal list as a quality criterion, we ensured that the studies included in the review had undergone a rigorous peer review process and were published in reputable journals. This process led to a final sample of 482 articles. Furthermore, the use of more broad keywords in our search enabled the possible contribution of more borderline studies on cryptocurrency investment. In Figure 1, we present our flow of information in addition to the different phases of our systematic review process, which was based on PRISMA (Page et al. 2021). We only used the WoS database since due to the use of the ABS journal guide list as a quality criterion, the articles provided by the Scopus database overlapped too significantly with WoS to be considered in this research.

Figure 1.

Flow of information through the different phases of our systematic review process (PRISMA).

In our analysis we used VOSviewer 1.6.17 (Bartolacci et al. 2020; Ding et al. 2014; Galvao et al. 2019; Rialti et al. 2019; Sadeghi Moghadam et al. 2021; van Eck and Waltman 2017) as a bibliometric tool and adopted bibliographic coupling in order to aggregate the selected articles (Bartolacci et al. 2020; van Eck and Waltman 2017). A bibliographic coupling analysis determines the relatedness of items based on the number of references they share (Bartolacci et al. 2020; Ding et al. 2014; Galvao et al. 2019; Rialti et al. 2019; Sadeghi Moghadam et al. 2021; van Eck and Waltman 2017). Unlike other bibliometric analysis on the literature on cryptocurrency (Aysan et al. 2021; Bariviera and Merediz-Solà 2021; García-Corral et al. 2022; Jalal et al. 2021; Liang et al. 2016; Merediz-Solá and Bariviera 2019), we used a bibliographic coupling analysis, highlighting its powerful and accurate analysis based on the number of references since those do not change over time as the number of citations does (Bartolacci et al. 2020; Ding et al. 2014; Galvao et al. 2019; Rialti et al. 2019; Sadeghi Moghadam et al. 2021; van Eck and Waltman 2017).

In addition, and in order to mitigate the bias against newer articles that might have fewer citations compared to older ones, we adopted the normalized citation option (Bartolacci et al. 2020; Caputo et al. 2019). In this option, the normalized citations are calculated as the total citations of an article divided by the average of the citations of all the articles that were published in the same year from the data collected (Bartolacci et al. 2020; van Eck and Waltman 2017).

3. Results

As a result of the VOSviwer bibliographic coupling, four clusters were obtained. Therefore, we decided to conduct our bibliometric analysis evidencing the differences between the resulting literature clusters. Namely, cluster 1 (red) included 166 articles that mostly investigated investor behavior, news effects, and investor sentiment. Cluster 2 (green) included 146 articles, particularly those that investigated portfolio diversification, hedge, and safe-haven properties. Cluster 3 (blue) included 138 articles that mainly explored the microstructure and efficiency of the cryptocurrency market. Finally, cluster 4 (yellow) included 32 articles encompassing several issues related to volatility and risk management in cryptocurrency investments.

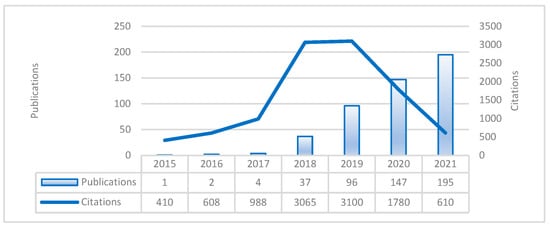

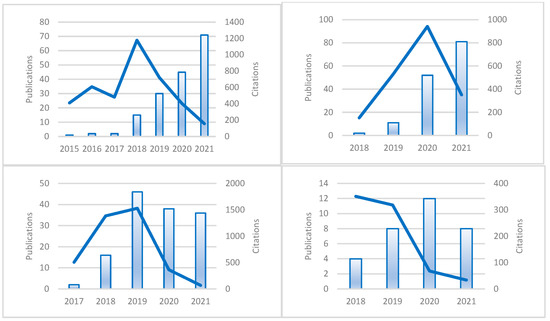

Recent years show a growing interest in this field (Figure 2 and Figure 3), from 1 article published in 2015 to 195 articles in November 2021. The year 2021 delivered 81 and 71 articles in clusters 2 and 1, respectively, and was the most productive year in our dataset. In clusters 3 and 4, the largest contributions were made in 2019 (46) and 2020 (12). These results highlight the growing interest of academia and the novelty of the research field scrutinized herein.

Figure 2.

Dataset citations and publications over time.

Figure 3.

Citations/publications over time: cluster 1 (upper left), cluster 2 (upper right), cluster 3 (lower left), cluster 4 (lower right).

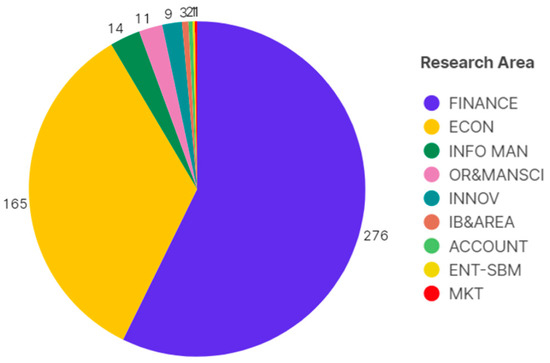

Figure 4 presents the most contributive areas of knowledge to this literature strand. As expected, finance and economics are the most relevant, with 276 and 165 publications, respectively.

Figure 4.

Most contributive research areas.

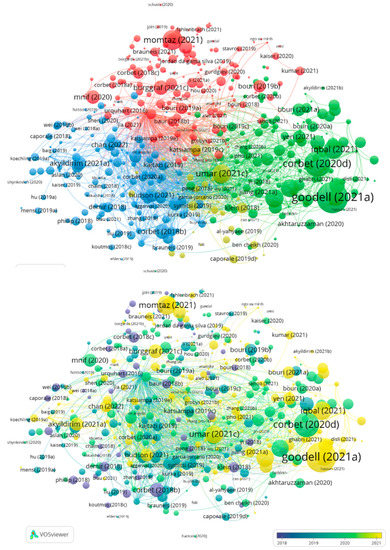

3.1. Cluster Network Analysis

Figure 5 shows that cluster 1 (red), cluster 2 (green), and cluster 3 (blue) express greater numbers of publications and citations. Cluster 4 (yellow) appears to be emerging from the other three clusters. However, until now, 2020 was the year that this cluster received more contributions, pointing toward a deceleration of publications in this theme, which may suggest that researchers and journals are now paying more attention to portfolio diversification, hedge, and safe-haven properties, investor behavior, news effects, and investor-sentiment-related themes. In addition, Figure 5 evidences that there are articles addressing thematics from more than one cluster, revealing that the boundaries between clusters are blurred. This is easily justified by the fact that the literature on cryptocurrency is still young; thus, many references are interconnected.

Figure 5.

Cluster network visualization (up) overlay visualization by year (down).

3.2. Cluster’s Top Articles

Table 1 highlights the top 10 most-cited articles in each cluster. Therefore, we can point out that the most-cited article in cluster 1 was Urquhart (2016), the most-cited article in cluster 2 was Corbet et al. (2020), the most-cited article in cluster 3 was Corbet et al. (2018a), and, finally, he most-cited article in cluster 4 was Klein et al. (2018).

Table 1.

Top ten most-cited articles by cluster.

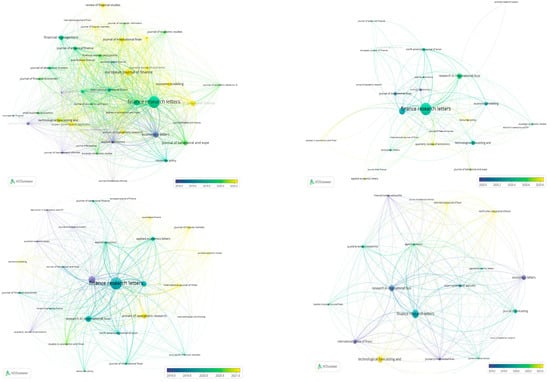

3.3. Journal Cluster Network Analysis

The average citations by a journal were 220, the mode was 16, and the median was 38, with a maximum of 3258 citations from Finance Research Letters with 109 publications and a minimum of 0 from Electronic Markets with 1 publication. In the dataset, The Journal of Monetary Economics presents the highest ratio of citations per publication, with 1 publication and 178 citations.

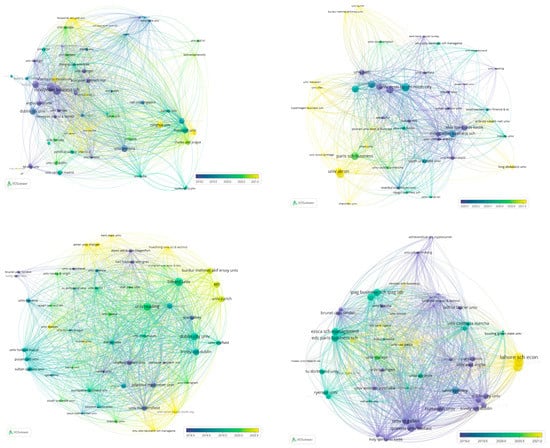

In Table A1 and Figure 6, we show that The Finance Research Letters, Economics Letters, and The International Review of Financial Analysis are the journals with more citations. In addition, the journal Finance Research Letters is present in all clusters and is the most-cited journal in clusters 1 and 2. The journal Economics Letters is the second most-cited journal in our dataset, and this fact remains in cluster 1. In cluster 3, Economics Letters is the most-cited journal. Therefore, it is evidenced that the journal Finance Research Letters contributed more to investor behavior, news effects, investor sentiment, portfolio diversification, hedge, and safe-haven properties. The journal Economics Letters contributed more on cryptocurrency market microstructure and efficiency. Finally, the journal The International Review of Financial Analysis contributed more to volatility and risk management in cryptocurrencies. In addition, Figure 6 shows that of the four clusters, cluster 1 presents the highest structured journal network. It is also shown that the journal with more recent citations in cluster 1 is The European Journal of Finance, in cluster 2 it is Resources Policy, in cluster 3 it is The Annals of Operation Research, and finally, in cluster 4, it is Technological Forecasting and Social Change.

Figure 6.

Cluster networks of the most-cited journals by year: cluster 1 (upper left), cluster 2 (upper right), cluster 3 (lower left), cluster 4 (lower right).

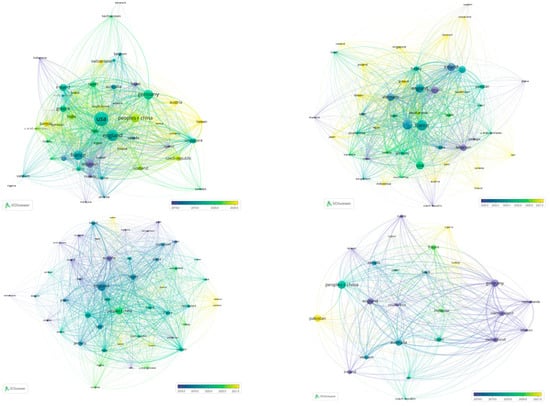

3.4. Country Cluster Network Analysis

Table A1 show the corresponding authors’ countries, evidencing that England is by far the country that produced the most articles, with 101 publications and 4218 citations. The average number of citations per country was 302, the mode was 0, and the median was 79. Additionally, Table A1 and Figure 7 and Figure 8 show evidence that England contributed more to investor behavior, news effects, investor sentiment, and cryptocurrency market microstructure and efficiency. Conversely, China contributed more to portfolio diversification, hedge, and safe-haven properties. Germany contributed more to volatility and risk management in cryptocurrencies. In addition, Figure 8 highlights the highly structured country networks in all clusters. It also shows that the country with more recent citations in cluster 1 is Tunisia; in cluster 2, it is Greece, in cluster 3, it is Lebanon, and in cluster 4, it is Pakistan.

Figure 7.

Publications by country world map.

Figure 8.

Cluster networks of the most-cited countries by year: cluster 1 (upper left), cluster 2 (upper right), cluster 3 (lower left), and cluster 4 (lower right).

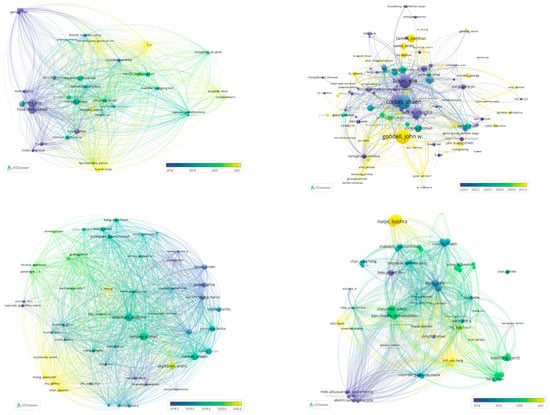

3.5. Author Cluster Network Analysis

Table A1 and Figure 9 present the most-cited authors, evidencing Shaen Corbet, Elie Bouri, David Roubaud, and Brian Lucey as the four most-cited authors in the dataset, with more than 1000 citations each. However, Eng-Tuck Cheah appears in the ninth position with a citation per publication ratio of 286, with only 2 published articles with a total of 572 citations. The average citations per author was 33, the mode was 0, and the median was 6.

Figure 9.

Cluster networks of the most-cited authors by year: cluster 1 (upper left), cluster 2 (upper right), cluster 3 (lower left), and cluster 4 (lower right).

This analysis highlights that Elie Bouri is the most published and cited in investor behavior, news effects, and investor sentiment, portfolio diversification, hedge, and safe-haven properties. Regarding cryptocurrency market microstructure and efficiency, Paraskevi Katsiampa is the most-cited author; however, the most published author was Andrew Urquhart (rank 5). Tony Klein and Thomas Walther share the rank of the most-cited and productive author in volatility and risk management in cryptocurrencies. In addition, Figure 9 emphasizes a highly structured author network in all clusters. It also shows that the author with more recent citations in cluster 1 is Panos Fousekis; in cluster 2, it is John Goodell, in cluster 3, it is Stephen Chan, and in cluster 4, it is Bushra Naqvi.

3.6. Institution Cluster Network Analysis

Table A1 and Figure 10 present the institutions that contributed the most to our research field. With 22 publications, Dublin City University is one of the institutions in the dataset that has contributed the most. It is also the institution for which the published articles have more citations (1198), which we can relate to our previous analysis, which revealed the most-cited author to be Shaen Corbet, who is solely responsible for Dublin City University’s rank in our dataset. In addition, in the top three ranked positions are Trinity Coll Dublin (1188) and Montpellier Business School (1166). The average number of citations per institution was 44, the mode was 0, and the median was 8.

Figure 10.

Cluster networks of the most-cited institutions by year: cluster 1 (upper left), cluster 2 (upper right), cluster 3 (lower left), and cluster 4 (lower right).

Montpellier Business School was the most-cited institution (747) that contributed to investor behavior, news effects, and investor sentiment; Trinity College Dublin was the most-cited institution (386) in portfolio diversification, hedge, and safe-haven properties, Sheffield Hallam University was the most-cited institution (507) in cryptocurrency market microstructure and efficiency; and Queens University Belfast was the most-cited institution (226) in volatility and risk management in cryptocurrencies. Figure 10 also reveals highly structured institution networks in all clusters. It shows that the institution with more recent citations in cluster 1 is Tsinghua University; in cluster 2, it is Akron University, in cluster 3, it is the Ho Chi Minh City University of Economy, and in cluster 4, it is the Lahore School of Economy.

3.7. Identification of Trend Topics

3.7.1. Cluster Keyword Co-Occurrence Analysis

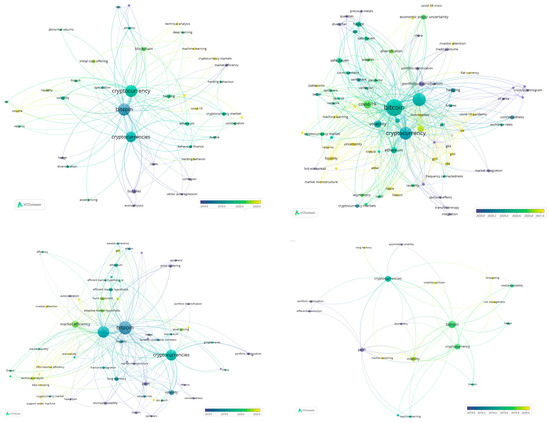

Figure 11 shows the relationship between keywords based on the number of articles in which they occur together. The top three keywords in all clusters are Bitcoin, cryptocurrency, and cryptocurrencies, which is in line with the findings of Jiang et al. (2021) and Jalal et al. (2021). The most recent co-occurrence of keywords in cluster 1 reveals that research is implementing machine learning and technical analysis and is highly concerned with the impact of COVID-19; in cluster 2, research is more concerned with uncertainty, liquidity, and with the COVID-19 impact; in cluster 3, there is the implementation of more support vector machine techniques and a focus on informational efficiency as well as investor attention; in cluster 4, the focus is on analyzing risk management, volatility spillovers, and the implementation of Markov regime switching models.

Figure 11.

Keywords network: cluster 1 (upper left), cluster 2 (upper right), cluster 3 (lower left), and cluster 4 (lower right).

3.7.2. Research Stream Analysis

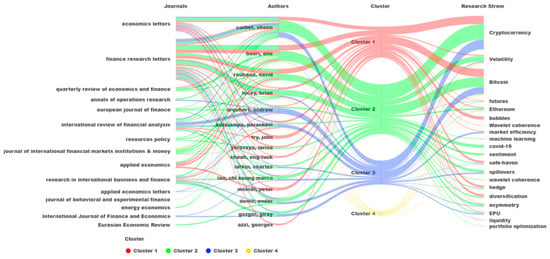

Following Jalal et al. (2021), we identified research streams in the literature. However, instead of using a co-citation analysis, as Alon et al. (2018) and Shonhe (2020), in which the relatedness of the items is determined based on the number of times they are cited together and therefore may change over time very easily, we adopted a bibliographic coupling analysis in which the relatedness of the items is determined based on the number of references they share, which do not change over time (Bartolacci et al. 2020; van Eck and Waltman 2017). We based our research stream on papers from the top 15 authors, resulting in a sample of 90 papers. In Figure 12, we show the relationship of the top 15 authors in our dataset with the most-cited journals, their contributions to the research stream, and consequently, to each cluster. Figure 12 reveals that out of the top 15 authors’ papers, cluster 2 seems to receive the highest flow, followed by cluster 1, cluster 3, and cluster 4. Cluster 1 and cluster 2 contribute to most of the research streams. On the other hand, Cluster 3 seems to contribute more to cryptocurrency, Bitcoin, market efficiency, spillovers, and asymmetry, and Cluster 4 contributes more to volatility, Bitcoin Ethereum, and spillovers. The main research stream are cryptocurrency, Bitcoin, and volatility, as found by Almeida and Gonçalves (2022).

Figure 12.

Journal–Author–Cluster–Research stream analysis.

3.8. Clusters’ Main Contributions to the Literature

3.8.1. Main Conclusions

In cluster 1, we identified that the main conclusions regarding investor behavior in the cryptocurrency markets are that: (1) the crypto market is dominated by irrational investors (Kaiser and Stöckl 2020); (2) news and media attention seem to influence the demand for Bitcoin, suggesting that investors’ beliefs can help in understanding the cryptocurrencies’ behavior (Flori 2019); (3) there is high level of herding behavior that can lead to market inefficiency (Raimundo Júnior et al. 2020; Bouri et al. 2019b); (4) risk-seeking behavior drives crypto investors (Pelster et al. 2019).

In cluster 2, the main conclusions concerning portfolio diversification, hedge, and safe-haven properties in cryptocurrency investments are: (1) cryptocurrencies’ ability to hedge against stocks, fiat currencies, geopolitical risks, and economic policy uncertainty (EPU) is time-varying (Mensi et al. 2020); (2) uncertainty is a determinant for cryptocurrency returns (Colon et al. 2021); (3) stablecoins have the ability to act as safe havens and diversifiers (Wang et al. 2020); (4) investors should consider gold, the European carbon market, CBOE Bitcoin futures, and crude oil to hedge against cryptocurrency market uncertainty (Huynh et al. 2020).

In cluster 3, we found the main conclusions about the cryptocurrency market structure to be that: (1) the level of inefficiency varies with time, thus supporting the adaptive market hypothesis (AMH) (Mensi et al. 2019); (2) when trade volume and market capitalization increase, liquidity uncertainty will tend to decrease (Koutmos 2018); (3) there is a connectedness with traditional assets (Kurka 2019); (4) cryptocurrencies’ returns and liquidity seem to have impact on the size effect (Li et al. 2020).

Finally, in cluster 4, regarding volatility and risk management on cryptocurrency investment, the main conclusions are: (1) cryptocurrencies’ new accepting venues can predict a cryptocurrency’s volatility (Sabah 2020); (2) Bitcoin’s price volatility presents an “anti-leverage effect” (Tan et al. 2020); (3) there are bidirectional volatility spillovers in the crypto market (Katsiampa et al. 2019b); (4) cryptocurrencies present diversification benefits on intraweek and monthly scales (Omane-Adjepong and Alagidede 2019).

3.8.2. Main Futures Lines of Research

As far as future lines of research, in investor behavior in the cryptocurrency markets, (cluster 1) we found: (1) the need to further investigate the disposition effect among cryptocurrency investors (Gemayel and Preda 2021); (2) the need to analyze the impact of monetary and governmental policies on cryptocurrency investors (Mnif et al. 2020); (3) the need to further investigate herding behavior in the crypto market (Papadamou et al. 2021); (4) the need to include variables such as perceived knowledge, emotional intelligence, profitability, anonymity, risk aversion, and convenience (Gupta et al. 2020).

Regarding portfolio diversification, hedge, and safe-haven properties in cryptocurrency investments, we found: (1) the need to further investigate the relationships between cryptocurrencies and other assets classes such as equities, bonds, currencies, and commodities (Bouri et al. 2021; Hsu et al. 2021); (2) the need to evaluate the change in efficient frontiers in a three-dimensional space (mean–variance–skewness) (Kwon 2020); (3) the use of more powerful deep learning algorithms and machine learning approaches (Huynh 2021); (4) the need to further investigate cryptocurrency futures and options (Qiao et al. 2020).

For cryptocurrency market structure, we found: (1) the need to explore market heterogeneity in the cryptocurrency market (Sapkota and Grobys 2021); (2) the need to use the generalized autoregressive score (GAS) framework (Matkovskyy 2019); (3) the need to investigate the time-varying market efficiency of the cryptocurrency markets (Charfeddine and Maouchi 2019); (4) the need to investigate how investor/borrower characteristics affect interest rates in bitcoin lending and defaults (Zhang et al. 2021).

Finally, for volatility and risk management in cryptocurrency investment, we found: (1) that GARCH models’ great variety should be further explored from the staking ensemble perspective (Aras 2021); (2) the need to further use the heterogeneous autoregressive regression (HAR) model (Hattori 2020); (3) the need to analyze if cryptocurrency-realized volatility or its trading volume drive the long-term volatility (Walther et al. 2019); (4) the need to understand cryptocurrencies’ returns and the magnitude of their volatility spillovers (Omane-Adjepong and Alagidede 2019).

4. Conclusions

Our study adds to the current literature a cluster bibliometric analysis which examines the literature’s contributions to cryptocurrency investment since its inception. We searched the WoS database and focused only on journals listed on the 2021 ABS list. We obtained a final sample of 482 articles. Empirical results show evidence of a growing interest in this field over the past few years. From our analysis, four literature clusters emerged, namely, investigating investor behavior; portfolio diversification; cryptocurrency market microstructure; and risk management in cryptocurrency investment. The most contributing institutions are located in Europe and China, as in the findings of Jiang et al. (2021), Yue et al. (2021), García-Corral et al. (2022), Almeida and Gonçalves (2022, 2023a, 2023b); however, the conclusions are different from the conclusions made Alsmadi et al. (2022). Finance Research Letters is the most-cited and productive journal, as in and Almeida and Gonçalves (2023b); however, this is different from the conclusions made by Almeida and Gonçalves (2022).

Our study, unlike previous studies (Aysan et al. 2021; Bariviera and Merediz-Solà 2021; García-Corral et al. 2022; Jalal et al. 2021; Liang et al. 2016; Merediz-Solá and Bariviera 2019) adds to the bibliometric analysis on the cryptocurrency literature, an insightful cluster-based systematic analysis, revealing complex network associations within each cluster. Additionally, it delivers a qualitative analysis revealing: (1) The main conclusions by cluster, in which we highlight the evidence of herding behavior in the cryptocurrency market that can lead to market inefficiency, the time-varying ability of cryptocurrencies to act as hedgers against stocks, fiat currencies, geopolitical risks, and economic policy uncertainty (EPU), the time-varying inefficiency of the cryptocurrency market, and the evidence of bidirectional volatility spillovers in the crypto market; (2) The future research venues by cluster in which we highlight the need to further investigate the disposition effect among cryptocurrency investors, to further investigate cryptocurrency futures and options, to investigate the time-varying market efficiency of the cryptocurrency markets, and to understand cryptocurrencies’ returns and the magnitude of their volatility spillovers. Our results are in line with other cryptocurrency literature reviews (Almeida and Gonçalves 2022, 2023a, 2023b; Ballis and Verousis 2022; Hairudin et al. 2020; Haq et al. 2021).

A study with these contributions is of the utmost importance for researchers, investors, regulators, and academics in general. Our findings provide researchers with cluster-based information and structured networking for research outlets and literature strands, with time-trended information relevant for future studies on cryptocurrency investment. In addition, it provides insights for regulators to effectively regulate cryptocurrencies.

The use of only one database (WoS) could be considered a limitation of the research. However, due to the use of the ABS journal guide list as a quality criterion, the marginal articles provided by the Scopus database were not significant. Future research should evolve and implement more machine learning analyses, improve investor sentiment research, and explore how the crypto market can become greener. Future studies should also analyze the relationship between decentralized cryptocurrencies and Central Bank Digital Currencies (CBDC) (Alonso et al. 2020), consider the effect of exchange failures on cryptocurrencies (Briola et al. 2023), and consider the environmental impact of the cryptocurrency market (J. Li et al. 2019; Náñez Alonso et al. 2021). Future research may also consider our analysis with the use of other databases, such as Scopus, as well as a systematic literature review on the research field scrutinized herein.

Author Contributions

Conceptualization, J.A.; methodology, J.A. and T.C.G.; software, J.A.; validation, J.A. and T.C.G.; formal analysis, J.A.; investigation, J.A.; resources, J.A. and T.C.G.; data curation, J.A.; writing—original draft preparation, J.A.; writing—review and editing, J.A. and T.C.G.; visualization, J.A. and T.C.G.; supervision, T.C.G.; project administration, J.A. and T.C.G. All authors have read and agreed to the published version of the manuscript.

Funding

The authors acknowledge financial support from the Fundação para a Ciência e a Tecnologia (grant UI/BD/151446/2021 and grant UID/SOC/04521/2020, respectively).

Data Availability Statement

The data to conduct our review were sourced from Clarivate Web of Science.

Conflicts of Interest

The authors declare that there are no conflicts of interest regarding the publication of this paper.

Appendix A

Table A1.

Dataset and cluster top five journals, articles, countries, and institutions.

Table A1.

Dataset and cluster top five journals, articles, countries, and institutions.

| Dataset | Ct | Pb | Ct/Pb | Cluster 1 | Ct | Pb | Ct/Pb | Cluster 2 | Ct | Pb | Ct/Pb | Cluster 3 | Ct | Pb | Ct/Pb | Cluster 4 | Ct | Pb | Ct/Pb | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Journals | ||||||||||||||||||||

| 1 | Finance research letters | 3258 | 109 | 29.9 | Finance research letters | 1185 | 21 | 56.4 | Finance research letters | 716 | 34 | 21.1 | Economics letters | 1651 | 21 | 78.6 | International review of financial analysis | 192 | 1 | 192.0 |

| 2 | Economics letters | 2921 | 41 | 71.2 | Economics letters | 1125 | 12 | 93.8 | International review of financial analysis | 345 | 16 | 21.6 | Finance research letters | 1222 | 48 | 25.5 | Research in international business and finance | 145 | 4 | 36.3 |

| 3 | International review of financial analysis | 994 | 30 | 33.1 | Applied economics | 247 | 5 | 49.4 | Research in international business and finance | 178 | 17 | 10.5 | Research in international business and finance | 303 | 9 | 33.7 | Finance research letters | 135 | 6 | 22.5 |

| 4 | Research in international business and finance | 750 | 42 | 17.9 | International review of financial analysis | 205 | 6 | 34.2 | Energy economics | 100 | 2 | 50.0 | International review of financial analysis | 252 | 7 | 36.0 | Economics letters | 92 | 2 | 46.0 |

| 5 | Applied economics | 344 | 18 | 19.1 | Journal of monetary economics | 178 | 1 | 178.0 | Journal of international financial markets institutions & money | 93 | 6 | 15.5 | North American journal of economics and finance | 75 | 5 | 15.0 | Expert systems with applications | 76 | 2 | 38.0 |

| Countries | ||||||||||||||||||||

| 1 | England | 4218 | 101 | 41.8 | England | 1503 | 36 | 41.8 | Peoples R. China | 686 | 35 | 19.6 | England | 1920 | 35 | 54.9 | Germany | 318 | 4 | 79.5 |

| 2 | France | 1474 | 46 | 32.0 | France | 801 | 12 | 66.8 | England | 614 | 27 | 22.7 | Turkey | 554 | 14 | 39.6 | North Ireland | 226 | 2 | 113.0 |

| 3 | Ireland | 1361 | 32 | 42.5 | Lebanon | 754 | 6 | 125.7 | France | 567 | 23 | 24.7 | Ireland | 450 | 7 | 64.3 | Switzerland | 226 | 2 | 113.0 |

| 4 | Australia | 1271 | 35 | 36.3 | USA | 662 | 27 | 24.5 | Ireland | 505 | 16 | 32.6 | Australia | 448 | 11 | 40.7 | Australia | 190 | 6 | 31.7 |

| 5 | Lebanon | 1192 | 19 | 62.7 | Norway | 487 | 4 | 121.8 | Vietnam | 415 | 18 | 23.1 | Spain | 305 | 11 | 27.7 | England | 181 | 3 | 60.3 |

| Authors | ||||||||||||||||||||

| 1 | Corbet, Shaen | 1198 | 22 | 54.5 | Bouri, Elie | 747 | 5 | 149.4 | Bouri, Elie | 404 | 11 | 36.7 | Katsiampa, Paraskevi | 522 | 5 | 104.4 | Klein, Tony | 226 | 2 | 113.0 |

| 2 | Bouri, Elie | 1185 | 18 | 65.8 | Roubaud, David | 747 | 5 | 149.4 | Roubaud, David | 389 | 9 | 43.2 | Corbet, Shaen | 450 | 6 | 75.0 | Walther, Thomas | 226 | 2 | 112.0 |

| 3 | Roubaud, David | 1136 | 14 | 81.1 | Fry, John | 632 | 3 | 210.7 | Corbet, Shaen | 379 | 11 | 34.5 | Lucey, Brian | 420 | 4 | 105.0 | Hien Pham Thu | 192 | 1 | 192.0 |

| 4 | Lucey, Brian | 1121 | 13 | 86.2 | Cheah, Eng-Tuck | 572 | 2 | 286.0 | Lucey, Brian | 346 | 6 | 57.7 | Yarovaya, Larisa | 385 | 3 | 128.3 | Baur, Dirk G. | 81 | 2 | 40.5 |

| 5 | Urquhart, Andrew | 873 | 13 | 67.2 | Molnar, Peter | 481 | 2 | 240.5 | Lau, Chi Keung Marco | 206 | 6 | 34.3 | Urquhart, Andrew | 381 | 8 | 47.6 | Dimpfl, Thomas | 81 | 1 | 81.0 |

| Institutions | ||||||||||||||||||||

| 1 | Dublin City Univ. | 1198 | 22 | 54.5 | Montpellier Business School | 747 | 5 | 149.40 | Trinity College Dublin | 386 | 9 | 42.89 | Sheffield Hallam Univ. | 507 | 4 | 126.75 | Queens Univ. Belfast | 226 | 2 | 113.00 |

| 2 | Trinity College Dublin | 1188 | 18 | 66.0 | Univ. Sheffield | 454 | 3 | 151.33 | Dublin City Univ. | 379 | 11 | 34.45 | Dublin City Univ. | 450 | 6 | 75.00 | Technical Univ.of Dresden | 226 | 2 | 113.00 |

| 3 | Montpellier Business School | 1166 | 20 | 58.3 | Univ. Southampton | 446 | 3 | 148.67 | Montpellier Business School | 372 | 12 | 31.00 | Trinity College Dublin | 420 | 4 | 105.00 | Univ. St Gallen | 226 | 2 | 113.00 |

| 4 | Holy Spirit Univ. | 774 | 13 | 59.4 | Holy Spirit Univ. | 377 | 4 | 94.25 | Holy Spirit Univ. | 363 | 8 | 45.38 | Anglia Ruskin Univ | 368 | 2 | 184.00 | Humboldt Univ. | 192 | 1 | 192.00 |

| 5 | Univ. Southampton | 737 | 13 | 56.7 | Norwegian Univ. Science Technology | 370 | 2 | 185.00 | Univ. Economics Ho Chi Minh City | 361 | 15 | 24.07 | Univ. Huddersfield | 323 | 5 | 64.60 | Univ. Sydney | 108 | 3 | 36.00 |

Ct—citation; Pb—publications; Ct/Pb—citations per publications ratio.

References

- Almeida, José. 2021. Cryptocurrencies and financial markets–extant literature and future venues. European Journal of Economics, Finance and Administrative Sciences 109: 29–40. [Google Scholar]

- Almeida, José, and Tiago Cruz Gonçalves. 2022. A Systematic Literature Review of Volatility and Risk Management on Cryptocurrency Investment: A Methodological Point of View. Risks 10: 107. [Google Scholar] [CrossRef]

- Almeida, José, and Tiago Cruz Gonçalves. 2023a. A systematic literature review of investor behavior in the cryptocurrency markets. Journal of Behavioral and Experimental Finance 37: 100785. [Google Scholar] [CrossRef]

- Almeida, José, and Tiago Cruz Gonçalves. 2023b. Portfolio Diversification, Hedge and Safe-Haven Properties in Cryptocurrency Investments and Financial Economics: A Systematic Literature Review. Journal of Risk and Financial Management 16: 3. [Google Scholar] [CrossRef]

- Alon, Ilan, John Anderson, Ziaul Haque Munim, and Alice Ho. 2018. A Review of the Internationalization of Chinese Enterprises. Asia Pacific Journal of Management 35: 573–605. [Google Scholar] [CrossRef]

- Alonso, Sergio Luis Náñez, Miguel Ángel Echarte Fernández, David Sanz Bas, and Jarosław Kaczmarek. 2020. Reasons fostering or discouraging the implementation of central bank-backed digital currency: A review. Economies 8: 41. [Google Scholar] [CrossRef]

- Alsmadi, Ayman Abdalmajeed, Najed Alrawashdeh, Ala’a Fouad Al-Dweik, and Mohammed Al-Assaf. 2022. Cryptocurrencies: A bibliometric analysis. International Journal of Data and Network Science 6: 619–28. [Google Scholar] [CrossRef]

- Angerer, Martin, Christian Hugo Hoffmann, Florian Neitzert, and Sascha Kraus. 2020. Objective and subjective risks of investing into cryptocurrencies. Finance Research Letters 40: 101737. [Google Scholar] [CrossRef]

- Aras, Serkan. 2021. Stacking hybrid GARCH models for forecasting Bitcoin volatility. Expert Systems with Applications 174: 114747. [Google Scholar] [CrossRef]

- Aysan, Ahmet Faruk, Hüseyin Bedir Demirtaş, and Mustafa Saraç. 2021. The Ascent of Bitcoin: Bibliometric Analysis of Bitcoin Research. Journal of Risk and Financial Management 14: 427. [Google Scholar] [CrossRef]

- Ballis, Antonis, and Thanos Verousis. 2022. Behavioural finance and cryptocurrencies. Review of Behavioral Finance 14: 545–62. [Google Scholar] [CrossRef]

- Bariviera, Aurelio F., and Ignasi Merediz-Solà. 2021. Where Do We Stand in Cryptocurrencies Economic Research? A Survey Based on Hybrid Analysis. Journal of Economic Surveys 35: 377–407. [Google Scholar] [CrossRef]

- Bartolacci, Francesca, Andrea Caputo, and Michela Soverchia. 2020. Sustainability and financial performance of small and medium sized enterprises: A bibliometric and systematic literature review. Business Strategy and the Environment 29: 1297–309. [Google Scholar] [CrossRef]

- Baur, Dirk G., and Thomas Dimpfl. 2018. Asymmetric volatility in cryptocurrencies. Economics Letters 173: 148–51. [Google Scholar] [CrossRef]

- Baur, Dirk G., Thomas Dimpfl, and Konstantin Kuck. 2018. Bitcoin, gold and the US dollar—A replication and extension. Finance Research Letters 25: 103–10. [Google Scholar] [CrossRef]

- Białkowski, Jędrzej. 2020. Cryptocurrencies in institutional investors’ portfolios: Evidence from industry stop-loss rules. Economics Letters 191: 108834. [Google Scholar] [CrossRef]

- Blau, Benjamin M. 2017. Price dynamics and speculative trading in bitcoin. Research in International Business and Finance 41: 493–99. [Google Scholar] [CrossRef]

- Bouri, Elie, Chi Keung Marco Lau, Brian Lucey, and David Roubaud. 2019a. Trading volume and the predictability of return and volatility in the cryptocurrency market. Finance Research Letters 29: 340–46. [Google Scholar] [CrossRef]

- Bouri, Elie, David Gabauer, Rangan Gupta, and Aviral Kumar Tiwari. 2021. Volatility connectedness of major cryptocurrencies: The role of investor happiness. Journal of Behavioral and Experimental Finance 30: 100463. [Google Scholar] [CrossRef]

- Bouri, Elie, Naji Jalkh, Peter Molnár, and David Roubaud. 2017a. Bitcoin for energy commodities before and after the December 2013 crash: Diversifier, hedge or safe haven? Applied Economics 49: 5063–73. [Google Scholar] [CrossRef]

- Bouri, Elie, Peter Molnár, Georges Azzi, David Roubaud, and Lars Ivar Hagfors. 2017b. On the hedge and safe haven properties of Bitcoin: Is it really more than a diversifier? Finance Research Letters 20: 192–98. [Google Scholar] [CrossRef]

- Bouri, Elie, Rangan Gupta, and David Roubaud. 2019b. Herding behaviour in cryptocurrencies. Finance Research Letters 29: 216–21. [Google Scholar] [CrossRef]

- Bouri, Elie, Syed Jawad Hussain Shahzad, and David Roubaud. 2019c. Co-explosivity in the cryptocurrency market. Finance Research Letters 29: 178–83. [Google Scholar] [CrossRef]

- Brauneis, Alexander, and Roland Mestel. 2018. Price discovery of cryptocurrencies: Bitcoin and beyond. Economics Letters 165: 58–61. [Google Scholar] [CrossRef]

- Briola, Antonio, David Vidal-Tomás, Yuanrong Wang, and Tomaso Aste. 2023. Anatomy of a Stablecoin’s failure: The Terra-Luna case. Finance Research Letters 51: 103358. [Google Scholar] [CrossRef]

- Caporale, Guglielmo Maria, and Timur Zekokh. 2019. Modelling volatility of cryptocurrencies using Markov-Switching GARCH models. Research in International Business and Finance 48: 143–55. [Google Scholar] [CrossRef]

- Caputo, Andrea, Giacomo Marzi, Jane Maley, and Mario Silic. 2019. Ten years of conflict management research 2007–2017: An update on themes, concepts and relationships. International Journal of Conflict Management 30: 87–110. [Google Scholar] [CrossRef]

- Chan, Wing Hong, Minh Le, and Yan Wendy Wu. 2019. Holding Bitcoin longer: The dynamic hedging abilities of Bitcoin. Quarterly Review of Economics and Finance 71: 107–13. [Google Scholar] [CrossRef]

- Charfeddine, Lanouar, and Youcef Maouchi. 2019. Are shocks on the returns and volatility of cryptocurrencies really persistent? Finance Research Letters 28: 423–30. [Google Scholar] [CrossRef]

- Cheah, Eng Tuck, and John Fry. 2015. Speculative bubbles in Bitcoin markets? An empirical investigation into the fundamental value of Bitcoin. Economics Letters 130: 32–36. [Google Scholar] [CrossRef]

- Colon, Francisco, Chaehyun Kim, Hana Kim, and Wonjoon Kim. 2020. Are cryptocurrencies a safe haven for equity markets? An international perspective from the COVID-19 pandemic. Research in International Business and Finance 54: 101248. [Google Scholar] [CrossRef] [PubMed]

- Colon, Francisco, Chaehyun Kim, Hana Kim, and Wonjoon Kim. 2021. The effect of political and economic uncertainty on the cryptocurrency market. Finance Research Letters 39: 101621. [Google Scholar] [CrossRef]

- Corbet, Shaen, Andrew Meegan, Charles Larkin, Brian Lucey, and Larisa Yarovaya. 2018a. Exploring the dynamic relationships between cryptocurrencies and other financial assets. Economics Letters 165: 28–34. [Google Scholar] [CrossRef]

- Corbet, Shaen, Brian Lucey, and Larisa Yarovaya. 2018b. Datestamping the Bitcoin and Ethereum bubbles. Finance Research Letters 26: 81–88. [Google Scholar] [CrossRef]

- Corbet, Shaen, Brian Lucey, Andrew Urquhart, and Larisa Yarovaya. 2019. Cryptocurrencies as a financial asset: A systematic analysis. International Review of Financial Analysis 62: 182–99. [Google Scholar] [CrossRef]

- Corbet, Shaen, Charles Larkin, and Brian Lucey. 2020. The contagion effects of the COVID-19 pandemic: Evidence from gold and cryptocurrencies. Finance Research Letters 35: 101554. [Google Scholar] [CrossRef]

- Demir, Ender, Giray Gozgor, Chi Keung Marco Lau, and Samuel A. Vigne. 2018. Does economic policy uncertainty predict the Bitcoin returns? An empirical investigation. Finance Research Letters 26: 145–49. [Google Scholar] [CrossRef]

- Ding, Ying, Ronald Rousseau, and Dietmar Wolfram. 2014. Measuring Scholarly Impact. Berlin/Heidelberg: Springer. [Google Scholar] [CrossRef]

- Fang, Fan, Waichung Chung, Carmine Ventre, Michail Basios, Leslie Kanthan, Lingbo Li, and Fan Wu. 2021. Ascertaining price formation in cryptocurrency markets with machine learning. European Journal of Finance, 1–23. [Google Scholar] [CrossRef]

- Flori, Andrea. 2019. News and subjective beliefs: A Bayesian approach to Bitcoin investments. Research in International Business and Finance 50: 336–56. [Google Scholar] [CrossRef]

- Fry, John, and Eng Tuck Cheah. 2016. Negative bubbles and shocks in cryptocurrency markets. International Review of Financial Analysis 47: 343–52. [Google Scholar] [CrossRef]

- Galvao, A., C. Mascarenhas, C. Marques, J. Ferreira, and V. Ratten. 2019. Triple helix and its evolution: A systematic literature review. Journal of Science and Technology Policy Management 10: 812–33. [Google Scholar] [CrossRef]

- Galvao, Anderson, Carla Mascarenhas, Carla Marques, João Ferreira, and Vanessa Ratten. 2018. Price manipulation in the Bitcoin ecosystem. Journal of Monetary Economics 95: 86–96. [Google Scholar] [CrossRef]

- García-Corral, Francisco Javier, José Antonio Cordero-García, Jaime de Pablo-Valenciano, and Juan Uribe-Toril. 2022. A bibliometric review of cryptocurrencies: How have they grown? Financial Innovation 8: 1–31. [Google Scholar] [CrossRef] [PubMed]

- Gemayel, Roland, and Alex Preda. 2021. Performance and learning in an ambiguous environment: A study of cryptocurrency traders. International Review of Financial Analysis 77: 101847. [Google Scholar] [CrossRef]

- Gkillas, Konstantinos, and Paraskevi Katsiampa. 2018. An application of extreme value theory to cryptocurrencies. Economics Letters 164: 109–11. [Google Scholar] [CrossRef]

- Goodell, John W., and Stephane Goutte. 2021. Co-movement of COVID-19 and Bitcoin: Evidence from wavelet coherence analysis. Finance Research Letters 38: 101625. [Google Scholar] [CrossRef]

- Gupta, Swati, Sanjay Gupta, Manoj Mathew, and Hanumantha Rao Sama. 2020. Prioritizing intentions behind investment in cryptocurrency: A fuzzy analytical framework. Journal of Economic Studies 48: 1442–59. [Google Scholar] [CrossRef]

- Hairudin, Aiman, Imtiaz Mohammad Sifat, Azhar Mohamad, and Yusniliyana Yusof. 2020. Cryptocurrencies: A survey on acceptance, governance and market dynamics. International Journal of Finance and Economics 27: 4633–59. [Google Scholar] [CrossRef]

- Haq, Inzamam Ul, Apichit Maneengam, Supat Chupradit, Wanich Suksatan, and Chunhui Huo. 2021. Economic policy uncertainty and cryptocurrency market as a risk management avenue: A systematic review. Risks 9: 163. [Google Scholar] [CrossRef]

- Hattori, Takahiro. 2020. A forecast comparison of volatility models using realized volatility: Evidence from the Bitcoin market. Applied Economics Letters 27: 591–95. [Google Scholar] [CrossRef]

- Hsu, Shu Han, Chwen Sheu, and Jiho Yoon. 2021. Risk spillovers between cryptocurrencies and traditional currencies and gold under different global economic conditions. North American Journal of Economics and Finance 57: 101443. [Google Scholar] [CrossRef]

- Huynh, Toan Luu Duc, Erik Hille, and Muhammad Ali Nasir. 2020. Diversification in the age of the 4th industrial revolution: The role of artificial intelligence, green bonds and cryptocurrencies. Technological Forecasting and Social Change 159: 120188. [Google Scholar] [CrossRef]

- Huynh, Toan Luu Duc. 2021. Does Bitcoin React to Trump’s Tweets? Journal of Behavioral and Experimental Finance 31: 100546. [Google Scholar] [CrossRef]

- Jalal, Raja Nabeel Ud Din, Ilan Alon, and Andrea Paltrinieri. 2021. A bibliometric review of cryptocurrencies as a financial asset. Technology Analysis and Strategic Management, 1–16. [Google Scholar] [CrossRef]

- Ji, Qiang, Elie Bouri, Chi Keung Marco Lau, and David Roubaud. 2019a. Dynamic connectedness and integration in cryptocurrency markets. International Review of Financial Analysis 63: 257–72. [Google Scholar] [CrossRef]

- Ji, Qiang, Elie Bouri, David Roubaud, and Ladislav Kristoufek. 2019b. Information interdependence among energy, cryptocurrency and major commodity markets. Energy Economics 81: 1042–55. [Google Scholar] [CrossRef]

- Jiang, Shangrong, Xuerong Li, and Shouyang Wang. 2021. Exploring evolution trends in cryptocurrency study: From underlying technology to economic applications. Finance Research Letters 38: 101532. [Google Scholar] [CrossRef]

- Kaiser, Lars, and Sebastian Stöckl. 2020. Cryptocurrencies: Herding and the transfer currency. Finance Research Letters 33. [Google Scholar] [CrossRef]

- Katsiampa, Paraskevi. 2017. Volatility estimation for Bitcoin: A comparison of GARCH models. Economics Letters 158: 3–6. [Google Scholar] [CrossRef]

- Katsiampa, Paraskevi, Shaen Corbet, and Brian Lucey. 2019a. High frequency volatility co-movements in cryptocurrency markets. Journal of International Financial Markets, Institutions and Money 62: 35–52. [Google Scholar] [CrossRef]

- Katsiampa, Paraskevi, Shaen Corbet, and Brian Lucey. 2019b. Volatility spillover effects in leading cryptocurrencies: A BEKK-MGARCH analysis. Finance Research Letters 29: 68–74. [Google Scholar] [CrossRef]

- Klein, Tony, Hien Pham Thu, and Thomas Walther. 2018. Bitcoin is not the New Gold—A comparison of volatility, correlation, and portfolio performance. International Review of Financial Analysis 59: 105–16. [Google Scholar] [CrossRef]

- Koutmos, Dimitrios. 2018. Liquidity uncertainty and Bitcoin’s market microstructure. Economics Letters 172: 97–101. [Google Scholar] [CrossRef]

- Kurka, Josef. 2019. Do cryptocurrencies and traditional asset classes influence each other? Finance Research Letters 31: 38–46. [Google Scholar] [CrossRef]

- Kwon, Ji Ho. 2020. Tail behavior of Bitcoin, the dollar, gold and the stock market index. Journal of International Financial Markets, Institutions and Money 67: 101202. [Google Scholar] [CrossRef]

- Li, Jingming, Nianping Li, Jinqing Peng, Haijiao Cui, and Zhibin Wu. 2019. Energy consumption of cryptocurrency mining: A study of electricity consumption in mining cryptocurrencies. Energy 168: 160–68. [Google Scholar] [CrossRef]

- Li, Rong, Sufang Li, Di Yuan, and Huiming Zhu. 2021. Investor attention and cryptocurrency: Evidence from wavelet-based quantile Granger causality analysis. Research in International Business and Finance 56: 101389. [Google Scholar] [CrossRef]

- Li, Yi, Zhang Wei, Xiong Xiong, and Wang Pengfei. 2020. Does size matter in the cryptocurrency market? Applied Economics Letters 27: 1141–49. [Google Scholar] [CrossRef]

- Liang, Xiaobei, Yibo Yang, and Jiani Wang. 2016. Internet finance: A systematic literature review and bibliometric analysis. Paper Presented at International Conference on Electronic Business (ICEB), Xiamen, China, December 4–8; pp. 386–98. [Google Scholar]

- Matkovskyy, Roman. 2019. Centralized and decentralized bitcoin markets: Euro vs. USD vs. GBP. Quarterly Review of Economics and Finance 71: 270–79. [Google Scholar] [CrossRef]

- Mensi, Walid, Mobeen Ur Rehman, Debasish Maitra, Khamis Hamed Al-Yahyaee, and Ahmet Sensoy. 2020. Does bitcoin co-move and share risk with Sukuk and world and regional Islamic stock markets? Evidence using a time-frequency approach. Research in International Business and Finance 53: 101230. [Google Scholar] [CrossRef]

- Mensi, Walid, Yun Jung Lee, Khamis Hamed Al-Yahyaee, Ahmet Sensoy, and Seong Min Yoon. 2019. Intraday downward/upward multifractality and long memory in Bitcoin and Ethereum markets: An asymmetric multifractal detrended fluctuation analysis. Finance Research Letters 31: 19–25. [Google Scholar] [CrossRef]

- Merediz-Solá, Ignasi, and Aurelio F. Bariviera. 2019. A bibliometric analysis of bitcoin scientific production. Research in International Business and Finance 50: 294–305. [Google Scholar] [CrossRef]

- Milian, Eduardo Z., Mauro de M. Spinola, and Marly M. de Carvalho. 2019. Fintechs: A literature review and research agenda. Electronic Commerce Research and Applications 34: 100833. [Google Scholar] [CrossRef]

- Mnif, Emna, Anis Jarboui, and Khaireddine Mouakhar. 2020. How the cryptocurrency market has performed during COVID 19? A multifractal analysis. Finance Research Letters 36: 101647. [Google Scholar] [CrossRef] [PubMed]

- Nakamoto, Satoshi. 2008. Bitcoin: A Peer-to-Peer Electronic Cash System. Available online: https://bitcoin.org/en/bitcoin-paper (accessed on 10 February 2021).

- Náñez Alonso, Sergio Luis, Javier Jorge-vázquez, Miguel Ángel Echarte Fernández, and Ricardo Francisco Reier Forradellas. 2021. Cryptocurrency mining from an economic and environmental perspective. Analysis of the most and least sustainable countries. Energies 14: 4254. [Google Scholar] [CrossRef]

- Omane-Adjepong, Maurice, and Imhotep Paul Alagidede. 2019. Multiresolution analysis and spillovers of major cryptocurrency markets. Research in International Business and Finance 49: 191–206. [Google Scholar] [CrossRef]

- Page, Matthew J., Joanne E. McKenzie, Patrick M. Bossuyt, Isabelle Boutron, Tammy C. Hoffmann, Cynthia D. Mulrow, Larissa Shamseer, Jennifer M. Tetzlaff, Elie A. Akl, Sue E. Brennan, and et al. 2021. The PRISMA 2020 statement: An updated guideline for reporting systematic reviews. Systematic Reviews 10: 89. [Google Scholar] [CrossRef]

- Papadamou, Stephanos, Nikolaos A. Kyriazis, Panayiotis Tzeremes, and Shaen Corbet. 2021. Herding behaviour and price convergence clubs in cryptocurrencies during bull and bear markets. Journal of Behavioral and Experimental Finance 30: 100469. [Google Scholar] [CrossRef]

- Pelster, Matthias, Bastian Breitmayer, and Tim Hasso. 2019. Are cryptocurrency traders pioneers or just risk-seekers? Evidence from brokerage accounts. Economics Letters 182: 98–100. [Google Scholar] [CrossRef]

- Peng, Yaohao, Pedro Henrique Melo Albuquerque, Jader Martins Camboim de Sá, Ana Julia Akaishi Padula, and Mariana Rosa Montenegro. 2018. The best of two worlds: Forecasting high frequency volatility for cryptocurrencies and traditional currencies with Support Vector Regression. Expert Systems with Applications 97: 177–92. [Google Scholar] [CrossRef]

- Phillip, Andrew, Jennifer Chan, and Shelton Peiris. 2018. A new look at Cryptocurrencies. Economics Letters 163: 6–9. [Google Scholar] [CrossRef]

- Phillip, Andrew, Jennifer Chan, and Shelton Peiris. 2019. On long memory effects in the volatility measure of Cryptocurrencies. Finance Research Letters 28: 95–100. [Google Scholar] [CrossRef]

- Qiao, Xingzhi, Huiming Zhu, and Liya Hau. 2020. Time-frequency co-movement of cryptocurrency return and volatility: Evidence from wavelet coherence analysis. International Review of Financial Analysis 71: 101541. [Google Scholar] [CrossRef]

- Raimundo, Júnior, Gerson de Souza, Rafael Baptista Palazzi, Ricardo de Souza Tavares, and Marcelo Cabus Klotzle. 2020. Market Stress and Herding: A New Approach to the Cryptocurrency Market. Journal of Behavioral Finance, 43–57. [Google Scholar] [CrossRef]

- Rialti, Riccardo, Giacomo Marzi, Cristiano Ciappei, and Donatella Busso. 2019. Big data and dynamic capabilities: A bibliometric analysis and systematic literature review. Management Decision 57: 2052–68. [Google Scholar] [CrossRef]

- Sabah, Nasim. 2020. Cryptocurrency accepting venues, investor attention, and volatility. Finance Research Letters 36: 101339. [Google Scholar] [CrossRef]

- Sadeghi Moghadam, Mohammad Reza, Hossein Safari, and Narjes Yousefi. 2021. Clustering quality management models and methods: Systematic literature review and text-mining analysis approach. Total Quality Management and Business Excellence 32: 241–64. [Google Scholar] [CrossRef]

- Sapkota, Niranjan, and Klaus Grobys. 2021. Asset market equilibria in cryptocurrency markets: Evidence from a study of privacy and non-privacy coins. Journal of International Financial Markets, Institutions and Money 74: 101402. [Google Scholar] [CrossRef]

- Sensoy, Ahmet. 2019. The inefficiency of Bitcoin revisited: A high-frequency analysis with alternative currencies. Finance Research Letters 28: 68–73. [Google Scholar] [CrossRef]

- Shonhe, Liah. 2020. Continuous Professional Development (CPD) of Librarians: A Bibliometric Analysis of Research Productivity Viewed Through WoS. Journal of Academic Librarianship 46: 102106. [Google Scholar] [CrossRef]

- Sun, Xiaolei, Mingxi Liu, and Zeqian Sima. 2020. A novel cryptocurrency price trend forecasting model based on LightGBM. Finance Research Letters 32: 101084. [Google Scholar] [CrossRef]

- Symitsi, Efthymia, and Konstantinos J. Chalvatzis. 2019. The economic value of Bitcoin: A portfolio analysis of currencies, gold, oil and stocks. Research in International Business and Finance 48: 97–110. [Google Scholar] [CrossRef]

- Tan, Shay Kee, Jennifer So Kuen Chan, and Kok Haur Ng. 2020. On the speculative nature of cryptocurrencies: A study on Garman and Klass volatility measure. Finance Research Letters 32: 101075. [Google Scholar] [CrossRef]

- Urquhart, Andrew. 2016. The inefficiency of Bitcoin. Economics Letters 148: 80–82. [Google Scholar] [CrossRef]

- Urquhart, Andrew. 2017. Price clustering in Bitcoin. Economics Letters 159: 145–48. [Google Scholar] [CrossRef]

- Urquhart, Andrew, and Hanxiong Zhang. 2019. Is Bitcoin a hedge or safe haven for currencies? An intraday analysis. International Review of Financial Analysis 63: 49–57. [Google Scholar] [CrossRef]

- van Eck, Nees Jan, and Ludo Waltman. 2017. Citation-based clustering of publications using CitNetExplorer and VOSviewer. Scientometrics 111: 1053–70. [Google Scholar] [CrossRef]

- Walther, Thomas, Tony Klein, and Elie Bouri. 2019. Exogenous drivers of Bitcoin and Cryptocurrency volatility—A mixed data sampling approach to forecasting. Journal of International Financial Markets, Institutions and Money 63: 101133. [Google Scholar] [CrossRef]

- Wang, Gang Jin, Chi Xie, Danyan Wen, and Longfeng Zhao. 2019. When Bitcoin meets economic policy uncertainty (EPU): Measuring risk spillover effect from EPU to Bitcoin. Finance Research Letters 31: 489–97. [Google Scholar] [CrossRef]

- Wang, Gang Jin, Xin yu Ma, and Hao yu Wu. 2020. Are stablecoins truly diversifiers, hedges, or safe havens against traditional cryptocurrencies as their name suggests? Research in International Business and Finance 54: 101225. [Google Scholar] [CrossRef]

- Wei, Wang Chun. 2018. Liquidity and market efficiency in cryptocurrencies. Economics Letters 168: 21–24. [Google Scholar] [CrossRef]

- Yi, Shuyue, Zishuang Xu, and Gang Jin Wang. 2018. Volatility connectedness in the cryptocurrency market: Is Bitcoin a dominant cryptocurrency? International Review of Financial Analysis 60: 98–114. [Google Scholar] [CrossRef]

- Yue, Yao, Xuerong Li, Dingxuan Zhang, and Shouyang Wang. 2021. How cryptocurrency affects economy? A network analysis using bibliometric methods. International Review of Financial Analysis 77: 101869. [Google Scholar] [CrossRef]

- Zhang, Shuai, Xinyu Hou, and Shusong Ba. 2021. What determines interest rates for bitcoin lending? Research in International Business and Finance 58: 101443. [Google Scholar] [CrossRef]

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).