1. Introduction

Considering the widespread global interest in predictive models and the rapidly evolving use of artificial intelligence, integrating machine learning techniques into predictive analysis has become essential for significantly enhancing the accuracy and reliability of financial distress predictions. Financial distress prediction is crucial for investors, creditors, regulators, and policymakers aiming to mitigate risks and maintain market stability. Various models have been developed to assess corporate financial health, notably the Altman Z-Score, introduced by Edward Altman [

1], which remains among the most widely validated quantitative tools. Integrating several financial ratios, this model quantitatively evaluates the probability of a firm’s financial distress [

1,

2].

In addition to financial variables, corporate governance plays a critical role in determining firm performance, risk management, and financial resilience. Companies exhibiting robust governance structures demonstrate higher accountability, transparency, and adaptability to economic challenges [

3,

4]. Thus, incorporating governance indicators into financial distress prediction models can enhance the comprehensiveness and accuracy of risk assessment.

Previous research acknowledges the predictive effectiveness of Altman Z-Scores and recognizes the complementary value provided by governance measures in refining distress predictions [

5,

6]. However, existing studies predominantly focus on developed financial markets, revealing a knowledge gap in emerging economies with evolving governance frameworks. Limited attention has been given to the combined predictive potential of these indicators using machine learning technology in emerging markets like Romania, analyzed by machine learning technology. Addressing this gap, this study investigates whether machine learning-enhanced analysis of Altman Z-Scores and Corporate Governance Compliance (CGC) indicators effectively signals financial distress in manufacturing firms listed on the Bucharest Stock Exchange (BSE).

Therefore, the research question of the study is “To what extent can machine learning techniques, specifically Random Forest Regression, improve the accuracy and reliability of Altman Z-Scores and Corporate Governance Compliance as signals for predicting financial distress among manufacturing firms listed on the Bucharest Stock Exchange?”.

Building upon Signaling Theory, the study explores how digitally assessed financial and governance signals influence market perception and predict financial distress. Utilizing a Random Forest classification model developed by Leo Breiman [

7] and further implemented by Andy Liaw and Matthew Wiener [

8], our research analyzes digitally collected financial and governance data for 60 manufacturing firms listed on the BSE over seven years (2016–2022) for 420 firm-year observations. Financial distress is classified into three categories: no distress, moderate distress, and severe distress. Digital technologies and advanced analytics, through Random Forest, allow a nuanced identification of critical predictive variables, enhancing the reliability and predictive accuracy of these combined indicators.

This study is structured to first highlight the significance of digitally measured Altman Z-Scores in financial distress prediction, followed by an examination of Corporate Governance Compliance signals. Ultimately, the analysis confirms that integrating digital measurement techniques with advanced machine learning approaches significantly enhances the predictive capability of combined financial and governance indicators. By evaluating the interaction between financial health and governance compliance indicators, the research provides actionable insights for strengthening corporate governance practices and enhancing financial stability within Romania’s manufacturing sector, contributing to more comprehensive guidelines and risk management frameworks suited for emerging markets.

3. Materials and Methods

3.1. Data Collection and Variables

The data for this study were extracted from the Orbis database, compiled by Bureau Van Dijk, targeting all 85 companies listed on the Bucharest Stock Exchange (BSE) as of 2023. The selection criteria included non-financial companies, and they had continuous listings on the BSE from 2016 to 2022, resulting in a sample of 60 manufacturing firms and a total of 420 observations. This sample size is comparable to that of the original study conducted by Altman in 1968. The starting year of 2016 was chosen because the last significant revision of the Corporate Governance Code in Romania was implemented that year, while 2022 was selected as the endpoint due to the availability of financial information for analysis. The dataset encompasses financial statements and Corporate Governance Compliance reports.

By integrating core accounting variables with machine learning techniques, financial forecasting evolves from static analysis into an adaptive and intelligent process, capable of learning from data patterns and providing more relevant, insightful predictions in today’s dynamic financial environment [

37].

To contextualize financial distress in emerging markets, this study builds on previous research that has examined how corporate governance influences firm performance and risk during periods of crisis in developing economies [

38]. Recent research has extensively examined financial distress within emerging markets [

39], focusing on identifying key predictors and enhancing predictive models by using machine learning techniques [

40,

41].

In our model, the dependent variable is “Financial Distress” (FD), categorized as “No Financial Distress” (1), “Moderate Financial Distress” (2), and “Severe Financial Distress” (3). Independent variables are the Altman Z-Score (ZS) and the Corporate Governance Compliance Index (CGC).

The Altman Z-Score is calculated according to the following specific formula:

where

= Working Capital/Total Assets,

= Retained Earnings/Total Assets,

= Earnings Before Interest and Taxes/Total Assets,

= Market Value of Equity/Book Value of Total Liabilities, and

= Sales/Total Assets.

The resulting Z-Scores were used to categorize companies’ financial health: a score above 2.99 indicated a low probability of financial distress, and, as a result, the company in question was rated as not being financially distressed or being “safe”; with a score between 1.81 and 2.99, a company was rated as having moderate financial distress or being in the “gray area” of potential distress; and with a score below 1.81, a company was rated as having a severe likelihood of financial distress or being “distressed”.

The primary data used to determine Corporate Governance Compliance Indexes were manually collected from the official websites of the companies listed on the Bucharest Stock Exchange (BSE). Data were extracted from the mandatory “Apply or Explain” statements, as required by the Romanian Corporate Governance Code (RCGC). For each company, we recorded the number of governance principles explicitly marked as “applied” in the statement.

The 34 principles of the RCGC are grouped into four thematic categories as structured in the Code, as resulting from

Table 1:

Each of the 34 principles of the RCGC was evaluated using a binary scoring system: “1” was assigned if the company explicitly stated compliance with a principle (i.e., “Apply”) and “0” was assigned if the company either failed to apply the principle or provided an “Explain” justification for deviation. This yes/no (binary) coding approach was adopted for its clarity, reproducibility, and alignment with the BSE’s governance monitoring criteria. While this method does not account for degrees of partial compliance, it ensures objectivity by focusing solely on what is declared and verifiable.

For each company, the CGC Index was calculated as the ratio between the total number of principles marked as “applied” and the total number of applicable principles (34) using the following formula:

Thus, the CGC Index ranges from 0 (no compliance) to 1 (full compliance). This simple proportional score enables cross-sectional comparison between firms while avoiding subjective interpretation of compliance quality. To strengthen validity and consistency, a sample of 10% of the firms was double coded independently by a second reviewer. Inter-coder agreement exceeded 95%, and discrepancies were discussed and resolved, reinforcing the reliability of the coding procedure. This approach provides a transparent, replicable, and empirically grounded measure of Corporate Governance Compliance suitable for machine learning models, including Random Forest analysis.

In order to investigate the determinants of financial distress and the predictive power of Corporate Governance Compliance, a Random Forest classification model was employed. The variables included in the model were selected based on their theoretical and empirical relevance and are summarized in

Table 2, along with their definitions and data sources. Each variable was categorized (numerical or categorical) and matched with its respective data source to ensure transparency and replicability.

The dependent variable is Financial Distress (FD), a categorical construction derived from the Altman Z-Score model, which classifies firms into three distinct categories: (1) No Financial Distress (Safe Zone); (2) Moderate Financial Distress (Gray Zone); (3) Severe Financial Distress (Distress Zone). The classification is grounded in the thresholds originally proposed by Altman [

1] and adapted to the industrial profile of the sample. The Z-Scores were calculated based on data retrieved from the ORBIS commercial financial database, developed by Bureau van Dijk. In addition to the Z-Score and its derivative classification, the Corporate Governance Compliance Index (CGC Index) is included as a core explanatory variable. This numerical index captures the quality of a firm’s governance practice and serves as a proxy for internal control, accountability, and transparency.

This structured set of variables enables the application of machine learning classification techniques to explore complex, non-linear interactions between governance practices and financial health. The inclusion of both quantitative financial indicators and qualitative governance compliance enhances the explanatory power and robustness of the Random Forest model.

3.2. Model Description and Hypothesis Development

To examine the predictive relationship between financial distress measured by Altman Z-Scores and Corporate Governance Compliance (CGC) Indexes, a Random Forest classification model was implemented using the XLSTAT Advanced statistical software package. Random Forest [

7] is particularly suitable due to its robustness in handling complex, non-linear relationships; overfitting multicollinearity; effectively managing categorical data; and significantly enhancing predictive accuracy over traditional methods such as logistic regression or discriminant analysis. Comparative analysis of machine learning models for bankruptcy prediction indicated that Random Forests provided superior predictive accuracy compared to traditional models like logistic regression and discriminant models and even artificial neural networks and support vector machines [

42,

43].

The Random Forest model is specified as follows:

where

denotes the financial distress status of firm

at time

represents the calculated Z-Score of firm

at time

,

signifies the Corporate Governance Compliance assessed for firm

at time

, and

represents the error term capturing unexplained variability.

For implementing machine learning algorithms, hyperparameter tuning options were set based on prior literature and empirical testing within the software capabilities. The number of trees in the forest (n_estimators) was set to 200, as this value provided a good balance between performance stability and computational time. The maximum tree depth and minimum number of observations per leaf were left at their default XLSTAT settings, which were internally optimized to prevent overfitting. The number of variables considered at each split was set automatically by XLSTAT based on the square root of the number of predictors, which is consistent with best practices for classification tasks. Model performance was evaluated using standard metrics, including accuracy, precision, recall, F1-score, and the area under the ROC curve (AUC). A confusion matrix was also generated to visualize the classification quality across the three financial distress categories. Additionally, XLSTAT provided a variable importance chart, which was used to assess the relative contribution of the Corporate Governance Compliance Index and financial indicators to the classification outcomes.

The relationship between corporate governance characteristics and financial distress was analyzed by employing both Logit and Random Forest models, and the results showed that corporate governance variables enhanced the predictive accuracy of the Random Forest model, underscoring the model’s ability to identify and rank influential predictors, thereby aiding in the turnaround process of distressed companies [

44].

Our research emphasizes emerging markets, particularly Romania, due to their distinct institutional frameworks, influencing the effectiveness of governance mechanisms and financial health indicators. The study investigated the combined impact of Altman Z-Scores and Corporate Governance Compliance on predicting financial distress among manufacturing companies listed on the Bucharest Stock Exchange (

Figure 1).

The model’s performance was assessed through stratified sampling and cross-validation techniques during the Random Forest implementation in XLSTAT. Furthermore, to ensure the stability of the results, we verified the model’s predictive power across multiple folds and evaluated key performance metrics (accuracy, precision, recall, and AUC). The consistency of variable importance rankings across these folds reinforced the reliability of our findings.

Based on the literature reviewed and Signaling Theory, the following hypotheses were formulated:

H0 (null): Digitally measured Altman Z-Scores and Corporate Governance Compliance indicators do not significantly enhance differentiation between financial distress categories among Romanian listed manufacturing companies.

H1 (alternative): Digitally measured Altman Z-Scores and Corporate Governance Compliance indicators significantly enhance differentiation between financial distress categories among Romanian listed manufacturing companies.

The hypotheses were tested using Random Forest analysis, with the model’s predictive performance assessed through accuracy metrics, variable importance analysis, and confusion matrices.

4. Results and Discussion

4.1. Descriptive Statistics and Random Forest Regression

Descriptive statistics for the Altman Z-Scores (ZSs) and Corporate Governance Compliance (CGC) Indexes across the three financial distress categories are summarized in

Table 3.

Firms classified as safe exhibit the highest mean Z-Score values (4575), signaling robust financial health, and these firms also maintain a moderate level of Corporate Governance Compliance (mean CGC = 0.683). Companies facing moderate financial distress have lower Z-Scores (mean ZS = 2.349), but they demonstrate higher governance compliance (mean CGC = 0.752). This might reflect strategic signaling behavior, where firms experiencing moderate distress proactively enhance governance transparency to reassure stakeholders. Firms in severe distress exhibit both poor financial health (negative mean Z-Score = −0.705) and lower compliance with governance standards (mean CGC = 0.475), indicating significant managerial and financial challenges. These findings suggest that while financial health and governance compliance generally move together, firms under moderate distress appear more proactive in adopting governance measures, possibly as a strategy to mitigate perceived financial instability.

The overall mean Z-Score for the sample (2.388) suggests moderate risk of financial distress within the Romanian manufacturing sector. Meanwhile, the mean CG score of 0.651 (65%) highlights a relatively high level of adherence to good corporate governance practices. In fact, these results are consistent with previous research by Achim et al. [

24], who reported similar compliance levels (around 60%) a decade ago, suggesting limited improvements since then.

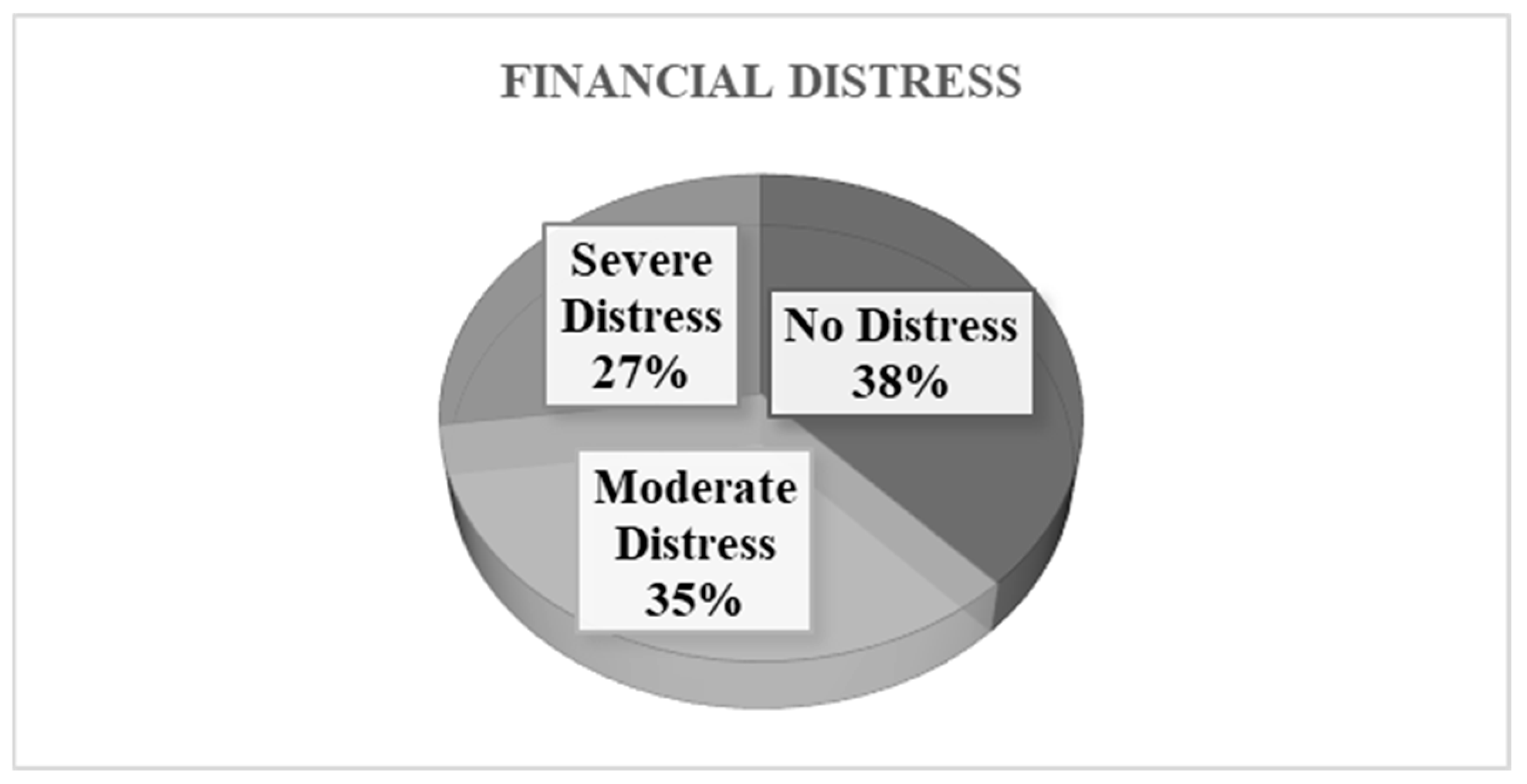

Figure 2 displays the firm distribution across distress categories from 2016 to 2022, illustrating that only 38% of firms remained financially stable during the observed period. In contrast, 62% experienced varying degrees of distress (35% moderate and 27% severe), highlighting considerable vulnerability within the sector. These findings underscore the need for enhanced corporate strategies and policy interventions.

This significant portion of distressed firms highlights the importance of close monitoring by investors, creditors, and policymakers, emphasizing the need for strategic interventions and preventive actions to reduce the likelihood of business failures. The distribution demonstrates a balanced representation among the three categories, ensuring adequate variation in the multinomial logistic regression model for discrimination between firms at various financial distress levels. As a result, an effective predictive model that can generalize effectively across all categories is aided by the distribution’s relative consistency.

Table 4 provides the summary statistics generated by the Random Forest model, a foundation for understanding the distribution of Z-Scores and CGC Indexes and their potential impact on financial distress levels.

The overall descriptive statistics further confirm considerable variability in financial stability across the sample, with Z-Scores ranging from highly negative (−18.16) to strongly positive (14.58) and a high standard deviation (3.120). In contrast, lower variability in CGC scores suggests consistent adherence to the Romanian Governance Code.

Table 5 displays a moderate positive correlation coefficient between Z-Scores and Corporate Governance Compliance Indexes (0.337), demonstrating that higher financial stability generally aligns with better governance practices, though it provides unique and complementary signaling information.

4.2. Random Forest Regressor Analysis

The Random Forest analysis performed in this study was a classification forest type, applying the bagging method for data sampling. The sampling was performed randomly with replacement from a sample size of 420 observations. The analysis constructed a total of 100 decision trees to ensure robust predictive performance. Randomness was controlled by setting a seed value to allow the replicability of results.

The Random Forest analysis achieved a notably low Out-of-Bag (OOB) misclassification rate of only 1.7%, demonstrating an exceptional predictive accuracy of 98.3%. The results of the confusion matrix underscore this precision and are summarized in

Table 6.

The confusion matrix shows strong classification accuracy across all categories, notably near-perfect accuracy for severe distress. The Altman Z-Score is clearly the dominant predictor, significantly outperforming Corporate Governance Compliance indicators in predicting financial distress. Corporate Governance Compliance still contributes, but its impact is relatively minor. Variable importance metrics demonstrate the dominant predictive role of financial health indicators and are provided in

Table 7.

The mean decrease in accuracy highlights the contribution of each predictor variable to the Random Forest model’s predictive accuracy. The Z-Score exhibits a significantly higher importance (170.303) compared to the Corporate Governance Compliance (CGC) score (3.070), underlining its dominant predictive strength. Specifically, the Z-Score demonstrates substantial predictive accuracy across all financial distress categories (No Distress: 93.480, Moderate Distress: 97.847, Severe Distress: 113.121). In contrast, CGC scores contribute minimally, with negligible predictive power for severe distress (0.000) and limited predictive strength for moderate (1.976) and no distress (2.800) scenarios.

These results confirm Z-Scores as the most reliable signals for predicting financial distress, while CGC scores provide useful supplementary insights. CGC scores show marginal significance in moderate and severe distress scenarios, highlighting their limited predictive capability, aligning with the findings of other studies [

5]. This finding aligns with signaling theory, reinforcing Z-Scores’ reliability as critical predictors, while suggesting a secondary, yet complementary, role for governance compliance indicators.

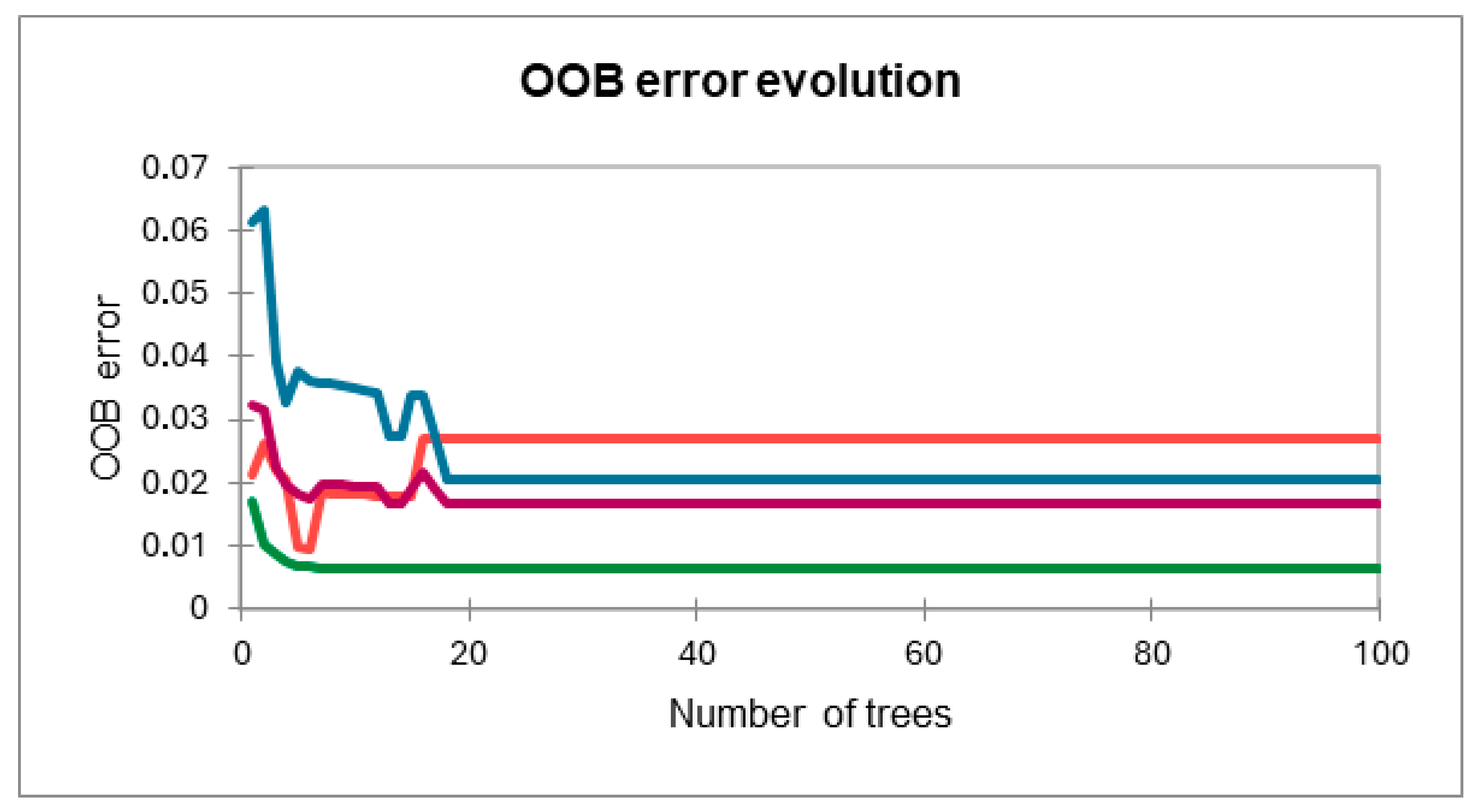

The evolution of the Out-of-Bag (OOB) error rate (

Figure 3) further supports the robustness of the Random Forest model. In the graph, each curve corresponds to a class in the classification problem, displaying how the OOB error for that class decreases as more trees are added, as result safe firms are represented in blue, moderate in magenta, distressed in red, and overall stabilization, in green. Initially, the OOB error decreases rapidly, indicating substantial model improvement as more trees are added. After approximately 20–30 trees, the error rate stabilizes, suggesting minimal additional accuracy gains beyond this point. The relatively flat lines from around 30 to 100 trees confirm the model’s optimal performance, highlighting its stability. Practically, this indicates that employing 100 trees effectively balances computational efficiency with predictive accuracy, reinforcing the reliability and robustness of the chosen Random Forest methodology.

The Random Forest classifier demonstrates strong predictive capability, effectively classifying companies into financial distress categories primarily based on Z-Scores and, to a lesser extent, CGC indicators. The robustness of the Z-Score as a financial health signal highlights its pivotal role in predicting distress, while Corporate Governance Compliance plays a complementary but secondary role. The exceptionally low OOB error rate and high classification accuracy indicate substantial practical utility for stakeholders, facilitating early identification of at-risk firms and enhancing strategic decision-making and risk management. These findings clearly underscore the value of integrating digital technologies in financial distress prediction models, aligning effectively with the research objectives.

The results strongly support the alternative hypothesis (H1). Z-Scores were highly significant predictors, clearly differentiating firms based on financial distress levels. Although CGC Indexes exhibited marginal significance for moderate distress scenarios, their overall predictive role remains complementary rather than independently decisive.

The interplay between CG compliance and financial distress is both structural and dependent by context; acting as a selective signal, its benefits are more pronounced in areas where accountability and resource allocation efficiency are directly observable [

45]. This nuanced perspective adds explanatory power to the Random Forest results and highlights the importance of integrated analytical approaches when assessing corporate viability.

5. Conclusions

This study demonstrates the applicability and robustness of the Random Forest classification model in signaling and predicting financial distress among manufacturing companies listed on the Bucharest Stock Exchange from 2016 to 2022. Consistent with Signaling Theory, the findings confirm that digitally measured Altman Z-Scores and Corporate Governance Compliance (CGC) indicators provide critical signals for stakeholders to identify potential financial distress effectively.

The Altman Z-Score emerged as a dominant, clear, and highly effective quantitative predictor, significantly contributing to accurate distress classification. Firms presenting higher Z-Scores effectively signal financial stability, thereby lowering perceived investment risk. This aligns with the theoretical notion that reliable signaling requires sustained operational excellence, making deceptive signals unlikely.

Conversely, the CGC indicator functioned primarily as a secondary, qualitative governance signal, exhibiting limited predictive strength compared to the Z-Score. While CGC showed modest predictive capability, particularly regarding moderate distress, it nonetheless provided complementary information valuable in scenarios characterized by informational asymmetry. Robust governance mechanisms, such as board independence, board size, and institutional ownership, were found to mitigate the tendency of financially distressed firms to increase leverage [

46]; as a result, governance acts as a stabilizing force, promoting more conservative and disciplined financial decisions during periods of volatility.

The Random Forest model exhibited exceptional predictive accuracy, with an overall accuracy of 98.3%, demonstrating particular strength in correctly classifying no distress (97.32%), moderate distress (97.96%), and severe distress scenarios (99.38%). The low Out-of-Bag (OOB) misclassification rate (1.7%) underscores the reliability and practical utility of the chosen analytical approach. Random Forest models offer a stable and resilient alternative to traditional Logit models in default prediction [

46], with advantages such as tolerance to multicollinearity, omitted variable bias, and non-linearity, characteristics also confirmed in our analysis.

From a signaling perspective, the considerable importance of Z-Scores, supported by their high variable importance measures, highlights the essential role of clear, quantitative financial signals in distress prediction. Meanwhile, the limited contribution of CGC signals suggests the need for firms to enhance qualitative governance indicators for improved signaling effectiveness.

Practically, the analysis highlights persistent financial distress within a significant portion of the manufacturing sector, despite relatively good governance compliance levels (approximately 65%). This underscores the need for proactive, integrated signaling strategies involving both robust financial performance and strong governance practices to enhance financial resilience.

This research addresses the central research question by confirming the importance of digital financial and governance signals in financial distress prediction. The results emphasize the necessity for firms to strategically manage and communicate both financial and governance health to stakeholders. Investors, creditors, and policymakers can leverage these findings to improve risk assessment methodologies, strengthen financial stability, and promote enhanced corporate governance within Romania’s manufacturing sector.

Recent studies in the literature emphasize how global economic shocks, particularly the COVID-19 pandemic, have exposed weaknesses in corporate risk management frameworks, revealing that firms with strong governance attributes are less exposed to corporate risk and better equipped to navigate systemic crises, demonstrating that Corporate Governance Compliance not only predicts financial distress but also operates as a selective yet powerful signal of financial resilience [

47].

Our findings reflect the regulatory, economic, and governance environment characteristic of the context of Romanian listed manufacturing companies subject to the Romanian Corporate Governance Code during the selected reporting period. While the results offer valuable insights into the relationship between governance compliance and financial distress within this setting, we acknowledge that caution is required when extrapolating these findings to other industries, jurisdictions, or time periods. Differences in governance frameworks, financial disclosure requirements, or macroeconomic conditions may affect model performance and variable importance.

Nevertheless, this study acknowledges certain other limitations, including potential measurement errors due to the manual data collection of Corporate Governance Compliance information and the simplistic binary approach to governance assessment. The lack of more nuanced qualitative governance measures, such as managerial expertise and strategic decision-making quality, further limits comprehensiveness. Future research could address these gaps by incorporating detailed governance metrics, employing advanced machine learning techniques, and exploring additional qualitative signals.

The study provides a direct and robust response to the research question, underlining the critical role of both financial and corporate governance signals in predicting financial distress. By employing the Random Forest model, its high predictive accuracy, and its ability to rank variable importance, the analysis offers deeper insights into the complex interplay between firm performance and governance structures; its methodological advantage enhances interpretability, making the findings not only statistically sound but also highly actionable.

The results underscore the strategic importance for companies to actively manage both financial health and governance quality, thereby sending consistent signals of stability and resilience to market participants. For investors and creditors, the model’s ability to highlight key risk drivers supports more refined and data-informed risk assessment frameworks. Likewise, policymakers can leverage these insights to design targeted regulations and policies that strengthen financial stability and promote better compliance with corporate governance standards, particularly within the Romanian manufacturing sector, where such measures can have significant economic impact.

In conclusion, by improving signaling practices across financial and governance dimensions and by utilizing machine learning techniques, firms can more effectively communicate their financial health, mitigate information asymmetries, and foster greater financial stability within emerging markets.

,

,

{kind=link}

{kind=link}

{kind=link}