Abstract

In the study we explore an oligopoly market for equilibrium and stability based on statistical data with the help of response functions rather than payoff maximization. To achieve this, we extend the concept of coupled fixed points to triple fixed points. We propose a new model that leads to generalized triple fixed points. We present a possible application of the generalized tripled fixed point model to the study of market equilibrium in an oligopolistic market dominated by three major competitors. The task of maximizing the payout functions of the three players is modified by the concept of generalized tripled fixed points of response functions. The presented model for generalized tripled fixed points of response functions is equivalent to Cournot payoff maximization, provided that the market price function and the three players’ cost functions are differentiable. Furthermore, we demonstrate that the contractive condition corresponds to the second-order constraints in payoff maximization. Moreover, the model under consideration is stable in the sense that it ensures the stability of the consecutive production process, as opposed to the payoff maximization model with which the market equilibrium may not be stable. A possible gap in the applications of the classical technique for maximization of the payoff functions is that the price function in the market may not be known, and any approximation of it may lead to the solution of a task different from the one generated by the market. We use empirical data from Bulgaria’s beer market to illustrate the created model. The statistical data gives fair information on how the players react without knowing the price function, their cost function, or their aims towards a specific market. We present two models based on the real data and their approximations, respectively. The two models, although different, show similar behavior in terms of time and the stability of the market equilibrium. Thus, the notion of response functions and tripled fixed points seems to present a justified way of modeling market processes in oligopoly markets when searching whether the market has reached equilibrium and if this equilibrium is unique and stable in time

Keywords:

fixed point; tripled fixed point; market equilibrium; response functions; oligopoly market MSC:

46B07; 46B20; 46B25; 55M20; 65D15

JEL Classification:

C02; D43; C62

1. Introduction

Modern markets are characterized by the consolidation of producers, which naturally leads to the replacement of the free market with a noncompetitive one. Since Cournot announced the theory of oligopolistic markets Cournot (1897) more than a century ago, there has been a growing interest in studying the dynamics in these markets. The classical payoff maximization technique has its drawbacks due to the possible irrational behavior of the participants. This behavior can be due both to their technological limitations or the presence of long-term contracts that do not allow them to make quick changes in the quantities of goods, as well as to the lack of reliable information about the demand function and, from there, the function of the price. Incorrect information about the price function can lead to the solution to the payoff maximization problem being different from the one generated by the market. Another disadvantage is the assumption of differentiability for the payoff functions, which in most cases can be even discontinuous ones. An approach proposed in (Dzhabarova et al. 2020; Kabaivanov et al. 2022) avoids these drawbacks by reducing the task of finding market equilibrium to the task of finding fixed points for maps that are the natural response functions of producers participating in the market under consideration. The results in (Dzhabarova et al. 2020; Dzhabarova and Zlatanov 2022; Kabaivanov et al. 2022) are theoretical. The first application of these results to the study of equilibrium, its uniqueness, and stability is proposed in Badev et al. (2024). We will try to demonstrate that this approach can be applied to other markets as well.

The Banach fixed point theorem Banach (1922), although a century old, has an enormous number of generalizations and applications. The generalizations may be classified in several directions: changing the contractive type condition, the underlying space, the fixed point notion, or all of them simultaneously. We will concentrate on only two of them, related to our investigation. The first is to change the contractive condition. Contractive assumptions on the self-map have been considered in Reich (1971), which cover several generalizations. The presented condition in Reich (1971) has been later simplified in Hardy and Rogers (1973) by exploiting the symmetry of the metric function. Another direction in the generalizations is the alteration of the fixed point notion. Coupled fixed points, introduced in Guo and Lakshmikantham (1987), are relevant from this perspective. Unfortunately, the system of equations and that define the coupled fixed points (Bhaskar and Lakshmikantham 2006; Guo and Lakshmikantham 1987) usually leads to an ordered pair such that . This drawback has been overcome in Zlatanov (2021), where a generalized coupled fixed point for an ordered pair of maps has been introduced. Following Guo and Lakshmikantham (1987), it has been proposed to search for an ordered triple satisfying , , and , Borcut and Berinde (2011). This idea has been further developed in Samet and Vetro (2010) by suggesting the notion of N-tuple being a fixed point of N-order for the map . This idea has been exploited in Dzhabarova and Zlatanov (2022). Combining all mentioned above, we will attempt to generalize the notion of a tripled fixed point to generalized tripled points for ordered triples of maps , satisfying the contractive condition of the Hardy-Rogers type Hardy and Rogers (1973).

We will apply the obtained results to the study of market equilibrium in noncompetitive markets where three manufacturers hold a dominant position.

An investigation of oligopoly markets, i.e., markets dominated by a few big producers that control the price and supply quantity of the goods being traded is presented in Cournot (1897). While the research in Cournot (1897) employed a highly simplified model, it has served as a fundamental framework for numerous investigations over a century.

The classical oligopoly model assumes that the firms sequentially respond to each other’s output in a rational way, i.e., pursuing to maximize their payoff function. The maximization problem leads to the solution of the first-order equations, which define the response function for each of the producers. The concept of deviating from rational player behavior has been explored in prior studies, such as (Rubinstein 1998; Ueda 2019). In another enhancement of the approach by Cellini and Lambertini (2004), each company endeavors to anticipate the production changes of other players at time t, while still relying on data up to period t.

Let us recall the Cournot model, with three companies producing perfectly substitute goods and competing for the same consumers. Let the overall production in the market be , where , is the quantity produced by the ith player. The market price is defined as , which corresponds to the demand function’s inverse. It is assumed that the price function is constant throughout time and that the producers have no control over it. Each firm has a cost function , . Assuming that all players are acting rationally, i.e., they are interested only in maximizing their profit, the payoff functions of the three players are represented by

respectively. Let us put , just to simplify some of the notations. Each company, if with a rational behavior, wants to maximize its profit, which is

We obtain the system of equations

assuming that functions P and , , are differentiable.

There are various approaches to pursuing a solution to (2). The direct approach of obtaining , and , called response functions Friedman (1983), may encounter significant technical limitations. For example, it may be difficult or impossible to obtain an exact solution to (2). Even if approximate solutions are found, if the model is not stable, this approximation is far from the equilibrium of the market. The solutions of (2) are only necessary conditions for a triple to be an equilibrium point that maximizes the payoff functions . A sufficient condition for a solution of (2) to also be a solution of (1) involves satisfying either that the payoff functions are concave or ensuring the second order conditions, i.e., for (Bischi et al. 2010; Okuguchi and Szidarovszky 1999). Finally, if the payoff functions are not differentiable or even continuous, different optimization techniques should be applied.

An alternative approach is pioneered in Dzhabarova et al. (2020) by finding an implicit formula for the response functions.

The general framework proposed in Dzhabarova et al. (2020) is as follows: for each ordered pair of sold production , where is the quantity sold by the ith, the ith producer chooses a new level of production , depending on their technological options and their policy on the market. Thus, in the next time interval, the ith player will produce . We are searching for a triple of productions that will not lead to a change in the productions of any of the players, i.e., .

Importantly, using the response function enables the transformation of the maximization problem from (1) into a tripled fixed point one, thus all assumptions of concavity, differentiability, or even continuity can be bypassed (Dzhabarova et al. 2020; Kabaivanov et al. 2022). Specifically, Kabaivanov et al. (2022) show that in the settings of Andaluz et al. (2020) their criteria for guaranteeing the uniqueness and existence of the market equilibrium can be expanded outside the settings of payoff function maximization.

One can find a comprehensive analysis of oligopolistic markets in (Bischi et al. 2010; Matsumoto and Szidarovszky 2018; Okuguchi 1976). Specifically in duopoly markets (Baik and Lee 2020; Liu and Sun 2020; Wang et al. 2020), some recent results on oligopoly markets are found (Alavifard et al. 2020; Geraskin 2020; Siegert and Ulbricht 2020; Strandholm 2020; Xiao and Wang 2020). Response function-based equilibrium analysis in duopoly markets was first presented in Dzhabarova et al. (2020) and has recently been further explored in Kabaivanov et al. (2022).

2. Materials and Methods

2.1. Fixed Points

Let A be a nonempty set. A point is said to be a fixed point for a map , if .

The Banach fixed point theorem Banach (1922), although being a century old, has many applications and generalizations. One such generalization is altering the contractive condition. We will introduce a version from Reich (1971), which will be necessary for our subsequent discussion.

Definition 1

(Reich (1971)). Let be a metric space and the map is called Hardy–Rogers, provided that the inequality

holds for all and for some constants , , verifying .

As pointed out in Hardy and Rogers (1973), the symmetry of the metric function implies that if (3) holds then the following inequality will also hold:

Thus, we may take into consideration maps that meet the inequality

so that , without sacrificing generality.

When a Banach contraction, if a Kannan contraction Kannan (1968), and if a Chatterjea contraction Chatterjea (1972) are obtained.

We shall assume in the remainder of our study that (4) is satisfied by a Hardy–Rogers map.

Theorem 1

(Hardy and Rogers (1973)). Let be a complete metric space and be a Hardy–Rogers map, then:

- 1.

- a unique fixed point of T exists and, moreover, for any first estimate , the iterated sequence for converges to the fixed point ξ

- 2.

- there comes a priori error estimate

- 3.

- there comes a posteriori error estimate

- 4.

- the rate of convergence is ,

where and are the constants from (4).

2.2. Coupled Fixed Points

A different approach in the generalization of fixed points has been proposed in Guo and Lakshmikantham (1987).

Definition 2

((Bhaskar and Lakshmikantham 2006; Guo and Lakshmikantham 1987)). Let be a set in a metric space , . An ordered pair is named a coupled fixed point of F in A, provided that and .

The initial results regarding the existence and uniqueness of coupled fixed points were obtained in Bhaskar and Lakshmikantham (2006), assuming that the underlying space is a Banach space, partially ordered by a cone. Later, more easily applicable results concerning coupled fixed points in a partially ordered complete metric space were derived in Guo and Lakshmikantham (1987), which is a starting point for a great number of investigations.

Petruşel (2018) provides an in-depth analysis of the relationship between fixed points and coupled fixed points. It is demonstrated there that instead of the map , one may examine the map , defined by . The ordered pair is a coupled fixed point for F if and only if it is a fixed point for T.

The notion to explore fixed points for existence and uniqueness in cyclic maps, i.e., and , rather than self-maps was first proposed in Kirk et al. (2003). This concept was expanded to include two-variable maps as well in Sintunavarat and Kumam (2012).

Definition 3

(Sintunavarat and Kumam (2012)). Let be sets in a metric space , the ordered pair of maps is called a cyclic one, provided that and .

Definition 4

(Sintunavarat and Kumam (2012)). Let be sets in a metric space and be a cyclic ordered pair of maps. An ordered pair is named a coupled fixed point of F in A, provided that and .

Definition 5

(Sintunavarat and Kumam (2012), Definition 3.4 and Theorem 4.1). Let be sets in a metric space and the ordered pair of maps be a cyclic one. We say that be a cyclic contraction if there is a constant so that the inequality

holds for any and .

Theorem 2

(Sintunavarat and Kumam (2012), Theorem 4.1). Let be closed sets in a complete metric space . The ordered pair has a unique common coupled fixed point , i.e., and , provided that be a cyclic contraction.

Moreover, Zlatanov (2021) proved that .

Zlatanov (2021) proposed considering two maps , and define an ordered pair as a coupled fixed point for if and . If we get the definition from (Bhaskar and Lakshmikantham 2006; Guo and Lakshmikantham 1987).

In order to apply the coupled fixed points approach to the study of market equilibrium, an extension of the previously discussed concepts was given Dzhabarova et al. (2020). Each participant in a duopoly market will inevitably respond differently depending on how their competition performs and how well they do on the market. Therefore, two response functions for were taken into consideration in Dzhabarova et al. (2020), assuming , , wherein is the player ’s production set, and and define the coupled fixed points. Thus we reach maps that are not self-maps and are not cyclic ones from Definition 3. The authors have termed these new types of maps cyclic once again in Dzhabarova et al. (2020). A more natural name a semi-cyclic map is introduced in Ajeti et al. (2022).

We obtain the concept of coupled fixed points from Definition 2 anytime and .

Definition 6

((Ajeti et al. 2022; Dzhabarova et al. 2020)). Let be sets in a metric space and , . An ordered pair is said to be an semi-cyclic ordered pair of maps.

Definition 7

((Ajeti et al. 2022; Dzhabarova et al. 2020)). Let be nonempty sets in a metric space and be an ordered pair of semi-cyclic maps. An ordered pair is said to be a coupled fixed point of , provided that and .

We obtain the concept of coupled fixed points from Definition 2 anytime and .

The existence and uniqueness of an equilibrium in duopoly markets are confirmed by a series of studies about coupled fixed points for semi-cyclic maps (Ajeti et al. 2022; Dzhabarova et al. 2020; Kabaivanov et al. 2022).

2.3. Tripled and n-Tupled Fixed Points

The attempt to generalize the coupled fixed point notion for ordered triples seems to lack uniqueness as different ideas have been proposed. Let . Following (Amini-Harandi 2013; Samet and Vetro 2010) a triple is said to be a tripled fixed point, provided that , and . Following Borcut and Berinde (2011) a triple is said to be a tripled fixed point, provided that , and .

An idea to consider n-tupled fixed points is presented in Samet and Vetro (2010).

It is proposed in Zlatanov (2021) to consider three maps and to define a tripled fixed point by the equalities for . This approach gives the possibility to consider models where the tripled fixed points do not need to satisfy . By a particular choice of the functions , Zlatanov (2021, ) it is possible to get the investigated maps in (Amini-Harandi 2013; Borcut and Berinde 2011; Samet and Vetro 2010).

2.4. Testing the Stationarity of Time Series Data

Investigating the stationarity of time series is an important factor for our study. A stationary time series is a series whose statistical measures, such as mean, variance, covariance, and standard deviation, are not a function of time. In other words, stationarity in a time series means a time series without trends or seasonal components. The two most popular statistical tests to ascertain whether or not a time series is stationary are the Phillips-Perron (PP) and augmented Dickey-Fuller (ADF) test Dickey and Fuller (1979). The Dickey-Fuller test evaluates the hypothesis of a unit root in the model , or, equivalently, the hypothesis of in

where denotes the value of a data point at period t, , - a pure random disturbance in t. Tests involving lagged changes are called augmented Dickey-Fuller tests and are also used for hypothesis testing . The null hypothesis means that the time series is non-stationary and indicates the presence of a trend; the alternative hypothesis means stationarity. Put otherwise, the small p-value indicates that it is improbable that a unit root exists.

2.5. The Least Squares Method

The Least Squares Method (LSM) is one of the most widely used methods in statistics and holds a special place in the development of science. Adrien-Marie Legendre Bretscher (1997) initially published the LSM, which was established by Carl Friedrich Gauss in 1795. The method is usually associated with linear (univariate and multivariate) statistical models where its efficacy is most evident. Determining the dependency of a single indicator y, the dependent variable, on a set of other —independent variables is the fundamental task, i.e., a model of the form

where denotes the summed effect of the factors, which are not reported in the explicit form . The residual component in the model (6) is required to be a relatively small random variable.

Depending on the type of function f, regression models can be linear or nonlinear. In much of the study of multivariate dependencies, the form of f is assumed to be linear. This can be justified in part by the fact that the Taylor expansion of a function f can separate the linear term and assign all subsequent terms, quadratic, cubic, etc., to the residual component . Assuming a linear form of dependence, model (6) can be written as:

where the coefficients are the ones we are searching for.

For n joint observations of the dependent and independent variable , (7) is presented in the following matrix form:

or in an equivalent form

is the variable observation vector of , X is the known matrix of with the first column consisting of ones, is the unknown parameter vector of , and of is the error vector. Finding the parameters so that the sum of the squares of the errors is as little as possible is the basic goal of the least squares approach, i.e.,

To apply the LSM in regression analysis, the dependent variable must be normally distributed. We verify the latter with Shaphiro and Wilk (1965) and Kolmogorov-Smirnov tests.

2.6. Statistical Measures for Model Estimation

We employ two basic statistical metrics to assess the effectiveness of the built models: the mean absolute percentage error (MAPE) and the coefficient of determination , which can be computed using the following equations

where the sample size is n, the predicted values are , the mean is , and the values of the dependent variable are . Our objective is to develop a model with the lowest MAPE and the maximum potential value of .

We aim try to generalize the proposed concepts of tripled fixed points so that the obtained results can be applied to the study of market equilibrium based on response functions for markets dominated by three producers. Using the statistical techniques discussed, we will construct response function models that are based on real data and examine these real markets for the presence of equilibrium and stability.

3. Main Result

The concepts from Dzhabarova et al. (2020) will be expanded upon by taking into account three distinct metric spaces , where .

Definition 8.

Let , and be nonempty sets. We will call the ordered triple of maps , for a semi-cyclic map.

Let us emphasize that even if we confine ourselves to a single set X, it is not possible to assume that , where in the application section. Here, we will investigate market equilibrium in oligopoly market, where the percentage shares of the three biggest players are , and and the response functions satisfy for .

Definition 9.

Let , and be nonempty sets and the ordered triple , for be a semi-cyclic map. An ordered pair is called a tripled fixed point of if , and .

Definition 10.

Let , and be nonempty sets and the ordered triple , for be a semi-cyclic map. We construct the sequences , , and for any triple by , , and , , for all .

We will assume that the sequences , , and are those specified in Definition 10 everywhere.

Theorem 3.

Let , , and be three complete metric spaces and the ordered triple , for be a semi-cyclic map. To fit some of the formulas within the text box, let us assign . Let there be constants for , such that and the ordered triple of maps satisfy the inequality:

for any . Then:

- 1.

- a unique tripled fixed point of exists and, moreover, for any first estimate the iterated sequences , , converge to the triple fixed point .

- 2.

- there comes a priori error estimate

- 3.

- there comes a posteriori error estimate

- 4.

- the rate of convergence is

where .

If , wherein be a complete metric space and , then the tripled fixed point verifies .

If , wherein be a complete metric space, and , then the tripled fixed point verifies .

Proof.

Consider the product space , supplied with the following metric:

The assumption that be complete metric spaces implies that be a complete metric space, too.

Following a smart idea from Petruşel (2018), let us define a map by . Then inequality (12) is equivalent to:

and consequently is a Hardy–Rogers map in the complete metric space . As a result, we can use Theorem 1, and we will conclude that there exists a unique , such that , i.e., , and . The error estimates were derived right away from the definition of the metric and Theorem 1.

If , , , with , subsequently for the fixed point of G, employing (12) for , , and we establish:

which is a contradiction and therefore , i.e., .

If , , and , subsequently for the fixed point of G, using (12) for , , and , we obtain

which is a contradiction and therefore , i.e., . □

3.1. Extension of Already Known Results on Tripled Fixed Points and Corollaries

Let us recall the main result from Dzhabarova and Zlatanov (2022).

Theorem 4.

Let be nonempty, closed sets in the complete metric space . Let the ordered triple of maps for be a semi-cyclic one. Let there be , such that and let the ordered triple satisfy the inequality

for every . Then there exists a unique tripled fixed point of . Moreover, for any first estimate the iterated sequences , , converge to the tripled fixed point .

Let us consider Theorem 3 for , , as closed and nonempty sets in a complete metric space , rather than being subsets of three distinct metric spaces and for constants . If we put , for in (14), we get:

where . Thus, Theorem 4 follows from Theorem 3.

A weaker contractive condition for the ordered triple of semi-cyclic maps than that in Theorem 4 can be obtained if we treat , , and as closed and nonempty sets in a complete metric space , as opposed to subsets of three distinct metric spaces and constants .

3.2. Application in the Study of Market Equilibrium in Tripodal Markets

The main task in most economic studies is to determine the factors affecting competitiveness, economic success, predicting consumer behavior, forecasting demand and sales. For this purpose, high-performance statistical models are built using classical or machine learning methods. Classical methods include panel regression, multiple linear regression, principal component analysis, Box-Jenkins ARIMA methodology (Török et al. 2020; Van Trang et al. 2022). The authors Jantyik et al. (2020) used most effective with high predictive power machine learning methods like as convolutional neural networks, long short-term memory network and ensemble methods. The present study is not concerned with building a high-performance statistical model of real data for prediction purposes. We are seeking a reasonably adequate statistical model that meets the conditions of Theorem…to examine the equilibrium point.

3.2.1. The Basic Model

Assume three enterprises compete for the same customers Friedman (1983) and aim to meet request with a total production of . The market price, , is the inverse of the demand function. The cost functions of the three players are for , respectively. The payoff functions are for . Assuming that every participant is rational, their purpose is to maximize profits, i.e.,

We get the equations:

provided the functions P and , are differentiable.

The solution of (16) represents the equilibrium triple of production Friedman (1983). Equation (16) frequently contains solutions in the form of , , and , known as response functions. Friedman (1983).

It may be challenging or even impossible to solve (16), hence it is commonly advised to look for an approximate solution. One big downside is that it may be unstable. Luckily, an implicit formula for the response function can be obtained through (16), i.e., .

We could eventually end up with response functions that do not maximize the payout . It is usually considered that every participant’s reaction is determined by both their own and others’ outputs. For instance, if the resulting quantities are at time n, and the first player adjusts their output to levels , the second and third players will also alter their outputs to amounts and , respectively. If there are , and , satisfying , and , we get an equilibrium. To guarantee that the solutions of (16) maximize the payoff functions, either is concave or (17) is satisfied. Matsumoto and Szidarovszky (2018):

The inequalities (17) are referred to in the literature as second-order conditions.

The inclusion of response functions changes the maximizing problem into a tripled fixed point problem, removing all concavity and differentiability requirements. The problem of finding triple fixed points for an ordered pair of mappings is the challenge of solving the equations , , and Samet and Vetro (2010, ). One important restriction, though, might be that participants aren’t allowed to alter output too quickly, which could prevent them from making the most money possible.

3.2.2. Relationship between the Contraction-Type Conditions and the Second-Order Ones

For an instance where and , , and are subsets of a metric space , we shall rephrase Theorem 3 in the language of economics. We employ Corollary 1 to demonstrate that, in the event that the response functions are differentiable, they fulfill the second-order criterion. Furthermore, Corollary 1 ensures the iterated process’s stability.

Corollary 1.

Let us consider an oligopoly market with three players, satisfying:

- 1.

- the three players are producing perfect substitutes of homogeneous

- 2.

- the first player can produce quantities from the set , and the second and the third ones can produce quantities from the sets and , respectively, where , and are closed, nonempty subsets of a complete metric space

- 3.

- let the ordered tripled , , be a semi-cyclic map that presents the response functions for players one, two, and three, respectively

- 4.

- let there be , so that the inequality:holds for all .

Then there is a unique market equilibrium triple in , i.e., , and .

Additionally, if and are fulfilled, then is satisfied by the market equilibrium triple .

In the event that is also true, is satisfied by the market equilibrium triple .

Example 1.

Following Kabaivanov et al. (2022), the response functions are defined as:

Corollary 1 not only provides sufficient requirements for the presence of a market equilibrium, but it also provides sufficient conditions for the process of the players’ successive reactions to be stable in the event that their behavior remains unchanged.

Example 2.

A model with the price function will be examined and, for , the cost functions .

By (16) we get:

The equilibrium points are the solution of the system of Equation (21) because it satisfies the second-order conditions, which are , , and . Sadly, condition (18) will not be satisfied by the response functions in the model, which are , , and .

Let us consider three starting states in the market from Example 2. The iterations of the successive changes of the output of the three players is presented in Table 1 and Table 2.

Table 1.

The iterated sequence’s values with initial conditions of .

Table 2.

The iterated sequence’s values with initial conditions of .

In the event that the starting point differs, Table 2 results.

Note that the system (16) may have several solutions that meet the second-order criteria (17). In this scenario, further inquiry will be required to determine which is the answer to the Cournot model’s optimization problem. Even though (18) imposes a stronger limitation than (17), the model from Corollary 1 differs from the well-known Cournot optimization problem.

The obtained results convince us that the study of market equilibrium using response functions is a generalization of Cournot’s theory for obtaining equilibrium using payoff maximization. As we have shown, if the response functions are obtained from the first-order conditions, then the tripled fixed points will necessarily be solutions to the optimization problem, and even more, we will have market stability. On the other hand, it is possible to have a market with irrational behavior among the participants, but if it is possible to find their response functions, then it is possible to give an answer: what are the market equilibrium levels, are they unique, and are they stable over time?

4. Empirical Data

In our analysis, we have monthly data on beer sales (1000 HLTRs) by five significant corporations that cover the whole Bulgarian beer industry. The percentage share of each company in the market distribution is calculated. To determine the market equilibrium, we consider the three companies with the largest percentage share of sales.

Monthly data on the percentage participation of each company (Company 1, Company 2, Company 3) contains a total of data from January 2017 until December 2020. Over the period, the three companies covered an average of .

Table 3 presents the descriptive statistics on the values of the volume of beer sold for each of the three company brands. The close values of the mean and the median, as well as the values close to zero of the skewness and kurtosis for the three variables, indicate that we may assume the data is normally distributed. This is confirmed by the Kolmogorov-Smirnov and Shapiro-Wilk tests, which are insignificant with p-value for the variables under consideration. Also, Table 3 shows the first firm has the largest average proportion of sales.

Table 3.

Descriptive statistics of the initial variables used.

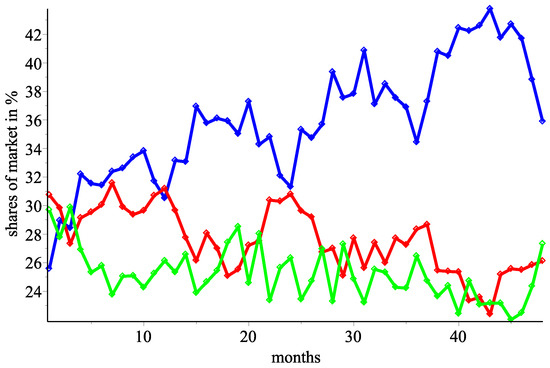

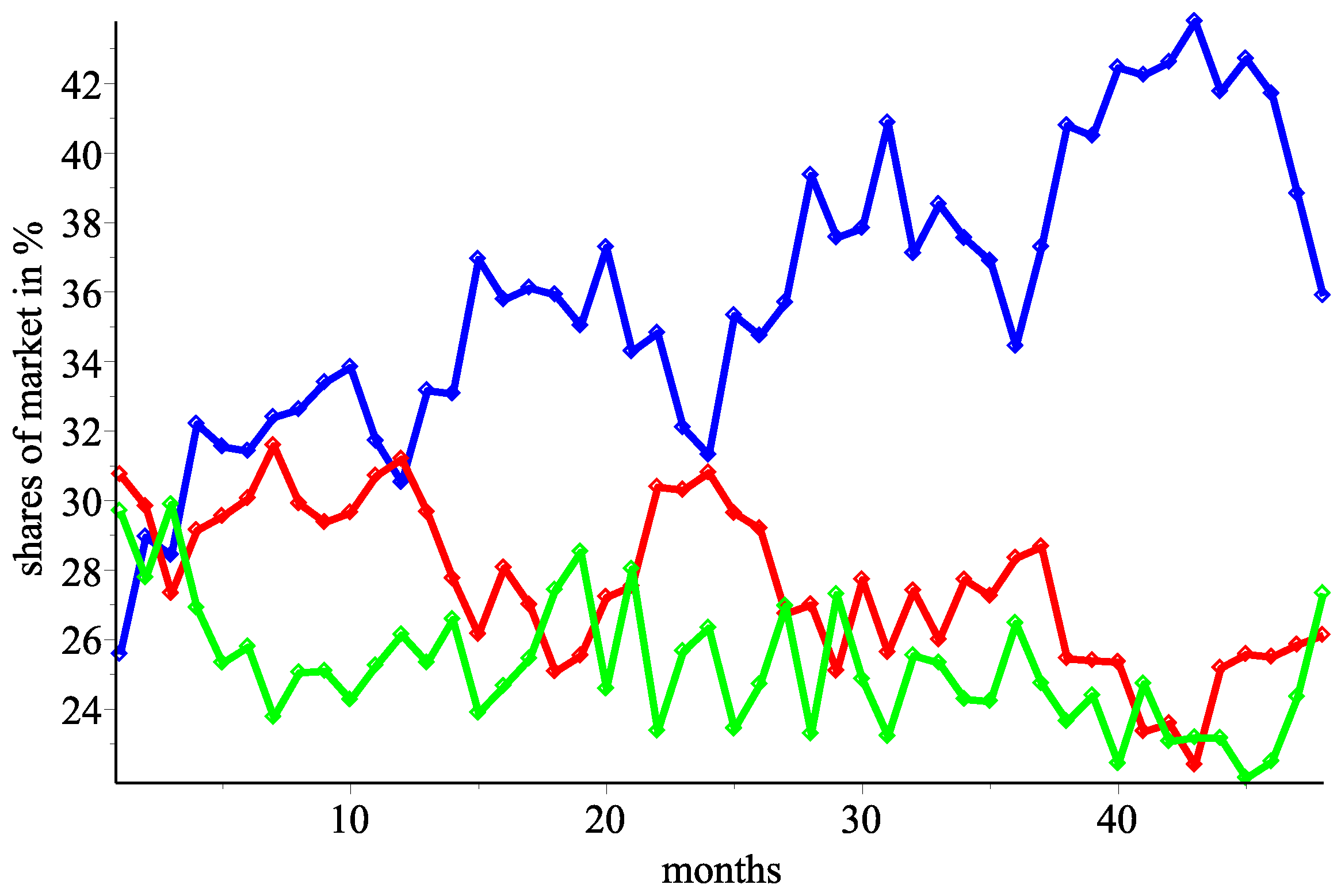

Figure 1 shows a sequence plot of the three companies’ percentage participation. The leading company’s trend is increasing, while the other two are somewhat decreasing.

Figure 1.

Percentage shares in the market over time for Company 1 in blue, Company 2 in red, and Company 3 in green color.

4.1. Results of the Unit Root Test for the Original and Differenced Time Series

The outcomes of the unit root tests for the original time series are shown in Table 4. Since all p-values for the initial variables are negligible, as Table 4 demonstrates, is the outcome of the unit root tests and the null hypothesis cannot be rejected. As a result, every initial time series exhibits a first-order trend and is non-stationary.

Table 4.

Result from the unit root tests of the initial time series.

For the differenced series DCompany1, DCompany2, and DCompany3, calculated by

and Table 5 provides the corresponding indices of the unit root tests. Since all of the p-values in this table are essentially zero, the unit root problem is resolved. Consequently, it is possible to reject the null hypothesis in this situation, and it is presumed that these variables are stationary.

Table 5.

Outcomes of the unit root test of the diffenreced time series.

The unit root tests corroborate the first-order trends in all variables. This effectively indicates that the time series values for each month can be expressed in terms of the preceding month’s data.

4.2. Modeling the Response Functions of the Three Producers

We have genuine statistics on the quantity sold for 48 consecutive months. As long as beer consumption varies by season, it is not suitable to include the quantities in the model. As a result, we converted the quantities into percentages. Figure 1 demonstrates substantial swings over 48 months. This is the basis for considering two models. The first will be based on true empirical data, while the second will be based on weighted moving average-smoothed data. We will suppose in the second instance that the huge oscillations in the real data (Figure 1) could be related to the fact that the producers do not sell their product.

Distributors may order a large quantity of items while their warehouses are empty, and a small quantity of goods when their warehouses are full. For the procedure to average over time, the percentage shares appear to be a better representation of producer-consumer interaction, as we will see later.

All of the reasons we mentioned for using moving averages are merely assumptions; therefore, we will present the two models, because working with real data is always the preferred option.

In the genuine data green the three players follow a normal distribution. An issue was that none of the algebra computer software could solve the least squares problem for arbitrary constants. Thus, we made some assumptions regarding three of the coefficients that represent each producer’s conduct in relation to their own results from the previous month. These coefficients were chosen to be similar to the correlation coefficients that we calculated for real data. As a result of these assumptions, we searched for the coefficient values that represent each producer’s conduct in relation to their competitors’ performance.

We choose to convert the real data using weighted moving averages. Although this strategy is mostly employed in financial markets Lorenzo (2013) to discover the exact time of trend change, it appears that this approach can be applied in the inquiry we are conducting. Using the classical average yields new data that is not normally distributed to the two smaller market players. When we employ a moving average using the first 5 Fibonacci numbers, the converted data follows a normal distribution for all producers. It is interesting to point out that in this example the algebra computer software was able to perform the least squares assignment with no additional assumptions.

4.3. Application of Lsm under Additional Conditions for Building Interactive Models

The presence of a first-order trend indicates that we can reasonably look for a dependence that describes the current state of each producer relative to the state one month ago. For this reason, we form three new lagged variables with one lag back, namely , , and , based on the main variables. For the three lagged variables, the Shapiro-Wilk and Kolmogorov-Smirnov tests are negligible for (p-values ). Therefore, the variables have a normal distribution. This allows us (Table 6) to determine the Pearson’s correlation coefficients. The table demonstrates that all correlation coefficients of the variables , , and and their lagged variables are statistically significant at a significance level .

Table 6.

Pearson Correlation Coefficients. We denote by Ci Company i.

Let , , and , , be the data for the three companies: Company 1, Company 2, and Company 3. Following Dzhabarova et al. (2020) we are looking for a model of the form (23)

, , subject to conditions

From Table 6 we can estimate , and .

The coefficients , are found by minimizing the sum of the squares of the differences

subject to the constraints (24) and the additional restriction on , , and .

The optimization problem has the following solution:

where .

Therefore, we get the ordered tripled defined by

that represent the response functions of each of the three players in the market and

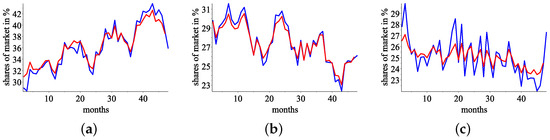

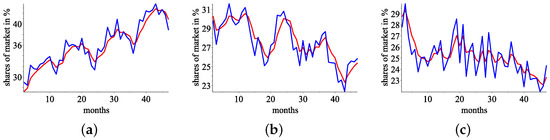

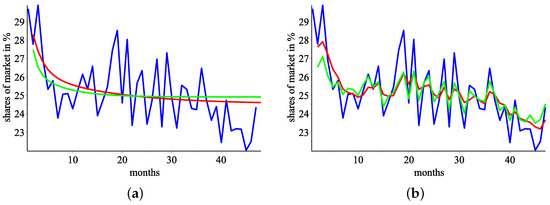

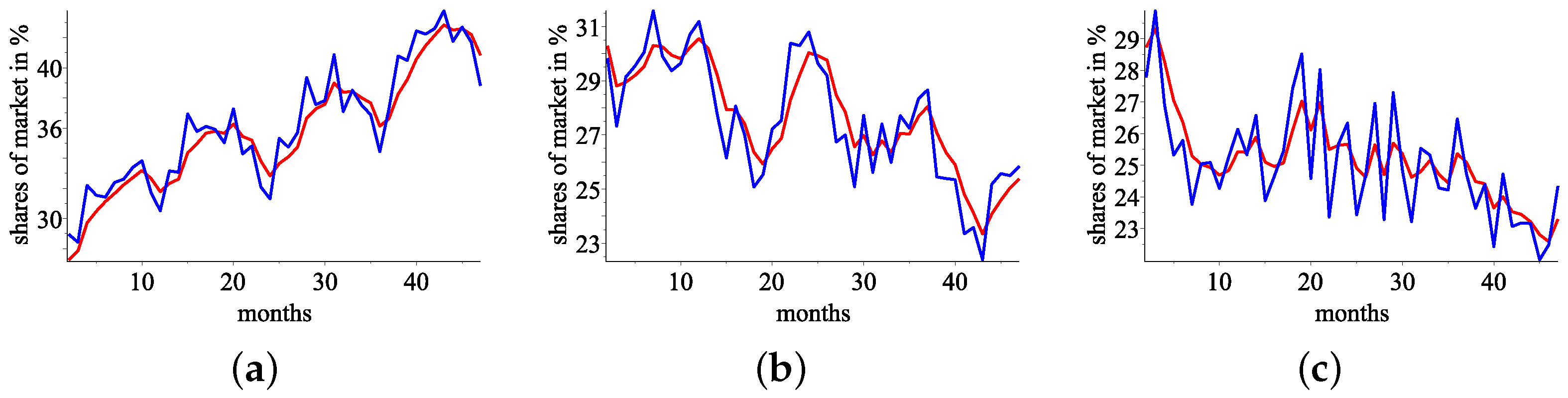

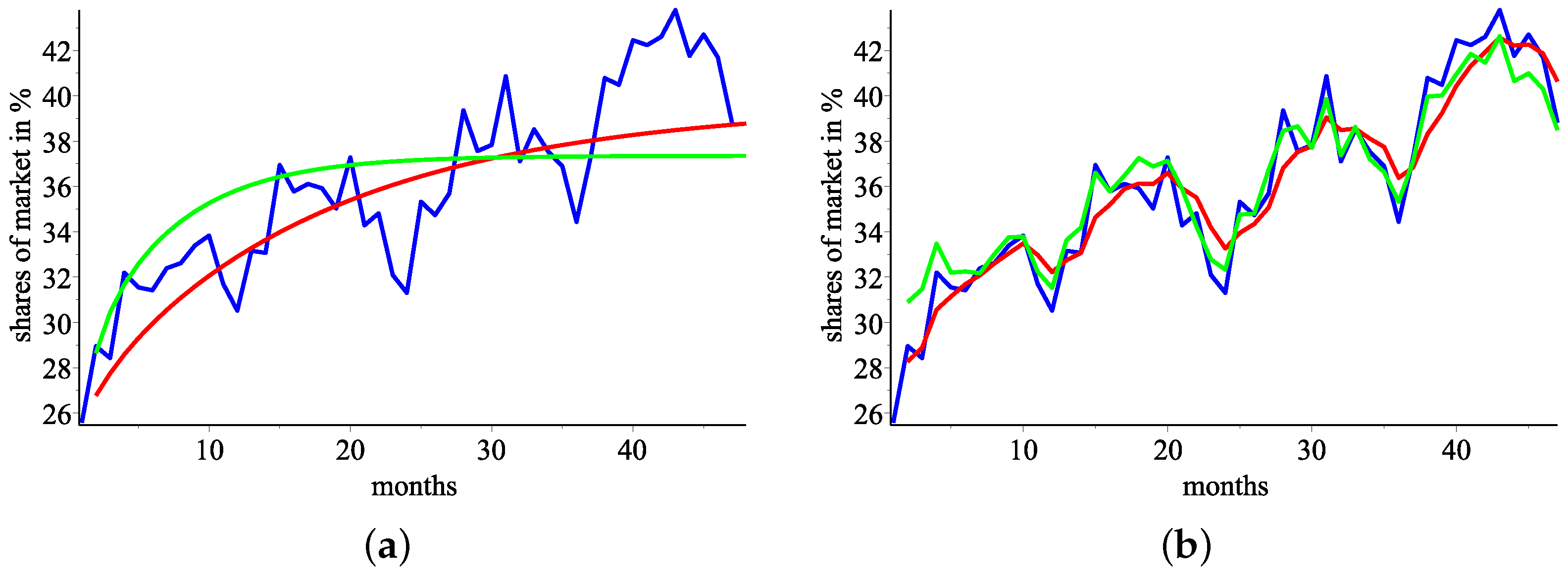

Figure 2 presents the observed and approximated values from the built models for each of the companies.

Figure 2.

Real data in blue vs approximated by response function in red. (a) Company 1, real data in blue vs approximated by response function shares in red; (b) Company 2, real data in blue vs approximated by response function shares in red; (c) Company 3, real data in blue vs approximated by response function shares in red.

In Table 7, for all companies, we see a high percentage: , , and respectively matching the data to the model, with an average absolute percentage error of less than .

Table 7.

Statistical performance of the created models.

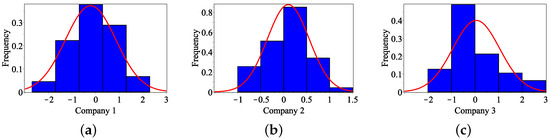

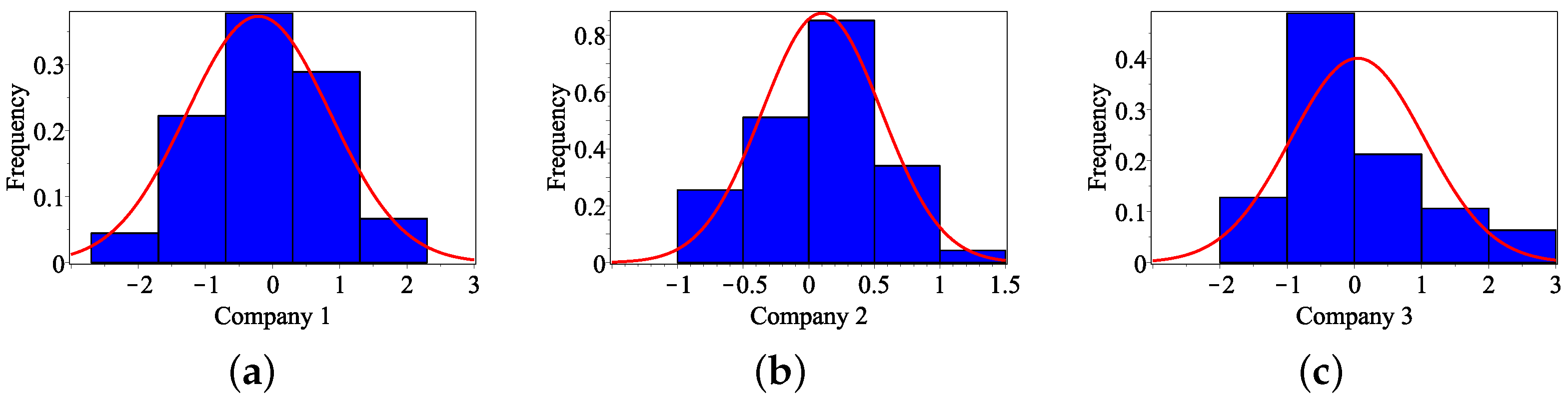

Figure 3 presents histograms of the residuals, which are seen to be normally distributed. The resulting models are statistically adequate.

Figure 3.

Histograms of the residuals. (a) Histograms of the residuals for Company 1 with mean and standard deviation: , . (b) Histograms of the residuals for Company 2 with mean and standard deviation: , . (c) Histograms of the residuals for Company 3 with mean and standard deviation: , .

The Kolmogorov-Smirnov tests for the match between the distribution of the data and the values predicted by the model in all cases are insignificant with p-value , and , respectively. This means that the null hypothesis that the datasets of real and predicted data have the same distribution is not rejected and the models adequately describe the data.

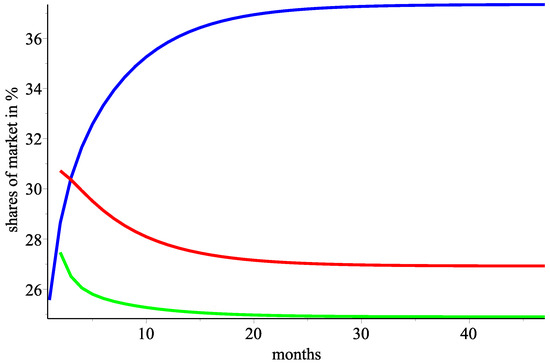

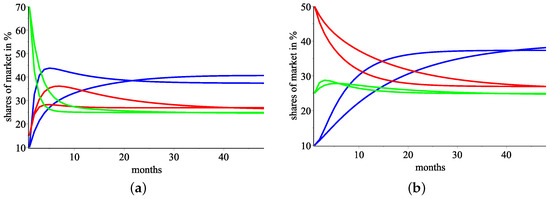

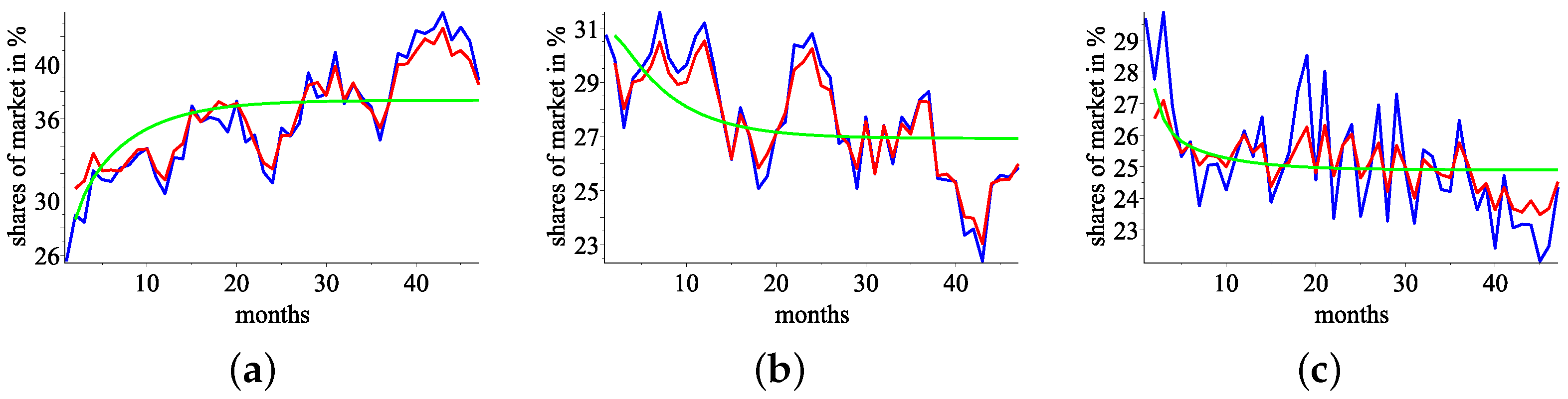

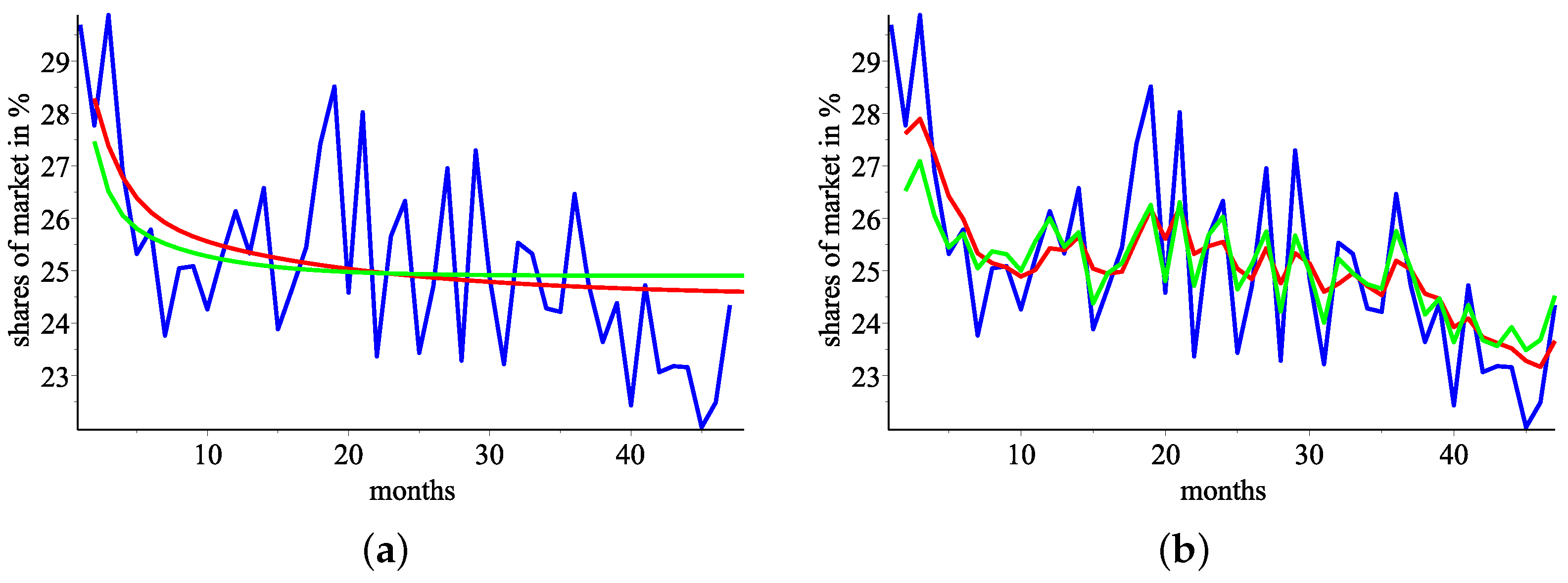

Applying the iterated process using the response functions (27) with the initial start of the market , we obtain how percentage shares will change over time. Figure 4a represents Company 1, Figure 4b represents Company 2, and Figure 4c represents Company 3.

Figure 4.

Real data vs iterated one. (a) Simulation of the sequence of successive percentage shares for Company 1, blue color for the real data, red color for , and green color for . (b) Simulation of the sequence of successive percentage shares for Company 2, blue color for the real data, red color for , and green color for . (c) Simulation of the sequence of successive percentage shares for Company 3, blue color for the real data, red color for , and green color for .

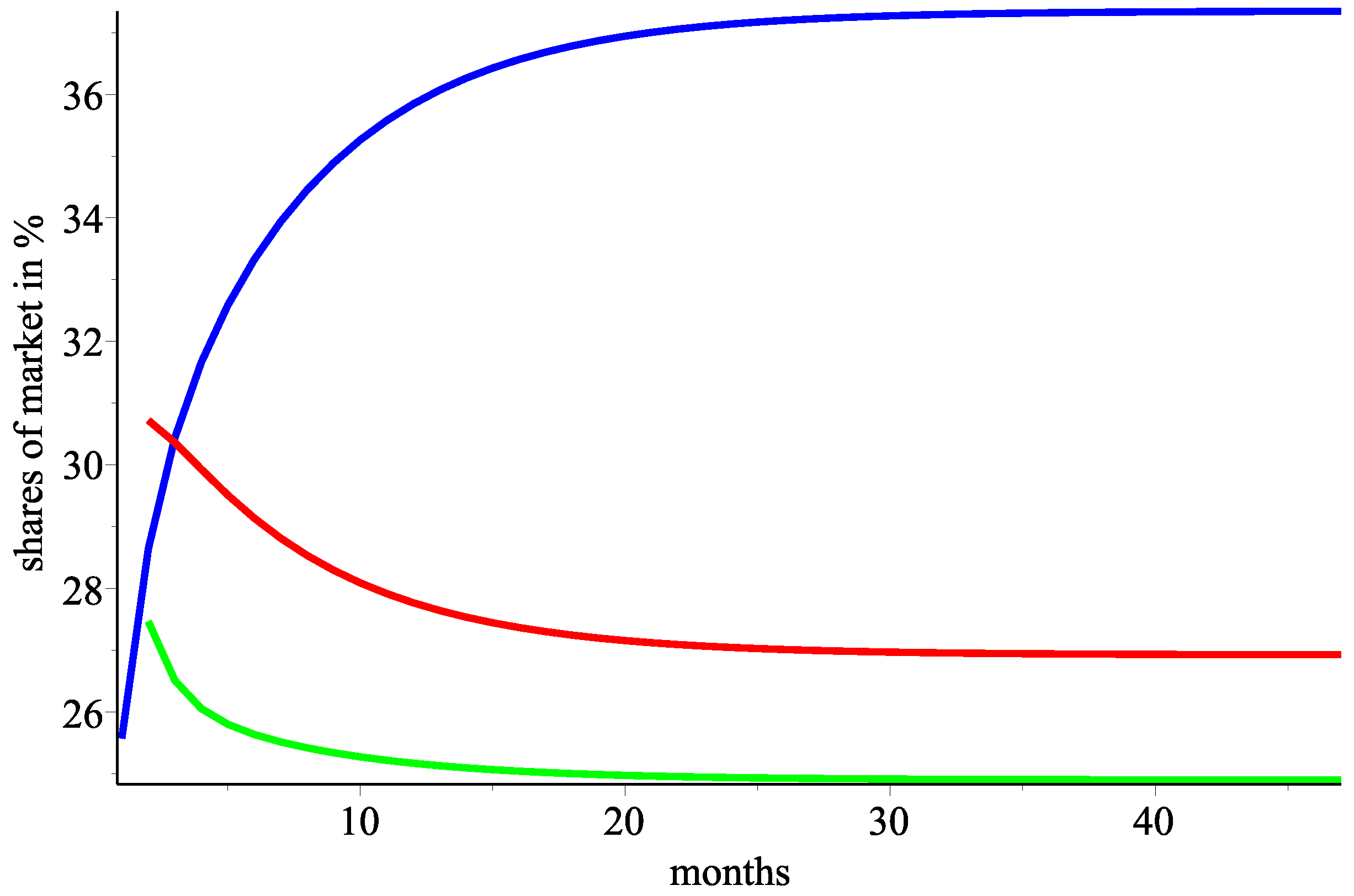

In Figure 5, we plot the predicted iterations of the three companies.

Figure 5.

Blue, red, and green colors for Companies 1, 2, and 3, respectively, for the sequences of successive iterations , .

4.4. Modeling the Response Functions after Smoothing the Empirical Data with Moving Averages

By replacing the data with its weighted moving averages at period 5 values we get Figure 6.

Figure 6.

(a) Company 1’s real data in blue vs the moving average data in red. (b) Company 2’s real data in blue vs the moving average data in red. (c) Company 3’s real data in blue vs the moving average data in red.

With the least squares method without imposing additional constraints we get the following response functions defined by

and it is easy to observe that and the ordered triple satisfies all the conditions in Corollary 1.

The Kolmogorov-Smirnov tests for the match between the distribution of the data and the values predicted by the model in all cases are insignificant with p-value , and , respectively. This means that the null hypothesis that the datasets of real and predicted data have the same distribution is not rejected and the models adequately describe the data.

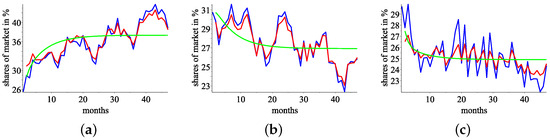

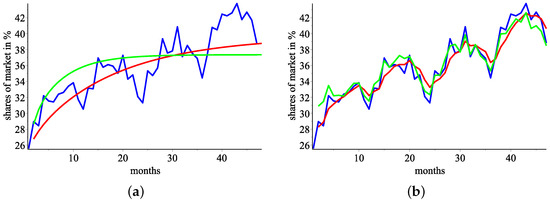

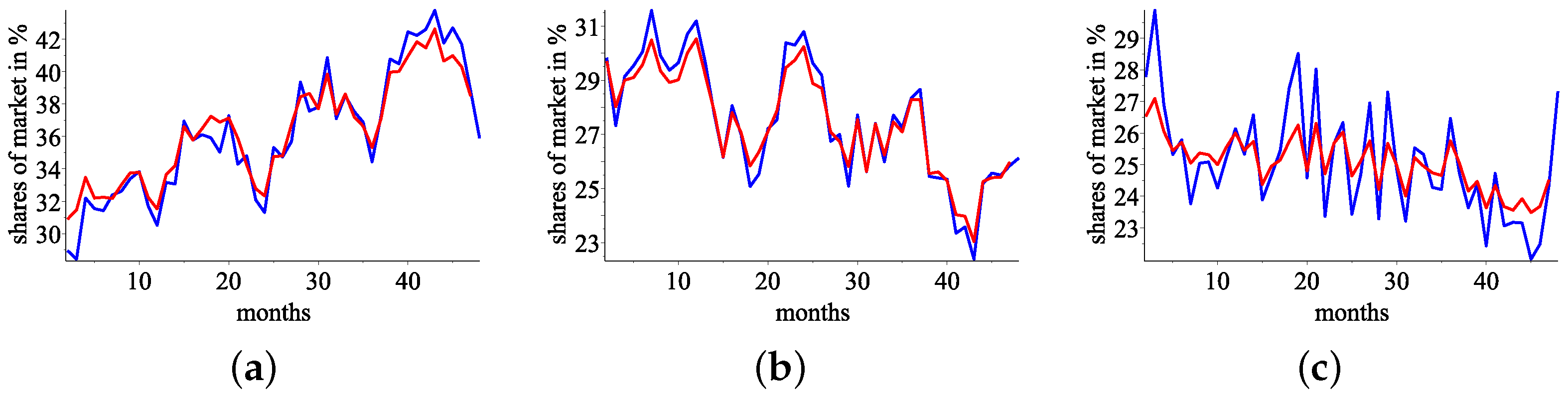

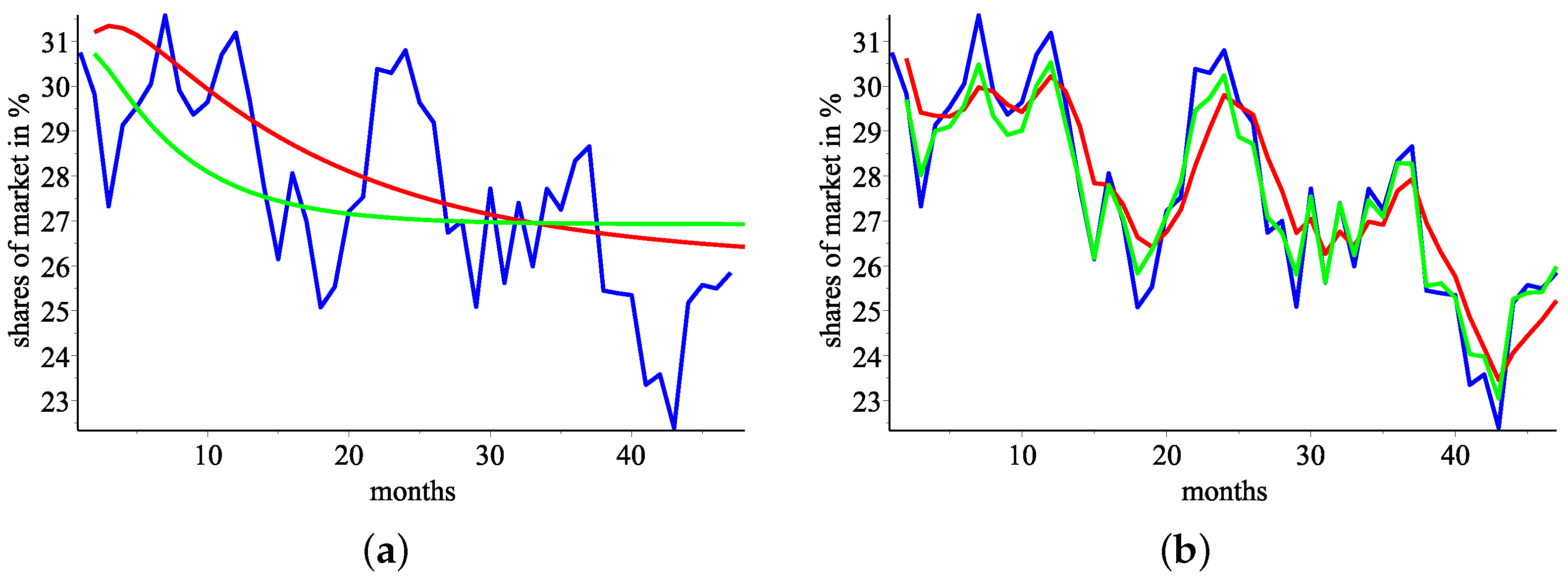

Figure 7a, Figure 8a, and Figure 9a present the real data in blue, the predicted values by iterating (the response function constructed by the real data) in red, predicted values by iterating (the response function constructed by the moving average data) in green.

Figure 7.

(a) Company 1’s real data in blue, predicted values by iterating in green, predicted values by iterating in red (the response functions constructed by the real data and by the moving average data, respectively). (b) Company 1’s real data in blue, predicted values by (the response function constructed by the real data) in green, predicted values by (the response function constructed by the moving average data) in red.

Figure 8.

(a) Company 2’s real data in blue, predicted values by iterating in green, predicted values by iterating in red (the response functions constructed by the real data and by the moving average data, respectively). (b) Company 2’s real data in blue, predicted values by (the response function constructed by the real data) in green, predicted values by (the response function constructed by the moving average data) in red.

Figure 9.

(a) Company 3’s real data in blue, predicted values by iterating in green, predicted values by iterating in red (the response functions constructed by the real data and by the moving average data, respectively). (b) Company 3’s real data in blue, predicted values by (the response function constructed by the real data) in red, predicted values by (the response function constructed by the moving average data) in green.

5. The Stability, Uniqueness, and Existence of the Market Equilibrium

We demonstrate that the hypothesis of Corollary 1 is satisfied by the response functions from (27). Indeed, the following inequalities hold:

and

After summing (29), (30), and (31), we get

where . Using the empirical data, we see that the sets of the percentage shares of the three major players in the market are , , and . It is easy to calculate

and

Thus, the assumptions of Corollary 1 are satisfied, and there exists a unique market equilibrium , which is the market shares in percentage. The total percentage is smaller that 100, because we have removed several small producers that represent approximately of the market.

Using comparable computations, we determine that the ordered triple of response functions meets Corollary 1’s assumption. and therefore there is a unique market equilibrium. Solving the system of equations , , and , we get that the market equilibrium, predicted by the smoothing data model, will be .

This model has an advantage compared to the first one. From (28) we see that the increase in sales of any of the companies leads to an increase in their production. We also see that any increase in the market shares of the second and third companies leads to a very small decrease in the performance of the first company (the largest one). Any increase in the percentage shares of the first player (the largest one) leads to a small decrease in the other two, and finally, any increase in the performance of any of the two small producers leads to an increment in the production of the other small one, i.e., there is a kind of symmetry between the responses of the big producer and the two smaller ones. Let us point out that in the optimization with least squares, there was no need for additional assumptions on the coefficients , .

6. Conclusions

Rather than solving a payoff maximization issue, we use an equilibrium theory based on reaction functions to experimentally examine the beer manufacturers in Bulgaria. Overall, this serves as an example of the paradigm that (Dzhabarova et al. 2020; Kabaivanov et al. 2022) presented to represent market equilibrium via response functions.

As demonstrated in Badev et al. (2024) during the examination of equilibrium in the US market for wireless telecommunications, the assumptions in the main theorem are only sufficient ones. This is demonstrated by presenting the market behavior, provided that the starting point of the market lies outside the domain of the response functions.

Data analysis shows that the idea proposed can be applied to real markets and determine whether the market is stable, has reached equilibrium, and whether this equilibrium is unique. This analysis is not specifically related to the beer industry. The obtained results demonstrate the possibility that the theory of equilibrium based on response functions has the potential to study the dynamics in oligopolistic markets. Such an example is proposed for mobile services in the US. It is possible to apply this technique in other markets as well, such as aircraft manufacturing, operating systems, and mobile phone manufacturers, where there are also a small number of manufacturers holding a large market share. As we mentioned in the text, the results can also be used by government bodies, statistical institutes, and companies. Firms may assume that the results show that to change their market share, it is necessary to make a significant change in their policy and technology.

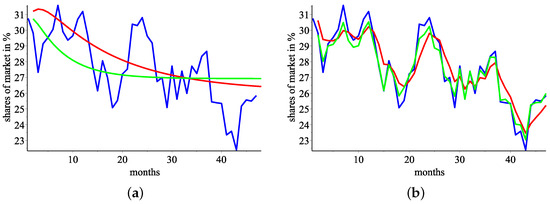

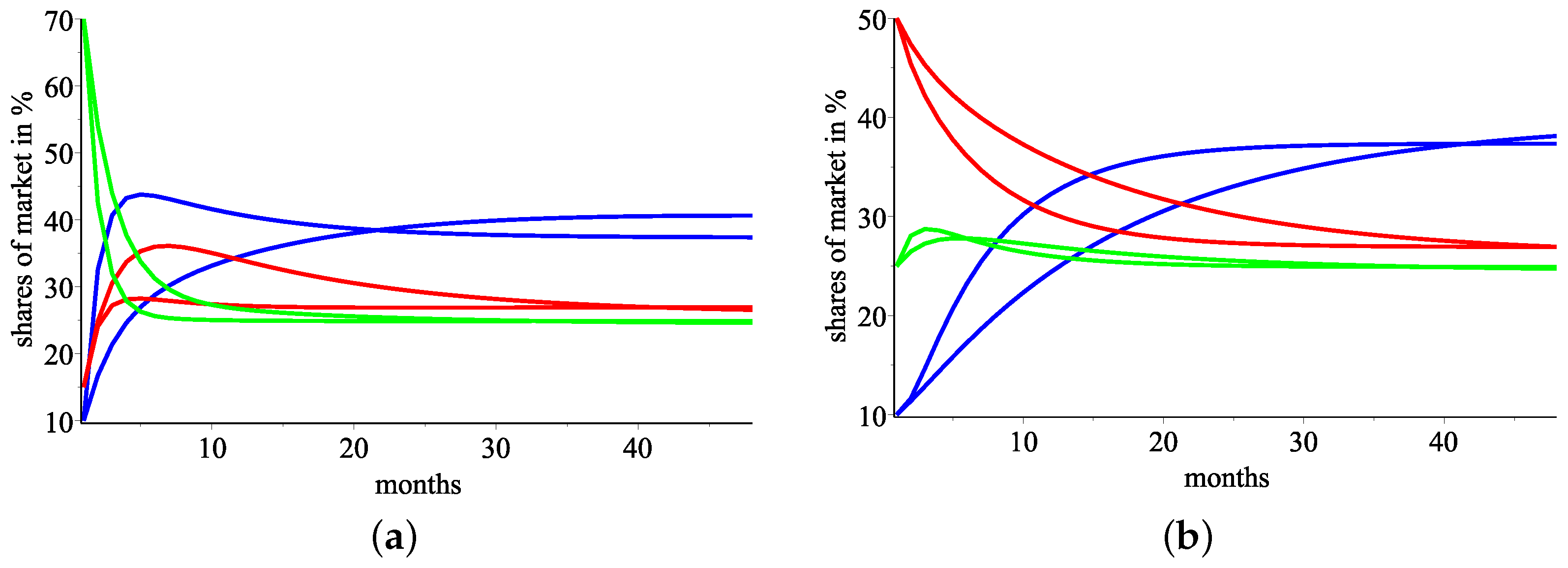

If we try to simulate such a state for the beer market with the obtained response functions and an initial start of the market arbitrary chosen, for example , we obtain Figure 10.

Figure 10.

(a) Simulation, with the two models, of the market with an initial start at levels Company 1, 2, and 3 in blue, red, and green colors respectively. (b) Simulation, with the two models, of the market with an initial start at levels Company 1, 2, and 3 in blue, red, and green colors respectively.

This simulation suggests that if , then it is possible for a sequence of successive productions to converge to the same market equilibrium too, which coincides with the observations made in Badev et al. (2024). Therefore, we can conclude that the imposed conditions in Corollary 1 and Theorem 3 are only sufficient ones.

Let us mention that when looking to model discrete data with continuous functions, there are infinite number models that can describe the available data statistically reliably. Therefore, the imposition of additional constraints on the modeling of real processes is adopted. Once the model is constructed, it is checked to see how much the continuous model differs statistically from the actual discrete data (Carr and Lykkesfeldt 2023; Eid et al. 2023; Gobin et al. 2023; Krishnasamy et al. 2023). What is interesting in the research is that both considered models give similar results for the levels at which market equilibrium is reached, that it is unique, and that it is stable. Also, simulations with an arbitrarily chosen initial state of the economy show that both models quickly stabilize around equilibrium levels.

An intriguing endeavor is to investigate other oligopolistic markets. Another open problem that we find interesting is the following: Let us have available data on the quantity sales and cost functions for the participants and have constructed the response functions. If we assume that the participants behave rationally, then let’s try to recover the price function and, from there, the demand function. Or if we have the price function, try to recover the cost function for the participants.

Given enough data, for example, light beer, non-alcoholic beer, and dark beer, a response function can be constructed for the entire basket of products offered. In addition, a Cornot-Bertrand model where producers compete simultaneously for quantities and prices is considered in Dzhabarova et al. (2020). If for the mentioned types of beer there are also their prices on the market, an equilibrium can be sought in terms of price and quantity, as proposed in Dzhabarova et al. (2020). In the orderly triad of quantity and price, one can add the code of marketing performance and seek balance in terms of quantities, prices, and marketing. This can be done for different types of industries, for example, petrol producers.

Author Contributions

Conceptualization, A.I., V.I., H.K., P.Y. and B.Z.; methodology, A.I., V.I., H.K., P.Y. and B.Z.; investigation, A.I., V.I., H.K., P.Y. and B.Z.; writing—original draft preparation, A.I., V.I., H.K., P.Y. and B.Z.; writing-review and editing, A.I., V.I., H.K., P.Y. and B.Z. The listed authors have contributed equally in the research and are listed in alphabetical order. All authors have read and agreed to the published version of the manuscript.

Funding

The research is partially financed by the European Union-NextGenerationEU, through the National Recovery and Resilience Plan of the Republic of Bulgaria, project DUECOS BG-RRP-2.004-0001-C01.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

Available at https://www.statista.com, accessed on 20 February 2024.

Acknowledgments

The authors appreciate the efforts of the anonymous reviewers in improving the quality and presentation of their work.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Ajeti, Laura, Atanas Ilchev, and Boyan Zlatanov. 2022. On coupled best proximity points in reflexive Banach spaces. Mathematics 10: 1304. [Google Scholar] [CrossRef]

- Alavifard, Farzad, Dmitry Ivanov, and Jian He. 2020. Optimal divestment time in supply chain redesign under oligopoly: Evidence from shale oil production plants. International Transactions in Operational Research 27: 2559–83. [Google Scholar] [CrossRef]

- Amini-Harandi, Alireza. 2013. Coupled and tripled fixed point theory in partially ordered metric spaces with application to initial value problem. Mathematical and Computer Modelling 57: 2343–48. [Google Scholar] [CrossRef]

- Andaluz, Joaquin, Abdelalim Elsadany, and Gloria Jarne. 2020. Dynamic Cournot oligopoly game based on general isoelastic demand. Nonlinear Dynamics 99: 1053–63. [Google Scholar] [CrossRef]

- Badev, Anton, Stanimir Kabaivanov, Peter Kopanov, Vasil Zhelinski, and Boyan Zlatanov. 2024. Long-Run Equilibrium in the Market of Mobile Services in the USA. Mathematics 12: 724. [Google Scholar] [CrossRef]

- Baik, Kyung Hwan, and Dongryul Lee. 2020. Decisions of duopoly firms on sharing information on their delegation contracts. Review of Industrial Organization 57: 145–65. [Google Scholar] [CrossRef]

- Banach, Stefan. 1922. Sur les opérations dan les ensembles abstraits et leurs applications aux integrales. Fundamenta Mathematicae 3: 133–81. [Google Scholar] [CrossRef]

- Berinde, Vasile, and Marin Borcut. 2011. Tripled fixed point theorems for contractive type mappings in partially ordered metric spaces. Nonlinear Analysis: Theory, Methods and Applications 74: 4889–97. [Google Scholar] [CrossRef]

- Bhaskar, Gnana, and Vangipuram Lakshmikantham. 2006. Fixed point theorems in partially ordered metric spaces and applications. Nonlinear Analysis: Theory, Methods and Applications 65: 1379–93. [Google Scholar] [CrossRef]

- Bischi, Gian-Italo, Carl Chiarella, Michael Kopel, and Ferenc Szidarovszky. 2010. Nonlinear Oligopolies Stability and Bifurcations. Berlin and Heidelberg: Springer. [Google Scholar] [CrossRef]

- Bretscher, Otto. 1997. Linear Algebra with Applications. Upper Saddle River: Prentice Hall. [Google Scholar]

- Carr, Anitra C., and Jens Lykkesfeldt. 2023. Factors Affecting the Vitamin C Dose-Concentration Relationship: Implications for Global Vitamin C Dietary Recommendations. Nutrients 15: 1657. [Google Scholar] [CrossRef] [PubMed]

- Cellini, Roberto, and Luca Lambertini. 2004. Dynamic oligopoly with sticky prices: Closed-loop, feedback and open-loop solutions. Journal of Dynamical and Control Systems 10: 303–14. [Google Scholar] [CrossRef]

- Chatterjea, Santi Kumar 1972. Fixed-point theorems. Comptes Rendus de L’Academie Bulgare des Sciences 25: 727–30.

- Cournot, Antoine Augustin. 1897. Researches Into the Mathematical Principles of the Theory of Wealth. New York: Macmillan. [Google Scholar]

- Dickey, David, and Wayne Fuller. 1979. Distribution of the estimators for autoregressive time series with a unit root. Journal of American Statistical Association 74: 427–31. [Google Scholar] [CrossRef]

- Dzhabarova, Yulia, and Boyan Zlatanov. 2022. A note on the market equilibrium in oligopoly with three industrial players. AIP Conference Proceedings 2449: 070013. [Google Scholar] [CrossRef]

- Dzhabarova, Yulia, Stanimir Kabaivanov, Margarita Ruseva, and Boyan Zlatanov. 2020. Existence, Uniqueness and Stability of Market Equilibrium in Oligopoly Markets. Administrative Sciences 10: 70. [Google Scholar] [CrossRef]

- Eid, Ebrahem M., Amr E. Keshta, Sulaiman A. Alrumman, Muhammad Arshad, Kamal H. Shaltout, Mohamed T. Ahmed, Dhafer A. Al-Bakre, Ahmed H. Alfarhan, and Damia Barcelo. 2023 Modeling Soil Organic Carbon at Coastal Sabkhas with Different Vegetation Covers at the Red Sea Coast of Saudi Arabia. Journal of Marine Science and Engineering 11: 295. [CrossRef]

- Friedman, James W. 1983. Oligopoly Theory. Cambradge: Cambradge University Press. [Google Scholar] [CrossRef]

- Geraskin, Mikhail. 2020. The properties of conjectural variations in the nonlinear stackelberg oligopoly model. Automation and Remote Control 81: 1051–72. [Google Scholar] [CrossRef]

- Gobin, Anne, Abdoul-Hamid Mohamed Sallah, Yannick Curnel, Cindy Delvoye, Marie Weiss, Joost Wellens, Isabelle Piccard, Viviane Planchon, Bernard Tychon, Jean-Pierre Goffart, and et al. 2023. Crop Phenology Modelling Using Proximal and Satellite Sensor Data. Remote Sensing 15: 2090. [Google Scholar] [CrossRef]

- Guo, Dajun, and Vangipuram Lakshmikantham. 1987. Coupled fixed points of nonlinear operators with applications. Nonlinear Analysis, Theory, Methods and Applications 11: 623–32. [Google Scholar] [CrossRef]

- Hardy, George E., and Thomas D. Rogers. 1973. A generalization of a fixed point theorem of Reich. Canadian Mathematical Bulletin 16: 201–6. [Google Scholar] [CrossRef]

- Jantyik, Lili, Áron Török, and Jeremiás Máté Balogh. 2020. Identification of the factors influencing the profitability of the Hungarian beer industry. Review on Agriculture and Rural Development 8: 163–67. [Google Scholar] [CrossRef]

- Kabaivanov, Stanimir, Vasil Zhelinski, and Boyan Zlatanov. 2022. Coupled Fixed Points for Hardy–Rogers Type of Maps and Their Applications in the Investigations of Market Equilibrium in Duopoly Markets for Non-Differentiable, Nonlinear Response Functions. Symmetry 14: 605. [Google Scholar] [CrossRef]

- Kannan, Rangachary. 1978. Some results on fixed points. Bulletin of the Calcutta Mathematical Society 10: 71–76. [Google Scholar]

- Kirk, William, Pinchi S. Srinivasan, and Panimalar Veeramani. 2003. Fixed points for mappings satisfying cyclical contractive conditions. Fixed Point Theory 4: 179–89. [Google Scholar]

- Krishnasamy, Sundaramoorthy, Mutlaq B. Alotaibi, Lolwah I. Alehaideb, and Qaisar Abbas. 2023. Development and Validation of a Cyber-Physical System Leveraging EFDPN for Enhanced WSN-IoT Network Security. Sensors 23: 9294. [Google Scholar] [CrossRef] [PubMed]

- Liu, Yifan, and Mei Sun. 2020. Application of duopoly multi-periodical game with bounded rationality in power supply market based on information asymmetry. Applied Mathematical Modelling 87: 300–16. [Google Scholar] [CrossRef]

- Lorenzo, Renato Di. 2013. Basic Technical Analysis of Financial Markets—A Modern Approach. Milan, Heidelberg, New York, Dordrecht and London: Springer. [Google Scholar] [CrossRef]

- Matsumoto, Akio, and Ferenc Szidarovszky. 2018. Dynamic Oligopolies with Time Delays. Singapore: Springer. [Google Scholar] [CrossRef]

- Okuguchi, Koji. 1976. Expectations and Stability in Oligopoly Models. Berlin and Heidelberg: Springer. [Google Scholar] [CrossRef]

- Okuguchi, Koji, and Ferenc Szidarovszky. 1999. The Theory of Oligopoly with Multi–Product Firms. Heidelberg, New York, Barcelona, Hongkong, London, Milan and Paris: Springer. [Google Scholar] [CrossRef]

- Petruşel, Adrian. 2018. Fixed points vs. coupled fixed points. Journal of Fixed Point Theory and Applications 20: 150. [Google Scholar] [CrossRef]

- Reich, Simeon. 1971. Kannan’s fixed point theorem. Bollettino della Unione Matematica Italiana. Series IV 4: 1–11. [Google Scholar]

- Rubinstein, Ariel. 1998. Modeling Bounded Rationality. Cambridge: MIT Press. [Google Scholar]

- Samet, Bessem, and Calogero Vetro. 2010. Coupled fixed point, F-invariant set and fixed point of N-order. Annals of Functional Analysis 1: 46–56. [Google Scholar] [CrossRef]

- Shaphiro, Samuel S., and Martin Bradbury Wilk. 1965. An Analysis of Variance Test for Normality (Complete Samples). Biometrika 52: 591–611. [Google Scholar] [CrossRef]

- Siegert, Caspar, and Robert Ulbricht. 2020. Dynamic oligopoly pricing: Evidence from the airline industry. International Journal of Industrial Organization 71: 102639. [Google Scholar] [CrossRef]

- Sintunavarat, Wutiphol, and Poom Kumam. 2012. Coupled best proximity point theorem in metric spaces. Fixed Point Theory and Applications 2012: 93. [Google Scholar] [CrossRef]

- Strandholm, John. 2020. Promotion of green technology under different environmental policies. Games 11: 32. [Google Scholar] [CrossRef]

- Török, Áron, Ákos Szerletics, and Lili Jantyik. 2020. Factors influencing competitiveness in the global beer trade. Sustainability 12: 5957. [Google Scholar] [CrossRef]

- Ueda, Masahiko. 2019. Effect of information asymmetry in Cournot duopoly game with bounded rationality. Applied Mathematics and Computation 362: 124535. [Google Scholar] [CrossRef]

- Van Trang, Nguyen Thi, Thi-Lich Nghiem, and Thi-Mai Do. 2020. Improving the Competitiveness for Enterprises in Brand Recognition Based on Machine Learning Approach. In Global Changes and Sustainable Development in Asian Emerging Market Economies Volume 1: Proceedings of EDESUS. Cham: Springer, pp. 359–73. [Google Scholar] [CrossRef]

- Wang, Xia, Jing Shen, and Zhengyao Sheng. 2020. Asymmetric model of the quantum Stackelberg duopoly with incomplete information. Physics Letters A 384: 126644. [Google Scholar] [CrossRef]

- Xiao, Guangnian, and Zihao Wang. 2020. Empirical study on bikesharing brand selection in China in the post-sharing era. Sustainability 12: 3125. [Google Scholar] [CrossRef]

- Zlatanov, Boyan. 2021. Coupled best proximity points for cyclic contractive maps and their applications. Fixed Point Theory 22: 431–52. [Google Scholar] [CrossRef]

- Zlatanov, Boyan. 2021. On a Generalization of Tripled Fixed or Best Proximity Points for a Class of Cyclic Contractive Maps. FILOMAT 35: 3015–31. [Google Scholar] [CrossRef]

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).