1. Introduction

Urgent response against climate change caused by anthropogenic greenhouse gas emissions is essential to counteract global risks, including food production shortages, rising sea levels, and catastrophic flooding. In this regard, emission abatement is the most viable option, which requires international efforts and cooperation. International top–down policy approaches, such as the Kyoto approach, have been assumed to be unsuccessful, and hence, bottom–up policy approaches, such as the Paris approach, have gained more attention [

1]. At the 21st Conference of the Parties in Paris in 2015, member states to the United Nations Framework Convention on Climate Change (UNFCCC) agreed to develop a sustainable low-carbon pathway via the stimulation of actions and enhancing low-carbon investments [

2]. The Paris Agreement aims to keep the increase in global average temperature to well below 2 °C above pre-industrial level and pursue endeavors to limit the increase to 1.5 °C [

2]. Most individual countries, including European countries, submitted national pledges of specific cuts in their carbon emissions by 2030, so-called Nationally Determined Contributions (NDCs). Note that there are countries that stated their emission reductions for other years, such as 2025 or 2035, and some countries did not even provide any quantified commitments and only provided qualitative efforts [

3].

These NDCs can be met through different market-based instruments such as the carbon pricing and emission trading system (ETS) (also known as “cap and trade”). By internalizing the costs of climate damage into prices, ETS allows for the international trade mechanism being taken into account and regions forming coalitions. Studies show that the linking of ETS can increase the efficiency of international greenhouse gas mitigation [

4,

5,

6,

7,

8]. For this reason, the linking of ETS is described as a central policy instrument to the Paris Agreement [

9] or viewed as a contingency option for achieving the Paris targets [

1].

Nevertheless, it is possible that the linking of ETS results in welfare losses in some of participating regions, and the aggregate welfare of the participating regions declines for reasons including international trade (also known as terms-of-trade) effects [

7,

10,

11]. As an example mechanism for this, compared to a non-trading scenario, if a specific region regains its international competitiveness through its relatively lower carbon prices while the rest of the participating regions become relatively less competitive through relatively higher carbon prices in an emission-trading scenario, then the region may gain welfare. At the same time, the rest of the regions may lose welfare. On this subject, some studies show that even if a region does not implement any climate policy, its welfare may be affected by the climate policy in other regions via terms-of-trade (ToT) effects [

11,

12]. Peterson and Weitzel [

13] suggest that in a global ETS, transfer payments are essential to balance indirect market effects. In this article, for the sake of brevity, transfer payments are not implemented. Studies such as [

14,

15,

16] discuss whether the different policy scenarios are stable or self-enforcing. If coalitions are not stable or self-enforcing, redistribution schemes are required to make them so.

The EU has one of the world’s most ambitious abatement policies and has established the world’s first cross-border carbon market and the largest by emissions covered at the time of establishment. The EU 2030 Climate and Energy Framework documents abatement intentions for sectors covered by the EU emission trading system (EU ETS) [

17]. Several papers have analyzed the welfare and distributional effects of the EU ETS (e.g., Tol [

18]; Böhringer [

19]; Vielle [

20]). In a multi-regional multi-sectoral CGE model intercomparison study using the GTAP9 data set [

21], the 36th round of Energy Modeling Forum (EMF36) investigates various policy regimes to fulfill different ambition levels and the widespread economic impacts such regimes may bring about [

6]. The Core EMF36 demonstrates that the results on the EU notably depend on the model in hand [

6]. While the Core EMF36 reports on the EU as an aggregate region, there are individual contributions that consider further disaggregating the EU [

22,

23,

24]. Analyzing the impacts of Norway joining the EU ETS, Faehn and Yonezawa [

22] model scenarios where two emission trading systems, with one international price each, co-exist. Their focus is on Norway, a small-open economy, while the rest of the EU is aggregated into one region. Disaggregating the EU into eight regions, Winkler et al. [

24] look into the circumstances under which ETS linking between the EU and China is most beneficial to the EU or China, but they do not consider two concurrent emission trading systems. Moreover, Kriegler et al. [

25] states that the EU reliance on coal and natural gas imports can decline more rapidly than oil imports—oil imports pose itself as a bottleneck, where the inefficiencies due to oil phase-out can create more elevated production costs.

The EU Commission has proposed applying emissions trading in new sectors where more acute mitigations are required to reach the 2030 target. According to the proposition, emissions from maritime transport will be incorporated into the current EU ETS, while a separate emissions trading system will cover emissions from fuels utilized in road transport and the building sector [

26]. Therefore, it is worthwhile to analyze the implications of such a proposal and its distributional impacts on the region.

In this study, the multi-regional multi-sectoral CGE model by Khabbazan and von Hirschhausen [

11] is used and the option that two international emission permit markets can be formed simultaneously is added. The underlying CGE model that Khabbazan and von Hirschhausen [

11] is based upon has also been used for the model intercomparison studies in Böhringer et al. [

6] and Akın-Olçum et al. [

4]. Using the GTAP10 Power data set [

27,

28], the EU region is further disaggregated into nine regions. The regional disaggregation of the EU is similar to that of Winkler et al. [

24], except that Ireland is disaggregated from Great Britain—since 2021, the UK has not been part of the EU ETS anymore. Then, after forward-calibration of the model based on International Energy Outlook (IEO) [

29] and World Energy Outlook (WEO) [

30] projections until 2030, marginal abatement cost curves (MACCs) are derived. In addition to the REF scenario in which no region collaborates, three policy scenarios are simulated:

- EU_EITE

where an ETS covers the emission-intensive sectors and electricity (EITE), mimicking the current EU ETS sectors, is formed.

- EU_MIX

where, in addition to an ETS covering EITE, another ETS covers NEIT sectors (i.e., all sectors rather than EITE).

- EU_Full

where one ETS covers all sectors.

Each policy scenario is run for four emission reduction targets, i.e., NDC, conditional NDC (NDC+), NDC to meet the 2-degree global average temperature target (NDC-2C), and NDC to meet the 1.5-degree global average temperature target (NDC-1.5C). Note that only the NDC targets are politically approved documents [

3], and the rest (NDC+, NDC-2C, and NDC-1.5C) are hypothetically calculated. Please see

Section 2.3.

Therefore, there are four main research questions:

What are the cost-effectiveness and welfare impacts of current the EU ETS, i.e., moving from the REF scenario to EU_EITE?

What does the EU region gain in effectiveness terms from involving in further regional flexibility, i.e., moving from EU_EITE to EU_MIX, and what are the distributional implications?

How will a fully flexible EU ETS regime impact effectiveness and welfare in the EU regions, i.e., moving to EU_Full?

How will the impacts evolve under different baselines and ambition levels?

Previous articles have studied linking regional allowance trading systems [

10,

22,

31,

32,

33,

34,

35]. Economic theories suggest that the abatement cost for the coalition as a whole “unambiguously declines as more flexibility is introduced” [

22]. In this regard, the overall reduction in the abatement cost is not necessarily associated with an overall increase in total welfare. Likewise, a Pareto improvement is not necessarily reached—some members of the coalition might lose [

32,

34].

The paper’s results on marginal abatement costs (MACs) indicate that NEIT MACs are more expensive than EITE MACs under both baselines. In addition, East Europe (EEU) and Germany have the lowest MACs among the EU regions. Additionally, the MACs under the WEO baseline are slightly higher than under the IEO baseline. In addition, this paper’s results suggest that the common carbon price in the emission permit market covering the NEIT is significantly higher than the common carbon price in the emission permit market covering the EITE. Moreover, moving from the EU_EITE scenario to the EU_MIX scenario can decrease the abatement cost for the EU and bring about a significant welfare gain as a whole. In addition, the results suggest that moving from the EU_MIX to the EU_Full scenario may decrease the overall welfare. The underlying reason is the slight loss of international competitiveness under the EU_Full scenario.

This paper proceeds as follows: the following section describes the framework for this paper in detail.

Section 3 presents and interprets the modeling results.

Section 4 comprises a discussion, and

Section 5 concludes the paper.

3. Results

In this section, the baseline results are first presented for the selected model regions. Then, the MAACs on EITE, NEIT, and All sectors for the selected model regions and EUR are presented. After that, the policy options using the IEO baseline are presented. Next, the extra scenarios using the IEO baseline follows. Finally, the results of policy scenarios using the WEO baseline are compared with those of the IEO baseline.

3.1. Baseline

Table 7 presents the welfare (measured as a composite of representative agent’s consumption) and the EITE and NEIT shares of emission in the baseline in 2030 for the selected model regions after the calibration (see

Section 2.3 for details on the calibration procedure). Note that the real growth rate of investment and government spendings are equal to the real growth rate of private consumption during the calibration. Hence, the private consumption approximately grows with the same GDP scales presented in

Figure 3. The shares of emissions show that the emissions in all regions have slightly shifted toward the NEIT sectors—the NEIT sectors emit slightly higher than 57% of emission in the EU region under both baselines. This information later will become helpful as it implies that a common carbon price in a policy scenario may lie toward the carbon price in certain regions or sectors. The EITE shares of emission are still the highest in DEU and EEU. The NEIT shares of emission in France are the highest compared to the rest. Except for SEU, the EITE shares are sightly higher under the IEO baseline than those under the WEO baseline.

3.2. Marginal Abatement Cost Curves

Marginal abatement cost curves (MACCs) are highly informative, specifically when studying the effects of carbon pricing and ETS linking. From a regional perspective, MACCs depend on several circumstances, including, but not limited to, domestic potentials for emission reduction and the opportunities of abatement by importing commodities with lower emissions.

Figure 4 shows the MACCs in percentage change in the selected EU regions in 2030 for EITE, NEIT, and all sectors (All) under the IEO and WEO baselines.

Figure 5 shows the MACCs in percentage change in EUR in 2030 for EITE, NEIT, and All sectors under the IEO and WEO baselines. As the Paris targets (NDCs) in this study are presented in percentage reductions in emissions, MACCs in percentage change can determine the approximate value of carbon price required for fulfilling the NDCs.

The EU regions vary in their MACCs. For EITE MACCs, EEU and Germany, in order, have the cheapest MACCs under both baselines. For a carbon price of 150 $/tCO2, EEU and Germany can reduce their EITE emission by more than 82% and 72% under the IEO baseline. France, BLX, and SCA have the most expensive MACCs for EITE under both baselines. For a carbon price of 100 $/tCO2, France, BLX, and SCA, respectively, can reduce their emission in the EITE sectors by about 37%, 40%, and 43% under the IEO baseline. Generally, comparing EITE MACCs in the IEO with those in the WEO, the MACCs under the WEO baseline are slightly more expensive than the MACCs under the IEO baseline.

Several insights emerge concerning the NEIT MACCs and All MACCs: (i) The NEIT MACCs are significantly more expensive than EITE MACCs for all the selected model regions. (ii) The differences in the NEIT MACCs along the EU regions are not as significant as in the EITE MACCs. (iii) EEU has the lowest NEIT MACCs. (iv) MACCs for All sectors fall in between EITE MACCs and NEIT MACCs for all the selected model regions. Furthermore, (v) NEIT and All MACCs under the WEO baseline are slightly more expensive than the MACCs under the IEO baseline.

Nevertheless, while the MACCs may suggest which region may act as an emission permit supplier or demander in a theoretical cooperation scenario, three remarks are necessary:

- 1.

The position of a specific region in the emission permit market depends not only on the regions’ relative MACCs but also on the regions’ ambition levels (NDCs). Therefore, one region having a cheaper MACC does not guarantee to enter the emission permit market as a supplier of emission permits.

- 2.

This analysis is solely based on the technologies available in the GTAP 10 Power data set, and, for example, there is no renewable backstop technology that could potentially reduce the MACCs.

- 3.

The MACCs are derived in the absence of climate policy in other regions.

Therefore, the following section investigates the policy options and cooperation scenarios in more detail.

3.3. Policy Scenarios under the IEO Baseline

This section implements policy scenarios in CO

2 emissions reductions in 2030 relative to the baseline CO

2 emissions when parallel emission trading markets can be formed in the EU (see

Table 5 in

Section 2.5). Here, changes in several macroeconomic variables for the selected model regions and EUR are reported. For the sake of brevity, here, only the results using the IEO baseline for the ambition levels NDC and NDC-1.5C as the lowest and highest targets are presented. The results for selected variables in NDC+ and NDC-2C using the IEO baseline are reported in

Appendix A. The results for selected variables under the WEO baseline and the results for the extra scenarios are presented in the following subsections.

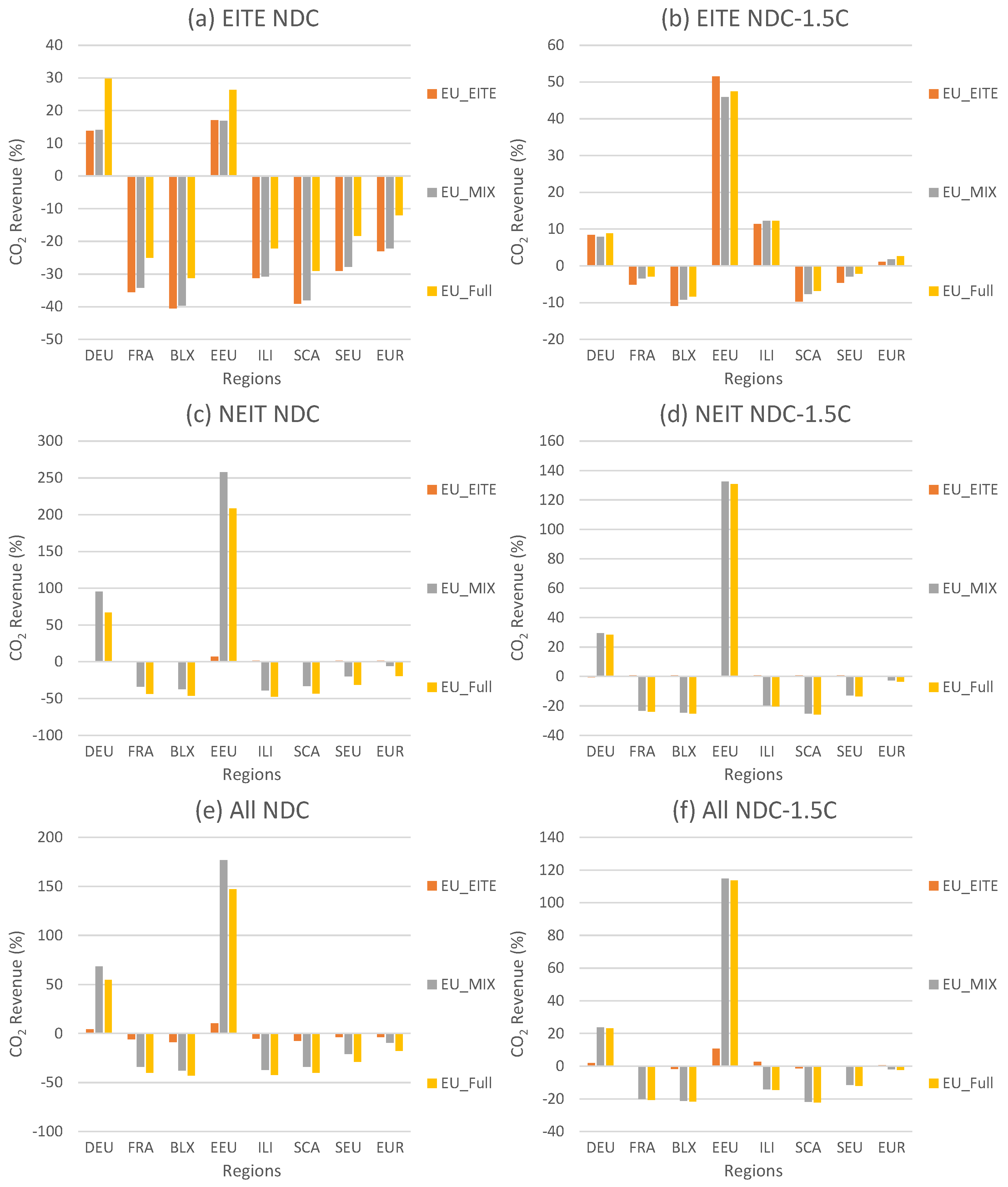

Table 8 shows the CO

2 prices for the EITE and NEIT sectors, and

Figure 6 and

Figure 7 present, respectively, the corresponding percentage changes in CO

2 emission and CO

2 revenues in EITE, NEIT, and All sectors. Note that the CO

2 revenues consist of the CO

2 revenues from the internal emission permit market plus the net CO

2 revenues from entering the emission trading markets. The results for import quantity and import price of fuels are reported in

Table 9 and

Table 10. In addition,

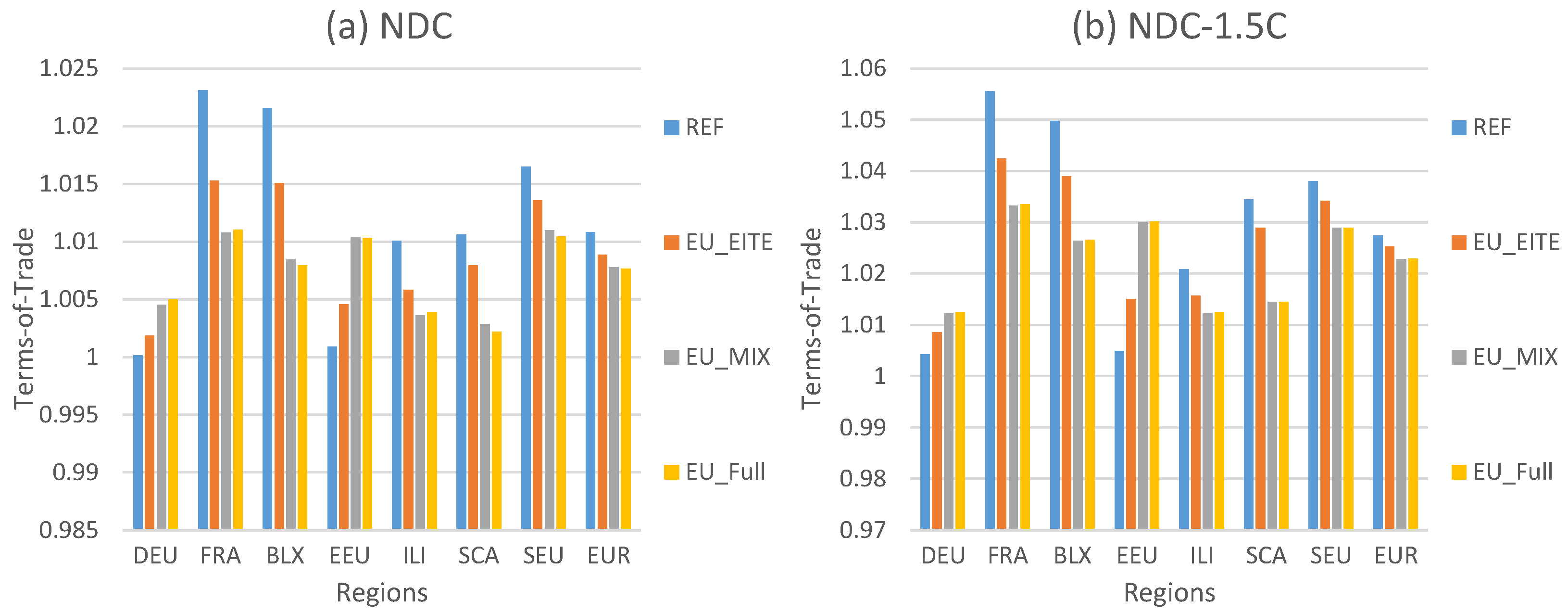

Figure 8 and

Figure 9, respectively, present ToT (Terms-of-Trade in Laspeyres index) and the percentage change in the welfare (measured as equivalent variation (EV) by calculating a composite of representative agent’s consumption) in the selected model regions. EUR shows the aggregated macro indicator or weighted average result for the EU regions in all results. In

Figure 7, the results are measured against the REF scenario, whereas in other figures, the results show the changes against the baseline.

In the REF scenario, the regions are restricted to their NDCs (see

Table 4 for NDCs), and the carbon prices demonstrate the availability of domestic abatement capacity and the astringency of the ambition level. Nonetheless, the REF scenario’s carbon prices may not precisely match the carbon prices on the MACCs (see

Section 2.4), as here, the ToT effects and climate policy in all regions are taken into account. Along with cooperation scenarios, by definition, the CO

2 emissions in regions that do not participate in coalitions do not alter and only change along NDCs. Nevertheless, the carbon prices in regions that do not participate in coalitions can be affected along with the cooperation scenarios, reflecting the ToT effect. The common carbon price will be placed between the highest and the lowest carbon prices in the regions participating in a coalition. Note that the welfare in a participating region is generally affected via: (i) increasing (decreasing) in its carbon emission, (ii) paying (receiving) for emission permits, and (iii) changing its international trade competitiveness.

It is worthwhile first to analyze the results under the REF scenario. The EEU has the lowest carbon price of about 52.9 $/tCO2 in NDC and about 200.5 $/tCO2 in NDC-1.5C due to its low MACCs. After the EEU, Germany and SEU, in order, have the lowest carbon price of about 108.9 $/tCO2 and 313.5 $/tCO2 in NDC and carbon price of about 458.2 $/tCO2 and 837.7 $/tCO2 in NDC-1.5C. France, BLX, ILI, and SCA have significantly higher carbon prices than EEU, Germany, and SEU. The carbon price in France, BLX, ILI, and SCA may go beyond 1000 $/tCO2 in NDC-1.5C.

Concerning the results under the REF scenario, several insights emerge: (i) Due to the cheaper MACCs in EITE than the MACCs in NEIT, a higher portion of the mitigation is achieved via decreasing the emission in EITE than in NEIT in all model regions and under all ambition levels. (ii) In all regions and under all ambition levels, the import of coal significantly reduces—the import of oil experiences the lowest reduction in the EU as a whole. Under the NDC, the import of oil by EEU even slightly increases. (iii) ToT in all EU regions improves. The ToT improvements are more significant for France, BLX, SCA, and SEU.

Several insights emerge concerning the EU_EITE scenario: (i) The common carbon prices under all ambition levels and baselines are only higher than the EEU’s and Germany’s carbon prices in the REF. Thus, these regions emerge as the suppliers of emission permits. The rest of the regions are the demanders of emission permits. (ii) While the import of fuels by most EU regions increases, the fuel imports decrease in EEU and Germany. Nevertheless, this phenomenon is more visible under the low ambition scenarios. (iii) While the ToT in the EEU and Germany improves, the ToT in the rest of the EU regions degrade. (iv) Forming an emission permit market covering EITE does not significantly influence regional carbon prices in the NEIT sector and only marginally increases them, except for Germany. (v) Except for Germany under the NDC and Germany and EEU under the NDC-1.5C, all the EU regions experience a significant welfare increase, and the welfare in EUR accordingly improves.

In addition, concerning the EU_MIX scenario, several insights emerge: (i) The common carbon price in the emission permit market covering NEIT is significantly higher than the common carbon price in the emission permit market covering EITE. This phenomenon is also influenced by the higher share of emissions in total NEIT from regions with relatively higher carbon prices, such as SEU, which is evident through the aggregate NEIT carbon price in the EUR under the REF scenario (see

Table 8 for details). (ii) The formation of the emission permit market covering NEIT does not markedly influence the emission permit market covering EITE, which is evident through insignificant changes in the common carbon prices in the ETS covering EITE sectors in all ambition levels. (iii) EEU and Germany enter the emission permit market covering NEIT as significant emission suppliers permits. Consequently, the overall CO

2 revenues in EEU and Germany rise significantly. The NEIT export reduction in these regions is compensated by the rise in ToT due to the significant decrease in fossil fuel imports. Hence, the welfare in these regions considerably increases. The EEU’s welfare exceptionally improves beyond its baseline level. (iv) Under all ambition levels, France, BLX, ILI, SCA, and SEU demand emission permits covering NEIT, increasing their total emission. However, as the import of fuels significantly increases in these regions, their ToT notably decreases. Nevertheless, it is only under the NDC-1.5C that the effects of emission rise in France and BLX are dominated by the payment and trade effects, and their welfares fall below their REF values. (v) The aggregate import of coal in EUR reduces, whereas the aggregate imports of oil and natural gas increase. The welfare gains in the EEU and Germany outweigh the losses in other regions, and the aggregate welfare in EUR improves.

Finally, concerning the EU_Full scenario, several insights emerge: (i) In all regions, compared to the EU_MIX scenario, mitigation and CO2 revenues in the EITE sectors increase, while mitigation and CO2 revenues in the NEIT sectors decrease. Nevertheless, this phenomenon is more pronounced for low than high ambition levels. (ii) Total (All) emissions for all the EU regions do not change significantly. (iii) The overall CO2 revenues (abatement cost) in all regions and EUR decrease. (v) Under the NDC, due to a further reduction in coal production, the EU regions become more dependent on imported oil. Under the NDC-1.5C, the composition of fossil fuel imports does not alter. Nevertheless, the ToT in the EU regions does not significantly change. (vi) All the EU regions under the low ambition levels experience a remarkable welfare loss. Nevertheless, such a welfare reduction is less significant under the high ambition levels. (vii) In the EEU, the welfare under EU_Full is still significantly higher than that under the REF scenario. In addition, (viii) while EUR under the EU_Full scenario has significantly higher welfare than the REF scenario, the aggregate welfare is slightly lower than that under the EU_EITE. However, the EUR welfare is greater than the EU_EITE under the high ambition levels but still slightly lower than the EU_MIX scenario.

3.4. Policy Scenarios under the WEO Baseline

This section compares the results of policy scenarios using the WEO baseline with the IEO baseline results. The results are presented as percentage change against the IEO baseline results. For the sake of brevity, only selected results are presented under the NDC ambition level.

Figure 10 shows the corresponding percentage changes in CO

2 emission and CO

2 revenues in the EITE, NEIT, and All sectors in the EU regions. In addition,

Figure 11 shows the percentage changes in ToT and welfare in the EU regions. For the comparison, absolute values of absolute CO

2 emissions, CO

2 revenues, ToT, and welfare are compared to get the percentage changes. Therefore, the baselines value and ambition levels are simultaneously taken into account.

Several insights emerge: (i) The absolute emissions under the WEO baseline in all regions in the REF scenario are less than the IEO, even though the NDC ambition levels under the WEO scenario are less ambitious than the IEO scenario for all regions, except for SCA. This is because the baseline emission factor in 2030 under the WEO baseline is less than that under the IEO baseline, except for SCA (see

Figure 3). (ii) The aggregate percentage reduction in NEIT emission in EUR is more than that in the EITE emission in the REF scenario. (iii) Except for SEU and ILI, all the EU regions experience emission reduction in their EITE and NEIT sectors in the REF scenario—EITE emissions in SEU significantly increase, and NEIT emissions in ILI slightly increase. (iv) The emission pattern holds for all regions under all scenarios, except for ILI and SCA, whose total emission under the WEO baseline can be higher than that under the IEO baseline. (v) Due to the substantial increase in REF carbon prices in SCA and ILI, their CO

2 revenues increase. For the rest of the regions, the CO

2 revenues decrease. (vi) In the REF scenario, the ToTs under the WEO baseline are degraded in all regions except BLX and SCA. Nevertheless, (vii) the lower abatement cost dominates the effects, and all EU regions have higher welfare under the WEO baseline than under the IEO baseline. Note that since the percentage changes in welfare are close, the conclusion that the EU regions have more welfare under the EU_MIX scenario than that under the EU_Full holds.

3.5. Additional Scenarios

This subsection presents the results of two different scenarios to help better understand the international trade effects with the policy scenarios in the previous subsection. The scenarios are described in

Table 6.

Figure 12 presents the corresponding percentage changes in CO

2 emission and CO

2 revenues in the EITE, NEIT, and ALL sectors in the EU regions. The results on CO

2 revenues are measured against the REF scenario. In addition,

Figure 13 shows ToT and the percentage change in the welfare in the EU regions.

Several insights emerge concerning the NO_ROW scenario: (i) While the combination of abatement in the EU does not depend on climate policy in other regions, the CO2 revenue reduction reveals that no climate policy in other regions implies a lower carbon price for the EU regions. This is due to the higher import price of fuels. (ii) Only ToT in Germany slightly increases, whereas ToT for the rest of the EU regions decreases. (iii) Due to the reduced cost of achieving the NDC target under No_ROW, most EU regions, except for ILI, experience an improvement in their welfare.

Regarding the No_EUR scenario, the results imply the following: (i) There can be a significant emission leakage to the EU regions due to the lower global price of fossil fuels—the aggregate emission in the EU rises by about 7%. Such leakage is more pronounced in the EITE sectors than in the NEIT. (ii) France, BLX, ILI, SCA, and SEU experience a significant reduction in their ToT compared to the baseline. ToT in Germany and EEU are not greatly affected. (iii) Compared to the baseline, the welfare effect for all the EU regions, except for ILI, is negative.

5. Conclusions

Through the Paris Agreement, individual countries, including European countries, have submitted national pledges of specific reductions in their carbon emissions by 2030, so-called Nationally Determined Contributions (NDCs). These NDCs can be met through different instruments such as carbon pricing and emission trading systems (ETS). The EU has established the world’s first cross-border ETS for greenhouse gas (GHG) emissions, currently covering aviation, emission-intensive sectors, and electricity (EITE).

To achieve the 2030 target, the EU Commission has suggested applying emissions trading in new sectors where sharper mitigations are needed. Under the proposition, emissions from maritime transport will be incorporated into the current EU ETS, while a separate emissions trading system will cover emissions from fuels utilized in road transport and the building sector. In response to the EU Commission’s suggestion, this article presents insights into the merits of alternative design options for greenhouse gas emissions trading in the EU, focusing on variations in the coverage of relevant sectors.

In this study, a multi-regional multi-sectoral CGE model is applied to operate with the option of forming two international emission permit markets simultaneously. Using the GTAP 10 Power data set, the EU region is aggregated into nine regions, including two individual countries (Germany and France) and seven aggregated regions. Then, after forward-calibration of the model based on International Energy Outlook (IEO) and World Energy Outlook (WEO) projections until 2030, marginal abatement cost curves (MACCs) are derived. Moreover, besides the REF scenario in which no region collaborates, three policy scenarios are simulated: (i) EU_EITE as an ETS covering the EITE, mimicking the current EU ETS sectors, (ii) EU_MIX where, in addition to an ETS covering EITE, another ETS covers the sectors other than EITE (NEIT), and (iii) EU_Full, where one ETS covers all sectors. In addition, two different scenarios are simulated where either only the EU or the rest of the model regions implement their climate policy. Each scenario is run for four emission reduction targets, i.e., post-2020 Nationally Determined Contributions (NDC), conditional NDC (NDC+), NDC to meet the 2-degree global average temperature target (NDC-2C), and NDC to meet the 1.5-degree global average temperature target (NDC-1.5C).

The results show that between 44.2% (Germany) and 70.2% (France) of the emissions are made by burning fossil fuels in the NEIT sectors in these regions under the IEO baseline. Emissions by the NEIT sectors are significantly higher under the WEO baseline than under the IEO baseline in all the EU regions, except for South Europe (SEU). Moreover, the results on MACCs indicate that NEIT MACCs are more expensive than EITE MACCs under both baselines. In addition, East Europe (EEU) and Germany have the lowest MACCs among the EU regions, whereas France, BLX, and SCA have the highest MACCs. Additionally, the MACCs under the WEO baseline are slightly higher than under the IEO baseline.

Policy scenarios show that in the REF scenario, more abatement is done via decreasing the emission in the EITE than in the NEIT. In addition, in the EU_EITE scenario, France, BLX, ILI, SCA, and SEU take the emission permit demander position. Hence, EITE emissions in these regions increase, whereas EEU and Germany supply emission permits. Except for Germany, all the participating regions in the emission permit market covering EITE sectors (EU_EITE) gain welfare under NDC, NDC+, and NDC-2C ambition levels. Concerning the EU_MIX scenario, the results show that the common carbon price in the emission permit market covering the NEIT is significantly higher than the common carbon price in the emission permit market covering the EITE. All EU regions gain welfare compared to the REF scenario under the EU_MIX scenario in NDC, NDC+, and NDC-2C—the EU_MIX is stable and self-enforcing. The welfare gain under the EU_MIX in EEU is so significant that its welfare improves significantly beyond its baseline value. The aggregate welfare in the EU further enhances under the EU_MIX scenario against the EU_EITE scenario. Additionally, due to a reduction in coal production, the EU regions become more dependent on importing oil under the EU_Full. Accordingly, the welfare in all EU regions decreases against the EU_MIX. This phenomenon is more significant under the low ambition levels.

Moreover, the results show that the climate policy in other regions does not significantly affect the EU regions’ welfare. Furthermore, the results reveal that baseline choice can affect the results—the CO2 revenues are considerably lower in all EU regions except for ILI and SCA, and welfare in all regions significantly increases using the WEO baseline than the IEO baseline. Nevertheless, the changes in welfare along the different policy scenarios are insignificant, and hence, the results qualitatively hold regardless of the baseline choice.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}