Review of Kalman Filter Employment in the NAIRU Estimation

Abstract

1. Introduction

2. Methods

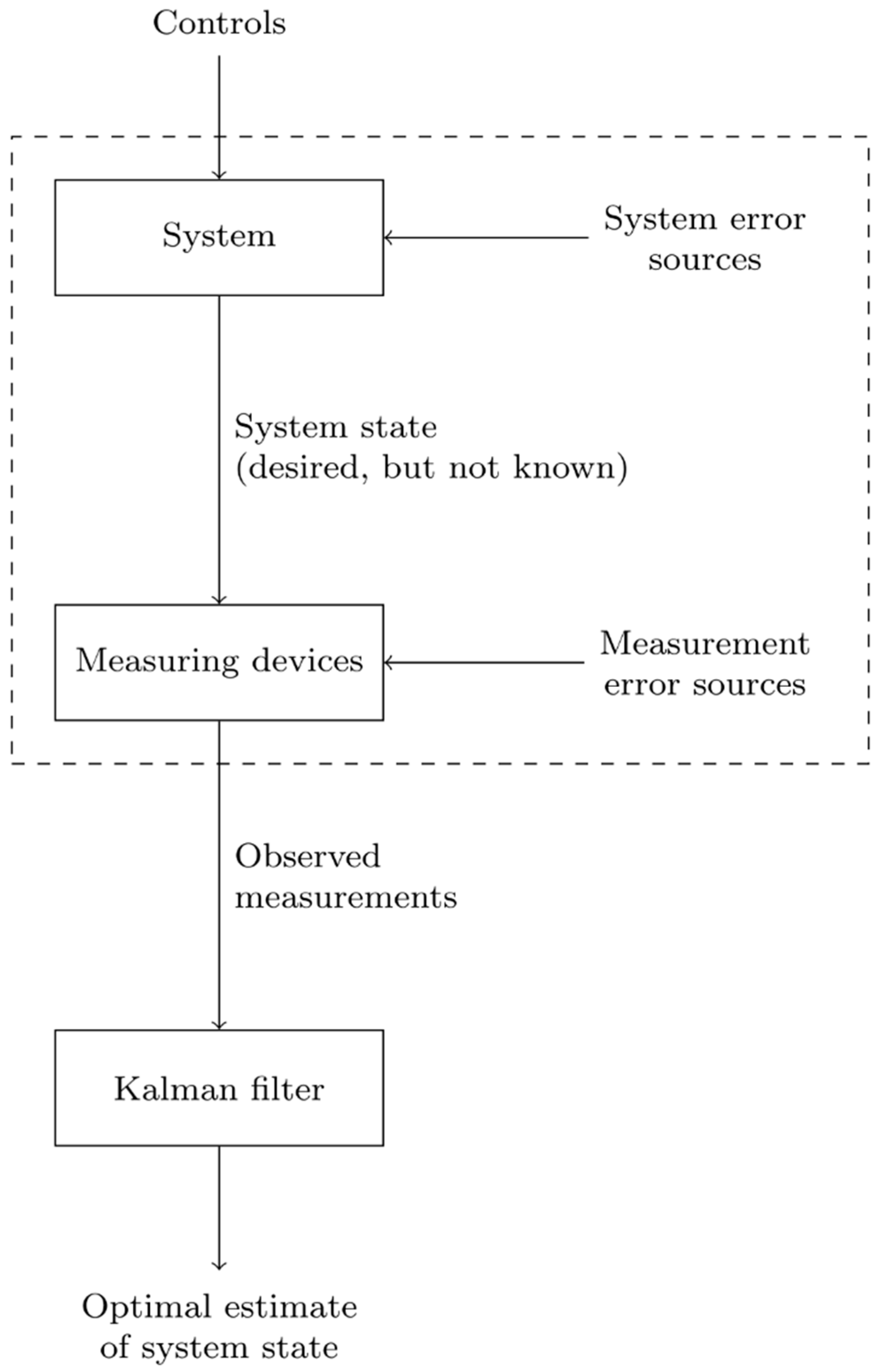

2.1. Kalman Filter

Algorithm of the Kalman Filter

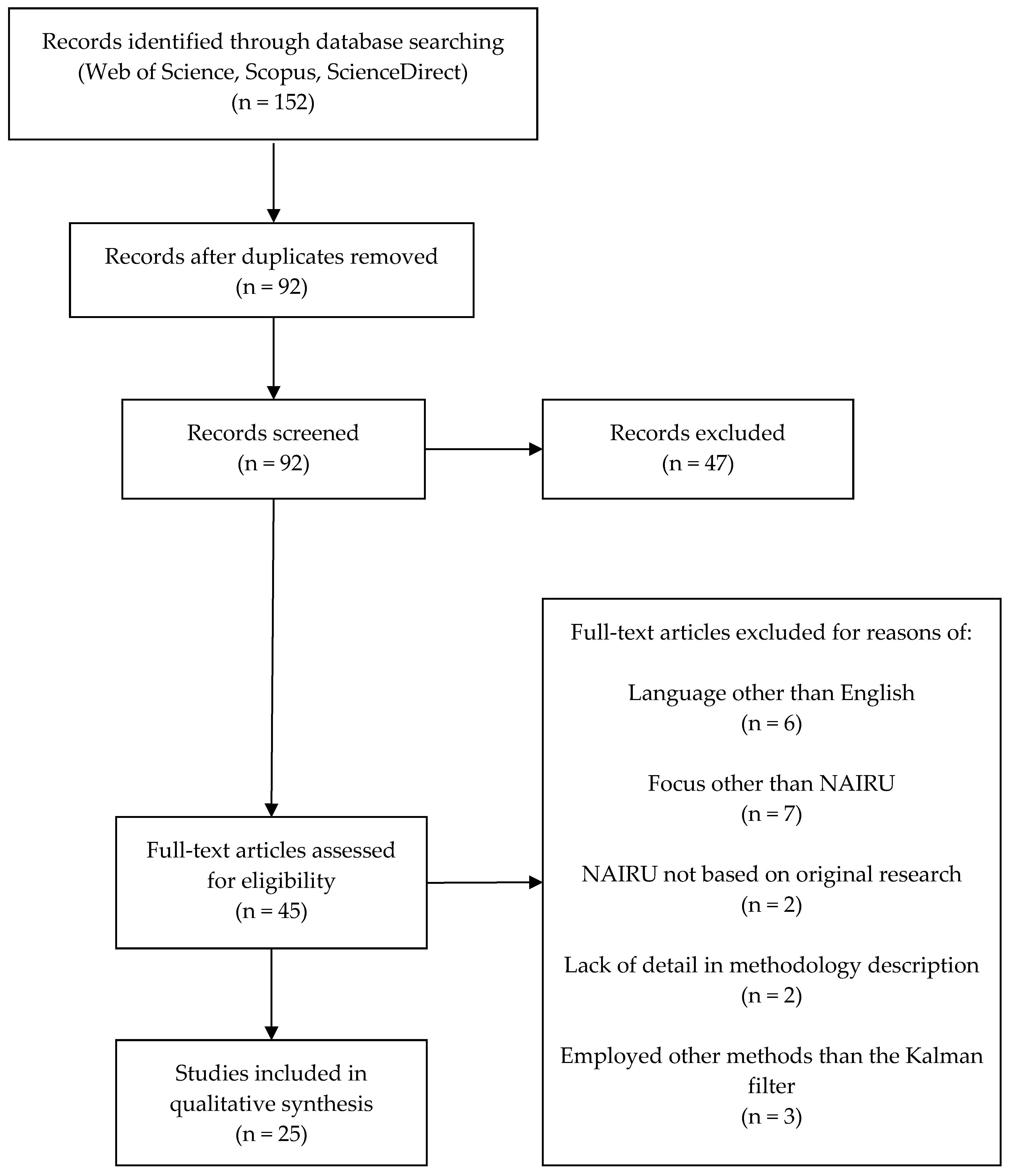

2.2. Search Strategy, Eligibility Criteria, Data Extraction, and Article Evaluation

- Published after 2005. We chose a fifteen-year timespan, even though most of the reviews focus on a ten-year timespan, to avoid obsolete studies. However, theoretical foundations for the target problem were published even before the year 2000, and observed paradigms were not fundamentally challenged since then. Secondly, data series of macroeconomics related statistics are available for much longer compared to, e.g., business-related time series. This advantage is due to the overall importance of fundamental macroeconomic identities data.

- Written in the English language. The criterion was chosen to maximize the readability of the described studies.

- Presenting original research. The criterion was applied to prevent the inclusion of papers which were based on NAIRU values presented in other papers. In such cases, NAIRU values usually served only as, e.g., inputs of a different model or economy development indicator.

- Describing a methodology related to an unobservable variable estimation. Methodology requirement was adopted since some studies stated very briefly that there was data treatment, yet there were no details on methods and settings, or other details.

- Focused on the NAIRU. An article had to be focused on the NAIRU estimation for individual economies, on a new method on how to obtain the estimates or to estimate and test the dependence of the NAIRU on several factors (such as unemployment versus structural factors, institutional factors, etc.). The NAIRU was in some articles included only to demonstrate an economic environment change, but a study focus was on the New economy paradigm, and the Kalman filter was employed for other purposes.

- Employing the Kalman filter. The last criterion deals with the fact that there are also other ways how to perform the NAIRU estimation by employing, e.g., the Hodrick–Prescott filter.

3. Results and Discussion

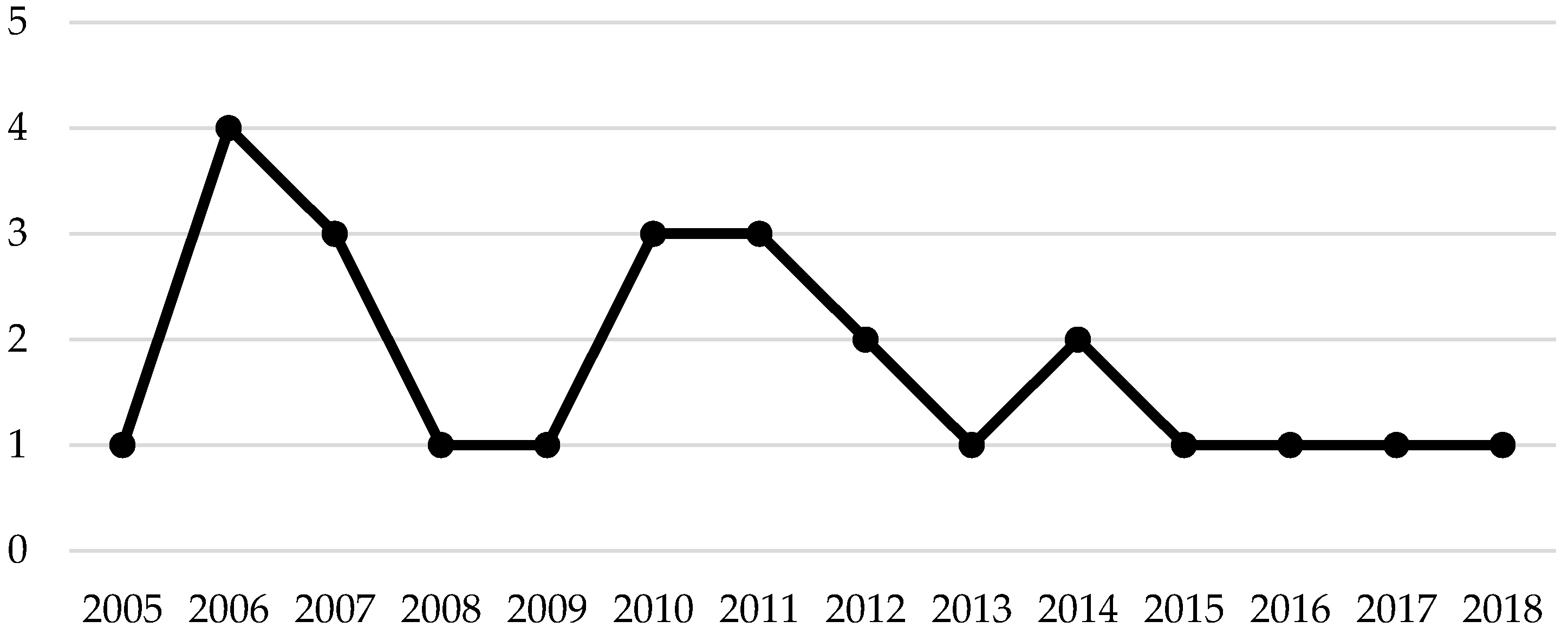

3.1. Overview of Analysed Studies

3.2. Description and Discussion of Approaches and Models Used in the Analysed Studies

3.3. Employment of the Kalman Filter and Related Issues

4. Conclusions

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

References

- Kalman, R.E. A New Approach to Linear Filtering and Prediction Problems. J. Basic Eng. 1960, 82, 35–45. [Google Scholar] [CrossRef]

- Friedman, M. The Role of Monetary Policy. Am. Econ. Rev. 1968, 58, 1–17. [Google Scholar]

- Eurostat. Total Unemployment Rate. Available online: https://ec.europa.eu/eurostat/tgm/table.do?tab=table&init=1&language=en&pcode=tps00203&plugin=1 (accessed on 28 April 2019).

- World Bank. Unemployment, Total (% of Total Labor Force) (Modeled ILO Estimate). Available online: https://data.worldbank.org/indicator/SL.UEM.TOTL.ZS (accessed on 28 April 2019).

- Maybeck, P.S. Stochastic Models, Estimation and Control, 1st ed.; Mathematics in Science and Engineering; Academic Press: New York, NY, USA, 1979; ISBN 978-0-12-480701-3. [Google Scholar]

- Grewal, M.S.; Andrews, A.P. Kalman Filtering: Theory and Practice Using MATLAB, 4th ed.; John Wiley & Sons Inc.: Hoboken, NJ, USA, 2015; ISBN 978-1-118-85121-0. [Google Scholar]

- Simon, D. Optimal State Estimation: Kalman, H [Infinity] and Nonlinear Approaches, 1st ed.; Wiley-Interscience: Hoboken, NJ, USA, 2006; ISBN 978-0-471-70858-2. [Google Scholar]

- Chickering, F.W.; Yang, S.Q. Evaluation and Comparison of Discovery Tools: An Update. Inf. Technol. Libr. 2014, 33, 5. [Google Scholar] [CrossRef]

- Breeding, M. Library Resource Discovery Products: Context, Library Perspectives, and Vendor Positions; American Library Association: Atlanta, GA, USA, 2014; ISBN 978-0-8389-5914-5. [Google Scholar]

- Aguiar, A.; Martins, M.M.F. Testing the significance and the non-linearity of the Phillips trade-off in the Euro Area. Empir. Econ. 2005, 30, 665–691. [Google Scholar] [CrossRef]

- Andrei, A.M. Using asymmetric Okun law and Phillips curve for potential output estimates: An empirical study for Romania. Adm. si Manag. Public 2014, 23, 6–18. [Google Scholar]

- Andrei, A.M.; Galupa, A.; Georgescu, I. Potential Output Estimate Using a Grey Production Function Approach. J. Grey Syst. 2017, 29, 1–14. [Google Scholar]

- Basistha, A.; Nelson, C.R. New measures of the output gap based on the forward-looking new Keynesian Phillips curve. J. Monet. Econ. 2007, 54, 498–511. [Google Scholar] [CrossRef]

- Batini, N.; Greenslade, J.V. Measuring the UK short-run NAIRU. Oxf. Econ. Pap. 2006, 58, 28–49. [Google Scholar] [CrossRef][Green Version]

- Berger, T. Estimating Europe’s natural rates. Empir. Econ. 2011, 40, 521–536. [Google Scholar] [CrossRef]

- Berger, T.; Everaert, G. Labour taxes and unemployment evidence from a panel unobserved component model. J. Econ. Dyn. Control 2010, 34, 354–364. [Google Scholar] [CrossRef]

- Botric, V. NAIRU estimates for Croatia. Zbornik Radova Ekonomskog Fakulteta u Rijeci Proc. Rijeka Fac. Econ. 2012, 30, 163–180. [Google Scholar]

- Claar, V.V. Is the NAIRU more useful in forecasting inflation than the natural rate of unemployment? Appl. Econ. 2006, 38, 2179–2189. [Google Scholar] [CrossRef]

- Constantinescu, M.; Nguyen, A.D.M. Unemployment or credit: Which one holds the potential? Results for a small open economy with a low degree of financialization. Econ. Syst. 2018, 42, 649–664. [Google Scholar] [CrossRef]

- Doménech, R.; Gómez, V. Estimating Potential Output, Core Inflation, and the NAIRU as Latent Variables. J. Bus. Econ. Stat. 2006, 24, 354–365. [Google Scholar] [CrossRef]

- Elkayam, D.; Ilek, A. Estimating the NAIRU for Israel, 1992–2013. Isr. Econ. Rev. 2016, 14, 53–74. [Google Scholar]

- Fitzenberger, B.; Franz, W.; Bode, O. The Phillips Curve and NAIRU Revisited: New Estimates for Germany. J. Econ. Stat. 2008, 228, 465–496. [Google Scholar] [CrossRef][Green Version]

- Heyer, E.; Reynès, F.; Sterdyniak, H. Structural and reduced approaches of the equilibrium rate of unemployment, a comparison between France and the United States. Econ. Model. 2007, 24, 42–65. [Google Scholar] [CrossRef]

- Leu, S.C.-Y.; Sheen, J. A small New Keynesian state space model of the Australian economy. Econ. Model. 2011, 28, 672–684. [Google Scholar] [CrossRef]

- Logeay, C.; Tober, S. Hysteresis and the NAIRU in the euro area. Scott. J. Polit. Econ. 2006, 53, 409–429. [Google Scholar] [CrossRef]

- Marjanovic, G.; Maksimovic, L.; Stanisic, N. Hysteresis and the NAIRU: The Case of Countries in Transition. Prague Econ. Pap. 2015, 24, 503–515. [Google Scholar] [CrossRef]

- Meļihovs, A.; Zasova, A. Assessment of the natural rate of unemployment and capacity utilisation in Latvia. Balt. J. Econ. 2009, 9, 25–46. [Google Scholar] [CrossRef]

- Napolitano, O.; Montagnoli, A. The European unemployment gap and the role of monetary policy. Econ. Bull. 2010, 30, 1346–1358. [Google Scholar]

- Planas, C.; Roeger, W.; Rossi, A. How much has labour taxation contributed to European structural unemployment? J. Econ. Dyn. Control 2007, 31, 1359–1375. [Google Scholar] [CrossRef]

- Rodriguez, G. Estimating output gap, core inflation, and the NAIRU for Peru, 1979–2007. Appl. Econom. Int. Dev. 2010, 10, 149–160. [Google Scholar]

- Rodríguez, A.; Ruiz, E. Bootstrap prediction mean squared errors of unobserved states based on the Kalman filter with estimated parameters. Comput. Stat. Data Anal. 2012, 56, 62–74. [Google Scholar] [CrossRef]

- Rusticelli, E. Rescuing the Phillips curve: Making use of long-term unemployment in the measurement of the NAIRU. OECD J. Econ. Stud. 2014, 1, 109–127. [Google Scholar]

- Shaheen, F.; Haider, A.; Javed, S.A. Estimating Pakistan’s time varying non-accelerating inflation rate of unemployment: An unobserved component approach. Int. J. Econ. Financ. Iss. 2011, 1, 172–179. [Google Scholar]

- Valadkhani, A.; Mehdee Araee, S.M. Estimating the time varying NAIRU in Iran. J. Econ. Stud. 2013, 40, 635–643. [Google Scholar] [CrossRef]

- Apel, M.; Jansson, P. A theory-consistent system approach for estimating potential output and the NAIRU. Econ. Lett. 1999, 64, 271–275. [Google Scholar] [CrossRef]

- Apel, M.; Jansson, P. System estimates of potential output and the NAIRU. Empir. Econ. 1999, 24, 373–388. [Google Scholar] [CrossRef]

- Harvey, A.C. Forecasting, Structural Time Series Models, and the Kalman Filter, 1st ed.; Cambridge University Press: Cambridge, UK; New York, NY, USA, 1989; ISBN 978-0-521-40573-7. [Google Scholar]

- Durbin, J.; Koopman, S.J. Time Series Analysis by State Space Methods, 2nd ed.; Oxford Statistical Science Series; Oxford University Press: Oxford, UK, 2012; ISBN 978-0-19-964117-8. [Google Scholar]

- Jong, P.D. The Diffuse Kalman Filter. Ann. Stat. 1991, 19, 1073–1083. [Google Scholar] [CrossRef]

- Hamilton, J.D. Time Series Analysis, 1st ed.; Princeton University Press: Princeton, NJ, USA, 1994; ISBN 978-0-691-04289-3. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

| Authors | Publication Year | Aim | Country | Time Series Data | |

|---|---|---|---|---|---|

| [10] | Aguiar, A.; Martins, M.M.F. | 2005 | Testing possible non-linearity in a NAIRU model, estimating the NAIRU | Euro area countries (aggregated) | Q, 1970:Q1–2002:Q3 |

| [11] | Andrei, A.M. | 2014 | Estimating the NAIRU and potential output | Romania | Q, 2001:Q1–2014:Q2 |

| [12] | Andrei, A.M.; Galupa, A.; Georgescu, I. | 2017 | Estimating potential output | Romania | Q, 2000–2013:Q2 |

| [13] | Basistha, A.; Nelson, C.R. | 2007 | Estimating the output gap | USA | Q, 1960:Q1–2003:Q1 |

| [14] | Batini, N.; Greenslade, J.V. | 2006 | Estimating the short-run NAIRU and discussing the usefulness of the NAIRU concept | UK | Q, 1973:Q1–2001:Q4 |

| [15] | Berger, T. | 2011 | Estimating the NRU, potential output and the core inflation rate | Euro area countries (aggregated) | Q, 1970–2005 |

| [16] | Berger, T.; Everaert, G. | 2010 | Analyzing effects of labor taxes on unemployment | OECD countries (16 countries grouped into three groups: AT, DK, FI, SE; BE, FR, DE, IT, NL, PT, ES, GR; JP, IE, US, GB) | A, 1970–2005 |

| [17] | Botric, V. | 2012 | Estimating the NAIRU | Croatia | Q, 2000:Q1–2011:Q2 |

| [18] | Claar, V.V. | 2006 | Estimating the NRU and evaluating its inflation-forecasting power relative to the NAIRU | USA | A, 1947–1998 |

| [19] | Constantinescu, M.; Nguyen, A.D.M. | 2018 | Estimating potential output | Lithuania | Q, 1998:Q1–2016:Q3 |

| [20] | Domenech, R.; Gomez, V. | 2006 | Estimating the NAIRU, the core inflation rate and the investment rate trend | USA | Q, 1947:Q1–2003:Q1 |

| [21] | Elkayam D.; Ilek A. | 2016 | Estimating the NAIRU | Israel | Q, 1992:Q1–2013:Q4 |

| [22] | Fitzenberger, B.; Franz, W.; Bode, O. | 2008 | Estimating the NAIRU | Germany | Q, 1976:Q2–1990:Q2 (West Germany), 1990:Q3–2006:Q4 (unified Germany) |

| [23] | Heyer, E.; Reynes, F.; Sterdyniak, H. | 2007 | Comparing two approaches for estimating the NAIRU | France, USA | Q, 1970–2003 |

| [24] | Leu, S. C.-Y.; Sheen, J. | 2011 | Estimating the NAIRU, potential output, the neutral real interest rate and the subjective discount factor | Australia | Q, 1984:Q1–2006:Q4 |

| [25] | Logeay, C.; Tober, S. | 2006 | Estimating the NAIRU and analyzing the hysteresis effect | Euro area countries (12 countries: DE, FR, IT, ES, NL, AT, PT, FI, IE, BE, LU, GR) | Q, 1970–2002 |

| [26] | Marjanovic, G.; Maksimovic, L.; Stanisic, N. | 2015 | Estimating the NAIRU and analyzing the hysteresis effect for countries in transition | Countries in transition (Eight countries: PL, HU, CZ, SK, SI, BG, RO, HR) | Q, 2000–2012 |

| [27] | Melihovs, A.; Zasova, A. | 2009 | Estimating the NAIRU and the NAIRCU | Latvia | Q, 1996:Q3–2008:Q4 |

| [28] | Napolitano O.; Montagnoli A. | 2010 | Estimating the NAIRU and analyzing the impact of monetary policy on the labor market | France, Germany, Italy | Q, 1972:Q1–2007:Q1 |

| [29] | Planas, C.; Roeger, W.; Rossi, A. | 2007 | Analyzing effects of labor taxes on unemployment, estimating the NAIRU | Euro area countries (aggregated 12 countries: DE, FR, IT, ES, NL, AT, PT, FI, IE, BE, LU, GR) | A, 1970–2004 |

| [30] | Rodriguez G. | 2010 | Estimating the NAIRU, the output gap and the core inflation | Peru | Q, 1979:Q1–2007:Q4 |

| [31] | Rodriguez, A.; Ruiz, E. | 2012 | Calculating uncertainty of the NAIRU, the output gap, the long-run investment rate and the core inflation estimates | USA | Q, 1948:Q1–2003:Q1 |

| [32] | Rusticelli E. | 2014 | Estimating the NAIRU considering the hysteresis effect | OECD countries (11 countries: CA, FR, DE, GR, IE, IT, JP, PT, ES, GB, US) | Q, 1987:Q1–2012:Q4 (different starting points for different countries) |

| [33] | Shaheen F.; Haider A.; Javed S. A. | 2011 | Estimating the NAIRU | Pakistan | A, 1973/74–2007/08 |

| [34] | Valadkhani A.; Araee S.M.M. | 2013 | Estimating the NAIRU | Iran | A, 1959–2008 |

| Model | Estimated Output Variables | Additional Input Variables | ||

|---|---|---|---|---|

| [10] | Backward-looking PC; OL | NAIRU | Deviation of imported inflation from domestic inflation in the previous quarter | |

| [11] | Backward-looking PC | NAIRU * | - | * NAIRU estimates are used for calculating potential output |

| [12] | Backward-looking PC | NAIRU * | - | * NAIRU is estimated in two steps; potential output is then estimated using the NAIRU estimates |

| [13] | NKPC; OL; decomposition of unemployment, output and inflation into gap and non-gap component, which are not identical to cycle and trend | NRU *, output gap | - | * NRU is used as a synonym for NAIRU |

| [14] | Backward-looking PC * | NAIRU ** | Change in real import prices, change in real oil prices | * 2 models ** The longer-run NAIRU is estimated using the Kalman filter and then the short-run NAIRU is derived from these estimates |

| [15] | NKPC; OL; trend-cycle decomposition of unemployment, output and inflation | NRU *, potential output, core inflation rate | Dummy for structural break | * NRU is used as a synonym for NAIRU |

| [16] | Trend-cycle decomposition of unemployment; decomposition of the trend into observable (a labor tax effect) and unobservable component | NAIRU, cyclical unemployment * | Labor taxes | * The main aim of the study is estimating unknown model parameters and testing their significance |

| [17] | Backward-looking PC | NAIRU | Change in real oil prices; dummy for crisis effect | |

| [18] | Trend-cycle decomposition of unemployment | NRU * | - | * NRU estimates are used for inflation forecasting; NRU is distinguished from NAIRU |

| [19] | Backward-looking PC; OL; trend-cycle decomposition of unemployment, output and inflation | NAIRU, potential output | - | |

| [20] | Forward-looking PC; OL; trend-cycle decomposition of output, investment equation | NAIRU, potential output, core inflation rate, investment rate trend | - | |

| [21] | Forward-looking PC | NAIRU | Change in real import prices | |

| [22] | Backward-looking PC; OL * | NAIRU | Relative inflation rate of imported raw materials, change rate of price wedge, rate of change of labor productivity minus trend rate of change; dummy for structural break; quarter dummies | * 6 models |

| [23] | Backward-looking PC * | NAIRU | Change in real import prices | * 2 models (differing from each other by the inclusion of additional exogenous variables in the NAIRU equation) |

| [24] | Hybrid NKPC; OL; New Keynesian dynamic IS equation; trend-cycle decomposition of unemployment, output and the real interest rate | NAIRU, potential output, neutral real interest rate, subjective discount factor | Dummy for the exogenous effect of the introduction of the Goods and Services Tax in Australia in 2000 | |

| [25] | Backward-looking PC | NAIRU | Change in real oil prices, change in labor productivity growth; dummy for structural break (Germany) | |

| [26] | Trend-cycle decomposition of unemployment | NAIRU | - | |

| [27] | Backward-looking PC; trend-cycle decomposition of unemployment | NAIRU * | Change in real oil prices, change in real import prices | * NAIRCU is estimated using different model |

| [28] | Trend-cycle decomposition of unemployment | NAIRU | - | |

| [29] | Trend-cycle decomposition of unemployment; decomposition of the trend into observable (a labor tax effect) and unobservable component | NAIRU | Labor taxes | |

| [30] | NKPC; OL; trend-cycle decomposition of output, investment equation | NAIRU, potential output, core inflation rate | - | |

| [31] | Forward-looking PC; OL; trend-cycle decomposition of output; investment equation | NAIRU, potential output, core inflation, long-run investment rate | - | |

| [32] | Backward-looking PC; trend-cycle decomposition of unemployment * | NAIRU | Change in real import price inflation weighted by import penetration, change in real oil price inflation weighted by oil intensity of production | * The change in the lagged long-term unemployment rate is included in the NAIRU equation to capture the hysteresis effect |

| [33] | Trend-cycle decomposition of unemployment; backward-looking PC * | NAIRU | Change in real oil prices; dummy for changes in inflation | * NAIRU is estimated in two steps (1. step: trend-cycle decomposition, 2. step: estimation using PC) |

| [34] | Backward-looking PC * | NAIRU | Aggregate import price index | * 2 models (the second model is augmented by the output gap calculated using the HP filter) |

| Backward-Looking PC | Forward-Looking PC | New Keynesian PC | Hybrid New Keynesian PC | Okun’s Law | Unemployment Decomposition | Output Decomposition | Inflation Decomposition | Real Interest Rate Decomposition | Investment Equation | |

|---|---|---|---|---|---|---|---|---|---|---|

| [10] | X | X | ||||||||

| [11] | X | |||||||||

| [12] | X | |||||||||

| [13] | X | X | X | X | X | |||||

| [14] | X | |||||||||

| [15] | X | X | X | X | X | |||||

| [16] | X | |||||||||

| [17] | X | |||||||||

| [18] | X | |||||||||

| [19] | X | X | X | X | X | |||||

| [20] | X | X | X | X | ||||||

| [21] | X | |||||||||

| [22] | X | X | ||||||||

| [23] | X | |||||||||

| [24] | X | X | X | X | X | |||||

| [25] | X | |||||||||

| [26] | X | |||||||||

| [27] | X | X | ||||||||

| [28] | X | |||||||||

| [29] | X | |||||||||

| [30] | X | X | X | X | ||||||

| [31] | X | X | ||||||||

| [32] | X | X | ||||||||

| [33] | X | X | ||||||||

| [34] | X |

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Fronckova, K.; Prazak, P.; Soukal, I. Review of Kalman Filter Employment in the NAIRU Estimation. Systems 2019, 7, 33. https://doi.org/10.3390/systems7030033

Fronckova K, Prazak P, Soukal I. Review of Kalman Filter Employment in the NAIRU Estimation. Systems. 2019; 7(3):33. https://doi.org/10.3390/systems7030033

Chicago/Turabian StyleFronckova, Katerina, Pavel Prazak, and Ivan Soukal. 2019. "Review of Kalman Filter Employment in the NAIRU Estimation" Systems 7, no. 3: 33. https://doi.org/10.3390/systems7030033

APA StyleFronckova, K., Prazak, P., & Soukal, I. (2019). Review of Kalman Filter Employment in the NAIRU Estimation. Systems, 7(3), 33. https://doi.org/10.3390/systems7030033