Determinants of the Cost of Financial Intermediation: Evidence from Emerging Economies

Abstract

1. Introduction

2. Review of the Determinants of the Cost of Financial Intermediation

3. Data, Variables, and Model

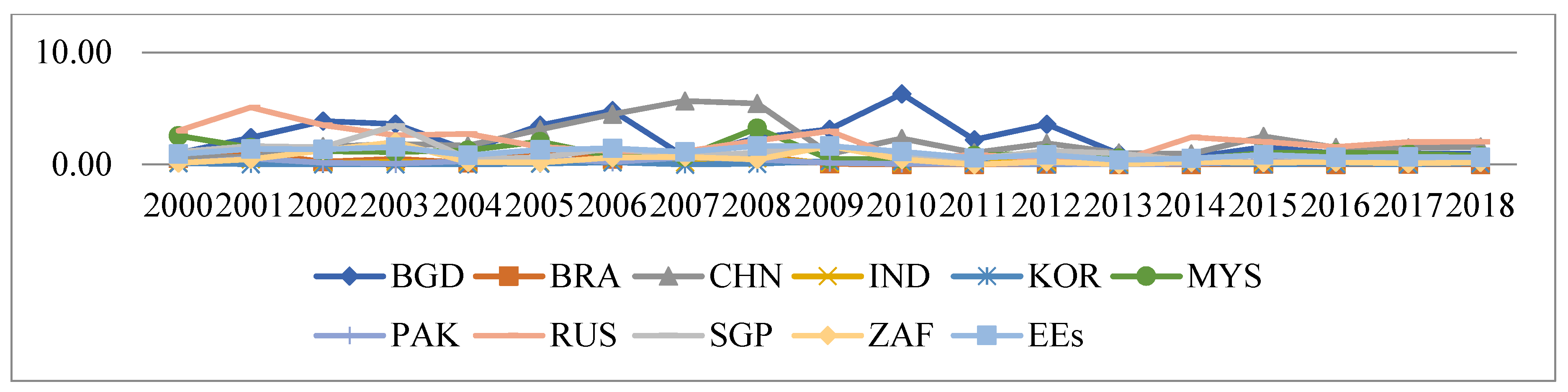

3.1. Sample

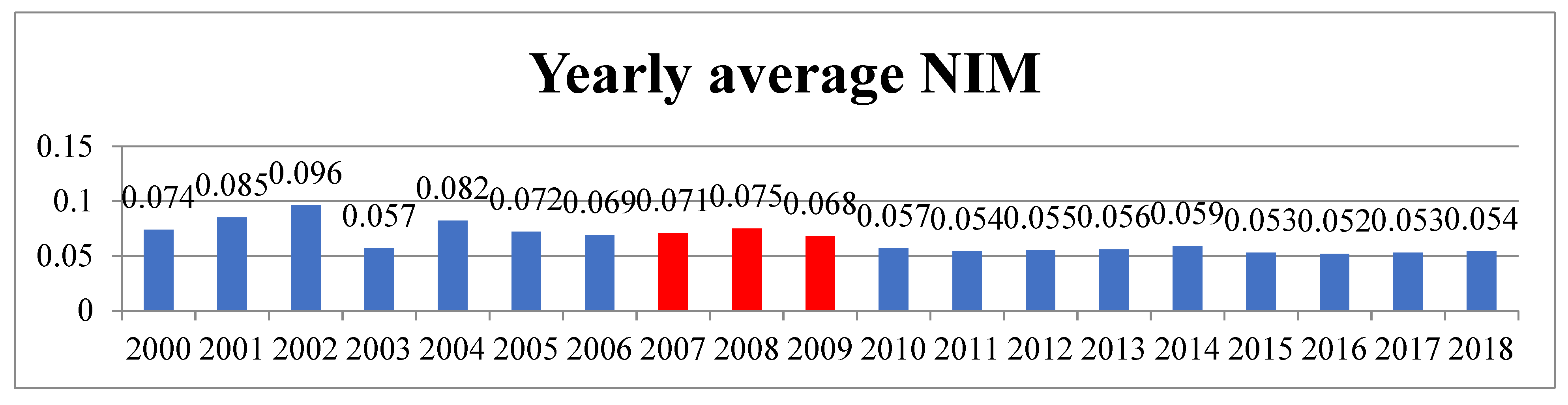

3.2. Measurement of Bank Net Interest Margin

3.3. Bank-Level Control Variables

3.4. Industry-Level Variable

3.5. Country-Level Determinants

3.6. Regulatory-Level Determinants

3.7. Institutional-Level Determinants

3.8. Macroeconomic-Level Determinants

3.9. Specified Model

4. Empirical Analysis

4.1. Summary Statistics and Correlation Matrix

4.2. Determinants of the Cost of Financial Intermediation: Main Specification

4.3. Elasticity: Alternative Specification

4.4. Impact of Global Financial Crisis (GFC)

4.5. Dropping the Contributing Variables and Endogeneity

4.6. Regression for BRICS Block and Dropped Russia from Whole Samples

4.7. Sensitivity Analysis: Methodological Issues

5. Conclusions and Policy Implications

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

| Variables/ Authors | Bank-Specific Determinants | Industry | Macro-Specific | Followed Model | Estimation Method | Period | Sample | |||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| GOVS | CINEY | OPCR | NPLTL | NLMIR | OETTA | NNIR | OCR | LL | TLTD | CIR | HHI | CR | INF | GDP | SDMIR | |||||

| We | (+) | (+) | (+) | (+) | (?) | (+) | (+) | (+) | (?) | (?) | (−) | (?) | N/A | (?) | (?) | (+) | Modified Dealership model * | FE, RE, OLS System GMM | 2000 to 2015 | 10 countries from Emerging Economies |

| (Ho and Saunders 1981) | N/A | N/A | N/A | (+) | N/A | N/A | (+) | (+) | N/A | N/A | N/A | N/A | (+) | N/A | N/A | (+) | Introduce Dealership model ** | OLS | 1976 to 1979 | 100 major US Banks |

| (Saunders and Schumacher 2000) | N/A | N/A | N/A | N/A | N/A | (+) | (+) | (+) | N/A | N/A | N/A | N/A | (+) | N/A | N/A | (+) | Dealership model ** | Cross- sectional OLS | 1988 to 1995 | US and six European banks |

| (Afanasieff et al. 2002) | N/A | N/A | (+) | N/A | N/A | N/A | N/A | (+) | (+) | N/A | N/A | N/A | N/A | (−) | (−) | (−) | Dealership model ** | GARCH model | 1997 to 2000 | Brazilian commercial banks (142) |

| (Angbazo 1997)19 | N/A | N/A | N/A | (+) | (?) | (+) | (?) | (+) | N/A | N/A | (+) | N/A | N/A | N/A | N/A | (−) | Dealership model ** | GLS | 1989 to 1993 | US commercial banks (286) |

| (McShane and Sharpe 1985) | N/A | N/A | N/A | N/A | N/A | (+) | N/A | N/A | (?) | N/A | N/A | N/A | (+) | N/A | N/A | (+) | Dealership model ** | Time series analysis | 1962 to 1981 | Australian Trading banks |

| (Brock and Suarez 2000)20 | N/A | N/A | (+) | (+) | N/A | N/A | N/A | (+) | N/A | N/A | N/A | N/A | N/A | (+) | (+) | (+) | Dealership model ** | Panel OLS regression | 1991 to 1996 | 7 countries from Latin America |

| (Maudos and De Guevara 2004) | N/A | N/A | (+) | N/A | (−) | (+) | (+) | N/A | (−) | N/A | (−) | (+) | (+) | N/A | N/A | (+) | Dealership model * | FE, OLS | 1993 to 2000 | 5 European countries |

| (J. Maudos and Solís 2009) | N/A | N/A | (+) | (+) | (−) | (+) | (+) | (+) | (+) | N/A | (−) | N/A | (+) | (?) | (?) | (+) | Dealership model ** | FE, GMM | 1993 to 2005 | Mexican Banking |

| (Valverde and Fernández 2007)21 | N/A | N/A | (+) | (+) | N/A | (+) | N/A | N/A | N/A | N/A | N/A | (?) | N/A | N/A | (−) | (+) | Dealership model ** | GMM | 1994 to 2001 | 7 European countries |

| (Hawtrey and Liang 2008) | N/A | N/A | (+) | (+) | (?) | (+) | (+) | (+) | (−) | N/A | (−) | (+) | N/A | N/A | (+) | Dealership model ** | Pooled GLS, FE | 1987 to 2001 | 14 OECD countries | |

| (Fungáčová and Poghosyan 2011)22 | N/A | N/A | N/A | (−) | N/A | (+) | N/A | N/A | (−) | N/A | N/A | (−) | N/A | N/A | N/A | N/A | Dealership model ** | FE | 1999 to 2007 | All Russian banks |

| (Tarus et al. 2012) | N/A | N/A | (+) | (+) | N/A | N/A | N/A | N/A | N/A | N/A | N/A | (−) | (−) | (+) | (−) | N/A | Dealership model ** | FE, Polled panel OLS | 1999 to 2007 | Kenyan banks |

| (Ash Demirgüç-Kunt and Huizinga 1999) | N/A | N/A | (+) | (+) | N/A | (+) | N/A | N/A | (?) | N/A | N/A | N/A | (?) | (+) | (?) | N/A | N/A | Pooled WLS | 1988 to 1995 | 80 countries worldwide |

| (Doliente 2005)23 | N/A | N/A | (+) | (+) | N/A | (+) | N/A | N/A | N/A | N/A | N/A | N/A | N/A | N/A | N/A | (+) | Dealership model ** | Pooled OLS | 1994 to 2001 | 4 Southeast Asian countries |

| (Gelos 2009) | N/A | N/A | (+) | N/A | N/A | (+) | N/A | (+) | (−) | N/A | N/A | N/A | (−) | (+) | (−) | (+) | N/A | FE, RE | 1999 to 2002 | 85 countries worldwide |

| (Khediri and Ben-Khedhiri 2010) | N/A | N/A | (+) | N/A | N/A | (+) | (+) | (+) | N/A | N/A | (−) | N/A | N/A | N/A | N/A | N/A | Dealership model ** | FE, RE | 1996 to 2005 | Tunisian Banks |

| (Claeys and Vennet 2008)24 | N/A | (+) | N/A | (+) | N/A | (+) | N/A | N/A | N/A | N/A | N/A | N/A | (+) | (+) | (−) | (+) | Dealership model ** | Cross-sectional OLS | 1994 to 2001 | 31 West and Eastern Euro. country |

| (Gounder and Sharma 2012) | N/A | N/A | (+) | (+) | N/A | (?) | (+) | (?) | N/A | N/A | (−) | N/A | (+) | N/A | N/A | N/A | Dealership model ** | PLS, FE, RE | 2000 to 2010 | Fijian banks |

| (Zhou and Wong 2008) | N/A | N/A | (+) | (+) | N/A | (−) | (+) | (+) | (−) | N/A | (−) | N/A | N/A | N/A | N/A | N/A | Dealership model ** | FE | 1996 to 2003 | Mainland Chinese banks |

| (Amuakwa-Mensah and Marbuah 2015) | N/A | N/A | (+) | (?) | N/A | (+) | N/A | N/A | (?) | N/A | N/A | (?) | N/A | (+) | (?) | N/A | N/A | System GMM | 1997 to 2011 | Ghanaian banks |

| (Horvath 2009) | N/A | N/A | (+) | (+) | N/A | (−) | N/A | N/A | (−) | N/A | N/A | (?) | N/A | (+) | (?) | N/A | N/A | System GMM | 2000 to 2006 | Czech banks |

| (Schwaiger and Liebeg 2007) | N/A | N/A | (+) | N/A | (−) | (+) | (+) | N/A | (?) | N/A | (−) | N/A | (+) | (+) | (+) | (+) | Dealership model ** | FE, OLS | 2000 to 2005 | 11 Central & eastern Euro. countries |

| (Hesse 2007) | N/A | N/A | (+) | N/A | N/A | (+) | N/A | N/A | N/A | N/A | N/A | (−) | N/A | (+) | N/A | N/A | Dealership model ** | Pooled OLS, FE | 2000 to 2005 | Nigerian banks |

| (Dablanorris and Floerkemeier 2007) | N/A | N/A | (+) | N/A | N/A | (−) | N/A | N/A | (?) | N/A | N/A | (+) | (+) | (?) | (?) | (+) | N/A | OLS | 2002 to 2006 | Armenian banks |

| (Williams 2007) | N/A | N/A | (+) | (+) | (?) | (−) | (+) | (?) | (?) | N/A | (−) | N/A | (+) | N/A | N/A | (?) | Dealership model ** | Pooled OLS, RE | 1989 to 2001 | Australian banks |

| (Poghosyan 2013)25 | N/A | N/A | (+) | (+) | N/A | (−) | N/A | (+) | (−) | N/A | N/A | (+) | (+) | (?) | (?) | N/A | Modified Dealership model * | FE, System GMM | 1996 to 2010 | Low income countries |

| (Islam and Nishiyama 2016) | N/A | N/A | (+) | (−) | (?) | (+) | (?) | N/A | (?) | (?) | (?) | (−) | (−) | (?) | (−) | (?) | Dealership model ** | FE | 1997 to 2012 | 4 countries from South Asia |

| 1 | Asli Demirgüç-Kunt et al. (2004) considered Economic and Banking freedom, but we especially capture the market-based banking scenario of Emerging Economies. |

| 2 | Saunders and Schumacher (2000) studied the USA and six EU countries, Maudos and De Guevara (2004) studied five European countries, Poghosyan (2013) examined low-income countries, Islam and Nishiyama (2016) studied four countries from South Asia. Moreover, Zhou and Wong (2008); Afanasieff et al. (2002), and Williams (2007) documented determinants of net interest margin in mainland China, Brazilian and Australian banks, respectively, among others. |

| 3 | This measure is based on purchasing power parity. Using market exchange rates, this share is 30% (European Central Bank 2015) (accessed on 21 March 2022). |

| 4 | For a detailed explanation, please refer to http://web.pdx.edu/~ito/trilemma_indexes.htm (accessed on 21 March 2022) |

| 5 | For a detailed explanation, please refer to http://www.heritage.org/index/explore?view=by-region-country-year (accessed on 11 March 2022) |

| 6 | For detail about the selection of home country and base country, please refer to “Notes on the Trilemma Measures”, it is open access and can be found from any browser. (accessed on 17 February 2022) |

| 7 | For details about the broad areas of IF and FF, please refer to “Methodology the index of Economic freedom by Heritage foundation”, it is open access and can be found from any browser. |

| 8 | The details about the 10 questions as a measure of capital stringency can be found in Ashraf et al. (2016), page no-284. |

| 9 | Denoted as quantity (Basel guideline) and quality (restrictions of funds used as capital). |

| 10 | Please go through Baseline result in Table 4, Hausman test p-value is 0.00. |

| 11 | Please go through Baseline result in Table 4, White test p-value is 0.00. |

| 12 | Price of fund = Interest expenses/total deposit, price of labor = personal expenses/total assets, price of capital = other operating expenses/total assets. |

| 13 | |

| 14 | The minimum value of NPLTL, NLMIR, OCR, HHI, and SDMIR is 3.64 × 10−6, 2.08 × 10−23, 3.45 × 10−7, 2.75 × 10−3, and 2.17 × 10−19, respectively. |

| 15 | Ho and Saunders’ (1981) basic two-step dealership model. |

| 16 | To measure the relevance of the instrument, we depend on the Kleibergen-Paap under-identification test and the Stock-Yogo weak identification test. The relevant Lm test for the Kleibergen-Paap under-identification delivers a zero p-value suggesting that the model is identified and the OPCR of banks is an appropriate external instrument for CINEY. Similarly, Stock-Yogo weak identification test is executed to test that OPCR is not a weak instrument for CINEY. Relevant F-test of the excluded exogenous variable is accomplished in the first-stage regression for examining the null hypothesis that the OPCR does not explain differences in CINEY. The null hypothesis is rejected at the 1% level advising that OPCR is not weakly correlated with the endogenous variable, CINEY. The results of both these tests indicate that the instrument is relevant. Since we consider one endogenous plus one instrumental variable, the regression is exactly-identified and thus the relevant over-identification test to check the exogeneity of the instrument is invalid here. |

| 17 | All the BRICS economies were hit by the 2007–2008 financial crisis and Brazil, Russia and South Africa even experienced a negative growth rate of −0.13%, −7.82%, and −1.54% in 2009, respectively. However, the BRICS economies recovered rapidly to a growth rate of 7.52% in Brazil, 4.50% in Russia, 10.26% in India, 10.63% in China, and 3.04% in South Africa in 2010 (http://data.worldbank.org/indicator). (Accessed on 11 November 2022) |

| 18 | To estimate the system GMM, we execute the xtbond2 command developed by Arellano and Bover (1995), suggesting employing a system of first-differenced and level equations, where lags of levels and lags of the first differences are employed as instruments. |

| 19 | |

| 20 | This study estimates the regression for individual sample countries and, therefore, the results would vary in some cases; we reported the maximum countries’ similarities of findings here. |

| 21 | This study is a multi-output framework considering SPREAD (Loan-to-deposit rate spread), LMSPR (three months interbank market rates minus bank loan rates), GROSS (Gross income to total assets), Learner index and the numerator of LERNER index as dependent variables. Since our study related to bank spread, particularly, we reported the determinants of spread only. We also employed some other bank-level variables which are not reported here. |

| 22 | We particularly emphasize ownership patterns as determinants of NIM. |

| 23 | This study also estimates the regression for individual sample countries and, therefore, the results would vary in some cases; we reported the maximum countries’ similarities of findings here. |

| 24 | This study is a comparison of West, Accession, and Non-accession countries in Europe and, therefore, the results will vary in some cases; we reported the maximum countries’ similarities of findings here. |

| 25 | This study is a comprehensive determinant of Bank interest margin including bank, industry, and macro-specific with the alteration of regulatory and institutional-level factors and thus we follow this study to generate our model with the extension of bank and country-level determinants. |

References

- Afanasieff, Tarsila Segalla, Priscilla M. Lhacer, and Márcio I. Nakane. 2002. The determinants of bank interest spread in Brazil. Money Affairs 15: 183–207. [Google Scholar]

- Agapova, Anna, and James E. McNulty. 2016. Interest rate spreads and banking system efficiency: General considerations with an application to the transition economies of Central and Eastern Europe. International Review of Financial Analysis 47: 154–65. [Google Scholar] [CrossRef]

- Aizenman, Joshua, Menzie D. Chinn, and Hiro Ito. 2010. The emerging global financial architecture: Tracing and evaluating new patterns of the trilemma configuration. Journal of International Money and Finance 29: 615–41. [Google Scholar] [CrossRef]

- Allen, Linda. 1988. The determinants of bank interest margins: A note. Journal of Financial and Quantitative Analysis 23: 231–35. [Google Scholar] [CrossRef]

- Amuakwa-Mensah, Franklin, and George Marbuah. 2015. The determinants of net interest margin in the Ghanaian banking industry. Journal of African Business 16: 272–88. [Google Scholar] [CrossRef]

- Angbazo, Lazarus. 1997. Commercial bank net interest margins, default risk, interest-rate risk, and off-balance sheet banking. Journal of Banking & Finance 21: 55–87. [Google Scholar]

- Arellano, Manuel, and Olympia Bover. 1995. Another look at the instrumental variable estimation of error-components models. Journal of Econometrics 68: 29–51. [Google Scholar] [CrossRef]

- Ashraf, Badar Nadeem. 2017. Political institutions and bank risk-taking behavior. Journal of Financial Stability 29: 13–35. [Google Scholar] [CrossRef]

- Ashraf, Badar Nadeem, Bushra Bibi, and Changjun Zheng. 2016. How to regulate bank dividends? Is capital regulation an answer? Economic Modelling 57: 281–93. [Google Scholar] [CrossRef]

- Barajas, Adolfo, Roberto Steiner, and Natalia Salazar. 1999. Interest spreads in banking in Colombia, 1974–1996. IMF Staff Papers 46: 196–224. [Google Scholar]

- Barth, James R., Gerard Caprio, and Ross Levine. 2013. Bank Regulation and Supervision in 180 Countries from 1999 to 2011. Journal of Financial Economic Policy 5: 111–219. [Google Scholar] [CrossRef]

- Baum, Christopher F., Mark E. Schaffer, and Steven Stillman. 2003. Instrumental variables and GMM: Estimation and testing. Stata Journal 3: 1–31. [Google Scholar] [CrossRef]

- Beck, Thorsten, Asli Demirguc-Kunt, and Ross Levine. 2003. Bank concentration and crises: National Bureau of Economic Research. Available online: https://www.nber.org/papers/w9921 (accessed on 25 November 2022).

- Brock, Philip L., and Liliana Rojas Suarez. 2000. Understanding the behavior of bank spreads in Latin America. Journal of Development Economics 63: 113–34. [Google Scholar] [CrossRef]

- Claeys, Sophie, and Rudi Vander Vennet. 2008. Determinants of bank interest margins in Central and Eastern Europe: A comparison with the West. Economic Systems 32: 197–216. [Google Scholar] [CrossRef]

- Dabla-Norris, Era, and Holger Floerkemeier. 2007. Bank Efficiency and Market Structure: What Determines Banking Spreads in Armenia? IMF Working Papers. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=994464 (accessed on 12 November 2022).

- Demirgüç-Kunt, Ash, and Harry Huizinga. 1999. Determinants of commercial bank interest margins and profitability: Some international evidence. The World Bank Economic Review 13: 379–408. [Google Scholar] [CrossRef]

- Demirguc-Kunt, Asli, Luc Laeven, and Ross Levine. 2004. Regulations, Market Structure, Institutions, and the Cost of Financial Intermediation. Journal of Money Credit & Banking 36: 593–622. [Google Scholar]

- Doliente, Jude. 2005. Determinants of bank net interest margins in Southeast Asia. Applied Financial Economics Letters 1: 53–57. [Google Scholar] [CrossRef]

- Finn, Timothy, II, and Joseph Frederick. 1992. Managing the margin. Aba Banking Journal 84: 50. [Google Scholar]

- Fungáčová, Zuzana, and Tigran Poghosyan. 2011. Determinants of bank interest margins in Russia: Does bank ownership matter? Economic Systems 35: 481–95. [Google Scholar] [CrossRef]

- Freedom_House. 2017. Available online: https://freedomhouse.org/report/freedom-world (accessed on 5 January 2022).

- Gelos, R. Gaston. 2009. Banking spreads in Latin America. Economic Inquiry 47: 796–814. [Google Scholar] [CrossRef]

- Gorton, Gary, and Andrew Winton. 1998. Banking in transition economies: Does efficiency require instability? Journal of Money, Credit and Banking 30: 621–50. [Google Scholar] [CrossRef]

- Gounder, Neelesh, and Parmendra Sharma. 2012. Determinants of bank net interest margins in Fiji, a small island developing state. Applied Financial Economics 22: 1647–54. [Google Scholar] [CrossRef]

- Gujarati, Damodar. 2007. Basic Econometrics. New Delhi: Tata McGraw Hill Publishing Company Limited, vol. 110, pp. 451–52. [Google Scholar]

- Hawtrey, Kim, and Hanyu Liang. 2008. Bank interest margins in OECD countries. North American Journal of Economics & Finance 19: 249–60. [Google Scholar]

- Hesse, Heiko. 2007. Financial Intermediation in the Pre-Consolidated Banking Sector in Nigeria. Herndon: World Bank Publications, vol. 4267. [Google Scholar]

- Ho, Thomas S. Y., and Anthony Saunders. 1981. The determinants of bank interest margins: Theory and empirical evidence. Journal of Financial and Quantitative Analysis 16: 581–600. [Google Scholar] [CrossRef]

- Horvath, Roman. 2009. The Determinants of Interest Rate Margins of the Czech Banks. Czech Journal of Economics & Finance 59: 128–36. [Google Scholar]

- Islam, Md Shahidul, and Shin-Ichi Nishiyama. 2016. The determinants of bank net interest margins: A panel evidence from South Asian countries. Research in International Business and Finance 37: 501–14. [Google Scholar] [CrossRef]

- Kaufmann, Daniel, Aart Kraay, and Massimo Mastruzzi. 2011. The worldwide governance indicators: Methodology and analytical issues. Hague Journal on the Rule of Law 3: 220–46. [Google Scholar] [CrossRef]

- Ben Khediri, Karim, and Hichem Ben-Khedhiri. 2010. Determinants of bank net interest margin in Tunisia: A panel data model. Applied Economics Letters 18: 1267–71. [Google Scholar] [CrossRef]

- Lerner, Eugene. 1981. Discussion: The determinants of bank interest margins: Theory and empirical evidence. Journal of Financial and Quantitative Analysis 16: 601–2. [Google Scholar] [CrossRef]

- López-Espinosa, Germán, Antonio Moreno, and Fernando Peréz de Gracia. 2011. Banks’ net interest margin in the 2000s: A macro-accounting international perspective. Journal of International Money and Finance 30: 1214–33. [Google Scholar] [CrossRef]

- Maudos, Joaquín, and Juan Fernandez De Guevara. 2004. Factors explaining the interest margin in the banking sectors of the European Union. Journal of Banking & Finance 28: 2259–81. [Google Scholar]

- Maudos, Joaquín, and Liliana Solís. 2009. The determinants of net interest income in the Mexican banking system: An integrated model. Journal of Banking & Finance 33: 1920–31. [Google Scholar]

- McShane, Robert Walter, and I. G. Sharpe. 1985. A time series/cross section analysis of the determinants of Australian trading bank loan/deposit interest margins: 1962–1981. Journal of Banking & Finance 9: 115–36. [Google Scholar]

- Peria, Maria Soledad Martinez, and Ashoka Mody. 2004. How foreign participation and market concentration impact bank spreads: Evidence from Latin America. Journal of Money, Credit and Banking 36: 511–37. [Google Scholar] [CrossRef]

- Pessarossi, Pierre, and Laurent Weill. 2015. Do capital requirements affect cost efficiency? evidence from China. Journal of Financial Stability 19: 119–27. [Google Scholar] [CrossRef]

- Poghosyan, Tigran. 2010. Re-examining the impact of foreign bank participation on interest margins in emerging markets. Emerging Markets Review 11: 390–403. [Google Scholar] [CrossRef]

- Poghosyan, Tigran. 2013. Financial intermediation costs in low income countries: The role of regulatory, institutional, and macroeconomic factors. Economic Systems 37: 92–110. [Google Scholar] [CrossRef]

- Rahman, Mohammed Mizanur, Badar Nadeem Ashraf, Changjun Zheng, and Munni Begum. 2017. Impact of cost efficiency on bank capital and the cost of financial intermediation: Evidence from BRICS countries. International Journal of Financial Studies 5: 32. [Google Scholar] [CrossRef]

- Rahman, Mohammed Mizanur, Changjun Zheng, Badar Nadeem Ashraf, and Mohammad Morshedur Rahman. 2018. Capital requirements, the cost of financial intermediation and bank risk-taking: Empirical evidence from Bangladesh. Research in International Business and Finance 44: 488–503. [Google Scholar] [CrossRef]

- Rahman, Mohammed Mizanur, Md Mominur Rahman, Mahfuzur Rahman, and Md Abdul Kaium Masud. 2021. The impact of trade openness on the cost of financial intermediation and bank performance: Evidence from BRICS countries. International Journal of Emerging Markets. [Google Scholar] [CrossRef]

- Rahman, Mohammed Mizanur, Munni Begum, Badar Nadeem Ashraf, and Md Abdul Kaium Masud. 2020. Does trade openness affect bank risk-taking behavior? Evidence from BRICS countries. Economies 8: 75. [Google Scholar] [CrossRef]

- Samargandi, Nahla, and Ali M. Kutan. 2016. Private credit spillovers and economic growth: Evidence from BRICS countries. Journal of International Financial Markets, Institutions and Money 44: 56–84. [Google Scholar] [CrossRef]

- Saunders, Anthony, and Liliana Schumacher. 2000. The determinants of bank interest rate margins: An international study. Journal of International Money and Finance 19: 813–32. [Google Scholar] [CrossRef]

- Schwaiger, Markus S., and David Liebeg. 2007. Determinants of Bank Interest Margins in Central and Eastern Europe. Financial Stability Report 14: 68–84. [Google Scholar]

- Sealey, Calvin W., Jr., and James T. Lindley. 1977. Inputs, outputs, and a theory of production and cost at depository financial institutions. The Journal of Finance 32: 1251–66. [Google Scholar] [CrossRef]

- Tan, Yong. 2016. The impacts of risk and competition on bank profitability in China. Journal of International Financial Markets, Institutions and Money 40: 85–110. [Google Scholar] [CrossRef]

- Tarus, Daniel K., Yonas B. Chekol, and Milcah Mutwol. 2012. Determinants of net interest margins of commercial banks in Kenya: A panel study. Procedia Economics and Finance 2: 199–208. [Google Scholar] [CrossRef]

- Valverde, Santiago Carbó, and Francisco Rodríguez Fernández. 2007. The determinants of bank margins in European banking. Journal of Banking & Finance 31: 2043–63. [Google Scholar]

- Williams, Barry. 2007. Factors determining net interest margins in Australia: Domestic and foreign banks. Financial Markets, Institutions & Instruments 16: 145–65. [Google Scholar]

- Zheng, Changjun, Mohammed Mizanur Rahman, Munni Begum, and Badar Nadeem Ashraf. 2017. Capital regulation, the cost of financial intermediation and bank profitability: Evidence from Bangladesh. Journal of Risk and Financial Management 10: 9. [Google Scholar] [CrossRef]

- Zhou, Kaiguo, and Michael C. S. Wong. 2008. The determinants of net interest margins of commercial banks in mainland China. Emerging Markets Finance and Trade 44: 41–53. [Google Scholar] [CrossRef]

| Variables | Symbol | Definition | Variable Reference | Data Source |

|---|---|---|---|---|

| Dependent Variables | ||||

| Net Interest Margin | NIM1 | Difference between interest income and interest expense over total earning assets | (Rahman et al. 2018) | BankFocus database |

| NIM2 | Difference between interest income and interest expense over total assets | (Rahman et al. 2018) | BankFocus | |

| Independent Control Variables | ||||

| Bank-Level | ||||

| Govt. securities | GOVS | Investment in govt. securities to total assets | Author’s Idea | BankFocus |

| Cost Inefficiency | CINEY | Use stochastic frontier 4.1 | (Rahman et al. 2021) | BankFocus |

| Operating Cost Ratio | OPCR | Operating expenses over total assets ratio | (Rahman et al. 2021) | BankFocus |

| Credit Risk | NPLTL | Non-performing loan to total loan ratio | (Rahman et al. 2021) | BankFocus |

| Credit Risk*SDint | NLMIR | NPL times SD of market interest rates | Author’s Calculation | BankFocus and Inter. Financial Stat. (IMF) |

| Capital Ratio | OETTA | Equity to total assets ratio | (Zheng et al. 2017) | BankFocus |

| Net Non-Interest Income Ratio | NNIR | Non-interest expense less non-interest revenue over total earning assets | (Rahman et al. 2017) | BankFocus |

| Opportunity Cost of Bank Reserves | OCR | Measured by the ratio of cash due from banks divided by total assets | Author’s Calculation | BankFocus |

| Size of Operations | LL | Logarithm of total loans | (Rahman et al. 2021) | BankFocus |

| Funding Strength | TLTD | Total loan to total deposit ratio | (Rahman et al. 2018) | BankFocus |

| Management Efficiency | CIR | Measured by the ratio of cost to income | (Rahman et al. 2017) | BankFocus |

| Industry-Level | ||||

| Hirschman-Herfindahl Index | HHI | Sum of square of market share is a proxy for market concentration variable | (Rahman et al. 2021) | BankFocus and Authors’ calculations |

| Country-Level | ||||

| Trilemma Index | TRMET | Composite of country scores in the area of Exchange Rate Stability, Monetary Independence, and Financial Openness4. For every measure, index ranges from 0 to 1 where a higher value indicates more Exchange Rate Stability, Monetary Independence, and Financial Openness | Author’s Idea | (Aizenman et al. 2010) |

| Market Openness | MKTOPN | Composite of country scores in the area of Trade Freedom, Investment Freedom, and Financial Freedom5. For every measure, index ranges from 0 to 1 where a higher value indicates more Trade Freedom, Investment Freedom, and Financial Freedom | Author’s Idea | Freedom_House (2017) |

| Regulatory-Level | ||||

| Capital Stringency | CAPR | CAPR is an index of required capital that accounts for both initial and overall capital stringency. The index ranges from 0 to 10 where a higher value indicates more stringent capital requirements for banks in a country | (Barth et al. 2013) | Bank Regulation and Supervision Database, World Bank; (Barth et al. 2013) |

| Activity Restrictions | ACTR | This variable score reflects the level of regulatory restrictiveness for bank participation in securities, insurance, real estate activities, and owning other firms. Variable ranges from 4 to 16, with higher values, indicating greater restrictiveness | (Barth et al. 2013) | Bank Regulation and Supervision Database, World Bank; (Barth et al. 2013) |

| Supervisory Power | SPR | SPR is an index measuring the power of supervisory agencies specifying the extent to which these authorities could take actions against bank and board management, shareholders, and bank auditors. Variable ranges from 0 to 14, with higher values, indicating more supervisory power | (Barth et al. 2013) | Bank Regulation and Supervision Database, World Bank; (Barth et al. 2013) |

| Institutional-Level | ||||

| Govt. Effectiveness | GVTETV | GVTETV is an index that reflects the perceptions of the quality of public services, the superiority of the civil service and the degree of its independence from political pressure, the quality of policy formulation and implementation, and the integrity of the government’s obligation to such policies. Variable ranges from −2.5 to 2.5, with higher values, indicating more Govt. Effectiveness | (Kaufmann et al. 2011) | (Kaufmann et al. 2011) |

| Rule of Law | ROL | ROL is an index that replicates the views of the extent to which peoples have confidence in and abide by the rules of society and in particular the quality of contract prosecution, property rights, the police, and the courts, as well as the possibility of crime and violence. Variable ranges from −2.5 to 2.5, with higher values, indicating more public-friendly law and enforcement | (Kaufmann et al. 2011) | (Kaufmann et al. 2011) |

| Macro-Level | ||||

| SD of Market Interest Rates | SDMIR | Annualized standard deviation of monthly average of daily money market interest rates for an individual country | Author’s Calculation | Inter. Financial Statistics (IMF), and Authors’ calculations |

| Inflation, Consumer Prices (annual %) | INF | Annual rate of inflation (%) | (Rahman et al. 2020) | World Development Indicators (WDI) |

| GDP growth (annual %) | GDP | Annual growth of GDP | (Rahman et al. 2020) | World Development Indicators (WDI) |

| 6VARIABLES | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 | 12 | 13 | 14 | 15 | 16 | 17 | 18 | 19 | 20 | 21 | 22 | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| NIM1 | (1) | 1 | |||||||||||||||||||||

| GOVS | (2) | 0.03 | 1 | ||||||||||||||||||||

| CINEY | (3) | 0.07 | 0.02 | 1 | |||||||||||||||||||

| NPLTL | (4) | 0.17 | 0.01 | 0.15 | 1 | ||||||||||||||||||

| NLMIR | (5) | 0.14 | 0.00 | 0.08 | 0.69 | 1 | |||||||||||||||||

| OETTA | (6) | 0.34 | 0.01 | −0.19 | 0.13 | 0.10 | 1 | ||||||||||||||||

| NNIR | (7) | 0.71 | 0.02 | 0.02 | 0.11 | 0.11 | 0.16 | 1 | |||||||||||||||

| OCR | (8) | −0.05 | −0.01 | −0.07 | −0.03 | −0.04 | −0.09 | −0.10 | 1 | ||||||||||||||

| LL | (9) | −0.28 | 0.01 | 0.033 | −0.06 | −0.09 | −0.52 | −0.22 | 0.06 | 1 | |||||||||||||

| TLTD | (10) | 0.00 | 0.00 | −0.02 | 0.00 | 0.01 | 0.01 | 0.01 | −0.02 | 0.00 | 1 | ||||||||||||

| CIR | (11) | 0.09 | −0.01 | −0.28 | 0.09 | 0.08 | 0.19 | 0.36 | −0.09 | −0.48 | 0.02 | 1 | |||||||||||

| HHI | (12) | −0.05 | 0.00 | 0.03 | 0.01 | −0.01 | −0.07 | −0.04 | 0.02 | 0.19 | 0.00 | −0.08 | 1 | ||||||||||

| TRMET | (13) | 0.01 | −0.02 | −0.32 | −0.07 | −0.14 | 0.13 | 0.03 | 0.04 | −0.21 | 0.00 | 0.17 | 0.04 | 1 | |||||||||

| MKTOPN | (14) | 0.05 | −0.01 | 0.02 | 0.05 | 0.13 | 0.02 | 0.04 | 0.01 | −0.07 | −0.01 | 0.02 | 0.04 | −0.11 | 1 | ||||||||

| CAPR | (15) | −0.02 | −0.02 | −0.08 | −0.01 | 0.04 | 0.05 | −0.01 | 0.00 | −0.10 | 0.01 | 0.09 | −0.05 | −0.12 | 0.05 | 1 | |||||||

| ACTR | (16) | −0.23 | 0.01 | 0.13 | −0.03 | −0.02 | −0.27 | −0.18 | 0.13 | 0.51 | −0.01 | −0.44 | 0.11 | −0.21 | −0.01 | −0.11 | 1 | ||||||

| SPR | (17) | 0.03 | 0.03 | 0.54 | 0.10 | 0.01 | −0.17 | −0.03 | −0.06 | 0.36 | −0.02 | −0.41 | 0.10 | −0.28 | 0.01 | −0.15 | 0.49 | 1 | |||||

| GVTETV | (18) | −0.16 | 0.01 | 0.20 | 0.02 | −0.06 | −0.16 | −0.12 | 0.15 | 0.45 | −0.01 | −0.26 | 0.14 | −0.06 | −0.01 | −0.01 | 0.34 | 0.31 | 1 | ||||

| ROL | (19) | −0.17 | 0.01 | 0.33 | 0.07 | −0.03 | −0.22 | −0.13 | 0.07 | 0.54 | −0.01 | −0.32 | 0.13 | −0.26 | −0.05 | 0.04 | 0.41 | 0.46 | 0.89 | 1 | |||

| SDMIR | (20) | 0.04 | 0.00 | −0.04 | 0.00 | 0.40 | 0.04 | 0.03 | −0.04 | −0.11 | 0.01 | 0.04 | −0.01 | −0.18 | 0.22 | 0.11 | −0.01 | −0.05 | −0.14 | −0.10 | 1 | ||

| INF | (21) | 0.15 | −0.01 | −0.20 | −0.01 | 0.20 | 0.20 | 0.12 | −0.07 | −0.45 | 0.02 | 0.28 | −0.05 | −0.02 | 0.43 | 0.24 | −0.40 | −0.29 | −0.47 | −0.54 | 0.37 | 1 | |

| GDP | (22) | −0.12 | 0.00 | 0.05 | −0.15 | −0.26 | −0.17 | −0.16 | 0.06 | 0.23 | −0.03 | −0.36 | 0.05 | 0.05 | −0.04 | −0.14 | 0.46 | 0.32 | 0.09 | 0.11 | −0.17 | −0.34 | 1 |

| MEAN | 0.062 | 0.025 | 0.250 | 0.049 | 0.001 | 0.173 | 0.032 | 0.067 | 5.48 | 0.793 | 0.719 | 0.002 | 1.33 | 1.39 | 6.60 | 8.51 | 9.12 | −0.17 | −0.55 | 0.014 | 8.10 | 3.68 | |

| S.D. | 0.057 | 0.038 | 0.238 | 0.081 | 0.001 | 0.133 | 0.059 | 0.072 | 2.75 | 2.95 | 0.29 | 0.02 | 0.20 | 0.225 | 1.30 | 1.91 | 2.18 | 0.447 | 0.478 | 0.016 | 3.77 | 4.39 | |

| MIN14 | −2.2 | 0.002 | 0.013 | 0.000 | 0.00 | −1.1 | −2.2 | 0.00 | −3.67 | 0.00 | 0.05 | 0.00 | 0.61 | 0.796 | 3.00 | 6.00 | 6.00 | −0.81 | −1.1 | 0.00 | −0.77 | −7.82 | |

| MAX | 0.859 | 0.25 | 1.77 | 1.25 | 0.022 | 0.992 | 0.903 | 0.821 | 14.42 | 25.91 | 8.40 | 0.735 | 2.32 | 2.55 | 9.00 | 15.00 | 14.00 | 2.43 | 1.89 | 0.207 | 21.46 | 15.24 | |

| OBS | 12,347 | 12,347 | 12,347 | 12,347 | 12,347 | 12,347 | 12,347 | 12,347 | 12,347 | 12,347 | 12,347 | ||||||||||||

| Variables | BGD | BRA | CHN | IND | KOR | MYS | PAK | RUS | SGP | ZAF |

|---|---|---|---|---|---|---|---|---|---|---|

| NIM1 | 0.0402 | 0.1033 | 0.0273 | 0.0322 | 0.0248 | 0.0254 | 0.0446 | 0.0672 | 0.0202 | 0.0645 |

| GOVS | 0.0230 | 0.0439 | 0.0278 | 0.01941 | 0.00553 | 0.01018 | 0.01284 | 0.02097 | 0.02824 | 0.03275 |

| CINEY | 0.1999 | 0.6808 | 0.2633 | 0.3394 | 0.2009 | 0.3187 | 0.3893 | 0.1565 | 0.2488 | 0.5083 |

| NPLTL | 0.0769 | 0.0881 | 0.0172 | 0.0454 | 0.0307 | 0.0571 | 0.1155 | 0.0429 | 0.0718 | 0.0628 |

| NLMIR | 0.0014 | 0.0010 | 0.00002 | 0.0011 | 0.0001 | 0.00003 | 0.0010 | 0.0007 | 0.0002 | 0.0003 |

| OETTA | 0.0765 | 0.1630 | 0.0861 | 0.0882 | 0.0813 | 0.1255 | 0.1502 | 0.2019 | 0.1665 | 0.1449 |

| NNIR | 0.0064 | 0.0593 | 0.0074 | 0.0072 | 0.0113 | 0.0054 | 0.0246 | 0.0367 | 0.0040 | 0.0050 |

| OCR | 0.0729 | 0.0153 | 0.1178 | 0.0511 | 0.0596 | 0.1417 | 0.0562 | 0.0657 | 0.0764 | 0.1364 |

| LL | 7.0496 | 6.4416 | 9.4795 | 7.9706 | 10.214 | 7.8112 | 6.2058 | 4.1805 | 8.5360 | 8.0142 |

| TLTD | 0.8548 | 0.82640 | 0.9440 | 0.56959 | 0.72130 | 0.90020 | 0.92021 | 0.71555 | 0.87902 | 0.77060 |

| CIR | 0.4906 | 0.6272 | 0.4092 | 0.4889 | 0.5945 | 0.5347 | 0.6890 | 0.8206 | 0.5315 | 0.5930 |

| HHI | 0.0040 | 0.0020 | 0.0033 | 0.0019 | 0.0038 | 0.0139 | 0.0156 | 0.0006 | 0.0265 | 0.0068 |

| TRMET | 1.3422 | 1.2008 | 1.4151 | 0.9588 | 1.4656 | 1.0989 | 1.0467 | 1.4013 | 2.0352 | 0.9945 |

| MKTOPN | 1.2689 | 1.3824 | 1.3199 | 1.4462 | 1.3374 | 1.3885 | 1.3857 | 1.3930 | 1.3271 | 1.3232 |

| CAPR | 5.7818 | 5.7101 | 4.4910 | 7.7877 | 7.1867 | 7.4171 | 7.9681 | 6.6903 | 6.9375 | 8.1073 |

| ACTR | 13.000 | 7.8309 | 12.789 | 11.0839 | 10.700 | 10.117 | 11.282 | 7.5270 | 9.8750 | 8.1631 |

| SPR | 11.109 | 13.424 | 10.721 | 10.2464 | 8.5933 | 11.126 | 13.106 | 7.8717 | 13.000 | 7.9227 |

| GVTETV | −0.774 | −0.078 | 0.1695 | −0.0611 | 1.1452 | 1.0287 | −0.717 | −0.359 | 2.2025 | 0.4259 |

| ROL | −0.775 | −0.233 | −0.389 | 0.0111 | 0.9690 | 0.5348 | −0.839 | −0.814 | 1.6961 | 0.1058 |

| SDMIR | 0.0223 | 0.0112 | 0.0012 | 0.0312 | 0.0020 | 0.0007 | 0.0086 | 0.0149 | 0.0021 | 0.0040 |

| INF | 7.2425 | 6.5368 | 2.6904 | 7.5814 | 1.9966 | 2.3688 | 7.6065 | 9.6417 | 2.2767 | 5.8616 |

| GDP | 6.1990 | 2.8491 | 8.5797 | 7.1576 | 3.4610 | 5.2102 | 4.2245 | 2.7272 | 5.7258 | 0.0645 |

| OBS | 197 | 1235 | 858 | 910 | 179 | 418 | 224 | 7914 | 134 | 278 |

| Variables | (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) |

|---|---|---|---|---|---|---|---|---|

| NIM1 | ||||||||

| Bank-Level | ||||||||

| GOVS | 0.001 ** | 0.002 *** | 0.001 *** | 0.001 ** | 0.002 *** | 0.001 *** | 0.002 ** | 0.003 *** |

| CINEY | 0.051 *** | 0.053 *** | 0.055 *** | 0.051 *** | 0.045 *** | 0.051 *** | 0.041 *** | 0.043 *** |

| NPLTL | 0.018 ** | 0.021 *** | 0.018 ** | 0.018 ** | 0.020 *** | 0.017 ** | 0.019 ** | 0.021 *** |

| NLMIR | −0.216 | −0.369 | −0.210 | −0.216 | −0.264 | −0.188 | −0.307 | −0.263 |

| OETTA | 0.105 *** | 0.106 *** | 0.105 *** | 0.105 *** | 0.105 *** | 0.105 *** | 0.106 *** | 0.105 *** |

| NNIR | 0.584 *** | 0.584 *** | 0.584 *** | 0.584 *** | 0.584 *** | 0.584 *** | 0.584 *** | 0.583 *** |

| OCR | 0.047 *** | 0.048 *** | 0.047 *** | 0.047 *** | 0.048 *** | 0.048 *** | 0.047 *** | 0.046 *** |

| LL | −0.001 * | −0.001 | −0.001 | −0.001 * | −0.001 | −0.001 ** | −0.001 ** | −0.001 |

| TLTD | −0.00001 | −0.00001 | −0.00001 | −0.00002 | −0.00002 | −0.00001 | −0.00002 | −0.00001 |

| CIR | −0.052 *** | −0.053 *** | −0.053 *** | −0.053 *** | −0.053 *** | −0.054 *** | −0.054 *** | −0.053 *** |

| Industry−Level | ||||||||

| HHI | −0.016 | −0.016 | −0.016 | −0.016 | −0.016 | −0.017 | −0.014 | -0.016 |

| Country-Level | ||||||||

| TRMET | −0.014 *** | |||||||

| MKTOPN | 0.002 * | |||||||

| Regulatory-Level | ||||||||

| CAPR | −0.001 * | |||||||

| ACTR | 0.001 ** | |||||||

| SPR | −0.001 ** | |||||||

| Institutional-Level | ||||||||

| GVTETV | −0.009 *** | |||||||

| ROL | −0.013 *** | |||||||

| Macro-Level | ||||||||

| SDMIR | 0.054 ** | 0.059 *** | 0.052 ** | 0.054 ** | 0.051 ** | 0.055 ** | 0.038 * | 0.061 *** |

| INF | 0.00003 | 0.00002 | 0.00002 | 0.00002 | 0.0002 | 0.00003 | 0.00002 | 0.00002 |

| GDP | −0.0001 | −0.0002 ** | −0.0001 | −0.0001 * | −0.0001 | −0.0001 * | −0.0001 * | −0.0001 |

| Constant | 0.050 *** | 0.068 *** | 0.047 *** | 0.051 *** | 0.042 *** | 0.058 *** | 0.056 *** | 0.046 *** |

| Country dummies | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Time dummies | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| R-squared | 0.566 | 0.568 | 0.567 | 0.566 | 0.567 | 0.567 | 0.567 | 0.567 |

| F-statistics (p-value) | 439.70 (0.00) | 487.68 (0.00) | 484.11 (0.00) | 483.65 (0.00) | 484.53 (0.00) | 484.46 (0.00) | 485.57 (0.00) | 485.66 (0.00) |

| Hausman Test, χ2 (p-value) | 473.32 (0.00) | 496.93 (0.00) | 476.85 (0.00) | 486.97 (0.00) | 438.44 (0.00) | 466.25 (0.00) | 456.55 (0.00) | 395.32 (0.00) |

| White Test, χ2 (p-value) | 185.75 (0.00) | 181.90 (0.00) | 171.02 (0.00) | 163.42 (0.00) | 174.64 (0.00) | 172.81 (0.00) | 160.77 (0.00) | 171.29 (0.00) |

| Observations | 12,347 | 12,347 | 12,347 | 12,347 | 12,347 | 12,347 | 12,347 | 12,347 |

| No of Banks | 1335 | 1335 | 1335 | 1335 | 1335 | 1335 | 1335 | 1335 |

| Variables | (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) |

|---|---|---|---|---|---|---|---|---|

| NIM2 | ||||||||

| Bank-level | ||||||||

| GOVS | 0.004 *** | 0.003 *** | 0.002 *** | 0.002 *** | 0.003 *** | 0.002 *** | 0.003 *** | 0.004 *** |

| OPCR | 0.016 *** | 0.017 *** | 0.018 *** | 0.016 *** | 0.016 *** | 0.016 *** | 0.017 *** | 0.016 *** |

| NPLTL | 0.003 | 0.005 | 0.002 | 0.003 | 0.005 | 0.002 | 0.004 | 0.007 |

| NLMIR | −0.252 | −0.360 | −0.245 | −0.252 | −0.351 | −0.242 | −0.372 | −0.376 |

| OETTA | 0.076 *** | 0.076 *** | 0.076 *** | 0.075 *** | 0.076 *** | 0.076 *** | 0.076 *** | 0.075 *** |

| NNIR | 0.426 *** | 0.426 *** | 0.426 *** | 0.426 *** | 0.426 *** | 0.426 *** | 0.426 *** | 0.425 *** |

| OCR | 0.021 *** | 0.021 *** | 0.021 *** | 0.022 *** | 0.019 *** | 0.021 *** | 0.021 *** | 0.022 *** |

| LL | −0.001 *** | −0.001 *** | −0.001 *** | −0.001 *** | −0.001 * | −0.001 *** | −0.001 *** | −0.001** |

| TLTD | −0.00001 | −0.00001 | −0.00001 | −0.00002 | −0.00001 | −0.00001 | −0.00001 | −0.00002 |

| CIR | −0.045 *** | −0.045 *** | −0.045 *** | −0.045 *** | −0.045 *** | −0.045 *** | −0.045 *** | −0.044 *** |

| Industry-Level | ||||||||

| HHI | −0.014 | −0.014 | −0.014 | −0.013 | −0.014 | −0.014 | −0.012 | −0.015 |

| Country-Level | ||||||||

| TRMET | −0.010 *** | |||||||

| MKTOPN | 0.002 ** | |||||||

| Regulatory-level | ||||||||

| CAPR | 0.001 * | |||||||

| ACTR | 0.002 *** | |||||||

| SPR | −0.001 ** | |||||||

| Institutional-Level | ||||||||

| GVTETV | −0.009 *** | |||||||

| ROL | −0.023 *** | |||||||

| Macro-Level | ||||||||

| SDMIR | 0.039 ** | 0.042 ** | 0.038 ** | 0.040 ** | 0.036 ** | 0.040 ** | 0.025 | 0.053 *** |

| INF | 0.00004 | 0.00003 | 0.00004 | 0.00003 | 0.00004 | 0.00004 | 0.00003 | 0.0001 * |

| GDP | −0.0003 ** | −0.0002 ** | −0.0003 ** | −0.0003 ** | −0.0003 ** | −0.0004 ** | −0.0004 ** | −0.0002 * |

| Constant | 0.061 *** | 0.074 *** | 0.058 *** | 0.060 *** | 0.046 *** | 0.064 *** | 0.064 *** | 0.049 *** |

| Country dummies | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Time dummies | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| R-squared | 0.538 | 0.539 | 0.538 | 0.538 | 0.539 | 0.538 | 0.539 | 0.542 |

| F-statistics (p-value) | 448.81 (0.00) | 402.06 (0.00) | 399.54 (0.00) | 398.97 (0.00) | 402.01 (0.00) | 398.94 (0.00) | 401.66 (0.00) | 408.47 (0.00) |

| Observations | 12,347 | 12,347 | 12,347 | 12,347 | 12,347 | 12,347 | 12,347 | 12,347 |

| No of Banks | 1335 | 1335 | 1335 | 1335 | 1335 | 1335 | 1335 | 1335 |

| Variables | (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) |

|---|---|---|---|---|---|---|---|---|

| NIM1 | ||||||||

| Bank-level | ||||||||

| GOVS | 0.002 *** | 0.002 *** | 0.003 *** | 0.003 | 0.002 *** | 0.003 *** | 0.002 *** | 0.003 *** |

| CINEY | 0.052 *** | 0.055 *** | 0.056 *** | 0.053 *** | 0.048 *** | 0.052 *** | 0.041 *** | 0.045 *** |

| NPLTL | 0.019 *** | 0.024 *** | 0.019 *** | 0.020 *** | 0.020 *** | 0.018** | 0.020 *** | 0.021 *** |

| NLMIR | −0.254 | −0.485 | −0.249 | −0.264 | −0.273 | −0.226 | −0.369 | −0.274 |

| OETTA | 0.105 *** | 0.105 *** | 0.105 *** | 0.105 *** | 0.105 *** | 0.105 *** | 0.105 *** | 0.105 *** |

| NNIR | 0.584 *** | 0.583 *** | 0.583 *** | 0.584 *** | 0.584 *** | 0.584 *** | 0.584 *** | 0.583 *** |

| OCR | 0.047 *** | 0.049 *** | 0.047 *** | 0.048 *** | 0.048 *** | 0.048 *** | 0.048 *** | 0.046 *** |

| LL | −0.001 ** | −0.001 * | −0.001 * | −0.001 ** | −0.001 | −0.001 *** | −0.001 *** | −0.001* |

| TLTD | −0.00002 | −0.00001 | −0.00001 | −0.00002 | −0.00001 | −0.00002 | −0.00002 | −0.00002 |

| CIR | −0.053 *** | −0.053 *** | −0.053 *** | −0.053 *** | −0.053 *** | −0.054 *** | −0.053 *** | −0.053 *** |

| Industry-Level | ||||||||

| HHI | −0.016 | −0.016 | −0.016 | −0.016 | −0.016 | −0.017 | −0.013 | −0.016 |

| Crisis dummy | 0.002 ** | 0.003 *** | 0.002 *** | 0.002 *** | 0.002 ** | 0.002 *** | 0.002 *** | 0.002 *** |

| Country-Level | ||||||||

| TRMET | −0.018 *** | |||||||

| MKTOPN | 0.003 ** | |||||||

| Regulatory- level | ||||||||

| CAPR | −0.001 * | |||||||

| ACTR | 0.002 *** | |||||||

| SPR | −0.001 ** | |||||||

| Institutional-Level | ||||||||

| GVTETV | −0.010 *** | |||||||

| ROL | −0.011 *** | |||||||

| Macro-Level | ||||||||

| SDMIR | 0.042 * | 0.038 * | 0.040 * | 0.038 * | 0.044 * | 0.043 * | 0.021 | 0.054 ** |

| INF | 0.00003 | 0.0002 ** | 0.00003 | 0.00004 | 0.00004 | 0.00003 | 0.00003 | 0.00003 |

| GDP | −0.0001 | −0.0002 ** | −0.0001 | −0.0001 | −0.0002 | −0.0001 ** | −0.0001 * | −0.0001 |

| Constant | 0.051 *** | 0.074 *** | 0.047 *** | 0.053 *** | 0.045 *** | 0.059 *** | 0.057 *** | 0.046 *** |

| Country dummies | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Time dummies | No | No | No | No | No | No | No | No |

| R-squared | 0.567 | 0.569 | 0.567 | 0.567 | 0.567 | 0.567 | 0.568 | 0.567 |

| F-statistics (p-value) | 784.64 (0.00) | 741.28 (0.00) | 736.07 (0.00) | 735.81 (0.00) | 735.77 (0.00) | 736.37 (0.00) | 737.87 (0.00) | 736.66 (0.00) |

| Observations | 12,347 | 12,347 | 12,347 | 12,347 | 12,347 | 12,347 | 12,347 | 12,347 |

| No of Banks | 1335 | 1335 | 1335 | 1335 | 1335 | 1335 | 1335 | 1335 |

| Variables | Dropped (GOVS) | Dropped (GOVS) | Dropped (TRMET) | Dropped (MKTOPN) | CINEY (First Stage) | NIM1 (Second Stage) |

|---|---|---|---|---|---|---|

| Endogeneity test: Instrumental variable regressions | ||||||

| (1) | (2) | (3) | (4) | (5) | (6) | |

| CINEY | 0.053 *** | 0.051 *** | 0.052 *** | 0.051 *** | 0.051 *** | |

| OPCR | 0.006 *** | |||||

| GOVS | 0.002 *** | 0.003 *** | −0.001 * | 0.002 *** | ||

| TRMET | −0.014 *** | |||||

| MKTOPN | 0.002* | |||||

| NPLTL | 0.021 *** | 0.018 ** | 0.018 ** | 0.018 ** | −0.067 *** | 0.018 ** |

| NLMIR | −0.370 | −0.210 | −0.216 | −0.216 | 3.285 *** | −0.216 |

| OETTA | 0.106 *** | 0.106 *** | 0.105 *** | 0.105 *** | −0.001 | 0.105 *** |

| NNIR | 0.584 *** | 0.584 *** | 0.584 *** | 0.584 *** | 0.005 | 0.584 *** |

| OCR | 0.048 *** | 0.047 *** | 0.047 *** | 0.047 *** | −0.019 *** | 0.047 *** |

| LL | −0.001 | −0.001 | −0.001 * | −0.001 * | −0.005 *** | −0.001 * |

| TLTD | −0.00002 | −0.00002 | −0.00001 | −0.00001 | 0.00004 | −0.00001 |

| CIR | −0.053 *** | −0.053 *** | −0.053 *** | −0.053 *** | −0.006 *** | −0.053 *** |

| HHI | −0.016 | −0.016 | −0.016 | −0.016 | 0.066 *** | −0.016 |

| SDMIR | 0.059 *** | 0.052 ** | 0.055 ** | 0.054 ** | −0.122 *** | 0.054 ** |

| INF | 0.00002 | 0.00003 | 0.00001 | 0.00003 | 0.00004 | 0.00003 |

| GDP | −0.0002 ** | −0.0001 | −0.0001 | −0.0001 | −0.0002 | −0.0002 |

| Constant | 0.068 *** | 0.047 *** | 0.051 *** | 0.050 *** | 0.284 *** | 0.050 *** |

| Country dummies | Yes | Yes | Yes | Yes | Yes | Yes |

| Time dummies | Yes | Yes | Yes | Yes | Yes | Yes |

| R-squared | 0.547 | 0.559 | 0.552 | 0.557 | 0.197 | 0.566 |

| F-statistics (p-value) | 493.88 (0.00) | 510.02 (0.00) | 498.92 (0.00) | 469.70 (0.00) | 470.85 (0.00) | 483.70 (0.00) |

| Observations | 12,347 | 12,347 | 12,347 | 12,347 | 12,347 | 12,347 |

| No of Banks | 1335 | 1335 | 1335 | 1335 | 1335 | 1335 |

| Variables | (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) |

|---|---|---|---|---|---|---|---|---|

| NIM1 | ||||||||

| Bank-Level | ||||||||

| GOVS | 0.001 ** | 0.001 ** | 0.002 ** | 0.002 ** | 0.002 ** | 0.001 ** | 0.002 ** | 0.001 ** |

| CINEY | 0.057 *** | 0.061 *** | 0.062 *** | 0.058 *** | 0.052 *** | 0.059 *** | 0.044 *** | 0.050 *** |

| NPLTL | 0.006 | 0.009 | 0.006 | 0.006 | 0.007 | 0.003 | 0.007 | 0.008 |

| NLMIR | 0.269 | 0.138 | 0.290 | 0.268 | 0.231 | 0.337 | 0.173 | 0.230 |

| OETTA | 0.104 *** | 0.105 *** | 0.104 *** | 0.104 *** | 0.104 *** | 0.104 *** | 0.104 *** | 0.104 *** |

| NNIR | 0.596 *** | 0.596 *** | 0.595 *** | 0.596 *** | 0.595 *** | 0.596 *** | 0.596 *** | 0.595 *** |

| OCR | 0.048 *** | 0.049 *** | 0.048 *** | 0.048 *** | 0.049 *** | 0.050 *** | 0.049 *** | 0.048 *** |

| LL | −0.001 * | −0.001 | −0.001 | −0.001 | −0.001 | −0.001 ** | −0.001 ** | −0.001 |

| TLTD | −0.00001 | −0.00001 | −0.00002 | −0.00002 | −0.00001 | −0.00001 | −0.00001 | −0.00001 |

| CIR | −0.062 *** | −0.062 *** | −0.062 *** | −0.062 *** | −0.062 *** | −0.064 *** | −0.063 *** | −0.062 *** |

| Industry-Level | ||||||||

| HHI | 0.038 | 0.043 | 0.038 | 0.038 | 0.038 | 0.033 | 0.044 | 0.036 |

| Country-Level | ||||||||

| TRMET | −0.019 *** | |||||||

| MKTOPN | 0.003 ** | |||||||

| Regulatory-Level | ||||||||

| CAPR | −0.002 * | |||||||

| ACTR | 0.001 ** | |||||||

| SPR | −0.001 *** | |||||||

| Institutional-Level | ||||||||

| GVTETV | −0.010 *** | |||||||

| ROL | −0.010 *** | |||||||

| Macro-Level | ||||||||

| SDMIR | 0.036 | 0.043 * | 0.034 | 0.035 | 0.033 | 0.037 | 0.017 | 0.042 * |

| INF | 0.00004 | 0.0001 * | 0.0001 | 0.0001 | 0.00004 | 0.0001 | −0.00004 | −0.00004 |

| GDP | −0.0001 | 0.0001 | −0.0002 | −0.0002 | −0.0001 | 0.0003 | 0.0003 | −0.0001 |

| Constant | 0.058 *** | 0.082 *** | 0.054 *** | 0.059 *** | 0.053 *** | 0.072 *** | 0.065 *** | 0.054 *** |

| Country dummies | No | No | No | No | No | No | No | No |

| Time dummies | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| R-squared | 0.576 | 0.577 | 0.576 | 0.584 | 0.575 | 0.572 | 0.579 | 0.571 |

| F-statistics (p-value) | 497.45 (0.00) | 449.85 (0.00) | 444.88 (0.00) | 444.25 (0.00) | 444.56 (0.00) | 446.38 (0.00) | 446.40 (0.00) | 445.28 (0.00) |

| Observations | 9382 | 9382 | 9382 | 9382 | 9382 | 9382 | 9382 | 9382 |

| No of Banks | 1136 | 1136 | 1136 | 1136 | 1136 | 1136 | 1136 | 1136 |

| Variables | (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) |

|---|---|---|---|---|---|---|---|---|

| NIM1 | ||||||||

| Bank-Level | ||||||||

| GOVS | 0.008 * | 0.007 * | 0.008 ** | 0.008 * | 0.007 ** | 0.006 * | 0.005 ** | 0.006 * |

| CINEY | 0.040 *** | 0.039 *** | 0.041 *** | 0.037 *** | 0.037 *** | 0.040 *** | 0.041 *** | 0.035 *** |

| NPLTL | 0.042 *** | 0.041 *** | 0.043 *** | 0.041 *** | 0.043 *** | 0.042 *** | 0.042 *** | 0.042 *** |

| NLMIR | 0.543 | 0.562 | 0.469 | 0.551 | 0.493 | 0.542 | 0.555 | 0.526 |

| OETTA | 0.117 *** | 0.117 *** | 0.117 *** | 0.116 *** | 0.117 *** | 0.117 *** | 0.117 *** | 0.116 *** |

| NNIR | 0.987 *** | 0.987 *** | 0.987 *** | 0.987 *** | 0.987 *** | 0.987 *** | 0.987 *** | 0.986 *** |

| OCR | 0.023 ** | 0.023 ** | 0.023 ** | 0.022 ** | 0.025 *** | 0.023 ** | 0.023 ** | 0.023 ** |

| LL | −0.003 *** | −0.003 *** | −0.002 *** | −0.003 *** | −0.003 *** | −0.003 *** | −0.003 *** | −0.003 *** |

| TLTD | −0.00002 | −0.00003 | −0.00004 | −0.00004 | −0.00003 | −0.00003 | −0.00002 | −0.00002 |

| CIR | −0.053 *** | −0.053 *** | −0.053 *** | −0.053 *** | −0.053 *** | −0.053 *** | −0.053 *** | −0.053 *** |

| Industry-Level | ||||||||

| HHI | −0.038 ** | −0.038 ** | −0.039 ** | −0.038 ** | −0.039 ** | −0.038 ** | −0.038 ** | −0.038 ** |

| Country-Level | ||||||||

| TRMET | −0.001 ** | |||||||

| MKTOPN | 0.004 ** | |||||||

| Regulatory-Level | ||||||||

| CAPR | −0.001 * | |||||||

| ACTR | 0.001 ** | |||||||

| SPR | −0.003 ** | |||||||

| Institutional-Level | ||||||||

| GVTETV | −0.002 * | |||||||

| ROL | −0.006 * | |||||||

| Macro-Level | ||||||||

| SDMIR | −0.006 | −0.007 | −0.007 | −0.003 | −0.006 | −0.006 | −0.004 | −0.003 |

| INF | 0.00002 | 0.00002 | 0.00001 | 0.00001 | 0.00001 | 0.00001 | −0.00001 | −0.00001 |

| GDP | −0.0001 | −0.0002 | −0.0002 | −0.0001 | −0.0002 | −0.0001 | −0.0001 | −0.0001 |

| Constant | 0.046 *** | 0.045 *** | 0.036 *** | 0.045 *** | 0.039 *** | 0.046 *** | 0.045 *** | 0.047 *** |

| Country dummies | No | No | No | No | No | No | No | No |

| Time dummies | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| R-squared | 0.874 | 0.875 | 0.848 | 0.847 | 0.849 | 0.842 | 0.857 | 0.846 |

| F-statistics (p-value) | 937.25 (0.00) | 954.46 (0.00) | 956.70 (0.00) | 955.88 (0.00) | 955.38 (0.00) | 949.40 (0.00) | 954.49 (0.00) | 955.63 (0.00) |

| Observations | 3715 | 3715 | 3715 | 3715 | 3715 | 3715 | 3715 | 3715 |

| No of Banks | 578 | 578 | 578 | 578 | 578 | 578 | 578 | 578 |

| Variables | (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) |

|---|---|---|---|---|---|---|---|---|

| NIM1 | ||||||||

| Bank-Level | ||||||||

| GOVS | 0.0001 *** | 0.0001 *** | 0.0001 *** | 0.0001 *** | 0.0001 *** | 0.0001 *** | 0.0001 *** | 0.0001 *** |

| CINEY | 0.015 *** | 0.015 *** | 0.017 *** | 0.015 *** | 0.013 *** | 0.015 *** | 0.015 *** | 0.017 *** |

| NPLTL | 0.065 *** | 0.065 *** | 0.066 *** | 0.065 *** | 0.062 *** | 0.065 *** | 0.066 *** | 0.070 *** |

| NLMIR | −1.62 *** | −1.62 *** | −1.65 *** | −1.67 *** | −0.99** | −1.63 *** | −1.68 *** | −1.87 *** |

| OETTA | 0.081 *** | 0.081 *** | 0.081 *** | 0.082 *** | 0.081 *** | 0.081 *** | 0.084 *** | 0.083 *** |

| NNIR | 0.714 *** | 0.714 *** | 0.714 *** | 0.713 *** | 0.715 *** | 0.714 *** | 0.713 *** | 0.713 *** |

| OCR | 0.031 *** | 0.031 *** | 0.031 *** | 0.031 *** | 0.038 *** | 0.030 *** | 0.036 *** | 0.033 *** |

| LL | −0.003 *** | −0.003 *** | −0.003 *** | −0.003 *** | −0.002 *** | −0.003 *** | −0.003 *** | −0.003 *** |

| TLTD | −0.00003 | −0.00004 | −0.00002 | −0.00004 | −0.00003 | −0.00003 | −0.00003 | −0.00002 |

| CIR | −0.058 *** | −0.058 *** | −0.058 *** | −0.058 *** | −0.062 *** | −0.058 *** | −0.058 *** | −0.059 *** |

| Industry-Level | ||||||||

| HHI | −0.005 | −0.005 | −0.003 | −0.008 | −0.000 | −0.004 | 0.007 | 0.004 |

| Country-Level | ||||||||

| TRMET | −0.001 *** | |||||||

| MKTOPN | 0.005 *** | |||||||

| Regulatory-Level | ||||||||

| CAPR | −0.001 *** | |||||||

| ACTR | 0.004 *** | |||||||

| SPR | −0.003 ** | |||||||

| Institutional-Level | ||||||||

| GVTETV | −0.008 *** | |||||||

| ROL | −0.009 *** | |||||||

| Macro-Level | ||||||||

| SDMIR | 0.028 | 0.028 | 0.033 | 0.031 | 0.079 *** | 0.029 | 0.034 | 0.057 ** |

| INF | 0.001 *** | 0.001 *** | 0.001 *** | 0.001 *** | 0.001 *** | 0.001 *** | 0.000 *** | 0.000 * |

| GDP | −0.003 *** | −0.003 *** | −0.002 *** | −0.002 *** | −0.002** | −0.003 *** | −0.002 *** | −0.002 *** |

| Constant | 0.072 *** | 0.072 *** | 0.077 *** | 0.077 *** | 0.104 *** | 0.073 *** | 0.071 *** | 0.067 *** |

| Country dummies | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Time dummies | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| R-squared | 0.630 | 0.630 | 0.620 | 0.631 | 0.640 | 0.630 | 0.633 | 0.634 |

| F-statistics (p-value) | 657.73 (0.00) | 673.77 (0.00) | 675.12 (0.00) | 675.79 (0.00) | 626.01 (0.00) | 673.87 (0.00) | 687.27 (0.00) | 690.90 (0.00) |

| Observations | 12,347 | 12,347 | 12,347 | 12,347 | 12,347 | 12,347 | 12,347 | 12,347 |

| No of Banks | 1335 | 1335 | 1335 | 1335 | 1335 | 1335 | 1335 | 1335 |

| Variables | (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) |

|---|---|---|---|---|---|---|---|---|

| NIM1 | ||||||||

| Bank-Level | ||||||||

| GOVS | 0.002 * | 0.001 ** | 0.002 * | 0.003 ** | 0.002 * | 0.002 * | 0.002 * | 0.003 ** |

| CINEY | 0.019 *** | 0.017 *** | 0.024 *** | 0.019 *** | 0.020 *** | 0.024 *** | 0.021 *** | 0.023 *** |

| NPLTL | 0.020 *** | 0.021 *** | 0.020 *** | 0.020 *** | 0.019 *** | 0.021 *** | 0.021 *** | 0.027 *** |

| NLMIR | −0.318 | −0.375 | −0.323 | −0.321 | −0.165 | −0.334 | −0.299 | −0.547 |

| OETTA | 0.095 *** | 0.095 *** | 0.095 *** | 0.095 *** | 0.095 *** | 0.095 *** | 0.096 *** | 0.097 *** |

| NNIR | 0.604 *** | 0.604 *** | 0.604 *** | 0.605 *** | 0.605 *** | 0.605 *** | 0.604 *** | 0.603 *** |

| OCR | 0.033 *** | 0.033 *** | 0.033 *** | 0.033 *** | 0.035 *** | 0.034 *** | 0.036 *** | 0.036 *** |

| LL | −0.003 *** | −0.003 *** | −0.003 *** | −0.003 *** | −0.003 *** | −0.003 *** | −0.003 *** | −0.002 *** |

| TLTD | −0.00002 | −0.00001 | −0.00002 | −0.00001 | −0.00001 | −0.00001 | −0.00002 | −0.00002 |

| CIR | −0.053 *** | −0.052 *** | −0.053 *** | −0.053 *** | 0.054 *** | −0.054 *** | −0.053 *** | −0.053 *** |

| Industry-Level | ||||||||

| HHI | −0.016 | −0.016 | −0.016 | −0.017 | −0.012 | −0.016 | −0.014 | −0.011 |

| Country-Level | ||||||||

| TRMET | −0.006 ** | |||||||

| MKTOPN | 0.001 * | |||||||

| Regulatory-Level | ||||||||

| CAPR | −0.0002 ** | |||||||

| ACTR | −0.002 *** | |||||||

| SPR | −0.001 *** | |||||||

| Institutional-Level | ||||||||

| GVTETV | −0.007 *** | |||||||

| ROL | −0.014 *** | |||||||

| Macro-Level | ||||||||

| SDMIR | 0.040 * | 0.040 * | 0.041 * | 0.040 * | 0.053 ** | 0.046 ** | 0.052 ** | 0.058 *** |

| INF | 0.00002 | 0.00001 | 0.00001 | 0.00002 | 0.0002 * | 0.0003 ** | 0.00001 | 0.00002 |

| GDP | −0.0002 | −0.0001 | −0.0001 | −0.0001 | −0.0002 | −0.0001 | −0.0002 | −0.0002 ** |

| Constant | 0.070 *** | 0.079 *** | 0.071 *** | 0.071 *** | 0.085 *** | 0.079 *** | 0.067 *** | 0.059 *** |

| Country dummies | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Time dummies | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| R-squared | 0.626 | 0.622 | 0.623 | 0.6199 | 0.632 | 0.623 | 0.630 | 0.620 |

| Wald Chi2 (p-value) | 14,750.66 29, (0.00) | 14,763.58 30, (0.00) | 14,750.63 30, (0.00) | 14,753.67 30, (0.00) | 14,876.41 30, (0.00) | 14,792.78 30, (0.00) | 14,811.24 30, (0.00) | 14,943.45 30, (0.00) |

| Observations | 12,347 | 12,347 | 12,347 | 12,347 | 12,347 | 12,347 | 12,347 | 12,347 |

| No of Banks | 1335 | 1335 | 1335 | 1335 | 1335 | 1335 | 1335 | 1335 |

| Variables | (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) |

|---|---|---|---|---|---|---|---|---|

| NIM1 | ||||||||

| NIM1(−1) | 0.042 *** | 0.046 *** | 0.041 *** | 0.037 *** | 0.039 *** | 0.047 *** | 0.042 *** | 0.037 *** |

| Bank-Level | ||||||||

| GOVS | 0.004 | 0.005 * | 0.004 * | 0.002 ** | 0.004 * | 0.005 * | 0.004 | 0.002 * |

| CINEY | 0.028 *** | 0.029 *** | 0.033 *** | 0.031 *** | 0.023 *** | 0.027 *** | 0.024 *** | 0.028 *** |

| NPLTL | 0.045 *** | 0.041 *** | 0.033 *** | 0.039 *** | 0.048 *** | 0.051 *** | 0.041 *** | 0.039 *** |

| NLMIR | −0.412 | −0.396 | −0.463 | −0.431 | −0.298 | −0.387 | −0.375 | −0.389 |

| OETTA | 0.059 *** | 0.046 *** | 0.042 *** | 0.049 *** | 0.059 *** | 0.048 *** | 0.049 *** | 0.057 *** |

| NNIR | 0.325 ** | 0.350 * | 0.369 * | 0.349 ** | 0.325 *** | 0.397 *** | 0.304 ** | 0.303 * |

| OCR | 0.058 ** | 0.052 * | 0.049 * | 0.043 | 0.046 * | 0.047 * | 0.048 ** | 0.049 |

| LL | −0.002 | −0.004 | −0.003 | −0.005 | −0.002 | −0.004 | −0.003 | −0.005 |

| TLTD | −0.00002 | −0.00001 | −0.00002 | −0.00001 | −0.00001 | −0.00001 | −0.00001 | −0.00002 |

| CIR | −0.078 *** | −0.069 *** | −0.067 *** | −0.077 *** | 0.075 *** | −0.071 *** | −0.065 *** | −0.079 *** |

| Industry-Level | ||||||||

| HHI | −0.008 | −0.007 | −0.005 | −0.006 | −0.008 | −0.005 | −0.004 | −0.008 |

| Country-Level | ||||||||

| TRMET | −0.009 ** | |||||||

| MKTOPN | 0.003 | |||||||

| Regulatory-Level | ||||||||

| CAPR | −0.005 * | |||||||

| ACTR | −0.007 * | |||||||

| SPR | −0.002 *** | |||||||

| Institutional-Level | ||||||||

| GVTETV | −0.004 ** | |||||||

| ROL | −0.014 *** | |||||||

| Macro-Level | ||||||||

| SDMIR | 0.010 * | 0.011 * | 0.015 * | 0.019 | 0.027 ** | 0.031 | 0.037 * | 0.015 ** |

| INF | 0.00002 | 0.00002 | 0.00003 | 0.00003 | 0.00002 | 0.00001 | 0.00003 | 0.00002 |

| GDP | −0.0002 | −0.0002 | −0.0001 | −0.0002 | 0.0002 | 0.0002 | −0.0001 | −0.0001 |

| Constant | 0.090 *** | 0.089 *** | 0.094 *** | 0.057 *** | 0.091 *** | 0.089 *** | 0.078 *** | 0.067 *** |

| Country dummies | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Time dummies | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| R-squared | 0.245 | 0.198 | 0.289 | 0.314 | 0.095 | 0.287 | 0.452 | 0.389 |

| Sargan test (p-value) | 0.246 | 0.569 | 0.145 | 0.396 | 0.062 | 0.229 | 0.087 | 0.251 |

| AR(1) p-value | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 |

| AR(2) p-value | 0.214 | 0.198 | 0.105 | 0.254 | 0.049 | 0.175 | 0.067 | 0.179 |

| Instruments | 32 | 34 | 34 | 35 | 34 | 35 | 35 | 34 |

| Observations | 12,347 | 12,347 | 12,347 | 12,347 | 12,347 | 12,347 | 12,347 | 12,347 |

| No of Banks | 1335 | 1335 | 1335 | 1335 | 1335 | 1335 | 1335 | 1335 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Rahman, M.M.; Rahman, M.; Masud, M.A.K. Determinants of the Cost of Financial Intermediation: Evidence from Emerging Economies. Int. J. Financial Stud. 2023, 11, 11. https://doi.org/10.3390/ijfs11010011

Rahman MM, Rahman M, Masud MAK. Determinants of the Cost of Financial Intermediation: Evidence from Emerging Economies. International Journal of Financial Studies. 2023; 11(1):11. https://doi.org/10.3390/ijfs11010011

Chicago/Turabian StyleRahman, Mohammed Mizanur, Mahfuzur Rahman, and Md. Abdul Kaium Masud. 2023. "Determinants of the Cost of Financial Intermediation: Evidence from Emerging Economies" International Journal of Financial Studies 11, no. 1: 11. https://doi.org/10.3390/ijfs11010011

APA StyleRahman, M. M., Rahman, M., & Masud, M. A. K. (2023). Determinants of the Cost of Financial Intermediation: Evidence from Emerging Economies. International Journal of Financial Studies, 11(1), 11. https://doi.org/10.3390/ijfs11010011