Abstract

The socioeconomic changes that many countries have been experiencing in recent decades, caused by structural factors or by specific circumstances, where the pandemic crisis of COVID-19 is only the most recent example, have posed challenges to organizations, which present themselves more and more and in various forms as threatened by the possibility of fulfilling their mission. Public and private sectors increasingly present themselves as insufficient to respond effectively to day-to-day requests. This context of instability and the resulting impacts for non-profit organizations pose serious problems to the way in which governance is exercised and served as a motivation for carrying out a study that aimed to understand the influence of strategy and human resources on the governance of these organizations. A review of the literature on the variables under study made it possible to identify the sub-dimensions associated with each one of them and the respective indicators. Thus, for a quantitative study, it was possible to apply a questionnaire to 242 Holy Houses of Mercy in Portugal to understand the direct and indirect influences of strategic management and human resources management on the governance of these institutions. The results obtained show the existence of a positive relationship between the variables under analysis, confirming that not only do these variables influence, by themselves and directly, the governance of the institutions studied, but also the strategy influences human resources policies, which in turn have implications for the way the Holy Houses of Mercy deal with aspects associated with governance. It is concluded that, in general, for these organizations to be more effective in efforts to improve their governance processes, they must focus on strategic management and human resources management instruments.

1. Introduction

The current pandemic situation that all countries of the world are going through has caused strong constraints on the development of economic activity, causing a worsening of social problems and, consequently, exerting strong pressure on social protection systems.

This context of rapid changes in the dynamics of the societies in which we live in has provided non-profit organizations (NPOs) a reinforcement in their important role, as they emerge as entities of great importance in combating poverty and other social problems, developing a commitment to the communities and assuming the development of social responses aimed at solving their needs, often filling gaps that the welfare state and the private sector do not solve or whose response is insufficient.

In view of this growing importance of society, it is important to study how NPOs’ governance is established, since the guidelines assumed will influence various areas of the management, such as strategic, financial and human resources, among others. “Amid the COVID-19 pandemic, nonprofit leaders face constantly changing circumstances-sometimes hourly-and are adjusting their service operations based on directives from all levels of government” [1] (p. 874).

However, the linearity of this reasoning may not be what is found in practice. Bearing in mind the constant changes in the external environment and the growing and diverse challenges that are imposed on NPOs in promoting social well-being, it is possible to admit that governance, even though it is the epicenter of the management of these institutions, can receive influences of these other management areas, leading us to effectively question where they come from and how the influences that determine governance performance are exercised.

Regarding this exercise of influences in the management of these organizations, we can then start by addressing aspects such as the search for autonomy and financial sustainability and efficiency in the management of resources and services [2,3,4,5,6,7], so that these institutions find a lasting, sustainable and stable path, such as the continuous improvement of their economic and social performance.

With regard to strategic management, governance has been gaining importance in NPOs, motivated by changes in the external environment caused by various factors such as: the attribution of state subsidies based on the principle of efficiency and effectiveness [8], the growing preponderance of partnerships based on collaboration agreements, to the detriment of sponsorships [9,10], and the capture of financing and subsidies based on performance and quality indicators of the work developed [11,12,13,14,15].

Regarding the management of human resources, we can verify that this dimension of management assumes a strategic role, by fostering organizational effectiveness and guaranteeing growth and competitiveness, enabling the maintenance and development of its competitive advantages [16,17,18,19,20,21,22,23]. In this regard, it is possible to see that, in the specific contexts of NPOs, even if the investment in human resources is lower than the average in other sectors, the results in terms of employee performance are positive and decisive for the fulfillment of their missions [24,25,26,27]. These organizations tend to assume that it is through their human resources that new personal and organizational capacities are developed, focusing them on the added value of the institution, so their maintenance and management tend to be considered essential [28,29,30,31,32].

Such considerations lead us to believe that the governance in NPOs takes place in a context that is, at least, very dynamic, where other areas of management, such as strategic management and human resources, may have an influential and determining role.

To investigate this relationship, a study was carried out on the particular case of the Holy Houses of Mercy, with the general objective of assessing the existence of interrelationships between the following management areas: strategic management, human resources management and governance.

The reasons for choosing this type of institution are centered on its widespread presence throughout the Portuguese territory, the age and history of its action, the diversity of social services it provides and the growing importance with which it contributes to the growth of the social economy.

The Holy Houses of Mercy appeared in Portugal and Spain at the end of the 15th century. These institutions have always played an important role in social care for local citizens, playing different roles in society, including health promotion, disease prevention and care from a curative perspective, rehabilitation and reintegration. “Their presence and performance have been, and are, fundamental to the Portuguese social security system” [2] (p. 1). With a strong social character, they continue to be relevant and present throughout the national territory, in the various decolonized countries of the old Portuguese empire and in other territories that were influenced by Portuguese emigration, playing an important role in social assistance to citizens [2].

According to the most recent data presented by the National Statistics Institute of Portugal, there were 387 Holy Houses of Mercy in 2016. The information contained in the Social Economy Satellite Account reveals that the gross value added generated by the Holy Houses of Mercy represents 12.4% of the total created by all institutions of the social economy (having increased 10.2% in the last 3 years). According to the same source, social services represented 26.3% of the total remuneration created in the sector, followed by health and education (15.2%), areas in which the Holy Houses of Mercy have a strong presence. As for jobs created, the Holy Houses of Mercy represent 16.8% of the total jobs created by NPOs.

Thus, the objective of this research is to verify the influence of strategy and human resources management on the governance of the Holy Houses of Mercy in Portugal. It is intended, therefore, to understand how the management areas related to strategy (STR) and human resources management (HRM) influence the governance (GOV) of these institutions. Once the importance of human resources was determined, the influence of strategy (STR) on governance (GOV) mediated by these human resources management (HRM) was also tested. The data were analyzed using structural equation modeling using the SPSS/AMOS 27 software.

Several authors have addressed the particularities of NPO management [33,34] and recognized the importance of applying management tools and practices to NPOs [32,35,36,37], not forgetting the social mission of these institutions and the values under which they are governed [38]. Thus, the proposed study is innovative in that it analyzes the impact of strategic management and human resources management on the governance of the Holy Houses of Mercy, as its influencers are not as dependent on governance, in a relationship that is not found in the relevant literature for the case of NPOs and, in particular, for the institutions under study.

This article contributes to the development of the literature by providing an empirical investigation of the effect of strategy and human resources management on governance, by measuring the influence and the statistical significance of the strategy and the human resources on the governance of NPOs.

The present study is a contribution to the practice in these institutions, in the sense that they exercise their activity in an increasingly complex environment, with implications for the decision-making process and the exercise of governance, with a bigger degree of uncertainty. By pointing out the areas of management, their sub-dimensions and the concrete performance indicators that influence the performance of governance, the study points out ways for better performance at this level.

Starting from the analysis of strategic management and human resources management, and, again, taking into account their sub-dimensions and indicators with an influence on governance, the study also provides clues so that these NPOs can implement diagnostic plans, adapted to their specific realities and liable to be adapted to different social, economic, cultural, demographic or geographical realities.

On the other hand, knowing how these areas of management influence the exercise of governance, the present study allows these NPOs to be able to intervene in a more effective and assertive way in strategic and human resources issues, that is, upstream of the problem, so that the governance performance can present a superior quality performance. In this segment, practical aspects such as skills or profiles of human resources to be privileged, or financial or action strategies in the face of social problems, among others, may be redefined, since through this study, it is possible to perceive the influence that they will have downstream.

This different approach to the issue in question presents itself as a new perspective for the literature to assess issues influencing governance in NPOs. When we put governance, not as a point of departure, but as a point of arrival, in relation to what is revealed in the practice of management in this type of organization, contrary to what the evidence presents, for example, for the private sector, the discussion and the possibility of new studies that deepen this dynamic in organizational management remain open.

The present work is structured as follows. It starts with this introduction. Then, a literature review follows that addresses the concepts of strategic management, governance and human resources management and evidences the works that deal with the relationship between these variables in the management of NPOs. Section 3 contains the methodology adopted. In Section 4 the main results obtained are presented and discussed. Section 5 provides an overview of the main conclusions of the present investigation, reveals its limitations and presents suggestions for future research.

This article contributes to the development of the current body of literature on the influence of strategy and human resources management, investigating empirically how these areas of management can have a direct and statistically significant influence on the governance of Portuguese NPOs.

2. Literature Review

2.1. Governance and Strategic Management

Governance can be defined as the set of processes that the entity will adopt in its management [39]. It is the set of practices that seeks to improve management in organizations.

The relationship between strategic management and governance has mainly been evidenced in numerous empirical studies applied to the business reality. For example, [40] studied how market-leading companies implement new strategic models and adopt governance principles. The results obtained show the existence of relationships between corporate governance, strategic management and corporate sustainability.

It also becomes evident that if the company’s vision and mission, essential components of strategic management, are taken into account in corporate governance, the quality of the results is higher, achieving financial stability and sustainability [40]. Thus, it was found that governance and strategic management influence the sustainability of organizations. Governance improvements also influence strategic management, as the change in internal and external factors that improve corporate governance will force changes in strategic management. In addition, corporate governance can be implemented in the human resources function through codes of ethics and social responsibility.

However, research is not that abundant when applied to the reality of the third sector. Several studies have shown a lack of professionalism and the secondary importance of management in third sector organizations. Works such as those by [41,42,43] reinforce the need to implement principles, methods and management practices in NPOs. For this application to become more efficient and profitable, its specificities must be respected and resort to assessment formats and governance applications adapted to its characteristics, namely, the mission, vision, principles and profile of the stakeholders.

In this sense, several authors, including [44,45,46,47], recognize the importance of establishing strategies and principles to integrate the principles of governance in NPOs as profitable. They also argue that, in community-based organizations, information related to governance should be optimized and made public. More significant mobilization and effective commitment provide more tangible support for encouraging decision making and stakeholders’ participation. Further, concerning the application of governance principles and practices, [48,49,50] consider that elements such as ethics, corporate responsibility, accountability and transparency are applicable and are of paramount importance in third sector organizations.

The author of [39] studied the management strategies of Private Institutions of Social Solidarity in the Lisbon region and concluded that without a correct updated/renewed use of management tools, NPOs will have serious difficulties in subsisting. These management tools include market orientation; the principles of good governance based on the existence of well-defined missions and clear objectives aligned with the organizational strategy, that is, the existence of strategic planning; internal and external communication plans; financial monitoring and control systems; and transparency in the presentation of accounts/results.

Although NPOs are not driven by profit generation, they must generate enough revenue to pursue their social objectives and their strategic management must be designed to achieve the goals of organizations [51]. Thus, their governance principles must be in accordance with their strategic management, so that their actions lead to the achievement of their objectives [51]. Regarding the specific case of the Holy Houses of Mercy, [5] carried out a study applied to a Holy House of Mercy in the health area and concluded that a business intelligence platform could be a useful instrument for decision making, as it provides factual information about the institution’s trends and needs, improving the quality of service and user satisfaction.

The author of [52] also considered that NPOs that conduct adequate strategic planning to deal with uncertainty, mitigate deficiencies and continue to evolve present better results and performance.

Aware of the evolution, trends and needs of NPOs and their agents, the OECD has developed a set of fundamental principles of corporate governance, including the rights and equal treatment of shareholders and main ownership functions, incentives for investors’ institutions and the importance of stock markets for good corporate governance, the disclosure and transparency of information and the responsibility of the board of directors [53].

The author of [39] considers that without correct/updated/renewed use of management tools, NPOs will have serious difficulties in subsisting. These tools include: market orientation; the principles of good governance based on the existence of well-defined missions and clear objectives aligned with the organizational strategy, that is, the existence of strategic planning; internal and external communication plans; financial monitoring and control systems; and transparency in the presentation of accounts/results. Thus, governance practices are influenced by the organizational strategy and must be in line with it so that the objectives are achieved.

In [46], the NPOs adopt cooperative and pluralist governance systems, which are determined by their strategic principles, and show a high capacity to better serve the interests of different stakeholders, improving the performance and institutional strength of the organizations. In this way, the organizations’ strategy will positively influence the applied governance principles, benefiting the action of stakeholders as social intermediaries.

Therefore, it is important to understand how the various dimensions of STR found in the institutions under study (strategy formulation, strategic choices, implementation of strategies, identification of externalities, measuring externalities, disclosure of externalities) have a direct and positive influence on the governance performance.

Based on the literature review, and supported by the work of [39,40,45,46,47,51,52], we propose the following hypothesis:

Hypothesis 1 (H1).

Strategy (STR) has a direct and positive influence on the governance (GOV) of the Holy Houses of Mercy.

2.2. Strategy and Human Resources Management

The relationship between strategic management and human resources management has also been studied over time. Several authors argued that the alignment between organizations’ strategies and their human resources practices is fundamental for human resources to be a competitive advantage source [54,55,56,57].

In 1982, [56] argued that if human resources were considered in strategic planning, both in formulation and implementation, companies would be able to design systems that reflect their philosophy and relate their attitudes and values to their strategic plans. The authors of [22] reinforce this idea, stating that the objectives and the organizational strategy influence the human resources management practices implemented, interfering with organizational performance.

For [57], multinational companies will only achieve their ambitious strategic objectives if they can attract, retain and develop highly qualified people to implement their strategies, arguing that human resources are the key elements to ensure successful strategies.

Considering the importance of the relationship between strategic management and human resource management in NPOs, human resources key features must assume special relevance and financial resources must be combined in the most effective manner, in such a way as to prevent extreme dependence on external funding sources [51].

Social organizations need to have the capacity to acquire, develop and maintain their human resources with the necessary skills to develop their organizational strategy. Therefore, the strategic principles of these organizations must be taken into account when formulating human resources strategies [58,59].

In this sense, it is becoming increasingly evident that NPOs must emphasize the financing needs of their activities and the management of human resources. As found in companies, in NPOs, the people who work in these organizations are fundamental to achieve the proposed objectives. Thus, the strategic management of human resources, combined with motivation, leadership and communication, is the basis for the effective use of human potential, becoming a source of success and efficiency in any organization [51].

This paper attempts to verify an evolutionary version of the resource-based view (RBV), according to which human resources become a competitive advantage [17]. Based on the relationship between human resources and competitive advantage, the RBV theory was complemented by other evolutionary perspectives on the creation of human resource competencies, such as [20], [60,61,62,63,64], that “can help us to understand the conditions under which human resources become scarce, valuable, firm-specific, difficult-to-imitate resources, i.e., ‘strategic assets’” [65] (p. 759). Further, [66,67] present an evolution of the RBV theory, assuming that human resources are “high-value” assets in the organizations and, therefore, considering that competitive advantage is related to their skills portfolio.

The proposed study was based on the approach to strategic management from Porter’s view [55] in its approach structure, behavior and performance. Following Porter’s perspective, it is possible to understand the internal factors and the external factors that influence an organization’s performance. Thus, based on strategic diagnoses (internal and external), action plans will be developed according to the results of such diagnoses and priority investments will be identified, based on competitive forces and internal assets, considering and minimizing vulnerabilities, and allocating and leveraging strategic resources to speed up new opportunities and challenges, which are continually changing.

Thus, it is important to understand whether and how the various dimensions of the STR applied to NPOs, which have already been pointed out previously, have a direct and positive influence on the human resources of these institutions. In other words, it is intended to ascertain how strategic management aspects influence motivation, performance, practices, training support instruments or volunteering.

Based on the literature review, and supported by the works of [51,57,59], we propose the following hypothesis:

Hypothesis 2a (H2a).

Strategy (STR) has a direct and positive influence on the human resources management (HRM) of the Holy Houses of Mercy.

Having been able to find evidence in the literature about the ubiquity of the influence of human resources on the generality of the management areas, in this type of institution, we intend to determine if the possible influence of STR in GOV could occur with the intermediation of HRM. In other words, it is intended to assess whether the strategic issues prevalent in these NPOs, which will influence the way governance is performed, are influenced by the motivation of human resources, individual performance, practices, training support instruments or volunteering, since these are sub-dimensions associated with human resources.

Once again, based on the literature review, and supported by the works of [51,57,58,59], we propose the following hypothesis:

Hypothesis 2b (H2b).

Strategy (STR) has a direct and positive influence on the governance (GOV) mediated by the human resources management (HRM) of the Holy Houses of Mercy.

The formulation of this hypothesis is based on the resource-based view theory that proposes a direct cause–effect relationship between strategy in governance, the influence of human resources management on governance, and a strategy’s ability to influence governance supported by the good functioning of human resources in these non-profit institutions [17]. Based on the relationship between human resources and competitive advantage, the RBV theory has been improved and investigated from other evolutionary perspectives related to the creation of competencies in human resources [60,61,62,63,64]. These human resources assume vital importance in the success of governance because they are scarce, valuable and specific assets in this type of institution [65]. Human resources are valuable assets for organizations and, therefore, capable of creating a competitive advantage that allows them to enhance governance [66,67].

2.3. Human Resource Management and Governance

Human resources are at the heart of the corporate governance, as it is impossible to achieve governance principles without the full contributions of human capital [68]. Knowing that the organization’s objectives and human resources management practices are mutually reinforcing, [68] defended the integration of the human resources management policies in the organization’s general corporate strategy, as well as the governance principles adopted.

The author of [40] states that corporate governance can be implemented in the human resources function through codes of ethics and social responsibility. Conversely, human resources strategies may influence the principles of governance.

The author of [69] studied the perceptions of NPO volunteers on NPOs’ governance, verifying that they have a significant impact on their individual commitment and identification with the NPOs, resulting in higher perceptions of organizational effectiveness. The empirical results emphasize the significant role of organizational identity and the commitment of volunteers as mediating variables, providing implications and practices for NPO managers.

The author of [70] considered that the organizations which invest in human resources practices and strategically align them with their mission, objectives and governance principles are able to increase the motivation and maintenance of their volunteers.

Thus, in this last study hypothesis, we intend to assess whether HRM, by itself, and as a dimension or area of management with considerable relevance for NPOs, has a direct and positive influence on GOV.

Based on the literature review, namely, the works of [40,68,69,70], we propose the following hypothesis:

Hypothesis 3 (H3).

Human resources management (HRM) has a direct and positive influence on the governance (GOV) of the Holy Houses of Mercy.

3. Methodology

For the present quantitative investigation, an exploratory methodological approach was adopted to better understand how the strategy and human resources management can influence the institutions’ governance under study. A literature review was conducted on these variables under study based on the calculated STR and HRM indicators. A questionnaire was developed and applied (Appendix A). This questionnaire was composed of three parts, where the first part contained a set of generic questions about the respondent and where the second and third parts were composed of sets of questions, with the possibility of answering according to the five-point Likert scale, varying from “totally disagree” to “totally agree” and aimed at determining the respondent’s degree of agreement for the different STR and HRM indicators.

The sample consists of 242 Holy Houses of Mercy, which correspond to 62.5% of the universe of 387 Holy Houses of Mercy currently in operation in Portugal.

The data were collected in person, between November 2018 and December 2019, through the application of questionnaires, within the scope of audits carried out through the program “Misericórdias–Gestão Sustentável” of the Union of Portuguese Mercies. For this purpose, managers, technicians and workers from these institutions were surveyed.

3.1. Validity and Reliability of the Measurement Model

To assess the convergent validity and reliability of the model, the average variance extracted (AVE), composite reliability (CR) and Cronbach alpha (α) were examined, only using the measurement items whose factor loadings (AVE > 0.5; CR > 0.7; α > 0.7) were within acceptable statistical parameters [71]. Concerning the sample size, this satisfies the criteria for structural equation analysis, which proposes a minimum of 5 observations for each variable of the model [72,73]. The author of [72] suggested similar limits but proposed complex models with few indicators per construct and larger samples. According to the sources referred to above, it can be stated that the sample used is sufficient for the use of structural equation models. The structural equation model presented allows a multivariate analysis to test more complex models than the traditional linear regression [74].

3.2. Confirmatory Factorial Analysis

The choice of the best factorial model is fundamental in CFA, being indispensable to observe factorial loads and errors that statistically validate it and corroborate its adequacy in the study conducted [75].

The analysis of the research model that has been proposed resorted to confirmatory factor analysis (CFA), using a structural equation model (SEM) and SPSS/AMOS 27 software [76]. The mediation model was tested (for validity and reliability of the measures) according to the literature, and several research hypotheses were tested to determine the meaning of loadings and coefficients of each path [71].

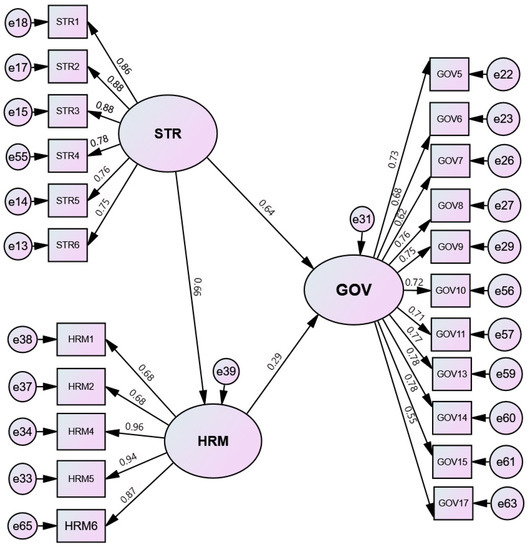

For the realization of the CFA, the model was tested with the nine dimensions of the strategy (STR), human resources management (HRM) and governance (GOV) items and factors, and it was verified, through the calculation of Cronbach’s alpha (α), that there is a good total internal consistency (α = 0.923) for the sample of 242 respondents. The internal consistency for all items that make up the model is demonstrated by Cronbach’s alpha (α) being higher than 0.9, revealing the validity and internal and explanatory reliability. The use of Cronbach’s alpha (α) is a statistical technique widely used and cited by several authors to demonstrate that the tests and scales that were built or adopted are relevant in explaining the investigation results [77]. It should be noted that the values of composite reliability (CR), average variance extracted (AVE) and Cronbach’s alpha (α) presented were obtained after removal of items with a factorial load below 0.5. The removal of these items allowed a substantial increase in all the robustness measures presented in Table 1. The final model (Figure 1) presented a more robust adjustment after removing the variables HRM3, HRM7, GOV1, GOV2, GOV3, GOV4, GOV12, GOV16 and GOV18 with loadings less than 0.5 (Table 1).

Table 1.

Validity and reliability of constructs.

Figure 1.

Final research model.

The CFA, with maximum likelihood, performed demonstrated that the model tested presented an adequate adjustment (χ2 = 1125,978, p = 0.001, df = 314, χ2/df = 3.586, RMSEA = 0.069, CFI = 0.901, GFI = 0.891) [60], after removing some items (HRM3, GOV1, GOV2, GOV3, GOV4, GOV5, GOV12, GOV13, GOV16 and GOV18) that made it statistically more robust, having excluded all items whose factorial loads were less than 0.5 [72,78]. Figure 1 shows the standardized path coefficients in which all the paths of the model were significant (p < 0.001).

4. Results

The tested research model (Figure 1) allowed verifying that STR influences (β = 0.660; p < 0.001) HRM, with (β = 0.290; p < 0.001), in the GOV of the NPOs under study. The model also explains that STR has an influence on HRM of (β = 0.640; p < 0.001) and, finally, STR has an influence on HRM-mediated GOV of (β = 0.422; p < 0.001), validating the hypotheses H1, H2a, H2b and H3.

In Table 2, it is possible to see a summary of the hypotheses that were tested.

Table 2.

Research hypotheses and statistical results.

The results of the structural model tested (Figure 1) indicate that the dimensions of STR and HRM have a direct, positive and statistically significant influence on GOV, supporting the research hypotheses formulated (H1, H2a, H2b and H3).

Analysis and Discussion of Results

Analyzing the influence of the STR and HRM dimensions on GOV (Table 1), we find that both dimensions have a strong impact on the GOV performance of the institutions under study, which confirms H1 and H3, echoing the studies by [40,46,51]. It was also possible to ascertain the influence of STR on HRM, which confirms H2a, and that from this combination between STR and HRM, once again, there is an impact on GOV, which confirms H2b. This demonstrated that strategy influences NPOs’ governance with human resources management as the predictive mediator. These results align with the studies by [58,59].

In this way, we move first to the analysis of H1’s confirmation. We advanced the study with the assumption that there would be an influence of STR on GOV, according to [40]. It was possible to ascertain that all the sub-dimensions that make up the STR (formulation of strategies, strategic choices, implementation of strategies, identification of externalities, measurement of externalities and disclosure of externalities) have statistical relevance in the performance of GOV.

This is equivalent to saying that, regarding the formulation of strategies, the first sub-dimension under analysis, it was possible to verify the existence of a set of relevant indicators for the STR composition, with a substantial impact on the institutions’ GOV. As they prove to be decisive for this influence among the variables under study, it is important to highlight the following STR indicators: a clear definition of the entity’s current strengths, weaknesses, threats and opportunities; a proactive attitude regarding the use of forces to combat threats; a proactive attitude regarding the use of opportunities to combat weaknesses; the exact definition of the institutions’ mission and vision; the existence of methods to compare the institutions’ performance with similar entities; the existence of a balanced balance sheet in terms of fulfilling the mission vs. economic and financial sustainability; the existence of reflection processes that allow anticipating future (predictable) developments; the existence of explicit strategies for attracting and integrating volunteers; the creation of strategic partnerships; the commitment of the entity’s managers to planning; the establishment of medium- and long-term objectives; and consideration of alternative scenarios. These indicators related to the sub-dimension “formulation of strategies” are echoed in [44].

With regard to strategic choices, the second sub-dimension under analysis, it was possible to identify another set of relevant indicators for this influence of STR on the GOV of these institutions: regular analysis of the direction of the performance of the entity with the specific intention of evaluating the effective strategies; regular management analysis of the needs and/or capabilities of the agents involved; definition of actions by the management in order to enhance their performance; the definition of indicators to assess the implementation of strategies and the establishment of periodic targets; translating strategies into action plans and identifying the resources needed for their implementation; having methods to compare their performance with similar entities; the alignment of resources with the key vectors of the strategy advocated by the entity; formal collection of updated information on the evolution of the community; the formal collection of information about potential users and their needs; the use of external agents in order to seek support for development and consolidate new strategies; the regular review and discussion of goals and indicators of achievement/achievement/achievement of the strategy; and taking corrective measures when there are deviations from compliance with the strategy. These indicators related to the sub-dimension “strategic choices” are related to [45]’s contributions.

A third sub-dimension that makes up an STR that influences GOV is the implementation of strategic choices. This corresponds to saying that when implementing its strategy, the institution must be transparent in accountability, in the scheduling of activities, in the distribution of resources and in the definition of priorities for employees, which is in line with [46]’s contributions.

The fourth sub-dimension that makes up the STR is the identification of externalities. This sub-dimension of STR corresponds to indicators such as the ability to sufficiently identify the externalities that the institution generates for the community, the entity’s constant concern with the improvement of the critical processes that effectively create value for its users (current and potential) and the attention given to users to be heard in the process of developing the entity’s mission, as key elements for the recognition of value creation. The indicators related to this sub-dimension are echoed in [47].

A fifth sub-dimension points to the measurement of externalities contributing to an STR with a substantial impact on GOV. For this, the institution must be able to sufficiently measure the externalities it generates for the community, to carry out studies that allow it to quantify the value generated in the community (positive externalities) and to ascertain the degree of satisfaction of the agents with which it relates, namely, family members, other reference groups of users and employees of the entity. The STR indicators calculated in this fifth STR dimension are related to [26]’s contributions.

Finally, the present study found that STR is composed of the last sub-dimension, the disclosure of externalities. For that purpose, the institution must be able to perceive the value of the positive externalities generated by the patrons and/or potential funders and must have the notion of the importance of the community to have a realistic perception of the value created by the entity, of the relevance of the community to understand that the institution fulfils its mission and of the importance of disseminating, for marketing purposes, the added value provided to the community and users. These indicators point in the direction of [51]’s contributions.

After analyzing the results that allow us to confirm H1, we focus our attention on the results related to the validation of H3. Regarding the strong impact found by HRM in GOV, with a direct positive influence on the structural model studied, which in turn confirms H3, it should be noted that such findings are in line with the literature considered for the present study, according to the authors of [41,42,43].

These authors reinforced the need to implement principles, methods and management practices in NPOs which include the increase in acceptable practices at the level of HRM in the typology of institutions targeted in this study, respecting their specificities and using format assessments and applications according to their characteristics, namely, regarding the mission, vision, principles and profile of the stakeholders.

From the analysis carried out, it was found that HRM is composed of five sub-dimensions (motivation, performance, practices, tools to support training and volunteering).

This is equivalent to saying that an HRM has an enormous direct influence on the GOV if, according to the first sub-dimension, employees have good levels of motivation, good levels of productivity and a high degree of proactivity, demonstrate a positive and optimistic attitude and feel like real managers of the entity, as an integral part, wearing the jersey. Also relevant are indicators such as a strong sense of organizational identity, care in the use of the organization’s resources, explicit knowledge of the organizational vision, mission and culture, the prevalence of an adequate level of collaboration between these employees, the non-verification of difficulties at the level of communication between them and the prevalence of a good relationship between the directors and employees of the entity. Finally, it is important to mention the importance of promoting activities that increase employees’ motivation levels and the promotion or incentive of teamwork. These contributions are echoed in the studies by [56].

The second sub-dimension of an HRM with a strong impact on GOV is performance. The constituent elements of this sub-dimension include the existence of some type of formal performance evaluation within the entity and the existence of a process for selecting employees through a professional area in the organization because the delegation of responsibilities is an established practice at the entity, due to the existence of a human resources management process (objectives, activities, performance, etc.) to be operationalized by a professional area. In addition to these indicators, others such as performance evaluation take into account factors that encourage and privilege teamwork, the prevalence of a good work environment experienced within the institution, the prevalence of an environment that enables the debate on problems/obstacles to satisfactory performance and the prevalence of good functioning of the institution (spirit of mutual help). The indicators of this second sub-dimension of HRM are related to [22]’s contributions.

To characterize the HRM that strongly influences GOV, a third sub-dimension is composed of practices. This sub-dimension is composed of indicators such as the employees’ salaries are regularized (up to date) because there are other tangible incentives, other than salaries, to motivate employees to pursue the objectives and a search for continuous improvement; and the existence of habits of employees in complying with the rules/internal regulations, for the existence of data that allows verifying that all respect the formal hierarchy and because there are formal moments of feedback between the entity’s management and employees, regarding the quality of its performance. This third dimension is also composed of indicators that go against [22]’s contributions.

The fourth sub-dimension of HRM is made up of instruments and training support. This includes indicators such as the identification of the training needs of employees; their periodical review and updating; the existence of a formal competence balance within the entity; the existence at the institution of any employee with training in the area of training management; the institution’s accreditation in the field of training organization; the prevalence of the notion that training is something assumed to be important within management; the existence of their own facilities where training actions can take place; the existence of adequate equipment for training; and the availability, to employees, of adequate support documentation (in quality and quantity). The indicators of this fourth sub-dimension of HRM are aligned with the contributions of [58].

Finally, the last dimension of an HRM that strongly influences GOV is volunteering. In this regard, it is essential to mention that it is crucial that the institution surveys each volunteer’s skills and abilities and proceeds to assess their work, which provides them with adequate feedback regarding their performance. It is also important that volunteers are assigned to activities according to their skills, and that the global impact of volunteer work is measured and disseminated. The institution should also provide specific training for the activities that they will perform, provide the opportunity for volunteers to work side by side with paid employees, performing the same tasks, ascertain whether the volunteers know and see themselves in the entity’s mission and identify the degree of ease in attracting volunteers. The indicators of this fifth sub-dimension of HRM that influence GOV are echoed in [59].

Having found the results that confirm H1 and H3 and identified the components that characterize and compose STR and HRM with a strong influence on the GOV of the institutions under study, it is now possible to notice that there is also a strong influence of STR on HRM, which confirms H2 advanced in the present study. It is possible to find an echo of this relationship in the literature through the contributions of [54,55,56]. These authors defend a close relationship between HRM and STR, even for organizations in the private sector. The authors of [22] reinforce this idea, stating that the objectives and the organizational strategy influence the human resources management practices implemented, interfering with organizational performance.

Thus, it is equivalent to say that, under the terms in which STR and HRM were previously presented, for the institutions under study, there is a powerful influence of the strategic formulations, the strategic choices, the implementation of strategies, the identification of externalities, the measurement of externalities and the disclosure of externalities on the performance of all HRM components.

Finally, focusing the attention on the positive influence on the structural model studied, which indicates that STR indirectly influences GOV by its impact on HRM, we can classify H2b as valid. Regarding this perspective, we can refer to the contributions of the authors of [44,45,46], who recognized the importance of establishing strategies and principles in order to increase the implementation of governance principles in NPOs, addressing the perspectives of STR and HRM in which the present study relies on.

It is thus possible to state that, under the terms in which STR and HRM were previously presented, for the institutions under study, strategic formulations, strategic choices, the implementation of strategies, the identification of externalities, the measurement of externalities, the disclosure of externalities, motivation of human resources, their performance, their practices, the instruments to support their training and the commitment to volunteering have a decisive influence on GOV.

In summary, the results of the present study constitute a reinforcement of the contributions of previous studies, in the context of NPOs, namely, [44,45,46,47], which point towards the existence of a relationship between STR and GOV. Further, the investigations developed by [57,58,59] evidence a relationship between STR and HRM, like our study. Lastly, the authors of [68,69,70], just like in this study, suggest the existence of a relationship between HRM and GOV.

5. Discussion: Open Innovation in Non-Profit Organizations

The relationship of NPOs with innovation management models is a fundamental aspect nowadays, since we are witnessing permanent changes in organizational contexts, in the implementation of the strategy, in the collaboration between people and entities and in the way that governance is exercised. It is also increasingly important to identify the activities that add value to these organizations. The so-called open innovation is a concept popularized in 2003 by Henry Chesbrough in the book Open Innovation: The new imperative for creating and profiting from technology, which was based precisely on the collaboration between people and external entities in organizations, with the use of the benchmarking technique, and that helps us to identify the relationship between the two concepts.

For [79], open innovation means that valuable ideas can come from inside or outside the company and reach the market. In reality, the idea of openness supposes a break with the traditional philosophy of not revealing issues of internal knowledge to the outside, recognizing the opportunity to obtain competitive advantages through the relationship with professionals and external organizations, sharing resources and knowledge and establishing alliances and partnerships. In a broader analysis, the objective is to accelerate internal innovation and expand markets for external use of innovation, influencing organizational results. Open innovation needs to combine internal research with external ideas and then implement those ideas, both in NPOs’ systems and in the systems of other organizations.

For [80], the key element for these organizations is to discover what the organization lacks, what can be achieved internally and what can be integrated, coming from the outside. Unlike the traditional model of vertical integration, open innovation also leads us to search for external sources of ideas, in addition to internal knowledge flows, in order to increase the innovation process [79]. This can provide NPOs the advantage to create new ideas, technologies, methodologies, processes and strategies and provides the possibility of expanding and/or diversifying the way in which governance is exercised.

However, in the case of NPOs, the literature on open innovation is scarce [81]. These organizations are not yet seen as a source of open innovation. In addition, many theoretical and practical contributions are still lacking in understanding the main benefits associated with open innovation practices in NPOs. While it can be argued that the literature clearly demonstrates the benefits of innovation for companies that have a focus on external engagement with diverse organizations, little attention has been paid to the specific context of NPOs as organizations in the context of open innovation.

For [82], open innovation, despite being a new model of innovation management, shows itself as a viable alternative to maintain and expand knowledge, capturing value and sustaining business, highlighting the acceleration of the time to launch and commercialize products, using external knowledge and the economic use of projects not developed by companies. Transposing this reality to the context of NPOs, and to the troubled moment in which these organizations try to respond to the requests of their target audience and when they try to fulfil their missions, it can be seen that, now more than ever, the adoption of these open innovation practices makes perfect sense.

Trying to understand how strategy and human resources management are exercised, in the light of the concept of open innovation and its implications for the way in which governance is exercised in these NPOs, is to meet the contributions of [79], who tells us that we have to analyze how to improve products and processes in an innovative way within the organization and understand what the external environment wants us to improve.

In the present investigation, it was found that, first, all the sub-dimensions that make up the strategy of these organizations (strategy formulation, strategic choices, strategy implementation, identification of externalities, measurement of externalities and dissemination of externalities) have direct statistical relevance in the governance of the organizations under study. Second, it was found that there are five sub-dimensions that make up human resources management (motivation, performance, practices, tools to support training and volunteering), with an equal influence on governance. Finally, it was found that the strategy, indirectly, also influences governance, through the impacts it causes in the management of human resources.

These results, in the light of open innovation, indicate that the governance of NPOs must have characteristics that allow a greater engagement of civil society, based on the formulation of their policies with more open and democratic principles, leading to new forms of democratic participation, where principles of polycentric governance predominate [83]. In doing so, it is helping to dissolve traditional boundaries between public, private and civil society actors [84].

In other words, when these organizations formulate, choose or implement strategies, when they identify, measure or disclose externalities, when they implement initiatives aimed at increasing the motivation or performance of their human resources or implement practices or instruments for the development of skills, or even when they bet on volunteering, in the light of open innovation, they should do so not through a non-traditional approach, but rather from a perspective that promotes an exchange of ideas and values between public and private actors, internal and external, according to the contributions of [85]. Further, [86] suggested that open social innovation supports and, in turn, is supported by new governance practices and that there is ample evidence that points to the reciprocal benefits resulting from strong relationships between local government and organizations of the civil society, for social cohesion, for organizational development and for sustainable development. Thus, the adoption of new approaches to governance translates into new ways of bringing organizational sustainability to these NPOs, which is essential for NPOs to be able to continue the path in the fulfilment of their missions.

In short, the current context of uncertainty and social instability in which we live in has brought new challenges to NPOs, which are increasingly seen as those organizations capable of supplying or mitigating the disabilities of the public or private sectors. This desire poses challenges in terms of fulfilling their missions. Governance practices, which are decisive for this purpose, are highly influenced by the measures or initiatives taken in terms of strategic management and human resources, in which the more they follow the principles of open innovation, the more benefits they will bring to these organizations and the more guarantees of a sustainable organizational offer.

6. Conclusions, Limitations and Future Research

6.1. Conclusions

In a context of particular social and economic instability, where all sectors of activity suffer from the consequences of the COVID-19 pandemic crisis, NPOs are increasingly challenged to provide social responses, according to their missions, since public and private sectors are unable to act as diligently as desired by society. In this context, studies that allow us to understand these organizations’ performance and dynamics become relevant. To this end, it is vital to understand how governance is exercised in NPOs and how management variables such as strategy and human resources influence, directly or indirectly, the performance of these organizations’ leadership.

A set of indicators grouped by sub-dimensions allowed us to characterize each of the dimensions under analysis with the influence on governance and showed that, both individually (H1 and H3) and indirectly (H2a and H2b), strategy and resource management influence the governance of the NPOs under analysis. In other words, not only implemented aspects related to strategy and human resources influence governance, but also the strategy influences human resources policy, resulting in a list of variables that also decisively influence governance.

In this sense, we can realize that NPOs, which seek to improve their performance in terms of governance, should pay particular attention to the aspects that have an impact on their strategy and their human resources, so that neglecting these variables, as an important part of the management, would bring additional difficulties in fulfilling their social missions. The results obtained influence the people management strategy and generate action plans for various organization levels and areas and can be considered a relevant contribution to the theory.

Thus, faced with an increasingly demanding environment, where the public and private sectors prove to be increasingly insufficient to provide the social responses that people and economic and social agents demand, NPOs play an increasingly essential role. This context means that, increasingly, the leaders of these organizations adopt a set of management processes, which must start with aspects related to their strategy and human resources, in order to optimize their governance practices, as emphasized in this investigation.

The indicators calculated for each sub-dimension of each variable under study, can be considered contributions to the practice, as they point out the essential aspects to be intervened, in case these institutions intend to improve their performance.

6.2. Limitations and Future Research

This study focuses on one type of NPO, the Portuguese Holy Houses of Mercy. As such, the traditional limitations of this typology apply to the non-possibility of generalizing the results to other types of organizations or sectors of activity.

The results of this investigation should be seen in the context of an exploratory study, an approach to a relatively little explored field of study, if we take into account its vastness and the special features of this type of organization and its differences for organizations in the private sector and the public. In this sense, it is important to emphasize the need and relevance of carrying out complementary studies that could confirm (or not) some of the main conclusions to which this study led us.

The determination of the influence of the variables under study in these organizations’ governance does not invalidate that there are no other dimensions of management that may also be relevant. As suggestions for future work, it would be interesting to investigate the influence of several important aspects that are important in the management of such special organizations, considering their social mission, such as: financial management, technologies and systems and information, communication and marketing, supply management, heritage management, knowledge management and even social responses management.

The study of the strategy, human resources and governance dimensions allowed for the accuracy of several sub-dimensions for each of these management perspectives in the organizations under study. The prevalence and weight of the indicators related to these sub-dimensions may be targets for future studies, in order to allow a better understanding of the dynamics of the dimensions under study in NPOs. The more in-depth this study is, the closer the scientific community will be to being able to point out a performance matrix to be implemented, in practice, by these NPOs.

Taking into account the sub-dimensions found in the present study, it is also recommended to carry out studies that analyze the impact of the implementation of concrete measures that prove to be contrary to the promotion of human resources strategies and policies, and that, in this way, may impair the performance governance of these NPOs.

Data collection, treatment and analysis took place in a context before and during the pandemic crisis of COVID-19. If this fact serves as a motivation to propel this study, at the same time, it presents itself as a limitation, since the organizational and cyclical reality that will occur at the end of this crisis may be dramatically different.

Only future comparative studies will allow us to understand how the social, political, economic or other consequences can influence the variables under study or other areas of the management of the Holy Houses of Mercy. Finally, it is suggested that this type of study be extended to other organizations in the non-profit sector, such as cooperatives, mutual societies, charities and local development, among others.

Author Contributions

Conceptualisation, M.O., M.S., R.S. and T.S.; methodology, R.S.; software, R.S.; validation, M.O. and R.S.; formal analysis, M.S. and T.S.; investigation, M.S. and T.S.; writing—original draft preparation, M.O., M.S., R.S. and T.S.; writing—review and editing, M.O.; visualisation, R.S.; supervision, M.O.; project administration, M.O. All authors have read and agreed to the published version of the manuscript.

Funding

The work of the author Rui Silva is supported by national funds, through the FCT-Portuguese Foundation for Science and Technology under the project UIDB/04011/2020.

Data Availability Statement

Not applicable.

Acknowledgments

The authors gratefully acknowledge the Polytechnic of Leiria (School of Education and Social Sciences), NECE-Research Center in Business Sciences, University of Beira Interior, CICS.NOVA.IPLeiria-Interdisciplinary Centre of Social Sciences, University of Trás-os-Montes and Alto Douro and CETRAD (Centre for Transdisciplinary Development Studies).

Conflicts of Interest

The authors declare no conflict of interest.

Appendix A

Questionnaire applied to the Holy Houses of Mercy within the scope of this investigation.

Table A1.

Questionnaire.

Table A1.

Questionnaire.

| Dimensions | Sub Dimensions | Questions | Authors Reference |

|---|---|---|---|

| Strategy (STR) | Strategy formulation | The entity periodically conducts an internal and external analysis to define objectives to formulate appropriate strategies. | Rodrigues and Malo [44] |

| Strategic choices | The entity periodically reviews its strategic choices, considering the goals and indicators of achievement of objectives. | Bukhari et al. [45] | |

| Implementation of strategies | The entity implements its strategic choices, rectifies deviations and establishes action plans, taking into account strategic partnerships, identifying and allocating resources, priorities, and activities to be developed. | Taylor [46] | |

| Identification of externalities | The entity can identify the externalities it generates for the community, considering the improvement of processes, development of the mission, and social value creation. | Cabral De Ávila and Bertero [47] | |

| Measuring externalities | The entity can quantify and measure the externalities it generates for the community. | Garcia [26] | |

| Disclosure of externalities | The entity can publicize the externalities it generates for the community and captures the perceived value. | Kicová [51] | |

| Human Resources Management (HRM) | Motivation | The entity’s human resources have good levels of motivation. | Devanna et al. [56] |

| Performance | Human resources are subject to a performance assessment, formal or informal, aimed at the entity’s proper functioning. | Boselie and Paauwe [22] | |

| Practices | The entity promotes practices aimed at promoting, developing, and encouraging human resources. | Boselie and Paauwe [22] | |

| Training support instruments | The entity identifies and provides resources that aim to provide human resources with better access to training. | Bloom and Chatterji [58] | |

| Volunteering | The entity promotes, disseminates and evaluates voluntary work. | Bloom and Smith [59] | |

| Governance (GOV) | Knowledge of the user’s family reality | The entity has strategies that promote the relationship with users’ family members to increase their family reality knowledge. | Saltaji [40] |

| Ethics and social responsibility | The entity has a system for promoting and monitoring ethical practices and social responsibility of its employees. | Tsai and Yamamoto [48] | |

| Action with the community | The entity promotes practices of action with the community, with positive impacts, whether at social, environmental, economic or financial levels, contributing to its sustainable development. | Leal and Famá [50] | |

| Performance impacts | The entity promotes external audits that include the impacts of its activities on a social, environmental, economic, financial level and the community’s sustainable development. | Machado Filho et al. [49] | |

| Quality system | The entity promotes a culture of quality, continuous improvement and adaptation of organizational processes. | Woerrlein and Scheck [15] | |

| Relationship networks | The entity promotes initiatives aimed at strengthening relations between people inside and outside the organization to capture and develop new ideas, good practices, and legislation compliance. | Saltaji [40] | |

| Communication plan | The entity has a communication plan, defined and diversified channels, to transmit its projects and their value to the community. | Garcia [26] | |

| Marketing | The entity has and streamlines marketing tools and strategies to cover the different target audiences in sufficient diversity. | Garcia [26] | |

| Community involvement | The organization organizes events open to the community and participates in third party events. | Saltaji [40] |

References

- Shi, Y.; Jang, H.S.; Keyes, L.; Dicke, L. Nonprofit Service Continuity and Responses in the Pandemic: Disruptions, Ambiguity, Innovation, and Challenges. Public Adm. Rev. 2020, 80, 874–879. [Google Scholar] [CrossRef] [PubMed]

- Macías Ruano, A.J.; Pires Manso, J.R.; de Pablo Valenciano, J.; Marruecos Rumí, M.E. The Misericórdias as Social Economy Entities in Portugal and Spain. Religions 2020, 11, 200. [Google Scholar] [CrossRef]

- Weerawardena, J.; McDonald, R.E.; & Mort, G.S. Sustainability of nonprofit organizations: An empirical investigation. J. World Bus. 2010, 45, 346–356. [Google Scholar] [CrossRef]

- Knutsen, W.L. Value as a self-sustaining mechanism: Why some nonprofit organizations are different from and similar to private and public organizations. Nonprofit Volunt. Sect. Q. 2013, 42, 985–1005. [Google Scholar] [CrossRef]

- Coelho, D.; Miranda, J.; Portela, F.; Machado, J.; Santos, M.F.; Abelha, A. Towards of a business intelligence platform to Portuguese Misericórdias. Procedia Comput. Sci. 2016, 100, 762–767. [Google Scholar] [CrossRef]

- Petitgand, C. Business tools in nonprofit organizations: A performative story. Int. J. Entrep. Behav. Res. 2018, 24, 667–682. [Google Scholar] [CrossRef]

- Suykens, B.; De Rynck, F.; Verschuere, B. Examining the influence of organizational characteristics on nonprofit commercialization. Nonprofit Manag. Leadersh. 2019, 30, 339–351. [Google Scholar] [CrossRef]

- Greiling, D. Performance Measurement in Nonprofit-Organisationen; Springer: Berlin, Germany, 2009. [Google Scholar]

- Meyer, M.; Simsa, R. Entwicklungsperspektiven des Nonprofit-Sektors. In Handbuch der Nonprofit-Organisation, 3rd ed.; Simsa, R., Meyer, M., Badelt, C., Eds.; Schäffer-Poeschel: Stuttgart, Germany, 2013. [Google Scholar]

- Zimmer, A.; Priller, E.; Anheier, H.K. Der Nonprofit-Sektor in Deutschland. Handb. Der Nonprofit-Organ. 2013, 5, 15–36. [Google Scholar]

- Dawson, A. A case study of impact measurement in a third sector umbrella organisation. Int. J. Product. Perform. Manag. 2010, 59, 519–533. [Google Scholar] [CrossRef]

- Grimes, M. Strategic sensemaking within funding relationships: The effects of performance measurement on organizational identity in the social sector. Entrep. Theory Pract. 2010, 34, 763–783. [Google Scholar] [CrossRef]

- Gill, S.J. Developing a Learning Culture in Nonprofit Organizations; Sage: Southend Oaks, CA, USA, 2010. [Google Scholar]

- Albrecht, K.; GAG, P.; Beck, S.; Hoelscher, P.; Plazek, M.; von der Ahe, B. Wirkungsorientierte Steuerung. In Non-Profit-Organisationen; Institut für den öffentlichen Sektor & KPMG, Ed.; PHINEO gAG: Berlin, Germany, 2013. [Google Scholar]

- Woerrlein, L.M.; Scheck, B. Performance management in the third sector: A literature-based analysis of terms and definitions. Public Adm. Q. 2016, 40, 220–255. [Google Scholar]

- Acosta-Prado, J.C.; López-Montoya, O.H.; Sanchís-Pedregosa, C.; Zárate-Torres, R.A. Human Resource Management and Innovative Performance in Non-profit Hospitals: The Mediating Effect of Organizational Culture. Front. Psychol. 2020, 11, 1422. [Google Scholar] [CrossRef]

- Wernerfelt, B. A resource-based view of the firm. Strateg. Manag. J. 1984, 5, 171–180. [Google Scholar] [CrossRef]

- Barney, J. Firm resources and sustained competitive advantage. J. Manag. 1991, 17, 99–120. [Google Scholar] [CrossRef]

- Conner, K.R. A historical comparison of resource-based theory and five schools of thought within industrial organization economics: Do we have a new theory of the firm? J. Manag. 1991, 17, 121–154. [Google Scholar] [CrossRef]

- Grant, R. The Resource Based Theory of Competitive Advantage: Implications for Strategy Formulation. Calif. Manag. Rev. 1991, 33, 114–135. [Google Scholar] [CrossRef]

- Collis, D.J.; Montgomery, C.A. Competing on Resources: Strategy in the 1990s. Knowl. Strategy 1995, 73, 25–40. [Google Scholar]

- Boselie, P.; Paauwe, J. Human resource function competencies in European companies. Pers. Rev. 2005, 34, 550–566. [Google Scholar] [CrossRef]

- Teece, D.J.; Pisano, G.; Shuen, A. Dynamic capabilities and strategic management. Strateg. Manag. J. 1997, 18, 509–533. [Google Scholar] [CrossRef]

- Nickson, D.; Warhurst, C.; Dutton, E.; Hurrell, S. A job to believe in: Recruitment in the Scottish voluntary sector. Hum. Resour. Manag. J. 2008, 18, 20–35. [Google Scholar] [CrossRef]

- Baines, D. ‘If We Don’t Get Back to Where We Were Before’: Working in the restructured non-profit social services. Br. J. Soc. Work 2010, 40, 928–945. [Google Scholar] [CrossRef]

- Atkinson, C.; Lucas, R. Worker responses to HR practice in adult social care in England. Hum. Resour. Manag. J. 2013, 23, 296–312. [Google Scholar] [CrossRef]

- Ariza-Montes, A.; Lucia-Casademunt, A.M. Nonprofit versus for-profit organizations: A european overview of employees’ work conditions. Hum. Serv. Organ. Manag. Leadersh. Gov. 2016, 40, 334–351. [Google Scholar] [CrossRef]

- Colbert, B.A. The complex resource-based view: Implications for theory and practice in strategic human resource management. Acad. Manag. Rev. 2004, 29, 341–358. [Google Scholar] [CrossRef]

- Akingbola, K. Resource-based view (RBV) of unincorporated social economy organizations. Can. J. Nonprofit Soc. Econ. Res. 2013, 4, 66–85. [Google Scholar] [CrossRef][Green Version]

- de Oliveira, S.B.; Toda, F.A. O planejamento estratégico e a visão baseada em recursos (RBV): Uma avaliação da tecnologia da informação na gestão hospitalar. Rev. Eletrônica Ciência Adm. 2013, 12, 39–57. [Google Scholar] [CrossRef][Green Version]

- Brown, W.A.; Andersson, F.O.; Jo, S. Dimensions of capacity in nonprofit human service organizations. Volunt. Int. J. Volunt. Nonprofit Organ. 2016, 27, 2889–2912. [Google Scholar] [CrossRef]

- Gile, P.P.; Buljac-Samardzic, M.; Van De Klundert, J. The effect of human resource management on performance in hospitals in Sub-Saharan Africa: A systematic literature review. Hum. Resour. Health 2018, 16, 34. [Google Scholar] [CrossRef]

- Nielsen, C.; Lund, M.; Montemari, M.; Palolone, F.; Massaro, M.; Dumay, J. Business Models: A Research Overview; Routledge: London, UK, 2019. [Google Scholar]

- Sanderse, J.; de Langen, F.; Salgado, F.P. Proposing a business model framework for nonprofit organizations. J. Appl. Econ. Bus. Res. 2020, 10, 40–53. [Google Scholar]

- Hwang, H.; Powell, W.W. The rationalization of charity: The influences of professionalism in the nonprofit sector. Adm. Sci. Q. 2009, 54, 268–298. [Google Scholar] [CrossRef]

- Hvenmark, J. Business as usual? On managerialization and the adoption of the balanced scorecard in a democratically governed civil society organization. Adm. Theory Prax. 2013, 35, 223–247. [Google Scholar]

- Laurett, R.; Ferreira, J.J. Strategy in nonprofit organizations: A systematic literature review and agenda for future research. Voluntas Int. J. Volunt. Nonprofit Organ. 2018, 29, 881–897. [Google Scholar] [CrossRef]

- Hudson, M. Managing without Profit: Leadership Management and Governance of Third Sector Organizations; Directory of Social Change: London, UK, 2009. [Google Scholar]

- Garcia, C.M.S. Governança: Uma estratégia para o terceiro setor face ao contexto de austeridade. Rev. Psicol. Criança Adolesc. 2016, 7, 1–2. [Google Scholar]

- Saltaji, I.M.F. Corporate Governance Relationship with Strategic Management. Intern. Audit. Risk Manag. 2013, 30, 301–308. [Google Scholar]

- Pimenta, S.M.; Brasil, E.R. Gestores e Competências Organizacionais no Terceiro Setor em Itabira. Gestão Reg. 2006, 22, 78–89. [Google Scholar]

- Cruz, J.A.W.; Quandt, C.O.; Martins, T.S.; da Silva, W.V. Performance no terceiro setor uma abordagem de Accountability: Estudo de caso em uma Organização Não Governamental Brasileira. Rev. Adm. Ufsm 2010, 3, 58–75. [Google Scholar] [CrossRef]

- da Silveira, D.; Borba, J.A. Evidenciação Contábil de Fundações Privadas de Educação e Pesquisa: Uma Análise da Conformidade das Demonstrações Contábeis de Entidades de Santa Catarina. Rev. Contab. Vista Rev. 2010, 21, 41–68. [Google Scholar]

- Rodrigues, A.L.; Malo, M.C. Estruturas de governança e empreendedorismo coletivo: O caso dos doutores da alegria. Rev. Adm. Contemp. 2006, 10, 29–50. [Google Scholar] [CrossRef]

- Bukhari, I.S.; Jabeen, N.; Jadoon, Z.I. Governance of third sector organizations in Pakistan: The role of advisory board. South Asian Stud. 2014, 29, 579–592. [Google Scholar]

- Taylor, K. Learning from the Co-operative Institutional Model: How to Enhance Organizational Robustness of Third Sector Organizations with More Pluralistic Forms of Governance. Adm. Sci. 2015, 5, 148–164. [Google Scholar] [CrossRef]

- Cabral De Ávila, L.; Bertero, C. Third sector governance: A case study in a university support foundation. Rev. Bus. Manag. 2016, 18, 125–144. [Google Scholar] [CrossRef]

- Tsai, P.Y.; Yamamoto, M.M. Governança corporativa: Análise comparativa entre o setor privado e o terceiro setor. In Proceedings of the Congresso USP Controladoria e Contabilidade, São Paulo, Brasil, 10–11 October 2005. [Google Scholar]

- Machado Filho, C.A.P.; Mizumoto, F.M.; Zylbersztajn, D. Governance and strategy of Private Interest Associations: A case study of the Brazilian Pasta Association. Rege Rev. Gestão 2006, 13, 1–10. [Google Scholar]

- Leal, E.A.; Famá, R. Governança nas organizações do terceiro setor: Um estudo de caso. In Proceedings of the SEMEAD—Seminários em Administração, São Paulo, Brasil, 9–10 September 2007. [Google Scholar]

- Kicová, E. Specifics of human resources in non-profit organizations in the process of globalization. SHS Web Conf. 2020, 74, 1011. [Google Scholar] [CrossRef]

- Miller, E.W. Nonprofit strategic management revisited. Can. J. Nonprofit Soc. Econ. Res. 2018, 9. [Google Scholar] [CrossRef]

- OECD. G20/OECD Principles of Corporate Governance. 2015. Available online: http://www.oecd.org/corporate/principles-corporate-governance/ (accessed on 10 January 2021).

- Ulrich, D. Recursos Humanos Champions; Ediciones Granica SA: Lavalle, Argentina, 1997. [Google Scholar]

- Porter, M. Clusters and the New Economics of Competition. Harv. Bus. Rev. 1998, 76, 75–90. [Google Scholar]

- Devanna, M.A.; Fombrun, C.; Tichy, N.; Warren, L. Strategic planning and human resource management. Hum. Resour. Manag. 1982, 21, 11–17. [Google Scholar] [CrossRef]

- Meyer, K.E.; Xin, K.R. Managing talent in emerging economy multinationals: Integrating strategic management and human resource management. Int. J. Hum. Resour. Manag. 2018, 29, 1827–1855. [Google Scholar] [CrossRef]

- Bloom, P.N.; Chatterji, A.K. Scaling social entrepreneurial impact. Calif. Manag. Rev. 2009, 51, 114–133. [Google Scholar] [CrossRef]

- Bloom, P.N.; Smith, B.R. Identifying the drivers of social entrepreneurial impact: Theoretical development and an exploratory empirical test of SCALERS. J. Soc. Entrep. 2010, 1, 126–145. [Google Scholar] [CrossRef]

- Winter, S. Knowledge and competence as strategic assets. In The Competitive Challenge: Strategies for Industrial Innovation and Renewal; Teece, D.J., Ed.; Ballinger: Cambridge, MA, USA, 1987; pp. 159–184. [Google Scholar]

- Amit, R.; Shoemaker, P.J.H. Strategic assets and organizational rent. Strateg. Manag. J. 1993, 14, 33–46. [Google Scholar] [CrossRef]

- Mueller, F. Strategic Human Resource Management and the Resource-Based View of the Firm: Toward a Conceptual Integration; Working Paper; Aston University Business School: Birmingham, UK, 1994. [Google Scholar]

- Peteraf, M.A. The cornerstones of competitive advantage: A resource-based view. Strateg. Manag. J. 1993, 14, 179–191. [Google Scholar] [CrossRef]

- Wright, P.M.; Mcmahan, G.C.; McWilliams, A. Human resources and sustained competitive advantage: A resource-based perspective. Int. J. Hum. Resour. Manag. 1994, 5, 301–326. [Google Scholar] [CrossRef]

- Mueller, F. Human Resources as Strategic Assets: An Evolutionary Resource-Based Theory. J. Manag. Stud. 1996, 33, 757–785. [Google Scholar] [CrossRef]

- Prahalad, C.K.; Hamel, G. A competência essencial da corporação. In Estratégia: A Busca da Vantagem Competitiva; Montegomery, C.A., Porter, M.E., Eds.; Elsevier: Rio de Janeiro, Brazil, 1998. [Google Scholar]

- Medeiros, N.; Meirelles, A.; Jeunon, E. A Gestão Estratégica nos departamentos de tratamento técnico a partir da visão de Porter e de Prahalad e Hamel: Fator de competitividade e sobrevivência das unidades de informação. Inf. Soc. 2008, 18, 171–182. [Google Scholar]

- Oyewunmi, O.A.; Osibanjo, A.O.; Falola, H.O.; Olujobi, J.O. Optimization by Integration: A corporate governance and human resource management dimension. Int. Rev. Manag. Mark. 2017, 7, 265–272. [Google Scholar]

- Zollo, L.; Laudano, M.C.; Boccardi, A.; Ciappei, C. From governance to organizational effectiveness: The role of organizational identity and volunteers’ commitment. J. Manag. Gov. 2019, 23, 111–137. [Google Scholar] [CrossRef]

- Akinlade, D.; Shalack, R. Strategic human resource management in nonprofit organizations: A case for mission-driven human resource practices. Glob. J. Manag. Mark. 2017, 1, 121–146. [Google Scholar]

- Hair, J.F., Jr.; Sarstedt, M.; Hopkins, L.; Kuppelwieser, V.G. Partial least squares structural equation modeling (PLS-SEM) An emerging tool in business research. Eur. Bus. Rev. 2014, 26, 106–121. [Google Scholar] [CrossRef]

- Hair, J.F.; Black, W.C.; Babin, B.J.; Anderson, R.E. Multivariate Data Analysis: Pearson New International Edition; Pearson: New York, NY, USA, 2013. [Google Scholar]

- Hoelter, J.W. The analysis of covariance structures: Goodness-of-fit indices. Sociol. Methods Res. 1983, 11, 325–344. [Google Scholar] [CrossRef]

- Bagozzi, R.P.; Yi, Y. Specification, evaluation, and interpretation of structural equation models. J. Acad. Mark. Sci. 2012, 40, 8–34. [Google Scholar] [CrossRef]

- Brown, T.A. Confirmatory Factor Analysis for Applied Research; Guilford Publications: New York, NY, USA, 2015. [Google Scholar]

- Ringle, C.M.; Wende, S.; Becker, J.M. SmartPLS 3; SmartPLS GmbH: Boenningstedt, Germany, 2015. [Google Scholar]