Research on Financing Risk Factors of Expressway REITs in China with a Hybrid Approach

Abstract

:1. Introduction

2. Literature Review

2.1. Research on Influencing Risks Factors of REITs

2.2. Research on Risk Prevention and Control of REITs

2.3. Research on the Risk of Expressway Asset Securitization

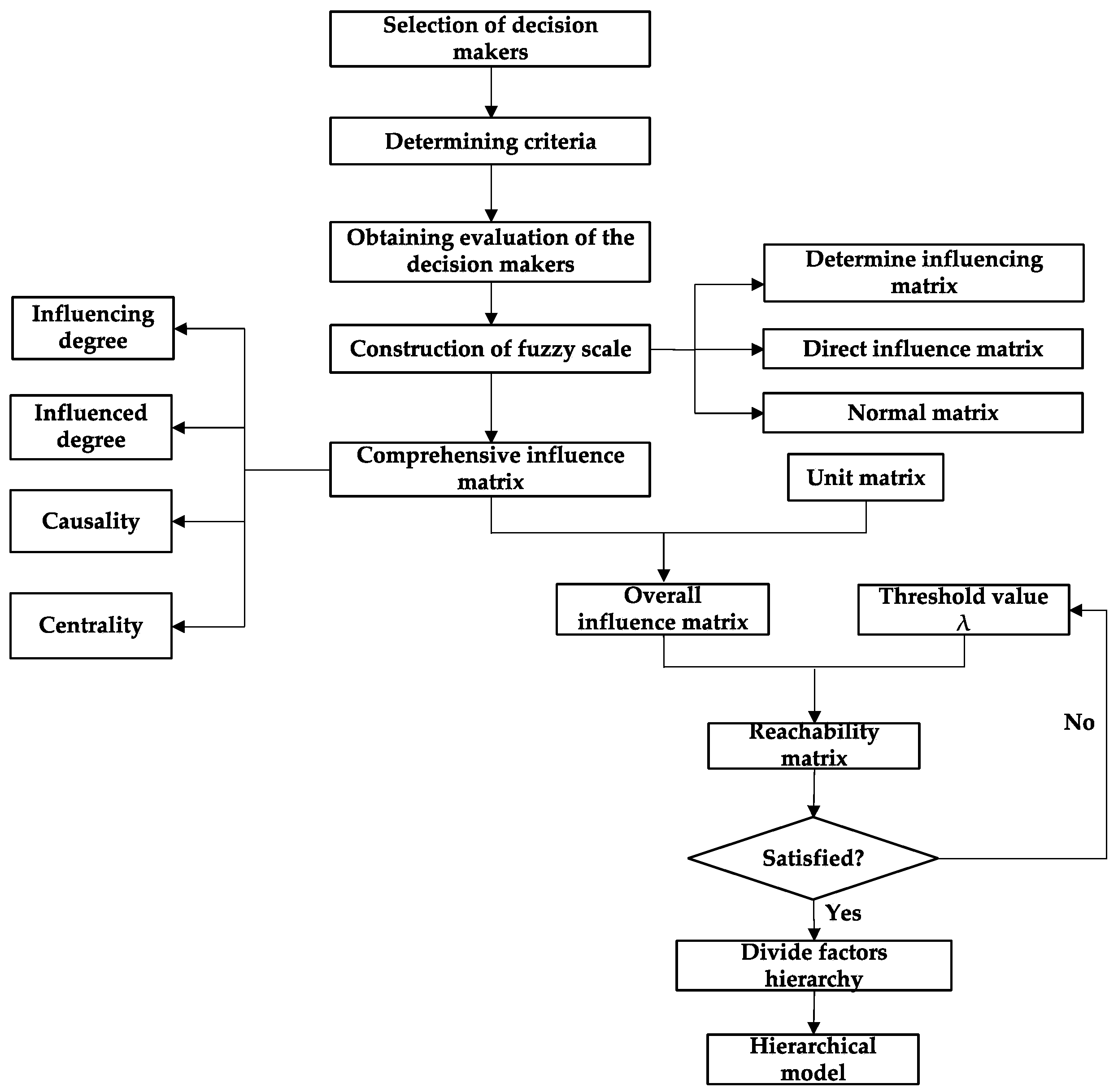

3. Research Methodology

3.1. Overview of Fuzzy, DEMATEL and ISM

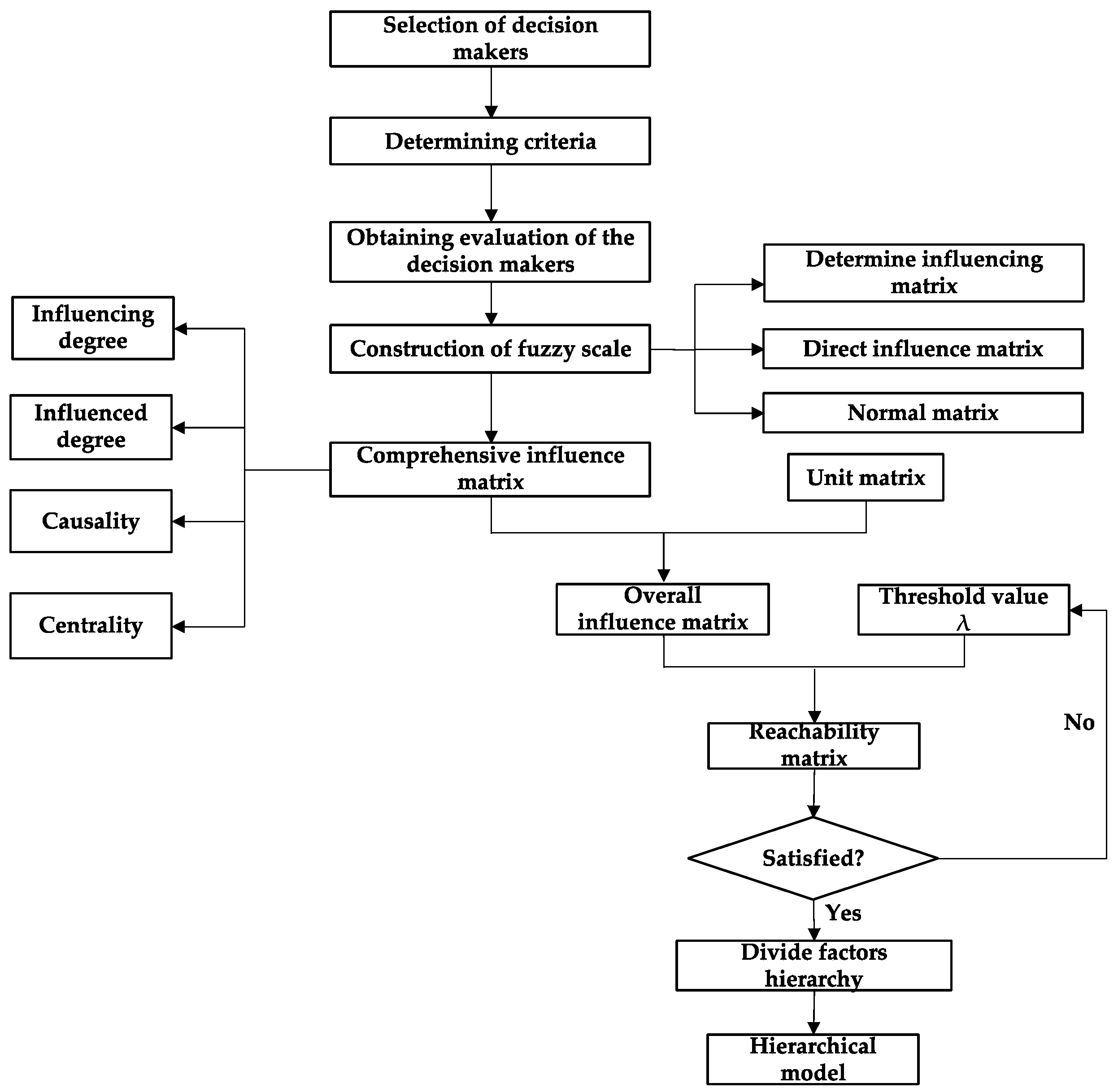

3.2. Procedure of the Fuzzy-DEMATEL-ISM Method

- (1)

- Standardization treatment of the triangle fuzzy numbers.

- (2)

- Calculation of the standard value of left and right.

- (3)

- Calculation of the crisp scores.

- (4)

- Integrate average value of crisp scores and obtain direct influence matrix.

4. Result

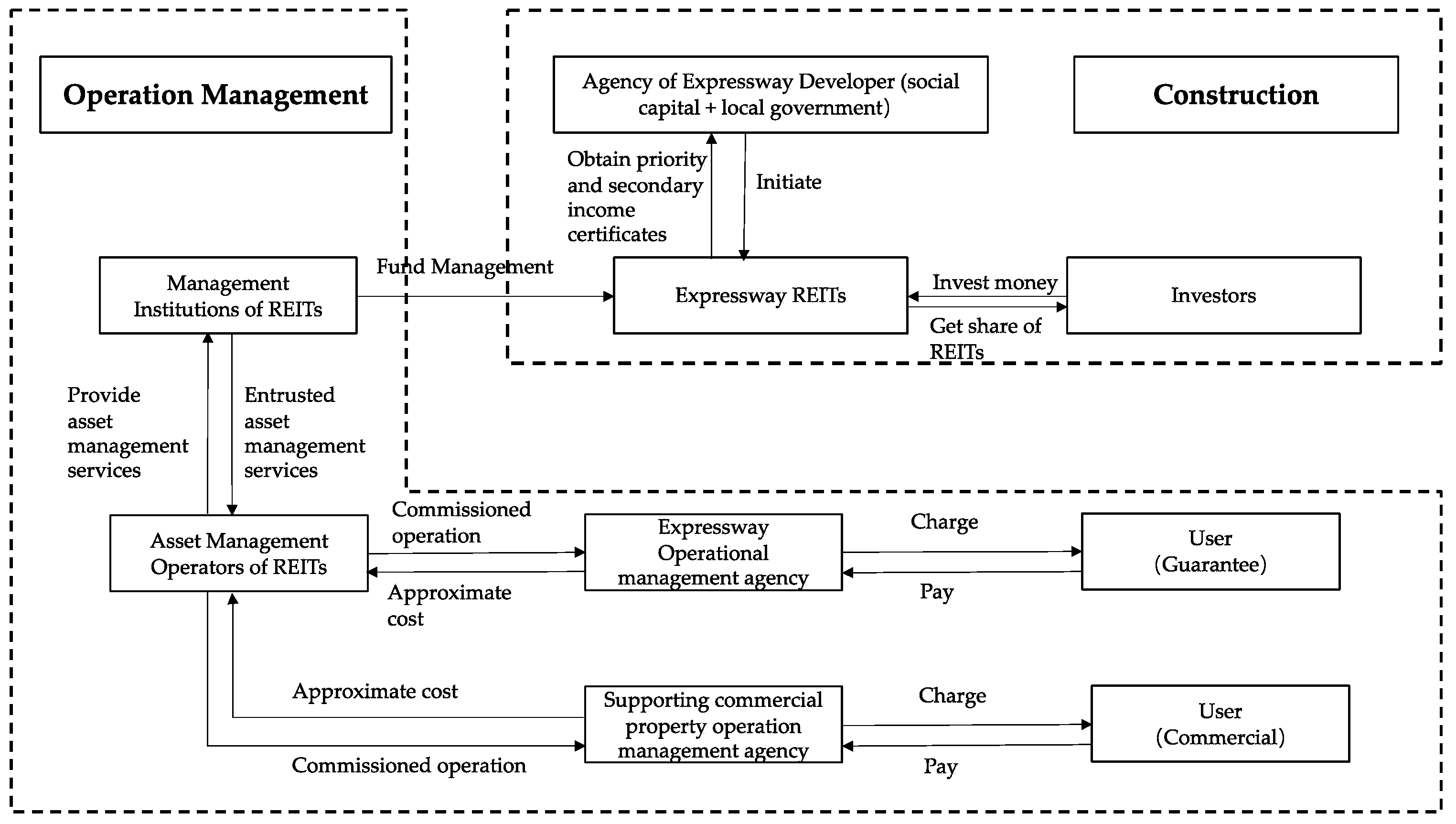

4.1. Flowchart for Developing a Financing Scheme

4.2. Identification of Influencing Factors

4.2.1. Data Source

4.2.2. Keyword Co-Occurrence Analysis

| Algorithm 1: Pseudo code of Average Perceptron |

| Training data: |

| 1. |

| 2. for |

| 3. for |

| 4. |

| 5. |

| 6. |

| 7. |

| 8. |

| 9. |

4.2.3. Keyword Cluster Analysis

| Algorithm 2: Pseudo code of K-Means |

| 1. sample a point uniformly at random from |

| 2. |

| 3. |

| 4. sample each point independently with probability |

| 5. |

| 6. |

| 7. For , set to be the number of points in closer to than any other point in |

| 8. Re-cluster the weighted points in to cluster |

4.2.4. Construction of Risk Factor System

4.3. Construct a Direct Impact Matrix

4.4. Construct Comprehensive Impact Matrix

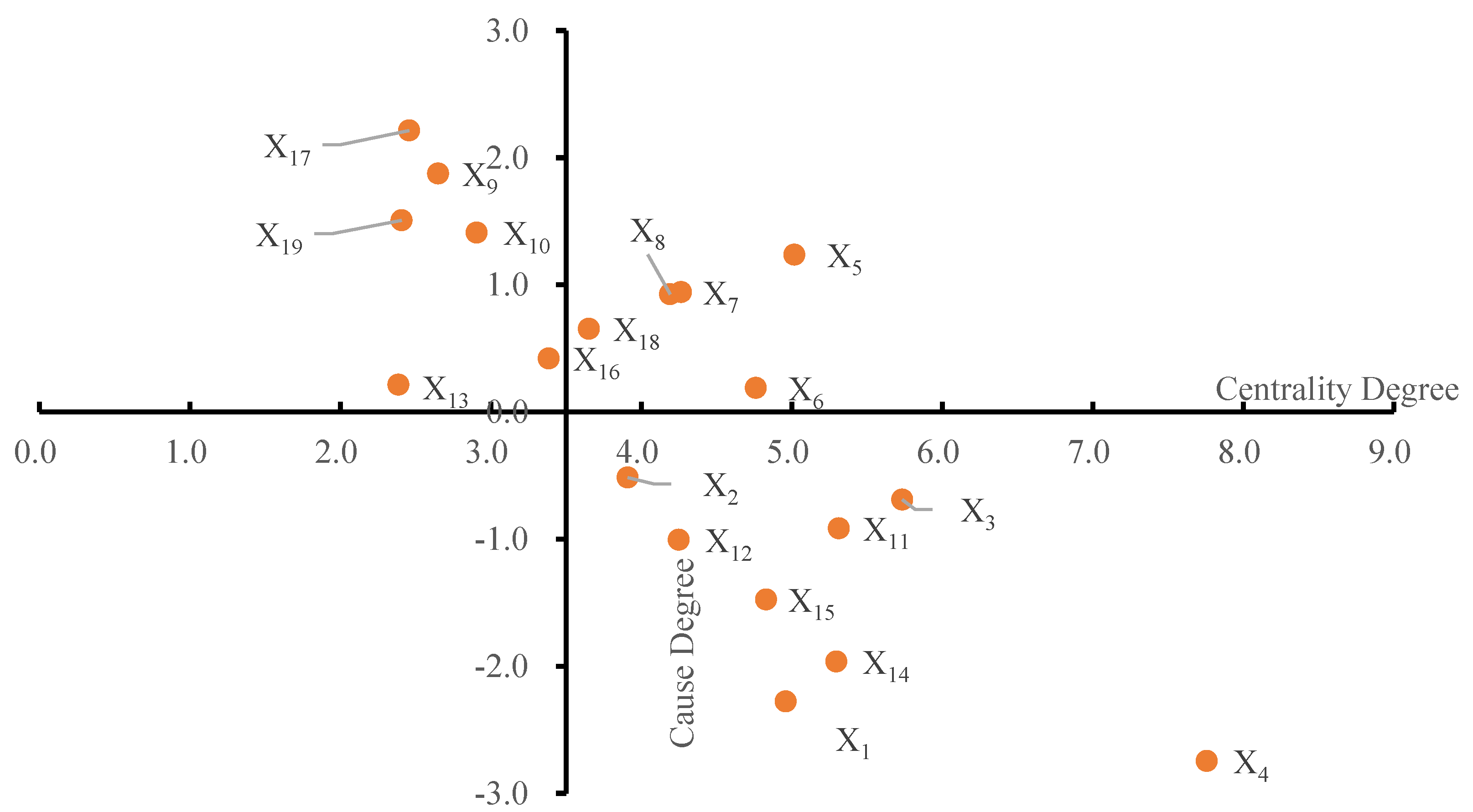

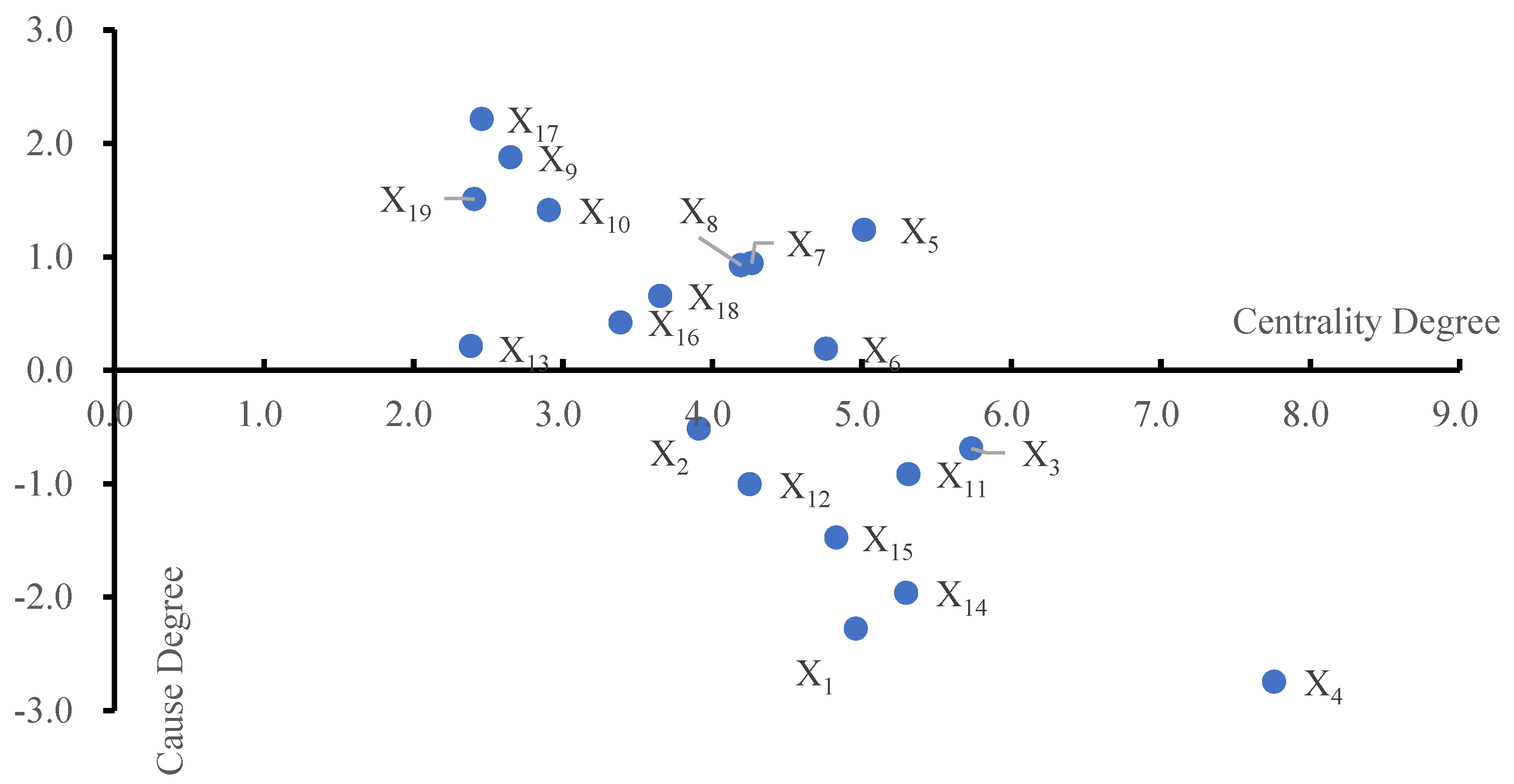

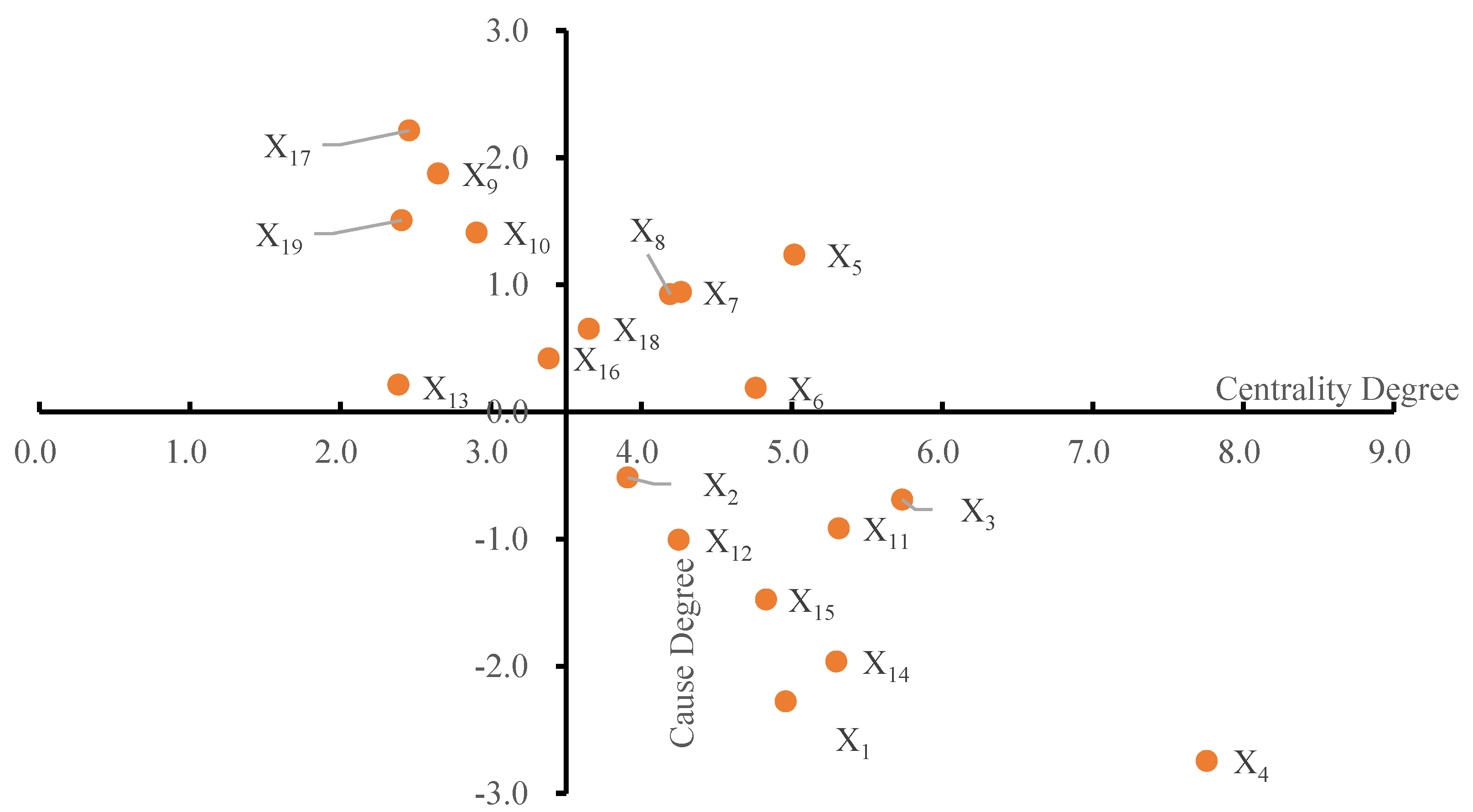

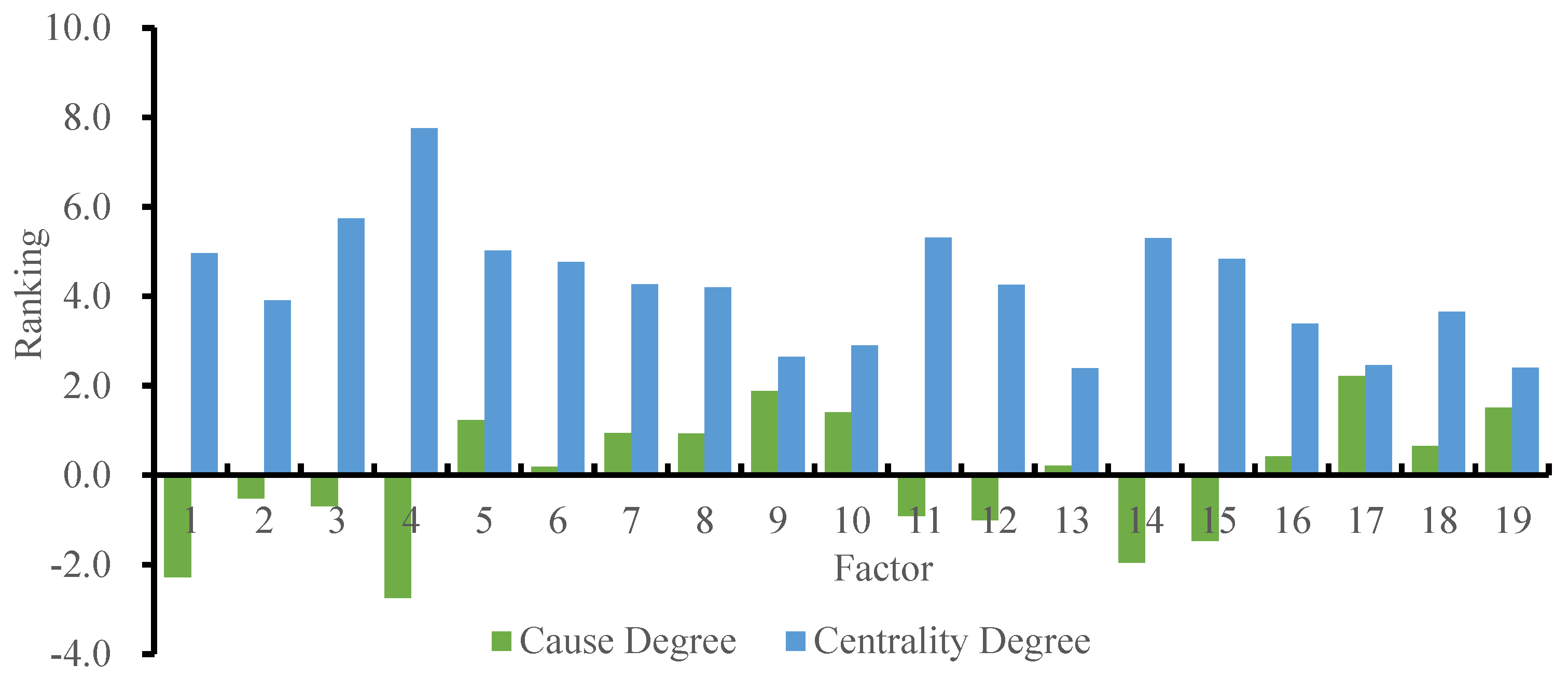

4.5. Calculate the Influence Degree, Influenced Degree, Centrality Degree and Cause Degree

4.6. Construct the Reachability Matrix

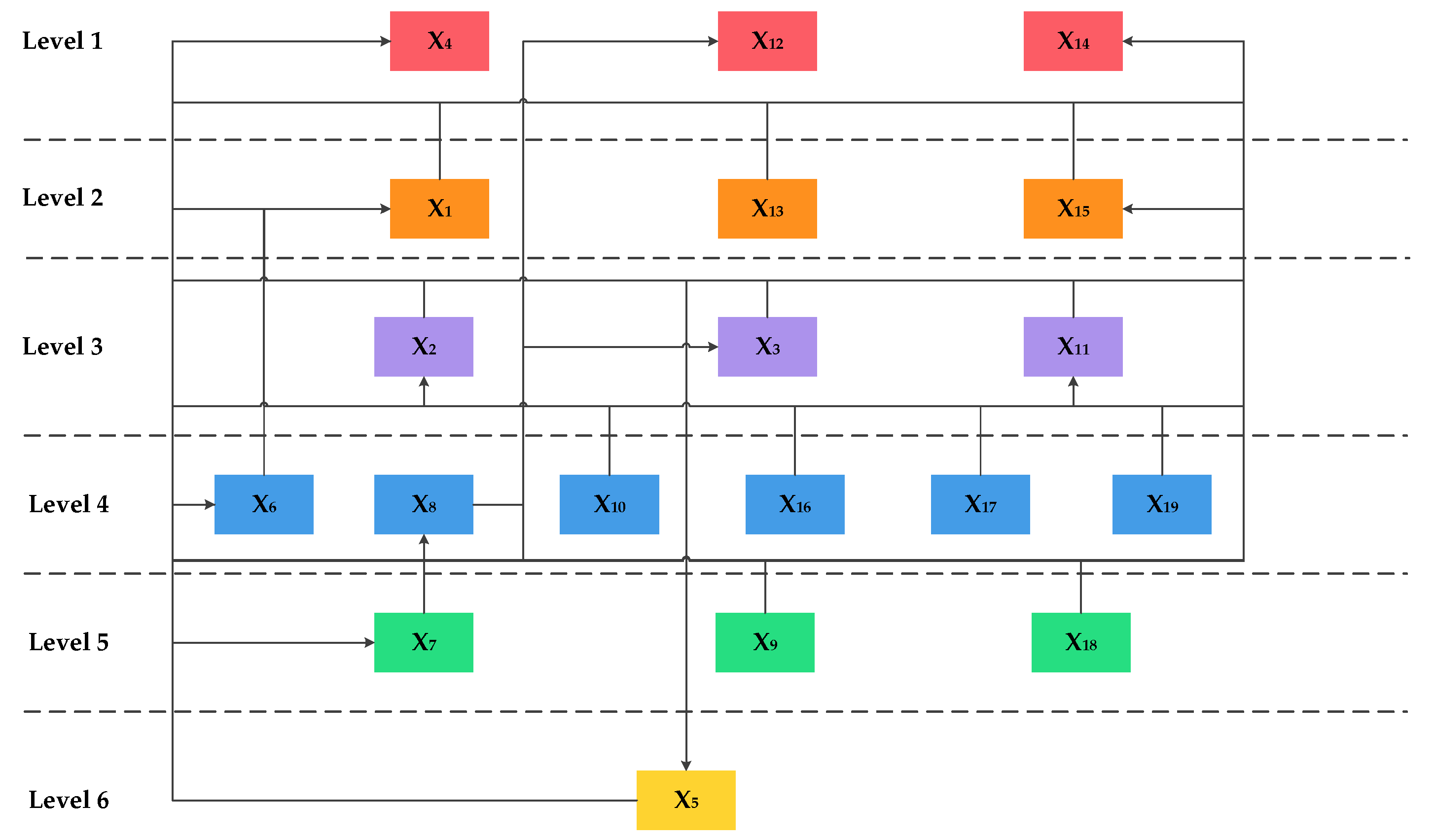

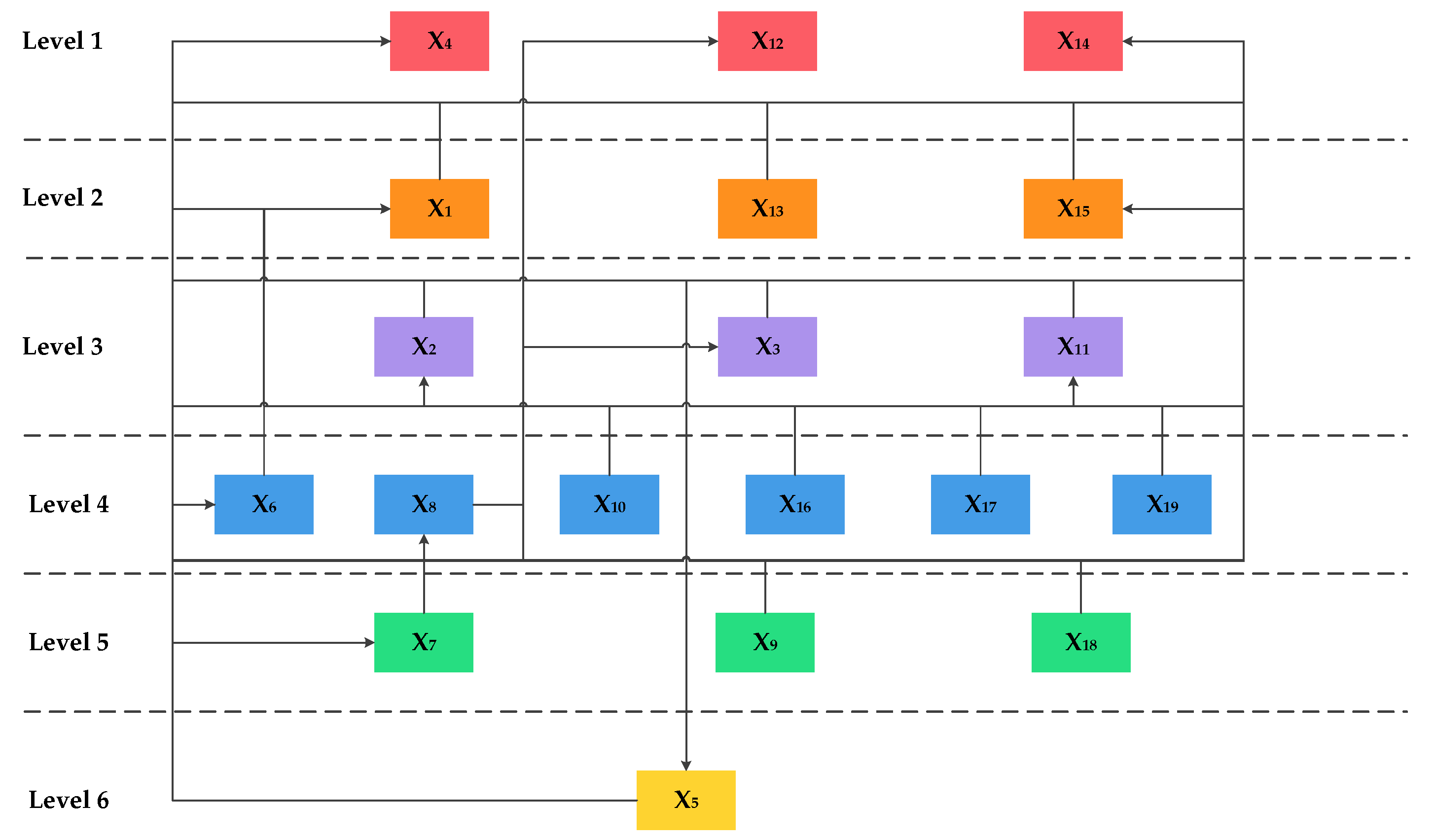

4.7. Establish a Multi-Layer Hierarchical Structure Model of Influencing Factors

5. Discussion

5.1. Analysis of Hierarchical Structure Model of Influencing Factors

- (1)

- Direct risk factors affecting the financing of expressway REITs

- (2)

- Indirect risk factors affecting the financing of expressway REITs

- (3)

- The fundamental influencing factors of the financing risk of expressway REITs

5.2. Analysis of Cause Degree and Result Degree

6. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Chan, S.H.; Erickson, J.; Wang, K. Real Estate Investment Trusts-Structure, Performance, and Investment Opportunities; Economic Science Press: Beijing, China, 2004; pp. 36–41. [Google Scholar]

- Wu, D.; Niu, Y.S.; Du, Z.Q.; Wang, S.Q. A Brief Description of US REITs and Its Inspiration. Proj. Manag. Rev. 2020, 5, 34–38. [Google Scholar]

- Zhu, Y.M.; Xiao, F.S. Practical analysis of infrastructure public REITs. Proj. Manag. Rev. 2021, 2, 48–53. [Google Scholar]

- Wu, D.; Niu, Y.S.; Du, Z.Q.; Wang, S.Q.; Ye, L. Risk measurement of infrastructure REITs market. Proj. Manag. Rev. 2020, 6, 34–39. [Google Scholar]

- Han, Z.F. REITs: China’s Road; People’s Publishing House: Beijing, China, 2021; pp. 298–301. [Google Scholar]

- Cui, M.; Wang, J.; Huang, L.Y.; Luo, S.Y. Investment and Financing Dilemma in Transportation Infrastructure and the Exploration of REITs in China. Highway 2022, 67, 291–294. [Google Scholar]

- Li, R.Y.M.; Chau, K.W. Econometric Analyses of International Housing Markets; Routledge: London, UK, 2016. [Google Scholar]

- Gao, Y. Research on Risk Management of Real Estate Investment Trusts (REITs); East China Normal University: Shanghai, China, 2006. [Google Scholar]

- Chen, G.L. Risk-return study of REITs and its applicability to the use of insurance funds. Insur. Res. 2006, 9, 60–63. [Google Scholar]

- Dai, H. Risk Management of China’s Real Estate Investment Trusts. China Gen. Account. 2014, 1, 133–135. [Google Scholar]

- Zhang, W.Y.; Lin, J.Y.; Chen, Q.M.; Chen, Z.X.; Fang, H.B.; Liu, Q.S. A study on the risk of real estate trust cash-out. China Mark. 2015, 25, 96–97. [Google Scholar]

- Wang, R.T. Research on risk prevention of real estate investment trusts in China. Explor. Econ. Issues 2008, 9, 153–156. [Google Scholar]

- Liu, W.; Xia, E.J.; Yang, S.H. Research on risk evaluation of real estate trust investment funds. Shandong Soc. Sci. 2016, 8, 154–159. [Google Scholar]

- Giannotti, C.; Mattarocci, G. Risk diversification in a real estate portfolio: Evidence from the Italian market. J. Eur. Real Estate Res. 2013, 269, 86–87. [Google Scholar] [CrossRef]

- Chaudhry, M.; Maheshwari, S.; Webb, J. REITs and idiosyncratic risk. J. Real Estate Res. 2004, 26, 207–222. [Google Scholar] [CrossRef]

- Rong, N.; Trick, S. Modelling the Dependence Structure between Australian Equity and Real Estate Markets—A Conditional Copula Approach. Australas. Account. Bus. Financ. J. 2014, 8, 93–113. [Google Scholar] [CrossRef] [Green Version]

- Kuang, L.C. The Nonlinear Effects of Expected and Unexpected Components of Monetary Policy on the Dynamics of REITs Returns. Econ. Model. 2011, 28, 911–920. [Google Scholar]

- Xu, N.; Dong, J.; Song, L.F. The position, model, and basic framework of real estate investment trusts in mainland China. China Real Estate 2006, 8, 43–45. [Google Scholar]

- Guo, J.Q. The operation mode, transaction structure design and risk control of CMBS and REIT-like in China. Tsinghua Financ. Rev. 2017, 12, 82–84. [Google Scholar]

- Long, T.W.; Chen, F.H.; Yu, O.Y.; Wang, K.J. Review and reflection on real estate investment trust fund risk research. J. Eng. Manag. 2017, 31(05), 129–134. [Google Scholar]

- Yin, A.D.; He, H.N. Research on risk control measures of real estate trusts. Technol. Ind. 2011, 11, 54–57. [Google Scholar]

- James, R., III. Customer satisfaction with apartment housing offered by Real Estate Investment Trusts (REITs). Int. J. Consum. Stud. 2009, 33, 572–580. [Google Scholar] [CrossRef]

- Campbell, R.D.; Ghosh, C.; Petrova, M.; Sirmans, C.F. Corporate Governance and Performance in the Market for Corporate Control: The Case of REITs. J. Real Estate Financ. Econ. 2011, 42, 451–480. [Google Scholar] [CrossRef]

- Chen, M.-C.; Tsai, I.-C.; Chen, K.L.; Lo, H.Y. A Preliminary Analysis for Measuring Operating Performance of Real Estate Investment Trusts in Taiwan: Net Income vs. Operation Funds. Contemp. Manag. Res. 2011, 7, 271–290. [Google Scholar] [CrossRef]

- Benveniste, L.M.; Berger, A.N. Securitization with recourse: An instrument that offers uninsured bank depositors sequential claims. J. Bank. Financ. 1987, 11, 403–424. [Google Scholar] [CrossRef]

- Chen, L.M. Exploration of the securitization path of highway assets under the new normal. Transp. Financ. Account. 2018, 6, 11–14. [Google Scholar]

- Sun, Y.F.; Yang, X.Y.; Wang, X.Y. The risk of asset securitization financing of expressway PPP projects and its prevention. Financ. Account. Mon. 2019, 9, 164–170. [Google Scholar]

- Tang, B. Exploring the financing path of highway construction asset securitization. Bus. Account. 2012, 5, 88–89. [Google Scholar]

- Tang, S.Y.; Liu, Y. Asset securitization financing path of highway listed companies and thinking about it. Soc. Sci. 2012, 1, 90–91. [Google Scholar]

- Gomez-Gonzalez, J.E.; Hirs-Garzon, J. Dynamic Spillovers between REITs and Stock Markets in Global Financial Markets. J. Real Estate Portf. Manag. 2021, 27, 20–28. [Google Scholar] [CrossRef]

- Bouri, E.; Gupta, R.; Wang, S. Nonlinear contagion between stock and real estate markets: International evidence from a local Gaussian correlation approach. Int. J. Financ. Econ. 2020; 1–21. [Google Scholar] [CrossRef]

- Lesame, K.; Bouri, E.; Gabauer, D.; Gupta, R. On the Dynamics of International Real Estate-Investment Trust-Propagation Mechanisms: Evidence from Time-Varying Return and Volatility Connectedness Measures. Entropy 2021, 23, 1048. [Google Scholar] [CrossRef]

- Albulescu, C.T.; Bouri, E.; Tiwari, A.K.; Roubaud, D. Quantile causality between banking stock and real estate securities returns in the US. Q. Rev. Econ. Financ. 2020, 78, 251–260. [Google Scholar] [CrossRef]

- Zhu, B. The Development of REIT Markets in Greater China. In Understanding China’s Real Estate Markets; Springer: Cham, Switzerland, 2021; pp. 203–219. [Google Scholar]

- Vlachos, I. The impact of transaction cost economics and competitive factors upon the design of contracts: A study using DEMATEL. Int. J. Decis. Sci. Risk Manag. 2012, 4, 217–232. [Google Scholar]

- Wang, F.W.; Xu, Y.S.; Wang, Z.K.; Yin, Z.X.; Ma, Y. Significant ship for major ships based on DEMATEL-ANP. J. Saf. Environ. 2021, 21, 62–69. [Google Scholar]

- Keskin, G.A. Using integrated fuzzy DEMATEl and fuzzy C: Means algorithm for supplier evaluation and selection. Int. J. Prod. Res. 2015, 53, 3586–3602. [Google Scholar] [CrossRef]

- Zhou, D.Q. Systems Engineering Methods and Applications; Electronic Industry Press: Beijing, China, 2015. [Google Scholar]

- Li, R. Fuzzy method in group decision making. Comput. Math. Appl. 1999, 38, 91–101. [Google Scholar] [CrossRef] [Green Version]

- Opricovic, S.; Tzeng, G.H. Defuzzification within a multicriteria decision model. Int. J. Uncertain. Fuzziness Knowl. Based Syst. 2003, 11, 635–652. [Google Scholar] [CrossRef]

- Bu, L.J.; Yu, Z.J.; Shao, Z.K. Study on factors influencing fire safety management in universities based on DEMATEL/ISM. China Saf. Sci. J. 2018, 28, 133–138. [Google Scholar]

- Yue, R.T.; Han, Y.X. Research on DEMATEL-ISM model of airline security risk factors. J. Saf. Environ. 2020, 20, 2091–2097. [Google Scholar]

- Singh, R.; Bhanot, N. An integrated DEMATEL-MMDE-ISM based approach for analysing the barriers of IoT implementation in the manufacturing industry. Int. J. Prod. Res. 2020, 58, 2454–2476. [Google Scholar] [CrossRef]

- Liu, M.F.; Chen, W. Research on the risk factors of the logistics service quality of the fresh cold chain front warehouse based on the integrated DEMATEL-ISM. Saf. Environ. Eng. 2020, 27, 118–125. [Google Scholar]

- Wang, W.H.; Zhu, Z.X.; Mi, H.P.; Wang, J.Q.; Liu, Y.L.; Jiang, X.S. Research on the Influencing Factors of Fire Accidents in Urban Underground Comprehensive Pipe Gallery Based on DEMATEL-ISM. Saf. Environ. Eng. 2020, 20, 793–800. [Google Scholar]

- Collins, M. Discriminative training methods for hidden markov models: Theory and experiments with perceptron algorithms. In Proceedings of the 2002 Conference on Empirical Methods in Natural Language Processing (EMNLP 2002), Stroudsburg, PA, USA, 6 July 2002; pp. 1–8. [Google Scholar]

- Bian, Z.Q.; Zhang, X.G. Pattern Recognition; Tsinghua University Press: Beijing, China, 1999. [Google Scholar]

- Luo, F.; Li, R.Y.M.; Crabbe, M.J.C.; Pu, R. Economic development and construction safety research: A bibliometrics approach. Saf. Sci. 2022, 145, 105519. [Google Scholar] [CrossRef]

- Zeng, L.; Li, R.Y.M.; Nuttapong, J.; Sun, J.; Mao, Y. Economic Development and Mountain Tourism Research from 2010 to 2020: Bibliometric Analysis and Science Mapping Approach. Sustainability 2022, 14, 562. [Google Scholar] [CrossRef]

- Kaufman, L.; Rousseeuw, P. Finding Groups in Data: An Introduction to Cluster Analysis; Willey: New York, NY, USA, 1990. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Linguistic Terms | Triangular Fuzzy Numbers |

|---|---|

| No influence | (0, 0, 0.25) |

| Very low influence | (0, 0.25, 0.5) |

| Low influence | (0.25, 0.5, 0.7) |

| High influence | (0.5, 0.75, 1.0) |

| Very high influence | (0.75, 1.0, 1.0) |

| Category | Influential Elements | Code | Brief Explanation |

|---|---|---|---|

| Credit risk R1 | credit risk of the project company | X1 | the project company has a credit default and cannot perform the risk of timely repayment of the loan principal and interest |

| credit risk of the original equity holder | X2 | the original equity holder has a credit default and cannot perform its obligations as a credit enhancement party and a trustee operator as agreed | |

| due diligence risk of the special plan manager | X3 | the manager of the special plan has not fulfilled due diligence in the management process or has not established an internal risk control system yet | |

| Underlying asset risk R2 | future cash flow under-expect risk | X4 | the future market revenue level of the project does not meet the expected value |

| risk of bankruptcy isolation of the underlying assets | X5 | the separation of revenue and franchise rights in the expressway REITs model fails to achieve true bankruptcy isolation | |

| underlying asset operation risk | X6 | the fund manager’s control over the project company’s board of directors and the right to amend the company’s articles of association are restricted | |

| Operational risk R3 | special account risk | X7 | the special plan did not keep separate accounts and independent accounting, resulting in the assets of the special plan not being managed separately from the inherent property of the manager |

| rating risk | X8 | inaccurate rating results due to unreasonable technical or rating methods of rating agencies | |

| legal risk | X9 | the current laws related to REITs are imperfect in China and cause adverse fluctuations in the returns of REITs products | |

| Market risk R4 | interest rate risk | X10 | the income of asset-backed securities holders may be affected by fluctuations in interest rates |

| expressway market risk | X11 | the return level of REITs with expressways as the underlying asset is subject to the risk of changes in the overall supply and demand of the market | |

| price risk | X12 | investors suffer losses due to price trends in the overall market for REITs that are unfavorable to investors | |

| tax risk | X13 | the transfer of assets to the project company is subject to VAT and stamp duty based on the appreciation of the appraised value | |

| Liquidity risk R5 | limited counterparty risk | X14 | with limited counterparties, holders of senior asset-backed securities may consider the inability to sell asset-backed securities at an appropriate price |

| realization risk on disposal of expressway-related interests | X15 | expressway toll rights as pledged assets and the disposal of accounts receivable from advertising operation income are subject to certain uncertainties, which may affect the realization of the expected income of asset-backed securities holders | |

| uncompleted exit risk | X16 | priority asset-backed securities that have applied for open-exit and have been confirmed have not completed exit; none of the original equity holders fulfilled their liquidity support obligations; priority asset-backed securities holders will encounter problems that cannot be withdrawn | |

| Other risk R6 | force majeure risk | X17 | the manager’s delay or failure to perform obligations and the loss of assets of the special plan directly or indirectly caused by circumstances beyond the manager’s control and the environment |

| risk related to public offering | X18 | the regulatory authority may stipulate that all or part of the REITs shares held by the original holders of REITs shares cannot be transferred during the lock-up period | |

| policy risk | X19 | during the period of the special plan, toll revenue of expressway vehicle will be reduced or even lost due to changes in China’s expressway toll policy in the future |

| Aij | X1 | X2 | X3 | X4 | X5 | X6 | X7 | X8 | X9 | X10 | X11 | X12 | X13 | X14 | X15 | X16 | X17 | X18 | X19 |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| X1 | 0.00 | 0.14 | 0.32 | 2.18 | 0.27 | 0.77 | 0.18 | 0.23 | 0.18 | 0.09 | 0.27 | 0.41 | 0.27 | 2.23 | 1.32 | 0.23 | 0.00 | 0.18 | 0.09 |

| X2 | 2.09 | 0.00 | 0.23 | 2.14 | 1.23 | 0.64 | 0.09 | 0.36 | 0.14 | 0.09 | 0.64 | 0.50 | 0.23 | 1.27 | 1.14 | 0.32 | 0.00 | 0.73 | 0.05 |

| X3 | 2.18 | 0.32 | 0.00 | 2.23 | 2.73 | 1.23 | 2.82 | 0.18 | 0.09 | 0.27 | 0.77 | 0.64 | 0.32 | 0.64 | 1.09 | 0.82 | 0.00 | 0.14 | 0.23 |

| X4 | 2.86 | 2.32 | 2.73 | 0.00 | 0.41 | 0.32 | 0.50 | 0.18 | 0.05 | 0.23 | 1.18 | 1.23 | 0.64 | 2.14 | 2.68 | 0.41 | 0.00 | 0.68 | 0.18 |

| X5 | 1.82 | 1.59 | 2.82 | 1.50 | 0.00 | 1.73 | 2.23 | 2.18 | 0.23 | 0.36 | 0.77 | 0.77 | 0.45 | 1.23 | 1.32 | 1.36 | 0.00 | 0.77 | 0.36 |

| X6 | 1.68 | 1.86 | 2.27 | 1.82 | 0.73 | 0.00 | 0.32 | 1.14 | 0.18 | 0.32 | 1.73 | 0.82 | 0.41 | 1.14 | 1.32 | 0.36 | 0.00 | 1.09 | 0.14 |

| X7 | 1.09 | 1.27 | 2.82 | 2.18 | 1.14 | 1.23 | 0.00 | 1.18 | 0.23 | 0.36 | 0.77 | 0.41 | 0.14 | 2.23 | 0.64 | 0.41 | 0.00 | 1.18 | 0.32 |

| X8 | 2.86 | 1.14 | 2.14 | 2.59 | 0.23 | 1.18 | 0.64 | 0.00 | 0.41 | 0.27 | 1.36 | 0.82 | 0.00 | 2.18 | 1.23 | 0.32 | 0.00 | 0.77 | 0.05 |

| X9 | 0.45 | 0.32 | 0.64 | 1.68 | 1.50 | 1.86 | 0.91 | 0.09 | 0.00 | 0.18 | 0.59 | 0.59 | 1.23 | 0.23 | 2.05 | 0.41 | 0.18 | 1.14 | 1.36 |

| X10 | 0.32 | 0.18 | 0.41 | 2.23 | 0.23 | 1.18 | 0.77 | 0.18 | 0.18 | 0.00 | 2.59 | 2.14 | 0.68 | 1.50 | 1.68 | 0.32 | 0.05 | 0.41 | 0.18 |

| X11 | 1.32 | 0.77 | 1.32 | 2.14 | 0.86 | 1.36 | 0.23 | 0.09 | 0.00 | 0.45 | 0.00 | 2.41 | 0.55 | 1.41 | 0.82 | 1.27 | 0.00 | 0.59 | 0.00 |

| X12 | 0.18 | 0.14 | 0.32 | 2.59 | 0.59 | 0.73 | 0.36 | 0.14 | 0.00 | 0.23 | 2.05 | 0.00 | 1.14 | 0.91 | 1.27 | 0.14 | 0.00 | 0.32 | 0.00 |

| X13 | 0.41 | 0.18 | 0.59 | 1.32 | 0.41 | 0.32 | 0.27 | 0.00 | 0.14 | 0.32 | 0.77 | 0.91 | 0.00 | 1.18 | 0.77 | 0.36 | 0.23 | 0.64 | 0.23 |

| X14 | 0.36 | 0.23 | 0.23 | 2.27 | 0.36 | 0.77 | 0.68 | 0.18 | 0.00 | 0.00 | 2.59 | 1.32 | 0.09 | 0.00 | 0.41 | 1.23 | 0.00 | 0.45 | 0.09 |

| X15 | 0.77 | 0.32 | 0.41 | 2.27 | 0.36 | 0.45 | 0.00 | 1.50 | 0.00 | 0.64 | 1.18 | 1.41 | 0.00 | 1.36 | 0.00 | 0.41 | 0.00 | 0.27 | 0.14 |

| X16 | 1.27 | 0.91 | 1.14 | 1.86 | 0.41 | 0.68 | 0.45 | 0.77 | 0.14 | 0.23 | 0.64 | 0.64 | 0.50 | 2.59 | 0.59 | 0.00 | 0.00 | 0.55 | 0.09 |

| X17 | 1.50 | 0.82 | 1.18 | 2.05 | 0.59 | 0.68 | 0.32 | 0.64 | 1.32 | 1.18 | 1.82 | 1.09 | 0.00 | 0.32 | 1.41 | 0.23 | 0.00 | 0.68 | 0.27 |

| X18 | 1.86 | 1.41 | 1.77 | 2.50 | 0.27 | 0.91 | 0.14 | 2.14 | 0.09 | 0.14 | 0.32 | 0.32 | 0.18 | 0.45 | 1.14 | 0.59 | 0.41 | 0.00 | 0.14 |

| X19 | 0.18 | 0.09 | 0.23 | 2.32 | 0.55 | 0.86 | 0.00 | 1.00 | 0.55 | 0.36 | 2.59 | 1.77 | 1.14 | 0.41 | 0.32 | 0.00 | 0.55 | 0.45 | 0.00 |

| Nij | X1 | X2 | X3 | X4 | X5 | X6 | X7 | X8 | X9 | X10 | X11 | X12 | X13 | X14 | X15 | X16 | X17 | X18 | X19 |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| X1 | 0.00 | 0.01 | 0.01 | 0.10 | 0.01 | 0.04 | 0.01 | 0.01 | 0.01 | 0.00 | 0.01 | 0.02 | 0.01 | 0.10 | 0.06 | 0.01 | 0.00 | 0.01 | 0.00 |

| X2 | 0.10 | 0.00 | 0.01 | 0.10 | 0.06 | 0.03 | 0.00 | 0.02 | 0.01 | 0.00 | 0.03 | 0.02 | 0.01 | 0.06 | 0.05 | 0.01 | 0.00 | 0.03 | 0.00 |

| X3 | 0.10 | 0.01 | 0.00 | 0.10 | 0.13 | 0.06 | 0.13 | 0.01 | 0.00 | 0.01 | 0.04 | 0.03 | 0.01 | 0.03 | 0.05 | 0.04 | 0.00 | 0.01 | 0.01 |

| X4 | 0.13 | 0.11 | 0.13 | 0.00 | 0.02 | 0.01 | 0.02 | 0.01 | 0.00 | 0.01 | 0.05 | 0.06 | 0.03 | 0.10 | 0.12 | 0.02 | 0.00 | 0.03 | 0.01 |

| X5 | 0.08 | 0.07 | 0.13 | 0.07 | 0.00 | 0.08 | 0.10 | 0.10 | 0.01 | 0.02 | 0.04 | 0.04 | 0.02 | 0.06 | 0.06 | 0.06 | 0.00 | 0.04 | 0.02 |

| X6 | 0.08 | 0.09 | 0.11 | 0.08 | 0.03 | 0.00 | 0.01 | 0.05 | 0.01 | 0.01 | 0.08 | 0.04 | 0.02 | 0.05 | 0.06 | 0.02 | 0.00 | 0.05 | 0.01 |

| X7 | 0.05 | 0.06 | 0.13 | 0.10 | 0.05 | 0.06 | 0.00 | 0.05 | 0.01 | 0.02 | 0.04 | 0.02 | 0.01 | 0.10 | 0.03 | 0.02 | 0.00 | 0.05 | 0.01 |

| X8 | 0.13 | 0.05 | 0.10 | 0.12 | 0.01 | 0.05 | 0.03 | 0.00 | 0.02 | 0.01 | 0.06 | 0.04 | 0.00 | 0.10 | 0.06 | 0.01 | 0.00 | 0.04 | 0.00 |

| X9 | 0.02 | 0.01 | 0.03 | 0.08 | 0.07 | 0.09 | 0.04 | 0.00 | 0.00 | 0.01 | 0.03 | 0.03 | 0.06 | 0.01 | 0.10 | 0.02 | 0.01 | 0.05 | 0.06 |

| X10 | 0.01 | 0.01 | 0.02 | 0.10 | 0.01 | 0.05 | 0.04 | 0.01 | 0.01 | 0.00 | 0.12 | 0.10 | 0.03 | 0.07 | 0.08 | 0.01 | 0.00 | 0.02 | 0.01 |

| X11 | 0.06 | 0.04 | 0.06 | 0.10 | 0.04 | 0.06 | 0.01 | 0.00 | 0.00 | 0.02 | 0.00 | 0.11 | 0.03 | 0.07 | 0.04 | 0.06 | 0.00 | 0.03 | 0.00 |

| X12 | 0.01 | 0.01 | 0.01 | 0.12 | 0.03 | 0.03 | 0.02 | 0.01 | 0.00 | 0.01 | 0.10 | 0.00 | 0.05 | 0.04 | 0.06 | 0.01 | 0.00 | 0.01 | 0.00 |

| X13 | 0.02 | 0.01 | 0.03 | 0.06 | 0.02 | 0.01 | 0.01 | 0.00 | 0.01 | 0.01 | 0.04 | 0.04 | 0.00 | 0.05 | 0.04 | 0.02 | 0.01 | 0.03 | 0.01 |

| X14 | 0.02 | 0.01 | 0.01 | 0.11 | 0.02 | 0.04 | 0.03 | 0.01 | 0.00 | 0.00 | 0.12 | 0.06 | 0.00 | 0.00 | 0.02 | 0.06 | 0.00 | 0.02 | 0.00 |

| X15 | 0.04 | 0.01 | 0.02 | 0.11 | 0.02 | 0.02 | 0.00 | 0.07 | 0.00 | 0.03 | 0.05 | 0.07 | 0.00 | 0.06 | 0.00 | 0.02 | 0.00 | 0.01 | 0.01 |

| X16 | 0.06 | 0.04 | 0.05 | 0.09 | 0.02 | 0.03 | 0.02 | 0.04 | 0.01 | 0.01 | 0.03 | 0.03 | 0.02 | 0.12 | 0.03 | 0.00 | 0.00 | 0.03 | 0.00 |

| X17 | 0.07 | 0.04 | 0.05 | 0.10 | 0.03 | 0.03 | 0.01 | 0.03 | 0.06 | 0.05 | 0.08 | 0.05 | 0.00 | 0.01 | 0.07 | 0.01 | 0.00 | 0.03 | 0.01 |

| X18 | 0.09 | 0.07 | 0.08 | 0.12 | 0.01 | 0.04 | 0.01 | 0.10 | 0.00 | 0.01 | 0.01 | 0.01 | 0.01 | 0.02 | 0.05 | 0.03 | 0.02 | 0.00 | 0.01 |

| X19 | 0.01 | 0.00 | 0.01 | 0.11 | 0.03 | 0.04 | 0.00 | 0.05 | 0.03 | 0.02 | 0.12 | 0.08 | 0.05 | 0.02 | 0.01 | 0.00 | 0.03 | 0.02 | 0.00 |

| Tij | X1 | X2 | X3 | X4 | X5 | X6 | X7 | X8 | X9 | X10 | X11 | X12 | X13 | X14 | X15 | X16 | X17 | X18 | X19 |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| X1 | 0.09 | 0.06 | 0.09 | 0.21 | 0.05 | 0.08 | 0.05 | 0.05 | 0.01 | 0.02 | 0.09 | 0.08 | 0.04 | 0.18 | 0.13 | 0.05 | 0.00 | 0.04 | 0.01 |

| X2 | 0.20 | 0.07 | 0.11 | 0.24 | 0.11 | 0.09 | 0.05 | 0.06 | 0.01 | 0.02 | 0.12 | 0.10 | 0.04 | 0.17 | 0.15 | 0.06 | 0.00 | 0.07 | 0.01 |

| X3 | 0.26 | 0.12 | 0.16 | 0.32 | 0.20 | 0.15 | 0.20 | 0.09 | 0.02 | 0.04 | 0.16 | 0.14 | 0.06 | 0.20 | 0.19 | 0.10 | 0.00 | 0.07 | 0.03 |

| X4 | 0.28 | 0.19 | 0.24 | 0.23 | 0.10 | 0.11 | 0.10 | 0.08 | 0.01 | 0.04 | 0.18 | 0.17 | 0.07 | 0.25 | 0.25 | 0.09 | 0.00 | 0.09 | 0.02 |

| X5 | 0.29 | 0.19 | 0.30 | 0.35 | 0.11 | 0.20 | 0.20 | 0.18 | 0.03 | 0.05 | 0.19 | 0.17 | 0.07 | 0.26 | 0.23 | 0.14 | 0.00 | 0.11 | 0.04 |

| X6 | 0.24 | 0.18 | 0.24 | 0.30 | 0.12 | 0.10 | 0.09 | 0.12 | 0.02 | 0.04 | 0.20 | 0.15 | 0.06 | 0.21 | 0.19 | 0.08 | 0.00 | 0.11 | 0.02 |

| X7 | 0.22 | 0.16 | 0.27 | 0.33 | 0.14 | 0.16 | 0.09 | 0.13 | 0.02 | 0.05 | 0.17 | 0.13 | 0.05 | 0.26 | 0.17 | 0.09 | 0.00 | 0.12 | 0.03 |

| X8 | 0.29 | 0.15 | 0.23 | 0.34 | 0.10 | 0.15 | 0.10 | 0.07 | 0.03 | 0.04 | 0.19 | 0.15 | 0.05 | 0.26 | 0.20 | 0.08 | 0.00 | 0.10 | 0.02 |

| X9 | 0.16 | 0.11 | 0.16 | 0.27 | 0.14 | 0.17 | 0.10 | 0.08 | 0.01 | 0.04 | 0.15 | 0.13 | 0.10 | 0.15 | 0.21 | 0.08 | 0.01 | 0.11 | 0.08 |

| X10 | 0.15 | 0.09 | 0.14 | 0.29 | 0.08 | 0.13 | 0.09 | 0.06 | 0.02 | 0.03 | 0.23 | 0.20 | 0.07 | 0.20 | 0.19 | 0.07 | 0.01 | 0.07 | 0.02 |

| X11 | 0.20 | 0.12 | 0.18 | 0.29 | 0.11 | 0.14 | 0.08 | 0.06 | 0.01 | 0.05 | 0.12 | 0.20 | 0.07 | 0.20 | 0.16 | 0.11 | 0.00 | 0.08 | 0.01 |

| X12 | 0.11 | 0.07 | 0.11 | 0.26 | 0.08 | 0.09 | 0.06 | 0.05 | 0.01 | 0.03 | 0.18 | 0.08 | 0.08 | 0.15 | 0.15 | 0.05 | 0.00 | 0.06 | 0.01 |

| X13 | 0.10 | 0.06 | 0.10 | 0.17 | 0.06 | 0.06 | 0.05 | 0.04 | 0.01 | 0.03 | 0.11 | 0.10 | 0.02 | 0.13 | 0.11 | 0.05 | 0.01 | 0.06 | 0.02 |

| X14 | 0.13 | 0.08 | 0.11 | 0.25 | 0.07 | 0.10 | 0.08 | 0.05 | 0.01 | 0.02 | 0.20 | 0.14 | 0.04 | 0.11 | 0.11 | 0.10 | 0.00 | 0.06 | 0.01 |

| X15 | 0.14 | 0.08 | 0.11 | 0.25 | 0.07 | 0.08 | 0.05 | 0.11 | 0.01 | 0.05 | 0.15 | 0.14 | 0.03 | 0.17 | 0.10 | 0.06 | 0.00 | 0.05 | 0.02 |

| X16 | 0.18 | 0.11 | 0.15 | 0.25 | 0.08 | 0.10 | 0.08 | 0.08 | 0.02 | 0.03 | 0.13 | 0.11 | 0.06 | 0.24 | 0.13 | 0.05 | 0.00 | 0.07 | 0.02 |

| X17 | 0.21 | 0.13 | 0.18 | 0.30 | 0.10 | 0.12 | 0.08 | 0.09 | 0.07 | 0.08 | 0.20 | 0.16 | 0.05 | 0.16 | 0.20 | 0.07 | 0.00 | 0.09 | 0.03 |

| X18 | 0.23 | 0.15 | 0.20 | 0.30 | 0.08 | 0.12 | 0.07 | 0.15 | 0.02 | 0.03 | 0.12 | 0.11 | 0.04 | 0.16 | 0.17 | 0.08 | 0.02 | 0.05 | 0.02 |

| X19 | 0.13 | 0.08 | 0.12 | 0.28 | 0.09 | 0.11 | 0.05 | 0.09 | 0.04 | 0.04 | 0.22 | 0.17 | 0.09 | 0.14 | 0.13 | 0.05 | 0.03 | 0.07 | 0.01 |

| Factors | Influence Degree | Influenced Degree | Cause Degree | Centrality Degree | Centrality Ranking |

|---|---|---|---|---|---|

| X1 | 1.34 | 3.62 | −2.28 | 4.96 | 6 |

| X2 | 1.70 | 2.21 | −0.52 | 3.91 | 12 |

| X3 | 2.52 | 3.21 | −0.69 | 5.73 | 2 |

| X4 | 2.51 | 5.25 | −2.75 | 7.76 | 1 |

| X5 | 3.13 | 1.89 | 1.24 | 5.02 | 5 |

| X6 | 2.47 | 2.29 | 0.19 | 4.76 | 8 |

| X7 | 2.60 | 1.66 | 0.94 | 4.26 | 9 |

| X8 | 2.56 | 1.63 | 0.93 | 4.19 | 11 |

| X9 | 2.26 | 0.39 | 1.88 | 2.65 | 16 |

| X10 | 2.16 | 0.75 | 1.41 | 2.91 | 15 |

| X11 | 2.20 | 3.11 | −0.92 | 5.31 | 3 |

| X12 | 1.62 | 2.63 | −1.01 | 4.25 | 10 |

| X13 | 1.30 | 1.09 | 0.21 | 2.39 | 19 |

| X14 | 1.67 | 3.63 | −1.96 | 5.30 | 4 |

| X15 | 1.68 | 3.15 | −1.48 | 4.83 | 7 |

| X16 | 1.90 | 1.48 | 0.42 | 3.38 | 14 |

| X17 | 2.34 | 0.12 | 2.21 | 2.46 | 17 |

| X18 | 2.15 | 1.50 | 0.65 | 3.65 | 13 |

| X19 | 1.96 | 0.45 | 1.51 | 2.41 | 18 |

| Hij | X1 | X2 | X3 | X4 | X5 | X6 | X7 | X8 | X9 | X10 | X11 | X12 | X13 | X14 | X15 | X16 | X17 | X18 | X19 |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| X1 | 1.09 | 0.06 | 0.09 | 0.21 | 0.05 | 0.08 | 0.05 | 0.05 | 0.01 | 0.02 | 0.09 | 0.08 | 0.04 | 0.18 | 0.13 | 0.05 | 0.00 | 0.04 | 0.01 |

| X2 | 0.20 | 1.07 | 0.11 | 0.24 | 0.11 | 0.09 | 0.05 | 0.06 | 0.01 | 0.02 | 0.12 | 0.10 | 0.04 | 0.17 | 0.15 | 0.06 | 0.00 | 0.07 | 0.01 |

| X3 | 0.26 | 0.12 | 1.16 | 0.32 | 0.20 | 0.15 | 0.20 | 0.09 | 0.02 | 0.04 | 0.16 | 0.14 | 0.06 | 0.20 | 0.19 | 0.10 | 0.00 | 0.07 | 0.03 |

| X4 | 0.28 | 0.19 | 0.24 | 1.23 | 0.10 | 0.11 | 0.10 | 0.08 | 0.01 | 0.04 | 0.18 | 0.17 | 0.07 | 0.25 | 0.25 | 0.09 | 0.00 | 0.09 | 0.02 |

| X5 | 0.29 | 0.19 | 0.30 | 0.35 | 1.11 | 0.20 | 0.20 | 0.18 | 0.03 | 0.05 | 0.19 | 0.17 | 0.07 | 0.26 | 0.23 | 0.14 | 0.00 | 0.11 | 0.04 |

| X6 | 0.24 | 0.18 | 0.24 | 0.30 | 0.12 | 1.10 | 0.09 | 0.12 | 0.02 | 0.04 | 0.20 | 0.15 | 0.06 | 0.21 | 0.19 | 0.08 | 0.00 | 0.11 | 0.02 |

| X7 | 0.22 | 0.16 | 0.27 | 0.33 | 0.14 | 0.16 | 1.09 | 0.13 | 0.02 | 0.05 | 0.17 | 0.13 | 0.05 | 0.26 | 0.17 | 0.09 | 0.00 | 0.12 | 0.03 |

| X8 | 0.29 | 0.15 | 0.23 | 0.34 | 0.10 | 0.15 | 0.10 | 1.07 | 0.03 | 0.04 | 0.19 | 0.15 | 0.05 | 0.26 | 0.20 | 0.08 | 0.00 | 0.10 | 0.02 |

| X9 | 0.16 | 0.11 | 0.16 | 0.27 | 0.14 | 0.17 | 0.10 | 0.08 | 1.01 | 0.04 | 0.15 | 0.13 | 0.10 | 0.15 | 0.21 | 0.08 | 0.01 | 0.11 | 0.08 |

| X10 | 0.15 | 0.09 | 0.14 | 0.29 | 0.08 | 0.13 | 0.09 | 0.06 | 0.02 | 1.03 | 0.23 | 0.20 | 0.07 | 0.20 | 0.19 | 0.07 | 0.01 | 0.07 | 0.02 |

| X11 | 0.20 | 0.12 | 0.18 | 0.29 | 0.11 | 0.14 | 0.08 | 0.06 | 0.01 | 0.05 | 1.12 | 0.20 | 0.07 | 0.20 | 0.16 | 0.11 | 0.00 | 0.08 | 0.01 |

| X12 | 0.11 | 0.07 | 0.11 | 0.26 | 0.08 | 0.09 | 0.06 | 0.05 | 0.01 | 0.03 | 0.18 | 1.08 | 0.08 | 0.15 | 0.15 | 0.05 | 0.00 | 0.06 | 0.01 |

| X13 | 0.10 | 0.06 | 0.10 | 0.17 | 0.06 | 0.06 | 0.05 | 0.04 | 0.01 | 0.03 | 0.11 | 0.10 | 1.02 | 0.13 | 0.11 | 0.05 | 0.01 | 0.06 | 0.02 |

| X14 | 0.13 | 0.08 | 0.11 | 0.25 | 0.07 | 0.10 | 0.08 | 0.05 | 0.01 | 0.02 | 0.20 | 0.14 | 0.04 | 1.11 | 0.11 | 0.10 | 0.00 | 0.06 | 0.01 |

| X15 | 0.14 | 0.08 | 0.11 | 0.25 | 0.07 | 0.08 | 0.05 | 0.11 | 0.01 | 0.05 | 0.15 | 0.14 | 0.03 | 0.17 | 1.10 | 0.06 | 0.00 | 0.05 | 0.02 |

| X16 | 0.18 | 0.11 | 0.15 | 0.25 | 0.08 | 0.10 | 0.08 | 0.08 | 0.02 | 0.03 | 0.13 | 0.11 | 0.06 | 0.24 | 0.13 | 1.05 | 0.00 | 0.07 | 0.02 |

| X17 | 0.21 | 0.13 | 0.18 | 0.30 | 0.10 | 0.12 | 0.08 | 0.09 | 0.07 | 0.08 | 0.20 | 0.16 | 0.05 | 0.16 | 0.20 | 0.07 | 1.00 | 0.09 | 0.03 |

| X18 | 0.23 | 0.15 | 0.20 | 0.30 | 0.08 | 0.12 | 0.07 | 0.15 | 0.02 | 0.03 | 0.12 | 0.11 | 0.04 | 0.16 | 0.17 | 0.08 | 0.02 | 1.05 | 0.02 |

| X19 | 0.13 | 0.08 | 0.12 | 0.28 | 0.09 | 0.11 | 0.05 | 0.09 | 0.04 | 0.04 | 0.22 | 0.17 | 0.09 | 0.14 | 0.13 | 0.05 | 0.03 | 0.07 | 1.01 |

| Factors | λ = 0.10 | λ = 0.15 | λ = 0.20 | λ = 0.25 |

|---|---|---|---|---|

| X1 | 22 | 16 | 12 | 6 |

| X2 | 20 | 8 | 4 | 2 |

| X3 | 29 | 20 | 12 | 6 |

| X4 | 29 | 27 | 23 | 18 |

| X5 | 22 | 13 | 8 | 6 |

| X6 | 25 | 14 | 7 | 3 |

| X7 | 18 | 12 | 7 | 5 |

| X8 | 17 | 11 | 6 | 5 |

| X9 | 14 | 8 | 4 | 3 |

| X10 | 19 | 7 | 6 | 3 |

| X11 | 29 | 19 | 10 | 3 |

| X12 | 24 | 11 | 5 | 3 |

| X13 | 7 | 3 | 2 | 2 |

| X14 | 27 | 19 | 11 | 6 |

| X15 | 27 | 15 | 6 | 3 |

| X16 | 15 | 6 | 4 | 3 |

| X17 | 12 | 9 | 5 | 3 |

| X18 | 16 | 8 | 5 | 3 |

| X19 | 10 | 5 | 4 | 3 |

| Sij | X1 | X2 | X3 | X4 | X5 | X6 | X7 | X8 | X9 | X10 | X11 | X12 | X13 | X14 | X15 | X16 | X17 | X18 | X19 |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| X1 | 1 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 |

| X2 | 1 | 1 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 |

| X3 | 1 | 0 | 1 | 1 | 1 | 1 | 1 | 0 | 0 | 0 | 1 | 0 | 0 | 1 | 1 | 0 | 0 | 0 | 0 |

| X4 | 1 | 1 | 1 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 1 | 0 | 1 | 1 | 0 | 0 | 0 | 0 |

| X5 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 0 | 0 | 1 | 1 | 0 | 1 | 1 | 0 | 0 | 0 | 0 |

| X6 | 1 | 1 | 1 | 1 | 0 | 1 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 1 | 1 | 0 | 0 | 0 | 0 |

| X7 | 1 | 1 | 1 | 1 | 0 | 1 | 1 | 0 | 0 | 0 | 1 | 0 | 0 | 1 | 1 | 0 | 0 | 0 | 0 |

| X8 | 1 | 0 | 1 | 1 | 0 | 0 | 0 | 1 | 0 | 0 | 1 | 1 | 0 | 1 | 1 | 0 | 0 | 0 | 0 |

| X9 | 1 | 0 | 1 | 1 | 0 | 1 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 1 | 1 | 0 | 0 | 0 | 0 |

| X10 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 1 | 1 | 1 | 0 | 1 | 1 | 0 | 0 | 0 | 0 |

| X11 | 1 | 0 | 1 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 1 | 0 | 1 | 1 | 0 | 0 | 0 | 0 |

| X12 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| X13 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 |

| X14 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 |

| X15 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 1 | 0 | 0 | 0 | 0 |

| X16 | 1 | 0 | 1 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 1 | 0 | 0 | 0 |

| X17 | 1 | 0 | 1 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 1 | 0 | 1 | 1 | 0 | 1 | 0 | 0 |

| X18 | 1 | 0 | 1 | 1 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 1 | 1 | 0 | 0 | 1 | 0 |

| X19 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 1 |

| Xi | R(Xi) | A(Xi) | R(Xi) ∩ A(Xi) |

|---|---|---|---|

| X1 | 1, 4, 14 | 1, 2, 3, 4, 5, 6, 7, 8, 9, 11, 16, 17, 18 | 1, 4 |

| X2 | 1, 2, 4, 14 | 2, 4, 5, 6 | 2, 4 |

| X3 | 1, 3, 4, 5, 6, 7, 11, 14, 15 | 3, 4, 5, 6, 7, 8, 9, 11, 16, 17, 18 | 3, 4, 5, 6, 7, 11 |

| X4 | 1, 2, 3, 4, 11, 12, 14, 15 | 1, 2, 3, 4, 5, 6, 7, 8, 9, 10, 11, 12, 13, 14, 15, 16, 17, 18, 19 | 1, 2, 3, 4, 11, 12, 14, 15 |

| X5 | 1, 2, 3, 4, 5, 6, 7, 8, 11, 12, 14, 15 | 5 | 5 |

| X6 | 1, 2, 3, 4, 6, 11, 14, 15 | 3, 5, 6, 7, 9 | 3, 6 |

| X7 | 1, 2, 3, 4, 6, 7, 11, 14, 15 | 3, 7 | 3, 7 |

| X8 | 1, 3, 4, 8, 11, 12, 14, 15 | 5, 8, 18 | 8 |

| X9 | 1, 3, 4, 6, 9, 14, 15 | 9 | 9 |

| X10 | 4, 10, 11, 12, 14, 15 | 10 | 10 |

| X11 | 1, 3, 4, 11, 12, 14, 15 | 3, 4, 5, 6, 7, 8, 10, 11, 12, 14, 17, 19 | 3, 4, 11, 12, 14 |

| X12 | 4, 11, 12 | 4, 5, 8, 10, 11, 12, 17, 19 | 4, 11, 12 |

| X13 | 4, 13 | 13 | 13 |

| X14 | 4, 11, 14 | 1, 2, 3, 4, 5, 6, 7, 8, 9, 10, 11, 14, 15, 16, 17, 18 | 4, 11, 14 |

| X15 | 4, 14, 15 | 3, 4, 5, 6, 7, 8, 9, 10, 11, 15, 17, 18 | 4, 15 |

| X16 | 1, 3, 4, 14, 16 | 16 | 16 |

| X17 | 1, 3, 4, 11, 12, 14, 15, 17 | 17 | 17 |

| X18 | 1, 3, 4, 8, 14, 15, 18 | 18 | 18 |

| X19 | 4, 11, 12, 19 | 19 | 19 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Song, Y.; Hao, S. Research on Financing Risk Factors of Expressway REITs in China with a Hybrid Approach. Systems 2022, 10, 38. https://doi.org/10.3390/systems10020038

Song Y, Hao S. Research on Financing Risk Factors of Expressway REITs in China with a Hybrid Approach. Systems. 2022; 10(2):38. https://doi.org/10.3390/systems10020038

Chicago/Turabian StyleSong, Yimeng, and Shengyue Hao. 2022. "Research on Financing Risk Factors of Expressway REITs in China with a Hybrid Approach" Systems 10, no. 2: 38. https://doi.org/10.3390/systems10020038

APA StyleSong, Y., & Hao, S. (2022). Research on Financing Risk Factors of Expressway REITs in China with a Hybrid Approach. Systems, 10(2), 38. https://doi.org/10.3390/systems10020038