1. Introduction

Univariate continuous distributions play a crucial role in modeling real-world phenomena. While well-known distributions like the normal, exponential, and Pareto distributions are commonly used, there is often a need for specialized distributions, to model specific data patterns. One established practice for defining more flexible distributions is through the quantile function (QF)

where

represents the cumulative distribution function (CDF) of the random variable

X. Thus, if

F is strictly increasing,

Q and

F are inverse functions of each other, and

. QFs possess numerous distinct characteristics that are absent in CDFs. We highlight that new and more flexible QFs can be easily constructed from the combination of existing QFs. For example, the product of QFs is still a valid QF.

Since the QF provides all valuable information about the distribution’s shape, several QF models have been proposed in the literature. The symmetric Tukey lambda distribution (

Tukey 1960) and its asymmetric version, known as the generalized lambda distribution (

Ramberg and Schmeiser 1972), are both defined in terms of their QF. Similarly, the quantile-based skew logistic distribution introduced by

Gilchrist (

2000) is also defined through its QF. More recently,

Sankaran et al. (

2016) introduce a new QF resulting from the sum of the QFs of the generalized Pareto and Weibull distributions.

In some cases, the density and distribution functions for distributions expressed through QFs are not available in closed form, except for specific parameter values. However, those functions can be easily computed by numerically inverting the corresponding QF. One significant advantage of these distributions is the simplicity of their QF, which facilitates the generation of random values through the use of uniform random variables and the application of inference procedures based on quantiles.

In this article, we are interested in the power–Pareto distribution introduced in

Gilchrist (

2000) and further studied in

Hankin and Lee (

2006). This is a versatile family of distributions for a non-negative random variable, such as income and wealth. This model is formed through the product of the power and Pareto QFs as

where

,

, and

. We write

whenever

X has the QF in Equation (

1). The parameter

c is related to the scale, while

and

control the shape of the distribution. By fixing or restricting some of this distribution’s parameters, we obtain well-known reduced versions. More precisely, if

and

, then

X follows a Pareto (type I) distribution with the QF

and if

and

,

X has a scaled power distribution with the QF

Furthermore, it can be observed that when

,

X has the well-known log-logistic distribution, which is a special case of

Burr (

1942) type XII and

Dagum (

1977) family of distributions (for further details, see

Caeiro and Mateus 2024). The case

is not considered here, as it results in a degenerate distribution at

c. In the literature, the power–Pareto model in Equation (

1) is also known as the Davies distribution (

Hankin and Lee 2006) or Hankin–Lee distribution (

Nair and Vineshkumar 2010).

Hankin and Lee (

2006) proposed two inference procedures to estimate the parameters

c,

, and

in Equation (

1), namely the maximum likelihood and the least squares method for the logged order statistics. Additionally, the authors compare the efficiency of those two estimation methods by comparing their variance. Since maximum likelihood estimators are often severely biased, for small sample sizes, we argue that solely considering the variance of the estimators may not provide a comprehensive assessment of their performance, and thus, it could lead to misleading conclusions. Therefore, the primary goal of this paper is to discuss a broader set of estimation techniques and consider alternative criteria for a more precise and unbiased comparison of the estimators.

The remainder of the paper is organized as follows. In

Section 2, we describe various known properties of the power–Pareto model, like probability density and distribution functions, moments, and quantile-based measures. Several inferential procedures for the parameters of the power–Pareto distribution are discussed in

Section 3. In

Section 4, we conduct Monte Carlo simulations to analyze the performance of the different inferential procedures. In

Section 5, we apply the inferential methods to two real datasets, and

Section 6 concludes the article.

3. Estimation Methods for the Power–Pareto Distribution

In this section, we discuss the parameter estimation methods employed in this paper. For the estimation of the parameters of the aforementioned reduced versions of the power–Pareto model, we refer to

Bhatti et al. (

2018);

Caeiro et al. (

2015);

Caeiro and Mateus (

2023);

Lu and Tao (

2007);

Mateus and Caeiro (

2022);

Rytgaard (

1990);

Shakeel et al. (

2016);

Zaka et al. (

2013). Concerning the three-parameter power–Pareto model, in Equation (

1),

Hankin and Lee (

2006) proposed the estimation of the parameters by two methods: maximum likelihood and quantile least squares. The variance–covariance matrix of those two methods is also provided in

Hankin and Lee (

2006). The maximum likelihood estimators possess desirable asymptotic properties. However, in the case of small samples, this method may exhibit lower efficiency, when compared to other estimation methods. Therefore, in this paper, we consider not only the estimation methods in

Hankin and Lee (

2006), but also new estimation methods. In the following, let

,

,

…,

represent a sample of size

n, from the power–Pareto distribution with all three parameters assumed unknown.

3.1. Maximum Likelihood (ML)

The maximum likelihood (ML) estimators of the three parameters are obtained by solving an optimization problem, which involves maximizing the likelihood function, or equivalently, minimizing the negative log-likelihood function. This can be expressed as follows:

where

represents the solution of the equation

. Here,

denotes the ML estimate of

.

While the ML estimation method provides asymptotically unbiased estimators and efficiency for large sample sizes, the lack of a closed-form expression for the probability density function requires to be obtained through a three-dimensional numerical search. This makes the ML method computationally intensive, and convergence of the negative log-likelihood to the global minimum can be sensitive to the initial values. Thus, this estimation method for the parameters of the power–Pareto can be computationally complex and challenging, especially for large datasets. Additionally, the ML method can be impacted by model misspecification. Therefore, it is crucial to consider alternative methods, potentially with closed-form expressions for the estimators.

3.2. Log Quantile Least Squares (LQLS)

Hankin and Lee (

2006) proposed a regression method for estimating the parameters of the power–Pareto distribution using order statistics. To achieve a simple linear relation involving the parameters, a log transformation is applied, yielding the sum of squares

that needs to be minimized with respect to the vector parameters

. Since

X is continuous, the inverse probability integral transform guarantees

, where

U denotes a uniform distribution on the interval

. Consequently,

where

denotes the

-order statistic from a sample of size

n from a uniform distribution on

. Note that

has a Beta distribution with parameters

i and

. Using Equation (

11), we have

with

. Thus,

where

is the digamma function, the derivative of the log gamma function. For

n integer,

where

is Euler’s constant. Then, by introducing the notation

, Equation (

10) can be expressed in matrix form as

where

is a column matrix with the logarithm of the order statistics from the sample,

, and

is an

matrix where the

row is given by

, with

. Applying the least squares method, the vector parameters are estimated by

Consequently,

The LQLS method offers several advantages. Firstly, it is more robust against outliers, as the logarithmic transformation reduces the influence of those values. Secondly, unlike the ML method, estimates are based on the order statistics and require straightforward calculations, leading to computational efficiency. However, the LQLS method may exhibit lower efficiency when compared to the ML method and can be sensitive to small sample sizes.

3.3. Percentile (P)

Percentile points were first used for the determination of parameters of the Weibull model (

Kao 1959). This method is nowadays popular due to its simplicity. Estimators are found from the relation, through the CDF or the QF, between probabilities and percentile values. To estimate the parameters, one must consider the same number of percentiles. Therefore, given three distinct cumulative probability levels

,

, and

(

), the corresponding

percentiles,

, are the values

,

, and

such that

with Q the QF in Equation (

1). Next, applying a log transformation to the ratio between two consecutive percentiles, we obtain

and

Solving the above two equations for

and

, we obtain

and

Next, we use the following equation for the second percentile:

The estimators are obtained by replacing, in Equations (

13)–(

15), the percentiles

, by the corresponding sample percentiles. A possible choice for the probabilities is

. Equivalently, let

I be a set of three distinct values from the first

n positive integer values,

, where

n denotes the sample size. Another possible choice of percentiles is

,

, associated to the cumulative probabilities

, where

a and

b are real constants. A popular choice of the constants is

and

.

The P method offers simplicity in computation and robustness against outliers. This makes it straightforward to implement and suitable for exploratory analysis and initial estimation, providing a quick and effective way to estimate parameters. However, it may be less efficient and less accurate compared to other methods.

3.4. Least Squares (LS) and Weighted Least Squares (WLS)

Here we consider the difference between the empirical and the theoretical CDF. Then, the least squares (LS) estimator of

, denoted by

, can be obtained as

Furthermore, the estimation of parameters using the weighted least squares (WLS) method, symbolized as

, can be determined by

The LS method involves minimizing the squared difference between the empirical and theoretical CDFs. This method is straightforward to implement and interpret, making it accessible for various applications. However, LS assumes homoscedasticity, which is not valid, since the variance of depends on the index i. This violation does not affect the bias of the estimators, but may increase their variance. On the other hand, the weighting scheme used in the WLS method addresses heteroscedasticity by assigning larger weights to observations that are closer to the center of the sample and smaller weights to observations that are closer to the edges of the sample. Additionally, both the LS and WLS methods are computationally intensive, since both depend on the CDF, which needs to be computed numerically.

3.5. Quantile Least Squares (QLS)

The quantile least squares (QLS) estimator of distribution parameters, denoted by

, can be derived by

with

defined in Equation (

8).

The QLS estimator minimizes the squared difference between the order statistics and their expected value, which can be easily obtained from Equation (

8). A limitation of this method is that

only exists if

; therefore, the QLS should only be considered if

is a small positive value. Furthermore, the accuracy of parameter estimates can be affected by the presence of large outliers.

A weighted version of this method was not considered because it would further restrict its domain of validity.

4. Comparison of the Estimation Methods by Monte Carlo Simulation

In this section, a Monte Carlo simulation study is carried out to compare the performance of the proposed P, LS, WLS, and QLS estimation methods, and to compare them with the ML and LQLS methods, proposed by

Hankin and Lee (

2006).

Davies package was used for the ML method. Parameter estimation with the LS, WLS, and QLS was performed with the R optimization function

optim of the R Software version 4.0.0 and using the starting values provided by the

davies.start function in

Davies package. The power–Pareto distribution was used to generate

samples with sizes

, 20, 50, 75, and 100. Sample values are generated using the inversion method. In the simulation study, the following parameter combinations were considered:

Case 1: ;

Case 2: ;

Case 3: ;

Case 4: ;

Case 5: .

All the parameter combinations provide a power–Pareto distribution with finite mean value and different levels of positive skewness and kurtosis. Both measures increase with respect to

and decrease with respect to

. The corresponding densities, for all five cases, are presented in

Figure 2.

For each of the three parameters of

, denoted generically by

, we computed the simulated average bias (ABias), median bias (MBias), and root mean squared error (RMSE) of the corresponding estimator

. The statistics are defined by

where

is the estimate of

computed using the

sample.

As a global criterion of comparison, we also computed the average absolute difference between the true and the estimated CDFs,

and the average of the maximum absolute difference between the true and estimated CDFs,

where

represents the

observation in the

sample. The smaller the values of

and

, the better the fit to the data.

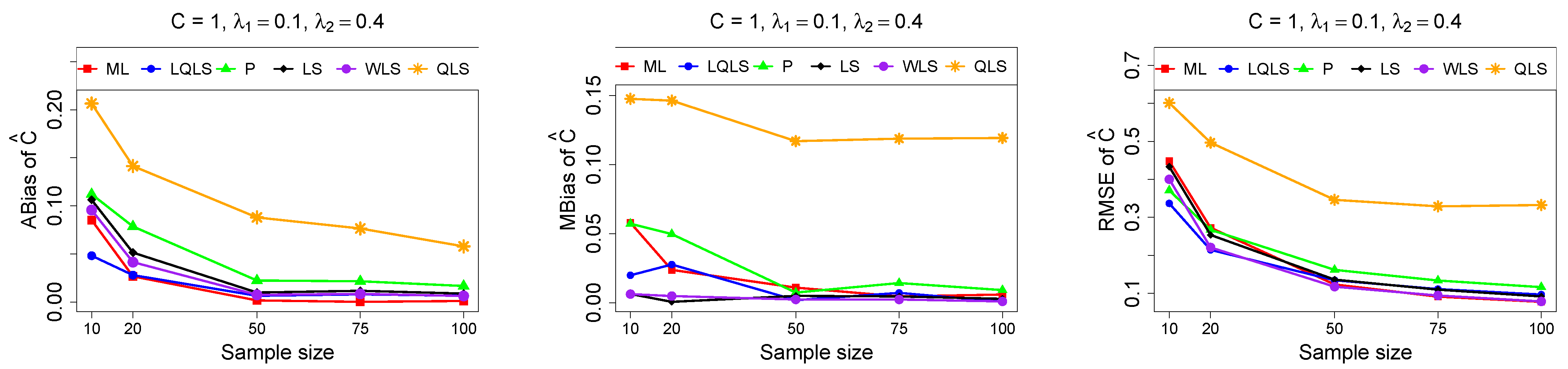

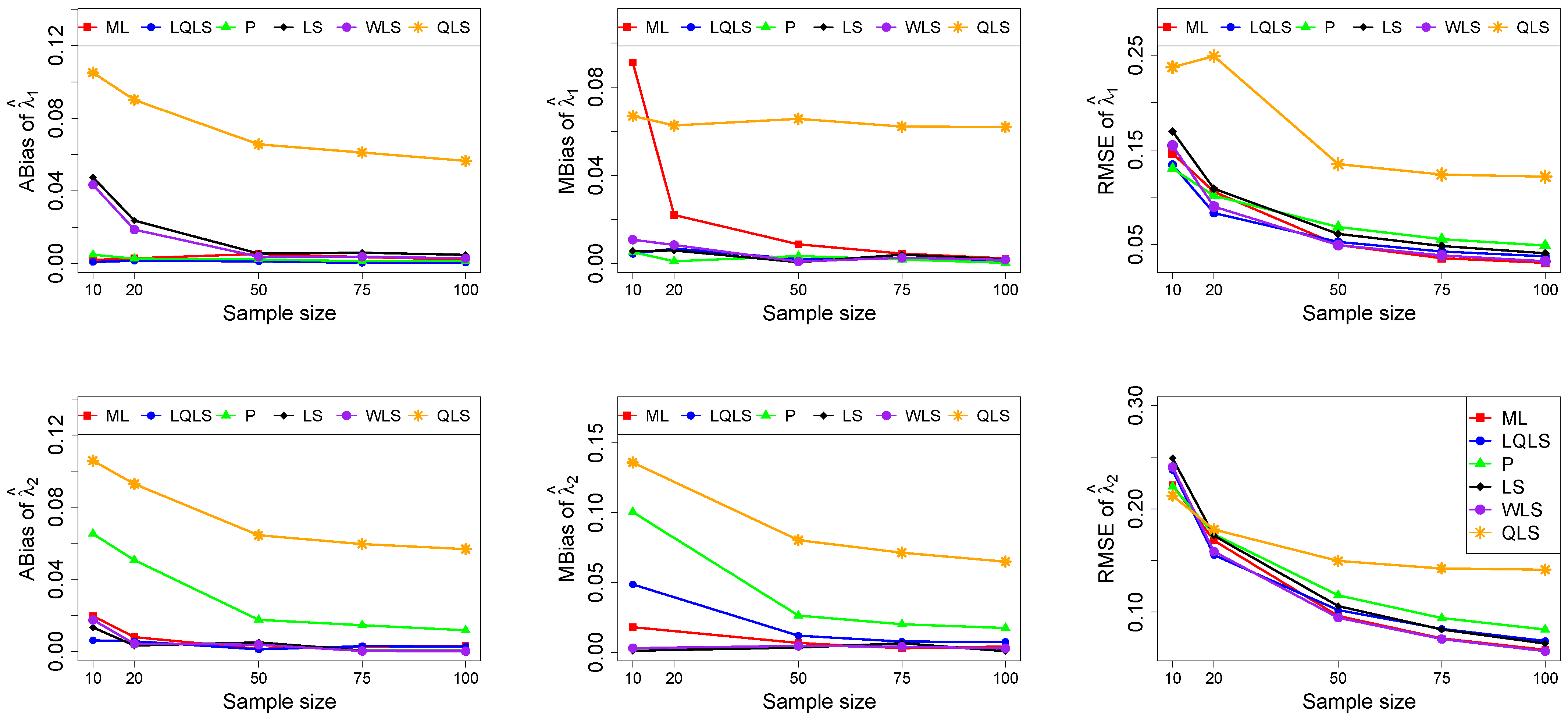

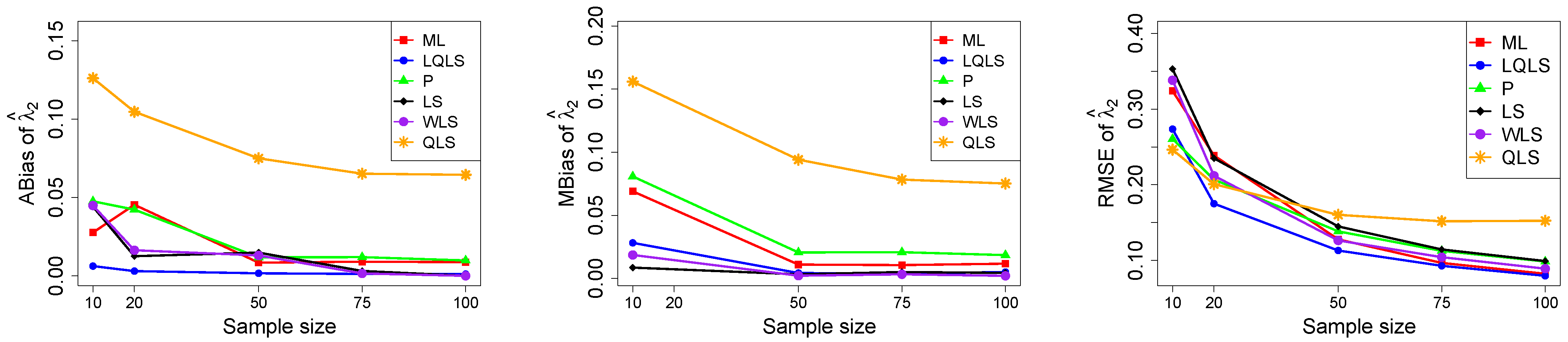

The ABias, MBias, and RMSE are presented in

Figure 3,

Figure 4,

Figure 5,

Figure 6 and

Figure 7, while the related

Table A1,

Table A2,

Table A3,

Table A4 and

Table A5, with the corresponding values, are given in

Appendix A. It is important to note that it was impossible to obtain estimates provided by the QLS method for a few samples. This was due to the non-convergence of the optimization method used to solve Equation (

18). The number of cases where convergence was achieved is indicated beneath each table. This issue is not critical, as the QLS method generally demonstrates the poorest performance. Thus, we do not advise its use.

Moreover, since only small sample sizes were considered, it is difficult to assess the convergence of both median and mean simulated bias to zero, likely attributed to sampling error. However, it is evident that if or , the simulated bias is usually closer to zero than if or . In almost all cases, the RMSE of the estimators of the parameters c, , and decreases toward zero, when the sample size increases.

Based on RMSE values in

Figure 3,

Figure 4,

Figure 5,

Figure 6 and

Figure 7, it is evident that the performance of various estimation methods varies based on the values of

and

, and also the sample size (

n). Regarding the RMSE, we also have the following additional comments:

For small sample sizes, such as , the P method generally demonstrates the highest efficiency. Moreover, it is not a recommended method for larger sample sizes.

The WLS method consistently outperforms the LS estimator in estimating each of the three parameters.

The LQLS method always has a good performance for samples of size . The WLS has a similar performance to the LQLS method if . If , LQLS and WLS methods have a similar performance for .

The ML method shows strong performance when and and when the sample size is equal to or larger than 50. Thus, we do not recommend its use for samples of size smaller than .

Table 1 and

Table 2 provide a comparative analysis of Monte Carlo simulated mean absolute difference and mean maximum absolute difference between true and estimated CDFs. The best values are highlighted in

bold. The insights derived from the analysis of these tables can be summarized as follows:

The performance rankings across different methods are consistent between the two tables.

The WLS methods demonstrate a very good performance, typically yielding the smallest or second smallest values of and .

The LS method consistently performs slightly worse than WLS, and LQLS shows similar performance to WLS when , except when and . The ML method is never the best performer, but it shows good performance if and or .

The remaining methods exhibit poor performance. Both P and WLS methods provide generally the largest absolute differences. The exception is the QLS method, for small sample sizes and .

5. Application

In this section, we use two real datasets to illustrate the behavior of the estimators, described in

Section 3. To compare the fitted power–Pareto model we computed the Kolmogorov–Smirnov (K-S) statistic and associated

p-value for each method. Since parameters are estimated, the

p-value of the K-S test is obtained using Monte Carlo simulation. To measure the goodness-of-fit, we also computed the empirical correlation coefficient

, between empirical quantiles

and the corresponding estimated quantiles

,

(

Beirlant et al. 2004). Since both vectors have monotonically increasing values,

will be non-negative.

5.1. Household Income by State in USA

The U.S. Census Bureau defines “household income” as the gross income of all people aged 15 years or older who live in the same housing unit, regardless of their relationship. Household income reflects the standard of living in distinct households and is an important indicator of the local and national economies.

Table 3 presents a dataset comprising the median household income in 2016 in the United States, in dollars, of

states, as available on the website data.world.

1The histogram and the boxplot of these observations, in

Figure 8, are compatible with the power–Pareto distribution.

Table 4 summarizes the estimated parameters, K-S statistics, associated

p-values, and the empirical correlation coefficient for various statistical methods applied to the household income dataset.

Regarding

Table 4, it is shown that all estimation techniques produce

p-values exceeding

, indicating a favorable fit of the power–Pareto distribution. Considering that a lower K-S statistic and a higher

p-value signify a better fit, and a higher

implies a stronger relationship between observed and expected quantiles, the P method stands out with notably high

p-value and

, indicating a good fit. Moreover, the LQLS method achieves the highest

, further supporting its efficacy. Although the QLS method has a large

value, the

p-value is the lowest.

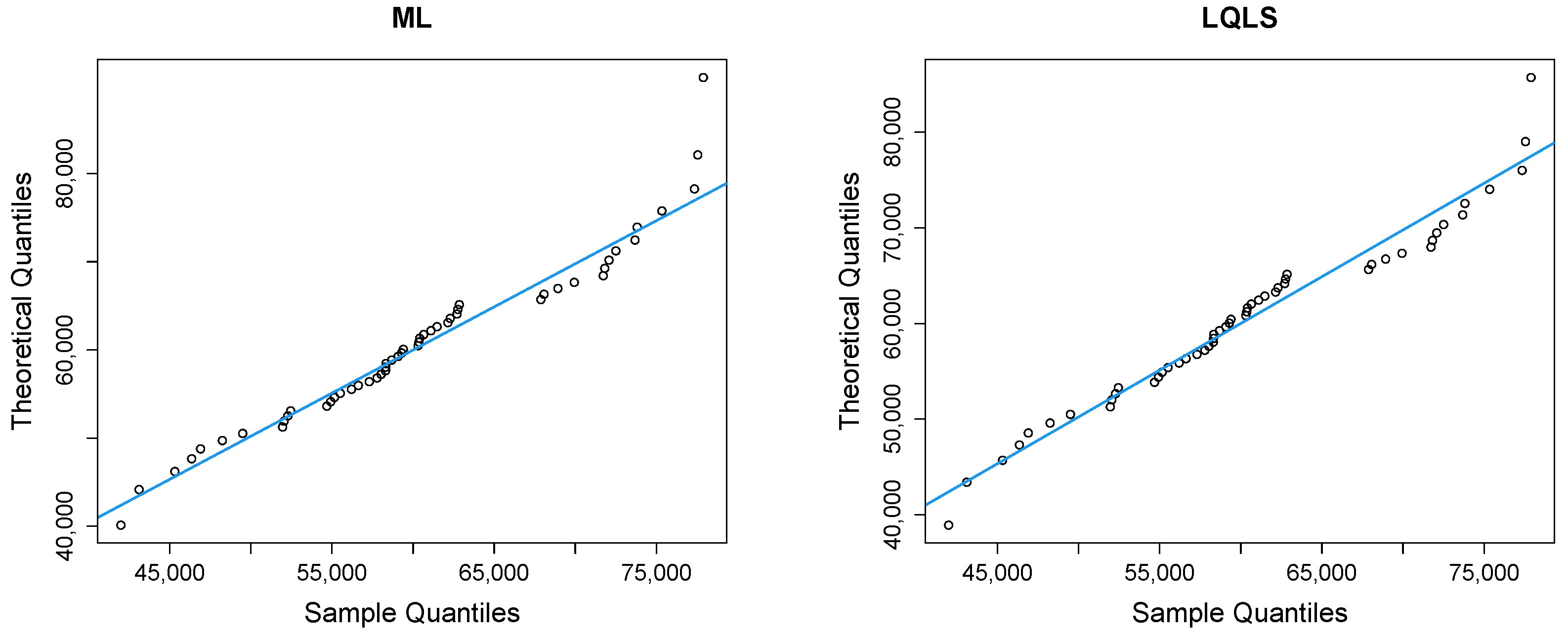

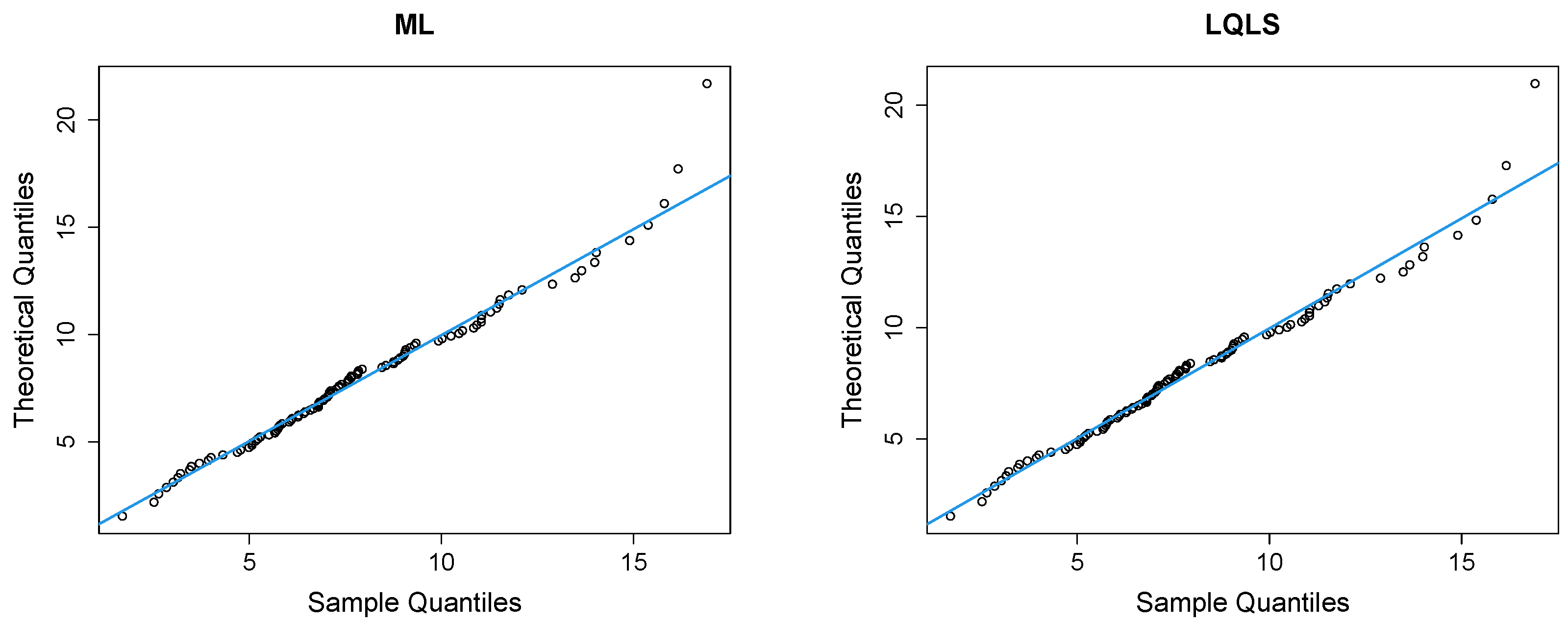

Figure 9 depicts Q-Q plots, comparing the observed data with the estimated quantiles provided from various methods. If the points in the Q-Q plots align closely along the diagonal line, it indicates that the estimated distribution provides an adequate statistical fit.

Figure 10 provides the empirical CDF vs. the fitted CDF, for the six different estimation methods.

Figure 9 shows a good similarity between empirical and fitted quantiles in the body of the distribution, although there are discrepancies in the right tail. All methods provide a good correspondence in the body of the distribution. But the LQLS and QLS methods provide the best correspondence in the right tail. Similar conclusions can be drawn from

Figure 10.

5.2. Peak Concentrations

For the examination of accidental releases of hazardous gases, a method commonly employed is the instantaneous release of a finite volume of gas into a surrounding flow field. Concentration measurements are then taken at a fixed location downwind. In a series of experiments conducted by

Hall (

1991) involving 100 repetitions, a key parameter for risk assessment was the peak concentrations achieved. The dataset, studied by

Hankin and Lee (

2006), is provided in

Table 5.

In

Figure 11, we present the histogram and the boxplot of the dataset. Both plots are compatible with the power–Pareto distribution.

Table 6 provides the estimated parameters, K-S statistics, the associated

p-values, and the empirical correlation coefficient for various statistical methods for the peak concentration dataset.

It is observed that the data conform well to the distribution for all estimation methods, with all associated p-values exceeding and empirical correlation coefficient close to 1. Results for the different estimation methods are similar, except for the QLS, which presents a much higher K-S value. Furthermore, the P, LS, and WLS methods demonstrate favorable outcomes, as indicated by the low K-S statistic, high p-value, and high empirical correlation coefficient, .

Figure 12 presents Q-Q plots, contrasting the observed data with the estimated quantiles derived from the fitted power–Pareto distribution. Both the P and WLS methods demonstrate a good correspondence, with similar patterns and some discrepancies in the right tail. The QLS again evidences overfitting in the right tail.

Figure 13 displays the empirical and fitted CDFs. All methods work quite well for analyzing this dataset. However, the P and WLS are the ones that provide the best correspondence between CDFs.

6. Conclusions

This study examines the power–Pareto model for non-negative variables. The model has three parameters and can exhibit various shapes, making it suitable for modelling both symmetrical and skewed data. The paper explores distributional characteristics, with a particular focus on different parameter estimation techniques, some of them introduced in this work.

The numerical analysis reveals the importance of selecting an appropriate estimation method based on both sample size and the values of the power–Pareto distribution parameters. Our results indicate that for very small sample sizes, the P method performs well in terms of RMSE. However, for larger sample sizes, the LQLS and WLS methods emerge as adequate choices and are recommended for practical applications.

Additionally, it is worth noting that the ML method also exhibits good performance for larger sample sizes, typically with at least 100 observations. However, it is essential to consider the computational time associated with this method, which is longer when compared to other methods, a factor to weigh in the decision-making process.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}