The Economics of Bulk Water Transport in Southern California

Abstract

:1. Introduction

2. Market Participants and Water Availability

2.1. Humboldt Bay MWD’s Potential Water Exports

2.2. Municipal Water Agencies Seeking New Water Supply Sources

2.2.1. San Francisco Public Utilities Commission

{kind=link}

| Agency | San Diego | San Francisco | Santa Cruz |

|---|---|---|---|

| End-use and wholesale customers, 2010 | 3.11 million | 2.60 million | 91,000 |

| 2010 Deliveries (MCM) | 697.88 | 313.81 | 13.33 |

| 2030 Projected Population | 3.76 million | 2.99 million | 98,000 |

| 2030 Normal Year Projected Demand (MCM) | 929.68 | 363.74 | 15.31 |

| New Resources Brought On-Line to Meet Projected Demand | Agricultural conservation and transfers; canal lining; purchases through MWD; ocean-water desalination; groundwater storage | Water transfers; ocean-water desalination; additional recycled water, groundwater, and conservation | Conservation; use curtailment in drought years; ocean-water desalination |

| Proposed Desal Facility (MCM) | 69.07 | 69.07 | 3.45 |

| Estimated Desal Costs ($/m3) | 1.77 | 0.31 | 3.22 |

| Distance from HBMWD (nautical·km) | 1048 | 355 | 435 |

| Data Sources | [17] | [16] | [18] |

2.2.2. City of Santa Cruz Water District

2.2.3. San Diego County Water Authority

3. Case Study

3.1. Water Supply Augmentation through Ocean-Water Desalination

| San Diego SDCWA | San Francisco SFPUC | Santa Cruz SCWD | |

|---|---|---|---|

| Total Capital Cost ($millions) | 1003 | 168.5 | 120 |

| Annual Capital Payment ($millions) | 63.5 | 10.68 | 7.60 |

| Annual Operating Costs ($millions) | 58.86 | 11.39 | 3.82 |

| Annual Total Payments ($millions) | 122.41 | 22.07 | 11.42 |

| Expected Plant Yield (MCM/yr) | 69.07 | 69.07 | 3.45 |

| Annual Per-Unit Cost ($/m3) | 1.77 | 0.32 | 3.31 |

| Data Sources | [17] | [16] | [18] |

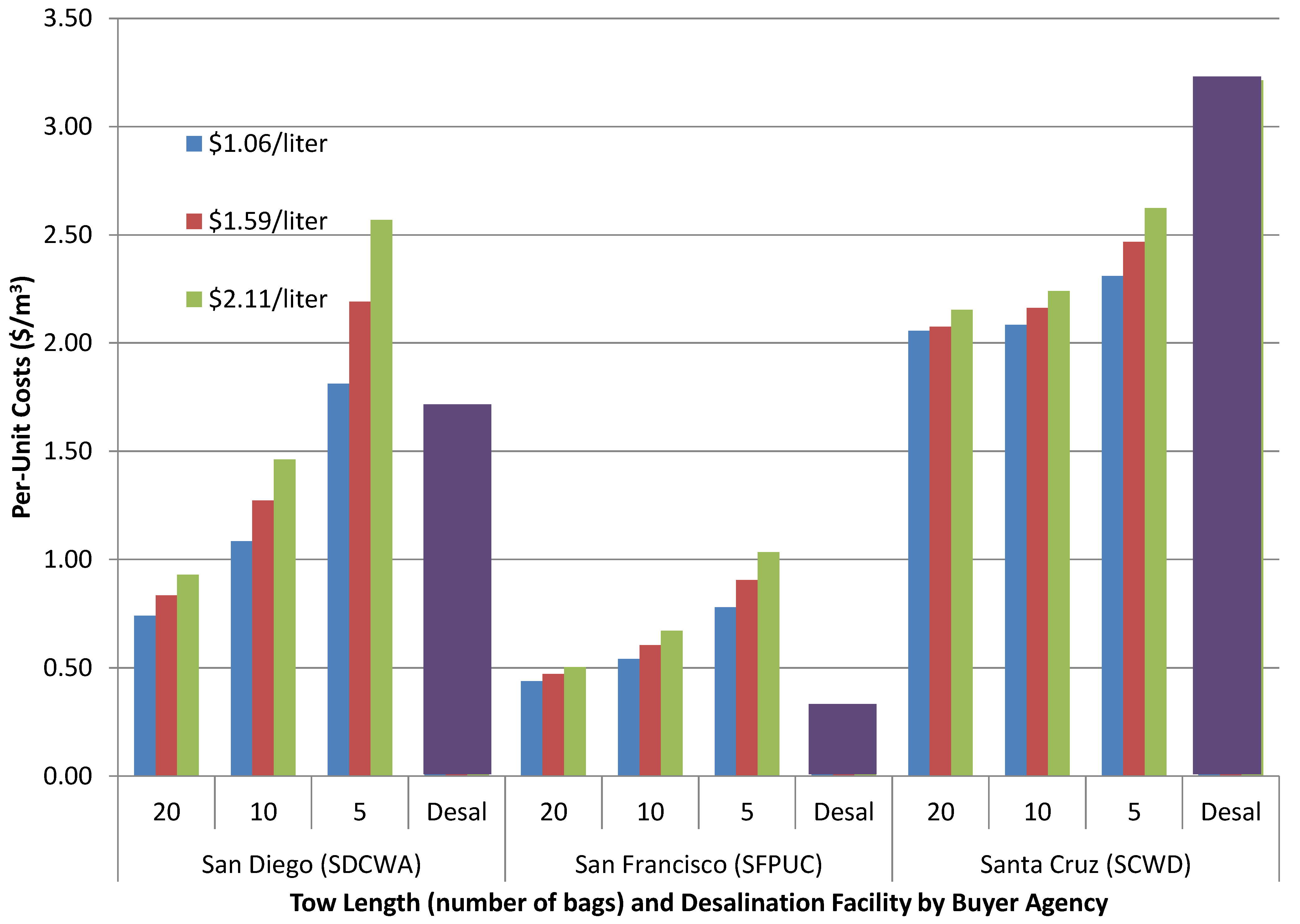

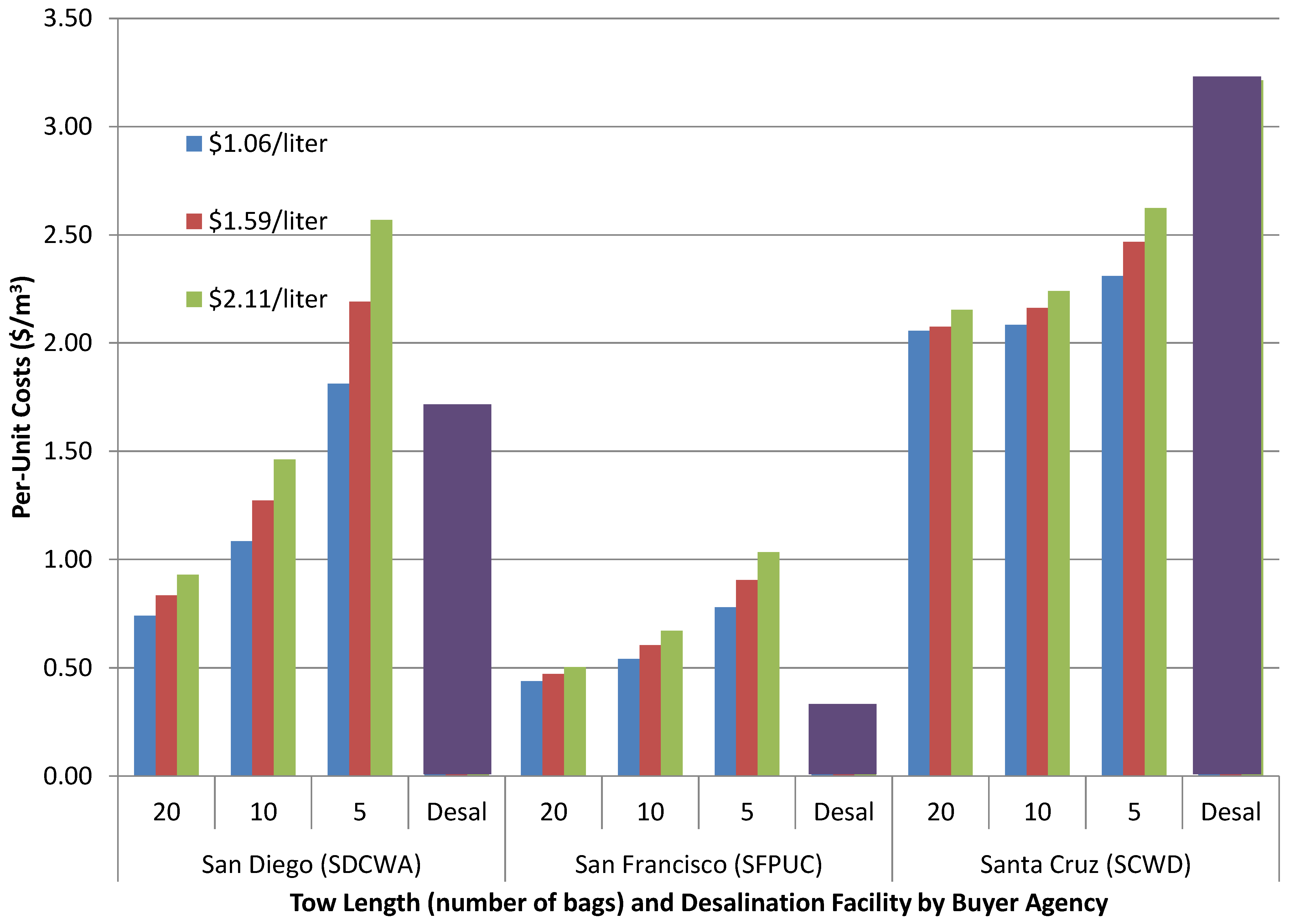

3.2. Bulk Water Transport

| Agency | Units | San Diego SDCWA | San Francisco SFPUC | Santa Cruz SCWD |

|---|---|---|---|---|

| Quantity | m3/yr | 69,074,936 | 69,074,936 | 3,453,747 |

| Number of tugs | 9 | 5 | 1 | |

| Number of bags per trip | 20 | 20 | 14 | |

| Number of trips per year | 203 | 36 | 14 | |

| Water cost | $/m3 | 0.05 | 0.05 | 0.05 |

| Fuel cost | $/m3 | 0.19 | 0.06 | 0.11 |

| Other variable costs | $/m3 | 0.28 | 0.17 | 0.21 |

| Capital cost | $/m3 | 0.21 | 0.15 | 1.68 |

| Total per-unit cost | $/m3 | 0.74 | 0.44 | 2.06 |

| Fuel as % of per-unit cost | % | 26% | 15% | 5% |

| Total capital costs | $in millions | 106 | 148 | 58 |

3.3. Cost-Effectiveness of Water Bags versus Desalination

4. Incorporating Reliability

4.1. Yield Risk

4.2. Cost Risk

4.3. Environmental/Regulatory Risk

4.4. New Technology/Adoption Risk

5. Discussion and Conclusions

Acknowledgments

Author Contributions

Conflicts of Interest

References

- California Department of Water Resources. Managing an Uncertain Future: Climate Change Adaptation Strategies for California’s Water. Available online: www.water.ca.gov/climatechange/articles.cfm (accessed on 1 October 2014).

- Jenkins, M.W.; Lund, J.R.; Howitt, R.E.; Draper, A.J.; Msangi, S.M.; Tanaka, S.K.; Ritzema, R.S.; Marques, G.F. Optimization of California’s water supply system: Results and insights. J. Water Resour. Plan. Manag. 2004, 130, 271–280. [Google Scholar] [CrossRef]

- Young, R. Why are there so few transactions among water users? Am. J. Agric. Econ. 1986, 68, 1143–1151. [Google Scholar] [CrossRef]

- Lach, D.; Ingram, H.; Rayner, S. Maintaining the status quo: How institutional norms and practices create conservative water organizations. Tex. Law Rev. 2005, 83, 2027–2053. [Google Scholar]

- Wolff, G.; Kasower, S. The Portfolio Approach to Water Supply: Some Examples and Guidance for Planners. Available online: http://www.waterboards.ca.gov/water_issues/programs/grants_loans/water_recycling/docs/econ_tskfrce/10.pdf (accessed on 1 August 2014).

- Hansen, K.; Howitt, R.; Williams, J. Water trades in the western United States: Risk, speculation, and property rights. In Water Trading and Global Water Scarcity: International Perspectives; Maestu, J., Ed.; RFF Press Water Policy Series: New York, NY, USA, 2013; pp. 55–67. [Google Scholar]

- Booker, J.F.; Young, R.A. Modeling intrastate and interstate markets for Colorado River water resources. J. Environ. Econ. Manag. 1994, 26, 66–87. [Google Scholar] [CrossRef]

- Ward, F.; Pulido-Velazquez, M. Economic costs of sustaining water supplies: Findings from the Rio Grande. Water Resour. Manag. 2012, 26, 2883–2909. [Google Scholar] [CrossRef]

- Winzler and Kelly Consulting Engineers. Humboldt County General Plan: Water Resources Technical Report (Draft); Prepared for the County of Humboldt Community Development Division; Eureka, CA, USA, 2007, pp. 1–83. Available online: http://humboldtgov.org/DocumentCenter/Home/View/1865 (accessed on 25 July 2014).

- Stillwater Sciences. Mad River Watershed Assessment. Available online: http://www.waterboards.ca.gov/northcoast/water_issues/programs/tmdls/mad_river/pdf/120329/FINAL_PDF_MRWA.PDF (accessed on 25 July 2014).

- Rische, C.; Humboldt Bay Municipal Water District, Eureka, CA USA. Personal communication, 18 January 2013.

- Getches, D.H. Water Law in a Nutshell, 4th ed.; Thomson/Reuters: St. Paul, MN, USA, 2009. [Google Scholar]

- Hanak, E. Stopping the drain: Third party responses to California’s water market. Contemp. Econ. Policy 2005, 23, 59–77. [Google Scholar] [CrossRef]

- Humboldt Bay Municipal Water District. Water Resource Planning, Implementation Plan to Evaluate and Advance Recommended Water Use Options. Available online: http://www.water.ca.gov/urbanwatermanagement/2010uwmps/Humboldt%20Bay%20Municipal%20WD/Appendix%20C%20-%20WRP%20Implementation%20Plan%20-%20Final%20Draft%20%28to%20Board%20on%20April%2014,%202011%29.pdf (accessed on 1 October 2014).

- California Urban Water Management Planning Act 1983, California Water Code Division 6, Part 2.6, Sections 10610 through 10656. 21 September 1983.

- San Francisco Public Utilities Commission. 2010 Urban Water Management Plan. Available online: http://www.sfwater.org/Modules/ShowDocument.aspx?documentID=1055 (accessed on 2 December 2013).

- San Diego County Water Authority Water Resources Department (SDCWA). 2010 Urban Water Management Plan. Available online: http://www.sdcwa.org/sites/default/files/files/water-management/2010UWMPfinal.pdf (accessed on 3 December 2013).

- City of Santa Cruz Water Department. 2010 Urban Water Management Plan. Available online: http://www.cityofsantacruz.com/Modules/ShowDocument.aspx?documentid=24687 (accessed on 3 December 2013).

- Hodges, A.J. The Economics of Bulk Water Transport in Southern California. Master’s Thesis, University of Wyoming, Laramie, Wyoming, 12 December 2014. [Google Scholar]

- Zhou, Y.; Tol, R.S.J. Evaluating the cost of desalination and water transport. Water Resour. Res. 2005, 41. [Google Scholar] [CrossRef]

- Desalination Tracker. Glob. Water Intell. 2014, 15, 43–54.

- Karagiannis, I.; Soldatos, P. Water desalination cost literature: Review and assessment. Desalination 2008, 223, 448–456. [Google Scholar] [CrossRef]

- Shannon, M.; Bohn, P.; Elimelech, M.; Georgiadis, J.; Marinas, B.; Mayes, A. Science and technology for water purification in the coming decades. Nature 2008, 452, 301–310. [Google Scholar] [CrossRef] [PubMed]

- Greenlee, L.; Lawler, D.; Freeman, B.; Marrot, B.; Moulin, P. Reverse osmosis desalination: Water sources, technology, and today’s challenges. Water Res. 2009, 43, 2317–2348. [Google Scholar] [CrossRef] [PubMed]

- Khayet, M. Solar desalination by membrane distillation: Dispersion in energy consumption analysis and water production (a review). Desalination 2013, 308, 89–101. [Google Scholar] [CrossRef]

- Wade, N. Distillation plant development and cost update. Desalination 2001, 136, 3–12. [Google Scholar] [CrossRef]

- Fiorenza, G.; Sharma, V.; Braccio, G. Techno-economic evaluation of a solar powered water desalination plant. Energy Convers. Manag. 2003, 44, 2217–2240. [Google Scholar] [CrossRef]

- Bondbuyer Indexes: Revenue Bond Index 2010–2013. Available online: http://www.bondbuyer.com/apps/custom/msa_search.php?product=bbi_averages (accessed on 1 October 2014).

- Cooley, H.; Ajami, N. Key Issue for Seawater Desalination in California: Cost and Financing; Pacific Institute: Oakland, CA, USA, 2012. Available online: http://pacinst.org/wp-content/uploads/sites/21/2013/02/financing_final_report3.pdf (accessed on 1 October 2014).

- Bay Area Regional Desalination Project: Pilot Testing, Appendix I Full-Scale Cost Estimates; Prepared by M. Lee Corporation, San Francisco, CA, USA, 2010; Available online: http://www.regionaldesal.com/downloads/Final%20Pilot%20Study%20Report%202/BARDP%20Pilot%20Report%20APPENDIX%20I%20Mar%2010%20Cost%20Estimates.pdf (accessed on 1 October 2014).

- City of Santa Cruz and Soquel Creek Water District. Agreement Endorsing Recommendations of Joint Task Force on Seawater Desalination Facility. Available online: http://www.scwd2desal.org/documents/Draft_EIR/Appendices/AppendixP.pdf (accessed on 25 July 2014).

- San Diego County Water Authority. Seawater Desalination: The Carlsbad Desalination Project. Available online: http://www.sdcwa.org/sites/default/files/desal-carlsbad-fs.pdf (accessed on 1 October 2014).

- Haddad, M.; Mizyed, N. Non-conventional options for water supply augmentation in the Middle East: A case study. Water Int. 2004, 29, 232–242. [Google Scholar] [CrossRef]

- Barlow, M.; Clarke, T. Blue Gold: The Fight to Stop the Corporate Theft of the World’s Water; The New Press: New York, NY, USA, 2005. [Google Scholar]

- Economic Fisheries Information Network. West Coast and Alaska Marine Fuel Prices 2011–2013; Pacific States Marine Fisheries Commission: Portland, OR, 2013. Available online: http://www.psmfc.org/efin/docs/2013FuelPriceReport.pdf (accessed on 25 July 2014).

- United States Bureau of Reclamation. Colorado River Basin Water Supply and Demand Study, Executive Summary. Available online: http://www.usbr.gov/lc/region/programs/crbstudy/finalreport/Executive%20Summary/CRBS_Executive_Summary_FINAL.pdf (accessed on 26 November 2013).

- United States Bureau of Reclamation. Colorado River Basin Water Supply and Demand Study, Appendix F4: Option Characterization—Importation. Available online: http://www.usbr.gov/lc/region/programs/crbstudy/finalreport/Executive%20Summary/CRBS_Executive_Summary_FINAL.pdf (accessed on 26 November 2013).

- Quinlan, B.; Thompson, G. Technical Evaluation of Options for Long-Term Augmentation of the Colorado River System: Water Imports Using Ocean Routes. Available online: https://www.usbr.gov/lc/region/programs/crbstudy/longtermaugmentationrpt.pdf (accessed on 25 July 2014).

© 2014 by the authors; licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Hodges, A.; Hansen, K.; McLeod, D. The Economics of Bulk Water Transport in Southern California. Resources 2014, 3, 703-720. https://doi.org/10.3390/resources3040703

Hodges A, Hansen K, McLeod D. The Economics of Bulk Water Transport in Southern California. Resources. 2014; 3(4):703-720. https://doi.org/10.3390/resources3040703

Chicago/Turabian StyleHodges, Andrew, Kristiana Hansen, and Donald McLeod. 2014. "The Economics of Bulk Water Transport in Southern California" Resources 3, no. 4: 703-720. https://doi.org/10.3390/resources3040703

APA StyleHodges, A., Hansen, K., & McLeod, D. (2014). The Economics of Bulk Water Transport in Southern California. Resources, 3(4), 703-720. https://doi.org/10.3390/resources3040703