Business Time Sampling Scheme with Applications to Testing Semi-Martingale Hypothesis and Estimating Integrated Volatility

Abstract

1. Introduction

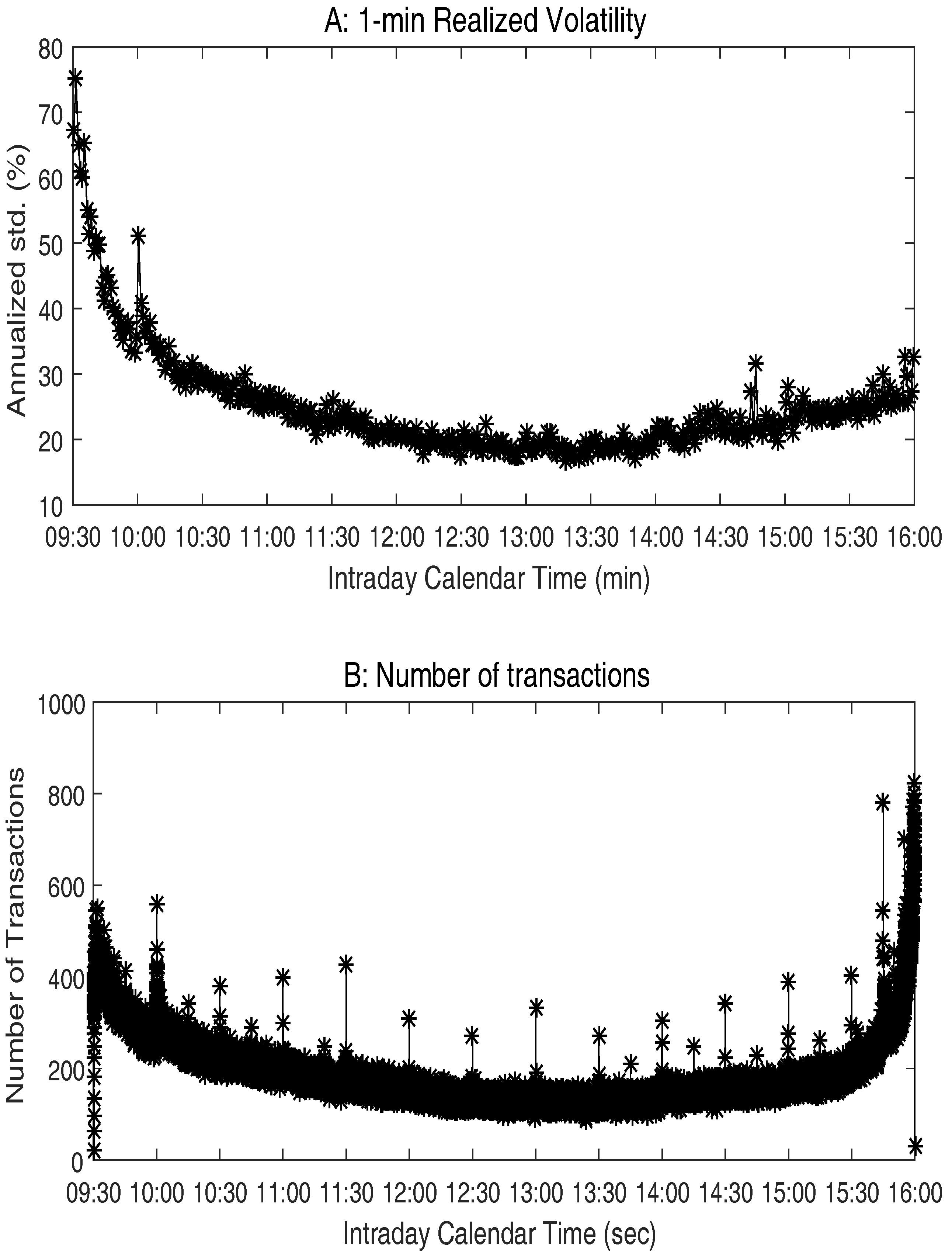

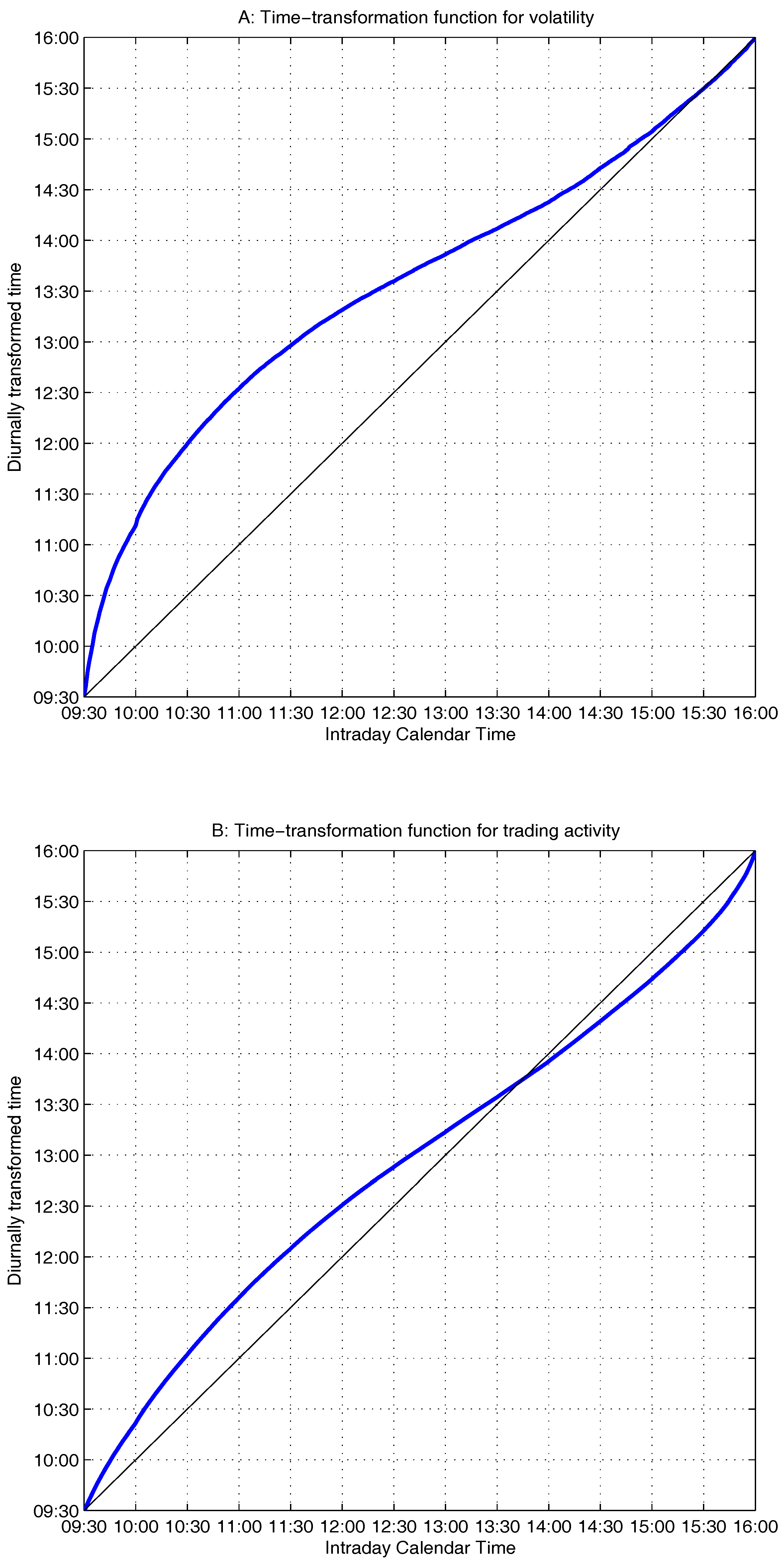

2. Intraday Periodicity and the BTS Scheme

3. Testing the Semi-Martingale Hypothesis Using BTS Returns

3.1. The Semi-Martingale Hypothesis

3.2. Empirical Results of the Tests

4. Estimation of Integrated Volatility

4.1. Integrated Volatility Estimation Using BT Returns

4.2. Integrated Volatility Estimation Using the Modified ACD-ICV Method

5. Monte Carlo Study

5.1. Simulation Models

5.2. Simulation Results

6. Conclusions

Supplementary Materials

Acknowledgments

Author Contributions

Conflicts of Interest

Appendix A

Appendix A.1. Jump Detection Procedure

Appendix A.2. Computation of the BT Time-Transformation Function

References

- Aït-Sahalia, Yacine, and Loriano Mancini. 2008. Out of sample forecasts of quadratic variation. Journal of Econometrics 147: 17–33. [Google Scholar] [CrossRef]

- Andersen, Torben G., Tim Bollerslev, and Dobrislav Dobrev. 2007. No-arbitrage semi-martingale restrictions for continuous-time volatility models subject to leverage effects, jumps and iid noise: Theory and testable distributional implications. Journal of Econometrics 138: 125–80. [Google Scholar] [CrossRef]

- Andersen, Torben G., Tim Bollerslev, Per Frederiksen, and Ørregaard Nielsen. 2010. Continuous-time models, realized volatilities, and testable distributional implications for daily stock returns. Journal of Applied Econometrics 25: 233–61. [Google Scholar] [CrossRef]

- Andersen, Torben G., Dobrislav Dobrev, and Ernst Schaumburg. 2012. Jump-robust volatility estimation using nearest neighbor truncation. Journal of Econometrics 169: 75–93. [Google Scholar] [CrossRef]

- Andersen, Torben G., Dobrislav Dobrev, and Ernst Schaumburg. 2014. A robust neighborhood truncation approach to estimation of integrated quarticity. Econometric Theory 30: 3–59. [Google Scholar] [CrossRef]

- Bajgrowicz, Pierre, Olivier Scaillet, and Adrien Treccani. 2016. Jumps in high-frequency data: Spurious detections, dynamics, and news. Management Science 62: 2198–217. [Google Scholar] [CrossRef]

- Barndorff-Nielsen, Ole E., and Neil Shephard. 2004. Power and bipower variation with stochastic volatility and jumps. Journal of Financial Econometrics 2: 1–37. [Google Scholar] [CrossRef]

- Barndorff-Nielsen, Ole E., and Neil Shephard. 2006. Econometrics of testing for jumps in financial economics using bipower variation. Journal of financial Econometrics 4: 1–30. [Google Scholar] [CrossRef]

- Barndorff-Nielsen, Ole E., Neil Shephard, and Matthias Winkel. 2006. Limit theorems for multipower variation in the presence of jumps. Stochastic Processes and Their Applications 116: 796–806. [Google Scholar] [CrossRef]

- Barndorff-Nielsen, Ole E., Peter Reinhard Hansen, Asger Lunde, and Neil Shephard. 2008. Designing realized kernels to measure the ex post variation of equity prices in the presence of noise. Econometrica 76: 1481–536. [Google Scholar]

- Boudt, Kris, Christophe Croux, and Sébastien Laurent. 2011. Robust estimation of intraweek periodicity in volatility and jump detection. Journal of Empirical Finance 18: 353–67. [Google Scholar] [CrossRef]

- Christensen, Kim, Roel Oomen, and Mark Podolskij. 2010. Realised quantile-based estimation of the integrated variance. Journal of Econometrics 159: 74–98. [Google Scholar] [CrossRef]

- Dacorogna, Michael M., Ulrich A. Müller, Robert J. Nagler, Richard B. Olsen, and Olivier V. Pictet. 1993. A geographical model for the daily and weekly seasonal volatility in the foreign exchange market. Journal of International Money and Finance 12: 413–38. [Google Scholar] [CrossRef]

- Dambis, Karl E. 1965. On the decomposition of continuous submartingales. Theory of Probability & Its Applications 10: 401–10. [Google Scholar]

- Dong, Yingjie, and Yiu-Kuen Tse. 2017. On estimating market microstructure noise variance. Economics Letters 150C: 59–62. [Google Scholar] [CrossRef]

- Dubins, Lester E., and Gideon Schwarz. 1965. On continuous martingales. Proceedings of the National Academy of Sciences of the United States of America 53: 913. [Google Scholar] [CrossRef] [PubMed]

- Engle, Robert F., and Jeffrey R. Russell. 1998. Autoregressive conditional duration: A new model for irregularly spaced transaction data. Econometrica 66: 1127–62. [Google Scholar] [CrossRef]

- Fernandes, Marcelo, and Joachim Grammig. 2006. A family of autoregressive conditional duration models. Journal of Econometrics 130: 1–23. [Google Scholar] [CrossRef]

- Hasbrouck, Joel. 1999. The dynamics of discrete bid and ask quotes. The Journal of Finance 54: 2109–42. [Google Scholar] [CrossRef]

- Heston, Steven L. 1993. A closed-form solution for options with stochastic volatility with applications to bond and currency options. Review of Financial Studies 6: 327–43. [Google Scholar] [CrossRef]

- Huang, Xin, and George Tauchen. 2005. The relative contribution of jumps to total price variance. Journal of Financial Econometrics 3: 456–99. [Google Scholar] [CrossRef]

- Jacod, Jean, and Mathieu Rosenbaum. 2013. Quarticity and other functionals of volatility: Efficient estimation. The Annals of Statistics 41: 1462–84. [Google Scholar] [CrossRef]

- Lee, Suzanne S., and Jan Hannig. 2010. Detecting jumps from Lévy jump diffusion processes. Journal of Financial Economics 96: 271–90. [Google Scholar] [CrossRef]

- Lee, Suzanne S., and Per A. Mykland. 2008. Jumps in financial markets: A new nonparametric test and jump dynamics. The Review of Financial Studies 21: 2535–63. [Google Scholar] [CrossRef]

- Lilliefors, Hubert W. 1967. On the Kolmogorov-Smirnov test for normality with mean and variance unknown. Journal of the American Statistical Association 62: 399–402. [Google Scholar] [CrossRef]

- Mykland, Per A. 2012. A Gaussian calculus for inference from high frequency data. Annals of Finance 8: 235–58. [Google Scholar] [CrossRef]

- Nowman, Khalid B. 1997. Gaussian Estimation of Single-Factor Continuous Time Models of The Term Structure of Interest Rates. The Journal of Finance 52: 1695–706. [Google Scholar] [CrossRef]

- Oomen, Roel C. A. 2006. Properties of realized variance under alternative sampling schemes. Journal of Business & Economic Statistics 24: 219–37. [Google Scholar]

- Peters, Remco T., and Robin G. De Vilder. 2006. Testing the continuous semimartingale hypothesis for the S&P 500. Journal of Business & Economic Statistics 24: 444–54. [Google Scholar]

- Tse, Yiu-Kuen, and Thomas Tao Yang. 2012. Estimation of high-frequency volatility: An autoregressive conditional duration approach. Journal of Business & Economic Statistics 30: 533–45. [Google Scholar]

- Tse, Yiu-Kuen, and Yingjie Dong. 2014. Intraday Periodicity Adjustments of Transaction Duration and Their Effects on High-Frequency Volatility Estimation. Journal of Empirical Finance 28: 352–61. [Google Scholar] [CrossRef]

- Zhou, Bin. 1998. F-consistency, De-volatilization and normalization of high-frequency financial data. In Nonlinear Modelling of High Frequency Financial Time Series. Edited by Christian Dunis and Bin Zhou. New York: Wiley, pp. 109–23. [Google Scholar]

| 1. | Dambis (1965) and Dubins and Schwarz (1965) show that a process compiled from a continuous local martingale with equal quadratic-variation increments is a Brownian motion. Leverage effect refers to the asymmetry between equity returns and volatility. That is, large negative returns tend to be associated with higher future volatility than positive returns of the same magnitude. Feedback effect refers to the case when the volatility function is correlated over time. |

| 2. | Results for other stocks can be found in the online supplementary material (Figure S1). |

| 3. | One drawback of the jump detection methods is the presence of the spurious detections due to multiple testing issues. See Bajgrowicz et al. (2016) for a discussion. |

| 4. | As there are 6.5 h of trades in a trading day for the NYSE, for m trading days we have s. at calendar time t (in s) is an increasing function of t, with , and . |

| 5. | Here, are calendar-time points which need not to be regularly spaced. We outline the detailed steps in calculating and , for , in the Appendix A. can be any suitable estimates of intraday integrated volatility. In this paper we use the TRV method of Barndorff-Nielsen et al. (2006) to calculate for its robustness to jumps. |

| 6. | We use the Matlab (2015a, Mathworks, Natick, MA, United States) command pchip in this paper. Given and the calendar-time point t, the diurnally transformed time is . Conversely, given and a diurnally transformed time , the corresponding calendar time is . |

| 7. | In the empirical applications in this paper, the time-transformation function for BTS is extended over the whole sample period, which takes account of varying volatility over different trading days. |

| 8. | The jump-adjustment procedure can be found in the Appendix A. |

| 9. | The Brownian semimartingale process can be defined as , where is the drift term, the instantaneous volatility process is càdlàg, and denotes a standard Brownian motion independent of the drift. In this paper, we further add jumps to the Brownian semimartingale and assume the price process to be a generic jump-diffusion process. That is, , where when there is a jump at time t, and otherwise, and denotes the jump size if a jump occurs at time t. We assume the jump component to be a finite activity jump process. Note that when there are infinite number of jumps in the data, our BTS method will work if we select BTS transactions based on estimated integrated volatility that are robust to the presence of Lévy-type jumps. See Lee and Hannig (2010) for the evidence of the presence of the Lévy-type jumps and see Barndorff-Nielsen et al. (2006) for an analysis of the multipower variation estimates when there are infinite number of jumps. |

| 10. | Note that, given and , is the minimum business time so that the integrated volatility over the interval reaches . |

| 11. | As our focus here is the testing of the semi-martingale hypothesis, the results of the jump detection are not presented. Details of the selected stocks and results of the jump tests can be found in the supplementary material (Tables S1–S3) for which sampling frequencies of 1 min, 5 min and 10 min are used. When the sampling frequency is equal to 1 min, more than 12 stocks report jump proportions with values exceeding 10% under all sampling schemes. This suggests that sampling frequency that is too high (such as 1 min) may render misleading results when they are used for jump detection using the method of Andersen et al. (2010). See Oomen (2006) for an analysis of the performance of the realized variance estimator among alternative sampling schemes. |

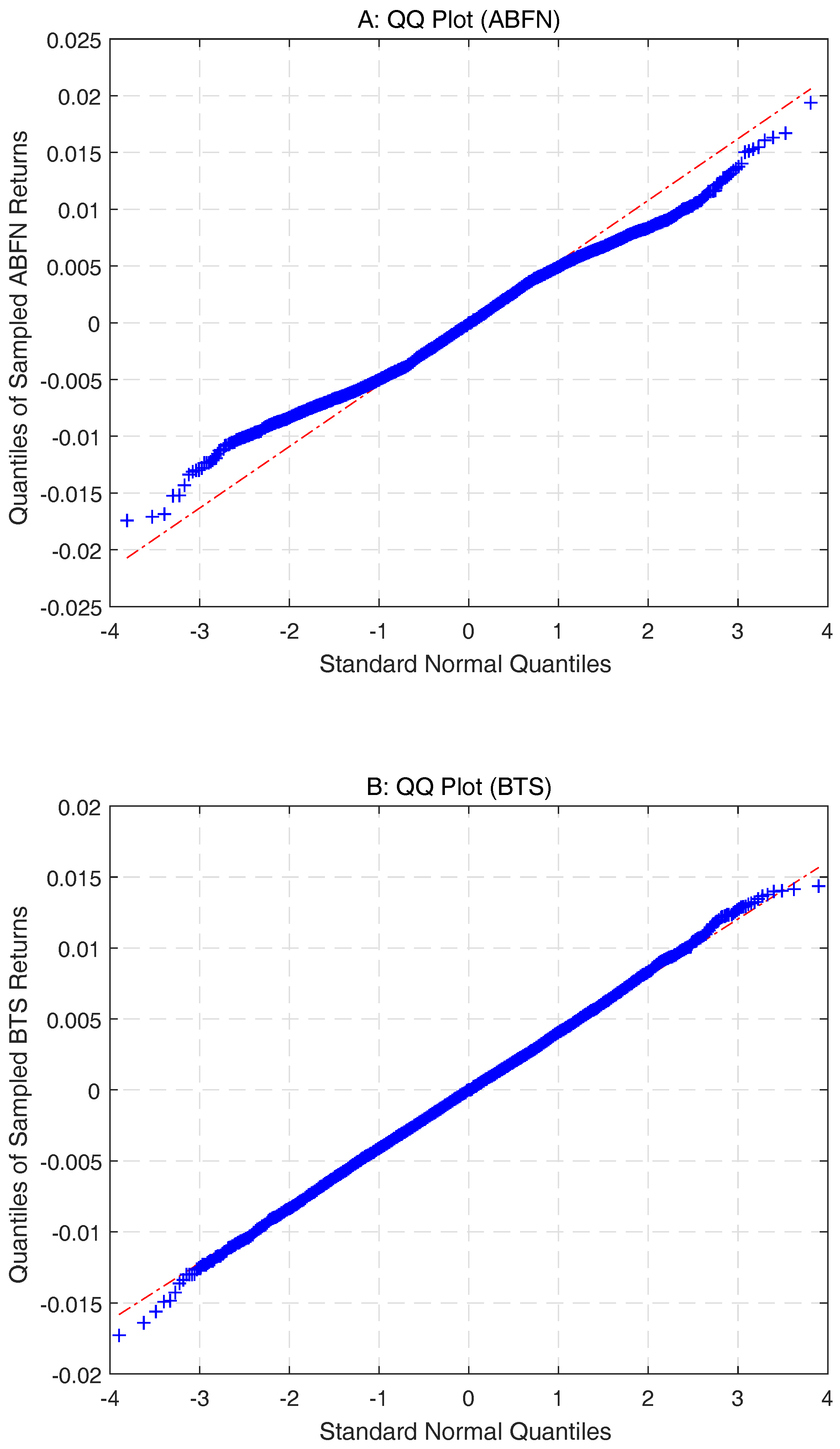

| 12. | QQ plots of the jump-adjusted ABFN returns and BTS returns at daily and weekly frequencies are very similar. We also calculate the ACF values of the sampled 30 min returns up to lag 150. All returns sampled using various methods exhibit no periodicity. The correlation between the ABFN returns and BTS returns increases as the sampling frequency decreases, and the value is around 13.5% at weekly frequency. |

| 13. | We do not use the bipower realized volatility method here since the TRV method is more robust to the presence of jumps, especially when the sampling frequency is high. |

| 14. | Note that, for ME1 and ME2, the returns are sampled by price events and the ACD models are fitted to diurnally transformed durations using the time-transformation function based on the number of trades. |

| 15. | The RK method is selected for comparison due to its superior performance among the RV estimators (see Barndorff-Nielsen et al. (2008)). To calculate the bandwidth of the RK method, we use the subsampling realized volatility estimator and 3 min TTS returns. For the ACD-ICV methods, all results in this paper are based on conditional duration models fitted using the power ACD (PACD) model (see Fernandes and Grammig 2006). |

| 16. | Sparsity occurs as empirically transactions are not observed sec by sec. Inactive stocks typically have more sparse transactions. |

| 17. | When there is intraday volatility periodicity, the BTS returns resemble more closely to normal distribution than the CTS and TTS returns. |

| 18. | This is in contrast to the findings in Tse and Yang (2012), which shows the superiority of the ACD-ICV method over the RK method via simulation using second-by-second transactions (sparsity of 1 s). The poor performance of ME1 is mainly due to the transaction sparsity, since using as the proxy for integrated volatility over one price event becomes unreliable when transactions are sparse. Supporting evidence is provided in our simulation study that the RMSE of ME1 increases when observed transactions are more sparse. |

| 19. | MD5 is a model with price jumps, and the TRV method is constructed to be robust to price jumps. |

{kind=link}

{kind=link}

{kind=link}

| Frequency | CTS | ABFN | BTS | |||

|---|---|---|---|---|---|---|

| 5% | 1% | 5% | 1% | 5% | 1% | |

| Weekly | 15 | 9 | 3 | 1 | 4 | 0 |

| Daily | 40 | 40 | 12 | 5 | 6 | 4 |

| 30 min | 40 | 40 | 40 | 40 | 30 | 26 |

| Measures of shape | CTS | TTS | ABFN | BTS |

|---|---|---|---|---|

| Skewness (diff.) | 0.1272 | 0.2091 | 0.1105 | 0.0384 |

| Kurtosis (diff.) | 5.3745 | 10.7893 | 2.3749 | 0.2792 |

| Model | Code | Description of Model | Description of Model Parameters |

|---|---|---|---|

| Heston Model (high volatility) | MD1 | , | , , , and Corr |

| Heston Model (low volatility) | MD2 | Same as MD1. | , all remaining parameters same as MD1. |

| Two-factor affine stochastic volatility model with U-shape intraday volatility pattern | MD3 | , | , , , , , , , , and . |

| Deterministic volatility model with U-shape intraday volatility pattern | MD4 | , where t is the day of trade and is the intraday time. is the volatility of day t, is the intraday variations at time of each day. | for with increasing linearly in t over 20 days to reach . It then remains level for the next 20 days and decreases linearly in t to over 20 days. is computed as in Tse and Yang (2012) using the IBM tick-by-tick transaction data in 2012. |

| MD1 with price jumps | MD5 | is a Poisson process with on average one price jump every two days. is the size of the jumps with . |

| Sparsity | NSR | Model | ME | RMSE | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1-min | 2-min | 3-min | 5-min | 10-min | 1-min | 2-min | 3-min | 5-min | 10-min | |||

| 5-s | 0.005% | MD1 | −0.4286 | 0.0470 | 0.0031 | 0.0004 | −0.1777 | 1.3869 | 1.7228 | 2.1610 | 2.8165 | 4.0975 |

| MD2 | −0.4321 | −0.0500 | −0.0513 | −0.0338 | −0.1309 | 0.9964 | 1.1706 | 1.4665 | 1.9242 | 2.7797 | ||

| MD3 | −0.4435 | 0.0200 | 0.0123 | −0.0019 | −0.1916 | 1.2425 | 1.5657 | 1.9431 | 2.5511 | 3.6823 | ||

| MD4 | −0.2403 | −0.0913 | 0.0126 | 0.0055 | −0.2069 | 1.0574 | 1.3723 | 1.6849 | 2.2278 | 3.2164 | ||

| MD5 | −0.0687 | 0.6282 | 0.7732 | 1.0940 | 1.6463 | 1.4163 | 2.0196 | 2.5587 | 3.4485 | 5.2161 | ||

| 0.01% | MD1 | 0.3382 | 0.4486 | 0.2625 | 0.1532 | −0.1142 | 1.3520 | 1.7646 | 2.1562 | 2.8077 | 4.0850 | |

| MD2 | 0.0786 | 0.2172 | 0.1192 | 0.0675 | −0.0884 | 0.9049 | 1.1831 | 1.4608 | 1.9152 | 2.7695 | ||

| MD3 | 0.3291 | 0.4002 | 0.2555 | 0.1439 | −0.1301 | 1.2126 | 1.6016 | 1.9521 | 2.5460 | 3.6734 | ||

| MD4 | 0.5904 | 0.3128 | 0.2734 | 0.1532 | −0.1474 | 1.1809 | 1.4043 | 1.7059 | 2.2373 | 3.2230 | ||

| MD5 | 0.7280 | 1.0331 | 1.0365 | 1.2492 | 1.7128 | 1.5989 | 2.1671 | 2.6391 | 3.4936 | 5.2306 | ||

| 0.02% | MD1 | 1.8463 | 1.2523 | 0.7789 | 0.4499 | 0.0126 | 2.2762 | 2.1053 | 2.2506 | 2.8148 | 4.0590 | |

| MD2 | 1.0802 | 0.7479 | 0.4603 | 0.2651 | −0.0059 | 1.4503 | 1.3864 | 1.5109 | 1.9145 | 2.7529 | ||

| MD3 | 1.7862 | 1.1644 | 0.7397 | 0.4265 | −0.0167 | 2.1440 | 1.9166 | 2.0542 | 2.5558 | 3.6603 | ||

| MD4 | 2.2616 | 1.1036 | 0.7889 | 0.4437 | −0.0291 | 2.4966 | 1.7643 | 1.8609 | 2.2798 | 3.2357 | ||

| MD5 | 2.2713 | 1.8503 | 1.5649 | 1.5559 | 1.8424 | 2.7080 | 2.6518 | 2.8753 | 3.5982 | 5.2587 | ||

| 10-s | 0.005% | MD1 | −0.9375 | −0.0435 | −0.0307 | −0.0333 | −0.1880 | 1.6335 | 1.8357 | 2.1600 | 2.8457 | 4.1021 |

| MD2 | −0.8123 | −0.1034 | −0.0778 | −0.0560 | −0.1417 | 1.2304 | 1.2500 | 1.4735 | 1.9394 | 2.7833 | ||

| MD3 | −0.8436 | −0.0958 | −0.0423 | −0.0340 | −0.2088 | 1.4854 | 1.6584 | 1.9742 | 2.5751 | 3.7013 | ||

| MD4 | −0.5797 | −0.2436 | −0.0830 | −0.0584 | −0.2432 | 1.2715 | 1.4404 | 1.7121 | 2.2547 | 3.2308 | ||

| MD5 | −0.5986 | 0.5429 | 0.7290 | 1.0637 | 1.6334 | 1.5659 | 2.0991 | 2.5573 | 3.4711 | 5.2171 | ||

| 0.01% | MD1 | 0.0713 | 0.3397 | 0.2356 | 0.1224 | −0.1251 | 1.3501 | 1.8561 | 2.1611 | 2.8355 | 4.0856 | |

| MD2 | −0.1345 | 0.1520 | 0.1010 | 0.0460 | −0.0992 | 0.9467 | 1.2544 | 1.4661 | 1.9323 | 2.7757 | ||

| MD3 | 0.1028 | 0.2815 | 0.2097 | 0.1090 | −0.1529 | 1.2390 | 1.6800 | 1.9774 | 2.5686 | 3.6909 | ||

| MD4 | 0.3144 | 0.1905 | 0.1929 | 0.0949 | −0.1830 | 1.1801 | 1.4321 | 1.7293 | 2.2613 | 3.2356 | ||

| MD5 | 0.4190 | 0.9362 | 0.9980 | 1.2244 | 1.6968 | 1.5275 | 2.2311 | 2.6363 | 3.5126 | 5.2337 | ||

| 0.02% | MD1 | 2.0479 | 1.1137 | 0.7770 | 0.4235 | −0.0051 | 2.5005 | 2.1285 | 2.2661 | 2.8358 | 4.0650 | |

| MD2 | 1.1815 | 0.6675 | 0.4586 | 0.2426 | −0.0175 | 1.5885 | 1.4198 | 1.5277 | 1.9301 | 2.7608 | ||

| MD3 | 1.9622 | 1.0222 | 0.7158 | 0.3933 | −0.0340 | 2.3465 | 1.9448 | 2.0766 | 2.5855 | 3.6804 | ||

| MD4 | 2.1082 | 1.0387 | 0.7207 | 0.3933 | −0.0644 | 2.4205 | 1.7728 | 1.8823 | 2.2997 | 3.2520 | ||

| MD5 | 2.4111 | 1.7259 | 1.5437 | 1.5352 | 1.8277 | 2.8718 | 2.6669 | 2.8772 | 3.6225 | 5.2623 | ||

| 20-s | 0.005% | MD1 | −1.9043 | −0.4650 | −0.1715 | −0.1586 | −0.3052 | 2.5154 | 1.9081 | 2.3632 | 2.8884 | 4.1176 |

| MD2 | −1.4513 | −0.3972 | −0.1718 | −0.1551 | −0.2189 | 1.8465 | 1.3232 | 1.6142 | 1.9728 | 2.8010 | ||

| MD3 | −1.7349 | −0.4945 | −0.1976 | −0.1617 | −0.3245 | 2.2880 | 1.7421 | 2.0996 | 2.6517 | 3.7326 | ||

| MD4 | −1.3673 | −0.5413 | −0.2730 | −0.2261 | −0.3586 | 1.9372 | 1.6463 | 1.8101 | 2.3044 | 3.2759 | ||

| MD5 | −1.5684 | 0.0539 | 0.6149 | 0.9467 | 1.5263 | 2.3452 | 2.0185 | 2.7000 | 3.4925 | 5.2178 | ||

| 0.01% | MD1 | −0.7727 | 0.0595 | 0.0795 | −0.0012 | −0.2474 | 1.8388 | 1.8658 | 2.3619 | 2.8691 | 4.1079 | |

| MD2 | −0.6930 | −0.0470 | −0.0025 | −0.0515 | −0.1798 | 1.3436 | 1.2747 | 1.6111 | 1.9649 | 2.7898 | ||

| MD3 | −0.6715 | 0.0110 | 0.0681 | −0.0090 | −0.2678 | 1.6684 | 1.6857 | 2.1131 | 2.6393 | 3.7245 | ||

| MD4 | −0.3601 | −0.0577 | 0.0292 | −0.0623 | −0.3056 | 1.4354 | 1.5473 | 1.7854 | 2.3140 | 3.2870 | ||

| MD5 | −0.4358 | 0.5872 | 0.8854 | 1.1072 | 1.5868 | 1.8245 | 2.1169 | 2.7876 | 3.5323 | 5.2285 | ||

| 0.02% | MD1 | 1.4062 | 1.0834 | 0.5790 | 0.3089 | −0.1229 | 2.2543 | 2.1942 | 2.4346 | 2.8722 | 4.0765 | |

| MD2 | 0.7467 | 0.6389 | 0.3302 | 0.1612 | −0.0953 | 1.4646 | 1.4674 | 1.6470 | 1.9576 | 2.7740 | ||

| MD3 | 1.3598 | 0.9923 | 0.5629 | 0.2802 | −0.1573 | 2.1106 | 1.9812 | 2.2102 | 2.6445 | 3.7064 | ||

| MD4 | 1.6100 | 0.9172 | 0.6508 | 0.2535 | −0.1811 | 2.1813 | 1.8069 | 1.9153 | 2.3599 | 3.2984 | ||

| MD5 | 1.7450 | 1.6299 | 1.4063 | 1.4237 | 1.7176 | 2.5623 | 2.6474 | 3.0191 | 3.6372 | 5.2592 | ||

| Average RMSE Difference of the TRV Estimates | 1-min | 2-min | 3-min | 5-min | 10-min |

|---|---|---|---|---|---|

| Avg. (RMSE(CTS)-RMSE(BTS)) | 0.3043 | 0.1666 | 0.1891 | 0.2215 | 0.1926 |

| Avg. (RMSE(CTS)-RMSE(BTS))/RMSE(BTS) (%) | 17.8262 | 9.8515 | 9.6493 | 8.8626 | 5.7456 |

| Avg. (RMSE(TTS)-RMSE(BTS)) | −0.0237 | 0.1261 | 0.1721 | 0.2240 | 0.2072 |

| Avg. (RMSE(TTS)-RMSE(BTS))/RMSE(BTS) (%) | −0.1011 | 7.9977 | 9.0710 | 9.1005 | 6.2101 |

| ME | RMSE | ||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Sparsity | NSR | RK | ACD-ICV | Avg. Sampling Frequency (ACD-ICV) | RK | ACD-ICV | Avg. Sampling Frequency (ACD-ICV) | ||||||||

| 1-min | 3-min | 5-min | 10-min | 15-min | 1-min | 3-min | 5-min | 10-min | 15-min | ||||||

| 5-s | 0.005% | −0.1087 | ME1 | −5.8450 | −3.4421 | −2.6778 | −1.8270 | −1.3546 | 2.2978 | ME1 | 6.2142 | 3.8881 | 3.3149 | 2.9738 | 2.9941 |

| ME2 | −0.2043 | −0.2366 | −0.2205 | −0.0928 | 0.0734 | ME2 | 1.7527 | 1.7500 | 1.9673 | 2.3810 | 2.6985 | ||||

| ME3 | −0.1120 | 0.0540 | 0.2446 | 0.4362 | 0.7306 | ME3 | 1.2772 | 1.4001 | 1.7261 | 1.4380 | 1.5706 | ||||

| 0.01% | −0.0876 | ME1 | −3.4503 | −2.0139 | −1.5554 | −1.0491 | −0.7357 | 2.2998 | ME1 | 3.8811 | 2.6241 | 2.4551 | 2.5735 | 2.7766 | |

| ME2 | 0.0437 | 0.0089 | 0.0301 | 0.1633 | 0.3410 | ME2 | 1.6266 | 1.6906 | 1.9326 | 2.3896 | 2.7213 | ||||

| ME3 | 0.1489 | 0.3076 | 0.4972 | 0.6950 | 0.9897 | ME3 | 1.2367 | 1.3710 | 1.7078 | 1.4948 | 1.6735 | ||||

| 0.02% | −0.0461 | ME1 | 1.4407 | 0.6924 | 0.4711 | 0.3438 | 0.3824 | 2.3040 | ME1 | 2.0920 | 1.8468 | 2.0100 | 2.4290 | 2.7559 | |

| ME2 | 0.5181 | 0.5045 | 0.5353 | 0.6804 | 0.8449 | ME2 | 1.5778 | 1.7868 | 2.0340 | 2.5118 | 2.8656 | ||||

| ME3 | 0.6677 | 0.8253 | 1.0079 | 1.2071 | 1.5051 | ME3 | 1.3320 | 1.4939 | 1.8291 | 1.7399 | 1.9751 | ||||

| 10-s | 0.005% | −0.1416 | ME1 | −10.9555 | −6.0669 | −4.6302 | −3.1722 | −2.4450 | 2.6341 | ME1 | 11.3935 | 6.4347 | 5.0926 | 3.9820 | 3.6161 |

| ME2 | −0.3400 | −0.3899 | −0.3720 | −0.2555 | −0.0909 | ME2 | 2.2864 | 1.8765 | 2.0363 | 2.4242 | 2.6968 | ||||

| ME3 | −0.2235 | −0.1976 | 0.0212 | 0.2764 | 0.5716 | ME3 | 1.4774 | 1.4302 | 1.5870 | 1.4764 | 1.5774 | ||||

| 0.01% | −0.1178 | ME1 | −8.5745 | −4.8751 | −3.7310 | −2.5558 | −1.9404 | 2.6363 | ME1 | 8.9899 | 5.2580 | 4.2561 | 3.4911 | 3.2988 | |

| ME2 | −0.0858 | −0.1337 | −0.1165 | 0.0015 | 0.1719 | ME2 | 2.0281 | 1.7825 | 1.9930 | 2.4033 | 2.7120 | ||||

| ME3 | 0.0409 | 0.0713 | 0.2829 | 0.5387 | 0.8356 | ME3 | 1.4179 | 1.3836 | 1.5621 | 1.5129 | 1.6586 | ||||

| 0.02% | −0.0710 | ME1 | −4.8863 | −2.6923 | −2.0864 | −1.4154 | −1.0327 | 2.6399 | ME1 | 5.3222 | 3.2140 | 2.8523 | 2.7546 | 2.8704 | |

| ME2 | 0.4241 | 0.3767 | 0.3976 | 0.5304 | 0.7014 | ME2 | 1.8341 | 1.7717 | 2.0131 | 2.4689 | 2.8195 | ||||

| ME3 | 0.5665 | 0.5917 | 0.8060 | 1.0634 | 1.3599 | ME3 | 1.4587 | 1.4454 | 1.6547 | 1.7292 | 1.9392 | ||||

| 20-s | 0.005% | −0.1987 | ME1 | −17.7796 | −9.5646 | −7.3266 | −5.0140 | −3.9444 | 3.0600 | ME1 | 18.3065 | 9.9612 | 7.7382 | 5.6130 | 4.7999 |

| ME2 | −0.6770 | −0.7315 | −0.7231 | −0.6051 | −0.4518 | ME2 | 3.1408 | 2.2301 | 2.2493 | 2.5140 | 2.7698 | ||||

| ME3 | −0.4760 | −0.5490 | −0.3795 | −0.0762 | 0.2182 | ME3 | 2.2789 | 1.6071 | 1.7431 | 1.5932 | 1.6135 | ||||

| 0.01% | −0.1723 | ME1 | −16.2877 | −8.6764 | −6.6429 | −4.5336 | −3.5434 | 3.0621 | ME1 | 16.8362 | 9.0603 | 7.0596 | 5.1679 | 4.4519 | |

| ME2 | −0.4067 | −0.4638 | −0.4586 | −0.3355 | −0.1811 | ME2 | 2.9539 | 2.0830 | 2.1464 | 2.4481 | 2.7132 | ||||

| ME3 | −0.2070 | −0.2778 | −0.1000 | 0.1926 | 0.4882 | ME3 | 2.2062 | 1.5119 | 1.7034 | 1.5809 | 1.6494 | ||||

| 0.02% | −0.1200 | ME1 | −12.8662 | −7.0624 | −5.3456 | −3.6371 | −2.8233 | 3.0670 | ME1 | 13.3676 | 7.4466 | 5.7892 | 4.3706 | 3.9009 | |

| ME2 | 0.1191 | 0.0629 | 0.0728 | 0.2021 | 0.3562 | ME2 | 2.6226 | 1.9304 | 2.0461 | 2.4303 | 2.7561 | ||||

| ME3 | 0.3287 | 0.2614 | 0.4493 | 0.7287 | 1.0260 | ME3 | 2.1632 | 1.4769 | 1.7526 | 1.7006 | 1.8539 | ||||

| ME | RMSE | ||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Sparsity | NSR | RK | ACD-ICV | Avg. Sampling Frequency (ACD-ICV) | RK | ACD-ICV | Avg. Sampling Frequency (ACD-ICV) | ||||||||

| 1-min | 3-min | 5-min | 10-min | 15-min | 1-min | 3-min | 5-min | 10-min | 15-min | ||||||

| 5-s | 0.005% | 5.4227 | ME1 | −5.8297 | −3.3882 | −2.5730 | −1.6045 | −1.0188 | 9.9602 | ME1 | 6.2026 | 3.8409 | 3.2360 | 2.8656 | 2.8789 |

| ME2 | 0.8058 | 0.7685 | 0.7892 | 0.9164 | 1.0902 | ME2 | 1.9098 | 1.9199 | 2.1430 | 2.6091 | 2.9672 | ||||

| ME3 | 0.8846 | 1.0464 | 1.2556 | 1.4577 | 1.7653 | ME3 | 1.6636 | 1.8671 | 2.1671 | 2.0848 | 2.2923 | ||||

| 0.01% | 5.4418 | ME1 | −3.4340 | −1.9407 | −1.4617 | −0.8313 | −0.3769 | 9.9686 | ME1 | 3.8603 | 2.5721 | 2.4208 | 2.5277 | 2.7279 | |

| ME2 | 1.0512 | 1.0187 | 1.0453 | 1.1758 | 1.3516 | ME2 | 1.9215 | 2.0070 | 2.2572 | 2.7266 | 3.0797 | ||||

| ME3 | 1.1471 | 1.3082 | 1.5160 | 1.7153 | 2.0254 | ME3 | 1.7863 | 1.9921 | 2.2839 | 2.2406 | 2.4745 | ||||

| 0.02% | 5.4794 | ME1 | 1.4728 | 0.7713 | 0.5849 | 0.5818 | 0.7257 | 9.9860 | ME1 | 2.0990 | 1.8775 | 2.0612 | 2.5042 | 2.8495 | |

| ME2 | 1.5310 | 1.5181 | 1.5467 | 1.6891 | 1.8715 | ME2 | 2.1539 | 2.3315 | 2.5607 | 3.0135 | 3.3723 | ||||

| ME3 | 1.6721 | 1.8222 | 2.0263 | 2.2336 | 2.5459 | ME3 | 2.1213 | 2.3145 | 2.5816 | 2.6222 | 2.8867 | ||||

| 10-s | 0.005% | 5.3907 | ME1 | −10.9449 | −6.0276 | −4.5318 | −2.9491 | −2.1042 | 10.0436 | ME1 | 11.3795 | 6.4015 | 5.0126 | 3.8136 | 3.4271 |

| ME2 | 0.6633 | 0.6106 | 0.6242 | 0.7470 | 0.9182 | ME2 | 2.3104 | 1.9461 | 2.1377 | 2.5742 | 2.9195 | ||||

| ME3 | 0.7705 | 0.7948 | 0.9985 | 1.2914 | 1.5981 | ME3 | 1.6828 | 1.8435 | 2.0209 | 2.0229 | 2.2163 | ||||

| 0.01% | 5.4121 | ME1 | −8.6446 | −4.8146 | −3.6363 | −2.3242 | −1.5842 | 10.0534 | ME1 | 9.0607 | 5.2047 | 4.1744 | 3.3347 | 3.1353 | |

| ME2 | 0.9153 | 0.8660 | 0.8891 | 1.0125 | 1.1800 | ME2 | 2.1941 | 1.9921 | 2.2058 | 2.6559 | 3.0205 | ||||

| ME3 | 1.0358 | 1.0604 | 1.2689 | 1.5548 | 1.8631 | ME3 | 1.7876 | 1.9431 | 2.1333 | 2.1752 | 2.3929 | ||||

| 0.02% | 5.4548 | ME1 | −4.8774 | −2.6232 | −1.9874 | −1.1786 | −0.6562 | 10.0727 | ME1 | 5.3053 | 3.1592 | 2.7833 | 2.6525 | 2.7837 | |

| ME2 | 1.4283 | 1.3848 | 1.4085 | 1.5407 | 1.7137 | ME2 | 2.2591 | 2.2408 | 2.4554 | 2.9128 | 3.2801 | ||||

| ME3 | 1.5657 | 1.5953 | 1.7983 | 2.0797 | 2.3929 | ME3 | 2.0947 | 2.2393 | 2.4394 | 2.5464 | 2.8021 | ||||

| 20-s | 0.005% | 5.3322 | ME1 | −17.8068 | −9.5419 | −7.2562 | −4.8115 | −3.5992 | 10.1532 | ME1 | 18.3394 | 9.9398 | 7.6740 | 5.4435 | 4.5299 |

| ME2 | 0.3397 | 0.2821 | 0.2882 | 0.4019 | 0.5596 | ME2 | 3.0755 | 2.1117 | 2.1666 | 2.5271 | 2.8374 | ||||

| ME3 | 0.5340 | 0.4639 | 0.6157 | 0.9473 | 1.2592 | ME3 | 2.2664 | 1.7445 | 1.9529 | 1.9189 | 2.0788 | ||||

| 0.01% | 5.3562 | ME1 | −16.4046 | −8.6377 | −6.5612 | −4.3376 | −3.2101 | 10.1639 | ME1 | 16.9502 | 9.0284 | 6.9857 | 5.0049 | 4.2219 | |

| ME2 | 0.6035 | 0.5473 | 0.5600 | 0.6682 | 0.8417 | ME2 | 2.9903 | 2.1008 | 2.1818 | 2.5643 | 2.9096 | ||||

| ME3 | 0.8043 | 0.7385 | 0.8828 | 1.2168 | 1.5292 | ME3 | 2.3152 | 1.8216 | 2.0152 | 2.0450 | 2.2400 | ||||

| 0.02% | 5.4036 | ME1 | −12.8619 | −7.0131 | −5.2494 | −3.4318 | −2.4897 | 10.1854 | ME1 | 13.3635 | 7.4026 | 5.6999 | 4.2129 | 3.6884 | |

| ME2 | 1.1378 | 1.0778 | 1.0905 | 1.2102 | 1.3818 | ME2 | 2.8324 | 2.2176 | 2.3262 | 2.7620 | 3.1219 | ||||

| ME3 | 1.3435 | 1.2746 | 1.4297 | 1.7565 | 2.0717 | ME3 | 2.5068 | 2.0651 | 2.2905 | 2.3864 | 2.6243 | ||||

| RK | ACD-ICV | Avg. Sampling Frequency (ACD-ICV) | ||||

|---|---|---|---|---|---|---|

| 1-min | 3-min | 5-min | 10-min | 15-min | ||

| 3.9198 | ME1 | 8.1955 | 4.7603 | 3.8640 | 3.2027 | 3.0690 |

| ME2 | 1.9321 | 1.6430 | 1.7542 | 2.1559 | 2.4848 | |

| ME3 | 1.4483 | 1.3958 | 1.5143 | 1.4755 | 1.6280 | |

© 2017 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Dong, Y.; Tse, Y.-K. Business Time Sampling Scheme with Applications to Testing Semi-Martingale Hypothesis and Estimating Integrated Volatility. Econometrics 2017, 5, 51. https://doi.org/10.3390/econometrics5040051

Dong Y, Tse Y-K. Business Time Sampling Scheme with Applications to Testing Semi-Martingale Hypothesis and Estimating Integrated Volatility. Econometrics. 2017; 5(4):51. https://doi.org/10.3390/econometrics5040051

Chicago/Turabian StyleDong, Yingjie, and Yiu-Kuen Tse. 2017. "Business Time Sampling Scheme with Applications to Testing Semi-Martingale Hypothesis and Estimating Integrated Volatility" Econometrics 5, no. 4: 51. https://doi.org/10.3390/econometrics5040051

APA StyleDong, Y., & Tse, Y.-K. (2017). Business Time Sampling Scheme with Applications to Testing Semi-Martingale Hypothesis and Estimating Integrated Volatility. Econometrics, 5(4), 51. https://doi.org/10.3390/econometrics5040051