Factors Influencing Investment Decisions in Financial Investment Companies

,

,  and

and

Abstract

1. Introduction

- Strategic planning: Determine which projects should be undertaken and share your findings with the industry.

- Investment design: Analyze context and alternatives and implement detailed project design.

- Implementation and monitoring: Carry out the assignment, track and report your progress toward your objectives, and adjust as needed.

- Evaluation and benefit: Assess past initiatives’ successes and failures in order to better shape future endeavors.

2. Conceptual Framework of Study

- The independent variable: is the factors affecting the investment decision (Nature of information, Disclosure, Perception, Internal factors, External factors, Information Technology).

- The dependent variable: is the appropriate investment decision.

3. Hypothesis of the Study

3.1. Examine the Correlation between the Researched Factors

3.1.1. Main Hypothesis 1

3.1.2. Sub Hypotheses of Correlation

- The quality of information significantly correlates with selecting the best investment option.

- Disclosing relevant information is highly correlated with making a good financial investment.

- The correct investment decision is strongly correlated with how things are perceived.

- Internal considerations are strongly correlated with making the right investment choice.

- There is a strong link between considering relevant outside issues and making the best possible financial investment.

- Information technology has a strong link to choosing the right investment.

3.2. Test the Effect between the Variables Studied

3.2.1. Main Hypothesis 2, “the Factors Impacting the Right Investment Decision-Making Have a Considerable Influence Link.”

3.2.2. Sub-Hypotheses of Effect

- The type of the proactive information plays a crucial role in determining the best investing strategy.

- The disclosure dimension has a substantial effect on the variable that measures how well one decides to invest.

- An important impact link exists between the perception dimension and the variable representing sound financial planning and investment choices.

- The optimal investment decision is a variable whose impact increases with the size of the internal elements involved.

- The proper investment decision-making variable is heavily influenced by the external factors dimension.

- The IT dimension has a considerable effect on the appropriate investment decision-making variable.

3.3. Test Main Hypothesis 3 of the Sequential or Sequential Regression

4. Research Sample Characteristics

- The age group (35–less than 40) years topped the ranking of the distribution of age groups, as it constituted slightly more than a third of the sample, with a rate of (36.9%), followed by the age group (30–less than 35) years, with a representation similar to the previous one, amounting to 32.3%, then the age group (40–less than 45 years) ranked third with a representation rate of 13.1% of the total research sample, and the age group (25–less than 30 years) ranked fourth with a representation rate of 9.2%. As for the remaining percentage (8.5%), it represented the sample whose age was 45 years and over, and these results reflect the diversity in the ages of the sample and the presence of a great youthful character in it.

- With regard to academic qualification, the results of Table 1 showed that slightly more than half of the respondents, at a rate of 50.8%, hold a bachelor’s degree, and nearly a quarter of the respondents (23.1%) hold a master’s degree, and the percentage was 21.5%. They hold a doctorate degree, while the remaining percentage (4.6%) of the total sample holds a higher diploma. It is noted from the results that holders of a bachelor’s degree emerged from those sample members, as well as a diversity in the educational attainment of the respondents, especially holders of higher degrees.

- When inquiring from the research sample about their scientific specialization, based on Table 1, it can be seen that nearly a third of the sample (28.5%) of the respondents specialize in accounting, 21.5% of the respondents specialize in various other specializations, 20% of the respondents specialize in business administration, and 19.2% of those respondents specialize in banking and financial sciences, while the remaining 10.8% of the respondents specialize in statistics. These results indicate a diversity in the specialization of the sample, with some leadership in the financial and accounting disciplines.

- With regard to the work of the respondents in the researched sample, as shown in Table 1, nearly a third of the respondents (32.3%) are investors, and 26.1% of the respondents work in various other jobs, and (24.6%) of those surveyed work. Their views were as certified public accountants, financial managers accounted for (10.8%) of the total research sample, while the remaining small percentage of the respondents (6.2%) represented those who work as financial analysts.

- By inquiring about the years of work experience among the respondents, as stated in Table 1, nearly a third of the respondents (29.2%) have work experience ranging from 1 to less than 5 years; 24.6% of the respondents have work experience ranges between 10 and less than 15 years; 22.3% of the respondents have work experience ranging from 5–less than 10 years; and 14.6% of the respondents have work experience estimated as 20 years or more, while the remaining percentage, amounting to 9.3%, represented the respondents who have work experience ranging between 15 and less than 20 years. These results reflect closeness or great compatibility with what was stated in the analysis of the ages of the sample in terms of the presence of a group of youthful participants trying to gain experience, as well as the elderly and experienced who give young people an opportunity to learn and gain more of those experiences at work.

5. Analysis of Research Community Data

5.1. Methodology

- Personal interviews: Although there are a variety of interview forms (such as structured, semi-structured, and open), analysts agree that they all share a common framework and differ mostly in the degree to which they adhere to that pattern. Moreover, there are a variety of interviewing techniques (e.g., active, neutral, formal, informal, controlled, and free) from which to choose. It is also possible for interviews to vary in formality (i.e., formal vs. casual) [23,24,25,26,27].

- B.

- Questionnaire: The questionnaire will be used extensively as it will serve as the primary method for gathering the data and information needed for the study. The study literature was used to inform the structure of its paragraphs. It was modified to fit the needs of the study. It had two major axes, which included Experience, and the second axis highlighted the primary study variables and the dimensions of those variables, which are:

- The first: the factors influencing appropriate investment decision-making, which included six dimensions (Information Nature, Disclosure, Perception, Internal Factors, External Factors, Information Technology). A different number of questions were put for each dimension, and the total number of questions was 51.

- The second: on “making the right investment choice”, included six questions, for a total of fifty-seven; all questions used the same five-point Likert scale (very much, somewhat, somewhat, not at all, or none) and weights (1, 2, 3, 4, 5) to ensure comparability.

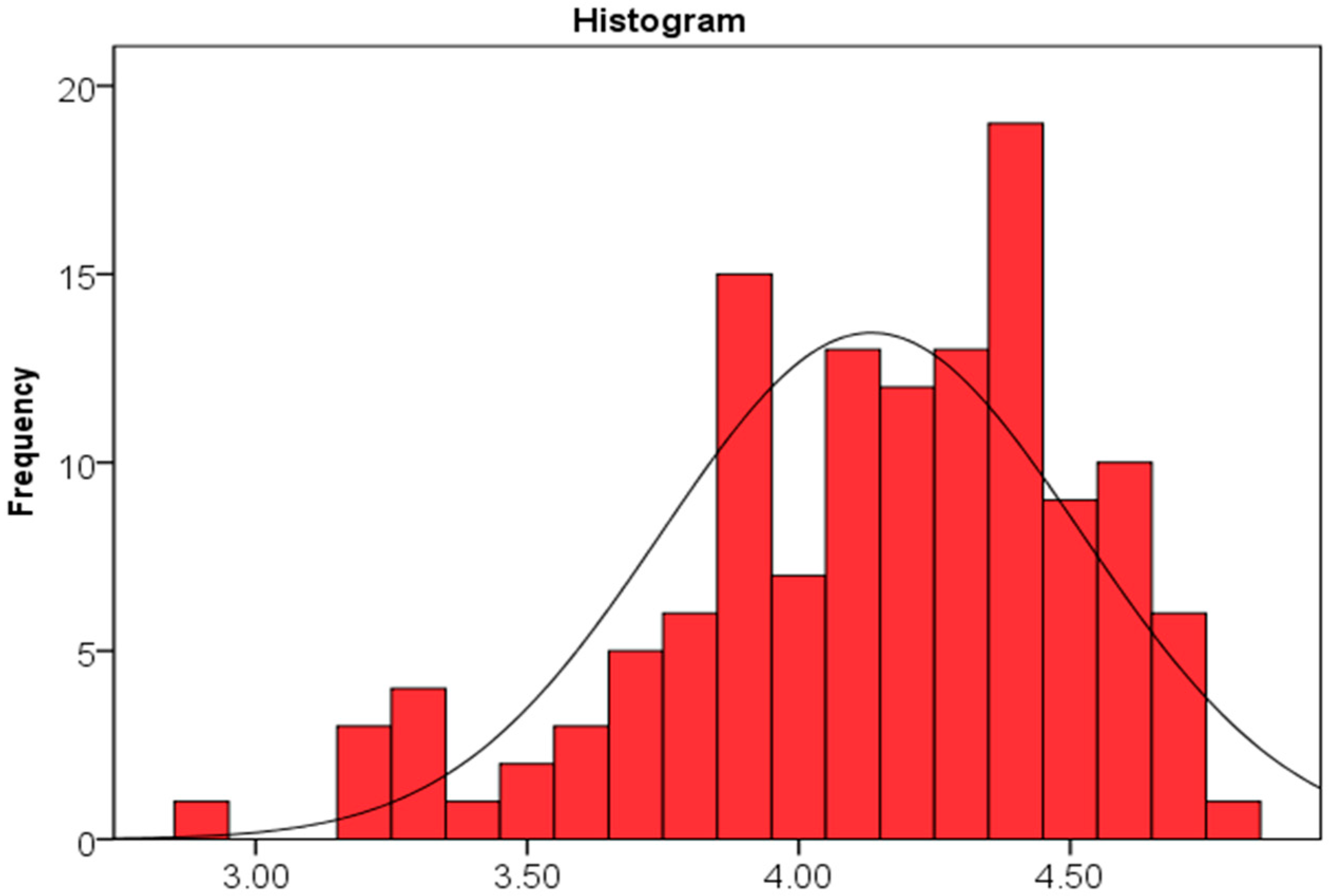

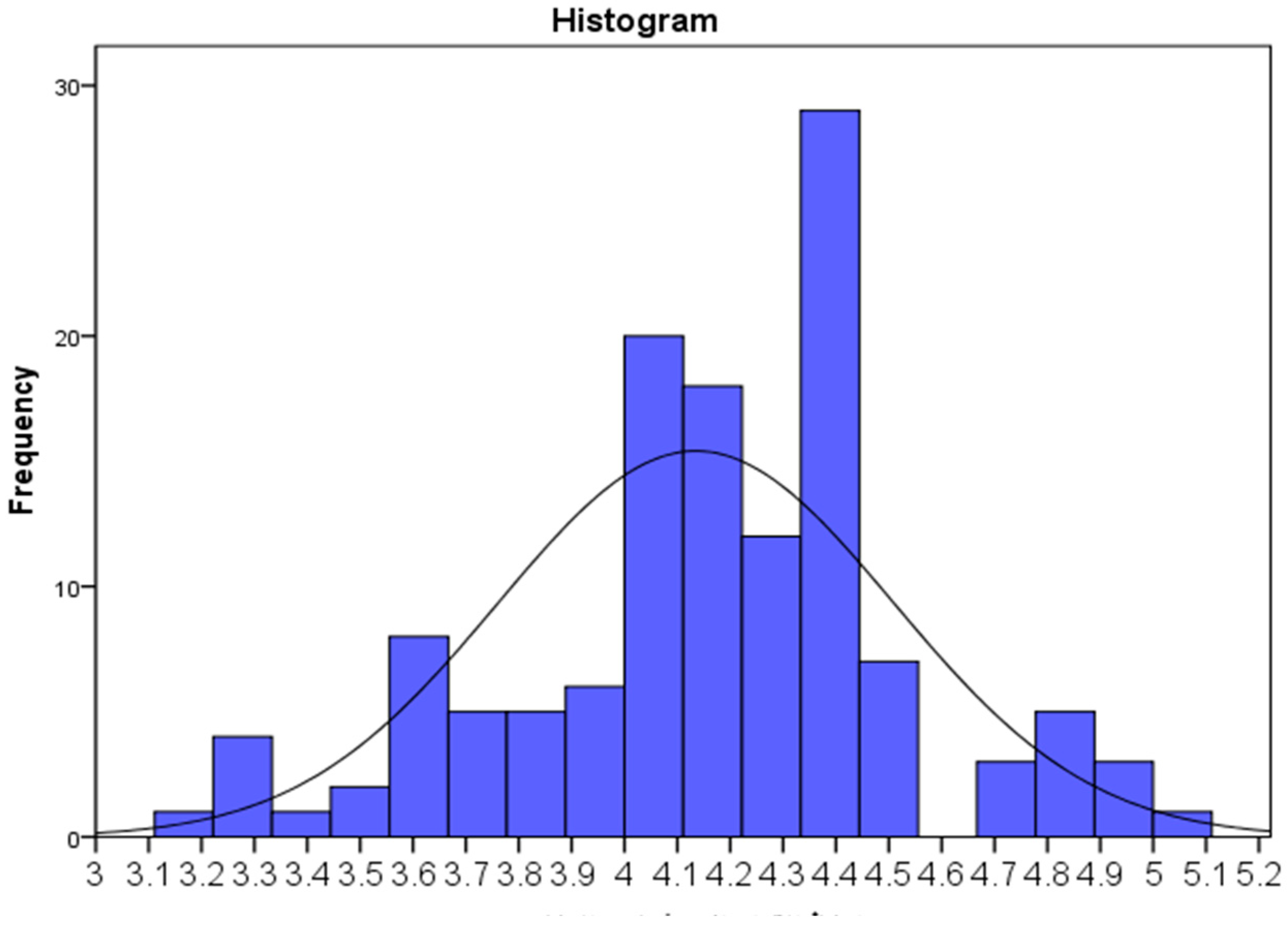

5.2. Test of Normal Distribution of Study Measures

5.2.1. Testing the Normal Distribution of the Factors Affecting Appropriate Investment Decision-Making

- The null hypothesis: the data on the axis of the factors influencing the appropriate investment decision-making are distributed normally.

- Alternative hypothesis: The data of the factors influencing the appropriate investment decision-making are not distributed normally.

5.2.2. The Normal Distribution Test for Making the Appropriate Investment Decision

- The null hypothesis: The data on the axis of making the appropriate investment decision are distributed normally.

- The alternative hypothesis: The data on the axis of making the appropriate investment decision are not distributed normally.

6. Poly-Linearity Problem Test

6.1. Validity and Reliability

6.1.1. Testing the Questionnaire Content Validity

6.1.2. Stability of the Questionnaire Content

- The half-partition method: The (61) items of the questionnaire were divided into two homogeneous equal halves, and for all the (130) questionnaires, the first half included the individual items, while the second half included the even items, with the exception of the middle paragraph. By calculating the correlation coefficient (Pearson) between the value of the two halves as 801.0 and using the corrective (Spearman–Brown) equation, the value of the stability coefficient according to the split-half method was (86.0) for the first half and (81.0) for the second half, which are very good stability values that call for the adoption of the research results and their generalization in future studies.

- Test and re-test method: This method depends on the consistency of the answers of the same respondent from one paragraph to another, as it used an intentional sample of the respondents amounting to 38 respondents who polled their opinions on the subject of the research, and the questionnaire was returned to them after a period of three weeks. Then the alpha-Cronbach coefficient was calculated for each axis of the questionnaire axes and the general stability coefficient for all the paragraphs of the questionnaire, and the test results showed that the value of the stability coefficient (alpha-Cronbach) reached 88.0, which is a good percentage that confirms the adoption of these results in this research and subsequent future studies, and Table 5 illustrates the value of stability coefficient for the research questionnaire.

7. Description and Analysis of the Response of the Research Sample

7.1. Describing Participant Reaction to the Scales of Factors Which Should Be Considered When Making a Sound Investment Choice

7.2. Describe the Response of the Research Sample to the Appropriate Investment Decision-Making Variable

8. Research Hypothesis Testing

8.1. Correlation Test:

8.1.1. Main Hypothesis 1: “There Is a Significant Correlation among the Factors Influencing and the Decision-Making of the Appropriate Investment.”

8.1.2. Testing Sub-Hypotheses of Correlation

- Sub-hypothesis 1: According to this theory, “the nature of the knowledge is significantly correlated with making the optimal investment decision”.

- Sub-hypothesis 2: The “significant correlation between disclosure and making the appropriate investment decision” hypothesis states that this relationship exists.

- Sub-hypothesis 3: which asserts, “There is a strong link between how things appear and making the right financial choice”.

- Sub-hypothesis 4: Internal aspects are highly correlated with making the right investment decision, as stated by this hypothesis.

- Sub-hypothesis 5: which asserts that “there is a considerable association between external factors and making the optimal investment decision”.

- Sub-hypothesis 6: which claims, “There is a strong link between IT and picking the right investment”.

8.2. Effect Test

8.2.1. Testing Main Hypothesis 2 of the Effect Relationship

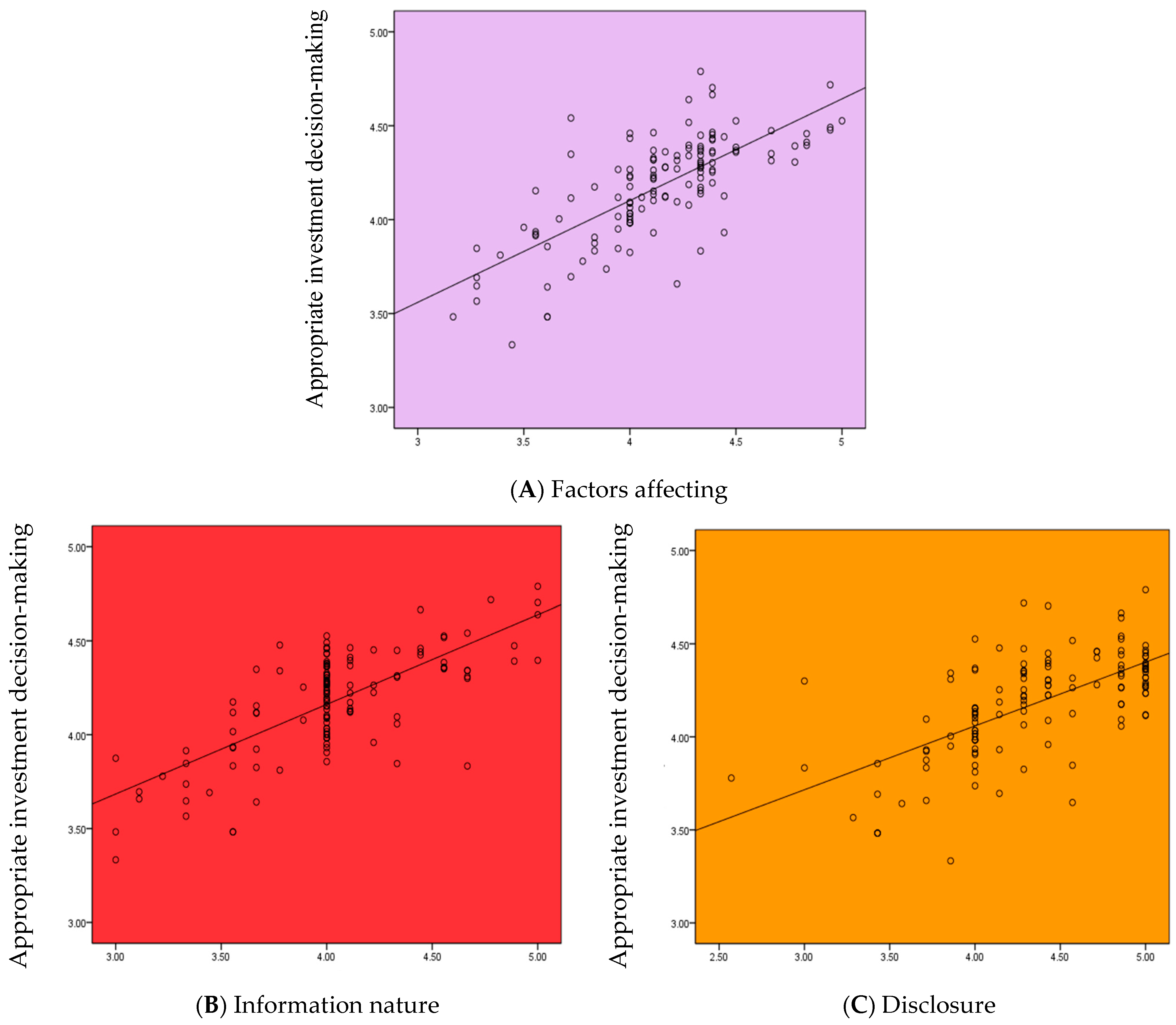

Making the Appropriate Investment Decision = 1.93 + (0.73) Factors Affecting Making the Appropriate Investment Decision

8.2.2. Testing the Effect Sub-Hypotheses

- Sub-hypothesis 1 states that “there is a significant effect relationship of the nature of the proactive in-formation in making the appropriate investment decision”.

Making the Appropriate Investment Decision = 2.25 + (0.62) Information Nature

- II.

- Sub-hypothesis 2 states that “there is a significant effect relationship of the disclosure dimension on the appropriate investment decision-making variable”.

Making the Appropriate Investment Decision = 2.08 + (0.64) Disclosure

- III.

- Sub-hypothesis 3 states that “there is a significant impact relationship of the perception dimension on the appropriate investment decision-making variable”.

Making the Appropriate Investment Decision = (2.11) + (0.69) Perception

- IV.

- Sub-hypothesis 4 states that “there is a significant impact relationship of the dimension of internal factors in the variable of making the appropriate investment decision”.

Making the Appropriate Investment Decision = 3.18 + (0.40) Internal Factors

- V.

- Sub-hypothesis 5 states that “there is a significant influence relationship for the dimension of External Factors in the appropriate investment decision-making variable”.

Making the Appropriate Investment Decision = 2.69 + (0.61) External Factors

- VI.

- Sub-hypothesis 6 states that “there is a significant impact relationship of the information technology dimension on the appropriate investment decision-making variable”.

Making the Right Investment Decision = 3.09 + (0.43) Information Technology

8.3. Regression Test

Making the Appropriate Investment Decision = 0.15 + (0.34) Information Nature + (0.32) Disclosure + (0.35) External Factors + (0.25) Information Technology + (0.30) Perception

9. Conclusions and Future Work

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A

- General budget.

- Profit and loss statement.

- Cash flow statement.

References

- Locurcio, M.; Tajani, F.; Morano, P.; Anelli, D.; Manganelli, B. Credit Risk Management of Property Investments through Multi-Criteria Indicators. Risks 2021, 9, 106. [Google Scholar] [CrossRef]

- Jain, J.; Walia, N.; Gupta, S. Evaluation of behavioral biases affecting investment decision making of individual equity investors by fuzzy analytic hierarchy process. Rev. Behav. Financ. 2020, 12, 297–314. [Google Scholar] [CrossRef]

- Niyozovna, N.I.; Azimov, O.O. The role of investment and modernization in the development of the uzbek economy. Res. J. Anal. Invent. 2021, 2, 140–145. [Google Scholar]

- Naqvi, M.H.A.; Jiang, Y.; Miao, M.; Naqvi, M.H. Linking biopsychosocial indicators with financial risk tolerance and satisfaction through macroeconomic literacy: A structural equation modeling approach. Cogent Econ. Financ. 2020, 8, 1730079. [Google Scholar] [CrossRef]

- Gill, S.; Khurshid, M.K.; Mahmood, S.; Ali, A. Factors effecting investment decision making behavior: The mediating role of information searches. Eur. Online J. Nat. Soc. Sci. 2018, 7, 758. [Google Scholar]

- Gardi, B.; Abdalla Hamza, P.; Sabir, B.Y.; Mahmood Aziz, H.; Sorguli, S.; Abdullah, N.N.; Al-Kake, F. Investigating the effects of financial accounting reports on managerial decision making in small and medium-sized enterprises. Turk. J. Comput. Math. Educ. (TURCOMAT) 2021, 12, 2134–2142. [Google Scholar] [CrossRef]

- Cohn, R.A.; Lewellen, W.G.; Lease, R.C.; Schlarbaum, G.G. Individual Investor Risk Aversion and Investment Portfolio Composition. J. Financ. 1975, 30, 605–620. [Google Scholar] [CrossRef]

- Riley, W.B., Jr.; Chow, K.V. Asset allocation and individual risk aversion. Financ. Anal. J. 1992, 48, 32–37. [Google Scholar] [CrossRef]

- LeBaron, D.; Farrelly, G.; Gula, S. Facilitating a dialogue on risk: A questionnaire approach. Financ. Anal. J. 1989, 45, 19–24. [Google Scholar] [CrossRef]

- Baker, H.K.; Haslem, J.A. Information needs of individual investors. J. Account. 1973, 136, 64–69. [Google Scholar]

- Baker, H.K.; Hargrove, M.B.; Haslem, J.A. An empirical analysis of the risk-return preferences of individual investors. J. Financ. Quant. Anal. 1977, 12, 377–389. [Google Scholar] [CrossRef]

- Nagy, R.A.; Obenberger, R.W. Factors influencing individual investor behavior. Financ. Anal. J. 1994, 50, 63–68. [Google Scholar] [CrossRef]

- Merilkas, A.; Prasad, D. Factors influencing Greek investor behavior on the Athens stock exchange. J. Bus. 2003, 66, 1–20. [Google Scholar]

- Bhagyasree, N.; Kishori, B. A study on performance evaluation of mutual funds schemes in India. Int. J. Innov. Res. Sci. Technol. 2016, 2, 812–816. [Google Scholar]

- Mutswenje, V.S. A Survey of the Factors Influencing Investment Decisions: The Case of Individual Investors at the NSE. Ph.D. Thesis, University of Nairobi, Nairobi, Kenya, 2009. [Google Scholar]

- Souza, T.T.; Aste, T. Predicting future stock market structure by combining social and financial network information. Phys. A Stat. Mech. Its Appl. 2019, 535, 122343. [Google Scholar] [CrossRef]

- Yeşildağ, E.; Atasever, M.; Kuduz, N.; Coşkun, A. Afyonkarahisar ve Kütahya illerindeki hisse senedi yatırımcılarının profili ve yatırım kararlarını etkileyen faktörlerin analizi [Afyonkarahisar and Kütahya illusions of stock investors’ analysis of the factors affecting the profile and investment decisions]. Akad. Sos. Araştırmalar Derg. 2017, 5, 257–277. [Google Scholar]

- Bernard, T. Cash Holdings and Corporate Investment: Evidence from COVID 19; Victoria University of Wellington: Wellington, New Zealand, 2020. [Google Scholar] [CrossRef]

- Khan, I.; Afeef, M.; Adil, M.; Ullah, W. Behavioral factors influencing investment decisions of institutional investors: Evidence from asset management industry in Pakistan. Ilkogr. Online 2021, 20, 603–614. [Google Scholar]

- Jones, T. Business Economics and Managerial Decision Making; John Wiley & Sons, Inc.: Hoboken, NJ, USA, 2022. [Google Scholar]

- Wang, X.; Lou, T. The effect of performance feedback on firms’ unplanned marketing investments. J. Bus. Res. 2020, 118, 441–451. [Google Scholar] [CrossRef]

- Mohseni, S.; Brent, A.C.; Kelly, S.; Browne, W.N. Demand response-integrated investment and operational planning of renewable and sustainable energy systems considering forecast uncertainties: A systematic review. Renew. Sustain. Energy Rev. 2022, 158, 112095. [Google Scholar] [CrossRef]

- Edwards, R.; Holland, J. What Is Qualitative Interviewing? Bloomsbury: London, UK, 2013. [Google Scholar]

- Stuckey, H.L. Three types of interviews: Qualitative research methods in social health. J. Soc. Health Diabetes 2013, 1, 56–59. [Google Scholar] [CrossRef]

- Gill, P.; Stewart, K.; Treasure, E.; Chadwick, B. Methods of data collection in qualitative research: Interviews and focus groups. Br. Dent. J. 2008, 204, 291–295. [Google Scholar] [CrossRef] [PubMed]

- Jamshed, S. Qualitative research method-interviewing and observation. J. Basic Clin. Pharm. 2014, 5, 87–88. [Google Scholar] [CrossRef] [PubMed]

- DiCicco-Bloom, B.; Crabtree, B.F. The qualitative research interview. Med. Educ. 2006, 40, 314–321. [Google Scholar] [CrossRef] [PubMed]

- Erjavec, J.; Popovič, A.; Trkman, P. The effect of personality traits and knowledge on the quality of decisions in supply chains. Econ. Res.-Ekon. Istraživanja 2019, 32, 2269–2292. [Google Scholar] [CrossRef]

- Miller, C.C.; Ireland, R.D. Intuition in strategic decision making: Friend of foe in the fast-paced 21st century. Acad. Manag. Exec. 2005, 19, 19–30. [Google Scholar]

- Pretz, J. Intuition versus analysis: Strategy and experience in complex everyday problem solving. Mem. Cogn. 2008, 36, 554–566. [Google Scholar] [CrossRef]

- Woiceshyn, J. Lessons from “Good Minds”: How CEOs Use Intuition, Analysis and Guiding Principles to Make Strategic Decisions. Long Range Plan. 2009, 42, 298–319. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| # | Details | Categories | Number | Percentage |

|---|---|---|---|---|

| 1 | Age | 25–less than 30 years old | 12 | 9.2 |

| 30–less than 35 years old | 42 | 32.3 | ||

| 35–less than 40 years old | 48 | 36.9 | ||

| 40–less than 45 years old | 17 | 13.1 | ||

| 45 years and over | 11 | 8.5 | ||

| Total | 130 | 100% | ||

| 2 | Qualification | secondary | 0 | 0 |

| BA | 66 | 50.8 | ||

| Higher Diploma | 6 | 4.6 | ||

| Master’s | 30 | 23.1 | ||

| PhD | 28 | 21.5 | ||

| Total | 130 | 100% | ||

| 3 | specialization | Accounting | 37 | 28.5 |

| Finance and Banking | 25 | 19.2 | ||

| Business Administration | 26 | 20.0 | ||

| Counting | 14 | 10.8 | ||

| other | 28 | 21.5 | ||

| Total | 130 | 100% | ||

| 4 | Position | Financial Manager | 14 | 10.8 |

| Financial Analyst | 8 | 6.2 | ||

| Accountant | 32 | 24.6 | ||

| Investor | 42 | 32.3 | ||

| other | 34 | 26.1 | ||

| Total | 130 | 100% | ||

| 5 | Experience | 1–less than 5 years old | 38 | 29.2 |

| 5–Less than 10 years old | 29 | 22.3 | ||

| 10–less than 15 years old | 32 | 24.6 | ||

| 15–less than 20 years old | 12 | 9.3 | ||

| 20 years and over | 19 | 14.6 | ||

| Total | 130 | 100% |

| Variable | Kolmogorov–Simonov Test | ||

|---|---|---|---|

| Morale Sig. | Sample Volume | Test Statistics | |

| Factors affecting making the right investment decision | 0.073 | 130 | 1.297 |

| Variable | Kolmogorov–Simonov Test | ||

|---|---|---|---|

| Morale Sig. | Sample Volume | Test Statistics | |

| Make the right investment decision | 0.068 | 130 | 1.282 |

| Variable | Poly-Linear Statistics | |

|---|---|---|

| Tolerance | VIF | |

| Information Nature | 0.567 | 1.763 |

| Disclosure | 0.806 | 1.240 |

| Perception | 0.564 | 1.774 |

| Internal factors | 0.491 | 2.036 |

| External factors | 0.809 | 1.236 |

| Information Technology | 0.911 | 1.098 |

| Questionnaire Variables | The Value of the Alpha-Cronbach Coefficient |

|---|---|

| Factors affecting making the appropriate investment decision | 0.91 |

| Taking the appropriate investment decision | 0.84 |

| Total | 0.88 |

| # | Response Nature or Interaction | Scale Range |

|---|---|---|

| 1 | High | 3.67–5 |

| 2 | Medium | 2.34–3.66 |

| 3 | low | 1–2.33 |

| # | Factors | Mean | S.D. | Weight Percent | Difference | Sort |

|---|---|---|---|---|---|---|

| 1 | Information Nature | 4.03 | 0.419 | 80.6 | 10.4 | 2 |

| 2 | Disclosure | 4.34 | 0.518 | 86.8 | 11.94 | 5 |

| 3 | Perception | 4.13 | 0.386 | 82.6 | 9.35 | 1 |

| 4 | Internal factors | 4.14 | 0.685 | 82.8 | 16.54 | 6 |

| 5 | External factors | 4.27 | 0.483 | 85.4 | 11.31 | 4 |

| 6 | Information Technology | 4.15 | 0.455 | 83 | 10.96 | 3 |

| Total | 4.13 | 0.341 |

| # | Paragraph | Answers | Mean | S.D. | Weight Percent | Difference | Sort | ||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| Very Much | Much | Moderately | Weak | Very Weak | |||||||

| 1 | Determining the main objective of the investment contributes to the success of the investment decision. | 67 | 55 | 7 | 1 | 0 | 4.45 | 0.636 | 89 | 14.29 | 1 |

| 2 | A successful investment decision depends on identifying the key factors in the investment decision. | 49 | 65 | 14 | 1 | 1 | 4.23 | 0.732 | 84.6 | 17.3 | 4 |

| 3 | Gathering appropriate information before making an investment decision contributes to making a rational investment decision. | 55 | 61 | 13 | 1 | 0 | 4.30 | 0.711 | 86 | 16.53 | 3 |

| 4 | Evaluating the expected returns of the available investment alternatives is a key factor in finding the best alternative. | 47 | 69 | 13 | 1 | 0 | 4.25 | 0.660 | 85 | 15.53 | 2 |

| 5 | I consider the financial reports issued by the companies in which I wish to invest, especially the dividend policy, sufficient to make the investment decision. | 48 | 65 | 11 | 5 | 1 | 4.18 | 0.805 | 83.6 | 19.26 | 5 |

| 6 | The investment strategy is based on achieving a balance between the elements of return and risk | 41 | 63 | 21 | 4 | 1 | 4.07 | 0.818 | 81.4 | 20.1 | 6 |

| Total | 4.25 | 0.604 | 85 | 14.21 | |||||||

| Y | X Dimensions of the Factors Influencing the Appropriate Investment Decision | Spearman Correlation Coefficient (r) | Calculated (T) Value | Significance |

|---|---|---|---|---|

| Take the appropriate investment decision | Information nature | ** 0.638 | 9.373 | √ |

| Disclosure | ** 0.640 | 9.423 | √ | |

| Perception | ** 0.698 | 11.027 | √ | |

| Internal factors | ** 0.525 | 6.978 | √ | |

| External factors | ** 0.582 | 8.097 | √ | |

| Information Technology | ** 0.326 | 3.901 | √ | |

| Total factors influencing the appropriate investment decision | ** 0.724 | 11.874 | √ |

| Variants | Fixed Limit A | Transactions | Significance | ||||

|---|---|---|---|---|---|---|---|

| Y | X Dimensions of the Factors Influencing the Appropriate Investment Decision | Regression Parameter Beta | Calculated (T) Value | Calculated (F) Value | Determination Coefficient (R2) | ||

| Take the appropriate investment Decision | Information Nature | 2.25 | 0.62 | 8.794 | 79.097 | 0.40 | √ |

| Disclosure | 2.08 | 0.64 | 9.462 | 85.529 | 0.41 | √ | |

| Perception | 2.11 | 0.69 | 10.874 | 118.253 | 0.48 | √ | |

| Internal factors | 3.18 | 0.40 | 8.962 | 54.626 | 0.33 | √ | |

| External factors | 2.69 | 0.61 | 8.617 | 74.254 | 0.37 | √ | |

| Information Technology | 3.09 | 0.43 | 5.253 | 28.643 | 0.18 | √ | |

| Total factors influencing the appropriate investment decision | 1.93 | 0.73 | 12.117 | 146.821 | 0.53 | √ | |

| Steps | Variables Included in the Form | Fixed Limit Value | Regression Coefficient Value | R2 | Calculated (F) Value | SIG (p Value) | Decision |

|---|---|---|---|---|---|---|---|

| 1 | Information nature | 2.52 | 0.72 | 0.52 | 139.09 | 0.000 | There is an effect |

| 2 | Information nature | 1.52 | 0.59 | 0.73 | 167.84 | 0.000 | There is an effect |

| Disclosure | 0.47 | ||||||

| 3 | Information nature | 0.89 | 0.50 | 0.87 | 284.97 | 0.000 | There is an effect |

| Disclosure | 0.42 | ||||||

| External factors | 0.39 | ||||||

| 4 | Information nature | 0.52 | 0.47 | 0.92 | 346.29 | 0.000 | There is an effect |

| Disclosure | 0.41 | ||||||

| External factors | 0.37 | ||||||

| Information Technology | 0.22 | ||||||

| 5 | Information nature | 0.15 | 0.34 | 0.98 | 973.57 | 0.000 | There is an effect |

| Disclosure | 0.32 | ||||||

| External factors | 0.35 | ||||||

| Information Technology | 0.25 | ||||||

| Perception | 0.30 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Abdul kareem, A.A.; Fayed, Z.T.; Rady, S.; Amin El-Regaily, S.; Nema, B.M. Factors Influencing Investment Decisions in Financial Investment Companies. Systems 2023, 11, 146. https://doi.org/10.3390/systems11030146

Abdul kareem AA, Fayed ZT, Rady S, Amin El-Regaily S, Nema BM. Factors Influencing Investment Decisions in Financial Investment Companies. Systems. 2023; 11(3):146. https://doi.org/10.3390/systems11030146

Chicago/Turabian StyleAbdul kareem, Ahmed Amer, Zaki T. Fayed, Sherine Rady, Salsabil Amin El-Regaily, and Bashar M. Nema. 2023. "Factors Influencing Investment Decisions in Financial Investment Companies" Systems 11, no. 3: 146. https://doi.org/10.3390/systems11030146

APA StyleAbdul kareem, A. A., Fayed, Z. T., Rady, S., Amin El-Regaily, S., & Nema, B. M. (2023). Factors Influencing Investment Decisions in Financial Investment Companies. Systems, 11(3), 146. https://doi.org/10.3390/systems11030146