ICT as a Key Determinant of Efficiency: A Bootstrap-Censored Quantile Regression (BCQR) Analysis for Vietnamese Banks

Abstract

:1. Introduction

2. Literature Review

3. Methodologies and Data

3.1. The First Stage: Evaluating Bank Efficiency Using Data Envelopment Analysis

3.2. The Second Stage: Using Bootstrap-Censored Quantile Regression (BCQR) to Examine the Determinants of DEA Efficiency

3.3. Variable Selection and Data

4. Results and Discussions

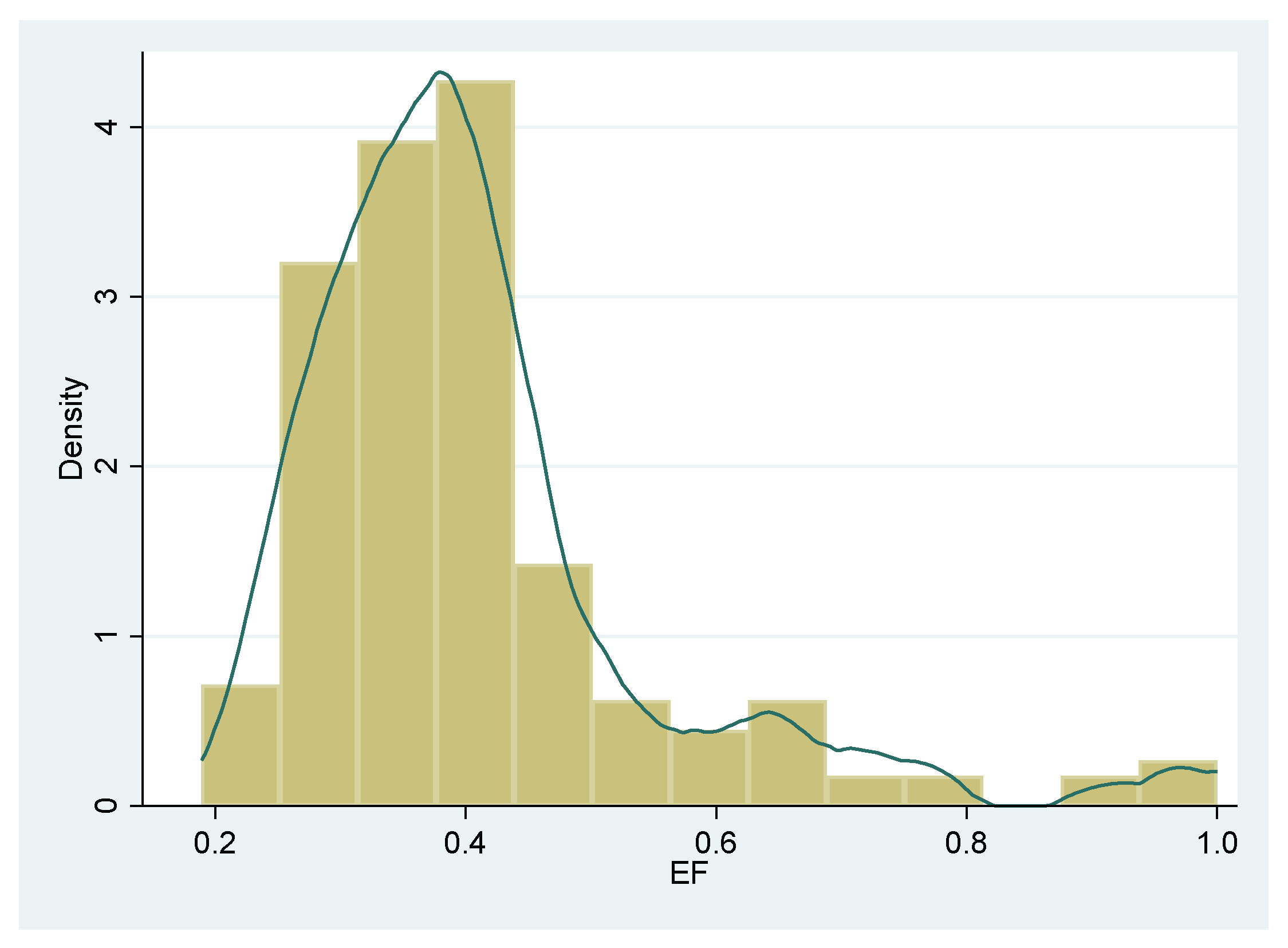

4.1. The Efficiency of Vietnamese Banks under DEA

4.2. The Relationship between ICT and Bank Efficiency under BCQR

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Aiello, Francesco, and Graziella Bonanno. 2016. Efficiency in banking: A meta-regression analysis. International Review of Applied Economics 30: 112–49. [Google Scholar] [CrossRef]

- Akhisar, İlyas, K. Batu Tunay, and Necla Tunay. 2015. The Effects of Innovations on Bank Performance: The Case of Electronic Banking Services. Procedia Social and Behavioral Sciences 195: 369–75. [Google Scholar] [CrossRef] [Green Version]

- Angrist, Joshua, Victor Chernozhukov, and Iván Fernández-Val. 2006. Quantile Regression under Misspecification, with an Application to the U.S. Wage Structure. Econometrica 74: 539–63. [Google Scholar] [CrossRef] [Green Version]

- Appiahene, Peter, Yaw Marfo Missah, and Ussiph Najim. 2019. Evaluation of information technology impact on bank’s performance: The Ghanaian experience. International Journal of Engineering Business Management 11: 1–10. [Google Scholar] [CrossRef] [Green Version]

- Arora, Hitesh, and Padmasai Arora. 2013. Effect of investments in information technology on bank performance: Empirical evidence from Indian public sector banks. International Journal of Business Information Systems 13: 400–17. [Google Scholar] [CrossRef]

- Avkiran, Necmi K. 2011. Association of DEA super-efficiency estimates with financial ratios: Investigating the case for Chinese banks. OMEGA 39: 323–34. [Google Scholar] [CrossRef]

- Baker, Matthew J. 2014. Adaptive Markov chain Monte Carlo sampling and estimation in Mata. Stata Journal 14: 623–61. [Google Scholar] [CrossRef] [Green Version]

- Banker, Rajiv D., Abraham Charnes, and William Wager Cooper. 1984. Some models for estimating technical and scale inefficiencies in data envelopment analysis. Management Science 30: 1078–92. [Google Scholar] [CrossRef] [Green Version]

- Beccalli, Elena. 2007. Does IT investment improve bank performance? Evidence from Europe. Journal of Banking & Finance 31: 2205–30. [Google Scholar] [CrossRef]

- Berger, Allen N., and Robert DeYoung. 2001. The Effects of Geographic Expansion on Bank Efficiency. Journal of Financial Services Research 19: 163–84. [Google Scholar] [CrossRef]

- Berger, Allen N., and Robert DeYoung. 2006. Technological progress and the geographic expansion of the banking industry. Journal of Money, Credit and Banking 38: 1483–513. [Google Scholar] [CrossRef] [Green Version]

- Berger, Allen N., and David B. Humphrey. 1997. Efficiency of financial institutions: International survey and directions for future research. European Journal of Operational Research 98: 175–212. [Google Scholar] [CrossRef] [Green Version]

- Berger, Allen N., and Loretta J. Mester. 1997. Inside the black box: What explains differences in the efficiencies of financial institutions? Journal of Banking & Finance 21: 895–947. [Google Scholar]

- Boubaker, Sabri, Asma Houcine, Zied Ftiti, and Hatem Masri. 2018. Does audit quality affect firms’ investment efficiency? Journal of the Operational Research Society 69: 1688–99. [Google Scholar] [CrossRef]

- Boubaker, Sabri, Duc Trung Do, Helmi Hammami, and Kim Cuong Ly. 2020. The role of bank affiliation in bank efficiency: A fuzzy multi-objective data envelopment analysis approach. Annals of Operations Research 311: 611–39. [Google Scholar] [CrossRef]

- Boubaker, Sabri, Tu D. Q. Le, and Thanh Ngo. 2022. Managing bank performance under COVID-19: A novel inverse DEA efficiency approach. International Transactions in Operational Research. Early view. [Google Scholar] [CrossRef]

- Castellano, Katherine Elizabeth, and Andrew Dean Ho. 2013. Contrasting OLS and Quantile Regression Approaches to Student “Growth” Percentiles. Journal of Educational and Behavioral Statistics 38: 190–215. [Google Scholar] [CrossRef]

- Charnes, A., William Wager Cooper, and Edwardo Rhodes. 1978. Measuring the efficiency of decision making units. European Journal of Operational Research 2: 429–44. [Google Scholar] [CrossRef]

- Chedrawi, Charbel, Bissane Harb, and Mariam Saleh. 2019. The E-Banking and the Adoption of Innovations from the Perspective of the Transactions Cost Theory: Case of the Largest Commercial Banks in Lebanon. In ICT for a Better Life and a Better World: The Impact of Information and Communication Technologies on Organizations and Society. Edited by Youcef Baghdadi and Antoine Harfouche. Cham: Springer International Publishing, pp. 149–64. [Google Scholar] [CrossRef]

- Ciciretti, Rocco, Iftekhar Hasan, and Cristiano Zazzara. 2009. Do internet activities add value? Evidence from the traditional banks. Journal of Financial Services Research 35: 81–98. [Google Scholar] [CrossRef]

- Dao, Thuy T. T., Xuan T. T. Mai, Thanh Ngo, Tu Le, and Huong Ho. 2021. From Efficiency Analyses to Policy Implications: A Multilevel Hierarchical Linear Model Approach. International Journal of the Economics of Business 28: 457–70. [Google Scholar] [CrossRef]

- Delis, Manthos, Maria Iosifidi, and Mike G. Tsionas. 2017. Endogenous bank risk and efficiency. European Journal of Operational Research 260: 376–87. [Google Scholar] [CrossRef] [Green Version]

- DeYoung, Robert. 2001. The financial performance of pure play Internet banks. Economic Perspectives 25: 60–75. [Google Scholar]

- Dinçer, Hasan, and Serhat Yüksel. 2020. The Role of IT Investment on the Bank Performance: A Cointegration and Causality Analysis for Asian Countries. In Role of IT- ITES in Economic Development of Asia: Issues of Growth, Sustainability and Governance. Edited by Soumyen Sikdar, Ramesh Chandra Das and Rajib Bhattacharyya. Singapore: Springer, pp. 13–25. [Google Scholar] [CrossRef]

- Dinh, Van Chuc. 2020. Information technology application in developing banking products and services in Vietnam. Journal of Finance 2: 1–5. (In Vietnamese). [Google Scholar]

- Dong, Yizhe, Robert Hamilton, and Mark Tippett. 2014. Cost efficiency of the Chinese banking sector: A comparison of stochastic frontier analysis and data envelopment analysis. Economic Modelling 36: 298–308. [Google Scholar] [CrossRef]

- Fujii, Hidemichi, Shunsuke Managi, and Roman Matousek. 2014. Indian bank efficiency and productivity changes with undesirable outputs: A disaggregated approach. Journal of Banking & Finance 38: 41–50. [Google Scholar]

- Gajewski, Byron J., Robert Lee, Marge Bott, Ubolrat Piamjariyakul, and Roma Lee Taunton. 2009. On estimating the distribution of data envelopment analysis efficiency scores: An application to nursing homes’ care planning process. Journal of Applied Statistics 36: 933–44. [Google Scholar] [CrossRef]

- Galvao, Antonio F. 2011. Quantile regression for dynamic panel data with fixed effects. Journal of Econometrics 164: 142–57. [Google Scholar] [CrossRef]

- Gardener, Edward, Philip Molyneux, and Hoai Nguyen-Linh. 2011. Determinants of efficiency in South East Asian banking. The Service Industries Journal 31: 2693–719. [Google Scholar] [CrossRef]

- Girmaye, Haftu. 2018. Information Communication Technology and Bank Profitability: Evidence from Ethiopia. Eastern Africa Social Science Research Review 34: 1–19. [Google Scholar] [CrossRef]

- GSO. 2019. Statistical yearbook of Vietnam. Hanoi: GSO. [Google Scholar]

- Hammami, Helmi, Thanh Ngo, David Tripe, and Dinh-Tri Vo. 2020. Ranking with a Euclidean common set of weights in data envelopment analysis: With application to the Eurozone banking sector. Annals of Operations Research 311: 675–94. [Google Scholar] [CrossRef]

- Hernando, Ignacio, and María J. Nieto. 2007. Is the Internet delivery channel changing banks’ performance? The case of Spanish banks. Journal of Banking & Finance 31: 1083–99. [Google Scholar]

- Ho, Shirley J., and Sushanta Kumar Mallick. 2010. The impact of information technology on the banking industry. Journal of the Operational Research Society 61: 211–21. [Google Scholar] [CrossRef]

- Ho, Tin H., Dat T. Nguyen, Thanh Ngo, and Tu D. Q. Le. 2021. Efficiency in Vietnamese Banking: A Meta-Regression Analysis Approach. International Journal of Financial Studies 9: 41. [Google Scholar] [CrossRef]

- Holden, Ken, and Magdi El-Bannany. 2004. Investment in information technology systems and other determinants of bank profitability in the UK. Applied Financial Economics 14: 361–65. [Google Scholar] [CrossRef]

- Koch, Timothy W., and S. Scott MacDonald. 2010. Bank Management, 7th ed. Mason: South-Western Cengage Learning. [Google Scholar]

- Koenker, Roger, and Kevin F. Hallock. 2001. Quantile Regression. Journal of Economic Perspectives 15: 143–56. [Google Scholar] [CrossRef]

- Lamarche, Carlos. 2021. Quantile Regression for Panel Data and Factor Models. In Oxford Research Encyclopedia of Economics and Finance. Oxford: Oxford University Press. [Google Scholar] [CrossRef]

- Le, Tu D. Q. 2018. Bank risk, capitalisation and technical efficiency in the Vietnamese banking system. Australasian Accounting Business & Finance Journal 12: 42–61. [Google Scholar] [CrossRef]

- Le, Tu D. Q. 2020a. Market discipline and the regulatory change: Evidence from Vietnam. Cogent Economics & Finance 8: 1757801. [Google Scholar] [CrossRef]

- Le, Tu D. Q. 2020b. Multimarket contacts and bank profitability: Do diversification and bank ownership matter? Cogent Economics & Finance 8: 1849981. [Google Scholar] [CrossRef]

- Le, Tu D. Q. 2021a. Geographic expansion, income diversification, and bank stability: Evidence from Vietnam. Cogent Business & Management 8: 1885149. [Google Scholar] [CrossRef]

- Le, Tu D. Q. 2021b. Can foreign ownership reduce bank risk? Evidence from Vietnam. Review of Economic Analysis 13: 1–24. [Google Scholar] [CrossRef]

- Le, Tu D. Q., and Thanh Ngo. 2020. The determinants of bank profitability: A cross-country analysis. Central Bank Review 20: 65–73. [Google Scholar] [CrossRef]

- Le, Tu D. Q., and Dat T. Nguyen. 2020. Intellectual capital and bank profitability: New evidence from Vietnam. Cogent Business & Management 7: 1859666. [Google Scholar] [CrossRef]

- Le, Tu D. Q., Son H. Tran, and Liem T. Nguyen. 2019. The impact of multimarket contacts on bank stability in Vietnam. Pacific Accounting Review 31: 336–57. [Google Scholar] [CrossRef]

- Le, Chau, Aleksandar Šević, Panayiotis G. Tzeremes, and Trong Ngo. 2022a. Bank efficiency in Vietnam: Do scale expansion strategies and non-performing loans matter? International Journal of Finance & Economics 27: 822–43. [Google Scholar] [CrossRef]

- Le, Tu D. Q., Tin H. Ho, Dat T. Nguyen, and Thanh Ngo. 2022b. A cross-country analysis on diversification, Sukuk investment, and the performance of Islamic banking systems under the COVID-19 pandemic. Heliyon 8: e09106. [Google Scholar] [CrossRef]

- Lozano-Vivas, Ana, and Fotios Pasiouras. 2010. The impact of non-traditional activities on the estimation of bank efficiency: International evidence. Journal of Banking & Finance 34: 1436–49. [Google Scholar]

- Lozano-Vivas, Ana, and Fotios Pasiouras. 2014. Bank Productivity Change and Off-Balance-Sheet Activities Across Different Levels of Economic Development. Journal of Financial Services Research 46: 271–94. [Google Scholar] [CrossRef]

- Martín-Oliver, Alfredo, and Vicente Salas-Fumás. 2008. The output and profit contribution of information technology and advertising investments in banks. Journal of Financial Intermediation 17: 229–55. [Google Scholar] [CrossRef] [Green Version]

- MIC. 2020. Vietnam ICT Index Reports. Hanoi: Ministry of Information and Communications (MIC). [Google Scholar]

- Mishkin, Frederic S. 2019. The Economics of Money, Banking, and Financial Markets, 12th ed. London: Pearson. [Google Scholar]

- Ngo, Thanh, and Tu D. Q. Le. 2017. Resource for Research: A Vietnamese Banking Database [Updated 2020]. Social Science Research Network. Available online: https://ssrn.com/abstract=3028996 (accessed on 2 February 2022).

- Ngo, Thanh, and Tu Le. 2019. Capital market development and bank efficiency: A cross-country analysis. International Journal of Managerial Finance 15: 478–91. [Google Scholar] [CrossRef]

- Ngo, Thanh, and Tu Le. 2022. Impact of Information and Communication Technology on Banking Efficiency: The Vietnamese Experiences (forthcoming). In Handbook of Banking and Finance in Emerging Markets. Edited by Duc Khuong Nguyen. Cheltenham: Edward Elgar. [Google Scholar]

- Ngo, Thanh, and Kan Wai Hong Tsui. 2020. A data-driven approach for estimating airport efficiency under endogeneity: An application to New Zealand airports. Research in Transportation Business & Management 34: 100412. [Google Scholar] [CrossRef]

- Nguyen, Tram, David Tripe, and Thanh Ngo. 2018. Operational Efficiency of Bank Loans and Deposits: A Case Study of Vietnamese Banking System. International Journal of Financial Studies 6: 14. [Google Scholar] [CrossRef] [Green Version]

- Nguyen, Hai-Dang, Thanh Ngo, Tu D. Q. Le, Huong Ho, and Hai T. H. Nguyen. 2019. The role of knowledge in sustainable agriculture: Evidence from rice farms’ technical efficiency in Hanoi, Vietnam. Sustainability 11: 2472. [Google Scholar] [CrossRef] [Green Version]

- Salim, Ruhul, Mohammad Ziaul Hoque, and Suyanto Suyanto. 2010. The role of governance, ICT and bad loans in Australian bank efficiency: An empirical study. Asia Pacific Journal of Economics and Business 14: 18–36. [Google Scholar]

- Santín, Daniel, and Gabriela Sicilia. 2017. Dealing with endogeneity in data envelopment analysis applications. Expert Systems with Applications 68: 173–84. [Google Scholar] [CrossRef]

- Sathye, Suneeta, and Milind Sathye. 2017. Do ATMs Increase Technical Efficiency of Banks in a Developing Country? Evidence from Indian Banks. Australian Accounting Review 27: 101–11. [Google Scholar] [CrossRef] [Green Version]

- Scott, Susan V., John Van Reenen, and Markos Zachariadis. 2017. The long-term effect of digital innovation on bank performance: An empirical study of SWIFT adoption in financial services. Research Policy 46: 984–1004. [Google Scholar] [CrossRef] [Green Version]

- Sealey, Calvin W., and James T. Lindley. 1977. Inputs, outputs, and a theory of production and cost at depository financial institutions. Journal of Finance 32: 1251–66. [Google Scholar] [CrossRef]

- Siddik, Md Nur Alam, Gang Sun, Sajal Kabiraj, Joghee Shanmugan, and Cui Yanjuan. 2016. Impacts of e-banking on performance of banks in a developing economy: Empirical evidence from Bangladesh. Journal of Business Economics and Management 17: 1066–80. [Google Scholar] [CrossRef] [Green Version]

- Simar, Leopold, and Paul W. Wilson. 2007. Estimation and inference in two-stage, semi-parametric models of production processes. Journal of Econometrics 136: 31–64. [Google Scholar] [CrossRef]

- Simper, Richard, Aristeidis Dadoukis, and Cormac Bryce. 2019. European bank loan loss provisioning and technological innovative progress. International Review of Financial Analysis 63: 119–30. [Google Scholar] [CrossRef]

- Sowlati, Taraneh, and Joseph C. Paradi. 2004. Establishing the “practical frontier” in data envelopment analysis. OMEGA 32: 261–72. [Google Scholar] [CrossRef] [Green Version]

- Stewart, Chris, Roman Matousek, and Thao Ngoc Nguyen. 2016. Efficiency in the Vietnamese banking system: A DEA double bootstrap approach. Research in International Business and Finance 36: 96–111. [Google Scholar] [CrossRef] [Green Version]

- Sun, Lei, and Tzu-Pu Chang. 2011. A comprehensive analysis of the effects of risk measures on bank efficiency: Evidence from emerging Asian countries. Journal of Banking & Finance 35: 1727–35. [Google Scholar]

- Sun, Xiaoyan, Limin Peng, Amita Manatunga, and Michele Marcus. 2016. Quantile regression analysis of censored longitudinal data with irregular outcome-dependent follow-up. Biometrics 72: 64–73. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Tone, Kaoru. 2001. A slacks-based measure of efficiency in data envelopment analysis. European Journal of Operational Research 130: 498–509. [Google Scholar] [CrossRef] [Green Version]

- Tripe, David. 2010. Using DEA to investigate bank safety and soundness—Which approach works best? Journal of Financial Economic Policy 2: 237–50. [Google Scholar] [CrossRef]

- Tunay, K. Batu, Necla Tunay, and İlyas Akhisar. 2015. Interaction Between Internet Banking and Bank Performance: The Case of Europe. Procedia Social and Behavioral Sciences 195: 363–68. [Google Scholar] [CrossRef] [Green Version]

- Valverde, S. Carbó, and David B. Humphrey. 2009. Technological innovation in banking: The shift to ATMs and implicit pricing of network convenience. In Financial Innovation in Retail and Corporate Banking. Edited by Luisa Anderloni, David T. Llewellyn and Reinhard H. Schmidt. Cheltenham: Edward Elgar. [Google Scholar]

- Vidal-García, Javier, Marta Vidal, Sabri Boubaker, and Majdi Hassan. 2018. The efficiency of mutual funds. Annals of Operations Research 267: 555–84. [Google Scholar] [CrossRef]

- Vietnamese Government. 2012a. Decision No. 254/QD-TTg on approving the scheme on “Restructuring the credit institutions System in the 2011–2015 Period”; Hanoi: Office of the Government.

- Vietnamese Government. 2012b. Decision No. 432/QD-TTg on the Viet Nam Sustainable Development Strategy for the 2011–2020; Hanoi: Office of the Government.

- Vietnamese Government. 2016a. Decision No. 2545/QD-TTg: Approval for Government Plan on Cashless Payment in the 2016–2020 Period; Hanoi: Office of the Government.

- Vietnamese Government. 2016b. Resolution No. 05-NQ/TW on Major Policies for Rennovation of Growth Models and Improvement of Growth Quality, Economic Productivity and Competitiveness; Hanoi: Office of the Government.

- Vietnamese Government. 2017. Directive No. 16/CT-TTg on the Strengthening of the Ability to Access the Fourth Industrial Revolution; Hanoi: Office of the Government.

- Weigelt, Carmen, and M. B. Sarkar. 2012. Performance implications of outsourcing for technological innovations: Managing the efficiency and adaptability trade-off. Strategic Management Journal 33: 189–216. [Google Scholar] [CrossRef]

{kind=link}

| First-Stage DEA | |||||

| N | Mean | SD | Min | Max | |

| Inputs | |||||

| STAFF | 180 | 8930.69 | 7706.57 | 523.00 | 38,240.00 |

| OE | 180 | 6770.00 | 7100.00 | 120.00 | 36,500.00 |

| Outputs | |||||

| OI | 180 | 20,800.00 | 21,700.00 | 357.00 | 115,000.00 |

| TA | 180 | 265,000.00 | 294,000.00 | 2940.00 | 1,490,000.00 |

| Second-Stage BCQR | |||||

| N | Mean | SD | Min | Max | |

| Control variables | |||||

| ICT | 180 | 0.52 | 0.12 | 0.25 | 0.81 |

| ITII | 177 | 0.47 | 0.12 | 0.24 | 0.82 |

| HITI | 177 | 0.47 | 0.24 | 0 | 1 |

| ITA | 177 | 0.51 | 0.20 | 0 | 1 |

| SPIDIT | 177 | 0.697 | 0.220 | 0 | 1 |

| SOCB | 180 | 0.228 | 0.421 | 0 | 1 |

| LLP | 180 | 1.285 | 0.511 | 0.193 | 3.702 |

| OBS | 180 | 0.180 | 0.241 | 0 | 1.390 |

| BRANCH | 180 | 5.297 | 0.920 | 3.367 | 7.723 |

| EFF | |||||||||

| 0.02 | ICT | ||||||||

| 0.07 | 0.65 *** | ITII | |||||||

| 0.04 | 0.51 *** | 0.22 *** | HITI | ||||||

| −0.06 | 0.62 *** | 0.22 *** | 0.03 | ITA | |||||

| −0.04 | 0.75 *** | 0.38 *** | 0.25 *** | 0.31 *** | SPIDIT | ||||

| 0.09 | 0.56 *** | 0.54 *** | 0.07 | 0.44 *** | 0.42 *** | SOCB | |||

| −0.16 ** | 0.34 *** | 0.36 *** | 0.06 | 0.24 *** | 0.3 *** | 0.53 *** | LLP | ||

| −0.05 | 0.07 | −0.01 | −0.02 | 0.01 | 0.07 | −0.03 | 0.18 ** | OBS | |

| −0.02 | 0.37 *** | 0.28 *** | −0.11 | 0.35 *** | 0.33 *** | 0.51 *** | 0.19 ** | 0.24 *** | BRANCH |

| Quantiles | 25th | 50th | 75th | 80th | 90th |

|---|---|---|---|---|---|

| ICT | 0.17 *** | 0.165 *** | 0.184 *** | 0.196 *** | 0.16 *** |

| (0.009) | (0.016) | (0.014) | (0.019) | (0.013) | |

| SOCB | 0.143 *** | 0.137 *** | 0.13 *** | 0.171 *** | 0.145 *** |

| (0.002) | (0.005) | (0.008) | (0.019) | (0.007) | |

| LLP | −0.092 *** | −0.008 *** | −0.067 *** | −0.088 *** | −0.096 *** |

| (0.005) | (0.011) | (0.002) | (0.011) | (0.016) | |

| OBS | −0.052 *** | −0.039 *** | −0.046 *** | −0.056 *** | −0.072 *** |

| (0.01) | (0.005) | (0.007) | (0.019) | (0.018) | |

| BRANCH | −0.05 *** | −0.037 *** | −0.037 *** | −0.053 *** | −0.001 |

| (0.01) | (0.007) | (0.009) | (0.01) | (0.028) | |

| Constant | −33.101 *** | −33.08 *** | −33.07 *** | −33.07 *** | −33.08 *** |

| (0.021) | (0.012) | (0.01) | (0.012) | (0.004) | |

| Time fixed effect | Yes | Yes | Yes | Yes | Yes |

| N | 180 | 180 | 180 | 180 | 180 |

| Quantiles | 25th | 50th | 75th | 80th | 90th |

|---|---|---|---|---|---|

| ITII | 0.101 *** | 0.11 *** | 0.11 *** | 0.112 *** | 0.081 *** |

| (0.01) | (0.005) | (0.009) | (0.009) | (0.018) | |

| HITI | 0.042 *** | 0.038 *** | 0.045 *** | 0.031 | 0.075 *** |

| (0.003) | (0.009) | (0.008) | (0.023) | (0.018) | |

| ITA | −0.042 *** | −0.037 *** | −0.04 *** | −0.04 *** | −0.064 *** |

| (0.002) | (0.003) | (0.006) | (0.005) | (0.007) | |

| SPIDIT | 0.039 *** | 0.054 *** | 0.066 *** | 0.051 *** | 0.093 *** |

| (0.013) | (0.006) | (0.011) | (0.015) | (0.014) | |

| SOCB | 0.164 *** | 0.153 *** | 0.126 *** | 0.147 *** | 0.116 *** |

| (0.01) | (0.008) | (0.026) | (0.008) | (0.015) | |

| LLP | −0.082 *** | −0.092 *** | −0.103 *** | −0.092 *** | −0.062 *** |

| (0.009) | (0.006) | (0.009) | (0.008) | (0.014) | |

| OBS | −0.049 *** | −0.035 *** | −0.041 *** | −0.044 *** | −0.017 |

| (0.005) | (0.007) | (0.003) | (0.012) | (0.027) | |

| BRANCH | −0.054 *** | −0.041 *** | −0.038 *** | −0.036 *** | 0.027 |

| (0.011) | (0.005) | (0.005) | (0.005) | (0.037) | |

| Constant | −34.18 *** | −34.18 *** | −34.16 *** | −34.18 *** | −34.19 *** |

| (0.002) | (0.003) | (0.02) | (0.03) | (0.01) | |

| Time fixed effect | Yes | Yes | Yes | Yes | Yes |

| N | 177 | 177 | 177 | 177 | 177 |

| Quantiles | 25th | 50th | 75th | 80th | 90th |

|---|---|---|---|---|---|

| ICT | 0.37 *** | 0.381 *** | 0.355 *** | 0.358 *** | 0.212 *** |

| (0.002) | (0.014) | (0.014) | (0.012) | (0.043) | |

| SOCB | 0.502 *** | 0.499 *** | 0.508 *** | 0.483 *** | 0.503 *** |

| (0.012) | (0.014) | (0.004) | (0.014) | (0.023) | |

| ICT × SOCB | −0.617 *** | −0.634 *** | −0.67 *** | −0.663 *** | −0.574 *** |

| (0.013) | (0.008) | (0.026) | (0.016) | (0.021) | |

| Constant | −32.88 *** | −32.89 *** | −32.85 *** | −32.87 *** | −32.83 *** |

| (0.002) | (0.009) | (0.02) | (0.015) | (0.031) | |

| Time fixed effect | Yes | Yes | Yes | Yes | Yes |

| Other control variables | Yes | Yes | Yes | Yes | Yes |

| N | 180 | 180 | 180 | 180 | 180 |

| Quantiles | 25th | 50th | 75th | 80th | 90th |

|---|---|---|---|---|---|

| ITII | 0.207 *** | 0.215 *** | 0.221 *** | 0.181 *** | 0.242 *** |

| (0.008) | (0.009) | (0.01) | (0.011) | (0.026) | |

| HITI | 0.077 *** | 0.114 *** | 0.139 *** | 0.135 *** | 0.131 *** |

| (0.022) | (0.007) | (0.014) | (0.015) | (0.012) | |

| ITA | −0.009 | −0.026 *** | −0.01 | −0.017 ** | −0.011 |

| (0.006) | (0.006) | (0.011) | (0.008) | (0.008) | |

| SPIDIT | 0.047 *** | 0.045 *** | 0.061 *** | 0.016 | 0.032 * |

| (0.003) | (0.004) | (0.007) | (0.022) | (0.019) | |

| SOCB | 0.441 *** | 0.424 *** | 0.444 *** | 0.41 *** | 0.428 *** |

| (0.009) | (0.013) | (0.008) | (0.015) | (0.009) | |

| ITII × SOCB | −0.056 *** | −0.054 *** | −0.027 *** | −0.054 *** | −0.072 *** |

| (0.01) | (0.008) | (0.01) | (0.01) | (0.026) | |

| HITI × SOCB | −0.313 *** | −0.295 *** | −0.306 *** | −0.301 *** | −0.296 *** |

| (0.008) | (0.003) | (0.015) | (0.003) | (0.008) | |

| ITA × SOCB | 0.004 | −0.007 | −0.01 | −0.023 | 0.024 |

| (0.009) | (0.006) | (0.008) | (0.017) | (0.017) | |

| SPIDIT × SOCB | −0.228 *** | −0.181 *** | −0.204 *** | −0.204 *** | −0.178 *** |

| (0.023) | (0.01) | (0.015) | (0.015) | (0.016) | |

| Constant | −30.688 *** | −30.7 *** | −30.67 *** | −30.69 *** | −30.7 *** |

| (0.005) | (0.01) | (0.014) | (0.01) | (0.013) | |

| Time fixed effect | Yes | Yes | Yes | Yes | Yes |

| Other control variables | Yes | Yes | Yes | Yes | Yes |

| N | 177 | 177 | 177 | 177 | 177 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Le, T.D.Q.; Ngo, T.; Ho, T.H.; Nguyen, D.T. ICT as a Key Determinant of Efficiency: A Bootstrap-Censored Quantile Regression (BCQR) Analysis for Vietnamese Banks. Int. J. Financial Stud. 2022, 10, 44. https://doi.org/10.3390/ijfs10020044

Le TDQ, Ngo T, Ho TH, Nguyen DT. ICT as a Key Determinant of Efficiency: A Bootstrap-Censored Quantile Regression (BCQR) Analysis for Vietnamese Banks. International Journal of Financial Studies. 2022; 10(2):44. https://doi.org/10.3390/ijfs10020044

Chicago/Turabian StyleLe, Tu D. Q., Thanh Ngo, Tin H. Ho, and Dat T. Nguyen. 2022. "ICT as a Key Determinant of Efficiency: A Bootstrap-Censored Quantile Regression (BCQR) Analysis for Vietnamese Banks" International Journal of Financial Studies 10, no. 2: 44. https://doi.org/10.3390/ijfs10020044

APA StyleLe, T. D. Q., Ngo, T., Ho, T. H., & Nguyen, D. T. (2022). ICT as a Key Determinant of Efficiency: A Bootstrap-Censored Quantile Regression (BCQR) Analysis for Vietnamese Banks. International Journal of Financial Studies, 10(2), 44. https://doi.org/10.3390/ijfs10020044