An Analysis of Regulatory Strategies for Recycling and Re-Use of Metals in Australia

Abstract

:1. Introduction

2. Changing Policy Contexts

“That is restorative or regenerative by intention and design. It replaces the “end-of-life” concept with restoration, shifts towards the use of renewable energy, eliminates the use of toxic chemicals, which impair reuse, and aims for the elimination of waste through the superior design of materials, products, systems, and, within this, business models.”[6]

- (1)

- Influence the economics of any part of the recycling chain; with particular consideration of policies affecting the cost of recycling activities and security of supply, including the relative cost of alternatives, taxation, subsidies, trade restrictions, labour regulation and energy costs;

- (2)

- Provide the incentives and means for stakeholders to exchange information and co-operate; with particular focus upon Extended Producer Responsibility (EPR);

- (3)

- Enhance the role of government as a stakeholder in the chain; with particular emphasis on waste collection and processing infrastructure provided by local government;

- (4)

- Coordinate interactions between relevant policy makers; with particular focus upon better cooperation between relevant government agencies to create a more holistic approach ([3], Chapter 7).

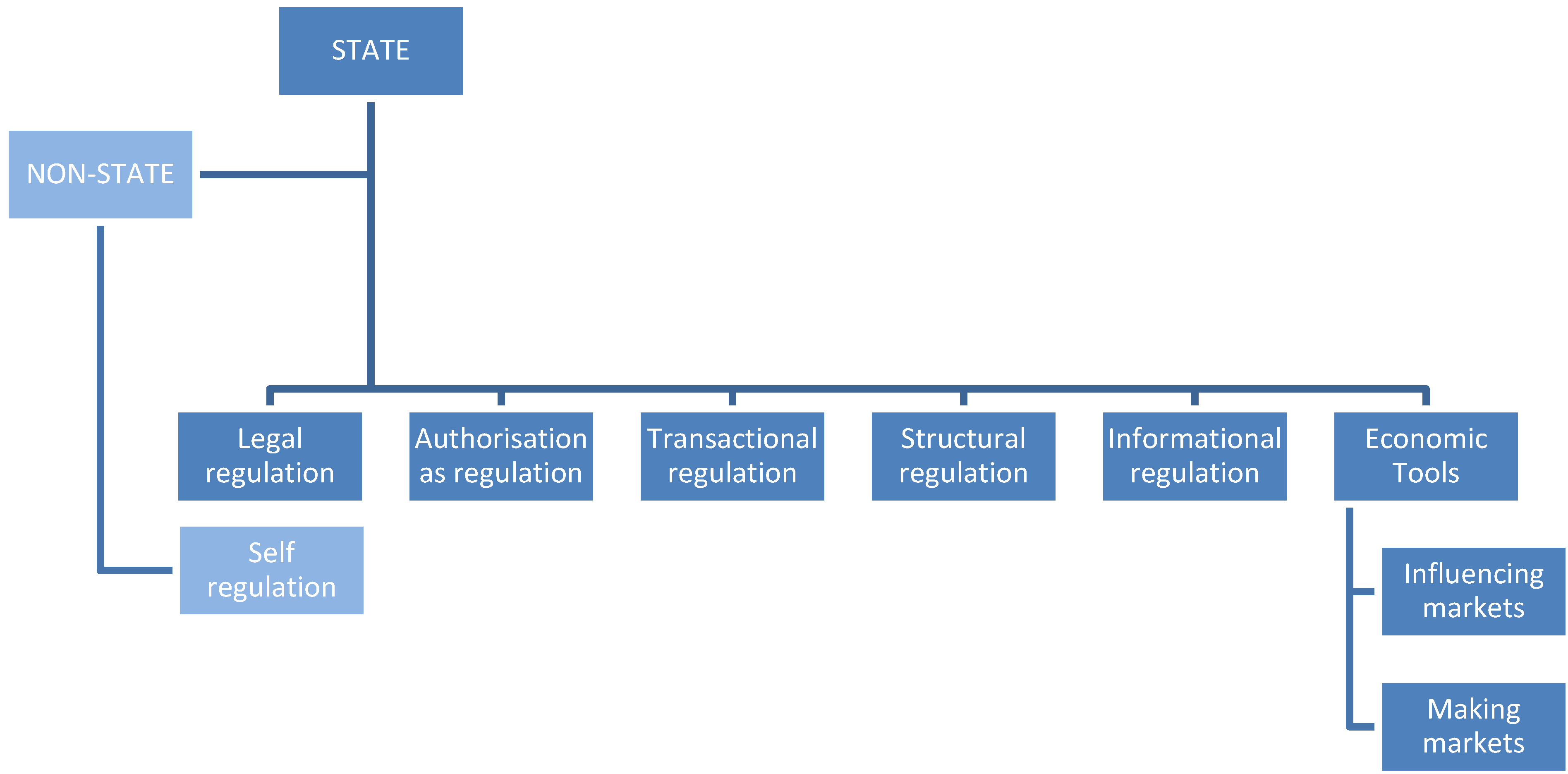

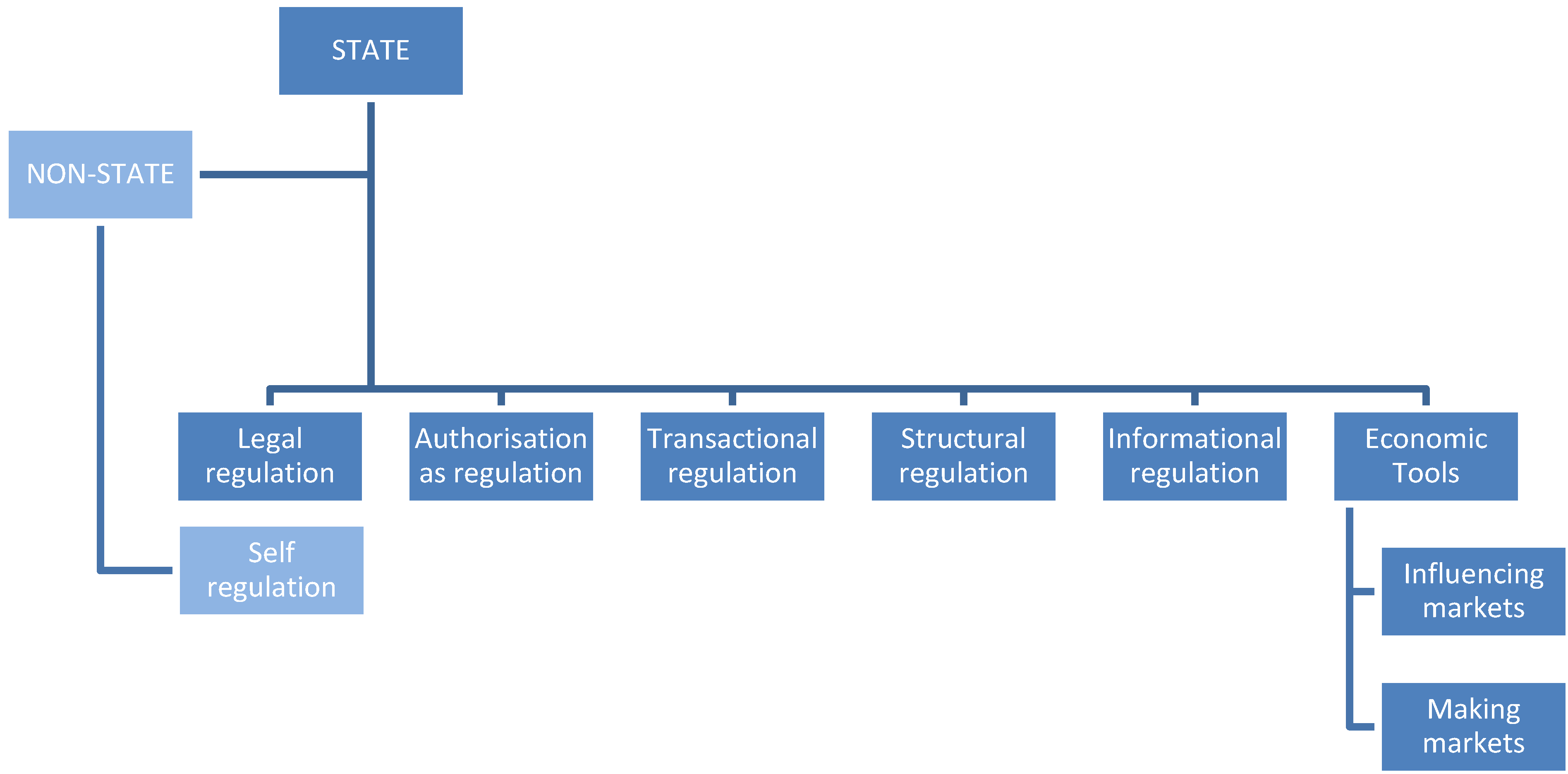

3. The Purpose and Approaches of Regulation

3.1. What Is Regulation

3.2. Trends in Environmental Regulation

3.2.1. Command and Control Approaches

3.2.2. Responsive Regulation

3.2.3. Outcome Based Regulation

3.2.4. Management Based Regulation

3.2.5. Reflexive Regulation

- (1)

- exploration and extraction;

- (2)

- processing and manufacturing; and

- (3)

- disposal and re-use.

4. The Regulatory Framework for the Life-Cycle of Minerals and Metals in Australia

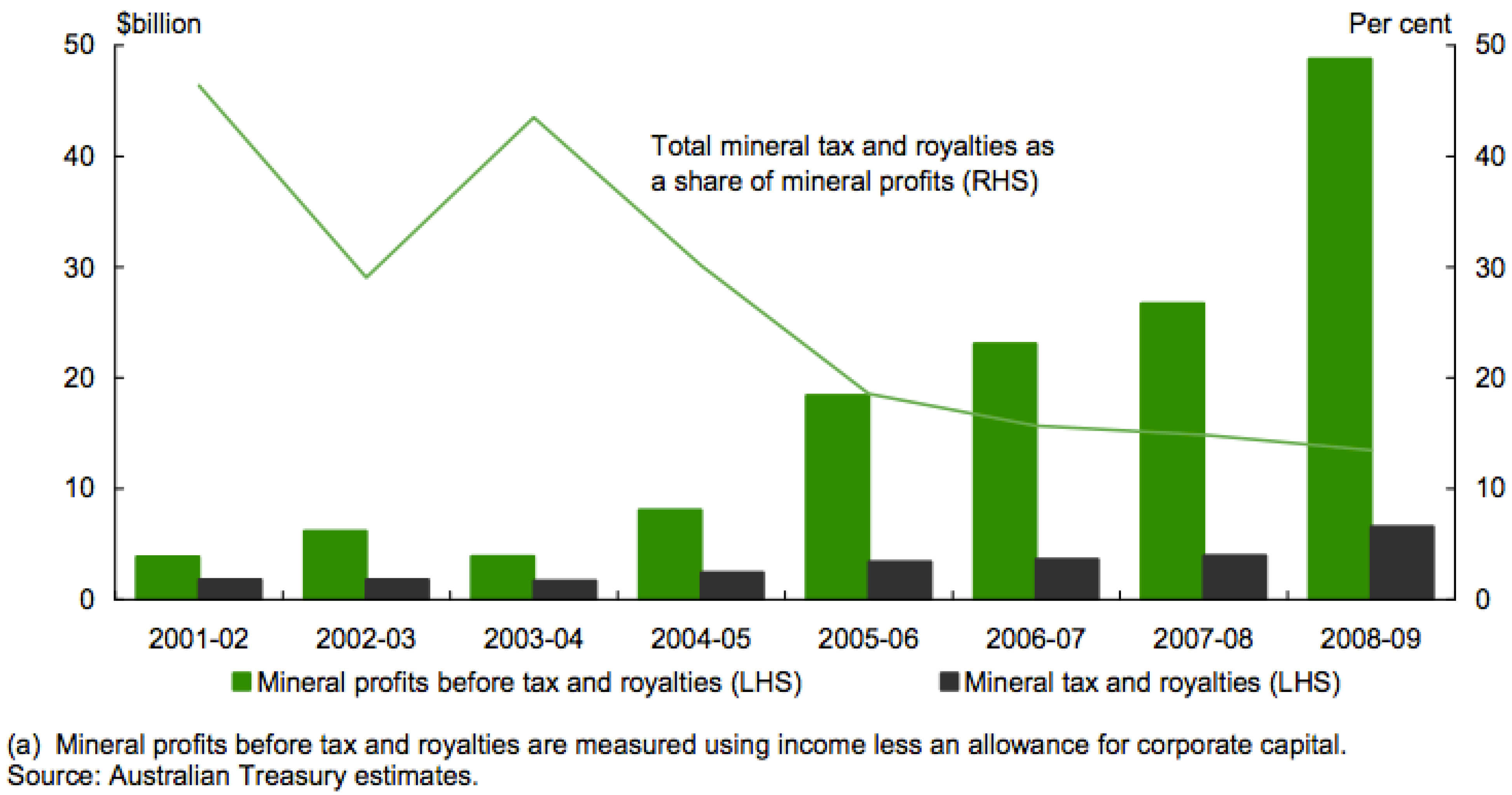

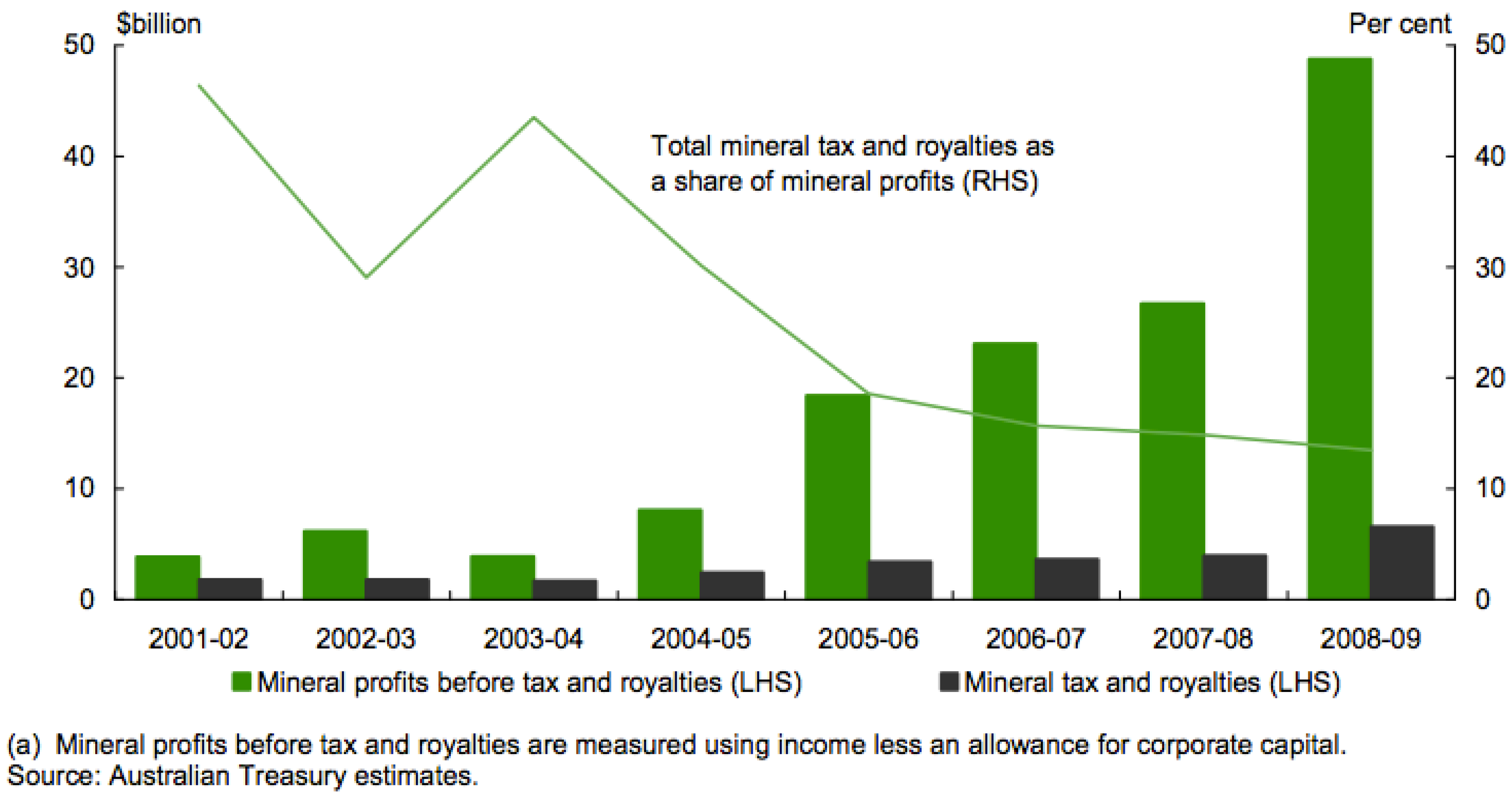

4.1. Regulation during Exploration and Extraction

“The NPI should operate principally as an instrument of environmental management and performance assessment, or to consider it principally as a more general tool for raising public and industry awareness of emissions to our environment and the need for cleaner production and waste minimisation. The former requires a higher level of funding to generate high quality data and more extensive data sets than the latter, but its effectiveness increases. It appears to be the direction in which international systems are headed.”

- advance understanding of the properties of metals and minerals and their life-cycle effects on human health and the environment;

- conduct or support research and innovation that promotes the use of products and technologies that are safe and efficient in their use of energy, natural resources and other materials;

- develop and promote the concept of integrated materials management throughout the metals and minerals value chain;

- provide regulators and other stakeholders with scientifically sound data and analysis regarding our products and operations as a basis for regulatory decisions;

- support the development of scientifically sound policies, regulations, product standards and material choice decisions that encourage the safe use of mineral and metal products.”

4.2. Regulation during Processing and Manufacture Phase

- (1)

- reasonable access to collection services in metropolitan, inner regional, outer regional and remote areas must be provided (free of charge to households);

- (2)

- certain recycling targets for each product in the class must be met in each year; and

- (3)

- a material recovery target must be met in each year (from 1 July 2014) ([58], Regulations 3.01–3.03).

4.3. Regulation of Disposal and Re-Use of Metals

5. Observations and Analysis

{kind=link}

{kind=link}

| (1) Exploration and Extraction Phase | |

|---|---|

| Regulatory Scheme (legislative instruments) | Regulatory Strategy Applied |

| State Government (Victoria) | |

| |

| Commonwealth Government | |

| |

| Industry self-regulation | |

| |

| (2) Processing and Manufacturing Phase | |

| State Government (Victoria) | |

| |

| Commonwealth Government | |

| |

| (3) Disposal and Re-Use Phase | |

| State Government (Victoria) | |

| |

| Commonwealth Government | |

| |

| International agreements | |

| |

6. Conclusions

References

- Graedel, T.E. On the future availability of energy metals. Annu. Rev. Mater. Res. 2011, 41, 323–335. [Google Scholar] [CrossRef]

- Michaux, S. Peak Mining & Implications for Natural Resource Management; Sustainable Population Institute of Australia: Canberra, Australia, 2013. [Google Scholar]

- Reuter, M.A.; Hudson, C.; van Schaik, A.; Heiskanen, K.; Meskers, C.; Hageliken, C. Metal Recycling: Opportunities, Limits, Infrastructure, a Report of the Working Group on Global Metals Flows to the International Resource Panel; United Nations Environment Program, International Resources Panel: Paris, France, 2013. [Google Scholar]

- Commonwealth of Australia. National Waste Policy: Less Waste More Resources; Department of the Environment, Water, Heritage and the Arts: Canberra, Australia, 2009.

- United Nations Conference on the Environment and Development (UNCED). Declaration of the Conference Held at Rio De Janiero from 3 to 14 June 1992 (“The Rio Declaration”); United Nations General Assembly: New York, NY, USA, 1992. [Google Scholar]

- Towards the Circular Economy; Economic and Business Rationale for an Accelerated Transition; Ellen MacArthur Foundation (EMF): Cowes, UK, 2012; Volume 1.

- Council of Australian Governments. Competition Principles Agreement—11 April 1995 (As Amended to 13 April 2007); Commonwealth of Australia: Canberra, Australia, 1995.

- Regulation Taskforce. In Rethinking Regulation: Report of the Taskforce on Reducing Regulatory Burdens on Business; Commonwealth of Australia: Canberra, Australia, 2006.

- Council of Australian Governments. Best Practice Regulation; A Guide for Ministerial Councils and National Standard Setting Bodies; Commonwealth of Australia: Canberra, Australia, 2007.

- Freiberg, A. The Tools of Regulation; The Federation Press: Sydney, Australia, 2010; p. 319. [Google Scholar]

- Gunningham, N.; Sinclair, D.; Grabosky, P. Instruments for Environmental Protection. In Smart Regulation: Designing Environmental Policy; Clarendon Press: Oxford, UK, 1998; pp. 37–91. [Google Scholar]

- Gumley, W.; Stoianoff, N. Carbon pricing options for a post-Kyoto response to climate change in Australia. Fed. Law Rev. 2011, 39, 131–160. [Google Scholar]

- Clean Air Act of 1970. 42 USC 7401-7626, 1970.

- Ayres, I.; Brathwaite, J. Responsive Regulation: Transcending the Deregulation Debate; Oxford University Press: New York, NY, USA, 1992. [Google Scholar]

- Porter, M.; van der Linde, C. Green and competitive: Ending the stalemate. Harv. Bus. Rev. 1995, 73, 120–134. [Google Scholar]

- Hirsch, D.D. Green business and the importance of reflexive law: What Michael Porter didn’t say. Adm. Law Rev. 2010, 62, 1063–1126. [Google Scholar]

- Coglianese, C.; Lazer, D. Management-based regulation: Prescribing private management to achieve public goals. Law Soc. Rev. 2003, 37, 691–730. [Google Scholar] [CrossRef]

- Teubner, G. Substantive and reflexive elements in modern law. Law Soc. Rev. 1983, 17, 239–285. [Google Scholar] [CrossRef]

- Dunphy, D.C.; Griffiths, A.; Benn, S. Organizational Change for Corporate Sustainability: A Guide for Leaders and Change Agents of the Future; Routledge: London, UK, 2003. [Google Scholar]

- Mineral Resources (Sustainable Development) Act (Vic). No. 92, 1990.

- Bates, G. Environmental Law in Australia, 8th ed.; LexisNexis: Chatswood, Australia, 2013. [Google Scholar]

- Victorian Government, Energy and Earth Resources. Get a Licence. Available online: http://www.energyandresources.vic.gov.au/earth-resources/licensing-and-approvals/minerals/get-a-licence (accessed on 17 February 2014).

- Mineral Resources (Sustainable Development) (Minerals Industries) Regulations 2013 (Vic). S.R No. 216, 2013.

- Australian Government. GST Distribution Review, Final Report; Commonwealth of Australia: Canberra, Australia, 2012.

- Petroleum Resource Rent Tax Assessment Act 1987 (Cth). No. 142, 1987.

- Mineral Resources Rent Tax Act 2012 (Cth). No. 13, 2012.

- Environment Effects Act 1978 (Vic). No. 9135, 1978.

- Victorian Government. Ministerial Guidelines for Assessment of Environmental Effects under the Environment Effects Act 1978; Department of Sustainability and Environment: Melbourne, Australia, 2006.

- Environmental Protection and Biodiversity Conservation Act 1999 (Cth). No. 91, 1999.

- International Association for Impact Assessment and the Institute of Environmental Assessments. Principles of Environmental Impact Assessment Best Practice; International Association for Impact Assessment: Fargo, ND, USA, 1999. [Google Scholar]

- Mining Act 1978 (WA). No. 107, 1978.

- Tarrant, J. Ownership of mining product, tailings and minerals. Aust. Resour. Energy Law J. 2005, 24, 321–330. [Google Scholar]

- Australian Government. National Environment Protection (National Pollutant Inventory) Measure 1998; Commonwealth of Australia: Canberra, Australia, 1998.

- Emergency Planning and Community Right-to-Know Act of 1984. 42 USC 11004-11049, 1984.

- Environment Link. Review of the National Pollutant Inventory; Department of Environment and Heritage: Canberra, Australia, 2005.

- Commonwealth of Australia. The Australian Atlas of Mineral Resources, Mines, and Processing Centres. Available online: http://www.australianminesatlas.gov.au/index.html (accessed on 17 February 2014).

- KPMG International. The KPMG Survey of Corporate Responsibility Reporting 2013; KPMG International Cooperative: Amstelveen, The Netherlands, 2013. [Google Scholar]

- Equator Principles Association. The Equator Principles III 2013. Available online: http://www.equator-principles.com/index.php/ep3 (accessed on 4 April 2014).

- Dow Jones and RobecoSAM. Dow Jones Sustainability Indeces. Available online: http://www.sustainability-indices.com/index.jsp (accessed on 4 April 2014).

- International Council on Mining and Metals (ICMM). Sustainable Development Framework; A Sustained Commitment to Improved Industry Performance; ICMM: London, UK, 2008. [Google Scholar]

- Henry Review Panel. Australia’s Future Tax System, Report to the Treasurer; Commonwealth of Australia: Canberra, Australia, 2010.

- Australian Government. Statement 5 Revenue, Budget Paper No. 1: Budget Strategy and Outlook 2012–2013; Department of Treasury: Canberra, Australia, 2013.

- Commonwealth of Australia. Tax Expenditures Statement 2012; Department of Treasury: Canberra, Australia, 2013.

- Kohler, A. Henry Tax Review: It’s Politics, Not Reform. Business Spectator, Southbank VIC: Austrilia, 2 May 2010. [Google Scholar]

- Planning and Environment Act 1987 (Vic). No. 45, 1987.

- Environment Protection Act 1970 (Vic). No. 8056, 1970.

- Environment Protection Authority Victoria (EPA Victoria). Past Sustainability Covenants. Available online: http://www.epa.vic.gov.au/our-work/programs/sustainability-covenants/past-sustainability-covenants (accessed on 17 February 2014).

- Delivering Business Benefits from Energy Efficiency: Achievements of EPA Victoria’s Industry Greenhouse Program (Publication 1165); EPA Victoria: Melbourne, Australia, 2007.

- Commonwealth of Australia. Energy Efficiency Opportunities. Available online: http://energyefficiencyopportunities.gov.au (accessed on 17 February 2014).

- Energy Efficiency Opportunities Act 2006 (Cth). No. 31, 2006.

- EREP Toolkit Module 1 of 5: Overview; EPA Victoria: Melbourne, Australia, 2008.

- EPA Annual Report 2012–2013; EPA Victoria: Melbourne, Australia, 2013.

- Victorian Competition and Efficiency Commission. An Inquiry into Victoria’s Regulatory Framework: Strengthening Foundations for the Next Decade, Final Report; State of Victoria: Melbourne, Australia, 2011.

- Regulatory Impact Solutions. In Cessation of Environment and Resource Efficiency Plan (EREP) Program; Regulatory Change Measurement Prepared for Department of Environment and Primary Industries; Department of Environment and Primary Industries, State of Victoria: Melbourne, Australia, 2013.

- Product Stewardship (Oil) Act 2000 (Cth). No 102, 2000.

- Australian Packaging Covenant Council. Australian Packaging Covenant; Commonwealth of Australia: Canberra, Australia, 2010.

- National Environment Protection Council. National Environment Protection (Used Packaging Materials) Measure 2011; Commonwealth of Australia: Canberra, Australia, 2011.

- Product Stewardship Act 2011 (Cth). No. 76, 2011.

- Product Stewardship (Televisions and Computers) Regulations 2011. Select Legislative Instrument No. 200, 2011.

- Australian Government. 2013–14 Product List. Available online: http://www.environment.gov.au/topics/environment-protection/national-waste-policy/product-stewardship/legislation (accessed on 17 February 2014).

- European Parliament. Directive 2012/19/EU of the European Parliament and of the Council of 4 July 2012 on waste electrical and electronic equipment (WEEE). Off. J. Eur. Union 2012, L197, 38–71. [Google Scholar]

- Directive 2000/53/EC of the European Parliament and of the Council on End-of Life Vehicles; European Parliament: Brussels, Belgium, 2000.

- Environment Protection (Industrial Waste Resource) Regulations 2009 (Vic). S.R. No. 77/2009, 2009.

- EPA Victoria. Landfill and Prescribed Waste Levies. Available online: http://www.epa.vic.gov.au/your-environment/waste/landfills/landfill-and-prescribed-waste-levies (accessed on 16 December 2013).

- Brouwer, G.E. Brookland Greens Estate—Investigation into Methane Gas Leaks; Ombudsman Victoria: Melbourne, Australia, 2009.

- Frost, P. Hazardous Waste Management; Victorian Auditor General’s Office: Melbourne, Australia, 2010.

- Krpan, S. Compliance and Enforcement Review: A Review of EPA Victoria’s Approach (Publication 1368); EPA Victoria: Melbourne, Australia, 2011.

- Batagol, C. EPA Delivers on Compliance and Enforcement Review (Publication 1557); EPA Victoria: Melbourne, Australia, 2013.

- State of Victoria. Getting Full Value: The Victorian Waste and Resource Recovery Policy; Department of Environment and Primary Industry: Melbourne, Australia, 2013.

- Barnaby, J.; Polhill, J. Take-Back to the Future: Progressing Waste Paint and Handheld Battery Stewardship Schemes in Australia. In Proceedings of WasteMINZ Conference 2013, Rotorua, New Zealand, 22 October 2013.

- United Nations Environment Program. 1989 Basel Convention on the Control of Transboundary Movements of Hazardous Wastes and Their Disposal; United Nations Environment Program: Basel, Switzerland, 1989. [Google Scholar]

- Gaba, J.M. Exporting waste: Regulation of the export of hazardous waste from the United States. William Mary Environ. Law Policy Rev. 2012, 36, 405–490. [Google Scholar]

- Hazardous Waste (Regulation of Exports and Imports) Act 1989 (Cth). No. 6, 1990.

- National Environment Protection Council. National Environment Protection (Movement of Controlled Waste Between States and Territories) Measure 2010; Commonwealth of Australia: Canberra, Australia, 2010.

- Kogan, L. ‘Enlightened’ Environmentalism or Disguised Protectionism? Assessing the Impact of EU Precaution-Based Standards on Developing Countries; National Foreign Trade Council: Washington, DC, USA, 2004. [Google Scholar]

- Widawsky, L. In my backyard: How enabling hazardous waste trade to developing nations can improve the basel convention’s ability to achieve environmental justice. Environ. Law 2008, 38, 577–625. [Google Scholar]

- Organisation for Economic Co-operation and Development (OECD). Decision of the Council Concerning the Control of Transboundary Movements of Wastes Destined for Recovery Operations Development—C(2001)107/FINAL; OECD: Paris, France, 2001. [Google Scholar]

- Roos, G. Business model innovation to creatye and capture resource value in future circular material chains. Resources 2014, 3, 248–274. [Google Scholar] [CrossRef]

- Corder, G.D.; Golev, A.; Fyfe, J.; King, S. The status of industrial ecology in Australia: Barriers and enablers. Resources 2013, 3, 340–361. [Google Scholar] [CrossRef]

- O’Reilly, J.T.; Cuzze, L.B. Trash or treasure? Industrial recycling and international barriers to the movement of hazardous wastes. J. Corp. Law 1997, 508–534. [Google Scholar]

© 2014 by the authors; licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution license (http://creativecommons.org/licenses/by/3.0/).

Share and Cite

Gumley, W. An Analysis of Regulatory Strategies for Recycling and Re-Use of Metals in Australia. Resources 2014, 3, 395-415. https://doi.org/10.3390/resources3020395

Gumley W. An Analysis of Regulatory Strategies for Recycling and Re-Use of Metals in Australia. Resources. 2014; 3(2):395-415. https://doi.org/10.3390/resources3020395

Chicago/Turabian StyleGumley, Wayne. 2014. "An Analysis of Regulatory Strategies for Recycling and Re-Use of Metals in Australia" Resources 3, no. 2: 395-415. https://doi.org/10.3390/resources3020395

APA StyleGumley, W. (2014). An Analysis of Regulatory Strategies for Recycling and Re-Use of Metals in Australia. Resources, 3(2), 395-415. https://doi.org/10.3390/resources3020395