Abstract

Project portfolio selection is essential for a company to achieve its strategic goals. Due to constraints such as budget and manpower, companies cannot undertake all projects simultaneously and must prioritize those offering the highest value. Projects often interact and progress through various phases, adding complexity to the selection process. To address these challenges, this study introduces a model that accounts for the multi-stage execution of projects, their interactions, and multiple objectives. A novel multi-objective optimization algorithm is developed to solve this problem, along with a refined project selection method designed to offer decision-makers enhanced insights. Finally, a numerical example is provided to demonstrate the effectiveness of the proposed approach.

1. Introduction

Project portfolio selection (PPS) is a key component of Project Portfolio Management (PPM), which focuses on selecting the most suitable projects from numerous candidates within constraints such as budget, personnel, and time [1]. The primary aim of PPM is ensuring portfolio alignment with organizational strategic objectives, optimizing business value through systematic selection, evaluation, and oversight. As a result, identifying the right projects for implementation is a crucial step for companies aiming to achieve their strategic objectives, making this topic a focal point of research across various fields. Based on the context of the study, projects are typically classified into six categories [2]: public and social projects [3], software/IT initiatives, research and development (R&D) efforts, production [4], construction and infrastructure, investment, and defense projects.

In contemporary management practices, PPS has become a vital mechanism for various organizations, particularly technology companies and research institutions, to achieve strategic objectives and sustain market competitiveness. Given the rapid evolution of market environments and the acceleration of technological innovation, the effective selection and optimization of R&D project portfolios have become crucial for enterprises seeking to secure a sustainable competitive advantage. Although numerous studies have delved into the issue of R&D project portfolio selection, several challenges have not been adequately tackled. First, there exist intricate interrelationships [5] among R&D projects, such as resource sharing and technological complementarity. These interactions cause projects to exhibit diverse variations in resource consumption and income at different stages of the implementation process, thereby making it arduous to plan project selection and resource allocation of the overall project plan in the early stages. Furthermore, the selection of projects merely addresses the question of “which to pursue”, without resolving the issue of “when to undertake”. Failure to complete projects within the expected timeframe can similarly lead to significant losses. Finally, the project portfolio encompasses diverse decision-makers with distinct concerns, and frequent conflicts exist among these goals. For instance, high returns may be accompanied by high risks, and rapid implementation may result in higher costs. These types of conflicts can be resolved by employing a multi-objective optimization method [6]. However, this approach also has drawbacks related to solution efficiency and the generation of more non-dominated solution sets [7]. These solutions do not dominate one another, making it challenging for decision makers to obtain the most satisfactory solution. Thus, conventional methods struggle to effectively resolve the issues present in R&D project portfolio selection. Additionally, existing research has yet to simultaneously consider these problems and provide a perfect solution. Therefore, there is an urgent need for a comprehensive model to address this issue.

Based on these characteristics, this paper is the first to describe the R&D project portfolio selection problem as follows. Decision-makers select projects that need to be developed for the next planning stage, and these projects have a fixed R&D duration. Simultaneously, interactive relationships exist among the projects, which impact the resources, success rates, and benefits during different periods, complicating the selection of a group of project portfolios that would maximize benefits and minimize risks. By comprehensively considering the project life cycle, project interaction, and various resource types, this study identifies and analyzes the characteristics of non-dominant solutions to provide a more comprehensive, refined, and inclusive project portfolio selection and decision-making model with the following features:

- Considering the full project lifecycle: Incorporating the construction timeline of each project into the selection process ensures completion within planned schedules, enabling more efficient resource allocation.

- Considering project interactions: Our method accounts for the complex interactions that may arise between projects. By evaluating the effects of these interactions, we gain a clearer understanding of the portfolio’s overall value, risks, and other key factors.

- Refined selection method: We introduce a new decision-making framework that assesses solution quality based on the specific characteristics of the solution set, providing decision-makers with more objective and informed outcomes.

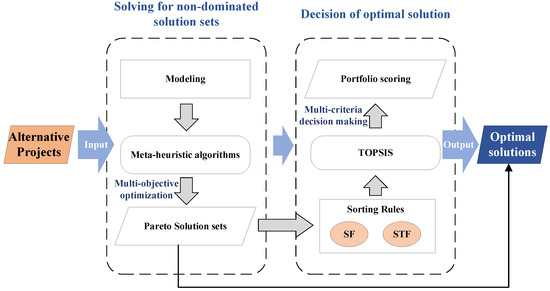

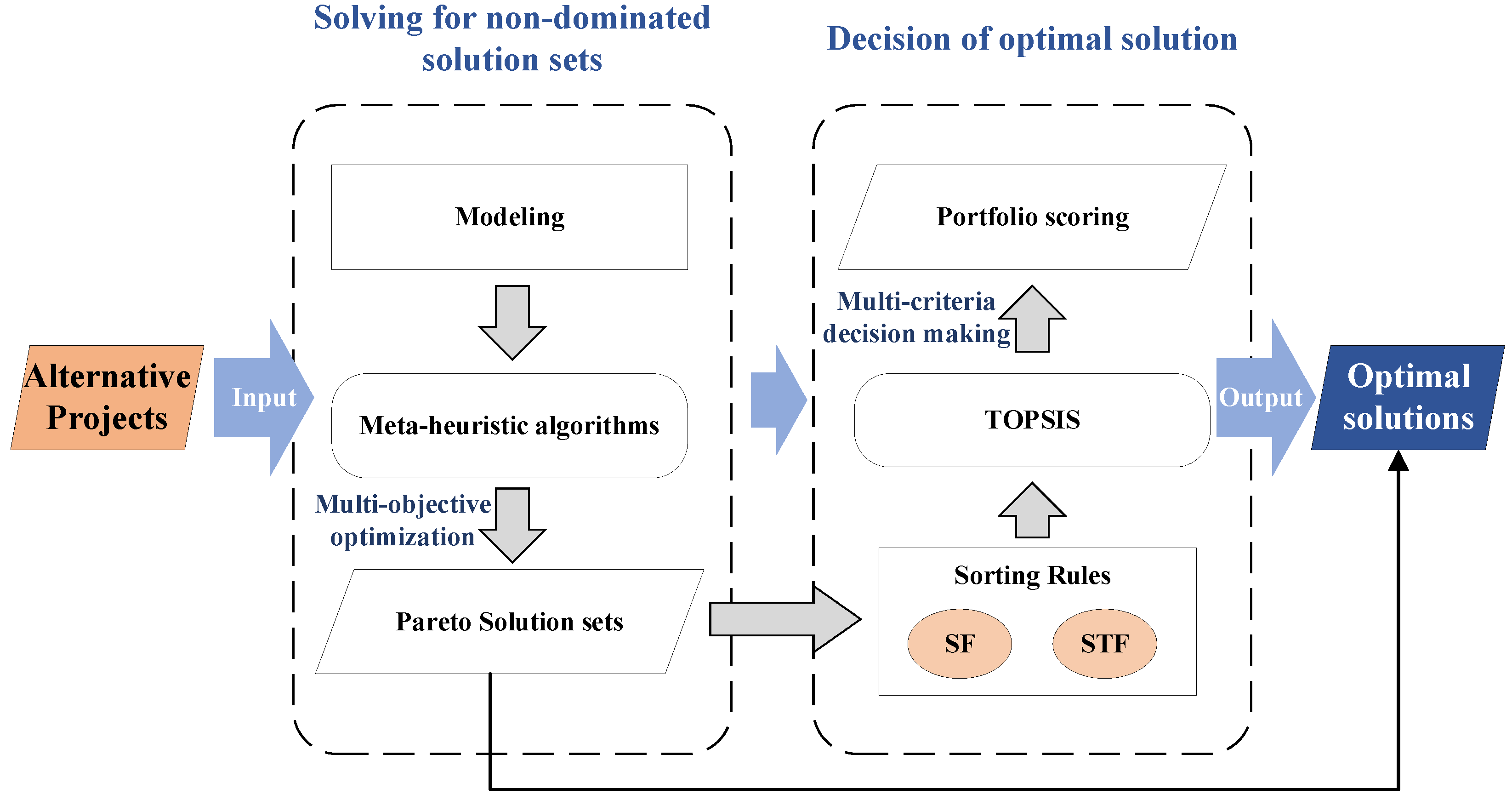

Accordingly, considering these proposed improvements, we built a comprehensive portfolio selection framework, which covers the entire process of project selection, as shown in Figure 1.

Figure 1.

Framework flowchart.

2. Literature Review

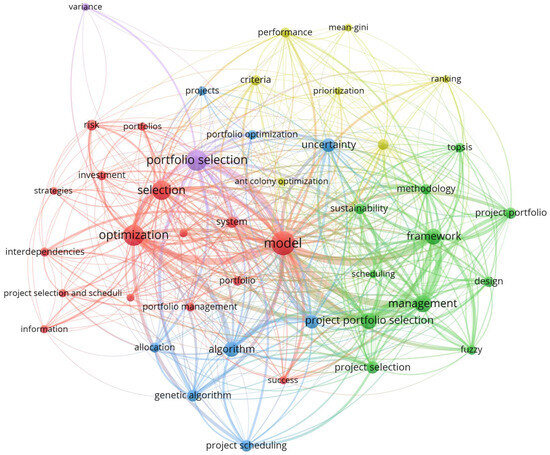

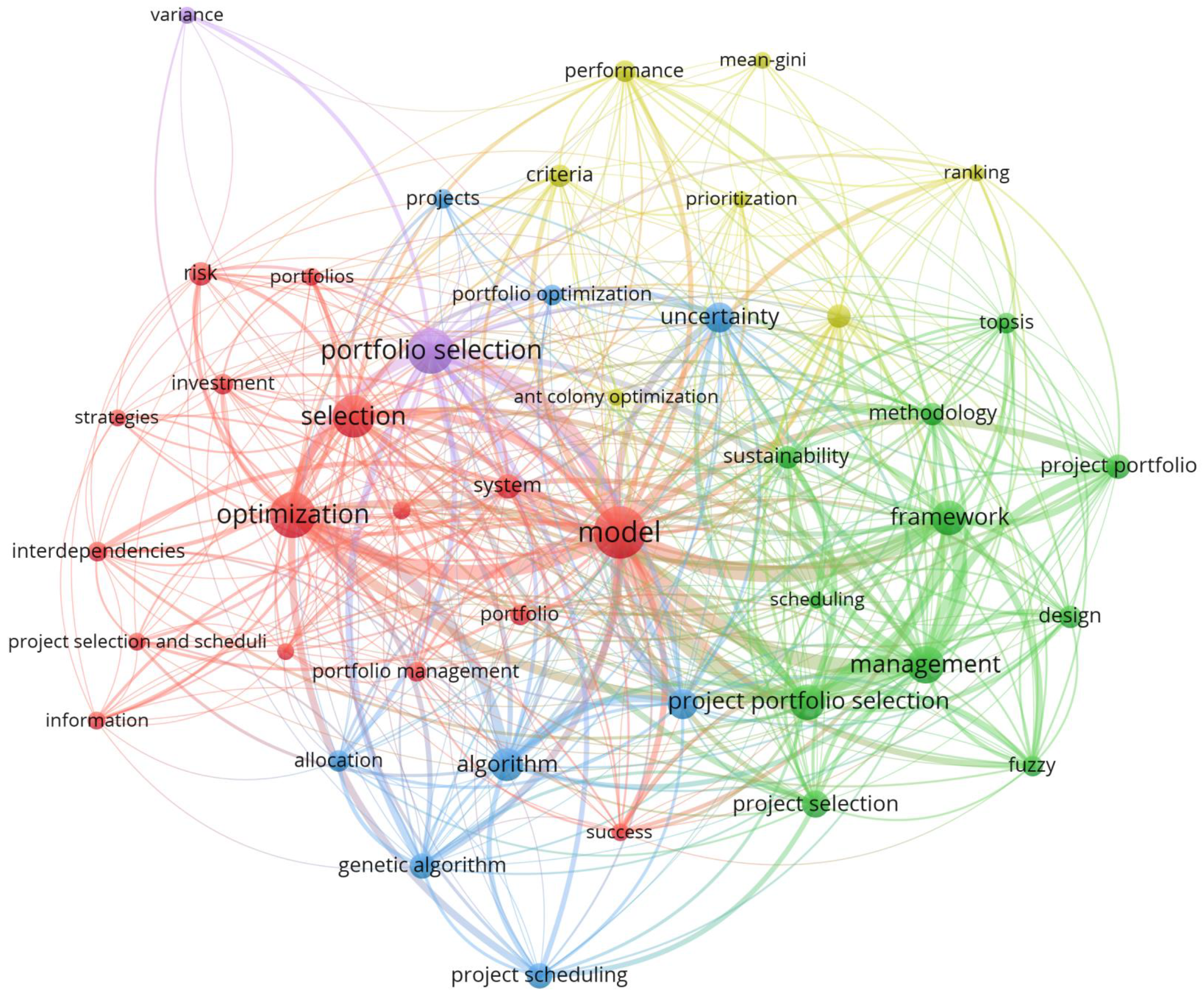

Through an extensive review of the literature, we identified that the primary research focuses in the project portfolio selection problem include multi-criteria decision making, uncertainty, algorithms, interdependencies, and scheduling, as shown in Figure 2. Numerous aspects are involved, and many researchers have previously provided comprehensive reviews on these topics. Therefore, based on the scope of our study, we will concentrate our review and summary on the following three aspects: collaborative modeling, multi-objective optimization, and resource constraints of project portfolios.

Figure 2.

The research point of project portfolio selection problem.

2.1. Project Portfolio Selection

The project portfolio selection problem (PPSP) originates from the knapsack problem [8]. It is a simplified knapsack problem with the intricate constraints and nonlinear conditions of the project portfolio selection eliminated. In essence, projects should be akin to the knapsack of an organization, aiming to maximize value creation. Project portfolio selection and scheduling can be considered incrementally or as an integrated approach. An essential tool in this process is portfolio evaluation, which helps identify the optimal combination.

To evaluate portfolio selection, Stummer [9] proposed an evaluation framework comprising five steps: pre-screening, individual project analysis, screening, portfolio selection, and adjustment. Additionally, some studies have focused on constructing a portfolio evaluation index system to identify evaluation indicators based on specific research problems and application directions.

Work on PPSP has demonstrated that the sequential consideration of portfolio selection and execution plans result in suboptimal solutions [10], indicating the need to address both aspects simultaneously. Despite this early observation, a significant portion of research in this area has predominantly focused on either project selection [11] or project scheduling [12,13], often neglecting to comprehensively integrate both [14].

2.2. Decision Criteria in Portfolio Selection

The portfolio measurement criterion serves as a critical component in decision making, reflecting value judgments that consider actual needs and information patterns. It forms the foundation of multi-objective portfolio optimization. Presently, this criterion is mainly based on the benefit standard, generally using the net present value, efficiency, cost ratio, and rate of return to measure economic benefits. Wang et al. [15] proposed a new mean-variance model of uncertainty by considering the probability variance of returns as the investment risk of a project. Tavana [16] and Carlsson [17] et al. adopted rough and fuzzy sets, respectively, to solve the problem of income uncertainty and optimize the benefits of the project portfolio. Risk criteria [18] and capability criteria [19] are also important reference factors.

This a very useful method for ranking schemes using the multi-criteria decision-making method. Souza et al. [20] argued that criteria determination is crucial, proposing the hypothesis that the criteria used in the development of PPS can be selected in an uncertain environment based on impact and importance, thereby proposing an innovative fuzzy logic multi-criteria decision-making method (MCDM) for this purpose. This method integrates the fuzzy analytic hierarchy process (AHP) and fuzzy decision-making trial and evaluation laboratory (DEMATEL) models to deal with uncertainty and complex criteria selection problems. Through a real case study of a representative public electric power R&D organization in Brazil, the effectiveness of this method in optimizing R&D project portfolio management was proven, especially in prioritizing environmental, social, and technical criteria, with practical guiding significance.

Multi-objective optimization is an important method for project portfolio optimization, in balancing multiple conflicting objectives such as costs, benefits, and risks of different projects, to finally select the optimal project portfolio [21]. The model of multi-objective optimization for project portfolios is more in line with the requirements of actual scenarios, with many constraint parameters and complex objective functions. In addition to heuristic algorithm solutions, intelligent optimization algorithms are a common way to solve the problem, by mainly simulating the intelligent behavior in nature (such as biological evolution and swarm intelligence) to solve complex project portfolio problems. It has global search ability, nonlinear problem processing ability, and adapts to real-time changing environments [22]. The core idea of an intelligent optimization algorithm is to search for a solution relatively close to the optimal global solution, which is often used to solve non-convex optimization problems, such as the genetic algorithm [23], ant colony algorithm [24], and particle swarm algorithm [25], among others. Multi-objective optimization methods have been applied in many industries to solve complex combination problems. Nielsen et al. [26] added the consideration of strategy, skills, and business objectives, and proposed a multi-objective optimization scheme to ensure that the selection of R&D projects is consistent with the enterprise objectives. Reza Alinezhad [27] established a dual-objective mixed integer nonlinear programming model with the aim of maximizing the net present value and minimizing the variance of renewable resources in resource balance, and realized the selection and scheduling of phased projects. Milad Ghanbari et al. [28] designed a multi-objective genetic algorithm to optimize the combination selection process with the goal of minimizing risk and maximizing net present value. Chen et al. [29] took a large number of projects as a case study, considered the unique characteristics of overseas oil investment compared with ordinary investment portfolios, incorporated political risk quantitatively into the model, developed a nonlinear multi-objective binary programming, and optimized the investment portfolio under three competitive objectives.

2.3. Scheduling Constraints in Project Portfolio Selection

Project portfolio constraints are divided into four categories: value, cost, rationality, and relationship constraints. The meanings of the value and cost constraints are the same as those of the value and cost classes in the objective function; however, the constraints are generally restricted by setting thresholds [30]. Multiple projects may require the same resources simultaneously, and these resources are often limited. This leads to resource competition among different projects, and the effective allocation of resources becomes a key issue in management [31]. Each project has its specific time node and schedule requirements, and the priority of resource allocation should consider not only the strategic importance of the project but also the urgency of time and dependency between projects [32]. Some researchers have organically linked project portfolio decision making and project scheduling, attempting to organically combine project scheduling with project portfolio decision making, to obtain results in practice [33,34]. Related research can be divided into project selection, overall scheduling, and project task scheduling. The selection of the project and the overall scheduling are regarded as an inseparable whole, with project scheduling only referring to the continuous execution of multiple stages of the entire project, without considering the scheduling of lower-level work plans [35]. Moon [36] optimized the robustness model of the project portfolio, by proposing the average absolute deviation model, obtaining the superiority of the model through test data, and reducing the strategic estimation error of the project portfolio. Smith-Perera et al. [37] introduced ANP to select and configure projects based on strategy considering the mutual influence of various elements in the network hierarchy, to achieve the optimal configuration effect. This provides a new idea for evaluating the consistency between project portfolio configuration and organizational strategy. Long et al. [38] used a fuzzy critical chain to solve the project scheduling problem considering resource constraints and project uncertainty. Laslo [31] constructed an optimization model to solve resource allocation and scheduling among projects in a project portfolio. Ghomi et al. [39] used the queuing theory to establish a model for resource allocation of multiple projects and provided a collective example.

2.4. Interaction Modeling in Project Portfolio Selection

The concept of project interactions was first introduced by Baker and Freeland [40], who argued that existing models fall short of practical requirements by failing to account for these interactions. Pendharkar and Rodger [41] further highlighted that portfolio value can be enhanced through synergies between projects. Killen [42] visualized these interactions, while Lopes and Almeida [43] employed a multi-attribute utility function to assess them.

Project interactions have since become an important research topic, generally classified into resource, benefit, and outcome interactions [44]. Zorluoğlu [45] considered complementarity and mutual exclusivity between projects, incorporating these as constraints in project portfolio selection and scheduling studies. Liesio [46] et al. modeled interactions using a combination effect function, explaining that interaction effects act as additional terms in an additive portfolio utility function. Their simulations, based on both randomly generated and real-world datasets, demonstrated the negative impact of ignoring project interactions on the expected utility of decision making and portfolio recommendations. Wei [47] et al. constructed a project interaction network using co-citation networks based on the dependencies between projects and technologies, incorporating these interactions as a regularization term in an additive function to represent their effect on portfolio value.

2.5. Findings of the Literature Review

Through a review of the literature, it can be found that this study offers the following three innovations:

- A comprehensive approach is proposed, which integrates project interactions, multi-objective optimization, and refined solution selection.

- A new heuristic algorithm is proposed, which combines the advantages of the two algorithms for a more efficient solution.

- A new scheme refinement selection method is proposed, which mines the ranking rules based on the features of the schemes and avoids the subjective preference in the decision of multiple schemes.

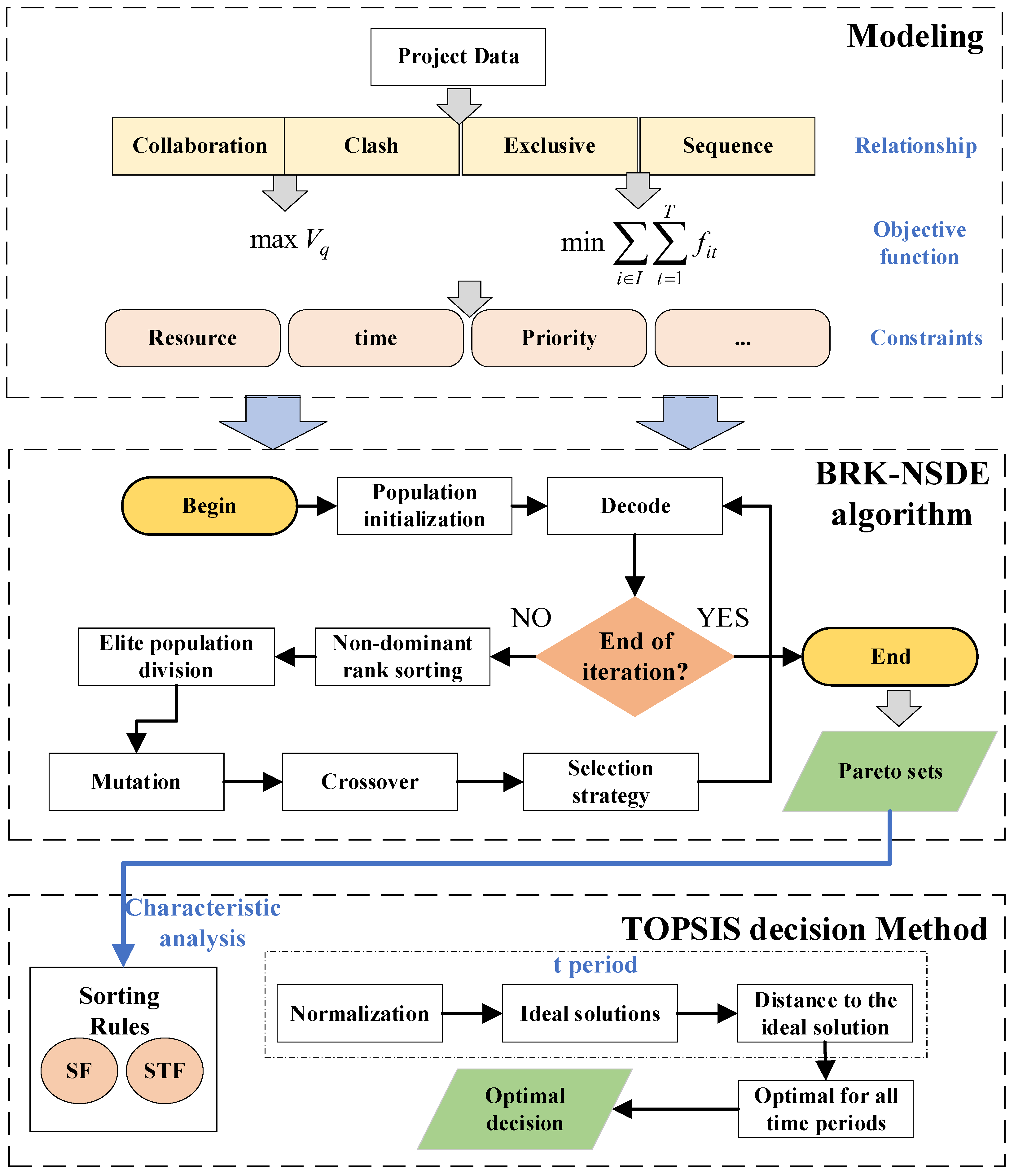

Accordingly, we designed the entire process framework from problem modeling to the solution method and then to the solution decision method and list the proposed technologies in detail. For the specific technologies and methods, the reader is referred to Figure 3.

Figure 3.

Technology roadmap.

3. Model Formulation

This section presents a mathematical model of the PPSP. The notations used are as follows. The portfolio definitions, objectives, and constraints are detailed in the following subsections.

3.1. Notations

Some common notations used in the model formulation are presented in Table 1.

Table 1.

Notations.

3.2. Decision Variable

The project portfolio selection problem typically uses two-dimensional variables to represent decision variables, as:

where i = 1, 2, …, I and t = 1, 2, …, T. = 1 indicates that project i is executed during period t. In this context, a vector x = {, , …, , , …, }, composed of I variables, denotes a project portfolio. With the known execution time for project i, this variable specifies the start and end times, forming a PPSP plan.

3.3. Objective Function

The optimization model is established as follows:

Subject to:

where Equations (2) and (3) represent the two objective functions: benefit maximization and risk minimization, respectively. Additionally, Equations (4) and (5) calculate the benefits, incorporating the additional gains resulting from project interactions across different periods. The risk calculation method follows the approach of [48,49,50], where the combined risk [51,52] of project interactions is determined using Equations (6)–(9).

Equation (10) determines the interaction between project i and project j at stage t. Equation (11) represents the cost constraint of the project portfolio, where the budget requirements must be met at each stage. Equation (12) represents the project quantity constraint, ensuring that the number of projects under construction at the same time does not exceed the demand, allowing the company to better control the progress of the projects. Equation (13) represents the project timeline constraint, indicating that the project must be completed within the specified time. Equation (14) states that each project can only be selected once; once selected, it must be completed. Equations (15) and (16) represent the project priority constraint. Equation (15) indicates that project i must start after project j is completed, while Equation (16) indicates that project i can only start after project j has begun. Equation (17) represents the mutual exclusivity constraint, where project i and project j cannot be selected at the same time.

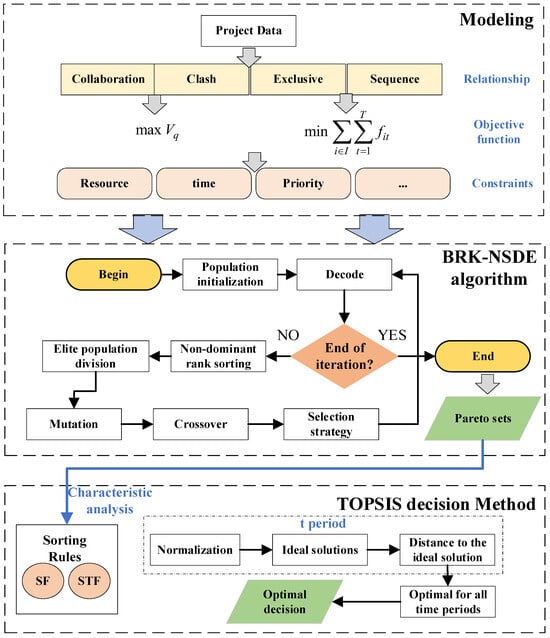

3.4. Solving Algorithm

The project portfolio selection problem (PPSP) is NP-hard, making it extremely challenging to solve using exact algorithms. To address this, researchers have developed numerous algorithms to tackle the PPSP. The Random Key Genetic Algorithm (RKGA) [53] is a real-valued variant of the Genetic Algorithm (GA) for combinatorial optimization, utilizing random keys. In this method, random numbers within the range [0, 1], known as random keys, act as sorting keys to decode individuals into their corresponding solutions. These decoded solutions are then evaluated and ranked according to their objective fitness. The Biased Random Key Genetic Algorithm (BRKGA) [54] is an enhanced version of RKGA, primarily differing in the approach to parent selection during crossover. In BRKGA, one parent is chosen from the elite population, while the other comes from the non-elite population, with the selection process favoring the elite, giving its genetic material a higher probability. BRKGA has demonstrated significant performance improvements over RKGA. Differential Evolution (DE) [55] is another evolutionary optimization algorithm that iteratively improves a population of candidate solutions. Initially, the population is randomly distributed within the feasible search space and updated through mutation, recombination, and selection. The recombination operator plays a central role in generating new trial positions. When a trial position offers better objective fitness than the current position, it replaces the previous one. This approach often enables DE to achieve faster convergence.

This paper introduces a novel multi-objective solution algorithm that combines the approaches of BRKGA and DE, leading to the development of the biased random key - non-dominated sorting differential evolution (BRK-NSDE) algorithm. The proposed algorithm combines several of these algorithms while retaining their advantages.

The following are the detailed steps of the algorithm.

3.4.1. Population Initialization

Given a population size N, the set of N randomly generated individuals is called population P. Each individual is represented as a vector of random keys in , where K represents the size of the planned projects in the project portfolio. When generating the initial population, each random key of an individual obeys a uniform distribution within the interval [0, 1].

Randomly generate N random key vectors from , where k is the number of projects, to represent the initial population P.

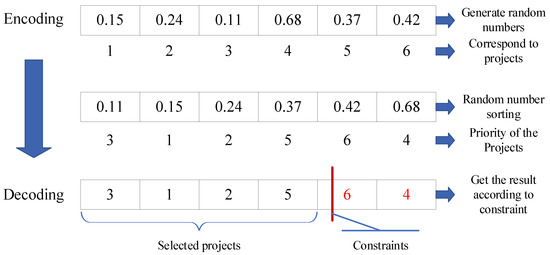

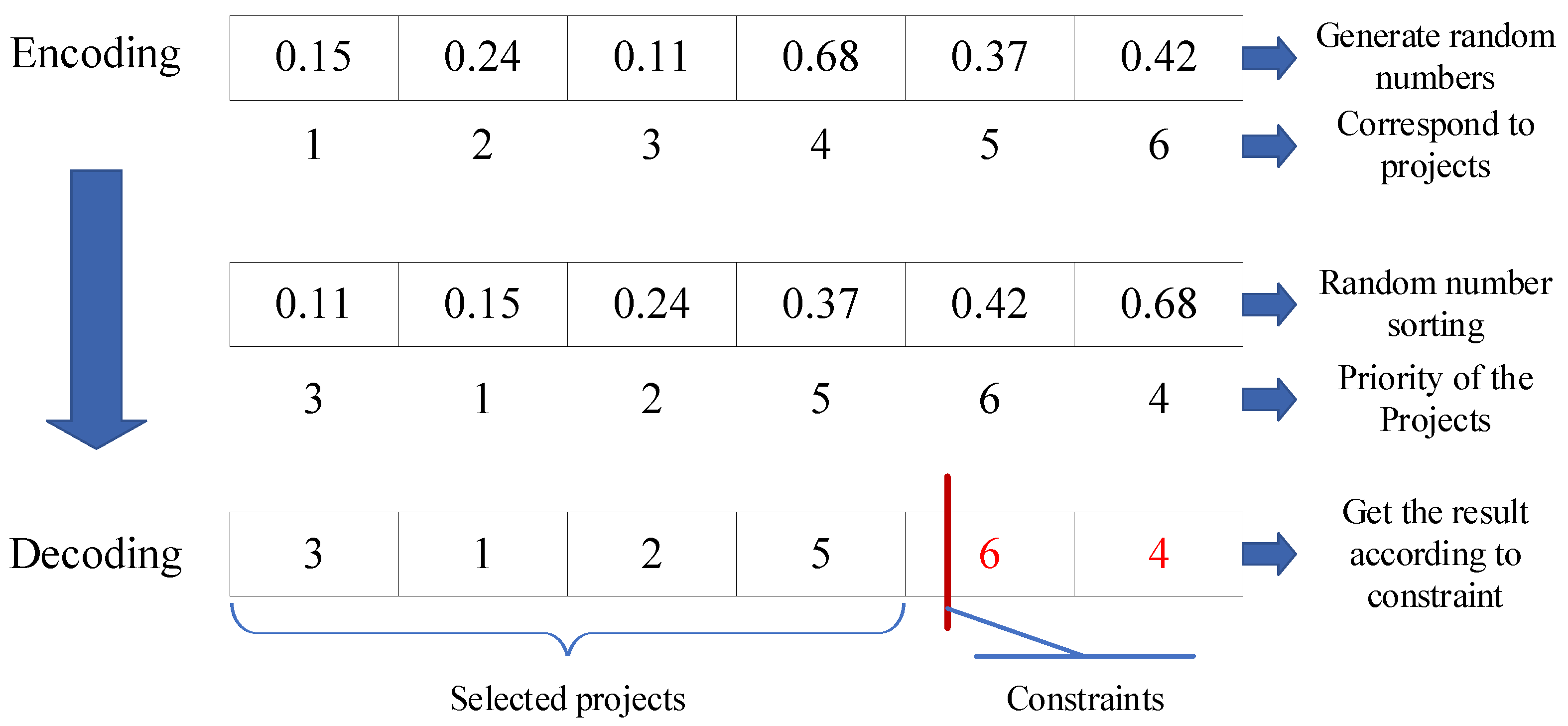

3.4.2. Decode

Each individual in the population is translated into a solution for the problem, and the associated fitness value vectors are computed. The random key vectors assigned to individuals are arranged in ascending order, establishing project priorities and determining the sequence in which the projects will be executed. Figure 4 provides an example to illustrate the encoding and decoding principles.

Figure 4.

Example of encoding and decoding.

3.4.3. Determine if Ended

Determine whether the iteration is complete. There are three conditions for the end of iterations:

- The number of iterations reaches the specified algebra;

- Some individuals in the current population have attained a satisfactory value for each objective function;

- After iteration of the specified algebra, the non-inferior solution set does not change.

If not, proceed to Step 4; otherwise, end the process and return the non-inferior solution set for the current population.

3.4.4. Non-Dominant Rank Sorting

In this study, the crowding ranking of NSDE-II was used for the non-dominant ranking.

3.4.5. Elite Population Division

According to the non-dominant ranking of the population, the top individuals are selected according to the proportion that are among the elite.

3.4.6. Mutation

The current population P is mutated to obtain a new population. The mutation strategy adopted in this study was based on the DE algorithm. Specifically, a parent vector is selected as the reference vector from the elite population, and two other vectors, and , are randomly selected as difference vectors to obtain , as shown in Equation (18).

3.4.7. Crossover

3.4.8. Select

Elites are selected from the offspring. These elite individuals are selected using the crowding comparison operator, which is a non-dominated sorting method.

4. Decision-Making Method

4.1. Decision-Making Indicators

Multi-attribute decision-making methods are commonly employed to select solutions. However, these criteria are still based on evaluating project attributes, which can lead to conflicts among the criteria and introduce some level of subjective bias into the final decision. To address this, this paper proposes a new decision-making method that is independent of project attribute values. This approach is more suitable for evaluating non-dominated solution sets, where direct comparisons of superiority or inferiority are not possible. The proposed decision method is based on the following criteria:

- Projects that appear more frequently than others in different non-dominated sets are likely to perform better and should receive more attention.

- Project interactions that are frequently activated are considered to help the project portfolio achieve higher benefits.

Therefore, the following indicators were designed based on the above principles, using variables P1 and P2 as examples.

4.1.1. Selected Frequency (SF)

SF is the number of times project P1 appears in all datasets within period t divided by the total number of datasets. The calculation of SF is shown in Equation (21), where frequent (P1) denotes the frequency of items P1 appearing, and ALLSample indicates the total number of datasets.

4.1.2. Selected Together Frequency (STF)

This can be explained as the association probability of certain items. The calculation method is shown in Equation (22).

4.2. Decision-Making Method Using TOPSIS

Technique for order preference by similarity to ideal solution (TOPSIS) compares the distance of all candidates with the positive and negative ideal points. The TOPSIS method is characterized by processing diverse types of data, identifying the optimal and worst schemes, having strong anti-interference ability, and presenting a good visualization effect, among others. In terms of anti-interference performance, considering the comprehensive performance of multiple indicators, TOPSIS is less sensitive to extreme values or outliers of individual indicators and is not readily affected by noisy data. The Pareto solution is situated at the edge, and other decision-making methods may cause interference. Therefore, this method can be used to compare the advantages and disadvantages of the proposed schemes.

Assume that m schemes exist, with the three criteria vectors denoted as and , where . The specific steps of the method are presented as follows.

4.2.1. Normalization

4.2.2. Determine Ideal Solutions

4.2.3. Distance to the Ideal Solution

Calculate the distance between the criterion set of each scheme and the positive and negative ideal solutions, as shown in Equations (28) and (29), respectively.

The relative distance to the negative ideal solution is calculated using Equation (30) as the TOPSIS value:

4.2.4. Calculate the Optimal Solution for All Time Phases

The results so far were calculated for each phase t. Because each solution is a scheduling scheme that contains multiple time phases, the sorting results of each time phase should be aggregated and weighted together as

where in Equation (31) represents the weight of each period.

5. Example Analysis

The case studies presented below demonstrate the feasibility and efficiency of the proposed models and methods.

5.1. Data Instruction

In the case study, part of the data comes from [56], while the other data are generated using the method proposed by [57,58].

Detailed data are presented in Table A1, Table A2, Table A3 and Table A4. Table A1 shows basic information on project revenue, including the total revenue of the project and expected revenue for each year of the development cycle. Table A2 lists the basic information of the project budget, including the total cost of the project and projected investment for each year of the development cycle. Table A3 shows the basic information on the R&D risk of the project, including the construction cycle of the project and annual risk probability within the R&D cycle. Table A4 shows the interaction relationship between projects, including projects that can generate interactions on revenue, cost, and risk, as well as their immediate projects and impact coefficients.

5.2. Results

To validate the effectiveness of the proposed method, the BRKGA and NSGA-II algorithms were selected for comparison. The initial population size was set at 500, and each algorithm was run for 100 generations.

The BRK-NSDE algorithm was implemented as described in this paper.

The BRKGA algorithm differs from the proposed method in its crossover and mutation processes, utilizing multi-point crossover and random-point mutation. During crossover, high-quality parent solutions may share identical genes, leading to offspring with the same encoding, which requires additional processing. Consequently, this makes the BRKGA algorithm slower than the proposed method.

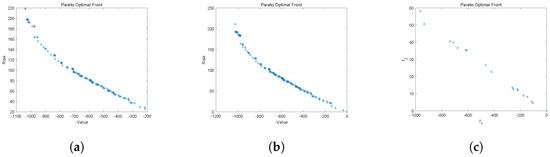

The NSGA-II algorithm employs standard encoding, with chromosomes consisting of 32 genes. The first 16 genes represent binary variables indicating project selection, while the remaining 16 specify the start times of the corresponding projects. Due to the large solution space, the algorithm may have difficulty finding a substantial number of non-dominated solutions within the given number of iterations. The solution times for each algorithm are presented in Table 2, while the Pareto fronts are shown in Figure 5.

Table 2.

The solving efficiency of the algorithms.

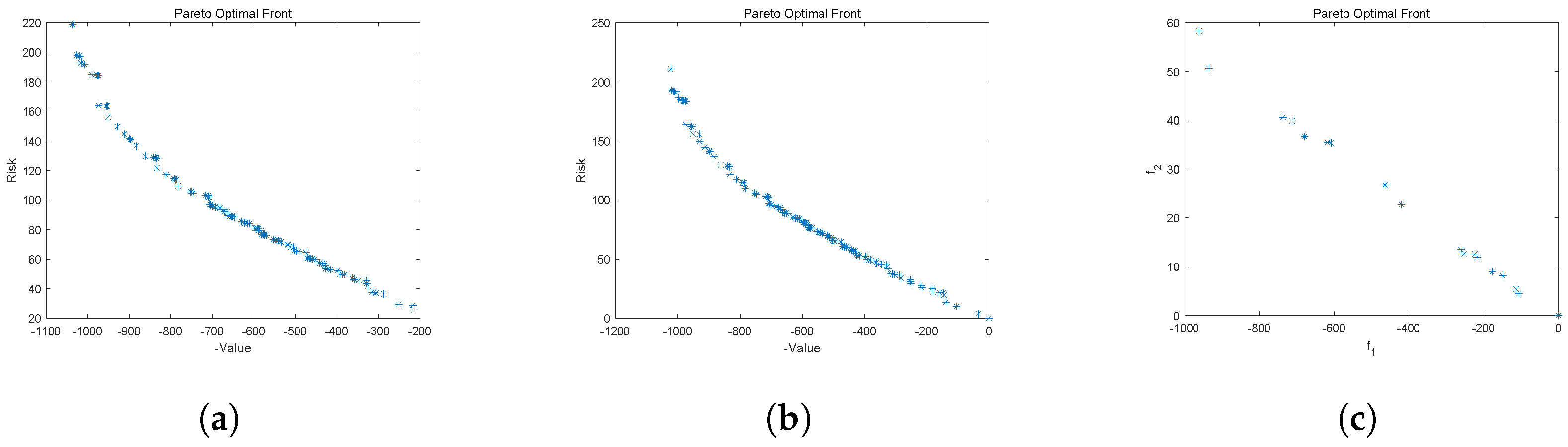

Figure 5.

Algorithm comparison graph. (a) BRK-NSDE. (b) BRKGA. (c) NSGA-2.

Table 2 presents the efficiency of different algorithms. In the BRKNSDE and BRKGA algorithms, special handling is applied to item constraints, resolving violations in advance. For instance, if decoded item i has a higher priority than decoded item j, but the two items are mutually exclusive, the priority of item j is adjusted to the last position during further decoding. This step enhances the solution quality, though it also contributes to the slower iteration speed of these two algorithms. Additionally, due to the large solution space of the NSGA algorithm, its iteration process frequently violates constraints, leading to penalties in the objective function. As a result, high-quality genes struggle to propagate and spread effectively within the population.

As seen in Figure 5, the solutions obtained by the BRK-NSDE and BRKGA algorithms are nearly identical, with both Pareto fronts being relatively smooth. However, the NSGA-II algorithm, constrained by its encoding and large solution space, fails to produce comparable results.

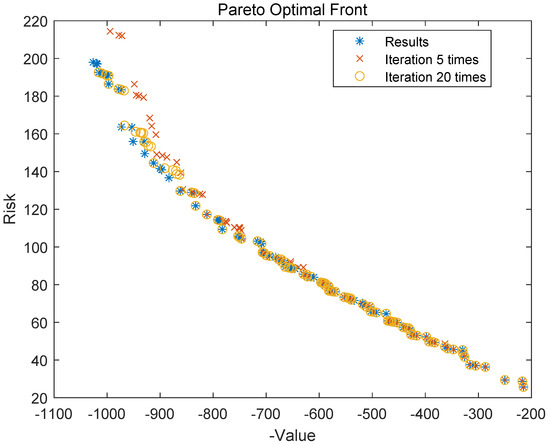

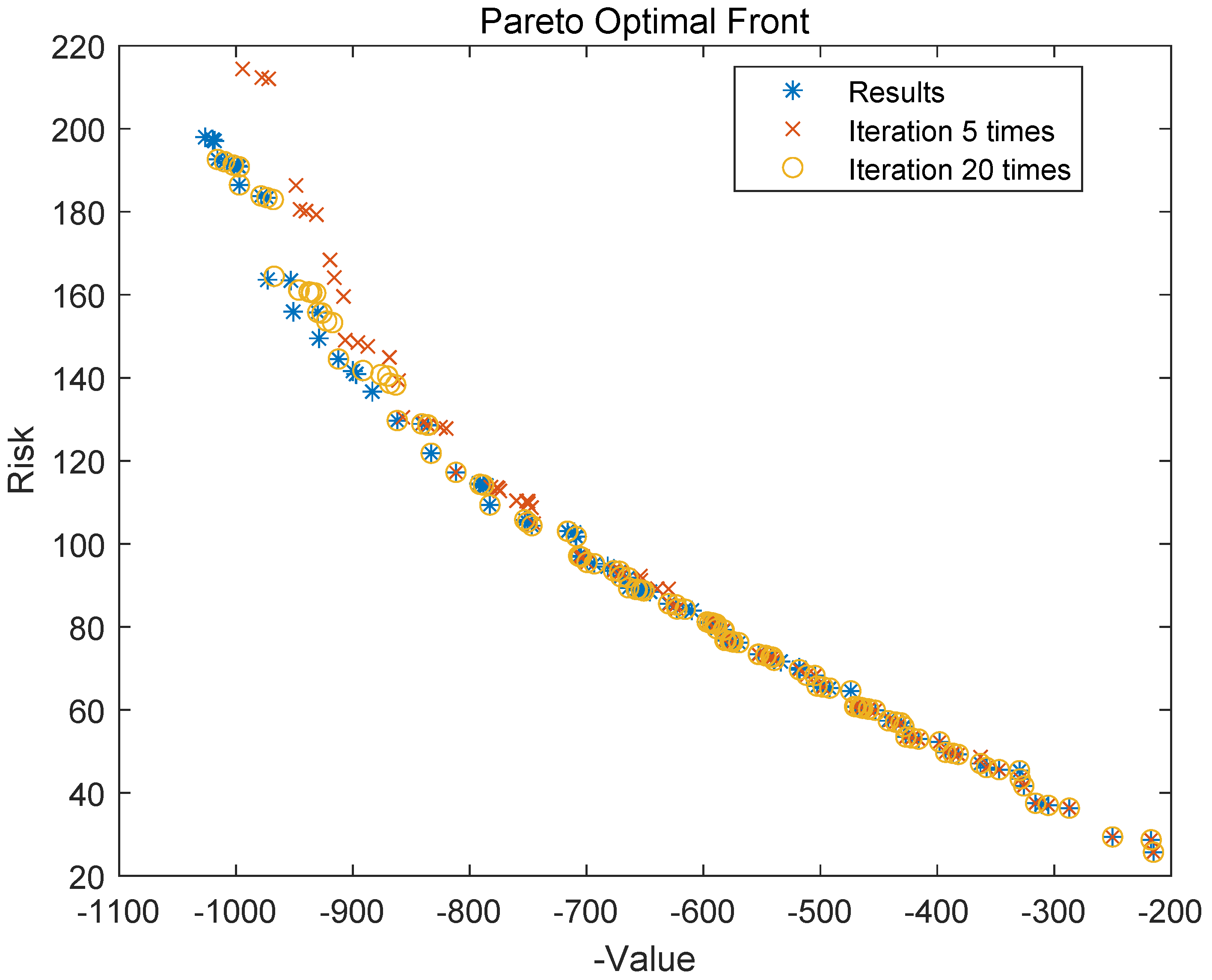

Figure 6 shows that solutions of the BRK-NSDE algorithm after 20 iterations are already close to the final results achieved after 100 iterations, demonstrating the superiority of the proposed method in addressing portfolio optimization problems.

Figure 6.

Algorithm iteration procedure.

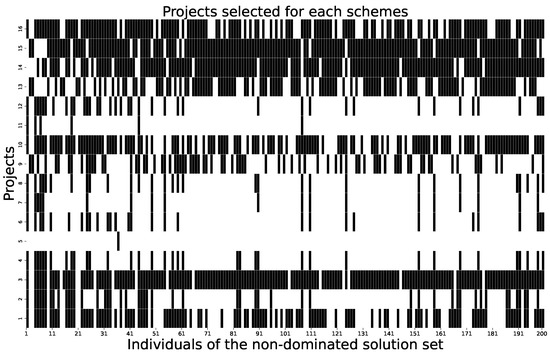

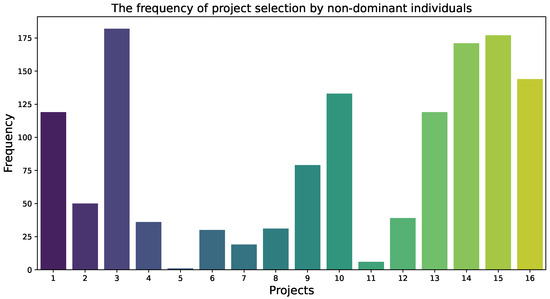

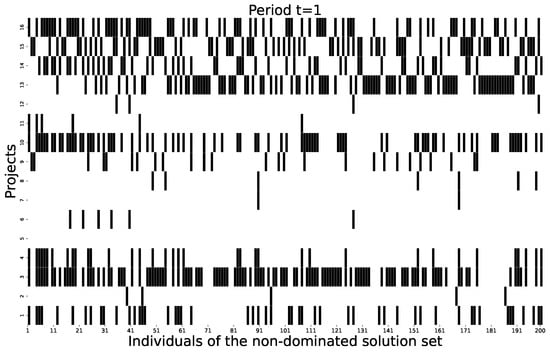

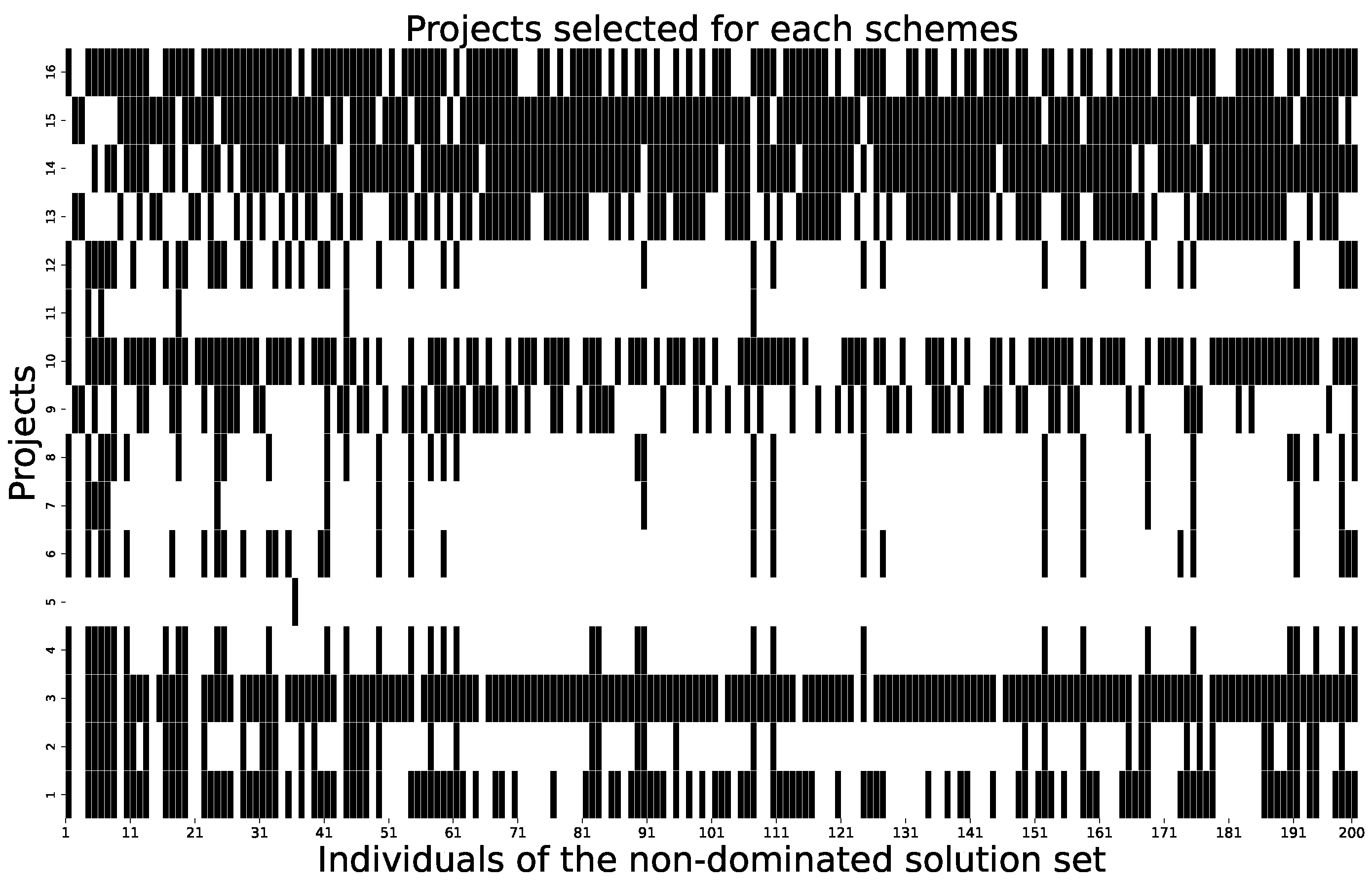

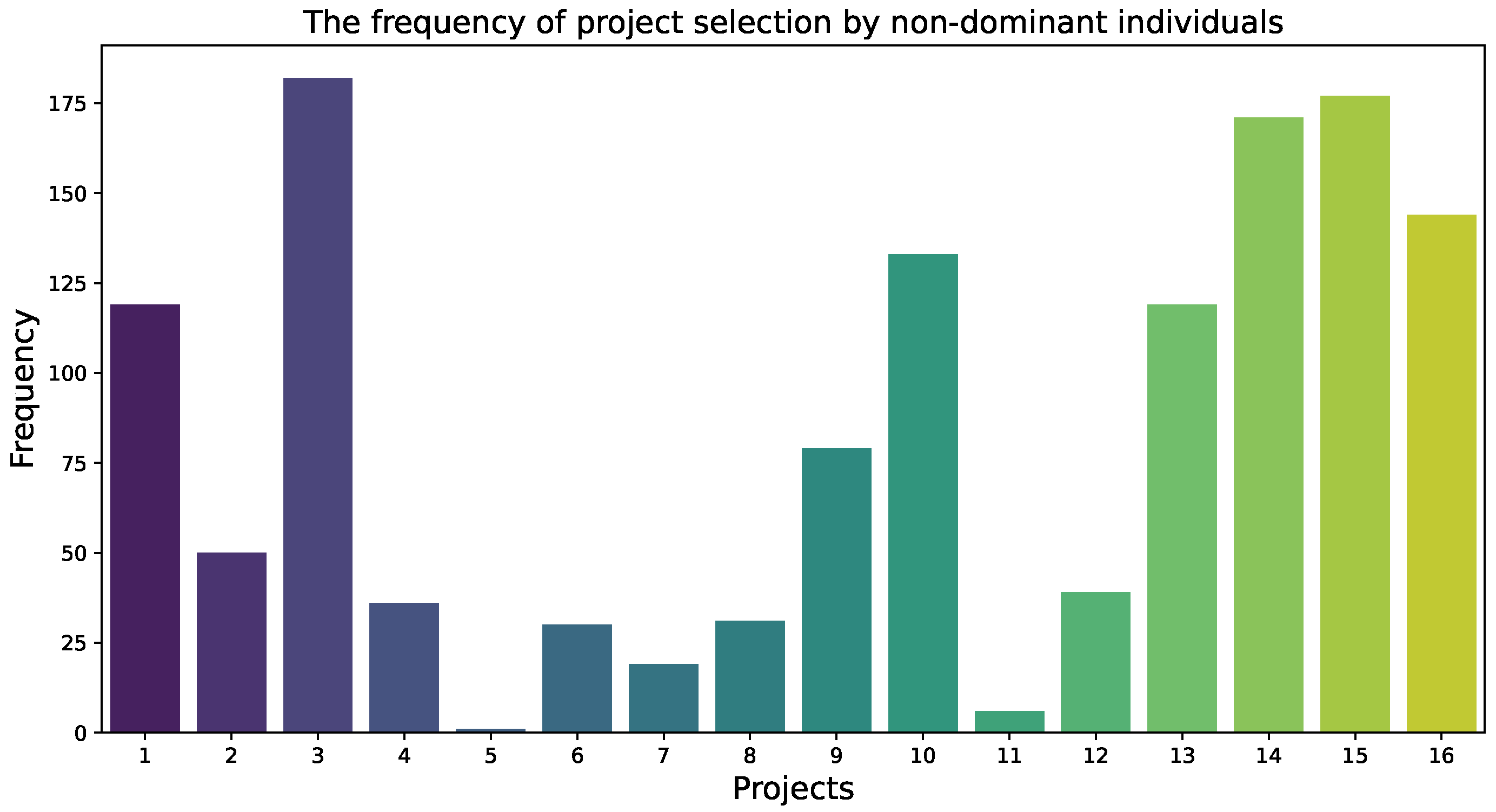

After obtaining the non-dominated solution set through algorithmic solving, we analyzed it to produce Figure 7 and Figure 8. Figure 7 illustrates the selection status of projects in different non-dominated solution sets, where black indicates the project was selected, and white indicates it was not. Figure 8 shows the frequency with which each project was selected across different non-dominated solution sets. By analyzing these results, it is evident that projects 3, 14, and 15 are selected most frequently. This indicates that these projects hold a higher priority over others and should be included in the optimal portfolio plan.

Figure 7.

Situations in which items are selected in different solutions.

Figure 8.

The number of times a project is selected in different solutions.

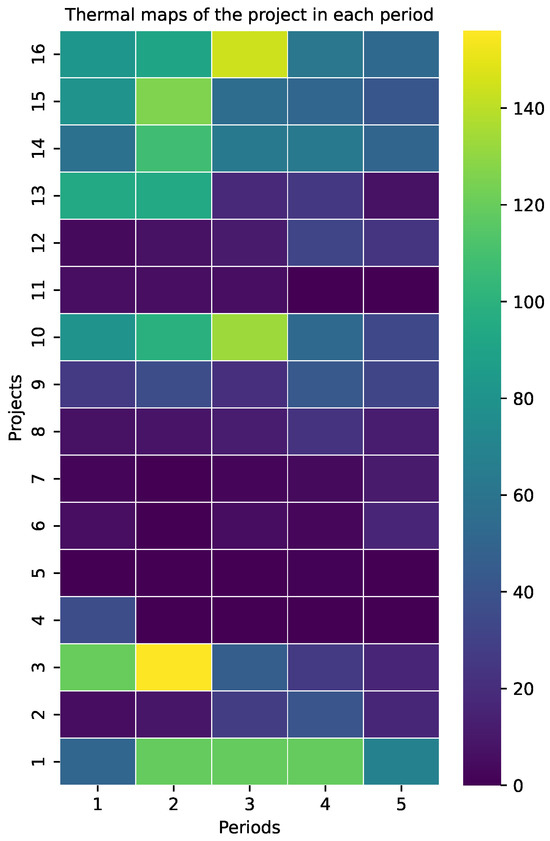

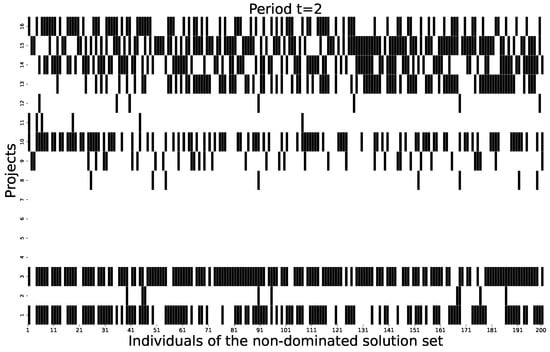

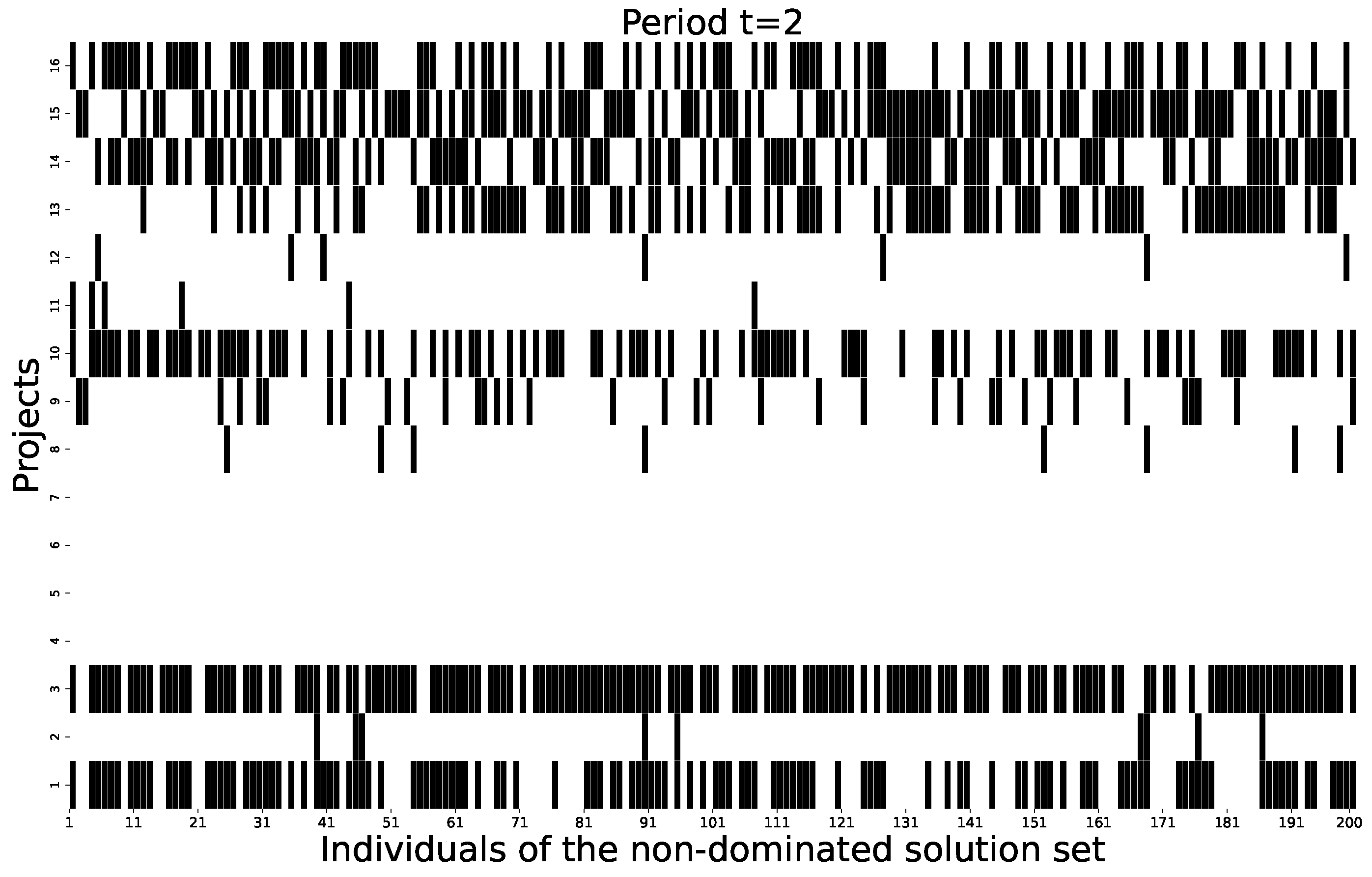

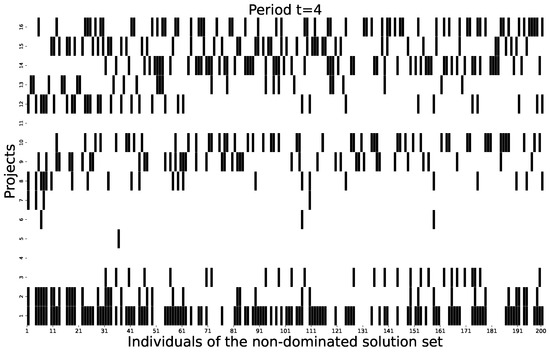

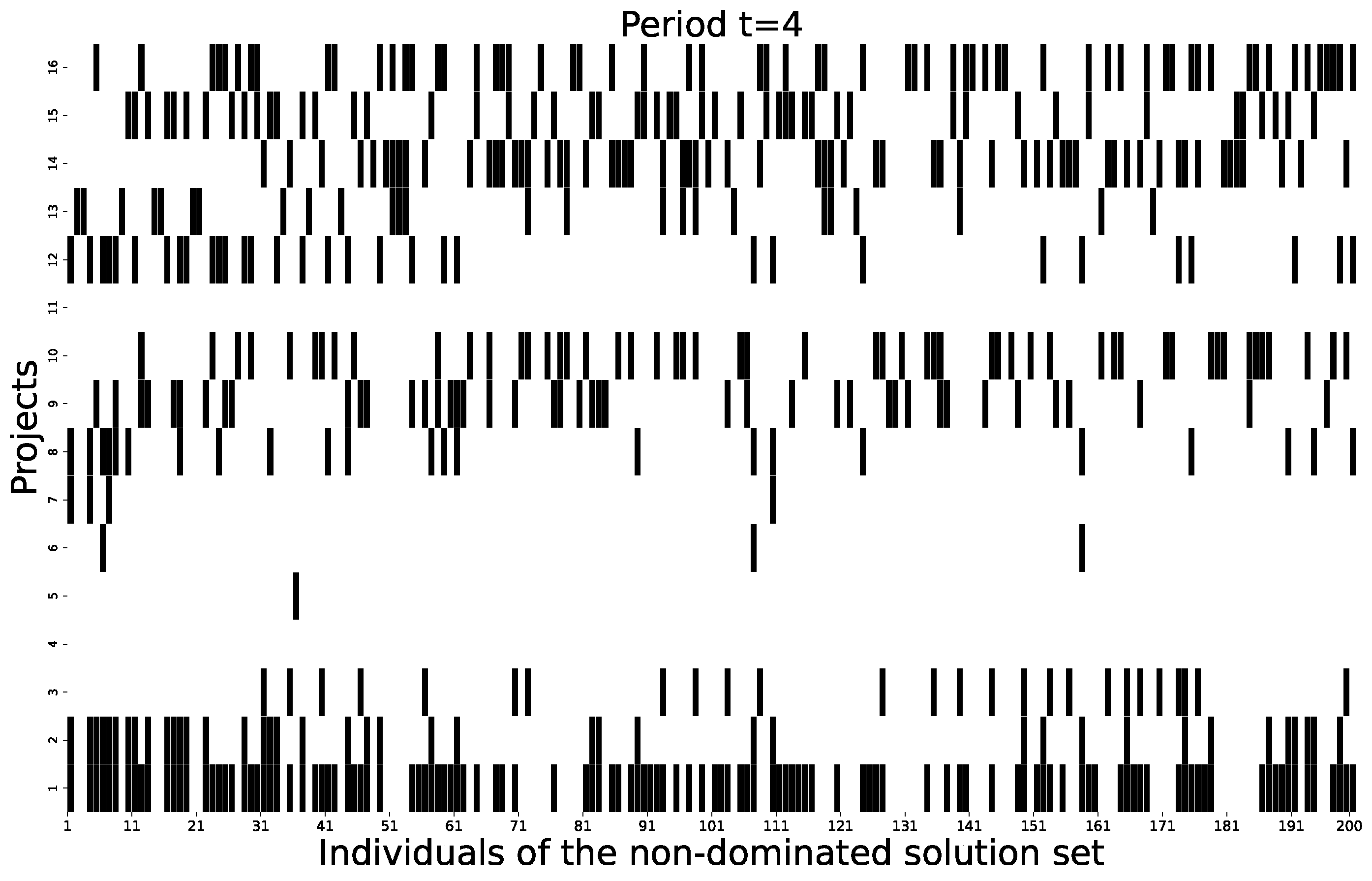

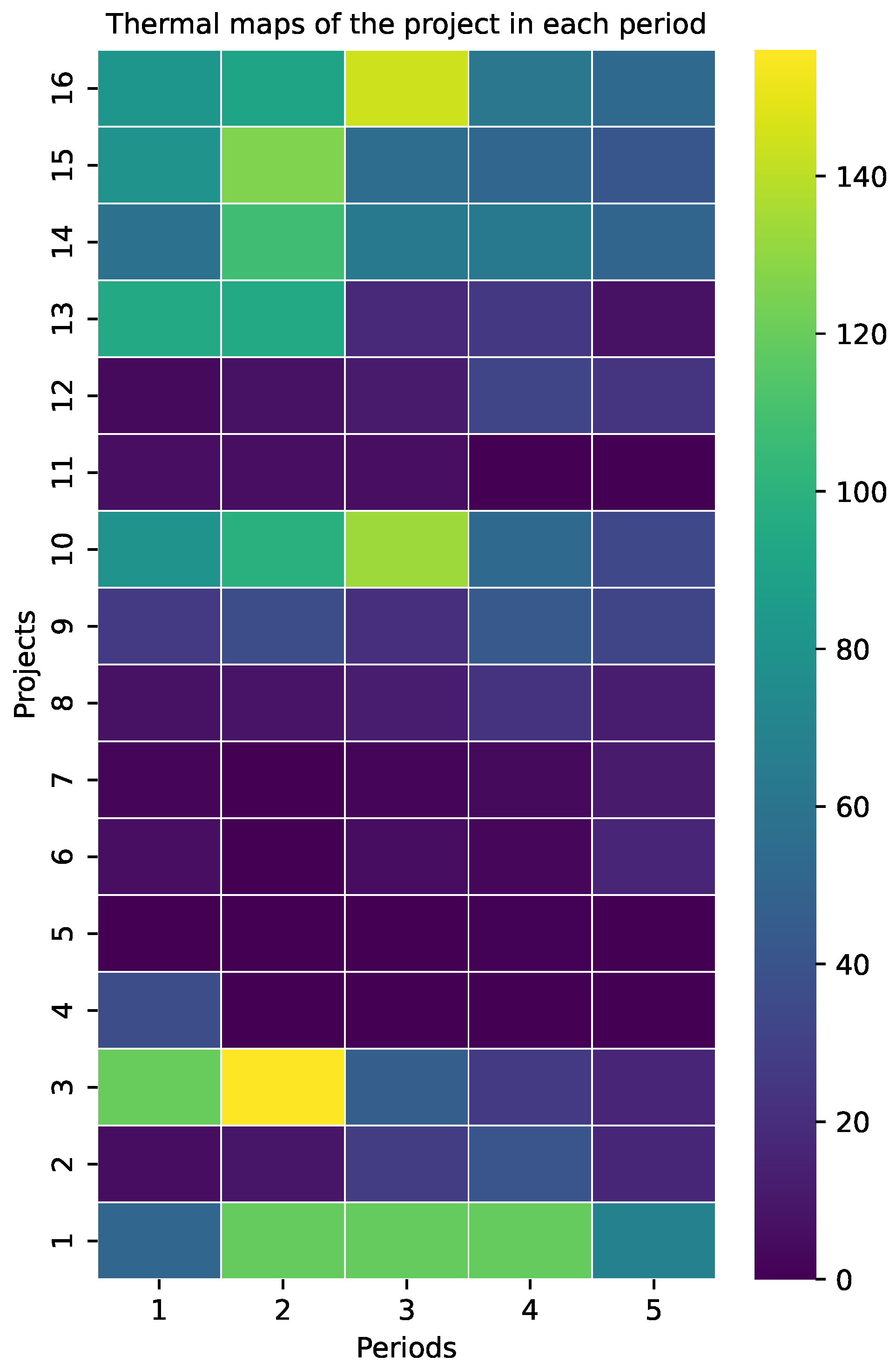

However, the data in Figure 7 and Figure 8 only reflect the selection frequency and do not provide insights into the specific timing for their selection or the potential synergistic relationships among items. Thus, this analysis alone does not fully address our research question. By examining the items selected at each stage within the non-dominated solution sets, we obtain the project schedules illustrated in Figure A1, Figure A2, Figure A3, Figure A4 and Figure A5. These figures clearly show the periods in which each item is most frequently scheduled, leading to the results summarized in Figure 9. Ultimately, applying the TOPSIS method to rank all solutions identifies the optimal plan.

Figure 9.

Thermal maps of the project at different periods.

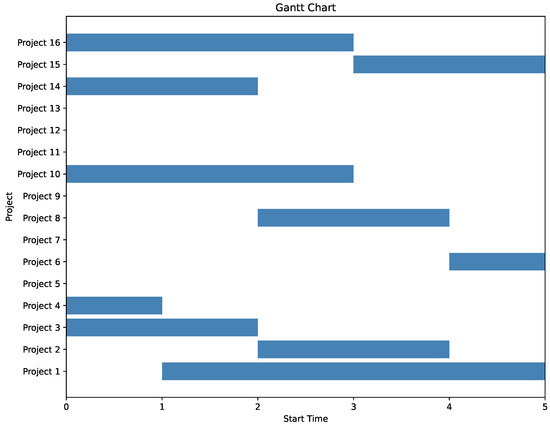

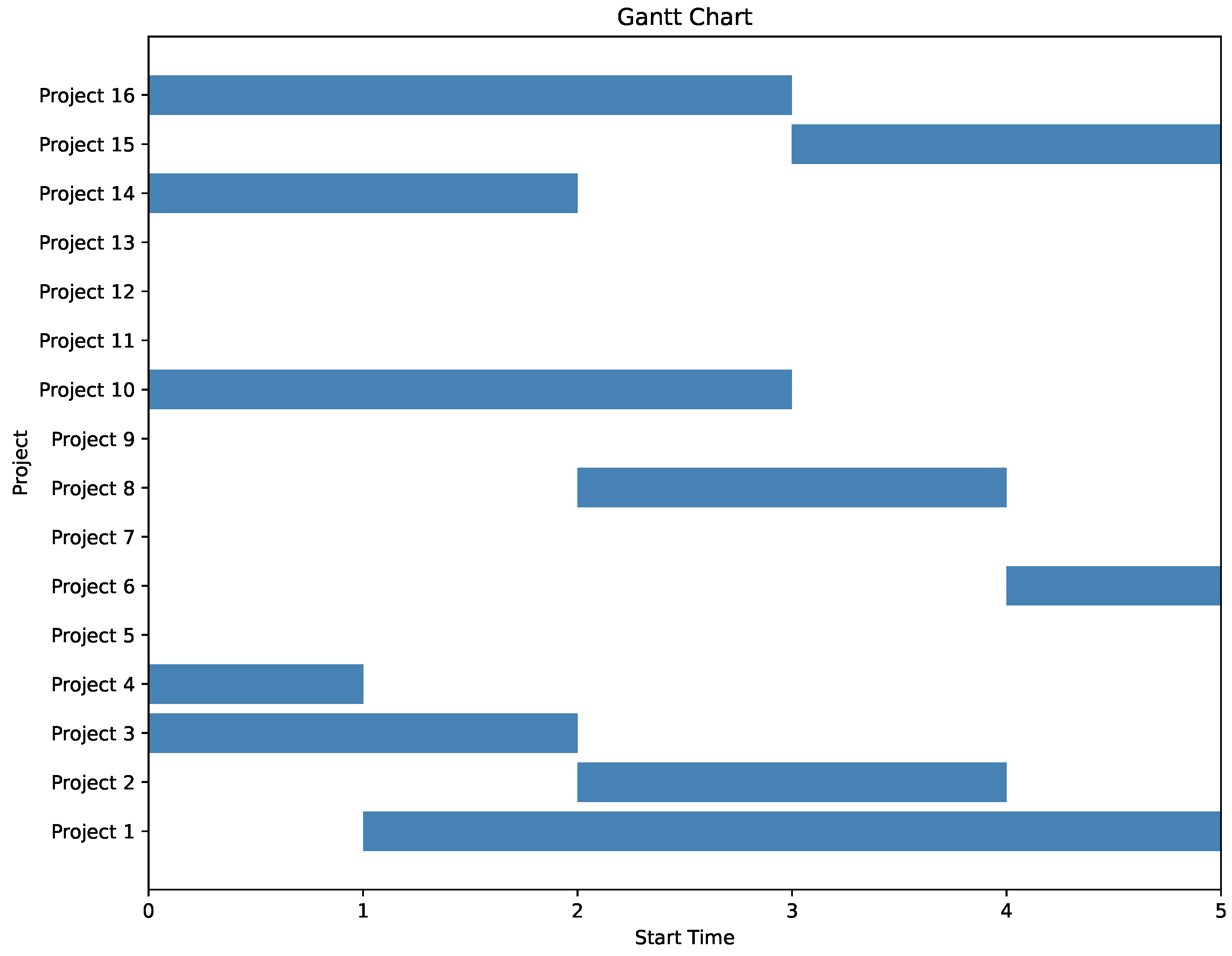

Based on the solved set of non-dominated solutions, the proposed method was used to select the non-dominated solutions to obtain the final solution result as [2, 3, 1, 1, 0, 5, 0, 3, 0, 1, 0, 0, 0, 1, 4, 1]. This solution implies that projects 3, 4, 10, 14, and 16 are scheduled to start in phase 1; project 1 in phase 2; projects 2 and 3 in phase 3; project 15 in phase 4; and project 6 in phase 5. The total benefit of the result is USD 916 million, and the expected implementation risk amounts to USD 142.5 million. The cost associated with this solution was also close to the upper limit of the cost constraints. In addition, the contents of Table A4 can be compared with those of project selection, with the interaction between projects mostly resulting in positive revenue. A Gantt chart of the project portfolio result is shown in Figure 10.

Figure 10.

Gantt chart of result.

6. Conclusions and Future Work

This paper introduces a new project portfolio selection model that accounts for interactions between multi-stage projects and incorporates these into the objective function. Based on the principle that genes appearing more frequently in the solution set are considered of higher quality, we developed a refined project selection method using TOPSIS. The method’s feasibility was demonstrated through case studies. This research integrates three key aspects: the multi-stage project lifecycle, project interactions, and refined selection, offering a project selection method under multiple optimization objectives. A novel heuristic algorithm was designed to solve the problem, providing a decision-making process from initial project screening to refined selection, serving as a reference for decision-makers in selecting appropriate projects.

Despite its contributions, this method has several limitations that we aim to address in future work.

First, the method does not account for uncertainty. In practical scenarios, decision attributes are often difficult to obtain or unclear, which this research does not fully address. Future work will explore incorporating uncertainty theory to better address these challenges. Second, the risk assessment approach used in this study is simplified. The sources and dynamics of risk are complex, and this paper does not consider external risks. Although there is significant research on project portfolio risk, we plan to extend our work within the current theoretical framework to address this complexity more effectively. Lastly, many new methods for solving combinatorial optimization problems have emerged, with deep reinforcement learning gaining popularity as a solution strategy. In future research, we aim to apply this approach to enhance the efficiency of our method. We will also continue to refine the model and validate its feasibility and effectiveness with real-world data.

Author Contributions

Conceptualization, B.Q.; methodology, B.Q.; software, B.Q.; validation, B.Q., Y.D. and Z.C.; formal analysis, B.Q. and Z.C.; investigation, B.Q. and Y.D.; resources, B.Q.; data curation, B.Q. and Z.C.; writing—original draft preparation, B.Q. and Y.D.; writing—review and editing, B.Q., Y.D. and Z.C.; visualization, B.Q.; supervision, Y.D. and Z.C.; project administration, Y.D. and Z.C.; funding acquisition, Y.D. and Z.C. All authors read and agreed to the published version of the manuscript.

Funding

This research was funded by the National Natural Science Foundation of China (NSFCunder Grants 72231011 and 72471239; the Youth Independent Innovation Science Fund Project, National University of Defense Technology, under Grant ZK24-28.

Institutional Review Board Statement

This article does not involve ethical research and does not require ethical approval.

Informed Consent Statement

Informed consent was obtained from all subjects involved in the study.

Data Availability Statement

The data required in the article are attached in Appendixes Appendix A and Appendix B.

Acknowledgments

We thank the Editor and the reviewers for their valuable comments and detailed suggestions that undoubtedly helped improve the paper. Furthermore, we acknowledge the partial support from the National Science Foundation of China under Grants 72231011 and 72471239, and the Youth Independent Innovation Science Fund Project, National University of Defense Technology, under Grant NO. ZK24-28.

Conflicts of Interest

The authors declare no conflicts of interest.

Appendix A. Basic Project Data

Table A1.

Criteria for project proposals—1.

Table A2.

Criteria for project proposals—2.

Table A3.

Criteria for project proposals—3.

Table A4.

Synergistic effects.

Appendix B. The Results of Project Selection in Different Periods

Figure A1.

The selection results of projects in the period where .

Figure A2.

The selection results of projects in the period where .

Figure A3.

The selection results of projects in the period where .

Figure A4.

The selection results of projects in the period where .

Figure A5.

The selection results of projects in the period where .

References

- Korotkov, V.; Wu, D. Evaluating the quality of solutions in project portfolio selection. Omega 2020, 91, 102029. [Google Scholar] [CrossRef]

- Kyle, R.H.; Ruhul, A.S. Evolutionary and Memetic Computing for Project Portfolio Selection and Scheduling; Springer International Publishing: Cham, Switzerland, 2022. [Google Scholar]

- Artūras, P.; Kristina, Č.; Aldona, J.; Pavlo, M.; Olegas, P. Algorithm for the assessment of heavyweight and oversize cargo transportation routes. J. Bus. Econ. Manag. 2017, 18, 1098–1114. [Google Scholar]

- Khorshidian, H.; Akbarpour, S.M.; Fatemi, G. An intelligent truck scheduling and transportation planning optimization model for product portfolio in a cross-dock. J. Intell. Manuf. 2019, 30, 163–184. [Google Scholar] [CrossRef]

- Tao, Y.; Luo, X.; Wu, Y.; Zhang, L.; Liu, Y.; Xu, C. Portfolio selection of power generation projects considering the synergy of project and uncertainty of decision information. Comput. Ind. Eng. 2023, 175, 108896. [Google Scholar] [CrossRef]

- Mohagheghi, V.; Mousavi, S.M.; Vahdani, B. A new multi-objective optimization approach for sustainable project portfolio selection: A real world application under interval-valued fuzzy environment. Iran. J. Fuzzy Syst. 2016, 13, 41–68. [Google Scholar]

- Abbasi, D.; Ashrafi, M.; Ghodsypour, S.H. A multi objective-BSC model for new product development project portfolio selection. Expert Syst. Appl. 2020, 162, 113757. [Google Scholar] [CrossRef]

- Fabián, D.; Franco, Q.; Óscar, C.V. The knapsack problem with scheduled items. Electron. Notes Discret. Math. 2018, 69, 293–300. [Google Scholar]

- Heidenberger, K.; Stummer, C. Research and development project selection and resource allocation: A review of quantitative modelling approaches. Int. J. Manag. Rev. 1999, 1, 197–224. [Google Scholar] [CrossRef]

- Khadija, B.; Laila, K. Project portfolio selection: Multi-criteria analysis and interactions between projects. Int. J. Comput. Sci. Issues 2014, 11, 134–143. [Google Scholar]

- Bai, L.; Zheng, K.; Wang, Z.; Liu, J. Service provider portfolio selection for project management using a BP neural net- work. Ann. Oper. Res. 2022, 308, 41–62. [Google Scholar] [CrossRef]

- David, S. Continuous-time formulations for multi-mode project scheduling. Comput. Oper. Res. 2023, 152, 106147. [Google Scholar]

- Ding, H.; Zhuang, C.; Liu, J. Extensions of the resource- constrained project scheduling problem. Autom. Constr. 2023, 153, 104958. [Google Scholar] [CrossRef]

- Song, S.; Yang, F.; Xia, Q. Multi-criteria project portfolio selection and scheduling problem based on acceptability analysis. Comput. Ind. Eng. 2019, 135, 793–799. [Google Scholar] [CrossRef]

- Wang, C.; Chen, W. A fuzzy model for R&D project portfolio selection. In Proceedings of the 2011 International Conference on Information Management, Innovation Management, and Industrial Engineering, Shenzhen, China, 26–27 November 2011; Volume 1, pp. 100–104. [Google Scholar]

- Tavana, M.; Khanjani, S.; Di, C. A chance-constrained portfolio selection model with random-rough variables. Neural Comput. Appl. 2019, 31, 931–945. [Google Scholar] [CrossRef]

- Carlsson, C.; Fuller, R.; Heikkilä, M.; Majlender, P. A fuzzy approach to R&D project portfolio selection. Int. J. Approx. Reason. 2007, 44, 93–105. [Google Scholar]

- Teller, J. Portfolio risk management and its contribution to project portfolio success: An investigation of organization, process, and culture. Proj. Manag. J. 2013, 44, 36–51. [Google Scholar] [CrossRef]

- Saeed, M.A.; Tabassum, H.; Zahid, M.M.; Jiao, Y.; Nauman, S. Organizational flexibility and project portfolio performance: The roles of environmental uncertainty and innovation capability. Eng. Manag. J. 2022, 34, 249–264. [Google Scholar] [CrossRef]

- Souza, D.G.B.; Silva, C.E.S.; Soma, N.Y. Selecting Projects on the Brazilian R&D Energy Sector: A Fuzzy-Based Approach for Criteria Selection. IEEE Access 2020, 8, 50209–50225. [Google Scholar]

- Archer, N.; Ghasemzadeh, F. Project portfolio selection and management. In The Wiley Guide to Project, Program & Portfolio Management; Morris, P., Pinto, J.K., Eds.; John Wiley & Sons: Hoboken, NJ, USA, 2007; pp. 94–112. [Google Scholar]

- Chao, R.O.; Kavadias, S. R&D intensity and the new product development portfolio. IEEE Trans. Eng. Manag. 2013, 60, 664–675. [Google Scholar]

- Mogbojuri, A.O.; Olanrewaju, O.A. Goal programming and genetic algorithm in multiple objective optimization model for project portfolio selection: A review. Niger. J. Technol. 2022, 41, 862–869. [Google Scholar] [CrossRef]

- Chen, R.; Liang, C.; Gu, D. IT project portfolio scheduling and multi-skilled staff assignment with ant colony optimization algorithm. Unpublished work. 2016. [Google Scholar]

- Mercangoz, B.A. Particle swarm algorithm: An application on portfolio optimization. In Metaheuristic Approaches to Portfolio Optimization; IGI Global: Hershey, PA, USA, 2019; pp. 27–59. [Google Scholar]

- Nielsen, M.K.J.; Jacobsen, A.M.S.Ø.; Carstensen, J.L.; Toft Nielsen, M.; Tambo, T. Industrial R&D project portfolio selection method using a multi-objective optimization program: A conceptual quantitative framework. J. Ind. Eng. Manag. 2024, 17, 217–234. [Google Scholar]

- Alinezhad, R.; Ansari, R.; Mahdikhani, M.; Banihashemi, S.A. Multi-phase projects selection and scheduling problem: A multi-objective optimization approach. Iran. J. Sci. Technol. Trans. Civ. Eng. 2022, 46, 2575–2591. [Google Scholar] [CrossRef]

- Ghanbari, M.; Jaber Olaikhan, A.A.; Skitmore, M. Enhancing project portfolio selection for construction holding firms: A multi-objective optimization framework with risk analysis. Eng. Constr. Archit. Manag. 2024. ahead of print. [Google Scholar] [CrossRef]

- Chen, H.; Li, X.; Lu, X.; Sheng, N.; Zhou, W.; Geng, H.; Yu, S. A multi-objective optimization approach for the selection of overseas oil projects. Comput. Ind. Eng. 2021, 151, 106977. [Google Scholar] [CrossRef]

- Beşikci, U.; Bilge, Ü.; Ulusoy, G. Multi-mode resource constrained multi-project scheduling and resource portfolio problem. Eur. J. Oper. Res. 2015, 240, 22–31. [Google Scholar] [CrossRef]

- Laslo, Z. Project portfolio management: An integrated method for resource planning and scheduling to minimize planning/scheduling-dependent expenses. Int. J. Proj. Manag. 2010, 28, 609–618. [Google Scholar] [CrossRef]

- Pérez, F.; Gómez, T.; Caballero, R.; Liern, V. Project portfolio selection and planning with fuzzy constraints. Technol. Forecast. Soc. Chang. 2018, 131, 117–129. [Google Scholar] [CrossRef]

- RezaHoseini, A.; Ghannadpour, S.F.; Hemmati, M. A comprehensive mathematical model for resource-constrained multi-objective project portfolio selection and scheduling considering sustainability and projects splitting. J. Clean. Prod. 2020, 269, 122073. [Google Scholar] [CrossRef]

- Trappey, C.V.; Trappey, A.J.C.; Chiang, T.A.; Kuo, J.Y. A strategic product portfolio management methodology considering R&D resource constraints for engineering-to-order industries. Int. J. Technol. Manag. 2009, 48, 258–276. [Google Scholar]

- Bai, L.; Zhang, K.; Shi, H.; An, M.; Han, X. Project portfolio resource risk assessment considering project interdependency by the fuzzy Bayesian network. Complexity 2020, 2020, 5410978. [Google Scholar] [CrossRef]

- Moon, Y.; Yao, T. A robust mean absolute deviation model for portfolio optimization. Comput. Oper. Res. 2011, 38, 1251–1258. [Google Scholar] [CrossRef]

- Smith-Perera, A.; García-Melón, M.; Poveda-Bautista, R.; Pastor-Ferrando, J.-P. A Project Strategic Index proposal for portfolio selection in electrical company based on the Analytic Network Process. Renew. Sustain. Energy Rev. 2010, 14, 1569–1579. [Google Scholar] [CrossRef]

- Long, L.D.; Ohsato, A. Fuzzy critical-chain method for project scheduling under resource constraints and uncertainty. Int. J. Proj. Manag. 2008, 26, 688–698. [Google Scholar] [CrossRef]

- Ghomi, S.M.T.F.; Ashjari, B. A simulation model for multi-project resource allocation. Int. J. Proj. Manag. 2002, 20, 127–130. [Google Scholar] [CrossRef]

- Baker, N.; Freeland, J. Recent advances in R&D benefit measurement and project selection methods. Manag. Sci. 1975, 21, 1164–1175. [Google Scholar]

- Pendharkar, P.C.; Rodger, J.A. Information technology capital budgeting using a knapsack problem. Int. Trans. Oper. Res. 2010, 13, 333–351. [Google Scholar] [CrossRef]

- Killen, C.P. Evaluation of project interdependency visualizations through decision scenario experimentation. Int. J. Proj. Manag. 2013, 31, 804–816. [Google Scholar] [CrossRef]

- Lopes, Y.G.; Almeida, A.T.D. Assessment of synergies for selecting a project portfolio in the petroleum industry based on a multi-attribute utility function. J. Pet. Sci. Eng. 2015, 126, 131–140. [Google Scholar] [CrossRef]

- Eilat, H.; Golany, B.; Shtub, A. Constructing and evaluating balanced portfolios of R&D projects with interactions: A DEA based methodology. Eur. J. Oper. Res. 2006, 172, 1018–1039. [Google Scholar]

- Zorluoğlu, Ö.Ş.; Kabak, Ö. An interactive multi-objective programming approach for project portfolio selection and scheduling. Comput. Ind. Eng. 2022, 169, 108191. [Google Scholar] [CrossRef]

- Liesiö, J.; Kee, T.; Malo, P. Modeling project interactions in multiattribute portfolio decision analysis: Axiomatic foundations and practical implications. Eur. J. Oper. Res. 2024, 316, 988–1000. [Google Scholar] [CrossRef]

- Wei, H.; Niu, C.; Xia, B.; Dou, Y.; Hu, X. A refined selection method for project portfolio optimization considering project interactions. Expert Syst. Appl. 2020, 142, 112952. [Google Scholar] [CrossRef]

- Wang, L.; Qian, C.; Goh, M. Integrated Approach for Project Risk Assessment and Evaluation under Risk Interactions. IEEE Trans. Eng. Manag. 2022, 71, 2418–2429. [Google Scholar] [CrossRef]

- Su, G.; Hastak, M.; Deng, X.; Khallaf, R. Risk Sharing Strategies for IPD Projects: Interactional Analysis of Participants’ Decision-Making. J. Manag. Eng. 2021, 37, 04020101. [Google Scholar] [CrossRef]

- Amir, F.F.; Hosein, D.; Kaveh, K.D.; Amir, H.S.; Mehdi, H. A framework for interactive risk assessment in projects: Case study of oil and gas megaprojects in presence of sanctions. J. Model. Manag. 2022, 17, 569–600. [Google Scholar]

- Zhao, J.; Guo, P.; Pan, N. Optimisation of Project Portfolio Risk Measurement and Selection Based on Interaction Effects. Oper. Res. Manag. 2011, 20, 120–126. [Google Scholar]

- Wang, J.; Guo, P.; Zhao, J. R&D Project Portfolio Robustness Risk Measurement and Selection Model. Oper. Res. Manag. 2017, 26, 140–148. [Google Scholar]

- Pinheiro, P.R.; Amaro, J.B.; Saraiva, R.D. A random-key genetic algorithm for solving the nesting problem. Int. J. Comput. Integr. Manuf. 2016, 29, 1159–1165. [Google Scholar] [CrossRef]

- Igor, M.; Gabriel, S.; Glaydston, M.R.; Israel, M.; Pedro, H.G. A Hybrid BRKGA Approach for the Multiproduct Two Stage Capacitated Facility Location Problem. In Proceedings of the 2022 IEEE Congress on Evolutionary Computation (CEC), Padua, Italy, 18–23 July 2022. [Google Scholar]

- Mojtaba, G.; Mohsen, Z.; Pavel, T.; Amir, Z.; Eva, T. A hybridizing-enhanced differential evolution for optimization. PeerJ Comput. Sci. 2023, 9, e1420. [Google Scholar]

- Pelc, K.I. Research and development project selection. R D Manag. 1998, 28, 53–54. [Google Scholar]

- Thiele, B.; Ryan, M.; Abbasi, A. Developing a dataset of real projects for portfolio, program and project control management research. Data Brief 2020, 34, 106659. [Google Scholar] [CrossRef] [PubMed]

- Harrison, K.R.; Elsayed, S.M.; Garanovich, I.L.; Weir, T.; Boswell, S.G.; Sarker, R.A. Generating datasets for the project portfolio selection and scheduling problem. Data Brief 2022, 42, 108208. [Google Scholar] [CrossRef] [PubMed]

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).