1. Introduction

Financial statements are tools to provide general information on the financial position, business results, and cash flow of an enterprise after a certain period of time (month, quarter, year). The users of financial statements are very diverse, from company managers, to investors, creditors, government authorities, employees, and others. By analyzing financial statements, users can make decisions relating to lending, investing, or issuing policies. Each person will make different decisions based on the usefulness of the information on the financial statements.

For that reason, governmental agencies have issued regulations regarding timely disclosure of financial statements. In Vietnam, these regulations are according to Circular No. 96/2020/TT-BTC dated 16 November 2020, guiding the disclosure of information on the stock market. Following these regulations, companies must disclose audited annual financial statements within 10 days from the day the auditing firm signs the audited reports but not exceeding 90 days from the end of the fiscal year. Particularly for listed public companies with consolidated financial statements, the State Securities Commission of Vietnam shall consider extending the time for publication provided the company’s written request, but no later than 100 days from the end of the financial year. Accordingly,

Vuran and Adiloglu (

2013) stated that, in Turkey, the time limit for submitting consolidated financial statements is 99 days and single financial statements is 71 days from the end of the financial year. Despite the issuance of such regulations, many companies listed on Hanoi Stock Exchange (HSX) and Ho Chi Minh City Stock Exchange (HOSE) in Vietnam request for late submission with justifications including complicated business operations, obstacles in creating consolidated reports, and having many subsidiaries (

Lien 2016;

Suong 2018).

Many scholars both in Vietnam and other countries around the world have been interested in the factors affecting the publication of annual financial statements for decades. Research has been conducted in both developed and developing countries. Prior to 2000, there were studies by

Ashton et al. (

1987) in the United States,

Ashton et al. (

1989) in Canada, and

Carslaw and Kaplan (

1991) in New Zealand. After 2000, this topic continued to attract the attention of scholars in different countries:

Haw et al. (

2000) in China,

Turel (

2010) in Turkey,

Khasharmeh and Aljifri (

2010) in Bahraini and the United Arab Emirates (UAE),

Modugu et al. (

2012) in Nigeria,

Vuran and Adiloglu (

2013) in Turkey,

Sakka and Jarboui (

2016) in Tunisia,

Khuong and Vy (

2017),

Ha et al. (

2018) in Vietnam,

Lukason and Camacho-Miñano (

2019) in Estonia, and

Dewi et al. (

2019) and

Raihani et al. (

2019) in Indonesia. Research results are quite diverse in both research methods and research results. There is no consensus on the direction of effects on the time of publication of annual financial statements. Research by

Ha et al. (

2018) suggested that financial leverage has no effect on the time of publication but the study of

Khasharmeh and Aljifri (

2010) with the research sample at Bharain and study of

Modugu et al. (

2012) argued that companies with a high percentage of debt to equity are likely to publish reports earlier than companies with a low ratio to reduce negotiation costs on loan contracts.

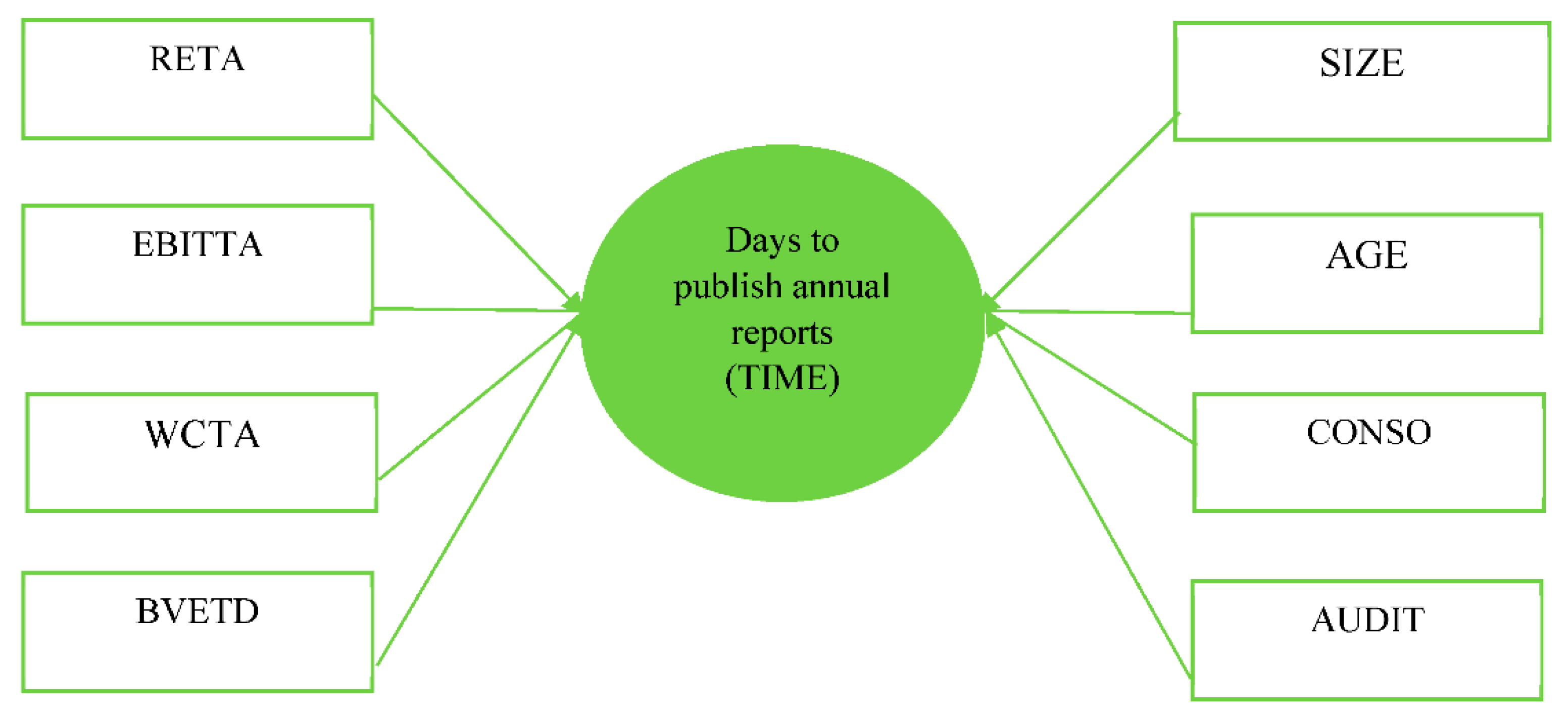

Vietnam is a developing country in Asia; accordingly, Vietnamese enterprises continually seek to receive foreign investment for development. Therefore, transparency and timely disclosure of financial information to investors is essential. Companies, especially those listed on the stock market, need to better serve the demands of accounting information to investors in time. Therefore, the study of “Determinants of time for publication annual reports: Empirical evidence from non-financial listed companies in Vietnam” is essential both in theory and practice because this topic has contributed to literature on timeliness of financial reports.

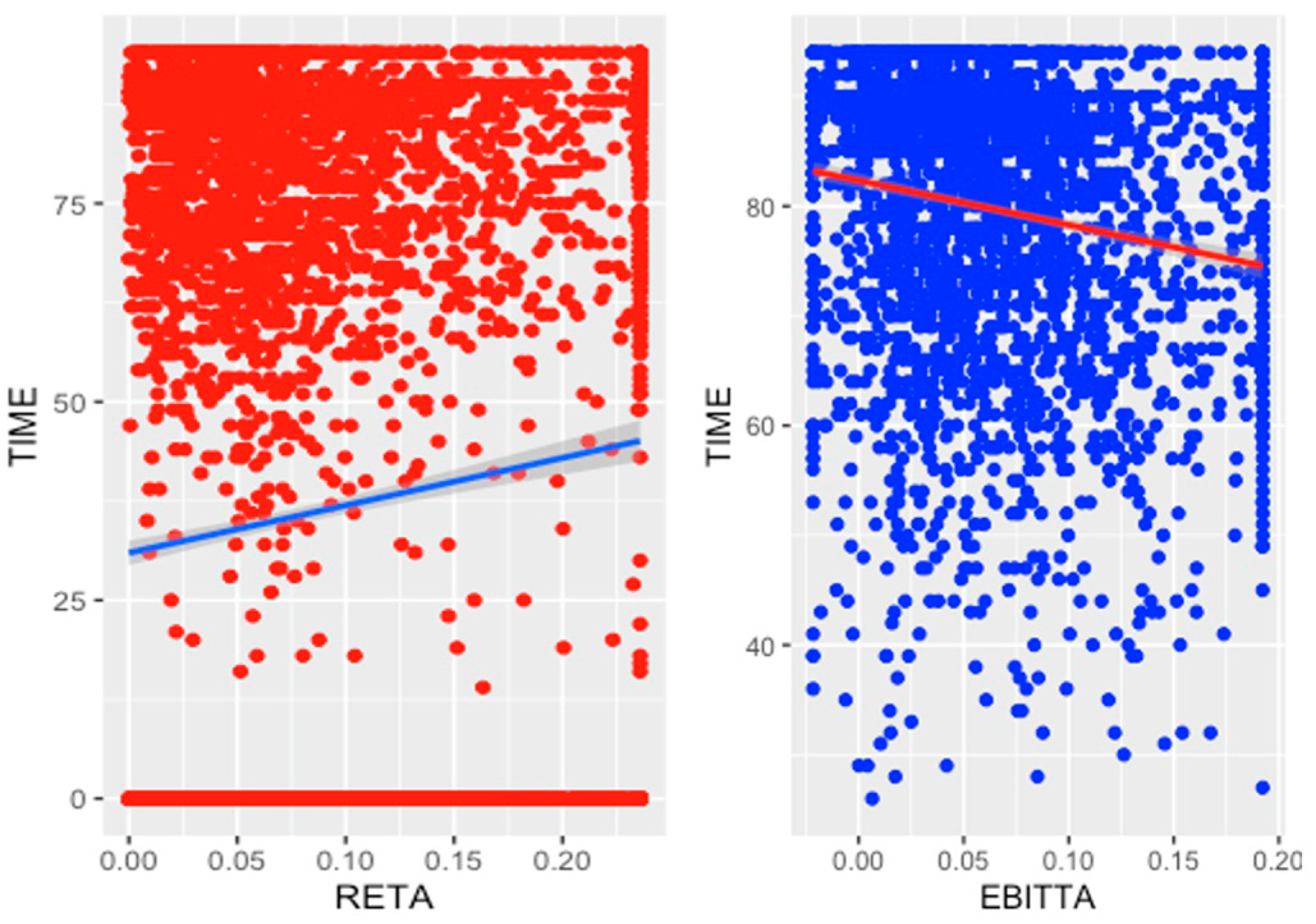

Analysis results of companies in Vietnam reveal that in the period from 2016 to 2020, the more retained earnings, the longer the time required to publish annual statements. Most companies decided to report early when their business results for the reporting year are profitable. Besides, when enterprises have been operating for a long time, they seem to be more cautious about reporting information and slower to publish reports than younger enterprises. In addition, the larger in size, the longer number of days required to publish financial accounts. Moreover, it can be said that companies in danger of bankruptcy shall not release annual reports early. Finally, complex of consolidated reports, liquidity, and capital structure of non-financial list companies in Vietnam are not influential on the annual reports’ publication time.

In relation with previous studies on the same topic, this study is the first study in Vietnam using bankruptcy risk as a new variable influencing the time to publish financial statements besides other factors which have been used by previous studies, such as: profitability, leverage, auditing firm type, and features of annual reports (

Vuran and Adiloglu 2013;

Sakka and Jarboui 2016;

Ha et al. 2018). In addition, this is the first study using recently updated data in a developing country. Many authors are also very interested in the disclosure of financial statements recently, but they examined other aspects of annual statements including: a study on the influence of information readability on financial statements on inventory liquidity in France (

Boubaker et al. 2019), or on cost of equity capital in US firms (

Rjiba et al. 2020).

This research contributes to the literature in several ways. First, this study is the first using both financial and nonfinancial information updated recent years to explore influencing factors on time of disclosure annual reports in Vietnam. Secondly, this research goes beyond the existing literature by providing feature of report (consolidated report) and bankruptcy risk in determinants of time for publication annual report.

The structure of the article in addition to the introduction and conclusion includes the following sections: (2) Theoretical framework and Literature review; (3) Hypothesis Development; (4) Research Methodology; (5) Empirical results; and (6) Discussions and Recommendations.

3. Hypothesis Development

First, the relationship between the company’s retained earnings and the time to publish annual reports.

For users of accounting information, retained earnings are one of the most attractive items on financial statements. Companies will publish high earnings figures sooner because this information will have a positive influence on the stock price (

Iyoha 2012). Thus, there is a relationship between a company’s earnings and the time of publication. This issue has attracted the attention of researchers around the world such as

Gulec (

2017),

Ha et al. (

2018),

Lukason and Camacho-Miñano (

2019), and

Raihani et al. (

2019). However, the research results have not been consistent in the direction of returns and publication date. According to

Gulec (

2017) and

Ha et al. (

2018), retained earnings (returns) have a negative relationship with the time of publication. In addition,

Lukason and Camacho-Miñano (

2019) also suggested that the higher the return on assets, the lower the possibility of the reports being published late. However, in the study by

Raihani et al. (

2019), the returns on assets of the company had no effect on the timeliness of financial statements. To supplement empirical evidence on the relationship between returns/retained earnings and reporting time, this study proposes hypothesis 1 as follows:

Hypothesis 1 (H1). Retained earnings have a positive effect on the number of days to publish annual reports of non-financial listed companies on the Vietnamese stock market.

Second, the relationship between the company’s income in the reporting year and the time to publish reports.

Operating income for the year is the difference between the revenue achieved during the year and the expenses incurred during the year. That kind of income is the most important indicator to make business decisions. Signaling theory suggests that the more profitable firms are, the earlier reports are released (

Ismail et al. 2005). The relationship between net income and the time of publication has been studied by many scholars such as

Turel (

2010),

Modugu et al. (

2012),

Khuong and Vy (

2017), and

Lukason and Camacho-Miñano (

2019).

This paper proposes hypothesis 2 as follows:

Hypothesis 2 (H2). A company’s income in the reporting year has a positive effect on the number of days to publish annual reports of non-financial listed companies on the Vietnamese stock market.

Third, the relationship between the company’s liquidity and time taken to publish annual reports.

The company’s liquidity is also a major concern to investors such as banks, credit institutions and creditors, suppliers, and employees. To borrow money from a bank or buy goods on credit from a supplier, companies must submit audited financial statements in a timely manner to creditors in order for them to assess the solvency of the companies. Many scholars around the world have studied the relationship between the company’s liquidity and time taken to publish annual reports, such as

Vuran and Adiloglu (

2013) and

Lukason and Camacho-Miñano (

2019). The research results of

Vuran and Adiloglu (

2013) confirmed that there is a relationship between the company’s liquidity and the time of publication. Meanwhile, the research results of

Lukason and Camacho-Miñano (

2019) confirmed that the higher the liquidity, the faster the report publication time. Therefore, this study put forward the following research hypothesis:

Hypothesis 3 (H3). Liquidity has a positive effect on the number of days to publish annual reports of non-financial listed companies on the Vietnamese stock market.

Fourth, the relationship between capital structure and the time taken to publish annual reports.

The company’s assets are formed from equity and debt. The proportion of equity to debt is called capital structure. There is competition between companies to get loans from banks based on how well the capital structure meets the requirements of the loan contract. The relationship between capital structure and reporting time has attracted scholars such as

Khasharmeh and Aljifri (

2010),

Gulec (

2017), and

Lukason and Camacho-Miñano (

2019). However, the research results of

Gulec (

2017) and

Lukason and Camacho-Miñano (

2019) suggested that there is no relationship between debt-to-total assets, debt-to-equity ratio, and time disclosure if it does not consider the influence of the industry group, whereas

Khasharmeh and Aljifri (

2010) showed that firms with high debt will publish reports faster than firms with low debt to reduce the negotiation costs on loan contracts. Therefore, this paper proposes hypothesis 4 as follows:

Hypothesis 4 (H4). Capital structure has a positive effect on the number of days to publish annual reports of non-financial companies listed on the Vietnamese stock market.

Fifth, the relationship between company size and the time taken to publish annual reports.

Firm size is one of the factors included in many studies (

Davies and Whittred (

1980),

Dyer and McHugh (

1975),

Carslaw and Kaplan (

1991),

Wu et al. (

2008),

Turel (

2010),

Sakka and Jarboui (

2016), and

Gulec (

2017)). There are studies measuring firm size by total asset value, such as those by

Davies and Whittred (

1980),

Dyer and McHugh (

1975),

Carslaw and Kaplan (

1991),

Turel (

2010), and

Hout (

2012). Studies in the past measured the size by total revenue in the year, such as those by

Aubert (

2009) and

Sakka and Jarboui (

2016). Reasons for the association between company size and report publication are vast. Foremost, in large-scale companies, internal control systems are often well-built (

Ng and Tai 1994) and thus facilitate audit work, shortening real-time taken for auditors to assess the quality of the internal control system, culminating in earlier publication of publishing reports relative to other companies. In addition, large companies are often the object of public interest, and are under pressure to disclose information to analysts, so they will release financial statements in a timely manner (

Owusu-Ansah and Yeoh 2005),

Ahmed (

2003). The research results, however, are not consistent among researchers. While

Khuong and Vy (

2017) stated that the larger the company, the longer it takes to publish reports,

Sakka and Jarboui (

2016),

Gulec (

2017), and

Ha et al. (

2018) agreed that the larger the company size, the sooner the time to publish. In contrast,

Turel (

2010),

Hout (

2012),

Raihani et al. (

2019) argued that there is no relationship between company size and the publication of annual financial statements. In juxtaposition, this paper proposes research hypothesis 5 as follows:

Hypothesis 5 (H5). The size of a company has a positive effect on the number of days to publish annual reports of non-financial companies listed on the Vietnamese stock market.

Sixth, the number of operating years and time to publish annual reports.

The number of operating years was considered in many studies such as

Iyoha (

2012) and

Hieu and Anh (

2020). The relationship between firm age and the time to publish annual reports, similarly, have been addressed in many studies:

Iyoha (

2012),

Ha et al. (

2018), and

Lukason and Camacho-Miñano (

2019).

Iyoha (

2012) concluded that the age of the company has a positive impact on timeliness. In contrast,

Ha et al. (

2018) found that firm size is negatively related to report publication.

Lukason and Camacho-Miñano (

2019) showed that the longer the company is in operation, the lower risk of late submission. Therefore, this study proposes hypothesis 6 as follows:

Hypothesis 6 (H6). The number of operating years has a positive effect on the number of days to publish annual reports of non-financial companies listed on the Vietnamese stock market.

Seventh, the characteristic of company’s financial statements and time to publish annual reports.

Companies in the process of doing business can contribute capital to many other companies. When the contributed capital of a company accounts for more than 50% of the capital of the receiving company or the control of a company in another company is more than 50%, that company is called the parent company, and the controlled companies are its subsidiaries. Parent companies must prepare and disclose consolidated financial statements. In fact, in Vietnam, most of the companies submitting their annual reports late indicated the cause to be by complications of consolidated statements (

Lien 2016;

Suong 2018).

Vuran and Adiloglu (

2013) did not find a relationship between late submission and the type of reports but

Gulec (

2017), and

Ha et al. (

2018) argued that companies preparing consolidated reports take a longer time to publish reports than other companies.

Therefore, this study proposes hypothesis 7 as follows:

Hypothesis 7 (H7). The characteristics of annual reports have a positive effect on the number of days to publish annual reports of non-financial companies listed on the Vietnamese stock market.

Eighth, the type of auditing firm and time to publish annual reports.

Hypothesis 8 (H8). The type of auditing firm has a positive effect on the number of days to publish annual reports of non-financial companies listed on the Vietnamese stock market.

Ninth, the company’s bankruptcy risk and time to publish annual reports.

Financial distress is a situation when a company experiences difficulties in meeting or paying its current financial obligations. Altman tried to combine several financial ratios into a predictive model with statistical techniques, specifically discriminant analysis that can be used to predict company bankruptcy risk. The bankruptcy prediction model has been developed by Altman over the years, shown in the following studies:

Altman (

1968),

Altman et al. (

1977),

Altman (

1983),

Altman and Hotchkiss (

2006),

Altman et al. (

2010),

Altman (

2013), and

Altman et al. (

2014). Through many developmental steps, studies on Altman’s bankruptcy forecasting model have helped investors identify bankruptcy risk to make reasonable decisions. The relationship between bankruptcy risk and financial reporting time has been studied by many authors. Some authors argued that financially distressed companies often hide the reason for poor performance, and thus try to delay the release of financial statements (

Whittred and Zimmer 1984;

Luypaert et al. 2016;

Lukason and Camacho-Miñano 2019). However, some authors argued that bankruptcy risk and the publication of annual financial statements have a negative relationship, and companies facing financial crisis will publish financial statements early (Siahaan et al. 2019 cited in

Khamisah et al. 2021;

Himawan and Venda 2020 cited in

Khamisah et al. 2021).

Therefore, this study proposes hypothesis 9 as follows:

Hypothesis 9 (H9). Bankruptcy risk has a positive effect on the number of days to publish annual reports of non-financial companies listed on the Vietnamese stock market.

{kind=link}

{kind=link}

{kind=link}

{kind=link}