The general simulation scheme goes as follows. We perform 10,000 simulations for a number of different stationary VAR(1) models and for a number of different sample sizes. In each simulation we draw the inital values of the series from a multivariate normal distribution with mean

and covariance matrix

. Likewise, the innovations are drawn randomly from a multivariate normal distribution with mean 0 and covariance matrix

. Based on the initial values and innovations we simulate the series forward in time until we have a sample of size

T. For each simulation we estimate a VAR(1) model using OLS and WLS. Furthermore, we correct the OLS estimate for bias using the analytical bias formula (6) (denoted ABF) and using a bootstrap procedure (denoted BOOT). Based on the 10,000 simulations we calculate the mean slope coefficients, bias, variance, and root mean squared error (RMSE) for each approach. The bootstrap procedure follows the outline presented in

Section 2.1. The innovations are drawn randomly with replacement from the residuals, and we also randomly draw initial values from the simulated data. This procedure is repeated 1,000 times for each simulation.

8 Regarding the analytical bias formula and WLS, we use the ‘plug-in’ approach, cf.

Section 2.5. In the analytical bias formula we calculate the covariance matrix of

as

. In both the analytical bias formula and bootstrapping we ensure stationarity by applying the approach by Kilian [

10], cf.

Section 2.3. In using this approach we choose the largest value of

κ that ensures that the bias-adjusted estimate no longer contains unit or explosive roots.

We deviate from this general scheme in a number of different ways, all of which will be clearly stated in the text. In

Section 3.1 we also allow for a fixed initial value, since the WLS estimator is based on the restricted likelihood, which is derived under the assumption that the initial value is fixed. In

Section 3.2 we investigate the effect of iterating on WLS and ABF and inverting ABF. In

Section 3.3 we analyze the consequences of not using Kilian’s [

10] approach to ensure stationarity and the properties of the YW estimator. In

Section 3.4 we allow for VAR(1) models with unit roots. In

Section 3.5 we investigate the finite-sample properties when data are skewed and fat-tailed instead of normally distributed, and we analyze the consequences of using a parametric bootstrap approach to adjust for bias using a wrong distributional assumption.

3.1. Bias-Correction in Stationary Models

Table 1 reports the simulation results for the following VAR(1) model

where the eigenvalues of Φ are 0.722 and 0.928. This VAR model is also used in simulation studies by Amihud and Hurvich [

6] and Amihud et al. [

32] in analyzing return predictability by persistent state variables. The table shows the mean slope coefficients and the average squared bias, variance, and RMSE

across the four slope coefficients for

. For expositional purposes bias

and variance are multiplied by 100. The final column shows the number of simulations in which the approach results in an estimate of Φ in the non-stationary region of the parameter space. For example, for

using OLS to estimate the VAR(1) model implies that 25 out of 10,000 simulations result in a non-stationary model. The estimates from these 25 simulations are included in the reported numbers. When the OLS estimate is in the non-stationary region of the parameter space, we do not perform any bias-adjustment and set the bias-adjusted estimate equal to the (non-stationary) OLS estimate. This implies that in 25 simulations the (non-stationary) OLS estimate is included in the numbers for ABF and BOOT. For these bias-adjustment procedures the number in the final column shows the number of simulations where OLS yields a stationary model, but where the bias-adjustment procedure pushes the model into the non-stationary region of the parameter space, and we use the approach by Kilian [

10] to ensure a stationary model.

Table 1.

Bias-correction in a stationary but persistent VAR(1) model. The results in this table are based on 10,000 simulations from the VAR(1) model given in (11). Bias, variance, and RMSE are reported as the average across the four slope coefficients. Average bias and variance are multiplied by 100. The final column (#NS) gives the number of simulations that result in a VAR(1) system in the non-stationary region. OLS are ordinary least squares estimates; WLS are estimates based on equation (8); ABF are bias-adjusted estimates based on the analytical bias formula, equation (7); BOOT are bias-adjusted estimates based on the bootstrap.

Table 1.

Bias-correction in a stationary but persistent VAR(1) model. The results in this table are based on 10,000 simulations from the VAR(1) model given in (11). Bias, variance, and RMSE are reported as the average across the four slope coefficients. Average bias and variance are multiplied by 100. The final column (#NS) gives the number of simulations that result in a VAR(1) system in the non-stationary region. OLS are ordinary least squares estimates; WLS are estimates based on equation (8); ABF are bias-adjusted estimates based on the analytical bias formula, equation (7); BOOT are bias-adjusted estimates based on the bootstrap.

| | | Mean Slope Coefficients | | | | |

| | | | | | | Bias | Variance | RMSE | #NS |

| OLS | 0.7082 | 0.0906 | 0.1036 | 0.7519 | 0.4538 | 1.9195 | 0.1534 | 25 |

| | WLS | 0.7441 | 0.0973 | 0.1040 | 0.7927 | 0.1606 | 1.9135 | 0.1438 | 198 |

| | ABF | 0.7743 | 0.0946 | 0.0995 | 0.8210 | 0.0382 | 1.7520 | 0.1336 | 1613 |

| | BOOT | 0.7779 | 0.0963 | 0.1016 | 0.8252 | 0.0281 | 1.8170 | 0.1357 | 2220 |

| OLS | 0.7548 | 0.0972 | 0.1035 | 0.8038 | 0.1049 | 0.7324 | 0.0913 | 2 |

| | WLS | 0.7776 | 0.1019 | 0.1034 | 0.8304 | 0.0225 | 0.7604 | 0.0883 | 18 |

| | ABF | 0.7931 | 0.0988 | 0.1003 | 0.8433 | 0.0024 | 0.6817 | 0.0826 | 304 |

| | BOOT | 0.7950 | 0.1001 | 0.1015 | 0.8458 | 0.0011 | 0.6965 | 0.0834 | 539 |

| OLS | 0.7783 | 0.0995 | 0.1017 | 0.8276 | 0.0245 | 0.3151 | 0.0581 | 0 |

| | WLS | 0.7924 | 0.1036 | 0.1021 | 0.8449 | 0.0025 | 0.3498 | 0.0592 | 0 |

| | ABF | 0.7985 | 0.1000 | 0.0999 | 0.8483 | 0.0001 | 0.3013 | 0.0548 | 0 |

| | BOOT | 0.7992 | 0.1005 | 0.1003 | 0.8492 | 0.0000 | 0.3041 | 0.0551 | 2 |

| OLS | 0.7917 | 0.0996 | 0.1014 | 0.8407 | 0.0039 | 0.1112 | 0.0339 | 0 |

| | WLS | 0.7991 | 0.1034 | 0.1025 | 0.8508 | 0.0005 | 0.1316 | 0.0363 | 0 |

| | ABF | 0.8000 | 0.0998 | 0.1005 | 0.8492 | 0.0000 | 0.1089 | 0.0329 | 0 |

| | BOOT | 0.8002 | 0.0999 | 0.1006 | 0.8494 | 0.0000 | 0.1091 | 0.0330 | 0 |

From

Table 1 it is clear that OLS yields severely biased estimates in small samples. Also, consistent with the univariate case we see that the autoregressive coefficients (

and

) are downward biased. For example, for

, the OLS estimate of

is 0.7519 compared to the true value of 0.85. As expected both bias and variance decrease when the sample size increases. Chen and Deo [

30] advocate the use of their weighted least squares estimator due to the smaller bias associated with this estimator compared to OLS, a small-sample property that is also clearly visible in

Table 1. However, the variance of WLS is larger than that of OLS for

, and for

this increase in variance more than offsets the decrease in bias resulting in a higher RMSE for WLS compared to OLS.

Turning to the bias correction methods we find that both ABF and BOOT yield a very large reduction in bias compared to both OLS and WLS. However, for very small samples even the use of these methods still implies fairly biased estimates. For example, for

the bias corrected estimate of

is roughly 0.82 for both methods compared to the true value of 0.85. It is also worth noting that the variance of ABF and BOOT is smaller than the variance of OLS. Hence, in this case the decrease in bias does not come at the cost of increased variance. Comparing ABF and BOOT we see that using a bootstrap procedure yields a smaller bias than the use of the analytical bias formula. The difference in bias is, however, very small across these two methods. For example, for

the estimate of

is 0.8252 for BOOT compared to 0.8210 for ABF. In contrast, the variance is lower for ABF than for BOOT, and this even to such a degree that ABF yields the lowest RMSE. These results suggest that the simple analytical bias formula has at least as good finite-sample properties as a more elaborate bootstrap procedure.

9To check the robustness of the results in

Table 1,

Table 2 shows the results based on the following VAR(1) model

where the eigenvalues of Φ are 0.087 and 0.863. This system corresponds fairly well to an empirically relevant VAR(1) model in finance consisting of stock returns (not persistent) and the dividend-price ratio (persistent), and where the innovations of the two series are strongly negatively correlated, see, e.g., Stambaugh [

4]. Overall, the results in

Table 2 follow the same pattern as in

Table 1, i.e. OLS yields highly biased estimates, WLS is able to reduce this bias but at the cost of increased variance, and both ABF and BOOT provide a large bias reduction compared to OLS and WLS.

However,

Table 2 also displays some interesting differences. The variances of the bias correction methods are now larger than that of OLS. This prompts the questions: What has caused this relative change in variances (Φ or

), and can the change imply a larger RMSE when correcting for bias than when not? To answer these questions,

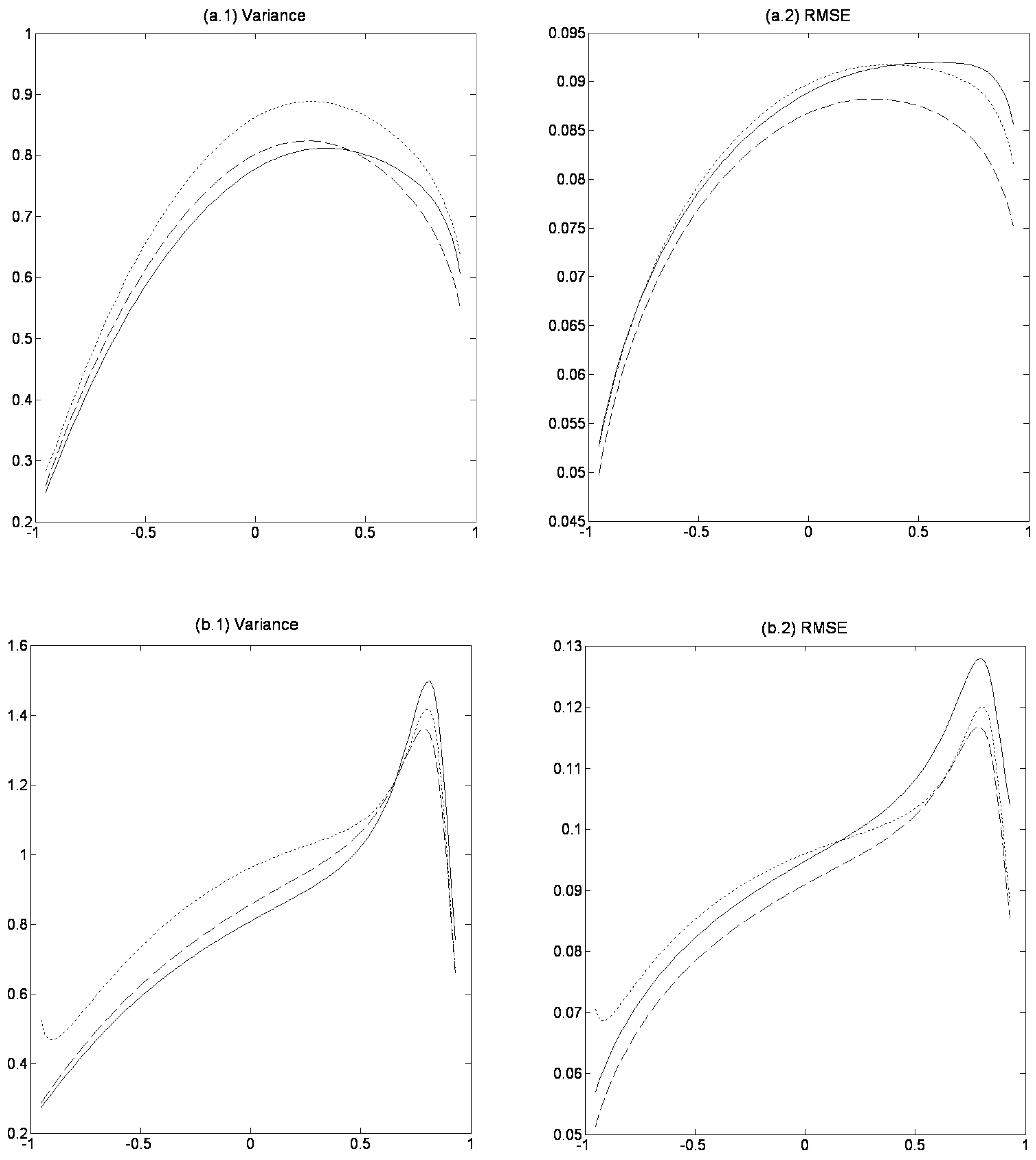

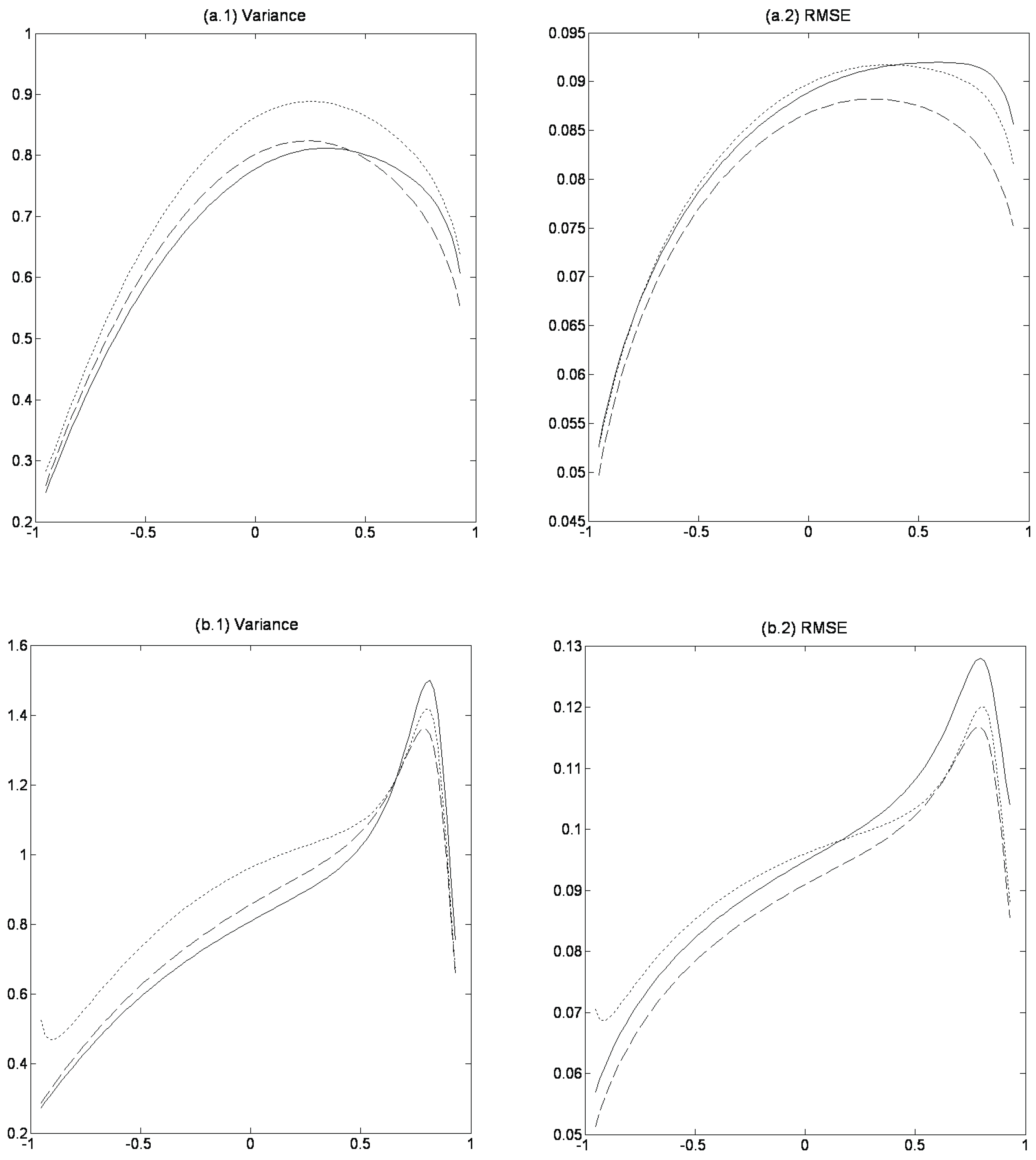

Figure 1 shows the variance of OLS, WLS, and ABF as a function of

with the remaining data-generating parameters equal to those given in (11) and (12), respectively. The interval for

is chosen to ensure stationarity. The variance is calculated as the average variance across the four slope coefficients based on 10,000 simulations with

.

10 For the data-generating parameters given in (11), Panel (a.1) shows that for

smaller (larger) than roughly

the variance of OLS is smaller (larger) than the variance of ABF. Panel (b.1) shows the corresponding results for the data-generating parameters given in (12), i.e. the only differences between the two panels is

. We see a similar result as in Panel (a.1), but now

has to be smaller (larger) than roughly 0.65 for the variance of OLS to be smaller (larger) than the variance of ABF.

Table 2.

Bias-correction in a stationary but persistent VAR(1) model. The results in this table are based on 10,000 simulations from the VAR(1) model given in (12). See also the caption to

Table 1.

Table 2.

Bias-correction in a stationary but persistent VAR(1) model. The results in this table are based on 10,000 simulations from the VAR(1) model given in (12). See also the caption to Table 1.

| | | Mean Slope Coefficients | | | | |

| | | | | | | Bias | Variance | RMSE | #NS |

| OLS | 0.1290 | 0.1841 | 0.0534 | 0.7509 | 0.4974 | 1.9419 | 0.1561 | 4 |

| | WLS | 0.0911 | 0.1222 | 0.1056 | 0.8260 | 0.0295 | 2.1234 | 0.1446 | 63 |

| | ABF | 0.1016 | 0.1162 | 0.0961 | 0.8312 | 0.0158 | 2.1547 | 0.1463 | 621 |

| | BOOT | 0.1015 | 0.1107 | 0.0970 | 0.8383 | 0.0065 | 2.1544 | 0.1460 | 669 |

| OLS | 0.1141 | 0.1400 | 0.0776 | 0.8030 | 0.1126 | 0.8412 | 0.0969 | 0 |

| | WLS | 0.0839 | 0.0979 | 0.1168 | 0.8536 | 0.0140 | 1.0066 | 0.0982 | 0 |

| | ABF | 0.0996 | 0.1038 | 0.1002 | 0.8457 | 0.0008 | 0.8978 | 0.0932 | 14 |

| | BOOT | 0.0993 | 0.1018 | 0.1006 | 0.8482 | 0.0002 | 0.9002 | 0.0933 | 7 |

| OLS | 0.1079 | 0.1195 | 0.0878 | 0.8270 | 0.0280 | 0.3925 | 0.0638 | 0 |

| | WLS | 0.0826 | 0.0877 | 0.1194 | 0.8650 | 0.0264 | 0.5321 | 0.0725 | 0 |

| | ABF | 0.1006 | 0.1012 | 0.0991 | 0.8486 | 0.0001 | 0.4049 | 0.0622 | 0 |

| | BOOT | 0.1005 | 0.1005 | 0.0994 | 0.8494 | 0.0000 | 0.4057 | 0.0622 | 0 |

| OLS | 0.1024 | 0.1070 | 0.0957 | 0.8414 | 0.0037 | 0.1506 | 0.0382 | 0 |

| | WLS | 0.0844 | 0.0860 | 0.1177 | 0.8664 | 0.0256 | 0.2372 | 0.0500 | 0 |

| | ABF | 0.0995 | 0.0996 | 0.1003 | 0.8501 | 0.0000 | 0.1524 | 0.0378 | 0 |

| | BOOT | 0.0995 | 0.0995 | 0.1003 | 0.8503 | 0.0000 | 0.1526 | 0.0378 | 0 |

Hence, the relative size of the variances for OLS and ABF depends on both Φ and

but in general, in highly persistent processes ABF has a lower variance than OLS. Panels (a.2) and (b.2) show that the RMSE for ABF remains below that of OLS for all values of

. Hence, despite a smaller variance for certain values of

, the larger bias using OLS results in a higher RMSE than in the case of ABF. This result does, however, not always hold.

Table 3 reports the simulation results for the much less persistent VAR(1) model

where the eigenvalues of Φ are 0.122 and 0.328. In contrast to the data-generating processes in (11) and (12) both variables now display little persistence. Although OLS in this case still yields somewhat biased estimates and WLS, ABF, and BOOT all reduce the bias, OLS has the lowest RMSE. This is due to a much lower variance for OLS than for the alternative estimator, WLS, and the two bias-correction methods, ABF and BOOT. The overall conclusion from

Table 3 is that estimating even highly stationary VAR models using OLS provides biased estimates, which suggests the use of WLS, ABF, or BOOT if bias is of primary concern, while OLS is preferable if both bias and variance are important.

Table 3.

Bias-correction in a stationary VAR(1) model. The results in this table are based on 10,000 simulations from the VAR(1) model given in (13). See also the caption to

Table 1.

Table 3.

Bias-correction in a stationary VAR(1) model. The results in this table are based on 10,000 simulations from the VAR(1) model given in (13). See also the caption to Table 1.

| | | Mean Slope Coefficients | | | | |

| | | | | | | Bias | Variance | RMSE | #NS |

| OLS | 0.1627 | 0.0932 | 0.0964 | 0.2073 | 0.0819 | 2.8504 | 0.1712 | 0 |

| | WLS | 0.1850 | 0.0959 | 0.0980 | 0.2307 | 0.0155 | 2.9535 | 0.1723 | 0 |

| | ABF | 0.1949 | 0.0985 | 0.0988 | 0.2427 | 0.0021 | 2.9530 | 0.1719 | 0 |

| | BOOT | 0.1953 | 0.0986 | 0.0988 | 0.2432 | 0.0018 | 2.9550 | 0.1719 | 0 |

| OLS | 0.1803 | 0.0973 | 0.0983 | 0.2295 | 0.0204 | 1.3280 | 0.1161 | 0 |

| | WLS | 0.1919 | 0.0993 | 0.0992 | 0.2424 | 0.0031 | 1.3599 | 0.1167 | 0 |

| | ABF | 0.1974 | 0.1000 | 0.0995 | 0.2483 | 0.0002 | 1.3528 | 0.1163 | 0 |

| | BOOT | 0.1976 | 0.1000 | 0.0995 | 0.2484 | 0.0002 | 1.3546 | 0.1164 | 0 |

| OLS | 0.1912 | 0.0985 | 0.0992 | 0.2403 | 0.0044 | 0.6522 | 0.0810 | 0 |

| | WLS | 0.1971 | 0.0997 | 0.0997 | 0.2470 | 0.0004 | 0.6627 | 0.0814 | 0 |

| | ABF | 0.2000 | 0.0999 | 0.0998 | 0.2500 | 0.0000 | 0.6580 | 0.0811 | 0 |

| | BOOT | 0.2001 | 0.0999 | 0.0998 | 0.2500 | 0.0000 | 0.6587 | 0.0812 | 0 |

| OLS | 0.1962 | 0.0996 | 0.0998 | 0.2462 | 0.0007 | 0.2545 | 0.0505 | 0 |

| | WLS | 0.1986 | 0.1000 | 0.1000 | 0.2489 | 0.0001 | 0.2558 | 0.0506 | 0 |

| | ABF | 0.1998 | 0.1001 | 0.1000 | 0.2501 | 0.0000 | 0.2554 | 0.0505 | 0 |

| | BOOT | 0.1999 | 0.1001 | 0.1000 | 0.2502 | 0.0000 | 0.2555 | 0.0505 | 0 |

Figure 1(a.1) shows that for all values of

WLS yields a larger variance than both OLS and ABF, and in

Figure 1(b.1) this is the case for

smaller than roughly 0.65. The bias-reduction from WLS compared to OLS only offsets this larger variance for

larger than roughly

and 0.2, respectively, cf.

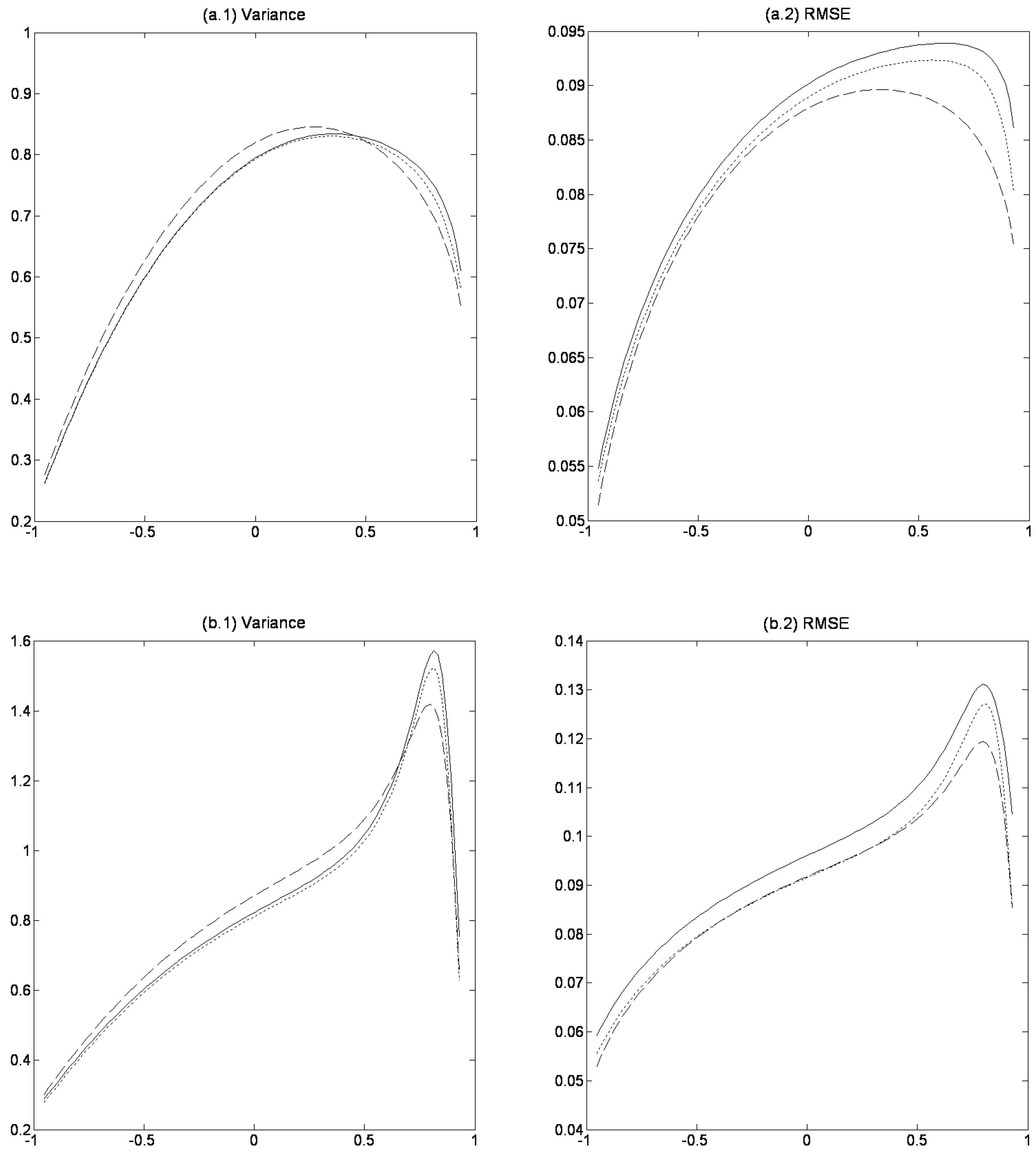

Figure 1(a.2) and (b.2). However, WLS is derived under the assumption of fixed initial values.

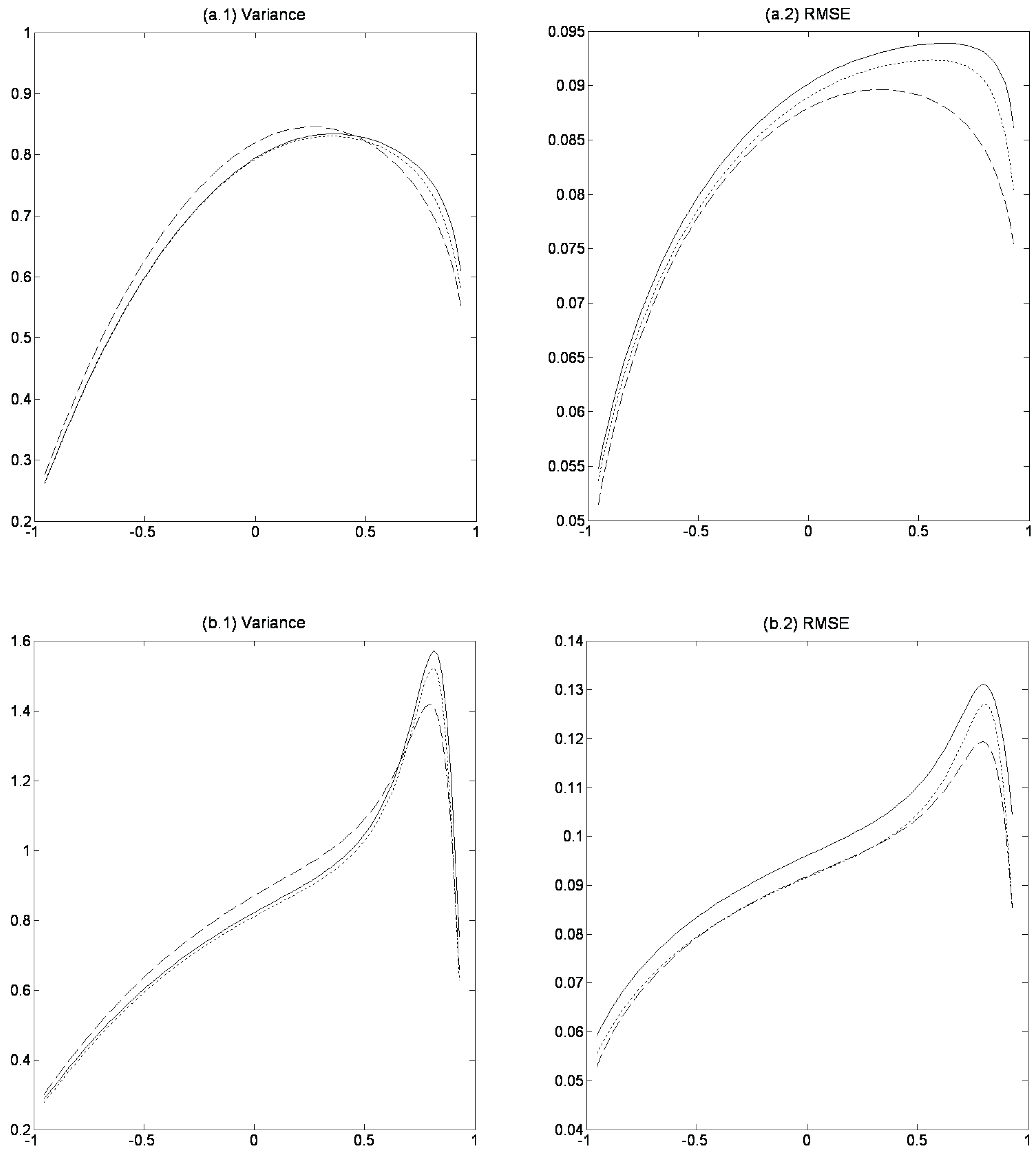

Figure 2 shows results corresponding to those in

Figure 1 but now with fixed initial values, which provides a more fair comparison of WLS to OLS and ABF. Comparing the two figures we see that fixed initial values clearly improve the finite-sample properties of WLS. The variance of WLS is now always smaller than or roughly equal to that of OLS, which together with a smaller bias implies that RMSE is lower for WLS than for OLS. However, despite better finite-sample properties under fixed initial values, WLS still does not yield a lower RMSE than ABF. Note, the relative findings on OLS and ABF are unaffected by the choice of random or fixed initial values.

Figure 1.

Variance and RMSE with random initial value. The figure shows the variance and RMSE in the VAR(1) slope coefficients based on 10,000 simulations as a function of for OLS (solid line), WLS (dotted line), and ABF (dashed line). The remaining data-generating parameters are in Panel a given in (11) and in Panel b given in (12). The sample size is 100. The variance and RMSE are reported as the average across the four slope coefficients. The variance is multiplied by 100.

Figure 1.

Variance and RMSE with random initial value. The figure shows the variance and RMSE in the VAR(1) slope coefficients based on 10,000 simulations as a function of for OLS (solid line), WLS (dotted line), and ABF (dashed line). The remaining data-generating parameters are in Panel a given in (11) and in Panel b given in (12). The sample size is 100. The variance and RMSE are reported as the average across the four slope coefficients. The variance is multiplied by 100.

Figure 2.

Variance and RMSE with fixed initial value. See caption to

Figure 1.

Figure 2.

Variance and RMSE with fixed initial value. See caption to

Figure 1.

3.2. Iterating and Inverting the Analytical Bias Formula

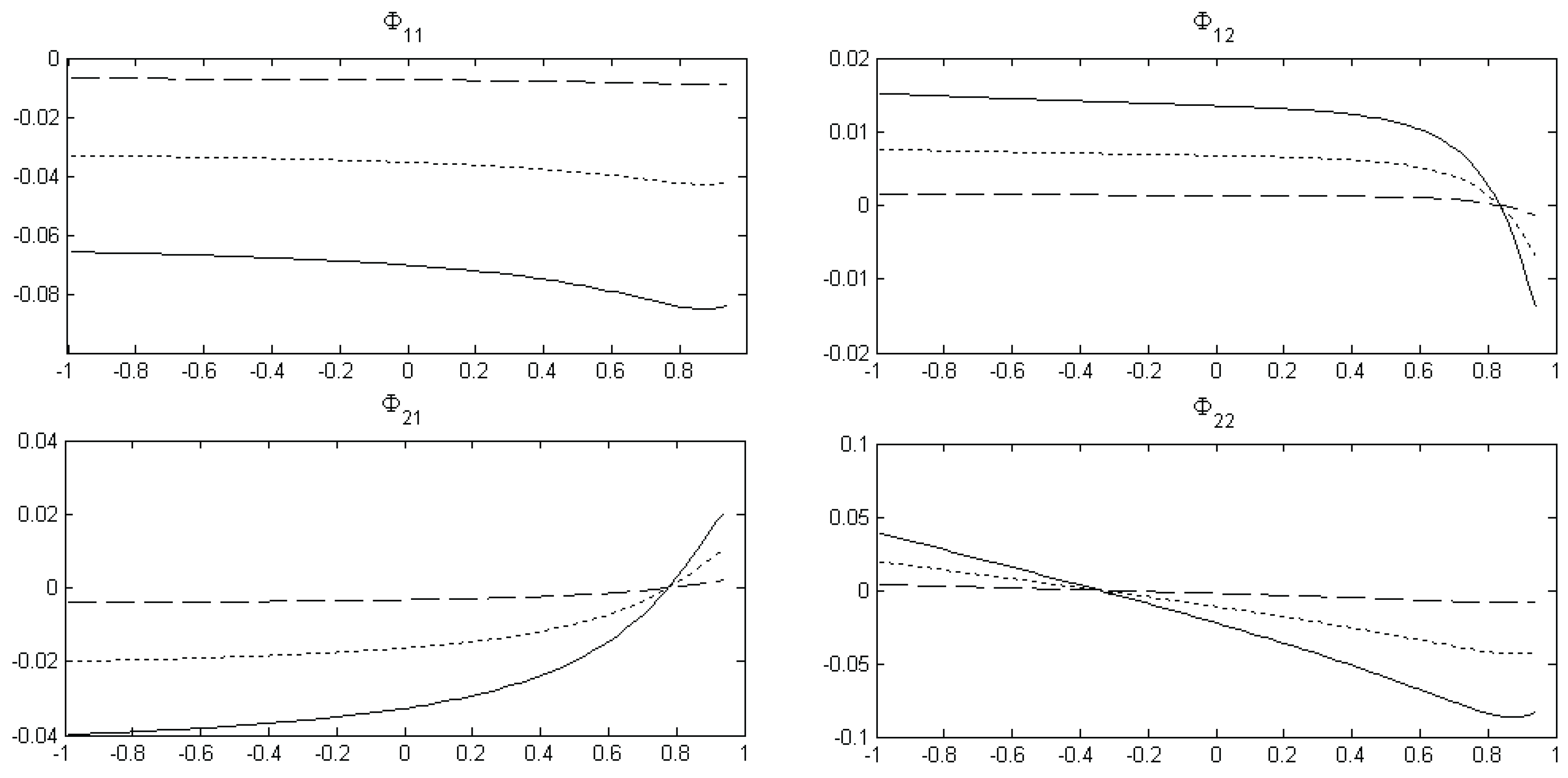

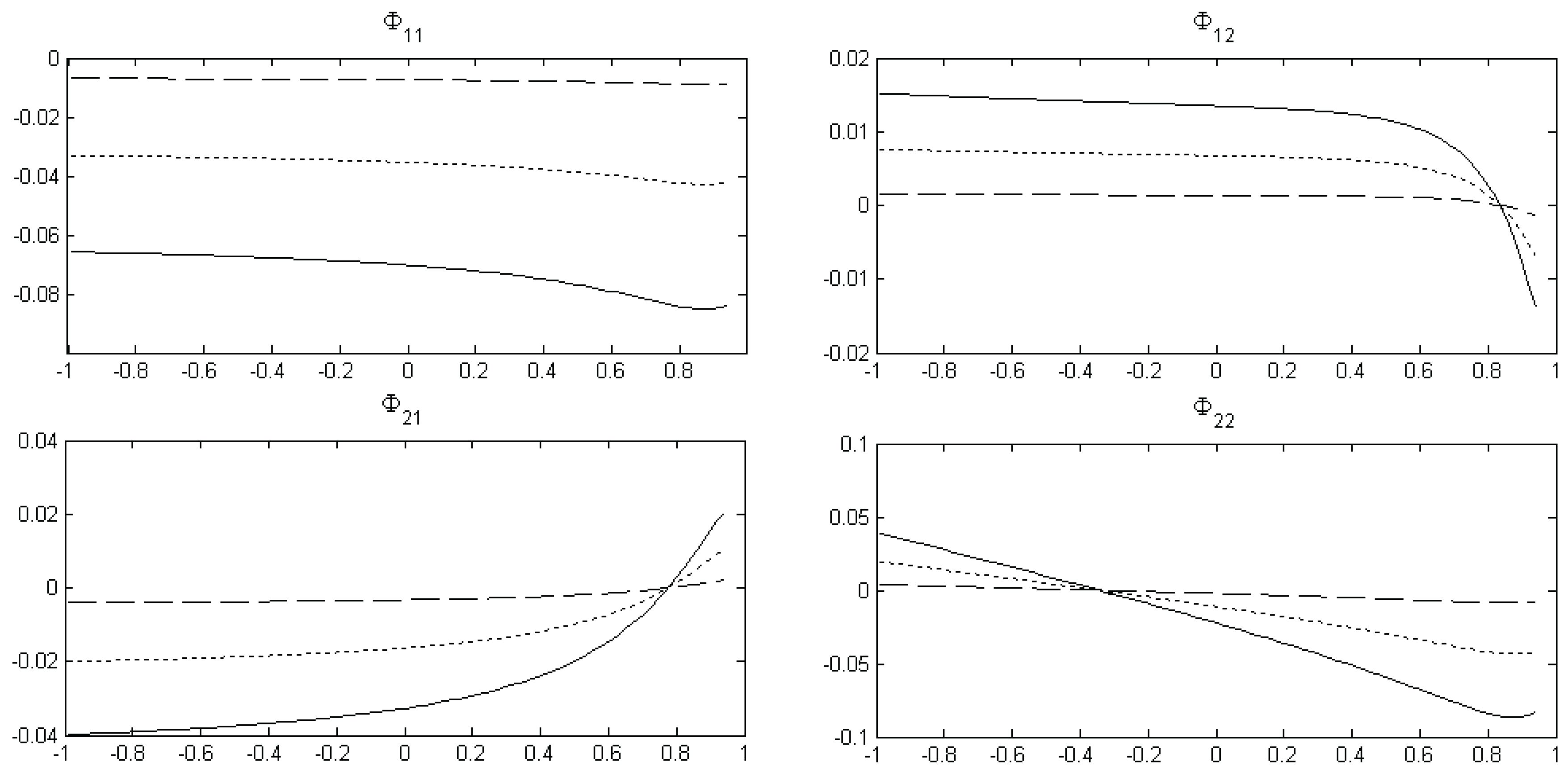

The use of an iterative scheme in the analytical bias formula is only relevant if the bias varies as a function of Φ.

11 Figure 3 shows the bias as a function of

in a bivariate VAR(1) system with the remaining data-generating parameters equal to those given in (11). As expected the bias function varies most for small sample sizes, but even for

the bias function for

is relatively flat. For

and

the bias function is relatively steep when the sample size is small and the second variable in the system is fairly persistent. For

the bias function is mainly downward sloping. Overall,

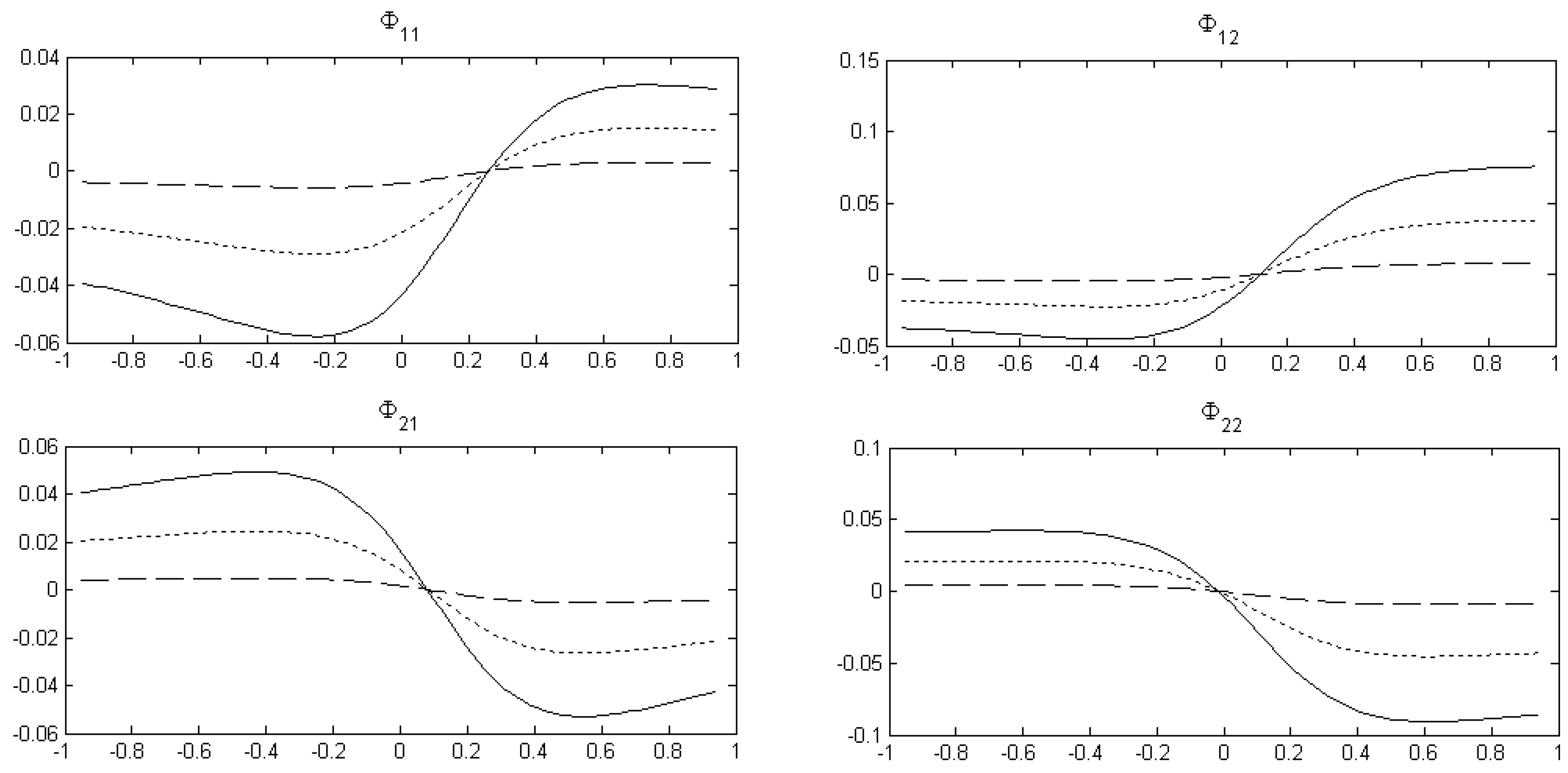

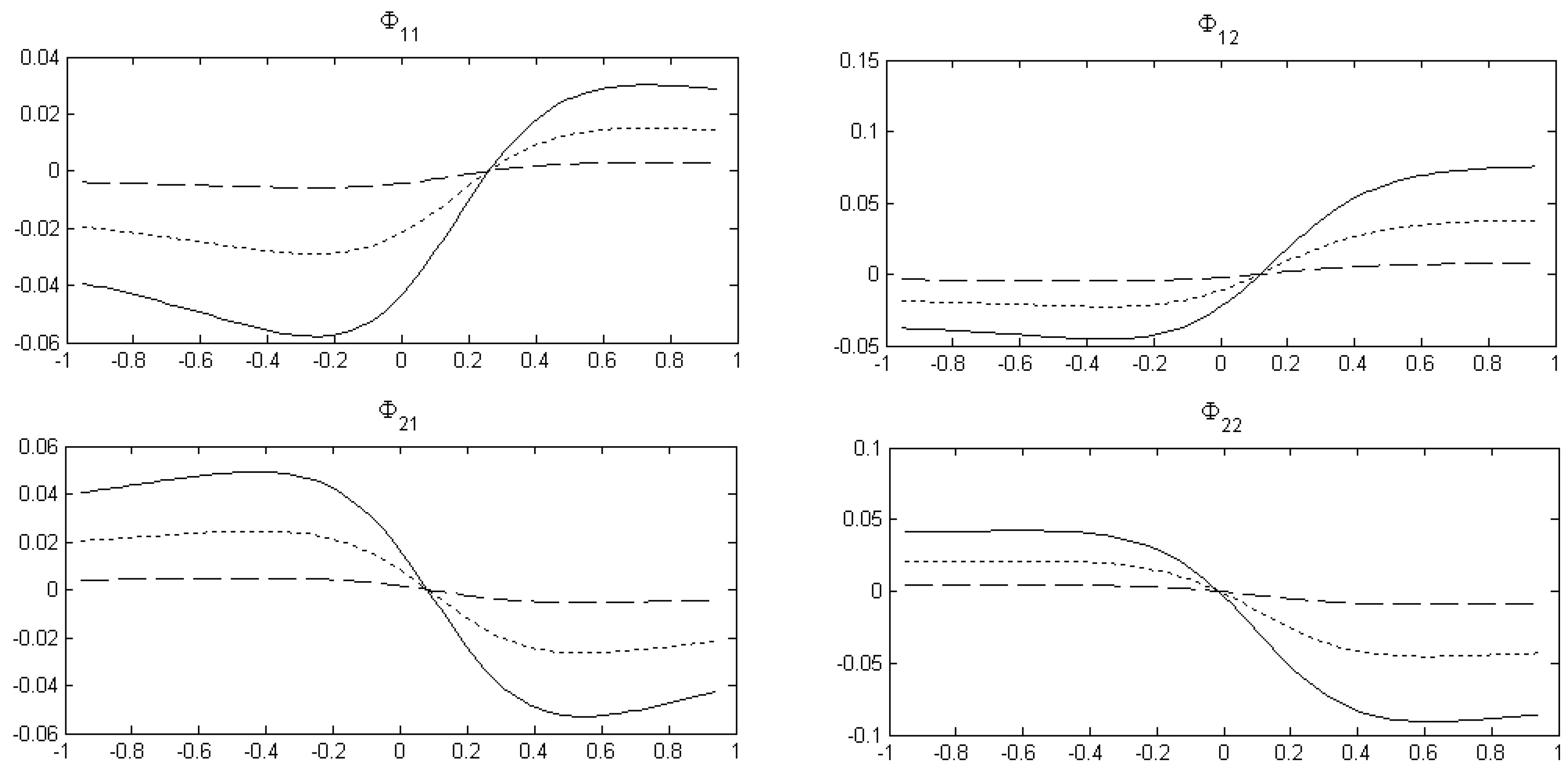

Figure 3 suggests that the use of an iterative scheme could potentially be useful if the sample size is small, while for larger sample sizes the gain appears to be limited. Of course these plots depend on Φ and the correlation between the innovations. To illustrate the effect of changing Φ and

,

Figure 4 shows the bias also as a function of

but with the remaining data-generating parameters equal to those given in (12). Comparing

Figure 4 with

Figure 3 it is clear that the bias functions are quite different. For example, all the bias functions are now very flat when the second variable is highly persistent, which suggests a limited effect of using an iterative scheme when the data-generating process is given by (12).

Figure 3.

Bias functions. The figure shows the least squares bias in the VAR(1) slope coefficients as a function of with the remaining data-generating parameters given in (11) for T = 50 (solid line), T = 100 (dotted line), and T = 500 (dashed line). The bias functions are calculated using the analytical bias formula (7).

Figure 3.

Bias functions. The figure shows the least squares bias in the VAR(1) slope coefficients as a function of with the remaining data-generating parameters given in (11) for T = 50 (solid line), T = 100 (dotted line), and T = 500 (dashed line). The bias functions are calculated using the analytical bias formula (7).

Figure 4.

Bias functions. The figure shows the least squares bias in the VAR(1) slope coefficients as a function of with the remaining data-generating parameters given in (12) for T = 50 (solid line), T = 100 (dotted line), and T = 500 (dashed line). The bias functions are calculated using the analytical bias formula (7).

Figure 4.

Bias functions. The figure shows the least squares bias in the VAR(1) slope coefficients as a function of with the remaining data-generating parameters given in (12) for T = 50 (solid line), T = 100 (dotted line), and T = 500 (dashed line). The bias functions are calculated using the analytical bias formula (7).

Table 4 shows simulation results for the iterative scheme using the data-generating processes in (11) and (12), respectively. The convergence criteria used in the iterative scheme is that the maximum difference across the slope coefficients between two consecutive iterations must be smaller than 10

.

12 We calculate

as

, which implies that we in applying the iterative scheme for the analytical bias formula also reestimate

for each iteration based on the ’new’ estimates of Φ and

.

13 For ease of comparison,

Table 4 also contains the results based on the simple ‘plug-in’ approach as reported in

Table 1 and

Table 2.

Regarding WLS,

Table 4 shows that with the data-generating process given in (11) iteration reduces the bias but increases the variance. Only for

is the bias reduction of a sufficient magnitude to offset the increase in variance implying a decrease in RMSE. For

RMSE increases when iterating on the WLS estimator.

14 For the data-generating process given in (12) the results for WLS are quite different. Using an iterative scheme, bias is now larger than for the ‘plug-in’ approach when

. Also, bias increases as a function of the sample size up to

. However, due to a large decrease in variance, RMSE still decreases as the sample size increases.

Table 4.

Bias-correction using an iterative scheme. The results in Panel A are based on 10,000 simulations from the VAR(1) model given in (11). The results in Panel B are based on the model given in (12). WLS

and ABF

give the results when using an iterative scheme for WLS and ABF, respectively. ABF

gives the results when inverting the analytical bias formula to obtain an estimate of the bias. See also the caption to

Table 1.

Table 4.

Bias-correction using an iterative scheme. The results in Panel A are based on 10,000 simulations from the VAR(1) model given in (11). The results in Panel B are based on the model given in (12). WLS and ABF give the results when using an iterative scheme for WLS and ABF, respectively. ABF gives the results when inverting the analytical bias formula to obtain an estimate of the bias. See also the caption to Table 1.

| | | Panel A | Panel B |

| | | Bias | Variance | RMSE | #NS | Bias | Variance | RMSE | #NS |

| WLS | 0.1606 | 1.9135 | 0.1438 | 198 | 0.0295 | 2.1234 | 0.1446 | 63 |

| | WLS | 0.0511 | 1.9831 | 0.1423 | 612 | 0.0104 | 2.4418 | 0.1531 | 182 |

| | ABF | 0.0382 | 1.7520 | 0.1336 | 1613 | 0.0151 | 2.1350 | 0.1456 | 446 |

| | ABF | 0.0284 | 1.7090 | 0.1317 | 1652 | 0.0082 | 2.1452 | 0.1456 | 535 |

| | ABF | 0.0409 | 1.5396 | 0.1254 | 5912 | 0.1897 | 2.1390 | 0.1514 | 3054 |

| WLS | 0.0229 | 0.7549 | 0.0880 | 21 | 0.0109 | 1.0095 | 0.0984 | 2 |

| | WLS | 0.0015 | 0.8646 | 0.0928 | 102 | 0.0284 | 1.1795 | 0.1062 | 6 |

| | ABF | 0.0025 | 0.6821 | 0.0826 | 307 | 0.0016 | 0.8992 | 0.0934 | 6 |

| | ABF | 0.0018 | 0.6750 | 0.0821 | 312 | 0.0009 | 0.9011 | 0.0934 | 7 |

| | ABF | 0.0444 | 0.6205 | 0.0813 | 2847 | 0.0796 | 0.9471 | 0.1003 | 337 |

| WLS | 0.0021 | 0.3471 | 0.0590 | 0 | 0.0264 | 0.5237 | 0.0720 | 0 |

| | WLS | 0.0019 | 0.4428 | 0.0664 | 3 | 0.0581 | 0.6566 | 0.0818 | 0 |

| | ABF | 0.0001 | 0.3004 | 0.0547 | 1 | 0.0001 | 0.4059 | 0.0621 | 0 |

| | ABF | 0.0001 | 0.2995 | 0.0546 | 1 | 0.0001 | 0.4062 | 0.0622 | 0 |

| | ABF | 0.0198 | 0.2854 | 0.0551 | 164 | 0.0230 | 0.4184 | 0.0652 | 0 |

| WLS | 0.0004 | 0.1322 | 0.0363 | 0 | 0.0227 | 0.2367 | 0.0496 | 0 |

| | WLS | 0.0030 | 0.1942 | 0.0442 | 0 | 0.0511 | 0.3338 | 0.0607 | 0 |

| | ABF | 0.0000 | 0.1091 | 0.0329 | 0 | 0.0000 | 0.1550 | 0.0381 | 0 |

| | ABF | 0.0000 | 0.1090 | 0.0329 | 0 | 0.0000 | 0.1550 | 0.0381 | 0 |

| | ABF | 0.0035 | 0.1067 | 0.0331 | 0 | 0.0036 | 0.1568 | 0.0389 | 0 |

For the analytical bias formula iteration generally yields a small reduction in bias compared to the ‘plug-in’ approach, while the effect on variance depends on the data-generating process. For the process given in (11) variance decreases slightly when iterating, while there is a small increase for the process given in (12). Comparing the effect on RMSE from using an iterative scheme relative to the ‘plug-in’ approach, we only see a noticeable decrease for (11) with

. This result is consistent with the bias functions shown in

Figure 3 and

Figure 4, and suggests that iteration often has a limited effect.

Instead of iterating on the analytical bias formula, we can (conditional on

) use it to back out the ’true’ Φ (and thereby

and

), which can then be inserted into the bias formula to obtain an estimate of the bias.

Table 4 shows that this approach generally has a noticeably larger bias than both the ‘plug-in’ approach and the iterative scheme.

15 The effect on the variance depends on the data-generating process. For the process given in (11) variance is lowest when inverting the bias formula resulting in a slightly lower RMSE compared to the other two approaches, while for (12) the variance and RMSE are both higher when inverting.

3.3. Bias-Correction in Nearly Non-Stationary Models

Although the true VAR system is stationary, we often face the risk of finding unit or explosive roots when estimating a persistent system based on a finite sample. In

Table 1 for

we found that in 25 out of 10,000 simulations, OLS yields a non-stationary system. When correcting for bias using either the analytical bias formula or a bootstrap procedure this number increases considerably. In this section we compare the finite-sample properties of OLS (both with and without bias-correction) to the Yule-Walker (YW) estimator, which is guaranteed to ensure a stationary system. We also analyze how Kilian’s [

10] approach to ensure stationarity affects the finite-sample properties of the bias-correction methods.

Table 5 reports simulation results for the following VAR(1) model

where the eigenvalues of Φ are 0.748 and 0.992. This VAR(1) model is also used in a simulation study by Amihud et al. [

32] and is more persistent than the ones used in

Table 1,

Table 2,

Table 3 and

Table 4, which increases the risk of estimating a non-stationary model using OLS and entering the non-stationary region of the parameter space when correcting for bias. Panel A shows the finite-sample properties of the OLS and YW estimators. Panel B reports the results when using Kilian’s approach to ensure stationarity when correcting for bias using the analytical bias formulas (6) and (8) and bootstrapping (only OLS), while Panel C shows the corresponding results without applying Kilian’s approach. The sample size is 100.

16 From Panel A it is clear that YW has a much larger bias than OLS. This is also the case for the variance and, hence, the RMSE for YW is larger than for OLS. However, in contrast to OLS, YW always results in a stationary system, which implies that it is always possible to adjust for bias using the analytical bias formula. In

Table 5, OLS yields a non-stationary model in 250 out of 10,000 simulations. The question now is if using the analytical bias formula for YW yields similar finite-sample properties as in the case of OLS? Panel B (where the procedure by Kilian [

10] is applied) shows that this is not the case. YW still has a larger bias than OLS and the variance is more that three times as large. Comparing the results for YW with and without bias correction we see that the bias is clearly reduced by applying the analytical bias formula, but the variance also more than doubles. It is also worth noting that in 7,055 out of 10,000 simulations the system ends up in the non-stationary region when correcting YW for bias compared to only 3,567 for OLS.

17

Table 5.

Bias-correction in a nearly non-stationary VAR(1) model. The results in this table are based on 10,000 simulations from the VAR(1) model given in (14). The sample size is 100. Panel A shows the results from estimating the VAR(1) model using ordinary least squares (OLS) and Yule-Walker (YW). Panel B and C show the results when adjusting the ordinary least squares estimate for bias using the analytical bias formula (7) (ABF) and bootstrapping (BOOT), and when adjusting the Yule-Walker estimate for bias using the analytical bias formula (8). In Panel B (in contrast to Panel C) the correction by Kilian (1998a) to ensure a stationary VAR system is applied. See also the caption to

Table 1.

Table 5.

Bias-correction in a nearly non-stationary VAR(1) model. The results in this table are based on 10,000 simulations from the VAR(1) model given in (14). The sample size is 100. Panel A shows the results from estimating the VAR(1) model using ordinary least squares (OLS) and Yule-Walker (YW). Panel B and C show the results when adjusting the ordinary least squares estimate for bias using the analytical bias formula (7) (ABF) and bootstrapping (BOOT), and when adjusting the Yule-Walker estimate for bias using the analytical bias formula (8). In Panel B (in contrast to Panel C) the correction by Kilian (1998a) to ensure a stationary VAR system is applied. See also the caption to Table 1.

| | Mean Slope Coefficients | | | | |

| | | | | | Bias | Variance | RMSE | #NS |

| Panel A | | | | | | | | |

| OLS | 0.7508 | 0.0885 | 0.1032 | 0.8890 | 0.1290 | 0.6056 | 0.0844 | 250 |

| YW | 0.6567 | -0.0649 | 0.1542 | 0.9582 | 1.2748 | 0.6578 | 0.1284 | 0 |

| Panel B | | | | | | | | |

| ABF (OLS) | 0.7813 | 0.0943 | 0.0968 | 0.9217 | 0.0182 | 0.5585 | 0.0745 | 3567 |

| ABF (YW) | 0.7829 | 0.0922 | 0.1105 | 0.9036 | 0.0448 | 1.7573 | 0.1297 | 7055 |

| BOOT | 0.7823 | 0.0951 | 0.0986 | 0.9234 | 0.0153 | 0.5709 | 0.0750 | 4266 |

| Panel C | | | | | | | | |

| ABF (OLS) | 0.7872 | 0.0951 | 0.0958 | 0.9276 | 0.0089 | 0.5599 | 0.0742 | 3567 |

| ABF (YW) | 0.8778 | 0.1465 | 0.1522 | 0.9398 | 0.2734 | 2 | 1.4960 | 7055 |

| BOOT | 0.7904 | 0.0962 | 0.0980 | 0.9311 | 0.0047 | 0.5785 | 0.0750 | 4266 |

Until now we have used the approach by Kilian [

10] to ensure a stationary VAR system after correcting for bias. Based on the same 10,000 simulations as in Panel B, Panel C shows the finite-sample properties without applying Kilian’s approach. For OLS (using both the analytical bias formula and a bootstrap procedure) bias decreases and variance increases slightly when we allow the system to be non-stationary after bias-correction. This result is not surprising. The VAR system is highly persistent and very small changes in Φ can result in a non-stationary system, e.g., if

is 0.95 instead of 0.94 the system has a unit root. Hence, when applying Kilian’s approach, we often force the estimated coefficients to be smaller than the true values. In contrast, when we allow the system to be non-stationary after bias-correction some of the estimated coefficients will be smaller than the true values and some will be larger and, hence, positive and negative bias will offset each other across the 10,000 simulations. Likewise, this will also imply that the variance is larger when we do not apply Kilian’s approach. However, comparing the results for OLS in Panel B and Panel C it is clear that these differences are very small, which implies that Kilian’s approach does not severely distort the finite-sample properties of the bias-correction methods; and this even though we apply the approach in roughly 4,000 out of 10,000 simulations. In contrast, for YW it turns out to be essential to use Kilian’s approach as seen from Panel C. Note also that allowing the system to be non-stationary (i.e. not applying Kilian’s approach) is not consistent with the fact that the analytical bias formula is derived under the assumption of stationarity.

3.4. Bias-Correction in Non-Stationary Models

One of the major advantages of the weighted least squares estimator by Chen and Deo [

30] compared to the analytical bias formula is that it allows for unit roots. In

Section 3.3 we simulated from a stationary but highly persistent VAR(1) model and we assumed that the researcher has a priori knowledge that the system is stationary and thus considered the approach by Kilian [

10] to ensure stationarity when correcting for bias. As a robustness check we now simulate from a bivariate VAR(1) model with unit roots and we assume that the researcher acknowledges that the system might be non-stationary and thus does not want to force the system to be stationary. The analytical bias formula is derived under the assumption of stationarity so the analysis in this section is in principle invalid for ABF. However, similar to the analysis of the properties of WLS under random initial values, it is also of interest to examine the finite-sample properties of ABF in the non-stationary case. To our knowledge the asymptotic theory of the properties of the bootstrap bias-corrected estimator for unit root models has not yet been developed.

Table 6.

Bias-correction in a bivariate VAR(1) model with one unit root. The results in this table are based on 10,000 simulations from the VAR(1) model given in (15). See also the caption to

Table 1.

Table 6.

Bias-correction in a bivariate VAR(1) model with one unit root. The results in this table are based on 10,000 simulations from the VAR(1) model given in (15). See also the caption to Table 1.

| | | Mean Slope Coefficients | | | | |

| | | | | | | Bias | Variance | RMSE | #NS |

| OLS | 0.9694 | -0.0505 | 0.1887 | 0.7900 | 0.5172 | 1.1895 | 0.1293 | 1153 |

| | WLS | 1.0227 | -0.0597 | 0.1933 | 0.8048 | 0.2682 | 1.0373 | 0.1138 | 3067 |

| | ABF | 1.0168 | -0.0319 | 0.1556 | 0.8583 | 0.1084 | 1.0444 | 0.1072 | 5830 |

| | BOOT | 1.0364 | -0.0479 | 0.1584 | 0.8615 | 0.0489 | 1.1038 | 0.1071 | 6772 |

| OLS | 1.0235 | -0.0521 | 0.1658 | 0.8451 | 0.1028 | 0.3098 | 0.0636 | 956 |

| | WLS | 1.0521 | -0.0580 | 0.1677 | 0.8497 | 0.0503 | 0.2624 | 0.0557 | 2972 |

| | ABF | 1.0426 | -0.0423 | 0.1441 | 0.8762 | 0.0274 | 0.2856 | 0.0558 | 5156 |

| | BOOT | 1.0553 | -0.0514 | 0.1460 | 0.8776 | 0.0083 | 0.2892 | 0.0544 | 6083 |

| OLS | 1.0483 | -0.0544 | 0.1534 | 0.8656 | 0.0222 | 0.0952 | 0.0340 | 754 |

| | WLS | 1.0626 | -0.0581 | 0.1541 | 0.8668 | 0.0108 | 0.0832 | 0.0306 | 3113 |

| | ABF | 1.0560 | -0.0501 | 0.1415 | 0.8791 | 0.0074 | 0.0928 | 0.0316 | 4819 |

| | BOOT | 1.0626 | -0.0545 | 0.1422 | 0.8797 | 0.0023 | 0.0919 | 0.0306 | 5777 |

| OLS | 1.0625 | -0.0580 | 0.1449 | 0.8754 | 0.0027 | 0.0258 | 0.0168 | 550 |

| | WLS | 1.0677 | -0.0595 | 0.1451 | 0.8755 | 0.0013 | 0.0240 | 0.0158 | 3150 |

| | ABF | 1.0650 | -0.0566 | 0.1401 | 0.8799 | 0.0009 | 0.0258 | 0.0163 | 4711 |

| | BOOT | 1.0674 | -0.0583 | 0.1402 | 0.8801 | 0.0002 | 0.0254 | 0.0160 | 5558 |

We consider two bivariate VAR(1) models.

Table 6 reports results for the following system

where the eigenvalues of Φ are 1 and 0.95, while

Table 7 reports results for the system

where both eigenvalues of Φ are 1. These two VAR(1) models are both used by Chen and Deo [

30] in a simulation study of the finite-sample properties of WLS. Due to an infinite variance of

in the presence of unit roots, in the simulation study initial values of

are fixed and equal to 0 rather than random.

Table 6 and

Table 7 both show that OLS delivers biased estimates and that WLS, ABF, and BOOT all reduce both bias and RMSE. Hence, even though ABF is derived under the assumption of stationarity, it still has better finite-sample properties than OLS. Comparing WLS, ABF, and BOOT in terms of bias we see that BOOT consistently delivers the smallest bias, irrespective of one or two unit roots. In contrast to the stationary case ABF performs noticeably worse than BOOT. It does, however, yield a smaller bias than WLS in the presence of one unit root, while the opposite is the case with two unit roots. With respect to variance WLS consistently performs best, especially so when there are two unit roots. Altogether these results imply that BOOT has the smallest RMSE when there is one unit root (and for small samples when there are two unit roots) while this is the case for WLS when there are two unit roots (and the sample size is not too small).

Table 7.

Bias-correction in a bivariate VAR(1) model with two unit roots. The results in this table are based on 10,000 simulations from the VAR(1) model given (16). See also the caption to

Table 1.

Table 7.

Bias-correction in a bivariate VAR(1) model with two unit roots. The results in this table are based on 10,000 simulations from the VAR(1) model given (16). See also the caption to Table 1.

| | | Mean Slope Coefficients | | | | |

| | | | | | | Bias | Variance | RMSE | #NS |

| OLS | 0.9575 | -0.0075 | 0.1914 | 0.8665 | 0.4975 | 0.9676 | 0.1169 | 3390 |

| | WLS | 1.0220 | -0.0247 | 0.2038 | 0.8749 | 0.1886 | 0.7893 | 0.0973 | 5748 |

| | ABF | 1.0064 | 0.0076 | 0.1630 | 0.9199 | 0.1922 | 0.8770 | 0.1021 | 7736 |

| | BOOT | 1.0413 | -0.0259 | 0.1731 | 0.9082 | 0.0501 | 0.9029 | 0.0958 | 8377 |

| OLS | 1.0146 | -0.0153 | 0.1704 | 0.9076 | 0.1289 | 0.2164 | 0.0549 | 4113 |

| | WLS | 1.0534 | -0.0292 | 0.1779 | 0.9072 | 0.0327 | 0.1576 | 0.0423 | 6533 |

| | ABF | 1.0352 | -0.0103 | 0.1566 | 0.9247 | 0.0731 | 0.2165 | 0.0522 | 8125 |

| | BOOT | 1.0620 | -0.0311 | 0.1638 | 0.9184 | 0.0105 | 0.2063 | 0.0449 | 8561 |

| OLS | 1.0455 | -0.0245 | 0.1634 | 0.9173 | 0.0362 | 0.0505 | 0.0269 | 4578 |

| | WLS | 1.0673 | -0.0339 | 0.1670 | 0.9160 | 0.0066 | 0.0347 | 0.0195 | 6942 |

| | ABF | 1.0547 | -0.0244 | 0.1585 | 0.9217 | 0.0223 | 0.0537 | 0.0261 | 8355 |

| | BOOT | 1.0710 | -0.0352 | 0.1615 | 0.9195 | 0.0027 | 0.0487 | 0.0216 | 8671 |

| OLS | 1.0659 | -0.0332 | 0.1605 | 0.9197 | 0.0061 | 0.0078 | 0.0106 | 4659 |

| | WLS | 1.0748 | -0.0374 | 0.1614 | 0.9193 | 0.0009 | 0.0052 | 0.0074 | 7059 |

| | ABF | 1.0696 | -0.0343 | 0.1595 | 0.9203 | 0.0035 | 0.0081 | 0.0100 | 8351 |

| | BOOT | 1.0764 | -0.0381 | 0.1601 | 0.9200 | 0.0004 | 0.0075 | 0.0084 | 8653 |

3.5. Bias-Correction When Data Are Skewed and Fat-Tailed

Until now we have generated data from a multivariate normal distribution. However, in many empirically relevant models the normality assumption often fails. The analytical bias formula is not derived under a normality assumption, but it is unclear how the finite-sample properties of bias-correction using ABF compare to those of bootstrapping if the data are, for example, very skewed and fat-tailed. Furthermore, researchers often use a parametric bootstrap based on a normal distribution instead of the usual residual-based bootstrap procedure. The obvious question here is: do we commit errors when using this parametric bootstrap approach when data are very skewed and fat-tailed? Also, WLS is derived under the assumption of normality. How does this estimator perform under skewed and fat-tailed data? In this section, we address these issues.

To obtain data that are skewed and have fat tails we use the data-generating parameters in (11) but follow Kilian [

24] and make random draws for the innovations from a Student’s

t-distribution with four degrees of freedom and a

-distribution with three degrees of freedom, respectively.

18 Table 8 shows the results. For the bias-correction methods we use the approach by Kilian [

10] to ensure stationarity. The sample size is 100.

19

Table 8.

Bias-correction in a VAR(1) model, skewed and fat-tailed innovations. The results in this table are based on 10,000 simulations from the VAR(1) model given in (11) but with innovations randomly drawn from Student’s t-distribution with four degrees of freedom (Panel A) and

-distribution with three degrees of freedom (Panel B). The sample size is 100. PARBOOT are bias-adjusted estimates from the bootstrap based on normally distributed innovations. See also the caption to

Table 1.

Table 8.

Bias-correction in a VAR(1) model, skewed and fat-tailed innovations. The results in this table are based on 10,000 simulations from the VAR(1) model given in (11) but with innovations randomly drawn from Student’s t-distribution with four degrees of freedom (Panel A) and -distribution with three degrees of freedom (Panel B). The sample size is 100. PARBOOT are bias-adjusted estimates from the bootstrap based on normally distributed innovations. See also the caption to Table 1.

| | Mean Slope Coefficients | | | | |

| | | | | | Bias | Variance | RMSE | #NS |

| Panel A | | | | | | | | |

| OLS | 0.7541 | 0.0968 | 0.1008 | 0.8038 | 0.1063 | 0.7525 | 0.0925 | 2 |

| WLS | 0.7694 | 0.1035 | 0.1025 | 0.8244 | 0.0402 | 0.7554 | 0.0890 | 8 |

| ABF | 0.7921 | 0.0994 | 0.0983 | 0.8438 | 0.0026 | 0.7053 | 0.0840 | 489 |

| BOOT | 0.7933 | 0.1003 | 0.0993 | 0.8454 | 0.0017 | 0.7160 | 0.0846 | 525 |

| PARBOOT | 0.7938 | 0.1002 | 0.0993 | 0.8458 | 0.0014 | 0.7150 | 0.0845 | 542 |

| Panel B | | | | | | | | |

| OLS | 0.7590 | 0.1000 | 0.1029 | 0.8102 | 0.0817 | 0.6642 | 0.0861 | 2 |

| WLS | 0.8135 | 0.0885 | 0.0900 | 0.8578 | 0.0119 | 0.8981 | 0.0952 | 132 |

| ABF | 0.7941 | 0.0998 | 0.0991 | 0.8453 | 0.0015 | 0.6242 | 0.0790 | 307 |

| BOOT | 0.7989 | 0.1029 | 0.1010 | 0.8520 | 0.0004 | 0.6315 | 0.0794 | 450 |

| PARBOOT | 0.7994 | 0.1028 | 0.1009 | 0.8524 | 0.0004 | 0.6314 | 0.0794 | 451 |

Overall, the results in

Table 8 are in line with our previous findings for stationary models with random initial values, namely that OLS yields highly biased estimates, WLS is able to reduce this bias but at the cost of increased variance and the bias correction methods provide a large bias reduction compared to both OLS and WLS. Comparing ABF and BOOT, we see that similar to the results in

Table 1,

Table 2,

Table 3 and

Table 5, BOOT yields a slightly smaller bias than ABF and has a slightly higher variance.

In addition to the residual-based bootstrap approach,

Table 8 also shows the results when applying a parametric bootstrap procedure based on an assumption of normally distributed data (PARBOOT). Given that the innovations are skewed and fat-tailed we could expect this approach to have inferior properties compared to both the residual-based bootstrap that directly takes into account the non-normality of the data, and the analytical bias formula that is derived without the assumption of normality. The results in

Table 8 show that this is not the case. PARBOOT has both smaller bias and lower variance than BOOT. However, the differences are very small, and for all practical purposes the results in

Table 8 suggest that the use of BOOT and PARBOOT will give similar results.

These results contrast those of Kilian [

24] who examines the coverage accuracy of various methods for constructing confidence intervals for impulse responses when data are non-normally distributed. Two of the methods he considers are based on the analytical bias formula combined with a residual-based and a parametric (assuming Gaussianity) bootstrap procedure, respectively. Kilian finds that in terms of constructing confidence intervals for impulse responses the residual-based bootstrap procedure strictly dominates the parametric approach when data have fat tails and are skewed. In the present paper we consider parameter estimates and not confidence intervals, which inevitably depend on the entire distribution of innovations. Our results show that with respect to point estimates using an incorrect parametric bootstrap has no negative consequences, which lend support to the use of a parametric bootstrap procedure when data do not match the assumed distribution.

{kind=link}

{kind=link}

{kind=link}

{kind=link}