Abstract

Novel Coronavirus, also known as COVID-19, is a health emergency that is having an ever-growing impact on the global economy. COVID-19 has caused economic disruption at an unprecedented speed and scale. The economic costs it will bring to society can only be measured in times to come. Millions of people across the globe have already become unemployed, and similarly, millions of businesses have either shut down or are on the verge of collapse. It is a great challenge for policymakers to minimize the economic impact of COVID-19 and put the economy on a growth trajectory once again. Unfortunately, there is so far no country in the world that can be viewed as a role model for its economic response to the COVID-19 pandemic. The present study proposes Islamic finance as a potential tool to help affected economies safely pass through the economic crisis resulting from the pandemic. This study identifies a four-stage COVID-19 model and proposes ten innovative Islamic financial services for each stage of the pandemic. In addition, it analyzes how these services can be effectively utilized at different stages to overcome the economic damage caused by the pandemic.

1. Introduction and Research Question

The COVID-19 pandemic, which started in Wuhan, China, has already infected more than 113 million people and has tragically taken the lives of more than 2.5 million individuals as of 12 January 2021 [1,2]. This infectious disease, which began as a health emergency and gradually became pervasive, has become one of the most influential economic stressors in modern history. Initially, governments and various authorities struggled to control the spread of infection and the resultant deaths due to the COVID-19 pandemic [3]. Various measures were applied to curb the spread of the virus, with many governments resorting to the sealing of national and international borders along with strict lockdowns. Currently, authorities are trying to reduce the spread of the pandemic by vaccinating frontline workers, elderly citizens and ultimately all segments of the population [4,5]. However, lockdowns have only partially been successful in controlling the spread of the virus [6,7,8]. Many experts are of the view that there is a need to extend lockdowns to 12 months or more to minimize the spread of the virus [9,10]. While the greatest loss is in the form of human lives, the associated economic losses are also devastating [11,12,13]. The tragic loss of lives is followed by the dejection of the loss of livelihood, as the biggest health crisis of the world has turned into a long economic slowdown [14]. The World Economic Outlook of the International Monetary Fund estimates that the global GDP could suffer a cumulative loss of well over $9 trillion over 2020–2021 [15]. On one hand, huge sums are being spent treating infected persons and sanitizing infected places; on the other hand, economic losses are accumulating due to suspended economic activities owing to lockdowns and the fear of the spread of infection. Undoubtedly, both lockdown and loss of human lives will have long-lasting consequences [16].

The world economy has already injected more than $5 trillion as a bailout and liquidity booster to negate the strength of the crisis [17]. The potential economic consequences of the current crisis are larger than any other crisis seen in recorded history [18]. There is still time for global policymakers to have a well-coordinated reaction to the pandemic and the associated economic impact [19]. After World War II, the unemployment rate increased by 2 percent due to the subsequent recession [20,21]. However, the scenario now is completely different from the situation prevailing after World War II. Comparison of the two situations can be dangerous and can lead to errors. The current crisis looks far worse because of shocks to both demand and supply as well as the limited economic tools available to eliminate the economic consequences [22]. Though governments have announced stimulus packages, there is very little room for these packages to handle damages of such a vast magnitude [23]. There is ample literature on the COVID-19 pandemic that discusses the magnitude of the economic crisis [12] and the resultant increase in unemployment, poverty and child labor [8,11,24]. However, few discuss the ways to tackle the crisis. There is a call for a new tool that can help to minimize and mitigate the severity of such a crisis [25]. The conventional financial system, which could not withstand the financial crisis of 2007–2008, a far less severe situation than the present global health and economic crisis, is grossly unprepared and inadequate to rescue the world from the present economic doom [26,27,28]. It is with this backdrop that Islamic finance could be harnessed to tackle the present economic crisis [29,30,31]. The principles of Islamic finance promote risk-sharing; prohibit riba-based transactions, which are a burden for the poor and the needy; and restrict short sales, deception, risk (Gharar) and gambling (Qimar). This ultimately leads to a greater discipline and stability in the financial system [32].

The objective of this article is to explore the insights of the economic crisis due to COVID-19 and propose alternative financial crisis management strategies considering Islamic principles. This study is intended to examine different Islamic financial services by identifying four different stages of economic situations resulting from the pandemic. Therefore, this study focuses on the core Islamic principles that are mandatory for Muslims, like Zakah (Islamic tax) [33] and various other Islamic financial services, to possibly reduce the economic losses due to the pandemic [34,35]. This research also proposes a suitable model to emphasize the approach and its stages.

COVID-19—the major health crisis that began in Wuhan (China) and was later declared a global pandemic by the World Health Organization (WHO)—has transformed into one of the worst economic crises of all time. The impact of the crisis is visible everywhere in the world, from migrant labor problems in India [36] to an increase in the number of the newly unemployed in the United States [37], and to the shutting down of the industries in the Gulf Cooperation Council [38]. Unfortunately, no country in the world so far can be viewed as a role model for its economic response to the pandemic [39]. The year 2020 started with the fear of diplomatic crisis between the USA and Iran and became packed with unmatched events that created a high level of uncertainty [40]. The major highlights of the economic crisis witnessed by the world within only a few months due to the pandemic are presented below.

- i

- Sudden lockdowns in many economies, leading to unemployment and shutting down of businesses and adding to the miseries of migrant laborers in particular.

- ii

- A steep fall in equity markets across the globe.

- iii

- Liquidity problems in banks and other financial institutions.

- iv

- The injection of more than $5 trillion by the governments as part of economic stimulus packages to promote liquidity and revive the economy.

- v

- An all-time dip in oil prices.

- vi

- Aggressive monetary policy interventions by the central banks to increase liquidity and to bring back normalcy in the financial markets.

- vii

- Volatility in the cryptocurrency market.

This paper proceeds as follows. In the next section, we provide an extensive review of the literature related to Islamic finance, Islamic financial systems and the scope of the Islamic financial system as the natural financial system to be used to address financial distress. Section 3 explains the methodology employed in the study. Section 4 presents the results and analysis of the proposed model, while Section 5 presents discussion and conclusions.

2. Literature Review and Research Framework

2.1. Islamic Finance

Islamic finance is based on the objectives of removing income inequality and bringing social justice. It cannot be achieved unless all institutions including the financial system contribute positively towards it [41,42]. One of the ways through which these ideals can be achieved is by bringing moral values into society in all facets of human life, including social, political and economic endeavors. This will help humans get rid of greed and self-indulgence, which has made them absorbed in self-satisfaction and accumulation of wealth as the measure of success and achievement [43]. To contribute towards the creation of a just and equitable society, the financial system must promote the fair distribution of income besides being a strong and stable system that can be relied upon. Even though the Islamic financial system has been adopted recently and is still evolving, it has enjoyed a steady, consistent growth during the last decade after the global financial crisis. Being able to withstand the test of time and remain profitable even during and after the crisis has established Islamic finance as a sustainable financial system [44,45].

There is consensus among scholars, economists and financial researchers about the size and magnitude of the current pandemic and its economic consequences [46]. Thus far, the “solution” to the economic damage of the current crisis seems to be far away. Several governments have already announced stimulus packages that neither present long-term solutions to the existing problem nor prepare the present system to mitigate similar crises in the future. While economists all around the world are searching for the solution and devising strategies to deal with the crisis, the aim of the current study is to reintroduce an alternative financial system that has the capability of limiting if not eliminating the economic impact of the pandemic and bringing stability into markets [47,48]. The study concludes that the current pandemic has presented the Islamic financial system an opportunity to validate its significance.

2.2. Islamic Financial System

Several Islamic scholars are of the opinion that Islamic finance is not only capable of fighting the economic consequences of the pandemic like this but that it also has the potential to emerge as an alternative financial system and can challenge the conventional financial system [49,50]. After the financial meltdown of 2008, the current pandemic has provided another opportunity for Islamic finance to prove its potential and shine [51]. The Islamic financial system is based on the principles of risk-sharing, ethics and morality, which equip it to act as a potential warrior to safeguard the interest of the poor and vulnerable under crisis [52]. The importance of Islamic finance can be understood in terms of how it strives to achieve the ideals of equal distribution of income and socio-economic justice [53]. There are specialized Islamic microfinance institutions that provide affordable finance to micro-entrepreneurs and the poor to increase their income, wealth and standard of living [54]. One of the objectives of Islamic finance is to provide an ethical alternative to the world, especially to Muslims [32]. Islamic finance does not support unethical trading practices such as betting, trading in alcohol and pornography, etc. It is not that Islamic finance was not affected during the global financial crisis of 2008; rather, it was certainly less impacted as compared to its conventional counterpart [55]. Similarly, during the present global economic crisis, owing to its intrinsic strength vis-à-vis the conventional finance system, Islamic finance has a lot to offer.

The above claims by contemporary Islamic scholars are based on the following theories of Islamic finance.

- i

- The first and foremost theory behind Islamic finance is the principle of equality and social justice. Islamic finance derives this from the fundamental values of Islam, which believes in fairness, equality, socio-economic justice and everlasting commitment to the safety and security of future generations by preserving the environment and caring for the valuable resources of the earth [56].

- ii

- Islamic finance believes in wealth distribution, not in wealth accumulation. Some of the financial products such as Sadaqa, Zakat and Qardh-Al-Hasan are examples that show that Islamic finance believes in preserving the rights of the poor by promoting the distribution of excess income by the rich [57].

- iii

- Islamic finance is based on the equity mode of financing rather than the debt mode of financing. The transactions are asset-backed based on commodity trading. Financial products such as bonds are declared Haram because they exploit the debtor. Islam is a complete code of life, and it preaches justice and fairness in every facet of life. It guides Muslims to live within their financial resources and prohibits them from indulging in transactions that are beyond their reach [58].

- iv

- Islamic finance is about risk-sharing and not about risk-taking. Islamic finance promotes risk-sharing and avoids putting undue risk on only one party. The relationship between the parties involved is based on honesty and transparency [59].

- v

- Islamic finance provides safe, socially responsible and ethical investment options to investors. It is not that Islamic finance is fraud-proof and that Muslims are not engaged in unethical trade practices. Rather, the Islamic finance principles are designed in such a way that they minimize the possibility of fraud and unethical practices [60].

In this context, is Islamic finance good enough during a situation like the economic crisis created by the current pandemic? The performance of Islamic financial institutions during and after the global financial crisis suggests so, and it can be interpreted as the vote of confidence in favor of Islamic finance [61,62]. The COVID-19 pandemic has certainly provided another opportunity to the Islamic financial system to emerge as a savior of the poor and affected by providing ethical financial services. This also gives an opportunity for the Islamic financial institutions to emerge as a strong contender to the conventional financial system. Of course, these opportunities are not without challenges. The next section describes various financial services that can be utilized at different stages of the pandemic to assist in the recovery of individuals and institutions.

2.3. Islamic Finance as a Natural Financial System in Fight against the Disaster

During the initial days of Islam, trading practices were based on participation and profit- and loss-sharing. Interest-based transactions were strictly prohibited because interest payment was considered to be the exploitation of the poor by the rich [63]. However, the situation began to change even in the Muslim countries and among the Muslim communities in the fifth century when interest-based transactions started dominating the finance world by replacing profit- and loss-sharing with interest and guaranteed profit [64]. The practice of profit and loss sharing was again revived in the twentieth century, and Islamic finance started to emerge in the form of a small cottage industry in Arab countries in the late 1970s. Islamic finance is different from conventional finance as it derives its principles from the Qura’an (words of Allah) and Sunnah (Hadith of the Prophet Muhammad ﷺ) [65,66].

To be consistent with the principles of sharia, Islamic financial institutions are not allowed to do certain things, such as [67,68],

- i

- To pay or receive interest (premium paid by the borrower to the lender).

- ii

- To buy and sell illegal and certain non-Islamic products such as alcohol, pork, non-certified meat and poultry and any product made of alcohol or haram animal fats.

- iii

- Transactions that lead to Gharar—Gharar literally means transactions that are highly uncertain and that may result in fraud or deception. The conventional finance-based derivatives products, such as options, futures and forward contracts, come under Gharar and are prohibited under sharia law.

- iv

- Maysir, which refers to transactions that are dependent on the occurrence of certain specific events.

- v

- Transactions that are not linked with underlying assets, such as bonds, conventional loans, etc.

- vi

- Charging extra money for late payment of a deferred transaction.

During the last four decades, many sharia-compliant financial products and services have been introduced all around the globe by Islamic financial institutions [69,70,71]. These products have been introduced in areas of consumer finance, investment banking, financing of poor and needy, venture capital and SME financing [72,73]. These products and services offered by the Islamic financial institutions are equity-based modes of financing, such as Musharakah, Diminishing Musharaka and Mudrabaha, and asset-backed financing, such as Murabaha, Ijarah, Istisna, Salam and Istisna [74,75]. Some other popular financial services include Qardh-Al-Hasan, Bay-Al-Sarf and Agency.

2.4. Research Framework: The Four-Stage Economic Impact of the COVID-19 Pandemic

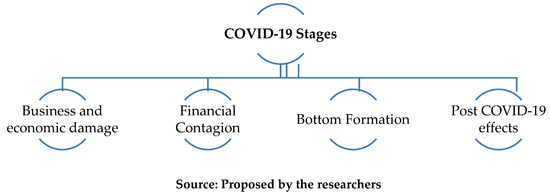

Epidemiologists across the globe are still figuring out the different stages of the COVID-19 pandemic, while economists are estimating the associated economic impact it is going to have at each stage. We try to explore below the different stages of the novel COVID-19 pandemic and the economic impact it will create on people’s lives and on institutions around the world. The economic impact of the novel COVID-19 pandemic can be classified into four stages [76,77]. The different phases can be classified as in Figure 1 and Table 1 below. The four stages include the first stage, identified as business and economic damage; the second stage, identified as financial contagion; the third stage, identified as bottom formation; and the fourth stage, identified as post-COVID-19 effects.

Figure 1.

Four stage model for economic impact of COVID-19.

Table 1.

The four-stage economic Impact of COVID-19.

- Stage 1: Business and economic damage: As the COVID-19 breaks out in a country, the first thing it does is disrupt the demand and supply. Since it can be fatal, it creates fear in the market by affecting both the manufacturing and the services sectors. This is a particularly dangerous situation for a small and fragile economy. At this stage, large and stable economies like the USA, China, Russia and a few Gulf countries are able to cope with the economic loss [78]. During this stage, the national governments take measures to control pandemics through lockdowns and restrictions on movements. Hereafter, the problem worsens, and people start panicking as supply chains are disrupted.

- Stage 2: Financial Contagion: This stage follows the disruption of economic activity, and many economies experienced this stage in mid-March or early April 2020. This stage is characterized by sharp downward movement in equity and crypto markets, forced leveraging and panic selling [79,80]. This stage is evidenced by the fact that liquidity starts falling, markets for new funds start freezing and central banks are forced to inject liquidity [81]. This stage is dangerous for small companies, households with low liquidity and larger debt obligations. Governments announce stimulus packages, but this is only a short-term and temporary solution [82].

- Stage 3: Bottom Formation: This is the most critical stage as far as the economic impact of this pandemic is concerned. Some countries, like Italy, Iran, India, and the United Kingdom, went through this stage during May 2020 [81,82]. This is evidenced by the fact that the financial markets seem to hit rock bottom. The actual cause for the bottom formation needs to be addressed, and economies should try to look for a long-term sustainable solution.

- Stage 4: Post-COVID-19 effects: The scar this virus is going to leave on us will be there for a long period of time. It is expected that there will be a further push for de-globalization, resulting in less travel and migration [83,84]. There are expectations that the world will not be the same post-COVID-19 as the companies will start factoring in the risk of global supply chain and will look for greater efficiency. The four stages with their characteristics are summarized in the following table:

3. Methodology

This research design is based on the theoretical approach considering the COVID-19 atmosphere. The present study intends to generate insights to explore the innovative Islamic approach to address the economic crisis that has occurred during the pandemic. Today’s pandemic has created a lot of uncertainty, volatility, ambiguity and complexity. To tackle this, we propose the effective use of the products/services of Islamic finance. The current study introduces Islamic approaches considering four stages of economic possibilities. These Islamic approaches are derived from the sacred text of Islam (Qura’an) and Traditions (Hadith) congregated from the life of the Prophet Mohammed (ﷺ). The Islamic financial system draws from Shariya principles that deal with many aspects of society, including economics, banking, contracts, business transactions, etc. The present study incorporates these principles and proposes suitable innovative tools [73]. The proposed model is based on the extensive review of the literature on conventional [85,86] as well as Islamic finance. Conventional finance literature is used to get a better understanding of the existing economic problem posed by the COVID-19 pandemic, and Islamic finance is used to provide a possible solution under different circumstances [75]. The study also proposes a suitable framework to utilize various Islamic finance products and concepts at each stage and its implication mechanism.

4. Result

There is a need for scholars in economics to take a more holistic view of the economic impact that this pandemic is going to create. The sooner the world can estimate the impact, the better prepared it will be to handle the situation during and after the pandemic. The next section discusses how Islamic finance can help during different stages of COVID-19.

The severity of the current pandemic has shaken economies and policymakers around the world. As we have seen during the global financial crisis in 2008, the foundations of conventional finance are based on capitalism and interest-based systems, and it was unable to handle the situation [87]. At the same time, it was observed that following Islamic finance and use of Islamic financial services will prevent such crises and will make the financial system more sustainable [88]. Relying on the intrinsic worth of Islamic finance, we identify ten Islamic financial services (as depicted in Table 2 below) that can be used during and after the pandemic to minimize the damages it causes.

Table 2.

Islamic Financial Services at each stage of COVID-19.

4.1. Musharaka

Musharaka is one of the most popular Islamic financial services used by Islamic financial institutions and banks to finance individuals and organizations. It refers to two or more persons coming together to contribute capital to do business and sharing profits and losses according to agreed terms and conditions. Musharaka is a very powerful Islamic financial service for expanding welfare and alleviating poverty [89]. Some basic characteristics of Musharaka are described below [90].

- i

- The capital is contributed by the partners (joint ownership).

- ii

- Rights and responsibilities are defined in the partnership.

- iii

- Profit and loss are to be shared by the partners in the agreed profit–loss sharing ratio. In the absence of any ratio, the profit is to be shared in the ratio of their capital. A sleeping partner cannot take more profit than the capital contribution.

- iv

- The Musharaka partnership is managed according to the partnership agreement. The partners may appoint one partner as an active partner and others can be silent or sleeping partners.

- v

- Active or managing partners have the right to receive more profit than their capital contribution.

Musharaka can potentially be one of the most effective tools against the economic consequences of COVID-19. It can be used at the fourth stage of COVID-19, i.e., post-COVID-19 effects. After the pandemic ends and financial experts start analyzing the losses caused and damages done to individuals and SMEs, then in that period there is scope for Musharaka to emerge as the true social finance tools. Islamic banks can enter the Musharaka contract with the individual and SMEs by sharing the risk and contributing capital. As we have learned from the global financial crisis, the morale of the investors is bound to be low during crises and during these times, and they need someone to share risk with them [91].

4.2. Mudarabah

Mudaraba is considered by both ancient and contemporary Islamic finance scholars to be one of the most popular and authentic modes of Islamic financial services. In the case of Mudaraba, a party who is a contributor of the capital is known as Rabb-Ul-Maal and the other party who manages the business of the Mudaraba contract is known as Mudarib [92]. The basic feature of Mudaraba can be summarized as follows

- i

- There are two main parties to the Mudaraba contract. The provider of capital is known as Rabbu-Ul-Maal, and the manager of the business is known as Mudarib.

- ii

- There is an agency relationship between the Mudarib and Rabb-Ul-Maal as there is master–agent relationship between the parties.

- iii

- The capital is solely contributed by the Rabb-Ul-Mall, and the Mudarib might contribute capital in some cases, wherein it becomes the combination of Musharaha and Mudaraba.

- iv

- The profit is shared between the parties according to the agreed terms and conditions. However, the loss can only be shared by the Rabb-Ul-Mall, as for the Mudarib, the loss is the foregone profit, which he loses in the case of incurring loss.

- v

- The capital of Mudaraba contract can be in cash or kind.

- vi

- Mudaraba contract can be applied in various contexts of modern business. The most popular application of Mudaraba is the saving and current deposit accounts with Islamic banks. In this case, the Islamic bank is the Mudarib, and the depositor is known as Rabb-Ul-Mall.

The nature of Musharaka and Mudaraba is the same, as both these financing instruments are based on profit- and loss-sharing. The only difference between them is that Mudaraba is considered a riskier investment than Musharaka [93].

Mudaraba can potentially be one of the most effective financing tools to finance COVID-19-affected individuals and SMEs. The income distribution in our society is already highly unequal; those who are rich are very rich, and the poor are very poor [94], and COVID-19 is only going to widen this gap between rich and poor. There is a need to develop an Islamic finance model that can use the Mudaraba contract and help in reducing this gap by mobilizing the resources from the rich and helping the poor and skilled people to start their own businesses. As millions of people have already lost their jobs and many others are expected to lose their livelihoods during COVID-19 [95], they can be given another lease on life by entering into a Mudaraba contract with those who have the money as well as intention of the welfare of the masses. Mudaraba can best be utilized at the fourth stage of the COVID-19.

4.3. Murabaha and COVID-19

Murabaha is basically the contract of sale in Islamic finance and is not a financing method. In the case of a Murabaha sale, the transaction is done on a cost-plus basis. Islamic finance makes a clear distinction between a normal sale and an Islamic sale, i.e., a Murabaha. A sale is defined in Islamic finance as the exchange of goods between parties with a mutual agreement [96]. To be a valid sale and comply with the principles of sharia, it must satisfy the following three conditions.

- i

- The goods must be in existence at the time of the sale agreement. Non-existing goods are not allowed for sale.

- ii

- The goods must be owned by the seller. The seller cannot sell something that he does not own. Something sold before acquiring the ownership of the goods is not a valid sale in Islamic finance.

- iii

- The goods must be in physical or constructive possession of the seller at the time of sale as derivatives contract like options and futures are haram in Islamic finance.

Murabaha contracts can potentially be an effective tool in Islamic finance to fight the economic consequences of the COVID-19. A Murabaha contract like BBA Murabaha (Bai-Bitamin Ajil) can help in financing COVID-19-affected individuals and SMEs. BBA Murabaha (deferred payment) is a type of sale in Islamic finance like personal finance or auto finance in conventional finance, with the only difference being that in the case of BBA Murabaha, goods financed by the bank or financer are owned by the bank [96]. COVID-19-affected individuals and SMEs will have liquidity problems [97], and consequently, they would require a financing tool such as Murabaha to meet their financing needs.

4.4. Ijarah and COVID-19

Ijarah means giving something to someone for a fee, rent or fare. Ijarah is the sharia-compliant version of a lease in conventional finance. Ijarah means granting someone the right to use a property for a fee, rent or fare [98]. Ijarah can be used in two ways. First, it is used when one employs a person’s services with a fee, The second type is related to the usage of the asset and properties for a fee or payment. The lease can be of two types in conventional finance: operating lease, a lease contract where the right to use of an asset is obtained, and capital lease, a lease contract where the ownership of the asset is transferred to the lessee at the end of the contract period. Islamic finance only recognizes the operating type of lease, whereas capital lease is not allowed as per sharia [99].

The recent development in Islamic finance has made Islamic financial services like Ijarah be a potential warrior against the crisis [100,101]. The changes have caused the demand for Ijarah contracts to increase. There is a need to develop user-friendly Ijarah contracts to suit the needs of the COVID-19-affected individuals and organizations. Islamic banks should provide Ijarah agreements based on the need of the individuals and SMEs. Ijarah is the best suited Islamic finance tool at stages 3 and 4 of COVID-19 [102].

4.5. Salam and COVID-19

Salam, along with the Istisna, is the exception to the contract of sale in Islamic finance. As explained earlier during the discussion in Murabaha, in order to become a valid sale, it must satisfy the three basic conditions of a sale. The Salam contract violates these principles as it a sale where a seller agrees to sell a certain commodity at a certain date at which is non-existent, and for the seller receives the payment in full at the time of agreement [103]. The key features of Salam contract are described as follows:

- i

- The commodity is to be delivered at a future date.

- ii

- The price for the Salam contract is paid in full at the time of the agreement.

- iii

- Salam is allowed by the Holy Prophet Muhammad ﷺ to help needy farmers after the prohibition of Riba.

- iv

- Salam contract is allowed only for a specific set of commodities like rice, wheat, dates, etc.

- v

- Salam contract can finance the immediate need of farmers and only for homogeneous goods.

Agriculture is the sector worst affected by COVID-19 [104]. Salam contract, which is farmer-friendly, can be a lease on life for already dying farmers. Salam is a much-needed contract for our farmers, and it must be used extensively by Islamic banks and governments to fulfill the financing needs of the farmers. COVID-19-affected farmers can enter into an agreement to obtain essential capital and supply the goods whenever they are available for delivery. It will help in injecting much-needed liquidity in the agriculture sector.

4.6. Istisna and COVID-19

Istisna is another exception to the general sale contract in Islamic finance. In the case of Istisna, a contract is allowed as an exception to the sale contract for goods that require manufacturing. It is very logical, as the manufacturer will not be ready to manufacture unless he gets commitment from the buyer [105,106]. The key characteristics of Istisna contract are as follows.

- i

- It is an order from a buyer for the manufacturer to produce something for him.

- ii

- It is allowed only for goods that require manufacturing, like work of a carpenter, jeweler or baker.

- iii

- The payment of Istisna can be deferred or spotted, unlike the Salam contract.

- iv

- The manufacturer must use his own material to produce the goods. If he uses the material provided by the customer, then in that case it will become a Service Ijarah.

- v

- The goods to be produced must be of a specified quality, type, color, etc. to avoid any element of Gharar. Gharar is an Arabic word that is described as the element of uncertainty, deception and excessive risk in an economic transaction, and it is declared Haram (forbidden) as per sharia law.

- vi

- There is the possibility to cancel the Istisna contract before the manufacturer starts manufacturing the product.

Most of the business owners eligible for an Istisna contract are in ventures such as carpentry and bakery and are small entrepreneurs [107]; they are the most affected by the consequences of the COVID-19. They can get help from this beautiful concept in Islamic finance by getting advance money to manufacture a product. It will enhance their liquidity during this pandemic and will contribute to the survival and revival of their business. It is best suited at stage four of the COVID-19 effects.

4.7. Qardh-Al-Hasan and COVID-19

Qardh-Al-Hasan is one of the most beautiful financing tools available in Islamic finance; it provides funds at the lowest possible cost to increase the demand level and also pushes the supply curve upward, resulting in a rise in output and lowering the overall price level in the economy [108]. Qardh-Al-Hasan maintains the price level as an increase in demand is offset by the increase in output. Some of the basic characteristics of Qardh-Al-Hasan are explained as follows:

- i

- Qardh-Al-Hasan is a form of interest-free loan that is extended by the lender to the borrower because of benevolence.

- ii

- The borrower pays back to the lender the principal amount without interest as it is fully complying with the principles of sharia that the borrower does not pay anything as interest.

- iii

- It is mainly used to provide short-term liquidity to the borrower.

- iv

- It can be an effective financing tool for the poor and COVID-19-affected SMEs.

Islamic banks provide a loan to the borrowers without interest. Islamic finance is based on the principles of ethics and morality, according to which only those who have an urgent need will apply for the loan, and it is the duty of the lender to provide funds to the person in need [109]. The COVID-19 pandemic has devastated the world economy, and the most affected are poor individuals and SMEs [110], and Qardh-Al-Hasan could prove to be a blessing for them. It could solve their urgent liquidity problems, and they will not even have any burden of immediate payment of installments. The most beautiful part of Qardh-Al-Hasan is that it must be paid at the convenience of the borrower. Qardh-Al-Hasan is most suited for the financing at the first and second stages of COVID-19, where millions of poor are suffering due to the lockdown, and it can be used to help the migrant labor.

4.8. Zakat and COVID-19

Zakat is another beautiful concept in Islamic finance and is purely based on the principle of ethics, morality and empathy [111]. Zakat is one of the five pillars of Islam along with the Tauheed, Salah, Saum and Hajj. Zakat is based on one’s possession of the wealth over and above the certain amount known as Nisab [112,113].

Basic characteristics of Zakat are as follows:

- i

- Zakat is one of the five pillars of Islam along with the Tauheed, Salah, Saum and Hajj.

- ii

- It is a compulsory 2.5% of one’s possession of wealth and income over and above the minimum amount known as Nisab. The Nisab is calculated as

- ▪

- Gold Nisab for gold is calculated as 3 ounces or 100 g.

- ▪

- Nisab for silver is calculated as 21 ounces or 700 g.

- ▪

- Cash equivalent to the present value of gold or silver as mentioned above.

- iii

- Zakat must be paid to eligible Muslims once a year.

Zakat is considered one of the trusted methods of poverty alleviation as per Holy Qura’an and Sunnah. It can prove to be an important Islamic finance tool to fight the adverse consequences of the COVID-19. Zakat is a compulsory payment by wealthy Muslims, and they are obliged to pay it as a part of their religious duty. COVID-19-affected people, especially the poor, can be provided with the essential items and/or cash as a relief. It is best suited at stage 1 and 2 to help the poor during lockdown, where daily wage laborers and migrant workers have nothing to feed their families.

4.9. Awqaf, Sadaqa and COVID-19

Awqaf has been considered a social financing tool over the years, and it has played an important role in sustainable financing for many poverty-alleviation programs such as education, health disaster relief, etc. [113]. The idea behind Awqaf in Islamic finance goes beyond religious significance, as it can be used for larger community development. Awqaf can be an important financing tool during COVID-19, as the wealth collected through Awqaf can be used for the welfare of COVID-19-affected people, and the objective of the larger community engagement can be achieved [114]. Awqaf is best suited at the fourth stage of COVID-19.

Sadaqa is another Islamic finance tool arising from the principle of benevolence. Sadaqa is a voluntary offering, and its amount is at the will of the benefactor. There are specific groups of people who are eligible to receive Sadaqa [115]. According to Holy Qura’an (Surah 9, Verse 60) Explanation: “Eight categories of people who are entitled to receive Sadaqa are- poor, needy, official appointed by government to receive, newly converted Muslim, to free slaves from non-muslim, person in debt trap, the preachers to spread the deen of Allah, Travelers who have no money to spend”.

As is evident from its basic nature, Sadaqa is best suited to be used as a financing tool during the COVID-19 period and its consequences afterward. It can be best utilized to help people stuck in lockdown and the people who have lost their business and belongings during COVID-19. Islamic banks and financial institutions can be assigned the sadaqa distribution respon-sibility to bring more efficiency and transparency [116,117].

5. Islamic Financial Service to Respond to the COVID-19, and Social Open Innovation

Social and open innovation are the two topics that are the need of the hour during an emergency like the current pandemic. Social innovation has the potential to change the face of the global social and economic structure [118]. The most important factor in the success of a social innovation is the backing from the political decision-makers and trust that the innovation will bring positive results and sustainable economic growth [119]. Social and open innovations are relevant in the pandemic and are another opportunity to emerge and provide open, innovative solutions to fight the economic shocks created by the pandemic. In fact, social and open innovations have the opportunity to provide an enduring and sustainable financial system. Open innovation brings more opportunity for corporate social responsibility and co-creation in an organization [120]. As discussed earlier, any innovation, whether social or open, is welcome in Islam as long as it does not violate the basic ethos and principles of sharia [121]. Islamic financial services are a type of ethical finance that are mainly based on the principle of ethics and morality and accept every innovation to improve the financial services [35,122]. Innovations like Financial technology (Fintech) and its associated financial services have already received acceptance among Islamic finance customers [123,124]. Certain restrictions like social distancing imposed during the COVID-19 pandemic have made these Fintech-based financial services more popular among Islamic finance customers [125,126]. Entrepreneurs and customers are already aware of the importance of creativity and innovation, believing that these innovations bring quality, efficiency, transparency, customer trust and profitability [127,128]. The unprecedented growth of the Islamic finance industry is partly due to the fact that it embraces innovation, including social and open innovation, and it has played a significant role in its growth in the past [129,130]. The fight against the economic consequences of the COVID-19 pandemic will be won with the social and open innovation in Islamic finance.

6. Conclusions

6.1. Conclusions

The aim of this study is to suggest tools from Islamic finance to deal with the economic crisis due to COVID-19. This study identifies four vital stages of economic crisis and ten Islamic financial concepts to be used at different stages of the crisis. The four stages of the COVID-19-induced economic crisis have already been experienced in different economies. Different countries are going through one or another stage of the crisis. The core capitalistic approach of the developed countries and the semi-socialistic approach of developing countries have failed to face the economic crisis. This atmosphere calls for the concepts such as Zakat and Sadaqa to support economically marginalized communities by generating a flow of money to encourage consumption. Mudaraba and Murabaha encourage start-ups and SMEs to either regain their job or initiate business. This encouragement enhances the morale of the individual and generates employment leading a to an increase in consumption. The Islamic investment fund contribution of various surplus funds to earn halal profit [125]. The compliance with sharia and various investments into different infrastructure like real estate, machinery or any other assets could contribute to economical normalcy. Therefore, the concept of Ijarah is one of the most considerable factors applicable in all stages of the pandemic. Islamic principles respect sheltering and hospitality for the needy. This principle contributes economy directly by accepting the infrastructural benefits rich and contributes to entrepreneurial class.

The study proposes the Islamic sustainability approach to face the challenges posed by the COVID-19 pandemic and ascertain the possible and practical solution. COVID-19 pandemic has only affected the human health and life rather it has directly disrupted the economic process throughout the world. The core socialistic and capitalistic approaches are unable to quantify the core value of social justice. Islamic finance believes in social development by spreading and sharing a surplus portion of wealth through Zakat, Waqf and sadaqa. These principles assist people to restore their business and establish fair trade practices. This study also encourages governments to introduce concepts like Salam to ensure that liquidity is made available to the farmers and other individuals.

The paper concludes that there is an immense potential that Islamic finance holds, i.e., the inclusion with stability and sustainability. Islamic financial services such as Islamic microfinance, Zakat, Sadaqah, Awqaf and Qardh-Al-Hasan are some of the broad range of financial services offered by the Islamic financial institutions that can be effectively utilized in the fight against the economic adversities of COVID-19 [132,133]. The paper proposes 10 financial services with a behavioral justification to be utilized to help the affected people due to COVID-19 at different stages. The paper also explains how these Islamic finance tools are helpful at different stages.

6.2. Limits with Future Research Topics

The present global pandemic has given Islamic finance another opportunity to prove its resilience; however, it also brought to light a few challenges which must be addressed going forward. Building a strong liquidity infrastructure for the Islamic financial institutions, aligning the reform efforts with the global financial regulatory reforms, and adoption of Financial technology (FinTech) and its optimum utilization are the prominent challenges that need to be addressed to make Islamic finance a sustainable alternative [133]. The study will prove to be a stepping stone for future researchers, academics and policymakers.

Author Contributions

Data curation, Y.N.; formal analysis, M.R.R. and M.A.M.A.; funding acquisition, M.R.R., M.A.M.A. and H.U.R.; investigation, M.A.; methodology, M.R.R., M.A.M.A., M.A. and Y.N.; project administration, Z.Z.; resources, H.U.R.; writing—original draft, M.R.R. and M.A.M.A.; writing—review and editing, Z.Z. All authors have read and agreed to the published version of the manuscript.

Funding

No funding was received from any source.

Data Availability Statement

Not applicable.

Conflicts of Interest

The authors declare no conflict of interest.

References

- World Health Organization. Weekly Operational Update on COVID-19; World Health Organization: Geneva, Switzerland, 2021; pp. 1–10. [Google Scholar]

- Bischoff-Ferrari, H.A. Infectious diseases: Supplementary Appendix: An interactive web-based dashboard to track COVID-19 in real time. Lancet Infect. Dis. 2021, 3099, 925–927. [Google Scholar]

- Duszak, R.; Maze, J.; Sessa, C.; Fleishon, H.B.; Golding, L.P.; Nicola, G.N.; Hughes, D.R. Characteristics of COVID-19 community practice declines in noninvasive diagnostic imaging professional work. J. Am. Coll. Radiol. 2020, 17, 1453–1459. [Google Scholar] [CrossRef]

- Teerawattananon, Y.; Dabak, S.V. COVID vaccination logistics: Five steps to take now. Nature 2020, 587, 194–196. [Google Scholar] [CrossRef] [PubMed]

- Grech, V.; Borg, M. Influenza vaccination in the COVID-19 era. Early Hum. Dev. 2020, 148, 105116. [Google Scholar] [CrossRef]

- Cozzi, G.; Zanchi, C.; Giangreco, M.; Rabach, I.; Calligaris, L.; Giorgi, R.; Conte, M.; Moressa, V.; Delise, A.; Poropat, F. The impact of the COVID-19 lockdown in Italy on a paediatric emergency setting. Acta Paediatr. Int. J. Paediatr. 2020, 109, 2157–2159. [Google Scholar] [CrossRef]

- Mahajan, A.; Sivadas, N.A.; Solanki, R. An epidemic model SIPHERD and its application for prediction of the spread of COVID-19 infection in India. Chaos Solitons Fractals 2020, 140. [Google Scholar] [CrossRef]

- Atalan, A. Is the lockdown important to prevent the COVID-9 pandemic? Effects on psychology, environment and economy-perspective. Ann. Med. Surg. 2020, 56, 38–42. [Google Scholar] [CrossRef] [PubMed]

- Killeen, G.F.; Kiware, S.S. Why lockdown? Why national unity? Why global solidarity? Simplified arithmetic tools for decision-makers, health professionals, journalists and the general public to explore containment options for the 2019 novel coronavirus. Infect. Dis. Model. 2020, 5, 442–458. [Google Scholar] [CrossRef] [PubMed]

- Ocampo, L.; Yamagishi, K. Modeling the lockdown relaxation protocols of the Philippine government in response to the COVID-19 pandemic: An intuitionistic fuzzy DEMATEL analysis. Socioecon. Plan. Sci. 2020, 72, 100911. [Google Scholar] [CrossRef]

- Martin, A.; Markhvida, M.; Hallegatte, S.; Walsh, B. Socio-Economic impacts of COVID-19 on household consumption and poverty. arXiv 2020, 4, 453–479. [Google Scholar] [CrossRef]

- Iacus, S.M.; Natale, F.; Santamaria, C.; Spyratos, S.; Vespe, M. Estimating and projecting air passenger traffic during the COVID-19 coronavirus outbreak and its socio-economic impact. Saf. Sci. 2020, 129, 104791. [Google Scholar] [CrossRef] [PubMed]

- Tisdell, C.A. Economic, social and political issues raised by the COVID-19 pandemic. Econ. Anal. Policy 2020, 68, 17–28. [Google Scholar] [CrossRef]

- Yoo, S.; Managi, S. Global mortality benefits of COVID-19 action. Technol. Forecast. Soc. Chang. 2020, 160, 120231. [Google Scholar] [CrossRef]

- International Monetary Fund. World Economic Outlook: A Long and Difficult Ascent; International Monetary Fund: Washington, DC, USA, 2020. [Google Scholar]

- Samadi, A.H.; Owjimehr, S.; Nezhad Halafi, Z. The cross-impact between financial markets, Covid-19 pandemic, and economic sanctions: The case of Iran. J. Policy Model 2020. [Google Scholar] [CrossRef]

- Sharma, G.D.; Talan, G.; Jain, M. Policy response to the economic challenge from COVID-19 in India: A qualitative enquiry. J. Public Aff. 2020, 20. [Google Scholar] [CrossRef]

- Jaspal, R.; Assi, M.; Maatouk, I. Potential impact of the COVID-19 pandemic on mental health outcomes in societies with economic and political instability: Case of Lebanon. Ment. Health Rev. J. 2020, 25, 215–219. [Google Scholar] [CrossRef]

- Pak, A.; Adegboye, O.A.; Adekunle, A.I.; Rahman, K.M.; McBryde, E.S.; Eisen, D.P. Economic Consequences of the COVID-19 Outbreak: The need for epidemic preparedness. Front. Public Health 2020, 8, 1–4. [Google Scholar] [CrossRef] [PubMed]

- Sachs, J.A.M.J. Bolivia’s Economic Crisis; National Bureau of Economic Research: Cambridge, MA, USA, 1988; pp. 1–40. [Google Scholar]

- Supoit, A. A legal perspective on the economic crisis of 2008. Int. Labour Rev. 2010, 149, 151–162. [Google Scholar] [CrossRef]

- García-Sánchez, I.M.; García-Sánchez, A. Corporate social responsibility during COVID-19 pandemic. J. Open Innov. Technol. Mark. Complex. 2020, 6, 126. [Google Scholar] [CrossRef]

- Hepburn, C.; O’Callaghan, B.; Stern, N.; Stiglitz, J.; Zenghelis, D. Will COVID-19 fiscal recovery packages accelerate or retard progress on climate change? Oxf. Rev. Econ. Policy 2020, 36. [Google Scholar] [CrossRef]

- International Labour Organization—ILO. COVID-19 Impact on Child Labour and Forced Labour: The Response of the IPEC + Flagship Programme; International Labour Organization—ILO: Geneva, Switzerland, 2020. [Google Scholar]

- Machmuddah, Z.; Utomo, S.D.; Suhartono, E.; Ali, S.; Ghulam, W.A. Stock market reaction to COVID-19: Evidence in customer goods sector with the implication for open innovation. J. Open Innov. Technol. Mark. Complex. 2020, 6, 99. [Google Scholar] [CrossRef]

- Acharya, V.V.; Schnabl, P. Do global banks spread global imbalances? Asset-backed commercial paper during the financial crisis of 2007–09. IMF Econ. Rev. 2010, 58, 37–73. [Google Scholar] [CrossRef]

- Jordà, Ò.; Schularick, M.; Taylor, A.M. Financial crises, credit booms, and external imbalances: 140 years of lessons. IMF Econ. Rev. 2011, 59, 340–378. [Google Scholar] [CrossRef]

- Mishkin, F.S. Global financial instability: Framework, events, issues. J. Econ. Perspect. 1999, 13, 3–20. [Google Scholar] [CrossRef]

- Zarrouk, H.; El Ghak, T.; Abu Al Haija, E. Financial development, Islamic finance and economic growth: Evidence of the UAE. J. Islam. Account. Bus. Res. 2017, 8, 2–22. [Google Scholar] [CrossRef]

- Souiden, N.; Rani, M. Consumer attitudes and purchase intentions toward Islamic banks: The influence of religiosity. Int. J. Bank Mark. 2015, 33, 143–161. [Google Scholar] [CrossRef]

- Abduh, M.; Azmi Omar, M. Islamic banking and economic growth: The Indonesian experience. Int. J. Islam. Middle East. Financ. Manag. 2012, 5, 35–47. [Google Scholar] [CrossRef]

- Aliyu, S.; Hassan, M.K.; Mohd Yusof, R.; Naiimi, N. Islamic banking sustainability: A review of literature and directions for future research. Emerg. Mark. Financ. Trade 2017, 440–470. [Google Scholar] [CrossRef]

- Al, R.; Saad, J.; Haniffa, R. Determinants of zakah (Islamic tax) compliance behavior. J. Islam. Account. Bus. Res. Jarita Duasa 2014, 5, 158–181. [Google Scholar]

- Hassan, M.K.; Rabbani, M.R.; Ali, M.A. Challenges for the Islamic finance and banking in post COVID era and the role of Fintech. J. Econ. Coop. Dev. 2020, 43, 3. [Google Scholar]

- Rabbani, M.R.; Abdullah, Y.; Bashar, A.; Khan, S.; Ali, M.A.M. Embracing of fintech in Islamic finance in the post COVID era. In Proceedings of the 2020 International Conference on Decision Aid Sciences and Application (DASA), Sakheer, Bahrain, 8–9 November 2020; pp. 1230–1234. [Google Scholar]

- Khanna, A. Impact of migration of labour force due to global COVID-19 pandemic with reference to India. J. Health Manag. 2020, 22, 181–191. [Google Scholar] [CrossRef]

- Blustein, D.L.; Duffy, R.; Ferreira, J.A.; Cohen-Scali, V.; Cinamon, R.G.; Allan, B.A. Unemployment in the time of COVID-19: A research agenda. J. Vocat. Behav. 2020, 119, 103436. [Google Scholar] [CrossRef]

- Usman, M.; Ali, Y.; Riaz, A.; Riaz, A.; Zubair, A. Economic perspective of coronavirus (COVID-19). J. Public Aff. 2020, 20, 1–5. [Google Scholar] [CrossRef] [PubMed]

- Mosteanu, N.R.; Faccia, A. Fintech frontiers in quantum computing, fractals, and blockchain distributed ledger: Paradigm shifts and open innovation. J. Open Innov. Technol. Mark. Complex. 2021, 7, 1–19. [Google Scholar]

- Banks, D.E. The diplomatic presentation of the state in international crises: Diplomatic collaboration during the US-Iran hostage crisis. Int. Stud. Q. 2019, 63, 1163–1174. [Google Scholar] [CrossRef]

- Gheeraert, L. Does Islamic finance spur banking sector development? J. Econ. Behav. Organ. 2014, 103. [Google Scholar] [CrossRef]

- Ahmed, A. Global financial crisis: An Islamic finance perspective. Int. J. Islam. Middle East. Financ. Manag. 2010, 3, 306–320. [Google Scholar] [CrossRef]

- Khan, A.; Hassan, M.K.; Maroney, N.; Boujlil, R.; Ozkan, B. Efficiency, diversification, and performance of US banks. Int. Rev. Econ. Financ. 2020, 67, 101–117. [Google Scholar] [CrossRef]

- Hassan, M.K.; Sanchez, B.; Yu, J.S. Financial development and economic growth in the organization of Islamic conference countries. J. King Abdulaziz Univ. Islam. Econ. 2011, 24. [Google Scholar] [CrossRef]

- Al-Sharkas, A.A.; Hassan, M.K. New evidence on shareholder wealth effects in bank mergers during 1980–2000. J. Econ. Financ. 2010, 34, 326–348. [Google Scholar] [CrossRef]

- Kalimullina, M.; Orlov, M.S. Islamic finance and food commodity trading: Is there a chance to hedge against price volatility and enhance food security? Heliyon 2020, 6, e05355. [Google Scholar] [CrossRef]

- Meltzer, M.I.; Cox, N.J.; Fukuda, K. The economic impact of pandemic influenza in the United States: Priorities for intervention. Emerg. Infect. Dis. 1999, 5, 659–671. [Google Scholar] [CrossRef]

- Aalbers, M.B. Financial geography: Introduction to the virtual issue. Trans. Inst. Br. Geogr. 2015, 40, 300–305. [Google Scholar] [CrossRef]

- Pitluck, A.Z. Islamic banking and finance: Alternative or façade? In Oxford Handbook of the Sociology of Finance; Oxford University Press: Oxford, UK, 2012; pp. 431–449. [Google Scholar]

- Pervez, I.A. Islamic finance. Arab Law Q. 1990, 5, 259–281. [Google Scholar] [CrossRef]

- Richardson, C. Islamic finance opportunities in the oil and gas sector: An introduction to an emerging field. Tex. Int. Law J. 2006, 42, 119. [Google Scholar]

- Mirakhor, A. Whither Islamic Finance? Risk Sharing in an Age of Crises. Munich Pers. RePEc Arch. 2010. Available online: https://mpra.ub.uni-muenchen.de/56341/ (accessed on 3 March 2021).

- Sakai, M. Establishing social justice through financial inclusivity: Islamic propagation by Islamic savings and credit cooperatives in Indonesia. In TRaNS Trans Reg. Natl. Stud. Southeast Asia 2014, 2, 201–222. [Google Scholar] [CrossRef]

- Rahim Abdul Rahman, A. Islamic microfinance: An ethical alternative to poverty alleviation. Humanomics 2010, 26, 284–295. [Google Scholar] [CrossRef]

- El-Gamal, M.A. Contemporary Islamic law and finance: The trade-off between brand-name distinctiveness and convergence. Berkeley J. Middle East. Islam. Law 2008, 1, 193–201. [Google Scholar] [CrossRef]

- Yasin, M.; Porcu, L.; Liébana-Cabanillas, F. Looking into the Islamic banking sector in Palestine: Do religious values influence active social media engagement behavior? J. Islam. Mark. 2020. [CrossRef]

- Syed, M.H.; Khan, S.; Rabbani, M.R.; Thalassinos, Y.E. An artificial intelligence and NLP based Islamic FinTech model combining zakat and Qardh-Al-Hasan for countering the adverse impact of COVID 19 on SMEs and individuals. Int. J. Econ. Bus. Adm. 2020, 8, 351–364. [Google Scholar] [CrossRef]

- Al-Jarhi, M.A. An economic theory of Islamic finance. ISRA Int. J. Islam. Financ. 2017, 9, 117–132. [Google Scholar] [CrossRef]

- Kamarudin, F.; Sufian, F.; Nassir, A.M.; Anwar, N.A.M.; Hussain, H.I. Bank efficiency in Malaysia a DEA approach. J. Cent. Bank. Theory Pract. 2019, 8, 133–162. [Google Scholar] [CrossRef]

- Wilson, R. Islamic finance and ethical investment. Int. J. Soc. Econ. 1997, 24, 1325–1342. [Google Scholar] [CrossRef]

- Binmahfouz, S.; Kabir Hassan, M. Sustainable and socially responsible investing: Does Islamic investing make a difference? Humanomics 2013, 29, 164–186. [Google Scholar] [CrossRef]

- Basher, S.A.; Hassan, M.K.; Islam, A.M. Time-Varying volatility and equity returns in Bangladesh stock market. Appl. Financ. Econ. 2007, 17. [Google Scholar] [CrossRef]

- Abdelsalam, O.; Fethi, M.D.; Matallín, J.C.; Tortosa-Ausina, E. On the comparative performance of socially responsible and Islamic mutual funds. J. Econ. Behav. Organ. 2014, 103, 1–21. [Google Scholar] [CrossRef]

- Nienhaus, V. Principles, problems and perspectives of Islamic banking. Intereconomics 1985, 20, 233–238. [Google Scholar] [CrossRef][Green Version]

- Akmansyah, M. Al-Qur’an dan al-sunnah Sebagai Dasar ideal Pendidikan Islam. J. Pengemb. Masy. Islam 2015, 8, 127–142. [Google Scholar]

- Izadi, S.; Hassan, M.L. Portfolio and hedging effectiveness of financial assets of the G7 countries. Eurasian Econ. Rev. 2018, 8, 183–213. [Google Scholar] [CrossRef]

- Djojosugito, R. Mitigating legal risk in Islamic banking operations. Humanomics 2008, 24, 110–121. [Google Scholar] [CrossRef]

- Iqbal, Z.; Mirakhor, A. Progress and challenges of Islamic banking. Thunderbird Int. Bus. Rev. 1999, 41, 381–405. [Google Scholar] [CrossRef]

- Šeho, M.; Bacha, O.I.; Smolo, E. The effects of interest rate on Islamic bank financing instruments: Cross-Country evidence from dual-banking systems. Pac. Basin Financ. J. 2020, 62, 101292. [Google Scholar] [CrossRef]

- Sunitha, B.K.; Gadiya, M.M.; Gulecha, M. A study on financial inclusion in India. Int. J. Manag. Stud. 2019, 6, 20. [Google Scholar] [CrossRef]

- Alsharari, N.M.; Alhmoud, T.R. The determinants of profitability in Sharia-Compliant corporations: Evidence from Jordan. J. Islam. Account. Bus. Res. 2019, 10, 546–564. [Google Scholar] [CrossRef]

- Jaballah, J.; Peillex, J.; Weill, L. Is being Sharia compliant worth it? Econ. Model. 2018, 72, 353–362. [Google Scholar] [CrossRef]

- Ben Jedidia, K.; Guerbouj, K. Effects of zakat on the economic growth in selected Islamic countries: Empirical evidence. Int. J. Dev. Issues 2020. [Google Scholar] [CrossRef]

- Bani Ata, H.M.A. Addressing financial bankruptcy from the Islamic perspective. Banks Bank Syst. 2019, 14, 9–19. [Google Scholar] [CrossRef]

- Sherif, M. The impact of Coronavirus (COVID-19) outbreak on faith-based investments: An original analysis. J. Behav. Exp. Financ. 2020, 28, 100403. [Google Scholar] [CrossRef]

- Akhtaruzzaman, M.; Boubaker, S.; Sensoy, A. Financial contagion during COVID–19 crisis. Financ. Res. Lett. 2020, 101604. [Google Scholar] [CrossRef]

- Topcu, M.; Gulal, O.S. The impact of COVID-19 on emerging stock markets. Financ. Res. Lett. 2020, 36, 101691. [Google Scholar] [CrossRef] [PubMed]

- Bherwani, H.; Nair, M.; Musugu, K.; Gautam, S.; Gupta, A.; Kapley, A.; Kumar, R. Valuation of air pollution externalities: Comparative assessment of economic damage and emission reduction under COVID-19 lockdown. Air Qual. Atmos. Health 2020, 13, 683–694. [Google Scholar] [CrossRef]

- Rabbani, M.R.; Khan, S.; Atif, M. Machine learning based P2P lending islamic FinTech model for small and medium enterprises (SMEs) in Bahrain. Int. J. Bus. Innov. Res. 2021, in press. [Google Scholar]

- Khan, S.; Rabbani, M.R. In depth analysis of blockchain, cryptocurrency and sharia compliance. Int. J. Bus. Innov. Res. 2021. [Google Scholar] [CrossRef]

- Corbet, S.; Larkin, C.; Lucey, B. The contagion effects of the COVID-19 pandemic: Evidence from gold and cryptocurrencies. Financ. Res. Lett. 2020, 35, 101554. [Google Scholar] [CrossRef]

- Chevallier, J. COVID-19 pandemic and financial contagion. J. Risk Financ. Manag. 2020, 13, 309. [Google Scholar] [CrossRef]

- Kumar, P.; Hama, S.; Omidvarborna, H.; Sharma, A.; Sahani, J.; Abhijith, K.V.; Debele, S.E.; Zavala-Reyes, J.C.; Barwise, Y.; Tiwari, A. Temporary reduction in fine particulate matter due to ‘anthropogenic emissions switch-off’ during COVID-19 lockdown in Indian cities. Sustain. Cities Soc. 2020, 62, 102382. [Google Scholar] [CrossRef] [PubMed]

- Carlsson-Szlezak, P.; Reeves, M.; Swartz, P. What coronavirus could mean for the global economy. Harv. Bus. Rev. 2020, 3, 1–10. [Google Scholar]

- Song, L.; Zhou, Y. The COVID-19 pandemic and its impact on the global economy: What does it take to turn crisis into opportunity? China World Econ. 2020, 28, 1–25. [Google Scholar] [CrossRef]

- Everingham, P.; Chassagne, N. Post COVID-19 ecological and social reset: Moving away from capitalist growth models towards tourism as Buen Vivir. Tour. Geogr. 2020, 22, 555–566. [Google Scholar] [CrossRef]

- Haron, S.; Nursofiza Wan Azmi, W. Determinants of Islamic and conventional deposits in the Malaysian banking system. Manag. Financ. 2008, 34, 618–643. [Google Scholar] [CrossRef]

- Hassan, M.K.; Rabbani, M.R.; Abdullah, Y. Socioeconomic impact of COVID-19 in MENA region and the role of Islamic finance. Int. J. Islam. Econ. Financ. 2021, 4, 1. [Google Scholar]

- Selim, M. Financing homes by employing Ijara based diminishing Musharaka. Int. J. Islam. Middle East. Financ. Manag. 2020, 13, 787–802. [Google Scholar] [CrossRef]

- Kabir Hassan, M.; Sanchez, B.A.; Ershad Hussain, M. Economic performance of the OIC countries and the prospect of an islamic common market. J. Econ. Coop. Dev. 2010, 31, 65–121. [Google Scholar]

- Ahmed, Z. Achieving Maqasid al Shariah through Takaful; International Centre for Education in Islamic Finance (INCEIF): Kuala Lumpur, Malaysia, 2013; pp. 203–213. [Google Scholar]

- Sapuan, N.M. An evolution of mudarabah contract: A viewpoint from classical and contemporary Islamic scholars. Procedia Econ. Financ. 2016, 35, 349–358. [Google Scholar] [CrossRef]

- Hassan, K.; Cebeci, I. Integrating the social maslaha into Islamic finance. Account. Res. J. 2012, 25, 166–184. [Google Scholar] [CrossRef]

- Poon, W.C. Users’ adoption of e-banking services: The Malaysian perspective. J. Bus. Ind. Mark. 2008, 23, 59–69. [Google Scholar] [CrossRef]

- Binder, C. Coronavirus fears and macroeconomic expectations. Rev. Econ. Stat. 2020, 102, 721–730. [Google Scholar] [CrossRef]

- Zaman, A. Crisis in Islamic economics: Diagnosis and prescriptions. J. King Abdulaziz Univ. Islam. Econ. 2012, 25, 147–169. [Google Scholar] [CrossRef]

- Haron, S.; Ahmad, N.; Planisek, S.L. Bank patronage factors of Muslim and Non-Muslim customers. Int. J. Bank Mark. 1994, 12, 32–40. [Google Scholar] [CrossRef]

- Gul Rashid, A.; Usmani, O.; Ejaz, L.; Faraz, H. Meezan bank: Category leader in Islamic banking. Emerald Emerg. Mark. Case Stud. 2017, 7, 1–23. [Google Scholar] [CrossRef]

- Rafay, A.; Sadiq, R.; Ajmal, M. Uniform framework for Sukuk al-Ijarah—A proposed model for all madhahib. J. Islam. Account. Bus. Res. 2017, 8, 420–454. [Google Scholar] [CrossRef]

- Ali, M.M.; Bashar, A.; Rabbani, M.R.; Abdullah, Y. Transforming business decision making with internet of things (IoT) and machine learning (ML). In Proceedings of the 2020 International Conference on Decision Aid Sciences and Application (DASA), Sakheer, Bahrain, 8–9 November 2020; pp. 674–679. [Google Scholar] [CrossRef]

- Rabbani, M.R. The competitive structure and strategic positioning of commercial banks in Saudi Arabia. Int. J. Emerg. Technol. 2020, 11, 43–46. [Google Scholar]

- Ehsan Wahla, A.; Hasan, H.; Bhatti, M.I. Measures of customers’ perception of car Ijarah financing. J. Islam. Account. Bus. Res. 2018, 9, 2–16. [Google Scholar] [CrossRef]

- Muneeza, A.; Nurul, N.; Yusuf, A.N.; Hassan, R. The possibility of application of Salam in Malaysian Islamic banking system. Humanomics 2011, 27, 138–147. [Google Scholar] [CrossRef]

- Wójcik, D. Financial geography II: The impacts of FinTech—Financial sector and centres, regulation and stability, inclusion and governance. Prog. Hum. Geogr. 2020, 1–12. [Google Scholar] [CrossRef]

- Hasmawati, A.; Mohamad, A. Potential application of Istisna’ financing in Malaysia. Qual. Res. Financ. Mark. 2019, 11, 211–226. [Google Scholar] [CrossRef]

- Muhammad, M.Z.; Chong, R. The contract of bay’ Al-Salam and Istisna’ in Islamic commercial law: A comparative analysis. Labu. E J. Muamalat Soc. 2007, 1, 21–28. [Google Scholar]

- Zarqa, M.A. Istisna‘ financing of infrastructure projects. J. Islam. Econ. Stud. 1997, 4, 67–74. [Google Scholar]

- Selim, M.; Hassan, M.K. Qard-al-Hasan-Based monetary policy and the role of the central bank as the lender of last resort. J. Islam. Account. Bus. Res. 2020, 11, 326–345. [Google Scholar] [CrossRef]

- Hassan, A.; Syafri Harahap, S. Exploring corporate social responsibility disclosure: The case of Islamic banks. Int. J. Islam. Middle East. Financ. Manag. 2010, 3, 203–227. [Google Scholar] [CrossRef]

- Morgan, T.; Anokhin, S.; Ofstein, L.; Friske, W. SME response to major exogenous shocks: The bright and dark sides of business model pivoting. Int. Small Bus. J. Res. Entrep. 2020, 38, 369–379. [Google Scholar] [CrossRef]

- Rabbani, M.R.; Khan, S.; Hassan, M.K.; Ali, M. Artificial intelligence and natural language processing (NLP) based FinTech model of zakat for poverty alleviation and sustainable development for Muslims in India. In ICOVID-19 and Islamic Social Finance; 104; Routledge: Abingdon, UK, 2021. [Google Scholar]

- Tanvir Mahmud, K.; Kabir Hassan, M.; Ferdous Alam, M.; Sohag, K.; Rafiq, F. Opinion of the zakat recipients on their food security: A case study on Bangladesh. Int. J. Islam. Middle East. Financ. Manag. 2014, 3, 333–345. [Google Scholar] [CrossRef]

- Muhammad Al-Amine, M.A.B. Risk and derivatives in islamic finance: A Shariah analysis. In Contemporary Islamic Finance: Innovations, Applications, and Best Practices; Wiley: Hoboken, NJ, USA, 2013. [Google Scholar]

- Ahmed, H. Role of Zakah and Awqaf in Poverty Alleviation; Cataloging-in-Publication Data; King Fahd National Library: Riyadh, Saudi Arabia, 2004.

- Singer, A. Soup and sadaqa: Charity in Islamic societies. Hist. Res. 2006, 79. [Google Scholar] [CrossRef]

- Rabbani, M.R.; Qadri, F.A.; Ishfaq, M. Service quality, customer satisfaction and customer loyalty: An empirical study on banks in India. VFAST Trans. Educ. Soc. Sci. 2017, 5, 39–47. [Google Scholar]

- Sun, H.; Rabbani, M.R.; Ahmad, N.; Sial, M.S.; Cheng, G.; Zia-Ud-Din, M.; Fu, Q. CSR, Co-Creation and Green Consumer Loyalty: Are Green Banking Initiatives Important? A Moderated Mediation Ap-proach from an Emerging Economy. Sustainability 2020, 12, 10688. [Google Scholar]

- Chesbrough, H.; Di Minin, A. Open social innovation. In New Frontiers in Open Innovation; Oxford University Press: Oxford, UK, 2014. [Google Scholar]

- Yun, J.J.; Egbetoku, A.A.; Zhao, X. How does a social open innovation succeed? Learning from burro battery and grassroots innovation festival of india. Sci. Technol. Soc. 2019, 24. [Google Scholar] [CrossRef]

- Sun, H.; Rabbani, M.R.; Ahmad, N.; Sial, M.S.; Guping, C.; Din, M.Z.U.; Fu, Q. CSR, co-creation and green consumer loyalty: Are green banking initiatives important? A moderated mediation approach from an emerging economy. Sustainability 2020, 12, 10688. [Google Scholar] [CrossRef]

- Rabbani, M.R.; Khan, S.; Thalassinos, E.I. FinTech, blockchain and Islamic finance: An extensive literature review. Int. J. Econ. Bus. Adm. 2020, 8, 65–86. [Google Scholar] [CrossRef]

- Khan, S.; Rabbani, M.R. Artificial Intelligence and NLP based Chatbot as Islamic Banking and Finance Expert. 2020 International Conference on Computational Linguistics and Natural Language Processing (CLNLP 2020), Seoul, Korea, 20–22 July 2020; pp. 20–22. [Google Scholar]

- Khan, S.; Hassan, M.K.; Rabbani, M.R. An artificial intelligence-based Islamic FinTech model on Qardh-Al-Hasan for COVID 19 affected SMEs. In Islamic Perspective for Sustainable Financial System; Istanbul University Press: Istanbul, Turkey, 2021. [Google Scholar]

- Khan, S.; Rabbani, M.R. Chatbot as Islamic Finance Expert (CaIFE): When finance meets Artificial Intelligence. 2020 International Conference on Computational Linguistics and Natural Language Processing (CLNLP 2020), Seoul, Korea, 20–22 July 2020; pp. 1–5. [Google Scholar]

- Khan, S.; Rabbani, M.R.; Sial, M.S.; Yu, S.; Filipe, J.A.; Cherian, J. Identifying big data’s opportunities, challenges, and implications in finance. Mathematics 2020, 8, 1738. [Google Scholar] [CrossRef]

- Yun, J.J.; Lee, M.H.; Park, K.B.; Zhao, X. Open innovation and serial entrepreneurs. Sustainability 2019, 11, 5055. [Google Scholar] [CrossRef]

- Sarri, K.K.; Bakouros, I.L.; Petridou, E. Entrepreneur training for creativity and innovation. J. Eur. Ind. Train. 2010, 3, 270–288. [Google Scholar] [CrossRef]

- Hamdani, J.; Wirawan, C. Open innovation implementation to sustain Indonesian SMEs. Procedia Econ. Financ. 2012, 4, 223–233. [Google Scholar] [CrossRef]

- Al-Salem, F.H. Islamic financial product innovation. Int. J. Islam. Middle East. Financ. Manag. 2009, 3, 187–200. [Google Scholar] [CrossRef]

- Maulana, B.; Usmani, T. pp. 1–9. 2012. Available online: https://Islam_Investment_Funds.Pdf (accessed on 3 March 2021).

- Hippler, W.J.; Hossain, S.; Hassan, M.K. Financial crisis spillover from Wall Street to Main Street: Further evidence. Empir. Econ. 2019, 56. [Google Scholar] [CrossRef]

- Kabir Hassan, M.; Choudhury, K.; Waheeduzzaman, M. On black market exchange rate and demand for money in developing countries: The case of Nigeria. Atl. Econ. J. 1995, 23, 35–44. [Google Scholar] [CrossRef]

- Atif, M.; Hassan, M.K.; Rabbani, M.R.; Khan, S. 6 Islamic FinTech. In COVID-19 and Islamic Social Finance; 91; Routledge: Abingdon, UK, 2021. [Google Scholar]

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).