The Moderating Effects of Host Country Governance and Trade Openness on the Relationship between Cultural Distance and Financial Performance of Foreign Subsidiaries in Latin America

Abstract

:1. Introduction

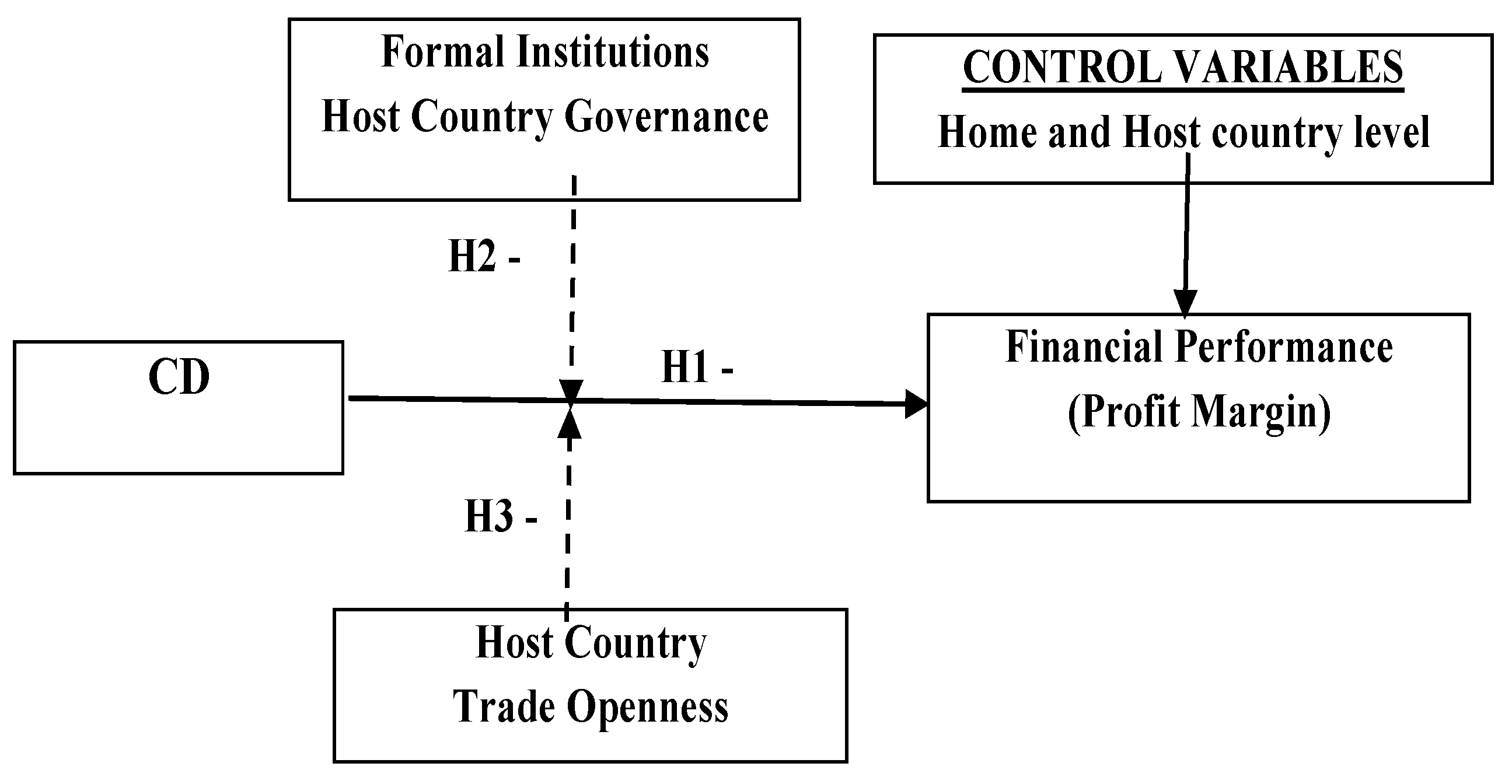

2. Literature Review, Theoretical Background and Hypothesis

2.1. Cultural Distance and Performance

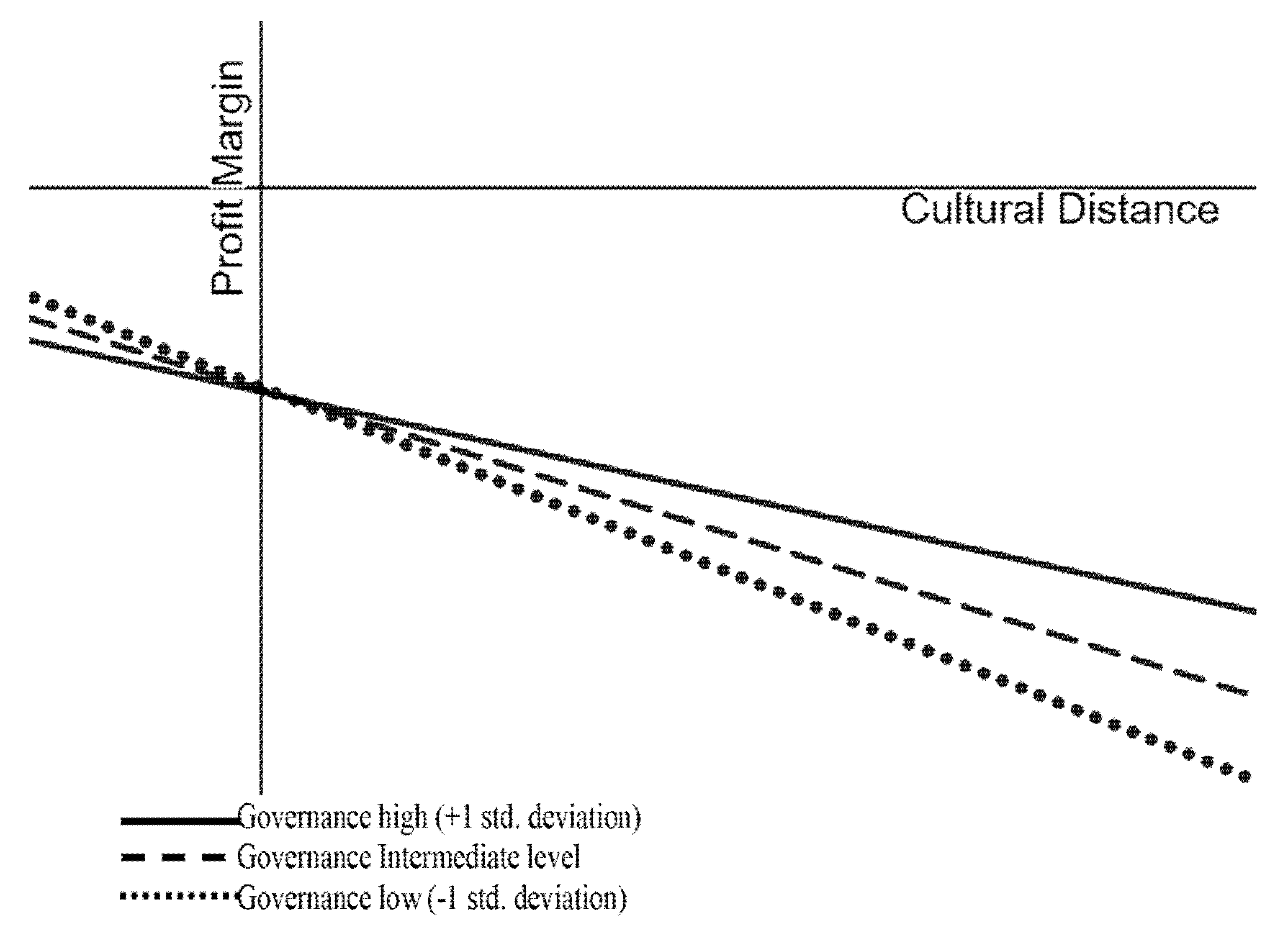

2.2. The Moderating Effects of Host Country Formal Institutions

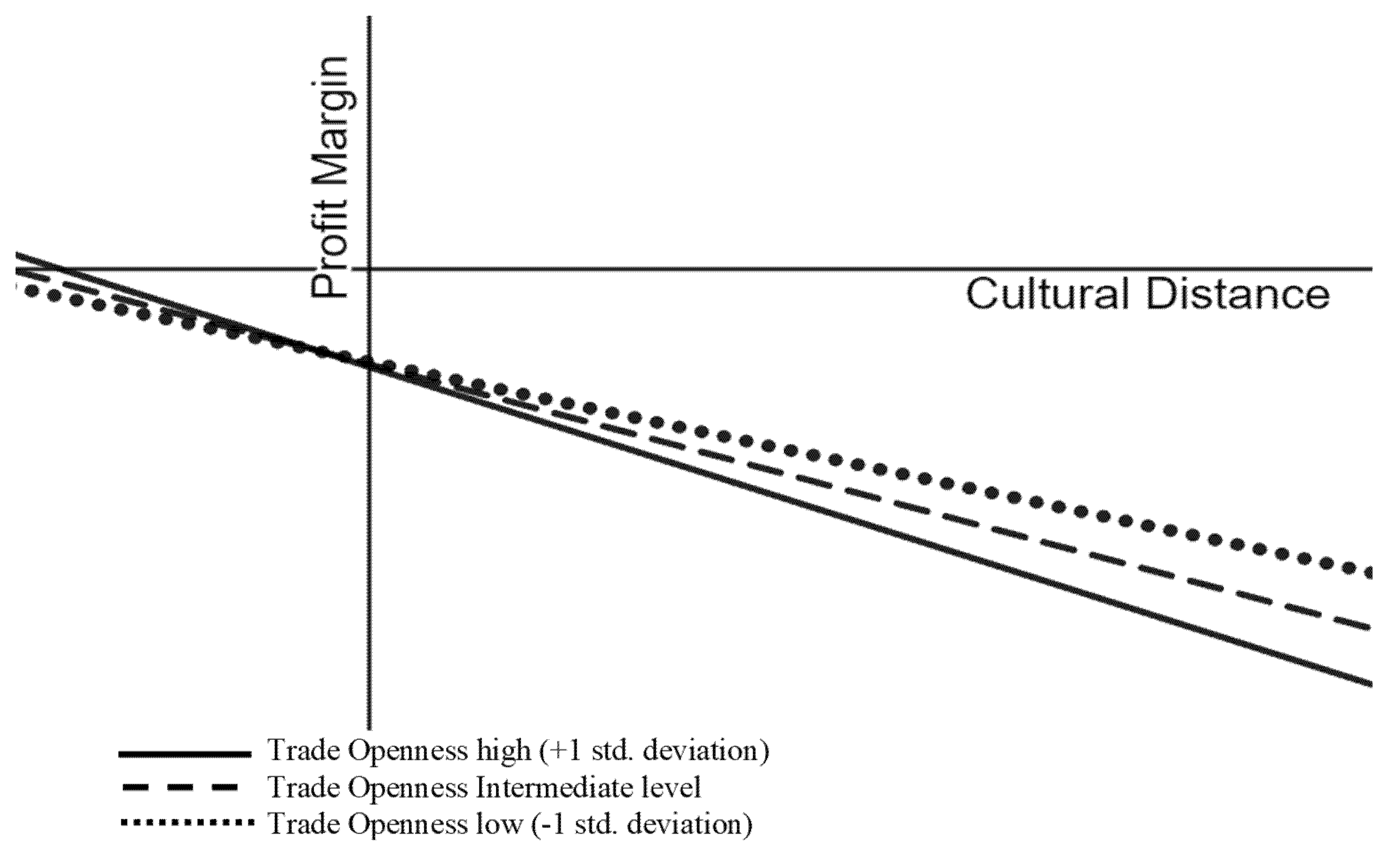

2.3. The Moderating Effects of Host Country Trade Openness

3. Methodology

3.1. Dependent Variable

3.2. Independent Variables

- (a)

- Cultural Distance (CD): Calculated using the Kogut and Singh (KS) (Kogut and Singh 1988) composite index using the four original dimensions of Hofstede (1980): individualism vs. collectivism, power distance, masculinity vs. femininity, and uncertainty avoidance.

- (b)

- Host Country Governance (Host Country Formal Institutions): In line with previous research, the quality of formal institutions in the host country is measured using the World Governance Indicators (WGI) from the World Bank developed by Kaufmann et al. (2009). The WGI is closely related to the normative and regulatory pillars and is extensively used in literature to assess the strength of formal institutions (Stein and Daude 2001; Globerman and Shapiro 2003; Gani 2007; Wernick et al. 2009; Mengistu and Adhikary 2011) The WGI includes six variables: voice and accountability (VOICE), political stability and absence of violence (POL), government effectiveness (GOV), regulatory quality (REG), rule of law (RULE) and control of corruption (CC)—they represent “the traditions and institutions by which authority in a country is exercised” (Kaufmann et al. 2011, p. 4). Due to the high correlation among the six WGI variables, the strength of host country governance is computed as a composite index calculated as the arithmetic means of the six WGI variables.

- (c)

- Trade Openness Index: Following previous studies, the trade openness index measures the sum of imports and exports as a percentage of total GDP (Kolstad and Wiig 2012; Reyes et al. 2019). The index data is collected from the World Bank.

3.3. Control Variables

3.4. The Moderation Tests

4. Results

5. Discussion

6. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Aguinis, Herman, Isabel Villamor, Sergio G. Lazzarini, Roberto S. Vassolo, José Ernesto Amorós, and David G. Allen. 2020. Conducting management research in Latin America: Why and what’s in it for you? Journal of Management 46: 615–36. [Google Scholar] [CrossRef] [Green Version]

- Andrews, Donald W. K. 1991. Heteroskedasticity and autocorrelation consistent covariance matrix estimation. Econometrica: Journal of the Econometric Society 59: 817–58. [Google Scholar] [CrossRef]

- Beugelsdijk, Sjoerd, Tatiana Kostova, Vincent E. Kunst, Ettore Spadafora, and Marc Van Essen. 2018. Cultural Distance and Firm Internationalization: A Meta-Analytical Review and Theoretical Implications. Journal of Management 44: 89–130. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Capon, Noel, John U. Farley, and Scott Hoenig. 1990. Determinants of financial performance: a meta-analysis. Management Science 36: 1143–59. [Google Scholar] [CrossRef] [Green Version]

- Chopra, Rohit, and Juan Mier. 2017. Profitability Trends in Emerging Markets Setting the Stage for Active Management. New York: Lazard Asset Management. [Google Scholar]

- Contractor, Farok J., Sumit K. Kundu, and Chin-Chun Hsu. 2003. A three-stage theory of international expansion: The link between multinationality and performance in the service sector. Journal of International Business Studies 34: 5–18. [Google Scholar] [CrossRef]

- Correa da Cunha, Henrique, Carlyle Farrell, Svante Andersson, Mohamed Amal, and Dinora Eliete Floriani. 2022a. Toward a more in-depth measurement of cultural distance: A re-evaluation of the underlying assumptions. International Journal of Cross Cultural Management, 1–32. [Google Scholar] [CrossRef]

- Correa da Cunha, Henrique, Carlyle Farrell, Svante Andersson, Mohamed Amal, and Dinora Eliete Floriani. 2020. The Direction of Cultural Distance and the Performance of Foreign Subsidiaries in Latin America. In Academy of Management Proceedings. Briarcliff Manor: Academy of Management, p. 22159. [Google Scholar]

- Correa da Cunha, Henrique, Vikkram Singh, and Shengkun Xie. 2022b. The Determinants of Outward Foreign Direct Investment from Latin America and the Caribbean: An Integrated Entropy-Based TOPSIS Multiple Regression Analysis Framework. Journal of Risk and Financial Management 15: 130. [Google Scholar] [CrossRef]

- Correa da Cunha, Henrique. 2019. Asymmetry and the Moderating Effects of Formal Institutional Distance on the Relationship between Cultural Distance and Performance: The Case of Multinational Foreign Subsidiaries in Latin America. Halmstad University, The Direction of Cultural Distance and the Performance of Foreign Subsidiaries in Latin America Dissertations No. 61. Halmstad: Halmstad University Press. [Google Scholar]

- Coyne, Christopher J., and Claudia R. Williamson. 2009. Trade Openness and Culture. No. 09-05. Morgantown: Department of Economics, West Virginia University. [Google Scholar]

- Cuervo-Cazurra, Alvaro, and Mehmet Erdem Genc. 2011. Obligating, pressuring, and supporting dimensions of the environment and the non-market advantages of developing-country multinational companies. Journal of Management Studies 48: 441–55. [Google Scholar] [CrossRef]

- Dikova, Desislava. 2009. Performance of foreign subsidiaries: Does psychic distance matter? International Business Review 18: 38–49. [Google Scholar] [CrossRef]

- Dow, Douglas. 2017. Are we at a Turning Point for Distance Research in International Business Studies? In Distance in International Business: Concept, Cost and Value. Bingley: Emerald Publishing Limited. [Google Scholar] [CrossRef]

- Drogendijk, Rian, and Arjen Slangen. 2006. Hofstede, Schwartz, or managerial perceptions? The effects of different cultural distance measures on establishment mode choices by multinational enterprises. International Business Review 15: 361–80. [Google Scholar] [CrossRef] [Green Version]

- Efron, Bradley, and Gail Gong. 1983. A leisurely look at the bootstrap, the jackknife, and cross-validation. The American Statistician 37: 36–48. [Google Scholar]

- Estrin, Saul, Delia Baghdasaryan, and Klaus E. Meyer. 2009. The impact of institutional and human resource distance on international entry strategies. Journal of Management Studies 46: 1171–96. [Google Scholar] [CrossRef] [Green Version]

- Gani, Azmat. 2007. Governance and foreign direct investment links: Evidence from panel data estimations. Applied Economics Letters 14: 753–56. [Google Scholar] [CrossRef]

- Globerman, Steven, and Daniel Shapiro. 2003. Governance infrastructure and US foreign direct investment. Journal of International Business Studies 34: 19–39. [Google Scholar] [CrossRef]

- Hall, Peter A., and David Soskice. 2001. Varieties of Capitalism: The Institutional Foundations of Comparative Advantage. Oxford: OUP Oxford. [Google Scholar]

- Hayes, Andrew F. 2013. Introduction to Mediation, Moderation, and Conditional Process Analysis: A Regression-Based Approach, 2nd ed. New York: Guilford Publications. [Google Scholar]

- Hernández, Virginia, and Maria J. Nieto. 2015. The effect of the magnitude and direction of institutional distance on the choice of international entry modes. Journal of World Business 50: 122–32. [Google Scholar] [CrossRef]

- Hitt, Michael A., M. Tina Dacin, Beverly B. Tyler, and Daewoo Park. 1997. Understanding the Differences in Korean and US Executives’Strategic Orientations. Strategic Management Journal 18: 159–67. [Google Scholar] [CrossRef]

- Hofstede, Geert. 1980. Culture’s Consequences. International Differences in Work-Related Values. Newcastle upon Tyne: Sage. [Google Scholar]

- Hofstede, Geert, Gert Jan Hofstede, and Michael Minkov. 2010. Cultures and Organizations. New York: Mc Graw Hill. [Google Scholar]

- Ionascu, Delia, Klaus E. Meyer, and Saul Estrin. 2004. Institutional Distance and International Business Strategies in Emerging Economies. No. wp728. Michigan: William Davidson Institute at the University of Michigan. [Google Scholar]

- Kaufmann, Daniel, Aart Kraay, and Massimo Mastruzzi. 2009. Governance Matters VIII: Aggregate and Individual Governance Indicators, 1996–2008. World Bank Policy Research Working Paper No. 4978. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=1424591 (accessed on 24 January 2022).

- Kaufmann, Daniel, Aart Kraay, and Massimo Mastruzzi. 2011. The Worldwide Governance Indicators: Methodology and Analytical Issues1. Hague Journal on the Rule of Law 3: 220–46. [Google Scholar] [CrossRef]

- Kirkman, Bradley L., Kevin B. Lowe, and Cristina B. Gibson. 2006. A quarter century of culture’s consequences: A review of empirical research incorporating Hofstede’s cultural values framework. Journal of International Business Studies 37: 285–320. [Google Scholar] [CrossRef]

- Kogut, Bruce, and Harbir Singh. 1988. The effect of national culture on the choice of entry mode. Journal of International Business Studies 19: 411–32. [Google Scholar] [CrossRef]

- Kolstad, Ivar, and Arne Wiig. 2012. What determines Chinese outward FDI? Journal of World Business 47: 26–34. [Google Scholar] [CrossRef]

- Konara, Palitha, and Vikrant Shirodkar. 2018. Regulatory institutional distance and MNCs’ subsidiary performance: Climbing up vs. climbing down the institutional ladder. Journal of International Management 24: 333–47. [Google Scholar] [CrossRef]

- Kostova, Tatiana. 1996. Success of the Transnational Transfer of Organizational Practices within Multinational Companies. Unpublished Doctoral dissertation, University of Minnesota, Minneapolis, MI, USA. [Google Scholar]

- Kostova, Tatiana, Sjoerd Beugelsdijk, W. Richard Scott, Vincent E. Kunst, Chei Hwee Chua, and Marc van Essen. 2020. The construct of institutional distance through the lens of different institutional perspectives: Review, analysis, and recommendations. Journal of International Business Studies 51: 467–97. [Google Scholar] [CrossRef]

- Lee, Dongyoung, and He Wen. 2020. Financial analyst coverage for US firms facing foreign competition: Evidence from trade liberalization. Journal of International Financial Management & Accounting 31: 139–68. [Google Scholar]

- Lu, Xun, and Halbert White. 2014. Robustness checks and robustness tests in applied economics. Journal of Econometrics 178: 194–206. [Google Scholar] [CrossRef]

- MacKinnon, James G., and Halbert White. 1985. Some heteroskedasticity-consistent covariance matrix estimators with improved finite sample properties. Journal of Econometrics 29: 305–25. [Google Scholar] [CrossRef] [Green Version]

- Magnani, Giovanna, Antonela Zucchella, and Dinora E. Floriani. 2018. The logic behind foreign market selection: Objective distance dimensions vs. strategic objectives and psychic distance. International Business Review 27: 1–20. [Google Scholar] [CrossRef] [Green Version]

- Maseland, Robbert. 2013. Parasitical cultures? The cultural origins of institutions and development. Journal of Economic Growth 18: 109–36. [Google Scholar] [CrossRef]

- Mengistu, Alemu A., and Bishnu K. Adhikary. 2011. Does good governance matter for FDI inflows? Evidence from Asian economies. Asia Pacific Business Review 17: 281–99. [Google Scholar] [CrossRef]

- Meyer, Klaus E., Saul Estrin, Sumon K. Bhaumik, and Mike W. Peng. 2009. Institutions, resources, and entry strategies in emerging economies. Strategic Management Journal 30: 61–80. [Google Scholar] [CrossRef] [Green Version]

- Michael Geringer, J., Paul W. Beamish, and Richard C. DaCosta. 1989. Diversification strategy and internationalization: Implications for MNE Performance. Strategic Management Journal 10: 109–19. [Google Scholar] [CrossRef]

- North, Douglas. 1990. Institutions, Institutional Change and Economic Performance. Cambridge: Cambridge University Press. [Google Scholar]

- Orlova, Svetlana V. 2020. Cultural and macroeconomic determinants of cash holdings management. Journal of International Financial Management & Accounting 31: 270–94. [Google Scholar]

- Pejovich, Svetozar. 1999. A Property Rights Analysis of the American Welfare State. Journal of Public Finance and Public Choice 17: 79–91. [Google Scholar] [CrossRef]

- Peng, Mike W., Sunny Li Sun, Brian Pinkham, and Hao Chen. 2009. The institution-based view as a third leg for a strategy tripod. Academy of Management Perspectives 23: 63–81. [Google Scholar] [CrossRef] [Green Version]

- Pizzi, Simone, Baldo Del Mara, Caputo Fabio, and Andrea Venturelli. 2021. Voluntary disclosure of Sustainable Development Goals in mandatory non-financial reports: The moderating role of cultural dimension. Journal of International Financial Management and Accounting 33: 83–106. [Google Scholar] [CrossRef]

- Reyes, Armando B., William Newburry, Jorge Carneiro, and Carlos Cordova. 2019. Using Latin America as a research laboratory: The moderating effect of trade openness on the relationship between inward and outward FDI. Multinational Business Review 27: 122–40. [Google Scholar] [CrossRef]

- Rogerson, Peter A. 2001. Data reduction: Factor analysis and cluster analysis. Statistical Methods for Geography 2001: 192–97. [Google Scholar]

- Salomon, Robert, and Zheying Wu. 2012. Institutional distance and local isomorphism strategy. Journal of International Business Studies 3: 343–67. [Google Scholar] [CrossRef]

- Scott, W. Richard. 1995. Institutions and Organizations. Newcastle upon Tyne: Sage. [Google Scholar]

- Selmer, Jan, Randy K. Chiu, and Oded Shenkar. 2007. Cultural distance asymmetry in expatriate adjustment. Cross Cultural Management: An International Journal 14: 150–60. [Google Scholar] [CrossRef]

- Shenkar, Oded. 2001. Cultural distance revisited: Towards a more rigorous conceptualization and measurement of cultural differences. Journal of International Business Studies 32: 519–35. [Google Scholar] [CrossRef]

- Shenkar, Oded. 2012. Beyond cultural distance: Switching to a friction lens in the study of cultural differences. Journal of International Business Studies 43: 12–17. [Google Scholar] [CrossRef]

- Shenkar, Oded, Stephen B. Tallman, Hao Wang, and Jie Wu. 2020. National culture and international business: A path forward. Journal of International Business Studies 53: 1–18. [Google Scholar] [CrossRef]

- Shenkar, Oded, Yadong Luo, and Orly Yeheskel. 2008. From “distance” to “friction”: Substituting metaphors and redirecting intercultural research. Academy of Management Review 33: 905–23. [Google Scholar] [CrossRef]

- Singh, Vikkram, Bin Li, and Eduardo Roca. 2017. How pervasive is the effect of culture on stock market linkages? Evidence across regions and economic cycles. Applied Economics 49: 4209–30. [Google Scholar] [CrossRef] [Green Version]

- Slangen, Arjen H., and Sjoerd Beugelsdijk. 2010. The impact of institutional hazards on foreign multinational activity: A contingency perspective. Journal of International Business Studies 41: 980–95. [Google Scholar] [CrossRef]

- Stein, Ernesto, and Christian Daude. 2001. Institutions, Integration and the Location of Foreign Direct Investment. In Global Forum on International Investment: New horizons for Foreign Direct Investment. Santiago: Chile, pp. 101–30. Available online: http://citeseerx.ist.psu.edu/viewdoc/download?doi=10.1.1.201.2180&rep=rep1&type=pdf (accessed on 20 January 2022).

- Venkatraman, Natarjan, and Vasudevan Ramanujam. 1986. Measurement of business performance in strategy research: A comparison of approaches. Academy of Management Review 11: 801–14. [Google Scholar] [CrossRef] [Green Version]

- Verbeke, Alain, Rob van Tulder, and Jonas Puck. 2017. Distance in International Business Studies: Concept, Cost and Value. In Distance in International Business: Concept, Cost and Value. Bingley: Emerald Publishing Limited. [Google Scholar] [CrossRef]

- Wang, Yi, and Jorma Larimo. 2020. Survival of full versus partial acquisitions: The moderating role of firm’s internationalization experience, cultural distance, and host country context characteristics. International Business Review 29: 101605. [Google Scholar] [CrossRef]

- Wernick, David A., Jerry Haar, and Shane Singh. 2009. Do governing institutions affect foreign direct investment inflows? New evidence from emerging economies. International Journal of Economics and Business Research 1: 317–32. [Google Scholar] [CrossRef]

- Whetten, David A. 1989. What constitutes a theoretical contribution? Academy of Management Review 14: 490–95. [Google Scholar] [CrossRef]

- White, Halbert. 1980. A heteroskedasticity-consistent covariance matrix estimator and a direct test for heteroskedasticity. Econometrica: Journal of the Econometric Society 48: 817–38. [Google Scholar] [CrossRef]

- Zaheer, Srilata. 1995. Overcoming the liability of foreignness. Academy of Management Journal 38: 341–63. [Google Scholar] [CrossRef]

- Zaheer, Srilata, Margaret S. Schomaker, and Lilach Nachum. 2012. Distance without direction: Restoring credibility to a much-loved construct. Journal of International Business Studies 43: 18–27. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

| Hypothesis H1 | Hypothesis H2 | |||

|---|---|---|---|---|

| CD | Governance Low (−1 std. Deviation) | Governance Intermediate | Governance High (+1 std. Deviation) | |

| Const | −88.191 *** | −87.036 *** | −87.945 *** | −88.855 *** |

| (7.301) | (7.293) | (7.301) | (7.311) | |

| [0.000] | [0.000] | [0.000] | [0.000] | |

| Industry or Service (dummy) | −1.444 *** | −1.518 *** | −1.518 *** | −1.518 *** |

| (0.382) | (0.383) | (0.383) | (0.383) | |

| [0.000] | [0.000] | [0.000] | [0.000] | |

| Total Assets | 0.000 *** | 0.000 *** | 0.000 *** | 0.000 *** |

| (0.000) | (0.000) | (0.000) | (0.000) | |

| [0.000] | [0.000] | [0.000] | [0.000] | |

| Sales Revenues | −0.000 | −0.000 | −0.000 | −0.000 |

| (0.000) | (0.000) | (0.000) | (0.000) | |

| [0.782] | [0.844] | [0.844] | [0.844] | |

| Market Share | −27,525.038 *** | −27,583.179 *** | −27,583.179 *** | −27,583.179 *** |

| (6637.171) | (6636.949) | (6636.949) | (6636.949) | |

| [0.000] | [0.000] | [0.000] | [0.000] | |

| Subsidiary Annual Sales Growth | −0.003 *** | −0.003 *** | −0.003 *** | −0.003 *** |

| (0.001) | (0.001) | (0.001) | (0.001) | |

| [0.001] | [0.001] | [0.001] | [0.001] | |

| Industry Annual Growth | 0.023 | 0.019 | 0.019 | 0.019 |

| (0.048) | (0.048) | (0.048) | (0.048) | |

| [0.632] | [0.694] | [0.694] | [0.694] | |

| Home Country | ||||

| Home Country GDP | 0.479 | 0.527 | 0.527 | 0.527 |

| (0.321) | (0.322) | (0.322) | (0.322) | |

| [0.136] | [0.102] | [0.102] | [0.102] | |

| Home Country Trade Openness | 0.004 | 0.004 | 0.004 | 0.004 |

| (0.003) | (0.003) | (0.003) | (0.003) | |

| [0.298] | [0.225] | [0.225] | [0.225] | |

| Home Country Governance | 1.621 *** | 1.569 *** | 1.569 *** | 1.569 *** |

| (0.344) | (0.344) | (0.344) | (0.344) | |

| [0.000] | [0.000] | [0.000] | [0.000] | |

| Host Country | ||||

| Host Country GDP | 7.144 *** | 7.092 *** | 7.092 *** | 7.092 *** |

| (0.546) | (0.546) | (0.546) | (0.546) | |

| [0.000] | [0.000] | [0.000] | [0.000] | |

| Host Country Trade Openness | 0.224 *** | 0.223 *** | 0.223 *** | 0.223 *** |

| (0.014) | (0.014) | (0.014) | (0.014) | |

| [0.000] | [0.000] | [0.000] | [0.000] | |

| Host Country Governance | 4.583 *** | 6.434 *** | ||

| (0.452) | (0.714) | |||

| [0.000] | [0.000] | |||

| CD_KS (main effect under investigation) | −0.664 *** | −1.033 *** | −0.806 *** | −0.578 ** |

| (0.245) | (0.269) | (0.249) | (0.247) | |

| [0.007] | [0.000] | [0.001] | [0.019] | |

| Host Country Governance Low | 6.434 *** | |||

| (0.714) | ||||

| [0.000] | ||||

| CD_KS * Host Country Governance Low | −1.611 *** | |||

| (0.480) | ||||

| [0.001] | ||||

| CD_KS * Host Country Governance Intermediate | −1.611 *** | |||

| (0.480) | ||||

| [0.001] | ||||

| Host Country Governance High | 6.434 *** | |||

| (0.714) | ||||

| [0.000] | ||||

| CD_KS * Host Country Governance High | −1.611 *** | |||

| (0.480) | ||||

| [0.001] | ||||

| Number of observations | 47,714 | 47,714 | 47,714 | 47,714 |

| Adj. R2 | 0.031 | 0.033 | 0.033 | 0.033 |

| P-value(F) | 0.000 | 0.000 | 0.000 | 0.000 |

| 1996 | 2000 | 2005 | 2010 | 2015 | 2020 | |

| Argentina | 0.19 | 0.08 | −0.23 | −0.27 | −0.31 | −0.12 |

| Brazil | −0.01 | 0.13 | −0.07 | 0.13 | −0.13 | −0.21 |

| Chile | 1.14 | 1.14 | 1.25 | 1.22 | 1.08 | 0.89 |

| Colombia | −0.66 | −0.59 | −0.55 | −0.36 | −0.20 | −0.14 |

| Ecuador | −0.45 | −0.61 | −0.73 | −0.78 | −0.61 | −0.46 |

| Mexico | −0.31 | −0.01 | −0.10 | −0.17 | −0.25 | −0.41 |

| Panama | 0.13 | 0.21 | 0.02 | 0.09 | 0.19 | 0.08 |

| Peru | −0.36 | −0.34 | −0.43 | −0.24 | −0.16 | −0.10 |

| Uruguay | 0.76 | 0.76 | 0.68 | 0.84 | 0.86 | 0.97 |

| Venezuela, RB | −0.52 | −0.60 | −1.03 | −1.29 | −1.43 | −1.82 |

| Hypothesis H3 | |||

|---|---|---|---|

| Trade Openness Low (−1 std. Deviation) | Trade Openness Intermediate | Trade Openness High (+1 std. Deviation) | |

| Const | −81.870 *** | −84.080 *** | −86.290 *** |

| (7.294) | (7.388) | (7.491) | |

| [0.000] | [0.000] | [0.000] | |

| Industry or Service (dummy) | −1.437 *** | −1.437 *** | −1.437 *** |

| (0.382) | (0.382) | (0.382) | |

| [0.000] | [0.000] | [0.000] | |

| Total Assets | 0.000 *** | 0.000 *** | 0.000 *** |

| (0.000) | (0.000) | (0.000) | |

| [0.000] | [0.000] | [0.000] | |

| Sales Revenues | −0.000 | −0.000 | −0.000 |

| (0.000) | (0.000) | (0.000) | |

| [0.701] | [0.701] | [0.701] | |

| Market Share | −22,801.866 *** | −22,801.866 *** | −22,801.866 *** |

| (6763.173) | (6763.173) | (6763.173) | |

| [0.001] | [0.001] | [0.001] | |

| Subsidiary Annual Sales Growth | −0.003 *** | −0.003 *** | −0.003 *** |

| (0.001) | (0.001) | (0.001) | |

| [0.001] | [0.001] | [0.001] | |

| Industry Annual Growth | 0.029 | 0.029 | 0.029 |

| (0.048) | (0.048) | (0.048) | |

| [0.549] | [0.549] | [0.549] | |

| Home Country | |||

| Home Country GDP | 0.473 | 0.473 | 0.473 |

| (0.321) | (0.321) | (0.321) | |

| [0.141] | [0.141] | [0.141] | |

| Home Country Trade Openness | 0.004 | 0.004 | 0.004 |

| (0.003) | (0.003) | (0.003) | |

| [0.267] | [0.267] | [0.267] | |

| Home Country Governance | 1.642 *** | 1.642 *** | 1.642 *** |

| (0.344) | (0.344) | (0.344) | |

| [0.000] | [0.000] | [0.000] | |

| Host Country | |||

| Host Country GDP | 7.000 *** | 7.000 *** | 7.000 *** |

| (0.548) | (0.548) | (0.548) | |

| [0.000] | [0.000] | [0.000] | |

| Host Country Trade Openness | 0.167 *** | ||

| (0.021) | |||

| [0.000] | |||

| Host Country Governance | 4.734 *** | 4.734 *** | 4.734 *** |

| (0.454) | (0.454) | (0.454) | |

| [0.000] | [0.000] | [0.000] | |

| CD_KS (main effect under investigation) | −1.738 *** | −2.173 *** | −2.609 *** |

| (0.384) | (0.482) | (0.589) | |

| [0.000] | [0.000] | [0.000] | |

| Host Country Trade Openness Low | 0.167 *** | ||

| (0.021) | |||

| [0.000] | |||

| CD_KS * Host Country Trade Openness Low | 0.033 *** | ||

| (0.009) | |||

| [0.000] | |||

| CD_KS * Host Country Trade Openness Intermediate | 0.033 *** | ||

| (0.009) | |||

| [0.000] | |||

| Host Country Trade Openness High | 0.167 *** | ||

| (0.021) | |||

| [0.000] | |||

| CD_KS * Host Country Trade Openness High | 0.033 *** | ||

| (0.009) | |||

| [0.000] | |||

| Number of observations | 47,714 | 47,714 | 47,714 |

| Adj. R2 | 0.033 | 0.033 | 0.033 |

| P-value(F) | 0.000 | 0.000 | 0.000 |

| 1980 | 1985 | 1990 | 1995 | 2000 | 2005 | 2010 | 2015 | 2020 | |

| Argentina | 11.5 | 18.0 | 15.0 | 19.8 | 22.6 | 40.6 | 35.0 | 22.5 | 30.1 |

| Brazil | 20.2 | 20.4 | 15.2 | 17.0 | 22.6 | 27.1 | 22.8 | 27.0 | 32.4 |

| Chile | 48.1 | 50.6 | 61.7 | 55.0 | 59.3 | 71.6 | 69.1 | 59.0 | 57.8 |

| Colombia | 31.8 | 26.3 | 34.8 | 35.5 | 32.7 | 37.4 | 34.3 | 38.4 | 33.7 |

| Ecuador | 35.0 | 35.7 | 44.6 | 45.9 | 59.5 | 56.1 | 60.3 | 45.2 | 43.3 |

| Mexico | 22.4 | 24.3 | 38.5 | 46.3 | 52.4 | 53.9 | 60.8 | 71.1 | 78.2 |

| Panama | 137.5 | 94.1 | 121.8 | 146.9 | 134.0 | 135.7 | 148.3 | 99.9 | 74.1 |

| Peru | 47.6 | 44.9 | 29.5 | 30.9 | 35.5 | 47.4 | 51.7 | 45.2 | 43.4 |

| Uruguay | 35.7 | 47.9 | 41.6 | 38.1 | 36.7 | 58.9 | 51.7 | 45.3 | 46.4 |

| Venezuela, RB | 57.4 | 39.4 | 57.7 | 47.3 | 47.9 | 60.1 | 46.1 | ||

| Latin America & Caribbean | 30.3 | 29.6 | 33.1 | 35.2 | 39.2 | 45.7 | 44.0 | 44.5 | 46.6 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Correa da Cunha, H.; Ruzgar, N.S.; Singh, V. The Moderating Effects of Host Country Governance and Trade Openness on the Relationship between Cultural Distance and Financial Performance of Foreign Subsidiaries in Latin America. Int. J. Financial Stud. 2022, 10, 26. https://doi.org/10.3390/ijfs10020026

Correa da Cunha H, Ruzgar NS, Singh V. The Moderating Effects of Host Country Governance and Trade Openness on the Relationship between Cultural Distance and Financial Performance of Foreign Subsidiaries in Latin America. International Journal of Financial Studies. 2022; 10(2):26. https://doi.org/10.3390/ijfs10020026

Chicago/Turabian StyleCorrea da Cunha, Henrique, Nursel Selver Ruzgar, and Vikkram Singh. 2022. "The Moderating Effects of Host Country Governance and Trade Openness on the Relationship between Cultural Distance and Financial Performance of Foreign Subsidiaries in Latin America" International Journal of Financial Studies 10, no. 2: 26. https://doi.org/10.3390/ijfs10020026

APA StyleCorrea da Cunha, H., Ruzgar, N. S., & Singh, V. (2022). The Moderating Effects of Host Country Governance and Trade Openness on the Relationship between Cultural Distance and Financial Performance of Foreign Subsidiaries in Latin America. International Journal of Financial Studies, 10(2), 26. https://doi.org/10.3390/ijfs10020026