When Environmental, Social, and Governance (ESG) Meets Shareholder Value: Unpacking the Long-Term Effects with a Multi-Period Difference-in-Differences (DID) Approach

Abstract

1. Introduction

2. Literature Review

2.1. ESG and Shareholder Value

2.2. ESG and Dividend Policy

2.3. Dividend Policy and Shareholder Value

2.4. The Role of Dividend Policy in the ESG-Shareholder Value Relationship

3. Methodology

3.1. Model Specification

- (1)

- Baseline DID Model

- (2)

- Dynamic DID Model

- (3)

- Mediation Model: Dividend Policy

3.2. Variable Definitions

3.3. Sample Selection and Data Sources

3.4. Descriptive Statistics

4. Empirical Results

4.1. Baseline Regression Results

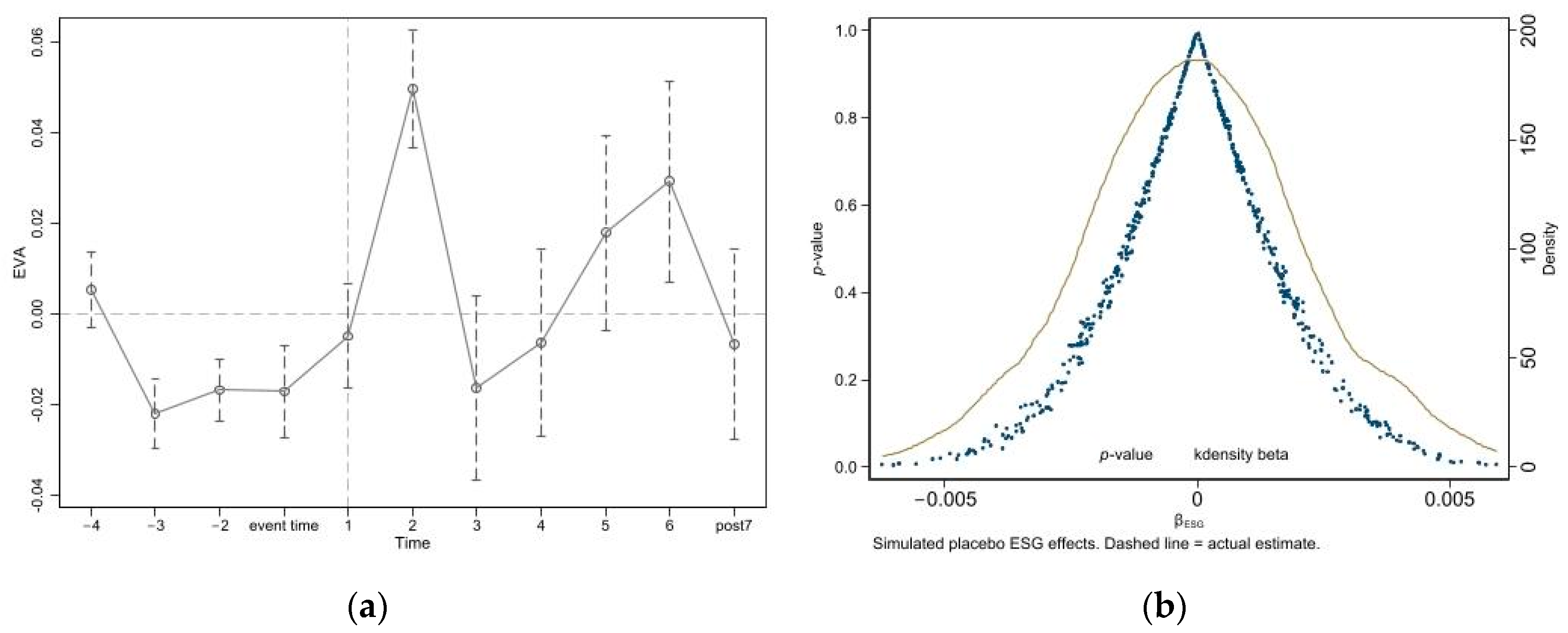

4.2. Parallel Trends Test

4.3. Robustness Test

4.4. Endogeneity Test

- (1)

- Placebo Test

- (2)

- Propensity Score Matching Difference-in-Differences (PSM-DID) Analysis

- (3)

- Instrumental Variables (IV) Method

4.5. Mechanism Test of Dividend Policy

5. Heterogeneous Analysis

6. Discussion and Conclusions

6.1. Findings

6.2. Discussions and Contributions

6.3. Limitations

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- Yu, T.; Mao, S. Does the establishment of China’s national innovation demonstration zone for sustainable development enhance urban sustainable competitiveness?—Policy effects assessment based on multi-period difference-in-differences models. J. Environ. Manag. 2024, 372, 123439. [Google Scholar] [CrossRef] [PubMed]

- Ni, K.; Zhang, R.; Tan, L.; Lai, X. How ESG enhances corporate competitiveness: Mechanisms and Evidence. Financ. Res. Lett. 2024, 69, 106249. [Google Scholar] [CrossRef]

- Rahat, B.; Nguyen, P. The impact of ESG profile on Firm’s valuation in emerging markets. Int. Rev. Financ. Anal. 2024, 95, 103361. [Google Scholar] [CrossRef]

- Tsang, A.; Frost, T.; Cao, H. Environmental, Social, and Governance (ESG) disclosure: A literature review. Br. Account. Rev. 2023, 55, 101149. [Google Scholar] [CrossRef]

- Chen, Y.; Li, T.; Zeng, Q.; Zhu, B. Effect of ESG performance on the cost of equity capital: Evidence from China. Int. Rev. Econ. Financ. 2023, 83, 348–364. [Google Scholar] [CrossRef]

- Alduais, F. Unravelling the intertwined nexus of firm performance, ESG practices, and capital cost in the Chinese business landscape. Cogent Econ. Financ. 2023, 11, 2254589. [Google Scholar] [CrossRef]

- Bhattacharya, S. Imperfect Information, Dividend Policy, and “The Bird in the Hand” Fallacy. Bell J. Econ. 1979, 10, 259–270. [Google Scholar] [CrossRef]

- Friske, W.; Hoelscher, S.A.; Nikolov, A.N. The impact of voluntary sustainability reporting on firm value: Insights from signaling theory. J. Acad. Mark. Sci. 2023, 51, 372–392. [Google Scholar] [CrossRef]

- Freeman, R.E. Strategic management: A stakeholder theory. J. Manag. Stud. 1984, 39, 1–21. [Google Scholar]

- Leoni, L. Integrating ESG and organisational resilience through system theory: The ESGOR matrix. Manag. Decis. 2024; ahead-of-print. [Google Scholar] [CrossRef]

- Song, J. Corporate ESG performance and human capital investment efficiency. Financ. Res. Lett. 2024, 62, 105239. [Google Scholar] [CrossRef]

- Barros, V.; Verga Matos, P.; Miranda Sarmento, J.; Rino Vieira, P. ESG performance and firms’ business and geographical diversification: An empirical approach. J. Bus. Res. 2024, 172, 114392. [Google Scholar] [CrossRef]

- Fredriksson, A.; Oliveira, G.M. Impact evaluation using Difference-in-Differences. RAUSP Manag. J. 2019, 54, 519–532. [Google Scholar] [CrossRef]

- Strumpf, E.C.; Harper, S.; Kaufman, J.S. Fixed effects and difference in differences. Methods Soc. Epidemiol. 2017, 1, 342. [Google Scholar]

- Roth, J.; Sant’Anna, P.H.C.; Bilinski, A.; Poe, J. What’s trending in difference-in-differences? A synthesis of the recent econometrics literature. J. Econom. 2023, 235, 2218–2244. [Google Scholar] [CrossRef]

- Hillman, A.J.; Keim, G.D. Shareholder value, stakeholder management, and social issues: What’s the bottom line? Strateg. Manag. J. 2001, 22, 125–139. [Google Scholar] [CrossRef]

- Hall, J.H. Corporate shareholder value creation as contributor to economic growth. Stud. Econ. Financ. 2024, 41, 148–176. [Google Scholar] [CrossRef]

- Martiny, A.; Taglialatela, J.; Testa, F.; Iraldo, F. Determinants of environmental social and governance (ESG) performance: A systematic literature review. J. Clean. Prod. 2024, 456, 142213. [Google Scholar] [CrossRef]

- Spence, M. Job Market Signaling. Q. J. Econ. 1973, 87, 355–374. [Google Scholar] [CrossRef]

- Aevoae, G.M.; Andrieș, A.M.; Ongena, S.; Sprincean, N. ESG and systemic risk. Appl. Econ. 2023, 55, 3085–3109. [Google Scholar] [CrossRef]

- Jensen, M.C.; Meckling, W.H. Theory of the Firm: Managerial Behavior, Agency Costs, and Ownership Structure. In Economics Social Institutions: Insights from the Conferences on Analysis & Ideology; Brunner, K., Ed.; Springer: Dordrecht, The Netherlands, 1979; pp. 163–231. [Google Scholar]

- Yadav, M.; Dhingra, B.; Batra, S.; Saini, M.; Aggarwal, V. ESG scores and stock returns during COVID-19: An empirical analysis of an emerging market. Int. J. Soc. Econ. 2024; ahead-of-print. [Google Scholar] [CrossRef]

- Kräussl, R.; Oladiran, T.; Stefanova, D. A review on ESG investing: Investors’ expectations, beliefs and perceptions. J. Econ. Surv. 2024, 38, 476–502. [Google Scholar] [CrossRef]

- Niyommaneerat, W.; Suwanteep, K.; Chavalparit, O. Sustainability indicators to achieve a circular economy: A case study of renewable energy and plastic waste recycling corporate social responsibility (CSR) projects in Thailand. J. Clean. Prod. 2023, 391, 136203. [Google Scholar] [CrossRef]

- Tziner, A.; Persoff, M. The interplay between ethics, justice, corporate social responsibility, and performance management sustainability. Front. Psychol. 2024, 15, 1323910. [Google Scholar] [CrossRef]

- Girau, E.A.; Bujang, I.; Paulus Jidwin, A.; Said, J. Corporate governance challenges and opportunities in mitigating corporate fraud in Malaysia. J. Financ. Crime 2022, 29, 620–638. [Google Scholar] [CrossRef]

- Donaldson, T.; Preston, L.E. The Stakeholder Theory of the Corporation: Concepts, Evidence, and Implications. Acad. Manag. Rev. 1995, 20, 65–91. [Google Scholar] [CrossRef]

- Bilyay-Erdogan, S.; Danisman, G.O.; Demir, E. ESG performance and dividend payout: A channel analysis. Financ. Res. Lett. 2023, 55, 103827. [Google Scholar] [CrossRef]

- Luo, D. ESG, liquidity, and stock returns. J. Int. Financ. Mark. Inst. Money 2022, 78, 101526. [Google Scholar] [CrossRef]

- Khan, M.A.; Hassan, M.K.; Maraghini, M.P.; Paolo, B.; Valentinuz, G. Valuation effect of ESG and its impact on capital structure: Evidence from Europe. Int. Rev. Econ. Financ. 2024, 91, 19–35. [Google Scholar] [CrossRef]

- Chouaibi, Y.; Zouari, G. The mediating role of real earnings management in the relationship between CSR practices and cost of equity: Evidence from European ESG data. EuroMed J. Bus. 2024, 19, 314–337. [Google Scholar] [CrossRef]

- Liu, D.; Gu, K.; Hu, W. ESG performance and stock idiosyncratic volatility. Financ. Res. Lett. 2023, 58, 104393. [Google Scholar] [CrossRef]

- Sun, Y.; Zhao, D.; Cao, Y. The impact of ESG performance, reporting framework, and reporting assurance on the tone of ESG disclosures: Evidence from Chinese listed firms. J. Clean. Prod. 2024, 466, 142698. [Google Scholar] [CrossRef]

- Yilmaz, M.K.; Aksoy, M.; Khan, A. Moderating role of corporate governance and ownership structure on the relationship of corporate sustainability performance and dividend policy. J. Sustain. Financ. Invest. 2024, 14, 988–1017. [Google Scholar] [CrossRef]

- Baron, R.M.; Kenny, D.A. The moderator–mediator variable distinction in social psychological research: Conceptual, strategic, and statistical considerations. J. Personal. Soc. Psychol. 1986, 51, 1173–1182. [Google Scholar] [CrossRef] [PubMed]

- Brück, C.; Knauer, T.; Schwering, A. Disclosure of value-based performance measures: Evidence from German listed firms. Account. Bus. Res. 2023, 53, 671–698. [Google Scholar] [CrossRef]

- Zhang, H.; Lai, J. Greening through ESG: Do ESG ratings improve corporate environmental performance in China? Int. Rev. Econ. Financ. 2024, 96, 103726. [Google Scholar] [CrossRef]

- Ellili, N.O. Impact of environmental, social and governance disclosure on dividend policy: What is the role of corporate governance? Evidence from an emerging market. Corp. Soc. Responsib. Environ. Manag. 2022, 29, 1396–1413. [Google Scholar] [CrossRef]

- Liu, Y.-Y.; Lee, P.-S. The impact of environmental, social and governance (ESG) performance on the duration of dividend sustainability: A survival analysis. Manag. Financ. 2025, 51, 337–352. [Google Scholar] [CrossRef]

- Marcus, M.; Sant’Anna, P.H.C. The Role of Parallel Trends in Event Study Settings: An Application to Environmental Economics. J. Assoc. Environ. Resour. Econ. 2020, 8, 235–275. [Google Scholar] [CrossRef]

- Sun, X.; Ci, F.; Cifuentes-Faura, J.; Liu, X. Firm-level climate risk and corporate violations: Perspective of corporate managers’ pressure perception. Manag. Decis. Econ. 2024, 45, 5430–5448. [Google Scholar] [CrossRef]

- Liu, W.; Suzuki, Y. Corporate governance, institutional ownership, and stock liquidity of SMEs: Evidence from China. Asia-Pac. J. Account. Econ. 2025, 32, 299–328. [Google Scholar] [CrossRef]

- La Ferrara, E.; Chong, A.; Duryea, S. Soap Operas and Fertility: Evidence from Brazil. Am. Econ. J. Appl. Econ. 2012, 4, 1–31. [Google Scholar] [CrossRef]

- Eggers, A.C.; Tuñón, G.; Dafoe, A. Placebo Tests for Causal Inference. Am. J. Political Sci. 2023, 68, 1106–1121. [Google Scholar] [CrossRef]

- Ghimire, A.; Ali, S.; Long, X.; Chen, L.; Sun, J. Effect of Digital Silk Road and innovation heterogeneity on digital economy growth across 29 countries: New evidence from PSM-DID. Technol. Forecast. Soc. Change 2024, 198, 122987. [Google Scholar] [CrossRef]

- Mogstad, M.; Torgovitsky, A.; Walters, C.R. Policy evaluation with multiple instrumental variables. J. Econom. 2024, 243, 105718. [Google Scholar] [CrossRef]

- Abdul Rahman, R.; Alsayegh, M.F. Determinants of Corporate Environment, Social and Governance (ESG) Reporting among Asian Firms. J. Risk Financ. Manag. 2021, 14, 167. [Google Scholar] [CrossRef]

- Mahmood, Y.; Rashid, A.; Rizwan, M.F. Do corporate financial flexibility, financial sector development and regulatory environment affect corporate investment decisions? J. Econ. Adm. Sci. 2022, 38, 485–508. [Google Scholar] [CrossRef]

- Hashmi, M.A.; Istaqlal, U.; Brahmana, R.K. Corporate governance and cost of equity: The moderating role of ownership concentration levels. South Asian J. Bus. Stud. 2024, 13, 282–302. [Google Scholar] [CrossRef]

- Matakanye, R.M.; van der Poll, H.M.; Muchara, B. Do Companies in Different Industries Respond Differently to Stakeholders’ Pressures When Prioritising Environmental, Social and Governance Sustainability Performance? Sustainability 2021, 13, 12022. [Google Scholar] [CrossRef]

- Wang, Z.; Zhang, C.; Wu, R.; Sha, L. From ethics to efficiency: Understanding the interconnected dynamics of ESG performance, financial efficiency, and cash holdings in China. Financ. Res. Lett. 2024, 64, 105419. [Google Scholar] [CrossRef]

- Luo, C.; Wei, D.; He, F. Corporate ESG performance and trade credit financing—Evidence from China. Int. Rev. Econ. Financ. 2023, 85, 337–351. [Google Scholar] [CrossRef]

- Lewellyn, K.; Muller-Kahle, M. ESG Leaders or Laggards? A Configurational Analysis of ESG Performance. Bus. Soc. 2023, 63, 1149–1202. [Google Scholar] [CrossRef]

- Cheng, Q.; Yang, J. High-speed rail, resource allocation and haze pollution in China. Transp. Policy 2024, 157, 124–139. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Variables | Symbol | Measurement |

|---|---|---|

| Independent Variable | ESG Performance | ESG_Score = Huazheng ESGrating (1 to 9) |

| Dependent Variables | Shareholder value (EVA) | EVA = NOPAT − (Capital Cost × Total Capital) NOPAT = Net Operating Profit After Tax |

| Mediating Variable | Dividend policy (DR) | |

| Control Variables | Leverage (Lev) | |

| Board Size (Board) | ||

| Proportion of Independent Directors (Indep) | ||

| Operating Revenue Growth Rate (Growth) | ||

| Firm Age (FirmAge) | ||

| Asset Market Value (TobinQ) | ||

| Dummy Variables | Firm Fixed Effects (Firm FE) | |

| Year Fixed Effects (Year FE) |

| Variable | N | Mean | SD | Min | Max |

|---|---|---|---|---|---|

| ESG | 23,467 | 3.831 | 1.272 | 0 | 6.250 |

| EVA | 23,467 | −0.00100 | 0.440 | −2.461 | 3.283 |

| Board | 23,467 | 2.079 | 0.188 | 1.609 | 2.708 |

| Lev | 23,467 | 0.366 | 0.195 | 0.0270 | 0.927 |

| Indep | 23,467 | 0.378 | 0.0520 | 0.273 | 0.600 |

| Growth | 23,467 | 0.187 | 0.402 | −0.653 | 3.894 |

| FirmAge | 23,467 | 2.843 | 0.363 | 1.099 | 3.611 |

| TobinQ | 23,467 | 2.138 | 1.397 | 0.802 | 16.65 |

| Variables | Baseline Regression Results | Robustness Test | ||||

|---|---|---|---|---|---|---|

| (1) EVA | (2) EVA | (3) EVA | (4) EVA | (5) L.EVA | (6) EVA | |

| ESG | 0.045 *** | 0.023 *** | 0.038 *** | 0.103 *** | 0.025 *** | |

| (0.002) | (0.003) | (0.006) | (0.007) | (0.003) | ||

| BloombergESG | 0.027 *** | |||||

| (0.004) | ||||||

| BM | −0.209 *** | |||||

| (0.015) | ||||||

| Mshare | 0.118 *** | |||||

| (0.039) | ||||||

| Controls | No | Yes | Yes | Yes | Yes | Yes |

| Firm FE | No | Yes | Yes | Yes | Yes | Yes |

| Year FE | No | Yes | Yes | Yes | Yes | Yes |

| Observations | 23,467 | 23,052 | 23,052 | 5404 | 18,802 | 22,796 |

| R-squared | 0.017 | 0.455 | 0.279 | 0.513 | 0.462 | 0.492 |

| r2_a | 0.0171 | 0.365 | 0.160 | 0.435 | 0.368 | 0.408 |

| Variables | (PSM-DID) Analysis | Instrumental Variables Methods | |

|---|---|---|---|

| EVA | First-Stage | Second-Stage | |

| ESG | EVA | ||

| DID | 0.158 *** | 1.031 *** | |

| (0.027) | (20.11) | ||

| ESG | 0.022 *** | ||

| (0.003) | |||

| IV1 | 0.124 *** | ||

| (12.05) | |||

| IV2 | 0.071 *** | ||

| (6.77) | |||

| Controls | YES | YES | YES |

| Observations | 22,843 | 22,269 | 22,269 |

| R-squared | 0.461 | 0.028 | - |

| Firm FE | YES | YES | YES |

| Year FE | YES | YES | YES |

| r2_a | 0.371 | - | - |

| F | 68.42 | - | - |

| Kleibergen–Paap rk LM | 413.898 | ||

| Cragg–Donald Wald F | 210.783 | ||

| Stock–Yogo weak ID | 19.93 | ||

| Variables | (1) DR | (2) EVA | (3) EVA |

|---|---|---|---|

| ESG | 0.0219 *** | 0.0229 *** | |

| (0.0019) | (0.0028) | ||

| DR | 0.0357 *** | 0.0290 *** | |

| (0.0095) | (0.0095) | ||

| Constant | 0.4264 *** | −0.7423 *** | −0.7931 *** |

| (0.1506) | (0.2850) | (0.2823) | |

| Observations | 22,843 | 22,843 | 22,843 |

| R-squared | 0.3784 | 0.4541 | 0.4564 |

| Controls | YES | YES | YES |

| Year FE | YES | YES | YES |

| Id FE | YES | YES | YES |

| Sobel | 0.0034 *** | ||

| Bootstrap results | (0.0028993, 0.0039704) | ||

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2025 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Zhou, Y.; Bu, W. When Environmental, Social, and Governance (ESG) Meets Shareholder Value: Unpacking the Long-Term Effects with a Multi-Period Difference-in-Differences (DID) Approach. Systems 2025, 13, 315. https://doi.org/10.3390/systems13050315

Zhou Y, Bu W. When Environmental, Social, and Governance (ESG) Meets Shareholder Value: Unpacking the Long-Term Effects with a Multi-Period Difference-in-Differences (DID) Approach. Systems. 2025; 13(5):315. https://doi.org/10.3390/systems13050315

Chicago/Turabian StyleZhou, Yong, and Wei Bu. 2025. "When Environmental, Social, and Governance (ESG) Meets Shareholder Value: Unpacking the Long-Term Effects with a Multi-Period Difference-in-Differences (DID) Approach" Systems 13, no. 5: 315. https://doi.org/10.3390/systems13050315

APA StyleZhou, Y., & Bu, W. (2025). When Environmental, Social, and Governance (ESG) Meets Shareholder Value: Unpacking the Long-Term Effects with a Multi-Period Difference-in-Differences (DID) Approach. Systems, 13(5), 315. https://doi.org/10.3390/systems13050315