The Effect of Financial Policies Implemented during COVID-19 on Bank Credit in the Central American Region

Abstract

1. Introduction

- (i)

- The effect of these policies can be more clearly identified, as its risk of mixing with the impact of other policies to support the economy is small due to the scarcity and very narrow scope of the latter. The IMF (2022) estimates that the fiscal response to the COVID-19 crisis, through additional spending and foregone revenue in some countries of Central America in a two year period, was less than 1.5% of GDP (Costa Rica (1.5%) and Nicaragua (1.3%)), and in others, between 2.5 and 3.5% of GDP (Guatemala (3.3%), Honduras (2.7%), El Salvador (2.6%), the Dominican Republic (3.3%), and Panama (3.4%)). This is in contrast to developed economies, where, for example, in the US, the figure was 25% of GDP; in Germany, 14%; Japan, 17%; and the United Kingdom, 16%.

- (ii)

- Their financial data are public, standardized (and thus, comparable), and robust in terms of frequency and length. They provide and disclose their data through the Central American Monetary Council (CMC),2 which gathers and organizes the data following the methodologies of the International Monetary Fund (IMF).

- (iii)

- They implemented a number of monetary and regulatory policies, which will be described in Section 3.

2. Literature Review

3. Exploration of Data

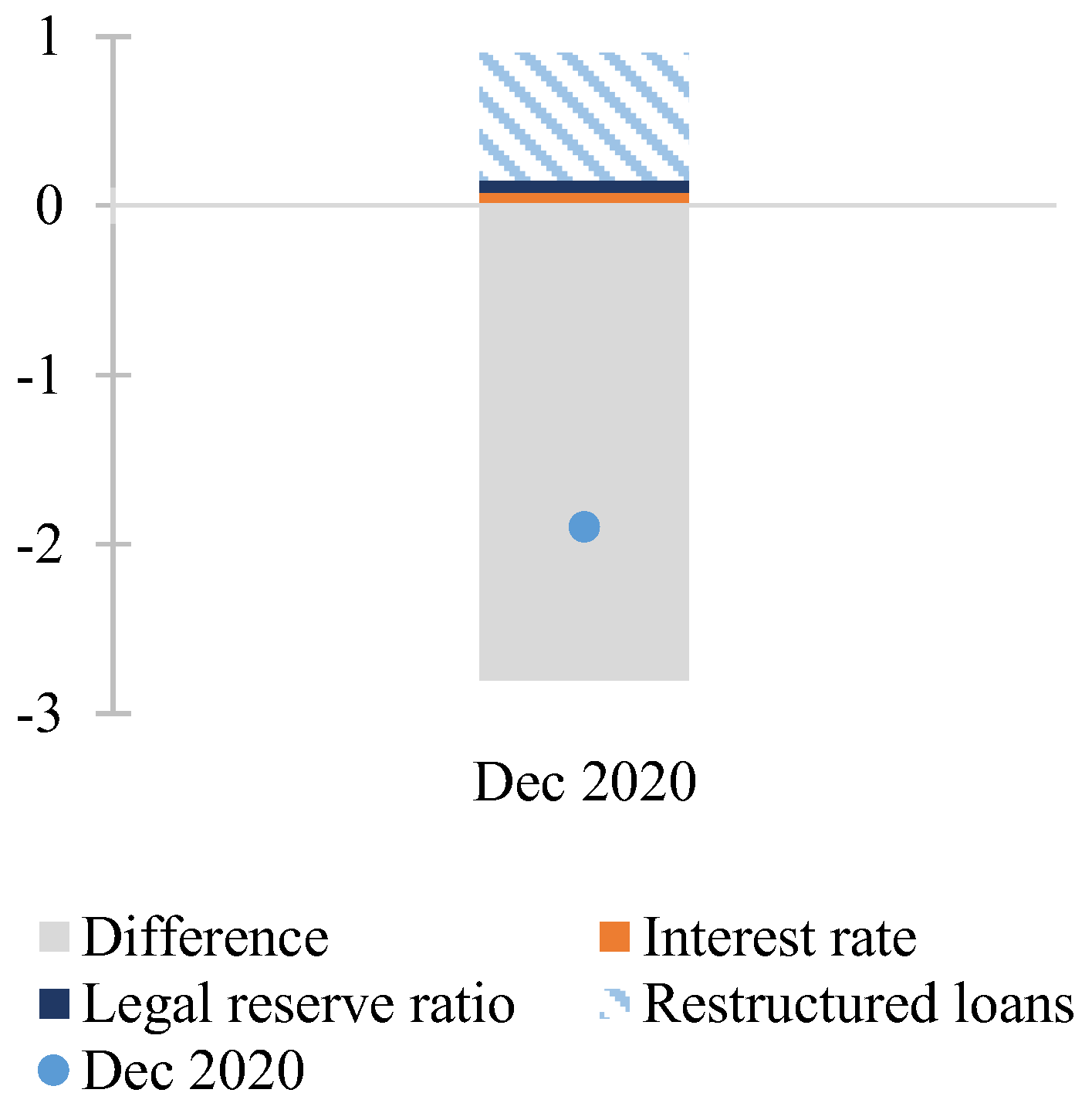

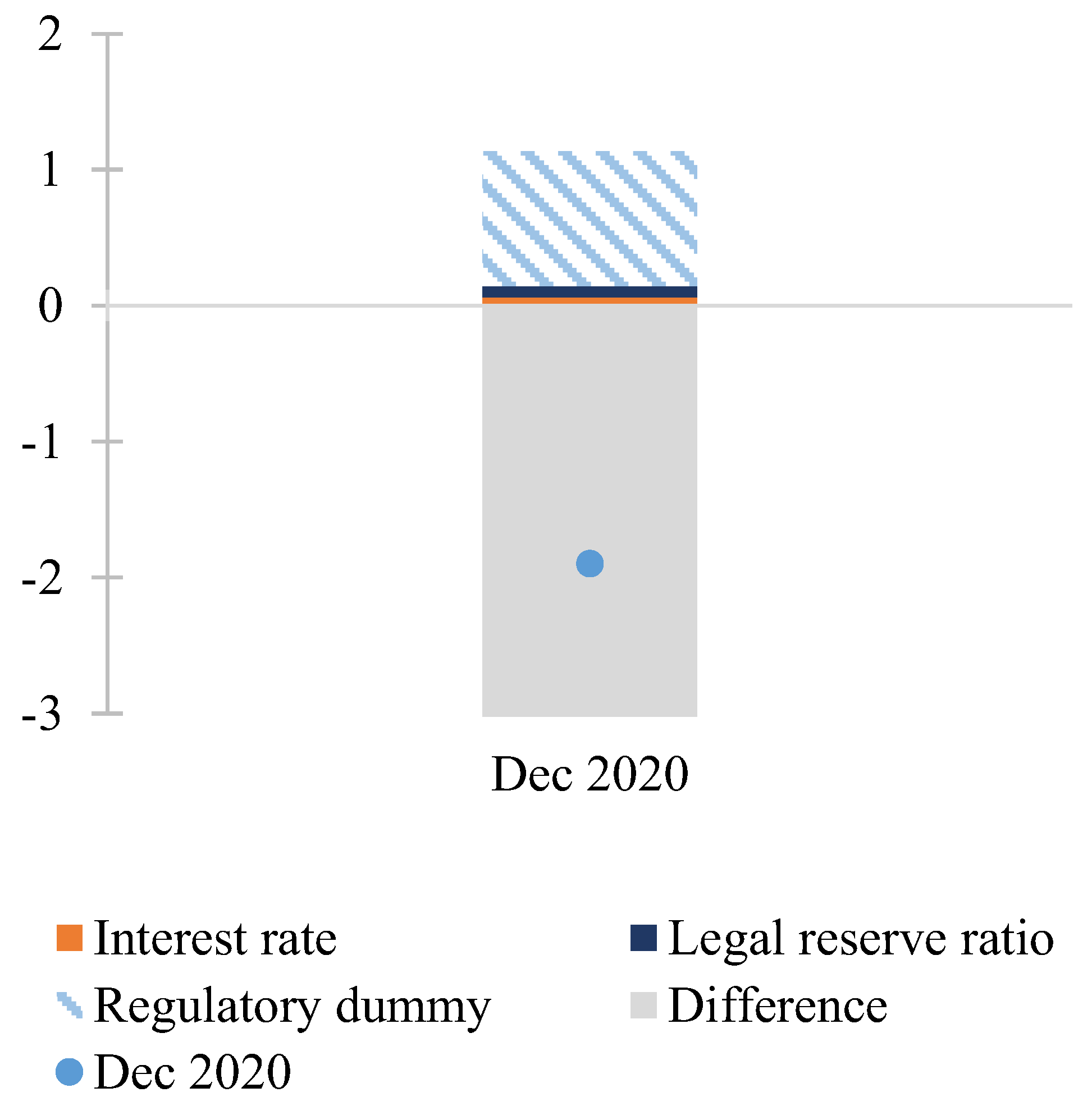

- (i)

- Monetary policy;

- (ii)

- Regulatory policy in support of the financial system;

- (iii)

- Lines of credit or guarantees through public sector institutions (especially public banks) for the private financial system.

- Monetary policy—neither El Salvador nor Panama applied any kind of monetary policies (as they are dollarized); Costa Rica, the Dominican Republic, Guatemala, and Honduras cut the monetary rate, reduced the legal reserve requirements, and provided liquidity facilities, while Nicaragua did not provide liquidity.

- Regulatory policies—neither the Dominican Republic nor Panama made changes in their regulatory policies. The remaining countries implemented several strategies, such as relaxing risk criteria and report requirements (Costa Rica, Honduras, and Nicaragua), and capital, liquidity, and provisions norms (Costa Rica, El Salvador, Guatemala, and Honduras). Guatemala allowed extensions to classify loans as uncollectible.

- Household and firm support—all the countries implemented a moratorium for payment of credit installments without affecting ratings.

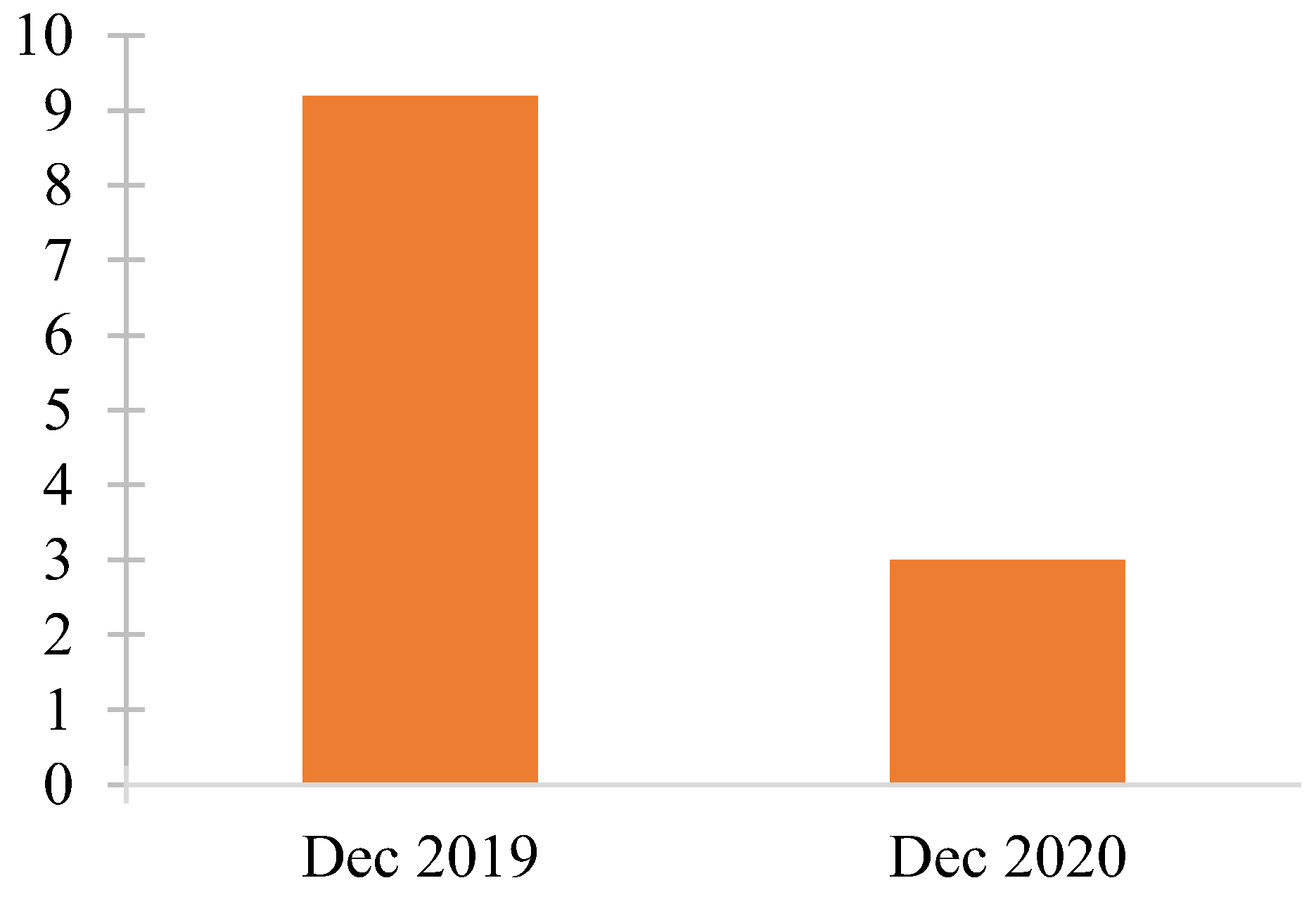

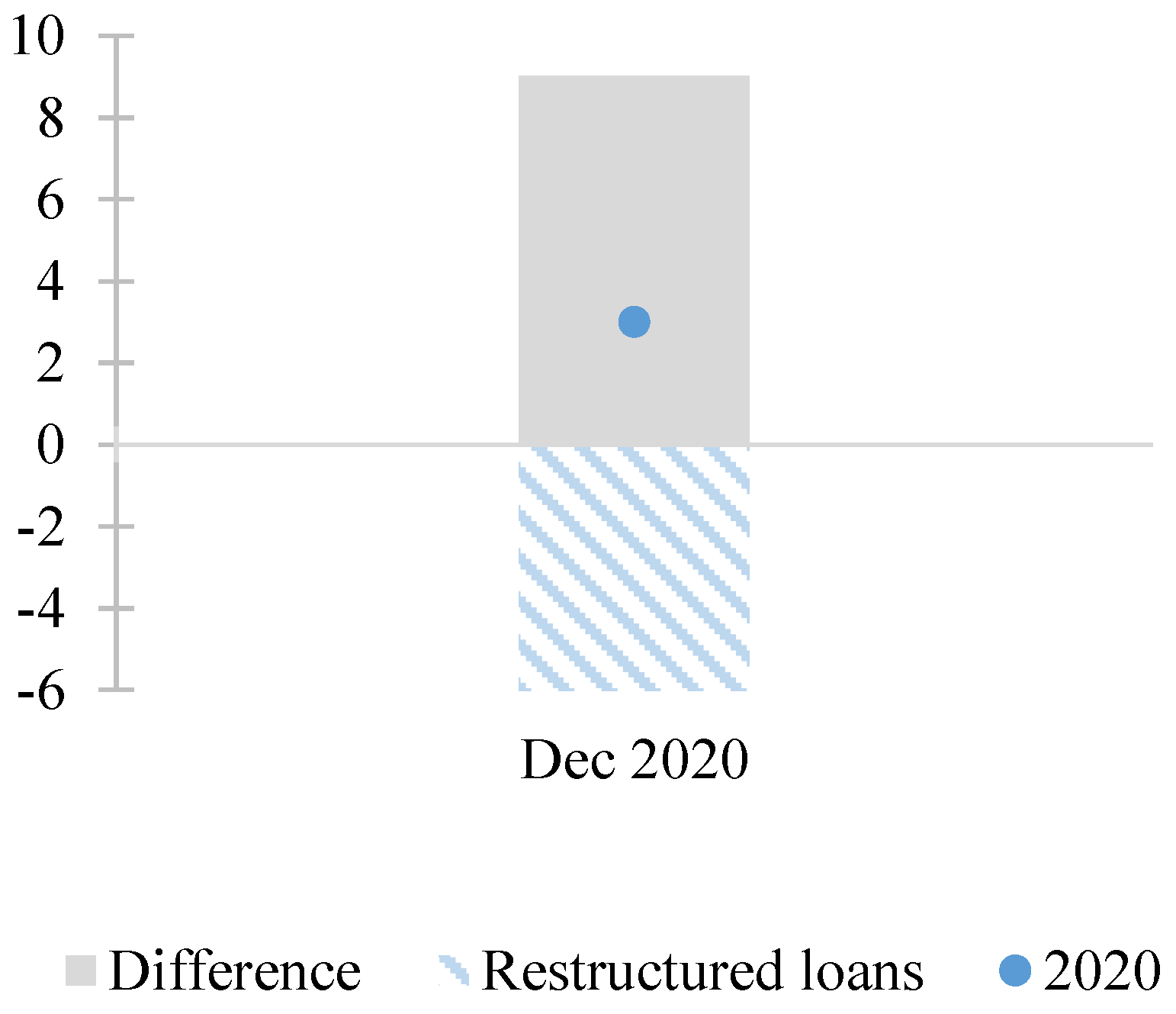

- El Salvador, Guatemala, Honduras, and Nicaragua provided credit lines to the private financial system.

4. Econometric Strategy

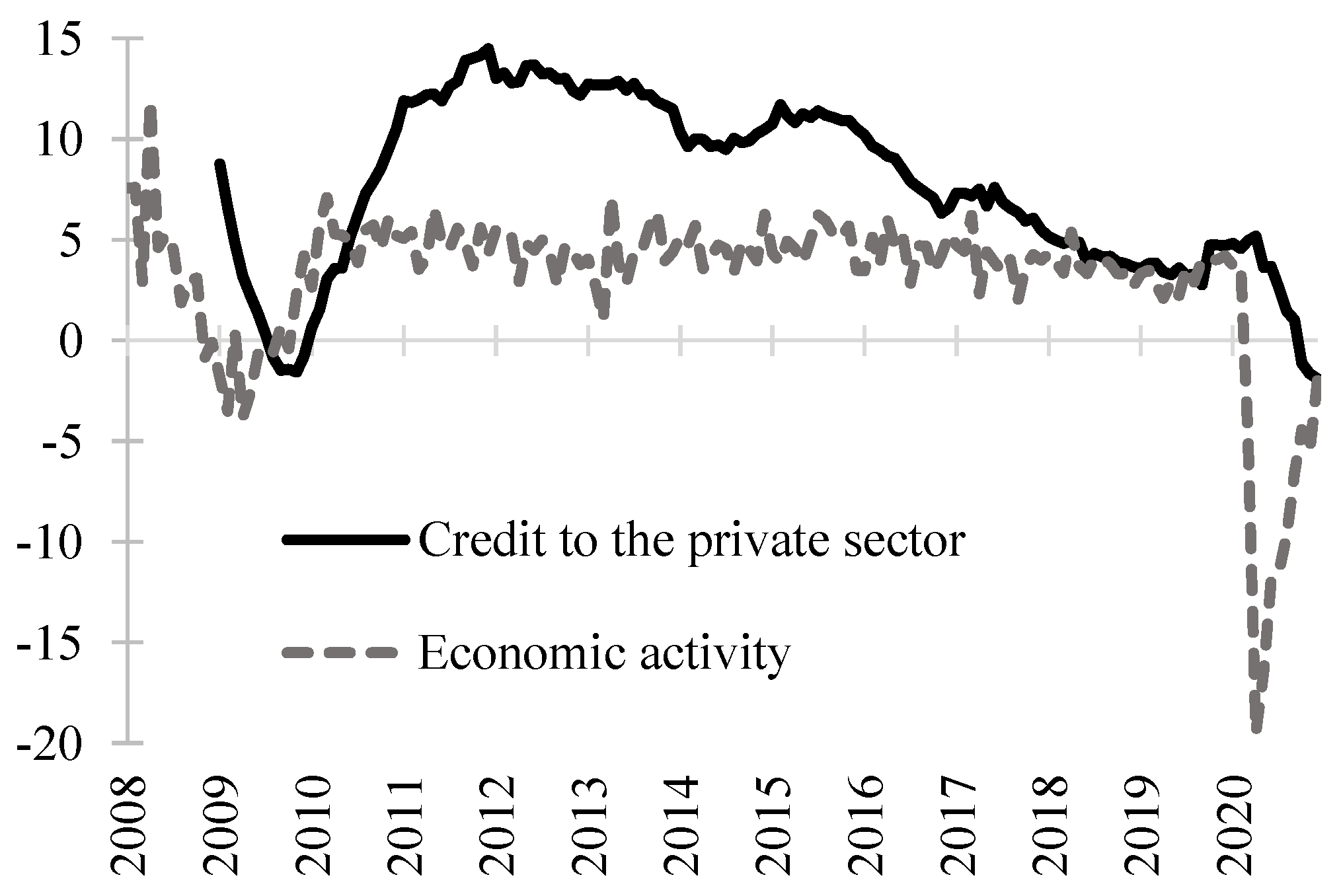

- The Private credit growth rate decreased substantially in El Salvador, Honduras, and Panama during the COVID-19 crisis, compared to before the crisis. The decrease was much smaller in the Dominican Republic, and negligible in Guatemala. Costa Rica experienced an increase in the growth rate, while Nicaragua improved its negative growth rate, but still remained negative (see Table 1).

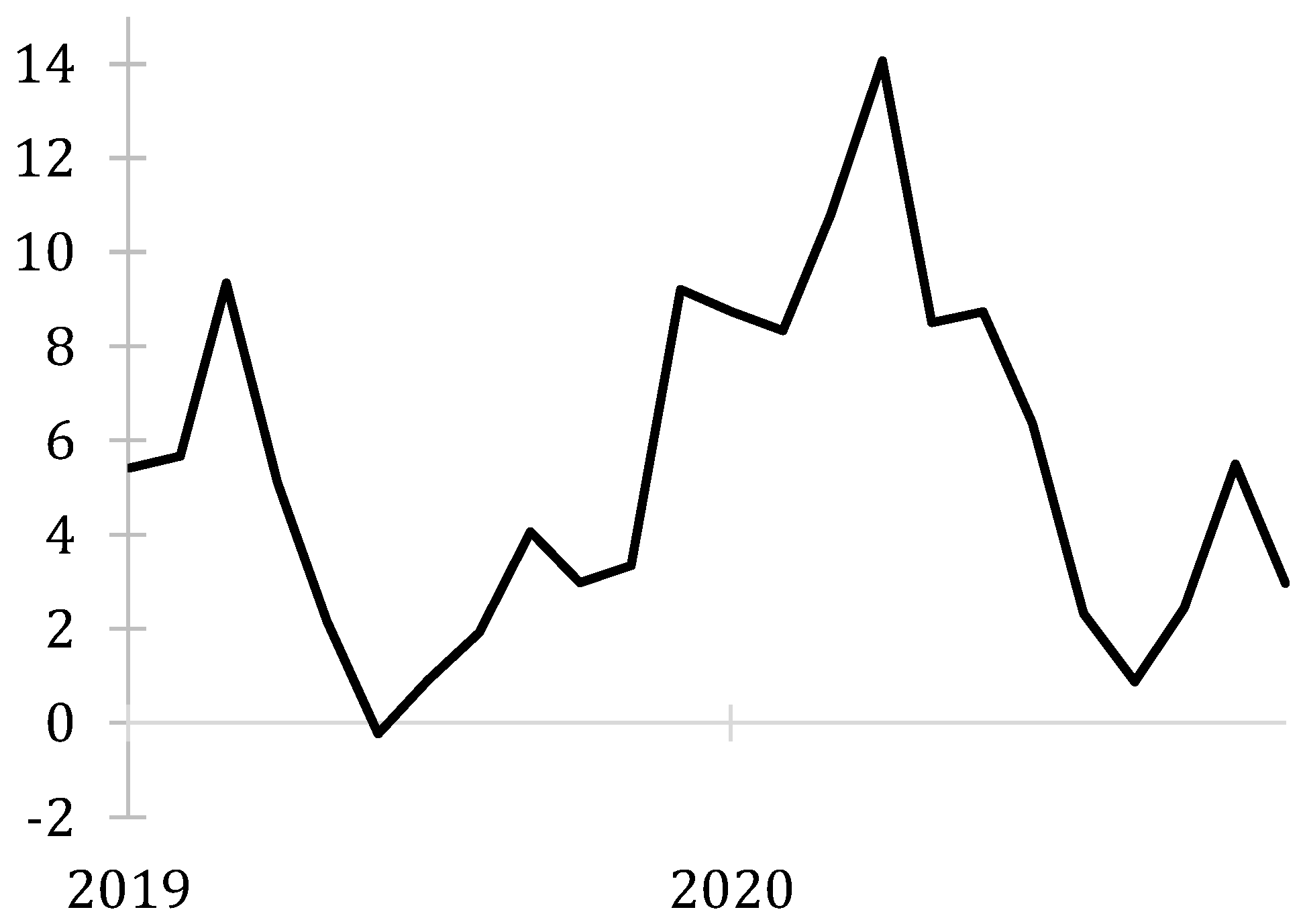

- The NPL growth rate was already negative in El Salvador before the crisis, and became even more negative during the crisis. It turned from positive to negative in Guatemala and Nicaragua; it increased significantly in Panama and the Dominican Republic. The NPL growth rate in Costa Rica was positive and slightly decreased (but still positive) during the crisis (see Table 1).

- The Economic activity indexes show the profound impact of the crisis on the region. Panama suffered the largest drop in production. Costa Rica, El Salvador, Honduras, the Dominican Republic, and Nicaragua also experienced sizeable decreases, but less than in the first case. Guatemala’s economic activity index was the least affected by the crisis (see Table 1 and Table 2).

- The delinquency rates increased slightly in Costa Rica, Honduras, Panama, and the Dominican Republic during the crisis. Only Nicaragua had a substantial increase in the delinquency rate index, whereas El Salvador and Guatemala improved (see Table 2).

4.1. Private Credit

4.2. Non-Performing Loans

5. Interpretation of the Results and Robustness Checks: Private Credit and Non-Performing Loans

6. Concluding Remarks

Supplementary Materials

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Variable | Private Credit | Non-Performing Loans |

|---|---|---|

| Lag | 3.81 | 1.45 |

| Constant | 4.33 | 4.54 |

| IMAE | 2.96 | 3.04 |

| CPI | 3.62 | 3.44 |

| Exchange rate | 1.55 | 1.38 |

| Legal reserve ratio | 1.1 | 1.21 |

| Interest rate | 1.3 | 1.29 |

| Number of banks | 1.09 | 1.07 |

| Restructured loans | 3.01 | 2.70 |

| COVID-19 cases | 1.99 | 1.52 |

| Mean VIF | 2.48 | 2.16 |

| Variable | Private Credit | Non-Performing Loans |

|---|---|---|

| Lag | 3.84 | 1.47 |

| Constant | 4.50 | 4.86 |

| IMAE | 3.00 | 3.09 |

| CPI | 3.62 | 3.44 |

| Exchange rate | 1.57 | 1.36 |

| Legal reserve ratio | 1.13 | 1.22 |

| Interest rate | 1.26 | 1.23 |

| Number of banks | 1.12 | 1.08 |

| Regulatory dummy | 2.99 | 2.73 |

| COVID-19 cases | 1.94 | 1.49 |

| Mean VIF | 2.50 | 2.20 |

| FE | FGLS | IV | AB | |

|---|---|---|---|---|

| (1) | (2) | (3) | (4) | |

| Lag (Credit) | 0.978 ** | 0.979 ** | 0.973 ** | 0.978 ** |

| (0.00722) | (0.00693) | (0.00718) | (0.00709) | |

| Y | 0.0943 ** | 0.0550 ** | 0.0874 ** | 0.0940 ** |

| (0.0148) | (0.0121) | (0.0146) | (0.0145) | |

| P | 0.0533 ** | 0.0222 | 0.0425 ** | 0.0547 ** |

| (0.0236) | (0.0175) | (0.0196) | (0.0231) | |

| E | 0.0239 | 0.00711 | 0.00598 | 0.0231 |

| (0.0167) | (0.0136) | (0.0136) | (0.0165) | |

| LR | −0.0204 ** | −0.0219 ** | −0.0194 ** | −0.0206 ** |

| (0.00358) | (0.00374) | (0.00358) | (0.00351) | |

| R | −0.0157 ** | −0.0105 ** | −0.0161 ** | −0.0156 ** |

| (0.00462) | (0.00427) | (0.00454) | (0.00456) | |

| Number of banks | 0.0189 ** | 0.0220 ** | 0.0164 ** | 0.0197 ** |

| (0.00863) | (0.00800) | (0.00811) | (0.00857) | |

| Regulatory dummy | 0.987 ** | 0.589 ** | 0.882 ** | 0.991 ** |

| (0.304) | (0.242) | (0.298) | (0.296) | |

| COVID-19 cases | −0.00861 ** | −0.0106 ** | −0.00807 ** | −0.00861 ** |

| (0.00379) | (0.00365) | (0.00372) | (0.00369) | |

| Constant | −0.425 ** | −0.118 * | −0.276 ** | −0.428 ** |

| (0.115) | (0.0665) | (0.0913) | (0.112) | |

| Observations | 833 | 833 | 828 | 827 |

| Pseudo R-squared | 0.974 | 0.973 | 0.974 | 0.974 |

| Test | Private Credit | Non-Performing Loans |

|---|---|---|

| Wooldridge autocorrelation test | 0.0472 | 0.0005 |

| Wald’s heteroskedasticity test | 0.000 | 0.001 |

| Breusch–Pagan test to identify contemporaneous correlation | 0.316 | 0.0270 |

| Test | Private Credit | Non-Performing Loans |

|---|---|---|

| F statistic | 3012.510 | 3489.550 |

| Sargan overidentification test | 0.2559 | 0.1216 |

| Test | Private Credit | Non-Performing Loans |

|---|---|---|

| Sargan test | 0.146 | 0.066 |

| Arellano–Bond test for zero autocorrelation in first-differenced errors | L1: 0.109 L2: 0.7891 | L1: 0.0308 L2: 0.450 |

| FE | FGLS | IV | AB | |

|---|---|---|---|---|

| (1) | (2) | (3) | (4) | |

| Lag (NPL) | 0.904 ** | 0.924 ** | 0.907 ** | 0.901 ** |

| (0.0131) | (0.0126) | (0.0133) | (0.0126) | |

| Y | −0.565 ** | −0.222 ** | −0.510 ** | −0.594 ** |

| (0.0906) | (0.0736) | (0.0868) | (0.0872) | |

| P | −0.168 | 0.0814 | 0.0446 | −0.136 |

| (0.138) | (0.0953) | (0.111) | (0.133) | |

| E | −0.0641 | 0.0609 | 0.0806 | −0.0518 |

| (0.0928) | (0.0717) | (0.0741) | (0.0891) | |

| LR | −0.0195 | −0.00817 | −0.0141 | −0.0206 |

| (0.0280) | (0.0267) | (0.0276) | (0.0269) | |

| R | −0.0267 | 0.0265 | −0.0286 | −0.0321 |

| (0.0207) | (0.0189) | (0.0206) | (0.0200) | |

| Number of banks | −0.0356 | −0.0701 | −0.0217 | −0.0161 |

| (0.0496) | (0.0437) | (0.0464) | (0.0481) | |

| Regulatory dummy | −8.454 ** | −4.329 ** | −7.762 ** | −8.748 ** |

| (1.712) | (1.397) | (1.675) | (1.641) | |

| COVID-19 cases | 0.158 ** | 0.129 ** | 0.146 ** | 0.161 ** |

| (0.0404) | (0.0336) | (0.0400) | (0.0387) | |

| Constant | 3.369 ** | 0.765 ** | 2.130 ** | 3.331 ** |

| (0.714) | (0.379) | (0.560) | (0.683) | |

| Observations | 833 | 833 | 832 | 827 |

| Pseudo R-squared | 0.898 | 0.897 | 0.899 | 0.898 |

| Variable | Mean | Std. Dev. | Min | Max | Observations | |||

|---|---|---|---|---|---|---|---|---|

| Non-performing loans | overall | 9.7258 | 23.4484 | −43.4170 | 129.2829 | N | = | 1012 |

| between | 5.7320 | 0.3350 | 17.2507 | n | = | 7 | ||

| within | 22.8377 | −48.6239 | 124.0760 | T | = | 144.571 | ||

| Private credit | overall | 8.8889 | 7.6541 | −20.8053 | 32.8830 | N | = | 1012 |

| between | 2.9337 | 3.1634 | 13.0145 | n | = | 7 | ||

| within | 7.1518 | −21.9324 | 31.7559 | T | = | 144.571 | ||

| Y | overall | 2.6685 | 5.0060 | −30.6079 | 14.0209 | N | = | 1018 |

| between | 0.9793 | 1.2004 | 4.1792 | n | = | 7 | ||

| within | 4.9232 | −31.5097 | 14.24752 | T | = | 145.429 | ||

| P | overall | 3.3786 | 2.5083 | −2.4691 | 13.5010 | N | = | 1028 |

| between | 1.4582 | 0.9983 | 5.2350 | n | = | 7 | ||

| within | 2.1135 | −1.9781 | 13.5783 | T | = | 146.857 | ||

| E | overall | 1.8277 | 3.4152 | −13.3830 | 17.6314 | N | = | 1012 |

| between | 2.0464 | 0.0000 | 4.8832 | n | = | 7 | ||

| within | 2.8412 | −12.7429 | 18.2714 | T | = | 144.571 | ||

| LR | overall | −0.5584 | 10.4454 | −44.4785 | 55.3044 | N | = | 858 |

| between | 2.6466 | −4.5101 | 3.0650 | n | = | 6 | ||

| within | 10.1691 | −43.5938 | 51.6810 | T | = | 143 | ||

| R | overall | −0.6077 | 14.0282 | −47.7155 | 63.9739 | N | = | 1018 |

| between | 1.6833 | −2.8647 | 2.1183 | n | = | 7 | ||

| within | 13.9413 | −45.4585 | 66.2309 | T | = | 145.429 | ||

| Number of

banks | overall | 0.4879 | 5.5431 | −14.2857 | 25 | N | = | 1000 |

| between | 1.7341 | −1.7596 | 3.4751 | n | = | 7 | ||

| within | 5.3024 | −15.0875 | 22.01281 | T | = | 142.857 | ||

| Restructured

loans | overall | 3.6649 | 12.3354 | 0.0000 | 60.0000 | N | = | 1134 |

| between | 1.8329 | 0.9630 | 5.9259 | n | = | 7 | ||

| within | 12.2181 | −2.2610 | 57.7390 | T | = | 162 | ||

| COVID-19

cases | overall | 6.7426 | 38.0105 | 0.0000 | 746.3580 | N | = | 1134 |

| between | 6.4683 | 0.1801 | 17.9121 | n | = | 7 | ||

| within | 37.5354 | −11.1695 | 735.1885 | T | = | 162 | ||

| 1 | These include Costa Rica, the Dominican Republic, Guatemala, Honduras, El Salvador, Nicaragua, and Panama. The Dominican Republic is included because it forms part of the Central American Integration System and its subgroups’ institutions. |

| 2 | In Spanish, Consejo Monetario Centroamericano. This is a multilateral institution that represents a group of central banks and other financial regulators, which forms part of the System of Economic Integration of Central America (SICA). |

| 3 | According to Berger and Demirgüç-Kunt (2021), the effect of the COVID-19 crisis did not have severe consequences for the US banking sector, thanks to the speed and size of the U.S. stimulus program and the prudential policies put in place during the global financial crisis. |

| 4 | For measures to mitigate bank risk, see Nguyen and Dang (2022, 2023) on risk governance structures and their effectiveness; Nguyen (2022) on audit committee effectiveness; and Alam et al. (2021) on deposits insurance. |

| 5 | |

| 6 | The effective reserve requirement ratio is the percentage of the total deposits received by commercial banks and financial institutions that are kept as cash reserves, in order to be able to respond to depositor cash withdrawals or to any unforeseen contingency. |

| 7 | Data source: Central American Monetary Council. |

| 8 | There is a risk that the explanatory variables are correlated with each other (multicolinearity). We therefore estimate the variance inflation factors (VIFs), which measure the proportion of the variance explained by correlation. The VIF test results are presented in Table A1 of Appendix A. In short, we found scant evidence of multicollinearity; the estimated VIF is less than 10, with a mean of 2.48. |

| 9 | Table 4A–C presents the tests for both estimates—private credit and non-performing loans. |

| 10 | |

| 11 | While most countries in the region registered average annual variations in their interest rates in 2020 (ranging from −16.8% in Costa Rica to −1.7% in Guatemala), two exceptional cases registered an increase (2.4% in El Salvador and 13.2% in Panama). Similarly, the legal reserve ratio decreased in most countries (from −21.5% in El Salvador to −4.2% in the Dominican Republic), though there was no change in one country (Guatemala) and an increase in another (13.8% in Honduras). |

References

- Alam, Nafis, Ganesh Sivarajah, and Muhammad Ishaq Bhatti. 2021. Do deposit insurance systems promote banking stability? International Journal of Financial Studies 9: 52. [Google Scholar] [CrossRef]

- Almustafa, Hamza, Quang Khai Nguyen, Jia Liu, and Van Cuong Dang. 2023. The impact of COVID-19 on firm risk and performance in MENA countries: Does national governance quality matter? PLoS ONE 18: e0281148. [Google Scholar] [CrossRef] [PubMed]

- Altavilla, Carlo, Francesca Barbiero, Miguel Boucinha, and Lorenzo Burlon. 2020. The Great Lockdown: Pandemic Response Policies and Bank Lending Conditions. Working Paper Series, No. 2465; Frankfurt: European Central Bank. [Google Scholar]

- Bartik, Alexander W., Marianne Bertrand, Zoë B. Cullen, Edward L. Glaeser, Michael Luca, and Christopher T. Stanton. 2020. How Are Small Businesses Adjusting to COVID-19? Early Evidence from a Survey; Working Paper No. w26989; Cambridge: National Bureau of Economic Research.

- Beck, Thorsten, and Jan Keil. 2020. Are Banks Catching Corona? Effects of COVID on Lending in the U.S. Available online: https://ssrn.com/abstract=3766831 (accessed on 1 October 2021).

- Beck, Thorsten, Asli Demirgüç-Kunt, and Vojislav Maksimovic. 2005. Financial and Legal Constraints to Growth: Does Firm Size Matter? Journal of Finance 60: 137–77. [Google Scholar] [CrossRef]

- Berger, Allen N., and Asli Demirgüç-Kunt. 2021. Banking research in the time of COVID-19. Journal of Financial Stability 57: 100939. [Google Scholar] [CrossRef]

- Bustamante, José, Walter Cuba, and Rafael Nivin. 2019. Determinants of Credit Growth and the Bank Lending Channel in Peru: A Loan Level Analysis. BIS Working Papers No. 803. Basel: Bank for International Settlements. [Google Scholar]

- Casanova, Catherine, Bryan Hardy, and Mert Onen. 2021. COVID-19 policy measures to support bank lending. In BIS Quarterly Review. Basel: Bank for International Settlements, pp. 45–59. [Google Scholar]

- CID-Gallup. 2021. National surveys of public opinion. In Survey Applied in the Second Fortnight of May 2021. San José: CID-Gallup. [Google Scholar]

- CMC. 2020. Matrix of Macroeconomic Policies: September 2020. Consejo Monetario Centroamericano. Available online: https://www.secmca.org/periodo_informe/trimestral/ (accessed on 1 October 2021).

- Duan, Yuejiao, Sadok El Ghoul, Omrane Guedhami, Haoran Li, and Xinming Li. 2021. Bank systemic risk around COVID-19: A cross-country analysis. Journal of Banking and Finance 133: 106299. [Google Scholar] [CrossRef] [PubMed]

- Duncan, Elizabeth, Akos Horvath, Diana Iercosan, Bert Loudis, Alice Maddrey, Francis Martinez, Timothy Mooney, Ben Ranish, Ke Wang, Missaka Warusawitharana, and et al. 2022. COVID-19 as a stress test: Assessing the bank regulatory framework. Journal of Financial Stability 61: 101016. [Google Scholar] [CrossRef]

- Fahlenbrach, Rüdiger, Kevin Rageth, and René M. Stulz. 2021. How valuable is financial flexibility when revenue stops? Evidence from the COVID-19 crisis. The Review of Financial Studies 34: 5474–521. [Google Scholar] [CrossRef]

- Falagiarda, Matteo, and Petra Köhler-Ulbrich. 2021. Bank lending to euro area firms—What have been the main drivers during the COVID-19 pandemic? European Economy 1: 119–43. [Google Scholar]

- Guo, Kai, and Vahram Stepanyan. 2011. Determinants of Bank Credit in EMEs. IMF Working Paper, No. 11/51. Washington: International Monetary Fund. [Google Scholar]

- IADB. 2020. The Impact of COVID-19 on the Economies of Central America, Haiti, Mexico, Panama and the Dominican Republic. Washington: Inter-American Development Bank. (In Spanish) [Google Scholar] [CrossRef]

- IADB. 2022. In Search of Better Indebtedness Conditions for Companies and Households: Economic Report on Central America, Mexico, Panama, and the Dominican Republic. Washington: Inter-American Development Bank. (In Spanish) [Google Scholar] [CrossRef]

- IMF. 2022. Fiscal Policies Database in Response to COVID-19. Washington: International Monetary Funds. Available online: https://www.imf.org/en/Topics/imf-and-covid19/Fiscal-Policies-Database-in-Response-to-COVID-19 (accessed on 1 November 2021).

- Ivanovic, Maja. 2016. Determinants of Credit Growth: The Case of Montenegro. Journal of Central Banking Theory and Practice 2: 101–18. [Google Scholar] [CrossRef]

- Jiménez, Gabriel, Steven Ongena, José-Luis Peydró, and Jesús Saurina. 2012. Credit Supply and Monetary Policy: Identifying the Bank Balance-Sheet Channel with Loan Applications. American Economic Review 102: 2301–26. [Google Scholar] [CrossRef]

- Li, Lei, Philip E. Strahan, and Song Zhang. 2020. Banks as lenders of first resort: Evidence from the COVID-19 crisis. The Review of Corporate Finance Studies 9: 472–500. [Google Scholar] [CrossRef]

- Liu, Zheng, and Pengfei Wang. 2014. Credit Constraints and Self-Fulfilling Business Cycles. American Economic Journal: Macroeconomics 6: 32–69. [Google Scholar] [CrossRef]

- Nguyen, Quang Khai. 2022. Audit committee structure, institutional quality, and bank stability: Evidence from ASEAN countries. Finance Research Letters 46: 102369. [Google Scholar] [CrossRef]

- Nguyen, Quang Khai, and Van Cuong Dang. 2022. The impact of risk governance structure on bank risk management effectiveness: Evidence from ASEAN countries. Heliyon 8: e11192. [Google Scholar] [CrossRef] [PubMed]

- Nguyen, Quang Khai, and Van Cuong Dang. 2023. Does the country’s institutional quality enhance the role of risk governance in preventing bank risk? Applied Economics Letters 30: 850–53. [Google Scholar] [CrossRef]

- Poschke, Markus. 2018. The Firm Size Distribution across Countries and Skill-Biased Change in Entrepreneurial Technology. American Economic Journal: Macroeconomics 10: 1–41. [Google Scholar] [CrossRef]

- Ruiz-Marín, Manuel, Mariluz Maté-Sánchez-Val, and Jose Noguera-Venero. 2023. Did Covid-19 modify the spatial concentration of business failure? Regional Statistics 13: 201–13. [Google Scholar] [CrossRef]

- Zhang, Dengjun, and Geir Sogn-Grundvåg. 2022. Credit constraints and the severity of COVID-19 impact: Empirical evidence from enterprise surveys. Economic Analysis and Policy 74: 337–49. [Google Scholar] [CrossRef] [PubMed]

- Žunić, Amila, Kemal Kozarić, and Emina Žunić Dželihodžić. 2021. Non-Performing Loan Determinants and Impact of COVID-19: Case of Bosnia and Herzegovina. Journal of Central Banking Theory and Practice 10: 5–22. [Google Scholar] [CrossRef]

| Private Credit | Non-Performing Loans | Economic Activity Index | Deliquency Rate | Private

Credit | Non-Performing

Loans | Economic Activity Index | Deliquency Rate | ||

|---|---|---|---|---|---|---|---|---|---|

| Country | Costa Rica | Dominican Republic | |||||||

| Mean | 2009 (January)–2021 (February) | 9.611 | 17.251 | 2.175 | 7.200 | 13.015 | 8.184 | 4.200 | −3.423 |

| 2019 (January)–2020 (February) | 0.420 | 4.985 | 1.938 | 4.714 | 10.872 | 0.222 | 5.028 | −9.146 | |

| 2020 (March)–2021 (February) | 1.200 | 4.423 | −6.188 | 3.361 | 9.153 | 29.610 | −7.578 | 20.820 | |

| Country | El Salvador | Guatemala | |||||||

| Mean | 2009 (January)–2021 (February) | 3.163 | 0.335 | 1.200 | −2.217 | 8.869 | 8.111 | 2.870 | −0.344 |

| 2019 (January)-2020 (February) | 5.166 | −0.205 | 2.946 | −5.066 | 6.479 | 4.439 | 3.837 | −1.902 | |

| 2020 (March)–2021 (February) | 2.807 | −6.518 | −9.349 | −9.091 | 6.725 | −7.865 | −1.755 | −13.690 | |

| Country | Honduras | Nicaragua | |||||||

| Mean | 2009 (January)–2021 (February) | 8.923 | 6.535 | 2.336 | −2.061 | 10.016 | 14.933 | 2.339 | 8.487 |

| 2019 (January)–2020 (February) | 11.553 | 14.301 | 3.149 | 1.648 | −16.804 | 58.298 | −2.708 | 91.051 | |

| 2020 (March)–2021 (February) | 2.624 | 18.864 | −10.366 | 14.888 | −6.872 | −4.000 | −3.499 | 2.981 | |

| Country | Panama | ||||||||

| Mean | 2009 (January)-2021 (February) | 8.676 | 12.896 | 3.570 | 4.566 | ||||

| 2019 (January)–2020 (February) | 5.823 | 6.025 | 3.619 | 3.135 | |||||

| 2020 (March)–2021 (February) | 2.258 | 14.314 | −20.406 | 15.692 | |||||

| Private Credit | Non-Performing Loans | Economic Activity Index | Deliquency Rate | Private Credit | Non-Performing Loans | Economic Activity Index | Deliquency Rate | ||

|---|---|---|---|---|---|---|---|---|---|

| Country | Costa Rica | Dominican Republic | |||||||

| Mean | 2008 (January)–2021 (February) | $12,170,990.183 | $279,672.322 | 89.639 | 2.228 | $564,275.67 | $13,416.35 | 138.411 | 2.456 |

| 2019 (January)–2020 (February) | $17,625,752.846 | $482,469.211 | 104.700 | 2.735 | $943,972.67 | $15,945.58 | 180.243 | 1.569 | |

| 2020 (March)–2021 (February) | $17,761,830.029 | $508,956.453 | 98.683 | 2.864 | $1,032,791.17 | $20,590.61 | 167.892 | 1.886 | |

| Country | El Salvador | Guatemala | |||||||

| Mean | 2008 (January)–2021 (February) | $10,303.348 | $265.755 | 100.010 | 2.677 | $ 131,019.62 | $2674.29 | 104.768 | 2.079 |

| 2019 (January)–2020 (February) | $12,739.54 | $237.14 | 112.550 | 1.852 | $ 188,921.80 | $4399.86 | 123.929 | 2.329 | |

| 2020 (March)–2021 (February) | $13,139.96 | $221.68 | 103.136 | 1.676 | $ 201,404.17 | $4123.00 | 122.108 | 2.048 | |

| Country | Honduras | Nicaragua | |||||||

| Mean | 2008 (January)–2021 (February) | $195,236.71 | $6062.99 | 203.232 | 3.347 | $94,240.77 | $1733.81 | 134.150 | 1.998 |

| 2019 (January)–2020 (February) | $307,970.19 | $6807.38 | 243.836 | 2.110 | $ 126,173.83 | $3900.46 | 145.771 | 3.101 | |

| 2020 (March)–2021 (February) | $316,840.41 | $8236.85 | 221.492 | 2.455 | $ 116,150.88 | $3858.47 | 140.060 | 3.324 | |

| Country | Panama | ||||||||

| Mean | 2008 (January)–2021 (February) | $37,091.31 | $627.29 | 267.359 | 1.584 | ||||

| 2019 (January)–2020 (February) | $52,713.29 | $1178.76 | 340.907 | 2.193 | |||||

| 2020 (March)–2021 (February) | $54,234.03 | $1355.66 | 279.027 | 2.539 | |||||

| FE | FGLS | IV | AB | |

|---|---|---|---|---|

| (1) | (2) | (3) | (4) | |

| Lag(C) | 0.979 *** | 0.980 *** | 0.974 *** | 0.979 *** |

| (0.00719) | (0.00691) | (0.00717) | (0.00706) | |

| Y | 0.0922 *** | 0.0508 *** | 0.0830 *** | 0.0918 *** |

| (0.0149) | (0.0118) | (0.0146) | (0.0145) | |

| P | 0.0506 ** | 0.0200 | 0.0396 ** | 0.0520 ** |

| (0.0236) | (0.0174) | (0.0196) | (0.0231) | |

| E | 0.0206 | 0.00472 | 0.00266 | 0.0200 |

| (0.0166) | (0.0136) | (0.0135) | (0.0164) | |

| R | −0.0195 *** | −0.0212 *** | −0.0187 *** | −0.0197 *** |

| (0.00364) | (0.00375) | (0.00364) | (0.00357) | |

| LR | −0.0184 *** | −0.0135 *** | −0.0185 *** | −0.0184 *** |

| (0.00458) | (0.00404) | (0.00449) | (0.00452) | |

| Number of banks | 0.0161 * | 0.0196 ** | 0.0136 * | 0.0168 ** |

| (0.00852) | (0.00781) | (0.00801) | (0.00845) | |

| Restructured loans | 0.0202 *** | 0.0123 ** | 0.0162 ** | 0.0202 *** |

| (0.00674) | (0.00619) | (0.00653) | (0.00658) | |

| COVID-19 cases | −0.0083 ** | −0.0101 *** | −0.00724 * | −0.00828 ** |

| (0.00384) | (0.00375) | (0.00377) | (0.00375) | |

| Constant | −0.405 *** | −0.0954 | −0.247 *** | −0.409 *** |

| (0.114) | (0.0637) | (0.0896) | (0.111) | |

| Observations | 833 | 833 | 828 | 827 |

| Pseudo R−squared | 0.974 | 0.973 | 0.974 | 0.974 |

| (A) | ||

| Test | Private Credit | Non-Performing Loans |

| Wooldridge autocorrelation test | 0.0467 | 0.0005 |

| Wald’s heteroskedasticity test | 0.000 | 0.000 |

| Breusch–Pagan test to identify contemporaneous correlation | 0.3526 | 0.0321 |

| (B) | ||

| Test | Private Credit | Non-Performing Loans |

| F statistic | 3030.290 | 3538.730 |

| Sargan overidentification test | 0.1925 | 0.1375 |

| (C) | ||

| Test | Private Credit | Non-Performing Loans |

| Sargan test | 0.1467 | 0.054 |

| Arellano–Bond test for zero autocorrelation in first-differenced errors | L1: 0.109 L2: 0.7435 | L1: 0.0306 L2: 0.465 |

| FE | FGLS | IV | AB | |

|---|---|---|---|---|

| (1) | (2) | (3) | (4) | |

| Lag (NPL) | 0.908 *** | 0.926 *** | 0.911 *** | 0.906 *** |

| (0.0131) | (0.0127) | (0.0132) | (0.0126) | |

| Y | −0.512 *** | −0.160 ** | −0.452 *** | −0.544 *** |

| (0.0915) | (0.0727) | (0.0864) | (0.0880) | |

| P | −0.143 | 0.0841 | 0.0651 | −0.111 |

| (0.139) | (0.0977) | (0.111) | (0.133) | |

| E | −0.0431 | 0.0709 | 0.0976 | −0.0303 |

| (0.0933) | (0.0738) | (0.0749) | (0.0894) | |

| LR | 0.00159 | 0.0147 | 0.00451 | 0.00167 |

| (0.0282) | (0.0262) | (0.0277) | (0.0270) | |

| R | −0.0314 | 0.0242 | −0.0324 | −0.0377 * |

| (0.0212) | (0.0197) | (0.0211) | (0.0205) | |

| Number of banks | −0.0139 | −0.0533 | −0.00145 | 0.00738 |

| (0.0496) | (0.0443) | (0.0464) | (0.0480) | |

| Restructured loans | −0.153 *** | −0.0626 * | −0.134 *** | −0.161 *** |

| (0.0380) | (0.0340) | (0.0364) | (0.0364) | |

| COVID-19 cases | 0.143 *** | 0.108 *** | 0.129 *** | 0.146 *** |

| (0.0410) | (0.0343) | (0.0406) | (0.0392) | |

| Constant | 2.961 *** | 0.493 | 1.721 *** | 2.931 *** |

| (0.704) | (0.371) | (0.543) | (0.673) | |

| Observations | 833 | 833 | 832 | 827 |

| Pseudo R-squared | 0.897 | 0.896 | 0.898 | 0.897 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Ventosa-Santaulària, D.; Marmolejo, A.; Alvarado, L. The Effect of Financial Policies Implemented during COVID-19 on Bank Credit in the Central American Region. Int. J. Financial Stud. 2023, 11, 68. https://doi.org/10.3390/ijfs11020068

Ventosa-Santaulària D, Marmolejo A, Alvarado L. The Effect of Financial Policies Implemented during COVID-19 on Bank Credit in the Central American Region. International Journal of Financial Studies. 2023; 11(2):68. https://doi.org/10.3390/ijfs11020068

Chicago/Turabian StyleVentosa-Santaulària, Daniel, Arnoldo Marmolejo, and Luis Alvarado. 2023. "The Effect of Financial Policies Implemented during COVID-19 on Bank Credit in the Central American Region" International Journal of Financial Studies 11, no. 2: 68. https://doi.org/10.3390/ijfs11020068

APA StyleVentosa-Santaulària, D., Marmolejo, A., & Alvarado, L. (2023). The Effect of Financial Policies Implemented during COVID-19 on Bank Credit in the Central American Region. International Journal of Financial Studies, 11(2), 68. https://doi.org/10.3390/ijfs11020068