The Impact of COVID-19 on Municipal Food Markets: Resilience or Innovative Attitude?

Abstract

:1. Introduction

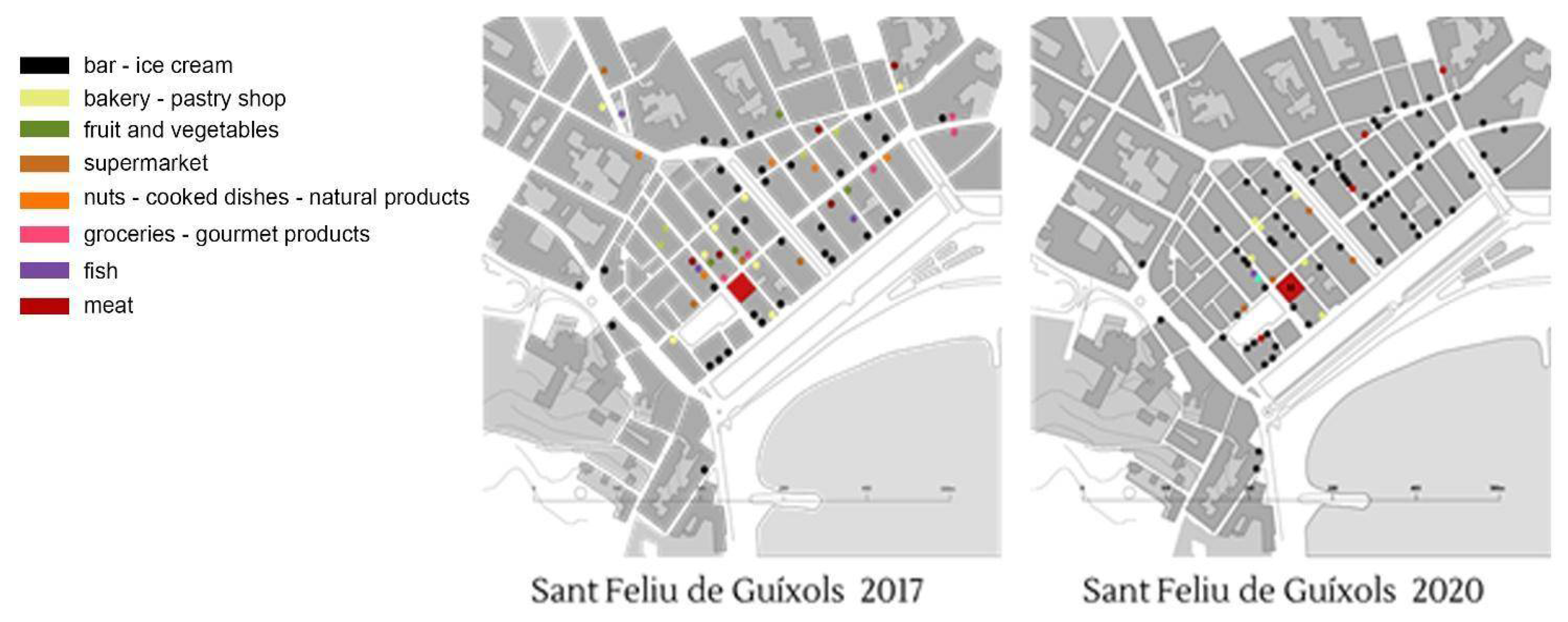

2. Case Study: Sant Feliu de Guíxols

3. Materials and Methods

3.1. Methodology and Data Collection

- -

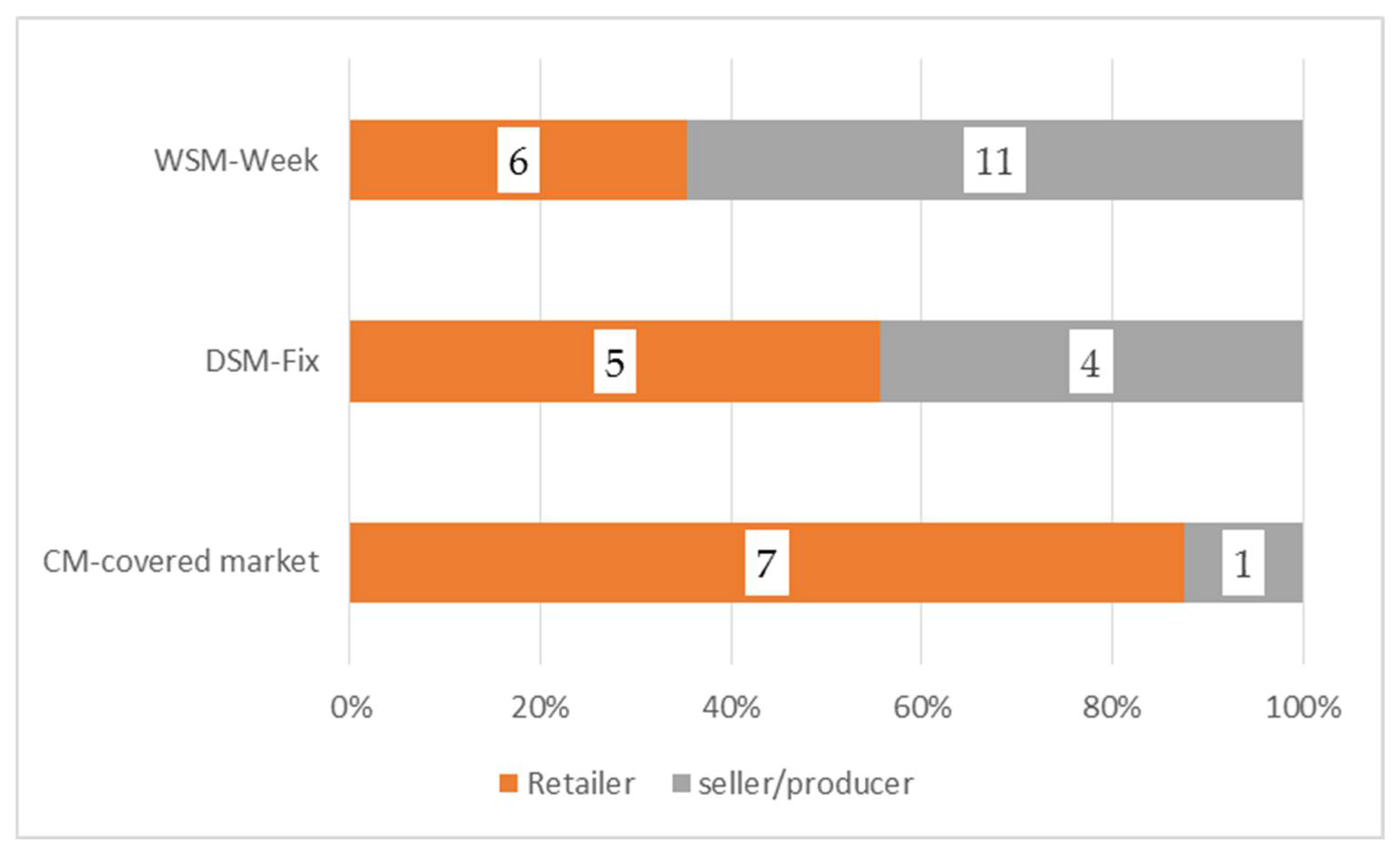

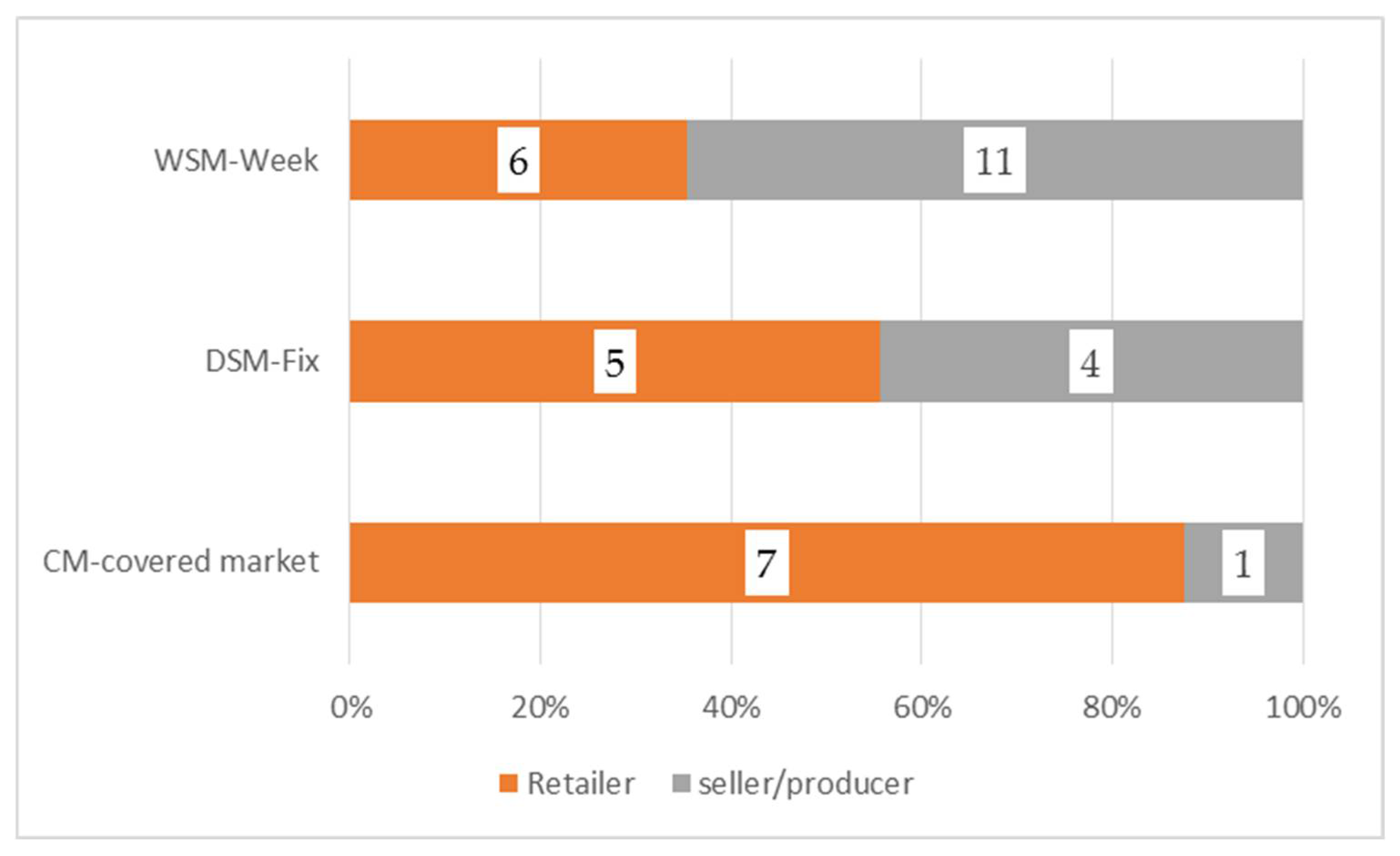

- All 34 vendors present in three markets, namely 16 agricultural seller/producers who sold their products and 18 retailers at their stalls in the three types of market: CM, DSM, and WSM.

- -

- A total of 30 consumers intercepted in the CM, DSM, and WSM. The use of masks and sanitary regulations made it difficult to carry out further face-to-face interviews the time and place of the interviews with sellers and consumers corresponded.

- Participant observation: on-site examination of the food retail urban structure in the central area of the town and in the food markets.

- One-to-one interviews with:

- Food retailers at MM;

- Sellers/producers at MM;

- Consumers at MM.

- The data obtained were processed using quantitative statistical analysis, topological analysis, and qualitative analysis. Most of the processing was done using SPSS version 21.

- -

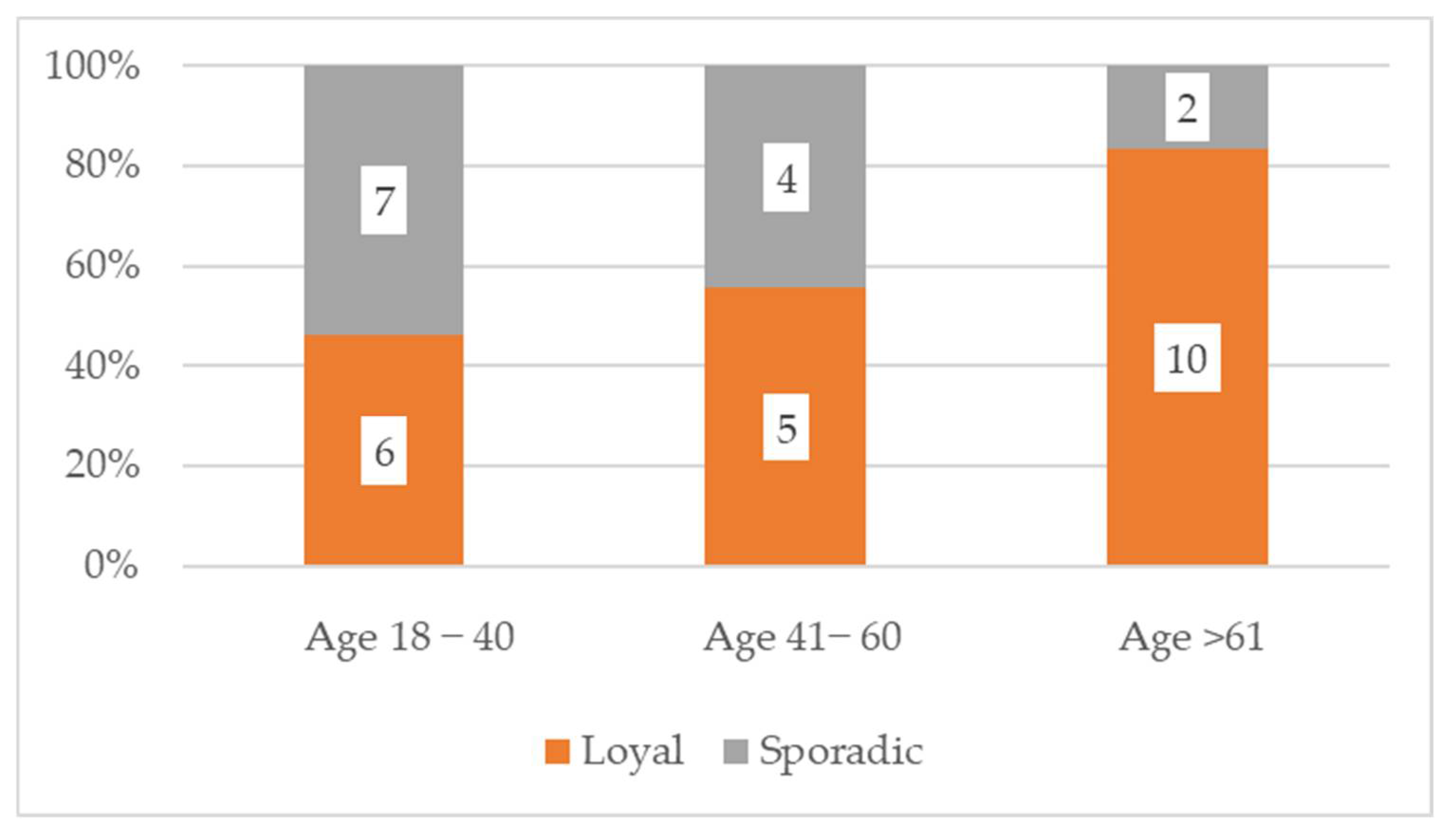

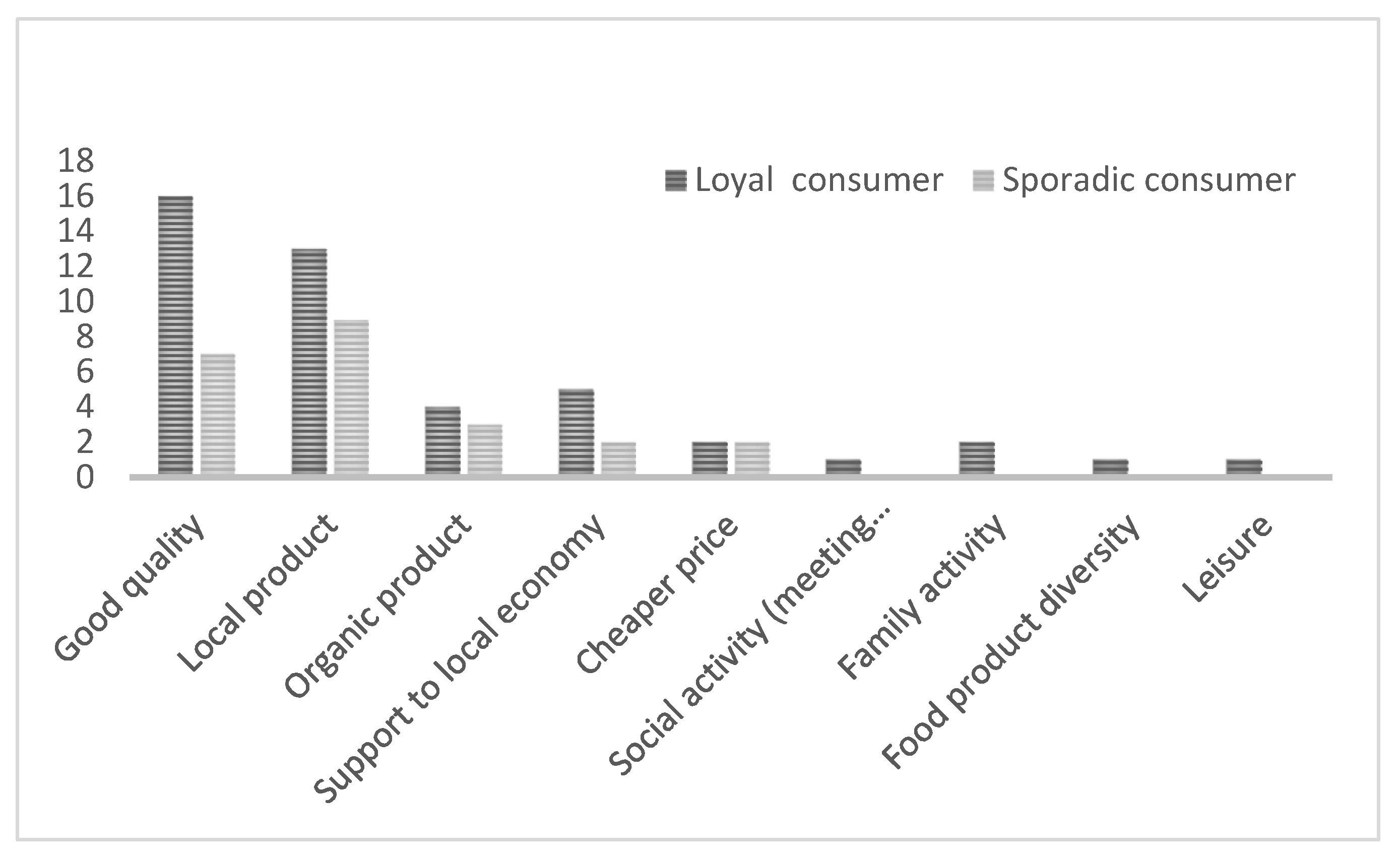

- Changes in users’ food purchasing habits during the COVID-19 lockdown, differentiating between loyal and sporadic customers;

- -

- Changes experienced by vendors during the COVID-19 lockdown, differentiating between sellers/producers and retailers and their abilities to adapt to a changing situation.

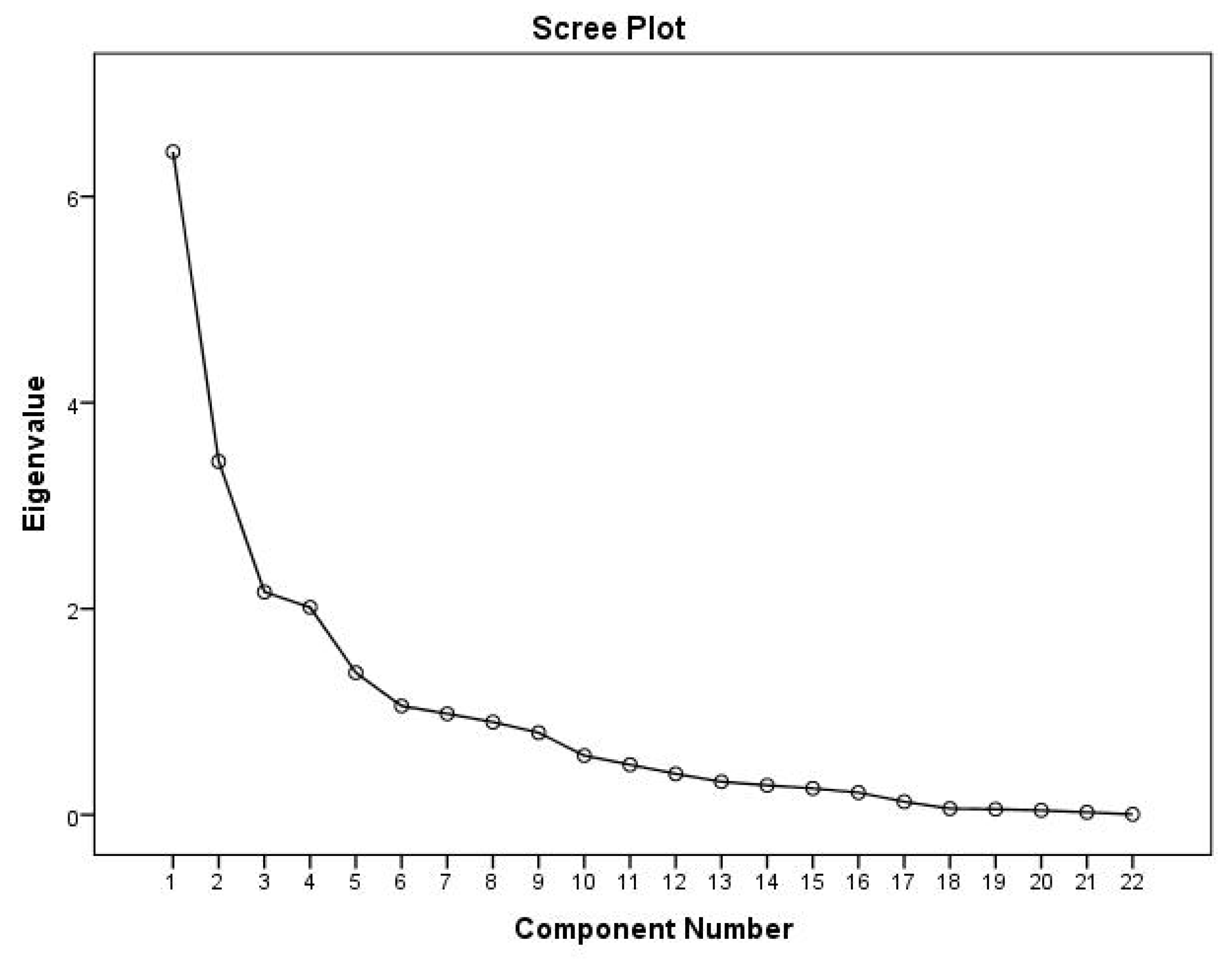

3.2. Factor Analysis and AGIL Model

4. Results

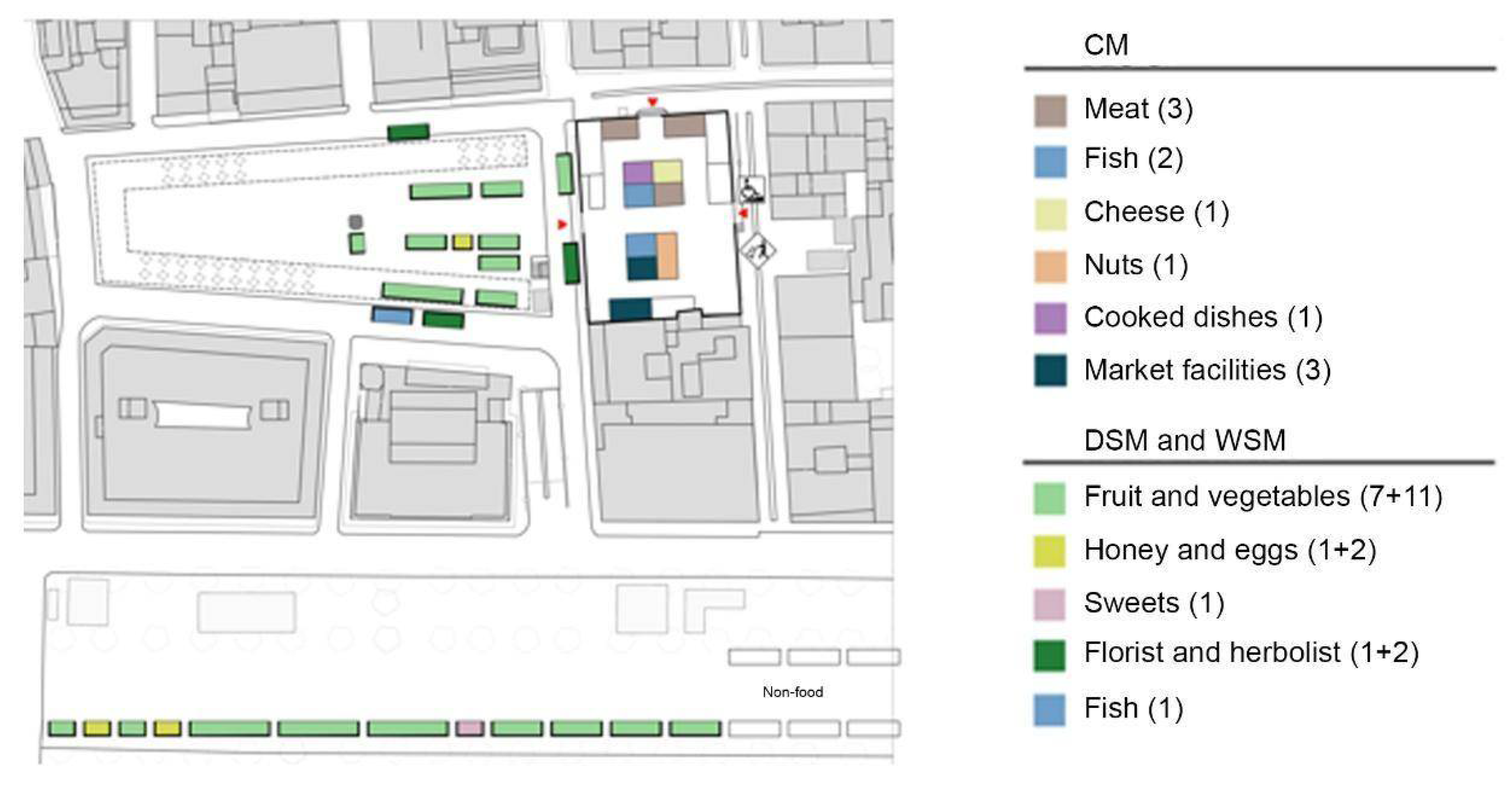

4.1. The Market as a Central Node of the Local City

4.2. Factor Analysis, AGIL Method, and Cluster Analysis

- -

- Adaption (A): This subsystem relates to the ability to adapt to the health emergency resulting from COVID-19 and indicates the possibility of rationalising decision-making processes and finding the solution with the resources available. This aspect is important because it identifies the changes that have occurred due to the pandemic, the sales and new demands of consumers, and security problems.

- -

- Achievement of the goal (G): This subsystem indicates the ability to achieve the goal of the sale. The principle of the realisation of business income follows.

- -

- Integration (I): This subsystem indicates the main characteristics of the sellers in the markets, such as the location of the stalls (CM, DSM, WSM), internal or external, the origin and distance of the products sold, the established habits, and the ability to associate.

- -

- Maintenance of the latent pattern (L): This subsystem captures the corporate culture, with the power of family businesses, the years of activity, the dynamism and presence in different markets, and the loyalty of customers taking on importance.

4.3. Cluster Analysis

- -

- Cluster 1—permanent sellers, attentive and available to the needs of the consumer (61.8%). The sellers in this group were mainly farmers, that is, producers/sellers (57%), the remaining were retailers (43%). The products and food that they sell came from nearby places in 90% of the cases (from distances less than 25 km). Almost all of the sellers have a family business. All subjects in the group stated that they have loyal consumers. They sell seven days a week in San Feliu (76%). The health problem caused by COVID-19 has neither increased sales nor increased the number of loyal consumers. It has definitely not caused changes in sales.

- -

- Cluster 2—occasional regular and open to consumer needs (23.5%). These are mainly sellers/traders, most with a stall in the covered market. In this case, the proximity of products prevails (from distances of less than 25 km). The businesses are family ones. Almost all of them also sell online. They have loyal consumers and all are present at the San Feliu market one to two days a week and also have stalls at other markets. During the COVID-19 lockdown period, some changes in sales occurred. There was an increase in consumers and sales. They stated that they gained some new loyal consumers.

- -

- Cluster 3—occasional regular (14.7%). This small group mainly contains farmers. The products come from areas that are more distant (25 km and up to 90 km). They do not sell online. They only stand at the San Feliu market one two days a week and sell at other markets. Due to COVID-19, they have not increased sales or attracted new consumers. They have not activated any different types of sale and have not registered any changes in requests for product sales.

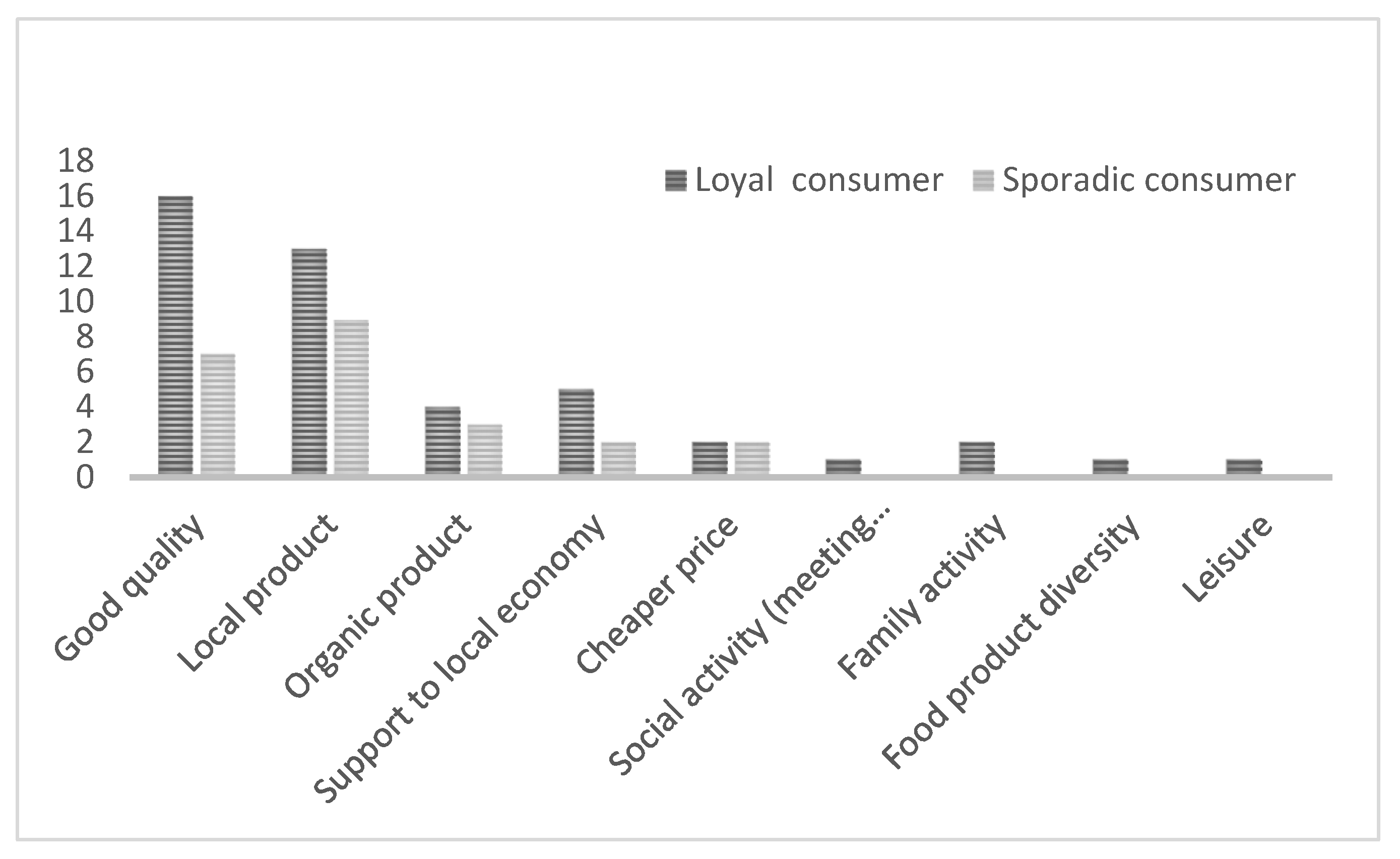

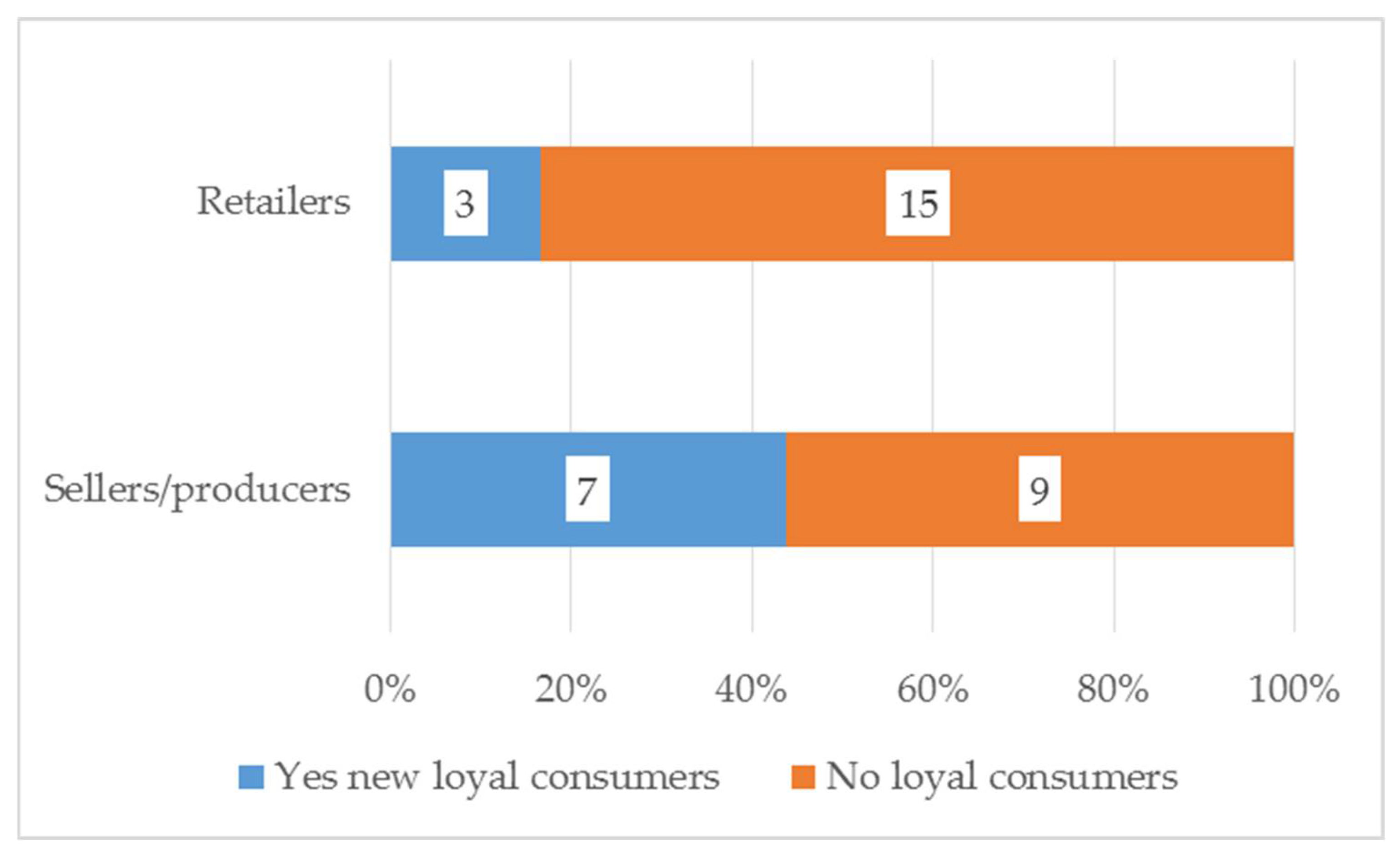

4.4. Loyal Consumers, New Loyalties, and Seller Innovation

5. Discussion

5.1. Adaptation or Transformation of the Food System after Pandemic

5.2. The Possibility of Open Innovation in Food Industry including Restaurant

6. Conclusions

6.1. Theoretical and Practical Implications of this Study

6.2. Limits and Future Research Topics

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix. A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Component | Initial Eigenvalues | Extraction Sums of Squared Loadings | Rotation Sums of Squared Loadings | ||||||

|---|---|---|---|---|---|---|---|---|---|

| Total | % of Variance | Cumulative % | Total | % of Variance | Cumulative % | Total | % of Variance | Cumulative % | |

| 1 | 6.435 | 29.250 | 29.250 | 6.435 | 29.250 | 29.250 | 5.187 | 23.576 | 23.576 |

| 2 | 3.429 | 15.587 | 44.837 | 3.429 | 15.587 | 44.837 | 4.123 | 18.743 | 42.319 |

| 3 | 2.163 | 9.830 | 54.667 | 2.163 | 9.830 | 54.667 | 2.113 | 9.603 | 51.922 |

| 4 | 2.014 | 9.153 | 63.819 | 2.014 | 9.153 | 63.819 | 2.103 | 9.557 | 61.479 |

| 5 | 1.379 | 6.269 | 70.088 | 1.379 | 6.269 | 70.088 | 1.691 | 7.685 | 69.163 |

| 6 | 1.056 | 4.802 | 74.889 | 1.056 | 4.802 | 74.889 | 1.260 | 5.726 | 74.889 |

| 7 | 0.980 | 4.457 | 79.346 | ||||||

| 8 | 0.899 | 4.088 | 83.434 | ||||||

| 9 | 0.796 | 3.620 | 87.055 | ||||||

| 10 | 0.575 | 2.612 | 89.667 | ||||||

| 11 | 0.485 | 2.206 | 91.873 | ||||||

| 12 | 0.397 | 1.805 | 93.679 | ||||||

| 13 | 0.321 | 1.460 | 95.138 | ||||||

| 14 | 0.286 | 1.298 | 96.437 | ||||||

| 15 | 0.256 | 1.164 | 97.601 | ||||||

| 16 | 0.216 | 0.980 | 98.581 | ||||||

| 17 | 0.127 | 0.575 | 99.156 | ||||||

| 18 | 0.060 | 0.273 | 99.429 | ||||||

| 19 | 0.054 | 0.244 | 99.673 | ||||||

| 20 | 0.043 | 0.1195 | 99.868 | ||||||

| 21 | 0.024 | 0.109 | 99.977 | ||||||

| 22 | 0.005 | 0.023 | 100.000 | ||||||

| Factors | |||||||

| 1 | 2 | 3 | 4 | 5 | 6 | ||

| 1 | Place | 0.695 | 0.267 | −0.279 | 0.473 | 0.141 | 0.021 |

| 2 | Market type | 0.878 | −0.083 | −0.144 | 0.391 | 0.088 | 0.034 |

| 3 | Seller/producer | 0.117 | −0.036 | −0.231 | 0.736 | 0.163 | −0.069 |

| 4 | Production place | 0.682 | −0.080 | 0.478 | −0.059 | 0.192 | −0.070 |

| 5 | Distance from the place of production | −0.623 | 0.429 | 0.142 | −0.485 | −0.045 | −0.240 |

| 6 | Years of activity | 0.014 | −0.114 | −0.014 | 0.230 | 0.731 | −0.166 |

| 7 | Family business | 0.112 | 0.275 | 0.733 | −0.118 | 0.071 | 0.094 |

| 8 | Residence of the seller/producer | 0.888 | −0.146 | 0.094 | −0.105 | −0.060 | −0.078 |

| 9 | Distance from the residence | 0.881 | −0.271 | −0.046 | −0.008 | −0.160 | −0.097 |

| 10 | Membership of associations | −0.057 | 0.135 | 0.101 | −0.039 | −0.211 | 0.831 |

| 11 | Product types per food stall | 0.360 | 0.149 | 0.430 | 0.437 | 0.188 | 0.262 |

| 12 | Online distribution | 0.029 | 0.343 | −0.486 | −0.509 | −0.048 | −0.283 |

| 13 | Revenue generated from sales or consumption | 0.137 | 0.062 | 0.267 | 0.550 | −0.113 | −0.392 |

| 14 | Types of loyal customers | −0.470 | −0.097 | −0.165 | 0.023 | 0.684 | 0.013 |

| 15 | Frequency of other markets | 0.354 | 0.251 | −0.739 | 0.011 | 0.042 | 0.085 |

| 16 | Sale in other spaces | −0.850 | 0.303 | 0.002 | −0.222 | 0.058 | −0.008 |

| 17 | Number of days in Sant Feliu market | −0.069 | 0.888 | −0.033 | 0.119 | −0.122 | −0.091 |

| 18 | COVID-19: number of consumers changes | −0.087 | 0.918 | 0.012 | 0.074 | −0.058 | 0.004 |

| 19 | COVID-19: changes in sales | −0.392 | 0.770 | 0.058 | −0.094 | −0.097 | 0.082 |

| 20 | COVID-19: new loyalists | 0.021 | 0.732 | 0.021 | −0.096 | −0.084 | 0.348 |

| 21 | COVID-19: different ways of buying after lockdown | −0.259 | 0.762 | −0.019 | −0.147 | 0.263 | −0.003 |

| 22 | COVID-19: purchase changes after lockdown | 0.187 | 0.061 | 0.289 | −0.063 | 0.598 | −0.039 |

| Questions | Answers |

|---|---|

| Food stall—place | Exterior stall [ ] |

| Interior stall [ ] | |

| Market type | Covered market (CM) [ ] |

| daily street market (DSM) [ ] | |

| weekly street market (WSM) [ ] | |

| Retailer or Seller/producer | Retailer [ ] |

| Seller/producer [ ] | |

| Production place | Sant Feliu de Guíxols [ ] |

| Girona [ ] | |

| Palamos and Calonge [ ] | |

| Llagostera [ ] | |

| Castell d’Aro [ ] | |

| Torrella de Mongri [ ] | |

| Lloret [ ] | |

| Vidreres [ ] | |

| Gaverres [ ] | |

| Palafrugell [ ] | |

| Tossa de Mar [ ] | |

| Roses [ ] | |

| Cassà de la Selva [ ] | |

| Mercat de las Flores [ ] | |

| Distance from the place of production (proximity < 25 km) | 0 km [ ] |

| 1–25 km [ ] | |

| 26–50 km [ ] | |

| over 50 [ ] | |

| Years of activity | Less than 10 years [ ] |

| 11–30 years [ ] | |

| 31–50 years [ ] | |

| 51–100 years [ ] | |

| no reply [ ] | |

| Family business | Family business [ ] |

| not a family business [ ] | |

| Residence of the seller/producer | Sant Feliu de Guíxols [ ] |

| Calonge [ ] | |

| Llagostera [ ] | |

| Girona [ ] | |

| Palamos [ ] | |

| Castell d’Aro [ ] | |

| Cassà de la Selva [ ] | |

| Palafrugell [ ] | |

| Tossa de Mar [ ] | |

| Distance from residence | Residence in Sant Feliu de Guíxols [ ] |

| residence 1–20 km away [ ] | |

| residence 21–50 km away [ ] | |

| residence 51–90 km away [ ] | |

| Membership in associations | Traders’ association [ ] |

| Producers association [ ] | |

| market sellers association [ ] | |

| No [ ] | |

| Products types per food stall | Fish [ ] |

| Meat [ ] | |

| Cheese [ ] | |

| dried food [ ] | |

| vegetables and fruit [ ] | |

| herbs/spices [ ] | |

| wine [ ] | |

| other products [ ] | |

| Online distribution | Yes [ ] |

| No [ ] | |

| Revenue generated from sales or consumption | Revenue generated from sales [ ] |

| Revenue generated from Consumption [ ] | |

| Types of customers | Loyal customers [ ] |

| not loyal customers [ ] | |

| Frequency of other markets | Yes [ ] |

| No [ ] | |

| Sale in other spaces | Yes [ ] |

| No [ ] | |

| Number of days in Sant Feliu market | 1 day [ ] |

| 2 days [ ] | |

| 7 days [ ] | |

| COVID-19: number of consumer changes | Yes consumers increased [ ] |

| No consumers did not increase [ ] | |

| no reply [ ] | |

| COVID-19: changes in sales | Yes sales increased [ ] |

| No sales did not increase [ ] | |

| no reply [ ] | |

| COVID-19: new loyal customers | Yes [ ] |

| No [ ] | |

| no reply [ ] | |

| COVID-19: different ways of buying after lockdown | Face-to-face [ ] |

| Online [ ] | |

| Telephone [ ] | |

| In any case [ ] | |

| no reply [ ] | |

| COVID-19: purchase changes after lockdown | Yes [ ] |

| No [ ] | |

| No reply [ ] |

References

- Bakalis, S.; Valdramidis, V.P.; Argyropoulos, D.; Ahrne, L.; Chen, J.; Cullen, P.J.; Cummins, E.; Datta, A.K.; Emmanouilidis, C.; Foster, T. Perspectives from CO+RE: How COVID-19 changed our food systems and food security paradigms. Curr. Res. Food Sci. 2020, 3, 166–172. [Google Scholar] [CrossRef] [PubMed]

- Bisoffi, S.; Ahrné, L.; Aschemann-Witzel, J.; Báldi, A.; Cuhls, K.; DeClerck, F.; Duncan, J.; Hansen, H.O.; Hudson, R.L.; Kohl, J.; et al. COVID-19 and Sustainable Food Systems: What Should We Learn Before the Next Emergency. Front. Sustain. Food Syst. 2021, 5, 650987. [Google Scholar] [CrossRef]

- Vittuari, M.; Bazzocchi, G.; Blasioli, S.; Cirone, F.; Maggio, A.; Orsini, F.; Penca, J.; Petruzzelli, M.; Specht, K.; Amghar, S.; et al. Envisioning the Future of European Food Systems: Approaches and Research Priorities After COVID-19. Front. Sustain. Food Syst. 2021, 5, 58. [Google Scholar] [CrossRef]

- Galanakis, C.M. The Food Systems in the Era of the Coronavirus (COVID-19) Pandemic Crisis. Foods 2020, 9, 523. [Google Scholar] [CrossRef]

- Marsden, T. Third Natures? Reconstituting Space through Place-making Strategies for Sustainability. Int. J. Sociol. Agric. Food 2012, 19, 257–274. [Google Scholar] [CrossRef]

- Fanzo, J.; Haddad, L.; McLaren, R.; Marshall, Q.; Davis, C.; Herforth, A.; Jones, A.; Beal, T.; Tschirley, D.; Bellows, A.; et al. The Food Systems Dashboard is a new tool to inform better food policy. Nat. Food 2020, 1, 243–246. [Google Scholar] [CrossRef]

- Clapp, J.; Moseley, W.G. This food crisis is different: COVID-19 and the fragility of the neoliberal food security order. J. Peasant Stud. 2020, 47, 1393–1417. [Google Scholar] [CrossRef]

- Picchioni, F.; Po, J.Y.T.; Forsythe, L. Strengthening resilience in response to COVID-19: A call to integrate social reproduction in sustainable food systems. Can. J. Dev. Stud. Rev. Can. Détudes Dév. 2021, 42, 28–36. [Google Scholar] [CrossRef]

- Nicolosi, A.; Fava, N.; Marcianò, C. Consumers’ Preferences for Local Fish Products in Catalonia, Calabria and Sicily. In New Metropolitan Perspectives; Springer: Cham, Switzerland, 2019; pp. 103–112. [Google Scholar] [CrossRef]

- González, S. Contested marketplaces: Retail spaces at the global urban margins. Prog. Hum. Geogr. 2020, 44, 877–897. [Google Scholar] [CrossRef]

- Morales, A. Public Marketplaces Promoting Resilience and Sustainability. Sustainability 2021, 13, 6025. [Google Scholar] [CrossRef]

- Nicolosi, A.; Cortese, L.; Petullà, M.; Laganà, V.R.; Di Gregorio, D.; Privitera, D. Sustainable Attitudes of Local People on the Purchase of Local Food. An Empirical Investigation on Italian Products. In New Metropolitan Perspectives; Springer: Cham, Switzerland, 2021; pp. 45–55. [Google Scholar] [CrossRef]

- Petrović, M.D.; Ledesma, E.; Morales, A.; Radovanović, M.M.; Denda, S. The Analysis of Local Marketplace Business on the Selected Urban Case—Problems and Perspectives. Sustainability 2021, 13, 3446. [Google Scholar] [CrossRef]

- Everts, J.; Jackson, P.; Juraschek, K.A. The socio-material practices of the transformation of urban food markets. Area 2021, 53, 389–397. [Google Scholar] [CrossRef]

- Fava, N. Traditional retailing versus modern retailing in a port city: Barcelona, 1859–1936. Hist. Retail. Consum. 2017, 3, 87–101. [Google Scholar] [CrossRef]

- Fava, N.; Guàrdia, M.; Oyón, J.L. Barcelona food retailing and public markets, 1876–1936. Urban Hist. 2016, 43, 454–475. [Google Scholar] [CrossRef]

- Fedushko, S.; Ustyianovych, T. E-Commerce Customers Behavior Research Using Cohort Analysis: A Case Study of COVID-19. J. Open Innov. Technol. Mark. Complex. 2022, 8, 12. [Google Scholar]

- Galanakis, C.M.; Rizou, M.; Aldawoud, T.M.S.; Ucak, I.; Rowan, N.J. Innovations and technology disruptions in the food sector within the COVID-19 pandemic and post-lockdown era. Trends Food Sci. Technol. 2021, 110, 193–200. [Google Scholar] [CrossRef]

- Hammond, J.; Siegal, K.; Milner, D.; Elimu, E.; Vail, T.; Cathala, P.; Gatera, A.; Karim, A.; Lee, J.E.; Douxchamps, S.; et al. Perceived effects of COVID-19 restrictions on smallholder farmers: Evidence from seven lower- and middle-income countries. Agric. Syst. 2022, 198, 103367. [Google Scholar] [CrossRef]

- Sitaker, M.; Kolodinsky, J.; Wang, W.; Chase, L.C.; Kim, J.V.; Smith, D.; Estrin, H.; Vlaanderen, Z.V.; Greco, L. Evaluation of Farm Fresh Food Boxes: A Hybrid Alternative Food Network Market Innovation. Sustainability 2021, 12, 10460. [Google Scholar] [CrossRef]

- Balińska, A.; Olejniczak, W. Experiences of Polish Tourists Traveling for Leisure Purposes during the COVID-19 Pandemic. Sustainability 2021, 13, 11919. [Google Scholar] [CrossRef]

- Skalkos, D.; Kosma, I.S.; Chasioti, E.; Skendi, A.; Papageorgiou, M.; Guiné, R.P.F. Consumers’ Attitude and Perception toward Traditional Foods of Northwest Greece during the COVID-19 Pandemic. Appl. Sci. 2021, 11, 4080. [Google Scholar] [CrossRef]

- COVID-19-Nutrition-Resources-UNSCN-Feb-2021. Available online: https://www.unscn.org/uploads/web/file/COVID-19-Nutrition-Resources-UNSCN-Feb-2021.pdf (accessed on 20 March 2022).

- EU COVID-19 and Food Safety Question and Answer. Available online: https://ec.europa.eu/food/system/files/2020-04/biosafety_crisis_covid19_qandas_en.pdf (accessed on 25 February 2022).

- Callau-Berenguer, S.; Roca-Torrent, A.; Montasell-Dorda, J.; Ricart, S. How to guarantee food supply during pandemics? Rethinking local food systems from peri-urban strategic agents’ behaviour: The case study of the Barcelona Metropolitan Region. Investig. Geográficas 2022, 77, 363–379. [Google Scholar] [CrossRef]

- Mathew, A.O.; Jha, A.N.; Lingappa, A.K.; Sinha, P. Attitude towards Drone Food Delivery Services—Role of Innovativeness, Perceived Risk, and Green Image. J. Open Innov. Technol. Mark. Complex. 2021, 7, 144. [Google Scholar] [CrossRef]

- Borsellino, V.; Kaliji, S.A.; Schimmenti, E. COVID-19 Drives Consumer Behaviour and Agro-Food Markets towards Healthier and More Sustainable Patterns. Sustainability 2020, 12, 8366. [Google Scholar] [CrossRef]

- Naja, F.; Hamadeh, R. Nutrition amid the COVID-19 pandemic: A multi-level framework for action. Eur. J. Clin. Nutr. 2020, 74, 1117–1121. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Morales, A. Public Markets as Community Development Tools. J. Plan. Educ. Res. 2009, 28, 426–440. [Google Scholar] [CrossRef]

- van der Ploeg, J.D. From biomedical to politico-economic crisis: The food system in times of COVID-19. J. Peasant Stud. 2020, 47, 944–972. [Google Scholar] [CrossRef]

- Sumi, R.S.; Kabir, G. Factors Affecting the Buying Intention of Organic Tea Consumers of Bangladesh. J. Open Innov. Technol. Mark. Complex. 2018, 4, 24. [Google Scholar] [CrossRef] [Green Version]

- Liu, R.; Pieniak, Z.; Verbeke, W. Consumers’ attitudes and behaviour towards safe food in China: A review. Food Control 2013, 33, 93–104. [Google Scholar] [CrossRef]

- Luu, T.T.A.; Baker, J.R. Exploring Consumers’ Purchase Intention of rPET Bottle-Based Apparel in an Emerging Economy. J. Open Innov. Technol. Mark. Complex. 2021, 7, 22. [Google Scholar] [CrossRef]

- Cavallo, C.; Sacchi, G.; Carfora, V. Resilience effects in food consumption behaviour at the time of COVID-19: Perspectives from Italy. Heliyon 2020, 6, e05676. [Google Scholar] [CrossRef]

- Cohen, M.J. Does the COVID-19 outbreak mark the onset of a sustainable consumption transition? Sustain. Sci. Pract. Policy 2020, 16, 1–3. [Google Scholar] [CrossRef]

- Uttama, N.P. Open Innovation and Business Model of Health Food Industry in Asia. J. Open Innov. Technol. Mark. Complex. 2021, 7, 174. [Google Scholar] [CrossRef]

- Moslehpour, M.; Al-Fadly, A.; Ehsanullah, S.; Chong, K.W.; Xuyen, N.T.M.; Tan, L.P. Assessing Financial Risk Spillover and Panic Impact of COVID-19 on European and Vietnam Stock market. Environ. Sci. Pollut. Res. 2022, 29, 28226–28240. [Google Scholar] [CrossRef] [PubMed]

- Jeong, H.; Lee, S.; Shin, K. Development of Food Packaging through TRIZ and the Possibility of Open Innovation. J. Open Innov. Technol. Mark. Complex. 2021, 7, 213. [Google Scholar] [CrossRef]

- Tarra, S.; Mazzocchi, G.; Marino, D. Food System Resilience during COVID-19 Pandemic: The Case of Roman Solidarity Purchasing Groups. Agriculture 2021, 11, 156. [Google Scholar] [CrossRef]

- Zollet, S.; Colombo, L.; De Meo, P.; Marino, D.; McGreevy, S.R.; McKeon, N.; Tarra, S. Towards Territorially Embedded, Equitable and Resilient Food Systems? Insights from Grassroots Responses to COVID-19 in Italy and the City Region of Rome. Sustainability 2021, 13, 2425. [Google Scholar] [CrossRef]

- Ali, S.; Khalid, N.; Javed, H.M.U.; Islam, D.M.Z. Consumer Adoption of Online Food Delivery Ordering (OFDO) Services in Pakistan: The Impact of the COVID-19 Pandemic Situation. J. Open Innov. Technol. Mark. Complex. 2021, 7, 10. [Google Scholar] [CrossRef]

- Degli Esposti, P.; Mortara, A.; Roberti, G. Sharing and Sustainable Consumption in the Era of COVID-19. Sustainability 2021, 13, 1903. [Google Scholar] [CrossRef]

- Fanelli, R.M. Changes in the Food-Related Behaviour of Italian Consumers during the COVID-19 Pandemic. Foods 2021, 10, 169. [Google Scholar] [CrossRef]

- Malenkov, Y.; Kapustina, I.; Kudryavtseva, G.; Shishkin, V.V.; Shishkin, V.I. Digitalization and Strategic Transformation of Retail Chain Stores: Trends, Impacts, Prospects. J. Open Innov. Technol. Mark. Complex. 2021, 7, 108. [Google Scholar] [CrossRef]

- Walker, B.; Gunderson, L.; Kinzig, A.; Folke, C.; Carpenter, S.; Schultz, L. A Handful of Heuristics and Some Propositions for Understanding Resilience in Social-Ecological Systems. Ecol. Soc. 2006, 11, 3. [Google Scholar] [CrossRef]

- Davoudi, S.; Brooks, E.; Mehmood, A. Evolutionary Resilience and Strategies for Climate Adaptation. Plan. Pract. Res. 2013, 28, 307–322. [Google Scholar] [CrossRef] [Green Version]

- Ong, A.K.S.; Cleofas, M.A.; Prasetyo, Y.T.; Chuenyindee, T.; Young, M.N.; Diaz, J.F.; Nadlifatin, R.; Redi, A.A. Consumer Behavior in Clothing Industry and Its Relationship with Open Innovation Dynamics during the COVID-19 Pandemic. J. Open Innov. Technol. Mark. Complex. 2021, 7, 211. [Google Scholar] [CrossRef]

- Moreno, C.; Allam, Z.; Chabaud, D.; Gall, C.; Pratlong, F. Introducing the “15-Minute City”: Sustainability, Resilience and Place Identity in Future Post-Pandemic Cities. Smart Cities 2021, 4, 93–111. [Google Scholar] [CrossRef]

- Chesbrough, H.; Bogers, M. Explicating Open Innovation: Clarifying an Emerging Paradigm for Understanding Innovation; Oxford University Press: Oxford, UK, 2014; p. 37. [Google Scholar]

- Valdez-Juárez, L.E.; Gallardo-Vázquez, D.; Ramos-Escobar, E.A. Online Buyers and Open Innovation: Security, Experience, and Satisfaction. J. Open Innov. Technol. Mark. Complex. 2021, 7, 37. [Google Scholar] [CrossRef]

- Mikheev, A.A.; Krasnov, A.; Griffith, R.; Draganov, M. The Interaction Model within Phygital Environment as an Implementation of the Open Innovation Concept. J. Open Innov. Technol. Mark. Complex. 2021, 7, 114. [Google Scholar] [CrossRef]

- Miralles, I.; Dentoni, D.; Pascucci, S. Understanding the organization of sharing economy in agri-food systems: Evidence from alternative food networks in Valencia. Agric. Hum. Values 2017, 34, 833–854. [Google Scholar] [CrossRef] [Green Version]

- Kassai, M.; Kaspar, J.; Deif, A.; Smith, H. Exploring farmers markets as a temporary cluster to improve local food economy. Br. Food J. 2018, 120, 1844–1858. [Google Scholar] [CrossRef]

- Ruggeri, G.; Mazzocchi, C.; Corsi, S. Urban Gardeners’ Motivations in a Metropolitan City: The Case of Milan. Sustainability 2016, 8, 1099. [Google Scholar] [CrossRef] [Green Version]

- Bernos, T.A.; Travouck, C.; Ramasinoro, N.; Fraser, D.J.; Mathevon, B. What can be learned from fishers’ perceptions for fishery management planning? Case study insights from Sainte-Marie, Madagascar. PLoS ONE 2021, 16, e0259792. [Google Scholar] [CrossRef]

- Gioia, D.A.; Corley, K.G.; Hamilton, A.L. Seeking Qualitative Rigor in Inductive Research: Notes on the Gioia Methodology. Organ. Res. Methods 2013, 16, 15–31. [Google Scholar] [CrossRef]

- Nicolosi, A.; Laganà, V.R.; Di Gregorio, D.; Privitera, D. Social Farming in the Virtuous System of the Circular Economy. An Exploratory Research. Sustainability 2021, 13, 989. [Google Scholar] [CrossRef]

- Onyango, B.; Govindasamy, R.; Alsup-Egbers, C. Uncovering success attributes for direct farmers’ markets and agri-tourism in the Mid-Atlantic region of the United States. Int. Food Agribus. Manag. Rev. 2015, 18, 63–78. Available online: https://bearworks.missouristate.edu/articles-coa/162. (accessed on 25 January 2021).

- Elam, A.; College, B.; Usa, B.P.; Sardana, D. The Potential of Parsons’ Systems Theory for the Study of Entrepreneurship. Front. Entrep. Res. 2008, 28, 12. [Google Scholar]

- Grosso, C.; Signori, P. Analisi multidimensionale della conversazione di marca nei Social Network. In Proceedings of the L’innovazione per la Competitività Delle Imprese, Ancona, Italy, 24–25 October 2013. [Google Scholar] [CrossRef]

- Ingrassia, M.; Altamore, L.; Bacarella, S.; Columba, P.; Chironi, S. The Wine Influencers: Exploring a New Communication Model of Open Innovation for Wine Producers—A Netnographic, Factor and AGIL Analysis. J. Open Innov. Technol. Mark. Complex. 2020, 6, 165. [Google Scholar] [CrossRef]

- Ingrassia, M.; Bellia, C.; Giurdanella, C.; Columba, P.; Chironi, S. Digital Influencers, Food and Tourism—A New Model of Open Innovation for Businesses in the Ho.Re.Ca. Sector. J. Open Innov. Technol. Mark. Complex. 2022, 8, 50. [Google Scholar] [CrossRef]

- Sciulli, D. Parsons, Talcott (1902-79). In International Encyclopedia of the Social & Behavioral Sciences, 2nd ed.; Wright, J.D., Ed.; Elsevier: Amsterdam, The Netherlands, 2015; pp. 520–524. [Google Scholar] [CrossRef]

- Sciortino, G. AGIL, History of. In International Encyclopedia of the Social & Behavioral Sciences, 2nd ed.; Wright, J.D., Ed.; Elsevier: Amsterdam, The Netherlands, 2015; pp. 381–393. [Google Scholar] [CrossRef]

- Parsons, T. An Outline of the Social System; University of Puerto Rico: San Juan, PR, USA, 1961; p. 20. [Google Scholar]

- Megawati, S.; Niswah, F.; Mahdiannur, M.A.; Segara, N.B. A-G-I-L scheme as social system to build characters caring for the environment through the Adiwiyata program. IOP Conf. Ser. Earth Environ. Sci. 2022, 950, 012070. [Google Scholar] [CrossRef]

- Altamore, L.; Bacarella, S.; Columba, P.; Chironi, S.; Ingrassia, M. The Italian Consumers’ Preferences for Pasta: Does Environment Matter? Chem. Eng. Trans. 2017, 58, 859–864. [Google Scholar] [CrossRef]

- Chironi, S.; Altamore, L.; Columba, P.; Bacarella, S.; Ingrassia, M. Study of Wine Producers’ Marketing Communication in Extreme Territories–Application of the AGIL Scheme to Wineries’ Website Features. Agronomy 2020, 10, 721. [Google Scholar] [CrossRef]

- Matsunaga, M. How to factor-analyze your data right: Do’s, don’ts, and how-to’s. Int. J. Psychol. Res. 2010, 3, 97–110. [Google Scholar] [CrossRef]

- Comrey, A.L.; Lee, H.B. A First Course in Factor Analysis, 2nd ed.; Lawrence Erlbaum Associates Inc.: Hillsdale, NJ, USA, 1992; pp. xii, 430. [Google Scholar]

- Lever, J.; Sonnino, R.; Cheetham, F. Reconfiguring local food governance in an age of austerity: Towards a place-based approach? J. Rural Stud. 2019, 69, 97–105. [Google Scholar] [CrossRef]

- Ihle, R.; Rubin, O.D.; Bar-Nahum, Z.; Jongeneel, R. Imperfect food markets in times of crisis: Economic consequences of supply chain disruptions and fragmentation for local market power and urban vulnerability. Food Secur. 2020, 12, 727–734. [Google Scholar] [CrossRef] [PubMed]

- Mengual-Recuerda, A.; Tur-Viñes, V.; Juárez-Varón, D.; Alarcón-Valero, F. Emotional Impact of Dishes versus Wines on Restaurant Diners: From Haute Cuisine Open Innovation. J. Open Innov. Technol. Mark. Complex. 2021, 7, 96. [Google Scholar] [CrossRef]

- Najib, M.; Ermawati, W.J.; Fahma, F.; Endri, E.; Suhartanto, D. FinTech in the Small Food Business and Its Relation with Open Innovation. J. Open Innov. Technol. Mark. Complex. 2021, 7, 88. [Google Scholar] [CrossRef]

- Morkunas, M.; Rudienė, E. The Impact of Social Servicescape Factors on Customers’ Satisfaction and Repurchase Intentions in Mid-Range Restaurants in Baltic States. J. Open Innov. Technol. Mark. Complex. 2020, 6, 77. [Google Scholar] [CrossRef]

- Arrigo, E. Open Innovation and Market Orientation: An Analysis of the Relationship. J. Knowl. Econ. 2018, 9, 150–161. [Google Scholar] [CrossRef]

- Mahdad, M.; Hasanov, M.; Isakhanyan, G.; Dolfsma, W. A smart web of firms, farms and internet of things (IOT): Enabling collaboration-based business models in the agri-food industry. Br. Food J. 2020, 3–5. [Google Scholar] [CrossRef]

- Solarte-Montufar, J.G.; Zartha-Sossa, J.W.; Osorio-Mora, O. Open Innovation in the Agri-Food Sector: Perspectives from a Systematic Literature Review and a Structured Survey in MSMEs. J. Open Innov. Technol. Mark. Complex. 2021, 7, 161. [Google Scholar] [CrossRef]

- Obradović, T.; Vlačić, B.; Dabić, M. Open innovation in the manufacturing industry: A review and research agenda. Technovation 2021, 102, 102221. [Google Scholar] [CrossRef]

- Paiva, T.; Ribeiro, M.; Coutinho, P. R&D Collaboration, Competitiveness Development, and Open Innovation in R&D. J. Open Innov. Technol. Mark. Complex. 2020, 6, 116. [Google Scholar] [CrossRef]

- Yun, J.J.; Park, K.; Gaudio, G.D.; Corte, V.D. Open innovation ecosystems of restaurants: Geographical economics of successful restaurants from three cities. Eur. Plan. Stud. 2020, 28, 2348–2367. [Google Scholar] [CrossRef]

- Klimek, M.; Bingen, J.; Freyer, B.; Paxton, R. From Schnitzel to Sustainability: Shifting Values at Vienna’s Urban Farmers Markets. Sustainability 2021, 13, 8327. [Google Scholar] [CrossRef]

- Di Gregorio, D.; Guida, A.; Laganà, V.R.; Cannavò, S.; Nicolosi, A. Eventos agroalimentarios y de productos típicos: Instrumentos de promoción para un territorio del sur de Italia. Pirineos 2022, 177, e069. [Google Scholar] [CrossRef]

| Variable n. | Variable Name | Description | Modalities |

|---|---|---|---|

| V1 | Food stall—place | Exterior stall, Interior stall | 1–2 |

| V2 | Market type | Covered market (CM), daily street market (DSM), weekly street market (WSM) | 1–3 |

| V3 | Retailer or Seller/producer | Retailer, Seller/producer | 1–2 |

| V4 | Production place | Sant Feliu de Guíxols, Girona, Palamos and Calonge, Llagostera, Castell d’Aro, Torrella de Mongri, More places (Lloret, Vidreres, Gaverres, Palafrugell, Tossa de Mar, Roses, Cassà de la Selva, Mercat de las Flores) | 1–7 |

| V5 | Distance from the place of production (proximity < 25 km) | 0 km, 1–25 km, 26–50 km, over 50 | 1–4 |

| V6 | Years of activity | Less than 10 years, 11–30 years, 31–50 years, 51–100 years, no reply | 1–5 |

| V7 | Family business | Family business, not a family business | 1–2 |

| V8 | Residence of the seller/producer | Sant Feliu de Guíxols, other places (Calonge, Llagostera, Girona, Palamos, Castell d’Aro, Cassà de la Selva, Palafrugell, Tossa de Mar) | 1–2 |

| V9 | Distance from residence | Residence in Sant Feliu de Guíxols, residence 1–20 km away, residence 21–50 km away, residence 51–90 km away | 1–4 |

| V10 | Membership in associations | Traders’ association, producers, market sellers, No | 1–4 |

| V11 | Products types per food stall | Fish, meat, cheese, dried food, vegetables and fruit, herbs/spices, wine, other products | 1–8 |

| V12 | Online distribution | Yes, No | 1–2 |

| V13 | Revenue generated from sales or consumption | Consumption, sales | 1–2 |

| V14 | Types of customers | Loyal customers, not loyal customers | 1–2 |

| V15 | Frequency of other markets | Yes, No | 1–2 |

| V16 | Sale in other spaces | Yes, No | 1–2 |

| V17 | Number of days in Sant Feliu market | 1 day, 2 days, 7 days | 1–3 |

| V18 | COVID-19: number of consumer changes | Yes consumers increased, No consumers did not increase, no reply | 1–3 |

| V19 | COVID-19: changes in sales | Yes sales increased, No sales did not increase, no reply | 1–3 |

| V20 | COVID-19: new loyal customers | Yes, No, no reply | 1–3 |

| V21 | COVID-19: different ways of buying after lockdown | +Face-to-face, +Online, +Telephone, In any case, no reply | 1–5 |

| V22 | COVID-19: purchase changes after lockdown | Yes, No, No reply | 1–3 |

| Sant Feliu de Guixols 2017 | Sant Feliu de Guixols 2020 | |||

|---|---|---|---|---|

| n. | % | n. | % | |

| Meat | 5 | 7.4 | 5 | 5.4 |

| Fish | 3 | 4.4 | 1 | 1.1 |

| Fruit and vegetable | 4 | 5.9 | 1 | 1.1 |

| Bakery | 6 | 8.8 | 3 | 3.3 |

| Patissery | 2 | 2.9 | 3 | 3.3 |

| Gourmet | 4 | 5.9 | 1 | 1.1 |

| Food store | 1 | 1.5 | 6 | 6.5 |

| Organic product | 1 | 1.5 | - | - |

| Dry fruits and sweet | 1 | 1.5 | - | - |

| Deli | 3 | 4.4 | 1 | 1.1 |

| Ice-cream | 1 | 1.5 | - | - |

| Bar-restaurant | 33 | 48.5 | 67 | 72.8 |

| Supermarket (>400 mq) | 4 | 5.9 | 4 | 4.3 |

| Total food retailing | 68 | 100.0 | 92 | 100.0 |

| Factors | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| Mean | Std. Deviation | 1 | 2 | 3 | 4 | 5 | 6 | ||

| 1 | Place | 1.76 | 0.43 | 0.695 | |||||

| 2 | Market type | 2.26 | 0.83 | 0.878 | |||||

| 3 | Seller/producer | 1.47 | 0.51 | 0.736 | |||||

| 4 | Production place | 7.76 | 70.12 | 0.682 | |||||

| 5 | Distance from the place of production | 3.23 | 10.74 | −0.623 | |||||

| 6 | Years of activity | 2.94 | 10.61 | 0.731 | |||||

| 7 | Family business | 1.12 | 0.41 | 0.733 | |||||

| 8 | Residence of the seller/producer | 5.06 | 40.99 | 0.888 | |||||

| 9 | Distance from the residence | 1.74 | 0.83 | 0.881 | |||||

| 10 | Membership of associations | 3.59 | 0.96 | 0.831 | |||||

| 11 | Product types per food stall | 5.91 | 30.19 | 0.437 | |||||

| 12 | Online distribution | 1.47 | 0.51 | -0.509 | |||||

| 13 | Revenue generated from sales or consumption | 1.97 | 0.17 | 0.550 | |||||

| 14 | Types of loyal customers | 1.09 | 0.29 | 0.684 | |||||

| 15 | Frequency of other markets | 1.56 | 0.50 | -0.739 | |||||

| 16 | Sale in other spaces | 1.76 | 0.43 | −0.850 | |||||

| 17 | Number of days in Sant Feliu market | 2.00 | 0.98 | 0.888 | |||||

| 18 | COVID-19: number of consumers changes | 2.00 | 0.65 | 0.918 | |||||

| 19 | COVID-19: changes in sales | 1.97 | 0.67 | 0.770 | |||||

| 20 | COVID-19: new loyalists | 1.91 | 0.71 | 0.732 | |||||

| 21 | COVID-19: different ways of buying after lockdown | 3.65 | 10.07 | 0.762 | |||||

| 22 | COVID-19: purchase changes after lockdown | 1.88 | 0.73 | 0.598 | |||||

| Percent of total variance explained | 23.6% | 18.7% | 9.6% | 9.6% | 7.7% | 5.7% | |||

| Total variance explained by Factors 1–6 = 74.9% | |||||||||

| GOAL ATTAINMENT (G) Subsystem—Management the system defines the goals achievement: Power, ability to reach the sales target despite COVID-19 Variables:

| ADAPTATION (A) Subsystem—Ability to adapt to the health emergency from COVID-19 Variables:

|

| INTEGRATION (I) Subsystem—Community Power of established habits and the ability to associate Variables:

| LATENT PATTERN MAINTENANCE (L) Subsystem—Corporate culture Power of family businesses Variables:

|

| Factor Extracts | Variance Explained in Each Factor (%) | Action System and Subsystem | Significance of Action System (%) | Meaning of AGIL Action System in the Resilience/Resistance Model |

|---|---|---|---|---|

| Factor extract 2 Effectiveness of adaptation | 18.743 | Adaptation (A) Capacity to adapt to the COVID-19 health emergency | 25.028 | Different ways of selling after lockdown, ability to change |

| Factor extract 4 Effectiveness of the sale | 9.557 | Goal Attainment (G) Ability to achieve the goal of the sale | 12.762 | Online networks, diversification (increase in product types per food stall) |

| Factor extract 1 + 6 Effectiveness of habits. Propension to association | 29.302 | Integration (I) Power of established habits. Associations consolidated | 39.127 | value attributed to the place of origin of the products |

| Factor extract 3 + 5 Effectiveness of family businesses, attendance in other markets | 17.288 | Latency (L) Power of family businesses | 23.085 | Attractiveness of local markets and family business |

| Total | 74.889 | AGIL | 100.000 |

| Application of Innovations | |||

|---|---|---|---|

| Yes | No | Total | |

| Sellers/producers | 32.3% (n° 11) | 14.7% (n° 5) | 47.1% (n° 16) |

| Retailers | 29.4% (n° 10) | 23.5% (n° 8) | 52.9%(n° 18) |

| Total | 61.7% (n° 21) | 38.2% (n° 13) | 100.0 (n° 34) |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Fava, N.; Laganà, V.R.; Nicolosi, A. The Impact of COVID-19 on Municipal Food Markets: Resilience or Innovative Attitude? J. Open Innov. Technol. Mark. Complex. 2022, 8, 87. https://doi.org/10.3390/joitmc8020087

Fava N, Laganà VR, Nicolosi A. The Impact of COVID-19 on Municipal Food Markets: Resilience or Innovative Attitude? Journal of Open Innovation: Technology, Market, and Complexity. 2022; 8(2):87. https://doi.org/10.3390/joitmc8020087

Chicago/Turabian StyleFava, Nadia, Valentina Rosa Laganà, and Agata Nicolosi. 2022. "The Impact of COVID-19 on Municipal Food Markets: Resilience or Innovative Attitude?" Journal of Open Innovation: Technology, Market, and Complexity 8, no. 2: 87. https://doi.org/10.3390/joitmc8020087

APA StyleFava, N., Laganà, V. R., & Nicolosi, A. (2022). The Impact of COVID-19 on Municipal Food Markets: Resilience or Innovative Attitude? Journal of Open Innovation: Technology, Market, and Complexity, 8(2), 87. https://doi.org/10.3390/joitmc8020087